Exhibit 99.1

Exhibit 99.1

Business Update

May 30-31, 2006

Forward-Looking Statement

This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements reflect Edison International’s current expectations and projections about future events based on Edison International’s knowledge of present facts and circumstances and assumptions about future events and include any statement that does not directly relate to a historical or current fact. In this presentation and elsewhere, the words “expects,” “believes,” “anticipates,” “estimates,” “projects,” “intends,” “plans,” “probable,” “may,” “will,” “could,” “would,” “should,” and variations of such words and similar expressions, or discussions of strategy or of plans, are intended to identify forward-looking statements. Such statements necessarily involve risks and uncertainties that could cause actual results to differ materially from those anticipated. Some of the risks, uncertainties and other important factors that could cause results to differ, or that otherwise could impact Edison International or its subsidiaries, include but are not limited to: the ability of Edison International to meet its financial obligations and to pay dividends on its common stock if its subsidiaries are unable to pay dividends; the ability of Southern California Edison (SCE) to recover its costs in a timely manner from its customers through regulated rates; decisions and other actions by the California Public Utilities Commission (CPUC) and other regulatory authorities and delays in regulatory actions; market risks affecting SCE’s energy procurement activities; access to capital markets and the cost of capital; changes in interest rates, rates of inflation and foreign exchange rates; governmental, statutory, regulatory or administrative changes or initiatives affecting the electricity industry, including the market structure rules applicable to each market and environmental regulations that could require additional expenditures or otherwise affect the cost and manner of doing business; risks associated with operating nuclear and other power generating facilities, including operating risks, nuclear fuel storage, equipment failure, availability, heat rate and output; the availability of labor, equipment and materials; the ability to obtain sufficient insurance, including insurance relating to SCE’s nuclear facilities; effects of legal proceedings, changes in or interpretations of tax laws, rates or policies, and changes in accounting standards; supply and demand for electric capacity and energy, and the resulting prices and dispatch volumes, in the wholesale markets to which MEHC generating units have access; the cost and availability of coal, natural gas, and fuel oil, nuclear fuel, and associated transportation; the cost and availability of emission credits or allowances for emission credits; transmission congestion in and to each market area and the resulting differences in prices between delivery points; the ability to provide sufficient collateral in support of hedging activities and purchased power and fuel; the extent of additional supplies of capacity, energy and ancillary services from current competitors or new market entrants, including the development of new generation facilities and technologies; general political, economic and business conditions; weather conditions, natural disasters and other unforeseen events; and changes in the fair value of investments and other assets accounted for using fair value accounting.

Additional information about risks and uncertainties, including more detail about the factors described above, is contained in Edison International’s reports filed with the Securities and

Exchange Commission. Readers are urged to read such reports and carefully consider the risks, uncertainties and other factors that affect Edison International’s business. Readers also should review future reports filed by Edison International with the Securities and Exchange Commission. The information contained in this presentation is subject to change without notice. Forward-looking statements speak only as of the date they are made and Edison International is not obligated to publicly update or revise forward-looking statements.

1 |

|

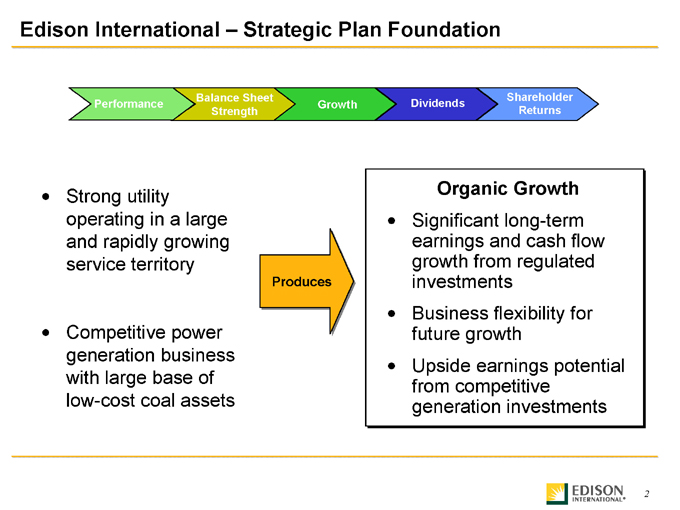

Edison International – Strategic Plan Foundation

Performance

Balance Sheet Strength

Growth

Dividends

Shareholder Returns

Strong utility operating in a large and rapidly growing service territory

Competitive power generation business with large base of low-cost coal assets

Produces

Organic Growth

Significant long-term earnings and cash flow growth from regulated investments Business flexibility for future growth Upside earnings potential from competitive generation investments

