UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| Caroline Kraus, Esq. | Copies to: | |

| Goldman, Sachs & Co. | Geoffrey R.T. Kenyon, Esq. | |

| 200 West Street | Dechert LLP | |

| New York, New York 10282 | 100 Oliver Street | |

| 40th Floor | ||

| Boston, MA 02110-2605 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: October 31

Date of reporting period: April 30, 2014

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| The Semi-Annual Report to Stockholders is filed herewith. |

Goldman Sachs Funds

| Semi-Annual Report | April 30, 2014 | |||

International Equity Insights Funds | ||||

Emerging Markets Equity Insights | ||||

International Equity Insights | ||||

International Small Cap Insights | ||||

Goldman Sachs International Equity

Insights Funds

| n | EMERGING MARKETS EQUITY INSIGHTS |

| n | INTERNATIONAL EQUITY INSIGHTS |

| n | INTERNATIONAL SMALL CAP INSIGHTS |

TABLE OF CONTENTS | ||||

Principal Investment Strategies and Risks | 1 | |||

Investment Process | 2 | |||

Market Review | 4 | |||

Portfolio Management Discussions and Performance Summaries | 7 | |||

Schedules of Investments | 22 | |||

Financial Statements | 42 | |||

Financial Highlights | 46 | |||

Notes to the Financial Statements | 52 | |||

Other Information | 68 | |||

| NOT FDIC-INSURED | May Lose Value | No Bank Guarantee | ||

GOLDMAN SACHS INTERNATIONAL EQUITY INSIGHTS FUNDS

Principal Investment Strategies and Risks

This is not a complete list of risks that may affect the Funds. For additional information concerning the risks applicable to the Funds, please see the Funds’ Prospectus.

The Goldman Sachs Emerging Markets Equity Insights Fund invests primarily in a diversified portfolio of equity investments in emerging country issuers. The Fund’s investments are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic and political developments. The securities markets of emerging countries have less government regulation and are subject to less extensive accounting and financial reporting requirements than the markets of more developed countries. At times, the Fund may be unable to sell certain of its illiquid investments without a substantial drop in price, if at all. The Investment Adviser’s use of quantitative models to execute the Fund’s investment strategy may fail to produce the intended result. Different investment styles (e.g., “quantitative”) tend to shift in and out of favor, and at times the Fund may underperform other funds that invest in similar asset classes. The Fund may have a high rate of portfolio turnover, which involves correspondingly greater expenses which must be borne by the Fund, and is also likely to result in short-term capital gains taxable to shareholders.

The Goldman Sachs International Equity Insights Fund invests primarily in a broadly diversified portfolio of equity investments in companies that are organized outside the United States or whose securities are principally traded outside the United States. The Fund’s investments are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. The Investment Adviser’s use of quantitative models to execute the Fund’s investment strategy may fail to produce the intended result. Different investment styles (e.g., “quantitative”) tend to shift in and out of favor, and at times the Fund may underperform other funds that invest in similar asset classes. The Fund may have a high rate of portfolio turnover, which involves correspondingly greater expenses which must be borne by the Fund, and is also likely to result in short-term capital gains taxable to shareholders.

The Goldman Sachs International Small Cap Insights Fund invests primarily in a broadly diversified portfolio of equity investments in small capitalization non-U.S. issuers. The Fund’s investments are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. The securities of mid- and small-capitalization companies involve greater risks than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements. The Investment Adviser’s use of quantitative models to execute the Fund’s investment strategy may fail to produce the intended result. Different investment styles (e.g., “quantitative”) tend to shift in and out of favor, and at times the Fund may underperform other funds that invest in similar asset classes. The Fund may have a high rate of portfolio turnover, which involves correspondingly greater expenses which must be borne by the Fund, and is also likely to result in short-term capital gains taxable to shareholders.

1

GOLDMAN SACHS INTERNATIONAL EQUITY INSIGHTS FUNDS

Goldman Sachs’ International Equity Insights Investment Process

| n | Comprehensive – We forecast returns on over 8,000 international stocks and 43 equity markets on a daily basis. |

| n | Rigorous – We evaluate stocks, countries and currencies based on fundamental investment criteria that have outperformed historically. |

| n | Objective – Our stock and equity market selection process is free from emotion that may lead to biased investment decisions. |

| n | Our computer optimization process allocates risk to our best investment ideas and constructs funds that strive to neutralize systematic risks and deliver better returns. |

| n | We use proprietary risk models that are designed to be more precise, more focused and faster to respond because they seek to identify, track and manage risk specific to our process, using daily data. |

Fully invested, well-diversified international portfolio that seeks to:

| n | Blend top-down market views with bottom-up stock selection. |

| n | Maintain style, sector, risk and capitalization characteristics similar to the benchmark. |

| n | Achieve excess returns by taking many small diversified stock positions. Additionally, in the Goldman Sachs Emerging Markets Equity Insights and the International Equity Insights Funds we take intentional country bets. |

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

2

GOLDMAN SACHS INTERNATIONAL EQUITY INSIGHTS FUNDS

Enhancements Made to Proprietary Quantitative Model during the Six-Month Period Ended April 30, 2014

We continuously look for ways to improve our investment process. Accordingly, we introduced a number of enhancements to our proprietary quantitative model during the six-month period ended April 30, 2014.

In the fourth quarter of 2013, we implemented an enhancement to our Profitability theme to incorporate cash returns on cash invested metrics. We believe this additional metric should further help us to select the stocks of companies that efficiently reinvest and grow earnings. In addition, we extended an enhancement to our Sentiment theme for the U.K. and Japan regions, seeking to identify investment trends through natural language processing. We use natural language processing to analyze hundreds of research reports from professional stock analysts. Rather than relying on broad stock recommendations, we read through the body of the text to gain a more nuanced understanding of the reports. Analysts’ evolving views are generally reflected in the body of their research reports before changes are made in their official recommendations. By reading the full text of the reports, we gain insight into the direction of future ratings changes.

We made no enhancements to our proprietary quantitative model within the international or emerging markets regions during the first quarter of 2014.

3

MARKET REVIEW

Goldman Sachs International Equity Insights Funds

Market Review

During the six-month period ended April 30, 2014 (the “Reporting Period”), emerging markets equities recorded a decline, while developed international equities generated solid gains.

Emerging Markets Equities

Emerging markets equities significantly lagged developed markets equities during the Reporting Period, as concerns over slowing economic growth, high inflation and election uncertainty weighed on many of the growth and emerging markets. Also contributing to weak performance of emerging market equities during the Reporting Period was the December 2013 announcement by the U.S. Federal Reserve (the “Fed”) that it would begin tapering its asset purchases in January 2014. The announcement ended seven months of speculation about the beginning of the end of ultra-loose monetary policy that had fueled many emerging market economies in recent years. Further, Argentina’s currency devaluation in January 2014 rippled through emerging market currency and equity markets, forcing many central banks to hike interest rates, which further pressured equity markets.

Looking at some key individual emerging markets more specifically, Chinese equities struggled during most of the Reporting Period amidst renewed concerns about China’s shadow banking system, credit quality and decelerating growth. The Russian equity market plunged during the Reporting Period due to the rapidly escalating geopolitical situation in Ukraine. Weakness in Latin American equity markets persisted into early 2014, though the region began to rebound later in the Reporting Period. After a slow start, Indian equities also rallied sharply later in the Reporting Period, as polls suggested that the Bharatiya Janata Party (“BJP”), which is perceived as business-friendly, is likely to win in the country’s upcoming election. Protest movements increased the political risk of some countries, such as Turkey, which was one of the worst performing markets during the Reporting Period. At the other end of the spectrum, Indonesia’s equity market rallied, largely due to an improving current account balance and strong foreign flows.

For the Reporting Period overall, the MSCI® Emerging Markets Standard Index (unhedged, with dividends reinvested, net of dividend withholding taxes) (the “MSCI® EM Index”) returned -2.98% .* Thirteen of the 21 countries in the MSCI® EM Index were down for the Reporting Period, with Russia (-22.95%) and Hungary (-14.20%) posting the largest losses. Russia was also the largest decliner on the basis of impact, which takes both weightings and total returns into account.

