Index

PART I

(Dollars in thousands)

Forward-Looking Statements

Certain matters contained in this report, including the information contained under the heading “Fiscal 2014 Outlook,” constitute forward-looking statements that are based on certain assumptions and involve certain risks and uncertainties. These include the following, without limitation: assumptions, risks and uncertainties associated with the Company’s future performance, the Company’s development and introduction of new technologies in general; the ability to protect and utilize the Company’s intellectual property; continued customer acceptance of the InLight technology; the adaptability of optically stimulated luminescence (“OSL”) technology to new platforms and formats; military and other government funding for the purchase of certain of the Company’s equipment and services; the impact on sales and pricing of certain customer group purchasing arrangements; changes in spending or reimbursement for medical products or services; the costs associated with the Company’s research and business development efforts; the usefulness of older technologies and related licenses and intellectual property; the effectiveness of and costs associated with the Company’s IT platform enhancements; the anticipated results of operations of the Company and its subsidiaries or ventures; valuation of the Company’s long-lived assets or business units relative to future cash flows; changes in pricing of services and products; changes in postal and delivery practices; the Company’s business plans; anticipated revenue and cost growth; the ability to integrate the operations of acquired businesses and to realize the expected benefits of acquisitions; the risks associated with conducting business internationally; costs incurred for potential acquisitions or similar transactions; other anticipated financial events; the effects of changing economic and competitive conditions, including instability in capital markets which could impact availability of short and long-term financing; the timing and extent of changes in interest rates; the level of borrowings; foreign exchange rates; government regulations; accreditation requirements; changes in the trading market that affect the costs of obligations under the Company’s benefit plans; and pending accounting pronouncements. These assumptions may not materialize to the extent assumed, and risks and uncertainties may cause actual results to be different from what is anticipated today. These risks and uncertainties also may result in changes to the Company’s business plans and prospects, and could create the need from time to time to write down the value of assets or otherwise cause the Company to incur unanticipated expenses. Additional information may be obtained by reviewing the information set forth in Item 1A “Risk Factors” and Item 7A “Quantitative and Qualitative Disclosures about Market Risk” and information contained in the Company's reports filed, from time to time, with the SEC. The Company does not undertake, and expressly disclaims, any duty to update any forward-looking statement whether as a result of new information, future events or changes in the Company’s expectations, except as required by law.

Item 1. Business

General Description

Landauer, Inc. is a Delaware corporation organized on December 22, 1987. As used herein, the “Company”, “we”, “our”, “us” or “Landauer” refers to Landauer, Inc. and its subsidiaries. The Company’s shares are listed on the New York Stock Exchange under the symbol LDR.

Landauer is a leading global provider of technical and analytical services to determine occupational and environmental radiation exposure, the leading domestic provider of outsourced medical physics services, and a provider of radiology related medical products. Since November 2011, the Company has operated in three primary business segments, Radiation Measurement, Medical Physics and Medical Products. Radiation Measurement has been the core business for over 50 years. The Company has provided complete radiation dosimetry services to hospitals, medical and dental offices, universities, national laboratories, nuclear facilities and other industries in which radiation poses a potential threat to employees. Landauer’s services include the manufacture of various types of radiation detection monitors, the distribution and collection of the monitors to and from customers, and the analysis and reporting of exposure findings. These services are provided to approximately 1.8 million individuals globally. In addition to providing analytical services, the Company may lease or sell dosimetry detectors and reading equipment to large customers that want to manage their own dosimetry programs, or into smaller international markets in which it is not economical to establish a direct service.

The majority of the Radiation Measurement revenues are realized from radiation measurement services and other services incidental to radiation dose measurement. The Company enters into agreements with customers to provide them with radiation measurement services, generally for a twelve-month period. Such agreements generally have a high renewal rate, resulting in customer relationships that are generally stable and recurring. As part of its services, the Company provides to its customers radiation detection badges, which are produced and owned by the Company. The badges are worn for a period selected by the customers (“wear period”), which is usually one, two, or three months in duration. At the end of the wear period, the badges are returned to the Company for analysis. The Company analyzes the badges that have been worn and provides its customers with a report indicating their radiation exposures. The Company recycles certain badge components for reuse, while also producing replacement badges on a continual basis.

The Company offers its service for measuring the dosages of x-ray, gamma radiation and other penetrating ionizing radiations to which the wearer has been exposed, primarily through badges, which contain OSL material, which are worn by customer personnel. This technology is marketed under the trade names Luxel+® and InLight®.

A key component of the Company’s dosimetry system is OSL crystal material. Radiation Measurement operates a crystal manufacturing facility in Stillwater, Oklahoma that it acquired in August 1998. The Company’s base OSL material is manufactured utilizing a proprietary process to create aluminum oxide crystals in a unique structure that is able to retain charged electrons following the crystal’s exposure to radiation.

Radiation Measurement’s InLight dosimetry system provides in-house and commercial laboratories with the ability to provide in-house radiation measurement services using OSL technology. InLight services may involve a customer acquiring or leasing dosimetry devices as well as analytical reading equipment from the Company. The system is based on the Company’s proprietary technology and instruments, and dosimetry devices developed in Japan. The InLight system allows customers the flexibility to tailor their precise dosimetry needs.

Radiation Measurement’s RadWatch-RadLight system provides the military and first responder user with a portable, field-ready option for tactical radiation monitoring using OSL technology. RadWatch-RadLight is offered through a partnership agreement with Yamasato, Fujiwara, Higa & Associates, Inc. (“YFH”) doing business as Aquila. RadWatch-RadLight solution fulfills a recognized gap for acquiring a legal dose of record for radiation emergency response teams.

Other radiation measurement-related services (“ancillary services”) augment the basic radiation measurement services that the Company offers, providing administrative and informational tools to customers for the management of their radiation safety programs.

In November 2009 Landauer completed the acquisition of Gammadata Mätteknik AB (“GDM”), a Swedish provider of radon measurement services. GDM is based near Stockholm, Sweden and provides measurement services throughout the Scandinavian region and Europe. In October 2009, Landauer acquired a dosimetry service in Sweden, now called Landauer Persondosimetri AB (“PDM”). As of November 2011, GDM and PDM are now known as Landauer Nordic AB. In December 2010, the Company established an unconsolidated joint venture in Turkey, which provides radiation measurement services. In August 2012 the Company invested $11.8 million for a 49% minority interest in YFH, doing business as Aquila, a small business supplier to the International Atomic Energy Agency as well as the U.S. Military. The Company provides dosimetry parts to Aquila for their military contract.

Medical physics services are provided through the Company’s Landauer Medical Physics (“LMP”) division. In November 2009, Landauer completed its first LMP acquisition by acquiring Global Physics Solutions, Inc. (“GPS”). With primary offices in Illinois and upstate New York, LMP has operations throughout the United States (“U.S”). The Company uses LMP as a platform to expand into the medical physics services market, serving domestic hospitals, radiation therapy centers and imaging centers. LMP is the leading nationwide service provider of clinical physics support, equipment commissioning and accreditation support and imaging equipment testing. Clinical physics support is provided by medical physicists, who individually focus on either imaging or therapeutic medical physics. Imaging physicists are concerned primarily with the radiation delivered by imaging equipment, image quality and compliance with safe practices in nuclear pharmacies. Therapeutic physicists are concerned with the safe delivery of radiation in cancer treatment. Therapeutic physicists contribute to the development of therapeutic

techniques, collaborate with radiation oncologists to design treatment plans, and monitor equipment and procedures to ensure that cancer patients receive the prescribed dose of radiation to the correct location. Both specialties are aligned with critical treatment trends in the continued increased utilization of radiation for the diagnosis and treatment of disease. The ability to target treatments and reduce the impact of surgical procedures is often aided by imaging and therapeutic techniques. In June 2010, Landauer, through its Medical Physics segment, completed the acquisition of the assets of Upstate Medical Physics (“UMP”), a provider of imaging physics services in upstate New York. In addition, four smaller regional practices were also acquired in fiscal 2011 and 2012 to augment the LMP operations. The Company reports the operating results of LMP in the Medical Physics reporting segment.

