UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05339

Concorde Funds, Inc.

(Exact name of registrant as specified in charter)

8383 Preston Center Plaza

Suite 360

Dallas, TX 75225

(Address of principal executive offices) (Zip code)

Gary B. Wood, President

8383 Preston Center Plaza, Suite 360

Dallas, TX 75225

(Name and address of agent for service)

(972)-701-5400

Registrant’s telephone number, including area code

Date of fiscal year end: September 30

Date of reporting period: September 30, 2024

Item 1. Reports to Stockholders.

| | |

| Concorde Wealth Management Fund | |

| CONWX (Principal U.S. Listing Exchange: NYSE) |

| Annual Shareholder Report | September 30, 2024 |

This annual shareholder report contains important information about the Concorde Wealth Management Fund for the period of October 1, 2023, to September 30, 2024. You can find additional information about the Fund at www.concordeco.com. You can also request this information by contacting us at 1-972-701-5400.

WHAT WERE THE FUND COSTS FOR THE PAST YEAR? (based on a hypothetical $10,000 investment)

| | |

Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Concorde Wealth Management Fund | $163 | 1.51% |

HOW DID THE FUND PERFORM LAST YEAR AND WHAT AFFECTED ITS PERFORMANCE?

For the 12-month period ended September 30, 2024, the Fund overperformed its benchmark, a blended index using 45% of the Russell 1000 Value, 45% of the Barclays Intermediate Agg, 5% of the Bank of America Merrill Lynch 1-3 Year Treasuries, and 5% of the Barclays U.S. TIPS.

For the year ended September 30, 2024, relative performance for the Concorde Wealth Management Fund was aided by an overweight position in the Precious metals, Information Technology sector, Financials, and Healthcare and underweights in the Consumer Discretionary and Materials sectors. Stock selection marginally benefited relative Fund performance in the Materials and Financials sectors. Relative performance was hindered by the Fund’s overweight position in the Energy sector and underweight positions in certain names in the Technology sector and specifically semiconductors. Stock selection detracted from relative performance in the Health Care and Consumer Discretionary sectors.

During the period, the strategy continued its high allocation to quality companies, as defined by the S&P Earnings growth and free cash flow. This significant overweight to quality and value detracted from the Fund’s relative returns during the period, which we believe were driven by increased investor appetite for risk following the U.S. avoidance of a recession and easing concerns over inflation in addition to exuberance regarding expected benefits of Artificial Intelligence.

We tactically maintained the short end on our fixed income exposure, avoiding duration risk. Our equity exposure remains diversified, with a concentration in Energy.

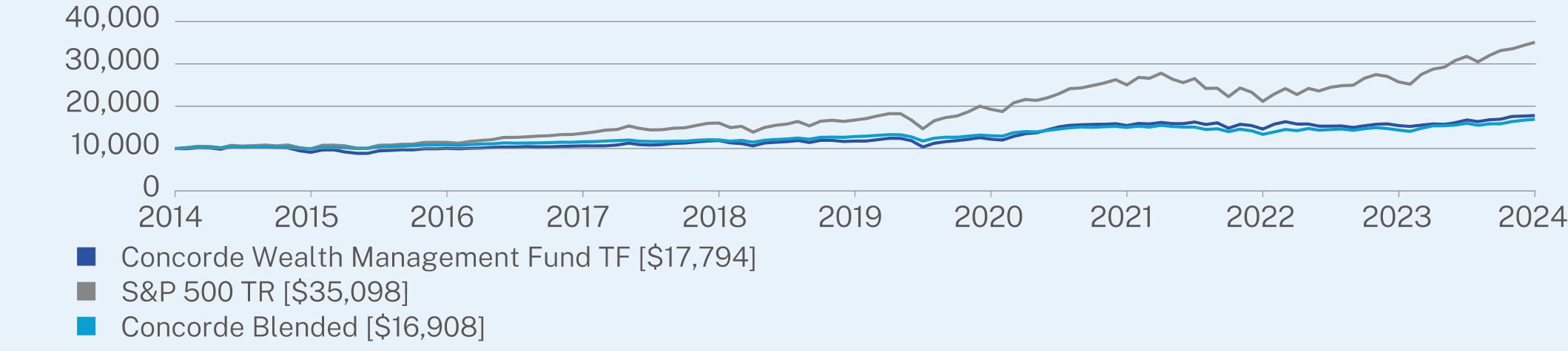

HOW DID THE FUND PERFORM OVER THE PAST 10 YEARS?*

The $10,000 chart reflects a hypothetical $10,000 investment in the class of shares noted and assumes the maximum sales charge. The chart uses total return NAV performance and assumes reinvestment of dividends and capital gains. Fund expenses, including 12b-1 fees, management fees and other expenses were deducted.

CUMULATIVE PERFORMANCE (Initial Investment of $10,000)

| Concorde Wealth Management Fund | PAGE 1 | TSR-AR-20651N307 |

ANNUAL AVERAGE TOTAL RETURN (%)

| | | |

| | 1 Year | 5 Year | 10 Year |

TF (without sales charge) | 15.41 | 8.61 | 5.93 |

S&P 500 TR | 36.35 | 15.98 | 13.38 |

Concorde Blended | 17.81 | 5.68 | 5.39 |

Visit www.concordeco.com for more recent performance information.

| * | The Fund’s past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

KEY FUND STATISTICS (as of September 30, 2024)

| |

Net Assets | $40,630,273 |

Number of Holdings | 64 |

Net Advisory Fee | $302,565 |

Portfolio Turnover | 30% |

Visit www.concordeco.com for more recent performance information.

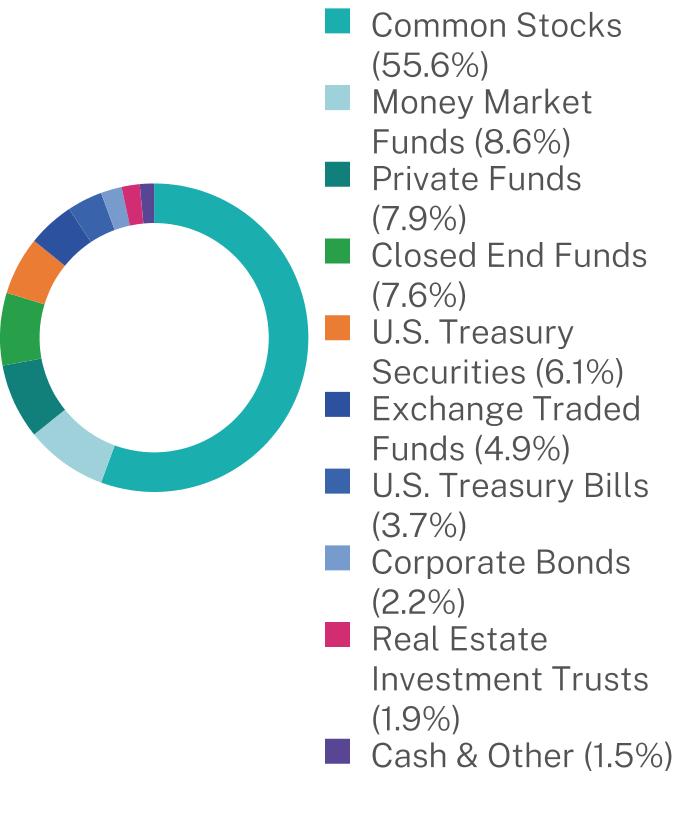

WHAT DID THE FUND INVEST IN? (as of September 30, 2024)

| |

Top Holdings | (%) |

MSILF Government Portfolio | 5.0% |

Texas Pacific Land Corp. | 4.3% |

LLR Equity Partners V, LP | 3.8% |

Black Stone Minerals LP | 3.7% |

Sprott Physical Gold Trust | 3.7% |

Invesco Government & Agency Portfolio | 3.7% |

United States Treasury Notes | 3.6% |

United States Treasury Bill | 3.6% |

Exxon Mobil Corp. | 3.3% |

JPMorgan Chase & Co. | 3.0% |

| |

Top 10 Issuers | (%) |

United States Treasury Notes | 6.1% |

MSILF Government Portfolio | 5.0% |

Texas Pacific Land Corp. | 4.3% |

Sprott Physical Gold Trust | 3.7% |

Black Stone Minerals LP | 3.7% |

LLR Equity Partners V, LP | 3.7% |

Invesco Government & Agency Portfolio | 3.7% |

United States Treasury Bill | 3.6% |

JPMorgan Chase & Co. | 3.0% |

Exxon Mobil Corp. | 3.3% |

Security Type Breakdown (%)

For additional information about the Fund; including its prospectus, financial information, holdings and proxyinformation, scan the QR code or visit www.concordeco.com.

