UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| | |

| Caroline Kraus, Esq. | | Copies to: |

| Goldman Sachs & Co. LLC | | Geoffrey R.T. Kenyon, Esq. |

| 200 West Street | | Dechert LLP |

| New York, New York 10282 | | 100 Oliver Street |

| | 40th Floor |

| | Boston, MA 02110-2605 |

(Name and address of agents for service)

Registrant’s telephone number, including area code:(312) 655-4400

Date of fiscal year end: October 31

Date of reporting period: April 30, 2019

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| | The Semi-Annual Report to Shareholders is filed herewith. |

Goldman Sachs Funds

| | | | |

| | |

| Semi-Annual Report | | | | April 30, 2019 |

| | |

| | | | Absolute Return Multi-Asset Fund |

It is our intention that beginning on January 1, 2021, paper copies of the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. At any time, you may elect to receive reports and certain communications from the Fund electronically by calling the applicable toll-free number below or by contacting your financial intermediary.

You may elect to receive all future shareholder reports in paper free of charge. If you hold shares of the Fund directly with the Fund’s transfer agent, you can inform the transfer agent that you wish to receive paper copies of reports by callingtoll-free 800- 621-2550 for Institutional, Class R6 and Class P shareholders or800-526-7384 for all other shareholders. If you hold shares of the Fund through a financial intermediary, please contact your financial intermediary to make this election. Your election to receive reports in paper will apply to all Goldman Sachs Funds held in your account if you invest through your financial intermediary or all Goldman Sachs Funds held with the Fund’s transfer agent if you invest directly with the transfer agent.

Goldman Sachs Absolute Return Multi-Asset Fund

| | | | |

| | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

What Differentiates Goldman Sachs Absolute Return Multi-Asset Fund’s Investment Process?

The Goldman Sachs Absolute Return Multi-Asset Fund (the “Fund”) seeks to deliver consistent returns in all market environments through broad diversification and dynamic management. The Fund aims to provide exposure beyond traditional asset classes, with less dependence on the direction of stock and bond markets, and thoughtfully combines the investment capabilities across Goldman Sachs Asset Management (GSAM).

| ∎ | | By investing across asset classes using less-traditional strategies and techniques, we aim to incorporate distinct sources of return into the portfolio that are different from traditional core equities and bond returns |

| ∎ | | We use a proprietary, factor-based risk-budgeting framework that seeks to balance risk across unique return drivers and active strategies |

| ∎ | | The Fund seeks to capitalize on the changing economic cycle and tactically adjusts for dislocations in the current environment, with the aim of enhancing returns and mitigating portfolio losses |

| ∎ | | We seek to profit from opportunities across medium- to shorter-term time horizons and multiple geographies |

| ∎ | | For over two decades, we have managed multi-asset class solutions for clients including sovereign wealth funds, pension plans, endowments, and foundations |

| ∎ | | We leverage the insights and alpha generation of GSAM’s 700+ investment professionals in 30 offices around the globe (as of September 30, 2018) |

| ∎ | | We monitor portfolio risk daily and have a robust risk management framework with multiple layers of oversight at the strategic allocation, security selection and firm levels |

Diversification does not protect an investor from market risk and does not ensure a profit. The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

1

FUND RESULTS

Goldman Sachs Absolute Return Multi-Asset Fund

Investment Objective

The Fund seeks to achieve long-term absolute return.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Global Portfolio Solutions Team discusses the Goldman Sachs Absolute Return Multi-Asset Fund’s (the “Fund”) performance and positioning for thesix-month period ended April 30, 2019 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, Class C, Institutional, Investor, Class P, Class R and Class R6 Shares generated cumulative total returns, without sales charges, of 4.01%, 3.61%, 4.22%, 4.10%, 4.27%, 3.90%, and 4.25%, respectively. These returns compare to the 1.34% cumulative total return of the Fund’s benchmark, the ICE BofAML U.S. Dollar Three-Month LIBOR Constant Maturity Index (the “Index”), during the same time period. |

| | References to the Fund’s benchmark and to other indices, if any, mentioned herein are for informational purposes only, and unless otherwise noted, are not indications of how the Fund is managed. The use of the Index as the Fund’s benchmark does not imply the Fund is being managed like cash and does not imply low risk or low volatility. |

| Q | | What economic and market factors most influenced the Fund during the Reporting Period? |

| A | | During the Reporting Period overall, the factors most influencing the financial markets and the Fund were global economic data, central bank monetary policy, crude oil prices and geopolitical events. |

| | In November 2018, when the Reporting Period began, global economic growth appeared to be stabilizing following previous weakness, with risk assets supported by less hawkish commentary from the U.S. Federal Reserve (“Fed”), decreased concerns around U.S.-China trade relations and improved Chinese economic data. (Hawkish tends to suggest higher interest rates; opposite of dovish.) Global equities recorded gains, led by emerging markets stocks. Within fixed income, the10-year U.S. Treasury yield fell. |

| | In December 2018, global economic growth moderated, as evidenced by declining manufacturing indicators across the U.S., Europe and China. The Fed hiked short-term interest rates by 25 basis points at its December meeting, in line with market expectations. (A basis point is 1/100th of a percentage point.) The less accommodative Fed and the slowing global economic growth backdrop weighed on risk assets during the month. Global equities declined, fueled by sell-offs in U.S. and Japanese stocks. Emerging markets equities posted negative returns, but outpaced developed markets stocks. In fixed income, the10-year U.S. Treasury yield fell on a combination of market-perceived safe-haven demand and lower crude oil prices. Crude oil prices fell during December 2018 in spite of proposed production cuts by the Organization of the Petroleum Exporting Countries and Russia, as weak investor risk appetite and market concerns around oversupply remained in focus. |

| | Risk assets broadly rebounded during the first quarter of 2019, as investor sentiment turned positive on a combination of dovish global central bank policy, tentative stabilization in Chinese economic growth and seemingly promising developments in U.S.-China trade talks. As inflationary pressures remained rather muted, the Fed and the European Central Bank (“ECB”) each made a dovish shift and then maintained monetary policy stances that were broadly supportive of economic growth. More specifically, the Fed signaled it would make no additional short-term interest rate hikes during 2019, and the ECB indicated it was reluctant to hike interest rates during the calendar year. Although global economic growth continued to decelerate, there were signs of improvement, including indications of a bottoming in Chinese credit growth, a modestpick-up in fixed asset investment and an uptick in March 2019 manufacturing data. Global equities posted a double-digit gain during the first calendar quarter, led by a rally in U.S. stocks. Emerging markets equities overall underperformed developed markets equities, but Chinese stocks rose significantly. In fixed income, the10-year U.S. Treasury yield fell during the first quarter of 2019. |

2

FUND RESULTS

| | In April 2019, risk assets continued to rally, supported by signs of stabilization in global economic growth and continued dovishness from major central banks amidst muted inflationary pressures. In the U.S., stocks reached new highs on the back of stronger than consensus expected corporate earnings. European stocks also posted solid gains. Although Japanese equities recorded positive returns, they lagged their developed markets counterparts due to weaker than market expected corporate earnings. In China, money supply and credit data were stronger than market anticipated, adding to investor expectations that Chinese economic growth might continue to recover. However, a less dovish stance by China’s central bank dampened market optimism. In fixed income, the U.S.10-year U.S. Treasury yield rose. Crude oil prices rallied, driven mostly by the U.S. Administration’s decision to end waivers on Iranian oil exports. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | The Fund seeks to achieve its investment objective through investments in different asset classes, geographic regions and security selection strategies in a portfolio primarily of equity, fixed income, real assets and currency asset classes. Real assets are physical assets that derive their value from their own intrinsic qualities (e.g., precious metals, commodities and real estate). The Fund also invests in multi-strategy liquid alternatives as it seeks to achieve its investment objective. Multi-strategy liquid alternatives invest across asset classes through both systematic and rules-based investment strategies. The Fund’s performance is driven by four sources of return: long-term strategic asset allocation to market exposures, medium-term cycle-aware allocation, short-term tactical allocation and excess returns from investments in Underlying Funds through which the Fund gains exposure to underlying asset classes. Strategic asset allocation is the process by which the Fund’s assets are allocated across underlying asset classes and strategies in a way that considers the risks of each underlying asset class and strategy. Medium-term cycle-aware allocation is the process by which we adjust the portfolio for changes in the business or economic cycle. Short-term tactical allocation is the implementation of tactical market views with the goal of improving the Fund’s risk-adjusted return. The risk-adjusted return on an investment takes into account the risk associated with that investment relative to other potential investments. |

| | During the Reporting Period, the Fund generated positive returns, driven primarily by strategic asset allocation and, to a lesser extent, by short-term tactical asset allocation. These results were offset somewhat by medium-term cycle-aware allocation and security selection within the Underlying Funds, which detracted from the Fund’s performance. |

