Exhibit 13

Orrstown Financial Services, Inc.

2006 Annual Financial Report

CONTENTS

| | |

| | | Page |

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | 1 |

| |

| MANAGEMENT’S REPORT ON INTERNAL CONTROL | | 3 |

| |

| CONSOLIDATED FINANCIAL STATEMENTS | | |

| |

Balance sheets | | 4 |

Statements of income | | 5 |

Statements of changes in shareholders’ equity | | 6 |

Statements of cash flows | | 7 |

Notes to consolidated financial statements | | 8 - 27 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF CONSOLIDATED FINANCIAL CONDITION AND RESULTS OF OPERATIONS | | 28 - 38 |

| |

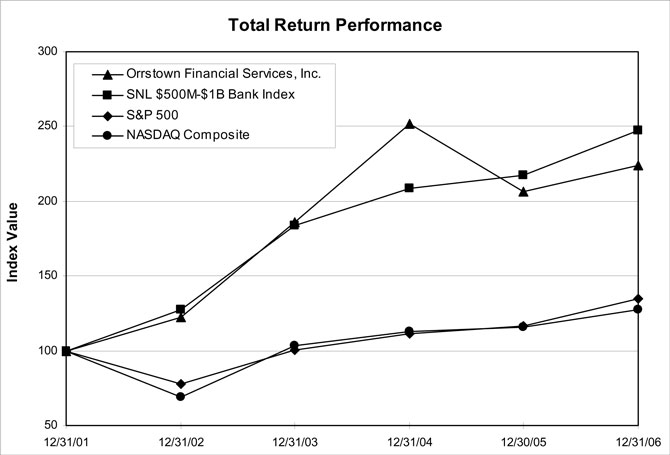

| PERFORMANCE GRAPH | | 39 |

| |

| SUMMARY OF QUARTERLY FINANCIAL DATA | | 40 |

| |

| SELECTED FIVE-YEAR FINANCIAL DATA | | 41 |

| |

| MARKET, DIVIDEND AND INVESTOR INFORMATION | | 42 |

Exhibit 13

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Shareholders of

Orrstown Financial Services, Inc.

We have audited the accompanying consolidated balance sheets of Orrstown Financial Services, Inc. and its wholly-owned subsidiaries as of December 31, 2006 and 2005, and the related statements of income, changes in shareholders’ equity, and cash flows for each of the years in the three-year period ended December 31, 2006. We also have audited management’s assessment, included in the accompanying Management’s Report on Internal Control, that Orrstown Financial Services, Inc. and its wholly-owned subsidiaries maintained effective internal control over financial reporting as of December 31, 2006, based on criteria established inInternal Control - Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). Orrstown Financial Services, Inc. and its wholly-owned subsidiaries’ management is responsible for these financial statements, for maintaining effective internal control over financial reporting, and for its assessment of the effectiveness of internal control over financial reporting. Our responsibility is to express an opinion on these financial statements, an opinion on management’s assessment, and an opinion on the effectiveness of the Corporation’s internal control over financial reporting based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement and whether effective internal control over financial reporting was maintained in all material respects. Our audit of financial statements included examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our audit of internal control over financial reporting included obtaining an understanding of internal control over financial reporting, evaluating management’s assessment, testing and evaluating the design and operating effectiveness of internal control, and performing such other procedures as we considered necessary in the circumstances. We believe that our audits provide a reasonable basis for our opinions.

A company’s internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company’s internal control over financial reporting includes those policies and procedures that (1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (3) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

- 1 -

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Orrstown Financial Services, Inc. and its wholly-owned subsidiaries as of December 31, 2006 and 2005, and the results of their operations and their cash flows for each of the years in the three-year period ended December 31, 2006 in conformity with accounting principles generally accepted in the United States of America. Also, in our opinion, management’s assessment that Orrstown Financial Services, Inc. and its wholly-owned subsidiaries maintained effective internal control over financial reporting as of December 31, 2006 is fairly stated, in all material respects, based on criteria established inInternal Control – Integrated Framework issued by COSO. Furthermore, in our opinion, Orrstown Financial Services, Inc. and its wholly-owned subsidiaries maintained, in all material respects, effective internal control over financial reporting as of December 31, 2006, based on criteria established inInternal Control – Integrated Frameworkissued by COSO.

As discussed in Note 1 to the Consolidated Financial Statements, the Corporation changed its policy for accounting for stock-based compensation in 2006.

|

|

| /S/SMITH ELLIOTT KEARNS & COMPANY, LLC |

| SMITH ELLIOTT KEARNS & COMPANY, LLC |

Chambersburg, Pennsylvania

March 12, 2007

- 2 -

MANAGEMENT’S REPORT ON INTERNAL CONTROL

To our shareholders,

Orrstown Financial Services, Inc.

Shippensburg, Pennsylvania

The management of Orrstown Financial Services, Inc. and its wholly-owned subsidiaries has the responsibility for establishing and maintaining an adequate internal control structure and procedures for financial reporting. Management maintains a comprehensive system of internal control to provide reasonable assurance of the proper authorization of transactions, the safeguarding of assets and the reliability of the financial records. The system of internal control provides for appropriate division of responsibility and is documented by written policies and procedures that are communicated to employees. Orrstown Financial Services, Inc. and its wholly-owned subsidiaries maintains an internal auditing program, under the supervision of the Audit Committee of the Board of Directors, which independently assesses the effectiveness of the system of internal control and recommends possible improvements.

Under the supervision and with the participation of the Corporation’s management, including its Chief Executive Officer and Chief Financial Officer, the Corporation has evaluated the effectiveness of its internal control over financial reporting as of December 31, 2006, using theInternal Control – Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission. Based upon this evaluation, the Chief Executive Officer and the Chief Financial Officer have concluded that the Corporation’s disclosure controls and procedures are adequate and effective to ensure that material information relating to the Corporation and its consolidated subsidiaries is made known to them by others within those entities. The Chief Executive Officer and the Chief Financial Officer believe that at December 31, 2006, Orrstown Financial Services, Inc. and its wholly-owned subsidiaries maintained an effective system of internal control over financial reporting.

The accounting firm Smith Elliott Kearns & Company, LLC has issued an attestation report on management’s assessment of the Corporation’s internal control over financial reporting. The accounting firm’s attestation report is included in this financial report.

| | | | |

/s/ Kenneth R. Shoemaker | | | | /s/ Bradley S. Everly |

| Kenneth R. Shoemaker | | | | Bradley S. Everly |

| President and Chief Executive Officer | | | | Senior Vice President and Chief Financial Officer |

| | |

| March 12, 2007 | | | | |

- 3 -

CONSOLIDATED BALANCE SHEETS

ORRSTOWN FINANCIAL SERVICES, INC. AND ITS WHOLLY-OWNED SUBSIDIARIES

| | | | | | | | |

| | | At December 31, | |

(Dollars in thousands) | | 2006 | | | 2005 | |

Assets | | | | | | | | |

Cash and due from banks | | $ | 20,730 | | | $ | 11,901 | |

Federal funds sold | | | 18,404 | | | | 23,430 | |

| | | | | | | | |

Cash and cash equivalents | | | 39,134 | | | | 35,331 | |

| | | | | | | | |

| | |

Interest bearing deposits with banks | | | 895 | | | | 3,445 | |

Securities available for sale | | | 87,543 | | | | 69,008 | |

Federal Home Loan Bank, Federal Reserve and Atlantic Central Bankers Bank stock, at cost which approximates market value | | | 3,850 | | | | 2,669 | |

| | |

Loans | | | | | | | | |

Commercial, financial and agricultural | | | 59,593 | | | | 50,104 | |

Real estate—Mortgages | | | 503,362 | | | | 373,410 | |

Real estate—Construction and land development | | | 46,947 | | | | 30,532 | |

Consumer | | | 8,925 | | | | 6,340 | |

| | | | | | | | |

| | | 618,827 | | | | 460,386 | |

Less: Allowance for loan losses | | | (5,520 | ) | | | (4,428 | ) |

| | | | | | | | |

Net Loans | | | 613,307 | | | | 455,958 | |

| | | | | | | | |

| | |

Premises and equipment, net | | | 19,852 | | | | 13,636 | |

Cash surrender value of life insurance | | | 15,573 | | | | 7,787 | |

Goodwill and intangible assets | | | 21,567 | | | | 1,935 | |

Accrued interest receivable | | | 3,279 | | | | 2,169 | |

Other assets | | | 4,031 | | | | 9,522 | |

| | | | | | | | |

Total assets | | $ | 809,031 | | | $ | 601,460 | |

| | | | | | | | |

| | |

Liabilities and Shareholders’ Equity | | | | | | | | |

Deposits: | | | | | | | | |

Non-interest bearing | | $ | 85,420 | | | $ | 68,697 | |

Interest bearing | | | 553,299 | | | | 394,125 | |

| | | | | | | | |

Total deposits | | | 638,719 | | | | 462,822 | |

| | | | | | | | |

| | |

Short-term borrowings | | | 41,703 | | | | 36,138 | |

Long-term debt | | | 32,440 | | | | 40,306 | |

Accrued interest and other liabilities | | | 6,781 | | | | 4,884 | |

| | | | | | | | |

Total liabilities | | | 719,643 | | | | 544,150 | |

| | | | | | | | |

| | |

Common stock, no par value—$ .05205 stated value per share 50,000,000 shares authorized with 6,145,049 shares issued at December 31, 2006; 5,439,227 shares issued at December 31, 2005 | | | 320 | | | | 283 | |

Additional paid—in capital | | | 72,023 | | | | 46,876 | |

Retained earnings | | | 16,934 | | | | 9,964 | |

Accumulated other comprehensive income | | | 507 | | | | 187 | |

Treasury stock—common, at cost 10,717 shares in 2006; 23 shares in 2005 | | | (396 | ) | | | 0 | |

| | | | | | | | |

Total shareholders’ equity | | | 89,388 | | | | 57,310 | |

| | | | | | | | |

Total liabilities and shareholders’ equity | | $ | 809,031 | | | $ | 601,460 | |

| | | | | | | | |

The Notes to Consolidated Financial Statements are an integral part of these statements.

