As filed with the Securities and Exchange Commission on July 16, 2003

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

APOGENT TECHNOLOGIES INC.

(Exact name of registrant as specified in its charter)

| Wisconsin | | 3843 | | 22-2849508 |

(State or other jurisdiction of incorporation or organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer Identification No.) |

AND ITS GUARANTOR SUBSIDIARIES

Delaware | | Apogent Finance Company | | 02-0522134 |

Delaware | | Apogent Holding Company | | 02-0688113 |

Delaware | | Apogent Service Corporation | | 32-0056654 |

Delaware | | Apogent Transition Corp. | | 13-3326805 |

California | | Applied Biotech, Inc. | | 33-0447325 |

Delaware | | Barnstead Thermolyne Corporation | | 13-3326802 |

Delaware | | BT Canada Holdings Inc. | | 02-0523030 |

Alabama | | Capitol Vial, Inc. | | 63-1091273 |

Wisconsin | | Chase Scientific Glass, Inc. | | 62-1711339 |

Wisconsin | | Consolidated Technologies, Inc. | | 74-2951231 |

Delaware | | Erie Scientific Company | | 13-3326819 |

Delaware | | Erie Scientific Company of Puerto Rico | | 22-2855227 |

Delaware | | Erie UK Holding Company | | 02-0523659 |

Wisconsin | | Ever Ready Thermometer Co., Inc. | | 22-3329530 |

California | | Forefront Diagnostics, Inc. | | 33-0733551 |

New York | | Genevac Inc. | | 13-3614495 |

Delaware | | G&P Labware Holdings Inc. | | 02-0528748 |

Delaware | | Lab-Line Instruments, Inc. | | 36-2160341 |

California | | Lab Vision Corporation | | 94-3204455 |

Delaware | | Marsh Bio Products, Inc. | | 03-0418855 |

Delaware | | Matrix Technologies Corporation | | 04-2876817 |

Delaware | | Metavac LLC | | 02-0530733 |

Delaware | | Microgenics Corporation | | 68-0148167 |

California | | Molecular BioProducts, Inc. | | 95-3244122 |

Delaware | | Nalge Nunc International Corporation | | 13-3326816 |

Wisconsin | | National Scientific Company | | 58-2315507 |

Connecticut | | The Naugatuck Glass Company | | 06-0465440 |

California | | Neomarkers, Inc. | | 94-3223858 |

Wisconsin | | NERL Diagnostics Corporation | | 05-0486109 |

Wisconsin | | Owl Separation Systems, Inc. | | 39-1915146 |

Wisconsin | | Remel Inc. | | 74-2826694 |

Wisconsin | | Richard-Allan Scientific Company | | 38-3235594 |

California | | Robbins Scientific Corporation | | 94-2456711 |

Delaware | | Samco Scientific Corporation | | 95-3145731 |

Delaware | | Separation Technology, Inc. | | 93-0968130 |

Delaware | | Seradyn Inc. | | 02-0530147 |

| | |

(State or other jurisdiction of incorporation or organization) | | (Exact name of Guarantor as specified in its Charter) | | (I.R.S. Employer Identification Number) |

30 Penhallow Street Portsmouth, New Hampshire 03801 (603) 433-6131 | | MICHAEL K. BRESSON Executive Vice President—General Counsel and Secretary Apogent Technologies Inc. 30 Penhallow Street Portsmouth, New Hampshire 03801 (603) 433-6131 |

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) | | (Name, address, including zip code, and telephone number, including area code of agent for service) |

Copies of all communications, including all communications sent to the agent should be sent to:

BRUCE C. DAVIDSON

JOSEPH D. MASTERSON

Quarles & Brady LLP

411 East Wisconsin Avenue

Milwaukee, WI 53202

(414) 277-5000

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this Form is filed t register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

Title of each class of securities to be registered | | Amount to be registered(1) | | Proposed maximum offering price per unit | | Proposed maximum aggregate offering price | | Amount of registration fee(1) |

|

Series B 6 1/2% Senior Subordinated Notes Due 2013 | | $250,000,000 principal amount | | 100% | | $250,000,000(2) | | $20,225 |

|

Guarantees of each of the Guarantor Subsidiaries | | (2) | | (3) | | (3) | | None(3) |

| (1) | Fee based upon $80.90 per $1 million of aggregate offering amount. |

| (2) | The Series B 6 1/2% Senior Subordinated Notes Due 2013 (the “Exchange Notes”) will be guaranteed by each of the Guarantor Subsidiaries. |

| (3) | No additional consideration will be paid by the recipients of the Exchange Notes for the Guarantees. Pursuant to Rule 457(n), no separate fee is payable for the Guarantees. |

The registrants hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrants shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS

SUBJECT TO COMPLETION DATED JULY 16, 2003

Apogent Technologies Inc.

OFFER TO EXCHANGE UP TO $250,000,000 IN PRINCIPAL AMOUNT OF ITS SERIES B 6 1/2% SENIOR SUBORDINATED NOTES DUE 2013 FOR ANY AND ALL OF ITS OUTSTANDING $250,000,000 IN PRINCIPAL AMOUNT OF 6 1/2% SENIOR SUBORDINATED NOTES DUE 2013

THE EXCHANGE OFFER WILL EXPIRE AT 5:00 P.M. NEW YORK CITY TIME ON , 2003, UNLESS EXTENDED.

Apogent Technologies Inc. (“Apogent” or the “Company”) is offering the Series B 6 1/2% Senior Subordinated Notes due 2013 (the “Exchange Notes”). We are offering to exchange (the “Exchange Offer”) up to $250,000,000 in aggregate principal amount of Exchange Notes for $250,000,000 aggregate principal amount of our outstanding 6 1/2% Senior Subordinated Notes due 2013 (the “Original Notes”). We sometimes refer to the Original Notes and the Exchange Notes collectively as the “notes.”

The terms of the Exchange Notes are substantially identical in all respects (including principal amount, interest rate and maturity) to the terms of the Original Notes for which they may be exchanged pursuant to the Exchange Offer, except that the Exchange Notes will be freely transferable by holders thereof (other than as described herein), are issued free of any covenant restricting transfer absent registration and will not have the right to receive liquidated damages in the event of a failure to timely register the Exchange Notes. The Exchange Notes will evidence the same debt as the Original Notes and contain terms that are substantially identical as the terms of the Original Notes. For a description of the terms of the notes, see “Description of Notes.” There will be no cash proceeds to Apogent from the Exchange Offer.

The Exchange Notes will bear interest from the most recent date to which interest has been paid on the Original Notes, or if no interest has been paid on the Original Notes, from June 2, 2003. Holders whose Original Notes are accepted for exchange will not receive any payment in respect of interest on the Original Notes otherwise payable on any interest payment date the record date for which occurs on or after consummation of the Exchange Offer. See “The Exchange Offer—Terms of the Exchange Offer.”

Like the Original Notes, the Exchange Notes will mature on May 15, 2013. Interest is fixed at an annual rate of 6 1/2% and is payable on May 15 and November 15 of each year, beginning on November 15, 2003. Interest will accrue from June 2, 2003. We may redeem some or all of the notes at any time on or after May 15, 2008. Prior to May 15, 2006, we may redeem up to 35% of the aggregate principal amount of the notes with the net cash proceeds of certain equity offerings. Redemption prices are set forth under “Description of Notes—Optional Redemption.” There is no sinking fund for the notes.

The notes will be Apogent Technologies Inc.’s general unsecured obligations and will be guaranteed on a senior subordinated basis by our domestic subsidiaries that have guaranteed, and our subsidiaries that will in the future guarantee, obligations under our revolving credit facility. The notes and the guarantees will rank junior in right of payment to all of Apogent Technologies Inc.’s and each subsidiary guarantor’s existing and future senior debt and will rankpari passu in right of payment with all of Apogent Technologies Inc.’s and each subsidiary guarantor’s senior subordinated debt.

