|

| | |

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| WASHINGTON, D.C. 20549 |

| | | |

| | | |

FORM 10-K |

|

| |

| (Mark One) |

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | FOR THE FISCAL YEAR ENDED DECEMBER 31, 2012. |

| | OR |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | FOR THE TRANSITION PERIOD FROM TO |

| COMMISSION FILE NUMBER 1-9750 |

___________________________________________________________________

(Exact name of registrant as specified in its charter)

__________________________________________________________________

|

| | | | | | | |

| Delaware | 38-2478409 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 1334 York Avenue | 10021 |

| New York, New York | (Zip Code) |

| (Address of principal executive offices) | |

| | | |

| | (212) 606-7000 | |

| | (Registrant’s telephone number, including area code) | |

| | Securities registered pursuant to Section 12(b) of the Act: | |

| | | | | | | |

| | Title of each class | | | Name of each exchange on which registered | |

| | | | | | | | |

| | | | | | | | |

| | Common Stock, | | | New York Stock Exchange | |

| | $0.01 Par Value | | | | |

| | | | | | | | |

| | Securities registered pursuant to Section 12(g) of the Act: None | |

| | | | | | | | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Act during the preceding 12 months (or for such shorter periods that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company (as defined in Rule 12b-2 of the Act). Large accelerated filer þ Accelerated filer o Non-accelerated filer o (Do not check if a smaller reporting company) Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes o No þ

As of June 30, 2012, the aggregate market value of the 66,893,407 shares of Common Stock held by non-affiliates of the registrant was $2,231,564,057 based upon the closing price ($33.36) on the New York Stock Exchange composite tape on such date for the Common Stock.

As of February 19, 2013, there were outstanding 67,913,661 shares of Common Stock.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s proxy statement for the 2013 annual meeting of shareholders are incorporated by reference into Part III of this Form 10-K.

TABLE OF CONTENTS

PART I

ITEM 1: DESCRIPTION OF BUSINESS

Overview

Sotheby’s (or, “the Company”) is one of the two largest global auctioneers of authenticated fine art, decorative art, and jewelry (collectively, “art” or “works of art” or “artwork” or "property"). Sotheby's primary global auction competitor is Christie’s International, PLC, a privately held, French-owned, auction house. To a much lesser extent, Sotheby’s also faces competition from smaller auction houses such as Bonhams and Phillips, as well as regional auction houses and a variety of art dealers across all collecting categories. In the Chinese art market, Sotheby's also competes with Beijing Poly International Auction Co. Ltd., China Guardian Auctions Co. Ltd., and Beijing Hanhai Auction Co. Ltd. In 2012, Sotheby’s accounted for approximately $4.5 billion, or 46%, of the total aggregate auction sales of the two major auction houses within the global auction market.

Sotheby’s operations are organized under three segments: Auction, Finance, and Dealer. The Auction segment functions as an agent by offering works of art for sale at auction and by brokering private sales of artwork. Sotheby’s also purchases and resells works of art through its Dealer segment, conducts art-related financing activities through its Finance segment and is engaged, to a lesser extent, in brand licensing activities. A more detailed explanation of the activities of each of Sotheby’s segments, as well as its brand licensing activities, is provided below.

Sotheby’s was initially incorporated in Michigan in August 1983. In October 1983, the Company acquired Sotheby Parke Bernet Group Limited, which was then a publicly held company listed on the International Stock Exchange of the United Kingdom and which, through its predecessors, had been engaged in the auction business since 1744. In 1988, Sotheby’s issued shares of common stock to the public. In June 2006, Sotheby’s reincorporated in the State of Delaware. Sotheby's common stock ("Common Stock") is listed on the New York Stock Exchange (the “NYSE”) and trades under the symbol “BID.” As successor to the business that began in 1744, Sotheby’s is the oldest company listed on the NYSE.

Auction Segment

Description of Business

The sale of works of art in the international art market is primarily effected through the major auction houses, numerous art dealers, smaller auction houses and also directly between collectors. Although art dealers and smaller auction houses generally do not report sales figures publicly, Sotheby’s believes that art dealers account for the majority of the volume of transactions in the international art market.

Sotheby’s Auction segment functions as an agent by accepting property on consignment, stimulating buyer interest through professional marketing techniques, and matching sellers (also known as consignors) to buyers through the auction or private sale process. Prior to offering a work of art for sale, Sotheby’s experts perform significant due diligence activities to authenticate and determine the ownership history of the property being sold.

Following the sale, Sotheby's invoices the buyer for the purchase price of the property (including the commission owed by the buyer), collects payment from the buyer and remits to the consignor the net sale proceeds after deducting its commissions, expenses and applicable taxes and royalties. Sotheby's auction commissions include those paid by the buyer ("buyer's premium") and those paid by the seller ("seller's commission") (collectively, "auction commission revenue"), both of which are calculated as a percentage of the hammer price of the property sold at auction. Sotheby's private sale commissions are stipulated in legally binding agreements between Sotheby’s and the seller, which outline the terms of the arrangement including the desired sale price and the amount or rate of commission to be earned. In 2012, 2011, and 2010, auction commission revenues accounted for 81%, 84%, and 86%, respectively, of Sotheby’s consolidated revenues and private sale commission revenues accounted for 10%, 8%, and 6%, respectively, of consolidated revenues.

Under Sotheby’s standard auction payment terms, payments from the buyer are due no more than 30 days from the sale date and payment to the consignor is due 35 days from the sale date. For private sales, payment from the buyer is typically due on the sale date with the net sale proceeds being due to the consignor shortly thereafter. Extended payment terms are sometimes provided to an auction or private sale buyer in order to support and market a sale. Such terms typically extend the payment due date to a date that is no longer than one year from the sale date. In limited circumstances, the payment due date may be extended to a date that is beyond one year from the sale date. Any changes from the standard auction and private sale payment terms are subject to management approval under Sotheby's policy. When providing extended payment terms, Sotheby’s attempts to match the timing of cash receipt from the buyer with the timing of payment to the consignor, but is not always successful in doing so.

Under the standard terms and conditions of its auction and private sales, Sotheby’s is not obligated to pay the consignor for property that has not been paid for by the buyer. If a buyer defaults on payment, the sale may be cancelled, and the property will be returned to the consignor. Alternatively, the consignor may reoffer the property at a future Sotheby's auction or negotiate a private sale with Sotheby's acting as its agent. However, in certain instances and subject to management approval under Sotheby’s policy, the consignor may be paid the net sale proceeds before payment is collected from the buyer and/or the buyer may be allowed to take possession of the property before making payment. In situations when the buyer takes possession of the property before making payment, Sotheby’s is liable to the seller for the net sale proceeds whether or not the buyer makes payment.

From time to time in the ordinary course of its business, Sotheby’s will guarantee to a consignor a minimum sale price in connection with the sale of property at auction (an “auction guarantee”). In the event that the property sells for less than the guaranteed price, Sotheby’s must perform under the auction guarantee by funding the difference between the sale price at auction and the amount of the auction guarantee. Sotheby’s is generally entitled to a share of the excess proceeds (the “overage”) if the property under the auction guarantee sells above the guaranteed price. If the property does not sell, the amount of the auction guarantee must be paid, but Sotheby’s has the right to recover such amount through the future sale of the property. In these situations, the guaranteed property is recorded as inventory on Sotheby's balance sheet at the lower of cost (i.e., the amount paid under the auction guarantee) or management’s estimate of the property's net realizable value (i.e., expected sale price upon disposition). The sale proceeds ultimately realized by Sotheby’s in these situations may equal, exceed or be less than the amount recorded as inventory on Sotheby's balance sheet.

Sotheby’s may reduce its financial exposure under auction guarantees through contractual risk and reward sharing arrangements under which a counterparty commits to bid a predetermined price on the guaranteed property (an “irrevocable bid”). Ordinarily, an irrevocable bid is either obtained concurrent with the issuance of the related auction guarantee or the issuance of the auction guarantee is conditional upon the receipt of an irrevocable bid. From time-to-time, auction guarantees are issued that are not conditional on the receipt of an irrevocable bid, and the corresponding irrevocable bid is secured after Sotheby's has issued the auction guarantee. If the irrevocable bid is the winning bid, the counterparty purchases the property at the predetermined price plus the applicable buyer’s premium, which is the same amount that any other successful bidder would pay at that price. If the irrevocable bid is not the winning bid, the counterparty is generally entitled to receive a share of the auction commission earned on the sale and/or a share of any overage.

