EX-99.(17)(c)

Goldman Sachs Funds

| Annual Report | October 31, 2014 | |||

Fundamental International Equity Funds | ||||

Focused International Equity* | ||||

International Small Cap | ||||

Strategic International Equity | ||||

*Effective at the close of business on February 28, 2014, the Goldman Sachs Concentrated International Equity Fund was renamed to the Goldman Sachs Focused International Equity Fund.

Goldman Sachs Fundamental International Equity Funds

| n | FOCUSED INTERNATIONAL EQUITY |

| n | INTERNATIONAL SMALL CAP |

| n | STRATEGIC INTERNATIONAL EQUITY |

TABLE OF CONTENTS | ||||

| 3 | ||||

| 4 | ||||

| 5 | ||||

| 7 | ||||

| 28 | ||||

| 36 | ||||

| 40 | ||||

| 46 | ||||

| 60 | ||||

| 61 | ||||

| NOT FDIC-INSURED | May Lose Value | No Bank Guarantee | ||

GOLDMAN SACHS FUNDAMENTAL INTERNATIONAL EQUITY FUNDS

Principal Investment Strategies and Risks

This is not a complete list of risks that may affect the Funds. For additional information concerning the risks applicable to the Funds, please see the Funds’ Prospectus.

The Goldman Sachs Focused International Equity Fund (formerly, Concentrated International Equity Fund) invests primarily in a diversified portfolio of equity investments in companies that are organized outside the United States or whose securities are principally traded outside the United States. The Fund is subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. Because the Fund may invest in a relatively small number of issuers, the Fund is subject to greater risk of loss.

The Goldman Sachs International Small Cap Fund invests primarily in a diversified portfolio of equity investments in non-U.S. small-capitalization companies. The Fund is subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. The securities of mid- and small-capitalization companies involve greater risks than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements.

The Goldman Sachs Strategic International Equity Fund invests primarily in a diversified portfolio of equity investments in companies that are organized outside the United States or whose securities are principally traded outside the United States. The Fund’s equity investments are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments.

3

GOLDMAN SACHS FUNDAMENTAL INTERNATIONAL EQUITY FUNDS

What Differentiates Goldman Sachs’ Fundamental International Equity Investment Process?

Goldman Sachs’ Fundamental International Equity investment process is based on the belief that strong, consistent results are best achieved through expert stock selection, performed by research teams working together on a global scale. Our deep, diverse and experienced team of research analysts and portfolio managers combines local insights with global, industry-specific expertise to identify its high conviction investment ideas.

| n | Fundamental research teams based in the United States, United Kingdom, Japan, China, Korea, Singapore, Brazil, and India and focusing on long-term business and management quality |

| n | Analysts collaborate regularly to leverage regional and industry-specific research and insights |

| n | Global perspective is informed by local market expertise |

| n | A common valuation framework, focusing on long-term earnings power, ensures consistency when valuing and comparing a company to its peers globally |

| n | Team of experienced Research Analysts is regionally aligned and has sector expertise |

| n | Team leverages the research of the approximately 80+ regional investment professionals |

| n | Decision-making process is informed by active participation in the global research process |

| n | Security selections are aligned with level of investment conviction |

| n | Risk monitoring considers whether investment and other risks to the Funds are intended and justified |

| n | Dedicated portfolio construction team assists in ongoing monitoring and adjustment of the Funds |

International equity portfolios that strive to offer:

| n | Access to markets across the world |

| n | Disciplined approach to stock selection |

| n | Optimal risk/return profiles |

4

MARKET REVIEW

Goldman Sachs Fundamental International Equity Funds

International equities declined modestly during the 12-month period ended October 31, 2014 (the “Reporting Period”). The Morgan Stanley Capital International (MSCI) Europe, Australasia, Far East (EAFE) Index (Net, USD, Unhedged) (the “MSCI EAFE Index”) posted an average annual total return of -0.60%.*

Stock markets in Japan and Europe reached new highs as late as December 2013. Japan’s Nikkei 225 Stock Average closed the calendar year at a six-year high, as the market reflected optimism about Prime Minister Shinzo Abe’s bold reforms and big stimulus. (The Nikkei 225 Stock Average is the leading and most respected index of Japanese stocks. It is a price-weighted index comprised of Japan’s top 225 blue chip companies on the Tokyo Stock Exchange.) Germany’s Xetra Dax also reached a new high in December 2013, as European equity markets continued to benefit from the European Central Bank’s (“ECB”) commitment to easy monetary policy and as economic growth returned to the region. (The Xetra Dax is a blue chip index in Germany that tracks the performance of the 30 most actively traded stocks on the Frankfurt Stock Exchange.)

International developed equity markets, however, stumbled in January 2014, as renewed concerns about a variety of issues in the growth and emerging markets weighed on performance, particularly in the Asia ex-Japan region. International developed equity markets rebounded in February 2014, but performance was relatively weak for the rest of the Reporting Period, as news from the developed markets was mixed.

The Eurozone economy grew at a stronger than expected 0.5% year-over-year rate for the fourth quarter of 2013, but growth then disappointed year to date through October 31, 2014. Purchasing Managers Index (“PMI”) data began to soften early in 2014; the Ifo survey of German business confidence began dropping; and Germany reduced its economic growth estimates. Further, deflation in the region remained a threat during the second half of the Reporting Period. Many corporate earnings reports and conservative guidance from management teams prompted downward revisions to estimates, even though in the end, most companies met or beat the revised estimates. The ECB cut its benchmark interest rate to 0.05%, reduced its bank deposit rate to -0.2% and announced it would begin to buy asset-backed securities. In contrast, economic data for the U.K. improved, particularly in terms of unemployment. In turn, markets began to anticipate the Bank of England might raise its interest rates by the end of 2014.

Similarly, Japanese equities got 2014 off to a weak start in anticipation of its consumption tax hike implemented in April 2014. Japanese equities then rallied back later in the Reporting Period as a number of economic indicators were more encouraging. Inflation in Japan continued to trend higher, and market sentiment improved as Prime Minister Abe revealed more details regarding corporate reform. Also, Japan’s manufacturing PMI rose to its highest level since March 2014, while the October 2014 Tankan survey of business sentiment was unexpectedly upbeat and revealed that large firms intend to increase spending. The Bank of Japan announced further monetary easing measures.

Performance of the Asia ex-Japan region generally improved through the second half of the Reporting Period. Indeed, the region posted the best performance within the MSCI EAFE Index for the full Reporting Period, largely due to the particularly strong performance of Hong Kong equities.

| *All | index returns are expressed in U.S. dollar terms. |

5

MARKET REVIEW

Looking Ahead

As we look toward the final quarter of 2014, it appears to us that the overall global economy continues to improve, though with growing regional variations. We expect a stronger macroeconomic environment to drive revenue and earnings growth. As equities appear to reach new heights in many markets, we believe the pace of their ascent is likely to slow, but we continue to believe that equity returns may look attractive versus other asset classes given what we consider to be their still above-average equity risk premium and reasonable valuations in light of growth prospects.

We see several main drivers of equity markets, including growth spending and structural reforms. In addition, we believe global consumption has the potential to be a significant driver of economies and equity markets both in the near and longer term. We believe a number of factors that have depressed consumer sentiment and spending in many regions could be reversing soon. We also believe the growth of the middle class and consumption in Asia and the emerging markets will likely be an important secular theme for several years. In our view, consumer behavior is likely to not only affect the consumer sectors but will also likely have a strong impact on the health care and information technology sectors, among others. Similarly, we believe increasing consumer spending in Asia and the emerging markets could have a significant impact on U.S., European and Japanese companies as well as on domestic companies.