- 4 -

CONSOLIDATED STATEMENTS OF INCOME

ORRSTOWN FINANCIAL SERVICES, INC. AND ITS WHOLLY-OWNED SUBSIDIARIES

| | | | | | | | | | |

| | | Years Ended December 31, |

(Dollars in thousands) | | 2006 | | 2005 | | | 2004 |

Interest and dividend income | | | | | | | | | | |

Interest and fees on loans | | $ | 40,086 | | $ | 28,527 | | | $ | 22,231 |

Interest and dividends on investment securities | | | | | | | | | | |

U.S. Government and agency | | | 2,198 | | | 2,006 | | | | 2,083 |

Tax exempt | | | 1,266 | | | 1,139 | | | | 1,206 |

Other investment income | | | 1,238 | | | 743 | | | | 372 |

| | | | | | | | | | |

Total interest and dividend income | | | 44,788 | | | 32,415 | | | | 25,892 |

| | | | | | | | | | |

| | | |

Interest expense | | | | | | | | | | |

Interest on deposits | | | 14,189 | | | 7,291 | | | | 5,201 |

Interest on short-term borrowings | | | 1,833 | | | 796 | | | | 304 |

Interest on long-term debt | | | 1,349 | | | 1,450 | | | | 1,481 |

| | | | | | | | | | |

Total interest expense | | | 17,371 | | | 9,537 | | | | 6,986 |

| | | | | | | | | | |

| | | |

Net interest income | | | 27,417 | | | 22,878 | | | | 18,906 |

Provision for loan losses | | | 390 | | | 144 | | | | 210 |

| | | | | | | | | | |

Net interest income after provision for loan losses | | | 27,027 | | | 22,734 | | | | 18,696 |

| | | | | | | | | | |

| | | |

Other income | | | | | | | | | | |

Service charges on deposit accounts | | | 4,671 | | | 3,815 | | | | 3,066 |

Other service charges, commissions and fees | | | 1,921 | | | 1,760 | | | | 1,016 |

Trust department income | | | 2,325 | | | 2,174 | | | | 1,863 |

Brokerage income | | | 1,382 | | | 990 | | | | 608 |

Investment securities gains (losses) | | | 41 | | | (60 | ) | | | 88 |

Other income | | | 743 | | | 380 | | | | 328 |

| | | | | | | | | | |

Total other income | | | 11,083 | | | 9,059 | | | | 6,969 |

| | | | | | | | | | |

| | | |

Other expenses | | | | | | | | | | |

Salaries | | | 9,116 | | | 6,028 | | | | 5,117 |

Employee benefits | | | 3,899 | | | 3,229 | | | | 2,792 |

Occupancy and equipment | | | 3,357 | | | 2,673 | | | | 2,398 |

Other operating expenses | | | 5,256 | | | 5,467 | | | | 4,411 |

| | | | | | | | | | |

Total other expenses | | | 21,628 | | | 17,397 | | | | 14,718 |

| | | | | | | | | | |

Income before income tax | | | 16,482 | | | 14,396 | | | | 10,947 |

Income tax expense | | | 4,850 | | | 4,409 | | | | 3,177 |

| | | | | | | | | | |

Net income | | $ | 11,632 | | $ | 9,987 | | | $ | 7,770 |

| | | | | | | | | | |

| | | |

Earnings per share: | | | | | | | | | | |

Basic earnings per share | | $ | 1.97 | | $ | 1.85 | | | $ | 1.45 |

Diluted earnings per share | | $ | 1.89 | | $ | 1.77 | | | $ | 1.40 |

Dividends per share | | $ | 0.78 | | $ | 0.58 | | | $ | 0.48 |

The Notes to Consolidated Financial Statements are an integral part of these statements.

- 5 -

CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

ORRSTOWN FINANCIAL SERVICES, INC. AND ITS WHOLLY-OWNED SUBSIDIARIES

| | | | | | | | | | | | | | | | | | | | | | | |

| | | Years Ended December 31, 2006, 2005 and 2004 | |

(Dollars in thousands) | | Common

Stock | | Additional Paid-In

Capital | | | Retained

Earnings | | | Accumulated Other Comprehensive

Income | | | Treasury

Stock | | | Total Shareholders’

Equity | |

Balance, December 31, 2003 | | $ | 264 | | $ | 32,928 | | | $ | 8,509 | | | $ | 1,134 | | | $ | 0 | | | $ | 42,835 | |

| | | | | | |

Comprehensive income | | | | | | | | | | | | | | | | | | | | | | | |

Net income | | | 0 | | | 0 | | | | 7,770 | | | | 0 | | | | 0 | | | | 7,770 | |

Change in unrealized loss on investment securities available for sale, net of tax of $159 | | | 0 | | | 0 | | | | 0 | | | | (308 | ) | | | 0 | | | | (308 | ) |

| | | | | | | | | | | | | | | | | | | | | | | |

Total comprehensive income | | | | | | | | | | | | | | | | | | | | | | 7,462 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Cash dividends ($.48 per share) | | | 0 | | | 0 | | | | (2,556 | ) | | | 0 | | | | 0 | | | | (2,556 | ) |

Stock-based compensation plans: | | | | | | | | | | | | | | | | | | | | | | | |

Issuance of stock | | | 2 | | | 591 | | | | 0 | | | | 0 | | | | 0 | | | | 593 | |

Issuance of stock through dividend reinvestment plan | | | 1 | | | 915 | | | | 0 | | | | 0 | | | | 0 | | | | 916 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Balance, December 31, 2004 | | | 267 | | | 34,434 | | | | 13,723 | | | | 826 | | | | 0 | | | | 49,250 | |

| | | | | | |

Comprehensive income | | | | | | | | | | | | | | | | | | | | | | | |

Net income | | | 0 | | | 0 | | | | 9,987 | | | | 0 | | | | 0 | | | | 9,987 | |

Change in unrealized loss on investment securities available for sale, net of tax of $329 | | | 0 | | | 0 | | | | 0 | | | | (639 | ) | | | 0 | | | | (639 | ) |

| | | | | | | | | | | | | | | | | | | | | | | |

Total comprehensive income | | | | | | | | | | | | | | | | | | | | | | 9,348 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Cash dividends ($.58 per share) | | | 0 | | | 0 | | | | (3,157 | ) | | | 0 | | | | 0 | | | | (3,157 | ) |

Stock dividends issued | | | 13 | | | 10,557 | | | | (10,570 | ) | | | 0 | | | | 0 | | | | 0 | |

Cash paid in lieu of fractional stock dividends | | | 0 | | | 0 | | | | (19 | ) | | | 0 | | | | 0 | | | | (19 | ) |

Stock-based compensation plans: | | | | | | | | | | | | | | | | | | | | | | | |

Issuance of stock | | | 1 | | | 490 | | | | 0 | | | | 0 | | | | 0 | | | | 491 | |

Issuance of stock through dividend reinvestment plan | | | 2 | | | 1,395 | | | | 0 | | | | 0 | | | | 0 | | | | 1,397 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Balance, December 31, 2005 | | | 283 | | | 46,876 | | | | 9,964 | | | | 187 | | | | 0 | | | | 57,310 | |

| | | | | | |

Comprehensive income | | | | | | | | | | | | | | | | | | | | | | | |

Net income | | | 0 | | | 0 | | | | 11,632 | | | | 0 | | | | 0 | | | | 11,632 | |

Change in unrealized gain on investment securities available for sale, net of tax of $177 | | | 0 | | | 0 | | | | 0 | | | | 320 | | | | 0 | | | | 320 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Total comprehensive income | | | | | | | | | | | | | | | | | | | | | | 11,952 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Cash dividends ($.78 per share) | | | 0 | | | 0 | | | | (4,662 | ) | | | 0 | | | | 0 | | | | (4,662 | ) |

Acquisition of First National—common stock issued | | | 36 | | | 24,805 | | | | 0 | | | | 0 | | | | 0 | | | | 24,841 | |

Stock-based compensation plans: | | | | | | | | | | | | | | | | | | | | | | | |

Compensation expense | | | 0 | | | 224 | | | | 0 | | | | 0 | | | | 0 | | | | 224 | |

Issuance of stock | | | 1 | | | 147 | | | | 0 | | | | 0 | | | | 0 | | | | 148 | |

Purchase of treasury stock (14,749 shares) | | | 0 | | | 0 | | | | 0 | | | | 0 | | | | (543 | ) | | | (543 | ) |

Issuance of treasury stock (4,055 shares) | | | 0 | | | (29 | ) | | | 0 | | | | 0 | | | | 147 | | | | 118 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Balance, December 31, 2006 | | $ | 320 | | $ | 72,023 | | | $ | 16,934 | | | $ | 507 | | | ($ | 396 | ) | | $ | 89,388 | |

| | | | | | | | | | | | | | | | | | | | | | | |

The Notes to Consolidated Financial Statements are an integral part of these statements.