In November 2011, Landauer completed the acquisition of IZI Medical Products, LLC (“IZI”), which is headquartered in Maryland. The Company completed the acquisition of IZI as a platform to expand into the radiation oncology, radiology, and image guided surgery end markets as its Medical Products segment. IZI is a leading domestic provider of high quality medical consumable accessories used in radiology, radiation therapy, and image guided surgery procedures. IZI’s customer base includes buyers at several stages along the supply chain including distributors, manufacturers of image guided navigation equipment, and product end users such as community hospitals, radiation oncology clinics, mammography clinics, and imaging centers. IZI’s medical accessories range from consumables used with MRI, CT, and mammography technologies to highly engineered passive reflective markers used during image guided surgery procedures. In alignment with treatment trends which increasingly utilize radiation for the diagnosis and treatment of disease, as well as growing demand for minimally invasive procedures, IZI products provide the ability to increase procedural accuracy while decreasing procedural time.

Landauer believes that its business is largely dependent upon the Company’s technical competence, the quality, reliability and price of its services and products, and its prompt and responsive service.

A summary of selected financial data for Landauer for the last five fiscal years is set forth in Item 6 of Part II of this Annual Report on Form 10-K. Financial information about geographic areas and segments is provided in the Notes to Consolidated Financial Statements in Item 8 of Part II of this Annual Report on Form 10-K.

Marketing and Sales

Landauer’s radiation measurement services and products are marketed in the U.S. and Canada primarily by full-time Company personnel located in five sales regions with support from telesales representatives. The Company’s non-U.S. and Canada radiation measurement services and products are marketed through its wholly owned subsidiaries operating in the United Kingdom, France and Sweden as well as its ventures in Japan and Turkey and its consolidated subsidiaries in Brazil, Australia, Mexico and China. Other firms and individuals market the Company’s radiation measurement products and services on a distributorship or commission basis, generally to small customers or in geographic regions in which the Company does not have a direct presence.

Worldwide, the Company’s Radiation Measurement segment serves approximately 73,000 customers representing approximately 1.8 million individuals annually. The customer base is diverse and fragmented with no single customer representing greater than 2% of revenue. Typically, a customer will contract on a subscription basis for one year of service in advance, representing monthly, bimonthly, quarterly, semi-annual or annual badges, readings and reports. Customer relationships in the radiation measurement market are generally stable and recurring. Details of the Company’s revenue recognition and deferred contract revenue policy are set forth in the “Critical Accounting Policies” section of Item 7 of this Annual Report on Form 10-K.

The Company’s U.S. and Canada radiation measurement services are largely based on the Luxel+ dosimeter system in which all analyses are performed at the Company’s laboratories in Glenwood, Illinois. Luxel+ employs the Company’s proprietary OSL technology. The Company’s InLight dosimetry system enables certain customers to make their own measurements using OSL technology.

For most radiation dosimetry laboratories operating around the world, the laboratory must maintain accreditation with a regulatory body to provide the user with a formal record of dose – a process that is expensive and time consuming. By combining the implementation of an InLight system in the laboratory and “dose of record” determination by Landauer or a Landauer affiliated and accredited facility, the user can provide its workers with the periodic radiation safety management infrastructure without the need to maintain its own accreditation. Additionally,

dosimetry management software options provide the ability to measure the incremental radiation dose of workers at regular intervals over long periods of time.

InLight also forms the basis for Landauer’s operations in Europe, Asia, and Latin America and other future operations that might occur where local requirements preclude using a U.S. or other foreign-based laboratory.

Medical physics outsourced services are marketed to hospitals and free-standing cancer centers or free-standing imaging centers across the United States. LMP medical physicists partner with other healthcare professionals to deliver services to address evolving technology, safety and regulatory needs, with the objective of improving patient outcomes through safe and effective use of radiation in medicine. The services are marketed to radiation oncology and imaging customers by a team of business development professionals supported by LMP’s senior leadership and physicists.

In November 2011, the Company acquired 100% of IZI, which became the Company’s Medical Products segment. IZI products are marketed to buyers at several stages along the supply chain including distributors, manufacturers of image guided navigation equipment, and product end users such as community hospitals, radiation oncology clinics, mammography clinics, and imaging centers. IZI's products are marketed in the U.S. and Canada primarily by full-time Company telesales representatives located in IZI’s Maryland facility. Outside of the U.S. and Canada, the Company primarily utilizes the companies that manufacture image-guided navigation equipment to market and distribute the navigation products. IZI uses distributors to sell its radiology and radiation therapy products.

Seasonality

The services provided by the Company to its radiation measurement customers are on-going and are of a subscription nature. As such, revenues are recognized in the periods in which such services are rendered, irrespective of whether invoiced in advance or in arrears. Given the subscription nature of Radiation Measurement services, quarterly revenues are fairly consistent.

There is no identifiable seasonality to the Company’s Medical Physics or Medical Products segments as their services and products are utilized in radiographic, radiation therapy and surgical procedures that are performed throughout the year.

International Activities

Information regarding the Company’s activities by geographic region is contained under the footnote “Geographic Information” in Item 8 of this Annual Report on Form 10-K.

Patents

The Company holds exclusive worldwide licenses to patent rights for certain technologies that measure and image radiation exposure to crystalline materials when stimulated with light. These licenses were acquired by the Company from Battelle Memorial Institute (“Battelle”) and Oklahoma State University (“OSU”) as part of collaborative efforts to develop and commercialize a new generation of radiation dosimetry technology. The underlying patents for these licenses expire in years 2014 through 2023. The Battelle patents address specific OSL materials and basic aspects of use. The OSU patents are specific to the stimulation process, imaging and data interpretation. As of September 30, 2013, the Company is using OSL technology to provide dosimetry services to the majority of its domestic and international customers. Landauer from time to time evaluates the continued need and benefits to licensing certain patent rights and may discontinue such licenses in instances where Landauer does not believe that such licenses remain necessary.

Additionally, the Company holds certain patents, generated from the Company’s research and development activities, that relate to various dosimeter designs, radiation measurement materials and methods, optical data storage techniques using aluminum oxide and marking technologies used in radiology, radiation therapy and image-guided procedures. These patents expire between 2017 and 2033.

Rights to inventions of employees working for the Company are assigned to the Company.

Raw Materials

The Company has multiple sources for most of its raw materials and supplies, and believes that the number of sources and availability of these items are adequate. Landauer internally produces certain of its requirements, such as OSL detector materials and plastic badge holders. All crystal materials used in the Company’s OSL technology are produced at the Company’s crystal manufacturing facility in Stillwater, Oklahoma. The InLight dosimetry system and its components are manufactured by a Japanese company under an exclusive agreement. The Company sources the Radwatch-RadLight analytical instrument sold for military and emergency radiological response applications from YFH on a sole source basis. IZI sources a key component of its medical products from a sole supplier. If the Company were to lose availability of its Stillwater facility or materials from the Japanese company or IZI’s sole supplier due to a fire, natural disaster or other disruptions, such loss could have a material adverse effect on the Company and its operations.

