UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark one)

xAnnual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2006 or

oTransition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

for the transition period from to .

Commission file no. 0-16469

Inter Parfums, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 13-3275609 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| | |

| 551 Fifth Avenue, New York, New York | 10176 |

| (Address of Principal Executive Offices) | (Zip Code) |

Registrant's telephone number, including area code: 212.983.2640.

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of exchange on which registered |

| | |

Common Stock, $.001 par value per share | The Nasdaq Stock Market, LLC |

Securities registered pursuant to Section 12(g) of the Act:

None.

Title of Class

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation SK is not contained herein and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10K or any other amendment to this Form 10K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filed. See definition of “accelerated filer” and “large accelerated filer” in Rule 12b-2 of the Exchange Act).

Large accelerated Filer o | Accelerated filer x | Non-accelerated filer o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant's most recently completed second fiscal quarter. $147,451,000 of voting equity and $-0- of non-voting equity.

Indicate the number of shares outstanding of the registrant's $.001 par value common stock as of the close of business on the latest practicable date March 5, 2007: 20,437,292.

Documents Incorporated By Reference: None.

Table of Contents |

| | Page |

| | |

Note on Forward Looking Statements | |

| | |

PART I | | |

| | | |

| Item 1. | Business | 1 |

| | | |

| Item 1A. | Risk Factors | 14 |

| | | |

| Item 1B. | Unresolved Staff Comments | 19 |

| | | |

| Item 2. | Properties | 20 |

| | | |

| Item 3. | Legal Proceedings | 21 |

| | | |

| Item 4. | Submissions of Matters to a Vote of Security Holders | 21 |

| | | |

PART II | | |

| | | |

| Item 5. | Market for Registrant’s Common Equity and Related Stockholder Matters | 22 |

| | | |

| Item 6. | Selected Financial Data | 24 |

| | | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 25 |

| | | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 35 |

| | | |

| Item 8. | Financial Statements and Supplementary Data | 36 |

| | | |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 37 |

| | | |

| Item 9A. | Controls and Procedures | 37 |

| | | |

| Item 9B. | Other Information | 39 |

| | | |

PART III | | |

| | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | 40 |

| | | |

| Item 11. | Executive Compensation | 46 |

| | | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 60 |

| | | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 63 |

| | | |

| Item 14. | Principal Accountant Fees and Services | 64 |

| | | |

PART IV | | |

| | | |

| Item 15. | Exhibits and Financial Statement Schedules | 66 |

| | | |

FINANCIAL STATEMENTS | F-1 |

| | |

SIGNATURES | |

FORWARD LOOKING STATEMENTS

This report includes forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, and if incorporated by reference into a registration statement under the Securities Act of 1933, as amended, within the meaning of Section 27A such act. When used in this report, the words “anticipate,” “believe,” “estimate,” “will,” “should,” “could,” “may,” “intend,” “expect,” “plan,” “predict,” “potential,” or “continue” or similar expressions identify certain of such forward-looking statements. Although we believe that our plans, intentions and expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such plans, intentions or expectations will be achieved.

Actual results, performance or achievements could differ materially from those contemplated, expressed or implied by the forward-looking statements contained in this report. Important factors that could cause actual results to differ materially from our forward-looking statements are set forth in this report, including under the heading “Risk Factors”. Such factors include dependence upon Burberry for a significant portion of our sales, continuation and renewal of existing license agreements, sales and marketing efforts of The Gap, Inc., protection of our intellectual property rights, effectiveness of sales and marketing efforts and product acceptance by consumers, dependence upon third party manufacturers and distributors, dependence upon management, competition, currency fluctuation and international tariff and trade barriers, governmental regulation and possible liability for improper comparative advertising or “Trade Dress”.

These factors are not intended to represent a complete list of the general or specific factors that may affect us. It should be recognized that other factors, including general economic factors and business strategies, may be significant, presently or in the future, and the factors set forth herein may affect us to a greater extent than indicated. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements set forth in this report. Except as required by law, we undertake no obligation to update any forward-looking statement, whether as a result of new information, future events or otherwise.

PART I

Item 1. Business

Introduction

We are Inter Parfums, Inc. We operate in the fragrance business, and manufacture, market and distribute a wide array of fragrances and fragrance related products. Organized under the laws of the State of Delaware in May 1985 as Jean Philippe Fragrances, Inc., we changed our name to Inter Parfums, Inc. on July 14, 1999. We have also retained our brand name, Jean Philippe Fragrances, for some of our mass-market products.

Our worldwide headquarters and the office of our three (3) wholly-owned subsidiaries, Jean Philippe Fragrances, LLC and Inter Parfums USA, LLC, both New York limited liability companies, and Nickel USA, Inc., a Delaware corporation, are located at 551 Fifth Avenue, New York, New York 10176, and our telephone number is 212.983.2640. Our consolidated wholly-owned subsidiary, Inter Parfums Holdings, S.A., its majority-owned subsidiary, Inter Parfums, S.A., and its two (2) wholly-owned subsidiaries, Inter Parfums Grand Public, S.A., and Inter Parfums Trademark, S.A., and its majority-owned subsidiary, Nickel, S.A., maintain executive offices at 4, Rond Point des Champs Elysees, 75008 Paris, France. Our telephone number in Paris is 331.5377.0000.

Our common stock is listed on The Nasdaq Global Select Market under the trading symbol "IPAR" and we are considered a “controlled company” under the applicable rules of The Nasdaq Stock Market. The common shares of our subsidiary, Inter Parfums S.A., are traded on the Euronext Exchange.

We maintain our internet website at www.interparfumsinc.com which is linked to the SEC Edgar database. You can obtain through our website, free of charge, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange as soon as reasonably practicable after we have electronically filed with or furnished them to the SEC.

Summary

The following summary is qualified in its entirety by and should be read together with the more detailed information and audited financial statements, including the related notes, contained or incorporated by reference in this report.

We operate in the fragrance business and manufacture, market and distribute a wide array of fragrances and fragrance related products. We manage our business in two segments, European based operations and United States based operations. Our prestige fragrance products are produced and marketed by our European operations through our 72% owned subsidiary in Paris, Inter Parfums, S.A., which is also a publicly traded company as 28% of Inter Parfums, S.A. shares trade on the Euronext. Prestige cosmetics and prestige skin care products represent less than 3% of consolidated net sales.

We produce and distribute our prestige fragrance products primarily under license agreements with brand owners and prestige product sales represented approximately 84% of net sales for 2006. We have built a portfolio of brands, which include Burberry, Lanvin, Paul Smith, S.T. Dupont, Christian Lacroix, Quiksilver/Roxy, Van Cleef & Arpels and Nickel whose products are distributed in over 120 countries around the world. Burberry is our most significant license, sales of Burberry products represented 57%, 60% and 62% of net sales for the years ended December 31, 2006, 2005 and 2004, respectively.

Our prestige products focus on niche brands with a devoted following. By concentrating in markets where the brands are known, Inter Parfums has had many successful launches. We typically launch new fragrance families for our brands every 2-3 years, with some frequent “seasonal” fragrances introduced as well.

Our specialty retail and mass-market fragrance and fragrance related products are marketed through our United States operation and represented 16% of sales for the year ended December 31, 2006. These fragrance products are sold under trademarks owned by us or pursuant to license or other agreements with the owners of the Gap, Banana Republic, Aziza and Jordache trademarks.

The creation and marketing of each product family is intimately linked with the brand���s name, its past and present positioning, customer base and, more generally, the prevailing market atmosphere. Accordingly, we generally study the market for each proposed family of fragrance products for almost a full year before we introduce any new product into the market. This study is intended to define the general position of the fragrance family and more particularly its scent, bottle, packaging and appeal to the buyer. In our opinion, the unity of these four elements of the marketing mix makes for a successful product.

