UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| Caroline Kraus, Esq. | Copies to: | |

| Goldman, Sachs & Co. | Geoffrey R.T. Kenyon, Esq. | |

| 200 West Street | Dechert LLP | |

| New York, New York 10282 | 100 Oliver Street | |

| 40th Floor | ||

| Boston, MA 02110-2605 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: October 31

Date of reporting period: April 30, 2014

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| The Semi-Annual Report to Stockholders is filed herewith. |

Goldman Sachs Funds

| Semi-Annual Report | April 30, 2014 | |||

Dividend Focus Funds | ||||

Income Builder | ||||

Rising Dividend Growth | ||||

|

Goldman Sachs Dividend Focus Funds

| n | INCOME BUILDER |

| n | RISING DIVIDEND GROWTH |

TABLE OF CONTENTS | ||||

Principal Investment Strategies and Risks | 1 | |||

Investment Process — Income Builder | 3 | |||

Portfolio Management Discussion and Performance Summary — Income Builder | 4 | |||

Portfolio Management Discussion and Performance Summary — Rising Dividend Growth | 14 | |||

Schedules of Investments | 22 | |||

Financial Statements | 34 | |||

Financial Highlights | 38 | |||

Notes to Financial Statements | 42 | |||

Other Information | 60 | |||

| NOT FDIC-INSURED | May Lose Value | No Bank Guarantee | ||

GOLDMAN SACHS DIVIDEND FOCUS FUNDS

Principal Investment Strategies and Risks

This is not a complete list of risks that may affect the Funds. For additional information concerning the risks applicable to the Funds, please see the Funds’ Prospectus.

The Goldman Sachs Income Builder Fund seeks to provide income through investments in fixed income securities (bonds) and high dividend paying equities, preferred equities and other similar securities (stocks), and seeks to provide capital appreciation primarily through equity investments. The Fund’s investments in fixed income securities are subject to the risks associated with debt securities generally, including credit and interest rate risk. High yield, lower rated investments involve greater price volatility and present greater risks, including greater liquidity risk, than higher rated fixed income securities. The Fund’s equity investments will be subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. Derivative instruments may involve a high degree of financial risk. These risks include the risk that a small movement in the price of the underlying security or benchmark may result in a disproportionately large movement, unfavorable or favorable, in the price of the derivative instrument; the risk of default by a counterparty; and liquidity risk. Different investment styles tend to shift in and out of favor, and at times the Fund may underperform other funds that invest in similar asset classes. Investing in REITs involves certain unique risks in addition to those risks associated with investing in the real estate industry in general. REITs whose underlying properties are concentrated in a particular industry or geographic region are also subject to risks affecting such industries and regions. The securities of REITs involve greater risks than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements because of interest rate changes, economic conditions and other factors. Investments in master limited partnerships (“MLPs”) are subject to certain risks, including risks related to limited control and limited rights to vote, potential conflicts of interest, cash flow risks, dilution risks, limited liquidity and risks related to the general partner’s right to force sales at undesirable times or prices.

The Goldman Sachs Rising Dividend Growth Fund invests primarily in equity investments of dividend paying U.S. and foreign companies with market capitalizations of at least $500 million. The equity investments in which the Fund invests may include common and preferred stocks as well as master limited partnerships (“MLPs”) and real estate investment trusts (“REITs”). The Fund’s equity investments are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Different investment styles tend to shift in and out of favor, and the Fund’s emphasis on companies with rising dividend payments could cause the Fund to underperform other funds that invest in similar asset classes but employ different investment styles. Investments in MLPs are subject to certain risks, including risks related to limited control and limited rights to vote, potential conflicts of interest, cash flow risks, dilution risks, limited liquidity and risks related to the general partner’s right to force sales at undesirable times or prices. MLPs are also subject to risks relating to their complex tax structure, including the risk that a distribution received by the Fund from an MLP is treated as a return of capital, which may increase the Fund’s tax liability and require the Fund to restate the character of its distributions and amend shareholder tax reporting previously issued, and the risk that an MLP could lose its tax status as a partnership, resulting in a reduction in the value of the Fund’s investment in the MLP and lower income to the Fund. Many MLPs in which the Fund may invest operate facilities within the energy sector and are also subject to risks affecting the energy sector. The securities of REITs and mid- and small-capitalization companies involve greater risks than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements (in the case of REITs, because of interest rate changes, economic conditions and other factors). REITs whose underlying properties are concentrated in a particular industry or region are also subject to risks affecting such industries and regions. The Fund may also invest in fixed income securities, which are subject to the

1

GOLDMAN SACHS DIVIDEND FOCUS FUNDS

risks associated with debt securities generally, including credit and interest rate risk. Foreign securities and emerging country securities may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic and political developments. The Fund’s investments in other investment companies (including ETFs) subject it to additional expenses. The Fund is “non-diversified” and may invest more of its assets in fewer issuers than “diversified” funds. Accordingly, the Fund may be more susceptible to adverse developments affecting any single issuer held in its portfolio and to greater losses resulting from these developments.

2

GOLDMAN SACHS INCOME BUILDER FUND

What Differentiates Goldman Sachs’ Income Builder Fund Investment Process?

Income Builder Fund is a broadly diversified portfolio that seeks to provide income and capital appreciation.

The Goldman Sachs Income Builder Fund provides exposure to the wealth-building opportunities of stocks and the regular income potential of bonds. The Fund invests in both equity and fixed income securities with a focus on yield enhancing strategies to earn a monthly income stream. The Fund seeks to maintain broad exposure to equities with lower than general equity market volatility.

We believe that similar themes can perform differently across asset classes. The Fund can potentially take advantage of these cross-asset class opportunities as it is a dynamic portfolio that allows the flexibility to allocate across equities and fixed income from a top-down perspective, given our views on macro opportunities and valuations.

In our risk management process, we identify, monitor and measure a fund’s risk profile. We consider the risk relative to the benchmark and the fund’s investment goal to seek income stability and capital growth.

The Fund’s portfolio comprises the ideas of two experienced Goldman Sachs investment groups:

Global Fundamental Equity Group: A group of investment professionals averaging over 17 years of investment experience and with a strong commitment to fundamental research.

Global Fixed Income Group: Broad, deep capabilities across global fixed income markets, with a total return investment philosophy.

3

PORTFOLIO RESULTS

Goldman Sachs Income Builder Fund

Investment Objective

The Goldman Sachs Income Builder Fund seeks to provide income and capital appreciation.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Fundamental Equity Team and the Goldman Sachs Fixed Income Investment Management Team, collectively the Goldman Sachs Income Builder Team (the “Income Builder Team”), discuss the Goldman Sachs Income Builder Fund’s (the “Fund”) performance and positioning for the six-month period ended April 30, 2014 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, B, C, Institutional and IR Shares generated cumulative total returns, without sales charges, of 5.70%, 5.34%, 5.32%, 5.89% and 5.83%, respectively. These returns compare to the 9.61% and 4.54% cumulative total returns of the Russell 1000® Value Index (with dividends reinvested) (the “Russell Index”) and the Bank of America Merrill Lynch BB to B U.S. High Yield Constrained Index (the “BofA Merrill Lynch Index”), respectively, during the same period. |

| Q | What economic and market factors most influenced the equity and fixed income markets as a whole during the Reporting Period? |

| A | When the Reporting Period began and through the end of 2013, the U.S. stock market continued to rally, reaching record highs during December 2013. Contributing to the strong performance of U.S. equities was the December announcement by the U.S. Federal Reserve (the “Fed”) that it would begin tapering its asset purchases in January 2014 — a signal of confidence in the U.S. economy. In the fixed income market, bond yields generally increased on improving economic data and the Fed’s taper announcement. |