2 |

|

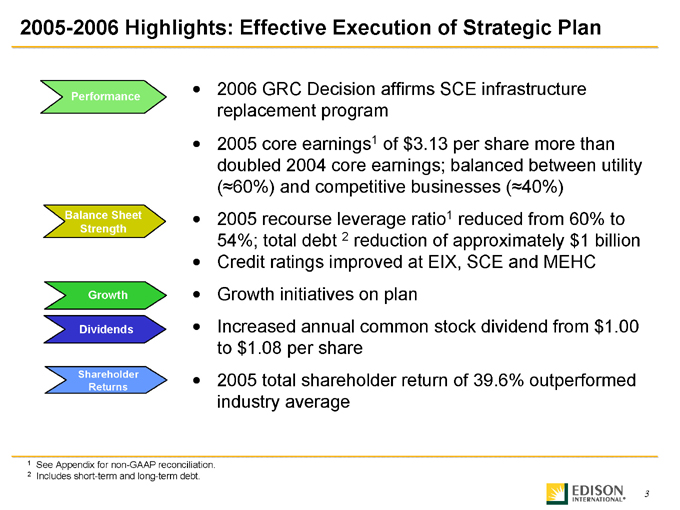

2005-2006 Highlights: Effective Execution of Strategic Plan

Performance

2006 GRC Decision affirms SCE infrastructure replacement program 2005 core earnings1 of $3.13 per share more than doubled 2004 core earnings; balanced between utility (60%) and competitive businesses (40%)

Balance Sheet Strength

2005 recourse leverage ratio1 reduced from 60% to 54%; total debt 2 reduction of approximately $1 billion Credit ratings improved at EIX, SCE and MEHC

Growth

Growth initiatives on plan

Dividends

Increased annual common stock dividend from $1.00 to $1.08 per share

Shareholder Returns

2005 total shareholder return of 39.6% outperformed industry average

1 |

| See Appendix for non-GAAP reconciliation. |

2 |

| Includes short-term and long-term debt. |

3 |

|

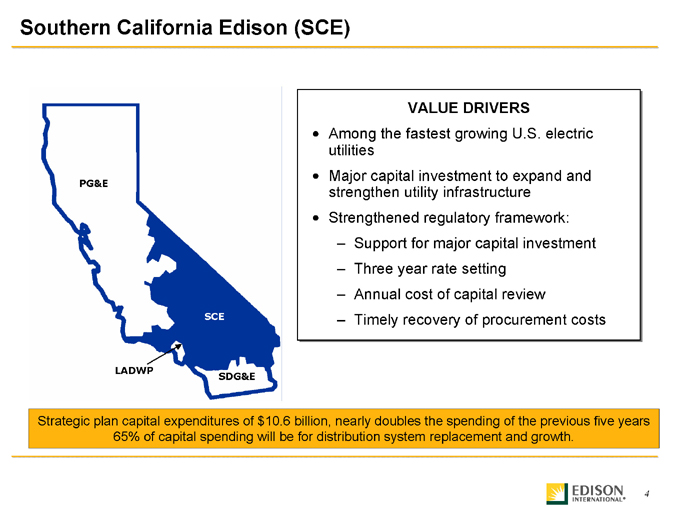

Southern California Edison (SCE)

PG&E

LADWP

SCE

SDG&E

VALUE DRIVERS

Among the fastest growing U.S. electric utilities Major capital investment to expand and strengthen utility infrastructure Strengthened regulatory framework:

Support for major capital investment Three year rate setting Annual cost of capital review Timely recovery of procurement costs

Strategic plan capital expenditures of $10.6 billion, nearly doubles the spending of the previous five years 65% of capital spending will be for distribution system replacement and growth.