Competition

In the U.S., the Company competes against a number of dosimetry service providers. One of these providers is a division of Mirion Technologies, a significant competitor with substantial resources. Other competitors in the U.S. that provide dosimetry services tend to be smaller companies, some of which operate on a regional basis. Most government agencies in the U.S., such as the Department of Energy and Department of Defense, have their own in-house radiation measurement services, as do many large private nuclear power plants. Outside of the U.S., radiation measurement activities are conducted by a combination of private entities and government agencies.

The Company competes on the basis of advanced technologies, competent execution of these technologies, the quality, reliability and price of its services, and its prompt and responsive performance. The Company’s InLight dosimetry system competes with other dosimetry systems based on the technical advantages of OSL methods combined with an integrated systems approach featuring comprehensive software, automation and value.

Medical physics outsourced services represents a large fragmented market where LMP has many small competitors. In addition, many facilities directly employ full-time physicists as an alternative for obtaining services from an outsourced provider. LMP competes with other outsourced medical physicists by having responsive regional practices that are backed by the safety, stability and standards of a global company. LMP offers a complementary alternative for clients who require support for their full-time staff in meeting patient care needs.

The Medical Products segment generally competes against a limited number of smaller companies. Two of its primary competitors are a division of Roper Industries, Inc., and Medtronics, each of which is a significant competitor with substantial resources.

Research and Development

The Company’s technological expertise has been an important factor in its growth. The Company regularly pursues product improvements to maintain its technical position. The development of OSL dosimetry, announced in 1994, was funded by the Company in its collaborative effort with Battelle and OSU. The Company commercialized this technology beginning in 1998 and has converted most of its customers to the technology. Current research efforts seek to expand the use of OSL, particularly as it applies to radiation measurements in therapeutic and imaging radiology and nuclear medicine as well as to environmental radiation dosimetry. In addition, the Company is evaluating new badge and InLight reader configurations that have military application and is designing a badge that will support global standardization.

The Company also participates regularly in several technical professional societies, both domestic and international, that are active in the fields of health physics and radiation detection and measurement.

IZI has a robust product development process, which focuses on identifying products that will increase the accuracy of procedures and reduce procedural time. Current research efforts are concentrated to radiology products, which reduce radiation exposure to physicians and patients, as well as products that increase the accuracy of imaging by using reference markers.

Over the last three years the company has spent $4.1 million, $4.0 million, and $2.4 million in research and development activities for the fiscal years 2013, 2012 and 2011, respectively.

Regulatory Matters

Domestic Regulations

The Company manufactures and markets products that are medical devices subject to regulation by the U.S. Food and Drug Administration (“FDA”), as well as other regulatory bodies. FDA regulations govern the following activities that the Company performs and will continue to perform: product design and development; document and purchasing controls; production and process controls; acceptance controls; product testing; product manufacturing; product safety; product labeling; product storage; recordkeeping; complaint handling; pre-market clearance; advertising and promotion; and product sales and distribution.

FDA pre-market clearance and approval requirements. Unless an exemption applies, each medical device the Company wishes to commercially distribute in the U.S. will require either prior 510(k) clearance or pre-market approval from the FDA. The FDA classifies medical devices into one of three classes. Devices deemed to pose lower risks are placed in either class I or II, which requires the manufacturer to submit to the FDA a pre-market notification to commercially distribute the device. This process is generally known as 510(k) clearance. Some low- risk devices are exempted from this requirement. Devices deemed by the FDA to pose the greatest risks, such as life-sustaining, life-supporting or implantable devices, or devices deemed not substantially equivalent to a previously cleared 510(k) device, are placed in class III and require pre-market approval. All of the Company’s current products are either class I or class II devices.

Pervasive and continuing regulation. After a device is placed on the market, numerous regulatory requirements apply. These include, but are not limited to:

· | Quality System Regulation, or QSR, which require manufacturers, including third-party manufacturers, to follow stringent design, testing, documentation and other quality assurance procedures during product design and throughout the manufacturing process; |

· | Labeling regulations and FDA prohibitions against the promotion of products for uncleared, unapproved or off-label uses and against making false and misleading claims; and |

· | Medical device reporting regulations, which require that manufacturers report to the FDA if their device may have caused or contributed to a death or serious injury or malfunctioned in a way that would likely cause or contribute to a death or serious injury if the malfunction were to recur. |

The FDA has broad post-market and regulatory enforcement powers. The Company is subject to unannounced inspections by the FDA to determine its compliance with the QSR and other regulations. The Company’s subcontractors also may be subject to FDA inspection.

For additional information regarding FDA regulations that impact the Company, please see the following risk factors set forth in Item 1A “Risk Factors” of this annual report:

· | “The Company’s medical device business is subject to many laws and government regulations governing the manufacture and sale of medical devices, including the FDA’s 510(k) clearance process.” |

· | “The FDA may change its policies, adopt additional regulations, or revise existing regulations, in particular relating to the 510(k) clearance process.” |

· | “The Company’s medical device business is subject to unannounced inspections by the FDA to determine our compliance with FDA requirements.” |

Environmental Regulations

The Company believes that it complies with federal, state and local provisions that have been enacted or adopted regulating the discharge of materials into the environment or otherwise protecting the environment. This compliance has not had, nor is it expected to have, a material effect on the capital expenditures, financial condition, liquidity, results of operations, or competitive position of the Company.

Other Governmental Regulations

Many of the Company’s technology-based services must comply with various national and international standards that are used by regulatory and accreditation bodies for approving such services and products. These accreditation bodies include, for example, the National Voluntary Laboratory Accreditation Program in the U.S. and governmental agencies, generally, in international markets. Changes in these standards and accreditation requirements can result in the Company having to incur costs to adapt its offerings and procedures. Such adaptations may introduce quality assurance issues during transition that need to be addressed to ensure timely and accurate analyses and data reporting. Additionally, changes affecting radiation protection practices, including new understandings of the hazards of radiation exposure and amended regulations, may impact how the Company’s services are used by its customers and may, in some circumstances, cause the Company to alter its products and delivery of its services. Finally, other healthcare regulatory and reimbursement factors may impact the Company. For additional information regarding healthcare and reimbursement laws and policies that may impact the Company, please see the following risk factors set forth in Item 1A “Risk Factors” of this annual report:

· | “The current U.S. and state health reform legislative initiatives could adversely affect our operations and business condition.” |

· | “The applicable healthcare fraud and abuse laws and regulations, along with the increased enforcement environment, may lead to an enforcement action targeting the Company, which could adversely affect our business.” |

Employees and Labor Relations

As of September 30, 2013, the Company employed approximately 650 full-time employees worldwide, of which 132 employees and 34 employees were in the Company’s Medical Physics and Medical Products segments, respectively. The Company believes that it generally maintains good relations with employees at all locations.

Available Information

The Company annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 may be accessed free of charge through Landauer’s website as soon as reasonably practicable after Landauer has electronically filed such material with, or furnished it to, the Securities and Exchange Commission. The address of Landauer’s website is http://www.landauer.com. A copy of any of these reports is available free of charge upon the written request from any shareholder. Requests should be submitted to the following address: Landauer, Inc., Attention: Corporate Secretary, 2 Science Road, Glenwood, Illinois 60425.

Pursuant to Section 303A.12(a), Landauer, Inc. has complied with the New York Stock Exchange requirement to provide an annual CEO certification no later than 30 days following the Company’s annual meeting.