| U. S. equities got off to a weak start in early 2014, but subsequently recovered, continuing to post fresh highs into April 2014 despite mixed news about the U.S. labor and housing markets as well as the broader U.S. economy. Many U. S. corporate earnings announcements reflected top-line growth, though overall management guidance for 2014 was less optimistic than consensus. In the fixed income market, bond yields declined overall as U.S. economic data weakened, primarily as a result of inclement winter weather. The Fed continued to reduce its asset purchases and suggested during March 2014 that it might adopt a more hawkish stance. That is, the Fed’s March 2014 policy announcements suggested a rate hike may come sooner than markets anticipated, possibly in mid-2015. At the same time, the Fed dropped the threshold of 6.5% unemployment as a condition for raising short-term interest rates. |

| Q | How did the Fund’s asset allocation affect performance during the Reporting Period? |

| A | As part of its principal investment strategies, the Fund has a baseline allocation of 60% to fixed income securities and 40% to equity securities, though in seeking to meet its investment objective, the Fund has the flexibility to opportunistically tilt the allocation to fixed income and equity securities up to 15% above or below that baseline allocation. The Fund seeks to provide a high and stable income stream with lower volatility than the equity market plus capital appreciation through investing in the highest conviction ideas of the Income Builder Team. Because of these stated goals of the Fund, the Income Builder Team believes the returns of the Russell Index and the BofA Merrill Lynch Index should be considered for reference only. |

At the beginning of the Reporting Period, the Fund was invested approximately 50% in equities and 48% in fixed income, with the balance in cash and cash equivalents. During the Reporting Period, the Fund’s allocation toward equities was trimmed to 47%, and its allocation to fixed income was increased to 52%, as the Income Builder Team sought to balance yield considerations and capital |

4

PORTFOLIO RESULTS

appreciation potential. Overall, this positioning had a positive impact on Fund performance during the Reporting Period. |

| Q | What was the Fund’s 12-month distribution rate during the Reporting Period? |

| A | The Fund seeks to provide investors with attractive and sustainable yield with lower volatility than the equity market by focusing its investments in fixed income securities and high dividend-paying equities, preferred equities and other similar securities (stocks). During the Reporting Period, the Fund’s Class A, B, C, Institutional and IR Shares provided attractive 12-month distribution rates of 3.60%, 2.88%, 2.97%, 3.90% and 3.77%, respectively. As of April 30, 2014, the Fund’s 30-day SEC yields (subsidized) for its Class A, B, C, Institutional and IR Shares were 2.97%, 2.39%, 2.40%, 3.54% and 3.39%, respectively. |

| Q | What key factors had the greatest impact on the performance of the Fund’s equity portfolio during the Reporting Period? |

| A | Relative to the Russell Index, stock selection had the greatest impact on the Fund’s equity portfolio during the Reporting Period. |

| Q | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | During the Reporting Period, the Fund’s positioning in the consumer discretionary, consumer staples and utilities sectors detracted from its performance relative to the Russell Index. The Fund’s positioning in the health care, information technology and financials sectors contributed positively to its relative returns. |

| Q | Which stocks detracted significantly from the Fund’s relative performance during the Reporting Period? |

| A | The largest detractors from the Fund’s relative performance during the Reporting Period were utilities company FirstEnergy; Finnish tire manufacturer Nokian Renkaat Oyj; and fashion retailer L Brands. |

| FirstEnergy, a diversified utilities company primarily engaged in the generation and distribution of electricity in the Midwest and Mid-Atlantic regions of the United States, detracted most from the Fund’s returns during the Reporting Period. In our view, the stock had a strong dividend yield that was fully supported by its regulated power distribution business. However, its shares declined during the Reporting Period, as many investors seemed disappointed by the lack of improvement in competitive power prices. FirstEnergy also cut its quarterly dividend to be more in line with its peers. At the end of the Reporting Period, we believed competitive power prices were showing signs of stabilization. We also considered it positive that transmission capital expenditures could drive growth in FirstEnergy’s rate base through at least 2017. In addition, we believe the company is committed to growing its regulated earnings mix. |

| The Fund’s position in Nokian Renkaat Oyj dampened relative returns during the Reporting Period. Nokian Renkaat Oyj’s stock price declined amid rising concerns surrounding Russia’s involvement in Ukraine. Approximately 35% of the tire manufacturer’s sales and 80% of its production are in Russia. At the end of the Reporting Period, we did not expect the company’s sales to be significantly affected going forward, given that the season for selling winter tires is largely over. In addition, the depreciation of the Russian ruble appeared to be positive for Nokian Renkaat Oyj because it lowers the company’s production costs. |

L Brands, with subsidiaries that include Victoria’s Secret and Bath & Body Works, detracted from the Fund’s relative results during the Reporting Period. The company’s shares moved sharply lower after reporting same-store sales growth that was below consensus expectations in both November and December 2013. Despite such weakness, we were encouraged by the strength of L Brands’ U.S. business, and we believe many of the company’s brands resonate globally, which gives us a positive view of the company’s international business. We also have confidence in management’s disciplined approach towards future expansion. At the end of the Reporting Period, we maintained our positive outlook on the stock, based on our belief that long-term growth may be driven by the company’s continued growth in U.S. square footage, product expansion into natural adjacencies and international expansion. We also anticipate operating margin expansion through supply chain improvements. In our view, the company is also committed to returning excess free cash flow to shareholders through dividends and share repurchases. Indeed, during February 2014, L Brands |

5

PORTFOLIO RESULTS

announced a special dividend of $1.00 and raised its dividend by approximately 13%, sending its stock price sharply higher. |

| At the end of the Reporting Period, the Fund maintained its positions in all three stocks. |

| Q | Which stocks contributed significantly to the Fund’s relative performance during the Reporting Period? |

| A | During the Reporting Period, the Fund benefited most relative to the Russell Index from its positions in commercial mortgage real estate investment trust (REIT) Starwood Property Trust, diversified computer systems company Hewlett-Packard and insurance holding company Direct Line Insurance Group. |

| The Fund’s top contributor during the Reporting Period was Starwood Property Trust. In January 2014, Starwood Property Trust announced the spin-off of Starwood Waypoint Residential Trust (“Starwood Waypoint”), a wholly owned subsidiary that focuses on the single-family rental business. Investors appeared to view the spin-off as positive, and Starwood Property Trust’s stock price appreciated. On the distribution date, each shareholder of record received one Starwood Waypoint common share for every five shares of Starwood Property Trust common stock held on the record date. At the end of the Reporting Period, we continued to have a favorable view of select commercial mortgage REITs because we believe an improving U.S. economy could help demand, while supply remains in check in most areas. In addition, we believe Starwood Property Trust’s assets, which tend to be interest rate-sensitive, differentiate it from many other mortgage REITs and also increase the potential that Starwood Property Trust can benefit in a rising interest rate environment. We also continue to have confidence in management’s ability to source attractive loans. The Fund continued to hold the stock at the end of the Reporting Period. |

| Hewlett-Packard added to relative returns during the Reporting Period. Its stock traded up following the release of its fiscal first quarter 2014 earnings, which included better than expected top- and bottom-line results. In addition, the company provided guidance for its fiscal second quarter that was in line with expectations, while raising the low end of its full year targeted range for its earnings per share. Hewlett-Packard also surprised investors with strong commercial notebook sales and solid results in its enterprise business. In early 2014, reports that Hewlett-Packard was planning to re-nominate its entire board appeared to be viewed positively by the market. We originally purchased the stock at a discount, and at the end of the Reporting Period, its yield was approximately 2%. The Fund maintained a position in the stock at the end of the Reporting Period. |

| The Fund benefited from a position in an American Depositary Receipt (“ADR”) representing Direct Line Insurance Group. (An ADR is a negotiable security that represents securities of a non-U.S. company that trades in the U.S. financial markets.) Direct Line Insurance Group is a U.K.-based holding company that provides general insurance services and operates through five segments, including motor, home, rescue and other personal lines, commercial and international. Its share price traded higher at the end of November 2013 after it completed the sale of Direct Line Life Insurance Company Limited to fellow U.K. insurance company Chesnara. Proceeds of the sale were returned to shareholders in the form of a special dividend. After the sale, we continued to have a positive outlook on the company and its opportunity to improve profit margins. In addition, the ADR held by the Fund has an attractive yield, which we believe the company is capable of supporting in the months ahead. |

| Q | Did the equity portion of the Fund make any significant purchases or sales during the Reporting Period? |

| A | The Fund purchased telecommunication services giant Verizon Communications during the Reporting Period. Verizon Communications and its peers have been negatively impacted by changes in the upgrade policies of North American carriers. The company’s stock also came under pressure as a result of its 2014 free cash flow guidance, which we believe created a buying opportunity. We also believe Verizon Communications has some of the best assets in the telecommunications industry. In our opinion, the company’s top line and earnings per share can grow during the next few years. In addition, at end of the Reporting Period, the stock offered an attractive dividend yield. |