Seven of the 10 sectors in the MSCI® EM Index were down for the Reporting Period, with energy (-10.80%) and materials (-6.46%) declining the most. The financials sector (-4.92%) was the largest detractor to MSCI® EM Index returns on the basis of impact.

4

MARKET REVIEW

International Equities

Developed international equities generated solid gains during the Reporting Period. Stock markets in Japan and Europe continued to make fresh highs through the end of 2013, with Japan’s Nikkei 225 Stock Average closing the year at a six-year high. The Japanese equity market’s strength reflected optimism about Prime Minister Shinzo Abe’s bold reforms and big stimulus. Encouragingly, Japan’s consumer price index (“CPI”) steadily increased through the end of the calendar year, boosting confidence that its economy was on a path to achieve its government’s inflation target of 2%. Germany’s Xetra Dax also reached a new high in December 2013, as European equity markets continued to benefit from the European Central Bank’s commitment to easy monetary policy and as economic growth returned to the region. (The Nikkei 225 Stock Average is a price-weighted index comprised of Japan’s top 225 blue chip companies on the Tokyo Stock Exchange. The Xetra Dax is a blue chip index in Germany that tracks the performance of the 30 most actively traded stocks on the Frankfurt Stock Exchange.) Weak performance from commodity-related sectors and a depreciating currency negatively impacted the Australian equity market toward the end of 2013.

January 2014 got off to a volatile start, as global developed equity market performance reflected a number of concerns in the emerging markets. However, most developed international equity markets then rebounded to make gains through April 2014. During the first quarter of 2014, it was reported that the Eurozone economy had grown at a stronger than expected 0.5% year over year rate during the fourth quarter of 2013, and the European Commission raised its estimates for Gross Domestic Product (“GDP”) growth in the region to 1.2% in 2014 and 1.8% in 2015. The Euro-area Flash Services Composite Purchasing Managers Index (“PMI”) recorded its highest level since 2011, while peripheral bond markets continued to normalize, with yields on Italian and Spanish bonds approximately half of what they were two years prior. (Flash Services Composite PMI is an early estimate of the Services PMI for a region, designed to provide an accurate advance indication of the final Services PMI data. As flash PMIs are among the first economic indicators for each month, providing evidence of changing economic conditions ahead of comparable government statistics, they can have a significant effect on currency markets.) However, many corporate earnings reports and conservative guidance from company managements disappointed, and disinflation remained a near-term threat. Japanese equities were weak for most of the calendar year through April 2014 in anticipation of the April 1, 2014 consumption tax increase, which is expected to obscure some economic data in the near term. Wage growth and business and consumer sentiment in Japan also disappointed.

For the Reporting Period overall, the MSCI® Europe, Australasia, Far East (“EAFE®”) Standard Index (unhedged, with dividends reinvested, net of dividend withholding taxes) (“MSCI® EAFE® Index”) returned 4.44% .* Seventeen of the 21 countries in the MSCI® EAFE® Index were up for the Reporting Period, with Denmark (+26.85%) and Israel (+22.71%) recording the largest gains. The U.K. (+7.18%) was the largest contributor on the basis of impact, which takes both weightings and total returns into account.

All 10 sectors in the MSCI® EAFE® Index generated positive returns for the Reporting Period, with health care (+12.58%) and energy (+11.75%) gaining the most. The health care sector was also the largest contributor to MSCI® EAFE® Index returns on the basis of impact.

In the international small cap arena, the MSCI® EAFE® Small Cap Index (unhedged, with dividends reinvested, net of dividend withholding taxes) (“MSCI® EAFE® Small Cap Index”) returned 5.38%* during the Reporting Period. Seventeen of the 22 countries in the MSCI®

5

MARKET REVIEW

EAFE® Small Cap Index were up for the Reporting Period, with Portugal (+47.10%) and Denmark (+19.51%) posting the largest gains. The U.K. (+7.51%) was the largest contributor on the basis of impact, which takes both weightings and total returns into account.

Nine of the 10 sectors in the MSCI® EAFE® Small Cap Index recorded positive results for the Reporting Period, with telecommunication services (+15.15%) and utilities (+11.68%) gaining the most. The industrials sector (+7.06%) was the largest contributor to MSCI® EAFE® Small Cap Index returns on the basis of impact.

Looking Ahead

At the end of the Reporting Period, we continued to believe that less expensive stocks are likely to outpace more expensive stocks. In addition, we believe stocks with good momentum would outperform those with poor momentum. We plan to focus on seeking companies about which fundamental research analysts are becoming more positive as well as profitable companies with sustainable earnings and a track record of using their capital to enhance shareholder value. As such, we anticipate remaining fully invested, with long-term performance likely to be the result of stock selection rather than sector or capitalization allocations.

We stand behind our investment philosophy that sound economic investment principles, coupled with a disciplined quantitative approach, can provide strong, uncorrelated returns over the long term. Our research agenda is robust, and we continue to enhance our existing models, add new proprietary forecasting signals and improve our trading execution as we seek to provide the most value to our shareholders.

| * | All index returns are expressed in U.S. dollar terms. |

6

PORTFOLIO RESULTS

Goldman Sachs Emerging Markets Equity Insights Fund

Investment Objective

The Fund seeks long-term growth of capital.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Quantitative Investment Strategies Team discusses the Goldman Sachs Emerging Markets Equity Insights Fund’s (the “Fund”) performance and positioning for the six-month period ended April 30, 2014 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, C, Institutional and IR Shares generated cumulative total returns, without sales charges, of -3.92%, -4.21%, -3.79% and -3.74%, respectively. These returns compare to the -2.98% cumulative total return of the Fund’s benchmark, the MSCI® Emerging Markets Standard Index (unhedged, with dividends reinvested, net of dividend withholding taxes) (the MSCI® “EM Index”), during the same period. During the period from inception on February 28, 2014 to April 30, 2014, the Fund’s Class R Shares generated a cumulative total return, without sales charges, of 2.78% . This compares to the 3.41% cumulative total return of the Index during the same time period. |

| Q | What key factors were most responsible for the Fund’s performance during the Reporting Period? |

| A | We use two distinct strategies — a bottom-up stock selection strategy and a top-down country/currency selection strategy — to manage the Fund. These strategies are uncorrelated, that is, they tend to perform independently of each other over time, which enables us to greater diversify the portfolio. During the Reporting Period, our country/currency selection strategy detracted from the Fund’s relative returns. Our stock selection strategy, which uses fundamental research and stock selection models based on six investment themes, added to relative performance. |

| Q | Which investment themes helped and which hurt within the Team’s stock selection strategy? |

| A | Our bottom-up stock selection strategy enhanced relative returns during the Reporting Period. We use a quantitative model and six investment themes to take a long-term view of market patterns and look for inefficiencies, selecting stocks for the Fund and overweighting or underweighting those stocks chosen by the model. Over time and by design, the performance of any one of our model’s investment themes tends to have a low correlation with the model’s other themes, demonstrating the diversification benefit of our theme-driven quantitative model. The variance in performance supports our research indicating that the diversification provided by our different investment themes is a significant investment advantage over the long term, even though the Fund may experience underperformance in the short term. Of course, diversification does not protect an investor from market risk nor does it ensure a profit. |

| During the Reporting Period, five of our six investment themes added to the Fund’s relative results. Momentum was our best performing theme. Momentum seeks to predict drifts in stock prices caused by delayed investor reaction to company-specific information and information about related companies. Our Valuation and Sentiment themes also contributed positively, while our Profitability and Quality themes added more modestly to relative returns. The Valuation theme attempts to capture potential mispricings of securities, typically by comparing a measure of the company’s intrinsic value to its market value. The Sentiment theme reflects selected investment views and decisions of individuals and financial intermediaries. The Profitability theme assesses whether a company is earning more than its cost of capital. The Quality theme seeks to assess both firm and management quality. |

| Our Management theme, which assesses the characteristics, policies and strategic decisions of company management, modestly detracted from relative results during the Reporting Period. |

| Q | How did the Fund’s sector and industry allocations affect relative results? |

| A | In constructing the portfolio, we focus on picking stocks rather than on making sector or industry bets. Consequently, |