Item 1A. Risk Factors

In addition to factors discussed elsewhere in this Annual Report on Form 10-K, set forth below are certain risks and uncertainties that could adversely affect the Company’s results of operations or financial condition and cause actual results or events to differ materially from those expressed in any forward-looking statements made by or on behalf of the Company.

We rely on a single facility for the primary manufacturing and processing of our dosimetry services and products, and a single facility for the manufacturing and processing of our medical devices.

The Company conducts its primary dosimetry manufacturing and laboratory processing operations and performs significant functions for some of its international operations from a single facility in Glenwood, Illinois. The Company’s IZI subsidiary conducts its medical device manufacturing and operations from a single facility in Baltimore, Maryland. If the Company were to lose availability of either of these primary facilities due to fire, natural disaster or other disruptions, the Company’s operations could be significantly impaired. Despite the Company’s business continuity preparedness efforts, there can be no assurance that such plan could ensure the Company’s ability to rapidly respond to such disaster. Although the Company maintains business interruption insurance, there can be no assurance that the proceeds of such insurance would be sufficient to offset any loss the Company might incur or that the Company would be able to retain its customer base if operations were so disrupted.

Increased IT security threats and more sophisticated and targeted computer crime could pose a risk to our systems, networks, products, solutions and services.

Increased global IT security threats and more sophisticated and targeted computer crime pose a risk to the security of our systems and networks and the confidentiality, availability and integrity of our data. While we attempt to mitigate these risks by employing a number of measures, including employee training; comprehensive monitoring of our networks and systems; and maintenance of backup and protective systems, our systems, networks, products, solutions and services remain potentially vulnerable to advanced persistent threats. Depending on their nature and scope, such threats could potentially lead to the compromising of confidential information; improper use of our systems and networks; manipulation and destruction of data; defective products; production downtimes; and operational disruptions, which in turn could adversely affect our reputation, competitiveness, and operating results.

We rely on a single source for the manufacturing of crystal material, a key component in our OSL technology, a single vendor for the manufacturing of InLight products and a single vendor for a key component of our medical devices.

Crystal material is a key component in Landauer’s OSL technology. The Company operates a single crystal manufacturing facility in Stillwater, Oklahoma that currently supplies all OSL crystal radiation measurement material used by the Company. Although multiple sources for raw crystal material exist, there can be no assurance that the Company could secure another source to produce finished crystal materials to Landauer’s specification in the event of a disruption at the Stillwater facility. The InLight dosimetry system and its components are manufactured by Panasonic Communications Company (“Panasonic”) under an exclusive agreement. IZI sources a key component of its medical accessories from a sole supplier. If the Company were to lose availability of its Stillwater facility or materials from Panasonic or IZI’s sole supplier due to a fire, natural disaster or other disruptions, such loss could have a material adverse effect on the Company and its operations.

If we are not successful in the development or introduction of new technologies, our financial condition and results of operations could be materially and adversely affected.

The Company’s radiation measurement business is a mature business and the number of workers being monitored for radiation exposure has not grown in recent years. Additionally, economic pressures can adversely affect the value of occupational measurement perceived by customers or increase pricing pressures. The Company believes that the development and introduction of new technologies and products will be essential to help counter these pressures. The Company regularly pursues product improvements to maintain its technical position. The development and introduction of new technologies, the adaptability of OSL to new platforms and new formats, the usefulness of older technologies and the introduction of new technologies by the competition present various risks to the Company’s business. The failure or lack of market acceptance of a new technology or the inability to respond to market requirements for new technology could adversely affect the Company’s operations or reputation with customers. The cancellation of technology projects or the cessation of use of an existing technology could result in write-downs and charges to the Company’s earnings.

As a medical device accessory provider, introducing new products is critical to growing the Company’s business. If the Company does not manage its new product development projects on time or experiences unforeseen

problems, the launch of those products would be put at risk which could have a negative effect on IZI’s revenue opportunity and the Company’s results of operations. The failure or lack of market acceptance of a new product or the inability to respond to market requirements for new technology could adversely affect the Company’s operations and reputation with customers.

We may fail to adequately protect our customer data.

We may fail to adequately protect our customer data. In the normal course of operations, we collect and maintain confidential data from our customers. Our failure to adequately preserve the security of this data, whether due to technological failures or errors in or deviations from our data maintenance policies and procedures, could result in data loss or corruption. If we fail to adequately maintain and protect our customer data, we could be exposed to potential litigation from our customers and could face risk for loss or breach of customer data under state privacy laws. Additionally, our reputation could be harmed, and we could lose existing and have difficulty attracting new customers, all of which could adversely affect our operating results.

If we are unable to successfully execute business development activities and diversification such as the acquisition and integration of strategic businesses, our on-going business and results of operations may be adversely affected.

A principal growth strategy of the Company is to explore opportunities to selectively enhance its business through development activities, such as strategic acquisitions, investments and alliances. In furtherance of this objective, in November 2009, the Company acquired GPS and Landauer Nordic AB. In November 2011, the Compnay acquired IZI. In August 2012 the Company acquired a 49% minority interest in YFH, doing business as Aquila, a small business supplier to the International Atomic Energy Agency as well as the U.S. Military. The Company may not be able to identify appropriate acquisition candidates or successfully negotiate, finance or integrate acquisitions. Covenants in the Company’s revolving credit facility may also limit the amount and types of indebtedness that it may incur to finance acquisitions. If the Company is unable to make further acquisitions, it may be unable to realize its growth strategy. Additionally, if the Company is unable to successfully manage acquisition risks, future earnings may be adversely affected. Acquisitions and other business development activities involve various significant challenges and risks, including the following:

· | Difficulty in acquiring desired businesses or assets on economically acceptable terms; |

· | Difficulty in integrating new employees, business systems and technology; |

· | Difficulty in consolidating facilities and infrastructure; |

· | Potential need to operate and manage new lines of business; |

· | Potential loss of key personnel; |

· | Diversion of management’s attention from on-going operations; |

· | Realization of satisfactory returns on investments; and |

· | Disputes with strategic partners, due to conflicting priorities or conflicts of interest. |

Development activities could result in the incurrence of debt, contingent liabilities, interest and amortization expenses or periodic impairment charges related to goodwill and other intangible assets as well as significant charges related to integration costs. If the Company is unable to successfully integrate and manage businesses that it acquires within expected terms and in a timely manner, its business and results of operations could be adversely affected.

Unforeseen problems with the stabilization and maintenance of our equipment and information systems could interfere with our operations.

In the normal course of its business, the Company must record and process significant amounts of data quickly and accurately and relies on various computer and telecommunications equipment and information technology systems. Any failure of such equipment or systems could adversely affect the Company’s operations.

The Company has recently implemented a new enterprise resource planning solution to manage certain business operations of its’ Order to Cash, Procure to Pay, and Radiation Measurement - Reporting and Analysis business processes. The Company will continue to incur additional costs associated with stabilization and ongoing development of the new solution. As new applications and functionality are added in order to increase the efficiency of the Company workforce and business processes, unforeseen problems could arise. Such problems could adversely impact the Company’s operations, including the ability to perform the following in a timely manner: customer quotes, customer orders, product shipment, customer services and support, order billing and tracking, contractual obligations fulfillment and other related operations.

Certain of our operations are conducted through joint ventures in which we rely significantly on our joint venture partners.