During the Reporting Period, the Fund initiated a position in The Gap, an apparel retail company with more 3,000 store locations. The Gap also has an accelerating e-commerce business, which we consider an important channel for retailers. In our view, The Gap is a high quality business led by a strong management team. We also believe the company’s share price did not fully reflect recent structural improvements wherein square footage was reduced by approximately 30%, putting the retailer in a position to accelerate growth domestically and expand its |

6

PORTFOLIO RESULTS

international presence. Additionally, in our opinion, The Gap stands to benefit from its strong inventory and supply chain management. Furthermore, we think the company could potentially increase shareholder value, as it recently participated in significant share repurchase activity. |

| The Fund exited its position in El Paso Pipeline Partners, LP during the Reporting Period. The master limited partnership (“MLP”) reported lower than expected distribution guidance at the end of 2013, which pushed down its share price. We reallocated the proceeds to MLP names in which we had higher conviction. |

| We eliminated the Fund’s position in MarkWest Energy Partners LP after the MLP reported lower than expected distribution guidance at the beginning of 2014, sending its stock lower. We reallocated the proceeds to MLP names that we viewed more favorably. |

| Q | What changes were made to the Fund’s equity weightings during the Reporting Period? |

| A | During the Reporting Period, we increased the Fund’s overweight relative to the Russell Index in the telecommunication services sector. We shifted the Fund from an underweight position in the financials sector to an overweight position. In addition, during the Reporting Period, we reduced the Fund’s overweighted position in the energy sector, and we increased its underweighted positions in the health care and industrials sectors. Compared to the Russell Index, at the end of the Reporting Period, the Fund was overweight the information technology, consumer discretionary and consumer staples sectors and was underweight the materials and utilities sectors. |

| Q | Which fixed income market sectors significantly affected the Fund’s performance during the Reporting Period? |

| A | Relative to the BofA Merrill Lynch Index, the Fund benefited from its holdings of investment grade corporate bonds and high yield corporate bonds in the commercial services and products industry and in the financial industry. In addition, the Fund’s credit quality positioning among corporate bonds — more specifically, its holdings of CCC-rated and B-rated securities — added to relative returns. |

| The Fund was hurt by its holdings of investment grade corporate bonds and high yield corporate bonds in the non-cellular telecommunications industry. |

| Q | How did the Fund’s duration and yield curve positioning strategies affect performance during the Reporting Period? |

| A | The Fund’s duration and yield curve positioning detracted from its results during the Reporting Period overall. Duration is a measure of the Fund’s sensitivity to changes in interest rates. Throughout the Reporting Period, the Fund held a short duration position relative to the BofA Merrill Lynch Index, which we tactically increased and decreased as we deemed necessary. The Fund was hurt by its short duration bias in January 2014 and April 2014 when U.S. Treasury prices increased. At the end of the Reporting Period, the Fund had a shorter duration bias than it did at the beginning of the Reporting Period because we believe U.S. interest rates should rise in response to the strengthening U.S. economy, a possible increase in inflation and potential changes in Fed monetary policy. |

| Q | What changes were made to the Fund’s fixed income weightings during the Reporting Period? |

| A | During the Reporting Period, we increased the Fund’s exposure to non-U.S. issuers because we see attractive investment opportunities outside of the U.S. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, the Income Builder Team did not use derivatives as part of its active management strategy within the equity portfolio. In the fixed income portfolio, the Fund used U.S. Treasury futures and Eurodollar futures to hedge and manage interest rate exposure and to facilitate specific duration and yield curve strategies. Eurodollar futures are contracts that have underlying assets linked to time deposits denominated in U.S. dollars at banks outside the U.S. The Fund also employed credit default swaps to implement specific credit-related investment strategies. It used forward foreign exchange contracts to hedge currency exposure. |

| Q | What is the Income Builder Team’s tactical view and strategy for the months ahead? |

| A | At the end of the Reporting Period, the Income Builder Team believed U.S. equities have further upside potential as the U.S. economy accelerates, with real earnings growth serving as a fundamental driver of performance. While we acknowledge that headwinds remain, such as geopolitical risks and political gridlock in Washington D.C., we believe |

7

PORTFOLIO RESULTS

there are ample tailwinds for U.S. equities, including the strengthening U.S. housing and employment markets. We believe U.S. corporate fundamentals are strong, evidenced by both healthy balance sheets and earnings resilience, which could provide companies with a number of ways to increase shareholder value. In addition, as the U.S. economy improves, we believe companies may potentially reinvest for future growth by increasing their capital expenditures, research and development, hiring and merger and acquisition activity, instead of keeping excess capital on their balance sheets. |

| Regardless of the direction of the U.S. equities market, our fundamental, bottom-up stock selection continues to drive our process, rather than headlines or sentiment. We maintain high conviction in the companies that we own and believe they have the potential to outperform relative to the broader market, whatever the growth environment. We maintain our disciplined approach, seeking to identify companies with strong or improving balance sheets, which are led by quality management teams. We continue to be focused on stocks trading at what we believe to be discounted valuations. At the end of the Reporting Period, we remained positive on financial companies that are improving returns on capital and those that could be beneficiaries of a rising rate environment. We also have a favorable view of high quality cyclical companies that have distinct growth opportunities and could benefit from a continued U.S. economic recovery. In addition, we remain constructive on the total return opportunity from dividend-paying technology stocks exposed to secular growth trends. We continue to find select non-U.S. common stocks attractive based on particular yield and valuation considerations. |

| Regarding the fixed income market, the Income Builder Team was concerned at the end of the Reporting Period that investors are too complacent about the situation in Ukraine and the potential for increased volatility stemming from geopolitical tensions. |

| Relative to high yield corporate bonds, the rally continued at the end of the Reporting Period, with the asset class benefiting from the strength of the U.S. Treasury market — as evidenced by the strong performance of higher credit quality securities. In addition, high yield corporate bond prices were supported by solid investment inflows. Going forward, continued strength in underlying credit fundamentals is likely, in our view, to help keep default rates near historic lows. At the end of the Reporting Period, we believe that low yields, upwardly trending interest rates and management teams’ increased willingness to engage in shareholder-friendly activities suggest high yield corporate bonds may experience more modest performance during 2014 than in recent time periods. |

| Within corporate credit, we see favorable trends among home builders and building products companies, as rising home prices have allowed for margin improvement and strengthening credit quality. We also continue to believe attractive income opportunities exist within consumer products names and in stable industries, such as cable, wireless and health care. In addition, we remain positive regarding the credit quality of banks given greater regulatory clarity, reasonable capital return programs and a lower probability for credit losses. |