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS

In August 2024, Brad A. Kinder, CPA (“Kinder”) declined to stand for re-election as the independent registered public accounting firm for the Concorde Wealth Management Fund and the Board of Directors of Concorde Funds, Inc. engaged Weaver and Tidwell, LLP to serve as the independent registered public accounting firm to audit the financial statements of the Fund for the fiscal year ending September 30, 2024. During the fiscal years ended September 30, 2022 and September 30, 2023 and the interim period October 1, 2023 through August 15, 2024, there were no disagreements with Kinder on any matter of accounting principles or practices, financial statement disclosure or auditing scope or procedure, which, if not resolved to the satisfaction of Kinder, would have caused it to make a reference in connection with its opinion to the subject matter of the disagreement.

| Concorde Wealth Management Fund | PAGE 2 | TSR-AR-20651N307 |

HOUSEHOLDING

To reduce Fund expenses, only one copy of most shareholder documents may be mailed to shareholders with multiple accounts at the same address (Householding). If you would prefer that your Concorde Financial Corporation documents not be householded, please contact Concorde Financial Corporation at 1-972-701-5400, or contact your financial intermediary. Your instructions will typically be effective within 30 days of receipt by Concorde Financial Corporation or your financial intermediary.

| Concorde Wealth Management Fund | PAGE 3 | TSR-AR-20651N307 |

10000911010040106421189911777121941543814605154191779410000993911472136071604416727192602504021165257413509810000994410868116031204712826130341498313358143521690855.68.67.97.66.14.93.72.21.91.5

Item 2. Code of Ethics.

The registrant has adopted a code of ethics that applies to the registrant’s principal executive officer and principal financial officer. The registrant has not made any substantive amendments to its code of ethics during the period covered by this report. The registrant has not granted any waivers from any provisions of the code of ethics during the period covered by this report.

A copy of the registrant’s Code of Ethics is filed herewith.

Item 3. Audit Committee Financial Expert.

The registrant’s board of directors has determined that that it does not have an audit committee financial expert serving on its audit committee. At this time, the registrant believes that the experience provided by each member of the audit committee together offers the registrant adequate oversight for the registrant’s level of financial complexity.

Item 4. Principal Accountant Fees and Services.

The registrant has engaged its principal accountant to perform audit services, audit-related services, tax services and other services during the past two fiscal years. “Audit services” refer to performing an audit of the registrant’s annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for those fiscal years. “Audit-related services” refer to the assurance and related services by the principal accountant that are reasonably related to the performance of the audit. “Tax services” refer to professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning. There were no “other services” provided by the principal accountant. The following table details the aggregate fees billed or expected to be billed for each of the last two fiscal years for audit fees, audit-related fees, tax fees and other fees by the principal accountant.

| | FYE 9/30/2024 | FYE 9/30/2023 |

| (a) Audit Fees | $45,000 | $38,000 |

| (b) Audit-Related Fees | None | None |

| (c) Tax Fees | 9,000 | $3,000 |

| (d) All Other Fees | None | None |

(e)(1) The audit committee has adopted pre-approval policies and procedures that require the audit committee to pre-approve all audit and non-audit services of the registrant, including services provided to any entity affiliated with the registrant.

(e)(2) The percentage of fees billed by Weaver and Tidwell LLP applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows:

| | FYE 9/30/2024 | FYE 9/30/2023 |

| Audit-Related Fees | 0% | 0% |

| Tax Fees | 0% | 0% |

| All Other Fees | 0% | 0% |

(f) N/A

(g) The following table indicates the non-audit fees billed or expected to be billed by the registrant’s accountant for services to the registrant and to the registrant’s investment adviser (and any other controlling entity, etc.—not sub-adviser) for the last two years.

| Non-Audit Related Fees | FYE 9/30/2024 | FYE 9/30/2023 |

| Registrant | None | None |

| Registrant’s Investment Adviser | $9,000 | $4,185 |

(h) The audit committee of the board of directors has considered whether the provision of non-audit services that were rendered to the registrant’s investment adviser is compatible with maintaining the principal accountant’s independence and has concluded that the provision of such non-audit services by the accountant has not compromised the accountant’s independence.

(i) Not applicable

(j) Not applicable

Item 5. Audit Committee of Listed Registrants.

(a) Not applicable

(b) Not applicable

Item 6. Investments.

| (a) | Schedule of Investments is included as part of the report to shareholders filed under Item 1 of this Form. |

Item 7. Financial Statements and Financial Highlights for Open-End Investment Companies.

Concorde Wealth Management Fund

Annual Financial Statements and Additional Information

September 30, 2024

TABLE OF CONTENTS

Item 7: Financial Statements and Financial Highlights for Open-End Management Investment Companies