| | Strategic asset allocation overall added to the Fund’s results during the Reporting Period. At the asset class level, allocations to equities, fixed income, real assets and currencies contributed positively. Strategic allocations to multi-strategy liquid alternatives detracted from returns. Within its strategic allocations to equities, the Fund’s positive performance was largely due to its exposure to emerging markets stocks. Investor sentiment was buoyed by a combination of constructive U.S.-China trade talks, the Fed’s considerably more dovish stance and market expectations for better Chinese economic data due to policy stimulus. In addition, the Fund benefited from its exposure to U.S. and international equities, as risk assets rallied during the first quarter of 2019. Within its strategic fixed income allocations, the Fund’s exposure to high yield corporate bonds added to performance, as credit spreads narrowed and interest rates broadly declined during the Reporting Period. (Credit spreads are yield differentials between corporate bonds and U.S. Treasury securities of comparable maturity.) The Fund was also aided by our long U.S. interest rate options strategy, through which we seek to profit if interest rates fall, remain constant or rise less than anticipated. This strategy bolstered the Fund’s performance, given that U.S. Treasury yields fell over the course of the Reporting Period. (Our long U.S. interest rate options strategy is a macroeconomic hedge that buys put options on short-term interest rates. A put option is an option contract giving the owner the right, but not the obligation, to sell a specified amount of an underlying asset at a specified price within a specified time.) Additionally, the Fund’s strategic allocations to U.S. dollar-denominated emerging markets debt and local currency emerging markets debt contributed positively. Within its strategic allocations to real assets, the Fund was helped by its exposure to U.S. and international real estate securities as well as by its exposure to global infrastructure securities. Within its strategic allocations to currencies, the Fund benefited from our decision to hedge foreign currency exposure back to the U.S. dollar (accomplished through foreign exchange currency forward contracts), as the U.S. dollar strengthened versus other major currencies during the Reporting Period. With its strategic allocations to multi-strategy liquid alternatives, the Fund was hurt, especially during the first quarter of 2019, by our U.S. equity volatility strategy, which seeks to benefit from the difference between |

3

FUND RESULTS

| | implied volatility (i.e., expectations of future volatility) and realized volatility (i.e., historical volatility) in equity markets. On the other hand, the Fund’s strategic allocation to the Goldman Sachs Alternative Premia Fund, which provides exposure to a diversified range of alternative investment strategies, and its strategic allocation to the Goldman Sachs Managed Futures Strategy Fund added to returns during the Reporting Period. |

| | Medium-term cycle-aware allocation detracted overall from the Fund’s performance. We held three medium-term cycle-aware views during the Reporting Period. The first view was to be short interest rate duration, which we expressed through the Fund’s short position in long-maturity German government bonds and the Fund’s short positions in specific segments of the U.S. Treasury yield curve. (Duration is a measure of the Fund’s sensitivity to changes in interest rates. Yield curve is a spectrum of interest rates based on maturities of varying lengths.) The Fund’s short position in long-maturity German government bonds hampered returns, as Germany’s long-term interest rates fell in response to slower European economic growth, dovish ECB monetary policy and benign inflation. The Fund’s short positioning in specific segments of the U.S. Treasury yield curve detracted from performance on the back of the broad decline in U.S. Treasury yields during the Reporting Period. The second medium-term cycle-aware view was to hold a long position in emerging markets equities versus developed markets equities. This positioning contributed positively to the Fund’s results, as emerging markets equities outperformed developed markets equities during the Reporting Period. The third medium-term cycle-aware view — to hold a long position in local currency emerging markets bonds versus U.S. high yield corporate bonds — also enhanced the Fund’s returns, as local currency emerging markets debt outperformed U.S. high yield corporate bonds during the Reporting Period. |

| | Tactical asset allocation added to the Fund’s performance during the Reporting Period, as the Goldman Sachs Tactical Exposure Fund (the “Underlying Tactical Fund”), which we use to express our tactical views, generated a positive return. |

| | Security selection overall detracted from the Fund’s returns during the Reporting Period. The Fund was hurt most by security selection within the Goldman Sachs Managed Futures Strategy Fund, followed by the marginally negative performance of our U.S. real estate strategy (implemented through the Goldman Sachs Real Estate Securities Fund). These results were partially offset by the positive contributions of our emerging markets equity strategy (implemented primarily through the Goldman Sachs Emerging Markets Equity Fund), emerging markets debt strategy (implemented primarily through the Goldman Sachs Local Emerging Markets Debt Fund and the Goldman Sachs Emerging Markets Debt Fund), international real estate strategy (implemented through the Goldman Sachs International Real Estate Securities Fund) and security selection within the Goldman Sachs Global Infrastructure Fund. |

| Q | | How was the Fund positioned at the beginning of the Reporting Period? |

| A | | At the beginning of the Reporting Period, the Fund had approximately 34% of its total net assets in long equity-related investments; approximately 34% of its total net assets in long fixed income-related investments; approximately 9% of its total net assets in long real assets investments; approximately 11% of its total net assets in long currency-related investments; and approximately 51% of its total net assets in long multi-strategy liquid alternatives. It had short positions of approximately-5% of its total net assets in equity-related investments; approximately-17% of its total net assets in fixed income-related assets; none of its total net assets in real asset investments; approximately-10% of its total net assets in currency-related investments; and none of its total net assets in multi-strategy liquid alternatives. The positioning breakout above is inclusive of derivatives exposure across all asset classes, which generally includes the use of equity index futures, equity options, interest rate futures, commodity futures and currency forwards. |

| Q | | How did you manage the Fund’s allocations during the Reporting Period? |

| A | | We took advantage of the rally in risk assets during the first quarter of 2019 to reduce the Fund’s overall exposure to risk. More specifically, we decreased the Fund’s strategic allocations to emerging markets equities, real estate securities and managed futures over the course of the first calendar quarter and increased its allocations to more traditional investments, such as U.S. large cap equities andnon-U.S. developed markets equities. As part of this effort, we also reduced the size of the Fund’s short-term tactical allocation by trimming its investment in the Underlying Tactical Fund. During January 2019, we eliminated the Fund’s short positions in futures on the S&P 500® Index and the MSCI EAFE Index, which sought to moderate exposure to equity beta, and adopted long positions in U.S. and international stocks (implemented through futures on the |

4

FUND RESULTS

| | S&P 500® Index and the MSCI EAFE Index). (Beta refers to the component of returns that is attributable to market risk exposure, rather than manager skill.) |

| | We also sought to adjust the Fund’s exposure for what we viewed as medium-term changes to the business or economic cycle. In January 2019, we removed our medium-term cycle-aware view that the Fund be overweight emerging markets equities versus developed markets equities. We had expected to see the start of a rebound in China’s economic data by the end of 2018 in response to policy initiatives that sought to stimulate growth, but fresh data releases showed continued deterioration. Although we continued to believe Chinese economic data would recover, we thought the likely timing had been pushed into the future and market uncertainty around it had increased. Finally, during March 2019, we reduced the Fund’s short position in long-maturity German government bonds, as Germany’s long-term interest rates fell. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, the Fund used exchange-traded index futures contracts to gain long exposure to U.S.large-cap equities,non-U.S. developed equities and emerging markets equities (each had a positive impact on performance). |

| | Interest rate futures were used to manage the Fund’s interest rate exposures and to facilitate the implementation of specific duration and yield curve views (negative impact on performance). The Fund employed U.S. Treasury futures to gain access to10-year U.S. Treasury notes (positive impact). German bund futures were utilized to express a view on the direction of long-term German interest rates (negative impact). The Fund used options on Eurodollar futures to take tactical positions on the U.S. interest rate yield curve (positive impact). (Eurodollar futures are contracts that have underlying assets linked to time deposits denominated in U.S. dollars at banks outside the U.S.) Different positions may be taken within the Fund based on expectations of changes in interest rates and expectations of changes in the yield curve. Changes in the shape of the yield curve will change the relative price of bonds represented by the curve. Also during the Reporting Period, the Fund used a specialized index of credit default swaps to gain exposure to U.S. high yield corporate bonds (positive impact). Interest rate options were employed as part of the Fund’s macroeconomic hedge (positive impact). |

| | To hedge its exposure tonon-U.S. developed markets currencies and emerging markets currencies, the Fund used forward foreign currency exchange contracts (positive impact on performance). |

| | Lastly, the Fund obtained exposure to the underlying asset classes through the use of the Underlying Funds, which may also invest in derivatives to provide exposure to equity, fixed income and commodity asset classes. Derivatives and similar instruments allow us to manage interest rate, credit and currency risks more effectively by allowing us both to apply active investment views with greater versatility and to afford greater risk management precision than we would otherwise be able to implement. |