- 6 -

CONSOLIDATED STATEMENTS OF CASH FLOWS

ORRSTOWN FINANCIAL SERVICES, INC. AND ITS WHOLLY-OWNED SUBSIDIARIES

| | | | | | | | | | | | |

| | | Years Ended December 31, | |

(Dollars in thousands) | | 2006 | | | 2005 | | | 2004 | |

Cash flows from operating activities | | | | | | | | | | | | |

Net income | | $ | 11,632 | | | $ | 9,987 | | | $ | 7,770 | |

Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | | | | | | | |

Depreciation and amortization | | | 1,730 | | | | 1,424 | | | | 1,197 | |

Provision for loan losses | | | 390 | | | | 144 | | | | 210 | |

Stock based compensation | | | 224 | | | | 0 | | | | 0 | |

(Gain) loss on disposal of other real estate owned | | | 62 | | | | (20 | ) | | | 45 | |

(Gain) on disposal of bank premises and equipment | | | 0 | | | | 0 | | | | (6 | ) |

Deferred income taxes | | | (493 | ) | | | (191 | ) | | | 28 | |

Investment securities (gains) losses | | | (41 | ) | | | 60 | | | | (88 | ) |

Increase in cash surrender value of life insurance | | | (564 | ) | | | (271 | ) | | | (282 | ) |

(Increase) in accrued interest receivable | | | (566 | ) | | | (394 | ) | | | (128 | ) |

Increase in accrued interest payable | | | 287 | | | | 119 | | | | 34 | |

Other, net | | | 635 | | | | (980 | ) | | | 589 | |

| | | | | | | | | | | | |

Net cash provided by operating activities | | | 13,296 | | | | 9,878 | | | | 9,369 | |

| | | | | | | | | | | | |

| | | |

Cash flows from investing activities | | | | | | | | | | | | |

Net (increase) decrease in interest bearing deposits with banks | | | 2,725 | | | | (2,321 | ) | | | (123 | ) |

Sales of available for sale securities | | | 577 | | | | 4,149 | | | | 6,407 | |

Maturities of available for sale securities | | | 15,352 | | | | 14,437 | | | | 17,518 | |

Purchases of available for sale securities | | | (5,036 | ) | | | (8,928 | ) | | | (15,101 | ) |

Net (purchases) sales of FHLB & FRB Stock | | | (785 | ) | | | 303 | | | | (60 | ) |

Net (increase) in loans | | | (86,347 | ) | | | (73,047 | ) | | | (44,328 | ) |

Purchases of bank premises and equipment | | | (5,165 | ) | | | (1,604 | ) | | | (3,182 | ) |

Purchases of intangible assets | | | 0 | | | | (600 | ) | | | (1,155 | ) |

Proceeds from disposal of other real estate owned | | | 1,882 | | | | 162 | | | | 228 | |

Proceeds from disposal of bank premises and equipment | | | 0 | | | | 0 | | | | 61 | |

Purchase price of shares exchanged for cash | | | (8,882 | ) | | | 0 | | | | 0 | |

Cash acquired in acquisition | | | 13,031 | | | | 0 | | | | 0 | |

Deposit on purchase of bank owned life insurance | | | 0 | | | | (4,500 | ) | | | 0 | |

| | | | | | | | | | | | |

Net cash (used) by investing activities | | | (72,648 | ) | | | (71,949 | ) | | | (39,735 | ) |

| | | | | | | | | | | | |

| | | |

Cash flows from financing activities | | | | | | | | | | | | |

Net increase in deposits | | | 70,395 | | | | 57,459 | | | | 46,720 | |

Net increase (decrease) in short term purchased funds | | | 5,565 | | | | 16,645 | | | | (9,947 | ) |

Proceeds from debt | | | 11,028 | | | | 6,757 | | | | 0 | |

Payments on debt | | | (18,894 | ) | | | (2,020 | ) | | | (1,624 | ) |

Dividends paid | | | (4,662 | ) | | | (3,157 | ) | | | (2,556 | ) |

Proceeds from issuance of common stock | | | 148 | | | | 1,888 | | | | 1,510 | |

Purchase of treasury stock | | | (543 | ) | | | 0 | | | | 0 | |

Net proceeds from issuance of treasury stock | | | 118 | | | | 0 | | | | 0 | |

Cash paid in lieu of fractional shares | | | 0 | | | | (19 | ) | | | 0 | |

| | | | | | | | | | | | |

Net cash provided by financing activities | | | 63,155 | | | | 77,553 | | | | 34,103 | |

| | | | | | | | | | | | |

Net increase in cash and cash equivalents | | | 3,803 | | | | 15,482 | | | | 3,737 | |

Cash and cash equivalents at beginning of period | | | 35,331 | | | | 19,849 | | | | 16,112 | |

| | | | | | | | | | | | |

Cash and cash equivalents at end of period | | $ | 39,134 | | | $ | 35,331 | | | $ | 19,849 | |

| | | | | | | | | | | | |

- 7 -

CONSOLIDATED STATEMENTS OF CASH FLOWS (Continued)

ORRSTOWN FINANCIAL SERVICES, INC. AND ITS WHOLLY-OWNED SUBSIDIARIES

| | | | | | | | | | | |

| | | Years Ended December 31, | |

(Dollars in thousands) | | 2006 | | 2005 | | | 2004 | |

Supplemental disclosure of cash flow information: | | | | | | | | | | | |

Cash paid during the period for: | | | | | | | | | | | |

Interest | | $ | 17,084 | | $ | 9,418 | | | $ | 6,952 | |

Income Taxes | | | 5,390 | | | 4,550 | | | | 3,205 | |

Supplemental schedule of noncash investing and financing activities: | | | | | | | | | | | |

Common stock issued for acquisition of bank | | | 24,841 | | | 0 | | | | 0 | |

Other real estate acquired in settlement of loans | | | 584 | | | 1,895 | | | | 61 | |

Unrealized gain (loss) on investments securities available for sale (net of tax effects) | | | 320 | | | (639 | ) | | | (308 | ) |

| | | | | | | | | | | |

The Notes to Consolidated Financial Statements are an integral part of these statements.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Nature of operations

Orrstown Financial Services, Inc. (the Corporation) is a financial holding company whose primary activity consists of supervising its wholly-owned subsidiaries, Orrstown Bank and The First National Bank of Newport (First National). The Corporation operates through its office in Shippensburg, Pennsylvania. Orrstown Bank and First National provide services through their network of offices in Franklin, Cumberland and Perry Counties of Pennsylvania and in Washington County, Maryland. The banks engage in lending services for commercial loans, residential loans, commercial mortgages and various forms of consumer lending. Deposit services include checking, savings, time and money market deposits. Orrstown Bank also provides investment and brokerage services through its Orrstown Financial Advisors division. Orrstown Bank has sixteen branches located in Shippensburg (2), Carlisle (4), Spring Run, Orrstown, Chambersburg (3), Mechanicsburg (2), Camp Hill and Greencastle, Pennsylvania and Hagerstown, Maryland. First National has four branches located in Newport (2), Duncannon, and New Bloomfield, Pennsylvania. The Corporation and its subsidiaries are subject to the regulation of certain federal and state agencies and undergo periodic examinations by such regulatory authorities.

Principles of consolidation

The consolidated financial statements include the accounts of the Corporation and its wholly-owned subsidiaries, Orrstown Bank and The First National Bank of Newport. All significant intercompany transactions and accounts have been eliminated. Pennbanks Insurance Company Cell P1 was a previously wholly-owned subsidiary of the Corporation. As of January 1, 2006, the Corporation has divested the Pennbanks Insurance Company Cell P1 insurance book of business. The liabilities associated with the insurance business were assumed by American General under a contractual arrangement.

Use of estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Material estimates that are particularly susceptible to significant change relate to the determination of the allowance for losses on loans and the valuation of real estate acquired in connection with foreclosures or in satisfaction of loans. In connection with the determination of the allowance for losses on loans and foreclosed real estate, management obtains independent appraisals for significant properties.

