Exhibit 17(b)

Goldman Sachs Funds

| Annual Report | August 31, 2016 | |||

Fundamental Equity Growth Funds | ||||

Capital Growth | ||||

Concentrated Growth | ||||

Dynamic U.S. Equity | ||||

Flexible Cap Growth | ||||

Focused Growth | ||||

Growth Opportunities | ||||

Small/Mid Cap Growth | ||||

Strategic Growth | ||||

Technology Opportunities | ||||

Goldman Sachs Fundamental Equity Growth Funds

| ∎ | CAPITAL GROWTH |

| ∎ | CONCENTRATED GROWTH |

| ∎ | DYNAMIC U.S. EQUITY |

| ∎ | FLEXIBLE CAP GROWTH |

| ∎ | FOCUSED GROWTH |

| ∎ | GROWTH OPPORTUNITIES |

| ∎ | SMALL/MID CAP GROWTH |

| ∎ | STRATEGIC GROWTH |

| ∎ | TECHNOLOGY OPPORTUNITIES |

TABLE OF CONTENTS |

| |||

| 3 | ||||

| 4 | ||||

| 6 | ||||

| 69 | ||||

| 86 | ||||

| 96 | ||||

| 114 | ||||

| 134 | ||||

| 135 | ||||

| NOT FDIC-INSURED | May Lose Value | No Bank Guarantee | ||

GOLDMAN SACHS FUNDAMENTAL EQUITY GROWTH FUNDS

What Differentiates the Goldman Sachs Growth Team’s Investment Process?

For over 30 years, the Goldman Sachs Growth Team has consistently applied a three-step investment process based on our belief that wealth is created through the long-term ownership of growing businesses.

| ∎ | Make decisions as long-term business owners rather than as stock traders |

| ∎ | Perform in-depth, fundamental research |

| ∎ | Focus on long-term structural and competitive advantages |

Result

Performance driven by the compounding growth of businesses over time — not short-term market movements

Long-term participation in growing businesses — less reliance on macroeconomic predictions, market timing, sector rotation or momentum

Identify high quality growth businesses. Some required investment criteria include:

| ∎ | Established brand names |

| ∎ | Dominant market shares |

| ∎ | Pricing power |

| ∎ | Recurring revenue streams |

| ∎ | Free cash flow |

| ∎ | Long product life cycles |

| ∎ | Favorable long-term growth prospects |

| ∎ | Excellent management |

Result

Investments in businesses that we believe are strategically positioned for consistent, sustainable long-term growth

| ∎ | Perform rigorous valuation analysis of every potential investment |

| ∎ | Use valuation tools and analytics to ensure that the high-quality business franchises we have identified also represent sound investments |

Result

Good investment decisions based on solid understanding of what each business is worth

Attractive buying opportunities as the stock prices of quality growth businesses fluctuate over time

3

MARKET REVIEW

Goldman Sachs Fundamental Equity Growth Funds

Overall, U.S. equities rallied during the 12 months ended August 31, 2016 (the “Reporting Period”), even amidst persistent volatility. The Standard & Poor’s 500® Index (the “S&P 500 Index”) ended the Reporting Period with a gain of 12.55%. The Russell 3000® Index generated a return of 11.44%.

Following a volatile summer, U.S. equities tumbled further in September 2015, alongside other global equity markets, before rebounding strongly in October 2015 and then finishing November 2015 roughly flat. In December 2015, the Federal Reserve (the “Fed”) finally delivered, as largely expected by markets, and voted unanimously for a 25 basis point hike in the targeted federal funds rate, its first rate hike since 2006. (A basis point is 1/100th of a percentage point.) The fairly dovish language in the Fed’s announcement, which reemphasized “gradual” adjustments to policy going forward, helped to somewhat assuage the markets (Dovish language or action tends to suggest lower interest rates (opposite of hawkish)).

Early in 2016, however, U.S. equities were embroiled in what was a global rout, triggered by investor concerns of an intensifying economic slowdown in China and exacerbated by a plunge in oil prices to less than $30 per barrel, the lowest level since 2003. The Fed’s statement in January 2016 acknowledged the risks from international markets and tightening financial conditions on the U.S. economy. U.S. equities stabilized somewhat in February 2016, as market sentiment appeared to improve on the more dovish tone set by global central banks. U.S. equities were also supported during the month by strong U.S. economic data, rallying as fourth quarter 2015 Gross Domestic Product (“GDP”) came in above market expectations. In March 2016, the Fed kept interest rates on hold and surprised on the dovish side, reducing its forecast to two interest rate increases in 2016, down from four. Along with receding global economic concerns, this helped drive a recovery in U.S. equities.

Following the rebound in March 2016, market sentiment remained sanguine in April 2016, as oil prices rose and Chinese economic growth concerns abated. U.S. equities fell near the end of the month, as investors were disappointed by a lack of additional stimulus from the Bank of Japan and by a weaker than consensus expected first quarter 2016 U.S. GDP growth of 0.5%. In May 2016, weaker payroll data drove expectations for a Fed hike in June 2016 temporarily lower, but subsequent hawkish Fed minutes revived market expectations (Hawkish language or action tends to suggest higher interest rates (opposite of dovish)). The Fed ultimately held interest rates steady in June 2016 and signaled a slower pace of hikes, acknowledging the slowdown in the labor market. Equity markets were otherwise dominated in June 2016 by the U.K. referendum on whether to leave the European Union, popularly known as Brexit. U.S. equities sold off in the global risk-off sentiment that dominated toward the end of June 2016 in the days following the surprise “leave” result. However, global equity markets rather quickly rebounded owing to a combination of improving risk sentiment as markets digested the outcome and on dovish remarks from the Bank of England’s Governor Carney.

U.S. equities were further buoyed by strong economic data and corporate earnings in July 2016, despite increased uncertainty post-Brexit. Growth in U.S. non-farm payrolls reached an eight-month high in June 2016, suggesting that the especially weak May 2016 reading had been an outlier in an otherwise strong job market. Such market sentiment was substantiated in August 2016, as payrolls data, released for July 2016, surprised to the upside for a second consecutive month. In her Jackson Hole speech toward the end of August, Fed Chair Janet Yellen acknowledged that the case for an interest rate hike had strengthened in recent months. Along with strong labor data and other recent hawkish comments from the Fed, this

4

MARKET REVIEW

significantly increased the market-implied probability of an interest rate hike by year-end 2016, causing U.S. equities to sell off and finish the month of August roughly flat.

For the Reporting Period overall, all market capitalizations posted solid positive returns, but large-cap companies performed best, followed by mid-cap companies and then small-cap companies. Value stocks significantly outpaced growth stocks across the capitalization spectrum of the U.S. equity market. (All as measured by Russell Investments indices.)

Looking Ahead

At the end of the Reporting Period, low economic growth, interest rates and visibility (or the extent to which a future situation is predictable) reinforced our expectations of lower than average U.S. equity returns. Brexit led to downward revisions to economic growth forecasts for the U.K. and Europe, and the risk of a U.K. recession increased, in our view. As a result, we expect central bank policy around the world to remain accommodative, keeping interest rates lower for longer.

That said, we believe U.S. equities can still post positive returns for calendar year 2016, driven by earnings growth. In our view, equities remain attractive in this environment, as other asset classes are likely to offer lower returns. Cash is likely to yield almost nothing for the foreseeable future, and government bond yields are likely to be at low or negative levels in major markets, in our view. The lack of yield in fixed income markets suggests to us that stocks with sustainable dividends and real estate investment trusts (“REITs”) may well continue to command a premium.