| Q | | How was the Fund positioned at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund had approximately 31% of its total net assets in long equity-related investments; approximately 52% of its total net assets in long fixed income-related investments; approximately 5% of its total net assets in long real assets investments; approximately 6% of its total net assets in long currency-related investments; and approximately 39% of its total net assets in long multi-strategy liquid alternatives. It had short positions of approximately-2% of its total net assets in equity-related investments; approximately-2% of its total net assets in fixed income-related assets; none of its total net assets in real asset investments; approximately-6% of its total net assets in currency-related investments; and none of its total net assets in multi-strategy liquid alternatives. The positioning breakout above is inclusive of derivatives exposure across all asset classes, which generally includes the use of equity index futures, equity options, interest rate futures, commodity futures and currency forwards. |

| Q | | What is the Fund’s tactical asset allocation view and strategy for the months ahead? |

| A | | At the end of the Reporting Period, we emphasized three macro themes. First, we expected to see an elongated U.S. economic expansion in 2019, with growth continuing and a downturn unlikely, in our view. Second, we expected to see signs of a synchronized rebound in economic growth across the U.S., Europe and China following the slowdown in activity near the beginning of 2019. Third, we believed risk assets were less likely to experience sell-offs in the very near term, though we anticipated episodic drawdowns later in 2019, which should create attractive investment |

5

FUND RESULTS

| | opportunities, in our opinion, if global economic growth flattens and bond yields become less well-anchored. |

| | At the asset class level, we had a positive outlook on equities over the medium term at the end of the Reporting Period. In our view, the macro environment is likely to support equities going into the summer months. We expect the equity market rally to continue thereafter, though we believe returns may be capped to some degree by more modest corporate earnings growth and there-rating seen in the first four months of 2019.(Re-rating occurs when market participants change their view of a company, and valuation measures, such as the price-earnings ratio, are revised substantially higher or lower.) As for fixed income, we remained bearish on government bonds at the end of the Reporting Period. In the near term, long-term interest rates are likely to remain range bound, in our view, given the Fed’s dovish shift during the Reporting Period and limited inflationary pressures. However, in the medium term, we expect the elongated U.S. economic cycle to lead to higher bond yields should the Fed hike short-term interest rates. As for credit spreads, while they compressed significantly during the first four months of 2019, we see scope for additional tightening into the summer and believe they are more likely than not to tighten further by the end of 2019. That said, we think late economic cycle dynamics, especially near calendaryear-end, could potentially push credit spreads wider. |

6

FUND BASICS

Index Definitions

S&P 500® Index is a U.S. stock market index based on the market capitalizations of 500 large companies having common stock listed on the New York Stock Exchange or NASDAQ. The S&P 500® Index components and their weightings are determined by S&P Dow Jones Indices.

MSCI EAFE Index is an equity index that captures large-cap and mid-cap representation across 21 developed markets countries around the world, excluding the U.S. and Canada. The index covers approximately 85% of the free float-adjusted market capitalization in each country. Developed markets countries in the index include Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the U.K.

It is not possible to invest directly in an unmanaged index.

7

FUND BASICS

Goldman Sachs Absolute Return Multi-Asset Fund

as of April 30, 2019

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | |

| | | November 1, 2018–April 30, 2019 | | Fund Total Return

(based on NAV)1 | | | ICE BofAML U.S. Dollar Three-Month

LIBOR Constant Maturity Index2 | |

| | | |

| | Class A | | | 4.01 | % | | | 1.34 | % |

| | Class C | | | 3.61 | | | | 1.34 | |

| | Institutional | | | 4.22 | | | | 1.34 | |

| | Investor | | | 4.10 | | | | 1.34 | |

| | Class P | | | 4.27 | | | | 1.34 | |

| | Class R | | | 3.90 | | | | 1.34 | |

| | | Class R6 | | | 4.25 | | | | 1.34 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The Fund’s benchmark index is the ICE BofAML U.S. Dollar Three-Month LIBOR Constant Maturity Index (the “Index”). The Index tracks the performance of a synthetic asset paying LIBOR to a stated maturity. The Index figures do not reflect any deduction of fees, expenses or taxes. It is not possible to invest directly in an index. |

| | | | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 | |

| | | | |

| | | For the period ended 3/31/19 | | One Year | | | Since Inception | | | Inception Date | |

| | | | |

| | Class A | | | -5.88 | % | | | -1.67 | % | | | 09/02/2015 | |

| | Class C | | | -2.05 | | | | -0.84 | | | | 09/02/2015 | |

| | Institutional | | | 0.11 | | | | 0.31 | | | | 09/02/2015 | |

| | Investor | | | -0.12 | | | | 0.15 | | | | 09/02/2015 | |

| | Class P | | | N/A | | | | -0.16 | | | | 04/16/2018 | |

| | Class R | | | -0.54 | | | | -0.34 | | | | 09/02/2015 | |

| | | Class R6 | | | 0.03 | | | | 0.30 | | | | 09/02/2015 | |

| | 3 | | The Standardized Total Returns are average annual total returns or cumulative total returns (only if the performance period is one year or less) as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.50% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Investor, Class R, Class R6 and Class P Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns.Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

8

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | | |

| | Class A | | | 1.43 | % | | | 4.32 | % |

| | Class C | | | 2.18 | | | | 5.07 | |

| | Institutional | | | 1.04 | | | | 3.93 | |

| | Investor | | | 1.18 | | | | 4.07 | |

| | Class P | | | 1.03 | | | | 3.92 | |

| | Class R | | | 1.68 | | | | 4.57 | |

| | | Class R6 | | | 1.03 | | | | 3.92 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to contractual arrangements, the Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2020, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | | | |

| | TOP TEN HOLDINGS AS OF 4/30/195 |

| | | |

| | | Holding | | % of Net Assets | | | Line of Business |

| | | |

| | Goldman Sachs Financial Square Government Fund – Institutional Shares | | | 21.9 | % | | Investment Companies |

| | Goldman Sachs Short-Term Conservative Income Fund – Class R6 Shares | | | 20.5 | | | Investment Companies |

| | Goldman Sachs Tactical Exposure Fund – Class R6 | | | 15.4 | | | Investment Companies |

| | Goldman Sachs Alternative Premia Fund – Class R6 | | | 14.9 | | | Investment Companies |

| | Goldman Sachs Managed Futures Strategy Fund – Class R6 | | | 10.4 | | | Investment Companies |

| | Goldman Sachs Emerging Markets Equity Fund – Class R6 | | | 5.4 | | | Investment Companies |

| | Goldman Sachs Local Emerging Markets Debt Fund – Class R6 | | | 5.1 | | | Investment Companies |

| | Goldman Sachs Global Infrastructure Fund – Class R6 | | | 3.4 | | | Investment Companies |

| | Goldman Sachs International Real Estate Securities Fund – Class R6 | | | 1.4 | | | Investment Companies |

| | | Goldman Sachs Emerging Markets Debt Fund – Class R6 | | | 1.1 | | | Investment Companies |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

9

FUND BASICS

| | | | | | |

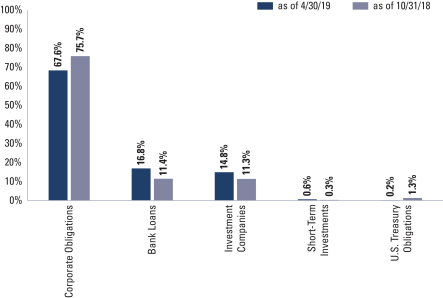

| | PORTFOLIO COMPOSITION6 | | | | |

| |

| | | As of April 30, 2019 |

| |

| | |  |

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”); however, the sector classifications used by the portfolio management team may differ from GICS. Underlying sector allocations of Investment Companies held by the Fund are not reflected in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