While management uses available information to recognize losses on loans and foreclosed real estate; future additions to the allowances may be necessary based on changes in local economic conditions. In addition, regulatory agencies, as an integral part of their examination process, periodically review the Corporation’s allowance for losses on loans and foreclosed real estate. Such agencies may require the Corporation to recognize additions to the allowance based on their judgments concerning information available to them at the time of their examination. Because of these factors, management’s estimate of credit losses inherent in the loan portfolio and the related allowance may change in the near term.

- 8 -

Investment securities

Under generally accepting accounting principles, the Corporation may segregate their investment portfolio into three specific categories: “securities held to maturity”, “trading securities” and “securities available for sale”. Securities held to maturity are to be accounted for at their amortized cost; securities classified as trading securities are to be accounted for at their current market value with unrealized gains and losses on such securities included in current period earnings; and securities classified as available for sale are to be accounted for at their current market value with unrealized gains and losses on such securities to be excluded from earnings and reported as a net amount in other comprehensive income.

Management determines the appropriate classification of securities at the time of purchase. If management has the intent and the Corporation has the ability at the time of purchase to hold securities until maturity, they are classified as securities held to maturity and carried at amortized historical cost. Securities to be held for indefinite periods of time and not intended to be held to maturity are classified as available for sale and carried at fair value. Securities held for indefinite periods of time include securities that management intends to use as part of its asset and liability management strategy and that may be sold in response to changes in interest rates, resultant prepayment risk and other factors related to interest rate and resultant prepayment risk changes.

The Corporation has classified all of its investment securities as “available for sale”.

Realized gains and losses on dispositions are based on the net proceeds and the adjusted book value of the securities sold, using the specific identification method. Unrealized gains and losses on investment securities available for sale are based on the difference between book value and fair value of each security. These gains and losses are credited or charged to other comprehensive income, whereas realized gains and losses flow through the Corporation’s results of operations.

Cash flows

For purposes of the Statements of Cash Flows, the Corporation has defined cash and cash equivalents as those amounts included in the balance sheet captions “Cash and due from banks” and “Federal funds sold”. The Corporation has elected to present the net increase or decrease in deposits with banks, loans, and deposits in the Statements of Cash Flows.

Premises and equipment

Buildings, improvements, equipment, furniture and fixtures are carried at cost less accumulated depreciation. Depreciation has been provided generally on the straight-line method and is computed over the estimated useful lives of the various assets as follows: buildings and improvements, 10 to 40 years, equipment, furniture and fixtures 3 to 15 years, and computer software is amortized over 3-5 years. Repairs and maintenance are charged to operations as incurred, while major additions and improvements are capitalized. Gain or loss on retirement or disposal of individual assets is recorded as income or expense in the period of retirement or disposal.

Goodwill and other intangible assets

The cost of acquired companies in excess of the fair value of their net assets at the date of acquisition is recorded as goodwill. Identifiable intangible assets relate to acquisitions of deposits from other banks and the purchase of investment management businesses. Goodwill is evaluated annually for impairment and other intangible assets are amortized over the identifiable life of the asset or 15 years.

Loans and allowance for loan losses

Loans are stated at the amount of unpaid principal, reduced by an allowance for loan losses. Interest on loans is calculated by using the simple interest method on daily balances of the principal amount outstanding. The allowance for loan losses is established through a provision for loan losses charged to expense. Loans are charged against the allowance when management believes that the collectibility of the principal is unlikely. Subsequent recoveries, if any, are credited to the allowance. The allowance is an amount that management believes will be adequate to absorb possible losses on existing loans that may become uncollectible. Evaluations of the allowance and collectibility of loans are made on a quarterly basis by management and are guided by the Corporation’s policies. The evaluations take into consideration such factors as prior loan loss experience, changes in the nature and volume of the loan portfolio, overall portfolio quality, review of specific problem loans, and current economic conditions that may affect the borrowers’ ability to pay. This evaluation is inherently subjective as it requires estimates that are susceptible to significant revision as additional information becomes available. An unallocated component is maintained in the allowance to cover uncertainties inherent in management’s underlying assumptions used to estimate probable losses.

Nonaccrual / Impaired loans

The accrual of interest income on loans ceases when principal or interest is past due 90 days or more and collateral is inadequate to cover principal and interest or immediately if, in the opinion of management, full collection is unlikely. Interest accrued but not collected as of the date of placement on nonaccrual status is reversed and charged against current income unless fully collateralized. Subsequent payments received are either applied to the outstanding principal balance or recorded as interest income, depending upon management’s assessment of the ultimate collectibility of principal.

- 9 -

A loan is considered impaired when, based on current information and events, it is probable that the Corporation will be unable to collect the scheduled payments of principal or interest when due according to the contractual terms of the loan agreement. Impairment is measured on a loan-by-loan basis by comparing the contractual principal and interest payments to the present value of expected future cash flows discounted at the loan’s effective interest rate, the loan’s obtainable market price, or the fair value of the collateral if the loan is collateral dependent. Consumer loans, comprised of smaller balance homogeneous loans, are collectively evaluated for impairment. Interest income generally is not recognized on specific impaired loans unless the likelihood of further loss is remote. Interest income on impaired loans is recognized only to the extent of interest payments received.

Loans serviced

The banks administer secondary market mortgage programs available through the Federal Home Loan Bank of Pittsburgh and the Federal National Mortgage Association and offer residential mortgage products and services to customers. The banks originate single-family residential mortgage loans for immediate sale in the secondary market, and retain the servicing of those loans. At December 31, 2006 and 2005 the balance of loans serviced for others was $71,242,000 and $49,288,000 respectively.

Foreclosed real estate

Real estate properties acquired through, or in lieu of, loan foreclosure are to be sold and are initially recorded at the lower of carrying value or fair value less estimated costs to sell the underlying collateral. Capitalized costs include accrued interest and any costs that significantly improve the value of the properties. After foreclosure, valuations are periodically performed by management and the real estate is carried at the lower of carrying amount or fair value less estimated cost to sell.

Earnings per share of common stock

Earnings per share is calculated as net income divided by the weighted average number of shares outstanding, after giving retroactive recognition to a two-for-one stock split effective February 2004, and a 5% stock dividend paid June 2005. For diluted net income per share, net income is divided by the weighted average of shares outstanding plus the incremental number of shares added as a result of converting common stock equivalents. The Corporation’s common stock equivalents consist of outstanding stock options.

A reconciliation of the weighted average shares outstanding used to calculate basic net income per share and diluted net income per share follows. There is no adjustment to net income to arrive at diluted net income per share.

| | | | | | | | | |

(in thousands, except per share data) | | 2006 | | 2005 | | 2004 |

Net income | | $ | 11,632 | | $ | 9,987 | | $ | 7,770 |

| | | | | | | | | |

| | | |

Weighted average number of shares outstanding (basic) | | | 5,906 | | | 5,407 | | | 5,362 |

Effect of dilutive stock options | | | 261 | | | 229 | | | 197 |

| | | | | | | | | |

Weighted average number of shares outstanding (diluted) | | | 6,167 | | | 5,636 | | | 5,559 |

| | | | | | | | | |

| | | |

Per share information: | | | | | | | | | |

Basic earnings per share | | $ | 1.97 | | $ | 1.85 | | $ | 1.45 |

Diluted earnings per share | | $ | 1.89 | | $ | 1.77 | | $ | 1.40 |

Stock-Based Compensation

The Corporation maintains two stock-based compensation plans. These plans provide for the granting of stock options to the Corporation’s employees and directors. The Corporation has historically accounted for the plans using the intrinsic-value method under the recognition and measurement principles of APB Opinion No. 25 and related Interpretations. In December 2004, the FASB issued a final FAS Statement No 123R, “Share-Based Payment”, which requires financial statement recognition of compensation cost for stock options and other stock-based awards. As of January 1, 2006, the Corporation has adopted the modified prospective method. This requires the recognition of compensation expense for the unvested portion of existing awards and new grants, but does not require a restatement of prior periods. All options that were awarded prior to January 1, 2006 were fully vested when granted and did not require any amounts to be expensed. Options have an exercise price equal to the fair market value as established by the average of the daily high bid and daily low offer quotations for the shares reported in the OTC Bulletin Board service during the ten trading days immediately preceding the date of grant. The fair value of each option grant was estimated on the date of grant using the Black-Scholes option-pricing model.

