UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive,

Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| | |

Copies to: |

Caroline Kraus, Esq. | | Geoffrey R.T. Kenyon, Esq. |

Goldman, Sachs & Co. | | Dechert LLP |

200 West Street | | One International Place, 40th Floor |

New York, New York 10282 | | 100 Oliver Street |

| | Boston, MA 02110 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: November 30

Date of reporting period: May 31, 2016

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| | The Semi-Annual Report to Shareholders is filed herewith. |

Goldman Sachs Funds

| | | | |

| | |

| Semi-Annual Report | | | | May 31, 2016 |

| | |

| | | | MLP Energy Infrastructure Fund |

Goldman Sachs MLP Energy Infrastructure Fund

| | | | |

TABLE OF CONTENTS | | | | |

| |

Investment Process | | | 1 | |

| |

Portfolio Management Discussion and Performance Summaries | | | 2 | |

| |

Schedule of Investments | | | 10 | |

| |

Financial Statements | | | 11 | |

| |

Financial Highlights | | | 14 | |

| |

Notes to Financial Statements | | | 16 | |

| |

Other Information | | | 28 | |

| | | | |

| | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

What Differentiates Goldman Sachs’ MLP

Energy Infrastructure Fund Investment Process?

With a quality-oriented approach, the MLP Energy Infrastructure Fund seeks total return through current income and capital appreciation. We have an experienced investment team integrated within Goldman Sachs Asset Management, L.P. (“GSAM”), allowing us to leverage franchise expertise and risk framework across multiple asset classes. We invest primarily in Master Limited Partnerships (“MLPs”), or similar structures, that own energy infrastructure assets.

| n | | To capture the full energy chain, we analyze energy production and user trends that ultimately impact energy infrastructure. |

| n | | We rigorously assess companies on both the asset and equity level. |

| n | | Macro Trend Analysis

First, we analyze overall energy trends through capital spending shifts and drilling trends, in addition to regional supply and demand imbalances. |

| n | | Top-Down Sector Selection

Secondly, we establish the impact of macro and regional trends on energy infrastructure. |

| n | | Bottom-Up Security Selection

Finally, we select names by evaluating a company’s management, assets, expected returns and technicals. |

| n | | Our team of MLP dedicated investment professionals includes lead portfolio managers averaging 10 years of investment experience. |

| n | | Ability to leverage energy related resources across GSAM Equity, Fixed Income and Commodity groups, as well as utilize risk management resources. |

| n | | Unique investment approach stemming from a more holistic view across the extremes of the energy value chain, corporate access, broader valuation understanding, and resource advantages. |

1

PORTFOLIO RESULTS

Goldman Sachs MLP Energy Infrastructure Fund

Investment Objective And Principal Strategy

The Fund seeks total return through current income and capital appreciation. The Fund, under normal circumstances, invests at least 80% of its net assets plus any borrowings for investment purposes (measured at the time of purchase) in energy infrastructure master limited partnership (“MLP”) investments. The Fund’s MLP investments may include, but are not limited to: MLPs structured as limited partnerships or limited liability companies; MLPs that are taxed as “C” corporations; institutional units issued by MLP affiliates; “C” corporations that hold significant interests in MLPs; private investments in public equities (“PIPEs”) issued by MLPs; and other U.S. and non-U.S. equity and fixed income securities and derivative instruments, including pooled investment vehicles and exchange-traded notes (“ETNs”), that provide exposure to MLPs. Energy infrastructure MLPs own and operate assets that are used in the energy sector, including assets used in exploring, developing, producing, generating, transporting (including marine), transmitting, terminal operation, storing, gathering, processing, refining, distributing, mining or marketing of natural gas, natural gas liquids, crude oil, refined products, coal or electricity, or that provide energy-related equipment or services. The Fund’s MLP investments may be of any capitalization size.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Energy and Infrastructure Team discusses the Goldman Sachs MLP Energy Infrastructure Fund’s (the “Fund”) performance and positioning for the six-month period ended May 31, 2016 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, C, Institutional, IR and R Shares generated cumulative total returns, without sales charges, of 3.33%, 2.99%, 3.69%, 3.57% and 3.22%, respectively. These returns compare to the 5.22% cumulative total return of the Alerian MLP Index (the “Alerian Index”). The Alerian Index is a leading measure of energy MLPs.1 |

| Q | | How did energy master limited partnerships (“MLPs”) overall perform during the Reporting Period? |

| A | | During the Reporting Period, energy MLPs, as represented by the Alerian Index, advanced on a total return basis. In addition, the Alerian Index (+5.22%) outperformed the S&P 500® Index (+1.93%) and the AMEX Energy Select Sector Index (-0.02%).2 The Alerian Index underperformed the utilities (+17.08%) and real estate investment trust (“REIT”) (+7.72%) sectors, as represented by the Philadelphia Stock Exchange (PHLX) Utility Sector Index and the FTSE NAREIT (National Association of Real Estate Investment Trusts) U.S. Real Estate Index, respectively.3 |

| | Weakness in commodity prices overall was a headwind for energy MLPs during the first half of the Reporting Period. The price of West Texas Intermediate (“WTI”) crude oil, which started the Reporting Period at $41.85 a barrel, 61% below its 2014 high, dropped another 37% through the close of trading on February 11, 2016.4 The price decline was due to market oversupply, driven in large part by the increase in U.S. production during the last several years. Global crude oil supplies grew by more than 10 million barrels per day between calendar year 2005 and calendar year 2015, with the U.S. accounting for almost 70% of the growth.5 The unit prices of energy MLPs also declined during the first half of the Reporting Period. Energy MLP unit prices and crude oil prices were closely correlated, a departure from the long-term |

| | 1 | | Source: Alerian. The Alerian Index is a float-adjusted, capitalization- weighted index, whose constituents represent approximately 85% of total float-adjusted market capitalization. It is disseminated real-time on a price-return basis (AMZ) and on a total-return basis (AMZX). |

| | 2 | | The S&P 500® Index is a diverse index that includes 500 American companies that represent more than 70% of the total market capitalization of the U.S. stock market. The AMEX Energy Select Sector Index (IXE) is a modified market capitalization-based index intended to track the movements of companies that are components of the S&P 500® Index and are involved in the development or production of energy products. |

| | 3 | | The PHLX Utility Sector Index is composed of geographically diverse public U.S. utility stocks. The FTSE NAREIT U.S. Real Estate Index Series is an index that spans the commercial real estate space across the U.S. economy, offering exposure to all investment and property sectors. |

| | 5 | | Source: U.S. Energy Information Administration. |

2

PORTFOLIO RESULTS

| | average.6 Energy MLP performance was also challenged during the first half of the Reporting Period by reduced access to the capital markets, negative investor sentiment and technical pressures. |

| | During the second half of the Reporting Period, the crude oil market started to work through the oversupply, and as a result, crude oil prices experienced a strong recovery. The price of WTI crude oil rallied 87% between the close of trading on February 11, 2016 and the end of the Reporting Period, finishing at $49.10 a barrel.7 As crude oil prices broadly rebounded, energy MLPs saw positive performance, with correlations between energy MLP unit prices and crude oil prices remaining tight. Additionally, energy MLPs benefited during the second half of the Reporting Period from increased access to the capital markets, which helped them address some of their funding needs and assuaged market concerns about the sustainability of energy MLP distributions. During the Reporting Period overall, energy MLP fundamentals remained strong, with cash flow generation staying resilient despite the commodity headwinds in the first half of the Reporting Period. |

| | Overall, weaker net investment inflows and increased short interest dampened the performance of energy MLPs, particularly during the first half of the Reporting Period. Net investment flows fell to their lowest point in five years8 during the fourth quarter of 2015 due to the significant drop in crude oil prices. Net investment inflows improved during the second half of the Reporting Period as volatility eased in the commodity market and the energy MLP sector. Short selling also added to technical pressure. Short interest (as measured by the Alerian MLP Index ETF) increased 8.6% during the Reporting Period overall.9 (Short interest is the quantity of shares that investors have sold short but not yet covered or closed out.) |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | Security selection drove the Fund’s performance during the Reporting Period, as volatility within the commodity markets increased the dispersion of individual stock returns. The volatility was magnified in companies that had greater exposure to commodities, making them the worst performers during the commodity price downturn and the best performers during the recovery. |