We believe economic and corporate fundamentals are still strongest in the U.S. Unemployment remains below 5%; job growth rebounded in the summer months; and home prices continued to rise. At the end of the Reporting Period, credit trends were benign (benign credit trends tend to suggest low risk of rising default rates), and oil prices seemingly stabilized. We believe stronger fundamentals and less uncertainty relative to other regions are likely to attract asset flows and buoy near-term U.S. equity performance. Still, we are on alert for anything that calls this view into question. In the intermediate term, a confluence of factors may be creating a more challenging environment for absolute returns. More specifically, at the end of the Reporting Period, the valuation of the S&P 500 Index remained high; the index level itself was near fresh highs; and some earnings headwinds persisted.

Regardless of market direction, our fundamental, bottom-up stock selection continues to drive our process, rather than headlines or sentiment. We maintain high conviction in the companies the Funds own and believe they have the potential to outperform relative to the broader market regardless of economic growth conditions. As always, we maintain our focus on seeking companies that we believe will generate long-term growth in today’s ever-changing market conditions.

5

PORTFOLIO RESULTS

Goldman Sachs Capital Growth Fund

Portfolio Composition

The Fund invests primarily in U.S. equity investments. Since the Fund’s inception, the Goldman Sachs Growth Equity Investment Team has focused on several key investment criteria that it believes can drive a company’s growth over the long term. These characteristics are: dominant market share, established brand name, pricing power, recurring revenue stream, free cash flow, high returns on invested capital, predictable growth, sustainable growth, long product life cycle, enduring competitive advantage, favorable demographic trends and excellent management. The Team strives to purchase these companies at reasonable valuations in order to capture the full benefits of their growth.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Growth Equity Investment Team discusses the Goldman Sachs Capital Growth Fund’s (the “Fund”) performance and positioning for the 12-month period ended August 31, 2016 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, C, Institutional, Service, IR, R and R6 Shares generated average annual total returns, without sales charges, of 5.79%, 4.98%, 6.19%, 5.66%, 6.05%, 5.51% and 6.19%, respectively. These returns compare to the 10.51% average annual total return of the Fund’s benchmark, the Russell 1000® Growth Index (with dividends reinvested) (the “Russell Index”), during the same period. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | The Fund posted solid absolute gains, but stock selection overall detracted from the Fund’s performance relative to the Russell Index during the Reporting Period. Sector allocation as a whole also detracted, albeit much more modestly. |

| Q | Which equity market sectors most significantly affected Fund performance? |

| A | Detracting from the Fund’s relative results most was weak stock selection in the health care, consumer staples and information technology sectors. The sectors that contributed most positively to the Fund’s relative performance during the Reporting Period were financials, materials and energy, wherein effective stock selection drove results. |

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | Among those stocks detracting most from the Fund’s results relative to the Russell Index were positions in global apparel company PVH, biotechnology firm Vertex Pharmaceuticals and global pharmaceutical company Allergan. |

| PVH was the top detractor from the Fund’s results during the Reporting Period. Weakness in the U.S. retail environment, high promotions in the industry, and currency headwinds added pressure to what we believe is otherwise a high quality company. While we continue to monitor the situation closely, at the end of the Reporting Period, we believed PVH remains a leading franchise with dominant market share, strong pricing power and solid fundamentals. We remained optimistic on what we see as the company’s significant free cash flow generation ability, quality of management and return potential. |

Vertex Pharmaceuticals was a top detractor from the Fund’s performance during the Reporting Period. Early in 2016, its shares came under pressure following a disappointing fiscal fourth quarter that fell short of consensus expectations. Additionally, lowered expectations surrounding the launch of Vertex Pharmaceuticals’ new cystic fibrosis treatment, orkambi, caused shares to decline. Despite this weakness, at the end of the Reporting Period, we believed Vertex Pharmaceuticals had strong underlying fundamentals, a promising product pipeline with significant short-term and long-term catalysts and an attractive valuation. We further believed the company, led by what we consider to be a capable management team, could continue to see growth given its dominant market share in its space and given |

6

PORTFOLIO RESULTS

geographic expansionary efforts that have contributed to meaningful profitability. |

| Allergan was among the Fund’s biggest detractors during the Reporting Period. Volatility related to mergers and acquisitions the company has been involved in as well as market concerns around drug pricing pressures weighed on Allergan’s stock during the Reporting Period. Despite the near-term volatility and underperformance, we continued to believe at the end of the Reporting Period that Allergan was a high quality growth business, trading at an attractive valuation with meaningful financial flexibility going forward. |

| Q | What were some of the Fund’s best-performing individual stocks? |

| A | Among those stocks the Fund benefited most from relative to the Russell Index were positions in specialty retailers Ulta Salon, Cosmetics & Fragrance, data center real estate investment trust (“REIT”) Equinix and water technology company Xylem. |

| After a challenging start to 2016 for Ulta Salon, Cosmetics & Fragrance, momentum started picking up for the company in the beginning of April 2016 after strong first quarter 2016 earnings and the company being added to the S&P 500 Index. Its strong results were driven by margins, revenues and e-commerce growth that were ahead of market expectations. In our view, the company is a strong brand that continues to gain recognition. We believe Ulta Salon, Cosmetics & Fragrance has an opportunity to grow market share through higher brand awareness, increasing loyalty to existing stores, expansion of new stores and e-commerce. |

| Equinix was a strong contributor to the Fund’s performance during the Reporting Period. The company reported solid quarterly results, positively beating market expectations for its organic revenue growth and earnings growth. The company also benefited from a move down in U.S. Treasury yields, which generally favors REITs given their attractive yield and growth potential relative to bonds. At the end of the Reporting Period, we thought that Equinix continued to have substantial pipeline opportunities, particularly with enterprise customers willing to pay a higher price. Continued integration with the company’s Telecity acquisition and a strategic partnership with Datang Telecom could further increase Equinix’s global presence and strengthen its competitive advantage, in our view. Further, we believe Equinix remains an asset with robust upside to its revenues and free cash flows, as it balances organic growth, low leverage and a sound capital structure. |

| During the Reporting Period, Xylem reported strong quarterly results, and toward the end of the Reporting Period, announced the purchase of Sensus, a smart water meter company, for approximately $1.7 billion in cash. The acquisition was viewed positively by investors, as it further bolsters Xylem’s product offering and technological advantage. At the end of the Reporting Period, we remained optimistic on Xylem’s margin expansion prospects and believed its management team has done well to position the company for sustainable long-term growth. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, we did not use derivatives as part of an active management strategy. |

| Q | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | We initiated a Fund position in fast-food retail giant McDonald’s. We believe improving sales and reductions in costs should lead to earnings upside and margin expansion. We further think that McDonald’s reduction in capital expenditures and further refranchising could lead to improving return on invested capital and free up additional capital to repurchase stock. In our view, McDonald’s is a high quality franchise with a proficient management team and what we consider to be attractive opportunities to drive top-line growth and earnings. |

| We established a Fund position in off-price retailer Ross Stores. Off-price retailers, such as Ross Stores, seek to take advantage of excess inventory from full-price retailers by purchasing goods at a significant discount to their original prices. We believe Ross Stores is well positioned within its industry and attractively valued for a high quality company. We are encouraged by Ross Stores’ consistent sales and earnings growth over time, strong free cash flows, and demonstrated track record of returning capital to shareholders. |

Conversely, we sold the Fund’s position in consumer products company Colgate-Palmolive. While we believe Colgate-Palmolive to be a quality business, we think there are better opportunities with more encouraging catalysts elsewhere in the industry. Additionally, we believe it is possible that Colgate-Palmolive could see an earnings |