Concorde Wealth Management Fund

Schedule of Investments

September 30, 2024

| | | | | | | |

COMMON STOCKS - 55.6%

| | | | | | |

Finance and Insurance - 4.9%

| | | | | | |

Chubb Ltd. | | | 2,700 | | | $778,653 |

JPMorgan Chase & Co. | | | 5,700 | | | 1,201,902 |

Seaport Entertainment Group, Inc.(b) | | | 833 | | | 22,841 |

| | | | | | 2,003,396 |

Information - 4.8%

| | | | | | |

Microsoft Corp.(a) | | | 2,600 | | | 1,118,780 |

Warner Bros Discovery, Inc.(b) | | | 98,550 | | | 813,037 |

| | | | | | 1,931,817 |

Manufacturing - 13.7%

| | | | | | |

AbbVie, Inc. | | | 5,200 | | | 1,026,896 |

Bunge Global SA | | | 1,550 | | | 149,792 |

Eastman Chemical Co. | | | 4,558 | | | 510,268 |

Hershey Co. | | | 1,990 | | | 381,642 |

Hubbell, Inc. | | | 1,600 | | | 685,360 |

Johnson & Johnson | | | 4,900 | | | 794,094 |

Louisiana-Pacific Corp.(a) | | | 6,100 | | | 655,506 |

Moderna, Inc.(a)(b) | | | 3,200 | | | 213,856 |

Northrop Grumman Corp. | | | 1,150 | | | 607,281 |

Texas Instruments, Inc. | | | 2,700 | | | 557,739 |

| | | | | | 5,582,434 |

Mining, Quarrying, and Oil and Gas Extraction - 21.2%

| | | | | | |

Black Stone Minerals LP | | | 100,336 | | | 1,515,074 |

Chesapeake Energy Corp. | | | 12,900 | | | 1,061,025 |

Diamondback Energy, Inc. | | | 5,000 | | | 862,000 |

Exxon Mobil Corp.(a) | | | 11,336 | | | 1,328,806 |

Franco-Nevada Corp. | | | 5,600 | | | 695,800 |

Martin Marietta Materials, Inc. | | | 1,000 | | | 538,250 |

Occidental Petroleum Corp. | | | 17,000 | | | 876,180 |

Texas Pacific Land Corp. | | | 1,985 | | | 1,756,209 |

| | | | | | 8,633,344 |

Real Estate - 1.5%

| | | | | | |

Howard Hughes Holdings, Inc.(b) | | | 7,500 | | | 580,725 |

Retail Trade - 5.6%

| | | | | | |

Amazon.com, Inc.(b) | | | 5,000 | | | 931,650 |

Lowe's Cos., Inc. | | | 2,200 | | | 595,870 |

TJX Cos., Inc. | | | 6,500 | | | 764,010 |

| | | | | | 2,291,530 |

Transportation and Warehousing - 1.4%

|

Canadian Pacific Kansas City Ltd. | | | 6,500 | | | 556,010 |

Wholesale Trade - 2.5%

| | | | | | |

Energy Transfer LP | | | 62,500 | | | 1,003,125 |

TOTAL COMMON STOCKS

(Cost $13,433,578) | | | | | | 22,582,381 |

PRIVATE FUNDS - 7.9%

| | | | | | |

CLI Capital(c) | | | 95,455 | | | 470,814 |

| | | | | | | |

| | | | | | | |

Hayman Hong Kong Opportunities Fund, L.P.(c) | | | 500,000 | | | $ — |

LLR Equity Partners V, L.P.(c) | | | 990,000 | | | 1,548,049 |

LRVHealth, L.P.(c) | | | 477,500 | | | 410,269 |

Moran Tice 20:20 Fund, L.P.(c) | | | 250,000 | | | 282,595 |

RCP Select Capital Fund, L.P.(c) | | | 500,000 | | | 500,000 |

SPAC Opportunity Partners, LLC -

Class A(c) | | | 1,000,000 | | | — |

TOTAL PRIVATE FUNDS

(Cost $3,910,330) | | | | | | 3,211,727 |

CLOSED END FUNDS - 7.6%

| | | | | | |

PIMCO Flexible Credit Income Fund - Class I | | | 58,813 | | | 426,398 |

Pioneer ILS Interval Fund | | | 117,583 | | | 1,140,553 |

Sprott Physical Gold Trust(b) | | | 74,500 | | | 1,518,310 |

TOTAL CLOSED END FUNDS

(Cost $2,473,110) | | | | | | 3,085,261 |

| | | | | | | |

| | | | | | | |

U.S. TREASURY SECURITIES - 6.1%

|

United States Treasury Notes

| | | | | | |

2.25%, 11/15/2024 | | | $500,000 | | | 498,395 |

4.38%, 08/15/2026 | | | 500,000 | | | 506,191 |

3.25%, 06/30/2029 | | | 1,500,000 | | | 1,477,383 |

TOTAL U.S. TREASURY SECURITIES

(Cost $2,461,828) | | | | | | 2,481,969 |

| | | | | | | |

| | | | | | | |

EXCHANGE TRADED FUNDS - 4.9%

|

JPMorgan Nasdaq Equity Premium Income ETF | | | 7,200 | | | 395,496 |

JPMorgan Ultra-Short Income ETF | | | 20,000 | | | 1,014,800 |

PIMCO Enhanced Short Maturity Active Exchange-Traded Fund | | | 6,000 | | | 604,140 |

TOTAL EXCHANGE TRADED FUNDS

(Cost $2,002,465) | | | | | | 2,014,436 |

| | | | | | | |

| | | | | | | |

CORPORATE BONDS - 2.2%

|

Energy - 0.4%

| | | | | | |

BP Capital Markets PLC, 4.38% to 09/22/2025 then 5 yr. CMT Rate + 4.04%, Perpetual | | | $150,000 | | | 148,558 |

Finance and Insurance - 0.8%

| | | | | | |

Discover Financial Services, 3.75%, 03/04/2025 | | | 150,000 | | | 149,026 |

JPMorgan Chase & Co., 6.10% to 10/01/2024 then 3 mo. Term SOFR + 3.59%, Perpetual | | | 150,000 | | | 150,000 |

| | | | | | | |

The accompanying notes are an integral part of these financial statements.

TABLE OF CONTENTS

Concorde Wealth Management Fund

Schedule of Investments

September 30, 2024(Continued)

| | | | | | | |

CORPORATE BONDS - (Continued)

|

Manufacturing - 0.3%

| | | | | | |

Motorola Solutions, Inc.,

7.50%, 05/15/2025 | | | $125,000 | | | $126,553 |

Mining, Quarrying, and Oil and Gas Extraction - 0.4%

| | | | | | |

Freeport-McMoRan, Inc.,

4.13%, 03/01/2028 | | | 175,000 | | | 173,797 |

Utilities - 0.3%

| | | | | | |

Cheniere Energy, Inc.,

4.63%, 10/15/2028 | | | 135,000 | | | 134,178 |

TOTAL CORPORATE BONDS

(Cost $881,947) | | | | | | 882,112 |

| | | | | | | |

| | | | | | | |

REAL ESTATE INVESTMENT TRUSTS - 1.9%

|

First Industrial Realty Trust, Inc. | | | 14,000 | | | 783,720 |

TOTAL REAL ESTATE INVESTMENT TRUSTS

(Cost $615,993) | | | | | | 783,720 |

OPEN END FUNDS - 1.5%

|

Absolute Convertible Arbitrage Fund - Class Institutional | | | 24,270 | | | 277,163 |

Baron Real Estate Fund - Class Institutional | | | 7,871 | | | 325,709 |

TOTAL OPEN END FUNDS

(Cost $588,730) | | | | | | 602,872 |

| | | | | | | |

| | | | | | | |

RIGHTS - 0.0%(d)

|

Finance and Insurance - 0.0%(d)

| | | | | | |

Seaport Entertainment Group, Inc., Expires 10/10/2024, Exercise Price $25.00(b) | | | 833 | | | 2,457 |

TOTAL RIGHTS

(Cost $2,606) | | | | | | 2,457 |

| | | | | | | |

| | | | | | | |

SHORT-TERM INVESTMENTS - 12.3%

|

Money Market Funds - 8.6%

| | | | | | |

Invesco Government & Agency Portfolio - Class Institutional, 4.78%(e) | | | 1,481,464 | | | $1,481,464 |

MSILF Government Portfolio - Class Institutional, 4.78%(e) | | | 2,027,888 | | | 2,027,888 |

| | | | | | 3,509,352 |

| | | | | | | |

| | | | | | | |

U.S. Treasury Bills - 3.7%

|

4.85%, 05/15/2025(f) | | | $1,500,000 | | | 1,462,475 |

TOTAL SHORT-TERM INVESTMENTS

(Cost $4,965,471) | | | | | | 4,971,827 |

TOTAL INVESTMENTS - 100.0% (Cost $31,336,058) | | | | | | $40,618,762 |

Other Assets in Excess of

Liabilities - 0.0%(d) | | | | | | 11,511 |

TOTAL NET ASSETS - 100.0% | | | | | | $40,630,273 |

| | | | | | | |

Percentages are stated as a percent of net assets.

CMT - Constant Maturity Treasury Rate

PLC - Public Limited Company

SA - Sociedad Anónima

SOFR - Secured Overnight Financing Rate

(a)

| Held in connection with written option contracts. See Schedule of Options Written for further information. |

(b)

| Non-income producing security. |

(c)

| Fair value determined using significant unobservable inputs in accordance with procedures established by and under the supervision of the Adviser, acting as Valuation Designee. These securities represented $3,211,727 or 7.9% of net assets as of September 30, 2024. |

(d)

| Represents less than 0.05% of net assets. |

(e)

| The rate shown represents the 7-day annualized effective yield as of September 30, 2024. |

(f)

| The rate shown is the effective yield as of September 30, 2024. |

The accompanying notes are an integral part of these financial statements.

TABLE OF CONTENTS

Concorde Wealth Management Fund

Schedule of Written Options

September 30, 2024

| | | | | | | | | | |

WRITTEN OPTIONS - (0.0)%

|

Call Options - (0.0)%(a)(b)(c)

| | | | | | | | | |

Exxon Mobil Corp., Expiration: 10/18/2024; Exercise Price: $121.00 | | | $(351,660) | | | (30) | | | $(2,820) |

Louisiana-Pacific Corp., Expiration: 10/18/2024; Exercise Price: $105.00 | | | (225,666) | | | (21) | | | (8,085) |

Microsoft Corp., Expiration: 10/18/2024; Exercise Price: $450.00 | | | (516,360) | | | (12) | | | (1,632) |

Total Call Options | | | | | | | | | (12,537) |

Put Options - (0.0)%(a)(b)(c)

| | | | | | | | | |

Moderna, Inc., Expiration: 10/18/2024; Exercise Price: $65.00 | | | (100,245) | | | (15) | | | (3,495) |

TOTAL WRITTEN OPTIONS

(Premiums received $15,645) | | | | | | | | | $ (16,032) |

| | | | | | | | | | |

Percentages are stated as a percent of net assets.

(a)

| Represents less than 0.05% of net assets. |

(b)

| 100 shares per contract. |

The accompanying notes are an integral part of these financial statements.

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

STATEMENT OF ASSETS AND LIABILITIES

September 30, 2024

| | | | |

ASSETS

| | | |

Investments in securities, at fair value (cost $31,336,058) | | | $40,618,762 |

Dividends and interest receivable | | | 77,422 |

Prepaid expenses | | | 11,963 |

Total assets | | | 40,708,147 |

LIABILITIES

| | | |

Investments in written options, at fair value (premiums received $15,645) | | | 16,032 |

Investment advisory fee payable (Note 6) | | | 26,368 |

Accrued audit fees | | | 3,019 |

Accrued directors fees and expenses | | | 500 |

Accrued other expenses | | | 31,955 |

Total liabilities | | | 77,874 |

NET ASSETS | | | $40,630,273 |

Composition of Net Assets:

| | | |

Net capital paid in on shares of capital stock | | | $28,662,871 |

Total distributable earnings | | | 11,967,402 |

Net assets | | | $40,630,273 |

Capital shares outstanding | | | 2,088,155 |

Net asset value, offering price and redemption price per share | | | $19.46 |

| | | | |

The accompanying notes are an integral part of these financial statements.