Sotheby's irrevocable bid counterparties are typically major international art dealers or major art collectors. Sotheby’s could be exposed to losses in the event any of these counterparties do not perform according to the terms of these contractual arrangements.

Prior to 2009, Sotheby's usually assumed the entire financial risk under its auction guarantees. However, beginning in 2009, Sotheby's changed its strategy with respect to auction guarantees and since then has generally entered into auction guarantees only when it is able to reduce its financial exposure through irrevocable bid arrangements. While it is management's intent to seek to reduce Sotheby's auction guarantee exposure through the use of irrevocable bids, management may not always be able to secure irrevocable bids on terms that are acceptable to Sotheby's and in some limited instances may not choose to seek an irrevocable bid.

Sotheby’s is obligated under the terms of certain auction guarantees to advance all or a portion of the guaranteed amount prior to auction.

(See Note D of Notes to Consolidated Financial Statements for financial information about the Auction segment. See Note E of Notes to Consolidated Financial Statements for information about auction and private sale receivables. See Note Q of Notes to Consolidated Financial Statements for information about auction guarantees.)

Seasonality

The worldwide art auction market has two principal selling seasons, which generally occur in the second and fourth quarters of the year. Accordingly, Sotheby’s auction results are seasonal, with peak revenues and operating income generally occurring in those quarters. Consequently, first and third quarter results have historically reflected a lower volume of auction activity when compared to the second and fourth quarters and, typically, a net loss due to the fixed nature of many of Sotheby’s operating expenses. (See Note U of Notes to Consolidated Financial Statements for Sotheby's quarterly results for the years ended December 31, 2012 and 2011.)

The Auction Market and Competition

Competition in the international art market is intense. A fundamental challenge facing any auctioneer or art dealer is to obtain high quality and valuable property for sale either as agent or as principal. Sotheby's primary global auction competitor is Christie’s International, PLC, a privately held, French-owned, auction house. To a much lesser extent, Sotheby’s also faces competition from smaller auction houses such as Bonhams and Phillips, as well as regional auction houses and a variety of art dealers across all collecting categories. In the Chinese art market, Sotheby's also competes with Beijing Poly International Auction Co. Ltd., China Guardian Auctions Co. Ltd. and Beijing Hanhai Auction Co. Ltd.

The owner of a work of art wishing to sell has four principal options: (i) sale or consignment to, or private sale by, an art dealer; (ii) consignment to, or private sale by, an auction house; (iii) private sale to a collector or museum without the use of an intermediary; or (iv) for certain categories of property (in particular, collectibles) consignment to, or private sale through, an internet-based service. The more valuable the property, the more likely it is that the owner will consider more than one option and will solicit proposals from more than one potential purchaser or agent, particularly if the seller is a fiduciary representing an estate or trust. A complex array of factors may influence the seller’s decision. These factors, which are not ranked in any particular order, include:

•The level and breadth of expertise of the art dealer or auction house with respect to the property;

•The extent of the prior relationship, if any, between the art dealer or auction house and its staff and the seller;

| |

| • | The reputation and historic level of achievement by the art dealer or auction house in attaining high sale prices in the property’s specialized category; |

| |

| • | The client’s desire for privacy; |

| |

| • | The amount of cash offered by an art dealer, auction house or other purchaser to purchase the property outright, which is greatly influenced by the amount and cost of capital resources available to such parties; |

| |

| • | The availability and terms of financial options offered by auction houses including auction guarantees, short-term financing and auction commission sharing arrangements; |

| |

| • | The level of pre-sale estimates; |

| |

| • | The desirability of a public auction in order to achieve the maximum possible price (a particular concern for fiduciary sellers, such as trustees and estate executors); |

| |

| • | The amount of commission charged by art dealers or auction houses to sell a work on consignment; |

| |

| • | The cost, style and extent of pre-sale marketing and promotion to be undertaken by an art dealer or auction house; |

| |

| • | Reputation and recommendations by third parties consulted by the seller; |

| |

| • | The desire of clients to conduct business with a publicly traded company; and |

| |

| • | The availability and extent of related services, such as tax or insurance appraisals. |

It is not possible to measure with any particular accuracy the entire international art market or to reach any conclusions regarding overall competition because privately owned art dealers and auction firms frequently do not publicly report annual totals for auction sales, revenues or profits, and the amounts reported may not be verifiable.

Auction Regulation

Regulation of the auction market varies from jurisdiction to jurisdiction. In many jurisdictions, Sotheby’s is subject to laws and regulations that are not directed solely toward the auction market, including, but not limited to, import and export regulations, antitrust laws, cultural property ownership laws, data protection and privacy laws, anti-money laundering laws, copyright and resale royalty laws, and laws and regulations involving sales, use, value-added and other indirect taxes. In addition, Sotheby’s is subject to local auction regulations, such as New York City Auction Regulations Subchapter M of Title 6 §§ 2-121–2-125, et. seq. Such regulations do not impose a material impediment to Sotheby’s business, but do affect the market generally. A material adverse change in such regulations, such as the Equity for Visual Artists bill introduced in the U.S. Congress which would impose a 7% resale royalty only on sales of art through large auction houses, could materially affect Sotheby's business. Additionally, export and import laws and cultural property ownership laws could affect the availability of certain kinds of property for sale at Sotheby’s principal auction locations or could increase the cost of moving property to such locations. In addition, failure to comply with local laws and regulations could subject Sotheby’s to civil and/or criminal penalties in such jurisdictions, or expose Sotheby's to legal claims or government inquiries. Sotheby’s has a Compliance Department which, amongst other activities, develops and updates compliance policies and audits, monitors, and provides training to its employees on compliance with many of these laws and regulations.

Finance Segment

Description of Business

Sotheby’s Finance segment provides certain collectors and art dealers with financing secured by works of art that Sotheby's either has in its possession or permits borrowers to possess. The Finance segment generally makes two types of secured loans: (1) advances secured by consigned property to borrowers who are contractually committed, in the near term, to sell the property at auction (a “consignor advance”); and (2) general purpose term loans secured by property not presently intended for sale (a “term loan”).

A consignor advance allows a seller to receive funds upon consignment for an auction that will typically occur up to one year in the future. Consignor advances normally have maturities ranging between three and six months and may sometimes be issued interest free as an incentive to the consignor for entering into the consignment agreement. Interest free consignor advances can represent a significant portion of the Finance segment loan portfolio as of the end of certain quarterly reporting periods in advance of peak selling seasons. Interest bearing consignor advances typically carry a variable rate of interest.

Term loans allow Sotheby's to establish or enhance mutually beneficial relationships with borrowers and may generate future auction consignments or private sale consignments and/or purchases. In certain situations, term loans are also made to refinance clients' auction and private sale purchases. Term loans normally have initial maturities of up to two years and typically carry a variable market rate of interest.

The collection of secured loans can be adversely impacted by a decline in the art market in general or in the value of the particular collateral. In addition, in situations when there are competing claims on the collateral and/or when a borrower becomes subject to bankruptcy or insolvency laws, Sotheby’s ability to realize on its collateral may be limited or delayed.

Sotheby’s target loan-to-value (“LTV”) ratio, which is defined as the principal loan amount divided by the low auction estimate of the collateral, is 50% or lower. However, loans are also made at an initial LTV higher than 50%. In addition, as a result of the periodic revaluation of loan collateral, the LTV ratio of certain loans may increase above the 50% target due to decreases in the low auction estimates of the collateral. The revaluation of loan collateral is performed by Sotheby’s specialists on an annual basis or more frequently if there is a material change in circumstances related to the loan or the disposal plans for the collateral.