7

PORTFOLIO RESULTS

the Fund is similar to the MSCI® EM Index in terms of its sector and industry allocations and its style. Changes in its sector or industry weights historically have not had a meaningful impact on relative returns. |

| Q | Did stock selection help or hurt Fund performance during the Reporting Period? |

| A | We seek to outpace the MSCI® EM Index by overweighting stocks we expect to outperform and underweighting those we think may lag. At the same time, we strive to maintain a risk profile similar to the Index. The Fund’s investments are selected using fundamental research and a variety of quantitative techniques based on our investment themes. For example, the Fund aims to hold a basket of stocks with better Momentum characteristics than the benchmark. |

| During the Reporting Period, our security selection added to the Fund’s relative returns. Investments in the health care, information technology and energy sectors contributed most positively. Our stock picks in the materials, consumer discretionary and industrials sectors hurt relative performance. |

| Q | Which stock positions contributed most to the Fund’s relative returns during the Reporting Period? |

| A | The Fund benefited from overweight positions in HCL Technologies, an India-based IT services company; Infosys, an Indian provider of business consulting, technology, engineering and outsourcing services; and Kroton Educacional, a Brazilian educational company. The overweights in HCL Technologies and Infosys were the result of our positive views on Momentum and Valuation. We chose to overweight Kroton Educacional because of our positive views on Momentum and Sentiment. |

| Q | Which Fund positions detracted most from results during the Reporting Period? |

| A | The Fund was hampered during the Reporting Period by its overweights in Brazilian steelmaker Cia Siderurgica Nacional, Russian telecommunications provider Mobile Telesystems and Russian bank Sberbank Rossii. The Fund was overweight Cia Siderurgica given our positive views on Momentum and Valuation, while the overweight in Mobile Telesystems was due to our positive views on Momentum and Profitability. We chose to overweight Sberbank as a result of our positive views on Valuation and Profitability. |

| Q | What impact did the Team’s country/currency selection strategy have on the Fund’s relative performance during the Reporting Period? |

| A | Our country/currency strategy detracted from relative performance during the Reporting Period. The Fund was hurt by its overweight positions in Russia, Hungary and Turkey. On the positive side, Fund performance was enhanced by overweight positions in Brazil and the Czech Republic as well as by an underweight position in Chile. |

| We made our picks using our proprietary models, which, during the Reporting Period, were based on three investment themes specific to our country/currency strategy — Valuation, Risk Premium and Macro. Valuation favors equity and currency markets that appear cheap relative to accounting measures of value and purchasing power. Risk Premium evaluates whether a country is overcompensating investors for various types of risk. Macro assesses a market’s macroeconomic environment and growth prospects. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, we did not use derivatives to hedge positions or as part of an active management strategy. |

| Q | What changes did you make to the Fund’s country weightings during the Reporting Period? |

| A | During the Reporting Period, we moved the Fund from underweight positions relative to the Index in Taiwan, Mexico and Poland to overweight positions. We shifted the Fund from overweight positions in South Africa and Brazil to underweight positions. We also decreased the Fund’s overweight in Russia. |

| Q | What were the Fund’s sector and country weightings at the end of the Reporting Period? |

| A | At the end of the Reporting Period, the Fund was overweight relative to the MSCI® EM Index in the information technology, health care, utilities, materials and industrials sectors relative to the Index. Compared to the Index, the Fund was underweight the consumer staples, telecommunication services, consumer discretionary and financials sectors at the end of the Reporting Period. Compared to the Index, the Fund was relatively neutral to the energy sector at the end of the Reporting Period. |

| In terms of countries, the Fund was overweight China, India, Turkey, Mexico, Poland, Taiwan, Hungary and Russia relative to the Index at the end of the Reporting Period. It was underweight in Malaysia, Korea, South Africa, Colombia, Chile, the Philippines, Greece, Peru, Indonesia, the Czech Republic and Egypt. Compared to the Index, the Fund was neutral in Thailand and Brazil at the end of the Reporting Period. |

8

FUND BASICS

Emerging Markets Equity Insights Fund

as of April 30, 2014

| PERFORMANCE REVIEW | ||||||||||

| November 1, 2013–April 30, 2014 | Fund Total Return (based on NAV)1 | MSCI® EMF Index2 | ||||||||

| Class A | -3.92 | % | -2.98 | % | ||||||

| Class C | -4.21 | -2.98 | ||||||||

| Institutional | -3.79 | -2.98 | ||||||||

| Class IR | -3.74 | -2.98 | ||||||||

| February 28, 2014–April 30, 2014 | MSCI® EM Index2 | |||||||||

| Class R | 2.78 | % | 3.41 | % | ||||||

| 1 | The net asset value (NAV) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The MSCI® EM Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. As of November 27, 2013, the MSCI® EM Index consisted of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey. Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index. |

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||

| For the period ended 3/31/14 | One Year | Five Years | Since Inception | Inception Date | ||||||||

| Class A | -9.72 | % | 13.80% | -2.30% | 10/5/07 | |||||||

| Class C | -6.25 | 14.25 | -2.12 | 10/5/07 | ||||||||

| Institutional | -4.25 | 15.55 | -1.07 | 10/5/07 | ||||||||

| Class IR | -4.31 | N/A | 4.45 | 8/31/10 | ||||||||

| Class R | N/A | N/A | 2.78 | 2/28/14 | ||||||||

| 3 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Class R and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

9

FUND BASICS

| EXPENSE RATIOS4 | ||||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.58 | % | 1.65 | % | ||||||

| Class C | 2.33 | 2.48 | ||||||||

| Institutional | 1.18 | 1.27 | ||||||||

| Class IR | 1.33 | 1.50 | ||||||||

| Class R | 1.83 | 1.92 | ||||||||

| 4 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| TOP TEN HOLDINGS AS OF 4/30/145 | ||||||||||

| Holding | % of Total Net Assets | Line of Business | Country | |||||||

| Samsung Electronics Co. Ltd. | 4.4 | % | Semiconductors & Semiconductor Equipment | South Korea | ||||||

| Taiwan Semiconductor Manufacturing Co. Ltd. ADR | 4.1 | Semiconductors & Semiconductor Equipment | Taiwan | |||||||

| China Construction Bank Corp. Class H | 2.9 | Banks | China | |||||||

| Itau Unibanco Holding SA ADR | 2.5 | Banks | Brazil | |||||||

| Bank of China Ltd. Class H | 2.5 | Banks | China | |||||||

| SK Hynix, Inc. | 2.1 | Semiconductors & Semiconductor Equipment | South Korea | |||||||

| BRF SA | 1.9 | Food, Beverage & Tobacco | Brazil | |||||||

| Kia Motors Corp. | 1.9 | Automobiles & Components | South Korea | |||||||

| America Movil SAB de CV Series L ADR | 1.9 | Telecommunication Services | Mexico | |||||||

| Industrial & Commercial Bank of China Ltd. Class H | 1.8 | Banks | China | |||||||

| 5 | The top 10 holdings may not be representative of the Fund’s future investments. |

10

FUND BASICS

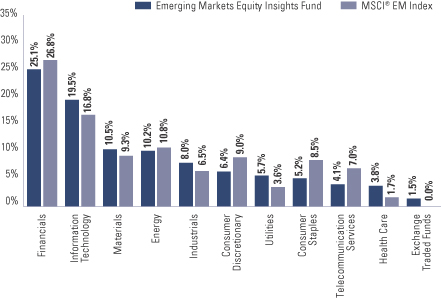

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 |

| As of April 30, 2014 |

| 6 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall industry sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. Underlying sector allocations of exchange traded funds held by the Fund are not reflected in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value (excluding investments in the securities lending reinvestment vehicle, if any). Investments in the securities lending reinvestment vehicle represented 2.4% of the Fund’s net assets at April 30, 2014. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