| | In terms of its exposures, the Fund was hurt by its overweight position in the general partner subsector,10 which was one of the worst performing subsectors during the Reporting Period. The general partner subsector fell out of favor during the commodity price downturn because of concerns about distributions, stemming from the economics between general partners and their underlying energy MLPs and how those economics might affect general partner distributions. Through incentive distribution rights, a general partner typically receives an incrementally growing percentage of cash flow from their underlying MLP as the MLP increases its distribution. As a result, the distributions paid by the MLP are of great significance to the distributions of the general partner. On the positive side, the Fund benefited from its overweight in natural gas and natural gas liquids infrastructure, one of the best performing subsectors of the Reporting Period. Within this subsector, the Fund held what we considered to be high quality companies well positioned to benefit from exposure to commodity prices. |

| Q | | What individual holdings detracted from the Fund’s relative performance during the Reporting Period? |

| A | | During the Reporting Period, the Fund was hampered relative to the Alerian Index by its positions in Energy Transfer Equity, LP; MPLX LP; and Tallgrass Energy GP LP. |

| | A top relative detractor was Energy Transfer Equity, LP (ETE). Through its interests in various underlying MLPs, ETE is involved in the natural gas midstream,11 transportation and storage business as well as in the retail propane business. ETE’s unit price weakened during the Reporting Period, partly because of its announced acquisition of Williams Companies, which the market viewed unfavorably. We decided to exit the Fund’s position in ETE during the Reporting Period. |

| | 6 | | Source: Goldman Sachs Investment Strategy Group, Bloomberg. |

| | 8 | | Source: U.S. Capital Advisors. |

| | 9 | | Source: Bloomberg, Goldman Sachs Asset Management. Data as of May 31, 2016. |

| | 10 | | Sector and subsector allocations are defined by GSAM and may differ from sector allocations used by the Alerian Index. |

| | 11 | | The midstream component of the energy industry is usually defined as those companies providing products or services that help link the supply side, i.e. energy producers, and the demand side, i.e. energy end-users, for any type of energy commodity. Such midstream business can include, but are not limited to, those that process, store, market and transport various energy commodities. |

3

PORTFOLIO RESULTS

| | MPLX LP (MPLX) also detracted from the Fund’s relative performance during the Reporting Period. MPLX is an energy MLP formed by Marathon Petroleum Corp. to own, operate, develop and acquire pipelines and other midstream assets related to the transportation and storage of crude oil, refined products and other hydrocarbon based products. During the Reporting Period, MPLX’s management cut its distribution growth rate guidance from 25% to a range between 12% and 15% because of a higher cost of capital and lower expected volume growth. We maintained the Fund’s position in MPLX at the end of the Reporting Period because of what we viewed as the company’s strong asset footprint in the northeastern U.S. through its acquisition of MarkWest Energy Partners, LP, completed in December 2015. |

| | Another detractor from the Fund’s relative performance was Tallgrass Energy GP LP (TEGP). TEGP is a holding company that owns, operates and develops midstream energy assets in North America through its underlying MLP, Tallgrass Energy Partners LP (TEP). TEP provides natural gas transportation and storage services to customers in the Rocky Mountains and midwestern regions of the U.S. via its Tallgrass Interstate Gas transportation system. TEGP weakened during the first half of the Reporting Period, driven by broad investor concerns about general partner distribution growth profiles that were linked to underlying MLPs through incentive distribution rights. (Incentive distribution rights give a general partner an increasing share in the underlying MLP’s incremental distributable cash flow.) Through incentive distribution rights, a general partner can grow its distribution at a much faster rate than the underlying MLP because it is allowed to receive a larger percentage of the MLP’s distributions if the MLP is able to reach certain distribution thresholds. On the other hand, incentive distribution rights can be a hindrance to a general partner if the underlying MLP cuts its distribution. We decided to sell the Fund’s position in TEGP during the Reporting Period, reallocating the proceeds to companies with what we considered to be better fundamentals. |

| Q | | What individual holdings added to the Fund’s relative performance during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s investments in Targa Resources Corp.; Phillips 66 Partners LP; and EQT Midstream Partners LP added to its relative returns. |

| | Targa Resources Corp. (TRGP) was a top relative contributor to Fund results during the Reporting Period. TRGP gathers, compresses, treats, processes and sells natural gas. In addition, it stores, fractionates,12 treats, transports and sells natural gas liquids and related products. TRGP benefited from its substantial exposure to commodities, which rallied strongly in the second half of the Reporting Period. The Fund continued to hold TRGP at the end of the Reporting Period. |

| | Another leading contributor was Phillips 66 Partners LP (PSXP), which owns, operates, develops and acquires crude oil, refined petroleum product, and natural gas liquid pipelines and terminals as well as other transportation and midstream assets, primarily in the central and Gulf Coast regions of the U.S. PSXP added to the Fund’s relative performance as it continued to acquire assets from its parent company. These acquisitions led to visible growth for PSXP while helping it to maintain a strong balance sheet. The Fund continued to own PSXP at the end of the Reporting Period. |

| | The Fund also benefited from a position in EQT Midstream Partners LP (EQM) during the Reporting Period. EQM acquires, owns, develops and operates midstream natural gas assets in the Appalachian Basin of the U.S., primarily the Marcellus Shale in southern Pennsylvania and northern West Virginia. EQM reported strong earnings during the Reporting Period and continued to provide future cash flow visibility. At the same time, it maintained what we viewed as a healthy balance sheet and credit profile. At the end of the Reporting Period, the Fund continued to hold EQM. |

| Q | | Were there any notable purchases or sales during the Reporting Period? |

| A | | During the Reporting Period, the Fund initiated a position in Plains All American Pipeline LP (PAA). PAA is involved in pipeline transportation, terminalling, storage and gathering services for crude oil, natural gas and refined products. As the energy MLP sector sold off in the first half of the Reporting Period, we took advantage of the opportunity to add this large-cap name to the Fund’s holdings. In our view, PAA offered an attractive yield, and we believed it would give the Fund exposure to possible rebounds in the commodity market and energy MLP sector. |

| | The Fund also added a position in Western Gas Partners, LP (WES), which owns, operates, acquires and develops |

| | 12 | | Fractionation is the process used to separate the base components of natural gas liquids. |

4

PORTFOLIO RESULTS

| | midstream energy assets located in east, west and south Texas, the Rocky Mountains, north-central Pennsylvania and the mid-continental U.S. WES is also in the business of gathering, compressing, treating and transporting natural gas. The Fund invested in the company because we believe it has sizable potential drop-down inventory from its parent company and organic growth opportunities in the Delaware/ Permian Basin. (Drop-down refers to the act of a parent company selling MLP-qualified assets to the associated MLP.) |

| | As mentioned previously, we sold the Fund’s position in Tallgrass Energy GP LP, reallocating the proceeds to companies with what we considered to be better fundamentals. |

| | Also, as mentioned previously, the Fund’s investment in Energy Transfer Equity, LP was eliminated. We sold ETE on price weakness and because it was involved in a complicated merger with Williams Companies, which we believed presented various legal, regulatory and financial risks. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, the Fund did not use derivatives or similar instruments. |

| Q | | What is the Fund’s tactical view and strategy for the months ahead? |

| A | | At the end of the Reporting Period, correlations between energy MLP unit prices and crude oil prices remained higher than the long-term average, a pattern we expect to continue in the near term.13 Therefore, if crude oil prices continue to rise, we anticipate positive momentum in the energy MLP sector. In the short term, the energy MLP sector has, we believe, moved to an enterprise value/EBITDA14 valuation model, similar to that of the utilities sector. Longer term, should U.S. energy production begin to rebound, we expect energy MLP total returns to be consistent with the yield plus growth model, which is how energy MLPs have historically been valued. Energy MLP valuations are generally based on the spread, or yield differential, between energy MLPs and 10-year U.S. Treasury notes. At the end of the Reporting Period, this spread was 5.7%, wider than the long-term average of 3.9%.15 Should commodity prices stabilize, we believe there is the potential of capital appreciation in the energy MLP sector, stemming from distribution growth and a possible market revaluation that shifts the valuation framework from the enterprise value/EBITDA model back to the yield plus growth model. That said, and despite what we consider to be positive fundamentals, the energy MLP sector may face further challenges. For example, rising interest rates could negatively impact energy MLP valuations, and access to the capital markets could be limited if investors lose confidence in the rebound in crude oil prices. |