7

PORTFOLIO RESULTS

decrease in the near term, as foreign currency pressures continue to impact the company. As a result, we decided to exit the position and pursue higher conviction ideas. |

| We sold the Fund’s position in Biogen, a biotechnology company. Like most companies within the health care sector, Biogen faced headwinds from increased U.S. regulation and felt increasing pressure after announcing a divestiture of its hemophilia business. At the beginning of June 2016, Biogen saw a notable decline in its share price after opicinumab, a drug for multiple sclerosis, missed an essential endpoint of its Phase II clinical trial. We sold the Fund’s position in Biogen, as we believe the stock is in deceleration mode. |

| Q | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | In constructing the Fund’s portfolio, we focus on picking stocks rather than on making industry or sector bets. We seek to outpace the benchmark index by overweighting stocks that we expect to outperform and underweighting those that we think may lag. Consequently, changes in its sector weights are generally the direct result of individual stock selection or of stock appreciation or depreciation. That said, during the Reporting Period, the Fund’s exposure to consumer staples and information technology increased and its allocations to consumer discretionary and financials decreased relative to the Russell Index. |

| Q | How was the Fund positioned relative to its benchmark index at the end of August 2016? |

| A | At the end of August 2016, the Fund had an overweighted position relative to the Russell Index in the consumer discretionary sector. On the same date, the Fund had an underweighted position compared to the Russell Index in health care. The Fund was rather neutrally weighted to the Russell Index in consumer staples, energy, financials, industrials, information technology, real estate and materials and had no position at all in utilities or telecommunication services at the end of the Reporting Period. |

8

FUND BASICS

Capital Growth Fund

as of August 31, 2016

| PERFORMANCE REVIEW | ||||||||||

| September 1, 2015–August 31, 2016 | Fund Total Return (based on NAV)1 | Russell 1000® Growth Index2 | ||||||||

| Class A | 5.79 | % | 10.51 | % | ||||||

| Class C | 4.98 | 10.51 | ||||||||

| Institutional | 6.19 | 10.51 | ||||||||

| Service | 5.66 | 10.51 | ||||||||

| Class IR | 6.05 | 10.51 | ||||||||

| Class R | 5.51 | 10.51 | ||||||||

| Class R6 | 6.19 | 10.51 | ||||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance reflects the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The Russell 1000® Growth Index is an unmanaged index that measures the performance of those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values. The Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index. |

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||||||

| For the period ended 6/30/16 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||||||||

| Class A | -8.00 | % | 9.69 | % | 6.41 | % | 8.81 | % | 4/20/90 | |||||||||||

| Class C | -4.33 | 10.11 | 6.21 | 4.97 | 8/15/97 | |||||||||||||||

| Institutional | -2.23 | 11.38 | 7.44 | 6.17 | 8/15/97 | |||||||||||||||

| Service | -2.69 | 10.83 | 6.91 | 5.65 | 8/15/97 | |||||||||||||||

| Class IR | -2.40 | 11.22 | N/A | 6.35 | 11/30/07 | |||||||||||||||

| Class R | -2.85 | 10.67 | N/A | 5.83 | 11/30/07 | |||||||||||||||

| Class R6 | N/A | N/A | N/A | -5.08 | 7/31/15 | |||||||||||||||

| 3 | The Standardized Total Returns are average annual total returns or cumulative total returns (only if the performance period is one year or less) as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Service, Class IR, Class R, and Class R6 Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

9

FUND BASICS

| EXPENSE RATIOS4 | ||||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.15 | % | 1.49 | % | ||||||

| Class C | 1.90 | 2.25 | ||||||||

| Institutional | 0.75 | 1.09 | ||||||||

| Service | 1.25 | 1.60 | ||||||||

| Class IR | 0.90 | 1.24 | ||||||||

| Class R | 1.40 | 1.74 | ||||||||

| Class R6 | 0.73 | 1.07 | ||||||||

| 4 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least December 29, 2016, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| TOP TEN HOLDINGS AS OF 8/31/165 | ||||||||

| Holding | % of Net Assets | Line of Business | ||||||

| Apple, Inc. | 6.1 | % | Technology Hardware, Storage & Peripherals | |||||

| Microsoft Corp. | 3.0 | Software | ||||||

| Facebook, Inc. Class A | 2.9 | Internet Software & Services | ||||||

| Amazon.com, Inc. | 2.8 | Internet & Direct Marketing Retail | ||||||

| MasterCard, Inc. Class A | 2.8 | IT Services | ||||||

| Comcast Corp. Class A | 2.3 | Media | ||||||

| Alphabet, Inc. Class A | 2.2 | Internet Software & Services | ||||||

| Alphabet, Inc. Class C | 2.2 | Internet Software & Services | ||||||

| Honeywell International, Inc. | 2.1 | Industrial Conglomerates | ||||||

| The Walt Disney Co. | 2.1 | Media | ||||||

| 5 | The top 10 holdings may not be representative of the Fund’s future investments. |