4 |

|

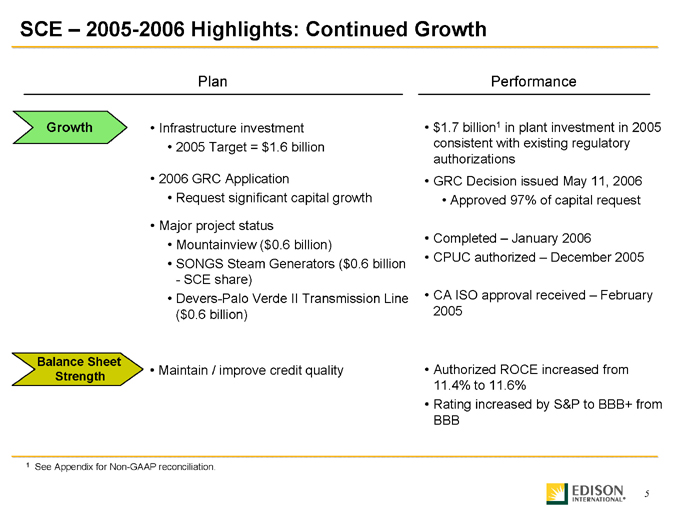

SCE – 2005-2006 Highlights: Continued Growth

Growth

Plan |

| Performance |

Infrastructure investment • $1.7 billion1 in plant investment in 2005 consistent with existing regulatory authorizations

2005 |

| Target = $1.6 billion |

2006 |

| GRC Application • GRC Decision issued May 11, 2006 |

Request |

| significant capital growth • Approved 97% of capital request |

Major |

| project status • Completed – January 2006 |

Mountainview |

| ($0.6 billion) • CPUC authorized – December 2005 |

SONGS |

| Steam Generators ($0.6 billion—SCE share) |

Devers-Palo |

| Verde II Transmission Line ($0.6 billion) • CA ISO approval received – February 2005 |

Balance Sheet Strength

Maintain |

| / improve credit quality Authorized ROCE increased from |

11.4% |

| to 11.6% |

Rating increased by S&P to BBB+ from

BBB

1 |

| See Appendix for Non-GAAP reconciliation. |

5 |

|

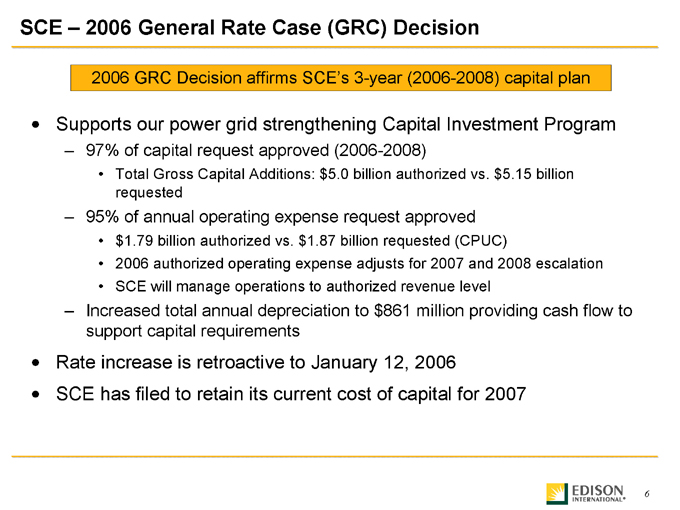

SCE – 2006 General Rate Case (GRC) Decision

2006 GRC Decision affirms SCE’s 3-year (2006-2008) capital plan

Supports our power grid strengthening Capital Investment Program

97% of capital request approved (2006-2008)

Total Gross Capital Additions: $5.0 billion authorized vs. $5.15 billion requested

95% of annual operating expense request approved $1.79 billion authorized vs. $1.87 billion requested (CPUC)

2006 authorized operating expense adjusts for 2007 and 2008 escalation SCE will manage operations to authorized revenue level

Increased total annual depreciation to $861 million providing cash flow to support capital requirements

Rate increase is retroactive to January 12, 2006 SCE has filed to retain its current cost of capital for 2007

6 |

|

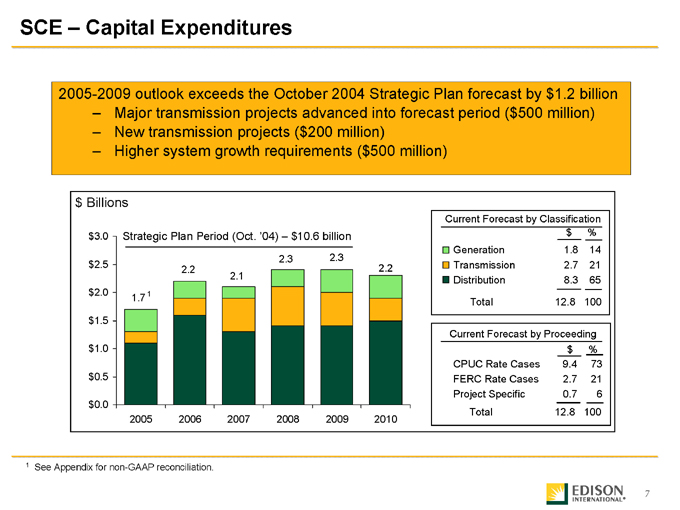

SCE – Capital Expenditures

2005-2009 outlook exceeds the October 2004 Strategic Plan forecast by $1.2 billion