11

PORTFOLIO RESULTS

Goldman Sachs International Equity Insights Fund

Investment Objective

The Fund seeks long-term growth of capital.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Quantitative Investment Strategies Team discusses the Goldman Sachs International Equity Insights Fund’s (the “Fund”) performance and positioning for the six-month period ended April 30, 2014 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, B, C, Institutional, Service, IR and R Shares generated cumulative total returns, without sales charges, of 4.63%, 4.28%, 4.24%, 4.79%, 4.66%, 4.78% and 4.50%, respectively. These returns compare to the 4.44% cumulative total return of the Fund’s benchmark, the MSCI® EAFE® Standard Index (unhedged, with dividends reinvested, net of dividend withholding taxes) (the “MSCI® EAFE® (net) Index”), during the same period. |

| Q | What key factors were most responsible for the Fund’s performance during the Reporting Period? |

| A | We use two distinct strategies — a bottom-up stock selection strategy and a top-down country/currency selection strategy — to manage the Fund. These strategies are uncorrelated, that is, they tend to perform independently of each other over time, which enables us to greater diversify the portfolio. Our bottom-up stock selection strategy, which uses fundamental research and stock selection models based on six investment themes, contributed positively during the Reporting Period. Our country/currency selection strategy detracted from the Fund’s relative performance. |

| Q | Which investment themes helped and which hurt within the Team’s stock selection strategy? |

| A | Our bottom-up stock selection strategy added to relative returns during the Reporting Period. We use a quantitative model and six investment themes to take a long-term view of market patterns and look for inefficiencies, selecting stocks for the Fund and overweighting or underweighting those stocks chosen by the model. Over time and by design, the performance of any one of our model’s investment themes tends to have a low correlation with the model’s other themes, demonstrating the diversification benefit of our theme-driven quantitative model. The variance in performance supports our research indicating that the diversification provided by our different investment themes is a significant investment advantage over the long term, even though the Fund may experience underperformance in the short term. Of course, diversification does not protect an investor from market risk nor does it ensure a profit. |

| During the Reporting Period, five of our six investment themes added to the Fund’s relative returns. Our best-performing theme was Momentum. The Momentum theme seeks to predict drifts in stock prices caused by delayed investor reaction to company-specific information and information about related companies. Sentiment, Profitability, Quality and Valuation also added to relative returns. The Sentiment theme reflects selected investment views and decisions of individuals and financial intermediaries. The Profitability theme assesses whether a company is earning more than its cost of capital. The Quality theme seeks to assess both firm and management quality. The Valuation theme attempts to capture potential mispricings of securities, typically by comparing a measure of the company’s intrinsic value to its market value. |

| The impact of our Management theme was relatively neutral during the Reporting Period. Management assesses the characteristics, policies and strategic decisions of company management. |

| Q | How did the Fund’s sector and industry allocations affect relative results? |

| A | In constructing the portfolio, we focus on picking stocks rather than on making sector or industry bets. Consequently, the Fund is similar to the MSCI® EAFE® (net) Index in terms of its sector and industry allocations and its style. Changes in its sector or industry weights historically have not had a meaningful impact on relative returns. |

| Q | Did stock selection help or hurt Fund performance during the Reporting Period? |

| A | We seek to outpace the MSCI® EAFE® (net) Index by overweighting stocks we expect to outperform and |

12

PORTFOLIO RESULTS

underweighting those we think may lag. At the same time, we strive to maintain a risk profile similar to the Index. The Fund’s investments are selected using fundamental research and a variety of quantitative techniques based on our investment themes. For example, the Fund aims to hold a basket of stocks with better Momentum characteristics than the benchmark. |

| During the Reporting Period, our security selection added to the Fund’s relative returns. Investments in the industrials, telecommunication services and information technology sectors contributed most positively. Stock picks in the consumer staples, materials and utilities sectors detracted from relative performance. |

| Q | Which stock positions contributed most to the Fund’s relative returns during the Reporting Period? |

| A | The Fund benefited from overweighted positions in AstraZeneca, a British-Swedish pharmaceutical and biologic company; Vestas Wind Systems, a Danish manufacturer of wind turbines; and easyJet, a London-headquartered airline company. We chose to overweight AstraZeneca because of our positive views on Valuation and Management. The Fund was overweight Vestas Wind Systems given our positive views on Momentum and Quality. Our positive views on Momentum and Sentiment led us to overweight easyJet. |

| Q | Which Fund positions detracted most from results during the Reporting Period? |

| A | An underweight in Novartis, a Swiss pharmaceutical company, detracted from the Fund’s relative performance. The Fund was also hampered by overweighted positions in Nomura Holdings, a Japanese financial holding company, and Sumitomo Mitsui Financial Group, a Japanese bank holding and financial services company. Our negative views on Momentum and Profitability resulted in the Fund’s underweight in Novartis. We assumed the overweight in Nomura Holdings due to our positive views on Profitability and Valuation, while the overweight in Sumitomo was because of our positive views on Momentum and Profitability. |

| Q | What impact did the Team’s country/currency selection strategy have on the Fund’s relative performance during the Reporting Period? |

| A | Our country/currency selection strategy detracted from Fund returns during the Reporting Period. The Fund was hurt by its overweight in Japan and its underweighted positions in Italy and Spain. It benefited from overweighted positions in Switzerland and Germany and an underweight in Hong Kong. We made our picks using our proprietary models, which, during the Reporting Period, were based on five investment factors specific to our country/currency strategy — Valuation, Momentum, Risk Premium, Fund Flows and Macro. Valuation favors equity and currency markets that appear cheap relative to accounting measures of value and purchasing power. The Momentum factor favors countries and currencies that have had strong recent outperformance. Risk Premium evaluates whether a country is overcompensating investors for various types of risk, while Fund Flows evaluates the strength of capital market inflows. Finally, Macro assesses a market’s macroeconomic environment and growth prospects. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, we used financial futures contracts to equitize the Fund’s cash holdings. In other words, we put the Fund’s cash holdings to work by using them as collateral for the purchase of financial futures contracts. |

| Q | What changes did you make to the Fund’s country weightings during the Reporting Period? |

| A | During the Reporting Period, we shifted the Fund from an underweighted position in Finland to an overweighted position. We decreased the Fund’s underweights in Spain and Hong Kong, but maintained underweighted positions. We moved the Fund from overweighted positions in France, the U.K. and Belgium to underweighted positions. |

| Q | What were the Fund’s sector and country weightings at the end of the Reporting Period? |

| A | At the end of the Reporting Period, the Fund was overweight the health care sector relative to the Index. The Fund was underweight compared to the Index in the financials, consumer discretionary and consumer staples sectors at the end of the Reporting Period. Compared to the Index, the Fund was relatively neutral in the information technology, industrials, utilities, energy, telecommunications and materials sectors at the end of the Reporting Period. |

| In terms of countries, the Fund was overweight relative to the Index in Japan, Switzerland, Finland, Norway, Germany and Singapore at the end of the Reporting Period. The Fund was underweight compared to the Index in Sweden, Australia, the U.K., Spain, Israel, France, Italy, the Netherlands, Ireland, Belgium, Denmark, Portugal, New Zealand and Austria at the end of the Reporting Period. Compared to the Index, the Fund was relatively neutral in Hong Kong at the end of the Reporting Period. |

13

FUND BASICS

International Equity Insights Fund

as of April 30, 2014

| PERFORMANCE REVIEW | ||||||||||

| November 1, 2013–April 30, 2014 | Fund Total Return (based on NAV)1 | MSCI EAFE (Net) Index2 | ||||||||

| Class A | 4.63 | % | 4.44 | % | ||||||

| Class B | 4.28 | 4.44 | ||||||||

| Class C | 4.24 | 4.44 | ||||||||

| Institutional | 4.79 | 4.44 | ||||||||

| Service | 4.66 | 4.44 | ||||||||

| Class IR | 4.78 | 4.44 | ||||||||

| Class R | 4.50 | 4.44 | ||||||||

| 1 | The net asset value (NAV) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The unmanaged MSCI® EAFE® (net) Index is a market capitalization-weighted composite of securities in 21 developed markets (as of November 27, 2013). The Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index. |