| | Although U.S. production declined during the Reporting Period, we still believe overall production volumes will continue to grow across crude oil, natural gas liquids and dry natural gas over the long term. Indeed, estimates from the U.S. Energy Information Administration show production growth in all three commodities. Going forward, we see significant opportunity in these three areas as a result of numerous positive catalysts. In terms of crude oil, following a relatively short-term production decline due to the drop in rig counts, we expect U.S. production growth to rebound if global demand continues to grow at its historical average rate of approximately one million barrels per day each year.16 We believe the U.S. will be a key source of the supply growth needed to meet such demand. In our view, this is because U.S. shale producers can respond quickly to crude oil price movements compared to international producers, which have historically been drivers of supply but may have higher costs and longer lead times for their projects. In terms of natural gas liquids, we believe recent and planned international expansion terminals and large-scale petrochemical developments should allow for the continued increase in demand channels. In terms of dry natural gas, catalysts include the transition from coal to natural gas power generation and the continued buildout of the U.S.’ export capabilities. |

| | Looking ahead, we believe the energy MLP sector could potentially provide attractive yield and capital appreciation over the long term. In the short term, we believe energy MLPs should continue to offer distribution growth, albeit at a slower pace than the double-digit growth seen before the recent steep drop in crude oil prices. While lower distribution |

| | 13 | | Source: Goldman Sachs Investment Strategy Group, Bloomberg. |

| | 14 | | Enterprise value is the market value of debt, common equity and preferred equity minus the value of cash. EBITDA is earnings before interest, taxes, depreciation and amortization. Enterprise value/ EBITDA is a financial ratio that measures a company’s value. |

| | 15 | | Source: Bloomberg; Goldman Sachs Asset Management. MLP yields reflect the market-cap weighted average yield of the 50 largest MLPs as represented by the Alerian Index. |

| | 16 | | Source: U.S. Energy Information Administration. |

5

PORTFOLIO RESULTS

| | growth trajectories will result, in our view, in smaller payout increases for investors in the near term, they will also allow energy MLPs to finance more of their capital expenditures with internal capital, thus reducing reliance, we believe, on external debt and equity markets. |

| | Finally, we believe investors should recognize a growing dispersion in performance. Rising U.S. production has greatly altered the energy landscape, proving beneficial to some regions and detrimental to others. As a result, we believe the dispersion between the energy “haves” and “have nots” has increased. In our opinion, rigorous fundamental analysis is essential in seeking to take advantage of the powerful energy revolution theme that we believe persists. |

6

FUND BASICS

Goldman Sachs MLP Energy Infrastructure Fund

as of May 31, 2016

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | December 1, 2015– May 31, 2016 | | Fund Total Return

(based on NAV)1 | | | Alerian MLP Index2 | |

| | Class A | | | 3.33 | % | | | 5.22 | % |

| | Class C | | | 2.99 | | | | 5.22 | |

| | Institutional | | | 3.69 | | | | 5.22 | |

| | Class IR | | | 3.57 | | | | 5.22 | |

| | | Class R | | | 3.22 | | | | 5.22 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The Alerian MLP Index is a composite of the 50 most prominent energy master limited partnerships calculated by Standard & Poor’s using a float-adjusted market capitalization methodology. The Index is disseminated by the New York Stock Exchange real-time on a price return basis (NYSE: AMZ). The corresponding total return index is calculated and disseminated daily through ticker AMZX. The Alerian MLP Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index. |

| | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 3/31/16 | | One Year | | | Since Inception | | | Inception Date |

| | Class A | | | -38.68 | % | | | -9.18 | % | | 3/28/13 |

| | Class C | | | -36.28 | | | | -8.14 | | | 3/28/13 |

| | Institutional | | | -34.88 | | | | -7.10 | | | 3/28/13 |

| | Class IR | | | -34.98 | | | | -7.22 | | | 3/28/13 |

| | | Class R | | | -35.28 | | | | -7.68 | | | 3/28/13 |

| | 3 | | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at net asset value. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the contingent deferred sales charge for Class C Shares (1% if shares are redeemed within 12 months of purchase). Because Institutional, Class IR and Class R Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

7

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Total Annual Fund

Operating

Expenses After

Fee Waiver and

Expense Limitation | | | Total Annual Fund

Operating

Expenses | |

| | Class A | | | 1.43 | % | | | 1.44 | % |

| | Class C | | | 2.18 | | | | 2.19 | |

| | Institutional | | | 1.03 | | | | 1.04 | |

| | Class IR | | | 1.18 | | | | 1.19 | |

| | | Class R | | | 1.70 | | | | 1.71 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least March 30, 2017, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. A deferred tax benefit of 1.80% is not included in the amounts reported in the table above. |

| | | | | | | | |

| | TOP TEN HOLDINGS AS OF 5/31/165 |

| | | Holding | | % of Net Assets | | | Line of Business |

| | Enterprise Products Partners LP | | | 10.6 | % | | Diversified Midstream |

| | Energy Transfer Partners LP | | | 8.2 | | | Diversified Midstream |

| | Magellan Midstream Partners LP | | | 7.4 | | | Liquids, Pipelines & Terminalling |

| | Sunoco Logistics Partners LP | | | 6.3 | | | Liquids, Pipelines & Terminalling |

| | MPLX LP | | | 5.9 | | | Liquids, Pipelines & Terminalling |

| | Buckeye Partners LP | | | 5.5 | | | Liquids, Pipelines & Terminalling |

| | Plains All American Pipeline LP | | | 5.5 | | | Liquids, Pipelines & Terminalling |

| | Williams Partners LP | | | 4.6 | | | Diversified Midstream |

| | Targa Resources Corp. | | | 4.6 | | | General Partner |

| | | Phillips 66 Partners LP | | | 4.1 | | | Liquids, Pipelines & Terminalling |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

8

FUND BASICS

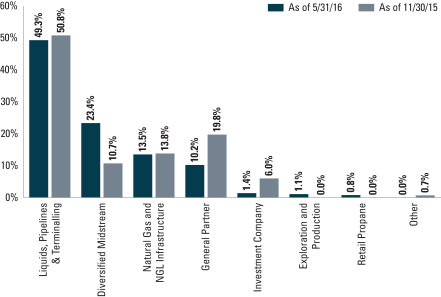

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of total net assets. Sector allocations are defined by GSAM and may differ from sector allocations used by the Alerian Index. |

9

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Schedule of Investments

May 31, 2016 (Unaudited)