Major transmission projects advanced into forecast period ($500 million) New transmission projects ($200 million) Higher system growth requirements ($500 million) $Billions

Strategic Plan Period (Oct. ’04) – $10.6 billion $3.0 $2.5 $2.0 $1.5 $1.0 $0.5 $0.0

1.7 1

2.2

2.1

2.3

2.3

2.2

2005 2006 2007 2008 2009 2010

Current Forecast by Classification

$ |

| % |

Generation |

| 1.8 14 |

Transmission |

| 2.7 21 |

Distribution |

| 8.3 65 |

Total |

| 12.8 100 |

Current |

| Forecast by Proceeding |

$ |

| % |

CPUC |

| Rate Cases 9.4 73 |

FERC |

| Rate Cases 2.7 21 |

Project |

| Specific 0.7 6 |

Total |

| 12.8 100 |

1 |

| See Appendix for non-GAAP reconciliation. |

7 |

|

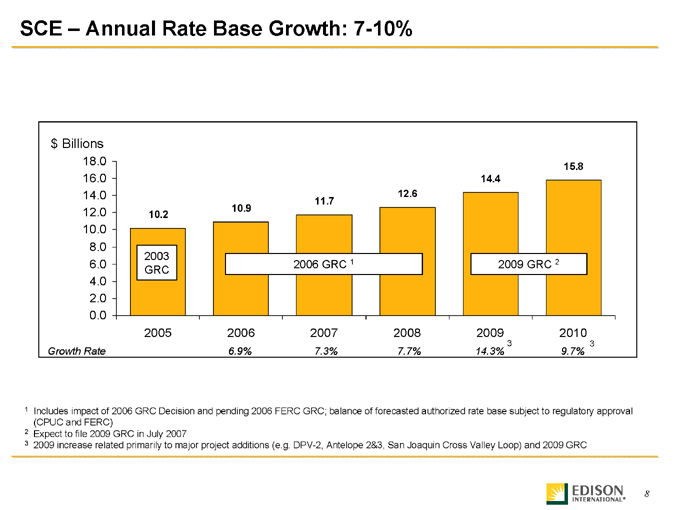

SCE – Annual Rate Base Growth: 7-10% $Billions

18.0 16.0 14.0 12.0 10.0 8.0 6.0 4.0 2.0 0.0

10.2

10.9

11.7

12.6

14.4

15.8

2003 GRC

2006 GRC 1

2009 GRC 2

2005

2006

2007

2008

2009

2010

3 |

| 3 |

Growth Rate 6.9% 7.3% 7.7% 14.3% 9.7%

1 Includes impact of 2006 GRC Decision and pending 2006 FERC GRC; balance of forecasted authorized rate base subject to regulatory approval (CPUC and FERC)

2 |

| Expect to file 2009 GRC in July 2007 |

3 2009 increase related primarily to major project additions (e.g. DPV-2, Antelope 2&3, San Joaquin Cross Valley Loop) and 2009 GRC

8 |

|

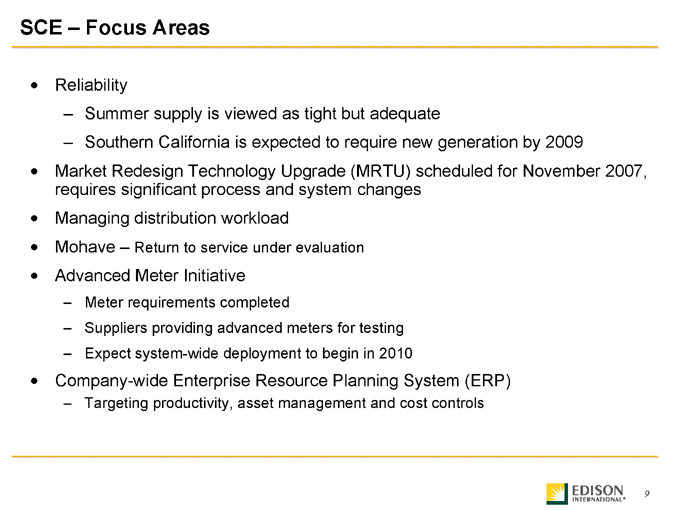

SCE – Focus Areas

Reliability

Summer supply is viewed as tight but adequate

Southern California is expected to require new generation by 2009

Market Redesign Technology Upgrade (MRTU) scheduled for November 2007, requires significant process and system changes Managing distribution workload Mohave – Return to service under evaluation