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

STATEMENT OF OPERATIONS

For the Year Ended September 30, 2024

| | | | |

Investment Income

| | | |

Dividends (net of foreign withholding taxes of $1,793) | | | $786,464 |

Interest | | | 373,101 |

Total investment income | | | 1,159,565 |

Expenses

|

Investment advisory fees (Note 6) | | | $302,565 |

Professional fees | | | 58,878 |

Administration fees (Note 7) | | | 52,870 |

Sub-transfer agent fees (Note 7) | | | 44,519 |

Fund accounting fees (Note 7) | | | 25,159 |

Transfer agent fees (Note 7) | | | 15,777 |

Insurance expense | | | 14,274 |

Printing, postage and delivery | | | 12,686 |

Custody fees (Note 7) | | | 12,287 |

Federal and state registration fees | | | 6,958 |

Directors fees and expenses | | | 2,250 |

Other expenses | | | 23,192 |

Total expenses | | | 571,415 |

Net investment income | | | 588,150 |

REALIZED AND UNREALIZED GAIN

| | | |

Net realized gain from:

| | | |

Investments | | | 3,617,779 |

Written options | | | 47,557 |

Net realized gain | | | 3,665,336 |

Net change in unrealized appreciation on:

| | | |

Investments | | | 1,328,645 |

Written options | | | 3,154 |

Net change in unrealized appreciation | | | 1,331,799 |

NET REALIZED AND UNREALIZED GAIN | | | 4,997,135 |

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | | $5,585,285 |

| | | | |

The accompanying notes are an integral part of these financial statements.

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

STATEMENTS OF CHANGES IN NET ASSETS

| | | | |

INCREASE IN NET ASSETS FROM OPERATIONS

| | | | | | |

Net investment income | | | $ 588,150 | | | $408,515 |

Net realized gain from investments, written options and capital gain distributions from investment companies | | | 3,665,336 | | | 743,153 |

Net change in unrealized appreciation on investments and written options | | | 1,331,799 | | | 748,036 |

Net increase in net assets resulting from operations | | | 5,585,285 | | | 1,899,704 |

DISTRIBUTIONS TO SHAREHOLDERS | | | (772,807) | | | (2,749,057) |

CAPITAL SHARE TRANSACTIONS

| | | | | | |

Proceeds from shares sold | | | 1,202,438 | | | 1,678,679 |

Dividends reinvested | | | 772,807 | | | 2,749,057 |

Cost of shares redeemed | | | (2,149,465) | | | (2,212,808) |

Net increase (decrease) in net assets derived from capital share

transactions | | | (174,220) | | | 2,214,928 |

Total increase in net assets | | | 4,638,258 | | | 1,365,575 |

NET ASSETS

| | | | | | |

Beginning of year | | | 35,992,015 | | | 34,626,440 |

End of year | | | $40,630,273 | | | $ 35,992,015 |

CHANGES IN SHARES OUTSTANDING

| | | | | | |

Shares sold | | | 67,196 | | | 93,657 |

Shares issued in reinvestment of distributions | | | 44,671 | | | 154,789 |

Shares redeemed | | | (120,044) | | | (127,043) |

Net increase (decrease) | | | (8,177) | | | 121,403 |

| | | | | | | |

The accompanying notes are an integral part of these financial statements.

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

FINANCIAL HIGHLIGHTS

(for a share of capital stock outstanding throughout the year)

| | | | |

PER SHARE OPERATING PERFORMANCE:

| | | | | | | | | | | | | | | |

Net asset value, beginning of year | | | $17.17 | | | $17.53 | | | $19.29 | | | $15.79 | | | $15.58 |

Income (loss) from investment operations:

| | | | | | | | | | | | |

Net investment income (loss)(a) | | | 0.28 | | | 0.20 | | | 0.36 | | | 0.06 | | | 0.12 |

Net realized and unrealized gain (loss) on investment transactions | | | 2.38 | | | 0.82 | | | (1.41) | | | 4.09 | | | 0.44 |

Total from investment operations | | | 2.66 | | | 1.02 | | | (1.05) | | | 4.15 | | | 0.56 |

Less distributions from:

| | | | | | | | | | | | | | | |

Net investment income | | | (0.37) | | | (0.06) | | | (0.26) | | | (0.17) | | | (0.22) |

Net realized gains | | | — | | | (1.32) | | | (0.45) | | | (0.48) | | | (0.13) |

Total distributions | | | (0.37) | | | (1.38) | | | (0.71) | | | (0.65) | | | (0.35) |

Net asset value, end of year | | | $19.46 | | | $17.17 | | | $17.53 | | | $19.29 | | | $15.79 |

TOTAL RETURN(b) | | | 15.41% | | | 5.57% | | | −5.40% | | | 26.61% | | | 3.54% |

RATIOS/SUPPLEMENTAL DATA:

| | | | | | | | | | | | | | | |

Net assets, end of year (in thousands) | | | $40,630 | | | $35,992 | | | $34,626 | | | $39,074 | | | $25,925 |

Ratio of expenses to average net assets | | | 1.51% | | | 1.44% | | | 1.41% | | | 1.46% | | | 1.68% |

Ratio of net investment income (loss) to average net assets | | | 1.55% | | | 1.05% | | | 1.88% | | | 0.32% | | | 0.77% |

Portfolio turnover rate | | | 30% | | | 28% | | | 28% | | | 12% | | | 36% |

| | | | | | | | | | | | | | | | |

(a)

| Based on average shares outstanding during the year.

|

(b)

| The return for the period does not include adjustments made related to valuation information obtained subsequent to period end. |

The accompanying notes are an integral part of these financial statements.

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

NOTES TO FINANCIAL STATEMENTS

September 30, 2024

Note 1 – Nature of Business and Reorganization and Summary of Significant Accounting Policies

NATURE OF BUSINESS AND REORGANIZATION

Concorde Wealth Management Fund (the “Fund”), is a diversified separate series of Concorde Funds, Inc. (the “Company”). Each series of the Company is organized as a class of common stock under the Company’s articles of incorporation. The Company was incorporated in the state of Texas in September of 1987, and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company. Each capital share in the Fund represents an equal, proportionate interest in the net assets of the Fund with each other capital share in such series and no interest in any other series. The Company may establish multiple series, each of which would be organized as a class of common stock under the Company’s articles of incorporation. The Company presently has no series other than the Fund.

The primary investment objective of the Fund are protection of capital and growth in value. The Fund is subject to various investment restrictions as set forth in the Statement of Additional Information.

SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies followed by the Fund. These policies are in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”). The Fund follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, Financial Services – Investment Companies.

VALUATION OF SECURITIES

All investments in securities are recorded at their estimated fair value, as described in Note 2.

FEDERAL INCOME TAXES

The Company’s policy is to continue to comply with the requirements of the Internal Revenue Code that are applicable to regulated investment companies and to distribute all its taxable income to its shareholders. The Company also intends to distribute sufficient net investment income and net capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. Therefore, no federal income tax or excise provision is required.

Net investment income (loss), net realized gains (losses) and the cost of investments in securities may differ for financial statement and income tax purposes. The character of distributions from net investment income or net realized gains may differ from their ultimate characterization for income tax purposes. Also, due to the timing of dividend distributions, the year in which amounts are distributed may differ from the year that the income or realized gains were recorded by the Fund. Permanent book and tax basis differences, if any, result in reclassifications to certain components of net assets. Any such reclassifications have no effect on net assets, results of operations or net asset value (“NAV”) per share.

Management has reviewed all open tax years and major tax jurisdictions and concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on returns filed or expected to be taken on a tax return. The tax returns of the Company for the prior three years are open for examination.

SECURITY TRANSACTIONS AND RELATED INCOME

Security transactions are accounted for on the trade date, the day securities are purchased or sold. Realized gains and losses from securities transactions are reported on the specific identification basis. Dividend income is recognized on the ex-dividend date, and interest income is recognized on an accrual basis. Discounts and premiums on securities purchased are accreted and amortized over the lives of the respective securities. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

DIVIDENDS AND DISTRIBUTIONS TO SHAREHOLDERS

Distributions to shareholders are determined in accordance with Federal income tax regulations and recorded on the ex-dividend date. The Fund intends to distribute all of its net investment income as dividends to its shareholders on an annual basis. The Fund intends to distribute all of its capital gains, as dividends to its shareholders on an annual basis. Distributions from net investment income and capital gains are generally declared and paid annually in December. The

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

NOTES TO FINANCIAL STATEMENTS

September 30, 2024(Continued)

treatment for financial reporting purposes of distributions made to shareholders during the year from net investment income or capital gains may differ from their ultimate treatment for Federal income tax purposes. These differences are caused primarily by differences in the timing of the recognition of certain components of income, expense or realized capital gain for Federal income tax purposes.