| | | | | | | | |

Shares | | | Description | | Value | |

| | Common Stocks – 98.3% | |

| | Diversified Midstream – 23.4% | |

| | 4,980,793 | | | Energy Transfer Partners LP | | $ | 180,603,554 | |

| | 8,344,940 | | | Enterprise Products Partners LP | | | 231,655,534 | |

| | 3,144,654 | | | Williams Partners LP | | | 100,377,356 | |

| | | | | | | | |

| | | | | | | 512,636,444 | |

| | |

| | Exploration and Production – 1.1% | |

| | 1,682,668 | | | Archrock Partners LP | | | 24,011,673 | |

| | |

| | General Partner – 10.2% | |

| | 2,445,018 | | | EQT GP Holdings LP | | | 63,814,970 | |

| | 2,596,110 | | | Plains GP Holdings LP Class A | | | 24,377,473 | |

| | 1,128,748 | | | SemGroup Corp. Class A | | | 35,882,899 | |

| | 2,335,485 | | | Targa Resources Corp. | | | 100,028,822 | |

| | | | | | | | |

| | | | | | | 224,104,164 | |

| | |

| | Liquids, Pipelines & Terminalling – 49.3% | |

| | 1,663,160 | | | Buckeye Partners LP | | | 119,614,467 | |

| | 110,481 | | | Delek Logistics Partners LP | | | 2,915,594 | |

| | 1,565,326 | | | Genesis Energy LP | | | 58,965,830 | |

| | 2,307,930 | | | Magellan Midstream Partners LP | | | 161,670,496 | |

| | 4,074,672 | | | MPLX LP | | | 129,982,037 | |

| | 925,940 | | | NuStar Energy LP | | | 45,528,470 | |

| | 1,632,734 | | | Phillips 66 Partners LP | | | 89,686,079 | |

| | 5,166,235 | | | Plains All American Pipeline LP | | | 119,495,015 | |

| | 2,378,470 | | | Shell Midstream Partners LP | | | 80,273,362 | |

| | 5,009,871 | | | Sunoco Logistics Partners LP | | | 137,520,959 | |

| | 945,868 | | | Sunoco LP | | | 31,374,442 | |

| | 1,254,498 | | | Tesoro Logistics LP | | | 61,658,577 | |

| | 864,693 | | | Valero Energy Partners LP | | | 40,009,345 | |

| | | | | | | | |

| | | | | | | 1,078,694,673 | |

| | |

| | Natural Gas and NGL Infrastructure – 13.5% | |

| | 3,613,935 | | | Antero Midstream Partners LP | | | 88,902,801 | |

| | 894,234 | | | DCP Midstream Partners LP | | | 29,983,666 | |

| | 838,709 | | | EQT Midstream Partners LP | | | 63,213,497 | |

| | 866,955 | | | ONEOK Partners LP | | | 32,900,942 | |

| | 1,796,190 | | | Rice Midstream Partners LP | | | 32,852,315 | |

| | 945,401 | | | Western Gas Partners LP | | | 47,109,332 | |

| | | | | | | | |

| | | | | | | 294,962,553 | |

| | |

| | Other – 0.0% | |

| | 86,600 | | | CSI Compressco LP | | | 795,854 | |

| | |

| | Retail Propane – 0.8% | |

| | 355,891 | | | AmeriGas Partners LP | | | 16,328,279 | |

| | |

| | TOTAL COMMON STOCKS | | | | |

| | (Cost $2,021,090,641) | | $ | 2,151,533,640 | |

| | |

| | | | | | |

Shares | | Rate | | Value | |

| Investment Company(a) – 1.4% | |

Goldman Sachs Financial Square Government Fund – FST Institutional Shares | |

| 31,707,013 | | 0.230% | | $ | 31,707,013 | |

(Cost $31,707,013) | | | | |

| |

| TOTAL INVESTMENTS – 99.7% | |

| (Cost $2,052,797,654) | | $ | 2,183,240,653 | |

| |

| OTHER ASSETS IN EXCESS OF | |

| LIABILITIES – 0.3% | | | 5,963,405 | |

| |

| NET ASSETS – 100.0% | | $ | 2,189,204,058 | |

| |

| | |

| The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. |

(a) | | Represents an affiliated fund. |

| | |

|

Investment Abbreviations: |

GP | | —General Partnership |

LP | | —Limited Partnership |

|

| | |

| 10 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Statement of Assets and Liabilities

May 31, 2016 (Unaudited)

| | | | | | |

| | | | | MLP Energy

Infrastructure Fund | |

| | Assets: | | | | |

| | Investments of unaffiliated issuers, at value (cost $2,021,090,641) | | $ | 2,151,533,640 | |

| | Investments of affiliated issuers, at value (cost $31,707,013) | | | 31,707,013 | |

| | Cash | | | 50,000 | |

| | Receivables: | | | | |

| | Investments sold | | | 14,853,978 | |

| | Fund shares sold | | | 8,243,261 | |

| | Current taxes | | | 6,464,648 | |

| | Dividends | | | 382,601 | |

| | Foreign tax reclaims | | | 306,686 | |

| | Reimbursement from investment adviser | | | 36,316 | |

| | Other assets | | | 7,000 | |

| | Total assets | | | 2,213,585,143 | |

| | | | | | |

| | Liabilities: | | | | |

| | Payables: | | | | |

| | Investments purchased | | | 18,209,796 | |

| | Fund shares redeemed | | | 3,648,785 | |

| | Management fees | | | 1,713,467 | |

| | Distribution and service fees and transfer agent fees | | | 352,406 | |

| | Accrued expenses | | | 456,631 | |

| | Total liabilities | | | 24,381,085 | |

| | | | | | |

| | Net Assets: | | | | |

| | Paid-in capital | | | 2,896,601,150 | |

| | Distributions in excess of net investment loss, net of taxes | | | (31,630,218 | ) |

| | Accumulated net realized loss, net of taxes | | | (806,178,609 | ) |

| | Net unrealized gain, net of taxes | | | 130,411,735 | |

| | | NET ASSETS | | $ | 2,189,204,058 | |

| | | Net Assets: | | | | |

| | | Class A | | $ | 304,310,346 | |

| | | Class C | | | 170,419,163 | |

| | | Institutional | | | 1,613,450,357 | |

| | | Class IR | | | 99,196,692 | |

| | | Class R | | | 1,827,500 | |

| | | Total Net Assets | | $ | 2,189,204,058 | |

| | | Shares Outstanding $0.001 par value (unlimited shares authorized): | | | | |

| | | Class A | | | 40,050,028 | |

| | | Class C | | | 22,998,083 | |

| | | Institutional | | | 209,390,528 | |

| | | Class IR | | | 12,933,585 | |

| | | Class R | | | 242,582 | |

| | | Net asset value, offering and redemption price per share:(a) | | | | |

| | | Class A | | | $7.60 | |

| | | Class C | | | 7.41 | |

| | | Institutional | | | 7.71 | |

| | | Class IR | | | 7.67 | |

| | | Class R | | | 7.53 | |

| | (a) | | Maximum public offering price per share is $8.04. At redemption, Class C Shares may be subject to a contingent deferred sales charge, assessed on the amount equal to the lesser of the current net asset value (“NAV”) or the original purchase price of the shares. |

| | |

| The accompanying notes are an integral part of these financial statements. | | 11 |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Statement of Operations

For the Six Months Ended May 31, 2016 (Unaudited)

| | | | | | |

| | | | | MLP Energy

Infrastructure Fund | |

| | Investment income: | | | | |

| | Dividends — unaffiliated issuers | | $ | 64,541,627 | |

| | Dividends — affiliated issuers | | | 51,960 | |

| | Less: Return of Capital on Dividends | | | (58,422,182 | ) |

| | Total investment income | | | 6,171,405 | |

| | | | | | |

| | Expenses: | | | | |

| | Management fees | | | 8,485,325 | |

| | Distribution and Service fees(a) | | | 1,089,079 | |

| | Transfer Agency fees(a) | | | 734,627 | |

| | Registration fees | | | 156,342 | |

| | Professional fees | | | 125,070 | |

| | Printing and mailing costs | | | 116,893 | |

| | Custody, accounting and administrative services | | | 87,860 | |

| | Trustee fees | | | 15,017 | |

| | Other | | | 103,430 | |

| | Total operating expenses, before taxes | | | 10,913,643 | |

| | Less — expense reductions | | | (75,253 | ) |

| | Net operating expenses, before taxes | | | 10,838,390 | |

| | NET INVESTMENT LOSS, BEFORE TAXES | | | (4,666,985 | ) |

| | Current and deferred tax benefit/(expense)(b) | | | — | |

| | NET INVESTMENT LOSS, NET OF TAXES | | | (4,666,985 | ) |

| | | | | | |

| | Realized and unrealized gain (loss): | | | | |

| | Net realized loss from: | | | | |

| | Investments — unaffiliated issuers | | | (355,797,545 | ) |

| | Investments — affiliated issuers | | | (42,263,856 | ) |

| | Foreign currency transactions | | | (675 | ) |

| | Current and deferred tax benefit/(expense)(b) | | | — | |

| | Net change in unrealized gain on: | | | | |

| | Investments — unaffiliated issuers | | | 493,372,037 | |

| | Investments — affiliated issuers | | | 17,915,913 | |

| | Foreign currency translation | | | 6,040 | |

| | Deferred tax benefit/(expense)(b) | | | — | |

| | Net realized and unrealized gain, net of taxes | | | 113,231,914 | |

| | NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 108,564,929 | |

| | (a) | | Class specific Distribution and Service, and Transfer Agency fees were as follows: |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Distribution and Service Fees | | | Transfer Agency Fees | |

Fund | | Class A | | | Class C | | | Class R | | | Class A | | | Class C | | | Institutional | | | Class IR | | | Class R | |

MLP Energy Infrastructure | | $ | 332,923 | | | $ | 752,476 | | | $ | 3,680 | | | $ | 253,021 | | | $ | 142,970 | | | $ | 253,998 | | | $ | 83,239 | | | $ | 1,399 | |

| | (b) | | Any net tax benefit was fully offset by a 100% valuation allowance recorded as of May 31, 2016. |

| | |

| 12 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Statements of Changes in Net Assets

| | | | | | | | | | |

| | | | | MLP Energy Infrastructure Fund | |

| | | | | For the Six Months Ended

May 31, 2016

(Unaudited) | | | For the Fiscal Year Ended

November 30, 2015 | |

| | From operations: | | | | | | | | |

| | Net investment loss, net of taxes | | $ | (4,666,985 | ) | | $ | (7,211,938 | ) |

| | Net realized loss, net of taxes | | | (398,062,076 | ) | | | (442,720,992 | ) |

| | Net change in unrealized gain (loss), net of taxes | | | 511,293,990 | | | | (423,816,161 | ) |

| | Net increase (decrease) in net assets resulting from operations | | | 108,564,929 | | | | (873,749,091 | ) |