10

FUND BASICS

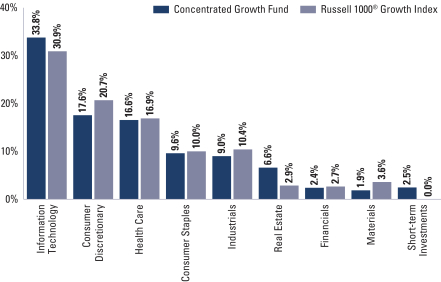

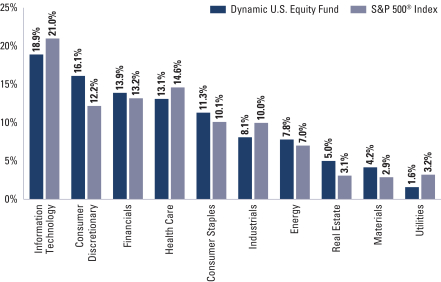

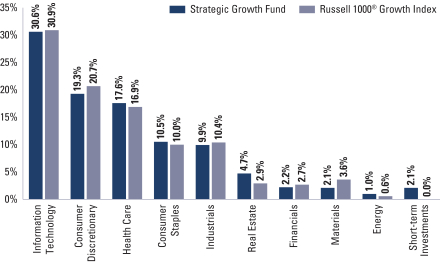

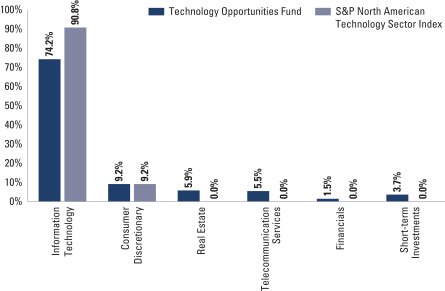

| FUND VS. BENCHMARK SECTOR ALLOCATION6 |

| As of August 31, 2016 |

| 6 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

11

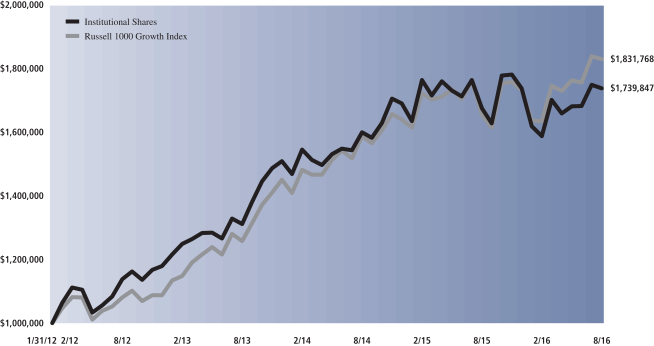

GOLDMAN SACHS CAPITAL GROWTH FUND

Performance Summary

August 31, 2016

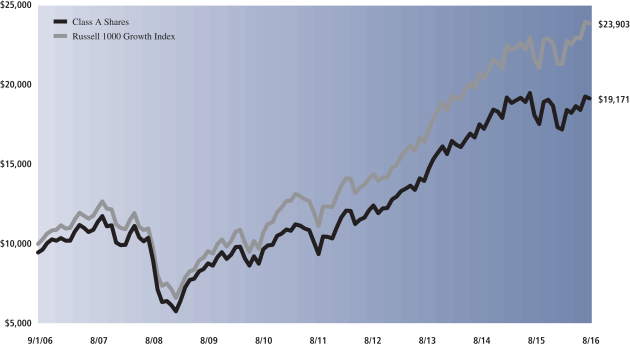

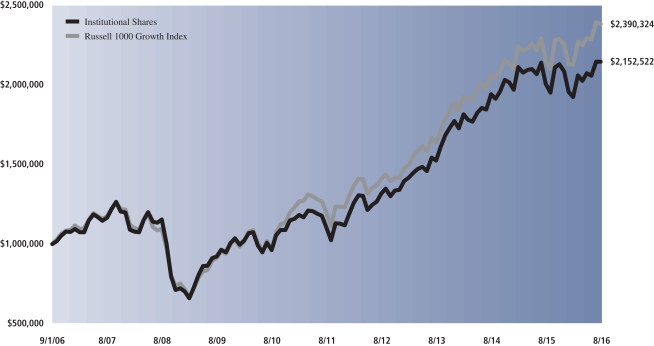

The following graph shows the value, as of August 31, 2016, of a $10,000 investment made on September 1, 2006 in Class A Shares (with the maximum sales charge of 5.5%). For comparative purposes, the performance of the Fund’s benchmark, the Russell 1000 Growth Index (with dividends reinvested), is shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations may cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance of Class C, Institutional, Service, Class IR, Class R and Class R6 Shares will vary from Class A Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding issuer/industry investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover and subscription and redemption cash flows affecting the Fund.

| Capital Growth Fund’s 10 Year Performance |

Performance of a $10,000 Investment, including any applicable sales charges, with distributions reinvested, from September 1, 2006 through August 31, 2016.

| Average Annual Total Return through August 31, 2016 | One Year | Five Years | Ten Years | Since Inception | ||||||||||

Class A (Commenced April 20, 1990) | ||||||||||||||

Excluding sales charges | 5.79% | 13.55% | 7.32% | 9.14% | ||||||||||

Including sales charges | 0.00% | 12.28% | 6.72% | 8.91% | ||||||||||

| ||||||||||||||

Class C (Commenced August 15, 1997) | ||||||||||||||

Excluding contingent deferred sales charges | 4.98% | 12.71% | 6.52% | 5.13% | ||||||||||

Including contingent deferred sales charges | 3.93% | 12.71% | 6.52% | 5.13% | ||||||||||

| ||||||||||||||

Institutional Class (Commenced August 15, 1997) | 6.19% | 14.00% | 7.75% | 6.34% | ||||||||||

| ||||||||||||||

Service Class (Commenced August 15, 1997) | 5.66% | 13.43% | 7.21% | 9.06% | ||||||||||

| ||||||||||||||

Class IR (Commenced November 30, 2007) | 6.05% | 13.83% | N/A | 6.70% | ||||||||||

| ||||||||||||||

Class R (Commenced November 30, 2007) | 5.51% | 13.26% | N/A | 6.17% | ||||||||||

| ||||||||||||||

Class R6 (Commenced July 31, 2015) | 6.19% | N/A | N/A | -1.19% | ||||||||||

| ||||||||||||||

12

PORTFOLIO RESULTS

Goldman Sachs Concentrated Growth Fund

Portfolio Composition

The Fund invests primarily in U.S. equity investments. The Fund typically holds 30-40 high quality growth companies and tends to be more concentrated in individual holdings, industries and sectors than the typical broadly diversified large-cap growth fund. Since the Fund’s inception, the Goldman Sachs Growth Equity Investment Team has focused on several key investment criteria that it believes can drive a company’s growth over the long term. These characteristics are: dominant market share, established brand name, pricing power, recurring revenue stream, free cash flow, high returns on invested capital, predictable growth, sustainable growth, long product life cycle, enduring competitive advantage, favorable demographic trends and excellent management. The Team strives to purchase these companies at reasonable valuations in order to capture the full benefits of their growth.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Growth Equity Investment Team discusses the Goldman Sachs Concentrated Growth Fund’s (the “Fund”) performance and positioning for the 12-month period ended August 31, 2016 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, C, Institutional, IR, R and R6 Shares generated average annual total returns, without sales charges, of 5.10%, 4.27%, 5.47%, 5.31%, 4.81% and 5.56%, respectively. These returns compare to the 10.51% average annual total return of the Fund’s benchmark, the Russell 1000® Growth Index (with dividends reinvested) (the “Russell Index”), during the same period. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | The Fund generated solid positive absolute returns, but stock selection overall detracted from the Fund’s performance relative to the Russell Index during the Reporting Period. Sector allocation as a whole also detracted, albeit much more modestly. |

| Q | Which equity market sectors most significantly affected Fund performance? |

| A | Challenging stock selection in the information technology, health care and consumer staples sectors detracted from the Fund’s relative results most during the Reporting Period. The only two sectors to contribute positively to the Fund’s relative performance during the Reporting Period were financials and industrials, wherein effective stock selection drove results. |

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | Among those stocks detracting most from the Fund’s results relative to its benchmark index were positions in global pharmaceutical company Allergan, global apparel company PVH and biotechnology firm Vertex Pharmaceuticals. |

| Allergan was the Fund’s biggest individual detractor during the Reporting Period. Volatility related to mergers and acquisitions the company has been involved in as well as market concerns around drug pricing pressures weighed on Allergan’s stock during the Reporting Period. Despite the near-term volatility and underperformance, we continued to believe at the end of the Reporting Period that Allergan was a high quality growth business, trading at an attractive valuation with meaningful financial flexibility going forward. |

| PVH was a top detractor from the Fund’s results during the Reporting Period. Weakness in the U.S. retail environment, high promotions in the industry, and currency headwinds added pressure to what we believe is otherwise a high quality company. While we continue to like the company and believe PVH remains a leading franchise with dominant market share, strong pricing power and solid fundamentals, near-term uncertainty led us to consolidate the Fund’s exposure into other consumer positions where we find the risk/reward opportunity more compelling. |

13

PORTFOLIO RESULTS

| Vertex Pharmaceuticals was a top detractor from the Fund’s performance during the Reporting Period. Early in 2016, its shares came under pressure following a disappointing fiscal fourth quarter that fell short of consensus expectations. Additionally, lowered expectations surrounding the launch of Vertex Pharmaceuticals’ new cystic fibrosis treatment, orkambi, caused shares to decline. Despite this weakness, at the end of the Reporting Period, we believed Vertex Pharmaceuticals had strong underlying fundamentals, a promising product pipeline with significant short-term and long-term catalysts and an attractive valuation. We further believed the company, led by what we consider to be a capable management team, could continue to see growth given its dominant market share in its space and given geographic expansionary efforts that have contributed to meaningful profitability. |

| Q | What were some of the Fund’s best-performing individual stocks? |

| A | The Fund benefited most relative to the Russell Index from positions in data center real estate investment trust (“REIT”) Equinix, online social media platform Facebook and e-commerce retailer Amazon.com. |

| Equinix was the strongest contributor to the Fund’s performance during the Reporting Period. The company reported solid quarterly results, positively beating market expectations for its organic revenue growth and earnings growth. The company also benefited from a move down in U.S. Treasury yields, which generally favors REITs given their attractive yield and growth potential relative to bonds. At the end of the Reporting Period, we thought that Equinix continued to have substantial pipeline opportunities, particularly with enterprise customers willing to pay a higher price. Continued integration with the company’s Telecity acquisition and a strategic partnership with Datang Telecom could further increase Equinix’s global presence and strengthen its competitive advantage, in our view. Further, we believe Equinix remains an asset with robust upside to its revenues and free cash flows, as it balances organic growth, low leverage and a sound capital structure. |