The Original Notes were sold on June 2, 2003, in a transaction that was not registered under the Securities Act. Accordingly, the Original Notes may not be offered or sold within the United States or to U.S. persons, except to qualified institutional buyers in reliance on the exemption from registration provided by Rule 144A and to certain persons in offshore transactions in reliance on Regulation S. We are offering the Exchange Notes to satisfy our obligations under the registration rights agreement relating to the Original Notes. See “The Exchange Offer—Purposes and Effects of the Exchange Offer.”

EACH BROKER-DEALER THAT RECEIVES EXCHANGE NOTES FOR ITS OWN ACCOUNT PURSUANT TO THE EXCHANGE OFFER MUST ACKNOWLEDGE THAT IT WILL DELIVER A PROSPECTUS IN CONNECTION WITH ANY RESALE OF THE EXCHANGE NOTES. THE LETTER OF TRANSMITTAL

STATES THAT BY SO ACKNOWLEDGING AND BY DELIVERING A PROSPECTUS, A BROKER-DEALER WILL NOT BE DEEMED TO ADMIT THAT IT IS AN “UNDERWRITER” WITHIN THE MEANING OF THE SECURITIES ACT. THIS PROSPECTUS, AS IT MAY BE AMENDED OR SUPPLEMENTED FROM TIME TO TIME, MAY BE USED BY A BROKER-DEALER IN CONNECTION WITH ANY RESALES OF EXCHANGE NOTES RECEIVED IN EXCHANGE FOR ORIGINAL NOTES WHERE THE ORIGINAL NOTES WERE ACQUIRED BY THE BROKER-DEALER AS A RESULT OF MARKET-MAKING ACTIVITIES OR OTHER TRADING ACTIVITIES. APOGENT HAS AGREED THAT, FOR A PERIOD OF 180 DAYS AFTER THE EXPIRATION DATE (AS DEFINED HEREIN), IT WILL MAKE THIS PROSPECTUS AVAILABLE TO ANY BROKER-DEALER FOR USE IN CONNECTION WITH ANY SUCH RESALE. SEE “PLAN OF DISTRIBUTION.”

The notes are not listed and will not be listed on any national securities exchange.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2003.

In making your investment decision, you should rely only on the information contained in this prospectus. We have not, and the initial purchasers have not, authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. You should assume that the information appearing in this prospectus is accurate as of the date on the front cover of this prospectus only. Our business, financial condition, results of operations and prospects may have changed since that date. Neither the delivery of this prospectus nor any sale made hereunder shall under any circumstances imply that the information herein is correct as of any date subsequent to the date on the cover of this prospectus.

TABLE OF CONTENTS

Apogent Technologies Inc. is a Wisconsin corporation. Our principal executive offices are located at 30 Penhallow Street, Portsmouth, New Hampshire 03801, and our telephone number at that address is (603) 433-6131. Our World Wide Web site address ishttp://www.apogent.com. The information in our website is not part of this prospectus.

This prospectus has been prepared based on information provided by us and by other sources that we believe are reliable. This prospectus summarizes certain documents and other information in a manner we believe to be accurate, but we refer you to the actual documents for a more complete understanding of what we discuss in this prospectus. You must rely on your own examination of our company and the terms of the offering and the notes, including the merits and risks involved.

We are not making any representation to you regarding the legality of an investment in the notes by you under any legal investment or similar laws or regulations. You should not consider any information in this prospectus to be legal, business, tax or other advice. You should consult your own attorney, business advisor and tax advisor for legal, business and tax advice regarding an investment in the notes.

The distribution of this prospectus and the offer and sale of the notes may be restricted by law in certain jurisdictions. Persons in whose possession this prospectus or any of the notes is delivered must inform themselves about, and observe, any such restrictions.

This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any of the notes to any person in any jurisdiction where it is unlawful to make such an offer or solicitation.

We expect that the notes sold pursuant to this prospectus will be represented by one or more global notes, which will be deposited with, or on behalf of, The Depository Trust Company and registered in the name of Cede

i

& Co. Beneficial interests in the global notes representing the notes will be shown on, and transfers thereof will be effected through, records maintained by The Depository Trust Company and its participants. After the initial issuance of the global notes, notes in certificated form will be issued in exchange for the global notes only under limited circumstances on the terms set forth in the indenture.

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR A LICENSE HAS BEEN FILED UNDER RSA 421-B WITH THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT A SECURITY IS EFFECTIVELY REGISTERED OR A PERSON IS LICENSED IN THE STATE OF NEW HAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OF STATE THAT ANY DOCUMENT FILED UNDER RSA 421-B IS TRUE, COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACT THAT AN EXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITY OR A TRANSACTION MEANS THAT THE SECRETARY OF STATE HAS PASSED IN ANY WAY UPON THE MERITS OR QUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON, SECURITY OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TO ANY PROSPECTIVE PURCHASER, CUSTOMER OR CLIENT ANY REPRESENTATION INCONSISTENT WITH THE PROVISIONS OF THIS PARAGRAPH.

FORWARD-LOOKING STATEMENTS

All statements other than statements of historical facts included in this prospectus, including, without limitation, statements under the captions “Risk Factors,” “Use of Proceeds,” and “Business,” are or could be deemed to be forward-looking statements. Words such as “anticipate,” “believe,” “continue,” “estimate,” “expect,” “goal,” “objective,” “outlook” and similar expressions signify forward-looking statements. These statements are based upon our expectations at the time we made them and are subject to risks and uncertainties, many of which are beyond our control, that could cause actual results to differ materially from those contemplated in the forward-looking statements. In addition to the assumptions and other factors referred to specifically in connection with forward-looking statements, factors that could cause our actual results to differ materially include the factors described under the caption “Cautionary Factors” in this prospectus and in our SEC filings incorporated by reference into this prospectus. The risks and uncertainties so identified are not the only ones facing our company. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial also may adversely affect us. Should any risks and uncertainties develop into actual events, these developments could have material adverse effects on our business, financial condition and results of operations. For these reasons, we caution you not to place undue reliance on our forward-looking statements.

INDUSTRY AND MARKET DATA

In this prospectus we rely on and refer to information and statistics regarding Apogent’s markets and our market share in the sectors in which we compete. We obtained this information and statistics from various third-party sources, discussions with our customers and our own internal estimates. We believe that these sources and estimates are reliable, but have not independently verified them and cannot guarantee their accuracy or completeness.

WHERE YOU CAN FIND MORE INFORMATION

We file annual, quarterly and special reports, proxy statements, and other documents with the Securities and Exchange Commission. Our SEC filings are available to the public at the SEC’s website athttp://www.sec.gov.

ii

You may also read and copy any document we file with the SEC at the public reference rooms maintained by the Commission at Judiciary Plaza, Room 1024, 450 Fifth Street, N.W., Washington, D.C. 20549. In addition, you may also obtain copies of the documents at prescribed rates by writing to the Public Reference Section of the SEC at 450 Fifth Street, N.W., Room 1024, Washington, D.C. 20549. You may obtain information regarding the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

In addition, because our common stock is listed on the New York Stock Exchange (ticker symbol “AOT”), you may read our reports, proxy statement, and other documents at the offices of the New York Stock Exchange at 20 Broad Street, New York, New York 10005.