The activities of the Finance segment, which are conducted through Sotheby’s wholly-owned subsidiaries, have in recent years been funded through the operating cash flows of the Auction segment. Sotheby's may supplement the funding of the Finance segment with revolving credit facility borrowings, but has not borrowed under its revolving credit facility during the last four years. As a result of Sotheby's significant cash balances and strong liquidity in recent years, as well as an increase in the demand for art-related financing, in 2012, the Finance segment loan portfolio and associated revenues increased significantly when compared to the two previous years. As demonstrated by the following table, this growth was achieved while maintaining Sotheby's traditional high loan underwriting standards (in thousands of dollars):

|

| | | | | | | | | | | | |

| As of and for the year ended December 31 | | 2012 | | 2011 | | 2010 |

| Finance segment loans | | $ | 425,138 |

| | $ | 223,029 |

| | $ | 241,631 |

|

| LTV ratio | | 48 | % | | 42 | % | | 45 | % |

| Finance revenues | | $ | 17,707 |

| | $ | 12,038 |

| | $ | 9,685 |

|

(See “Liquidity and Capital Resources” under “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”) (See Note D of Notes to Consolidated Financial Statements for additional financial information about the Finance segment. See Note E of Notes to Consolidated Financial Statements for information about Finance segment loans.)

The Finance Market and Competition

A considerable number of traditional lending sources offer conventional loans at a lower cost to borrowers than the average cost of loans offered by Sotheby’s Finance segment. Additionally, many traditional lenders offer borrowers a variety of integrated financial services such as wealth management services, which are not offered by Sotheby’s. Few lenders, however, are willing to accept works of art as sole collateral as they do not possess the ability to both appraise and sell works of art within a vertically integrated organization. Sotheby’s believes that through a combination of its art expertise and skills in international law and finance, it has the ability to tailor attractive financing packages for clients who wish to obtain immediate access to liquidity from their art assets.

Dealer Segment

Description of Business

Sotheby’s Dealer segment includes the activities of Noortman Master Paintings (or “NMP”), an art dealer that sells works of art from inventory directly to private collectors and museums and, from time-to-time, acts as a broker in private purchases and sales of art. The activities of the Dealer segment also include the purchase and resale of artworks directly by Sotheby’s and, to a lesser extent, retail wine sales and the activities of certain equity investees, including Acquavella Modern Art (or “AMA”). Under certain circumstances, the Dealer segment, with the assistance of Finance segment employees, sometimes provides secured loans to certain art dealers to finance the purchase of works of art. In these situations, the Dealer segment acquires a partial ownership interest in the purchased property in addition to providing the loan. Upon its eventual sale, the loan is repaid and any profit or loss is shared by Sotheby's and the art dealer according to their respective ownership interests.

NMP was acquired by Sotheby's on June 7, 2006 for initial consideration of 1,946,849 shares of Common Stock (the “Initial Consideration”). Pursuant to the terms of the acquisition, if NMP failed to achieve a minimum level of financial performance during the five years following the acquisition, up to 20% of the Initial Consideration would be returned to Sotheby's. The minimum level of financial performance was not achieved by NMP as of May 31, 2011 and, as a result, 147,341 shares of Common Stock were returned to Sotheby's.

In the third quarter of 2011, following the fifth anniversary of the acquisition of NMP and the expiration of the related financial performance targets, management initiated a plan to restructure NMP’s business and sales strategy. As a result of the restructuring of its business and sales strategy, NMP has reduced its inventory of lower valued Old Master Paintings and shifted its focus to a select group of high-valued works of art. In furtherance of this strategy and due in part to a lower level of profitable sales, in the third quarter of 2012, management closed NMP's Amsterdam office and consolidated its operations into NMP's London office.

(See Note D of Notes to Consolidated Financial Statements for financial information about the Dealer segment. See Note E of Notes to Consolidated Financial Statements for information about Dealer segment lending activity. See Note G of Notes to Consolidated Financial Statements for information about AMA.)

The Dealer Market and Competition

The Dealer segment operates in the same markets as Sotheby’s Auction segment and is impacted to varying degrees by many of the same competitive factors (as discussed above under “The Auction Market and Competition”). The most prominent competitive factors impacting the Dealer segment, which are not ranked in any particular order, include: (i) reputation and relationships and personal interaction between the buyer or seller and the art dealer; (ii) access to, and participation in, art fairs; (iii) the level of specialized expertise of the art dealer; (iv) the ability of the art dealer to locate and purchase quality works of art for resale; and (v) the ability of the art dealer to finance purchases of art.

Brand Licensing Activities

Prior to 2004, Sotheby’s engaged in the marketing and brokerage of luxury residential real estate sales through Sotheby’s International Realty (or “SIR”). In 2004, Sotheby’s sold SIR to a subsidiary of Realogy Corporation (or “Realogy”), formerly Cendant Corporation. In conjunction with the sale, Sotheby’s entered into an agreement with Realogy to license the SIR trademark and certain related trademarks for an initial 50-year term with a 50-year renewal option (the “Realogy License Agreement”). The Realogy License Agreement is applicable worldwide.

The Realogy License Agreement provides for an ongoing license fee during its term based on the volume of commerce transacted under the licensed trademarks. In 2012, 2011, and 2010, Sotheby’s earned $5 million, $3.9 million, and $3.1 million, respectively, in license fee revenue related to the Realogy License Agreement.

The Sotheby’s name is also licensed for use in connection with the art auction business in Australia, art education services in the U.S. and the United Kingdom (“U.K.”) and print management services. Management will consider additional opportunities to license the Sotheby’s brand in businesses where appropriate.

Strategic Initiatives

Continued Focus on Sotheby’s Most Valuable Relationships

Sotheby’s focus on the high-end of the art market has been an important contributor to its success. Accordingly, management is continuing to dedicate significant time, energy and resources to broadening and extending the breadth and depth of Sotheby’s relationships with major clients. These efforts are part of a multi-year strategy to invest in those areas which serve Sotheby’s most valuable clients best.

Over the past several years, Sotheby’s has made substantial investments in information technology designed to improve client service. A portfolio of enterprise systems anchored by SAP has been deployed across the organization, which has enhanced the quality of information and the processing of sales and inventory tracking, as well as financial management. Sotheby’s has also implemented systems enhancements to significantly reengineer and improve the post-sale client experience. In particular, enhancements were made to improve client invoicing, facilitate the shipment and tracking of purchased property, and inform clients of important information such as bid confirmation, sale results, and payment confirmation. In addition, Sotheby's reorganized its staff so that clients have a single point of contact for post-sale inquiries at its sales centers in New York and London.

Sotheby's also continues to invest in its digital media strategy via the sothebys.com website and its iPad† application to facilitate Sotheby's accessibility to clients on mobile platforms. In particular, a new blog channel was developed for arts-related and life-style articles, the Preferred Program was enhanced to enable easier access to its services, rewards and newsletter, and the iPad† application was improved to better facilitate the auction experience through the delivery of real-time auction results, note taking, 360° views for three-dimensional objects, artist search and background processing, and to provide faster access to the iPad† catalogue. Also, in 2010, the sothebys.com website was enhanced with several important features including BIDnow™ (an online bidding feature). The BIDnow™ feature has satisfied a demand from clients for online bidding capabilities and its impact in certain categories such as wine, jewelry and books has been dramatic.

In addition, Sotheby's continues to leverage social media channels with a presence on Facebook†, YouTube†, and Twitter†, and has also expanded its reach to Asian clients with a presence on Weibo†.

Client relationships are a key driver of Sotheby’s success and its clients expect a consistently high level of service. Management believes these initiatives will have a meaningful positive impact on the future of Sotheby’s business.

† iPAD, Facebook, YouTube, Twitter and Weibo are third-party marks over which Sotheby's does not make any claims.

Continued Development of Sotheby's Presence in China and Other Emerging Markets

In recent years, Sotheby's has focused on developing its presence in China and the growth in activity from buyers in this region has been dramatic. Auction and related revenues attributable to Hong Kong have become an increasingly significant contributor to Sotheby's financial results, accounting for approximately 15% of aggregate auction and related revenues in 2012, as compared to approximately 7% in 2007.