10

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Schedule of Investments

April 30, 2019 (Unaudited)

| | | | | | | | | | |

| Shares | | | Dividend

Rate | | | Value | |

|

| Investment Companies(a) – 100.1% | |

| Dynamic – 40.6% | |

| | Goldman Sachs Alternative Premia Fund – Class R6 Shares | |

| | 81,580 | | | | N/A | | | $ | 668,141 | |

| Goldman Sachs Managed Futures Strategy Fund –

Class R6 Shares |

|

| | 44,525 | | | | N/A | | | | 467,954 | |

| | Goldman Sachs Tactical Exposure Fund – Class R6 Shares | |

| | 72,995 | | | | N/A | | | | 690,536 | |

| | | | | | | | | | �� |

| | | | | | | | | 1,826,631 | |

| | |

| Equity – 11.0% | |

| Goldman Sachs Emerging Markets Equity Fund –

Class R6 Shares |

|

| | 11,236 | | | | N/A | | | | 241,910 | |

| | Goldman Sachs Global Infrastructure Fund – Class R6 Shares | |

| | 13,642 | | | | N/A | | | | 154,842 | |

| Goldman Sachs International Real Estate Securities Fund –

Class R6 Shares |

|

| | 9,995 | | | | N/A | | | | 63,471 | |

| | Goldman Sachs Real Estate Securities Fund – Class R6 Shares | |

| | 2,133 | | | | N/A | | | | 32,128 | |

| | | | | | | | | | |

| | | | | | | | | 492,351 | |

| | |

| Fixed Income – 48.5% | |

| | Goldman Sachs Emerging Markets Debt Fund – Class R6 Shares | |

| | 3,890 | | | | 4.494 | % | | | 47,220 | |

| Goldman Sachs Financial Square Government Fund –

Institutional Shares |

|

| | 982,153 | | | | 2.464 | | | | 982,153 | |

| Goldman Sachs Local Emerging Markets Debt Fund –

Class R6 Shares |

|

| | 39,786 | | | | 4.996 | | | | 227,576 | |

| Goldman SachsShort-Term Conservative Income Fund –

Class R6 Shares |

|

| | 91,913 | | | | 2.822 | | | | 922,803 | |

| | | | | | | | | | |

| | | | | | | | | 2,179,752 | |

| | |

| | TOTAL INVESTMENT COMPANIES | |

| | (Cost $4,519,936) | | | $ | 4,498,734 | |

| | |

| | TOTAL INVESTMENTS – 100.1% | |

| | (Cost $4,519,936) | | | $ | 4,498,734 | |

| | |

| LIABILITIES IN EXCESS OF

OTHER ASSETS – (0.1)% |

| | | (4,142 | ) |

| | |

| | NET ASSETS – 100.0% | | | $ | 4,494,592 | |

| | |

| | |

|

| The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. |

| |

(a) | | Represents affiliated funds. |

| | |

|

Currency Abbreviations: |

AUD | | —Australian Dollar |

CAD | | —Canadian Dollar |

CHF | | —Swiss Franc |

DKK | | —Danish Krone |

EUR | | —Euro |

GBP | | —British Pound |

HKD | | —Hong Kong Dollar |

JPY | | —Japanese Yen |

SEK | | —Swedish Krona |

USD | | —U.S. Dollar |

|

Investment Abbreviations: |

PLC | | —Public Limited Company |

|

| | |

| The accompanying notes are an integral part of these financial statements. | | 11 |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Schedule of Investments(continued)

April 30, 2019 (Unaudited)

|

| ADDITIONAL INVESTMENT INFORMATION |

FORWARD FOREIGN CURRENCY EXCHANGE CONTRACTS — At April 30, 2019, the Fund had the following forward foreign currency exchange contracts:

FORWARD FOREIGN CURRENCY EXCHANGE CONTRACTS WITH UNREALIZED GAIN

| | | | | | | | | | | | | | | | | | | | |

| Counterparty | | Currency

Purchased | | | Currency Sold | | | Settlement

Date | | | Unrealized

Gain | |

MS & Co. Int. PLC | | USD | | | 20,123 | | | CHF | | | 20,000 | | | | 06/19/19 | | | $ | 398 | |

| | USD | | | 4,593 | | | DKK | | | 30,000 | | | | 06/19/19 | | | | 65 | |

| | USD | | | 79,884 | | | EUR | | | 70,000 | | | | 06/19/19 | | | | 1,031 | |

| | USD | | | 46,319 | | | GBP | | | 35,000 | | | | 06/19/19 | | | | 557 | |

| | USD | | | 7,667 | | | HKD | | | 60,000 | | | | 06/19/19 | | | | 13 | |

| | USD | | | 63,176 | | | JPY | | | 7,000,000 | | | | 06/19/19 | | | | 77 | |

| | | USD | | | 8,139 | | | SEK | | | 75,000 | | | | 06/19/19 | | | | 210 | |

| | | | | | |

| TOTAL | | | | | | | | | | | | | | | | | | $ | 2,351 | |

FORWARD FOREIGN CURRENCY EXCHANGE CONTRACTS WITH UNREALIZED LOSS

| | | | | | | | | | | | | | | | | | | | |

| Counterparty | | Currency

Purchased | | | Currency Sold | | | Settlement

Date | | | Unrealized

Loss | |

MS & Co. Int. PLC | | USD | | | 14,074 | | | AUD | | | 20,000 | | | | 06/19/19 | | | $ | (42 | ) |

| | | USD | | | 22,375 | | | CAD | | | 30,000 | | | | 06/19/19 | | | | (48 | ) |

| | | | | | |

| TOTAL | | | | | | | | | | | | | | | | | | $ | (90 | ) |

FUTURES CONTRACTS — At April 30, 2019, the Fund had the following futures contracts:

| | | | | | | | | | | | | | | | |

| Description | | Number of

Contracts | | | Expiration

Date | | | Notional

Amount | | | Unrealized

Appreciation/

(Depreciation) | |

Long position contracts: | | | | | | | | | | | | | | | | |

10 Year U.S. Treasury Notes | | | 5 | | | | 06/19/19 | | | $ | 618,359 | | | $ | 7,850 | |

Mini MSCI EAFE Index | | | 1 | | | | 06/21/19 | | | | 95,850 | | | | 4,548 | |

S&P 500E-Mini Index | | | 1 | | | | 06/21/19 | | | | 147,425 | | | | 3,361 | |

| | | | |

| Total | | | | | | | | | | | | | | $ | 15,759 | |

Short position contracts: | | | | | | | | | | | | | | | | |

Eurodollars | | | (10 | ) | | | 09/14/20 | | | | (2,445,750 | ) | | | (9,273 | ) |

MSCI Emerging Markets Index | | | (1 | ) | | | 06/21/19 | | | | (54,010 | ) | | | 168 | |

| | | | |

| Total | | | | | | | | | | | | | | $ | (9,105 | ) |

| | | | |

| TOTAL FUTURES CONTRACTS | | | | | | | | | | | | | | $ | 6,654 | |

| | |

| 12 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

|

| ADDITIONAL INVESTMENT INFORMATION (continued) |

SWAP CONTRACTS — At April 30, 2019, the Fund had the following swap contracts:

CENTRALLY CLEARED CREDIT DEFAULT SWAP CONTRACT

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Referenced Obligation/Index | | Financing Rate

Received/

(Paid) by the

Fund(a) | | Credit

Spread at

April 30,

2019(b) | | | Termination

Date | | | Notional

Amount

(000s) | | | Value | | | Upfront

Premiums

(Received)

Paid | | | Unrealized

Appreciation/

(Depreciation) | |

Protection Sold: | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

CDX.NA.HY Index 32 | | 5.000% | | | 3.251% | | | | 06/20/24 | | | $ | 560 | | | $ | 46,023 | | | $ | 34,293 | | | $ | 11,730 | |

| | (a) | | Payments made quarterly. |

| | (b) | | Credit spread on the referenced obligation, together with the term of the swap contract, are indicators of payment/performance risk. The likelihood of a credit event occurring which would require a fund or its counterparty to make a payment or otherwise be required to perform under the swap contract is generally greater as the credit spread and the term of the swap contract increase. |

OVER THE COUNTER TOTAL RETURN SWAP CONTRACTS

| | | | | | | | | | | | | | |

| Reference Obligation/Index | | Financing Rate

Paid by the

Fund(a) | | Counterparty | | Termination

Date(b) | | Notional

Amount

(000s) | | | Unrealized

Appreciation/

(Depreciation)* | |

| | | | | |

MSCBCSSB Index(c) | | 0.200% | | MS & Co. Int. PLC | | 09/16/19 | | $ | 952 | | | $ | (15,035 | ) |

| | * | | There are no upfront payments on the swap contracts, therefore the unrealized gain (loss) on the swap contracts is equal to their market value. |

| | (a) | | Payments made semi-annually. |

| | (b) | | The Fund pays/receives annual coupon payments in accordance with the swap contract(s). On the termination date of the swap contract(s), the Fund will either receive from or pay to the counterparty an amount equal to the net of the accrued financing fees and the value of the reference security subtracted from the original notional cost (notional multiplied by the price change of the reference security, converted to U.S. Dollars). |

| | (c) | | The components are shown below. |

A basket (MSCBCSSB) of options on equity indices

| | | | | | | | | | | | | | | | | | | | |

| Description | | Strike

Price | | | Expiration

Date | | | Contracts | | | Value | | | Weight | |

Call - S&P 500 Index | | $ | 2,985 | | | | 05/31/2019 | | | | 104 | | | $ | (1,593 | ) | | | 10.59 | % |