8

FUND BASICS

Income Builder Fund

as of April 30, 2014

| PERFORMANCE REVIEW | ||||||||||||||

| November 1, 2013–April 30, 2014 | Fund Total Return (based on NAV)1 | Russell 1000 Value Index2 | BofA Merrill Lynch BB to B U.S. High Yield Constrained Index3 | |||||||||||

| Class A | 5.70 | % | 9.61 | % | 4.54 | % | ||||||||

| Class B | 5.34 | 9.61 | 4.54 | |||||||||||

| Class C | 5.32 | 9.61 | 4.54 | |||||||||||

| Institutional | 5.89 | 9.61 | 4.54 | |||||||||||

| Class IR | 5.83 | 9.61 | 4.54 | |||||||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 Index companies with lower price-to-book ratios and lower expected growth values. This index is constructed to provide a comprehensive and unbiased barometer for the large-cap value segment. The Index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect value characteristics. |

| 3 | The BofA Merrill Lynch BB to B US High Yield Constrained Index contains all securities in The BofA Merrill Lynch US High Yield Index rated BB1 through B3, based on an average of Moody’s, S&P and Fitch, but caps issuer exposure at 2%. Index constituents are capitalization-weighted, based on their current amount outstanding, provided the total allocation to an individual issuer does not exceed 2%. Issuers that exceed the limit are reduced to 2% and the face value of each of their bonds is adjusted on a pro-rata basis. Similarly, the face values of bonds of all other issuers that fall below the 2% cap are increased on a pro-rata basis. In the event there are fewer than 50 issuers in the Index, each is equally weighted and the face values of their respective bonds are increased or decreased on a pro-rata basis. The Index figures do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

9

FUND BASICS

| PERFORMANCE REVIEW CONTINUED | ||||||||||||||

| November 1, 2013–April 30, 2014 | 12-Month Distribution Rate4 | 30-Day Standardized Subsidized Yield5 | 30-Day Standardized Unsubsidized Yield5 | |||||||||||

| Class A | 3.60 | % | 2.97 | % | 2.76 | % | ||||||||

| Class B | 2.88 | 2.39 | 2.18 | |||||||||||

| Class C | 2.97 | 2.40 | 2.18 | |||||||||||

| Institutional | 3.90 | 3.54 | 3.32 | |||||||||||

| Class IR | 3.77 | 3.39 | 3.17 | |||||||||||

| 4 | The 12 month distribution rate is calculated by taking the sum of all cash distributions over the past 12 months and dividing by the month end NAV in the last month of the period. Distributions may include interest from fixed income, dividends from equities, short term and long term capital gains, return of capital, and special distributions. Return of capital distribution may include a return of some or all of the money that an investor invested in Fund shares. Distributions from securities such as MLPs passing through the fund may also be characterized as return of capital. Special distributions may include any off-cycle distributions that occur outside of regular interest or dividend payment dates, such as when a company opts to pay a special dividend. The amounts and sources of distribution are not provided for tax reporting purposes. The Fund reports the character of distributions for federal income tax purposes each calendar year on Form 1099-DIV. Distributions will fluctuate over time and a large proportion of the distribution may occur at the end of the year in the form of capital gains. Distributions and market value movements affect the NAV of the fund and will also affect this calculation. 12 month distribution rate numbers are based on historical distributions and NAVs and are not predictive of future distributions or yields. 12 month distribution rate is calculated to provide a sense of the total cash flow associated with investment in the Fund, but should not be confused with SEC yield, dividend yield or interest yield. |

| 5 | The method of calculation of the 30-Day Standardized Subsidized Yield is mandated by the Securities and Exchange Commission and is determined by dividing the net investment income per share earned during the last 30 days of the period by the maximum public offering price (“POP”) per share on the last day of the period. This number is then annualized. The 30-Day Standardized Subsidized Yield reflects fee waivers and/or expense reimbursements recorded by the Fund during the period. Without waivers and/or reimbursements, yields would be reduced. This yield does not necessarily reflect income actually earned and distributed by the Fund and, therefore, may not be correlated with the dividends or other distributions paid to shareholders. The 30-Day Standardized Unsubsidized Yield does not adjust for any fee waivers and/or expense reimbursements in effect. If the Fund does not incur any fee waivers and/or expense reimbursements during the period, the 30-Day Standard Subsidized Yield and 30-Day Standardized Unsubsidized Yield will be identical. |

10

FUND BASICS

| STANDARDIZED TOTAL RETURNS6 | ||||||||||||||||

| For the period ended 3/31/14 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||||

| Class A | 5.67 | % | 14.95% | 6.23% | 7.10 | % | 10/12/94 | |||||||||

| Class B | 5.73 | 15.13 | N/A | 6.10 | 5/1/96 | |||||||||||

| Class C | 9.89 | 15.38 | 6.04 | 4.35 | 8/15/97 | |||||||||||

| Institutional | 12.25 | 16.74 | 7.36 | 5.61 | 8/15/97 | |||||||||||

| Class IR | 12.02 | N/A | N/A | 13.70 | 8/31/10 | |||||||||||

| 6 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares, the assumed contingent deferred sales charge for Class B Shares (5% maximum declining to 0% after six years) and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Class B Shares convert to Class A Shares on or about the fifteenth day of the last month of the calendar quarter that is eight years after purchase. Returns for Class B Shares for the period after conversion reflect the performance of Class A Shares. Because Institutional and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. The Fund’s Class B Shares are no longer available for purchase by new or existing shareholders (although current Class B shareholders may continue to reinvest income and capital gains distributions into Class B Shares, and Class B shareholders may continue to exchange their shares for Class B Shares of certain other Goldman Sachs Funds). |

The returns set forth in the table above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| EXPENSE RATIOS7 | ||||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 0.95 | % | 1.27 | % | ||||||

| Class B | 1.70 | 2.03 | ||||||||

| Class C | 1.70 | 2.02 | ||||||||

| Institutional | 0.55 | 0.86 | ||||||||

| Class IR | 0.70 | 1.01 | ||||||||

| 7 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

11

FUND BASICS

| TOP TEN EQUITY HOLDINGS AS OF 4/30/148 | ||||||||

| Holding | % of Net Assets | Line of Business | ||||||

| General Electric Co. | 2.3 | % | Industrial Conglomerates | |||||

| JPMorgan Chase & Co. | 1.2 | Commercial Banks | ||||||

| Capital One Financial Corp. | 1.1 | Consumer Finance | ||||||

| Merck & Co., Inc. | 1.1 | Pharmaceuticals | ||||||

| Pfizer, Inc. | 1.1 | Pharmaceuticals | ||||||

| FirstEnergy Corp. | 1.0 | Electric Utilities | ||||||

| Ares Capital Corp. | 1.0 | Capital Markets | ||||||

| Total SA ADR | 0.9 | Oil, Gas & Consumable Fuels | ||||||

| Starwood Property Trust, Inc. | 0.9 | Real Estate Investment Trusts | ||||||

| Microsoft Corp. | 0.9 | Software | ||||||

| 8 | The top 10 holdings may not be representative of the Fund’s future investments. |

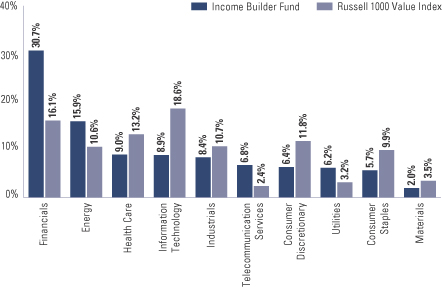

| FUND’S EQUITY SECTOR ALLOCATIONS VS. BENCHMARK9 |

| As of April 30, 2014 |

| 9 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of the total value of the Fund’s equity investments. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

12

FUND BASICS

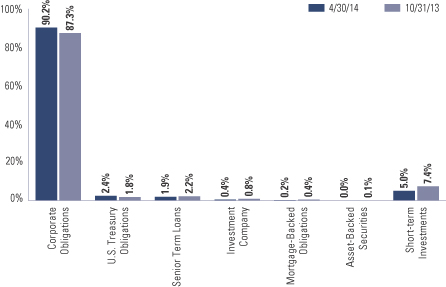

| FUND’S FIXED INCOME FUND COMPOSITION10 |

| As of April 30, 2014 |

| 10 | The percentage shown for each investment category reflects the value of investments in that category as a percentage of the Fund’s fixed income investments. Short-term investments represent repurchase agreements. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

13

PORTFOLIO RESULTS

Goldman Sachs Rising Dividend Growth Fund

Investment Objective

The Fund seeks long-term growth of capital and current income.