- 10 -

As a result of adopting Statement 123R, the Corporation’s income before taxes and net income for the year ended December 31, 2006, are $224,000 and $146,000 lower, respectively, than if it had continued to account for share-based compensation under Opinion 25. Basic and diluted earnings per share for the year ended December 31, 2006 are $.02 and $.02 lower, respectively, than if the company had continued to account for share-based compensation under Opinion 25. The following table illustrated the effect on net income and earnings per share if the Corporation had applied the fair value recognition provisions of FASB Statement No. 123, “Accounting for Stock-Based Compensation”, to stock-based employee and/or director compensation during 2005 and 2004.

| | | | | | |

| | | Years Ended December 31, |

(in thousands, except per share data) | | 2005 | | 2004 |

Net income | | | | | | |

As reported | | $ | 9,987 | | $ | 7,770 |

Pro forma | | | 9,710 | | | 7,385 |

| | |

Basic earnings per share | | | | | | |

As reported | | $ | 1.85 | | $ | 1.45 |

Pro forma | | $ | 1.80 | | $ | 1.38 |

| | |

Diluted earnings per share | | | | | | |

As reported | | $ | 1.77 | | $ | 1.40 |

Pro forma | | $ | 1.72 | | $ | 1.33 |

Federal income taxes

For financial reporting purposes, the provision for loan losses charged to operating expense is based on management’s judgment, whereas for federal income tax purposes, the amount allowable under present tax law is deducted. Deferred compensation is charged to operating expense in the period the liability is incurred for financial reporting purposes, whereas for federal income tax purposes, these expenses are deducted when paid. Amortization of goodwill is not deducted unless the asset is considered impaired for financial reporting purposes and, if deductible, is deducted on a straight line basis over a fifteen year life for federal income tax purposes. As a result of these, unrealized gains and losses on securities available for sale, and timing differences in depreciation expense and insurance company reserves, deferred income taxes are provided for in the financial statements. See Note 12 for further details.

Fair values of financial instruments

The Corporation meets the requirements for disclosure of fair value information about financial instruments, whether or not recognized in the balance sheet. In cases where quoted market prices are not available, fair values are based on estimates using present value or other valuation techniques. Those techniques are significantly affected by the assumptions used, including the discount rate and estimates of future cash flows. In that regard, the derived fair value estimates cannot be substantiated by comparison to independent markets and, in many cases, could not be realized in immediate settlement of the instruments. Certain financial instruments and all non-financial instruments are excluded from disclosure requirements. Accordingly, the aggregate fair value amounts presented do not represent the underlying value of the Corporation.

The following methods and assumptions were used by the Corporation in estimating fair values of financial instruments as disclosed herein:

Cash, Due from Banks, Short-Term Investments, and Federal Funds Sold. The carrying amounts of cash, due from banks, short-term investments, and federal funds sold approximate their fair value.

Securities Available for Sale. Fair values for investment securities are based on quoted market prices.

Loans Receivable. For variable-rate loans that reprice frequently and have no significant change in credit risk, fair values are based on carrying values. Fair values for fixed rate loans are estimated using discounted cash flow analyses, using interest rates currently being offered for loans with similar terms to borrowers of similar credit quality. Fair values for impaired loans are estimated using discounted cash flow analyses or underlying collateral values, where applicable.

Deposit Liabilities. The fair values disclosed for demand deposits are, by definition, equal to the amount payable on demand at the reporting date (that is, their carrying amounts). The carrying amounts of variable-rate, fixed-term money market accounts and certificates of deposit approximate their fair values at the reporting date. Fair values for fixed-rate certificates of deposits and IRA’s are estimated using a discounted cash flow calculation that applies interest rates currently being offered to a schedule of aggregated expected maturities on time deposits.

- 11 -

Short-Term Borrowings.The carrying amounts of federal funds purchased, borrowings under repurchase agreements, and other short-term borrowings maturing within 90 days approximate their fair values. Fair values of other short-term borrowings are estimated using discounted cash flow analyses based on the Corporation’s current incremental borrowing rates for similar types of borrowing arrangements.

Long-Term Borrowings. The fair value of the Corporation’s long-term debt is estimated using a discounted cash flow analysis based on the Corporation’s current incremental borrowing rate for similar types of borrowing arrangements.

Accrued Interest. The carrying amounts of accrued interest approximate their fair values.

Off-Balance-Sheet Instruments. The Corporation generally does not charge commitment fees. Fees for standby letters of credit and other off-balance-sheet instruments are not significant.

Comprehensive income

Under generally accepted accounting principles, comprehensive income is defined as the change in equity from transactions and other events from non-owner sources. It includes all changes in equity except those resulting from investments by shareholders and distributions to shareholders. Comprehensive income includes net income and certain elements of “other comprehensive income” such as foreign currency transactions; accounting for futures contracts; employers accounting for pensions; and accounting for certain investments in debt and equity securities.

The Corporation has elected to report its comprehensive income in the statement of changes in shareholders’ equity. The only element of “other comprehensive income” that the Corporation has is the unrealized gain or loss on available for sale securities.

The components of the change in net unrealized gains (losses) on securities were as follows:

| | | | | | | | | | | | |

(Dollars in thousands) | | 2006 | | | 2005 | | | 2004 | |

Gross unrealized holding gains (losses) arising during the year | | $ | 538 | | | $ | (1,028 | ) | | $ | (379 | ) |

Reclassification adjustment for (gains) losses realized in net income | | | (41 | ) | | | 60 | | | | (88 | ) |

| | | | | | | | | | | | |

Net unrealized holding gains (losses) before taxes | | | 497 | | | | (968 | ) | | | (467 | ) |

Tax effect | | | (177 | ) | | | 329 | | | | 159 | |

| | | | | | | | | | | | |

Net change | | $ | 320 | | | $ | (639 | ) | | $ | (308 | ) |

| | | | | | | | | | | | |

NOTE 2. ACQUISITION

On May 1, 2006, Orrstown Financial Services, Inc. completed the acquisition of The First National Bank of Newport, a national banking institution with $120 million of assets. First National has four banking offices in Perry County, Pennsylvania and operates as a wholly-owned subsidiary of Orrstown Financial Services, Inc. under the name “The First National Bank of Newport”.

Under the terms of the agreement, each share of First National common stock outstanding at the time of the transaction was exchanged for 1.75 shares of Orrstown Financial Services, Inc. common stock and $22.20 in cash. The purchase price for shares exchanged for common stock was $35.49 with 400,000 shares of First National common stock outstanding. In accordance with SFAS No. 141, “Business Combinations”, the Corporation recorded this transaction using the purchase accounting method. As a result of the acquisition, the results of operations of the Corporation include First National from and after May 1, 2006.

The following table summarizes the preliminary purchase price allocation based on estimated fair values of the assets acquired and liabilities assumed at the date of acquisition.

| | | |

(Dollars in thousands) |

Assets | | | |

Cash and cash equivalents | | | 13,031 |

Investment securities | | | 29,398 |

Net Loans | | | 71,976 |

Core deposit intangible | | | 1,665 |

Other assets | | | 5,828 |

| | | |

Total identifiable assets | | $ | 121,898 |

| | | |

- 12 -

NOTE 2. ACQUISITION (Continued)

| | | |

(Dollars in thousands) | | |

Liabilities | | | |

Total deposits | | | 105,502 |

Short term borrowings | | | 0 |

Long term borrowings | | | 0 |

Other liabilities | | | 547 |

| | | |

Total liabilities | | $ | 106,049 |

| | | |

Merger related expenses of $286,000 were paid in the second quarter of 2006 and recorded as goodwill and associated deferred taxes. All goodwill resulting from the merger was recorded on the balance sheet of First National. The $18,160,000 of goodwill resulting from the acquisition is calculated below.

| | | | | | | |

(Dollars in thousands, except per share data) | | | | | |

Orrstown Financial Services, Inc common stock issued | | | 699,949 | | | | |

Average purchase price per Orrstown common shares | | $ | 35.49 | | | | |

| | | | | | | |

| | | | | | $ | 24,841 |

Cash price paid at $22.20 per share plus 51 fractional shares | | | | | | | 8,882 |

Merger costs | | | | | | | 286 |

| | | | | | | |

Total purchase price | | | | | | | 34,009 |

| | |

Net assets acquired: | | | | | | | |

First National’s shareholders’ equity | | | 13,648 | | | | |

| | |

Adjustments to reflect assets acquired at fair value: | | | | | | | |

Investments | | | 0 | | | | |

Loans | | | 329 | | | | |

Bank premises | | | 1,189 | | | | |

Core deposit intangible | | | 1,665 | | | | |

Deferred tax assets | | | (1,165 | ) | | | |

Adjustments to reflect liabilities acquired at fair value: | | | | | | | |

Time deposits | | | 183 | | | | |

| | | | | | | |

| | | | | | | 15,849 |

| | | | | | | |

Goodwill resulting from merger | | | | | | $ | 18,160 |

| | | | | | | |

As a result of the amortization or accretion of premiums, discounts and intangible assets, net income before taxes was reduced by $29,000. The table below sets forth the periods and methods of amortization or accretion and the estimated remaining lives by intangible class.

| | | | | | | | | | |

| | | | | | Amortization | | |

(Dollars in thousands) | | Gross Amount | | | Period | | Method | | Remaining

Life |

Commercial loans | | $ | (378 | ) | | 4 years | | Declining balance – annual | | 3.3 years |

Consumer loans | | | 13 | | | 4 years | | Declining balance – annual | | 3.3 years |

Mortgage loans | | | 694 | | | 9 years | | Declining balance – annual | | 8.3 years |