USE OF ESTIMATES

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

OPTION WRITING

To generate additional income or hedge against a possible decline in the value of securities it holds, the Fund may write covered call options and write put options. When the Fund writes an option, an amount equal to the premium received by the Fund is recorded as a liability and subsequently adjusted to the current fair value of the option written. Premiums received from writing options that expire unexercised are treated by the Fund on the expiration date as realized gains from options written. The difference between the premium and amount paid on effecting a closing purchase transaction, including brokerage commissions, is also treated as a realized gain or, if the premium is less than the amount paid for the closing purchase transaction, as a realized loss. If a call option is exercised, the premium is added to the proceeds from the sale of the underlying security in determining whether the Fund has realized a gain or loss. If a put option is exercised, the premium reduces the cost basis of the securities purchased by the Fund. The Fund as writer of an option bears the market risk of an unfavorable change in the price of the security underlying the written option.

The objective, as stated above, is to hedge against a possible decline in the value of securities it holds or to generate additional income when certain securities are locked in a trading range. With regards to hedging against a possible decline, the Fund may sell covered calls with strike prices below the price of a security at the time of writing the call. Regarding additional income, the Fund may sell calls on certain securities that are within a trading range, generally selling calls on securities where the strike prices are above the fair value price of the subject security.

COMMITMENTS

On February 23, 2018, the Fund executed an agreement to invest in LLR Equity Partners V, L.P., a limited partnership. The capital commitment of this investment is $1,000,000. The remaining commitment as of September 30, 2024, is $10,000 and distributions subject to recall total $142,327.

On March 15, 2019, the Fund executed an agreement to invest in LRVHealth, L.P., a limited partnership. The capital commitment of this investment is $500,000. The remaining commitment as of September 30, 2024 is $35,000.

Note 2 – Securities Valuation

Concorde Financial Corporation d/b/a Concorde Investment Management (“Concorde” or the “Advisor”) has established fair value methodologies for determining and calculating the fair value of Fund investments, in its capacity as the “valuation designee” under Rule 2a-5 of the Company Act of 1940. The Company’s Board of Directors (the “Board”) oversees the valuation designee.

The Fund utilizes various methods to measure the fair value of most of its investments on a recurring basis. FASB ASC Topic 820, Fair Value Measurements and Disclosures (“ASC 820”) defines fair value, establishes a hierarchy that prioritizes inputs to valuation techniques used to measure fair value in accordance with U.S. GAAP and requires disclosure about fair value measurements. Under ASC 820, various inputs are used in determining the value of the Fund’s investments. The three levels of inputs are as follows:

Level 1 –

Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access at the date of measurement.

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

NOTES TO FINANCIAL STATEMENTS

September 30, 2024(Continued)

Level 2 –

Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments in active markets, interest rates, credit risk, yield curves, default rates and similar data.

Level 3 –

Model derived valuations in which one or more significant inputs or significant value drivers are unobservable. Unobservable inputs are those inputs that reflect the Fund’s own assumptions that market participants would use in valuing the asset or liability at the measurement date and would be based on the best available information.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

Following is a description of the valuation techniques applied to the Fund’s major categories of assets and liabilities measured at fair value on a recurring basis.

Equity Securities – Equity securities, usually common stocks, foreign issued common stocks, exchange traded funds (“ETFs”), real estate investment trusts (“REITs”), royalty trusts, master limited partnerships and preferred stocks traded on a national securities exchange are valued at the last sale price on the exchange on which such securities are traded, as of the close of business on the day the securities are being valued or, lacking any reported sales, at the mean between the last available bid and asked price. To the extent these securities are actively traded and valuation adjustments are not applied, they are categorized in Level 1 of the fair value hierarchy.

Mutual Funds – Mutual funds, including open and closed-end funds, are generally priced at the ending NAV provided by the service agent of the mutual funds and are categorized in Level 1 of the fair value hierarchy.

Investment Funds – Investment funds that are private funds can be difficult to value, particularly to the extent that their underlying investments are not publicly traded. In the event a private fund does not report a value to the Fund on a timely basis, the Advisor will determine the fair value of the Fund’s investment based on the most recent NAV reported by the private fund, as well as any other relevant information available at the time the Fund values its investments. It is anticipated that fair value, portfolio holdings and other value information of the private funds could be available on no more than a semi-annual basis, with up to a 90 day lag. In the absence of specific transaction activity in a particular investment fund, the Advisor will consider whether it is appropriate, in light of all relevant circumstances, to value the Fund’s investment at the NAV reported by the private fund at the time of valuation or to adjust the value to reflect a premium or discount. Certain investment funds may include adjustments made subsequent to period end related to subsequent valuation information obtained. Therefore, the net assets and NAV reflected for financial statement purposes may differ from the reported NAV of the Fund as of September 30, 2024. Investment funds are categorized in Level 3 of the fair value hierarchy unless measured at fair value using the NAV per share (or its equivalent), in which case, practical expedient is used for private funds and are not categorized in the fair value hierarchy.

Debt Securities – Bonds, notes, and U.S. government obligations are valued at an evaluated bid price obtained from an independent pricing service that uses a matrix pricing method or other analytical models. Demand notes are valued at amortized cost, which approximates fair value. These securities will generally be categorized in Level 2 of the fair value hierarchy.

Short-Term Securities – Short-term equity investments, including money market funds, are valued in the manner specified above for equity securities. Fixed income securities with maturities of less than 60 days when acquired, or which subsequently are within 60 days of maturity, are valued by an independent pricing service that uses a matrix

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

NOTES TO FINANCIAL STATEMENTS

September 30, 2024(Continued)

pricing method or other analytical models. Short-term securities are generally classified in Level 1 or Level 2 of the fair value hierarchy depending on the inputs used and market activity levels for specific securities.

Derivative Instruments – Listed derivatives, including options, rights, and warrants that are actively traded are valued based on quoted prices from the exchange. If there is no such reported sale on the valuation date, the mean between the highest bid and lowest asked quotations at the close of the exchanges will be used. These securities will generally be categorized in Level 1 of the fair value hierarchy.

All other assets of the Fund are valued in such manner as the Advisor in good faith deems appropriate to reflect their fair value.

As a general matter, the fair value of the Fund’s interest in investment funds that are private funds (“Non-Traded Funds”), will represent the amount that the Fund could reasonably expect to receive from the Non-Traded Fund if the Fund’s interest was redeemed at the time of valuation, based on information reasonably available at the time the valuation is made and that the Fund believes to be reliable. Investments in Non-Traded Funds are recorded at fair value, using the Non-Traded Fund’s net asset value as a practical expedient. Based on guidance provided by FASB, investments for which fair value is measured using the NAV practical expedient are not required to be categorized in the fair value hierarchy. In the event a Non-Traded Fund does not report a value to the Fund on a timely basis, the Advisor will determine the fair value of the Fund’s investment based on the most recent value reported by the Non-Traded Fund, as well as any other relevant information available at the time the Fund values its investments. In the absence of specific transaction activity in a particular investment fund, the Advisor will consider whether it is appropriate, in light of all relevant circumstances, to value the Fund’s investment at the NAV reported by the Non-Traded Fund at the time of valuation or to adjust the value to reflect a fair value.

Securities for which market quotations are not readily available or if the closing price does not represent fair value, are valued at fair value as determined in good faith by the Advisor. Factors used in determining fair value vary by investment type and may include: trading volume of security and markets, value of other like securities and news events with direct bearing to security or market. Depending on the relative significance of the valuation inputs, these securities may be categorized in either Level 2 or Level 3 of the fair value hierarchy.

Certain restricted securities may be considered illiquid. Restricted securities are often purchased in private placement transactions, are not registered under the Securities Act of 1933, may have contractual restrictions on resale, and may be valued under methods approved by the Board as reflecting fair value. Certain restricted securities eligible for resale to qualified institutional investors, including Rule 144A securities, are not subject to the limitation on the Funds’ investments in illiquid securities if they are determined to be liquid in accordance with procedures adopted by the Board.