INCORPORATION BY REFERENCE

The SEC allows us to “incorporate by reference” information in documents that we file with it. We have elected to use this procedure in connection with this prospectus, which means that we can disclose important information by referring you to documents that contain that information, and the information incorporated by reference is considered part of this prospectus. Information that we file later with the SEC is automatically incorporated by reference and will update and supersede the previously filed information. Note that we filed our documents under the name Sybron International Corporation until our name was formally changed to Apogent Technologies Inc. on January 31, 2001, so you may need to look under both names to find all information that is of interest to you. We incorporate by reference into this prospectus:

| | �� | our annual report on Form 10-K for the fiscal year ended September 30, 2002; |

| | • | our quarterly reports on Form 10-Q for the quarters ended December 31, 2002 and March 31, 2003; |

| | • | our current reports on Form 8-K or 8-K/A dated as of December 18, 2002, January 6, 2003, April 22, 2003, May 13, 2003, May 22, 2003, and June 2, 2003; and |

| | • | any future filings we make with the SEC under Sections 13(a), 13(c), 14 or 15(d) of the Securities Exchange Act of 1934 until we sell all of the securities offered by this prospectus or terminate the offering. |

You may request copies of these filings, at no cost, by writing or calling us at Apogent Technologies Inc., Attn: Investor Relations, 30 Penhallow Street, Portsmouth, New Hampshire 03801, (603) 433-6131.

We maintain an Internet web site athttp://www.apogent.com. Our web site and information at that site, or connected to that site, are not incorporated into this prospectus.

iii

PROSPECTUS SUMMARY

This summary highlights some information from this prospectus, but it may not contain all of the information that is important to you. You should read this summary together with the entire prospectus, especially “Risk Factors” beginning on p. . For more complete information about Apogent, its business, its financial statements and related matters, you should refer to the documents mentioned in the section of this prospectus entitled “Incorporation by Reference.” For a more complete understanding of the notes, please refer to the section of this document entitled “Description of Notes.” Unless the context otherwise requires, all references to “Apogent,” “us,” “we,” “our,” and, “our company” refer to Apogent Technologies Inc., the issuer of the notes, and its subsidiaries. Our fiscal year ends on September 30.

In the second quarter of our 2003 fiscal year, we made the decision to exit two of our businesses, Applied Biotech, Inc. and BioRobotics Group Ltd., which have been reclassified as discontinued operations. All historical financial information in this prospectus has been restated to reflect this reclassification and, accordingly, the results of operations of these businesses are not included in net sales, cost of sales, or other components of operating income but, instead, are included in discontinued operations.

Apogent Technologies Inc.

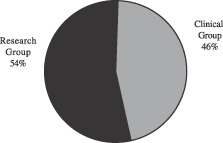

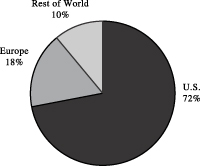

Apogent is a leading global developer, manufacturer, and marketer of value-added consumable products and equipment for the clinical and research industries. We manufacture and sell approximately 10,000 different consumable and non-consumable products. Consumable products, which are ordered on a recurring basis by our customers and end-users, represented over 80% of our net sales for the twelve months ended March 31, 2003. We are organized into two business segments, the Clinical Group and the Research Group, which serve our customers involved in clinical and research activities globally. Our Clinical Group develops and manufactures a full line of clinical and commercial laboratory products, and our Research Group develops and manufactures a full line of research and life science products. We reach our customers and end-users through a network of independent distributors and through our direct sales force. We manufacture most of the products we sell in our 62 manufacturing facilities. We have approximately 7,200 employees in over 125 facilities worldwide. Our customers include distributors, pharmaceutical and biotechnology companies, clinical, academic, governmental, research, and industrial laboratories, and OEMs. Approximately 72% of our consolidated net sales in fiscal 2002 were to customers in the U.S. and the remainder was to customers, primarily in Europe and Japan. For the twelve-month period ended March 31, 2003, we generated net sales of $1,073.3 million and net cash provided by operating activities of $165.6 million.

We focus on developing and manufacturing products that are industry staples and that are used in the majority of clinical and research laboratories. Most of our products have established brand names, many of which have been in existence for decades. We believe industry professionals demand our products because of our reputation for quality and the essential role that our products play in the research and development and diagnostic activities of our end-users.

In December 2000, we spun off our dental business by way of a pro rata distribution to our shareholders of all of the outstanding common stock and related preferred stock purchase rights of Sybron Dental Specialties, Inc. As a result of the spin-off, Sybron Dental Specialties became an independent public company operating what was our dental business. We changed our name from Sybron International Corporation to Apogent Technologies Inc. in 2001. Our financial statements in this prospectus reflect the dental business as a discontinued operation.

1

The following charts show our net sales for the twelve months ended March 31, 2003 by business segment and geographic area.

| Net Sales by Business Segment | | Net Sales by Geography |

| |  |

Clinical Group

Our Clinical Group manufactures and sells products primarily to clinical and commercial laboratories and to scientific research and industrial customers. These products are used in a number of diagnostic applications, including specimen collection, specimen transportation, drug testing, therapeutic drug monitoring, infectious disease detection, and glucose tolerance testing. Other applications include anatomical pathology (histology and cytology) and immunohistochemistry, with an emphasis on cancer applications. Clinical Group products include:

| | • | microscope slides, cover glass, and glass tubes and vials; |

| | • | histology and immunochemistry instrumentation; |

| | • | sample vials used in diagnostic testing; |

| | • | diagnostic reagents; and |

| | • | other products used in detecting causes of various infectious diseases, conditions, and therapeutic drugs or drugs of abuse. |

For the twelve-month period ended March 31, 2003, our Clinical Group generated net sales of $496.9 million and operating income of $124.7 million.

Research Group

Our Research Group manufactures, distributes, and sells products primarily to the research and clinical life sciences industries. Applications of these products include general everyday laboratory uses as well as genomics, proteomics, high-throughput screening for drug discovery, combinatorial chemistry, cell culture, filtration, and liquid handling. In addition, this segment manufactures basic laboratory equipment needed by medical, pharmaceutical, and scientific laboratories. Research Group products include:

| | • | reusable plastic and glass products (e.g., bottles, carboys, graduated ware, beakers, flasks, and plastic bottles for consumer use); |

| | • | disposable plastic and glass products; |

| | • | products for critical packaging applications; |

2

| | • | environmental and safety containers; |

| | • | liquid handling automation products; |

| | • | autosampler vials and seals used in chromatography analysis; |

| | • | various consumable products for use in applications of cell culture, filtration, molecular biology, cryopreservation, immunology, electrophoresis, liquid handling, genomics, and high-throughput screening for pharmaceutical drug discovery; and |

| | • | heating, cooling, shaking, stirring, mixing, and temperature control instruments. |

For the twelve-month period ended March 31, 2003, our Research Group generated net sales of $576.4 million and operating income of $123.6 million.

Industry

We believe the size of the global life sciences and laboratory products supply markets that we address is approximately $35.0 billion. There are a number of trends in the laboratory supply business that we believe will support continuing growth in the overall market, including:

| | • | growing number of in vitro diagnostic tests per person; |

| | • | increasing rates of cancer; |

| | • | increasing R&D budgets at pharmaceutical companies; |

| | • | growth in large-scale cell culture products; and |

| | • | increasing economic development in emerging market countries. |

Competitive Strengths

Our competitive strengths include:

| | • | Recurring revenue from sale of consumables. Sales of consumable products ordered on a recurring basis by our customers and end-users account for a substantial portion of our net sales. For the twelve months ended March 31, 2003, consumable products sales represented over 80% of our net sales. We supply a significant portion of the consumables used in specimen examinations by pathologists and our products are used in the majority of non-discretionary physician-prescribed clinical applications. We believe our long-standing relationships with loyal customers who purchase our consumable products provide a stable and predictable recurring revenue stream. |

| | • | Strong cash flow generation. We generate substantial cash flow from operations and our manufacturing operations require relatively modest investment. During the twelve months ended March 31, 2003, we generated cash flow from operations of $165.6 million and spent $69.1 million on capital expenditures. Our cash flow provides us with a high degree of flexibility to fund our internal and acquisition growth initiatives and to service our balance sheet obligations. |

| | • | Diverse product mix. We manufacture, distribute, and sell a unique mix of products, including high-margin industry staples and products in new, higher growth markets. Industry staples are composed largely of routine disposable lab supplies and consumable products. Higher growth markets include life sciences products used in diagnostic, biotechnology, and pharmaceutical laboratories. |

| | • | Leading market positions and industry leading brands. We have well established brands in both our Clinical Group and our Research Group. Key brands in our Clinical Group include Remel®, Erie Scientific®, Chase Scientific™, Richard-Allan Scientific®, and Microgenics®. Key brands in our Research Group include Nalgene®, Nunc®, Barnstead International™, Molecular BioProducts™, Matrix®, and ABgene™. We believe we have leading positions in the majority of our key product lines. |