At the end of the Reporting Period, we were watching for signs of market excess, such as ballooning market capitalizations, the number and quality of initial public offerings (“IPOs”), and valuations that may no longer be connected to fundamentals. We also believe that while many central banks still have a bias toward easing, the U.S. Federal Reserve (the “Fed”) is moving in the opposite direction. Lastly, in our view, currency is increasingly becoming an issue for companies, economies and equity markets. We believe a strengthening U.S. dollar could be a headwind for the U.S. economy and companies with foreign sales, such as many information technology companies. In contrast, in our opinion, Europe and Japan could benefit significantly from currency weakness.

As regions, countries, equity markets and companies differentiate themselves with revenue and earnings growth, we believe fundamental active managers have an excellent opportunity to similarly differentiate their portfolios and performance. As always, we maintain our focus on seeking companies that we believe will generate long-term growth in today’s ever-changing market conditions.

6

PORTFOLIO RESULTS

Goldman Sachs Focused International Equity Fund

Investment Objective

The Fund seeks long-term capital appreciation.

Portfolio Management Discussion and Analysis

Effective at the close of business on February 28, 2014, the Goldman Sachs Concentrated International Equity Fund was renamed the Goldman Sachs Focused International Equity Fund (the “Fund”). Below, the Goldman Sachs Global Equity Team discusses the Fund’s performance and positioning for the 12-month period ended October 31, 2014 (the “Reporting Period”).

| Q | How did the Fund perform during Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, B, C, Institutional, Service and IR Shares generated average annual total returns, without sales charges, of -7.16%, -7.82%, -7.83%, -6.79%, -7.28% and -6.90%, respectively. These returns compare to the -0.60% average annual total return of the Fund’s benchmark, the Morgan Stanley Capital International (MSCI) Europe, Australasia, Far East (EAFE) Index (Net, USD, Unhedged) (the “MSCI EAFE Index”), during the same period. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | The Fund’s underperformance in comparison of the MSCI EAFE Index during the Reporting Period can be primarily attributed to individual stock selection. |

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | The biggest detractors from Fund performance relative to the MSCI EAFE Index during the Reporting Period were Adidas, Rexel and Tullow Oil. |

| Adidas, a sports footwear, apparel and equipment manufacturer, detracted most from the Fund’s relative returns during the Reporting Period. The company cut its net income target for 2014, indicating that conditions in Russia and challenges in the U.S. golf market were creating potential risks. Adidas announced it would curtail its planned store rollout in Russia given the challenges continuing sanctions may have on the country. We believe these announcements discredited our original investment thesis that Adidas’ margins were set to see improvement, and thus we decided to sell out of the Fund’s position in the company. |

| Electrical equipment company Rexel was a top detractor from the Fund’s relative results during the Reporting Period. Its poor performance can be attributed to disappointing second calendar quarter results following market concerns about economic growth in Europe, which accounts for a significant portion of the company’s profits. Based on its second calendar quarter results, the company lowered its full year 2014 growth guidance. However, at the end of the Reporting Period, we continued to believe Rexel is a well-run business with strong cost controls and ongoing focus on increasing shareholder value, and thus maintained the Fund’s position in its stock. |

| Oil and gas exploration and production company Tullow Oil detracted from the Fund’s relative performance. Its shares declined due to falling oil prices. However, at the end of the Reporting Period, we remained positive on Tullow Oil, as we believe it possesses a good reputation for gas exploration and looks, in our view, to be a possible takeover candidate in the future. |

| Q | What were some of the Fund’s best-performing individual stocks? |

| A | The greatest contributors to Fund performance relative to the MSCI EAFE Index during the Reporting Period were Shire, Novo-Nordisk and Bayer. |

U.K.-based biopharmaceuticals company Shire was the top positive contributor to the Fund’s relative results during the Reporting Period. Its shares rose after the company announced better than expected third quarter 2013 results and raised its 2013 guidance. At the end of the Reporting Period, we believed Shire had a strong product pipeline that should |

7

PORTFOLIO RESULTS

continue to provide attractive long-term growth opportunities and was trading at an attractive valuation relative to its peers. |

| Denmark-based pharmaceutical company Novo-Nordisk was a strong contributor during the Reporting Period. The company delivered a good set of fiscal year 2013 results in February 2014, and a number of concerns that had impacted its performance during 2013 began to diminish. Namely, one of its key competitors was not able to show superiority to Novo-Nordisk’s Type 2 diabetes drug. Further, the impact of losing a supply contract with Express Script seemed to be less severe than initially anticipated, as a number of patients already on Novo-Nordisk’s drugs were grandfathered in and allowed to continue usage. Lastly, Novo-Nordisk’s pipeline was starting to attract attention, as its oral insulin drug completed Phase 1 trials and progressed into Phase 2. The company has a dominant presence in the U.S. and Europe and was growing its revenues in the emerging markets. At the end of the Reporting Period, we believed the company was well positioned to perform well over the longer term given the sustainability of growth in its diabetes franchise and its innovative product pipeline. |

| While our views ahead on both Shire and Novo-Nordisk remained positive at the end of the Reporting Period, we sold the Fund’s positions in each in an effort to reduce exposure to European names. We decided to take profits in each and invest in other high conviction ideas. |

| German-based chemical and pharmaceutical conglomerate Bayer performed well during the Reporting Period on the back of strong results. Its stock performed particularly well in September 2014 when the company announced it was going to spin off its materials science, or plastics, division, which is a low margin cyclical business. The market responded favorably to the company’s statement that it was making this structural change in order to refocus on its life sciences business, which is a higher margin area and, according to many, has better growth prospects. |

| Q | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | The sectors that detracted most from the Fund’s relative results during the Reporting Period were financials, consumer discretionary and energy, where stock selection in each weighed most negatively on performance. |

| The only sector to contribute positively to the Fund’s performance relative to the MSCI EAFE Index during the Reporting Period was health care, due primarily to effective stock selection. |

| Q | Which countries most affected the Fund’s performance during the Reporting Period? |

| A | Typically, the Fund’s individual stock holdings will significantly influence the Fund’s performance within a particular country or region relative to the MSCI EAFE Index. This effect may be even more pronounced in a concentrated portfolio or in countries that represent only a modest proportion of the MSCI EAFE Index. |

| That said, the countries that detracted most from the Fund’s performance during the Reporting Period were Japan, the U.K. and Switzerland, where stock selection in each hampered results. Effective stock selection in Denmark, Australia and the Netherlands boosted the Fund’s relative returns most. Having an underweighted allocation to the Netherlands also helped, as its equity market lagged the MSCI EAFE Index during the Reporting Period. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, we did not use derivatives to hedge positions or as part of an active management strategy, but we used index futures on an opportunistic basis to ensure the Fund remained almost fully exposed to equities following cash inflows or stock sales. |

| Q | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | We established new Fund positions during the Reporting Period in the Netherlands’ independent oil and gas company Royal Dutch Shell, Italian bank Intesa Sanpaolo and Japanese banking company Mitsubishi UFJ Financial Group. |

| We initiated a Fund position in Royal Dutch Shell because, in our view, the company was trading at an attractive valuation moving into a key phase of its investment cycle. We believe Royal Dutch Shell is well positioned to drive potential earnings growth through improved operational performance, cost reduction and improved capital allocation. Furthermore, its management appears to us to be committed to returning cash to shareholders through dividends and buybacks, which should reinforce positive shareholder sentiment, in our view. |