A substantial portion of the Company’s operations are conducted through joint ventures with third parties. In Australia, Brazil, China, and Mexico, the Company has a controlling interest in the related joint ventures. The Company has a 50% interest in Nagase-Landauer, Ltd. located in Japan and Epsilon-Landauer located in Turkey as well as a 49% interest in YFH. In all of these joint ventures and others, the Company relies significantly on the services and skills of its joint venture partners to manage and conduct the local operations and ensure compliance with local laws and regulations. If the joint venture partners were unable to perform these functions adequately, the Company’s operations in such regions could be adversely affected.

There can be no assurances that our operations will generate cash flows in an amount sufficient to enable us to pay our indebtedness.

The Company’s ability to make scheduled payments on its existing or future debt obligations and fund operations will depend on its future financial and operating performance. While the Company believes it will continue to have sufficient cash flows to operate its businesses, there can be no assurances that its operations will generate sufficient cash flows to enable it to pay its remaining indebtedness or to fund its other liquidity needs. If the Company cannot make scheduled payments on its debt, the Company will be in default and, as a result, among other things, all outstanding principal and interest under its revolving credit facility will automatically be due and payable which could force the Company to liquidate certain assets or substantially restructure or alter its business operations or debt obligations. Moreover, if the Company is unable to obtain additional capital or if its current sources of financing are reduced or unavailable, the Company may be required to eliminate or reduce the scope of its plans for expansion and growth and this could affect its overall operations.

If we experience decreasing prices for our goods and services and we are unable to reduce our expenses, our results of operations could suffer.

The Company may experience decreasing prices for the goods and services it offers due to customer consolidation, increased influence of hospital group purchasing organizations, and pricing pressure experienced by its customers from managed care organizations, the Medicare and Medicaid programs and other third-party payers. Decreasing prices may also be due to increased market power of its customers as the medical industry consolidates and increased competition among dosimetry and physics services providers. If the prices for its goods and services decrease and it is unable to reduce its expenses, the Company’s results of operations could be adversely affected.

The Company may also experience decreasing prices for the products offered by its medical device business due to potential changes in the reimbursement levels of hospitals and other customers. The customers and the other entities with which the Company has a business relationship are affected by changes in statutes, regulations and limitations in governmental spending for Medicare, Medicaid and other programs. Recent government actions and future legislative and administrative changes could limit government spending for the Medicare and Medicaid programs, limit payments to hospitals and other providers, increase emphasis on competition, consolidation, or integrated delivery systems, impose price controls, initiate new and expanded value-based reimbursement programs and/or create other programs that potentially could have an adverse effect on the Company’s customers and the other entities with which it has a business relationship. If the Company’s pricing experiences significant downward pressure, its business will be less profitable and its results of operations could be adversely affected.

We may be subject to future impairment losses due to potential declines in the fair value of our assets.

As a result of acquisitions and capital expenditures, the Company has goodwill, intangible assets and fixed assets on our balance sheets. The Company tests goodwill, intangible assets and fixed assets for impairment on a periodic basis as required and whenever events or changes in circumstances indicate that the carrying value may not be recoverable. The events or changes that could require the Company to test our goodwill, intangible assets and fixed assets for impairment include a reduction in the Company’s stock price and market capitalization, changes in estimated future cash flows, changes in rates of growth in the Company’s industry or in any of the Company’s reporting units.

The potential for goodwill impairment is increased during a period of economic uncertainty. To the extent the Company acquires a company at a negotiated price based on anticipated future performance, subsequent market conditions may result in the acquired business performing at a lower level than was anticipated at the time of the acquisition. Any of these charges would reduce our operating results and could cause the price of our common stock to decline. A slowing recovery in the U.S., a prolonged recovery or second recession in Europe, and slowing growth in the global economy may result in declining performance that would require the Company to examine goodwill for potential additional impairment.

The Company will continue to evaluate the carrying value of the remaining goodwill, intangible assets and fixed assets, and if they determine in the future that there is a potential further impairment, the Company may be required to record additional losses, which could materially and adversely affect operating results.

Restrictions in our revolving credit facility could adversely affect our business, financial condition, and results of operations.

The Company has a committed $175.0 million, secured revolving credit facility syndicated with a group of commercial banks that expires on August 2, 2018.

The facility also contains certain financial covenants, but no net worth covenant. The maximum leverage ratio covenant is a range of 3.50 to 1.00 for the period of September 30, 2013 through June 30, 2015, and to a maximum 3.25 to 1.00 for the periods September 30, 2015 and thereafter. The minimum fixed charge coverage ratio covenant is a range of 1.10 to 1.00 for the period of September 30, 2013 through June 30, 2015, and to a minimum 1.15 to 1.00 for the periods September 30, 2015 and thereafter. Interest rate equal to LIBOR plus a margin of between 1.25% and 2.50% and for the base rate a margin of between 0.25% and 1.50%.

If the Company has significant borrowings under the facility and it violates a covenant or an event of default occurs and the lenders accelerate the maturity of any outstanding borrowings and terminate their commitment to make future loans, it could have a material adverse effect on the Company’s business, results of operations and financial condition. There can be no assurance that the Company will be able to comply with its financial or other covenants or that any covenant violations will be waived. In addition, if the Company fails to comply with its financial or other covenants, it may need additional financing in order to service or extinguish its indebtedness. In the future, the Company may not be able to obtain financing or refinancing on terms acceptable to it, if at all.

Our radiation-measurement and technology-based services business is subject to extensive domestic and foreign government regulations, which could increase our costs, cause us to incur liabilities and adversely affect our results of operations.

Regulation, present and future, is a constant factor affecting the Company’s business. The radiation measurement industry is subject to federal, state and international governmental regulation. Unknown matters, new laws and regulations, or stricter interpretations of existing laws or regulations may materially affect the Company’s business or operations in the future and/or could increase the cost of compliance. The equipment commissioning business of LMP, which the Company first acquired in November 2009, and the employment of physicists and other healthcare professionals also are subject to federal, state and international governmental regulation and licensing requirements.

Many of the Company’s technology-based services must comply with various domestic and international standards that are used by regulatory and accreditation bodies for approving such services and products. The failure of the Company to obtain accreditation for its services and products may adversely affect the Company’s business, require the Company to alter its products or procedures or adversely affect the market perception of the effectiveness of its services and products. Changes in these standards and accreditation requirements may also result in the Company having to incur substantial costs to adapt its offerings and procedures to maintain accreditations and approvals. Such adaptations may introduce quality assurance issues during transition that need to be addressed to ensure timely and accurate analyses and data reporting. Additionally, changes affecting radiation protection practices, including new understandings of the hazards of radiation exposure and amended regulations, may impact how the Company’s services are used by its customers and may, in some circumstances, cause the Company to alter its products and delivery of its services.

The Company’s medical device business is subject to many laws and government regulations governing the manufacture and sale of medical devices, including the FDA’s 510(k) clearance process.

IZI’s products are medical devices that are subject to extensive regulation in the U.S. by the federal government, including by the FDA. The FDA regulates virtually all aspects of a medical device’s design, development, testing, manufacturing, labeling, storage, record keeping, adverse event reporting, sale, promotion, distribution and shipping. The Company must report to the FDA when evidence suggests that one of its devices may have caused or contributed to death or serious injury or has malfunctioned and the device or a similar device would be likely to cause or contribute to death or serious injury if the malfunction were to recur. If such adverse event occurred, the Company could incur substantial expense and harm to its reputation and the Company’s business and results of operations could be adversely affected.