Additional information on each illiquid restricted security held by the Fund on September 30, 2024 is as follows:

| | | | | | | | | | | | | | | | |

LLR Equity Partners V, L.P. | | | March 14, 2018 | | | 990,000 | | | $739,531 | | | $1,548,049 | | | 3.66% |

PIMCO Flexible Credit Income Fund – Institutional Class | | | March 15, 2018 | | | 58,813 | | | 575,000 | | | 426,398 | | | 1.05 |

Pioneer ILS Interval Fund | | | August 27, 2018 | | | 117,583 | | | 1,140,000 | | | 1,140,553 | | | 2.81 |

LRVHealth, L.P. | | | July 16, 2019 | | | 477,500 | | | 420,799 | | | 410,269 | | | 1.01 |

Moran Tice 20:20 Fund, L.P. | | | July 31, 2020 | | | 250,000 | | | 250,000 | | | 282,595 | | | 0.70 |

SPAC Opportunity Partners, LLC -

Class A | | | March 24, 2021 | | | 1,000,000 | | | 1,000,000 | | | — | | | — |

RCP Select Capital Fund, L.P. | | | June 7, 2021 | | | 500,000 | | | 500,000 | | | 500,000 | | | 1.23 |

Hayman Hong Kong Opportunities Fund, L.P. | | | May 6, 2022 | | | 500,000 | | | 500,000 | | | — | | | — |

CLI Capital | | | December 20, 2022 | | | 95,455 | | | 500,000 | | | 470,814 | | | 1.16 |

| | | | | | | | | $5,625,330 | | | $4,778,678 | | | 11.62 |

| | | | | | | | | | | | | | | | |

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

NOTES TO FINANCIAL STATEMENTS

September 30, 2024(Continued)

The following table summarizes the inputs used to value the Fund’s investments measured at fair value as of September 30, 2024.

| | | | | | | | | | | | | | | | |

Investments - Assets:

| | | | | | | | | | | | | | | |

Common Stocks** | | | $— | | | $22,582,381 | | | $— | | | $ — | | | $22,582,381 |

Exchange Traded Funds | | | — | | | 2,014,436 | | | — | | | — | | | 2,014,436 |

Rights | | | — | | | 2,457 | | | — | | | — | | | 2,457 |

Closed-End Funds | | | — | | | 3,085,261 | | | — | | | — | | | 3,085,261 |

Open-End Funds | | | — | | | 602,872 | | | — | | | — | | | 602,872 |

Private Funds | | | 3,211,727^ | | | — | | | — | | | — | | | 3,211,727 |

REITs** | | | — | | | 783,720 | | | — | | | — | | | 783,720 |

Corporate Bonds** | | | — | | | — | | | 882,112 | | | — | | | 882,112 |

U.S. Treasury Securities | | | — | | | — | | | 2,481,969 | | | — | | | 2,481,969 |

Treasury Bills | | | — | | | — | | | 1,462,475 | | | — | | | 1,462,475 |

Money Market Funds | | | — | | | 3,509,352 | | | — | | | — | | | 3,509,352 |

Total Investments | | | $3,211,727 | | | $32,580,479 | | | $4,826,556 | | | $— | | | $40,618,762 |

Other Financial Instruments - Liabilities:

| | | | | | | | | | | | | | | |

Written Options | | | $— | | | $(16,032) | | | $— | | | $— | | | $(16,032) |

| | | | | | | | | | | | | | | | |

*

| Certain investments that are measured at fair value using the net asset value per share (or its equivalent) practical expedient have not been categorized in the fair value hierarchy. The fair value amounts presented in this table are intended to permit reconciliation of the fair value hierarchy to the amounts present in the schedule of investments. |

**

| See Schedule of Investments for industry classifications. |

| | | | | | | | | | | | | | | | | | | |

| | | CLI Captial | | | No | | | Not Applicable | | | To generate income from the various loans and bonds purchased. | | | Real estate investment trust (REIT) that primarily invests in direct mortgage loans and other debt obligations secured by real estate assets. They concentrate in providing mortgage financing and investing in mortgage loans of niche markets with limited competition for short-term to mid-term lending needs. The Company makes interim construction and short-term to mid-term loans for the acquisition, renovation and construction of facilities in these markets. | | | None |

| | | Hayman Hong Kong Opportunities | | | Yes | | | 30 Days | | | To generate superior risk-adjusted rates of return | | | Non-diversified portfolio investing in foreign currency forward and option contracts and options of East Asia Countries, may invest in interest rate derivatives to benefit from the stresses imposed on the Hong | | | None |

| | | | | | | | | | | | | | | | | | | |

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

NOTES TO FINANCIAL STATEMENTS

September 30, 2024(Continued)

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | Kong Monetary Authority’s Linked Exchange Rate System. Will seek to exploit opportunities in the foreign exchange and interest rate markets in Asia. | | | |

| | | LLR Equity Partners V, L.P. | | | No | | | Not Applicable | | | Capital Appreciation | | | Diversified portfolio of equity investments in lower middle market growth companies primarily focused on software and services | | | Not Applicable |

| | | LRVHealth, L.P. | | | No | | | Not Applicable | | | Capital Appreciation | | | Non-diversified portfolio of insurance-linked securities | | | Not Applicable |

| | | Moran Tice 20:20 Fund L.P. | | | Yes | | | 30 days | | | Value | | | Diversified portfolio of investments the Investment Manager believes will be influenced by macro-economic trends and/or event-driven situations. | | | None |

| | | SPAC Opportunity Partners, LLC - Class A | | | Yes | | | 93 days | | | Capital Appreciation | | | Diversified portfolio of special purpose acquisition companies, or “SPACs”. | | | 2 years |

| | | RCP Select Capital Fund, L.P. | | | No | | | Not Applicable | | | Total Return | | | Diversified portfolio of ground-up development, value-add and income producing real estate projects and real estate financings the Investment Manager expects to achieve high internal rates of return. | | | Not Applicable |

| | | | | | | | | | | | | | | | | | | |

Level 3 Reconciliation Disclosure

The Fund did not hold any investments during the year ended September 30, 2024 with significant unobservable inputs which would be classified as Level 3.

Note 3 – Derivative Instruments

The average monthly value outstanding of options written during the fiscal year ended September 30, 2024 for the Fund was $17,081.

The following is a summary of the effect of derivative instruments on the Fund’s Statements of Assets and Liabilities as of September 30, 2024:

| | | | | | | |

Written Options | | | $ — | | | $16,032 |

| | | | | | | |

The following is a summary of the effect of derivative instruments on the Fund’s Statements of Operations as of September 30, 2024:

| | | | | | | |

Written Options | | | $47,557 | | | $3,154 |

| | | | | | | |

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

NOTES TO FINANCIAL STATEMENTS

September 30, 2024(Continued)

Note 4 – Investment Transactions

Purchases and sales of investment securities, excluding U.S. government obligations and short-term investments, for the Fund during the year ended September 30, 2024, were $8,527,161 and $8,863,997, respectively.

Purchases and sales/maturities of long-term U.S. government obligations for the Fund during the year ended September 30, 2023 were $2,417,163 and $3,426,287, respectively.

Note 5 – Principal Risks

The Fund in the normal course of business makes investments in financial instruments and derivatives where the risk of potential loss exists due to changes in the market (market risk), or failure or inability of the counterparty to a transaction to perform (credit and counterparty risk). See below for a detailed description of select principal risks.

American Depositary Receipts (“ADRs”) and Global Depository Receipts (“GDRs”) Risk. ADRs and GDRs may be subject to some of the same risks as direct investment in foreign companies, which includes international trade, currency, political, regulatory and diplomatic risks. In a sponsored ADR arrangement, the foreign issuer assumes the obligation to pay some or all of the depositary’s transaction fees. Under an unsponsored ADR arrangement, the foreign issuer assumes no obligations and the depositary’s transaction fees are paid directly by the ADR holders. Because unsponsored ADR arrangements are organized independently and without the cooperation of the issuer of the underlying securities, available information concerning the foreign issuer may not be as current as for sponsored ADRs and voting rights with respect to the deposited securities are not passed through. GDRs can involve currency risk since, unlike ADRs, they may not be U.S. dollar-denominated.

Convertible Securities Risk. A convertible security is a fixed-income security (a debt instrument or a preferred stock) which may be converted at a stated price within a specified period of time into a certain quantity of the common stock of the same or a different issuer. Convertible securities are senior to common stock in an issuer’s capital structure, but they are subordinated to any senior debt securities. While providing a fixed-income stream (generally higher in yield than the income derivable from common stock but lower than that afforded by a similar non-convertible security), a convertible security also gives an investor the opportunity, through its conversion feature, to participate in the capital appreciation of the issuing company depending upon a market price advance in the convertible security’s underlying common stock.

Counterparty Risk. When the Fund enters into an investment contract, such as a derivative or a repurchase agreement, the Fund is exposed to the risk that the other party may be unable or unwilling to fulfill its obligations, which could adversely impact the value of the Fund. Contractual provisions and applicable law may prevent or delay the Fund from exercising its rights to terminate an investment or transaction with a financial institution experiencing financial difficulties, or to realize on collateral, and another institution may be substituted for that financial institution without the consent of the Fund. If the credit rating of a derivatives counterparty declines, the Fund may nonetheless choose or be required to keep existing transactions in place with the counterparty, in which event the Fund would be subject to any increased credit risk associated with those transactions.