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||

| For the period ended 3/31/14 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||

| Class A | 12.89 | % | 13.21% | 5.14% | 3.49% | 8/15/97 | ||||||||

| Class B | 13.58 | 13.33 | 5.09 | 3.58 | 8/15/97 | |||||||||

| Class C | 17.64 | 13.61 | 4.96 | 3.19 | 8/15/97 | |||||||||

| Institutional | 20.07 | 14.94 | 6.16 | 4.37 | 8/15/97 | |||||||||

| Service | 19.31 | 14.34 | 5.63 | 3.85 | 8/15/97 | |||||||||

| Class IR | 19.76 | 14.74 | N/A | -0.89 | 11/30/07 | |||||||||

| Class R | 19.19 | 14.22 | N/A | -1.35 | 11/30/07 | |||||||||

| 3 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares, the assumed contingent deferred sales charge for Class B Shares (5% maximum declining to 0% after six years) and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Class B Shares convert to Class A Shares on or about the fifteenth day of the last month of the calendar quarter that is eight years after purchase. Returns for Class B Shares for the period after conversion reflect the performance of Class A Shares. Because Institutional, Service, Class IR and Class R Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. The Fund’s Class B Shares are no longer available for purchase by new or existing shareholders (although current Class B shareholders may continue to reinvest income and capital gains distributions into Class B Shares, and Class B shareholders may continue to exchange their shares for Class B Shares of certain other Goldman Sachs Funds). |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

14

FUND BASICS

| EXPENSE RATIOS4 | ||||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.29 | % | 1.37 | % | ||||||

| Class B | 2.04 | 2.11 | ||||||||

| Class C | 2.04 | 2.11 | ||||||||

| Institutional | 0.89 | 0.96 | ||||||||

| Service | 1.39 | 1.46 | ||||||||

| Class IR | 1.04 | 1.11 | ||||||||

| Class R | 1.54 | 1.61 | ||||||||

| 4 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| TOP TEN HOLDINGS AS OF 4/30/145 | ||||||||||

| Holding | % of Total Net Assets | Line of Business | Country | |||||||

| Roche Holding AG | 3.2 | % | Pharmaceuticals, Biotechnology & Life Sciences | Switzerland | ||||||

| HSBC Holdings PLC | 2.9 | Banks | United Kingdom | |||||||

| BP PLC ADR | 2.4 | Energy | United Kingdom | |||||||

| British American Tobacco PLC | 1.9 | Food, Beverage & Tobacco | United Kingdom | |||||||

| Royal Dutch Shell PLC Class A | 1.5 | Energy | Netherlands | |||||||

| BHP Billiton PLC | 1.5 | Materials | United Kingdom | |||||||

| Vodafone Group PLC ADR | 1.5 | Telecommunication Services | United Kingdom | |||||||

| ABB Ltd. (Registered) | 1.4 | Capital Goods | Switzerland | |||||||

| Commonwealth Bank of Australia | 1.3 | Banks | Australia | |||||||

| GlaxoSmith Kline PLC ADR | 1.3 | Pharmaceuticals, Biotechnology & Life Sciences | Netherlands | |||||||

| 5 | The top 10 holdings may not be representative of the Fund’s future investments. |

15

FUND BASICS

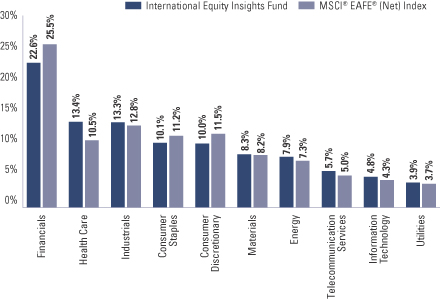

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 |

| As of April 30, 2014 |

| 6 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall industry sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value (excluding investments in the securities lending reinvestment vehicle, if any). Investments in the securities lending reinvestment vehicle represented 6.6% of the Fund’s net assets at April 30, 2014. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

16

PORTFOLIO RESULTS

Goldman Sachs International Small Cap Insights Fund

Investment Objective

The Fund seeks long-term growth of capital.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Quantitative Investment Strategies Team discusses the Goldman Sachs International Small Cap Insights Fund’s (the “Fund”) performance and positioning for the six-month period ended April 30, 2014 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, C, Institutional and IR Shares generated cumulative total returns, without sales charges, of 5.00%, 4.56%, 5.22% and 5.20%, respectively. These returns compare to the 5.38% cumulative total return of the Fund’s benchmark, the MSCI® EAFE® Small Cap Index (unhedged, with dividends reinvested, net of dividend withholding taxes) (the “MSCI® EAFE® Small Cap (net) Index”), during the same period. |

| Q | What key factors were most responsible for the Fund’s performance during the Reporting Period? |

| A | Although our quantitative model and its investment themes added to relative returns, the Fund underperformed the Index during the Reporting Period due mainly to stock selection. |

| Q | What impact did the Fund’s investment themes have on performance during the Reporting Period? |

| A | As expected, and in keeping with our investment approach, our quantitative model and six investment themes had the greatest impact on relative performance. We use these themes to take a long-term view of market patterns and look for inefficiencies, selecting stocks for the Fund and overweighting or underweighting those stocks chosen by the model. Over time and by design, the performance of any one of our model’s investment themes tends to have a low correlation with the model’s other themes, demonstrating the diversification benefit of our theme-driven quantitative model. The variance in performance supports our research indicating that the diversification provided by our different investment themes is a significant investment advantage over the long term, even though the Fund may experience underperformance in the short term. Of course, diversification does not protect an investor from market risk nor does it ensure a profit. |

| During the Reporting Period, all six of our investment themes added to the Fund’s relative returns. Momentum was the Fund’s best performing theme. Momentum seeks to predict drifts in stock prices caused by delayed investor reaction to company-specific information and information about related companies. Valuation and Sentiment also contributed positively. The Valuation theme attempts to capture potential mispricings of securities, typically by comparing a measure of the company’s intrinsic value to its market value. The Sentiment theme reflects selected investment views and decisions of individuals and financial intermediaries. In addition, Quality, Management and Profitability added value, though to a lesser extent. Quality seeks to assess both firm and management quality. Management assesses the characteristics, policies and strategic decisions of company management. Profitability assesses whether a company is earning more than its cost of capital. |

| Q | How did the Fund’s sector and industry allocations affect relative results? |

| A | In constructing the portfolio, we focus on picking stocks rather than on making sector or industry bets. Consequently, the Fund is similar to the MSCI® EAFE® Small Cap (net) Index in terms of its sector and industry allocations and its style. Changes in its sector or industry weights historically have not had a meaningful impact on relative returns. |

17

PORTFOLIO RESULTS

| Q | Did stock selection help or hurt Fund performance during the Reporting Period? |

| A | We seek to outpace the MSCI® EAFE® Small Cap (net) Index by overweighting stocks we expect to outperform and underweighting those we think may lag. At the same time, we strive to maintain a risk profile similar to the MSCI® EAFE® Small Cap (net) Index. The Fund’s investments are selected using fundamental research and a variety of quantitative techniques based on our investment themes. For example, the Fund aims to hold a basket of stocks with better Momentum characteristics than the benchmark. |

| During the Reporting Period, our stock picks dampened relative performance. Security selection in the health care, information technology and energy sectors detracted from relative returns. Investments in the financials, consumer discretionary and telecommunication services sectors contributed positively. |

| Q | Which Fund positions detracted most from results during the Reporting Period? |

| A | Detracting from relative returns was the Fund’s overweight in Takara Bio, a Japanese biomedical business; Tella, a Japanese company that engages in the research and development of regenerative and cell medicines; and Blinkx, a London-based Internet media platform. The Fund was overweight Takara Bio and Tella given our positive views on Momentum and Sentiment. The overweight in Blinkx was established because of our positive views on Momentum and Profitability. |

| Q | Which stock positions contributed most to the Fund’s relative returns during the Reporting Period? |