We established a Fund position in Intesa Sanpaolo, widely recognized as the leading bank in Italy. Since the recent asset quality review/stress test on European banks implemented by the European Central Bank, the holding contributed positively to the Fund’s results. At the time of purchase, the |

8

PORTFOLIO RESULTS

bank had a 10 billion euro buffer while still being able to generate enough return on equity to pay a high dividend. In our view, Intesa Sanpaolo offered an attractive risk/reward profile at its price at the time of purchase, with upside potential should the Eurozone continue its economic recovery and reduced downside risk given the current high profitability of the bank. |

| We purchased a Fund position in Mitsubishi UFJ Financial Group during the Reporting Period. In our view, what we considered to be the company’s earnings momentum and attractive valuation provided an opportunistic entry point. Furthermore, we believe the company is well positioned to protect its net profit better than its competitors, as it is supported by overseas companies linked on its balance sheet, such as Morgan Stanley and Bank of Ayudhya. |

| In addition to those sales already mentioned, we sold out of the Fund’s positions in Telecity Group, Air Liquide and BP during the Reporting Period. |

| We exited the Fund’s position in Telecity, a U.K.-based operator of European data centers, as we lost conviction that our investment thesis — that Telecity’s operating profits and cash flow would grow quickly as new capacity matured — would play out. The company continued to reduce pricing and margin progression expectations, suggesting increased competition and excess capacity. Given diminished conviction in our investment thesis, we concluded that we would reallocate the capital to what we considered to be more attractive investment opportunities. |

| We sold the Fund’s position in French multinational industrial gases company Air Liquide. We believe the stock’s price/earnings discount to the market had narrowed along with marginal disappointment around its base growth. These factors contributed to a notable sell-off in the stock during the Reporting Period. |

| We eliminated the Fund’s position in U.K.-based oil and gas company BP. The stock had performed well, and we decided to sell and take profits. |

| Q | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | In this Fund, both sector weightings and country allocations are largely the result of our bottom-up stock selection process rather than any top-down macroeconomic views or regional, country, sector or industry bets. We seek to outpace the MSCI EAFE Index by overweighting stocks that we expect to outperform and underweighting those we think may lag. Consequently, changes in its sector or country weightings are generally the direct result of individual stock selection or of stock appreciation or depreciation. That said, during the Reporting Period, the Fund’s exposure to industrials, energy, financials, utilities and telecommunication services increased relative to the MSCI EAFE Index during the Reporting Period, while its relative exposure to information technology, materials, health care, consumer staples and consumer discretionary decreased. From a country perspective, the Fund’s exposure to Switzerland, Italy, Sweden, South Korea and Belgium increased relative to the MSCI EAFE Index during the Reporting Period, while its relative exposure to the U.K., France, Germany and Australia decreased. |

| Q | Were there any changes to the Fund’s portfolio management team during the Reporting Period? |

| A | During the Reporting Period, Edward Perkin, managing director and chief investment officer (“CIO”) of International and Emerging Markets Equity and a lead portfolio manager of the Fund, left the firm. Suneil Mahindru, current lead portfolio manager for the firm’s Global Equity Partners strategy, became the CIO of International Equity and was named a lead portfolio manager on the Fund with Alexis Deladerriere. |

| Q | How was the Fund positioned relative to the MSCI EAFE Index at the end of the Reporting Period? |

| A | At the end of the Reporting Period, the Fund had more exposure to South Korea, Switzerland, Italy, Ireland, Taiwan, Sweden and Spain and less exposure to Japan, France, Germany and Australia relative to the MSCI EAFE Index. At the end of the Reporting Period, the Fund held neutral positions relative to the MSCI EAFE Index in several countries and had no position at all in several other countries, most notably Singapore, the Netherlands, Israel, Finland and Hong Kong. |

| From a sector allocation perspective, the Fund had overweight positions relative to the MSCI EAFE Index in industrials, information technology, energy and financials at the end of the Reporting Period. On the same date, the Fund had underweighted positions compared to the MSCI EAFE Index in consumer discretionary, consumer staples, health care, telecommunication services and materials and was rather neutrally weighted compared to the MSCI EAFE Index in utilities. |

| As always, we remained focused on individual stock selection, with sector and country positioning being a secondary, closely-monitored effect. |

9

FUND BASICS

Focused International Equity Fund

as of October 31, 2014

| PERFORMANCE REVIEW | ||||||||||

| November 1, 2013–October 31, 2014 | Fund Total Return (based on NAV)1 | MSCI EAFE Index (Net, USD, Unhedged)2 | ||||||||

| Class A | -7.16 | % | -0.60 | % | ||||||

| Class B | -7.82 | -0.60 | ||||||||

| Class C | -7.83 | -0.60 | ||||||||

| Institutional | -6.79 | -0.60 | ||||||||

| Service | -7.28 | -0.60 | ||||||||

| Class IR | -6.90 | -0.60 | ||||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The MSCI® EAFE Index (Net, USD, Unhedged) is a market capitalization-weighted composite of securities in 22 developed markets. The Index approximates the minimum possible dividend reinvestment. The dividend is reinvested after deduction for withholding tax, applying the rate to non-resident individuals who do not benefit from double taxation treaties. MSCI Barra uses withholding tax rates applicable to Luxembourg holding companies, as Luxembourg applies the highest rates. The Index is unmanaged and the figures for the Index do not include any deduction for fees or expenses. It is not possible to invest directly in an index. |

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||||||

| For the period ended 9/30/14 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||||||||

| Class A | -6.90 | % | 5.05 | % | 3.91 | % | 4.65 | % | 12/01/92 | |||||||||||

| Class B | -7.13 | 5.13 | 3.87 | 3.29 | 5/01/96 | |||||||||||||||

| Class C | -3.24 | 5.46 | 3.73 | 1.96 | 8/15/97 | |||||||||||||||

| Institutional | -1.10 | 6.68 | 4.92 | 4.46 | 2/07/96 | |||||||||||||||

| Service | -1.59 | 6.13 | 4.39 | 3.85 | 3/06/96 | |||||||||||||||

| Class IR | -1.20 | N/A | N/A | 8.86 | 8/31/10 | |||||||||||||||

| 3 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares, the assumed contingent deferred sales charge for Class B Shares (5% maximum declining to 0% after six years) and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Class B Shares convert automatically to Class A Shares on or about the fifteenth day of the last month of the calendar quarter that is eight years after purchase. Returns for Class B Shares for the period after conversion reflect the performance of Class A Shares. Because Institutional, Service and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. The Fund’s Class B Shares are no longer available for purchase by new or existing shareholders. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

10

FUND BASICS

| EXPENSE RATIOS4 | ||||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.32 | % | 1.69 | % | ||||||

| Class B | 2.07 | 2.43 | ||||||||

| Class C | 2.06 | 2.44 | ||||||||

| Institutional | 0.92 | 1.29 | ||||||||

| Service | 1.42 | 1.79 | ||||||||

| Class IR | 1.06 | 1.44 | ||||||||

| 4 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| TOP TEN HOLDINGS AS OF 10/31/145 | ||||||||||

| Holding | % of Net Assets | Line of Business | Country | |||||||

| Royal Dutch Shell PLC Class A | 4.9 | % | Energy | Netherlands | ||||||

| Intesa Sanpaolo SpA | 4.0 | Banks | Italy | |||||||

| Mitsubishi UFJ Financial Group, Inc. | 3.3 | Banks | Japan | |||||||

| Bayer AG (Registered) | 3.1 | Pharmaceuticals, Biotechnology & Life Sciences | Germany | |||||||

| Credit Suisse Group AG (Registered) | 3.1 | Diversified Financials | Switzerland | |||||||

| Reckitt Benckiser Group PLC | 3.1 | Household & Personal Products | United Kingdom | |||||||

| Vodafone Group PLC | 3.1 | Telecommunication Services | United Kingdom | |||||||

| Safran SA | 3.1 | Capital Goods | France | |||||||

| MediaTek, Inc. | 3.0 | Semiconductors & Semiconductor Equipment | Taiwan | |||||||

| Volvo AB Class B | 3.0 | Capital Goods | Sweden | |||||||

| 5 | The top 10 holdings may not be representative of the Fund’s future investments. |