Over the past five years, we have grown our business at both the top line and the bottom line. We have grown from $130.4 million in sales in 2002 to $321.1 million in 2006, representing a compounded annual growth rate of 25%. During the same period, our net income grew from $9.4 million in 2002 to $17.7 million in 2006, representing a compounded annual growth rate of 17%. Our management targets organic long term sales growth of approximately 10% (measured on an annual basis) and long term net income growth of approximately 12% - 15% (measured on an annual basis). There can be no assurance that we will achieve these targets in any particular period, or at all, however.

2006 Developments

Van Cleef & Arpels

In September 2006, our Paris-based subsidiary, Inter Parfums, S.A., and Van Cleef & Arpels Logistics SA, entered into an exclusive, worldwide license agreement for the creation, development and distribution of fragrance and related bath and body products under the Van Cleef & Arpels brand and related trademarks. The term of the license expires on December 31, 2018, and each party has the right to extend the term for five years on or before June 1, 2018 if certain sales targets are met in year 2017. Our rights under such license agreement are subject to certain minimum advertising expenditures and royalty payments as are customary in our industry.

In January 2007 Inter Parfums S.A. paid €18 million (approximately $23.4 million) to Van Cleef & Arpels Logistics SA as a lump sum, up front royalty payment, and purchased the existing inventory held by YSL Beauté, the former licensee, for approximately $2.1 million.

Quiksilver/Roxy

In March 2006 our Paris-based subsidiary, Inter Parfums S.A., and QS Holdings SARL signed an exclusive worldwide license agreement for the creation, development and distribution of fragrance, suncare, skincare and related products under the Roxy brand and suncare and related products under the Quiksilver brand. The term of the license expires in December 2017. Our rights under such license agreement are subject to certain minimum advertising expenditures and royalty payments as are customary in our industry.

Gap and Banana Republic

In March 2006, we entered into an addendum to our exclusive agreement with Gap, whereby we obtained the additional rights to develop, produce, manufacture and distribute personal care and home fragrance products for Gap Outlet and Banana Republic Factory Stores in the United States and Canada.

In September 2006, we launched the Banana Republic Discover Collection, a family of five fragrances, we developed and supply to Banana Republic’s North American stores. The collection consists of three scents for women and two for men, each named after a luxurious, natural material that is both emotional and authentic. A separate family of fragrance and personal care products is also in the works for Gap’s North American stores. That fragrance family is scheduled for an initial launch in May 2007, with the rollout continuing throughout the balance of the year and into 2008. In addition, we have been supplying Banana Republic and Gap stores with their existing personal care products, and we have created new holiday programs for this past holiday season.

Our Prestige Products

We produce and distribute our prestige fragrance products primarily under license agreements with brand owners and prestige product sales represented approximately 84% of net sales for 2006. We have built a portfolio of brands, which include Burberry, Lanvin, Paul Smith, S.T. Dupont, Christian Lacroix, Quiksilver/Roxy, Van Cleef & Arpels and Nickel whose products are distributed in over 120 countries around the world. Burberry is our most significant license, sales of Burberry products represented 57%, 60% and 62% of net sales for the years ended December 31, 2006, 2005 and 2004, respectively.

Under license agreements, we obtain the right to use the brand name, create new fragrances and packaging, determine positioning and distribution, and market and sell the licensed products, in exchange for the payment of royalties. Our rights under license agreements are also generally subject to certain minimum sales requirements and advertising expenditures.

The following is a summary of the prestige brand names owned or licensed by us:

Brand Name | Licensed Or Owned | Date Acquired | Term, Including Option Periods |

| Burberry | Licensed | July 2004 | 12.5 years and additional 5-year optional term that requires mutual consent |

| Lanvin | Licensed | July 2004 | 15-year |

| S.T. Dupont | Licensed | July 1997 | Through June 30, 2011. |

| Paul Smith | Licensed | Dec. 1998 | 12 years |

| Celine | Licensed | May 2000 | Through December 31, 2007. |

| Nickel | Owned | April 2004 | N/A |

| Christian Lacroix | Licensed | March 1999 | 11 years |

| Quiksilver/Roxy | Licensed | March 2006 | Through December 31, 2017 |

| Van Cleef & Arpels | Licensed | Oct. 2006 | Through December 31, 2018, plus a 5-year option if certain sales targets are met |

Prestige Fragrances

BURBERRY -- Burberry is our leading prestige fragrance brand and we operate under an exclusive worldwide license with Burberry Limited that was originally entered into in 1993 and replaced by a new agreement in 2004.

We have had significant success in introducing new fragrance families under the Burberry brand name. We have introduced several fragrance families including Burberry, Burberry Week End, Burberry Touch, Burberry Brit and Burberry London. Successful distribution has been achieved in more than a hundred countries around the world by differentiating the positioning and target consumer of each of the families. Our success is evidenced by a 32% five-year compounded annual growth rate in sales of fragrances under the Burberry brand since 2001.

The largest Burberry fragrance family, Burberry Brit, of which the women’s scent was launched in fall 2003 and the men’s scent launched in fall 2004, has received much industry recognition. Burberry Brit for Women was named the Fragrance of the Year in the Women’s Luxe category at the Annual Fragrance Foundation FiFi Awards in 2004. Burberry Brit for Men received two awards at the Annual Fragrance Foundation FiFi Awards in April 2005 for Best Men’s Fragrance in the Luxe category and for Best Print National Advertising Campaign of the Year. The most recent Burberry fragrance family, Burberry London, of which the women’s scent was launched in fall 2005 and the men’s scent launched in spring of 2006, has also been well received. The success of the Burberry London launch and subsequent rollout was slightly offset by a modest decline by other fragrances within the brand. As the Burberry brand continues to develop and expand by attracting new customers, the Burberry fragrance portfolio follows suit expanding and continuing to post sales growth.

LANVIN -- In June 2004, Inter Parfums S.A. and Lanvin S.A. signed a worldwide license agreement to create, develop and distribute fragrance lines under the Lanvin brand name. A synonym of luxury and elegance, the Lanvin fashion house, founded in 1889 by Jeanne Lanvin, expanded into fragrances in the 1920s. Today, Lanvin fragrances occupy important positions in the selective distribution market in France, Europe and Asia, particularly with the lines Arpège (created in 1927), Lanvin L’Homme (1997) and Eclat d’Arpège (2002). Our first Lanvin fragrance, Arpège pour Homme, debuted in late 2005. Arpège by Lanvin won the honor of entering the Fragrance Hall of Fame at the 2005 FiFi Awards, an honor given to the best fragrance sold for at least 15 years that has been revitalized. During 2006, we began the launch Rumeur, our first new Lanvin fragrance for women, which was followed by a wider geographic rollout over the early months of 2007. In addition to the successful debut of Lanvin Rumeur, solid sales gains made by Éclat d’Arpège which has been a strong seller since its introduction in 2002.

PAUL SMITH -- We signed an exclusive license agreement with Paul Smith in December 1998, our first designer fragrance, for the creation, manufacture and worldwide distribution of Paul Smith perfumes and cosmetics. Paul Smith is an internationally renowned British designer who creates fashion with a clear identity. Paul Smith has a modern style which combines elegance, inventiveness and a sense of humor and enjoys a loyal following, especially in the UK and Japan. Fragrances include: Paul Smith, Paul Smith Extreme and Paul Smith London. Paul Smith London for Men was awarded a FiFi award in April 2005 for Best Men’s Fragrance in the Nouveau Niche category. In the fourth quarter of 2006 we launched the men’s fragrance, Paul Smith Story, and in the Fall of 2007, we have scheduled the launch of a new women’s fragrance for Paul Smith.