3

| | • | Long established customer relationships. We have long-standing relationships with our core customers, particularly our three primary laboratory distributors with whom we have conducted business for an average of 30 years, and with our key OEMs. |

| | • | Strong and experienced management team. We have assembled an experienced and successful management team. On average, each member of our senior executive management team has over 20 years of relevant industry experience. Our management has demonstrated a strong capability for growing our business and successfully managing our balance sheet and cash flows. |

Business Strategy

Our goal is to consistently grow our worldwide market presence, net sales, earnings, and cash flows. Annual revenue growth in fiscal 2002 was $89.1 million, or 9.5% over the prior year, and in the first six months of fiscal 2003 was $45.4 million or 9.3% over the comparable prior year period. Key elements of our strategy continue to be:

| | • | Maintain prudent capital structure. We consider our ability to manage our balance sheet effectively to be a core competence. Strategic investments which require an outlay of capital are put through a rigorous review process to ensure the investment provides an acceptable cash return which exceeds our cost of capital. We maintain a capital structure which provides us with the financial flexibility to compete effectively in our core markets. |

| | • | Develop profitable new products. We consistently strive to develop and introduce new products that contribute to sales, earnings, and cash flows. These products include new offerings and improvements of our existing products. We are especially focused on developing new products for our life sciences research, and clinical diagnostics customers. |

| | • | Increase sales to existing and new customers. We seek to leverage our strong market presence and excellent customer and distributor relationships into increased sales to current customers and sales to new customers. We believe that our extensive product offering is conducive to cross-selling products to existing customers. This broad product offering is also conducive to negotiating favorable terms with our distributors. |

| | • | Improve operating efficiencies. We are focused on improving our operating efficiencies through vertical integration, streamlined manufacturing techniques, better product sourcing, and the sharing of technology and best practices across our company. We believe that our focus on efficiencies improves our gross margins while maintaining or improving the quality of our products and increases customer satisfaction. |

| | • | Make strategic acquisitions. Our acquisition program has been and continues to be focused on adding complementary products and technologies that enhance our market position. Our operating subsidiaries generally have been able to use their existing channels to market our acquired products. We have a rigorous process of candidate identification, due diligence, and integration designed to mitigate acquisition risk. Acquired businesses are converted to our standard financial reporting system. In most cases, we retain the senior management of acquired businesses and have an integration plan and budget in place at the time the acquisition closes. We presently intend to reduce our emphasis on our acquisition strategy and focus on steadily increasing our earnings and cash flows through the development of new products, increasing sales to existing and new customers, and focusing on improving efficiencies. |

The Recapitalization

On April 23, 2003, we initiated a tender offer for up to 15.0 million of our common shares, representing approximately 15% of our outstanding shares, pursuant to a modified Dutch auction tender offer at a price of not

4

less than $15.00 or more than $17.50 per share. We entered into an amendment of our revolving credit facility which allowed us to consummate the tender offer. The tender offer expired May 21, 2003. We purchased approximately 6.0 million common shares in the tender offer at $17.50 per share, or a total cost of $105.4 million. We used approximately 42% the proceeds of the Original Notes offering to finance our purchase of shares in the tender offer. We have used or expect to use the remaining net proceeds of the Original Notes offering to repurchase shares of our common stock in the open market or otherwise, to repay the outstanding balance under our revolving credit facility, and for general corporate purposes.

Recent Developments

We recently realigned our lines of business for financial reporting purposes. Our three former business segments (Clinical Diagnostics, Labware and Life Sciences, and Laboratory Equipment) have been reclassified into two business segments: Clinical Group and Research Group. The Clinical Group business segment is the former Clinical Diagnostics business segment. The Research Group business segment is composed of the former Labware and Life Sciences and Laboratory Equipment business segments. All financial data presented in this prospectus reflect this change in reporting business segments.

During the second quarter of our 2003 fiscal year, we made the decision to exit two of our businesses: the rapid diagnostic test business (on-site rapid tests in the detection of pregnancy, drugs of abuse, and infectious diseases) as conducted by our Applied Biotech, Inc. subsidiary; and the manufacture and sale of automated microarray instrumentation for the genomics market as conducted by our BioRobotics Group subsidiary. This decision was based in part on our ongoing strategy of strengthening the market positions of our leading brands and focusing on sales of our consumable laboratory products that have more stable growth expectations.

On April 23, 2003, we initiated the tender offer relating to our recapitalization, which expired at midnight, New York City time, on May 21, 2003. On April 23, 2003, in response to the announcement of our tender offer and the offering of the Original Notes, Standard & Poor’s Ratings Services lowered our corporate credit and senior unsecured debt ratings to “BBB-” from “BBB.” In addition, on May 9, 2003, Moody’s Investors Service downgraded our revolving credit facility, senior notes, and senior convertible contingent notes from a rating of Baa3 to Ba1 and assigned a rating of Ba2 to the notes offered in this prospectus. On May 13, 2003, Standard & Poor’s assigned a rating of BB+ to the notes. Under the terms of the indenture which governs the notes, we are subject to certain restrictive covenants until the notes are rated investment grade. See “Description of Notes—Certain Covenants.”

5

The Exchange Offer

Purpose of Exchange Offer | | We sold the Original Notes in a private offering to certain accredited institutions through Lehman Brothers, Credit Suisse First Boston, JPMorgan, ABN AMRO Incorporated, Banc of America Securities LLC, Banc One Capital Markets, Inc., Comerica Securities, Fleet Securities, Inc., Goldman, Sachs & Co., Robert W. Baird & Co., Scotia Capital, SunTrust Robinson Humphrey, The Royal Bank of Scotland, and Wachovia Securities (the “initial purchasers”). In connection with that offering, we executed and delivered for the benefit of holders of the Original Notes a registration rights agreement, which is an exhibit to the registration statement of which this prospectus is a part, providing for, among other things, the Exchange Offer. The Exchange Offer is intended to make the Exchange Notes freely transferable by the holders thereof without registration or any prospectus delivery requirements under the Securities Act, except that a “dealer” or any “affiliate” of a “dealer” (as those terms are defined under the Securities Act) who exchanges Original Notes held for its own account (a “Restricted Holder”) will be required to deliver copies of this prospectus in connection with any resale of the Exchange Notes issued in exchange for those Original Notes. See “The Exchange Offer—Purposes and Effects of the Exchange Offer” and “Plan of Distribution.” |

| |

The Exchange Offer | | We are offering to exchange pursuant to the Exchange Offer up to $250 million aggregate principal amount of our new Series B