11

FUND BASICS

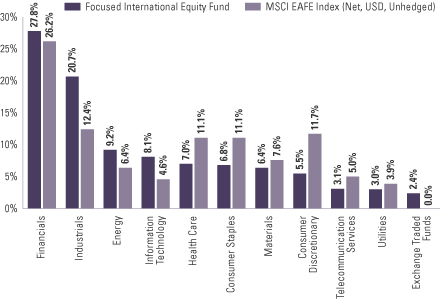

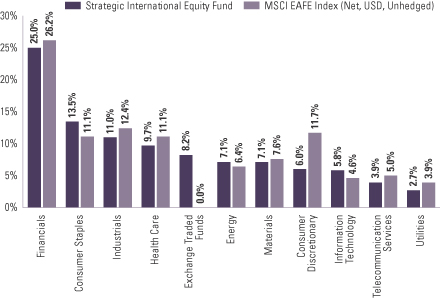

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 | ||

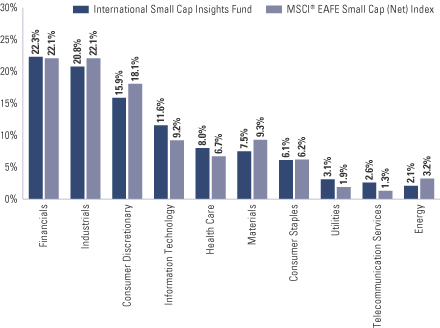

| As of October 31, 2014 | ||

| 6 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. Underlying sector allocations of exchange traded funds held by the Fund are not reflected in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

12

GOLDMAN SACHS FOCUSED INTERNATIONAL EQUITY FUND

Performance Summary

October 31, 2014

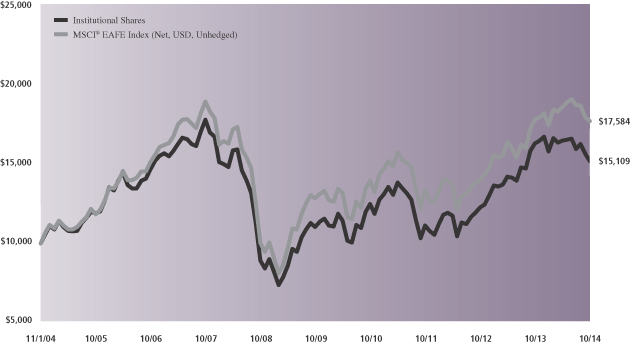

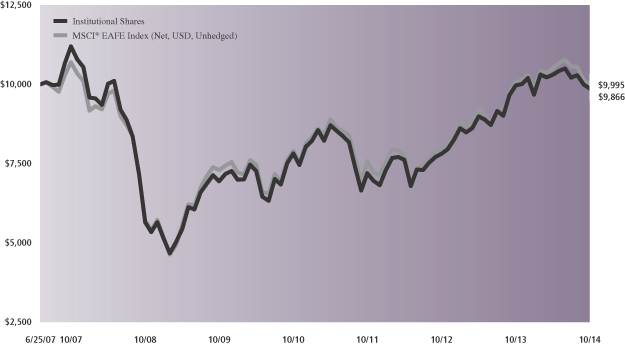

The following graph shows the value, as of October 31, 2014, of a $10,000 investment made on November 1, 2004 in Institutional Shares at NAV. For comparative purposes, the performance of the Fund’s benchmark, the MSCI® EAFE Index (Net, USD, Unhedged) is shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations will cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance of Class A, Class B, Class C, Service and Class IR Shares will vary from Institutional Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding issuer/industry/country investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover, and subscription and redemption cash flows affecting the Fund.

| Focused International Equity Fund’s 10 Year Performance |

Performance of a $10,000 Investment, with distributions reinvested, from November 1, 2004 through October 31, 2014.

| Average Annual Total Return through October 31, 2014 | One Year | Five Years | Ten Years | Since Inception | ||||||||||

Class A (Commenced December 1, 1992) | ||||||||||||||

Excluding sales charges | -7.16% | 6.07% | 3.80% | 4.75% | ||||||||||

Including sales charges | -12.25% | 4.88% | 3.21% | 4.48% | ||||||||||

| ||||||||||||||

Class B (Commenced May 1, 1996)* | ||||||||||||||

Excluding contingent deferred sales charges | -7.82% | 5.33% | 3.17% | 3.10% | ||||||||||

Including contingent deferred sales charges | -12.43% | 4.98% | 3.17% | 3.10% | ||||||||||

| ||||||||||||||

Class C (Commenced August 15, 1997) | ||||||||||||||

Excluding contingent deferred sales charges | -7.83% | 5.31% | 3.03% | 1.76% | ||||||||||

Including contingent deferred sales charges | -8.75% | 5.31% | 3.03% | 1.76% | ||||||||||

| ||||||||||||||

Institutional (Commenced February 7, 1996) | -6.79% | 6.51% | 4.21% | 4.26% | ||||||||||

| ||||||||||||||

Service (Commenced March 6, 1996) | -7.28% | 5.98% | 3.69% | 3.66% | ||||||||||

| ||||||||||||||

Class IR (Commenced August 31, 2010) | -6.90% | N/A | N/A | 7.87% | ||||||||||

| ||||||||||||||

| * | Effective at the close of business on November 14, 2014, Class B Shares of the Fund have converted to Class A Shares of the Fund. In addition, effective October 15, 2014, all redemptions of Class B Shares have not been subject to a contingent deferred sales charge. Average annual total returns for Class B Shares through October 31, 2014 have not been adjusted to reflect this change. |

13

PORTFOLIO RESULTS

Goldman Sachs International Small Cap Fund

Investment Objective

The Fund seeks long-term capital appreciation.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Global Equity Team discusses the Goldman Sachs International Small Cap Fund’s (the “Fund”) performance and positioning for the 12-month period ended October 31, 2014 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, B, C, Institutional, Service and IR Shares generated average annual total returns, without sales charges, of -0.48%, -1.18%, -1.19%, -0.06%, -0.57% and -0.23%, respectively. These returns compare to the -0.79% average annual total return of the Fund’s benchmark, the Standard and Poor’s (S&P) Developed Ex-U.S. Small Cap Index (Net, USD, Unhedged) (the “S&P Index”), during the same period. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | The Fund generated disappointing absolute returns but most of its share classes outperformed the S&P Index on a relative basis during the Reporting Period, attributable primarily to individual stock selection. Country allocation contributed positively as well, albeit more modestly. Sector allocation overall detracted slightly. |

| Q | What were some of the Fund’s best-performing individual stocks? |

| A | The greatest contributors to Fund performance relative to the S&P Index during the Reporting Period were Ashtead Group, Ingenico and Sierra Wireless. |