S.T. DUPONT -- In June 1997, we signed an exclusive license agreement with S.T. Dupont for the creation, manufacture and worldwide distribution of S.T. Dupont perfumes. Fragrances include: S.T. Dupont Paris, S.T. Dupont Essence Pure and L’Eau de S.T. Dupont. During 2006 we extended the term of this license until June 30, 2011. In addition, during 2006 we launched the new men’s fragrance, S.T. Dupont Noir, which was received well in Eastern Europe and the Middle East. For 2007 we are planning to launch a new women’s fragrance for S.T. Dupont.

CHRISTIAN LACROIX -- In March 1999, we entered into an exclusive license agreement with the Christian Lacroix Company, formerly a division of LVMH Moet Hennessy Louis Vuitton S.A., for the worldwide development, manufacture and distribution of perfumes. For us, this association with a prestigious fashion label is another key area for growth which we expect will further strengthen our position in the prestige fragrance market. Our Christian Lacroix fragrances families for both men and women include: Eau Florale, Bazar and Tumulte. A new women’s fragrance for is slated for Spring 2007.

VAN CLEEF & ARPELS -- In September 2006, our Paris-based subsidiary, Inter Parfums, S.A., and Van Cleef & Arpels Logistics SA, entered into an exclusive, worldwide license agreement for the creation, development and distribution of fragrance and related bath and body products under the Van Cleef & Arpels brand and related trademarks. The term of the license expires on December 31, 2018. We believe this agreement with Van Cleef & Arpels, the prestigious and legendary world-renowned jewelry designer, is an important step in our development. We also believe its growth potential will strengthen opportunities for expansion of our fragrance business in the high luxury segment. In 1976, Van Cleef & Arpels was a pioneer among jewelers with its launch of the fragrance, First, which exemplified the tradition of boldness of the jewelry house. We plan to build upon sales base by promoting the two strongest families, First and Tsar, and then create an entirely new line for launch in 2008.

QUIKSILVER/ROXY -- In March 2006 our Paris-based subsidiary, Inter Parfums S.A., and QS Holdings SARL signed an exclusive worldwide license agreement for the creation, development and distribution of fragrance, suncare, skincare and related products under the Roxy brand and suncare and related products under the Quiksilver brand. The term of the license expires in December 2017.

We intend to develop entirely new product categories for each of the two brands, which are important brands for the global youth market and synonymous with the heritage and culture of surfing, skateboarding and snowboarding. Quiksilver Inc.’s apparel and footwear brands represent a casual lifestyle for young-minded people that connect with its board riding culture and heritage, while its winter sports and golf brands symbolize a long-standing commitment to technical expertise and competitive success on the mountains and on the links.

Our initial plans call for the first new product family under the agreement, a Roxy fragrance family, to be introduced in late 2007, followed by a Quiksilver suncare line.

CELINE -- In May 2000, we entered into an exclusive worldwide license agreement for the development, manufacturing and distribution of fragrance lines under the Celine brand name with Celine, a division of LVMH Moet Hennessy Louis Vuitton S.A. Celine, a French luxury fashion and accessory company is known throughout the world for its luxury and quality products. By mutual agreement with Celine, we agreed to terminate the license on December 31, 2007.

Prestige Skin Care

NICKEL -- In April 2004 Inter Parfums, S.A. acquired a 67.5% interest in Nickel S.A. Established in 1996 by Philippe Dumont, Nickel has developed two innovative concepts in the world of cosmetics: spas exclusively for male customers and skin care products for men. The Nickel skin care products for the face and body are sold through prestige department and specialty stores primarily in France, the balance of Western Europe and in the United States, as well as through our men’s spas in Paris and New York.

After the opening of a licensed Nickel Spa in London in spring 2006, similar initiatives for Berlin, Dubai and Moscow are currently under consideration. However, we cannot assure you that any further licensed spas will be opened, or if opened, that they will generate substantial revenue.

Specialty Retail and Mass Market Products

In July 2005, we entered into an exclusive agreement with The Gap, Inc. to develop, produce, manufacture and distribute fragrance, personal care and home fragrance products for Gap and Banana Republic brand names to be sold in Gap and Banana Republic retail stores in the United States and Canada.

In March 2006, we entered into an addendum to our exclusive agreement with The Gap, Inc, whereby we obtained the additional rights to develop, produce, manufacture and distribute fragrance, personal care and home fragrance products for Gap Outlet and Banana Republic Factory Stores in the United States and Canada.

In September 2006, we launched the Banana Republic Discover Collection, a family of five fragrances, we developed and supply to Banana Republic’s North American stores. The collection consists of three scents for women and two for men, each named after a luxurious, natural material that is both emotional and authentic. A separate family of fragrance and personal care products is also in the works for Gap’s North American stores. That fragrance family is scheduled for an initial launch to begin in May 2007, with the rollout continuing throughout the balance of the year and into 2008. In addition, we have been supplying Banana Republic and Gap stores with their existing personal care products, and we have created new holiday programs for this coming holiday season.

Our mass market products are also comprised of fragrances and fragrance related products. We produce a variety of alternative designer fragrances and personal care products that sell at a substantial discount from their brand name counterparts. Our alternative designer fragrances are similar in scent to highly advertised designer fragrances that are marketed at a higher retail price. Our mass market fragrance brands include several proprietary brand names as well as a license for the Jordache brand. We also market our Aziza line of low priced eye shadow kits, mascara, and pencils, focusing on the young teen market and a line of health and beauty aids under our Intimate brand name consisting of shampoo, conditioner, hand lotion and baby oil. All of theses products are distributed to the same mass market retailers and discount chains.

Business Strategy

Focus on prestige beauty brands. Prestige beauty brands contribute significantly to our growth. Over the past few years, prestige brands have accounted for a larger portion of our business — 84% of total business in 2006 from 68% in 2002. We focus on developing and launching quality fragrances utilizing internationally renowned brand names. By identifying and concentrating in the most receptive market segments and territories where our brands are known, and executing highly targeted launches that capture the essence of the brand, Inter Parfums has had a history of successful launches. Certain fashion designers and other licensors choose Inter Parfums as a partner because the company’s size enables us to work more closely with them in the product development process as well as because of our successful track record.

Grow portfolio brands through new product development and marketing. We grow through the creation of fragrance family extensions within the existing brands in our portfolio. Every two to three years, we create a new family of fragrances for each brand in our portfolio. We frequently introduce “seasonal” fragrances as well. With new introductions, we leverage our ability and experience to gauge trends in the market and further leverage the brand name into different product families in order to maximize sales and profit potential. We have had success in introducing new fragrance families (sub-brands, or flanker brands) within our brand franchises. Furthermore, we promote the smooth and consistent performance of our prestige perfume operations through knowledge of the market, detailed analysis of the image and potential of each brand name, a “good dose” of creativity and a highly professional approach to international distribution channels.

Continue to add new brands to our portfolio, through new licenses or acquisitions. Prestige brands are the core of our business — we intend to add new prestige beauty brands to our portfolio. Over the past decade, we have built our portfolio of well-known prestige brands through acquisitions and new license agreements. We intend to further build on our success in prestige fragrances and pursue new licenses and acquire new brands to strengthen our position in the prestige beauty market. We identify prestige brands that can be developed and marketed into a full and varied product families and, with our technical knowledge and practical experience gained over time, take licensed brand names through all phases of concept development, manufacturing, and marketing.

Expand existing portfolio into new categories. We plan to broaden our product offering beyond the fragrance category and offer other personal care products such as skin care, cosmetics and hair care under some of our existing brands. We believe such product offerings meet customer needs and further strengthen customer loyalty. We also plan to draw upon the skin care product expertise that the Nickel team brings, as we explore other opportunities in the treatment side of the beauty business beyond the Nickel brand. Furthermore, the license agreement with Burberry signed in 2004 extends to skin care.