Management is continuing to focus on developing Sotheby's presence in China by deepening its relationships with Chinese art collectors in a number of ways, including:

| |

| • | The implementation of regional marketing initiatives such as the publishing of Hong Kong sales catalogues in Chinese, the launching of a Chinese language website that includes e-catalogues for sales of Asian Art and Sotheby's major Impressionist and Contemporary sales, and the hosting of various private selling exhibitions. |

| |

| • | Continued investments in new staff with the requisite skills to service Asian clients at Sotheby's Hong Kong, New York, and London locations, as well as to support the growth of the Chinese art market. |

| |

| • | The expansion in 2012 of Sotheby's facilities in Hong Kong to accommodate growth opportunities in the Chinese art market. The expansion included the addition of a state-of-the-art gallery with over 15,000 square feet of selling and exhibition space, as well as significant enhancements to the existing Hong Kong administrative offices. |

| |

| • | Conducting a greater number of auctions and private selling events in Hong Kong. Typically, Sotheby's major Hong Kong auctions are held in early April and early October. The premises expansion discussed above enables Sotheby's to conduct more auctions in Hong Kong throughout the year, in addition to its traditional auctions held in April and October. (See statement on Forward Looking Statements.) |

In September 2012, Sotheby's entered into a 10-year equity joint venture agreement with Beijing GeHua Art Company (“GeHua”) to form Sotheby's Beijing Auction Co., Ltd. (or the “Beijing Joint Venture”). The Beijing Joint Venture will allow Sotheby's to take advantage of a planned free port project that GeHua is developing within the Tianzhu Free Trade Zone in Beijing (the “Beijing Free Port”), which will serve as a tax-advantaged storage location and provide a platform for art-related auctions and private selling exhibitions of non-cultural relics, traveling exhibitions, and educational activities. The date of completion of the Beijing Free Port and the commencement and scope of any storage, auction or private selling activities by the Beijing Joint Venture, as well as any earnings or losses resulting from the operation of the Beijing Joint Venture, are uncertain. However, management believes that the Beijing Joint Venture will strategically enhance Sotheby's long-term presence in mainland China and allow it to potentially capitalize on the opportunities presented by the Chinese art market, which Sotheby's currently serves through its existing operations in Hong Kong. (See statement on Forward Looking Statements and Item 1A, "Risk Factors.")

Sotheby's is also currently in negotiations with the Chinese government to obtain the license required to operate as a Foreign-Invested Commercial Enterprise ("FICE") in order to establish a wholly-owned subsidiary, through which Sotheby's would operate independently in China outside of the Beijing Free Port in the same or similar businesses conducted by the Beijing Joint Venture. Management intends to establish the FICE in Beijing in 2013, with an initial focus on private sales, the hosting of traveling exhibitions and other client liaison activities. (See statement on Forward Looking Statements and Item 1A, "Risk Factors.")

In addition to Sotheby’s progress in China, investments have also been made in emerging markets such as Russia, the Middle East and South America, with offices opened in Moscow, Russia and Doha, Qatar in 2008 and São Paulo, Brazil in 2011.

Enhance Private Sales Initiatives

Private sales have become increasingly important to Sotheby's overall financial performance, with private sale commission revenues representing approximately 10% of total revenues in 2012. Prior to 2012, private sale commission revenues represented between 5% and 8% of total revenues during the five-year period between 2007 and 2011.

Over the past several years, Sotheby's has hosted a number of new and innovative private selling exhibitions and, in 2011, Sotheby's completed the construction of a dedicated private sale exhibition gallery, S|2, at its York Avenue headquarters in New York. In 2012, a new Private Sales website was launched, promoting Sotheby's private selling exhibitions and S|2. In addition, with the expansion of its Hong Kong premises in 2012, Sotheby's was able to host a number of private selling exhibitions in Hong Kong. In 2013, Sotheby's expects to open an S|2 gallery in London and host private selling exhibitions in Beijing through the Beijing Joint Venture. (See statement on Forward Looking Statements.)

Strengthen Core Business Capabilities

Sotheby's is largely a service business in which the ability of its employees to cultivate and maintain relationships with potential sellers and buyers of works of art is vital to its success. Accordingly, Sotheby's is focused on retaining key personnel through active employee engagement programs and by aligning rewards with performance, behaviors and values essential to Sotheby's. In addition, in 2013, Sotheby's intends to selectively add personnel across its global sourcing network in order to drive the growth initiatives mentioned above. (See statement on Forward Looking Statements.)

Financial and Geographical Information about Segments

See Note D of Notes to Consolidated Financial Statements for financial and geographical information about Sotheby’s segments.

Employees

As of December 31, 2012, Sotheby’s had 1,501 employees with 599 located in North America and South America; 520 in the U.K.; 223 in Continental Europe; and 159 in Asia. Sotheby’s regards its relations with its employees as good. The table below provides a breakdown of Sotheby’s employees by segment as of December 31, 2012 and 2011.

|

| | | | | | |

| December 31 | | 2012 | | 2011 |

| Auction | | 1,302 |

| | 1,271 |

|

| Finance | | 7 |

| | 7 |

|

| Dealer | | 3 |

| | 10 |

|

| All Other | | 189 |

| | 158 |

|

| Total | | 1,501 |

| | 1,446 |

|

Employees classified within “All Other” principally relate to Sotheby’s central corporate and information technology departments.

Website Address

Sotheby’s makes available free of charge its annual report on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K through a hyperlink from its website, http://investor.shareholder.com/bid/index.cfm, a website maintained by an unaffiliated third-party service. Such reports are made available on the same day that they are electronically filed with or furnished to the Securities and Exchange Commission (the "SEC"). Information available on the website is not incorporated by reference and is not deemed to be part of this Form 10-K.

ITEM 1A: RISK FACTORS

Sotheby's operating results and liquidity are significantly influenced by a number of risk factors, many of which are not within its control. These factors, which are not ranked in any particular order, are discussed below.

The global economy and the financial markets and political conditions of various countries may negatively affect Sotheby's business and clients, as well as the supply of and demand for works of art.

The international art market is influenced over time by the overall strength and stability of the global economy and the financial markets of various countries, although this correlation may not be immediately evident. In addition, global political conditions and world events may affect Sotheby's business through their effect on the economies of various countries, as well as on the willingness of potential buyers and sellers to purchase and sell art in the wake of economic uncertainty. Sotheby's business can be particularly influenced by the economies, financial markets and political conditions of the U.S., the U.K., China and the other major countries or territories of Europe and Asia (including the Middle East). Accordingly, weakness in those economies and financial markets can adversely affect the supply of and demand for works of art and Sotheby's business. Furthermore, global political conditions may also influence the enactment of legislation that could adversely impact Sotheby's business.

Government laws and regulations may restrict or limit Sotheby's business or impact the value of its real estate assets.

Many of Sotheby's activities are subject to laws and regulations including, but not limited to, import and export regulations, cultural property ownership laws, data protection and privacy laws, anti-money laundering laws, antitrust laws, copyright and resale royalty laws, laws and regulations involving sales, use, value-added and other indirect taxes, and regulations related to the use of real estate. In addition, Sotheby's is subject to local auction regulations, such as New York City Auction Regulations Subchapter M of Title 6 §§ 2-121-2-125, et. seq. Such regulations currently do not impose a material impediment to the worldwide business of Sotheby's, but do affect the market generally. A material adverse change in such regulations, such as the Equity for Visual Artists bill introduced in the U.S. Congress which would impose a 7% resale royalty on sales of art through large auction houses, could affect Sotheby's business. Additionally, export and import laws and cultural property ownership laws could affect the availability of certain kinds of property for sale at Sotheby's principal auction locations, increase the cost of moving property to such locations, or expose Sotheby's to legal claims or government inquiries.

Foreign currency exchange rate movements can significantly impact Sotheby's results of operations and financial condition.

Sotheby's has operations throughout the world, with approximately 56% of its revenues earned outside of the U.S. in 2012. Additionally, Sotheby's has significant assets and liabilities denominated in the Pound Sterling and the Euro. Revenues and expenses relating to Sotheby's foreign operations are translated using weighted average monthly exchange rates during the period in which they are recognized and assets and liabilities relating to Sotheby's foreign operations are translated using month-end exchange rates. Accordingly, fluctuations in foreign currency exchange rates, particularly for the Pound Sterling and the Euro, can significantly impact Sotheby's results of operations and financial condition.

Competition in the international art market is intense and may adversely impact Sotheby's results of operations.

Sotheby's competes with other auctioneers and art dealers to obtain valuable consignments to offer for sale either at auction or through private sale. The level of competition is intense and can adversely impact Sotheby's ability to obtain valuable consignments for sale, as well as the commission margins achieved on such consignments.

Sotheby's cannot be assured of the amount and quality of property consigned for sale, which may cause significant variability in its financial results.