| Ashtead Group was the greatest positive contributor to the Fund’s relative performance during the Reporting Period. A new purchase for the Fund during the Reporting Period, Ashtead Group is a British construction equipment rental business focused on the non-residential sector but generates approximately 90% of its profits in the U.S. Ashtead Group used the industry downturn to refresh its equipment fleet, improve its balance sheet and build out detailed expansion plans. With early indications that the U.S. non-residential cycle may have turned, its business benefited from its earlier efforts. Indeed, the company’s recent results show encouraging progress both on the top and bottom lines. Already number two in the U.S. market, we believe the business’ top line benefited from three trends. First, a strong recovery in U.S. construction spending. Second, contractors increasingly choosing to rent rather than buy equipment. Third, the company successfully executing on its ambition to double its market share. Combined with strict cost controls, its top line growth also drove substantial improvements in absolute profits, margins and returns on capital. |

| French-based Ingenico was also a strong contributor to the Fund’s relative results. The company is a member of the duopoly that dominates the point-of-sale terminal market (i.e. terminals that take card payments in physical stores). We believe its hardware business is positioned favorably, as it has barriers beyond pure technology leadership and is raising barriers further by investing in associated areas. Its stock performed well, as the company continued to eliminate concerns about new mobile payments entrants and continued to invest in the faster growing online payments space. |

| Sierra Wireless is the world’s largest provider of communications modules that allow devices to communicate over wireless networks. We believe Sierra Wireless is well positioned to benefit from the increasing momentum behind the Internet of Things and should be able, in our view, to defend its strong market position. Following a span of underperformance, the stock rebounded strongly. (The Internet of Things is the interconnection of unique identifiable embedded computing devices within the existing Internet infrastructure.) |

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | The biggest detractors from Fund performance relative to the S&P Index during the Reporting Period were GFK, Nokian Renkaat and Cairn Energy. |

14

PORTFOLIO RESULTS

| Headquartered in Germany, GFK is the world’s fourth largest market research company, albeit with a revenue base biased toward Europe. Improved strategic positioning and efforts to streamline its business by implementing what it calls its “One GFK” strategy were hindered during the Reporting Period by a challenging macro environment and a requirement to continue to invest in global digital product offerings. This resulted in downgraded earnings expectations, which, in turn, weighed on GFK’s share price during the Reporting Period. |

| Nokian Renkaat also detracted from the Fund’s relative performance during the Reporting Period, as the market reacted negatively to the Finnish tire manufacturer’s exposure to Russia given recent geopolitical tensions in the area. Approximately 35% of Nokian Renkaat’s sales can be attributed to Russia and approximately 80% of its production. The company also performed poorly in the final quarter of 2013 and the first quarter of 2014, attributable largely to paying an additional tax charge relating to 2007 earnings and to a weak Russian car market. Given the significant exposure the company has to the region, we sold out of the Fund’s position in Nokian Renkaat based primarily on escalating sanctions imposed on Russia. |

| Cairn Energy is a U.K.-based oil and gas exploration and development company. Cairn Energy has what we consider to be an interesting series of exploration wells to be drilled in 2014 as well as interest in two North Sea production facilities expected to come on stream in the next two years. The company also holds an approximately 10% stake in Cairn India that was worth approximately $1 billion at market price at the end of the Reporting Period. However, the Indian Income Tax Department instructed Cairn Energy not to sell this stake in Cairn India, as it is investigating to see if Cairn Energy is liable for any retrospective capital gains tax on transfer of assets in 2006-2007. The company stated it intends to respond to the notice and refute the claim, but the announcement of the notice nevertheless materially impacted its share price during the Reporting Period. |

| Q | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | The sectors that contributed most to the Fund’s performance relative to the S&P Index were information technology, financials and health care, due primarily to effective stock selection in each. Having an overweighted allocation to health care, which outpaced the S&P Index during the Reporting Period, added value as well. |

| The biggest detractors from the Fund’s results during the Reporting Period were telecommunication services, utilities and materials, where stock selection overall hurt relative performance. |

| Q | Which countries most affected the Fund’s performance during the Reporting Period? |

| A | Typically, the Fund’s individual stock holdings will significantly influence the Fund’s performance within a particular country or region relative to the S&P Index. This effect may be even more pronounced in countries that represent only a modest proportion of the S&P Index. |

| That said, the Fund’s stock selection in the U.K., Australia and China contributed most positively to the Fund’s performance during the Reporting Period. Conversely, the countries that detracted most from the Fund’s performance during the Reporting Period were Germany, South Korea and Switzerland, where stock selection in each proved disappointing. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, we did not use derivatives to hedge positions or as part of an active management strategy, but we used index futures on an opportunistic basis to ensure the portfolio remained almost fully exposed to equities following cash inflows or stock sales. |

| Q | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | In addition to the purchase of Ashtead Group, already mentioned, we established Fund positions in Klepierre and Hays during the Reporting Period. |

| We initiated a Fund position in Klepierre, a continental Europe shopping center owner. At the end of 2013, it announced a transformational deal, wherein it disposed of more than 120 small shopping galleries to a joint venture led by Carrefour. This deal closed at the end of the first quarter of 2014. In our view, this deal was a major step in a planned strategic portfolio shift that Klepierre had started in 2012 toward fewer and larger centers. However, the stock price reaction was fairly muted, which we think is attributable to a strong price performance leading up to the third quarter of 2013. The company reported strong results in the first quarter of 2014, and the market acknowledged the magnitude of change in its portfolio because of the Carrefour deal. This, coupled with lower interest rates in continental Europe with the prospect of the central bank monetary easing, led to strong performance in the second quarter of 2014. We |

15

PORTFOLIO RESULTS

believe further upside could be supported by the likelihood of a low interest rate environment and continued internal improvements at the company. |

| We established a Fund position in U.K.-listed Hays, a global staffing company, during the Reporting Period. We believe the company has a favorable set of end-markets in the U.K., where growth has been strong; in Europe, where structural penetration should help the company grow for several years; and in Australia, which could see a recovery in the next 24 to 36 months from currently low activity levels. We believe Hays also has a market-leading information technology advantage. For example, it pairs with LinkedIn to identify candidates whose online behavior suggests they may be looking to move jobs. |

| In addition to the sale of Nokian Renkaat, mentioned earlier, we eliminated the Fund’s positions in Derwent London and Flughafen Zurich during the Reporting Period. |

| We eliminated the Fund’s position in Derwent London, a company that owns, operates and develops offices in central London. In our view, Derwent London is a high quality company with a strong track record. However, in our view, its valuation was getting stretched, with the stock trading at a premium. While rents in London rose rapidly during the Reporting Period, we believe we may be getting close to the top of the cycle, as rents at the end of the Reporting Period were in range of the previous cycle peak. |

| We sold the Fund’s position in Flughafen Zurich, the largest international airport in Switzerland, as a result of our concerns around Swiss Airways’ capacity plans, which are not expected to grow at the Zurich airport for the next 12 months or so. Furthermore, we had increasing doubts about the company’s plans to grow retail spending per passenger or to move forward on a real estate project called The Circle. |

| Q | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | In this Fund, both sector weightings and country allocations are largely the result of our bottom-up stock selection process rather than any top-down macroeconomic views or industry bets. We seek to outpace the S&P Index by overweighting stocks that we expect to outperform and underweighting those we think may lag. Consequently, changes in its sector or country weightings are generally the direct result of individual stock selection or of stock appreciation or depreciation. That said, during the Reporting Period, the Fund’s exposure to materials and health care increased relative to the S&P Index during the Reporting Period, while its relative exposure to information technology, consumer discretionary and industrials decreased. From a country perspective, the Fund’s exposure to Italy, Belgium and Sweden increased relative to the S&P Index during the Reporting Period, while its relative exposure to the U.K., Germany and the Netherlands decreased. |

| Q | How was the Fund positioned relative to the S&P Index at the end of the Reporting Period? |

| A | At the end of the Reporting Period, the Fund had more exposure to the U.K., China, Belgium and Italy and less exposure to Switzerland, Germany, Spain, the Netherlands and Hong Kong relative to the S&P Index. At the end of the Reporting Period, the Fund held neutral positions relative to the S&P Index in several countries, most notably Canada, and had no position at all in several other countries, most notably Thailand and Finland. |

| From a sector allocation perspective, the Fund had overweighted positions relative to the S&P Index in materials, health care and information technology at the end of the Reporting Period. On the same date, the Fund had underweighted positions compared to the S&P Index in financials, industrials, consumer discretionary and consumer staples and was rather neutrally weighted relative to the S&P Index in energy, utilities and telecommunication services. |

| As always, we remained focused on individual stock selection, with sector and country positioning being a secondary, closely-monitored effect. |