| A | The Fund benefited from overweighted positions in Adways, a Japanese digital advertising network and game publisher; Banca Popolare di Milano, an Italian cooperative bank; and Aperam, a Luxembourg-based producer of stainless and specialty steel. We chose to overweight Adways and Aperam because of our positive views on Momentum and Sentiment. The Fund’s overweight in Banca Popolare di Milano was due to our positive views on Momentum and Valuation. |

| Q | What impact did country selection have on the Fund’s relative performance during the Reporting Period? |

| A | To construct the portfolio, we focus on security selection rather than on making country bets. As a result, the Fund is similar to the MSCI® EAFE® Small Cap (net) Index in terms of its country allocation; changes in its country weightings are generally the result of our stock picking. That said, the Fund benefited during the Reporting Period from its overweights relative to the MSCI® EAFE® Small Cap (net) Index in the Netherlands, Germany and Switzerland. Compared to the MSCI® EAFE® Small Cap (net) Index, the Fund was hurt by its overweight in Japan and by its underweighted positions in Singapore and Finland. Security selection in all six countries added to returns. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, we used financial futures contracts to equitize the Fund’s cash holdings. In other words, we put the Fund’s cash holdings to work by using them as collateral for the purchase of financial futures contracts. |

| Q | What changes did you make to the Fund’s country weightings during the Reporting Period? |

| A | During the Reporting Period, we moved the Fund from an underweighted position relative to the Index in Hong Kong to an overweighted position. We increased the Fund’s overweights in Italy and France. In addition, we shifted the Fund from overweighted positions in Spain and Belgium to underweighted positions. We also increased the Fund’s underweight compared to the Index in the U.K. |

| Q | What were the Fund’s sector and country weightings at the end of the Reporting Period? |

| A | At the end of the Reporting Period, the Fund was overweight the industrials, information technology and utilities sectors relative to the Index. Compared to the Index, the Fund was underweight the consumer staples, financials, energy, consumer discretionary and telecommunication services sectors at the end of the Reporting Period. Compared to the Index, the Fund was relatively neutral to the health care and materials sectors at the end of the Reporting Period. |

| In terms of countries, the Fund was overweight Germany, Australia, Italy, the Netherlands, Switzerland, Japan, France and Sweden relative to the Index. The Fund was underweight compared to the Index in the U.K., Singapore, Finland, Norway, Israel, Ireland, Belgium and New Zealand at the end of the Reporting Period. At the end of the Reporting Period, the Fund was relatively neutral compared to the Index in Hong Kong, Denmark, Spain, Portugal and Austria. |

18

FUND BASICS

International Small Cap Insights Fund

as of April 30, 2014

| PERFORMANCE REVIEW | ||||||||||

| November 1, 2013–April 30, 2014 | Fund Total Return (based on NAV)1 | MSCI® EAFE® Small Cap (net) Index2 | ||||||||

| Class A | 5.00 | % | 5.38 | % | ||||||

| Class C | 4.56 | 5.38 | ||||||||

| Institutional | 5.22 | 5.38 | ||||||||

| Class IR | 5.20 | 5.38 | ||||||||

| 1 | The net asset value (NAV) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charge. |

| 2 | The MSCI EAFE Small Cap (Net) Index (unhedged and net of dividend withholding taxes) is a free float-adjusted market capitalization index that is designed to measure developed market equity performance, excluding the US and Canada. MSCI selects the most liquid securities across developed markets relative to their market capitalization, and targets for index inclusion 40% of the full market capitalization of the eligible small cap universe within each industry group, within each country. Its returns include net reinvested dividends but, unlike Fund returns, do not reflect the payment of sales commissions or other expenses incurred in the purchase or sale of the securities included in the Index. It is not possible to invest directly in an index. |

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||

| For the period ended 3/31/14 | One Year | Five Years | Since Inception | Inception Date | ||||||||||||

| Class A | 17.05 | % | 22.55 | % | 3.52 | % | 9/28/07 | |||||||||

| Class C | 21.85 | 23.00 | 3.67 | 9/28/07 | ||||||||||||

| Institutional | 24.47 | 24.40 | 4.85 | 9/28/07 | ||||||||||||

| Class IR | 24.22 | N/A | 17.64 | 8/31/10 | ||||||||||||

| 3 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

19

FUND BASICS

| EXPENSE RATIOS4 | ||||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.30 | % | 1.48 | % | ||||||

| Class C | 2.05 | 2.24 | ||||||||

| Institutional | 0.90 | 1.07 | ||||||||

| Class IR | 1.05 | 1.26 | ||||||||

| 4 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| TOP TEN HOLDINGS AS OF 4/30/145 | ||||||||||

| Holding | % of Total Net Assets | Line of Business | Country | |||||||

| Vestas Wind Systems A/S | 1.2 | % | Capital Goods | Denmark | ||||||

| Pennon Group PLC | 0.8 | Utilities | United Kingdom | |||||||

| Challenger Ltd. | 0.8 | Diversified Financials | Australia | |||||||

| CSR Ltd. | 0.7 | Materials | Australia | |||||||

| Banca Popolare di Milano Scarl | 0.7 | Banks | Italy | |||||||

| Leoni AG | 0.7 | Automobiles & Components | Germany | |||||||

| Thomas Cook Group PLC | 0.7 | Consumer Services | United Kingdom | |||||||

| Gamesa Corp. Tecnologica SA | 0.7 | Capital Goods | Spain | |||||||

| Investa Office Fund (REIT) | 0.7 | Real Estate | Australia | |||||||

| Nordex SE | 0.7 | Capital Goods | Germany | |||||||

| 5 | The top 10 holdings may not be representative of the Fund’s future investments. |

20

FUND BASICS

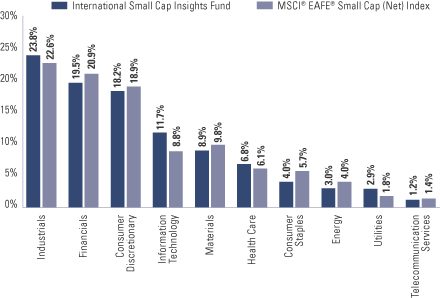

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 |

| As of April 30, 2014 |

| 6 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall industry sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value (excluding investments in the securities lending reinvestment vehicle, if any). Investments in the securities lending reinvestment vehicle represented 7.7% of the Fund’s net assets at April 30, 2014. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

21

GOLDMAN SACHS EMERGING MARKETS EQUITY INSIGHTS FUND

Schedule of Investments

April 30, 2014 (Unaudited)

Shares | Description | Value | ||||||

| Common Stocks – 92.0% | ||||||||

| Brazil – 6.4% | ||||||||

| 247,400 | AMBEV SA ADR (Food, Beverage & Tobacco) | $ | 1,793,650 | |||||

| 651,500 | Banco Bradesco SA (Banks) | 10,007,344 | ||||||

| 295,500 | Banco do Brasil SA (Banks) | 3,102,435 | ||||||

| 43,600 | Banco Santander Brasil SA ADR (Banks) | 289,940 | ||||||

| 550,000 | BRF SA (Food, Beverage & Tobacco) | 12,456,553 | ||||||

| 703,100 | Companhia de Saneamento Basico do Estado de Sao Paulo ADR (Utilities)(a) | 6,665,388 | ||||||

| 48,900 | Mahle-Metal Leve SA Industria e Comercio (Automobiles & Components) | 482,695 | ||||||

| 425,500 | Porto Seguro SA (Insurance) | 6,201,929 | ||||||

| 54,200 | Sul America SA (Insurance) | 397,430 | ||||||

|

| |||||||

| 41,397,364 | ||||||||

|

| |||||||

| Chile – 0.6% | ||||||||

| 73,093 | Latam Airlines Group SA (Transportation) | 1,116,794 | ||||||

| 86,854 | Sociedad Quimica y Minera de Chile SA ADR (Materials)(a) | 2,770,643 | ||||||

|

| |||||||

| 3,887,437 | ||||||||

|

| |||||||

| China – 17.2% | ||||||||

| 63,000 | AAC Technologies Holdings, Inc. (Technology Hardware & Equipment) | 352,758 | ||||||