The amount and quality of property consigned for sale is influenced by a number of factors not within Sotheby's control. Many major consignments, and specifically single-owner sale consignments, often become available as a result of the death or financial or marital difficulties of the owner, all of which are unpredictable and may cause significant variability in Sotheby's financial results from period to period.

The demand for art is unpredictable, which may cause significant variability in Sotheby's results of operations.

The demand for art is influenced not only by overall economic conditions, but also by changing trends in the art market as to which collecting categories and artists are most sought after and by the collecting preferences of individual collectors, all of which are difficult to predict and which may adversely impact the ability of Sotheby's to obtain and sell consigned property, potentially causing significant variability in Sotheby's results of operations from period to period.

The loss of key personnel could adversely impact Sotheby's ability to compete.

Sotheby's is largely a service business in which the ability of its employees to develop and maintain relationships with potential sellers and buyers of works of art is essential to its success. Moreover, Sotheby's business is unique, making it important to retain key specialists and members of management. Accordingly, Sotheby's business is highly dependent upon its success in attracting and retaining qualified personnel.

The strategic initiatives being implemented by Sotheby's may not succeed.

Sotheby's strategic initiatives are focused on extending the breadth and depth of its relationships with its most valuable clients, developing a presence in China and other emerging markets, enhancing its private sales capabilities, and the retention of key personnel. Sotheby's future operating results are dependent, in part, on management's success in implementing these and other strategic initiatives. Furthermore, the inability of Sotheby's to successfully implement its strategic initiatives could result in, among other things, the loss of clients, the loss of key personnel, the impairment of assets, and inefficiencies from operating in new and emerging markets. Also, Sotheby's short-term operating results could be unfavorably impacted by the opportunity and financial costs associated with the implementation of its strategic plans. (See "Strategic Initiatives" within Item 1, "Description of Business," and statement on Forward Looking Statements.)

Sotheby's recently approved joint venture in China is a foreign-invested enterprise under Chinese law. As such, enforcement of certain of Sotheby's rights within the joint venture are subject to approval from the Chinese government, which could limit Sotheby's ability of the joint venture to operate and succeed.

In September 2012, Sotheby's received approval from the Chinese government to form and operate a 10-year equity joint venture with Beijing GeHua Art Company in China, which management believes will strategically enhance Sotheby's long-term presence in mainland China and allow it to potentially capitalize on the opportunities presented by the Chinese art market. (See "Strategic Initiatives" within Item 1, "Description of Business.")

Because the joint venture is a foreign-invested enterprise under Chinese law, all changes in shareholding and constitution of the joint venture will be subject to approval by the Chinese government, including in the event Sotheby's is seeking to terminate the joint venture agreement, exercise its put option, or wind-up the joint venture. Accordingly, Sotheby's ability to successfully operate the joint venture and enforce the joint venture agreement provisions could be constrained by the Chinese government and other unforeseen circumstances.

Sotheby's is currently in negotiations with the Chinese government to obtain the license required to operate as a Foreign-Invested Commercial Enterprise in order to establish a wholly-owned subsidiary in China. Sotheby's negotiations to obtain the license required to operate as a Foreign-Invested Commercial Enterprise in China may not be successful.

Sotheby's establishment of a wholly-owned subsidiary in China is subject to the receipt of a license from the Chinese government. Sotheby's may not be successful in obtaining this license, which could delay or inhibit its ability to further implement its strategic initiatives in China. (See "Strategic Initiatives" within Item 1, "Description of Business.")

A breach of the security measures protecting Sotheby's global network of information systems may occur.

Sotheby's is dependent on a global network of information systems to conduct its business. A breach of the security measures protecting Sotheby's information systems could adversely impact its operations, reputation, and brand.

Sotheby's business continuity plans may not be effective in addressing the impact of unexpected events that could impact its business.

Sotheby's inability to successfully implement its business continuity plans in the wake of an unexpected event, such as an act of God or a terrorist attack occurring near one of its major selling and/or sourcing offices and/or any other unexpected event, could disrupt its ability to operate and adversely impact its operations.

Sotheby's relies on a small number of clients who make a significant contribution to its revenues, profitability and operating cash flows.

Sotheby's relies on a small number of clients who make a significant contribution to its revenues, profitability, and operating cash flows. Accordingly, Sotheby's revenues, profitability, and operating cash flows are highly dependent upon its ability to develop and maintain relationships with this small group of clients, as well as the financial strength of these clients.

Subject to management approval under Sotheby's policy, Sotheby's may pay the consignor before payment is collected from the buyer and/or may allow the buyer to take possession of purchased property before payment is received. In these situations, Sotheby's is exposed to losses in the event the buyer does not make payment.

Under the standard terms and conditions of its auction and private sales, Sotheby's is not obligated to pay the consignor for property that has not been paid for by the buyer. However, in certain instances and subject to management approval under Sotheby's policy, the consignor may be paid the net sale proceeds before payment is collected from the buyer while Sotheby's retains possession of the property. In such situations, if the buyer does not make payment, Sotheby's will take title to the property, but could be exposed to losses if the value of the property declines. In certain other situations and subject to management approval under Sotheby's policy, the buyer is allowed to take possession of purchased property before making payment. In these situations, Sotheby's is liable to the seller for the net sale proceeds whether or not the buyer makes payment and would incur losses in the event of buyer default. (See Note E of Notes to Consolidated Financial Statements for information about auction and private sale receivables.)

Sotheby's ability to collect auction receivables may be adversely impacted by buyers from emerging markets, as well as by the banking and foreign currency laws and regulations, and judicial systems of the countries in which it operates and in which its clients reside.

Sotheby's operates in 40 countries and has a worldwide client base that has grown in recent years due in part to a dramatic increase in the activity of buyers from emerging markets, and in particular, China. The collection of auction receivables related to buyers from emerging markets may be adversely impacted by the buyer's lack of familiarity with the auction process and the buyer's financial condition. Sotheby's ability to collect auction receivables may also be adversely impacted by the banking and foreign currency laws and regulations regarding the movement of funds out of certain countries, as well as by Sotheby's ability to enforce its rights as a creditor in jurisdictions where the applicable laws and regulations may be less defined, particularly in emerging markets.

Demand for art-related financing is unpredictable, which may cause variability in Sotheby's results of operations.

Sotheby's business is, in part, dependent on the demand for art-related financing, which can be significantly influenced by overall economic conditions and by the often unpredictable financial requirements of owners of major art collections. Accordingly, the financial results of Sotheby's Finance segment are subject to variability from period to period.

The ability of Sotheby's to realize proceeds from the sale of collateral for Finance segment loans may be delayed or limited.

In situations when there are competing claims on the collateral for Finance segment loans and/or when a borrower becomes subject to bankruptcy or insolvency laws, Sotheby's ability to realize proceeds from the sale of its collateral may be limited or delayed.

The value of art is subjective and often fluctuates, exposing Sotheby's to losses in the value of its inventory and loan collateral and significant variability in its results of operations.

The art market is not a highly liquid trading market. As a result, the valuation of art is inherently subjective, and the realizable value of art often fluctuates over time. Accordingly, Sotheby's is at risk both as to the realizable value of art held in inventory and as to the realizable value of art pledged as collateral for client loans.

In estimating the realizable value of art, management relies on the opinions of Sotheby's specialists, who consider the following complex array of factors when valuing art: (i) whether the artwork is expected to be offered at auction or sold privately, in the ordinary course of Sotheby's business; (ii) the supply and demand for works of art, taking into account economic conditions and changing trends in the art market as to which collecting categories and artists are most sought after; and (iii) recent sale prices achieved in the art market for comparable works of art within a particular collecting category and/or by a particular artist.

If management determines that the estimated realizable value of a specific artwork held in inventory is less than its carrying value, a loss is recorded to reflect management's revised estimate of realizable value. In addition, if the estimated realizable value of the art pledged as collateral for a client loan is less than the corresponding loan balance, management assesses whether it is necessary to record a loss to reduce the carrying value of the loan, after taking into account the ability of the borrower to repay any shortfall between the value of the collateral and the amount of the loan. These factors may cause significant variability in Sotheby's financial results from period to period.

Sotheby's could be exposed to losses as a result of various claims and lawsuits incidental to the ordinary course of its business.