6½% Senior Subordinated Notes Due 2013 (the “Exchange Notes”) for $250 million aggregate principal amount of our outstanding 6 ½% Senior Subordinated Notes Due 2013 (the “Original Notes”). We sometimes refer to the Original Notes and the Exchange Notes collectively as the “notes.” The terms of the Exchange Notes are substantially identical in all respects (including principal amount, interest rate and maturity) to the terms of the Original Notes, except that the Exchange Notes are freely transferable by the holders thereof (other than as provided herein), and are not subject to any covenant regarding registration under the Securities Act. See “The Exchange Offer—Terms of the Exchange Offer” and “The Exchange Offer—Procedures for Tendering.” The Exchange Offer is not conditioned upon any minimum aggregate principal amount of Original Notes being tendered for exchange. |

| |

Expiration Date | | The Exchange Offer will expire at 5:00 p.m., New York City time on , 2003, unless extended (the “Expiration Date”). |

| |

Conditions of the Exchange Offer | | Our obligation to consummate the Exchange Offer is subject to certain conditions. We will not be required to accept for exchange any Original Notes tendered and may terminate the Exchange Offer before acceptance of any Original Notes if, among other |

6

| | | things, legal actions or proceedings are instituted that challenge or seek to prohibit the exchange or there shall have been proposed, adopted or enacted any law, statute or regulation materially affecting the benefits of the Exchange Offer. See “The Exchange Offer—Conditions of the Exchange Offer.” We reserve the right to terminate or amend the Exchange Offer at any time prior to the Expiration Date upon the occurrence of any of the conditions. |

| |

Procedures for Tendering Original Notes | | To accept the Exchange Offer, you must complete, sign and date the Letter of Transmittal, or a facsimile of it, in accordance with the instructions in this prospectus and contained in the Letter of Transmittal, and mail or otherwise deliver the Letter of Transmittal or facsimile, together with the Original Notes and any other required documentation, to the exchange agent (the “Exchange Agent”) at the address set forth therein. Physical delivery of the Original Notes is not required if a confirmation of a book-entry transfer of the Original Notes to the Exchange Agent’s account at The Depository Trust Company (“DTC” or the “Depository”) is timely delivered. By executing the Letter of Transmittal, you will represent to us that: • you are acquiring the Exchange Notes in the ordinary course of business, • you are not engaged in, do not intend to engage in, and have no arrangement or understanding with any person to participate in, the distribution of the Original Notes or the Exchange Notes within the meaning of the Securities Act, and • you are not an “affiliate” of Apogent as defined under the Securities Act, or if you are an affiliate, that you will comply with the registration and prospectus delivery requirements of the Securities Act, to the extent applicable. In addition, each broker or dealer that receives Exchange Notes for its own account in exchange for any Original Notes that were acquired by the broker or dealer as a result of market-making activities or other trading activities must acknowledge that it will deliver a prospectus in connection with any resale of the Exchange Notes. See “The Exchange Offer—Procedures for Tendering” and “Plan of Distribution.” |

| |

Special Procedures for Beneficial Owners | | If you are a beneficial owner whose Original Notes are registered in the name of a broker dealer, commercial bank, trust company or other nominee and you wish to tender, you should contact the registered holder promptly and instruct the registered holder to tender on your behalf. If the Original Notes are in certificated |

7

| | | form and you are a beneficial owner who wishes to tender on the registered holder’s behalf, prior to completing and executing the Letter of Transmittal and delivering the Original Notes, you must either make appropriate arrangements to register ownership of the Original Notes in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time. See “The Exchange Offer—Procedures for Tendering.” |

| |

Guaranteed Delivery Procedures | | If the Original Notes are in certificated form and you wish to tender your Original Notes in the Exchange Offer and your Original Notes are not immediately available for delivery, you may still tender your shares by completing, signing and delivering the Letter of Transmittal and any other documents required by the Letter of Transmittal to the Exchange Agent prior to the Expiration Date and tendering your Original Notes according to the guaranteed delivery procedures set forth in “The Exchange Offer—Guaranteed Delivery Procedures.” |

| |

Withdrawal Rights | | You may withdraw your tenders at any time prior to 5:00 p.m. New York City time on the Expiration Date. See “The Exchange Offer—Withdrawal of Tenders.” |

| |

Acceptance of Original Notes and Delivery of Exchange Notes | | We will accept for exchange any and all Original Notes that are properly tendered to the Exchange Agent prior to 5:00 p.m. New York City time on the Expiration Date. The Exchange Notes issued pursuant to the Exchange Offer will be delivered promptly following the Expiration Date. See “The Exchange Offer—Terms of the Exchange Offer.” |

| |

Exchange Agent | | The Bank of New York, New York, New York, is serving as the Exchange Agent in connection with the Exchange Offer. See “The Exchange Offer—Exchange Agent.” |

| |

Effect on Holders of the Original Notes | | As a result of making this Exchange Offer, and upon acceptance for exchange of all validly tendered Original Notes pursuant to the terms of this Exchange Offer, we will have fulfilled one of our obligations contained in the registration rights agreement and, accordingly, there will be no registration default and therefore no liquidated damages with respect to the Exchange Offer on the Original Notes pursuant to the registration rights agreement. Holders of Original Notes who do not tender their Original Notes will continue to be entitled to all the rights and limitations applicable thereto under the indenture dated as of June 2, 2003, among Apogent Technologies Inc., the Guarantors, and The Bank of New York, as trustee (the “Trustee”) relating to the Original Notes and the Exchange Notes (the “indenture”), except for any rights under the indenture or the registration’ rights agreement which by their terms terminate or cease to have further |

8

| | | effectiveness as a result of the making of, and the acceptance for exchange of all validly tendered Original Notes pursuant to, the Exchange Offer. All Original Notes that remain outstanding will continue to be subject to the restrictions on transfer provided for in the Original Notes and the indenture. To the extent that Original Notes are tendered and accepted in the Exchange Offer, the trading market for Original Notes could be adversely affected. |

| |

Use of Proceeds | | There will be no cash proceeds to Apogent from the exchange pursuant to the Exchange Offer. |

Terms of the Notes

The Exchange Offer applies to the entire outstanding $250 million principal amount of Original Notes. The terms of the Exchange Notes are identical in all material respects to the Original Notes, except for certain transfer restrictions and registration and other rights relating to the exchange of the Original Notes for Exchange Notes. The Exchange Notes will evidence the same debt as the Original Notes and will governed by the same indenture under which the Original Notes were issued. See “Description of Notes.”

Issuer | | Apogent Technologies Inc. |

| |

Securities Offered | | $250,000,000 aggregate principal amount of Series B 6½% Senior Subordinated Notes due 2013. |

| |

Maturity Date | | May 15, 2013. |

| |

Interest Payment Dates | | May 15 and November 15 of each year, commencing on November 15, 2003. |

| |

Optional Redemption | | We may redeem the notes in whole or in part at any time on or after May 15, 2008, at the redemption prices described under “Description of Notes—Optional Redemption.” Prior to May 15, 2006, we may redeem up to 35% of the aggregate principal amount of the notes (including additional notes, if any) with the net cash proceeds of qualified equity offerings. |

| |

Change of Control | | If we experience specific kinds of changes of control, we must offer to repurchase the notes at 101% of their principal amount, plus accrued and unpaid interest, if any, to the date of repurchase. For more details, see “Description of Notes—Repurchase at the Option of Holders—Change of Control.” |

| |

Guarantees | | All payments with respect to the notes, including principal and interest, will be fully and unconditionally guaranteed, jointly and severally, on a senior subordinated basis by all of our current and future domestic subsidiaries that have guaranteed, and will in the future guarantee, obligations under our revolving credit facility, subject to their release in certain instances described under “Description of Notes—Brief Description of the Notes and the |

