Filed pursuant to Rule 433

Registration No. 333-238461

October 5, 2021

Final Term Sheet

USD 500,000,000 SOFR Floating Rate Global Notes due 2024

To be fungible and form a single series with KfW’s

USD 1,000,000,000 SOFR Floating Rate Global Notes due 2024

issued on February 12, 2021

Terms:

| Issuer: | KfW | |||

| Guarantor: | Federal Republic of Germany | |||

| Aggregate Principal Amount: | USD 500,000,000 | |||

| Denomination: | USD 200,000 | |||

| Date of Pricing: | October 5, 2021 | |||

| Closing Date: | October 13, 2021 | |||

| Maturity Date: | February 12, 2024 | |||

| Redemption Amount: | 100% | |||

| Rate of Interest: | SOFR Average (as defined below) plus the Margin (as defined below) | |||

| Margin: | 1.00% per annum | |||

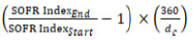

| SOFR Average: | Subject to the “SOFR Average Fallback Provisions” as set forth below, SOFR Average will be calculated by the Calculation Agent on each interest determination date in accordance with the provisions set out below and the following formula (with the resulting percentage being rounded to the nearest one ten-thousandth of a percentage point, with 0.00005 being rounded upwards): | |||

SOFR Average =

|  | |||

where:

“SOFR IndexStart” means the SOFR Index value on the day which is five U.S. Government Securities Business Days (as defined below) prior to the first date of such interest period;

“SOFR IndexEnd” means the SOFR Index value on the day which is five U.S. Government Securities Business Days prior to the interest payment date relating to such interest period (or in the final interest period, the maturity date);

“dc” means the number of calendar days in the Observation Period (as defined below) relating to such interest period. | ||||

| Interest Payment Dates: | Quarterly in arrears every February 12, May 12, August 12 and November 12, commencing on November 12, 2021. | |

| First Interest Payment Date: | November 12, 2021 (for interest accrued from, and including, August 12, 2021 to but excluding November 12, 2021) | |

| Interest Period: | The period from (and including) each Interest Payment Date to (but excluding) the next following Interest Payment Date. | |

| Interest Determination Date: | The fifth U.S. Government Securities Business Day (as defined below) prior to the Interest Payment Date of the relevant Interest Period. | |

| U.S. Government Securities Business Day: | means any day, except for a Saturday, Sunday or a day on which the Securities Industry and Financial Markets Association recommends that the fixed income departments of its members be closed for the entire day for purposes of trading in U.S. government securities. | |

| Observation Period: | In respect of each Interest Period, the period beginning (and including) the date five U.S. Government Securities Business Days prior to the first day of the relevant Interest Period and ending (but excluding) the date five U.S. Government Securities Business Days prior to the relevant Interest Payment Date for the relevant Interest Period. | |

| SOFR Index: | “SOFR Index” in relation to any U.S. Government Securities Business Day shall be the value published by the SOFR administrator (as defined below) on the New York Fed’s Website (as defined below) on or about 8:00 a.m. (New York City time) on such U.S. Government Securities Business Day. Currently, the SOFR administrator publishes the SOFR Index on its website https://apps.newyorkfed.org/markets/autorates/sofr-avg-ind. In the event that the value originally published by the SOFR administrator on or about 8:00 a.m. (New York City time) on any U.S. Government Securities Business Day is subsequently corrected and such corrected value is published by the SOFR administrator on or about 2:30 p.m. (New York City time) on the original date of publication, then such corrected value, instead of the value that was originally published, shall be deemed the SOFR Index in relation to such U.S. Government Securities Business Day. | |

| Accrued Interest: | In the aggregate amount of USD 904,166.67 from, and including, August 12, 2021 to, but excluding, October 13, 2021 | |

| Minimum Rate of Interest: | 0.00% | |

| Currency of Payments: | USD | |

| Price to Public/Issue Price: | 102.125% | |

-2-

Underwriting Commissions: | 0.00% | |||

| Proceeds to Issuer: | 102.125% | |||

| Format: | SEC-registered global notes | |||

| Listing: | Luxembourg Stock Exchange (regulated market) | |||

| Business Day: | London, Frankfurt and New York | |||

| Business Day Convention: | Modified following, adjusted | |||

| Day Count Fraction: | ACTUAL/360 | |||

| Governing Law/Jurisdiction: | German law; District Court Frankfurt am Main | |||