Sotheby's becomes involved in various claims and lawsuits incidental to the ordinary course of its business. Management is required to assess the likelihood of any adverse judgments or outcomes in these matters, as well as potential ranges of probable or reasonably possible losses. A determination of the amount of losses, if any, to be recorded or disclosed as a result of these contingencies is based on a careful analysis of each individual exposure with, in some cases, the assistance of outside legal counsel. The amount of losses recorded or disclosed for such contingencies may change in the future due to new developments in each matter or a change in settlement strategy.

Sotheby's could be exposed to losses in the event of title or authenticity claims arising from the sale of works of art.

The assessment of works of art offered for auction or private sale can involve potential claims regarding title and authenticity. Items sold by Sotheby's may be subject to statutory warranties as to title and to a limited guarantee as to authenticity under the Conditions of Sale and Terms of Guarantee that are published in Sotheby's auction sale catalogues and the terms stated in, and the laws applicable to, agreements governing private sale transactions. The authentication of works of art is based on scholarship and research, but necessarily requires a degree of judgment from Sotheby's art experts. In the event of a title or authenticity claim against Sotheby's, Sotheby's may have recourse against the seller of the property and may have the benefit of insurance, but a claim could nevertheless expose Sotheby's to losses and to reputational risk.

Auction guarantees create the risk of loss resulting from the potential inaccurate valuation of art.

As discussed above, the art market is not a highly liquid trading market and, as a result, the valuation of art is inherently subjective. Accordingly, Sotheby's is at risk with respect to management's ability to estimate the likely selling prices of works of art offered with auction guarantees. If management's judgments about the likely selling prices of works of art offered with auction guarantees prove to be inaccurate, there could be a significant adverse impact on Sotheby's results of operations, financial condition and liquidity. (See Note Q of Notes to Consolidated Financial Statements for information related to auction guarantees.)

Sotheby's could be exposed to losses in the event of nonperformance by its counterparties in auction guarantee risk and reward sharing arrangements.

In certain situations, Sotheby's reduces its financial exposure under auction guarantees through risk and reward sharing arrangements. Sotheby's counterparties to these risk and reward sharing arrangements are typically major international art dealers or major art collectors. Sotheby's could be exposed to losses in the event any of these counterparties do not perform according to the terms of these contractual arrangements.

Future costs and obligations related to the Sotheby's U.K. Pension Plan are dependent on unpredictable factors, which may cause significant variability in employee benefit costs.

Future costs and obligations related to Sotheby's defined benefit pension plan in the U.K. are heavily influenced by changes in interest rates, investment performance in the debt and equity markets, changes in statutory requirements in the U.K., and actuarial assumptions, each of which is unpredictable and may cause significant variability in Sotheby's employee benefit costs.

Tax matters may cause significant variability in Sotheby's financial results.

Sotheby's operates in many tax jurisdictions throughout the world and the provision for income taxes involves a significant amount of management judgment regarding interpretation of relevant facts and laws in the jurisdictions in which Sotheby's operates. Sotheby's effective income tax rate can vary significantly between periods due to a number of complex factors including, but not limited to: (i) future changes in applicable laws; (ii) projected levels of taxable income; (iii) pre-tax income being lower than anticipated in countries with lower statutory rates or higher than anticipated in countries with higher statutory rates; (iv) increases or decreases to valuation allowances recorded against deferred tax assets; (v) tax audits conducted by various tax authorities; (vi) adjustments to income taxes upon finalization of income tax returns; (vii) the ability to claim foreign tax credits; (viii) the repatriation of non-U.S. earnings for which Sotheby's has not previously provided for income taxes; and (ix) tax planning.

Sotheby's clients reside in various tax jurisdictions throughout the world. To the extent that there are changes to tax laws or tax reporting obligations in any of these jurisdictions, such changes could adversely impact the ability and/or willingness of clients to purchase or sell works of art through Sotheby's. Additionally, Sotheby's is subject to laws and regulations in many countries involving sales, use, value-added and other indirect taxes which are assessed by various governmental authorities and imposed on certain revenue-producing transactions between Sotheby's and its clients. The application of these laws and regulations to Sotheby's unique business and global client base, and the estimation of any related liabilities, is complex and requires a significant amount of judgment. These indirect tax liabilities are generally not those of Sotheby’s unless it fails to collect the correct amount of sales, value-added, or other indirect taxes. Failure to collect the correct amount of indirect tax on a transaction may expose Sotheby's to claims from tax authorities.

Insurance coverage for artwork may become more difficult to obtain, exposing Sotheby's to losses for artwork in Sotheby's possession.

Sotheby's maintains insurance coverage through brokers and underwriters for the works of art it owns and for works of art consigned to it by its clients, which are exhibited and stored at Sotheby's facilities around the world. An inability to adequately insure such works of art due to limited capacity of the global art insurance market could, in the future, have a material adverse impact on Sotheby's business.

Due to the nature of its business, valuable works of art are exhibited and stored at Sotheby's facilities around the world. Such works of art could be subject to damage or theft, which could have a material adverse effect on Sotheby's business and reputation.

Valuable works of art are exhibited and stored at Sotheby's facilities around the world. Although Sotheby's maintains state of the art security measures at its premises, valuable artworks may be subject to damage or theft. The damage or theft of valuable artworks despite Sotheby's security measures could have a material adverse impact on Sotheby's business and reputation. Sotheby's maintains insurance coverage for the works of art that are exhibited and stored at its facilities, which could significantly mitigate any potential losses resulting from the damage or theft of such works of art.

ITEM 1B: UNRESOLVED STAFF COMMENTS

None.

ITEM 2: PROPERTIES

Sotheby’s is headquartered at 1334 York Avenue, New York, New York (the “York Property”). The York Property contains approximately 439,000 square feet of building area and is home to Sotheby’s sole North American auction salesroom and principal North American exhibition space, including S|2, a private sale exhibition gallery. The York Property is also home to Sotheby's U.S. Dealer and Finance operations, as well as its corporate offices. The York Property was purchased by Sotheby's on February 6, 2009 for $370 million and had a net book value of $276.3 million as of December 31, 2012 (see Notes H and J of Notes to Consolidated Financial Statements). Prior to this purchase, Sotheby’s occupied the York Property subject to a 20-year lease which was entered into in conjunction with a sale-leaseback transaction in February 2003. Sotheby’s also leases office and exhibition space in several other major cities in North and South America.

Sotheby’s U.K. operations (primarily Auction) are centered at New Bond Street, London, where the main salesrooms, exhibition space and administrative offices are located. Sotheby's invested approximately $2.8 million in 2012 as part of a multi-year refurbishment of the gallery and exhibition space at New Bond Street. Management is expecting to invest an additional $2.8 million to complete the final phase of the refurbishment project in 2013 (see statement on Forward Looking Statements). Almost the entire New Bond Street complex is either owned or held under various freehold and long-term lease arrangements. In addition, Sotheby's leases 52,000 square feet for a warehouse facility in Greenford, West London under a lease that expires in 2030 and rents 950 square feet of gallery space in London for Noortman Master Paintings.

Below is a table summarizing Sotheby’s ownership, freehold and lease arrangements related to its London properties as of December 31, 2012 (in thousands of dollars, except for square footage):

|

| | | | | | | | | | | | | | | | | | |

| | Square Footage | | Net Book Value of Land | | Net Book Value of Buildings and Building Improvements | | Net Book Value of Leasehold Improvements | | Total Net Book Value of London Premises |

| Owned property | 10,907 |

| | $ | 5,857 |

| | $ | 2,375 |

| | $ | — |

| | $ | 8,232 |

|

| Freeholds * | 84,563 |

| | — |

| | — |

| | 26,034 |

| | 26,034 |

|

| Leases with a remaining term greater than 10 Years | 106,896 |

| | — |

| | — |

| | 12,231 |

| | 12,231 |

|

| All other leases | 29,207 |

| | — |

| | — |

| | 2,062 |

| | 2,062 |

|

| Total | 231,573 |

| | $ | 5,857 |

| | $ | 2,375 |

| | $ | 40,327 |

| | $ | 48,559 |

|

* Freeholds are occupancy arrangements in which there is no rent paid and the arrangement has no termination date.

In 2012, Sotheby's completed an expansion of its Hong Kong facilities located at One Pacific Place, which cost approximately $7.5 million. The expansion included the addition of a state-of-the-art gallery with over 15,000 square feet of selling and exhibition space, as well as significant enhancements to the existing Hong Kong administrative offices.