| Facebook was a top positive contributor to the Fund’s relative results during the Reporting Period. The company reported strong quarterly results during the Reporting Period, underpinned by advertisement revenue growth well above market expectations. Demand from advertisers was robust across most segments and geographies, and the company benefited from its three key levers — user growth, time spent and ad load. At the end of the Reporting Period, we remained positive on Facebook’s high operating expenditures, at what we consider to be manageable levels, which should allow the company to invest aggressively in substantial growth opportunities and simultaneously increase earnings. We think additional tailwinds in the form of lower and decreasing tax rates — and video-driven growth — may further benefit the company in coming years. In our view, Facebook’s strong fundamentals, high barriers to entry and robust contribution from Instagram warrant a constructive outlook on its long- term growth prospects. |

| Amazon.com reported strong third quarter 2015 results and solid first quarter 2016 results, with revenues and earnings well ahead of market expectations. Fundamentals were robust, and its management’s guidance implied continued strength. At the end of the Reporting Period, we believed the business remained strong in retail and Amazon Web Services (“AWS”) and that Amazon Prime’s membership growth could potentially position Amazon.com as a long-term outperformer in the retail industry. We continued to view Amazon.com’s business favorably and believed the company could well be the beneficiary of its scale and competitive advantages over the long term. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, we did not use derivatives as part of an active management strategy. |

| Q | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | We initiated a Fund position in Comcast, a broadband cable and media company. We believe Comcast is a best-in-class name that provides on-demand content, innovates well on channel mediums, and, despite cord cutting trends and satellite expansion, outperforms in cable. (Cord cutting refers to the practice of stopping a cable or satellite television service or getting rid of a landline phone in favor of less expensive options.) We like Comcast’s diversification across content and distribution as well as its diversification across content businesses. Given what we perceive to be the company’s positive near-term outlook and strong underlying fundamentals, we are optimistic on Comcast’s long-term return and thus established a position in the Fund. |

We established a Fund position in Microsoft. Share price weakness on the back of challenging quarterly results had created an opportunity, in our view, to initiate a position, and we believe the company presents good risk/reward potential. We are optimistic on what we believe are some solid growth |

14

PORTFOLIO RESULTS

and improved profitability focus areas, including Azure, Office 365 and Xbox. We believe Microsoft is attractively valued with a strong balance sheet, high free cash flow yield and a management that we believe is moving the company in the right direction. |

| Conversely, in addition to those sales already mentioned, we eliminated the Fund’s position in information storage company EMC. We believed that any complications with respect to its acquisition by Dell could add negative pressure to its stock, thus making the risk/reward profile less compelling, in our view. The stock had performed relatively well in the recent downturn, and so we took the opportunity to exit the Fund’s position to allocate the proceeds to other ideas with what we considered to have more compelling upside. |

| Q | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | In constructing the Fund’s portfolio, we focus on picking stocks rather than on making industry or sector bets. We seek to outpace the benchmark index by overweighting stocks that we expect to outperform and underweighting those that we think may lag. Consequently, changes in its sector weights are generally the direct result of individual stock selection or of stock appreciation or depreciation. That said, during the Reporting Period, the Fund’s exposure to industrials increased as did its position in cash, while its allocations to consumer discretionary, consumer staples, energy and financials decreased relative to the Russell Index. |

| Q | How was the Fund positioned relative to its benchmark index at the end of August 2016? |

| A | At the end of August 2016, the Fund had overweighted positions relative to the Russell Index in the real estate and information technology sectors. On the same date, the Fund had underweighted positions compared to the Russell Index in consumer discretionary, industrials and materials. The Fund was rather neutrally weighted relative to the Russell Index in consumer staples, financials and health care and had no position at all in the utilities and telecommunication services sectors at the end of the Reporting Period. |

15

FUND BASICS

Concentrated Growth Fund

as of August 31, 2016

| PERFORMANCE REVIEW | ||||||||||

| September 1, 2015–August 31, 2016 | Fund Total Return (based on NAV)1 | Russell 1000® Growth Index2 | ||||||||

| Class A | 5.10 | % | 10.51 | % | ||||||

| Class C | 4.27 | 10.51 | ||||||||

| Institutional | 5.47 | 10.51 | ||||||||

| Class IR | 5.31 | 10.51 | ||||||||

| Class R | 4.81 | 10.51 | ||||||||

| Class R6 | 5.56 | 10.51 | ||||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance reflects the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The Russell 1000® Growth Index is an unmanaged index that measures the performance of those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values. The Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index. |

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||||||

| For the period ended 6/30/16 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||||||||

| Class A | -8.61 | % | 8.52 | % | 6.01 | % | 6.48 | % | 9/03/02 | |||||||||||

| Class C | -5.02 | 8.93 | 5.80 | 6.11 | 9/03/02 | |||||||||||||||

| Institutional | -2.88 | 10.21 | 7.03 | 7.35 | 9/03/02 | |||||||||||||||

| Class IR | -3.04 | 10.04 | N/A | 5.25 | 11/30/07 | |||||||||||||||

| Class R | -3.55 | 9.48 | N/A | 4.74 | 11/30/07 | |||||||||||||||

| Class R6 | N/A | N/A | N/A | -5.24 | 7/31/15 | |||||||||||||||

| 3 | The Standardized Total Returns are average annual total returns or cumulative total returns (only if the performance period is one year or less) as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Class IR, Class R and Class R6 Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

16

FUND BASICS

| EXPENSE RATIOS4 | ||||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.22 | % | 1.60 | % | ||||||

| Class C | 1.97 | 2.35 | ||||||||

| Institutional | 0.82 | 1.20 | ||||||||

| Class IR | 0.97 | 1.35 | ||||||||

| Class R | 1.47 | 1.87 | ||||||||

| Class R6 | 0.80 | 1.18 | ||||||||

| 4 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least December 29, 2016, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| TOP TEN HOLDINGS AS OF 8/31/165 | ||||||||

| Holding | % of Net Assets | Line of Business | ||||||

| Apple, Inc. | 7.5 | % | Technology Hardware, Storage & Peripherals | |||||

| Facebook, Inc. Class A | 4.8 | Internet Software & Services | ||||||

| Amazon.com, Inc. | 4.1 | Internet & Direct Marketing Retail | ||||||

| Alphabet, Inc. Class A | 4.1 | Internet Software & Services | ||||||

| American Tower Corp. | 4.0 | Equity Real Estate Investment Trusts (REITs) | ||||||

| Costco Wholesale Corp. | 3.8 | Food & Staples Retailing | ||||||

| MasterCard, Inc. Class A | 2.9 | IT Services | ||||||

| Comcast Corp. Class A | 2.9 | Media | ||||||

| Honeywell International, Inc. | 2.9 | Industrial Conglomerates | ||||||

| Microsoft Corp. | 2.7 | Software | ||||||

| 5 | The top 10 holdings may not be representative of the Fund’s future investments. |

17

FUND BASICS

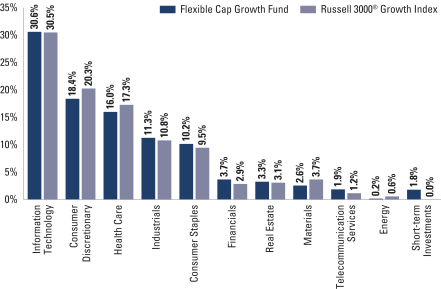

| FUND VS. BENCHMARK SECTOR ALLOCATION6 |

| As of August 31, 2016 |

| 6 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. Short-term investments represent repurchase agreements. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