Bank premises | | | 1,189 | | | 30 years | | Straight line | | 29.3 years |

Core deposit intangible | | | 1,665 | | | 10 years | | Straight line | | 9.3 years |

Time deposits | | | 183 | | | 6 years | | Declining balance – monthly | | 5.3 years |

| | | | | | | | | | |

Weighted average amortization period | | | | | | 14.9 years | | | | |

| | | | | | | | | | |

- 13 -

NOTE 2. ACQUISITION (Continued)

The following pro forma combined results of operations for the years ended December 31, 2006 and December 31, 2005, and gives effect to the merger as if the merger had been completed on January 1, 2006 and January 1, 2005, respectively. The pro forma information shows the combination of First National’s historical results into Orrstown Financial Services, Inc. results of operations under the purchase method of accounting. While certain adjustments have been made for the estimated impact of purchase accounting adjustments, the pro forma results of operations is presented for illustrative purposes only and does not indicate the financial results of the Corporation had the companies actually been combined at the beginning of the period presented.

| | | | |

(Dollars in thousands, except per share data) | | Pro forma |

| | | Years Ended December 31, |

| | | 2006 | | 2005 |

Net interest income | | 28,973 | | 27,310 |

Other income | | 11,268 | | 9,829 |

Net income | | 11,949 | | 11,461 |

| | |

Earnings per share | | 1.95 | | 1.88 |

NOTE 3. INVESTMENTS

At December 31, 2006 and 2005 the investment securities portfolio was comprised of securities classified as “available for sale”, resulting in investment securities being carried at fair value.

The amortized cost and fair values of investment securities available for sale at December 31 were:

| | | | | | | | | | | | |

| | | Amortized

Cost | | Gross

Unrealized

Gains | | Gross

Unrealized

Losses | | Fair

Value |

(Dollars in thousands) | | 2006 |

U. S. Treasury securities and obligations of U. S. Government corporations and agencies | | $ | 25,344 | | $ | 7 | | $ | 241 | | $ | 25,110 |

Obligations of states and political subdivisions | | | 28,096 | | | 846 | | | 92 | | | 28,850 |

Mortgage-backed securities | | | 29,963 | | | 40 | | | 664 | | | 29,339 |

Corporate bonds | | | 1,302 | | | 0 | | | 10 | | | 1,292 |

Equity securities | | | 2,448 | | | 537 | | | 33 | | | 2,952 |

| | | | | | | | | | | | |

Totals | | $ | 87,153 | | $ | 1,430 | | $ | 1,040 | | $ | 87,543 |

| | | | | | | | | | | | |

| |

| | | 2005 |

U. S. Treasury securities and obligations of U. S. Government corporations and agencies | | $ | 16,492 | | $ | 0 | | $ | 282 | | $ | 16,210 |

Obligations of states and political subdivisions | | | 20,531 | | | 949 | | | 33 | | | 21,447 |

Mortgage-backed securities | | | 29,529 | | | 59 | | | 728 | | | 28,860 |

Equity securities | | | 2,172 | | | 365 | | | 46 | | | 2,491 |

| | | | | | | | | | | | |

Totals | | $ | 68,724 | | $ | 1,373 | | $ | 1,089 | | $ | 69,008 |

| | | | | | | | | | | | |

- 14 -

NOTE 3. INVESTMENTS (Continued)

The following table shows gross unrealized losses and fair value, aggregated by investment category and length of time that individual securities have been in a continuous unrealized loss position, at December 31:

| | | | | | | | | | | | | | | | | | |

| | | Less Than 12 Months | | 12 Months or More | | Total |

| | | Fair Value | | Unrealized

Losses | | Fair Value | | Unrealized

Losses | | Fair Value | | Unrealized

Losses |

(Dollars in thousands) | | 2006 |

U. S. Treasury securities and obligations of U. S. Government corporations and agencies | | $ | 7,419 | | $ | 87 | | $ | 13,179 | | $ | 154 | | $ | 20,598 | | $ | 241 |

Obligations of states and political subdivisions | | | 3,663 | | | 69 | | | 1,683 | | | 23 | | | 5,346 | | | 92 |

Mortgage-backed securities | | | 6,028 | | | 148 | | | 20,288 | | | 516 | | | 26,316 | | | 664 |

Corporate bonds | | | 893 | | | 10 | | | 0 | | | 0 | | | 893 | | | 10 |

| | | | | | | | | | | | | | | | | | |

Total debt securities | | | 18,003 | | | 314 | | | 35,150 | | | 693 | | | 53,153 | | | 1,007 |

| | | | | | | | | | | | | | | | | | |

Equity securities | | | 201 | | | 20 | | | 71 | | | 13 | | | 272 | | | 33 |

| | | | | | | | | | | | | | | | | | |

Total temporarily impaired securities | | $ | 18,204 | | $ | 334 | | $ | 35,221 | | $ | 706 | | $ | 53,425 | | $ | 1,040 |

| | | | | | | | | | | | | | | | | | |

| |

| | | 2005 |

U. S. Treasury securities and obligations of U. S. Government corporations and agencies | | $ | 4,053 | | $ | 67 | | $ | 12,157 | | $ | 215 | | $ | 16,210 | | $ | 282 |

Obligations of states and political subdivisions | | | 492 | | | 8 | | | 1,205 | | | 25 | | | 1,697 | | | 33 |

Mortgage-backed securities | | | 1,940 | | | 43 | | | 23,930 | | | 685 | | | 25,870 | | | 728 |

| | | | | | | | | | | | | | | | | | |

Total debt securities | | | 6,485 | | | 118 | | | 37,292 | | | 925 | | | 43,777 | | | 1,043 |

| | | | | | | | | | | | | | | | | | |

Equity securities | | | 438 | | | 26 | | | 76 | | | 20 | | | 514 | | | 46 |

| | | | | | | | | | | | | | | | | | |

Total temporarily impaired securities | | $ | 6,923 | | $ | 144 | | $ | 37,368 | | $ | 945 | | $ | 44,291 | | $ | 1,089 |

| | | | | | | | | | | | | | | | | | |

The previous table represents one hundred twenty-one investment securities at December 31, 2006 and fifty-two investment securities at December 31, 2005 where the current fair value is less than the related amortized cost. Management believes the impairments to be temporary in all cases for both years disclosed. Consideration is given to the extent to which the fair value has been less than cost, the financial condition and near-term prospects of the issuer, and the intent and ability of the Corporation to retain its investment in the issuer for a period of time sufficient to allow for any anticipated recovery in fair value.

At December 31, 2006, the Corporation held 8 issues of high quality US treasuries and US government agency obligations and 2 municipal securities with fair values less than the related amortized cost for twelve months or more. In addition, 14 issues of US government agency mortgage backed securities were held with fair values less than the related amortized cost for twelve months or more. All 24 of these issues had been purchased during lower rate periods and carry lower than current rates. They do not reflect any deterioration of the credit worthiness of the issuing entities. As management has the ability to hold these securities for the foreseeable future in all cases, no decline is deemed to be other than temporary. Three marketable equity securities have unrealized losses for twelve months or more. All three companies are profitable and paying dividends. Since these companies are considered viable and carry the possibility of price appreciation in the future, impairments are considered temporary.

At December 31, 2005, US treasuries, state and municipal and mortgage-backed securities combined, had twenty-three issues with fair values less than the related amortized cost for twelve months or more; and four marketable equity securities had fair values less than the related amortized cost for twelve months or more.

The amortized cost and fair values of investment securities available for sale at December 31, 2006, by contractual maturity are shown below. Contractual maturities will differ from expected maturities because borrowers may have the right to call or prepay obligations with or without call or prepayment penalties.

| | | | | | |

(Dollars in thousands) | | Amortized Cost | | Fair Value |

Due in one year or less | | $ | 13,170 | | $ | 13,062 |

Due after one year through five years | | | 15,472 | | | 15,330 |

Due after five years through ten years | | | 10,724 | | | 10,820 |

Due after ten years | | | 15,376 | | | 16,040 |

Mortgage-backed securities | | | 29,963 | | | 29,339 |

Equity securities | | | 2,448 | | | 2,952 |

| | | | | | |

| | $ | 87,153 | | $ | 87,543 |

| | | | | | |

- 15 -

NOTE 3. INVESTMENTS (Continued)

Proceeds from sales of securities available for sale for the years ended December 31, 2006, 2005, and 2004, were $577,000, $4,149,000 and $6,407,000, respectively. Gross gains and losses on 2006 sales were $57,000 and $16,000 respectively. Gross gains and losses on 2005 sales were $49,000 and $109,000, respectively. Gross gains and losses on 2004 sales were $164,000 and $76,000, respectively.

The Corporation owned $2,580,000 of Federal Home Loan Bank stock, $64,000 of Atlantic Central Bankers Bank stock and $1,206,000 of Federal Reserve Bank stock at December 31, 2006. At December 31, 2005, the Corporation owned $2,426,000 of Federal Home Loan Bank stock, $54,000 of Atlantic Central Bankers Bank stock and $189,000 of Federal Reserve Bank stock. Market value approximates cost since none of the stocks are actively traded.