| 22,731,000 | Agricultural Bank of China Ltd. Class H (Banks) | 9,564,767 | ||||||

| 2,241,500 | Anhui Conch Cement Co. Ltd. Class H (Materials)(a) | 8,369,205 | ||||||

| 36,255,000 | Bank of China Ltd. Class H (Banks) | 15,973,898 | ||||||

| 27,102,000 | China Construction Bank Corp. Class H (Banks) | 18,764,710 | ||||||

| 4,407,000 | China Merchants Bank Co. Ltd. Class H (Banks) | 7,896,376 | ||||||

| 1,194,000 | China Railway Construction Corp. Ltd. Class H (Capital Goods) | 990,837 | ||||||

| 1,595,000 | China Shanshui Cement Group Ltd. (Materials) | 616,987 | ||||||

| 1,464,000 | CNOOC Ltd. (Energy) | 2,419,771 | ||||||

| 3,912,500 | Fosun International Ltd. (Materials)(a) | 4,743,597 | ||||||

| 944,000 | Haitian International Holdings Ltd. (Capital Goods) | 1,901,799 | ||||||

| 3,246,000 | Huaneng Power International, Inc. Class H (Utilities) | 3,177,468 | ||||||

| 19,962,000 | Industrial & Commercial Bank of China Ltd. Class H (Banks) | 11,927,659 | ||||||

| 686,000 | Jiangsu Expressway Co. Ltd. Class H (Transportation) | 772,853 | ||||||

| 8,530,000 | PetroChina Co. Ltd. Class H (Energy) | 9,841,702 | ||||||

| 173,500 | Shanghai Pharmaceuticals Holding Co. Ltd. Class H (Health Care Equipment & Services) | 317,776 | ||||||

|

| |||||||

| Common Stocks – (continued) | ||||||||

| China – (continued) | ||||||||

| 6,041,000 | Sihuan Pharmaceutical Holdings Group Ltd. (Pharmaceuticals, Biotechnology & Life Sciences) | $ | 6,677,185 | |||||

| 116,600 | Tencent Holdings Ltd. (Software & Services) | 7,341,130 | ||||||

|

| |||||||

| 111,650,478 | ||||||||

|

| |||||||

| Greece – 0.1% | ||||||||

| 26,675 | Hellenic Telecommunications Organization SA (Telecommunication Services)* | 426,153 | ||||||

|

| |||||||

| Hong Kong – 3.0% | ||||||||

| 376,000 | China Gas Holdings Ltd. (Utilities) | 612,053 | ||||||

| 3,844,000 | China Power International Development Ltd. (Utilities) | 1,384,078 | ||||||

| 1,040,000 | China Resources Cement Holdings Ltd. (Materials) | 724,016 | ||||||

| 4,236,000 | China Resources Power Holdings Co. Ltd. (Utilities) | 10,646,591 | ||||||

| 8,860,000 | GCL-Poly Energy Holdings Ltd. (Semiconductors & Semiconductor Equipment)* | 2,661,284 | ||||||

| 728,000 | Guangdong Investment Ltd. (Utilities) | 791,487 | ||||||

| 803,500 | NetDragon Websoft, Inc. (Software & Services) | 1,375,678 | ||||||

| 1,572,000 | Sino Biopharmaceutical Ltd. (Pharmaceuticals, Biotechnology & Life Sciences) | 1,233,671 | ||||||

|

| |||||||

| 19,428,858 | ||||||||

|

| |||||||

| Hungary – 0.6% | ||||||||

| 229,992 | Magyar Telekom Telecommunications PLC (Telecommunication Services) | 328,124 | ||||||

| 192,914 | Richter Gedeon Nyrt (Pharmaceuticals, Biotechnology & Life Sciences) | 3,304,124 | ||||||

|

| |||||||

| 3,632,248 | ||||||||

|

| |||||||

| India – 8.2% | ||||||||

| 58,196 | Bajaj Holdings and Investment Ltd. (Diversified Financials) | 1,012,725 | ||||||

| 1,525,396 | Cairn India Ltd. (Energy) | 8,484,077 | ||||||

| 59,398 | CESC Ltd. (Utilities) | 448,578 | ||||||

| 582,504 | GAIL India Ltd. (Utilities) | 3,577,622 | ||||||

| 283,304 | HCL Technologies Ltd. (Software & Services) | 6,592,597 | ||||||

| 182,056 | Lupin Ltd. (Pharmaceuticals, Biotechnology & Life Sciences) | 3,108,179 | ||||||

| 1,215,282 | Oil & Natural Gas Corp. Ltd. (Energy) | 6,560,141 | ||||||

| 502,620 | Reliance Industries Ltd. (Energy) | 7,812,785 | ||||||

| 671,208 | Sun Pharmaceutical Industries Ltd. (Pharmaceuticals, Biotechnology & Life Sciences) | 7,051,197 | ||||||

|

| |||||||

| 22 | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS EMERGING MARKETS EQUITY INSIGHTS FUND

Shares | Description | Value | ||||||

| Common Stocks – (continued) | ||||||||

| India – (continued) | ||||||||

| 610,117 | Tata Motors Ltd. (Automobiles & Components) | $ | 4,220,339 | |||||

| 482,711 | Wipro Ltd. (Software & Services) | 4,183,534 | ||||||

|

| |||||||

| 53,051,774 | ||||||||

|

| |||||||

| Indonesia – 2.2% | ||||||||

| 479,600 | PT Astra Agro Lestari Tbk (Food, Beverage & Tobacco) | 1,221,151 | ||||||

| 1,537,000 | PT Astra International Tbk (Automobiles & Components) | 990,277 | ||||||

| 7,521,400 | PT Bank Mandiri (Persero) Tbk (Banks) | 6,426,406 | ||||||

| 1,520,500 | PT Bank Negara Indonesia (Persero) Tbk (Banks) | 635,485 | ||||||

| 1,901,400 | PT Bank Rakyat Indonesia (Persero) Tbk (Banks) | 1,632,838 | ||||||

| 1,222,900 | PT Indofood Sukses Makmur Tbk (Food, Beverage & Tobacco) | 748,087 | ||||||

| 3,040,800 | PT Perusahaan Gas Negara (Persero) Tbk (Utilities) | 1,404,405 | ||||||

| 659,600 | PT United Tractors Tbk (Capital Goods) | 1,240,134 | ||||||

|

| |||||||

| 14,298,783 | ||||||||

|

| |||||||

| Malaysia – 1.1% | ||||||||

| 5,601,200 | Genting Malaysia Bhd (Consumer Services) | 7,244,911 | ||||||

| 462,105 | YTL Power International Bhd (Utilities)* | 222,369 | ||||||

|

| |||||||

| 7,467,280 | ||||||||

|

| |||||||

| Mexico – 6.6% | ||||||||

| 602,580 | America Movil SAB de CV Series L ADR (Telecommunication Services) | 12,099,806 | ||||||

| 548,376 | Cemex SAB de CV ADR (Materials)* | 6,931,473 | ||||||

| 389,900 | Gruma SAB de CV Class B (Food, Beverage & Tobacco)* | 3,444,585 | ||||||

| 58,910 | Grupo Aeroportuario del Pacifico SAB de CV ADR (Transportation) | 3,552,273 | ||||||

| 77,760 | Grupo Aeroportuario del Sureste SAB de CV ADR (Transportation) | 9,506,160 | ||||||

| 464,800 | Grupo Bimbo SAB de CV Series A (Food, Beverage & Tobacco) | 1,283,971 | ||||||

| 90,900 | Grupo Carso SAB de CV Series A-1 (Capital Goods) | 462,047 | ||||||

| 1,978,600 | Kimberly-Clark de Mexico SAB de CV Class A (Household & Personal Products) | 5,143,581 | ||||||

| 37,800 | Promotora y Operadora de Infraestructura SAB de CV (Capital Goods)* | 528,338 | ||||||