18

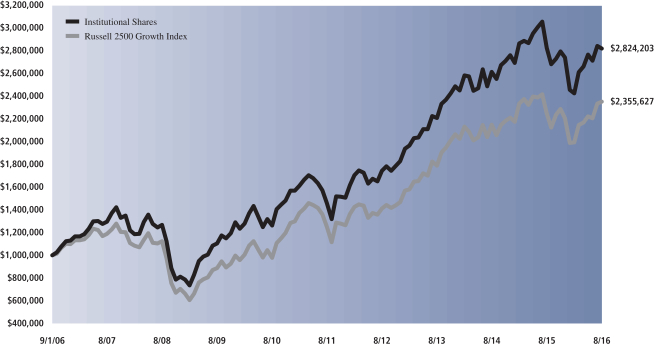

GOLDMAN SACHS CONCENTRATED GROWTH FUND

Performance Summary

August 31, 2016

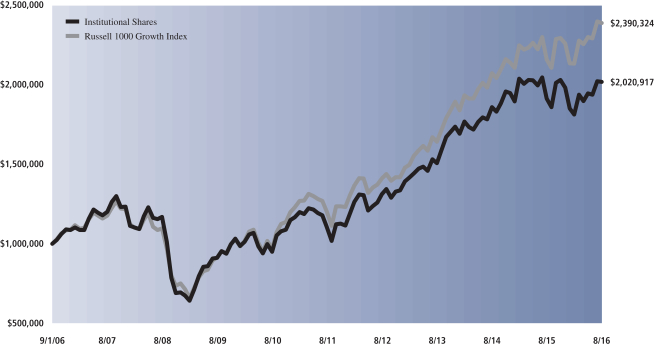

The following graph shows the value, as of August 31, 2016, of a $1,000,000 investment made on September 1, 2006 in Institutional Shares at NAV. For comparative purposes, the performance of the Fund’s benchmark, the Russell 1000 Growth Index (with dividends reinvested), is shown. This performance data represents past performance and should not be considered indicative of future performance which will fluctuate with changes in market conditions. These performance fluctuations may cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance of Class A, Class C, Class IR, Class R, and Class R6 Shares will vary from Institutional Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding issuer/industry investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover and subscription and redemption cash flows affecting the Fund.

| Concentrated Growth Fund’s 10 Year Performance |

Performance of a $1,000,000 Investment, including any applicable sales charges, with distributions reinvested, from September 1, 2006 through August 31, 2016.

| Average Annual Total Return through August 31, 2016 | One Year | Five Years | Ten Years | Since Inception | ||||||||||

Class A (Commenced September 3, 2002) | ||||||||||||||

Excluding sales charges | 5.10% | 12.38% | 6.86% | 7.14% | ||||||||||

Including sales charges | -0.63% | 11.11% | 6.25% | 6.71% | ||||||||||

| ||||||||||||||

Class C (Commenced September 3, 2002) | ||||||||||||||

Excluding contingent deferred sales charges | 4.27% | 11.55% | 6.06% | 6.33% | ||||||||||

Including contingent deferred sales charges | 3.23% | 11.55% | 6.06% | 6.33% | ||||||||||

| ||||||||||||||

Institutional Class (Commenced September 3, 2002) | 5.47% | 12.83% | 7.28% | 7.57% | ||||||||||

| ||||||||||||||

Class IR (Commenced November 30, 2007) | 5.31% | 12.66% | N/A | 5.63% | ||||||||||

| ||||||||||||||

Class R (Commenced November 30, 2007) | 4.81% | 12.11% | N/A | 5.13% | ||||||||||

| ||||||||||||||

Class R6 (Commenced July 31, 2015) | 5.56% | N/A | N/A | -1.12% | ||||||||||

| ||||||||||||||

19

PORTFOLIO RESULTS

Goldman Sachs Dynamic U.S. Equity Fund

Portfolio Composition

The Fund invests primarily in U.S. equity investments. Since the Fund’s inception, the Goldman Sachs Growth Equity Investment Team and the Goldman Sachs Fundamental Equity Value Investment Team have focused on several key investment criteria that they believe can drive a company’s growth over the long term. These characteristics are: dominant market share, established brand name, pricing power, recurring revenue stream, free cash flow, high returns on invested capital, predictable growth, sustainable growth, long product life cycle, enduring competitive advantage, favorable demographic trends and excellent management. The Teams strive to purchase these companies at reasonable valuations in order to capture the full benefits of their growth.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Growth Equity Investment Team and the Goldman Sachs Value Equity Investment Team discuss the Goldman Sachs Dynamic U.S. Equity Fund’s (the “Fund”) performance and positioning for the 12-month period ended August 31, 2016 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, C, Institutional, IR, R and R6 Shares generated average annual total returns, without sales charges, of 4.39%, 3.66%, 4.84%, 4.67%, 4.18% and 4.86%, respectively. These returns compare to the 12.52% average annual total return of the Fund’s benchmark, the Standard & Poor’s 500® Index (the “S&P 500 Index”), during the same period. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | The Fund posted positive absolute returns, but stock selection overall detracted from the Fund’s performance relative to the S&P 500 Index during the Reporting Period. Sector allocation as a whole also detracted, albeit more modestly. |

| Q | Which equity market sectors most significantly affected Fund performance? |

| A | Challenging stock selection in information technology, health care and consumer staples detracted from the Fund’s relative results most. Having an underweighted allocation to information technology, which outpaced the S&P 500 Index during the Reporting Period, also hurt. The only sector to contribute positively to the Fund’s relative performance during the Reporting Period was financials, wherein effective stock selection more than offset the detracting effect of having an overweight in the comparatively weakly performing sector. |

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | Detracting most from the Fund’s results relative to its benchmark index were positions in global apparel retailer Gap, global pharmaceutical company Allergan and online professional network provider LinkedIn. |

| Gap reported several quarters of disappointing earnings results driven by weaker than consensus expected sales and foreign exchange headwinds from a stronger U.S. dollar. Product design initiatives had been unable to turn around same-store sales trends, and a challenging macroeconomic environment for apparel retailers remained a headwind for the company. Additionally, news of Old Navy’s president leaving in 2015 was a slight negative for the company. As a result, we believe the risk/reward profile for Gap is less compelling over the near term, and so we exited the Fund’s position by the end of the Reporting Period. |

| Allergan was among the Fund’s biggest detractors during the Reporting Period. Volatility related to mergers and acquisitions the company has been involved in as well as market concerns around drug pricing pressures weighed on Allergan’s stock during the Reporting Period. Despite the near-term volatility and underperformance, we continued to believe at the end of the Reporting Period that Allergan was a high quality growth business, trading at an attractive valuation with meaningful financial flexibility going forward. |

| LinkedIn reported solid fourth quarter 2015 results, with revenues and earnings ahead of market estimates, and |

20

PORTFOLIO RESULTS

| healthy user engagement. Of note, however, was top and bottom line guidance below market expectations, which led to a stock price decline. Specifically, its management attributed the slowdown to macroeconomic pressures in the Europe, Middle East and Africa (“EMEA”) and Asia-Pacific (“APAC”) regions, and it indicated its plans to shut down its acquired Bizo asset. We believe these factors have led investors to question the company’s growth outlook, which is additionally affected by foreign exchange headwinds. We were optimistic on the company’s competitive positioning and unique offering, but our concerns around its long-term business model — as well as its lower guidance — led us to exit the Fund’s position and invest in higher conviction ideas. |

| Q | What were some of the Fund’s best-performing individual stocks? |

| A | The Fund benefited most relative to the S&P 500 Index from positions in e-commerce retailers Amazon.com and eBay and industrial conglomerate General Electric. |

| Amazon.com reported strong third quarter 2015 results and solid first quarter 2016 results, with revenues and earnings well ahead of market expectations. Fundamentals were robust, and its management’s guidance implied continued strength. At the end of the Reporting Period, we believed the business remained strong in retail and Amazon Web Services (“AWS”) and that Amazon Prime’s membership growth could potentially position Amazon.com as a long-term outperformer in the retail industry. We continued to view Amazon.com’s business favorably and believed the company could well be the beneficiary of its scale and competitive advantages over the long term. |