Portfolio Management Discussion and Analysis

Below, the Dividend Assets Capital portfolio management team, the Fund’s sub-adviser, discusses the Goldman Sachs Rising Dividend Growth Fund’s (the “Fund”) performance and positioning for the six-month period ended April 30, 2014 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, C, Institutional, IR and R Shares generated cumulative total returns, without sales charges, of 7.33%, 6.89%, 7.55%, 7.42% and 7.17%, respectively. These returns compare to the 8.36% cumulative total return of the Fund’s benchmark, the Standard & Poor’s® 500 Index (with dividends reinvested) (the “S&P 500 Index”), during the same time period. |

| Q | What economic and market factors most influenced the equity markets as a whole during the Reporting Period? |

| A | The performance of the U.S. equity markets during the Reporting Period was a tale of two markets. During the first two months of the Reporting Period, the S&P 500 Index was up 4.42%. During the last four months of the Reporting Period, the S&P 500 Index was up just 2.56%. |

| In our view, there was no single event that caused the slowdown in the last four months of the Reporting Period, but the list of concerns that were evident in late 2013, largely ignored for the year as a whole, became more pronounced in 2014. Further, with the S&P 500 Index up so strongly in calendar year 2013, some investors may have simply been taking some gains in the early months of 2014. |

| Clearly, one factor impacting the U.S. equity markets was a long list of geopolitical issues that paraded across the world stage during the Reporting Period, including political hotspots such as Russia, Ukraine and elsewhere, as heightened tensions and worries around potential sanctions imposed and/or possible military actions taken by the West weighed on investor sentiment. |

| Economic growth around the world remained subpar. The U.S., for example, produced Gross Domestic Product (“GDP”) for the first quarter of 2014 of only 0.1%, according to the “advance” estimate released by the Bureau of Economic Analysis (“advance estimate”). The harsh winter weather has been blamed for much of the poor result. It is possible, we believe, that monthly data received late in the first calendar quarter and not available for the advance estimate may cause the next estimate for U.S. GDP to be revised up. That said, early in the first calendar quarter, a number of data reports were erratic, probably affected by the harsh weather. For example, various measures of housing activity showed signs of weakening. However, as the weather turned more spring-like, employment numbers indicated strength, as evidenced by April 2014’s 288,000 addition to non-farm payrolls. Also, motor vehicle sales for April 2014 were 16.0 million on a seasonally adjusted annual rate for the second month in a row. |

The role of the Federal Reserve (the “Fed”) in the economy continued to be accommodative during the Reporting Period. |

14

PORTFOLIO RESULTS

The transition from the Bernanke-led Fed to new chair Janet Yellen was accomplished without upsetting either the fixed income or the equity markets. The tapering of purchases of mortgage-backed securities and long-term U.S. Treasuries, which began in January 2014 and continued each month of 2014 to date, also took place without major upset of either asset class market. The Fed continued to work on its twin objectives of lower unemployment and somewhat higher inflation. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | The Fund generated solid absolute gains but underperformed the S&P 500 Index. The detracting impact of having an average 3.9% position in cash during a Reporting Period when the S&P 500 Index rose more than offset the positive contribution made by effective equity positioning overall and by its positioning in the energy sector in particular, the majority of which was achieved via energy-related Master Limited Partnerships (“MLPs”). |

| Q | Which equity market sectors most significantly affected Fund performance? |

| A | As indicated earlier, cash was a significant negative affecting Fund performance during the Reporting Period. Of the sectors within the S&P 500 Index, the largest detractors were materials, financials and information technology, in each case due primarily to stock selection. Having an underweighted allocation to information technology, which outpaced the S&P 500 Index during the Reporting Period, also hurt. It is worth noting that in financials, strong returns in the S&P 500 Index were mostly due to banks and real estate companies, which typically do not have 10-year consecutive dividend growth rates at averages of 10% per year. The Fund’s strategy of only buying the stocks of companies where the dividend has increased every year for at least ten years at an average rate of approximately 10% per year1 thus limited the Fund’s selections within the financials sector. Similarly, in information technology, strong performance in the S&P 500 Index was mostly driven by no-yield/high growth names in which the Fund can not participate. |

| Partially offsetting these detractors were the positive contributions made by positioning in the energy, health care and telecommunication services sectors. In energy, effective stock selection along with an overweighted allocation to the strongly performing sector contributed positively to Fund results. The Fund’s energy sector holdings were primarily comprised of MLPs, which are not components of the S&P 500 Index but which, as measured by the Alerian MLP Index, outperformed the S&P 500 Index during the Reporting Period. We placed a focus on U.S.-concentrated energy midstream companies based on our view they would perform well as demand for energy increases. (The midstream component of the energy industry is usually defined as those companies providing products or services that help link the supply side, i.e. energy producers, and the demand side, i.e. energy end-users, for any type of energy commodity. Such midstream business can include, but are not limited to, those that process, store, market and transport various energy commodities.) Indeed, North America experienced extreme winter weather from December 2013 through April 2014 that boosted demand for energy as did geopolitical tension between Ukraine and Russia and unrest in the Middle East. During the Reporting Period, West Texas Intermediate (“WTI”) crude oil prices rose 5.42% to end April 2014 at $99.74. Brent crude oil prices rose 2.04% during the same timeframe to end the Reporting Period at $108.07 per barrel, and Henry Hub natural gas prices soared 37.06% during the same timeframe to end the Reporting Period at $4.82 per million British thermal units (“BTUs”). (Henry Hub is a natural gas pipeline located in Erath, Louisiana that serves as the official delivery location for futures contracts on the New York Mercantile Exchange (“NYMEX”). The Henry Hub is owned by Sabine Pipe Line LLC and has access to many of the major gas markets in the United States. As of June 2007, the hub connects to four intrastate and nine interstate pipelines, including the Transcontinental, Acadian and Sabine pipeline. The settlement prices at the Henry Hub are used as benchmarks for the entire North American natural gas market.) |

| In health care, effective stock selection more than offset the detracting impact of the Fund’s underweight position in the strongly performing sector. The health care sector’s performance was mostly driven by improved revenue growth in the large pharmaceutical industry. The Fund had no exposure to the telecommunication services sector, and the sector significantly underperformed the S&P 500 Index during the Reporting Period. As the 10-year U.S. Treasury yield moved higher and the Fed continued tapering its monthly asset purchase program, investors appeared willing to take more risks and exited the traditionally defensive telecommunication services sector. |

| 1 | Dividends are not guaranteed and a company’s future ability to pay dividends may be limited. |