Securities with a market value of $66,574,000 and $60,916,000 at December 31, 2006 and 2005, respectively, were pledged to secure public funds and for other purposes as required or permitted by law.

NOTE 4. CONCENTRATION OF CREDIT RISK

The Corporation grants agribusiness, commercial, residential and consumer loans to customers in its market area. Although the Corporation maintains a diversified loan portfolio, a significant portion of its customers’ ability to honor their contracts is dependent upon economic sectors for construction contractors, non-residential building operators, sales finance, sub-dividers and developers. Management evaluates each customer’s creditworthiness on a case-by-case basis. The amount of collateral obtained, if collateral is deemed necessary by the Corporation upon the extension of credit, is based on management’s credit evaluation of the customer. Collateral held varies but generally includes real estate and equipment.

NOTE 5. ALLOWANCE FOR LOAN LOSSES

An allowance amount has been established for the acquired credit risk of the loan portfolio less any amounts attributable to loans with credit quality issues acquired in the May 1, 2006 acquisition of The First National Bank of Newport. Activity in the allowance for loan losses is summarized as follows:

| | | | | | | | | |

(Dollars in thousands) | | 2006 | | 2005 | | 2004 |

Balance at beginning of period | | $ | 4,428 | | $ | 4,318 | | $ | 4,161 |

Recoveries | | | 79 | | | 48 | | | 32 |

Provision for loan losses charged to income | | | 390 | | | 144 | | | 210 |

| | | | | | | | | |

Total | | | 4,897 | | | 4,510 | | | 4,403 |

Losses | | | 97 | | | 82 | | | 85 |

Additions established for acquired credit risk | | | 720 | | | 0 | | | 0 |

| | | | | | | | | |

Balance at end of period | | $ | 5,520 | | $ | 4,428 | | $ | 4,318 |

| | | | | | | | | |

NOTE 6. LOANS TO RELATED PARTIES

The Corporation has granted loans to the officers and directors of the Corporation and its subsidiary and to their associates. Related party loans are made on substantially the same terms, including interest rates and collateral, as those prevailing at the time for comparable transactions with unrelated persons and do not involve more than normal risk of collectibility. The aggregate dollar amount of these loans was $2,508,000 at December 31, 2006, and $1,227,000 at December 31, 2005. During 2006, $1,250,000 of loans to officers and directors were acquired with the purchase of First National, $1,050,000 of new loans were granted and repayments totaled $1,019,000. Outstanding loans to employees totaled $4,825,000 and $3,074,000 at December 31, 2006 and 2005, respectively.

- 16 -

NOTE 7. DELINQUENT AND NONACCRUAL LOANS

Loans 90 days or more past due (still accruing interest) were as follows at December 31:

| | | | | | | | | |

(Dollars in thousands) | | 2006 | | 2005 | | 2004 |

Commercial, financial and agricultural | | $ | 0 | | $ | 16 | | $ | 0 |

Real estate | | | 1,067 | | | 390 | | | 2,541 |

Consumer | | | 17 | | | 5 | | | 9 |

| | | | | | | | | |

Total | | $ | 1,084 | | $ | 411 | | $ | 2,550 |

| | | | | | | | | |

The following table shows the principal balances of nonaccrual loans as of December 31:

| | | | | | | | | | |

(Dollars in thousands) | | 2006 | | | 2005 | | 2004 |

Nonaccrual loans | | $ | 120 | | | $ | 52 | | $ | 314 |

| | | | | | | | | | |

Interest income that would have been accrued at original contract rates | | | 23 | | | | 30 | | | 31 |

Amount recognized as interest income | | | 27 | | | | 10 | | | 13 |

| | | | | | | | | | |

Foregone (recovered) revenue | | $ | (4 | ) | | $ | 20 | | $ | 18 |

| | | | | | | | | | |

The Corporation had no impairment of loans as of December 31, 2006, 2005, and 2004.

During 2006, the Corporation foreclosed on four loans secured by real estate property. Nine properties were sold during 2006 at a gain of $62,000. This amount is included in other income on the statements of income. Net gains (losses) from sales of foreclosed property for the years ended December 31, 2005 and 2004 were $20,000 and ($45,000), respectively. At December 31, 2006, the Corporation held one property obtained through foreclosure. The carrying value for this property totaled $318,000, which is included in other assets on the balance sheet at December 31, 2006. At December 31, 2005, the Corporation held six properties obtained through foreclosure. The carrying value for these properties totaled $1,754,000, which is included in other assets on the balance sheet at December 31, 2005.

NOTE 8. FINANCIAL INSTRUMENTS WITH OFF-BALANCE-SHEET RISK

The Corporation is a party to financial instruments with off-balance-sheet risk in the normal course of business to meet the financial needs of its customers and to reduce its own exposure to fluctuations in interest rates. These financial instruments include commitments to extend credit and standby letters of credit. Those instruments involve, to varying degrees, elements of credit and interest rate risk in excess of the amount recognized in the balance sheets. The contract amounts of those instruments reflect the extent of involvement the Corporation has in particular classes of financial instruments.

The Corporation’s exposure to credit loss in the event of nonperformance by the other party to the financial instrument for commitments to extend credit and standby letters of credit and financial guarantees written is represented by the contractual amount of those instruments. The Corporation uses the same credit policies in making commitments and conditional obligations as it does for on-balance-sheet instruments.

| | | | | | |

| | | Contract or Notional Amount |

(Dollars in thousands) | | 2006 | | 2005 |

Financial instruments whose contract amounts represent credit risk at December 31: | | | | | | |

Commitments to extend credit | | $ | 128,197 | | $ | 125,490 |

Standby letters of credit and financial guarantees written | | | 21,517 | | | 16,401 |

| | | | | | |

Commitments to extend credit are agreements to lend to a customer as long as there is no violation of any condition established in the contract. Commitments generally have fixed expiration dates or other termination clauses and may require payment of a fee. Since many of the commitments are expected to expire without being drawn upon, the total commitment amounts do not necessarily represent future cash requirements. The Corporation evaluates each customer’s credit-worthiness on a case-by-case basis. The amount of collateral obtained, if deemed necessary by the Corporation upon extension of credit, is based on management’s credit evaluation of the customer. Collateral held varies but may include accounts receivable, inventory, equipment, residential real estate, and income-producing commercial properties.

Standby letters of credit and financial guarantees written are conditional commitments issued by the Corporation to guarantee the performance of a customer to a third party. Those guarantees are primarily issued to support public and private borrowing arrangements. The credit risk involved in issuing letters of credit is essentially the same as that involved in extending loans to customers. The Corporation holds collateral supporting those commitments when deemed necessary by management.

- 17 -

NOTE 9. PREMISES AND EQUIPMENT

A summary of bank premises and equipment is as follows:

| | | | | | |

(Dollars in thousands) | | 2006 | | 2005 |

Land | | $ | 3,545 | | $ | 2,043 |

Buildings and improvements | | | 14,584 | | | 9,677 |

Leasehold improvements | | | 321 | | | 279 |

Furniture and equipment | | | 12,344 | | | 9,376 |

Construction in progress | | | 574 | | | 630 |

| | | | | | |

Total | | | 31,368 | | | 22,005 |

Less accumulated depreciation and amortization | | | 11,516 | | | 8,369 |

| | | | | | |

Bank premises and equipment, net | | $ | 19,852 | | $ | 13,636 |

| | | | | | |

Depreciation expense amounted to $1,408,000, $1,190,000, and $1,073,000 for the years ended December 31, 2006, 2005 and 2004, respectively.

NOTE 10. RETIREMENT PLANS

The Corporation maintains 401(k) profit-sharing plans for those employees who meet the eligibility requirements set forth in the plans. Employer contributions to the plans are based on performance and are at the discretion of the subsidiary bank Boards of Directors. The plans contain limited match or safe harbor provisions. Substantially all of the Corporation’s employees are covered by the plan and the contributions charged to operations were $1,228,000, $977,000 and $899,000 for the years ended December 31, 2006, 2005, and 2004, respectively.

The Corporation has a deferred compensation arrangement with certain present and former board directors whereby a director or his beneficiaries will receive a monthly retirement benefit at age 65. The arrangement is funded by an amount of life insurance on the participating director calculated to meet the Corporation’s obligations under the compensation agreement. The cash value of the life insurance policies is an unrestricted asset of the Corporation. The estimated present value of future benefits to be paid, which is included in other liabilities, amounted to $119,000 and $120,000 at December 31, 2006 and 2005, respectively. Total annual expense for this deferred compensation plan was approximately $12,000 for each of the years ended December 31, 2006, 2005 and 2004.

The Corporation also has supplemental discretionary deferred compensation plans for directors and executive officers. The plans are funded annually with director fees and salary reductions which are either placed in a trust account invested by the Corporation’s Orrstown Financial Advisors division or recognized as a liability. The trust account balance was $809,000 and $683,000 at December 31, 2006 and 2005, respectively, and is included in other assets on the balance sheets, offset by other liabilities in the same amount. The liability account for the plan at First National stood at $113,000 on December 31, 2006. Total amount contributed to the plans was $103,000, $86,000 and $77,000, for the years ended December 31, 2006, 2005, and 2004, respectively.