| Gross-Up: | No gross-up if tax deduction or withholding is imposed | |||

| Cross-Default: | None | |||

| Clearing System: | DTC (deliverable through CBL and Euroclear) | |||

| ISIN: | US500769JK15 | |||

| CUSIP: | 500769JK1 | |||

| Selling Restrictions: | European Economic Area, UK, Japan, Canada, Hong Kong | |||

| Ratings of Issuer:1 | Aaa by Moody’s Investors Service, AAA by Scope Ratings and AAA by S&P Global Ratings | |||

| Managers: | BMO Capital Markets Citigroup | |||

| Stabilization Manager: | Citigroup Global Markets Europe AG | |||

| Calculation Agent: | Citibank N.A., London Branch | |||

| Registrar: | Citibank N.A., London Branch | |||

| Paying Agent: | Citibank N.A., London Branch | |||

| Additional Paying Agent: | Citibank Europe Plc, Frankfurt Branch | |||

| SOFR Average Fallback Provisions: | If SOFR IndexStart or SOFR IndexEndis not published on the relevant interest determination date, “SOFR Average” will be calculated by the Calculation Agent for the applicable interest period for which such index is not available in accordance with the provisions set out below and the following formula for Compounded SOFR (with the resulting percentage being rounded to the nearest one ten-thousandth of a percentage point, with 0.00005 being rounded upwards): | |||

Compounded SOFR = |  | |||

| 1 | A security rating is not a recommendation to buy, sell or hold securities. Ratings are subject to revision or withdrawal at any time by the assigning rating organization. Each rating should be evaluated independently of any other rating. |

-3-

where:

“SOFR” means, in respect of any U.S. Government Securities Business Day, the daily SOFR provided by the Federal Reserve Bank of New York, as the administrator of the benchmark (or a successor administrator) (the “SOFR administrator”), as published on the New York Fed’s Website on or about 8:00 a.m. (New York City time) on the U.S. Government Securities Business Day immediately following such U.S. Government Securities Business Day. In the event that the rate originally published by the SOFR administrator on or about 8:00 a.m. (New York City time) on any U.S. Government Securities Business Day is subsequently corrected and such corrected rate is published by the SOFR administrator on or about 2:30 p.m. (New York City time) on the original date of publication, then such corrected rate, instead of the rate that was originally published, shall be deemed the SOFR in relation to such U.S. Government Securities Business Day.

“do” means the number of U.S. Government Securities Business Days in the relevant Observation Period;

“i” means a series of whole numbers from one to do, each representing the relevant U.S. Government Securities Business Day in chronological order from (and including) the first U.S. Government Securities Business Day in the relevant Observation Period;

“ni” for any U.S. Government Securities Business Day “i” means the number of calendar days from (and including) the relevant U.S. Government Securities Business Day “i” up to (but excluding) the immediately following U.S. Government Securities Business Day;

“d” means the number of calendar days in the relevant Observation Period.

“SOFRi” means for any day “i” in the relevant Observation Period, the reference rate equal to SOFR in respect of that day “i”.

“New York Fed’s Website” means the website of the Federal Reserve Bank of New York currently at http://www.newyorkfed.org or any successor website officially designated by the Federal Reserve Bank of New York.