| | | | | | | | | | |

| | Distributions to shareholders: | | | | | | | | |

| | From capital | | | | | | | | |

| | Class A Shares | | | (9,601,137 | ) | | | (20,466,377 | ) |

| | Class C Shares | | | (5,480,677 | ) | | | (11,331,574 | ) |

| | Institutional Shares | | | (46,117,717 | ) | | | (70,394,348 | ) |

| | Class IR Shares | | | (3,112,744 | ) | | | (6,431,628 | ) |

| | Class R Shares | | | (55,674 | ) | | | (26,341 | ) |

| | Total distributions to shareholders | | | (64,367,949 | ) | | | (108,650,268 | ) |

| | | | | | | | | | |

| | From share transactions: | | | | | | | | |

| | Proceeds from sales of shares | | | 1,005,794,188 | | | | 1,690,469,105 | |

| | Reinvestment of distributions | | | 63,025,533 | | | | 107,490,030 | |

| | Cost of shares redeemed | | | (712,151,472 | ) | | | (1,575,166,588 | ) |

| | Net increase in net assets resulting from share transactions | | | 356,668,249 | | | | 222,792,547 | |

| | TOTAL INCREASE (DECREASE) | | | 400,865,229 | | | | (759,606,812 | ) |

| | | | | | | | | | |

| | Net assets: | | | | | | | | |

| | Beginning of period | | | 1,788,338,829 | | | | 2,547,945,641 | |

| | End of period | | $ | 2,189,204,058 | | | $ | 1,788,338,829 | |

| | Distributions in excess of net investment loss, net of taxes | | $ | (31,630,218 | ) | | $ | (26,963,233 | ) |

| | |

| The accompanying notes are an integral part of these financial statements. | | 13 |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Financial Highlights

Selected Data for a Share Outstanding Throughout Each Period

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | From

investment operations | | | Distributions

to shareholders | |

| | | Year - Share Class | | Net asset

value,

beginning

of period | | | Net

investment

income (loss)(a) | | | Net realized

and unrealized

gain (loss) | | | Total from

investment

operations | | | From net

investment

income | | | From

capital | | | Total

distributions | |

| | FOR THE SIX MONTHS ENDED May 31, (UNAUDITED) | |

| | 2016 - A | | $ | 7.62 | | | $ | (0.01 | ) | | $ | 0.23 | | | $ | 0.22 | | | $ | — | | | $ | (0.24 | ) | | $ | (0.24 | ) |

| | 2016 - C | | | 7.46 | | | | (0.04 | ) | | | 0.23 | | | | 0.19 | | | | — | | | | (0.24 | ) | | | (0.24 | ) |

| | 2016 - Institutional | | | 7.70 | | | | (0.02 | ) | | | 0.27 | | | | 0.25 | | | | — | | | | (0.24 | ) | | | (0.24 | ) |

| | 2016 - IR | | | 7.67 | | | | — | (g) | | | 0.24 | | | | 0.24 | | | | — | | | | (0.24 | ) | | | (0.24 | ) |

| | 2016 - R | | | 7.56 | | | | (0.03 | ) | | | 0.24 | | | | 0.21 | | | | — | | | | (0.24 | ) | | | (0.24 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | FOR THE FISCAL YEARS ENDED NOVEMBER 30, | |

| | 2015 - A | | | 11.98 | | | | (0.05 | ) | | | (3.82 | ) | | | (3.87 | ) | | | — | | | | (0.49 | ) | | | (0.49 | ) |

| | 2015 - C | | | 11.83 | | | | (0.12 | ) | | | (3.76 | ) | | | (3.88 | ) | | | — | | | | (0.49 | ) | | | (0.49 | ) |

| | 2015 - Institutional | | | 12.06 | | | | (0.01 | ) | | | (3.86 | ) | | | (3.87 | ) | | | — | | | | (0.49 | ) | | | (0.49 | ) |

| | 2015 - IR | | | 12.04 | | | | (0.03 | ) | | | (3.85 | ) | | | (3.88 | ) | | | — | | | | (0.49 | ) | | | (0.49 | ) |

| | 2015 - R | | | 11.93 | | | | 0.18 | | | | (4.06 | ) | | | (3.88 | ) | | | — | | | | (0.49 | ) | | | (0.49 | ) |

| | 2014 - A | | | 10.81 | | | | (0.08 | ) | | | 1.75 | | | | 1.67 | | | | (0.12 | ) | | | (0.38 | ) | | | (0.50 | ) |

| | 2014 - C | | | 10.76 | | | | (0.15 | ) | | | 1.72 | | | | 1.57 | | | | (0.12 | ) | | | (0.38 | ) | | | (0.50 | ) |

| | 2014 - Institutional | | | 10.84 | | | | (0.01 | ) | | | 1.73 | | | | 1.72 | | | | (0.12 | ) | | | (0.38 | ) | | | (0.50 | ) |

| | 2014 - IR | | | 10.83 | | | | (0.02 | ) | | | 1.73 | | | | 1.71 | | | | (0.12 | ) | | | (0.38 | ) | | | (0.50 | ) |

| | 2014 - R | | | 10.79 | | | | (0.11 | ) | | | 1.75 | | | | 1.64 | | | | (0.12 | ) | | | (0.38 | ) | | | (0.50 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | FOR THE PERIOD ENDED NOVEMBER 30, | |

| | 2013 - A(h) | | | 10.00 | | | | (0.07 | ) | | | 1.27 | | | | 1.20 | | | | — | | | | (0.39 | ) | | | (0.39 | ) |

| | 2013 - C(h) | | | 10.00 | | | | (0.06 | ) | | | 1.21 | | | | 1.15 | | | | — | | | | (0.39 | ) | | | (0.39 | ) |

| | 2013 - Institutional(h) | | | 10.00 | | | | (0.01 | ) | | | 1.24 | | | | 1.23 | | | | — | | | | (0.39 | ) | | | (0.39 | ) |

| | 2013 - IR(h) | | | 10.00 | | | | (0.05 | ) | | | 1.27 | | | | 1.22 | | | | — | | | | (0.39 | ) | | | (0.39 | ) |

| | 2013 - R(h) | | | 10.00 | | | | (0.06 | ) | | | 1.24 | | | | 1.18 | | | | — | | | | (0.39 | ) | | | (0.39 | ) |

| | (a) | | Calculated based on the average shares outstanding methodology. |

| | (b) | | Assumes investment at the NAV at the beginning of the period, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the period and no sales or redemption charges. Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total returns for periods less than one full year are not annualized. |

| | (c) | | Current and deferred tax expense/(benefit) for the ratio calculation is derived from net investment income (loss), and realized and unrealized gains (losses). |

| | (d) | | Current and deferred tax expense/(benefit) for the ratio calculation is derived from net investment income (loss) only. |

| | (e) | | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| | (f) | | Annualized with the exception of tax expenses. |

| | (g) | | Amount is less than $0.005 per share. |

| | (h) | | Commenced operations on March 28, 2013. |

| | |

| 14 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | Ratio of Expenses

to Average Net Assets | | | | | Ratio of Investment income (loss)

to Average Net Assets | | | | | | |

| | | Net asset

value, end

of period | | | | | Total

return(b) | | | | | Net assets,

end of period (in 000s) | | | | | After expense

reimbursements

and tax (benefit)/

expense(c) | | | | | Before expense

reimbursements

and after tax (benefit)/

expense(c) | | | | | Net of expense

reimbursements

and before

tax (benefit)/

expense | | | | | Before expense

reimbursements

and

tax benefit/

(expense) | | | | | After expense

reimbursements

and tax benefit/

(expense)(d) | | | | | Net of expense

reimbursements

and before tax

benefit/

(expense) | | | | | Before expense

reimbursements

and tax benefit/

(expense) | | | | | Portfolio

turnover

rate(e) | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | $ | 7.60 | | | | | | 3.33 | % | | | | $ | 304,310 | | | | | | 1.46 | %(f) | | | | | 1.46 | %(f) | | | | | 1.46 | %(f) | | | | | 1.46 | %(f) | | | | | (0.37 | )%(f) | | | | | (0.37 | )%(f) | | | | | (0.37 | )%(f) | | | | | 55 | % |

| | | 7.41 | | | | | | 2.99 | | | | | | 170,419 | | | | | | 2.21 | (f) | | | | | 2.21 | (f) | | | | | 2.21 | (f) | | | | | 2.21 | (f) | | | | | (1.15 | )(f) | | | | | (1.15 | )(f) | | | | | (1.15 | )(f) | | | | | 55 | |