The Corporation has also adopted three supplemental retirement and salary continuation plans for directors and executive officers. These plans are funded with single premium life insurance on the plan participants. The cash value of the life insurance policies is an unrestricted asset of the Corporation. The estimated present value of future benefits to be paid totaled $1,849,000 and $1,368,000 at December 31, 2006 and 2005, respectively, which is included in other liabilities. Total annual expense for these plans amounted to $481,000, $233,000 and $217,000, for the years ended December 31, 2006, 2005, and 2004, respectively.

- 18 -

NOTE 11. STOCK COMPENSATION PLANS

During 2000, the Corporation implemented two stock option plans, one for employees and one for nonemployee directors. Under the Corporation’s stock option plans, the Corporation may grant options to its directors, officers, and employees for up to 532,507 shares of common stock. Both incentive stock options and nonqualified stock options may be granted under the plans. The exercise price of each option equals the market price of the Corporation’s stock on the date of grant and an option’s maximum term is ten years. All options are fully vested upon issuance.

A summary of the status of the Corporation’s stock option plans at December 31, 2006, 2005 and 2004 is presented below:

| | | | | | | | | | | | | | | | | | |

| | | Shares | | | Weighted Average Exercise

Price | | Shares | | | Weighted Average Exercise

Price | | Shares | | | Weighted Average Exercise

Price |

| | | 2006 | | 2005 | | 2004 |

Outstanding at beginning of year | | 244,108 | | | $ | 28.37 | | 211,841 | | | $ | 24.64 | | 190,603 | | | $ | 19.98 |

Granted | | 34,712 | | | | 37.32 | | 48,616 | | | | 42.01 | | 48,202 | | | | 38.88 |

Exercised | | (4,208 | ) | | | 23.67 | | (16,349 | ) | | | 20.62 | | (26,964 | ) | | | 17.22 |

Forfeited | | 0 | | | | 0.00 | | 0 | | | | 0.00 | | 0 | | | | 0.00 |

| | | | | | | | | | | | | | | | | | |

Options exercisable at year end | | 274,612 | | | $ | 29.57 | | 244,108 | | | $ | 28.37 | | 211,841 | | | $ | 24.64 |

| | | | | | | | | | | | | | | | | | |

Information pertaining to options outstanding at December 31, 2006 is as follows:

| | | | | | | | | | | | |

Options Outstanding | | Options Exercisable |

Range of Exercise Prices | | Number Outstanding | | Weighted Average Remaining Contractual Life (Years) | | Weighted Average Exercise Price | | Number Exercisable | | Weighted Average Exercise Price |

$16.20 - $17.11 | | 18,658 | | 3.44 | | $ | 16.42 | | 18,658 | | $ | 16.42 |

$17.12 - $17.32 | | 37,568 | | 4.46 | | | 17.29 | | 37,568 | | | 17.29 |

$17.33 - $19.99 | | 43,884 | | 5.47 | | | 19.67 | | 43,884 | | | 19.67 |

$20.00 - $25.99 | | 43,497 | | 6.47 | | | 25.50 | | 43,497 | | | 25.50 |

$30.00 - $37.99 | | 34,712 | | 9.47 | | | 37.32 | | 34,712 | | | 37.32 |

$38.00 - $42.15 | | 96,293 | | 7.99 | | | 40.46 | | 96,293 | | | 40.46 |

| | | | | | | | | | | | |

$16.20 - $42.15 | | 274,612 | | 6.74 | | $ | 29.57 | | 274,612 | | $ | 29.57 |

| | | | | | | | | | | | |

The aggregate intrinsic value of outstanding stock options at December 31, 2006 is $1,917,000 and the total intrinsic value of stock options exercised during 2006 was $49,000.

The fair value of each option granted is estimated on the date of grant using the Black-Scholes option-pricing model with the following weighted-average assumptions:

| | | | | | | | | | | | | | |

| | | Grant-Date Fair Value | | Dividend Yield | | | Expected Volatility | | | Risk Free Interest Rate | | | Expected Life (Yrs) |

Nonemployee director stock option plan | | | | | | | | | | | | | | |

2006 | | $ | 6.96 | | 2.23 | % | | 15.74 | % | | 4.83 | % | | 7 |

2005 | | | 9.28 | | 1.28 | | | 19.47 | | | 4.29 | | | 7 |

2004 | | | 14.05 | | 1.11 | | | 32.80 | | | 3.38 | | | 7 |

Employee stock option plan | | | | | | | | | | | | | | |

2006 | | $ | 6.39 | | 2.11 | % | | 14.83 | % | | 5.18 | % | | 5 |

2005 | | | 8.59 | | 1.33 | | | 19.41 | | | 3.74 | | | 5 |

2004 | | | 12.00 | | 1.18 | | | 32.18 | | | 3.85 | | | 5 |

During 2000, the Corporation implemented an employee stock purchase plan under which 173,643 shares of common stock have been reserved for issuance to employees. The number of shares which may be issued to each participant is determined annually, based on individual earnings, and their cost is equal to 85% of the fair market value as established by the average of the average of the daily high bid and daily low offer quotations for the shares reported in the OTC Bulletin Board service, during the ten trading days immediately preceding the date of purchase. If no bid or offer quotation for the shares is reported through the OTC Bulletin Board service during the ten business day period, the fair market value is the price of the last trade reported through the OTC Bulletin Board service prior to the purchase date. A total of 139,086 shares of common stock remained reserved at December 31, 2006 for future grants under the plan. Employees purchased 5,695, 4,911 and 4,111 shares at a weighted average price of $29.19, $31.26 and $31.18 per share in 2006, 2005 and 2004, respectively. During 1998, the Corporation implemented a Dividend Reinvestment Plan under which 995,557 shares of common stock have been reserved for issuance to shareholders enrolled in the plan. The Board of directors temporarily suspended the dividend Reinvestment Plan effective the first quarter of 2006.

- 19 -

NOTE 11. STOCK COMPENSATION PLANS (Continued)

Shares of common stock registered and available for issuance through approved plans at December 31, 2006 are as follows:

| | |

| | | Number of Shares |

Stock option plans | | 207,493 |

Employee stock purchase plan | | 139,086 |

Dividend reinvestment plan | | 729,647 |

| | |

Total registered shares | | 1,076,226 |

| | |

NOTE 12. INCOME TAXES

The components of federal income tax expense are summarized as follows:

| | | | | | | | | | | |

(Dollars in thousands) | | 2006 | | | 2005 | | | 2004 |

Current year provision | | $ | 5,343 | | | $ | 4,600 | | | $ | 3,149 |

Deferred income taxes (benefits) | | | (493 | ) | | | (191 | ) | | | 28 |

| | | | | | | | | | | |

Net federal income tax expense | | $ | 4,850 | | | $ | 4,409 | | | $ | 3,177 |

| | | | | | | | | | | |

Federal income taxes were computed after reducing pretax accounting income for non-taxable income in the amount of $2,553,000, $1,613,000 and $1,713,000 for 2006, 2005 and 2004, respectively.

A reconciliation of the effective applicable income tax rate to the federal statutory rate is as follows:

| | | | | | | | | |

| | | 2006 | | | 2005 | | | 2004 | |

Federal income tax rate | | 35.0 | % | | 34.0 | % | | 34.0 | % |

Reduction resulting from nontaxable income | | 5.6 | % | | 3.4 | % | | 5.0 | % |

| | | | | | | | | |

Effective income tax rate | | 29.4 | % | | 30.6 | % | | 29.0 | % |

| | | | | | | | | |

Deferred tax liabilities have been provided for taxable temporary differences related to accumulated depreciation, unrealized gains on available for sale securities and deductible amortization expense of goodwill, intangibles and purchase accounting adjustments. Deferred tax assets have been provided for deductible temporary differences related to the allowance for loan losses, asset impairment, deferred compensation, stock options, capitalized merger expenses and retirement plans. The Corporation has not recorded a valuation allowance for deferred tax assets as it is more likely than not that they will be ultimately realized.

The net deferred tax assets (liabilities) included in the accompanying consolidated balance sheets includes the following significant components:

| | | | | | | | |

(Dollars in thousands) | | 2006 | | | 2005 | |

Deferred tax assets | | | | | | | | |

Allowance for loan losses | | $ | 1,794 | | | $ | 1,431 | |

Deferred fees | | | 7 | | | | 26 | |

Asset impairment | | | 14 | | | | 13 | |

Deferred compensation | | | 359 | | | | 273 | |

Stock options expense | | | 78 | | | | 0 | |

Capitalized merger expenses | | | 14 | | | | 0 | |

Retirement plans and salary continuation | | | 638 | | | | 466 | |

| | | | | | | | |

Total deferred tax assets | | | 2,904 | | | | 2,209 | |

| | | | | | | | |

Deferred tax liabilities | | | | | | | | |