Continue to build global distribution footprint. Our business is a global business and we intend to continue to build our global distribution footprint. In order to adapt to changes in the environment and our business, we have modified our distribution model, and are in process of forming joint ventures in the major markets of the United Kingdom, Italy, Spain and Germany for distribution of prestige fragrances. Further, we may enter into future joint ventures arrangements or acquire distribution companies within other key markets to distribute certain of our licensed prestige brands. However, we cannot assure you that we will be able to enter into any future joint venture arrangements or acquire distribution companies, or if we do, that any such transaction will be successful. We believe that in certain markets vertical integration of our distribution network is key to the future growth of our company, and ownership of such distribution should enable us to better serve our customers’ needs in local markets and adapt more quickly as situations may determine.

Build specialty retail through the Gap relationship. We believe the beauty industry has experienced a significant growth in specialty retail and our relationship with Gap has provided an entry into this distribution channel. We are responsible for product development, formula creation, packaging and manufacturing under Gap and Banana Republic brands. Gap, a leading international specialty retailer offering clothing, accessories and personal care products for men, women, children and babies, is responsible for marketing and selling the newly launched fragrance and fragrance related products in its stores. In addition, we have been approached by other specialty retailers to determine if there is interest in establishing a relationship whereby we would design, produce and manufacture fragrance and fragrance related products similar to our existing relationship with Gap. However, we cannot assure you that we will be able to enter into any similar future arrangements, or if we do, that any such arrangement will be successful.

Production and Supply

The stages of the development and production process for all fragrances are as follows:

| · | Simultaneous discussions with perfume designers and creators (includes analysis of esthetic and olfactory trends, target clientele and market communication approach); |

| · | Produce mock-ups for final acceptance of bottles and packaging; |

| · | Receive bids from component suppliers (glass makers, plastic processors, printers, etc.) and packaging companies; |

| · | Schedule production and packaging; |

| · | Issue component purchase orders; |

| · | Follow quality control procedures for incoming components; and |

| · | Follow packaging and inventory control procedures. |

Suppliers who assist us with product development include:

| · | Independent perfumery design companies (Federico Restrepo, Fabien Baron, Aesthete, Ateliers Dinand); |

| · | Perfumers (IFF, Firmenich, Robertet, Quest, Givaudan,Wessel Fragrances) which create a fragrance consistent with our expectations and, that of the fragrance designers and creators; |

| · | Contract manufacturers of components such as glassware (Saint Gobain, Saverglass, Pochet, Nouvelles Verreries de Momignie), caps (MT Packaging, Codiplas, Risdon, Newburgh) or boxes (Printor Packaging, Draeger, Dannex Manufacturing); |

| · | Production specialists who carry out packaging (MF Production, Brand, CCI, IKI Manufacturing) or logistics (SAGA for storage, order preparation and shipment). |

For our prestige products, approximately 80% of component and production needs are purchased from approximately 20 suppliers out of a total of over 120 active suppliers. The suppliers' accounts for our European operations are primarily settled in Euros and for our United States operations, suppliers' accounts are primarily settled in U.S. dollars.

Marketing and Distribution

Prestige Products

For our international distribution of prestige products, we contract with independent distribution companies specializing in luxury goods. In each country, we designate anywhere from one to three distributors with the status of "exclusive representative" for one or more of our name brands. We also distribute our prestige products through a variety of duty-free operators, such as airports and airlines and select vacation destinations.

Our distributors vary in size depending on the number of competing brands they represent. This extensive and diverse network provides us with a significant presence in over 120 countries around the world. Approximately 50 distributors out of a total of over 250 active accounts represent 80% of international prestige fragrance sales. One customer represented 15% of sales for the year ended December 31, 2006.

Our business is a global business and we intend to continue to build our global distribution footprint. In order to adapt to changes in the environment and our business, we have modified our distribution model, and are in process of forming joint ventures in the major markets of the United Kingdom, Italy, Spain and Germany for distribution of prestige fragrances. Further, we may enter into future joint ventures arrangements or acquire distribution companies within other key markets to distribute certain of our licensed prestige brands. However, we cannot assure you that we will be able to enter into any future joint venture arrangements or acquire distribution companies, or if we do, that any such transaction will be successful. We believe that in certain markets vertical integration of our distribution network is key to the future growth of our company, and ownership of such distribution should enable us to better serve our customers’ needs in local markets and adapt more quickly as situations may determine.

Approximately 34% of our prestige fragrance net sales are denominated in U.S. dollars. In an effort to reduce our exposure to foreign currency exchange fluctuations, we engage in a program of cautious hedging of foreign currencies to minimize the risk arising from operations. Our sales are not subject to material seasonal fluctuations.

Distribution in France of our prestige products is carried out by a sales team who oversee some 1,200 points of sale including, retail perfumers (chain stores) such as

or specialized independent points of sale. Approximately 80% of prestige product sales in France are made to approximately 200 customers out of a total of over 1,200 active accounts.

Specialty Retail and Mass Market Products

We do not presently market and distribute Gap and Banana Republic specialty retail products to third parties. Marketing and distribution are the responsibility of Gap, Inc., which markets and sells the products we produce in its own retail locations.

Mass merchandisers are the target customers for our mass market products. In addition, our mass market products are sold to wholesale distributors, specialty store chains, and to multiple locations of accessory, jewelry and clothing outlets. These products are sold through a highly efficient and dedicated in-house sales team and reach approximately 12,000 retail outlets throughout the United States and abroad.

Our 140,000 square foot distribution center has provided us with the opportunity and resources to meet our customers' requirements.

Geographic Areas

Export sales from United States operations were approximately $7.2 million, $6.4 million and $9.6 million in 2006, 2005 and 2004, respectively.

Consolidated net sales to customers by region is as follows (in thousands):

| | Year Ended December 31 |

| | 2006 | 2005 | 2004 |

| North America | $ 107,400 | $ 81,800 | $ 67,400 |

| Europe | 128,300 | 116,800 | 105,200 |

| Central and South America | 24,500 | 21,800 | 21,400 |

| Middle East | 21,900 | 19,800 | 17,900 |

| Asia | 37,700 | 32,200 | 22,700 |

| Other | 1,300 | 1,100 | 1,400 |

| | $ 321,100 | $ 273,500 | $ 236,000 |

| | | | |

Consolidated net sales to customers in major countries is as follows (in thousands):

| | Year Ended December 31 |

| | 2006 | 2005 | 2004 |

| United States | $104,000 | $80,000 | $66,000 |

| United Kingdom | 28,000 | 26,000 | 29,000 |

| France | 21,000 | 17,000 | 15,000 |

The Market

The fragrance and cosmetic market can be broken down into two (2) types of retail distribution:

| · | Selective distribution - perfumeries and specialty sections of department stores, which sell brand name products with a luxury image, and |

| · | Specialty retail and mass distribution - Specialty retail, or retail outlets which sell their own brand name products and mass merchandisers, discount stores and supermarkets, which sell low to moderately-priced mass market products for a broad customer base with limited purchasing power. |

Selective Distribution

The following information is based on information from the Fédération des Industries de la Parfumerie.

During 2006, the French perfume industry, which accounts for about approximately 35% of the world market, reported a 5.7% growth rate, as compared to a 4.9% growth rate in 2005 and a 2.6% growth rate in 2004.

Net sales in 2006 for the French domestic market reported a 3.5 % growth rate as compared to 2005, while the export market increased by 7.4% as compared to 2005:

The European Union: Sales increased overall by 5.4%, in this the largest market for French exports. Sales were strongest in new markets, Czech Republic (+41%), Poland (+23%) and Slovenia (+21%). Sales increased in other European Union members, Italy (+7%), Spain (+6,6%), Belgium (6,5%) and Germany(+6%).