| | | 7.71 | | | | | | 3.69 | | | | | | 1,613,450 | | | | | | 1.06 | (f) | | | | | 1.06 | (f) | | | | | 1.06 | (f) | | | | | 1.06 | (f) | | | | | (0.51 | )(f) | | | | | (0.51 | )(f) | | | | | (0.52 | )(f) | | | | | 55 | |

| | | 7.67 | | | | | | 3.57 | | | | | | 99,197 | | | | | | 1.21 | (f) | | | | | 1.21 | (f) | | | | | 1.21 | (f) | | | | | 1.21 | (f) | | | | | (0.11 | )(f) | | | | | (0.11 | )(f) | | | | | (0.12 | )(f) | | | | | 55 | |

| | | 7.53 | | | | | | 3.22 | | | | | | 1,828 | | | | | | 1.71 | (f) | | | | | 1.71 | (f) | | | | | 1.71 | (f) | | | | | 1.71 | (f) | | | | | (0.89 | )(f) | | | | | (0.89 | )(f) | | | | | (0.90 | )(f) | | | | | 55 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 7.62 | | | | | | (33.27 | ) | | | | | 292,686 | | | | | | (0.38 | ) | | | | | (0.38 | ) | | | | | 1.42 | | | | | | 1.42 | | | | | | (0.57 | ) | | | | | (0.53 | ) | | | | | (0.54 | ) | | | | | 96 | |

| | | 7.46 | | | | | | (33.79 | ) | | | | | 173,427 | | | | | | 0.37 | | | | | | 0.38 | | | | | | 2.17 | | | | | | 2.18 | | | | | | (1.27 | ) | | | | | (1.23 | ) | | | | | (1.23 | ) | | | | | 96 | |

| | | 7.70 | | | | | | (33.05 | ) | | | | | 1,225,024 | | | | | | (0.78 | ) | | | | | (0.78 | ) | | | | | 1.02 | | | | | | 1.02 | | | | | | (0.10 | ) | | | | | (0.06 | ) | | | | | (0.06 | ) | | | | | 96 | |

| | | 7.67 | | | | | | (33.13 | ) | | | | | 95,825 | | | | | | (0.63 | ) | | | | | (0.63 | ) | | | | | 1.17 | | | | | | 1.17 | | | | | | (0.32 | ) | | | | | (0.28 | ) | | | | | (0.28 | ) | | | | | 96 | |

| | | 7.56 | | | | | | (33.50 | ) | | | | | 1,376 | | | | | | (0.11 | ) | | | | | (0.11 | ) | | | | | 1.69 | | | | | | 1.69 | | | | | | 1.97 | | | | | | 2.01 | | | | | | 2.01 | | | | | | 96 | |

| | | 11.98 | | | | | | 15.59 | | | | | | 513,722 | | | | | | 3.57 | | | | | | 3.57 | | | | | | 1.46 | | | | | | 1.46 | | | | | | (0.56 | ) | | | | | (0.61 | ) | | | | | (0.61 | ) | | | | | 25 | |

| | | 11.83 | | | | | | 14.61 | | | | | | 241,841 | | | | | | 4.32 | | | | | | 4.32 | | | | | | 2.21 | | | | | | 2.21 | | | | | | (1.19 | ) | | | | | (1.24 | ) | | | | | (1.24 | ) | | | | | 25 | |

| | | 12.06 | | | | | | 15.91 | | | | | | 1,613,322 | | | | | | 3.17 | | | | | | 3.17 | | | | | | 1.06 | | | | | | 1.06 | | | | | | (0.06 | ) | | | | | (0.11 | ) | | | | | (0.11 | ) | | | | | 25 | |

| | | 12.04 | | | | | | 15.73 | | | | | | 178,966 | | | | | | 3.32 | | | | | | 3.32 | | | | | | 1.21 | | | | | | 1.21 | | | | | | (0.10 | ) | | | | | (0.15 | ) | | | | | (0.15 | ) | | | | | 25 | |

| | | 11.93 | | | | | | 15.23 | | | | | | 96 | | | | | | 3.82 | | | | | | 3.84 | | | | | | 1.71 | | | | | | 1.73 | | | | | | (0.89 | ) | | | | | (0.93 | ) | | | | | (0.95 | ) | | | | | 25 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 10.81 | | | | | | 12.12 | | | | | | 51,363 | | | | | | 9.36 | (f) | | | | | 9.71 | (f) | | | | | 1.51 | (f) | | | | | 1.86 | (f) | | | | | (1.00 | )(f) | | | | | (1.23 | )(f) | | | | | (1.63 | )(f) | | | | | 96 | |

| | | 10.76 | | | | | | 11.71 | | | | | | 20,112 | | | | | | 10.11 | (f) | | | | | 10.45 | (f) | | | | | 2.26 | (f) | | | | | 2.60 | (f) | | | | | (0.90 | )(f) | | | | | (1.14 | )(f) | | | | | (1.54 | )(f) | | | | | 96 | |

| | | 10.84 | | | | | | 12.53 | | | | | | 206,886 | | | | | | 8.95 | (f) | | | | | 9.50 | (f) | | | | | 1.11 | (f) | | | | | 1.66 | (f) | | | | | (0.17 | )(f) | | | | | (0.40 | )(f) | | | | | (1.03 | )(f) | | | | | 96 | |

| | | 10.83 | | | | | | 12.42 | | | | | | 12,229 | | | | | | 9.11 | (f) | | | | | 9.49 | (f) | | | | | 1.26 | (f) | | | | | 1.64 | (f) | | | | | (0.72 | )(f) | | | | | (0.96 | )(f) | | | | | (1.39 | )(f) | | | | | 96 | |

| | | 10.79 | | | | | | 12.02 | | | | | | 32 | | | | | | 9.59 | (f) | | | | | 10.13 | (f) | | | | | 1.75 | (f) | | | | | 2.29 | (f) | | | | | (0.86 | )(f) | | | | | (1.09 | )(f) | | | | | (1.71 | )(f) | | | | | 96 | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 15 |

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements

May 31, 2016 (Unaudited)

Goldman Sachs Trust (the “Trust”) is a Delaware statutory trust registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company. The Trust includes the Goldman Sachs MLP Energy Infrastructure Fund (the “Fund”). The Fund is a non-diversified portfolio under the Act offering five classes of shares — Class A, Class C, Class IR, Class R and Institutional Shares. Class A Shares are sold with a front-end sales charge of up to 5.50%. Class C Shares are sold with contingent deferred sales charge (“CDSC”) of 1.00%, which is imposed on redemptions made within 12 months of purchase. Institutional, Class IR and Class R are not subject to a sales charge.

Goldman Sachs Asset Management, L.P. (“GSAM”), an affiliate of Goldman, Sachs & Co. (“Goldman Sachs”), serves as investment adviser to the Fund pursuant to a management agreement (“Agreement”) with the Trust.

|

| 2. SIGNIFICANT ACCOUNTING POLICIES |

The financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) and require management to make estimates and assumptions that may affect the reported amounts and disclosures. Actual results may differ from those estimates and assumptions.

A. Investment Valuation — The Fund’s valuation policy is to value investments at fair value.

B. Investment Income and Investments — Investment income includes interest income and dividend income, net of any foreign withholding taxes, less any amounts reclaimable. Interest income is accrued daily and adjusted for amortization of premiums and accretion of discounts. Dividend income is recognized on ex-dividend date or, for certain foreign securities, as soon as such information is obtained subsequent to the ex-dividend date. Investment transactions are reflected on trade date. Realized gains and losses are calculated using identified cost. Investment transactions are recorded on the following business day for daily net asset value (“NAV”) calculations. Distributions from master limited partnerships (“MLPs”) are generally recorded based on the characterization reported on the Fund’s schedule K-1 received from the MLPs. The Fund records its pro-rata share of the income/loss and capital gains/losses, allocated from the underlying partnerships and adjusts the cost basis of the underlying partnerships accordingly.

C. Class Allocations and Expenses — Investment income, realized and unrealized gain (loss), and non-class specific expenses of the Fund are allocated daily based upon the proportion of net assets of each class. Non-class specific expenses directly incurred by a Fund are charged to the Fund, while such expenses incurred by the Trust are allocated across the applicable Funds on a straight-line and/or pro-rata basis depending upon the nature of the expenses. Class specific expenses, where applicable, are borne by the respective share classes and include Distribution and Service, Transfer Agency and Service and Shareholder Administration fees.

D. Distributions to Shareholders — Over the long term, the Fund makes distributions to its shareholders each fiscal quarter at a rate that is approximately equal to the distributions the Fund receives from the MLPs and other securities in which it invests. To permit the Fund to maintain more stable quarterly distributions, the distribution for any particular quarterly period may be more or less than the amount of total investment income actually earned by the Fund. The Fund estimates that only a portion of the distributions paid to shareholders will be treated as income. The remaining portion of the Fund’s distribution, which may be significant, is expected to be a return of capital. These estimates are based on the Fund’s operating results during the period, and their final federal income tax characterization may differ.