| Shares of eBay gained through July 2016 following strong second quarter 2016 earnings results that were well ahead of market expectations. The company raised its third quarter 2016 outlook for earnings and revenues. eBay also announced an additional $1 billion stock repurchase. At the end of the Reporting Period, we believed eBay’s management team was taking the right steps to ensure the company continues to grow and improve its offerings to customers. In our view, eBay has a strong balance sheet and good cash flow generation, which is a reason for us to have strong conviction in the company and its financial flexibility to invest in its business for future growth. |

| Throughout the Reporting Period, General Electric reported earnings results that exceeded consensus expectations, driven by strong organic revenue growth and operating margin improvement. Additionally, investors reacted positively to General Electric’s long-awaited announcement to spin off its majority stake in Synchrony Financial to existing shareholders. At the end of the Reporting Period, we remained optimistic on General Electric’s growth prospects, as a strong backlog of orders and what we believe to be accretive synergies from recent transactions could be supportive to its earnings in a potentially slow global economic growth environment. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, we did not use derivatives as part of an active management strategy. |

| Q | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | We initiated a Fund position in online social media platform Facebook during the Reporting Period. Over time, Facebook has established an important position as a consumer utility and has captured a significant portion of today’s mobile application mindshare. In our view, demand for Facebook’s business remains strong, and along with its Instagram franchise and online video features, the company is well positioned to capitalize on significant advertising growth. |

| We established a Fund position in MasterCard. MasterCard is a leading global payments and technology company that connects consumers, financial institutions, merchants, governments and businesses worldwide, enabling them to use electronic forms of payment instead of cash and checks. The company offers a wide range of payment solutions that enable the development and implementation of credit, debit, prepaid, commercial and related payment programs and solutions for consumers and merchants. In our view, the company performed well during the fourth quarter of 2015, exceeding its own estimates of gross revenues and billings, although an ongoing rebate and incentive program dragged a bit on net revenue growth. We are positive on the current macroeconomic trends, especially consumer spending, which we believe should benefit the company. We also believe MasterCard has a high quality management team, an investment grade balance sheet and strong free cash flow and operating margins. |

| Conversely, we sold the Fund’s position in financial services company American International Group (“AIG”). We believe any complications with respect to its newly announced strategic plan could add negative pressure to the stock, as major changes within such a complex organization take time |

21

PORTFOLIO RESULTS

| to harmonize, in our view. We took the opportunity to exit the Fund’s position in AIG to pursue higher conviction ideas. |

| We eliminated the Fund’s position in information storage company EMC. We believed that any complications with respect to its acquisition by Dell could add negative pressure to its stock, thus making the risk/reward profile less compelling, in our view. The stock had performed relatively well in the recent downturn, and so we took the opportunity to exit the Fund’s position to allocate the proceeds to other ideas with what we considered to have more compelling upside. |

| Q | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | In constructing the Fund’s portfolio, we focus on picking stocks rather than on making industry or sector bets. We seek to outpace the benchmark index by overweighting stocks that we expect to outperform and underweighting those that we think may lag. Consequently, changes in its sector weights are generally the direct result of individual stock selection or of stock appreciation or depreciation. That said, during the Reporting Period, the Fund’s exposure to consumer discretionary, energy, health care, information technology and materials increased and its allocations to consumer staples, financials and industrials decreased compared to the S&P 500 Index. The Fund’s position in cash also declined during the Reporting Period. |

| Q | How was the Fund positioned relative to its benchmark index at the end of August 2016? |

| A | At the end of August 2016, the Fund had overweighted positions relative to the S&P 500 Index in consumer discretionary, materials, real estate and consumer staples. On the same date, the Fund had underweighted positions compared to the S&P 500 Index in information technology, industrials, utilities and health care and was rather neutrally weighted to the S&P 500 Index in energy and financials. |

| The Fund had no position at all in telecommunication services at the end of the Reporting Period. |

22

FUND BASICS

Dynamic U.S. Equity Fund

as of August 31, 2016

| PERFORMANCE REVIEW | ||||||||||

| September 1, 2015–August 31, 2016 | Fund Total Return (based on NAV)1 | S&P 500® Index2 | ||||||||

| Class A | 4.39 | % | 12.52 | % | ||||||

| Class C | 3.66 | 12.52 | ||||||||

| Institutional | 4.84 | 12.52 | ||||||||

| Class IR | 4.67 | 12.52 | ||||||||

| Class R | 4.18 | 12.52 | ||||||||

| Class R6 | 4.86 | 12.52 | ||||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance reflects the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The S&P 500® Index is the Standard & Poor’s 500 Composite Index of 500 stocks, an unmanaged index of common stock prices. The Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index. |

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||

| For the period ended 6/30/16 | One Year | Five Years | Since Inception | Inception Date | ||||||||||||

| Class A | -11.74 | % | 7.64 | % | 8.80 | % | 11/30/09 | |||||||||

| Class C | -8.20 | 8.07 | 8.91 | 11/30/09 | ||||||||||||

| Institutional | -6.24 | 9.31 | 10.18 | 11/30/09 | ||||||||||||

| Class IR | -6.46 | 9.13 | 10.00 | 11/30/09 | ||||||||||||

| Class R | -6.82 | 8.62 | 9.47 | 11/30/09 | ||||||||||||

| Class R6 | N/A | N/A | -6.98 | 7/31/15 | ||||||||||||

| 3 | The Standardized Total Returns are average annual total returns or cumulative total returns (only if the performance period is one year or less) as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Class IR, Class R and Class R6 Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

23

FUND BASICS

| EXPENSE RATIOS4 | ||||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.22 | % | 2.81 | % | ||||||

| Class C | 1.97 | 3.56 | ||||||||

| Institutional | 0.82 | 2.42 | ||||||||

| Class IR | 0.97 | 2.63 | ||||||||

| Class R | 1.47 | 3.10 | ||||||||

| Class R6 | 0.80 | 2.40 | ||||||||

| 4 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least December 29, 2016, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| TOP TEN HOLDINGS AS OF 8/31/165 | ||||||||

| Holding | % of Net Assets | Line of Business | ||||||

| Bank of America Corp. | 5.2 | % | Banks | |||||

| Amazon.com, Inc. | 5.1 | Internet & Direct Marketing Retail | ||||||

| Pfizer, Inc. | 4.2 | Pharmaceuticals | ||||||

| Apple, Inc. | 3.9 | Technology Hardware, Storage & Peripherals | ||||||

| Facebook, Inc. Class A | 3.8 | Internet Software & Services | ||||||

| MasterCard, Inc. Class A | 3.5 | IT Services | ||||||

| JPMorgan Chase & Co. | 3.4 | Banks | ||||||

| McKesson Corp. | 3.2 | Health Care Providers & Services | ||||||

| General Electric Co. | 3.1 | Industrial Conglomerates | ||||||

| Abbott Laboratories | 3.1 | Health Care Equipment & Supplies | ||||||

| 5 | The top 10 holdings may not be representative of the Fund’s future investments. |

24

FUND BASICS

| FUND VS. BENCHMARK SECTOR ALLOCATION6 |

| As of August 31, 2016 |

| 6 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

25

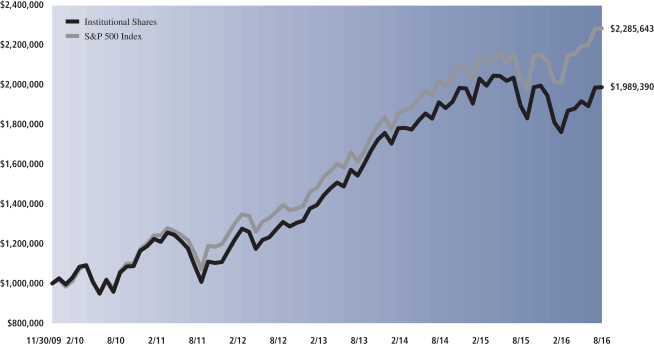

GOLDMAN SACHS DYNAMIC U.S. EQUITY FUND

Performance Summary

August 31, 2016

The following graph shows the value, as of August 31, 2016, of a $1,000,000 investment made on November 30, 2009 (commencement of operations) in Institutional Shares at NAV. For comparative purposes, the performance of the Fund’s benchmark, the S&P 500 Index (with dividends reinvested), is shown. Through April 30, 2015, the Fund had been known as the Goldman Sachs U.S. Equity Fund and certain of its strategies differed. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations may cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance of Class A, Class C, Class IR, Class R and Class R6 Shares will vary from Institutional Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding issuer/industry investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover and subscription and redemption cash flows affecting the Fund.