16

FUND BASICS

International Small Cap Fund

as of October 31, 2014

| PERFORMANCE REVIEW | ||||||||||

| November 1, 2013–October 31, 2014 | Fund Total Return (based on NAV)1 | S&P Developed Ex-U.S. Small Cap Index (Net, USD, Unhedged)2 | ||||||||

| Class A | -0.48 | % | -0.79 | % | ||||||

| Class B | -1.18 | -0.79 | ||||||||

| Class C | -1.19 | -0.79 | ||||||||

| Institutional | -0.06 | -0.79 | ||||||||

| Service | -0.57 | -0.79 | ||||||||

| Class IR | -0.23 | -0.79 | ||||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The S&P Developed Ex-U.S. Small Cap Index (Net, USD, Unhedged) is the small capitalization stock component of the S&P Developed Broad Market Index (BMI). The BMI is a float-weighted index that spans 32 countries (inclusive of the US) and includes the listed shares of all companies with an available market capitalization (float) of at least $100 million at the annual rebalance. The Small Cap Ex-U.S. is defined as those stocks falling in the bottom 15% of the cumulative available capital in each country. MSCI Barra reflects returns net of withholding taxes applied to foreign investors, calculated daily based on tax rates that would be applied to a Luxembourg-based investor. The Index is unmanaged and the figures for the Index do not include any deduction for fees or expenses. It is not possible to invest directly in an index. |

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||||||

| For the period ended 9/30/14 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||||||||

| Class A | -2.57 | % | 9.26 | % | 5.95 | % | 5.65 | % | 5/01/98 | |||||||||||

| Class B | -2.65 | 9.42 | 5.93 | 5.73 | 5/01/98 | |||||||||||||||

| Class C | 1.32 | 9.71 | 5.77 | 5.33 | 5/01/98 | |||||||||||||||

| Institutional | 3.59 | 11.00 | 7.02 | 6.55 | 5/01/98 | |||||||||||||||

| Service | 2.99 | 10.41 | 6.46 | 6.00 | 5/01/98 | |||||||||||||||

| Class IR | 3.37 | N/A | N/A | 12.68 | 8/31/10 | |||||||||||||||

| 3 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares, the assumed contingent deferred sales charge for Class B Shares (5% maximum declining to 0% after six years) and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Class B Shares convert automatically to Class A Shares on or about the fifteenth day of the last month of the calendar quarter that is eight years after purchase. Returns for Class B Shares for the period after conversion reflect the performance of Class A Shares. Because Institutional, Service and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. The Fund’s Class B Shares are no longer available for purchase by new or existing shareholders. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

17

FUND BASICS

| EXPENSE RATIOS4 | ||||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.38 | % | 1.88 | % | ||||||

| Class B | 2.13 | 2.63 | ||||||||

| Class C | 2.13 | 2.63 | ||||||||

| Institutional | 0.98 | 1.46 | ||||||||

| Service | 1.48 | 1.98 | ||||||||

| Class IR | 1.13 | 1.62 | ||||||||

| 4 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least June 30, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| TOP TEN HOLDINGS AS OF 10/31/145 | ||||||||||

| Holding | % of Net Assets | Line of Business | Country | |||||||

| Klepierre | 1.4 | % | Real Estate | France | ||||||

| Ingenico | 1.4 | Technology Hardware & Equipment | France | |||||||

| Inchcape PLC | 1.2 | Retailing | United Kingdom | |||||||

| St. James’s Place PLC | 1.2 | Insurance | United Kingdom | |||||||

| Ashtead Group PLC | 1.1 | Capital Goods | United Kingdom | |||||||

| Hays PLC | 1.1 | Commercial & Professional Services | United Kingdom | |||||||

| Cie d’Entreprises CFE | 1.1 | Capital Goods | Belgium | |||||||

| Melrose Industries PLC | 1.1 | Capital Goods | United Kingdom | |||||||

| Persimmon PLC | 1.1 | Consumer Durables & Apparel | United Kingdom | |||||||

| MARR SpA | 1.1 | Food & Staples Retailing | Italy | |||||||

| 5 | The top 10 holdings may not be representative of the Fund’s future investments. |

18

FUND BASICS

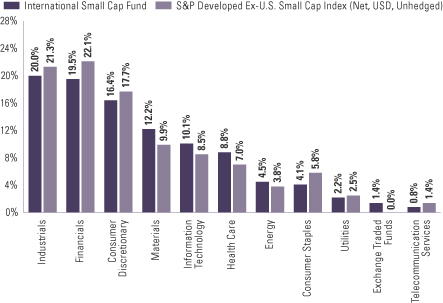

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 | ||

| As of October 31, 2014 | ||

| 6 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. Underlying sector allocations of exchange traded funds held by the Fund are not reflected in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

19

GOLDMAN SACHS INTERNATIONAL SMALL CAP FUND

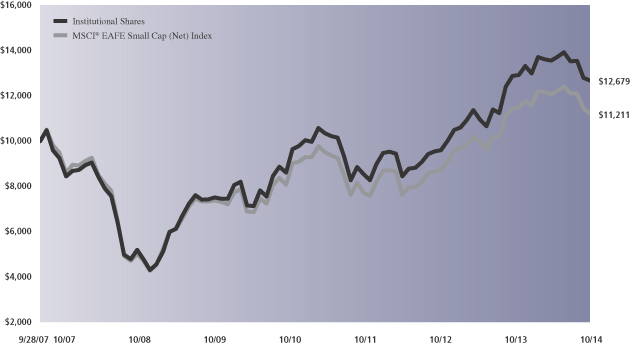

Performance Summary

October 31, 2014

The following graph shows the value, as of October 31, 2014, of a $10,000 investment made on November 1, 2004 in Institutional Shares at NAV. For comparative purposes, the performance of the Fund’s benchmark, the S&P Developed Ex-U.S. Small Cap Index (Net, USD, Unhedged) is shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations will cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance of Class A, Class B, Class C, Service and Class IR Shares will vary from Institutional Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding issuer/industry/country investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover, and subscription and redemption cash flows affecting the Fund.

| International Small Cap Fund’s 10 Year Performance |

Performance of a $10,000 Investment, with distributions reinvested, from November 1, 2004 through October 31, 2014.

| Average Annual Total Return through October 31, 2014 | One Year | Five Years | Ten Years | Since Inception | ||||||||||

Class A (Commenced May 1, 1998) | ||||||||||||||

Excluding sales charges | -0.48% | 11.03% | 6.32% | 5.93% | ||||||||||

Including sales charges | -5.95% | 9.79% | 5.72% | 5.57% | ||||||||||

|

|

|

|

|

|

|

| |||||||

Class B (Commenced May 1, 1998)* | ||||||||||||||

Excluding contingent deferred sales charges | -1.18% | 10.23% | 5.69% | 5.65% | ||||||||||