9

| | | Guarantees—The Guarantees.” Each guarantee of the notes: • is a general unsecured obligation of the guarantor; • is subordinated in right of payment to all existing and future senior debt of that guarantor; and • ispari passu in right of payment with any future senior subordinated indebtedness of that guarantor. Apogent Technologies Inc. and our material domestic subsidiary guarantors owned 77% of our assets at September 30, 2002 and generated 85% of our income from continuing operations for the fiscal year ended September 30, 2002. |

| |

Ranking | | The notes will be our unsecured senior subordinated obligations. Accordingly, they will rank: • subordinate in right of payment to all of our and our subsidiary guarantors’ existing and future senior indebtedness, including our obligations under our revolving credit facility, 8% senior notes due 2011 and 2.25% Senior Convertible Contingent Debt SecuritiesSM (CODESSM) due 2021, in each case issued by us and guaranteed by certain of our subsidiary guarantors; • effectively subordinate to all of the existing and future indebtedness and other liabilities of our non-guarantor subsidiaries (other than indebtedness and other liabilities owed to us); • pari passu in right of payment to our and our subsidiary guarantors’ future senior subordinated indebtedness; and • senior in right of payment to our and our subsidiary guarantors’ future subordinated indebtedness. On March 31, 2003, after giving pro forma effect to the sale of the Original Notes and the recapitalization, we and our subsidiaries would have had total indebtedness of $923.7 million (of which $250.0 million would have consisted of the notes and the balance would have consisted of our senior indebtedness). Neither we nor our subsidiary guarantors currently have any indebtedness that is expressly subordinated to the notes. |

| |

Certain Covenants | | The notes contain limitations on, among other things: • the payment of dividends and other distributions with respect to our capital stock and the purchase, redemption, or retirement of our capital stock; • our ability to incur additional indebtedness and issue preferred stock; • the right of restricted subsidiaries to make certain payments and distributions; |

10

| | | • asset sales; • transactions with affiliates; • the incurrence of liens; • engaging in certain business activities; and • certain mergers or consolidations and transfers of assets. In the event that the notes are assigned a rating of Baa3 or better by Moody’s Investor Service and BBB- or better by Standard and Poor’s Rating Group, Inc., and no event of default has occurred and is continuing, certain covenants in the indenture will be terminated. For more details, see the section “Description of Notes—Certain Covenants.” |

| |

Exchange Offer, Registration Rights | | In connection with the Original Notes offering, under the registration rights agreement between us, our subsidiary guarantors, and the initial purchasers of the notes entered into on June 2, 2003, we have agreed to: • file with the SEC this registration statement offering to exchange (the “Registered Exchange Offer”) the notes for new notes having substantially identical terms (the “Exchange Notes”) (except that the Exchange Notes will not contain terms with respect to transfer restrictions) within 90 days after the issue date of the Original Notes; and • use our best efforts to cause this registration statement to become effective under the Securities Act within 150 days after the issue date of the Original Notes. Under certain circumstances, in lieu of a Registered Exchange Offer, we have agreed to file a shelf registration statement with respect to the notes and to use our best efforts to keep the shelf registration statement effective for at least two years after its effective date. If we do not comply with these registration obligations, then we will be required to pay liquidated damages to holders of the notes under certain circumstances. See “Description of Notes—Registration Rights; Liquidated Damages.” |

Risk Factors

Prospective purchasers of the notes should carefully consider all information contained in this prospectus, including the risk factors beginning on page 13.

11

Summary Consolidated Financial Data

The following table presents our summary consolidated financial information for the six month periods ended March 31, 2003 and 2002, and the years ended September 30, 2002, 2001, and 2000. The financial information for the six months ended March 31, 2003 and 2002 is derived from our unaudited financial statements which, in the opinion of our management, contain all adjustments necessary for a fair presentation of this information. The financial information for the six months ended March 31, 2003 is not necessarily indicative of the results expected for the full year. The financial information for each of the years ended September 30, 2002, 2001, and 2000 is derived from our audited financial statements. The financial information set forth below should be read in conjunction with our consolidated financial statements and the related notes, “Selected Consolidated Financial Information” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” all included elsewhere in this prospectus.

| | | Twelve Months Ended March 31, 2003

| | | Six Months Ended March 31,

| | | Year Ended September 30,

| |

| | | 2003

| | | 2002

| | | 2002

| | | 2001

| | | 2000

| |

| | | (unaudited) | | | (unaudited) | | | | | | | | | | |

| | | (dollar amounts in thousands) | |

Consolidated Statement of Income Data: | | | | | | | | | | | | | | | | | | | | | | | | |

Net sales | | $ | 1,073,287 | | | $ | 534,436 | | | $ | 489,062 | | | $ | 1,027,913 | | | $ | 938,819 | | | $ | 843,567 | |

Total cost of sales | | | 550,266 | | | | 278,366 | | | | 250,119 | | | | 522,019 | | | | 471,318 | | | | 426,004 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Gross profit | | | 523,021 | | | | 256,070 | | | | 238,943 | | | | 505,894 | | | | 467,501 | | | | 417,563 | |

Total selling, general and administrative expenses | | | 274,690 | | | | 140,272 | | | | 123,536 | | | | 257,954 | | | | 256,485 | | | | 234,018 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Operating income | | | 248,331 | | | | 115,798 | | | | 115,407 | | | | 247,940 | | | | 211,016 | | | | 183,545 | |

Interest expense | | | 40,951 | | | | 20,792 | | | | 20,578 | | | | 40,737 | | | | 48,820 | | | | 49,584 | |

Net income (loss) | | $ | 44,580 | | | $ | (27,649 | ) | | $ | 48,920 | | | $ | 121,149 | | | $ | 95,941 | | | $ | 128,321 | |

| | | | | | |

Other Data: | | | | | | | | | | | | | | | | | | | | | | | | |

Gross margin | | | 48.7 | % | | | 47.9 | % | | | 48.9 | % | | | 49.2 | % | | | 49.8 | % | | | 49.5 | % |

Depreciation and amortization | | $ | 60,778 | | | $ | 30,935 | | | $ | 25,571 | | | $ | 55,414 | | | $ | 73,348 | | | $ | 62,901 | |

Expenditures for property, plant and equipment | | | 69,091 | | | | 22,560 | | | | 17,099 | | | | 63,630 | | | | 50,120 | | | | 41,324 | |

Net cash provided by operating activities | | | 165,636 | | | | 56,964 | | | | 83,478 | | | | 192,150 | | | | 179,393 | | | | 115,375 | |

Ratio of earnings to fixed charges(1) | | | 5.1x | | | | 4.8x | | | | 4.9x | | | | 5.2x | | | | 4.2x | | | | 3.5x | |

Consolidated Balance Sheet Data (at end of period): | | | | | | | | | | | | | | | | | | | | | | | | |

Cash and cash equivalents | | | | | | $ | 17,406 | | | $ | 42,415 | | | $ | 16,327 | | | $ | 9,192 | | | $ | 12,411 | |

Working capital | | | | | | | 293,692 | | | | 191,919 | | | | 230,125 | | | | 150,371 | | | | 269,396 | |

Total assets | | | | | | | 1,984,730 | | | | 1,981,662 | | | | 2,036,085 | | | | 1,828,080 | | | | 1,792,364 | |

Total liabilities | | | | | | | 1,089,463 | | | | 1,099,555 | | | | 1,060,947 | | | | 989,590 | | | | 1,042,848 | |

Shareholders’ equity | | | | | | $ | 895,267 | | | $ | 882,107 | | | $ | 975,138 | | | $ | 838,490 | | | $ | 749,516 | |

| (1) | The ratio of earnings to fixed charges is computed by dividing: |

| | • | income from continuing operations before income taxes and extraordinary item, plus fixed charges, by |

Fixed charges consist of interest expense, amortization of deferred financing fees, and an estimate of interest within rental expense.

The unaudited pro forma ratio of earnings to fixed charges for the year ended September 30, 2002 and the six months ended March 31, 2003 was 4.2 and 3.9, respectively. This ratio has been prepared assuming that the sale of the notes was completed on October 1, 2001.