Sotheby’s also leases space primarily for Auction operations in various locations throughout Continental Europe, including salesrooms in Geneva and Zurich, Switzerland; Milan, Italy, and Paris, France.

Management believes Sotheby’s worldwide premises are adequate for the current conduct of its business. However, management continually analyzes Sotheby’s worldwide premises and related fixed assets for its current and future business needs as part of management's ongoing efforts to manage infrastructure and overhead costs. Management will evaluate available alternatives and, where appropriate, make any necessary changes to address Sotheby’s premises requirements with a continued focus on long-term shareholder value.

ITEM 3: LEGAL PROCEEDINGS

See Note P of Notes to Consolidated Financial Statements for information related to Legal Proceedings.

ITEM 4: MINE SAFETY DISCLOSURES

Not applicable.

PART II

ITEM 5: MARKET FOR THE REGISTRANT’S COMMON EQUITY AND RELATED SHAREHOLDER MATTERS

Market Information

The principal market for Sotheby’s Common Stock is the NYSE (symbol: BID). As of February 15, 2013, there were 1,037 holders of record of Sotheby’s Common Sock. The quarterly price ranges on the NYSE of Sotheby’s Common Stock during 2012 and 2011 were as follows:

|

| | | | | | | | | | | | | | | | |

| | | 2012 | | 2011 |

| | | High | | Low | | High | | Low |

| Quarter Ended | | | | | | | | |

| March 31 | | $ | 40.81 |

| | $ | 28.16 |

| | $ | 52.95 |

| | $ | 38.23 |

|

| June 30 | | $ | 40.38 |

| | $ | 28.91 |

| | $ | 55.67 |

| | $ | 37.17 |

|

| September 30 | | $ | 36.00 |

| | $ | 27.43 |

| | $ | 48.90 |

| | $ | 27.53 |

|

| December 31 | | $ | 34.22 |

| | $ | 27.98 |

| | $ | 37.61 |

| | $ | 25.00 |

|

Sotheby’s is party to a credit agreement with an international syndicate of lenders led by General Electric Capital, Corporate Finance, under which there are no limitations on dividend payments provided that: (i) there are no Events of Default, as defined in the credit agreement, (ii) the Aggregate Borrowing Availability, as defined in the credit agreement, equals or exceeds $100 million, and (iii) the Total Liquidity Amount, as defined in the credit agreement, equals or exceeds $150 million. (See “Liquidity and Capital Resources” under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note J of Notes to Consolidated Financial Statements for detailed information related to Sotheby's credit agreement led by General Electric Capital, Corporate Finance.)

The following table summarizes dividends declared and paid for each of the quarterly periods in 2012 and 2011 (in thousands of dollars, except per share amounts):

|

| | | | | | | | | | | | | | | | |

| | | 2012 | | 2011 |

| | | Per Share | | Amount | | Per Share | | Amount |

| Quarter Ended | | | | | | | | |

| March 31 | | $ | 0.08 |

| | $ | 5,519 |

| | $ | 0.05 |

| | $ | 3,451 |

|

| June 30 | | $ | 0.08 |

| | $ | 5,432 |

| | $ | 0.05 |

| | $ | 3,420 |

|

| September 30 | | $ | 0.08 |

| | $ | 5,438 |

| | $ | 0.05 |

| | $ | 3,425 |

|

| December 31 | | $ | 0.28 |

| | $ | 18,834 |

| | $ | 0.08 |

| | $ | 4,555 |

|

| Total | | $ | 0.52 |

| | $ | 35,223 |

| | $ | 0.23 |

| | $ | 14,851 |

|

In December 2012, the Board of Directors declared and Sotheby's paid accelerated first and second quarter of 2013 cash dividends totaling $0.20 per share (approximately $13.6 million), reflecting a 25% increase in Sotheby's quarterly dividend rate. This accelerated dividend is intended to be in lieu of quarterly dividends that would have otherwise been declared and paid in the first and second quarters of 2013.

The declaration and payment of future dividends to shareholders remains at the discretion of Sotheby’s Board of Directors and is dependent upon many factors, including Sotheby’s financial condition, cash flows (in particular, its U.S. liquidity), legal requirements, and other factors as the Board of Directors deems relevant. It is the intention of Sotheby’s to continue to pay quarterly dividends at a rate of $0.10 per share beginning in the third quarter of 2013, subject to approval by the Board of Directors and depending on economic, financial, market and other conditions at the time. (See statement on Forward Looking Statements.)

Equity Compensation Plans

The following table provides information as of December 31, 2012 related to shares of Sotheby’s Common Stock that may be issued under its existing equity compensation plans, including the Sotheby’s 1997 Stock Option Plan (the “Stock Option Plan”), the Sotheby’s Restricted Stock Unit Plan (the “Restricted Stock Unit Plan”), and the Sotheby’s Amended and Restated Stock Compensation Plan for Non-Employee Directors (the “Directors Stock Plan”):

|

| | | | | | | | | | |

| | | (A) | | (B) | | (C) |

| Plan Category (1) | | Number of Securities to be Issued Upon Exercise of Outstanding Options, Warrants and Rights (2) | | Weighted Average Exercise Price of Outstanding Options, Warrants and Rights (3) | | Number of Securities Remaining Available for Future Issuance Under Equity Compensation Plans (4) |

| | | (In thousands, except per share data) |

| Equity compensation plans approved by shareholders | | 2,261 |

| | $ | 21.92 |

| | 1,306 |

|

| Equity compensation plans not approved by shareholders | | — |

| | — |

| | — |

|

| Total | | 2,261 |

| | $ | 21.92 |

| | 1,306 |

|

_____________________________________________________________

| |

| (1) | See Note N of Notes to Consolidated Financial Statements for a description of the material features of Sotheby’s equity compensation plans. |

| |

| (2) | Includes 1,912,163 shares awarded under the Restricted Stock Unit Plan for which vesting is contingent upon future employee service and/or Sotheby’s achievement of certain profitability targets and 348,750 stock options for which vesting is contingent upon future employee service. |

| |

| (3) | The weighted-average exercise price includes the exercise price of stock options and does not take into account 1,912,163 shares awarded under the Restricted Stock Unit Plan, which have no exercise price. |

| |

| (4) | Includes 1,221,305 shares available for future issuance under the Restricted Stock Unit Plan, 35,350 shares available for issuance under the Stock Option Plan and 49,671 shares available for issuance under the Directors Stock Plan. |