If the SOFR is not published as specified in the first paragraph of this section “SOFR Average Fallback Provisions”, on any particular U.S. Government Securities Business Day, unless both a SOFR cessation event (as defined below) and a SOFR cessation effective date (as defined below) have occurred, the rate of SOFR for such U.S. Government Securities Business Day shall be equal to the rate of SOFR in respect of the last U.S. Government Securities Business Day for which such rate was published on the New York Fed’s Website. |

-4-

If the SOFR is not published as specified in the first paragraph of this section “SOFR Average Fallback Provisions” on any particular U.S. Government Securities Business Day, and both a SOFR cessation event and a SOFR cessation effective date have occurred, the rate of SOFR for each U.S. Government Securities Business Day in the relevant Observation Period on or after such SOFR cessation effective date will be determined as if references to SOFR were references to the rate (inclusive of any spreads or adjustments) recommended as the replacement for SOFR by the U.S. Federal Reserve Board and/or the Federal Reserve Bank of New York, or by a committee officially endorsed or convened by the U.S. Federal Reserve Board and/or the Federal Reserve Bank of New York for the purpose of recommending a replacement for SOFR (which rate may be produced by the Federal Reserve Bank of New York or another designated administrator).

If no such rate is recommended as described in the preceding paragraph within one U.S. Government Securities Business Day of the SOFR cessation event and no OBFR cessation event (as defined below) has occurred, then the rate of SOFR will be determined by applying the above formula for Compounded SOFR as described in the first paragraph of this section “SOFR Average Fallback Provisions” mutatis mutandis as if for each U.S. Government Securities Business Day occurring on or after the SOFR cessation effective date:

- references to “SOFR” were references to the daily Overnight Bank Funding Rate (“OBFR”) as provided by the Federal Reserve Bank of New York, as the administrator of such rate (or any successor administrator of such rate) (the “OBFR administrator”), on the New York Fed’s Website on or about 9:00 a.m. (New York City time) on each day on which commercial banks are open for general business (including dealings in foreign exchange and foreign currency deposits) in New York City (“New York City Banking Day”) in respect of the New York City Banking Day immediately preceding such day. In the event that the rate originally published by the OBFR administrator on or about 9:00 a.m. (New York City time) on any New York City Banking Day is subsequently corrected and such corrected rate is published by the OBFR administrator on or about 2:30 p.m. (New York City time) on the original date of publication, then such corrected rate, instead of the rate that was originally published, shall be deemed the OBFR in respect of the New York City banking day immediately preceding such day;

- references to “U.S. Government Securities Business Day” were references to “New York City Banking Day”;

- references to “SOFR cessation event” were references to “OBFR cessation event” (as defined below); and |

-5-

- references to “SOFR cessation effective date” were references to “OBFR Cessation Effective Date” (as defined below).

If no such rate has been recommended as described in the second preceding paragraph above within one U.S. Government Securities Business Day of the SOFR cessation event and an OBFR Cessation Event has occurred, then the rate of SOFR will be determined by applying the above formula for Compounded SOFR as described in the first paragraph of this section “SOFR Average Fallback Provisions” mutatis mutandis as if for each U.S. Government Securities Business Day occurring on or after the later of the SOFR cessation effective date and the OBFR Cessation Effective Date:

- references to “SOFR” were references to the short-term interest rate target set by the Federal Open Market Committee and published on the website of the Board of Governors of the Federal Reserve System currently at https://www.federalreserve.gov , or any successor website of the Board of Governors of the Federal Reserve System (the “Federal Reserve’s website”) or, if the Federal Open Market Committee does not target a single rate, the mid-point of the short-term interest rate target range set by the Federal Open Market Committee and published on the Federal Reserve’s Website (calculated as the arithmetic average of the upper bound of the target range and the lower bound of the target range, rounded, if necessary, to the nearest second decimal place, 0.005 being rounded upwards);

- references to “U.S. Government Securities Business Day” were references to “New York City Banking Day”; and

- references to the “New York Fed’s Website” were references to the “Federal Reserve’s Website”.

Any substitution of the SOFR, as specified in the preceding three paragraphs above, will remain effective for the remaining term to maturity of the Notes and shall be published by us.

“SOFR cessation event” means the occurrence of one or more of the following events, as determined by KfW and notified by KfW to the Calculation Agent:

- a public statement by the Federal Reserve Bank of New York (or a successor administrator of SOFR) announcing that it has ceased or will cease to provide SOFR permanently or indefinitely, provided that, at that time, there is no successor administrator that will continue to provide SOFR;

- the publication of information which reasonably confirms that the Federal Reserve Bank of New York (or a successor administrator of SOFR) has ceased or will cease to provide SOFR permanently or indefinitely, provided that, at that time, there is no successor administrator that will continue to provide SOFR; or |

-6-

- a public statement by a U.S. or EU regulator or other U.S. or EU official sector entity, such as the European Central Bank, the European Securities and Markets Authority (ESMA), the Federal Reserve Bank of New York, the Commodity Futures Trading Commission (CFTC) or the Securities and Exchange Commission (SEC), prohibiting the use of SOFR.