12

RISK FACTORS

You should carefully consider the following risk factors, in addition to the other information presented in this prospectus and the documents incorporated by reference into this prospectus, in evaluating us, our business and an investment in the notes. Any of the following risks, as well as other risks and uncertainties, could harm our business and financial results and cause the value of the notes to decline, which in turn could cause you to lose all or part of your investment. The risks below are not the only ones facing our company. Additional risks not currently known to us or that we currently deem immaterial also may impair our business.

Risks Relating to the Exchange Offer

You must carefully follow the required procedures in order to exchange your Original Notes.

The Exchange Notes will be issued in exchange for Original Notes only after timely receipt by the Exchange Agent of a duly executed letter of transmittal and all other required documents. Therefore, if you wish to tender your Original Notes, you must allow sufficient time to ensure timely delivery. Neither the Exchange Agent nor we have any duty to notify you of defects or irregularities with respect to tenders of Original Notes for exchange. Any holder of Original Notes who tenders in the Exchange Offer for the purpose of participating in a distribution of the Exchange Notes will be required to comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale transaction. Each broker or dealer that receives Exchange Notes for its own account in exchange for Original Notes that were acquired in market-making or other trading activities must acknowledge that it will deliver a prospectus in connection with any resale of the Exchange Notes. See “Plan of Distribution.”

If you do not exchange Original Notes for Exchange Notes, transfer restrictions will continue and trading of the Original Notes may be adversely affected.

The Original Notes have not been registered under the Securities Act and are subject to substantial restrictions on transfer. Original Notes that are not tendered for exchange for Exchange Notes or are tendered but are not accepted will, following completion of the Exchange Offer, continue to be subject to existing restrictions upon transfers. We do not currently expect to register the Original Notes under the Securities Act. To the extent that Original Notes are tendered and accepted in the Exchange Offer, the trading market for Original Notes could be adversely affected. See “The Exchange Offer—Consequences of Failure to Exchange.”

Risks Relating to Our Company

Our ability to service our indebtedness depends on our receipt of funds from our subsidiaries. Restrictions on their ability to loan or distribute funds to us could adversely affect our ability to service our indebtedness.

We are organized as a holding company, with all of our net sales generated through our subsidiaries. Consequently, our operating cash flow and ability to service indebtedness depend in part upon the operating cash flow of our subsidiaries, including our foreign subsidiaries, and the payment of funds by them to us in the form of loans, dividends or otherwise. Their ability to pay dividends and make loans, advances and other payments to us depends upon any statutory or other contractual restrictions that apply, which may include requirements to maintain minimum levels of working capital and other assets.

A significant portion of our revenue is generated from foreign activities; changes in exchange rates and other changes in foreign economies could have an adverse effect on our business.

We have significant operations outside the United States. Approximately 22% of our net sales and 6% of our operating cash flow for 2002 were from foreign subsidiaries. We are therefore subject to risks affecting our

13

international operations, including relevant foreign currency exchange rates, which can affect the cost of our products or the ability to sell our products in foreign markets, and the value in U.S. dollars of sales made in foreign currencies. Our net sales were increased by $2.9 million in 2002 and reduced by $10.1 million in 2001 by the impact of currency fluctuations. Other factors include our ability to obtain effective hedges against fluctuations in currency exchange rates; foreign trade, monetary and fiscal policies; laws, regulations and other activities of foreign governments, agencies, and similar organizations; risks associated with having major manufacturing facilities located in countries that have historically been less stable than the United States in several respects, including fiscal and political stability; and risks associated with an economic downturn in other countries.

In addition, world events can increase the volatility of the currency markets, and such volatility could affect our financial results. In particular, the September 11, 2001 attacks in New York and Washington, D.C. disrupted commerce throughout the United States and other parts of the world. The continued threat of similar attacks throughout the world and military action taken and to be taken by the United States and other nations in Iraq and elsewhere, as well as the threat of military confrontation on the Korean peninsula, may cause significant disruption to commerce throughout the world. In addition, severe acute respiratory syndrome (SARS) has caused disruption in commerce in East Asia and may cause significant disruption to commerce throughout the world. To the extent that such disruptions further slow the global economy or, more particularly, result in delays or cancellation of purchase orders, our business and results of operations could be materially and adversely affected. We are unable to predict whether the threat of new epidemics or attacks or the responses thereto will result in any long-term commercial disruptions or if such activities or responses will have a long-term material adverse effect on our business, results of operations, or financial condition.

The operating and financial restrictions imposed by our debt agreements, including our revolving credit facility and the indenture relating to the notes, limit our ability to finance operations and capital needs and engage in other business activities.

Our debt agreements contain covenants that restrict our ability to:

| | • | incur additional indebtedness (including guarantees); |

| | • | pay dividends and make other restricted payments; |

| | • | issue some types of preferred stock; |

| | • | enter into sale and leaseback transactions; |

| | • | make loans and investments; |

| | • | enter into new lines of business; |

| | • | enter into some leases; and |

| | • | engage in some transactions with affiliates. |

In addition, our credit facilities require us to comply with specified financial covenants including minimum interest coverage ratios, maximum leverage ratios, and minimum net worth requirements.

Our ability to meet these covenants and requirements in the future may be affected by events beyond our control, including prevailing economic, financial, and industry conditions. Our breach or failure to comply with any of these covenants could result in a default under our credit facilities or the indenture governing the notes. If we default under our credit facilities, the lenders could cease to make further extensions of credit, cause all of our

14

outstanding balances under these credit facilities to become due and payable, require us to apply all of our available cash to repay the indebtedness under these credit facilities, prevent us from making debt service payments on any other indebtedness we owe and/or proceed against the collateral granted to them to secure repayment of those amounts. If a default under the indenture occurs, the holders of the notes could elect to declare the notes immediately due and payable. If the indebtedness under our credit facilities or the notes is accelerated, we may not have sufficient assets to repay amounts due under these existing debt agreements or on other debt securities then outstanding. We also may amend the provisions and limitations of our credit facilities from time to time in a manner that could adversely affect you, as a holder of the notes, without your consent. See “Description of Other Indebtedness” and “Description of Notes.”

Our failure to keep pace with the technological demands of our customers or with the products and services offered by our competitors could significantly harm our business.

Some of the industries we serve are characterized by rapid technological changes and new product introductions. Some of our competitors may invest more heavily in research or product development than we do. Successful new product offerings depend upon a number of factors, including our ability to:

| | • | accurately anticipate customer needs; |

| | • | innovate and develop new technologies and applications; |

| | • | successfully commercialize new products in a timely manner; |

| | • | price our products competitively and manufacture and deliver our products in sufficient volumes and on time; and |

| | • | differentiate our offerings from those of our competitors. |

If we do not introduce new products in a timely manner and make enhancements to meet the changing needs of our customers, some of our products could become obsolete over time, in which case our customer relationships, revenue, and operating results would suffer.

Our operating results may suffer if the industries into which we sell our products are in downward cycles.

Some of the industries and markets into which we sell our products are cyclical. Any further downturn in our customers’ markets or in general economic conditions could result in reduced demand for our products and could harm our business.

Acquisitions have been an important part of our growth strategy; failure to successfully integrate acquisitions could adversely impact our results.

A significant portion of our growth over the past several years has been achieved through our acquisition program. Although we intend to reduce our emphasis on acquisitions, our ability to grow our business through acquisitions is subject to various factors including the cost of capital, the availability of suitable acquisition candidates at reasonable prices, competition for appropriate acquisition candidates, our ability to realize the synergies expected to result from acquisitions, our ability to retain key personnel in connection with acquisitions, and the ability of our existing personnel to efficiently handle increased transitional responsibilities resulting from acquisitions.

We may incur restructuring or impairment charges that would reduce our earnings.