15

PORTFOLIO RESULTS

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | Detracting most from the Fund’s results relative to its benchmark index were positions in natural gas processor Markwest Energy Partners LP, natural gas transportation and terminaling facilities operator El Paso Pipeline Partners LP and industry supply distributor WW Grainger. |

| Markwest Energy Partners LP reaffirmed its 2014 guidance on distributable cash flow and increased its fee-based revenue expectation, but its unit price moved lower due to concern about its operational constraints and soft Southwest results. |

| Despite lower year over year maintenance expenditures, El Paso Pipeline Partners LP’s coverage ratio dropped during the Reporting Period. (Coverage ratio is a measure of a company’s ability to meet its financial obligations. In broad terms, the higher the coverage ratio, the better the ability of the enterprise to fulfill its obligations to its lenders.) Its near-term headwinds are related to adverse settlements and a lack of immediate organic growth projects. Further, after growing its distributions at an average annual rate of 16% over the past five years, its new distribution growth rate is projected to be only about 5% in 2014. Also, rate cases at a couple of its subsidiaries caused downward pressure on its stock price. We sold the Fund’s position in El Paso Pipeline Partners LP in mid-December 2013. |

| The harsh winter in North America impacted WW Grainger’s monthly sales particularly hard, as weather-related disruptions resulted in facility closures. Nearly 90% of the company’s sales are generated in the U.S. and Canada. Despite these difficulties, WW Grainger continued to realize price benefits and continued to execute product line expansion, further mature its e-commerce and improve customer experience. As of the end of 2013, WW Grainger had increased its dividends for 42 consecutive years and was among an elite 3% of S&P 500 Index companies that have increased its dividend each year for more than four decades. |

| Q | What were some of the Fund’s best-performing individual stocks? |

| A | The top contributors to the Fund’s relative performance during the Reporting Period were pharmaceuticals company Novo Nordisk and midstream natural gas companies EQT Midstream Partners LP and Energy Transfer Equity LP. |

| Novo Nordisk remained committed to returning excess cash to shareholders through dividend increases and share buybacks despite the Food and Drug Administration’s (“FDA”) rejection of the company’s new insulin drug Tresiba and its demand for more study on heart risk of the product. Novo Nordisk is the world leader in diabetes care, holding a global value market share of approximately 27% and also has one of the highest gross margins among its European Union large pharmaceuticals peers. Novo Nordisk announced it expected to have interim data on the cardiovascular outcomes trial for Tresiba in mid-2015, one year earlier than previously expected. At the end of 2013, Novo Nordisk split its stock five for one and gave shareholders a 25% dividend increase. At the beginning of 2014, the company announced it would reduce its share count by 3.6% through a share repurchase program. |

| EQT Midstream Partners LP performed well during the Reporting Period. The MLP has no debt on its balance sheet, and 80% of its revenue was being generated by fee-based long-term contracts. Its unit price strength continued, as the MLP generated 22% 3-year adjusted earnings before interest, taxes, depreciation and amortization (“EBITDA”) growth and guided 29% distribution growth for 2014 over 2013 and 22% distribution growth for 2015 over 2014 (not assuming any additional acquisitions). |

| Shares of Energy Transfer Equity LP rose during the Reporting Period on strong unit price appreciation, as the MLP announced its sixth consecutive quarterly cash distribution increase. |

| Q | How did the Fund use derivatives during the Reporting Period? |

| A | The Fund did not use derivatives during the Reporting Period. |

| Q | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | We initiated a Fund position in luxury jewelry store operator Tiffany & Co. during the Reporting Period. Our bullish view of high-end consumers’ spending power led us to search for names with strong brand recognition and the potential to participate in the global growth of the high-end jewelry market. In our view, Tiffany & Co. fit what we were looking for. As the costs of precious diamonds and metals appear to be retreating from their highs, we anticipate multi-year margin expansion for Tiffany & Co. The company has strong brand pricing power in a fragmented jewelry and specialty market, and despite a tough selling environment in recent |

16

PORTFOLIO RESULTS

years, it has seen a rebound with steady sales increases. We believe Tiffany & Co.’s focus on organic geographic expansion in low penetration markets, such as greater China, along with much anticipated new jewelry designs being rolled out in 2014, create an opportunity for an attractive long-term earnings per share growth rate. |

| We established a Fund position in aerospace and defense parts provider United Technologies. Based on our expectations for continued North American economic recovery, flat to moderate economic growth in the European Union and steady economic growth in China, we are positive in our view for cyclical industries. In turn, we see the potential for United Technologies to move to a premium valuation compared to the market and its peer group. We believe the fiscal year 2014 outlook for United Technologies’ risk profile seems substantially reduced by a well-positioned pension status, strong order momentum across its business segments and better than expected synergies from its Goodrich and IAE acquisitions. In our view, United Technologies’ strong balance sheet, positive cash flow and conversion rate allow the company to not only focus on research and development but also on shareholder returns through dividends, buybacks and debt reduction. |

| We initiated a Fund position in NGL Energy Partners LP in search of higher distribution growth midstream MLPs. NGL Energy Partners LP is a diversified midstream growth MLP offering stable cash flow, an attractive yield and potential to grow its distribution, in our view. Since its initial public offering in May 2011, the MLP has acquired and integrated 26 companies totaling $2.9 billion, while at the same time increasing its distribution every quarter at a compound annual growth rate of 21%. We believe NGL Energy Partners LP offers favorable growth potential in the water treatment, crude oil, propane and natural gas liquids businesses with strong geographic diversification, including coast-to-coast rail, terminal and retail operations. |

| In addition to those sales already mentioned, we sold the Fund’s position in mining industry safety products manufacturer MSA Safety during the Reporting Period. Having invested in MSA Safety since February 2011, we believe our investment thesis played out as expected. Its stock appreciated at an annual rate of more than 18%. MSA Safety was one of the few mid-capitalization stocks among our holdings with significant liquidity constraints, and our decision to exit the position was primarily based on what we considered to be increasing liquidity risks outweighing further appreciation potential. |

| We sold the Fund’s position in medical equipment manufacturer Danaher, taking profits. In our view, Danaher offers a less cyclical profile compared to its industrial peer group, primarily due to its diversified products offering. As Danaher failed to meet the qualifications of our investment criteria by failing to increase its quarterly dividend in December 2013, we exited the position. |

| Q | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | The most significant change we made during the Reporting Period was increasing the Fund’s allocation relative to the S&P 500 Index in the consumer discretionary sector. |

| Q | How was the Fund positioned relative to its benchmark index at the end of the Reporting Period? |

| A | At the end of April 2014, the Fund had overweighted positions relative to the S&P 500 Index in energy (mostly MLPs), materials, consumer discretionary, consumer staples and industrials. On the same date, the Fund had underweighted positions compared to the S&P 500 Index in health care and financials. The Fund had no exposure to the utilities and telecommunication services sectors at the end of the Reporting Period. |

| Q | What is the Fund’s tactical view and strategy for the months ahead? |

| A | At the end of the Reporting Period, we believed continued economic recovery was the theme for 2014, despite a weak first quarter U.S. GDP, based on positive economic data releases that supported a view of pent-up demand following disruption from a particularly harsh winter. Indeed, at the end of the Reporting Period, economists still projected 2.7% GDP growth for the U.S. in 2014 compared to 1.9% GDP growth in 2013; European GDP growth of 1.1% in 2014 compared to two consecutive years of contraction; and world GDP growth of 2.79% in 2014 compared to 2.06% in 2013. Should the global economy gradually improve, we believe such growth will likely be countered by low but gradually rising interest rates, which could lead to positive but volatile equity market returns. Given our view, we believe dividend growth stocks supported by strong balance sheets and growing businesses should perform well going forward. We particularly believe economic upside may come from improvement in disposable income, recovery of housing values, improvement in commercial construction, strength in industrial and manufacturing activities and an ongoing U.S. energy renaissance. In turn, we favored dividend growth stocks in the consumer discretionary, materials and industrials sectors at the end of the Reporting Period. |

17

PORTFOLIO RESULTS

| Similarly, we are constructive in our view for higher distribution growth energy MLPs that have reduced commodity exposure and strong drop down potential from their sponsor. (Drop down refers to the act of a parent company selling MLP-qualified assets to the associated MLP with favorable terms. Once an MLP is spun off from its integrated parent company, additional assets may be placed into the MLP to increase the capital base. Other drop downs may occur when the General Partner acquires another company with certain assets more suitable for the MLP than its own balance sheet.) Our emphasis is on those MLPs with attractive fee based revenue, long-term contracts and adequate access to capital markets. At the end of the Reporting Period, we preferred crude oil, refined products and natural gas liquid logistics MLPs. We also preferred gathering and processing MLPs focused on higher economic return basins, such as the liquid-rich Eagle Ford and Bakken basins, the Niobara-Wattenberg field and the Marcellus shale. |

| Factors that might impact our strategy include any sudden deterioration of the economy, or any sudden hike in interest rates due to high inflation, either of which could reverse secular bull market sentiment and result in a multi-year correction. Geopolitical risk or a negative regulatory environment could impact the supply/demand balance in the energy sector, thus resulting in price pressures on commodities, including oil and gas. |

| As always, we continue to monitor domestic and global economies, geopolitical factors, interest rates and equity market fundamentals as we actively manage the Fund, with a focus on income through quality in an effort to offer investors the potential for rising income and competitive total returns with lower volatility. |