Europe (excluding the European Union countries): Net sales increased by 35%, with substantial growth in Russia (+43.7%), Ukraine (+29.5%) and Romania (+29.5%).

Asia: Net sales increased by 5.4%. Asia is the second largest market for French cosmetics and perfumes, net sales increased in China (+39.5%), India (+11.3%), Singapore (+7.7%) and South Korea (+4%). For two years running net sales in Japan were disappointed (+0,1%).

North America: Net sales increased to 7.8% in the United States and 1.2% in Canada.

South America: Net sales to South America increased by +12.5%, a now stabilized trend for three years: Argentina (+40%), Chili (+22.6%), Mexico (13.5%) and Uruguay (+12.6%). Net sales in Brazil decreased 1.6%

While our market share, based on our internal data, is less than 1% in France, in other countries such as the United States, United Kingdom, Italy, Germany, Spain and Hong Kong, we estimate that our market share is between 1% and 4% of French perfume imports.

Specialty retail and mass Distribution

Our specialty retail and mass market products are designed for a broad customer base with a more limited purchasing power. We sell our products both in the United States and abroad. Mass merchandisers, discount stores and supermarkets are out target customers. We do not presently distribute Gap and Banana Republic specialty retail products to third parties. Gap, Inc. sells the products we produced in its own retail locations.

Competition

The market for fragrances and beauty related products is highly competitive and sensitive to changing preferences and demands. The prestige fragrance industry is highly concentrated around certain major players with resources far greater than ours. We compete with an original strategy-- regular and methodical development of quality fragrances for a growing portfolio of internationally renowned brand names.

In the specialty retail market, we are presently selling products only to Gap and Banana Republic stores, so we do not have any direct competition. However, such special retail stores compete directly with other specialty retail stores such as Abercrombie & Fitch and Victoria Secret, which thereby indirectly compete with us.

We compete in the mass market for fragrances, color cosmetics health and beauty aids primarily on the basis of price. At the present time, we are aware of approximately four established companies which market alternative designer fragrances similar to ours. Many of our competitors of both mass market color cosmetics (such as L’Oreal and Revlon) and health and beauty aids (such as Proctor and Gamble) have substantial financial resources as well as national and international marketing campaigns. However, we believe that consumer recognition of our two brands, Aziza for mass market color cosmetics, and Intimate for health and beauty aids, together with competitive pricing of our products, helps us compete in those markets.

Inventory

We purchase raw materials and component parts from suppliers based on internal estimates of anticipated need for finished goods, which enables us to meet production requirements for finished goods. We generally deliver product to customers within 72 hours of the receipt of their orders.

Product Liability

We maintain product liability coverage in an amount of $5,000,000. Based upon our experience, we believe this coverage is adequate and covers substantially all of the exposure we may have with respect to our products. We have never been the subject of any material product liability claims.

Government Regulation

A fragrance is defined as a “cosmetic” under the Federal Food, Drug and Cosmetics Act. A fragrance must comply with the labeling requirements of this FDC Act as well as the Fair Packaging and Labeling Act and its regulations. Some of our color cosmetic products may contain menthol and are also classified as a “drug”. Under U.S. law, a product may be classified as both a cosmetic and a drug. Additional regulatory requirements for products which are “drugs” include additional labeling requirements, registration of the manufacturer and the semi-annual update of a drug list.

Our fragrances are subject to the approval of the Bureau of Alcohol, Tobacco and Firearms as a result of the use of specially denatured alcohol. So far we have not experienced any difficulties in obtaining the required approvals.

Our fragrances that are manufactured in France are subject to certain regulatory requirements of the European Union, but as of the date of this report, we have not experienced any material difficulties in complying with such requirements.

Trademarks

The market for our products depends to a significant extent upon the value associated with our trademarks and brand names. We own, or have licenses or other rights to use, the material trademark and brand name rights used in connection with the packaging, marketing and distribution of our major products both in the United States and in other countries where such products are principally sold. Therefore, trademark and brand name protection is important to our business. Although most of our brand names are registered in the United States and in certain foreign countries in which we operate, we may not be successful in asserting trademark or brand name protection. In addition, the laws of certain foreign countries may not protect our intellectual property rights to the same extent as the laws of the United States. The costs required to protect our trademarks and brand names may be substantial.

Under various license and other agreements we have the right to use certain registered trademarks throughout the world (except as otherwise noted). These registered trademarks include:

| · | Gap (United States and Canada only) |

| · | Banana Republic (United States and Canada only) |

In addition, we are the registered trademark owner of many trademarks, including:

| · | Regal Collections, Royal Selections, Euro Collections and Apple |

Employees

As of March 1, 2007 we had 235 full-time employees world-wide. Of these, 134 are full-time employees in Paris, with 92 employees engaged in sales activities and 42 in administrative, production and marketing activities. In the United States, 101 employees work full-time, and of these, 40 were engaged in sales activities and 61 in administrative, production and marketing activities.

We believe that our relationship with our employees is good.

Item 1A. Risk Factors.

You should carefully consider these risk factors, together with all of the other information contained or incorporated by reference in this report, before you decide to purchase or sell shares of our common stock. These factors could cause our future results to differ materially from those expressed or implied in forward-looking statements made by us. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also harm our business. The trading price of our common stock could decline due to any of these risks, and you may lose all or part of your investment.

We are dependent upon Burberry for a significant portion of our sales, and the loss of this license will have a material adverse effect on us.

Burberry is our leading prestige brand name, as sales of Burberry products represented 57% 60% and 62% of net sales for the years ended December 31, 2006, 2005 and 2004, respectively.

In October 2004 our Paris-based subsidiary, Inter Parfums, S.A., entered into a 12.5-year, exclusive world-wide fragrance license with Burberry Limited, effective as of July 1, 2004, which replaced the original 1993 license. This license includes an additional five-year optional term that requires the consent of both Burberry and Inter Parfums, S.A., and must be exercised, if at all, prior to December 31, 2014. In addition, Burberry has the right on December 31, 2009 and December 31, 2011 to buy back the license at its then fair market value. Further, this license provides for a termination on a change in control of either Inter Parfums, S.A., the licensee, or Inter Parfums, Inc., the guarantor.

This license is subject to Inter Parfums, S.A. making required royalty payments (which are subject to certain minimums), minimum advertising and promotional expenditures and meeting minimum sales requirements. The new royalty rates, which are approximately double the rates under the prior license, commenced as of July 1, 2004. The new advertising and promotional expenditures, which commenced on January 1, 2005, as well as the minimum sales requirements, are substantially higher than under the prior license.

We are dependent upon the continuation and renewal of various licenses for a significant portion of our sales, and the loss of one or more licenses could have a material adverse effect on us.

Substantially all of our prestige fragrance brands are licensed from unaffiliated third parties and our business is dependent upon the continuation and renewal of such licenses on terms favorable to us. Each license is for a specific term and may have additional optional terms. In addition, each license is subject to us making required royalty payments (which are subject to certain minimums), minimum advertising and promotional expenditures and meeting minimum sales requirements. Just as the loss of a license may have a material adverse effect on us, a renewal on less favorable terms may also negatively impact us.

If we are unable to protect our intellectual property rights, specifically trademarks and brand names, our ability to compete could be negatively impacted.

The market for our products depends to a significant extent upon the value associated with our trademarks and brand names. We own, or have licenses or other rights to use, the material trademark and brand name rights used in connection with the packaging, marketing and distribution of our major products both in the United States and in other countries where such products are principally sold. Therefore, trademark and brand name protection is important to our business. Although most of our brand names are registered in the United States and in certain foreign countries in which we operate, we may not be successful in asserting trademark or brand name protection. In addition, the laws of certain foreign countries may not protect our intellectual property rights to the same extent as the laws of the United States. The costs required to protect our trademarks and brand names may be substantial.