Including contingent deferred sales charges | -6.12% | 9.94% | 5.69% | 5.65% | ||||||||||

|

|

|

|

|

|

|

| |||||||

Class C (Commenced May 1, 1998) | ||||||||||||||

Excluding contingent deferred sales charges | -1.19% | 10.21% | 5.54% | 5.25% | ||||||||||

Including contingent deferred sales charges | -2.18% | 10.21% | 5.54% | 5.25% | ||||||||||

|

|

|

|

|

|

|

| |||||||

Institutional (Commenced May 1, 1998) | -0.06% | 11.52% | 6.78% | 6.46% | ||||||||||

|

|

|

|

|

|

|

| |||||||

Service (Commenced May 1, 1998) | -0.57% | 10.91% | 6.23% | 5.92% | ||||||||||

|

|

|

|

|

|

|

| |||||||

Class IR (Commenced August 31, 2010) | -0.23% | N/A | N/A | 12.20% | ||||||||||

|

|

|

|

|

|

|

|

| * | Effective at the close of business on November 14, 2014, Class B Shares of the Fund have converted to Class A Shares of the Fund. In addition, effective October 15, 2014, all redemptions of Class B Shares have not been subject to a contingent deferred sales charge. Average annual total returns for Class B Shares through October 31, 2014 have not been adjusted to reflect this change. |

20

PORTFOLIO RESULTS

Goldman Sachs Strategic International Equity Fund

Investment Objective

The Fund seeks long-term growth of capital.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Global Equity Team discusses the Goldman Sachs Strategic International Equity Fund’s (the “Fund”) performance and positioning for the 12-month period ended October 31, 2014 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, B, C, Institutional, IR and R Shares generated average annual total returns, without sales charges, of -1.41%, -2.15%, -2.10%, -1.05%, -1.14% and -1.58%, respectively. These returns compare to the -0.60% average annual total return of the Fund’s benchmark, the Morgan Stanley Capital International (MSCI) Europe, Australasia, Far East (EAFE) Index (Net, USD, Unhedged) (the “MSCI EAFE Index”), during the same period. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | The Fund’s underperformance relative to the MSCI EAFE Index during the Reporting Period can be primarily attributed to individual stock selection. |

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | Among the biggest detractors from Fund performance relative to the MSCI EAFE Index during the Reporting Period were Adidas, Nomura Real Estate and Tullow Oil. |

| Adidas, a sports footwear, apparel and equipment manufacturer, detracted most from the Fund’s relative returns during the Reporting Period. The company cut its net income target for 2014, indicating that conditions in Russia and challenges in the U.S. golf market were creating potential risks. Adidas announced it would curtail its planned store rollout in Russia given the challenges continuing sanctions may have on the country. We believe these announcements discredited our original investment thesis that Adidas’ margins were set to see improvement, and thus we decided to sell out of the Fund’s position in the company. |

| Nomura Real Estate, a Japanese real estate holding company, detracted from the Fund’s relative returns during the Reporting Period. The company underperformed the MSCI EAFE Index in spite of better than consensus fiscal second quarter 2014 results and upward revision of its fiscal year forecasts. Nomura Real Estate had benefited from a spike in demand of condo contracts before Japan’s consumption tax increase took effect. However, its shares declined after investors began to have concerns about a possible decline in demand for condos after the consumption tax hike. We decided to exit the Fund’s position in Nomura Real Estate in favor of higher conviction opportunities. |

| Oil and gas exploration and production company Tullow Oil detracted from the Fund’s relative performance. Its shares declined due to falling oil prices. However, at the end of the Reporting Period, we remained positive on Tullow Oil, as we believe it possesses a good reputation for gas exploration and looks, in our view, to be a possible takeover candidate in the future. |

| Q | What were some of the Fund’s best-performing individual stocks? |

| A | The greatest contributors to Fund performance relative to the MSCI EAFE Index during the Reporting Period were Shire, Scania and Novo-Nordisk. |

| U.K.-based biopharmaceuticals company Shire was the top positive contributor to the Fund’s relative results during the Reporting Period. Its shares rose after the company announced better than expected third quarter 2013 results and raised its 2013 guidance. At the end of the Reporting Period, we believed Shire had a strong product pipeline that should continue to provide attractive long-term growth opportunities and was trading at an attractive valuation relative to its peers. While our view ahead on Shire remained positive at the end of the Reporting Period, we sold the Fund’s position in an effort to reduce exposure to European names. We decided to take profits and invest in other high conviction ideas. |

21

PORTFOLIO RESULTS

Sweden-based truck manufacturer Scania was another top contributor to the Fund’s relative results during the Reporting Period. Its shares rose after Volkswagen announced it would make an offer for the remaining outstanding shares of Scania that it does not already own. We decided to sell out of the Fund’s position in Scania in favor of higher conviction opportunities. |

| Denmark-based pharmaceutical company Novo-Nordisk was a strong contributor during the Reporting Period. The company delivered a good set of fiscal year 2013 results in February 2014, and a number of concerns that had impacted its performance during 2013 began to diminish. Namely, one of its key competitors was not able to show superiority to Novo-Nordisk’s Type 2 diabetes drug. Further, the impact of losing a supply contract with Express Script seemed to be less severe than initially anticipated, as a number of patients already on Novo-Nordisk’s drugs were grandfathered in and allowed to continue usage. Lastly, Novo-Nordisk’s pipeline was starting to attract attention, as its oral insulin drug completed Phase 1 trials and progressed into Phase 2. The company has a dominant presence in the U.S. and Europe and was growing its revenues in the emerging markets. At the end of the Reporting Period, we believed the company was well positioned to perform well over the longer term given the sustainability of growth in its diabetes franchise and its innovative product pipeline. |

| Q | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | The biggest detractors from the Fund’s results during the Reporting Period were financials, utilities and energy, where weak stock selection in each hurt most. |

| The sectors that contributed most to the Fund’s performance relative to the MSCI EAFE Index were health care, industrials and consumer discretionary. Stock selection in all three sectors proved effective during the Reporting Period. |

| Q | Which countries most affected the Fund’s performance during the Reporting Period? |

| A | Typically, the Fund’s individual stock holdings will significantly influence the Fund’s performance within a particular country or region relative to the MSCI EAFE Index. This effect may be even more pronounced in countries that represent only a modest proportion of the MSCI EAFE Index. |

| That said, the countries that detracted most from the Fund’s relative performance were the U.K., Finland and Switzerland, wherein stock selection overall in each proved disappointing. Conversely, effective individual stock selection in France and Denmark contributed most positively to the Fund’s results relative to the MSCI EAFE Index. Having exposure to India, which is not a component of the MSCI EAFE Index and which significantly outperformed the MSCI EAFE Index, also boosted the Fund’s relative results. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, we did not use derivatives to hedge positions or as part of an active management strategy, but we used index futures on an opportunistic basis to ensure the portfolio remained almost fully exposed to equities following cash inflows or stock sales. |

| Q | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | During the Reporting Period, we purchased Fund positions in Italian bank Intesa Sanpaolo, Japanese banking company Mitsubishi UFJ Financial Group and the Netherlands’ independent oil and gas company Royal Dutch Shell. |

| We established a Fund position in Intesa Sanpaolo, widely recognized as the leading bank in Italy. Since the recent asset quality review/stress test on European banks implemented by the European Central Bank, the holding contributed positively to the Fund’s results. At the time of purchase, the bank had a 10 billion euro buffer while still being able to generate enough return on equity to pay a high dividend. In our view, Intesa Sanpaolo offered an attractive risk/reward profile at its price at the time of purchase, with upside potential should the Eurozone continue its economic recovery and reduced downside risk given the current high profitability of the bank. |

| We purchased a Fund position in Mitsubishi UFJ Financial Group during the Reporting Period. In our view, what we considered to be the company’s earnings momentum and attractive valuation provided an opportunistic entry point. Furthermore, we believe the company is well positioned to protect its net profit better than its competitors, as it is supported by overseas companies linked on its balance sheet, such as Morgan Stanley and Bank of Ayudhya. |