Before a new medical device can be marketed in the U.S., it must first receive either premarket approval or 510(k) clearance from the FDA, unless an exemption exists. The same rule applies when a manufacturer plans to market a medical device for a new use. The process can be costly and time-consuming. The FDA is expected to respond to a section 510(k) notification in 90 days, but often takes much longer. The premarket approval process usually takes six months to three years, but may take longer. The Company cannot assure that any new medical devices or new use for an existing medical device that IZI develops will be cleared or approved in a timely or cost-effective manner, if cleared or approved at all. Even if such devices are cleared or approved, the products may not be cleared or approved for all indications. Because medical devices may only be marketed for cleared or approved indications, this could significantly limit the market for that product and may adversely affect the Company’s results of operations.

Currently, all IZI medical devices have been cleared through the 510(k) clearance process or are exempt from this requirement. Any modification to a 510(k) device that could significantly affect its safety or efficacy, or that would constitute a significant change in its intended use, will require a new clearance process. Any modification to an exempt device could potentially subject the exempt device to the 510(k) clearance requirements. The FDA requires device manufacturers to make their own determination regarding whether a modification requires a new clearance; however, the FDA can review and invalidate a manufacturer’s decision not to file for a new clearance. The Company cannot guarantee that the FDA will agree with its decisions not to seek clearances for particular device modifications or that it will be successful in obtaining 510(k) clearances for modifications. Any such additional clearance processes with the FDA could delay the Company’s ability to market a modified product and may adversely affect the Company’s results of operations.

The FDA may change its policies, adopt additional regulations, or revise existing regulations, in particular relating to the 510(k) clearance process.

The FDA also may change its policies, adopt additional regulations, or revise existing regulations, each of which could prevent or delay premarket approval or 510(k) clearance of a device, or could impact the Company’s ability to market its currently cleared devices. The Company anticipates significant changes in the near future that will affect the way the 510(k) clearance program will operate. On August 3, 2010, the FDA released for public comment two internal working group reports with numerous recommendations to improve the 510(k) process and utilize science in regulatory decision making to encourage innovation yet maintain predictability of the clearance

process. In July, 2011, the Institute of Medicine, which was asked by the FDA to evaluate and make recommendations on the 510(k) program, released its report entitled “Medical Devices and the Public’s Health, The FDA 510(k) Clearance Process.” The report contained numerous and broad recommendations that, if followed, will have a significant impact on the medical device industry. Also in July, 2011, the FDA issued a draft guidance titled “510(k) Device Modifications: Deciding When to Submit a 510(k) for a Change to an Existing Device.” This draft guidance document was withdrawn on July 17, 2012 in accordance with Section 510(n)(2)(B) of the Federal Food, Drug, and Cosmetic Act as amended by Food and Drug Administration Safety and Innovation Act. An existing 1997 guidance on the same topic therefore remains in effect, but any future reforms could require the Company to file new 510(k)s and could increase the total number of 510(k)s to be filed. The Company cannot predict what effect these reforms will have on its ability to obtain 510(k) clearances in a timely manner. The Company also cannot predict the nature of other regulatory reforms and their resulting effects on its business.

The Company’s medical device business is subject to unannounced inspections by the FDA to determine our compliance with FDA requirements.

FDA inspections can result in inspectional observations on FDA’s Form-483, warning letters or other forms of more significant enforcement action. More specifically, if FDA concludes that the Company is not in compliance with applicable laws or regulations, or that any of IZI’s medical devices are ineffective or pose an unreasonable health risk, the FDA could:

· | require the Company to notify health professionals and others that its devices present unreasonable risk of substantial harm to public health; |

· | order the Company to recall, repair, replace or refund the cost of any medical device that it manufactured or distributed; |

· | detain, seize or ban adulterated or misbranded medical devices; |

· | refuse to provide the Company with documents necessary to export its products; |

· | refuse requests for 510(k) clearance or premarket approval of new products or new intended uses; |

· | withdraw 510(k) clearances or premarket approvals that are already granted; |

· | impose operating restrictions, including requiring a partial or total shutdown of production; |

· | enjoin or restrain conduct resulting in violations of applicable law pertaining to medical devices; and/or |

· | assess criminal or civil penalties against the Company’s officers, employees or the Company. |

If the FDA concludes that the Company failed to comply with any regulatory requirement during an inspection, it could have a material adverse effect on its business and financial condition. The Company could incur substantial expense and harm to its reputation and its ability to introduce new or enhanced products in a timely manner could be adversely affected.

The current United States and state health reform legislative initiatives could adversely affect our operations and business condition.

In both the U.S. and some foreign jurisdictions, there have been a number of legislative and regulatory proposals to change the health care system in ways that might affect the Company’s business. In March 2010, President Obama signed into law the Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act, or collectively, the Health Care Reform Law, a sweeping law intended to broaden access to health insurance, reduce or constrain the growth of healthcare spending, enhance remedies against fraud and abuse, add new transparency requirements for healthcare and health insurance industries, impose new taxes and fees on the health industry and impose additional health policy reforms. This legislation includes reforms and reductions that could affect Medicare reimbursements and health insurance coverage for certain services and treatments. Effective January 1, 2013, The Health Reform Law also imposed a 2.3% excise tax on the sale of certain medical devices by manufacturers or importers in the U.S. The Health Reform Law continues to be implemented, including with the new American Health Benefit Insurance Exchanges and their qualified health plans, which are scheduled to begin coverage on January 1, 2014. Some states also have pending health reform legislative initiatives. Further, the Joint Select Committee on Deficit Reduction, which was created by the Budget Control Act of 2011, concluded its work in November 2011, and issued a statement that it was not able to make a bipartisan agreement, thus triggering the sequestration process. The sequestration process combined with past and

potential future government shutdowns have resulted and may result in spending reductions and have and could result in reduced Medicare, Medicaid and other Federal health care reimbursements for the Company’s services and products. Changes in reimbursements and coverages, including risk-sharing arrangements and quality-based reimbursement initiatives, could adversely affect hospitals and other medical services and products providers, which could result in reduced demand for certain services and products offered by the Company, including services offered by its Medical Physics business and products manufactured by its Medical Products business. The Company will not know the full effects of the Health Care Reform Law until applicable federal and state agencies issue regulations or guidance under the new law. The Company cannot predict whether or when future healthcare reform initiatives at the Federal or state level or other initiatives affecting its business will be proposed, enacted or implemented or what impact those initiatives may have on its business, financial condition or results of operations. The Company’s customers and the other entities with which it has a business relationship could react to these initiatives and the uncertainty surrounding these proposals by curtailing or deferring investments, including those for the Company’s services and products.

The applicable healthcare fraud and abuse laws and regulations, along with the increased enforcement environment, may lead to an enforcement action targeting the Company, which could adversely affect our business.

The medical device business recently acquired by the Company is subject to healthcare fraud and abuse laws and regulations including, but not limited to, the Federal Anti-Kickback Statute, state anti-kickback statutes, the Federal False Claims Act, and state false claims acts. Additionally, to the extent the Company maintains financial relationships with physicians and other healthcare providers, the Company may be subject to Federal and state physician payment sunshine laws and regulations, which require the Company to track and disclose these financial relationships. These and other laws regulate interactions amongst health care entities and with sources of referrals of business, among other things. The Federal Anti-Kickback Statute is a criminal statute that imposes substantial penalties on persons or entities that offer, solicit, pay or receive payments in return for referrals, recommendations, purchases or orders of items or services that are reimbursable by Federal healthcare programs. The False Claims Act imposes liability on any person or entity that submits or causes to be submitted a claim to the Federal government that he or she knows (or should know) is false. The Health Reform Law further provides that a claim submitted for items or services, the provision of which resulted from a violation of the Anti-Kickback Statute, is “false” under the False Claims Act and certain other false claims statutes.