|

| |||||||

| 42,952,234 | ||||||||

|

| |||||||

| Philippines – 0.1% | ||||||||

| 262,870 | Universal Robina Corp. (Food, Beverage & Tobacco) | 863,203 | ||||||

|

| |||||||

| Common Stocks – (continued) | ||||||||

| Poland – 3.2% | ||||||||

| 9,842 | Bank Pekao SA (Banks) | $ | 631,664 | |||||

| 7,531 | Bank Zachodni WBK SA (Banks) | 925,949 | ||||||

| 77,702 | KGHM Polska Miedz SA (Materials) | 2,813,429 | ||||||

| 776,384 | PGE SA (Utilities) | 5,394,940 | ||||||

| 78,120 | Powszechny Zaklad Ubezpieczen SA (Insurance) | 11,081,404 | ||||||

|

| |||||||

| 20,847,386 | ||||||||

|

| |||||||

| Russia – 4.9% | ||||||||

| 1,624,925 | OAO Gazprom ADR (Energy) | 11,743,231 | ||||||

| 87,506 | OAO Lukoil ADR (Energy) | 4,632,520 | ||||||

| 571,880 | OAO Rosneft GDR (Energy) | 3,595,467 | ||||||

| 40,696 | OAO Tatneft ADR (Energy) | 1,399,802 | ||||||

| 5,005,340 | Sberbank of Russia (Banks)* | 10,214,288 | ||||||

|

| |||||||

| 31,585,308 | ||||||||

|

| |||||||

| South Africa – 6.3% | ||||||||

| 98,195 | African Rainbow Minerals Ltd. (Materials) | 1,848,927 | ||||||

| 183,871 | Investec Ltd. (Diversified Financials) | 1,618,327 | ||||||

| 366,527 | Liberty Holdings Ltd. (Insurance) | 4,396,533 | ||||||

| 612,825 | Life Healthcare Group Holdings Ltd. (Health Care Equipment & Services) | 2,436,928 | ||||||

| 465,040 | Mondi Ltd. (Materials) | 7,743,665 | ||||||

| 402,558 | MTN Group Ltd. (Telecommunication Services) | 8,076,043 | ||||||

| 95,390 | Nedbank Group Ltd. (Banks) | 2,044,867 | ||||||

| 62,716 | Sasol Ltd. (Energy) | 3,514,876 | ||||||

| 1,444,796 | Sibanye Gold Ltd. (Materials) | 3,731,955 | ||||||

| 123,706 | Sun International Ltd. (Consumer Services) | 1,222,891 | ||||||

| 568,608 | Super Group Ltd. (Retailing)* | 1,532,070 | ||||||

| 225,509 | Vodacom Group Ltd. (Telecommunication Services) | 2,691,259 | ||||||

|

| |||||||

| 40,858,341 | ||||||||

|

| |||||||

| South Korea – 12.7% | ||||||||

| 3,432 | Dong-A ST Co. Ltd. (Pharmaceuticals, Biotechnology & Life Sciences) | 352,526 | ||||||

| 97,490 | Hansol Paper Co. Ltd. (Materials) | 1,073,774 | ||||||

| 20,790 | Hyundai Corp. (Capital Goods) | 634,889 | ||||||

| 30,330 | Hyundai Development Co. – Engineering & Construction (Capital Goods) | 869,578 | ||||||

| 1,195 | Hyundai Mobis (Automobiles & Components) | 341,392 | ||||||

| 2,054 | Hyundai Motor Co. (Automobiles & Components) | 457,973 | ||||||

| 5,240 | KCC Corp. (Capital Goods) | 2,613,061 | ||||||

| 223,565 | Kia Motors Corp. (Automobiles & Components) | 12,403,885 | ||||||

| 21,893 | Korea Gas Corp. (Utilities)* | 1,311,098 | ||||||

| 39,526 | KT&G Corp. (Food, Beverage & Tobacco) | 3,167,694 | ||||||

| 171,280 | LG Uplus Corp. (Telecommunication Services) | 1,686,910 | ||||||

|

| |||||||

| The accompanying notes are an integral part of these financial statements. | 23 |

GOLDMAN SACHS EMERGING MARKETS EQUITY INSIGHTS FUND

Schedule of Investments (continued)

April 30, 2014 (Unaudited)

Shares | Description | Value | ||||||

| Common Stocks – (continued) | ||||||||

| South Korea – (continued) | ||||||||

| 27,166 | Mando Corp. (Automobiles & Components) | $ | 3,268,009 | |||||

| 11,456 | NCSoft Corp. (Software & Services) | 2,279,507 | ||||||

| 21,767 | Samsung Electronics Co. Ltd. (Semiconductors & Semiconductor Equipment) | 28,383,322 | ||||||

| 14,855 | Samyang Holdings Corp. (Food, Beverage & Tobacco) | 1,035,969 | ||||||

| 39,762 | SK Holdings Co. Ltd. (Capital Goods) | 7,052,997 | ||||||

| 345,130 | SK Hynix, Inc. (Semiconductors & Semiconductor Equipment)* | 13,457,821 | ||||||

| 3,920 | SK Telecom Co. Ltd. (Telecommunication Services) | 811,656 | ||||||

| 88,764 | Sungwoo Hitech Co. Ltd. (Automobiles & Components) | 1,433,805 | ||||||

|

| |||||||

| 82,635,866 | ||||||||

|

| |||||||

| Taiwan – 13.1% | ||||||||

| 1,231,000 | AcBel Polytech, Inc. (Capital Goods) | 1,617,519 | ||||||

| 3,025,000 | Asia Cement Corp. (Materials) | 3,979,676 | ||||||

| 348,000 | Chicony Electronics Co. Ltd. (Technology Hardware & Equipment) | 906,249 | ||||||

| 1,006,000 | Chin-Poon Industrial Co. Ltd. (Technology Hardware & Equipment) | 1,888,269 | ||||||

| 1,795,000 | Elitegroup Computer Systems Co. Ltd. (Technology Hardware & Equipment) | 1,330,326 | ||||||

| 1,354,000 | Faraday Technology Corp. (Semiconductors & Semiconductor Equipment) | 1,845,614 | ||||||

| 4,420,000 | Fubon Financial Holding Co. Ltd. (Diversified Financials) | 5,720,728 | ||||||

| 636,000 | Gigabyte Technology Co. Ltd. (Technology Hardware & Equipment) | 993,368 | ||||||

| 545,000 | Grape King Bio Ltd. (Household & Personal Products) | 2,443,788 | ||||||

| 156,000 | Holtek Semiconductor, Inc. (Semiconductors & Semiconductor Equipment) | 280,900 | ||||||

| 775,000 | Hon Hai Precision Industry Co. Ltd. (Technology Hardware & Equipment) | 2,225,770 | ||||||

| 729,000 | Huang Hsiang Construction Co. (Real Estate) | 1,109,118 | ||||||

| 1,659,000 | King Yuan Electronics Co. Ltd. (Semiconductors & Semiconductor Equipment) | 1,266,879 | ||||||

| 1,098,000 | Lite-On Technology Corp. (Technology Hardware & Equipment) | 1,679,690 | ||||||

| 80,000 | Merry Electronics Co. Ltd. (Consumer Durables & Apparel) | 434,976 | ||||||

| 552,000 | Nien Hsing Textile Co. Ltd. (Consumer Durables & Apparel) | 544,689 | ||||||

| 170,000 | Radiant Opto-Electronics Corp. (Semiconductors & Semiconductor Equipment) | 685,401 | ||||||

| 356,000 | Simplo Technology Co. Ltd. (Technology Hardware & Equipment) | 1,854,608 | ||||||

|

| |||||||

| Common Stocks – (continued) | ||||||||

| Taiwan – (continued) | ||||||||

| 111,000 | Sirtec International Co. Ltd. (Technology Hardware & Equipment) | $ | 201,940 | |||||

| 1,787,000 | Taiflex Scientific Co. Ltd. (Technology Hardware & Equipment) | 3,473,675 | ||||||

| 4,516,000 | Taiwan Cement Corp. (Materials) | 7,175,645 | ||||||

| 1,314,200 | Taiwan Semiconductor Manufacturing Co. Ltd. ADR (Semiconductors & Semiconductor Equipment) | 26,415,420 | ||||||