The characterization of distributions to shareholders for financial reporting purposes is determined in accordance with federal income tax rules, which may differ from GAAP. Certain components of the Fund’s net assets on the Statement of Assets and Liabilities reflect permanent GAAP/Tax differences based on the appropriate tax character.

16

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

|

| 2. SIGNIFICANT ACCOUNTING POLICIES (continued) |

E. Income Taxes — The Fund does not intend to qualify as a regulated investment company pursuant to Subchapter M of the Internal Revenue Code of 1986, as amended, but will rather be taxed as a corporation. As a result, the Fund is obligated to pay federal, state and local income tax on its taxable income. The Fund invests primarily in MLPs, which generally are treated as partnerships for federal income tax purposes. As a limited partner in the MLPs, the Fund must report its allocable share of the MLPs’ taxable income or loss in computing its own taxable income or loss. The Fund’s tax expense or benefit is included in the Statement of Operations based on the component of income or gains/losses to which such expense or benefit relates. Deferred income taxes reflect the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. Such temporary differences are principally: (i) taxes on unrealized gains/losses, which are attributable to the temporary difference between fair market value and tax basis, (ii) the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting and income tax purposes, and (iii) the net tax benefit of accumulated net operating losses and capital loss carryforwards. The Fund will accrue a deferred income tax liability balance, at the currently effective statutory United States (“U.S.”) federal income tax rate (currently 35%) plus an estimated state and local income tax rate, for its future tax liability associated with the capital appreciation of its investments and the distributions received by the Fund on interests of MLPs considered to be return of capital and for any net operating gains. The Fund may also record a deferred tax asset balance, which reflects an estimate of the Fund’s future tax benefit associated with net operating losses and/or unrealized losses.

To the extent the Fund has a deferred tax asset, consideration is given to whether or not a valuation allowance, which would offset the value of some or all of the deferred tax asset balance, is required. A valuation allowance is required if based on the evaluation criterion provided by Accounting Standards Codification (“ASC”) 740, Income Taxes (ASC 740) it is more likely than not that some portion, or all, of the deferred tax asset will not be realized. The factors considered in assessing the Fund’s valuation allowance include: the nature, frequency and severity of current and cumulative losses, the duration of the statutory carryforward periods and the associated risks that operating and capital loss carryforwards may expire unutilized. From time to time, as new information becomes available, the Fund will modify its estimates or assumptions regarding the deferred tax liability or asset. Unexpected significant decreases in cash distributions from the Fund’s MLP investments or significant declines in the fair value of its investments may change the Fund’s assessment regarding the recoverability of their deferred tax assets and may result in a valuation allowance. If a valuation allowance is required to reduce any deferred tax asset in the future, it could have a material impact on the Fund’s NAV and results of operations in the period it is recorded. The Fund will rely to some extent on information provided by MLPs, which may not be provided to the Fund on a timely basis, to estimate operating income/loss and gains/losses and current taxes and deferred tax liabilities and/or asset balances for purposes of daily reporting of NAVs and financial statement reporting.

It is the Fund’s policy to classify interest and penalties associated with underpayment of federal and state income taxes, if any, as income tax expense on its Statement of Operations. The Fund anticipates filing income tax returns in the U.S. federal jurisdiction and various states, and such returns are subject to examination by the tax jurisdictions. The Fund has reviewed all major jurisdictions and concluded that there is no significant impact on its net assets and no tax liability resulting from unrecognized tax benefits or expenses relating to uncertain tax positions expected to be taken on its tax returns.

Return of Capital Estimates — Distributions received from the Fund’s investments in MLPs generally are comprised of income and return of capital. The Fund records investment income and return of capital based on estimates made at the time such distributions are received. Such estimates are based on historical information available from each MLP and other industry sources. These estimates may subsequently be revised based on information received from MLPs after their tax reporting periods are concluded.

17

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements (continued)

May 31, 2016 (Unaudited)

|

| 2. SIGNIFICANT ACCOUNTING POLICIES (continued) |

F. Foreign Currency Translation — The accounting records and reporting currency of the Fund is maintained in U.S. dollars. Assets and liabilities denominated in foreign currencies are translated into U.S. dollars using the current exchange rates at the close of each business day. The effect of changes in foreign currency exchange rates on investments is included within net realized and unrealized gain (loss) on investments. Changes in the value of other assets and liabilities as a result of fluctuations in foreign exchange rates are included in the Statement of Operations within net change in unrealized gain (loss) on foreign currency translations. Transactions denominated in foreign currencies are translated into U.S. dollars on the date the transaction occurred, the effects of which are included within net realized gain (loss) on foreign currency transactions.

|

| 3. INVESTMENTS AND FAIR VALUE MEASUREMENTS |

The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). The levels used for classifying investments are not necessarily an indication of the risk associated with investing in these investments. The three levels of the fair value hierarchy are described below:

Level 1 — Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities;

Level 2 — Quoted prices in markets that are not active or financial instruments for which significant inputs are observable (including, but not limited to, quoted prices for similar investments, interest rates, foreign exchange rates, volatility and credit spreads), either directly or indirectly;

Level 3 — Prices or valuations that require significant unobservable inputs (including GSAM’s assumptions in determining fair value measurement).

Changes in valuation techniques may result in transfers into or out of an assigned level within the hierarchy. In accordance with the Fund’s policy, transfers between different levels of the fair value hierarchy resulting from such changes are deemed to have occurred as of the beginning of the reporting period.

The Board of Trustees (“Trustees”) has approved Valuation Procedures that govern the valuation of the portfolio investments held by the Fund, including investments for which market quotations are not readily available. The Trustees have delegated to GSAM day-to-day responsibility for implementing and maintaining internal controls and procedures related to the valuation of the Fund’s portfolio investments. To assess the continuing appropriateness of pricing sources and methodologies, GSAM regularly performs price verification procedures and issues challenges as necessary to third party pricing vendors or brokers, and any differences are reviewed in accordance with the Valuation Procedures.

A. Level 1 and Level 2 Fair Value Investments — The valuation techniques and significant inputs used in determining the fair values for investments classified as Level 1 and Level 2 are as follows:

Equity Securities — Equity securities traded on a United States (“U.S.”) securities exchange or the NASDAQ system, or those located on certain foreign exchanges, including but not limited to the Americas, are valued daily at their last sale price or official closing price on the principal exchange or system on which they are traded. If there is no sale or official closing price or such price is believed by GSAM to not represent fair value, equity securities are valued at the last bid price for long positions and at the last ask price for short positions. To the extent these investments are actively traded, they are classified as Level 1 of the fair value hierarchy, otherwise they are generally classified as Level 2.

18

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

|

| 3. INVESTMENTS AND FAIR VALUE MEASUREMENTS (continued) |

Unlisted equity securities for which market quotations are available are valued at the last sale price on the valuation date, or if no sale occurs, at the last bid price.

Private Investments in Public Equities — Private investments in public equities (“PIPEs”) are valued the same as other equity securities as noted above. A Liquidity Value Adjustment (LVA) may be applied to securities which are subject to externally imposed and legally enforceable trading restrictions or which convert to publicly traded securities in the future when certain conditions are met. An LVA is a discount to the market price of an issuer’s common stock, which is based on the length of the lock-up time period and volatility of the underlying security. PIPEs are classified as Level 2 until such time as the transfer restriction is removed.

Money Market Funds — Investments in the Goldman Sachs Financial Square Government Fund (“Underlying Fund”) are valued at the NAV of the FST Institutional Share class on the day of valuation. These investments are generally classified as Level 1 of the fair value hierarchy. For information regarding an Underlying Fund’s accounting policies and investment holdings, please see the Underlying Fund’s shareholder report.

B. Level 3 Fair Value Investments — To the extent that significant inputs to valuation models and other alternative pricing sources are unobservable, or if quotations are not readily available, or if GSAM believes that such quotations do not accurately reflect fair value, the fair value of the Fund’s investments may be determined under Valuation Procedures approved by the Trustees. GSAM, consistent with its procedures and applicable regulatory guidance, may make an adjustment to the most recent valuation prices of either domestic or foreign securities in light of significant events to reflect what it believes to be the fair value of the securities at the time of determining a Fund’s NAV. Significant events which could affect a large number of securities in a particular market may include, but are not limited to: significant fluctuations in U.S. or foreign markets; market dislocations; market disruptions; or unscheduled market closings. Significant events which could also affect a single issuer may include, but are not limited to: corporate actions such as reorganizations, mergers and buy-outs; ratings downgrades; and bankruptcies.