The Company may be subject to liability under these laws based on the activities of its recently acquired medical device company for its conduct prior to acquisition and may also be subject to liability for any future conduct that is deemed by the government or the courts to violate these laws. Additionally, over the past ten years, partially as the result of the passage of the Health Insurance Portability and Accountability Act of 1996 and of the Health Reform Law, the government has pursued an increasing number of enforcement actions. This increased enforcement environment may increase scrutiny of the Company, directly or indirectly, and could increase the likelihood of an enforcement action targeting the Company. The Company’s Medical Products segment has entered into complex distribution and collaboration agreements, as well as purchase agreements with a number of its customers, including parties that bill Federal healthcare programs for the Company’s products, which may be subject to government scrutiny. Finally, to the extent that any of the agreements are breached or terminated, the Company’s medical device business may experience a decrease in sales, and accordingly, revenue. In addition, to the extent that its customers, many of whom are providers, may be affected by this increased enforcement environment, the Company’s business could correspondingly be affected. It is possible that a review of the Company’s business practices or those of its customers by courts or government authorities could result in a determination with an adverse effect on its business. The Company cannot predict the effect of possible future enforcement actions on the Company.

Changes in, or interpretations of, tax rules and regulations may adversely affect our effective tax rates.

The Company is subject to income and other taxes in the U.S. and several foreign jurisdictions. Significant judgment is required in evaluating our provision for income taxes. During the ordinary course of business, there are many transactions for which the ultimate tax determination is uncertain. For example, there could be changes in the valuation of our deferred tax assets and liabilities; or changes in the relevant tax, accounting, and other laws, regulations, principles and interpretations. The Company is subject to audits in various jurisdictions, and such

jurisdictions may assess additional tax against us. Although the Company believes our tax estimates are reasonable, the final determination of tax audits and any related litigation could be materially different from our historical income tax provisions and accruals. The results of an audit or litigation, or the effects of a change in tax policy in the U.S. or international jurisdictions where we do business, could have a material effect on our operating results in the period or periods for which that determination is made.

As a portion of our business is conducted outside of the United States, adverse international developments could negatively impact our business and results of operations.

The Company conducts business in numerous international markets such as Australia, Brazil, Canada, China, France, Japan, Mexico, Sweden, Turkey and the United Kingdom. Foreign operations are subject to a number of special risks, including, among others, currency exchange rate fluctuations; disruption in relations; political and economic unrest; trade barriers; exchange controls; expropriation; and changes in laws and policies, including those governing foreign owned operations.

Fluctuations in currency exchange rates could adversely affect our results.

The Company is exposed to market risk, including changes in foreign currency exchange rates. The financial statements of the Company’s non-U.S. subsidiaries are remeasured into U.S. dollars using the U.S. dollar as the reporting currency. To date, the market risk associated with foreign currency exchange rates has not been material in relation to the Company’s financial position, results of operations or cash flows. These risks could increase, however, as the Company expands in international markets.

Several of our current and potential competitors have significantly greater resources and increased competition could impair sales of our products.

The Company competes on the basis of advanced technologies, competent execution of these technologies, the quality, reliability and price of its services and its prompt and responsive performance. In much of the world, radiation measurement activities are conducted by a combination of private entities and governmental agencies. The Company’s primary radiation measurement and medical physics competitor in the U.S., Global Dosimetry Solutions, a division of Mirion Technologies, is large, has substantial resources, and has been particularly active in recent years in soliciting business from the Company’s customers. IZI generally competes against a limited number of smaller companies. Two of its primary competitors are a division of Roper Industries, Inc., and Medtronics, each of which is a significant competitor with substantial resources.

Our failure to attract, motivate and retain qualified and key personnel to support our business may have a material adverse effect on our business plans, prospects, results of operations and financial condition.

The Company’s success depends, in large part, upon the talent and efforts of key individuals including highly skilled scientists, physicists and engineers, as well as experienced senior management, sales, marketing and finance personnel. Competition for these individuals is intense and there can be no assurance that the Company will be successful in attracting, motivating, or retaining key personnel. The loss of the services of one or more of these senior executives or key employees, or the inability to continue to attract these personnel may have a material effect on its business plans, prospects, results of operations and financial condition. The Company’s continued ability to compete effectively depends on its ability to attract new skilled employees and to retain and motivate its existing employees.

The Medical Physics business involves the delivery of professional services and is highly labor-intensive. Its success depends largely on its general ability to attract, develop, motivate and retain highly skilled licensed medical physicists (“physicists”). Further, the Company must successfully maintain the right mix of physicists with relevant experience and skill sets as the Company continues to grow, as it expands into new service offerings, and as the market evolves. The loss of a significant number of its physicists, the inability to attract, hire, develop, train and retain additional skilled personnel, or not maintaining the right mix of professionals could have a serious negative effect on the Company, including its ability to manage, staff and successfully complete its existing engagements and

obtain new engagements. Qualified physicists are in great demand, and the Company faces significant competition for both senior and junior physicists with the requisite credentials and experience. The Company’s principal competition for talent comes from other outsourced medical physicist firms, hospitals and free-standing radiation therapy centers. Many of these competitors may be able to offer significantly greater compensation and benefits or more attractive lifestyle choices, career paths or geographic locations than those of the Company. Therefore, the Company may not be successful in attracting and retaining the skilled physicists it requires to conduct and expand its operations successfully. Increasing competition for these revenue-generating medical physicists may also significantly increase the Company’s labor costs, which could negatively affect its margins and results of operations.

We could be subject to professional liability lawsuits, some of which we may not be fully insured against or reserved for, which could adversely affect our financial condition and results of operations.

In recent years, physicians, hospitals and other participants in the healthcare industry have become subject to an increasing number of lawsuits alleging medical malpractice and related legal theories such as negligent hiring, supervision and credentialing, and vicarious liability for acts of their employees or independent contractors. In addition, the level and effect of radiation being administered by certain radiation equipment is also attracting increased scrutiny and giving rise to patient safety claims. Many of these lawsuits involve large claims and substantial defense costs. As the Company increases its presence in the healthcare industry, through the Medical Physics business, it could be exposed to litigation or subject to fines, penalties or suspension of services relating to the compliance with regulatory requirements.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

The Company owns three adjacent buildings totaling approximately 59,000 square feet in Glenwood, Illinois, about 30 miles south of Chicago, leases a 24,000 square foot warehouse and leases 6,100 square feet of office space in Chicago. The properties house the Company’s administrative offices, information technology resources, and laboratory, assembly and reading operations. The properties and equipment of the Company are in good condition and, in the opinion of management, are suitable and adequate for the Company’s operations. For its Radiation Measurement operations, the Company leases a crystal growth facility in Stillwater, Oklahoma and maintains laboratories in Australia, Brazil, China, France, Mexico, Sweden, and Turkey, as well as a sales office in England. The Company’s joint venture in Japan, Nagase-Landauer, owns a manufacturing facility which began operating in April 2010. The Company leases offices in New York, North Carolina and Missouri for its Medical Physics operations, and leases manufacturing and office space in Maryland for its Medical Products operations.

Item 3. Legal Proceedings

The Company is a party, from time to time, to various legal proceedings, lawsuits and other claims arising in the ordinary course of its business. The Company does not believe that any such litigation pending as of September 30, 2013, if adversely determined, would have a material effect on its business, financial position, results of operations, or cash flows.