Credit Risk. In connection with the Fund’s investments in fixed income securities, the value of the Fund may change in response to the credit ratings of the Fund’s portfolio securities. The degree of risk for a particular security may be reflected in its credit rating. Generally, investment risk and price volatility increase as a security’s credit rating declines. Credit risk is the risk that the issuer of a bond will fail to make payments when due or default completely. If the issuer of the bond experiences an actual or anticipated deterioration in credit quality, the price of the bond may be negatively impacted. The degree of credit risk depends on the financial condition of the issuer and the terms of the bond.

Debt/Fixed Income Securities Risk. An increase in interest rates typically causes a fall in the value of the debt securities in which the Fund may invest. The value of your investment in the Fund may change in response to changes in credit ratings of the Fund’s portfolio of debt securities. Current market conditions pose heightened risks for funds that invest in debt securities given the current interest rate environment. Any future interest rate increases or other adverse conditions (e.g., inflation/deflation, increased selling of certain fixed-income investments across other pooled investment vehicles or accounts, changes in investor perception, or changes in government intervention in the markets) could cause the value of the Fund’s investments in debt securities to decrease. Moreover, rising interest rates or lack of market participants may lead to decreased liquidity in the bond and loan markets, making it more difficult for the Fund

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

NOTES TO FINANCIAL STATEMENTS

September 30, 2024(Continued)

to sell its holdings at a time when the Fund’s manager might wish to sell. Lower rated securities (“junk bonds”) are generally subject to greater risk of loss of your money than higher rated securities. Debt securities are also subject to prepayment risk when interest rates decrease. Prepayment risk is the risk that the borrower will prepay some or all of the principal owed to the issuer. If prepayment occurs, the Fund may have to replace the security by investing the proceeds in a less attractive security. Many debt securities previously utilized LIBOR as the reference or benchmark rate for variable interest calculations. As of June 30, 2023, the ICE Benchmark Administration (“IBA”), as LIBOR administrator, ceased publication of U.S. dollar (“USD”) LIBOR for the most common tenors (overnight and one, three, six and twelve months), and as of December 31, 2021, the IBA had ceased publication of USD LIBOR for the less commonly used tenors of one week and two months as well as all tenors of non-USD LIBOR. Until September 30, 2024, the IBA will continue to publish the one-month, three month and six-month USD LIBOR tenors using a synthetic methodology that is permanently unrepresentative of the underlying markets such tenors previously sought to measure. The U.S. Congress passed the Adjustable Interest Rate (LIBOR) Act on March 15, 2022. The LIBOR Act replaces references to LIBOR for U.S. contracts that did not mature before June 30, 2023 with benchmark replacements based on the Secured Overnight Financing Rate (“SOFR”). SOFR is a broad measure of the cost of borrowing cash overnight collateralized by U.S. Treasury securities and is published daily by the Federal Reserve Bank of New York. The benchmark replacement rate may not have the same value or economic equivalence as LIBOR. The transition from LIBOR could have a significant impact on the financial markets, including increased volatility and illiquidity in markets for instruments that currently rely on LIBOR to determine interest rates and a reduction in the values of some LIBOR-based investments. The transition to an alternative interest rate may not be orderly, may occur over various time periods or may have unintended consequences.

Emerging Markets Risk. The Fund may invest in emerging markets, which may carry more risk than investing in developed foreign markets. Risks associated with investing in emerging markets include limited information about companies in these countries, greater political and economic uncertainties compared to developed foreign markets, underdeveloped securities markets and legal systems, potentially high inflation rates, and the influence of foreign governments over the private sector.

Equity and General Market Risk. Equities, such as common stocks, or other equity related investments are susceptible to general stock market fluctuations and to volatile increases and decreases in value. The stock market may experience declines or stocks in the Fund’s portfolio may not increase their earnings at the rate anticipated. The Fund’s NAV and investment return will fluctuate based upon changes in the value of its portfolio securities. A rise in protectionist trade policies, slowing global economic growth, risks associated with the United Kingdom’s exit from the European Union, the trade dispute between the United States and China, the risk of trade disputes with other countries, and the possibility of changes to some international trade agreements, could affect the economies of many nations, including the United States, in ways that cannot necessarily be foreseen at the present time, and may negatively impact the financial markets.

These developments as well as other events could result in further market volatility and negatively affect financial asset prices, the liquidity of fixed income or other securities held by the Fund and the normal operations of securities exchanges and other markets, despite government efforts to address market disruptions. The investment adviser will monitor developments and seek to manage the Fund in a manner consistent with achieving the Fund’s investment objective, but there can be no assurance that it will be successful in doing so.

Exchange Traded Fund Risk. ETFs may trade at a discount to the aggregate value of the underlying securities and although expense ratios for ETFs are generally low, frequent trading of ETFs by the Fund can generate brokerage expenses. Shareholders of the Fund will indirectly be subject to the fees and expenses of the individual ETFs in which the Fund invests, in addition to the Fund’s own fees and expenses.

Foreign Securities Risk. The Fund may invest in foreign securities and, if so, it will be subject to risks associated with foreign markets, such as adverse political, currency, social and economic developments; accounting standards or governmental supervision that are not consistent with that to which U.S. companies are subject; limited information about foreign companies; less liquidity in foreign markets; and less protection. In addition, policy and legislative changes in foreign countries and other events affecting global markets, such as the United Kingdom’s exit from the European Union (or Brexit), may contribute to decreased liquidity and increased volatility in the financial markets.

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

NOTES TO FINANCIAL STATEMENTS

September 30, 2024(Continued)

High Yield Risk. The Fund’s investment program permits it to invest in non-investment grade debt obligations, sometimes referred to as “junk bonds” (hereinafter referred to as “lower-quality securities”). Lower-quality securities are those securities that are rated lower than investment grade and unrated securities believed by the Advisor to be of comparable quality. Although these securities generally offer higher yields than investment grade securities with similar maturities, lower-quality securities involve greater risks, including the possibility of default or bankruptcy. In general, they are regarded to be more speculative with respect to the issuer’s capacity to pay interest and repay principal.

Investments in Other Investment Companies Risk. Shareholders of the Fund will indirectly be subject to the fees and expenses of the other investment companies in which the Fund invests and these fees and expenses are in addition to the fees and expenses that Fund shareholders directly bear in connection with the Fund’s own operations. In addition, shareholders will be exposed to the investment risks associated with investments in other investment companies.

Liquidity Risk. Certain securities held by the Fund may be difficult (or impossible) to sell at the time and at the price the Fund would like. As a result, the Fund may have to hold these securities longer than it would like and may forego other investment opportunities. There is the possibility that the Fund may lose money or be prevented from realizing capital gains if it cannot sell a security at a particular time and price.

Private Funds Risk. The sale or transfer of investments in private funds may be limited or prohibited by contract or law. Private funds are generally fair valued in good faith by the Advisor, as they are not traded frequently. The Fund may be required to hold such positions for several years, if not longer, regardless of valuation, which may cause the Fund to be less liquid.

Private Placement Risk. The Fund may invest in privately issued securities of domestic common and preferred stock, convertible debt securities, ADRs and REITs, including those which may be resold only in accordance with Rule 144A under the Securities Act of 1933, as amended. Privately issued securities are restricted securities that are not publicly traded. Delay or difficulty in selling such securities may result in a loss to the Fund. Privately issued securities and other restricted securities will have the effect of increasing the level of Fund illiquidity to the extent that the Fund finds it difficult to sell these securities when the Advisor believes it is desirable to do so, especially under adverse market or economic conditions or in the event of adverse changes in the financial condition of the issuer, and the prices realized could be less than those originally paid or less than the fair market value. At times, the illiquidity of the market, as well as the lack of publicly available information regarding these securities also may make it difficult to determine the fair value of such securities for purposes of computing the NAV of the Fund.

Real Estate Investment Trust and Real Estate Risk. The value of the Fund’s investments in REITS may change in response to changes in the real estate market such as declines in the value of real estate, lack of available capital or financing opportunities, and increases in property taxes or operating costs.

Security Selection Risk. The Advisor may misjudge the risk and/or return potential of a security. This misjudgment can result in a loss or a significant deviation relative to its benchmarks.

Smaller and Medium Capitalization Company Risk. Securities of smaller and medium-sized companies may be more volatile and more difficult to liquidate during market downturns than securities of larger companies. Additionally, the price of smaller companies may decline more in response to selling pressures.