“SOFR cessation effective date” means, in respect of a SOFR cessation event, the date on which the Federal Reserve Bank of New York (or a successor administrator of SOFR) ceases to publish SOFR or the date as of which SOFR may no longer be used;

“OBFR cessation event” means the occurrence of one or more of the following events, as determined by KfW and notified by KfW to the Calculation Agent:

- a public statement by the Federal Reserve Bank of New York (or a successor administrator of OBFR) announcing that it has ceased or will cease to provide OBFR permanently or indefinitely, provided that, at that time, there is no successor administrator that will continue to provide OBFR;

- the publication of information which reasonably confirms that the Federal Reserve Bank of New York (or a successor administrator of OBFR) has ceased or will cease to provide OBFR permanently or indefinitely, provided that, at that time, there is no successor administrator that will continue to provide OBFR; or

- a public statement by a U.S. or EU regulator or other U.S. or EU official sector entity, such as the European Central Bank, the European Securities and Markets Authority (ESMA), the Federal Reserve Bank of New York, the Commodity Futures Trading Commission (CFTC) or the Securities and Exchange Commission (SEC), prohibiting the use of OBFR.

“OBFR cessation effective date” means, in respect of a OBFR cessation event, the date on which the Federal Reserve Bank of New York (or any successor administrator of OBFR), ceases to publish OBFR, or the date as of which OBFR may no longer be used. |

ADDITIONAL INFORMATION AND CERTAIN CONSIDERATIONS RELATED TO THE SOFR AND SOFR-BASED NOTES

Investors should consult their own financial and legal advisors about the risks associated with an investment in the notes and the suitability of investing in the notes in light of their particular circumstances, and possible scenarios for economic, interest rate and other factors that may affect their investment.

-7-

Composition and Characteristics of SOFR

On June 22, 2017, the Alternative Reference Rates Committee (“ARRC”) convened by the Board of Governors of the Federal Reserve System and the Federal Reserve Bank of New York identified the SOFR as the rate that, in the consensus view of the ARRC, represented best practice for use in certain new U.S. dollar derivatives and other financial contracts. SOFR is a broad measure of the cost of borrowing cash overnight collateralized by U.S. treasury securities, and has been published by the Federal Reserve Bank of New York since April 2018. The Federal Reserve Bank of New York has also begun publishing historical indicative SOFR from 2014. Investors should not rely on any historical changes or trends in SOFR as an indicator of future changes in SOFR.

The composition and characteristics of SOFR are not the same as those of the London Interbank Offered Rate (“LIBOR”), and SOFR is fundamentally different from LIBOR for two key reasons. First, SOFR is a secured rate, while LIBOR is an unsecured rate. Second, SOFR is an overnight rate, while LIBOR is a forward-looking rate that represents interbank funding over different maturities (e.g., three months). As a result, there can be no assurance that SOFR (including SOFR Average) will perform in the same way as LIBOR would have at any time, including, without limitation, as a result of changes in interest and yield rates in the market, market volatility or global or regional economic, financial, political, regulatory, judicial or other events.

Since the initial publication of SOFR, daily changes in SOFR have, on occasion, been more volatile than daily changes in other benchmark or market rates, such as USD LIBOR. Although changes in SOFR Average generally are not expected to be as volatile as changes in daily levels of SOFR, the return on and value of the notes may fluctuate more than floating rate securities that are linked to less volatile rates. In addition, the volatility of SOFR has reflected the underlying volatility of the overnight U.S. Treasury repurchase agreement (“repo”) market. The Federal Reserve Bank of New York has at times conducted operations in the overnight U.S. Treasury repo market in order to help maintain the federal funds rate within a target range. There can be no assurance that the Federal Reserve Bank of New York will continue to conduct such operations in the future, and the duration and extent of any such operations is inherently uncertain. The effect of any such operations, or of the cessation of such operations to the extent they are commenced, is uncertain and could be materially adverse to investors in the notes.