| Dynamic U.S. Equity Fund’s Lifetime Performance |

Performance of a $1,000,000 Investment, including any applicable sales charges, with distributions reinvested, from November 30, 2009 through August 31, 2016.

| Average Annual Total Return through August 31, 2016 | One Year | Five Years | Since Inception | |||||||

Class A (Commenced November 30, 2009) | ||||||||||

Excluding sales charges | 4.39% | 12.38% | 10.27% | |||||||

Including sales charges | -1.34% | 11.12% | 9.35% | |||||||

| ||||||||||

Class C (Commenced November 30, 2009) | ||||||||||

Excluding contingent deferred sales charges | 3.66% | 11.54% | 9.43% | |||||||

Including contingent deferred sales charges | 2.62% | 11.54% | 9.43% | |||||||

| ||||||||||

Institutional Class (Commenced November 30, 2009) | 4.84% | 12.82% | 10.71% | |||||||

| ||||||||||

Class IR (Commenced November 30, 2009) | 4.67% | 12.64% | 10.53% | |||||||

| ||||||||||

Class R (Commenced November 30, 2009) | 4.18% | 12.10% | 9.99% | |||||||

| ||||||||||

Class R6 (Commenced July 31, 2015) | 4.86% | N/A | -2.12% | |||||||

| ||||||||||

26

PORTFOLIO RESULTS

Goldman Sachs Flexible Cap Growth Fund

Portfolio Composition

The Fund invests primarily in U.S. equity investments in small-, mid- and large-capitalization issuers. Since the Fund’s inception, the Goldman Sachs Growth Equity Investment Team has focused on several key investment criteria that it believes can drive a company’s growth over the long term. These characteristics are: dominant market share, established brand name, pricing power, recurring revenue stream, free cash flow, high returns on invested capital, predictable growth, sustainable growth, long product life cycle, enduring competitive advantage, favorable demographic trends and excellent management. The Team strives to purchase these companies at reasonable valuations in order to capture the full benefits of their growth.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Growth Equity Investment Team discusses the Goldman Sachs Flexible Cap Growth Fund’s (the “Fund”) performance and positioning for the 12-month period ended August 31, 2016 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class A, C, Institutional, IR, R and R6 Shares generated average annual total returns, without sales charges, of 4.93%, 4.12%, 5.29%, 5.20%, 4.61% and 5.29%, respectively. These returns compare to the 9.96% average annual total return of the Fund’s benchmark, the Russell 3000® Growth Index (with dividends reinvested) (the “Russell Index”), during the same period. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | The Fund generated solid positive absolute returns, but stock selection overall detracted from the Fund’s performance relative to the Russell Index during the Reporting Period. Sector allocation as a whole also detracted, albeit much more modestly. |

| Q | Which equity market sectors most significantly affected Fund performance? |

| A | The sectors that detracted most from the Fund’s relative results during the Reporting Period were information technology, consumer staples and health care, wherein stock selection proved challenging. The sectors that contributed positively to the Fund’s relative performance during the Reporting Period were financials, energy and consumer discretionary, wherein effective stock selection drove results. |

| Q | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | Detracting most from the Fund’s results relative to the Russell Index were positions in luxury household furnishing company Restoration Hardware Holdings, online professional network provider LinkedIn and software giant Microsoft. |

| During the Reporting Period, Restoration Hardware Holdings experienced headwinds of an increasingly challenging retail industry, especially around the high-end consumer. Given the lower and volatile demand, we exited the Fund’s position to invest in what we considered to be more compelling ideas. |

| LinkedIn reported solid fourth quarter 2015 results, with revenues and earnings ahead of market estimates, and healthy user engagement. Of note, however, was top and bottom line guidance below market expectations, which led to a stock price decline. Specifically, its management attributed the slowdown to macroeconomic pressures in the Europe, Middle East and Africa (“EMEA”) and Asia-Pacific (“APAC”) regions, and it indicated its plans to shut down its acquired Bizo asset. We believe these factors have led investors to question the company’s growth outlook, which is additionally affected by foreign exchange headwinds. We were optimistic on the company’s competitive positioning and unique offering, but our concerns around its long-term business model — as well as its lower guidance — led us to exit the Fund’s position and invest in higher conviction ideas. |

27

PORTFOLIO RESULTS

| Microsoft was a new purchase for the Fund during the Reporting Period. Share price weakness on the back of challenging quarterly results had created an opportunity, in our view, to initiate a position, and we believe the company presents good risk/reward potential. During the Reporting Period, Microsoft’s stock performed strongly in absolute returns, but an underweight in the Fund compared to the Russell Index led to it being a detractor from relative returns. Microsoft reported fiscal fourth quarter results that meaningfully exceeded market expectations, with solid revenue trends. Its management also guided down for the following quarter, although the downward revision was more muted than what we have seen in some other quarters. At the end of the Reporting Period, we were optimistic on what we believe are some solid growth and improved profitability focus areas, including Azure, Office 365 and Xbox. We also believed Microsoft was attractively valued with a strong balance sheet, high free cash flow yield and a management that we believe is moving the company in the right direction. |

| Q | What were some of the Fund’s best-performing individual stocks? |

| A | Among those stocks the Fund benefited most from relative to the Russell Index were positions in data center real estate investment trust (“REIT”) Equinix, specialty retailer Ulta Salon, Cosmetics & Fragrance and water technology company Xylem. |

| Equinix was the strongest contributor to the Fund’s performance during the Reporting Period. The company reported solid quarterly results, positively beating market expectations for its organic revenue growth and earnings growth. The company also benefited from a move down in U.S. Treasury yields, which generally favors REITs given their attractive yield and growth potential relative to bonds. At the end of the Reporting Period, we thought that Equinix continued to have substantial pipeline opportunities, particularly with enterprise customers willing to pay a higher price. Continued integration with the company’s Telecity acquisition and a strategic partnership with Datang Telecom could further increase Equinix’s global presence and strengthen its competitive advantage, in our view. Further, we believe Equinix remains an asset with robust upside to its revenues and free cash flows, as it balances organic growth, low leverage and a sound capital structure. |

| After a challenging start to 2016 for Ulta Salon, Cosmetics & Fragrance, momentum started picking up for the company in the beginning of April 2016 after strong first quarter 2016 earnings and the company being added to the S&P 500 Index. Its strong results were driven by margins, revenues and e-commerce growth that were ahead of market expectations. In our view, the company is a strong brand that continues to gain recognition. We believe Ulta Salon, Cosmetics & Fragrance has an opportunity to grow market share through higher brand awareness, increasing loyalty to existing stores, expansion of new stores and e-commerce. |

| During the Reporting Period, Xylem reported strong quarterly results, and toward the end of the Reporting Period, announced the purchase of Sensus, a smart water meter company, for approximately $1.7 billion in cash. The acquisition was viewed positively by investors, as it further bolsters Xylem’s product offering and technological advantage. At the end of the Reporting Period, we remained optimistic on Xylem’s margin expansion prospects and believed its management team has done well to position the company for sustainable long-term growth. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, we did not use derivatives as part of an active management strategy. |

| Q | Did the Fund make any significant purchases or sales during the Reporting Period? |