Style Risk. The Advisor generally follows an investing style that favors value investments. The value investing style may, over time, go in and out of favor. At time when the value investing style is out of favor, the Fund may underperform other funds that use different investing styles. Investors should be prepared to tolerate volatility in Fund returns.

Note 6 – Investment Advisory Fees and Transactions with Affiliate

The Company has an Investment Advisory Agreement with Concorde to act as the Fund’s investment advisor. The Advisor provides the Fund with investment management and advisory services consistent with the Fund’s investment objectives, policies and restrictions, supervises the purchase and sale of investment transactions and administers the business and administrative operations of the Fund. For such services, for the period ended September 30, 2024, Concorde received an annual fee of 0.80% of the Fund’s average daily net assets, computed daily and paid on a monthly basis. The investment advisory fee was $302,565 for the year ended September 30, 2024, of which $26,368 was payable at September 30, 2024. Certain officers and directors of the Company are also officers and directors of Concorde.

TABLE OF CONTENTS

CONCORDE WEALTH MANAGEMENT FUND

NOTES TO FINANCIAL STATEMENTS

September 30, 2024(Continued)

Note 7 – Service Organizations

U.S. Bancorp Fund Services, LLC, doing business as U.S. Bank Global Fund Services (“Fund Services”), provides the Fund with administrative, fund accounting, and transfer agent services. U.S. Bank, N.A., (“USB”) an affiliate of Fund Services, serves as the Fund’s custodian. Fees incurred by the Fund to Fund Services and USB during the period ended September 30, 2024, were $96,806 and $12,287, respectively, of which $15,844, and $3,145, respectively, were payable at September 30, 2024.

The Company has an administrative agreement with National Financial Services, LLC (“NFS”). The agreement provides for monthly payments by the Fund to NFS for providing certain shareholder services (sub-transfer agent fees). Sub-transfer agent fees incurred by the Fund to NFS for the year ended September 30, 2024 were $44,519, of which $7,507 was payable at September 30, 2024.

Note 8 – Federal Tax Information

At September 30, 2024, the Fund’s most recent fiscal year end, the Fund’s investments and components of total distributable earnings on a tax basis were as follows:

| | | | |

Federal Tax Cost of Investments | | | $32,202,319 |

Gross Tax Unrealized Appreciation | | | $11,308,682 |

Gross Tax Unrealized Depreciation | | | (2,949,066) |

Net Tax Unrealized Appreciation | | | 8,359,616 |

Undistributed Ordinary Income | | | 267,576 |

Undistributed Long-Term Gains | | | 3,283,766 |

Other Accumulated Gain | | | (387) |

Total Distributable Earnings | | | $11,910,571 |

| | | | |

The difference between book-basis and tax-basis net unrealized appreciation is primarily attributable to the realization for tax purposes of the unrealized gains on an investment in a passive foreign investment company and adjustments to the tax basis of investments in partnerships.

At September 30, 2024, the Fund’s fiscal year end, the Fund had no tax basis capital loss carryovers to offset future capital gains. The Fund did not utilize a capital loss carryover during the year ended September 30, 2024, the Fund’s fiscal year end. The Fund had no late year loss deferrals and no post-October loss.

The tax character of distributions paid during the year ended September 30, 2024 and year ended September 30, 2023 was as follows:

| | | | |

Ordinary income(1) | | | $772,807 | | | $257,082 |

Long-term capital gain | | | — | | | 2,491,975 |

| | | $772,807 | | | $2,749,057 |

| | | | | | | |

(1)

| Ordinary income includes short-term capital gains. |

Note 9 – Subsequent Events

Management has evaluated the Fund’s events and transactions that occurred subsequent September 30, 2024, through the date of issuance of the Fund’s financial statements. There were no events or transactions that occurred during this period that materially impacted the amounts or disclosures in the Fund’s financial statements.

TABLE OF CONTENTS

Report of Independent Registered Public Accounting Firm

Board of Directors and Shareholders

Concorde Wealth Management Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Concorde Wealth Management Fund, a series of Concorde Funds, Inc., including the schedule of investments in securities and written options, as of September 30, 2024, and the related statements of operations and changes in net assets and the financial highlights for the year then ended, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of Concorde Wealth Management Fund as of September 30, 2024, and the results of its operations, the changes in net assets, and the financial highlights for the year then ended in conformity with accounting principles generally accepted in the United States of America.

The financial statements and financial highlights of Concorde Wealth Management Fund as of and for the year ended September 30, 2023, and prior, were audited by other auditors whose report dated November 29, 2023, expressed an unqualified opinion on those statements.

Basis for Opinion

These financial statements are the responsibility of the entity’s management. Our responsibility is to express an opinion on these financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to Concorde Wealth Management Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2024 by correspondence with the custodian, transfer agent and brokers. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provides a reasonable basis for our opinion.

We have served as Concorde Wealth Management Fund’s auditor since 2024.

WEAVER AND TIDWELL, L.L.P.

Fort Worth, Texas

November 27, 2024

TABLE OF CONTENTS

Item 8. Changes in and Disagreements with Accountants for Open-End Investment Companies.

Effective August 15, 2024, the Board of Directors of Concorde Funds, Inc. engaged Weaver and Tidwell, LLP (“Weaver”) to serve as the independent registered public accounting firm to audit the financial statements of the Concorde Wealth Management Fund for the fiscal year ending September 30, 2024, replacing Brad A. Kinder, CPA (“Kinder”).

Kinder’s reports on the Fund’s financial statements for each of the fiscal years ended September 30, 2022, and September 30, 2023, contained no adverse opinion or disclaimer of opinion nor were they qualified or modified as to uncertainty, audit scope or accounting principles. During the Funds’ fiscal years ended September 30, 2022 and September 30, 2023 and the interim period October 1, 2023 through August 15, 2024 (the “Interim Period”), (i) there were no disagreements with Kinder on any matter of accounting principles or practices, financial statement disclosure or auditing scope or procedure, which disagreements, if not resolved to the satisfaction of Kinder, would have caused Kinder to make reference to the subject matter of the disagreements in connection with its reports on the Funds’ financial statements for such years, and (ii) there were no “reportable events” of the kind described in Item 304(a)(1)(v) of Regulation S-K under the Securities Exchange Act of 1934, as amended.

During the Funds’ fiscal years ended September 30, 2022 and September 30, 2023 and the Interim Period, neither the Fund nor anyone on its behalf has consulted Weaver on items which (i) concerned the application of accounting principles to a specified transaction, either completed or proposed, or the type of audit opinion that might be rendered on the Funds’ financial statements or (ii) concerned the subject of a disagreement (as defined in paragraph (a)(1)(iv) of Item 304 of Regulation S-K and related instructions) or reportable events (as described in paragraph (a)(1)(v) of said Item 304). The selection of Weaver does not reflect any disagreements or dissatisfaction by the Fund or the Board with the performance of Kinder.

The Fund requested that Kinder furnish it with a letter addressed to the Securities and Exchange Commission stating whether Kinder agrees with the statements contained above. A copy of the letter from Kinder to the Securities and Exchange Commission is filed as an exhibit hereto.

Item 9. Proxy Disclosure for Open-End Investment Companies.

There were no matters submitted to a vote of shareholders during the period covered by this report.

Item 10. Remuneration Paid to Directors, Officers, and Others of Open-End Investment Companies.

See Item 7(a).

Item 11. Statement Regarding Basis for Approval of Investment Advisory Contract.

At its meeting held on May 30, 2024, the Board of Directors (the “Board”) of Concorde Funds, Inc. (the “Company”), including all the Directors who are not “interested persons” (as defined in the Investment Company Act of 1940), considered and then voted to approve the renewal of the investment advisory agreement (the “Advisory Agreement”) between Concorde Financial Corporation (the “Advisor”) and the Company, on behalf of the Concorde Wealth Management Fund (the “Fund”). In connection with its approval of the continuation of the Advisory Agreement, the Board reviewed and discussed the specific services provided by the Advisor. The Board considered the following factors, among others:

The Advisor:

1)

| Provides daily investment management for the Concorde Wealth Management Fund. In providing investment management, Concorde Financial Corporation oversees the trading of securities and the rebalancing of the portfolio. |

2)

| Retains the services of the Fund’s Chief Compliance Officer and makes all reasonable efforts to insure that the Fund is in compliance with the securities laws. |

3)

| Provides responsive customer and shareholder servicing which consists of responding to shareholder inquiries received, including specific mutual fund account information, in addition to calls directed to the transfer agent call center. |

4)

| Oversees distribution of the Fund through third-party broker/dealers and independent financial institutions. |

5)

| Oversees those third party service providers that support the Fund in providing fund accounting, fund administration, transfer agency and custodial services. |

TABLE OF CONTENTS