Put - S&P 500 Index | | | 2,890 | | | | 05/31/2019 | | | | 81 | | | | (1,592 | ) | | | 10.59 | |

Call - S&P 500 Index | | | 2,925 | | | | 05/03/2019 | | | | 28 | | | | (719 | ) | | | 4.78 | |

Put - S&P 500 Index | | | 2,830 | | | | 05/03/2019 | | | | 1,198 | | | | (719 | ) | | | 4.78 | |

Call - S&P 500 Index | | | 2,930 | | | | 05/10/2019 | | | | 25 | | | | (717 | ) | | | 4.77 | |

Put - S&P 500 Index | | | 2,840 | | | | 05/10/2019 | | | | 205 | | | | (717 | ) | | | 4.77 | |

Call - S&P 500 Index | | | 2,940 | | | | 05/17/2019 | | | | 25 | | | | (713 | ) | | | 4.74 | |

Put - S&P 500 Index | | | 2,850 | | | | 05/17/2019 | | | | 94 | | | | (713 | ) | | | 4.74 | |

Call - S&P 500 Index | | | 2,970 | | | | 05/24/2019 | | | | 40 | | | | (706 | ) | | | 4.70 | |

Put - S&P 500 Index | | | 2,875 | | | | 05/24/2019 | | | | 51 | | | | (706 | ) | | | 4.70 | |

Call - Euro Stoxx 50 Index | | | 3,375 | | | | 05/17/2019 | | | | 6 | | | | (638 | ) | | | 4.25 | |

Put - Euro Stoxx 50 Index | | | 3,200 | | | | 05/17/2019 | | | | 375 | | | | (638 | ) | | | 4.25 | |

Call - S&P 500 Index | | | 2,895 | | | | 05/31/2019 | | | | 9 | | | | (635 | ) | | | 4.22 | |

Put - S&P 500 Index | | | 2,730 | | | | 05/31/2019 | | | | 109 | | | | (635 | ) | | | 4.22 | |

Call - S&P 500 Index | | | 3,010 | | | | 06/28/2019 | | | | 28 | | | | (598 | ) | | | 3.98 | |

Put - S&P 500 Index | | | 2,870 | | | | 06/28/2019 | | | | 19 | | | | (598 | ) | | | 3.98 | |

Call - Euro Stoxx 50 Index | | | 3,500 | | | | 06/21/2019 | | | | 16 | | | | (597 | ) | | | 3.97 | |

Put - Euro Stoxx 50 Index | | | 3,325 | | | | 06/21/2019 | | | | 23 | | | | (597 | ) | | | 3.97 | |

Call - Euro Stoxx 50 Index | | | 3,450 | | | | 05/10/2019 | | | | 3 | | | | (152 | ) | | | 1.01 | |

Put - Euro Stoxx 50 Index | | | 3,350 | | | | 05/10/2019 | | | | 66 | | | | (152 | ) | | | 1.01 | |

Call - Euro Stoxx 50 Index | | | 3,475 | | | | 05/03/2019 | | | | 5 | | | | (152 | ) | | | 1.01 | |

Put - Euro Stoxx 50 Index | | | 3,375 | | | | 05/03/2019 | | | | 217 | | | | (152 | ) | | | 1.01 | |

Call - Euro Stoxx 50 Index | | | 3,500 | | | | 05/17/2019 | | | | 7 | | | | (149 | ) | | | 0.99 | |

Put - Euro Stoxx 50 Index | | | 3,400 | | | | 05/17/2019 | | | | 14 | | | | (149 | ) | | | 0.99 | |

Call - Euro Stoxx 50 Index | | | 3,500 | | | | 05/24/2019 | | | | 6 | | | | (149 | ) | | | 0.99 | |

Put - Euro Stoxx 50 Index | | | 3,400 | | | | 05/24/2019 | | | | 8 | | | | (149 | ) | | | 0.99 | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 13 |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Schedule of Investments(continued)

April 30, 2019 (Unaudited)

|

| ADDITIONAL INVESTMENT INFORMATION (continued) |

PURCHASED OPTIONS CONTRACTS — At April 30, 2019, the Fund had the following purchased options:

EXCHANGE TRADED OPTIONS ON FUTURES

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Description | | | | Exercise

Price | | Expiration

Date | | | Number of

Contracts | | | Notional

Amount | | | Market

Value | | | Premiums Paid

(Received) by

Portfolio | | | Unrealized

Appreciation/

(Depreciation) | |

Purchased option contracts | | | | | | | | | | | | | | | | | |

Calls | | | | | | | | | | | | | | | | | |

Eurodollar Futures | | | | $97.75 | | | 06/17/2019 | | | | 1 | | | $ | 2,500 | | | $ | 6 | | | $ | 2,752 | | | $ | (2,746 | ) |

Eurodollar Futures | | | | 99.00 | | | 06/17/2019 | | | | 2 | | | | 5,000 | | | | 13 | | | | 205 | | | | (192 | ) |

Eurodollar Futures | | | | 97.75 | | | 09/16/2019 | | | | 1 | | | | 2,500 | | | | 75 | | | | 627 | | | | (552 | ) |

Eurodollar Futures | | | | 97.50 | | | 06/15/2020 | | | | 6 | | | | 15,000 | | | | 5,475 | | | | 3,813 | | | | 1,662 | |

Eurodollar Futures | | | | 97.50 | | | 09/14/2020 | | | | 6 | | | | 15,000 | | | | 6,675 | | | | 4,658 | | | | 2,017 | |

Eurodollar Futures | | | | 97.50 | | | 12/14/2020 | | | | 6 | | | | 15,000 | | | | 7,237 | | | | 5,722 | | | | 1,515 | |

Eurodollar Futures | | | | 97.00 | | | 03/15/2021 | | | | 1 | | | | 2,500 | | | | 2,263 | | | | 1,790 | | | | 473 | |

Eurodollar Futures | | | | 97.50 | | | 03/15/2021 | | | | 6 | | | | 15,000 | | | | 7,950 | | | | 6,765 | | | | 1,185 | |

Eurodollar Futures | | | | 97.00 | | | 06/14/2021 | | | | 1 | | | | 2,500 | | | | 2,268 | | | | 1,852 | | | | 416 | |

Eurodollar Futures | | | | 97.50 | | | 06/14/2021 | | | | 5 | | | | 12,500 | | | | 6,813 | | | | 5,833 | | | | 980 | |

Eurodollar Futures | | | | 98.00 | | | 06/14/2021 | | | | 3 | | | | 7,500 | | | | 2,288 | | | | 2,444 | | | | (156 | ) |

Eurodollar Futures | | | | 97.00 | | | 09/13/2021 | | | | 1 | | | | 2,500 | | | | 2,293 | | | | 2,452 | | | | (159 | ) |

Eurodollar Futures | | | | 98.00 | | | 09/13/2021 | | | | 7 | | | | 17,500 | | | | 5,644 | | | | 6,512 | | | | (868 | ) |

| | | | | | | | |

| TOTAL | | | | | | | | | | | 46 | | | $ | 115,000 | | | $ | 49,000 | | | $ | 45,425 | | | $ | 3,575 | |

| | |

|

Abbreviations: |

CDX.NA.HY Index 32 | | —CDX North America High Yield Index 32 |

MS & Co. Int. PLC | | —Morgan Stanley & Co. International PLC |

|

| | |

| 14 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Statement of Assets and Liabilities