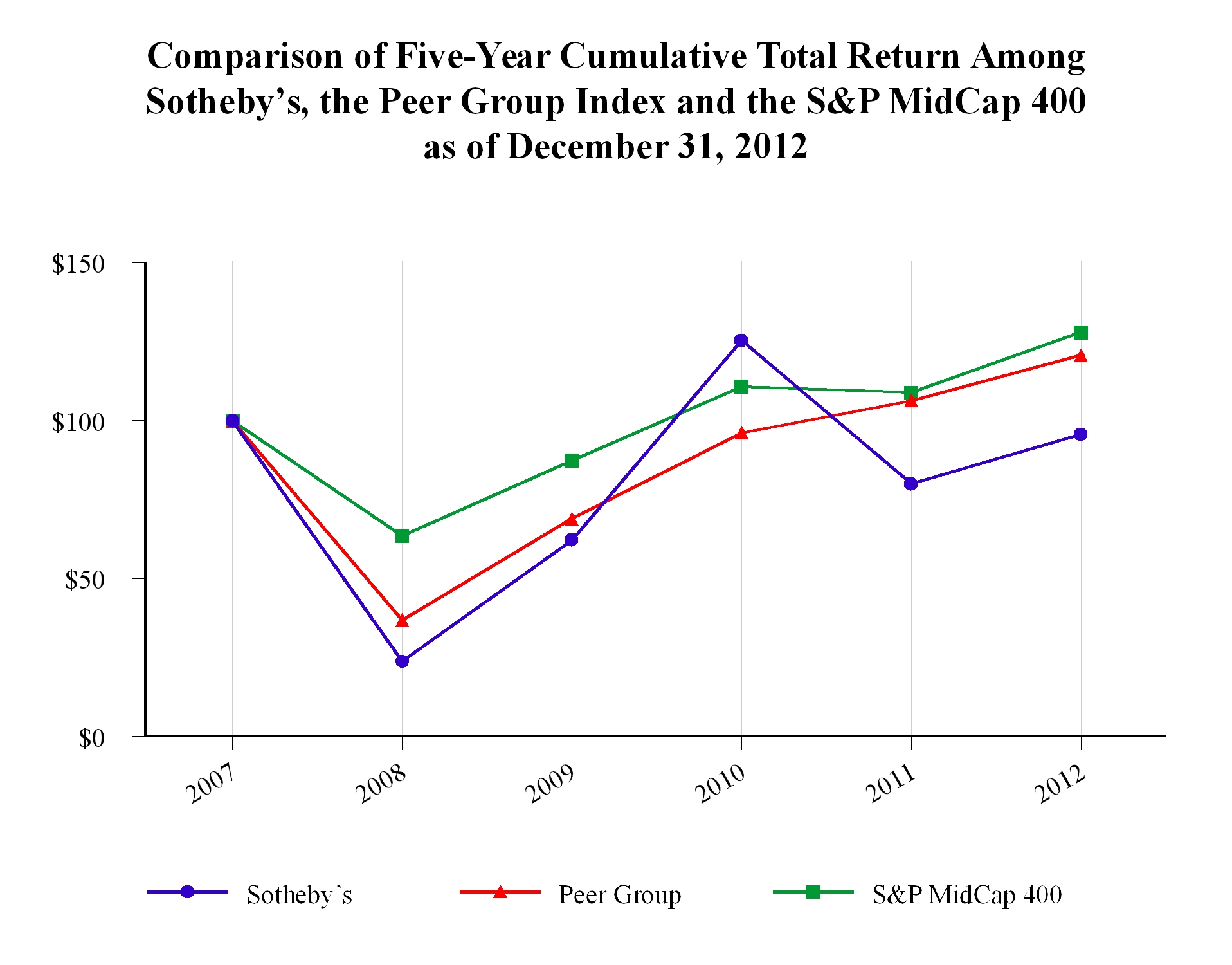

Performance Graph

The following graph compares the cumulative total shareholder return on Sotheby’s Common Stock for the five-year period from December 31, 2007 to December 31, 2012 with the cumulative return of the Standard & Poor’s MidCap 400 Stock Index (“S&P MidCap 400”) and Sotheby’s Peer Group (“the Peer Group”). The Peer Group consists of Nordstrom, Inc., Saks Holdings, Inc., Tiffany & Co. and Movado, Inc. Management believes the members of the Peer Group to be purveyors of luxury goods appealing to a segment of the population consistent with Sotheby’s own clientèle, as no other auction house of comparable market share or capitalization is publicly traded.

The graph reflects an investment of $100 in Sotheby’s Common Stock, the S&P MidCap 400, which includes Sotheby’s, and its Peer Group, respectively, on December 31, 2007, and a reinvestment of dividends at the average of the closing stock prices at the beginning and end of each quarter.

|

| | | | | | | | | | | | | | | | | | |

| | 12/31/07 | 12/31/08 | 12/31/09 | 12/31/10 | 12/31/11 | 12/31/12 |

| Sotheby's | $ | 100.00 |

| $ | 23.96 |

| $ | 62.23 |

| $ | 125.40 |

| $ | 80.01 |

| $ | 95.76 |

|

| Peer Group | $ | 100.00 |

| $ | 37.04 |

| $ | 69.05 |

| $ | 96.24 |

| $ | 106.36 |

| $ | 120.73 |

|

| S&P MidCap 400 | $ | 100.00 |

| $ | 63.71 |

| $ | 87.52 |

| $ | 110.85 |

| $ | 108.94 |

| $ | 128.40 |

|

ITEM 6: SELECTED FINANCIAL DATA

|

| | | | | | | | | | | | | | | | | | | | |

| Year ended December 31 | | 2012 | | 2011 | | 2010 | | 2009 | | 2008 |

| | | (Thousands of dollars, except per share data) |

| Statistical Metric: | | |

| | |

| | |

| | |

| | |

|

| Net Auction Sales (a) | | $ | 3,809,656 |

| | $ | 4,240,573 |

| | $ | 3,644,764 |

| | $ | 1,912,589 |

| | $ | 4,189,735 |

|

| Income Statement Data: | | |

| | |

| | |

| | |

| | |

|

| Auction and related revenues | | $ | 717,231 |

| | $ | 791,738 |

| | $ | 731,021 |

| | $ | 448,768 |

| | $ | 616,625 |

|

| Finance revenues | | 17,707 |

| | 12,038 |

| | 9,685 |

| | 9,073 |

| | 14,183 |

|

| Dealer revenues | | 26,180 |

| | 21,790 |

| | 29,092 |

| | 22,339 |

| | 55,596 |

|

| License fee revenues | | 6,124 |

| | 5,228 |

| | 3,682 |

| | 3,270 |

| | 3,438 |

|

| Other revenues | | 1,250 |

| | 1,042 |

| | 829 |

| | 1,508 |

| | 1,717 |

|

| Total revenues | | $ | 768,492 |

| | $ | 831,836 |

| | $ | 774,309 |

| | $ | 484,958 |

| | $ | 691,559 |

|

| Net interest expense | | $ | (42,879 | ) | | $ | (37,496 | ) | | $ | (45,080 | ) | | $ | (40,351 | ) | | $ | (31,652 | ) |

| Net income (loss) | | $ | 108,292 |

| | $ | 171,416 |

| | $ | 160,950 |

| | $ | (6,528 | ) | | $ | 26,456 |

|

| Basic earnings (loss) per share | | $ | 1.59 |

| | $ | 2.52 |

| | $ | 2.37 |

| | $ | (0.10 | ) | | $ | 0.39 |

|

| Diluted earnings (loss) per share | | $ | 1.57 |

| | $ | 2.46 |

| | $ | 2.34 |

| | $ | (0.10 | ) | | $ | 0.38 |

|

| Cash dividends declared per share | | $ | 0.52 |

| | $ | 0.23 |

| | $ | 0.20 |

| | $ | 0.30 |

| | $ | 0.60 |

|

| Balance Sheet Data: | | |

| | |

| | |

| | |

| | |

|

| Working capital | | $ | 706,244 |

| | $ | 728,984 |

| | $ | 573,020 |

| | $ | 525,892 |

| | $ | 662,993 |

|

| Total assets | | $ | 2,575,095 |

| | $ | 2,399,414 |

| | $ | 2,178,628 |

| | $ | 1,586,123 |

| | $ | 1,662,968 |

|

| Long-term debt, net (b) | | $ | 515,197 |

| | $ | 464,552 |

| | $ | 472,862 |

| | $ | 512,939 |

| | $ | 461,663 |

|

| Shareholders’ equity | | $ | 992,826 |

| | $ | 903,667 |

| | $ | 771,508 |

| | $ | 576,985 |

| | $ | 572,093 |

|

| |

| (a) | Represents the hammer (sale) price of property sold at auction. See "Results of Operations for the Years Ended December 31, 2012 and 2011" under Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations," for other statistical metrics. |

| |

| (b) | Includes the York Property capital lease obligation of $167.2 million as of December 31, 2008. Sotheby's purchased the York Property on February 6, 2009 and financed the purchase, in part, through the assumption of an existing $235 million mortgage (see Note J of Notes to Consolidated Financial Statements). |

| |

ITEM 7: | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF |

OPERATIONS

Seasonality

The worldwide art auction market has two principal selling seasons, which generally occur in the second and fourth quarters of the year. Accordingly, Sotheby’s auction results are seasonal, with peak revenues and operating income generally occurring in those quarters. Consequently, first and third quarter results have historically reflected a lower volume of auction activity when compared to the second and fourth quarters and, typically, a net loss due to the fixed nature of many of Sotheby’s operating expenses. (See Note U of Notes to Consolidated Financial Statements for Sotheby's quarterly results for the years ended December 31, 2012 and 2011.)

Use of Non-GAAP Financial Measures

GAAP refers to generally accepted accounting principles in the United States of America. Included in Management's Discussion and Analysis of Financial Condition and Results of Operations (or “MD&A”) are financial measures presented in accordance with GAAP and also on a non-GAAP basis. EBITDA, EBITDA Margin, and Net Liquidity, as presented in MD&A under “Statistical Metrics,” are supplemental financial measures that are not required by or presented in accordance with GAAP.