The success of our products is dependent on public taste.

Our revenues are substantially dependent on the success of our products, which depends upon, among other matters, pronounced and rapidly changing public tastes, factors which are difficult to predict and over which we have little, if any, control. In addition, we have to develop successful marketing, promotional and sales programs in order to sell our fragrances and fragrance related products. If we are not able to develop successful marketing, promotional and sales programs, then such failure will have a material adverse effect on our business, financial condition and operating results.

We are subject to extreme competition in the fragrance industry.

The market for fragrances and fragrance related products is highly competitive and sensitive to changing market preferences and demands. Many of our competitors in this market (particularly in the prestige fragrance industry) are larger than we are and have greater financial resources than are available to us, potentially allowing them greater operational flexibility.

Our success in the prestige fragrance industry is dependent upon our ability to continue to generate original strategies and develop quality products that are in accord with ongoing changes in the market.

In the specialty retail market, we are presently selling products only to Gap and Banana Republic stores, so we do not have any direct competition. However, such special retail stores compete directly with other specialty retail stores such as Abercrombie & Fitch and Victoria Secret, which thereby indirectly compete with us.

Our success with mass market fragrance and fragrance related products is dependent upon our ability to competitively price quality products and to quickly and efficiently develop and distribute new products.

If there is insufficient demand for our existing fragrances and fragrance related products, or if we do not develop future strategies and products that withstand competition or we are unsuccessful in competing on price terms, then we could experience a material adverse effect on our business, financial condition and operating results.

Consumers may reduce discretionary purchases of our products as a result of a general economic downturn.

We believe that consumer spending on beauty products is influenced by general economic conditions and the availability of discretionary income. Accordingly, we may experience sustained periods of declines in sales during economic downturns, or if terrorism or diseases affect customers’ purchasing patterns. In addition, a general economic downturn may result in reduced traffic in our customers’ stores which may, in turn, result in reduced net sales to our customers. Any resulting material reduction in our sales could have a material adverse effect on our business, financial condition and operating results.

We are dependent upon Gap to sell products that we develop for The Gap, Inc..

We have an exclusive agreement with The Gap, Inc. to develop, produce, manufacture and distribute personal care and home fragrance products for Gap and Banana Republic brand names to be sold in Gap and Banana Republic retail stores in the United States and Canada. Under the terms of such agreement, the products that we develop are subject to sales and marketing efforts of The Gap, Inc.

If the sales and marketing efforts of The Gap, Inc. are not successful for the products that we have developed, then our future growth potential could be negatively impacted.

If we are unable to acquire or license additional brands, or obtain the required financing for these agreements and arrangements, the growth of our business could be impaired.

Our future expansion through acquisitions or new product distribution arrangements, if any, will depend upon the capital resources and working capital available to us. We may be unsuccessful in identifying, negotiating, financing and consummating such acquisitions or arrangements on terms acceptable to us, or at all, which could hinder our ability to increase revenues and build our business.

We may engage in future acquisitions that we may not be able to successfully integrate or manage. These acquisitions may dilute our stockholders and cause us to incur debt and assume contingent liabilities.

We continuously review acquisition prospects that would complement our current product offerings, increase our size and geographic scope of operations or otherwise offer growth and operating efficiency opportunities. The financing for any of these acquisitions could significantly dilute our stockholders, result in an increase in our indebtedness or both. While there are no current agreements or negotiations underway with respect to any material acquisitions, we may acquire or make investments in businesses or products in the future. Acquisitions may entail numerous integration risks and impose costs on us, including:

| · | difficulties in assimilating acquired operations or products, including the loss of key employees from acquired businesses; |

| · | diversion of management’s attention from our core business; |

| · | adverse effects on existing business relationships with suppliers and customers; |

| · | risks of entering markets in which we have no or limited prior experience; |

| · | dilutive issuances of equity securities; |

| · | incurrence of substantial debt; |

| · | assumption of contingent liabilities; |

| · | incurrence of significant amortization expenses related to intangible assets and the potential impairment of acquired assets; and |

| · | incurrence of significant immediate write-offs. |

Our failure to successfully complete the integration of any acquired business could have a material adverse effect on our business, financial condition and operating results.

We are dependent upon Messrs. Jean Madar and Philippe Benacin, and the loss of their services could harm our business.

Jean Madar, our Chief Executive Officer, and Philippe Benacin, our President and Chief Executive Officer of Inter Parfums, S.A., are responsible for day-to-day operations as well as major decisions. Termination of their relationships with us, whether through death, incapacity or otherwise, could have a material adverse effect on our operations, and we cannot assure you that qualified replacements can be found. We maintain key man insurance on the lives of both Mr. Madar ($1 million) and Mr. Benacin ($3.6 million). However, we cannot assure you that we would be able to retain suitable replacements for either Mr. Madar or Mr. Benacin.

Our reliance on third party manufacturers could have a material adverse effect on us.

We rely on outside sources to manufacture our fragrances and cosmetics. The failure of such third party manufacturers to deliver either components or finished goods on a timely basis could have a material adverse effect on our business. Although we believe there are alternate manufacturers available to supply our requirements, we cannot assure you that current or alternative sources will be able to supply all of our demands on a timely basis. We do not intend to develop our own manufacturing capacity. As these are third parties over which we have little or no control, the failure of such third parties to provide components or finished goods on a timely basis could have a material adverse effect on our business, financial condition and operating results.

Our reliance on third party distributors could have a material adverse effect on us.

We sell our prestige fragrances mostly through independent distributors specializing in luxury goods. Given the growing importance of distribution, we have begun to modify our distribution model by the formation of joint ventures or company owned subsidiaries within key markets. We have little or no control over third party distributors and the failure of such third parties to provide services on a timely basis could have a material adverse effect on our business, financial condition and operating results. In addition, if we replace existing third party distributors with new third party distributors or with our own distribution arrangements, then transition issues could have a material adverse effect on our business, financial condition and operating results.

The loss of or disruption in our distribution facilities could have a material adverse effect on our business, financial condition and operating results.

We currently have one distribution facility in Paris and one in New Jersey. The loss of one or both of those facilities, as well as the inventory stored in those facilities, would require us to find replacement facilities and assets. In addition, terrorist attacks, or weather conditions, such as natural disasters, could disrupt our distribution operations. If we cannot replace our distribution capacity and inventory in a timely, cost-efficient manner, it could have a material adverse effect on our business, financial condition and operating results.

The international character of our business renders us subject to fluctuation in foreign currency exchange rates and international trade tariffs, barriers and other restrictions.

A portion of our Paris subsidiary’s net sales (approximately 34% in 2006) are sold in U.S. dollars. In an effort to reduce our exposure to foreign currency exchange fluctuations, we engage in a program of cautious hedging of foreign currencies to minimize the risk arising from operations. Despite such actions, fluctuations in foreign currency exchange rates for the U.S. dollar, particularly with respect to the Euro, could have a material adverse effect on our operating results. Possible import, export, tariff and other trade barriers, which could be imposed by the United States, other countries or the European Union might also have a material adverse effect on our business.

Our business is subject to governmental regulation, which could impact our operations.

Fragrances and fragrance related products must comply with the labeling requirements of the Federal Food, Drug and Cosmetics Act as well as the Fair Packaging and Labeling Act and their regulations. Some of our color cosmetic products may also be classified as a “drug”. Additional regulatory requirements for products which are “drugs” include additional labeling requirements, registration of the manufacturer and the semi-annual update of a drug list.

Our fragrances are subject to the approval of the Bureau of Alcohol, Tobacco and Firearms as a result of the use of specially denatured alcohol. So far we have not experienced any difficulties in obtaining the required approvals.