April 30, 2019 (Unaudited)

| | | | | | |

| | | | | | |

| | Assets: | |

| | Investments of affiliated issuers, at value (cost $4,519,936) | | $ | 4,498,734 | |

| | Purchased options, at value (cost $45,425) | | | 49,000 | |

| | Cash | | | 68,693 | |

| | Foreign currencies, at value (cost $35,969) | | | 36,059 | |

| | Unrealized gain on forward foreign currency exchange contracts | | | 2,351 | |

| | Variation margin on futures contracts | | | 753 | |

| | Variation margin on swap contracts | | | 416 | |

| | Receivables: | | | | |

| | Reimbursement from investment adviser | | | 44,739 | |

| | Collateral on certain derivative contracts(a) | | | 35,207 | |

| | Dividends and interest | | | 5,142 | |

| | Foreign tax reclaims | | | 1,001 | |

| | Other assets | | | 59,123 | |

| | Total assets | | | 4,801,218 | |

| | | | | | |

| | Liabilities: | |

| | Unrealized loss on swap contracts | | | 15,035 | |

| | Unrealized loss on forward foreign currency exchange contracts | | | 90 | |

| | Payables: | | | | |

| | Investments purchased | | | 5,142 | |

| | Fund shares redeemed | | | 1,450 | |

| | Management fees | | | 1,059 | |

| | Distribution and service fees and transfer agency fees | | | 1,029 | |

| | Collateral on certain derivative contracts(b) | | | 157 | |

| | Accrued expenses | | | 282,664 | |

| | Total liabilities | | | 306,626 | |

| | | | | | |

| | Net Assets: | |

| | Paid-in capital | | | 4,896,692 | |

| | Total distributable earnings (loss) | | | (402,100 | ) |

| | | NET ASSETS | | $ | 4,494,592 | |

| | | Net Assets: | | | | |

| | | Class A | | $ | 2,643,594 | |

| | | Class C | | | 24,257 | |

| | | Institutional | | | 1,502,418 | |

| | | Investor | | | 25,157 | |

| | | Class P | | | 249,152 | |

| | | Class R | | | 24,703 | |

| | | Class R6 | | | 25,311 | |

| | | Total Net Assets | | $ | 4,494,592 | |

| | | Shares Outstanding $0.001 par value (unlimited number of shares authorized): | | | | |

| | | Class A | | | 278,284 | |

| | | Class C | | | 2,572 | |

| | | Institutional | | | 157,035 | |

| | | Investor | | | 2,640 | |

| | | Class P | | | 26,124 | |

| | | Class R | | | 2,603 | |

| | | Class R6 | | | 2,654 | |

| | | Net asset value, offering and redemption price per share:(c) | | | | |

| | | Class A | | | $9.50 | |

| | | Class C | | | 9.43 | |

| | | Institutional | | | 9.57 | |

| | | Investor | | | 9.53 | |

| | | Class P | | | 9.54 | |

| | | Class R | | | 9.49 | |

| | | Class R6 | | | 9.54 | |

| | (a) | | Includes amounts segregated for initial margin and/or collateral on futures transactions, options and swaps transactions of $4,087, $53 and $31,067, respectively, for the Fund. |

| | (b) | | Includes amounts segregated for collateral on swaps transactions. |

| | (c) | | Maximum public offering price per share for Class A Shares is $10.05. At redemption, Class C Shares may be subject to a contingent deferred sales charge, assessed on the amount equal to the lesser of the current net asset value ("NAV") or the original purchase price of the shares. |

| | |

| The accompanying notes are an integral part of these financial statements. | | 15 |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Statement of Operations

For the Six Months Ended April 30, 2019 (Unaudited)

| | | | | | |

| | Investment income: | |

| | |

| | Dividends — affiliated issuers | | $ | 40,280 | |

| | |

| | Interest | | | 2,118 | |

| | |

| | Total investment income | | | 42,398 | |

| | | | | | |

| | Expenses: | |

| | |

| | Professional fees | | | 81,452 | |

| | |

| | Custody, accounting and administrative services | | | 80,004 | |

| | |

| | Registration fees | | | 57,999 | |

| | |

| | Printing and mailing costs | | | 37,240 | |

| | |

| | Management fees | | | 20,314 | |

| | |

| | Trustee fees | | | 7,925 | |

| | |

| | Distribution and Service fees(a) | | | 3,472 | |

| | |

| | Transfer Agency fees(a) | | | 2,838 | |

| | |

| | Other | | | 8,284 | |

| | |

| | Total expenses | | | 299,528 | |

| | |

| | Less — expense reductions | | | (288,016 | ) |

| | |

| | Net expenses | | | 11,512 | |

| | |

| | NET INVESTMENT INCOME | | | 30,886 | |

| | | | | | |

| | Realized and unrealized gain (loss): | |

| | |

| | Capital gain distributions from Affiliated Underlying Funds | | | 61,305 | |

| | |

| | Net realized gain (loss) from: | | | | |

| | |

| | Investments — affiliated issuers | | | (45,379 | ) |

| | |

| | Purchased options | | | 11,923 | |

| | |

| | Futures contracts | | | 9,471 | |

| | |

| | Written options | | | 6 | |

| | |

| | Swap contracts | | | (42,740 | ) |

| | |

| | Forward foreign currency exchange contracts | | | 6,434 | |

| | |

| | Foreign currency transactions | | | (580 | ) |

| | |

| | Net change in unrealized gain (loss) on: | | | | |

| | |

| | Investments — unaffiliated issuers | | | 46 | |

| | |

| | Investments — affiliated issuers | | | 86,642 | |

| | |

| | Purchased options | | | 29,066 | |

| | |

| | Futures contracts | | | 17,020 | |

| | |

| | Swap contracts | | | 35,509 | |

| | |

| | Forward foreign currency exchange contracts | | | (2,909 | ) |

| | |

| | Foreign currency translation | | | (1,231 | ) |

| | |

| | Net realized and unrealized gain | | | 164,583 | |

| | |

| | NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 195,469 | |

| | (a) | | Class specific Distribution and/or Service and Transfer Agency fees were as follows: |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Distribution and/or Service Fees | | | Transfer Agency Fees | |

Class A | | | Class C | | | Class R | | | Class A | | | Class C | | | Institutional | | | Investor | | | Class P | | | Class R | | | Class R6 | |

| $ | 3,295 | | | $ | 117 | | | $ | 60 | | | $ | 2,372 | | | $ | 21 | | | $ | 362 | | | $ | 22 | | | $ | 36 | | | $ | 22 | | | $ | 4 | |

| | |

| 16 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Statements of Changes in Net Assets

| | | | | | | | | | |

| | | | | For the Six

Months Ended

April 30, 2019

(Unaudited) | | | For the Fiscal

Year Ended

October 31, 2018 | |

| | From operations: | |

| | | |

| | Net investment income | | $ | 30,886 | | | $ | 332,305 | |

| | | |

| | Net realized gain (loss) | | | 440 | | | | (407,275 | ) |

| | | |

| | Net change in unrealized gain (loss) | | | 164,143 | | | | (667,911 | ) |

| | | |

| | Net increase (decrease) in net assets resulting from operations | | | 195,469 | | | | (742,881 | ) |

| | | | | | | | | | |

| | Distributions to shareholders: | | | | | | | | |

| |

| | From distributable earnings | |

| | | |

| | Class A Shares | | | (85,274 | ) | | | (9,391 | ) |

| | | |

| | Class C Shares | | | (569 | ) | | | — | |

| | | |

| | Institutional Shares | | | (57,789 | ) | | | (102,701 | ) |

| | | |

| | Investor Shares | | | (823 | ) | | | (63 | ) |

| | | |

| | Class P Shares(a) | | | (8,528 | ) | | | — | |

| | | |

| | Class R Shares | | | (693 | ) | | | — | |

| | | |

| | Class R6 Shares | | | (864 | ) | | | (105 | ) |

| | | |

| | Total distributions to shareholders | | | (154,540 | ) | | | (112,260 | ) |

| | | | | | | | | | |

| | From share transactions: | | | | | | | | |

| | | |

| | Proceeds from sales of shares | | | 612,982 | | | | 1,584,140 | |

| | | |

| | Reinvestment of distributions | | | 151,936 | | | | 111,949 | |

| | | |

| | Cost of shares redeemed | | | (1,226,116 | ) | | | (26,178,033 | ) |

| | | |

| | Net decrease in net assets resulting from share transactions | | | (461,198 | ) | | | (24,481,944 | ) |

| | | |

| | TOTAL DECREASE | | | (420,269 | ) | | | (25,337,085 | ) |

| | | | | | | | | | |

| | Net assets: | | | | | | | | |

| | | |

| | Beginning of period | | | 4,914,861 | | | | 30,251,946 | |

| | | |

| | End of period | | $ | 4,494,592 | | | $ | 4,914,861 | |

| | (a) | | Commenced operations on April 16, 2018. |

| | |

| The accompanying notes are an integral part of these financial statements. | | 17 |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Financial Highlights