18

FUND BASICS

Rising Dividend Growth Fund

as of April 30, 2014

| PERFORMANCE REVIEW | ||||||||||

| November 1, 2013–April 30, 2014 | Fund Total Return (based on NAV)1 | S&P 500 Index2 | ||||||||

| Class A | 7.33 | % | 8.36 | % | ||||||

| Class C | 6.89 | 8.36 | ||||||||

| Institutional | 7.55 | 8.36 | ||||||||

| Class IR | 7.42 | 8.36 | ||||||||

| Class R | 7.17 | 8.36 | ||||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance reflects the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The S&P 500 Index is the Standard & Poor’s 500 Composite Index of 500 stocks, an unmanaged index of common stock prices. The Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index. |

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||

| For the period ended 3/31/14 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||||

| Class A | 12.52 | % | 17.61% | 8.13% | 8.26 | % | 3/23/04 | |||||||||

| Class C | 17.20 | 18.35 | N/A | 8.61 | 4/14/05 | |||||||||||

| Institutional | 19.54 | 19.47 | N/A | 8.81 | 3/21/07 | |||||||||||

| Class IR | 19.32 | N/A | N/A | 15.64 | 2/27/12 | |||||||||||

| Class R | 18.79 | N/A | N/A | 15.09 | 2/27/12 | |||||||||||

| 3 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. Effective February 27, 2012, the Rising Dividend Growth Fund, a series of Dividend Growth Trust (the “Predecessor Fund”), was reorganized into the Fund. As accounting successor to the Predecessor Fund, the Fund has assumed the Predecessor Fund’s historical performance. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Prior to February 27, 2012 (the effective date of the reorganization of the Predecessor Fund into the Fund), the maximum initial sales charge applicable to sales of Class A Shares of the Predecessor Fund was 5.75%, which is not reflected in the average annual total return figures shown. Because Institutional, Class IR and Class R Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

19

FUND BASICS

| EXPENSE RATIOS4 | ||||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.18 | % | 1.21 | % | ||||||

| Class C | 1.93 | 1.96 | ||||||||

| Institutional | 0.78 | 0.81 | ||||||||

| Class IR | 0.93 | 0.96 | ||||||||

| Class R | 1.42 | 1.45 | ||||||||

| 4 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| TOP TEN HOLDINGS AS OF 4/30/145 | ||||||||

| Holding | % of Net Assets | Line of Business | ||||||

| VF Corp. | 3.1 | % | Textiles, Apparel & Luxury Goods | |||||

| EOG Resources, Inc. | 2.9 | Oil, Gas & Consumable Fuels | ||||||

| Roche Holding AG ADR | 2.9 | Pharmaceuticals | ||||||

| Perrigo Co. PLC | 2.9 | Pharmaceuticals | ||||||

| The Sherwin-Williams Co. | 2.8 | Chemicals | ||||||

| Cardinal Health, Inc. | 2.6 | Health Care Providers & Services | ||||||

| Roper Industries, Inc. | 2.6 | Industrial Conglomerates | ||||||

| PepsiCo., Inc. | 2.6 | Beverages | ||||||

| Monsanto Co. | 2.5 | Chemicals | ||||||

| Polaris Industries, Inc. | 2.5 | Leisure Equipment & Products | ||||||

| 5 | The top 10 holdings may not be representative of the Fund’s future investments. |

20

FUND BASICS

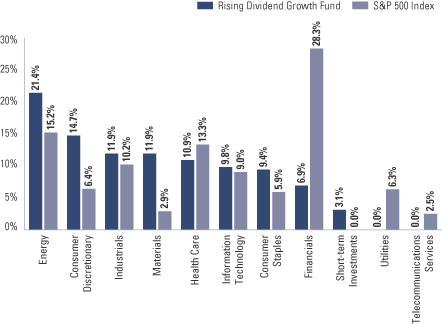

| FUND VS. BENCHMARK SECTOR ALLOCATION6 |

| As of April 30, 2014 |

| 6 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of the total value of the Fund’s equity investments. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

21

GOLDMAN SACHS INCOME BUILDER FUND

Schedule of Investments

April 30, 2014 (Unaudited)