Our fragrances and fragrance related products that are manufactured in France are subject to certain regulatory requirements of the European Union, but as of the date of this report, we have not experienced any material difficulties in complying with such requirements.

However, we cannot assure you that, should we develop or market fragrances and fragrance related products with different ingredients, or should existing regulations or requirements be revised, we would not in the future experience difficulty in complying with such requirements, which could have a material adverse effect on our results of operations.

We may become subject to possible liability for improper comparative advertising or “Trade Dress.”

Brand name manufacturers and sellers of brand name products may make claims of improper comparative advertising or trade dress (packaging) with respect to the likelihood of confusion between some of our mass market products and those of brand name manufacturers and sellers. They may seek damages for loss of business or injunctive relief to seek to have the use of the improper comparative advertising or trade dress halted. However, we believe that our displays and packaging constitute fair competitive advertising and are not likely to cause confusion between our products and others. Further, we have not experienced to any material degree, any of such problems to date.

Item 1B. Unresolved Staff Comments. None.

Item 2. Properties

Use | Location | Approximate Size | Annual Rent (All are subject to escalations, except where noted) | Term Expires | Other Information |

| Office Space-corporate headquarters and United States operations | 551 Fifth Avenue, New York, NY. | 11,000 square feet | $388,000 | February 28, 2013 | |

Distribution center | 60 Stults Road Dayton, NJ | 140,000 square foot | $684,000 | October 31, 2010 | |

| Office Space-Paris corporate headquarters and Paris based operations | 4 Rond Point Des Champs Elysees Ground and 1st Fl. Paris, France | 571 square meters | 315,000 Euros | March 2013 | Lessee has early termination right every 3 years on 6 months notice |

| Office Space-Paris corporate headquarters and Paris based operations | 4 Rond Point Des Champs Elysees 4th Fl. Paris, France | 531 square meters | 264,000 Euros | June 2014 | Lessee has early termination right every 3 years on 6 months notice |

| Office Space-Paris corporate headquarters and Paris based operations | 4 Rond Point Des Champs Elysees 5th Fl- left Paris, France | 155 square meters | 75,200 Euros | March 2013 | Lessee has early termination right on 3 months notice |

| Office Space-Paris corporate headquarters and Paris based operations | 4 Rond Point Des Champs Elysees 6th Fl-Right Paris, France | 157 square meters | 64,627 Euros | March 2013 | Lessee has early termination right every 3 years on 6 months notice |

Office Space- Paris Accounting and Legal | 39 avenue Franklin Roosevelt, 2nd Floor Paris, France | 360 square meters | 154,800 Euros to December 15, 2006; 165,600 Euros to December 15, 2007; 172,800 Euros thereafter | December 2014 | Lessee has early termination right every 3 years on 6 months notice |

Men’s Spa | 48 Rue des Francs Bourgeois, Paris, France | 116 square meters | 44,000 Euros | June 2011 | Lessee has early termination right every 3 years on 6 months notice |

| Men’s Spa | Unit C2, 300 West 14th Street, New York, N.Y. | 4,500 Square Feet | $248,000 | October 31, 2009 | 5-year term option term |

Inter Parfums, S.A. has an agreement with Sagatrans, S.A. for warehousing and distribution services through September 2011. Fees are calculated based upon a percentage of sales, which are customary in the industry. Minimum future lease payments range from 2.6 million euro in 2006 increasing to 3.0 million euro in 2011.

We believe our office and warehouse facilities are satisfactory for our present needs and those for the foreseeable future.

Item 3. Legal Proceedings

We are not a party to any material lawsuits.

Item 4. Submissions Of Matters To A Vote Of Security Holders

Not applicable.

PART II

Item 5. Market For Registrant's Common Equity And Related Stockholder Matters

The Market for Our Common Stock

Our company's common stock, $.001 par value per share, is traded on The Nasdaq Global Select Market under the symbol "IPAR". The following table sets forth in dollars, the range of high and low closing prices for the past two fiscal years for our common stock.

| Fiscal 2006 | High Closing Price | Low Closing Price |

| Fourth Quarter | $ 21.77 | $ 17.63 |

| Third Quarter | $ 19.56 | $ 15.75 |

| Second Quarter | $ 19.99 | $ 15.39 |

| First Quarter | $ 20.38 | $ 17.07 |

| Fiscal 2005 | High Closing Price | Low Closing Price |

| Fourth Quarter | $ 19.70 | $ 14.74 |

| Third Quarter | $ 21.50 | $ 18.13 |

| Second Quarter | $ 20.89 | $ 13.12 |

| First Quarter | $ 15.92 | $ 14.01 |

As of March 1, 2007 the number of record holders, which include brokers and broker's nominees, etc., of our common stock was 58. We believe there are in excess of 1,750 beneficial owners of our common stock.

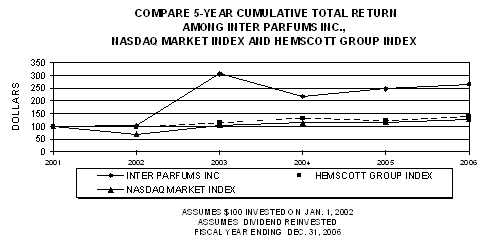

Corporate Performance Graph

The following graph compares the performance for the periods indicated in the graph of our common stock with the performance of the Nasdaq Market Index and the average performance of a group of the company’s peer corporations consisting of: Alberto-Culver, Avon Products Inc., Blyth Inc., CCA Industries, Inc., Colgate-Palmolive Co., Elizabeth Arden, Inc., Estee Lauder Cosmetics, Inc., Inter Parfums, Inc., Oralabs Holding Corp., Parlux Fragrances Inc., Playtex Products, Inc., Revlon, Inc., Spectrum Brands, Inc., The Stephan Company, United Guardian, Inc., and Yankee Candle Co., Inc. The graph assumes that the value of the investment in our common stock and each index was $100 at the beginning of the period indicated in the graph, and that all dividends were reinvested.

Dividends

In March 2005 our board of directors increased the cash dividend from $.12 to $.16 per share per annum, payable $0.04 on a quarterly basis. In December 2005 our board of directors authorized the continuation of our cash dividend of $.16 per share per annum, payable $.04 on a quarterly basis. In December 2006 our board of directors increased the cash dividend from $.16 to $.20 per share per annum, payable $0.05 on a quarterly basis. The first cash dividend for 2007 of $.05 per share is to be paid on April 13, 2007 to shareholders of record on March 30, 2007.

Our Certificate of Incorporation provides for the requirement of unanimous approval of the members of our board of directors for the declaration or payment of dividends, if the aggregate amount of dividends to be paid by us and our subsidiaries in any fiscal year is more than thirty percent (30%) of our annual net income for the last completed fiscal year, as indicated by our consolidated financial statements.

Sales of Unregistered Securities

The following sets forth certain information as to the sales of unregistered securities, including options granted to purchase our common stock during the last quarter of the last fiscal year and through the date of this report, which were not registered under the Securities Act. In each of the transactions, we either issued shares to 2 executive officers upon the exercise of outstanding stock options, or granted options to our non-employee directors, who are all deemed our affiliates. The transactions were exempt from the registration requirements of Section 5 of the Securities Act under Sections 4(2) and 4(6) of the Securities Act. Each option holder agreed that, if the option is exercised, the option holder would purchase his common stock for investment and not for resale to the public. Also, we provide all option holders with all reports we file with the SEC and press releases issued by us.

In November 2006 both the Chief Executive Officer and the President exercised an aggregate of 100,000 outstanding stock options of the Company’s common stock. The aggregate exercise prices of $0.8 million in 2006, were paid by them tendering to the Company in 2006 an aggregate of 37,278 of the Company’s common stock, previously owned by them, valued at fair market value on the date of exercise. All shares issued pursuant to these option exercises were issued from treasury stock of the Company. In addition, the Chief Executive Officer tendered in 2006 an additional 7,840 shares, respectively, for payment of certain withholding taxes resulting from his option exercise.