Selected Share Data for a Share Outstanding Throughout Each Period

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | Goldman Sachs Absolute Return Multi-Asset Fund | |

| | | | | Class A Shares | |

| | | | | Six Months Ended

April 30, 2019

(Unaudited) | | | Year Ended October 31, | | | Period Ended

October 31,

2015(a) | |

| | | | | 2018 | | | 2017 | | | 2016 | |

| | Per Share Data | |

| | | | | | |

| | Net asset value, beginning of period | | $ | 9.43 | | | $ | 10.00 | | | $ | 9.75 | | | $ | 9.93 | | | $ | 10.00 | |

| | | | | | |

| | Net investment income (loss)(b) | | | 0.05 | | | | 0.09 | | | | — | (c) | | | 0.05 | | | | (0.01 | ) |

| | | | | | |

| | Net realized and unrealized gain (loss) | | | 0.31 | | | | (0.64 | ) | | | 0.34 | | | | (0.19 | ) | | | (0.06 | ) |

| | | | | | |

| | Total from investment operations | | | 0.36 | | | | (0.55 | ) | | | 0.34 | | | | (0.14 | ) | | | (0.07 | ) |

| | | | | | |

| | Distributions to shareholders from net investment income | | | (0.29 | ) | | | (0.02 | ) | | | (0.09 | ) | | | (0.04 | ) | | | — | |

| | | | | | |

| | Net asset value, end of period | | $ | 9.50 | | | $ | 9.43 | | | $ | 10.00 | | | $ | 9.75 | | | $ | 9.93 | |

| | | | | | |

| | Total return(d) | | | 4.01 | % | | | (5.46 | )% | | | 3.54 | % | | | (1.36 | )% | | | (0.70 | )% |

| | | | | | |

| | Net assets, end of period (in 000s) | | $ | 2,644 | | | $ | 2,804 | | | $ | 3,909 | | | $ | 83 | | | $ | 25 | |

| | | | | | |

| | Ratio of net expenses to average net assets(e) | | | 0.64 | %(f) | | | 0.94 | % | | | 1.05 | % | | | 0.79 | % | | | 1.23 | %(f) |

| | | | | | |

| | Ratio of total expenses to average net assets(e) | | | 12.63 | %(f) | | | 6.36 | % | | | 3.21 | % | | | 5.28 | %(g) | | | 3.81 | %(f) |

| | | | | | |

| | Ratio of net investment income (loss) to average net assets | | | 1.14 | %(f) | | | 0.96 | % | | | (0.01 | )% | | | 0.53 | % | | | (0.36 | )%(f) |

| | | | | | |

| | Portfolio turnover rate(h) | | | 41 | % | | | 228 | % | | | 96 | % | | | 38 | % | | | 1 | % |

| | (a) | | Commenced operations on September 2, 2015. |

| | (b) | | Calculated based on the average shares outstanding methodology. |

| | (c) | | Amount is less than $0.005 per share. |

| | (d) | | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. Total returns for periods less than one full year are not annualized. |

| | (e) | | Expense ratios exclude the expenses of the Underlying Funds in which the Fund invests. |

| | (g) | | The amount previously reported as 4.01% has been corrected to include certain professional fees. |

| | (h) | | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| | |

| 18 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Financial Highlights(continued)

Selected Share Data for a Share Outstanding Throughout Each Period

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | Goldman Sachs Absolute Return Multi-Asset Fund | |

| | | | | Class C Shares | |

| | | | | Six Months Ended

April 30, 2019

(Unaudited) | | | Year Ended October 31, | | | Period Ended

October 31,

2015(a) | |

| | | | | 2018 | | | 2017 | | | 2016 | |

| | Per Share Data | |

| | | | | | |

| | Net asset value, beginning of period | | $ | 9.33 | | | $ | 9.94 | | | $ | 9.68 | | | $ | 9.92 | | | $ | 10.00 | |

| | | | | | |

| | Net investment income (loss)(b) | | | 0.02 | | | | 0.01 | | | | (0.06 | ) | | | — | (c) | | | (0.02 | ) |

| | | | | | |

| | Net realized and unrealized gain (loss) | | | 0.31 | | | | (0.62 | ) | | | 0.34 | | | | (0.22 | ) | | | (0.06 | ) |

| | | | | | |

| | Total from investment operations | | | 0.33 | | | | (0.61 | ) | | | 0.28 | | | | (0.22 | ) | | | (0.08 | ) |

| | | | | | |

| | Distributions to shareholders from net investment income | | | (0.23 | ) | | | — | | | | (0.02 | ) | | | (0.02 | ) | | | — | |

| | | | | | |

| | Net asset value, end of period | | $ | 9.43 | | | $ | 9.33 | | | $ | 9.94 | | | $ | 9.68 | | | $ | 9.92 | |

| | | | | | |

| | Total return(d) | | | 3.61 | % | | | (6.14 | )% | | | 2.75 | % | | | (2.01 | )% | | | (0.90 | )% |

| | | | | | |

| | Net assets, end of period (in 000s) | | $ | 24 | | | $ | 23 | | | $ | 25 | | | $ | 24 | | | $ | 26 | |

| | | | | | |

| | Ratio of net expenses to average net assets(e) | | | 1.40 | %(f) | | | 1.68 | % | | | 1.80 | % | | | 1.65 | % | | | 1.98 | %(f) |

| | | | | | |

| | Ratio of total expenses to average net assets(e) | | | 13.38 | %(f) | | | 7.45 | % | | | 4.05 | % | | | 5.73 | %(g) | | | 4.55 | %(f) |

| | | | | | |

| | Ratio of net investment income (loss) to average net assets | | | 0.36 | %(f) | | | 0.15 | % | | | (0.59 | )% | | | (0.02 | )% | | | (1.10 | )%(f) |

| | | | | | |

| | Portfolio turnover rate(h) | | | 41 | % | | | 228 | % | | | 96 | % | | | 38 | % | | | 1 | % |

| | (a) | | Commenced operations on September 2, 2015. |

| | (b) | | Calculated based on the average shares outstanding methodology. |

| | (c) | | Amount is less than ($0.005) per share. |

| | (d) | | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. Total returns for periods less than one full year are not annualized. |

| | (e) | | Expense ratios exclude the expenses of the Underlying Funds in which the Fund invests. |

| | (g) | | The amount previously reported as 4.46% has been corrected to include certain professional fees. |

| | (h) | | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| | |

| The accompanying notes are an integral part of these financial statements. | | 19 |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Financial Highlights(continued)

Selected Share Data for a Share Outstanding Throughout Each Period

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | Goldman Sachs Absolute Return Multi-Asset Fund | |

| | | | | Institutional | |

| | | | | Six Months Ended

April 30, 2019

(Unaudited) | | | Year Ended October 31, | | | Period Ended

October 31,

2015(a) | |

| | | | | 2018 | | | 2017 | | | 2016 | |

| | Per Share Data | |

| | | | | | |

| | Net asset value, beginning of period | | $ | 9.49 | | | $ | 10.04 | | | $ | 9.78 | | | $ | 9.94 | | | $ | 10.00 | |

| | | | | | |

| | Net investment income(b) | | | 0.07 | | | | 0.15 | | | | 0.05 | | | | 0.11 | | | | 0.00 | (c) |

| | | | | | |

| | Net realized and unrealized gain (loss) | | | 0.32 | | | | (0.66 | ) | | | 0.34 | | | | (0.21 | ) | | | (0.06 | ) |

| | | | | | |

| | Total from investment operations | | | 0.39 | | | | (0.51 | ) | | | 0.39 | | | | (0.10 | ) | | | (0.06 | ) |

| | | | | | |

| | Distributions to shareholders from net investment income | | | (0.31 | ) | | | (0.04 | ) | | | (0.13 | ) | | | (0.06 | ) | | | — | |

| | | | | | |

| | Net asset value, end of period | | $ | 9.57 | | | $ | 9.49 | | | $ | 10.04 | | | $ | 9.78 | | | $ | 9.94 | |

| | | | | | |

| | Total return(d) | | | 4.22 | % | | | (5.11 | )% | | | 4.02 | % | | | (0.93 | )% | | | (0.70 | )% |

| | | | | | |

| | Net assets, end of period (in 000s) | | $ | 1,502 | | | $ | 1,776 | | | $ | 26,242 | | | $ | 24,542 | | | $ | 24,718 | |

| | | | | | |

| | Ratio of net expenses to average net assets(e) | | | 0.26 | %(f) | | | 0.57 | % | | | 0.65 | % | | | 0.49 | % | | | 0.82 | %(f) |

| | | | | | |

| | Ratio of total expenses to average net assets(e) | | | 12.23 | %(f) | | | 3.06 | % | | | 2.91 | % | | | 4.58 | %(g) | | | 3.40 | %(f) |

| | | | | | |

| | Ratio of net investment income to average net assets | | | 1.49 | %(f) | | | 1.48 | % | | | 0.55 | % | | | 1.13 | % | | | 0.04 | %(f) |

| | | | | | |

| | Portfolio turnover rate(h) | | | 41 | % | | | 228 | % | | | 96 | % | | | 38 | % | | | 1 | % |

| | (a) | | Commenced operations on September 2, 2015. |

| | (b) | | Calculated based on the average shares outstanding methodology. |

| | (c) | | Amount is less than $0.005 per share. |

| | (d) | | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. Total returns for periods less than one full year are not annualized. |

| | (e) | | Expense ratios exclude the expenses of the Underlying Funds in which the Fund invests. |

| | (g) | | The amount previously reported as 3.31% has been corrected to include certain professional fees. |

| | (h) | | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| | |

| 20 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Financial Highlights(continued)