Item 4. Mine Safety Disclosures

Not Applicable

PART II

(Dollars in thousands, except per share data)

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities

The Company’s common stock is traded on the New York Stock Exchange under the trading symbol LDR. The following table indicates the reported high and low market prices of the Company’s common stock and dividends paid per share for each quarterly period during the last two fiscal years:

| | | | | | | | | | |

| | | | | | | | | | |

Year | Quarter | | | High | | | Low | | | Dividends

Paid Per Share |

2013 | | | | | | | | | | |

| First | | $ | 63.85 | | $ | 54.48 | | $ | 0.55 |

| Second | | $ | 66.04 | | $ | 55.70 | | $ | 0.55 |

| Third | | $ | 57.35 | | $ | 48.21 | | $ | 0.55 |

| Fourth | | $ | 51.73 | | $ | 45.89 | | $ | 0.55 |

2012 | | | | | | | | | | |

| First | | $ | 53.40 | | $ | 45.69 | | $ | 0.55 |

| Second | | $ | 60.95 | | $ | 50.87 | | $ | 0.55 |

| Third | | $ | 57.74 | | $ | 47.56 | | $ | 0.55 |

| Fourth | | $ | 61.93 | | $ | 54.79 | | $ | 0.55 |

The Company expects to continue paying regular quarterly cash dividends, although there is no assurance as to future dividends because they depend on future earnings, capital requirements and financial condition. In December 2013, the Board of Directors declared a fiscal 2014 first quarter cash dividend of $0.55 per common share.

As of November 28, 2013, there were 273 shareholders of record.

Issuer Purchases of Equity Securities

| | | | | | | | |

| | | | | | | | |

Period | Total Number of Shares Purchased(a) | | | Average Price Paid Per Share | | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | | Maximum Number of Shares that May Yet be Purchased Under the Plans or Programs |

October 1 – October 31, 2012 | - | | $ | - | | - | | - |

November 1 – November 30, 2012 | 1,100 | | | 59 | | - | | - |

December 1 – December 31, 2012 | 9,715 | | | 58 | | - | | - |

Total for quarter ended December 31, 2012 | 10,815 | | $ | 58 | | - | | - |

January 1 – January 31, 2013 | - | | | - | | - | | - |

February 1 – February 29, 2013 | 88 | | | 59 | | - | | - |

March 1 – March 31, 2013 | - | | | - | | - | | - |

Total for quarter ended March 31, 2013 | 88 | | $ | 59 | | - | | - |

April 1 – April 30, 2013 | - | | | - | | - | | - |

May 1 – May 31, 2013 | - | | | - | | - | | - |

June 1 – June 30, 2013 | - | | | - | | - | | - |

Total for quarter ended June 30, 2013 | - | | $ | - | | - | | - |

July 1 – July 31, 2013 | 249 | | | 48 | | - | | - |

August 1 – August 31, 2013 | 410 | | | 47 | | - | | - |

September 1 – September 30, 2013 | 4,987 | | | 51 | | - | | - |

Total for quarter ended September 30, 2013 | 5,646 | | $ | 51 | | - | | - |

(a) | This column includes the deemed surrender of existing shares of the Company’s common stock to the Company by stock-based compensation plan participants to satisfy the exercise price or tax liability of employee stock awards at the time of exercise or vesting. These surrendered shares are not part of any publicly announced share repurchase program. |

The Company funds its share repurchases with cash on hand and cash generated from operations.

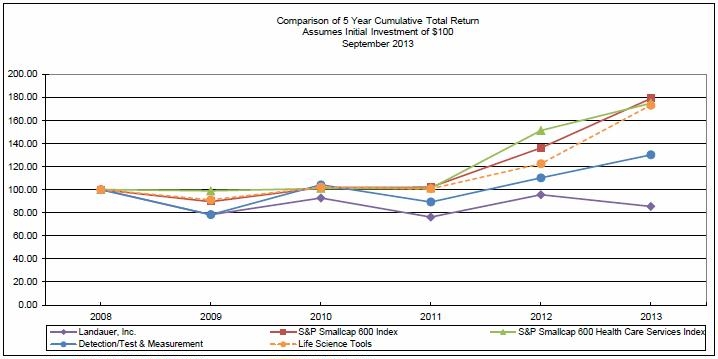

Performance Graph

The following graph reflects a comparison of the cumulative total return (change in stock price plus reinvested dividends) assuming $100 invested in: (a) Landauer’s common stock, (b) a group of detection/test and measurement companies composed of ticker symbols LDR, ES, OSIS, VAR, ASEI, (c) the S&P 600 industry index represented by a group of health care services companies, (d) a group of life science tool companies composed of ticker symbols LDR, QGEN, SIAL, BRKR, PKI, TMO, A, WAT, LIFE, FEIC and MTD and (e) the S&P 600 industry index represented by a group of health care services companies during the period from September 30, 2008 through September 30, 2013. The comparisons in the following table are historical and are not intended to forecast or be indicative of possible future performance of Landauer’s common stock.

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Value of Investment at September 30, |

(Dollars) | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

Landauer, Inc. | $ | 100 | $ | 78 | $ | 93 | $ | 76 | $ | 96 | $ | 85 |

Detection/Test and Measurement | | 100 | | 78 | | 104 | | 89 | | 110 | | 130 |

S&P Smallcap 600 Index | | 100 | | 90 | | 102 | | 102 | | 136 | | 179 |

Life Science Tools | | 100 | | 91 | | 102 | | 101 | | 122 | | 173 |

S&P Health Care Services | | 100 | | 99 | | 101 | | 101 | | 151 | | 175 |

Item 6. Selected Financial Data

Five Year Selected Financial Data

Landauer, Inc. and Subsidiaries

For the Years Ended September 30,

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

(Dollars in Thousands, Except per Share) | | 2013 | 2012 | 2011 | 2010 | 2009 |

Operating results | | | | | | | | | | | | | | | |

Net revenues | | $ | 150,200 | | $ | 152,400 | | $ | 120,458 | | $ | 114,367 | | $ | 93,827 |

Operating income(1) | | | 4,120 | | | 28,170 | | | 34,883 | | | 34,637 | | | 32,518 |

Net income attributable to Landauer, Inc. | | | 4,836 | | | 19,270 | | | 24,538 | | | 23,674 | | | 23,366 |

Basic net income per share | | $ | 0.50 | | $ | 2.04 | | $ | 2.60 | | $ | 2.53 | | $ | 2.51 |

Diluted net income per share | | $ | 0.49 | | $ | 2.03 | | $ | 2.58 | | $ | 2.52 | | $ | 2.49 |

Weighted average diluted shares outstanding | | | 9,482 | | | 9,437 | | | 9,477 | | | 9,349 | | | 9,366 |

Cash dividends per share | | $ | 2.20 | | $ | 2.20 | | $ | 2.20 | | $ | 2.15 | | $ | 2.10 |

Total assets | | $ | 276,833 | | $ | 302,125 | | $ | 168,656 | | $ | 150,696 | | $ | 125,205 |

Short-term debt | | $ | - | | $ | - | | $ | 19,805 | | $ | 12,504 | | $ | - |

Long-term debt | | $ | 142,785 | | $ | 141,347 | | $ | - | | $ | - | | $ | - |

(1)In fiscal 2013 results are impacted by goodwill impairment of $22,700.

Non-GAAP Financial Measures