On February 1, 2007, we granted options to purchase an aggregate of 9,500 shares for a five-year period at the exercise price of $19.845 per share, the fair market value on the date of grant, to 7 directors under our 2004 Non-Employee Director Stock Option Plan. Such options vest 25% each year over a four year period on a cumulative basis.

Repurchases of Our Common Stock

Except as set forth above with respect to the tendering of shares for the payment of the exercise price and taxes, we did not repurchase any of our Common Stock during the fourth quarter of fiscal year ended December 31, 2006.

Item 6. Selected Financial Data

The following selected financial data have been derived from our financial statements, and should be read in conjunction with those financial statements, including the related footnotes.

| | | Years Ended December 31, | |

| (In thousands except per share data) | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| | |

Income Statement Data: | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Net Sales | | $ | 321,054 | | $ | 273,533 | | $ | 236,047 | | $ | 185,589 | | $ | 130,352 | |

| | | | | | | | | | | | | | | | | |

| Cost of Sales | | | 143,855 | | | 115,827 | | | 113,988 | | | 95,449 | | | 71,630 | |

| | | | | | | | | | | | | | | | | |

| Selling, General and Administrative | | | 141,074 | | | 126,353 | | | 89,516 | | | 64,147 | | | 41,202 | |

| | | | | | | | | | | | | | | | | |

| Operating Income | | | 36,125 | | | 31,353 | | | 32,543 | | | 25,993 | | | 17,520 | |

| | | | | | | | | | | | | | | | | |

Income Before Taxes and Minority Interest | | | 37,135 | | | 31,724 | | | 31,638 | | | 26,632 | | | 17,581 | |

| | | | | | | | | | | | | | | | | |

| Net Income | | | 17,742 | | | 15,263 | | | 15,703 | | | 13,837 | | | 9,405 | |

| | | | | | | | | | | | | | | | | |

| Net Income per Share: | | | | | | | | | | | | | | | | |

| Basic | | $ | 0.87 | | $ | 0.76 | | $ | 0.82 | | $ | 0.73 | | $ | 0.50 | |

| Diluted | | $ | 0.86 | | $ | 0.75 | | $ | 0.77 | | $ | 0.69 | | $ | 0.47 | |

| | | | | | | | | | | | | | | | | |

| Average Common Shares Outstanding: | | | | | | | | | | | | | | | | |

| Basic | | | 20,324 | | | 20,078 | | | 19,205 | | | 19,032 | | | 18,777 | |

| Diluted | | | 20,568 | | | 20,487 | | | 20,494 | | | 20,116 | | | 19,948 | |

| | | | | | | | | | | | | | | | | |

| Depreciation and Amortization | | $ | 5,347 | | $ | 4,513 | | $ | 3,988 | | $ | 3,344 | | $ | 2,220 | |

| | | As at December 31, | |

| (In thousands except per share data) | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| | | | | | | | | | | | |

Balance Sheet And Other Data: | | | | | | | | | | | |

| | | | | | | | | | | | |

| Cash and Cash Equivalents and Short-Term Investments | | $ | 71,047 | | $ | 59,532 | | $ | 40,972 | | $ | 58,958 | | $ | 38,290 | |

| | | | | | | | | | | | | | | | | |

| Working Capital | | | 138,547 | | | 131,084 | | | 129,866 | | | 115,970 | | | 83,828 | |

| | | | | | | | | | | | | | | | | |

| Total Assets | | | 333,045 | | | 240,910 | | | 230,485 | | | 194,001 | | | 129,370 | |

| | | | | | | | | | | | | | | | | |

| Short-Term Bank Debt | | | 6,033 | | | 989 | | | 748 | | | 121 | | | 1,794 | |

| | | | | | | | | | | | | | | | | |

| Long-Term Debt (including current portion) | | | 10,769 | | | 13,212 | | | 19,617 | | | -0- | | | -0- | |

| | | | | | | | | | | | | | | | | |

| Stockholders’ Equity | | | 155,272 | | | 127,727 | | | 126,509 | | | 104,916 | | | 80,916 | |

| | | | | | | | | | | | | | | | | |

| Dividends per Share | | $ | 0.16 | | $ | 0.16 | | $ | 0.12 | | $ | 0.08 | | $ | 0.06 | |

| Item 7. | Management's Discussion And Analysis Of Financial Condition And Results Of Operation |

Overview

We operate in the fragrance business, and manufacture, market and distribute a wide array of fragrances and fragrance related products. We manage our business in two segments, European based operations and United States based operations. Our prestige fragrance products are produced and marketed by our European operations through our 72% owned subsidiary in Paris, Inter Parfums, S.A., which is also a publicly traded company as 28% of Inter Parfums, S.A. shares trade on the Euronext. Prestige cosmetics and prestige skin care products represent less than 3% of consolidated net sales.

We produce and distribute our prestige products primarily under license agreements with brand owners and prestige product sales represented approximately 84% of net sales for 2006. We have built a portfolio of brands, which include Burberry, Lanvin, Paul Smith, S.T. Dupont, Christian Lacroix, Quiksilver/Roxy, Van Cleef & Arpels and Nickel whose products are distributed in over 120 countries around the world. Burberry is our most significant license, sales of Burberry products represented 57%, 60% and 62% of net sales for the years ended December 31, 2006, 2005 and 2004, respectively.

Our specialty retail and mass-market fragrance and fragrance related products are marketed through our United States operation and represented 16% of sales for the year ended December 31, 2006. These products are sold under trademarks owned by us or pursuant to license or other agreements with the owners of the Gap, Banana Republic, Aziza and Jordache trademarks.

We grow our business in two distinct ways. First, we grow by adding new brands to our portfolio, either through new licenses or out-right acquisitions of brands. Second, we grow through the creation of fragrance family extensions within the existing brands in our portfolio. Every two to three years, we create a new family of fragrances for each brand in our portfolio.

Our business is not capital intensive, and it is important to note that we do not own any manufacturing facilities. We act as a general contractor and source our needed components from our suppliers. These components are received at one of our distribution centers and then, based upon production needs, the components are sent to one of several third party fillers which manufacture the finished good for us and ship it back to our distribution center.

Recent Important Events

Van Cleef & Arpels

In September 2006, we entered into an exclusive, worldwide license agreement with Van Cleef & Arpels Logistics SA, for the creation, development and distribution of fragrance and related bath and body products under the Van Cleef & Arpels brand and related trademarks. Van Cleef & Arpels is a prestigious and legendary world-renowned jewelry designer. The agreement runs through December 31, 2018. As an inducement to enter into this license agreement we agreed to pay, in January 2007, €18 million (approximately $23.4 million) to Van Cleef & Arpels Logistics SA in a lump sum, up front royalty payment, and we agreed to purchase existing inventory held by YSL Beauté, the current licensee. The license agreement became effective on January 1, 2007.

Quiksilver

In March 2006, we entered into an exclusive worldwide license agreement with Quiksilver, Inc. for the creation, development and distribution of fragrance, suncare, skincare and related products under the Roxy brand and suncare and related products under the Quiksilver brand. Quiksilver, Inc. is one of the world’s leading outdoor sports lifestyle company whose products are sold in 90 countries. The agreement runs through 2017.

The Roxy and Quiksilver names are hugely popular in the global youth market and are synonymous with the heritage and culture of surfing, skateboarding and snowboarding. Our goal is to leverage the passion and loyalty of the Roxy and Quiksilver brands as we bring their customers exciting new products. Our plans call for the first new product family under the agreement, a Roxy fragrance family, to be introduced in late 2007, followed by a Quiksilver suncare line.

Gap and Banana Republic