Selected Share Data for a Share Outstanding Throughout Each Period

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | Goldman Sachs Absolute Return Multi-Asset Fund | |

| | | | | Investor Shares | |

| | | | | Six Months Ended

April 30, 2019

(Unaudited) | | | Year Ended October 31, | | | Period Ended

October 31,

2015(a) | |

| | | | | 2018 | | | 2017 | | | 2016 | |

| | Per Share Data | |

| | | | | | |

| | Net asset value, beginning of period | | $ | 9.48 | | | $ | 10.02 | | | $ | 9.76 | | | $ | 9.93 | | | $ | 10.00 | |

| | | | | | |

| | Net investment income(b) | | | 0.06 | | | | 0.11 | | | | 0.04 | | | | 0.10 | | | | — | (c) |

| | | | | | |

| | Net realized and unrealized gain (loss) | | | 0.31 | | | | (0.63 | ) | | | 0.33 | | | | (0.22 | ) | | | (0.07 | ) |

| | | | | | |

| | Total from investment operations | | | 0.37 | | | | (0.52 | ) | | | 0.37 | | | | (0.12 | ) | | | (0.07 | ) |

| | | | | | |

| | Distributions to shareholders from net investment income | | | (0.32 | ) | | | (0.02 | ) | | | (0.11 | ) | | | (0.05 | ) | | | — | |

| | | | | | |

| | Net asset value, end of period | | $ | 9.53 | | | $ | 9.48 | | | $ | 10.02 | | | $ | 9.76 | | | $ | 9.93 | |

| | | | | | |

| | Total return(d) | | | 4.10 | % | | | (5.25 | )% | | | 3.97 | % | | | (1.18 | )% | | | (0.70 | )% |

| | | | | | |

| | Net assets, end of period (in 000s) | | $ | 25 | | | $ | 24 | | | $ | 25 | | | $ | 25 | | | $ | 25 | |

| | | | | | |

| | Ratio of net expenses to average net assets(e) | | | 0.40 | %(f) | | | 0.68 | % | | | 0.80 | % | | | 0.65 | % | | | 0.98 | %(f) |

| | | | | | |

| | Ratio of total expenses to average net assets(e) | | | 12.39 | %(f) | | | 6.43 | % | | | 3.05 | % | | | 4.74 | %(g) | | | 3.57 | %(f) |

| | | | | | |

| | Ratio of net investment income to average net assets | | | 1.36 | %(f) | | | 1.15 | % | | | 0.41 | % | | | 0.98 | % | | | (0.11 | )%(f) |

| | | | | | |

| | Portfolio turnover rate(h) | | | 41 | % | | | 228 | % | | | 96 | % | | | 38 | % | | | 1 | % |

| | (a) | | Commenced operations on September 2, 2015. |

| | (b) | | Calculated based on the average shares outstanding methodology. |

| | (c) | | Amount is less than ($0.005) per share. |

| | (d) | | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. Total returns for periods less than one full year are not annualized. |

| | (e) | | Expense ratios exclude the expenses of the Underlying Funds in which the Fund invests. |

| | (g) | | The amount previously reported as 3.47% has been corrected to include certain professional fees. |

| | (h) | | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| | |

| The accompanying notes are an integral part of these financial statements. | | 21 |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Financial Highlights(continued)

Selected Share Data for a Share Outstanding Throughout Each Period

| | | | | | | | | | |

| | | | | Goldman Sachs Absolute Return

Multi-Asset Fund | |

| | | | | Class P Shares | |

| | | | | Six Months Ended

April 30, 2019

(Unaudited) | | | Period Ended

October 31,

2018(a) | |

| | | |

| | Per Share Data | |

| | | |

| | Net asset value, beginning of period | | $ | 9.49 | | | $ | 9.90 | |

| | | |

| | Net investment income(b) | | | 0.07 | | | | 0.06 | |

| | | |

| | Net realized and unrealized gain (loss) | | | 0.32 | | | | (0.47 | ) |

| | | |

| | Total from investment operations | | | 0.39 | | | | (0.41 | ) |

| | | |

| | Distributions to shareholders from net investment income | | | (0.34 | ) | | | — | |

| | | |

| | Net asset value, end of period | | $ | 9.54 | | | $ | 9.49 | |

| | | |

| | Total return(c) | | | 4.27 | % | | | (4.14 | )% |

| | | |

| | Net assets, end of period (in 000s) | | $ | 249 | | | $ | 239 | |

| | | |

| | Ratio of net expenses to average net assets(d)(e) | | | 0.25 | % | | | 0.31 | % |

| | | |

| | Ratio of total expenses to average net assets(d)(e) | | | 12.24 | % | | | 11.95 | % |

| | | |

| | Ratio of net investment income to average net assets(e) | | | 1.51 | % | | | 1.15 | % |

| | | |

| | Portfolio turnover rate(f) | | | 41 | % | | | 228 | % |

| | (a) | | Commenced operations on April 16, 2018. |

| | (b) | | Calculated based on the average shares outstanding methodology. |

| | (c) | | Assumes investment at the NAV at the beginning of the period, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the period and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. Total returns for periods less than one full year are not annualized. |

| | (d) | | Expense ratios exclude the expenses of the Underlying Funds in which the Fund invests. |

| | (f) | | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| | |

| 22 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Financial Highlights(continued)

Selected Share Data for a Share Outstanding Throughout Each Period

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | Goldman Sachs Absolute Return Multi-Asset Fund | |

| | | | | Class R Shares | |

| | | | | Six Months Ended

April 30, 2019

(Unaudited) | | | Year Ended October 31, | | | Period Ended

October 31,

2015(a) | |

| | | | | 2018 | | | 2017 | | | 2016 | |

| | Per Share Data | |

| | | | | | |

| | Net asset value, beginning of period | | $ | 9.41 | | | $ | 9.98 | | | $ | 9.72 | | | $ | 9.93 | | | $ | 10.00 | |

| | | | | | |

| | Net investment income (loss)(b) | | | 0.04 | | | | 0.06 | | | | (0.01 | ) | | | 0.05 | | | | (0.01 | ) |

| | | | | | |

| | Net realized and unrealized gain (loss) | | | 0.31 | | | | (0.63 | ) | | | 0.33 | | | | (0.22 | ) | | | (0.06 | ) |

| | | | | | |

| | Total from investment operations | | | 0.35 | | | | (0.57 | ) | | | 0.32 | | | | (0.17 | ) | | | (0.07 | ) |

| | | | | | |

| | Distributions to shareholders from net investment income | | | (0.27 | ) | | | — | | | | (0.06 | ) | | | (0.04 | ) | | | — | |

| | | | | | |

| | Net asset value, end of period | | $ | 9.49 | | | $ | 9.41 | | | $ | 9.98 | | | $ | 9.72 | | | $ | 9.93 | |

| | | | | | |

| | Total return(c) | | | 3.90 | % | | | (5.71 | )% | | | 3.36 | % | | | (1.64 | )% | | | (0.80 | )% |

| | | | | | |

| | Net assets, end of period (in 000s) | | $ | 25 | | | $ | 24 | | | $ | 25 | | | $ | 24 | | | $ | 25 | |

| | | | | | |

| | Ratio of net expenses to average net assets(d) | | | 0.90 | %(e) | | | 1.18 | % | | | 1.30 | % | | | 1.15 | % | | | 1.48 | %(e) |

| | | | | | |

| | Ratio of total expenses to average net assets(d) | | | 12.88 | %(e) | | | 6.96 | % | | | 3.56 | % | | | 5.24 | %(f) | | | 4.07 | %(e) |

| | | | | | |

| | Ratio of net investment income (loss) to average net assets | | | 0.86 | %(e) | | | 0.65 | % | | | (0.09 | )% | | | 0.48 | % | | | (0.62 | )%(e) |

| | | | | | |

| | Portfolio turnover rate(g) | | | 41 | % | | | 228 | % | | | 96 | % | | | 38 | % | | | 1 | % |

| | (a) | | Commenced operations on September 2, 2015. |

| | (b) | | Calculated based on the average shares outstanding methodology. |

| | (c) | | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. Total returns for periods less than one full year are not annualized. |

| | (d) | | Expense ratios exclude the expenses of the Underlying Funds in which the Fund invests. |

| | (f) | | The amount previously reported as 3.97% has been corrected to include certain professional fees. |

| | (g) | | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| | |

| The accompanying notes are an integral part of these financial statements. | | 23 |

GOLDMAN SACHS ABSOLUTE RETURN MULTI-ASSET FUND

Financial Highlights(continued)

Selected Share Data for a Share Outstanding Throughout Each Period

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | Goldman Sachs Absolute Return Multi-Asset Fund | |