Fair Value Hierarchy — The following is a summary of the Fund’s investments classified in the fair value hierarchy as of May 31, 2016:

| | | | | | | | | | | | |

| | | |

| Investment Type | | Level 1 | | | Level 2 | | | Level 3 | |

| Assets | | | | | | | | | | | | |

Common Stocks(a) | | | | | | | | | | | | |

North America | | $ | 2,151,533,640 | | | $ | — | | | $ | — | |

Investment Company | | | 31,707,013 | | | | — | | | | — | |

| Total | | $ | 2,183,240,653 | | | $ | — | | | $ | — | |

| (a) | | Amounts are disclosed by continent to highlight the impact of time zone differences between local market close and the calculation of NAV. Security valuations are based on the principal exchange or system on which they are traded, which may differ from country of domicile noted in table. |

For further information regarding security characteristics, see the Schedule of Investments.

Currently, the highest marginal federal income tax rate for a corporation is 35%. The Fund may also be subject to a 20% alternative minimum tax to the extent that its alternative minimum tax exceeds its regular federal income tax. Total income taxes are computed by applying the federal statutory rate plus a blended state income tax rate. During the period ended May 31, 2016, the Fund re-evaluated its blended state income tax rate, decreasing the rate from 2.01% to 1.80% due to anticipated decrease of state apportionment of income and gains.

19

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements (continued)

May 31, 2016 (Unaudited)

The reconciliation between the federal statutory income tax rate of 35% and the effective tax rate on net investment income/loss and realized and unrealized gain/loss is as follows:

| | | | | | | | |

| | |

| Description | | Amount | | | Rate | |

Application of statutory income tax rate | | $ | 37,997,725 | | | | 35.00 | % |

State income taxes, net of federal benefit | | | 1,954,169 | | | | 1.80 | |

Effect of permanent differences | | | (1,619,606 | ) | | | (1.49 | ) |

Change in estimated state tax rate, net of federal tax benefit (expense) | | | 1,698,179 | | | | 1.56 | |

Other adjustments | | | 724,572 | | | | 0.68 | |

Valuation allowance | | | (40,755,039 | ) | | | (37.55 | ) |

Total current and deferred income tax expense/(benefit), net | | $ | — | | | | 0.00 | % |

At May 31, 2016, components of the Fund’s deferred tax assets and liabilities are as follows:

| | | | |

| | | | |

| Deferred tax assets: | | | | |

Net operating loss carryforward — see table below for expiration | | $ | 37,304,254 | |

Capital loss carryforward (tax basis) — see table below for expiration | | | 259,741,169 | |

Valuation allowance | | | (259,170,793 | ) |

Total Deferred Tax Assets | | $ | 37,874,630 | |

| Deferred tax liabilities: | | | | |

Net unrealized gains on investment securities (tax basis) | | $ | (16,081,758 | ) |

Income recognized from MLP investments | | | (20,462,703 | ) |

Other tax liabilities | | | (1,330,169 | ) |

Total Deferred Tax Liabilities | | $ | (37,874,630 | ) |

At May 31, 2016 the Fund had net operating loss carryforwards which may be carried forward for 20 years, as follows:

| | | | | | | | |

| From Fiscal Year Ended | | Amount | | | Expiration | |

November 30, 2016 | | $ | 101,370,254 | | | | November 30, 2036 | |

At May 31, 2016 the Fund had capital loss carryforwards, which may be carried forward for 5 years, as follows:

| | | | | | | | |

| From Fiscal Year Ended | | Amount | | | Expiration | |

November 30, 2015 | | $ | 438,692,023 | | | | November 30, 2020 | |

November 30, 2016 | | | 267,132,410 | | | | November 30, 2021 | |

The Fund reviews the recoverability of its deferred tax assets based upon the weight of the available evidence. When assessing, the Fund’s management considers available carrybacks, reversing temporary taxable differences, and tax planning, if any. As a result of its analysis of the recoverability of its deferred tax assets, the Fund recorded $259,170,793 of valuation allowance, which represents 100% of the net deferred tax asset as of May 31, 2016.

20

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

For the six months ended May 31, 2016, components of the Fund’s current and deferred tax benefit are as follows:

| | | | | | | | | | | | |

| | | Current | | | Deferred | | | Total | |

Federal | | $ | — | | | $ | 37,198,352 | | | $ | 37,198,352 | |

State | | $ | — | | | $ | 3,556,687 | | | $ | 3,556,687 | |

Valuation Allowance | | $ | — | | | $ | (40,755,039 | ) | | $ | (40,755,039 | ) |

Total | | $ | — | | | $ | — | | | $ | — | |

For the six months ended May 31, 2016, the Fund does not have any interest or penalties associated with the underpayment of any income taxes. At May 31, 2016, gross unrealized appreciation and depreciation of investments, based on cost, for federal income tax purposes was as follows:

| | | | |

| | | | |

Tax Cost | | $ | 2,052,228,041 | |

Gross unrealized gain | | | 229,855,068 | |

Gross unrealized loss | | | (130,549,469 | ) |

Net unrealized security gain | | $ | 99,305,599 | |

Any difference between cost amounts for financial statement and federal income tax purposes is due primarily to timing differences related to the tax treatment of partnership investments. For the six months ended May 31, 2016, GSAM estimates that 100% of the MLP distributions received will be treated as a return of capital.

For the six months ended May 31, 2016, the Fund distributions are estimated to be comprised of 100% return of capital. Shareholders will be informed of the final tax characterization of the distributions in February 2017. The Fund’s first three years are open for examination by U.S. and state tax authorities. Management of the Fund is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits or expenses will significantly change in the next 12 months.

|

| 5. AGREEMENTS AND AFFILIATED TRANSACTIONS |

A. Management Agreement — Under the Agreement, GSAM manages the Fund, subject to the general supervision of the Trustees.

As compensation for the services rendered pursuant to the Agreement, the assumption of the expenses related thereto and administration of the Fund’s business affairs, including providing facilities, GSAM is entitled to a management fee, accrued daily and paid monthly, equal to an annual percentage rate of the Fund’s average daily net assets.

For the six months ended May 31, 2016, contractual and effective net management fee with GSAM were at the following rates:

| | | | | | | | | | | | | | | | | | | | | | |

Contractual Management Rate | |

First $1 billion | | | Next $1 billion | | | Next $3 billion | | | Next $3 billion | | | Over $8 billion | | | Effective Rate^ | |

| | 1.00% | | | | 0.90% | | | | 0.86% | | | | 0.84% | | | | 0.82% | | | | 0.94% | * |

| ^ | | Effective Net Management Rate includes the impact of management fee waivers of affiliated underlying funds, if any. |

| * | | GSAM has agreed to waive a portion of its management fee payable by the Fund in an amount equal to any management fees it earns as an investment adviser to any of the affiliated funds in which the Fund invests. The management fee waiver will remain in effect through at least March 30, 2017. Prior to such date, GSAM may not terminate the arrangement without the approval of the Trustees. |

21

GOLDMAN SACHS MLP ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements (continued)

May 31, 2016 (Unaudited)

|

| 5. AGREEMENTS AND AFFILIATED TRANSACTIONS (continued) |

The Goldman Sachs MLP Energy Infrastructure Fund invests in FST Shares of the Goldman Sachs Financial Square Government Fund, which is an affiliated Underlying Fund. GSAM has agreed to waive a portion of its management fee payable by the Fund in an amount equal to the management fee it earns as an investment adviser to any of the affiliated Underlying Funds in which the Fund invests. For the six months ended May 31, 2016, GSAM waived $38,937 of the Fund’s management fee.

B. Distribution and Service Plans — The Trust, on behalf of the Fund, has adopted Distribution and Service Plans (the “Plans”). Under the Plans, Goldman Sachs, which serves as distributor (the “Distributor”), is entitled to a fee accrued daily and paid monthly, for distribution services and personal and account maintenance services, which may then be paid by Goldman Sachs to authorized dealers, at the following annual rates calculated on the Fund’s average daily net assets of each respective share class:

| | | | | | | | | | | | |

| | | Distribution and Service Plan Rates | |

| | | Class A* | | | Class C | | | Class R* | |

Distribution Plan | | | 0.25 | % | | | 0.75 | % | | | 0.50 | % |

Service Plan | | | — | | | | 0.25 | | | | — | |