The Federal Reserve Bank of New York states on its publication page for SOFR that use of SOFR is subject to important disclaimers, limitations and indemnification obligations, including that the Federal Reserve Bank of New York may alter the methods of calculation, publication schedule, rate revision practices or availability of SOFR at any time without notice.

Market Acceptance of SOFR, SOFR Average and SOFR Index

According to the ARRC, SOFR was developed for use in certain U.S. dollar derivatives and other financial contracts as an alternative to USD LIBOR, in part because it is considered a good representation of general funding conditions in the overnight U.S. Treasury repo market. However, as a rate based on transactions secured by U.S. Treasury securities, it does not measure bank-specific credit risk and, as a result, is less likely to correlate with the unsecured short-term funding costs of banks. This may mean that market participants would not consider SOFR a suitable replacement or successor for all of the purposes for which USD LIBOR has historically been used (including, without limitation, as a representation of the unsecured short-term funding costs of banks), which may, in turn, lessen market acceptance of SOFR. Any failure of SOFR to gain market acceptance could adversely affect the return on and value of the notes and the price at which investors can sell the notes in the secondary market.

-8-

In addition, if SOFR does not prove to be widely used as a benchmark in securities that are similar or comparable to the notes, the trading price of the notes may be lower than those of securities that are linked to rates that are more widely used. Since SOFR is a relatively new market index, SOFR-linked debt securities likely have no established trading market when issued, and an established trading market for the SOFR-linked notes may not be as liquid as the market for the issuer’s other floating rate debt securities. Market terms for floating-rate debt securities linked to SOFR, such as the spread over the base rate reflected in interest rate provisions or the manner of compounding the base rate, may evolve over time and trading prices of the notes may be lower than those of later-issued SOFR-based debt securities as a result. Similarly, if SOFR does not prove to be widely used in securities that are similar or comparable to the SOFR-linked notes, the trading price of the SOFR-linked notes may be lower than those of securities that are linked to rates that are more widely used. Investors in the notes may not be able to sell the notes at all or may not be able to sell the notes at prices that will provide them with a yield comparable to similar investments that have a developed secondary market, and may consequently suffer from increased pricing volatility and market risk.

For each interest period, the rate of interest on the notes is based on SOFR Average, which is calculated using the SOFR Index published by the Federal Reserve Bank of New York according to the specific formula described under “SOFR Average” above, not the SOFR rate published on or in respect of a particular date during such interest period or an arithmetic average of SOFR rates during such period. For this and other reasons, the rate of interest on the notes during any interest period will not necessarily be the same as the rate of interest on other SOFR-linked investments that use an alternative basis to determine the applicable interest rate. Further, if the SOFR rate in respect of a particular date during an interest period is negative, its contribution to the SOFR Index will be less than one, resulting in a reduction to SOFR Average used to calculate the interest payable on the notes on the interest payment date for such interest period.

Very limited market precedent exists for securities that use SOFR as the interest rate and the method for calculating an interest rate based upon SOFR in those precedents varies. In addition, the Federal Reserve Bank of New York only began publishing the SOFR Index on March 2, 2020. Accordingly, the use of the SOFR Index or the specific formula for the SOFR Average used in the notes may not be widely adopted by other market participants, if at all. If the market adopts a different calculation method, that would likely adversely affect the market value of the notes.

Determination of SOFR Average and replacements of SOFR Average

The level of SOFR Average applicable to a particular interest period and, therefore, the amount of interest payable with respect to such interest period, will be determined on the interest determination date for such interest period. Because each such date is near the end of such interest period, investors will not know the amount of interest payable with respect to a particular interest period until shortly prior to the related interest payment date and it may be difficult for investors to reliably estimate the amount of interest that will be payable on each such interest payment date. In addition, some investors may be unwilling or unable to trade the notes without changes to their information technology systems, both of which could adversely impact the liquidity and trading price of the notes.