| Shares | Description | Value | ||||||

| Common Stocks – 45.4% | ||||||||

| Aerospace & Defense – 0.6% | ||||||||

| 62,284 | The Boeing Co. | $ | 8,035,882 | |||||

|

| |||||||

| Auto Components – 0.5% | ||||||||

| 363,161 | Nokian Renkaat OYJ ADR | 7,219,641 | ||||||

|

| |||||||

| Automobiles – 0.4% | ||||||||

| 145,772 | Bayerische Motoren Werke AG ADR | 6,083,066 | ||||||

|

| |||||||

| Beverages – 0.7% | ||||||||

| 38,486 | Anheuser-Busch InBev NV ADR | 4,072,588 | ||||||

| 61,392 | PepsiCo, Inc. | 5,272,959 | ||||||

|

| |||||||

| 9,345,547 | ||||||||

|

| |||||||

| Capital Markets – 2.1% | ||||||||

| 353,150 | AllianceBernstein Holding LP | 8,980,605 | ||||||

| 66,111 | Ameriprise Financial, Inc. | 7,379,971 | ||||||

| 790,744 | Ares Capital Corp. | 13,577,074 | ||||||

|

| |||||||

| 29,937,650 | ||||||||

|

| |||||||

| Chemicals – 0.4% | ||||||||

| 4,045 | Ashland, Inc. | 390,747 | ||||||

| 81,924 | Celanese Corp. Series A | 5,032,591 | ||||||

|

| |||||||

| 5,423,338 | ||||||||

|

| |||||||

| Commercial Banks – 2.8% | ||||||||

| 240,974 | Australia & New Zealand Banking Group Ltd. ADR | 7,730,446 | ||||||

| 170,204 | HSBC Holdings PLC ADR | 8,734,869 | ||||||

| 312,013 | JPMorgan Chase & Co. | 17,466,488 | ||||||

| 43,057 | M&T Bank Corp. | 5,253,385 | ||||||

|

| |||||||

| 39,185,188 | ||||||||

|

| |||||||

| Commercial Services & Supplies – 0.6% | ||||||||

| 202,519 | Waste Management, Inc. | 9,001,970 | ||||||

|

| |||||||

| Communications Equipment – 1.5% | ||||||||

| 372,091 | Cisco Systems, Inc. | 8,599,023 | ||||||

| 82,676 | QUALCOMM, Inc. | 6,507,428 | ||||||

| 470,207 | Telefonaktiebolaget LM Ericsson ADR | 5,637,782 | ||||||

|

| |||||||

| 20,744,233 | ||||||||

|

| |||||||

| Computers & Peripherals – 1.5% | ||||||||

| 11,085 | Apple, Inc. | 6,541,148 | ||||||

| 220,448 | EMC Corp. | 5,687,558 | ||||||

| 266,881 | Hewlett-Packard Co. | 8,823,086 | ||||||

|

| |||||||

| 21,051,792 | ||||||||

|

| |||||||

| Consumer Finance – 1.6% | ||||||||

| 162,442 | Capital One Financial Corp. | 12,004,464 | ||||||

| 404,066 | SLM Corp. | 10,404,699 | ||||||

|

| |||||||

| 22,409,163 | ||||||||

|

| |||||||

| Containers & Packaging – 0.6% | ||||||||

| 123,590 | Packaging Corp. of America | 8,234,802 | ||||||

|

| |||||||

| Common Stocks – (continued) | ||||||||

| Diversified Telecommunication Services – 2.0% | ||||||||

| 291,108 | AT&T, Inc. | $ | 10,392,555 | |||||

| 333,097 | Telefonica SA ADR | 5,579,375 | ||||||

| 256,012 | Verizon Communications, Inc. | 11,963,441 | ||||||

|

| |||||||

| 27,935,371 | ||||||||

|

| |||||||

| Electric Utilities – 2.0% | ||||||||

| 115,811 | Edison International | 6,550,270 | ||||||

| 418,723 | FirstEnergy Corp. | 14,131,901 | ||||||

| 81,151 | NextEra Energy, Inc. | 8,102,928 | ||||||

|

| |||||||

| 28,785,099 | ||||||||

|

| |||||||

| Energy Equipment & Services – 0.4% | ||||||||

| 180,448 | Seadrill Partners LLC | 5,606,519 | ||||||

|

| |||||||

| Food & Staples Retailing – 0.4% | ||||||||

| 73,264 | Wal-Mart Stores, Inc. | 5,839,873 | ||||||

|

| |||||||

| Food Products – 0.7% | ||||||||

| 308,030 | ConAgra Foods, Inc. | 9,397,995 | ||||||

|

| |||||||

| Health Care Providers & Services – 0.5% | ||||||||

| 113,540 | Cardinal Health, Inc. | 7,892,165 | ||||||

|

| |||||||

| Hotels, Restaurants & Leisure – 0.3% | ||||||||

| 63,302 | Starwood Hotels & Resorts Worldwide, Inc. | 4,852,098 | ||||||

|

| |||||||

| Household Products – 0.7% | ||||||||

| 114,185 | The Procter & Gamble Co. | 9,425,972 | ||||||

|

| |||||||

| Industrial Conglomerates – 2.3% | ||||||||

| 1,204,649 | General Electric Co. | 32,393,012 | ||||||

|

| |||||||

| Insurance – 3.5% | ||||||||

| 167,948 | Arthur J. Gallagher & Co. | 7,561,019 | ||||||

| 462,696 | Direct Line Insurance Group PLC ADR | 7,958,371 | ||||||

| 37,489 | Everest Re Group Ltd. | 5,924,387 | ||||||

| 156,387 | MetLife, Inc. | 8,186,859 | ||||||

| 102,440 | Prudential Financial, Inc. | 8,264,859 | ||||||

| 198,725 | Validus Holdings Ltd. | 7,366,736 | ||||||

| 145,939 | Zurich Insurance Group AG ADR | 4,197,206 | ||||||

|

| |||||||

| 49,459,437 | ||||||||

|

| |||||||

| Machinery – 0.6% | ||||||||

| 85,051 | Caterpillar, Inc. | 8,964,375 | ||||||

|

| |||||||

| Media – 0.5% | ||||||||

| 82,583 | Viacom, Inc. Class B | 7,017,903 | ||||||

|

| |||||||

| Multi-Utilities – 0.4% | ||||||||

| 130,557 | PG&E Corp. | 5,950,788 | ||||||

|

| |||||||

| Oil, Gas & Consumable Fuels – 7.4% | ||||||||

| 109,038 | BP PLC ADR | 5,519,504 | ||||||

| 130,170 | Chesapeake Energy Corp. | 3,742,387 | ||||||

| 152,736 | DCP Midstream Partners LP | 8,171,376 | ||||||

| 135,975 | Devon Energy Corp. | 9,518,250 | ||||||

| 171,074 | Energy Transfer Partners LP | 9,441,574 | ||||||

|

| |||||||

| 22 | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS INCOME BUILDER FUND

| Shares | Description | Value | ||||||

| Common Stocks – (continued) | ||||||||

| Oil, Gas & Consumable Fuels – (continued) | ||||||||

| 80,572 | Enterprise Products Partners LP | $ | 5,892,230 | |||||

| 55,112 | Exxon Mobil Corp. | 5,644,020 | ||||||

| 175,022 | NGL Energy Partners LP | 6,768,101 | ||||||

| 72,891 | ONEOK Partners LP | 4,154,058 | ||||||

| 113,759 | Plains All American Pipeline LP | 6,347,752 | ||||||

| 225,025 | Regency Energy Partners LP | 6,129,681 | ||||||

| 37,641 | Rose Rock Midstream LP | 1,569,630 | ||||||

| 90,334 | Spectra Energy Partners LP | 4,918,686 | ||||||

| 141,689 | Targa Resources Partners LP | 8,389,406 | ||||||

| 39,242 | TC Pipelines LP | 2,081,396 | ||||||

| 67,143 | Teekay LNG Partners LP | 2,874,392 | ||||||

| 183,985 | Total SA ADR | 13,107,091 | ||||||

|

| |||||||

| 104,269,534 | ||||||||

|

| |||||||

| Pharmaceuticals – 3.9% | ||||||||

| 178,504 | Eli Lilly & Co. | 10,549,587 | ||||||

| 272,606 | Merck & Co., Inc. | 15,963,807 | ||||||

| 80,583 | Novartis AG ADR | 7,005,886 | ||||||

| 475,261 | Pfizer, Inc. | 14,866,164 | ||||||

| 117,026 | Sanofi ADR | 6,295,999 | ||||||

|

| |||||||

| 54,681,443 | ||||||||

|

| |||||||

| Real Estate Investment Trusts – 2.3% | ||||||||

| 48,282 | AvalonBay Communities, Inc. | 6,592,907 | ||||||

| 11,135 | Simon Property Group, Inc. | 1,928,582 | ||||||

| 510,974 | Starwood Property Trust, Inc. | 12,288,925 | ||||||

| 1,108,038 | Two Harbors Investment Corp. | 11,501,434 | ||||||

|

| |||||||

| 32,311,848 | ||||||||

|

| |||||||

| Semiconductors & Semiconductor Equipment – 0.2% | ||||||||

| 72,149 | Altera Corp. | 2,346,285 | ||||||

|

| |||||||

| Software – 1.2% | ||||||||

| 301,168 | Microsoft Corp. | 12,167,187 | ||||||

| 135,830 | Oracle Corp. | 5,552,731 | ||||||

|

| |||||||

| 17,719,918 | ||||||||

|

| |||||||

| Specialty Retail – 1.3% | ||||||||

| 174,323 | L Brands, Inc. | 9,448,307 | ||||||

| 245,428 | The Gap, Inc. | 9,645,320 | ||||||

|

| |||||||

| 19,093,627 | ||||||||

|

| |||||||

| Thrifts & Mortgage Finance – 0.5% | ||||||||

| 501,910 | New York Community Bancorp, Inc. | 7,734,433 | ||||||

|

| |||||||

| Tobacco – 0.4% | ||||||||

| 133,778 | Altria Group, Inc. | 5,365,836 | ||||||

|

| |||||||

| Wireless Telecommunication Services – 0.6% | ||||||||

| 232,571 | Vodafone Group PLC ADR | 8,828,395 | ||||||

|

| |||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $596,880,771) | $ | 642,544,198 | ||||||

|

| |||||||

| Preferred Stocks – 3.5% | ||||||||

| Consumer Finance – 0.4% | ||||||||

Capital One Financial Corp. |

| |||||||

| 175,000 | 6.000 | % | $ | 4,168,500 | ||||

CoBank ACB(a)(b) |

| |||||||

| 10,000 | 6.250 | 1,022,188 | ||||||

|

| |||||||

| 5,190,688 | ||||||||

| ||||||||

| Diversified Telecommunication Services – 0.7% | ||||||||

Intelsat SA |

| |||||||

| 57,200 | 5.750 | 2,934,246 | ||||||

Verizon Communications, Inc. |

| |||||||

| 299,250 | 5.900 | 7,493,440 | ||||||