We have in the past and may in the future restructure some of our operations. In such circumstances, we may take actions that would result in a charge and reduce our earnings, including as a result of our inability to dispose of discontinued operations or risks associated with discontinued operations. These restructurings have or may be undertaken to realign our subsidiaries, eliminate duplicative functions, rationalize our operating facilities

15

and products, and reduce our staff. These restructurings may be implemented to improve the operations of recently acquired subsidiaries as well as subsidiaries that have been part of our operations for many years. For a discussion of our recent restructuring activities, see “Business—Restructuring.” Additionally, on October 1, 2001 we adopted Statement of Financial Accounting Standards (SFAS) No. 142, “Goodwill and Other Intangible Assets,” which requires that goodwill and intangible assets that have an indefinite useful life be tested at least annually for impairment. We carry a very significant amount of goodwill and intangible assets and SFAS No. 142 requires us to perform an annual assessment for possible impairment.

We rely heavily upon sales to key distributors and original equipment manufacturers, and could lose sales if any of them stop doing business with us.

Our three most significant distributors represent a significant portion of our revenues. For example, sales to Fisher Scientific, VWR, and Allegiance Corporation accounted for approximately 14%, 11%, and 7% of revenues in fiscal 2002, respectively. Our reliance on major independent distributors for a substantial portion of our sales subjects our sales performance to volatility in demand from distributors. We can experience volatility when distributors merge or consolidate, when inventories are not managed to end-user demand, or when distributors experience softness in their sales. We rely primarily upon the long-standing and mutually beneficial nature of our relationships with our key distributors, rather than on contractual rights, to protect these relationships. Volatility in end-user demand can also arise with large OEM and private label customers to whom we sell directly, particularly when our customers fail to manage inventories to end-user demand, discontinue product lines, or switch business to other manufacturers. Sales to our OEM customers are sometimes unpredictable and wide variances sometimes occur quarter to quarter.

We rely heavily on manufacturing operations to produce the products we sell, and we could be injured by disruptions of our manufacturing operations.

We rely upon our manufacturing operations to produce most of the products we sell. Any significant disruption of those operations for any reason, such as strikes, labor disputes, or other labor unrest, power interruptions, fire, war, or other force majuere, could adversely affect our sales and customer relationships and therefore adversely affect our business. In particular, nearly all of the white glass used in our Clinical Group’s worldwide manufacturing operations is produced in our glass manufacturing facility in Switzerland. Disruption in this supply can result from delays encountered in connection with the periodic rebuilding of the sheet glass furnace or furnace malfunctions. Although most of our raw materials are available from a number of potential suppliers, our operations also depend upon our ability to obtain raw materials at reasonable prices.

The success of many of our products depends on the effectiveness of our patents, trademarks, and licenses to defend our intellectual property rights. If we fail to adequately defend our intellectual property rights, competitors may produce and market products similar to ours.

Our success with many of our products depends, in part, on our ability to protect our current and future innovative products and to defend our intellectual property rights. Our subsidiaries’ products are sold under a variety of trademarks and trade names. They own or license all of the trademarks and trade names we believe to be material to the operation of their businesses. We also rely upon a combination of non-disclosure and other contractual agreements and trade secret, copyright, patent, and trademark laws to protect our intellectual property rights. Disputes may arise concerning the ownership of intellectual property or the applicability of confidentiality agreements. If we fail to adequately protect our intellectual property, competitors may manufacture and market products similar to ours.

We are subject to risk of product liability and other litigation which could adversely affect our business.

We are subject to the risks of claims involving our products (including those of businesses we no longer own) and other legal and administrative proceedings, including the expense of investigating, litigating, and

16

settling any claims. Although we currently maintain insurance against some of these risks, uninsured losses, which may be material, could occur.

Our business is subject to regulatory risks, and changes in regulation could adversely affect our business.

Our ability to continue manufacturing and selling those of our products that are subject to regulation by the United States Food and Drug Administration or other domestic or foreign governments or agencies is subject to a number of risks. In the future, some of our products may be affected by the passage of stricter laws or regulations, reclassification of our products into categories subject to more stringent requirements, or the withdrawal of approvals needed to sell one or more of our products. Additionally, violations of any environmental, health and safety laws or regulations, or the release of toxic or hazardous materials used in our operations into the environment could expose us to significant liability. Similarly, third party lawsuits relating to environmental and workplace safety issues could result in substantial liability.

Demand for and pricing of some of our products are affected by general levels of insurance and reimbursement and changes in the levels of insurance or reimbursement could affect the demand for such products or the prices we are able to charge.

The demand for and pricing of some of our products can be affected by changing levels of public and private health care budgets, including reimbursement by private or governmental insurance programs.

We could be harmed by the loss of key management.

The success of our operations depends in significant part upon the experience and expertise of our management team, both within Apogent and in our operating subsidiaries. Any loss of these key personnel could harm our business.

Our separation from Sybron Dental Specialties poses a potential tax sharing and indemnification risk.

In December 2000, we spun off our dental businesses which are now owned by Sybron Dental Specialties. We and Sybron Dental Specialties each agreed to indemnify the other with respect to certain indebtedness, liabilities, and obligations, including potential tax liabilities if future transactions change the tax treatment of the spin-off. Our ability to collect on these indemnities from Sybron Dental Specialties, if applicable, depends upon the future financial strength of Sybron Dental Specialties.

Our business is subject to quarterly variations in operating results due to factors outside of our control.

Our business is subject to quarterly variation in operating results caused by a number of factors, including business and industry conditions, timing of acquisitions, distribution and OEM customer issues, and other factors listed here. All these factors make it difficult to predict operating results for any particular period.

Risks Relating to the Notes

Our substantial indebtedness could adversely affect our financial health and prevent us from fulfilling our obligations under these notes.

We have now and, after the offering, will continue to have a significant amount of indebtedness. On March 31, 2003, after giving pro forma effect to the sale of the Original Notes and the recapitalization, we would have had total indebtedness of $923.7 million (of which $250.0 million would have consisted of the notes and the balance would have consisted of senior debt).

17

Our substantial indebtedness could have important consequences to you. For example, it could:

| | • | make it more difficult for us to satisfy our obligations with respect to these notes; |

| | • | increase our vulnerability to general adverse economic and industry conditions; |

| | • | reduce the availability of our cash flow to fund working capital, capital expenditures, research and development efforts, program investment efforts and other general corporate needs; |

| | • | limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

| | • | place us at a competitive disadvantage compared to our competitors with less debt; |

| | • | expose us to the risk of increased interest rates because some of our debt bears interest at variable rates; and |

| | • | limit our ability to borrow additional funds. |

Any default under the agreements governing our indebtedness, including a default under our revolving credit facility that is not waived by the required lenders, and the remedies sought by the holders of such indebtedness could make us unable to pay principal, premium, if any, and interest on the notes and substantially decrease the market value of the notes.

Despite current indebtedness levels, we and our subsidiaries may still be able to incur substantially more debt. This could further exacerbate the risks associated with our substantial leverage.

We and our subsidiaries may be able to incur substantial additional indebtedness in the future. The terms of the indenture do not fully prohibit us or our subsidiaries from doing so. Assuming we had completed the recapitalization on March 31, 2003, our revolving credit facility would have permitted additional borrowings of up to $470.8 million after the sale of the Original Notes and all of those borrowings would rank senior to the notes. If new debt is added to our and our subsidiaries’ current debt levels, the related risks that we and they now face would increase.

To service our indebtedness, we will require a significant amount of cash. Our ability to generate cash depends on many factors beyond our control.

Our ability to make payments on and to refinance our indebtedness, including the notes, and to fund planned capital expenditures, program investment efforts, and research and development efforts will depend on our ability to generate cash in the future. This, to a certain extent, is subject to general economic, financial, competitive, legislative, regulatory, and other factors that are beyond our control.

Based on our current level of operations, we believe our cash flow from operations, available cash and available borrowings under our revolving credit facility will be adequate to meet our liquidity needs for the foreseeable future.