The SOFR Index is published by the Federal Reserve Bank of New York based on data received by it from sources other than the issuer, and the issuer has no control over its methods of calculation, publication schedule, rate revision practices or availability of SOFR and the SOFR Index at any time. There can be no guarantee, particularly given its relatively recent introduction, that the SOFR Index will not be discontinued or fundamentally altered in a manner that is materially adverse to the interests of investors in the notes. In addition, the Federal Reserve Bank of New York may alter the methods of calculation, publication schedule, rate revision practices or availability of SOFR at any time without notice. If the manner in which the SOFR Index is calculated, including the manner in which SOFR is calculated, is changed, that change may result in a reduction in the amount of interest payable on the notes and the trading prices of the notes. In addition, the Federal Reserve Bank of New York may withdraw, modify or amend the published SOFR Index or SOFR data in its sole discretion and without notice. The rate of interest for any interest period will not be adjusted for any modifications or amendments to the SOFR Index or SOFR data that the Federal Reserve Bank of New York may publish after the rate of interest for that interest period has been determined.

-9-

Furthermore, to the extent that the SOFR Index is no longer published as specified herein, the applicable rate to be used to calculate the rate of interest on the notes will be determined using the alternative methods described under “SOFR Average Fallback Provisions” above. Any of these fallbacks may result in interest payments that are lower than, or do not otherwise correlate over time with, the payments that would have been made on the notes if SOFR and/or the SOFR Index had been provided by the Federal Reserve Bank of New York in its current form. In addition, Compounded SOFR, the first available fallback, is the compounded average of the daily SOFR calculated in arrears, and very limited market precedent exists for securities that use Compounded SOFR as the rate basis, and the method for calculating Compounded SOFR in those precedents varies.

The application of the fallbacks may result in determinations being made by the issuer that may adversely affect the value of the notes, the return on the notes and the price at which investors can sell such notes. Moreover, certain determinations to be made by the issuer may require the exercise of discretion and the making of subjective judgments, such as with respect to the occurrence or non-occurrence of a SOFR cessation event or an OBFR cessation event as described under “SOFR Average Fallback Provisions” above. These potentially subjective determinations may adversely affect the value of the notes, the return on the notes and the price at which investors can sell such notes.

The issuer has filed a registration statement (including a prospectus) with the SEC for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents the issuer has filed with the SEC for more complete information about the issuer and this offering. You may get these documents for free by visiting EDGAR on the SEC Website at www.sec.gov.

The prospectus supplement relating to the notes is available under the following link: https://www.sec.gov/Archives/edgar/data/821533/000119312520205362/d889048d424b3.htm.

The prospectus relating to the notes is available through the following link: https://www.sec.gov/Archives/edgar/data/821533/000119312520205348/d889037d424b3.htm.

Alternatively, Citigroup will arrange to send you the prospectus, which you may request by calling toll-free +1-800-831-9146.

Notice by Bank of Montreal Europe plc and Citigroup Global Markets Europe AG to Distributors Regarding MiFID II Product Governance

Bank of Montreal Europe plc and Citigroup Global Markets Europe AG acting in their capacity as manufacturers of the notes in the meaning of Directive 2014/65/EU and implementing legislation (as amended, “MiFID II”) hereby inform prospective distributors for the purpose of the product governance rules under MiFID II that the target market assessment made by Bank of Montreal Europe plc and Citigroup Global Markets Europe AG in respect of the notes in accordance with the product governance rules under MiFID II has led Bank of Montreal Europe plc and Citigroup Global Markets Europe AG to the conclusion that: (i) the target market for the notes is eligible counterparties and professional clients only, each as defined in MiFID II; and (ii) all channels for distribution of the notes are appropriate. Any distributor should take into consideration the target market assessment of Bank of Montreal Europe plc and Citigroup Global Markets Europe AG; however, a distributor subject to MiFID II is responsible for undertaking its own target market assessment in respect of the notes (by either adopting or refining the target market assessment of Bank of Montreal Europe plc and Citigroup Global Markets Europe AG), determining appropriate distribution channels and performing the suitability and appropriateness assessment with respect to each client.

-10-