We initiated a Fund position in Royal Dutch Shell because, in our view, the company was trading at an attractive valuation moving into a key phase of its investment cycle. We believe Royal Dutch Shell is well positioned to drive potential earnings growth through improved operational performance, cost reduction and improved capital allocation. Furthermore, |

22

PORTFOLIO RESULTS

its management appears to us to be committed to returning cash to shareholders through dividends and buybacks, which should reinforce positive shareholder sentiment, in our view. |

| In addition to the sales already mentioned, we sold out of the Fund’s positions in HSBC, BNP Paribas and Sumitomo Mitsui Financial Group during the Reporting Period. We sold the Fund’s position in U.K.-based HSBC, as regulatory pressures were a drag on the bank’s capital. After meeting with the chief financial officer and head of commercial banking of HSBC, who highlighted the increasing regulatory burden banks are currently facing, we believed such pressures would result in HSBC having to retain more capital, making it difficult for the bank to generate an attractive return on equity. |

| We eliminated the Fund’s position in BNP Paribas when it was announced that the French bank was under investigation by U.S. authorities for dealings with countries under U.S. sanctions. The $9 billion settlement as well as the dollar- clearing suspension represented, in our view, significant setbacks for BNP Paribas in the build-up of its capital position and the normalization of its business. |

| Japanese bank group Sumitomo Mitsui Financial Group detracted from the Fund’s relative performance during the Reporting Period. Its stock underperformed the MSCI EAFE Index after it announced its quarterly net income, which declined substantially compared to last fiscal year due to lower bond trading gains. The loan-deposit spread in its banking unit also narrowed. We decided to sell the Fund’s position in Sumitomo Mitsui Financial Group. |

| Q | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | In this Fund, both sector weightings and country allocations are largely the result of our bottom-up stock selection process rather than any top-down macroeconomic views or regional, country, sector or industry bets. We seek to outpace the MSCI EAFE Index by overweighting stocks that we expect to outperform and underweighting those we think may lag. Consequently, changes in its sector or country weightings are generally the direct result of individual stock selection or of stock appreciation or depreciation. That said, during the Reporting Period, the Fund’s exposure to consumer staples, utilities and industrials increased relative to the MSCI EAFE Index during the Reporting Period, while its relative exposure to materials, telecommunication services, health care and consumer discretionary decreased. From a country perspective, the Fund’s exposure to Japan, Switzerland, Sweden, Spain, Italy and Ireland increased relative to the MSCI EAFE Index during the Reporting Period, while its relative exposure to the U.K., France and Russia decreased. |

| Q | Were there any changes to the Fund’s portfolio management team during the Reporting Period? |

| A | During the Reporting Period, Edward Perkin, managing director and chief investment officer (“CIO”) of International and Emerging Markets Equity and a lead portfolio manager of the Fund, left the firm. Suneil Mahindru, current lead portfolio manager for the firm’s Global Equity Partners strategy, became the CIO of International Equity and was named a lead portfolio manager on the Fund with Alexis Deladerriere. |

| Q | How was the Fund positioned relative to the MSCI EAFE Index at the end of the Reporting Period? |

| A | At the end of the Reporting Period, the Fund had more exposure to Belgium, South Korea, Ireland, Switzerland, Sweden, Taiwan and Russia relative to the MSCI EAFE Index and less exposure to the U.K., Australia, Germany and the Netherlands relative to the MSCI EAFE Index. At the end of the Reporting Period, the Fund held neutral positions relative to the MSCI EAFE Index in several countries and had no position at all in several other countries, most notably Hong Kong, Finland and Norway. |

| From a sector allocation perspective, the Fund had overweight positions relative to the MSCI EAFE Index in consumer staples and information technology at the end of the Reporting Period. On the same date, the Fund had underweighted positions compared to the MSCI EAFE Index in consumer discretionary, financials, industrials, health care, telecommunication services and utilities and rather neutral positions relative to the MSCI EAFE Index in energy and materials. |

| As always, we remained focused on individual stock selection, with sector and country positioning being a secondary, closely-monitored effect. |

23

FUND BASICS

Strategic International Equity Fund

as of October 31, 2014

| PERFORMANCE REVIEW | ||||||||||

| November 1, 2013–October 31, 2014 | Fund Total Return (based on NAV)1 | MSCI EAFE Index (Net, USD, Unhedged)2 | ||||||||

| Class A | -1.41 | % | -0.60 | % | ||||||

| Class B | -2.15 | -0.60 | ||||||||

| Class C | -2.10 | -0.60 | ||||||||

| Institutional | -1.05 | -0.60 | ||||||||

| Class IR | -1.14 | -0.60 | ||||||||

| Class R | -1.58 | -0.60 | ||||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The MSCI® EAFE Index (Net, USD, Unhedged) is a market capitalization-weighted composite of securities in 22 developed markets. The Index approximates the minimum possible dividend reinvestment. The dividend is reinvested after deduction for withholding tax, applying the rate to non-resident individuals who do not benefit from double taxation treaties. MSCI Barra uses withholding tax rates applicable to Luxembourg holding companies, as Luxembourg applies the highest rates. The Index is unmanaged and the figures for the Index do not include any deduction for fees or expenses. It is not possible to invest directly in an index. |

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||

| For the period ended 9/30/14 | One Year | Five Years | Since Inception | Inception Date | ||||||||||||

| Class A | -2.57 | % | 5.36 | % | -1.16 | % | 6/25/07 | |||||||||

| Class B | -2.69 | 5.40 | -1.16 | 6/25/07 | ||||||||||||

| Class C | 1.31 | 5.76 | -1.14 | 6/25/07 | ||||||||||||

| Institutional | 3.51 | 6.96 | -0.01 | 6/25/07 | ||||||||||||

| Class IR | 3.39 | 6.91 | -1.18 | 11/30/07 | ||||||||||||

| Class R | 2.84 | 6.29 | -1.74 | 11/30/07 | ||||||||||||

| 3 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares, the assumed contingent deferred sales charge for Class B Shares (5% maximum declining to 0% after six years) and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Class B Shares convert automatically to Class A Shares on or about the fifteenth day of the last month of the calendar quarter that is eight years after purchase. Returns for Class B Shares for the period after conversion reflect the performance of Class A Shares. Because Institutional, Class R and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. The Fund’s Class B Shares are no longer available for purchase by new or existing shareholders. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

24

FUND BASICS

| EXPENSE RATIOS4 | ||||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.33 | % | 1.88 | % | ||||||

| Class B | 2.08 | 2.63 | ||||||||

| Class C | 2.08 | 2.63 | ||||||||

| Institutional | 0.93 | 1.48 | ||||||||

| Class IR | 1.08 | 1.63 | ||||||||

| Class R | 1.58 | 2.12 | ||||||||

| 4 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| TOP TEN HOLDINGS AS OF 10/31/145 | ||||||||||