Advanced Meter Initiative

Meter requirements completed

Suppliers providing advanced meters for testing Expect system-wide deployment to begin in 2010

Company-wide Enterprise Resource Planning System (ERP)

Targeting productivity, asset management and cost controls

9

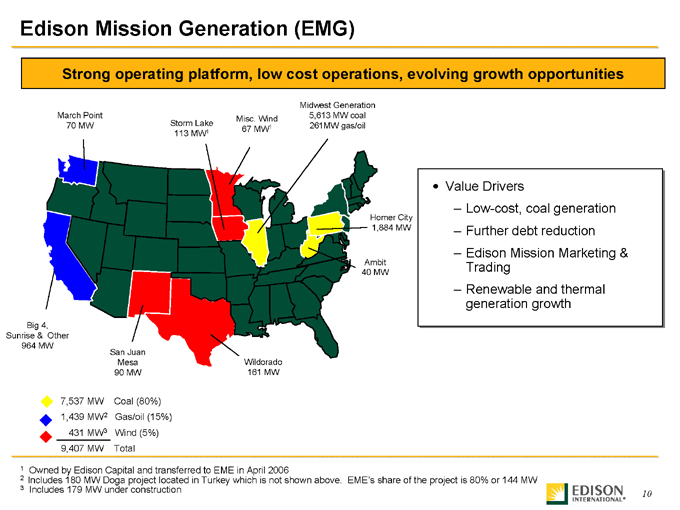

Edison Mission Generation (EMG)

Strong operating platform, low cost operations, evolving growth opportunities

March Point 70 MW

Misc. Wind Storm Lake 67 MW1 113 MW1

Midwest Generation 5,613 MW coal 261MW gas/oil

Big 4, Sunrise & Other 964 MW

San Juan Mesa 90 MW

Wildorado 161 MW

Ambit 40 MW

Homer City 1,884 MW

Value Drivers

Low-cost, coal generation Further debt reduction Edison Mission Marketing & Trading Renewable and thermal generation growth

7,537 MW Coal (80%) 1,439 MW2 Gas/oil (15%) 431 MW3 Wind (5%) 9,407 MW Total

1 |

| Owned by Edison Capital and transferred to EME in April 2006 |

2 |

| Includes 180 MW Doga project located in Turkey which is not shown above. EME’s share of the project is 80% or 144 MW |

3 |

| Includes 179 MW under construction |

10

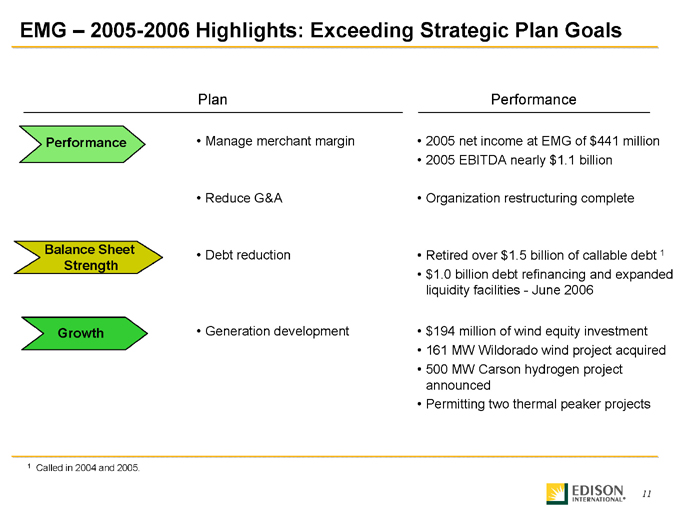

EMG – 2005-2006 Highlights: Exceeding Strategic Plan Goals

Performance

Balance Sheet Strength

Growth

Plan |

| Performance |

• |

| Manage merchant margin • 2005 net income at EMG of $441 million |

• 2005 EBITDA nearly $1.1 billion

• |

| Reduce G&A • Organization restructuring complete |

• |

| Debt reduction • Retired over $1.5 billion of callable debt 1 |

• |

| $1.0 billion debt refinancing and expanded |

liquidity facilities—June 2006

• |

| Generation development • $194 million of wind equity investment |

• 161 MW Wildorado wind project acquired

• 500 MW Carson hydrogen project

announced

• Permitting two thermal peaker projects

1 |

| Called in 2004 and 2005. |

11

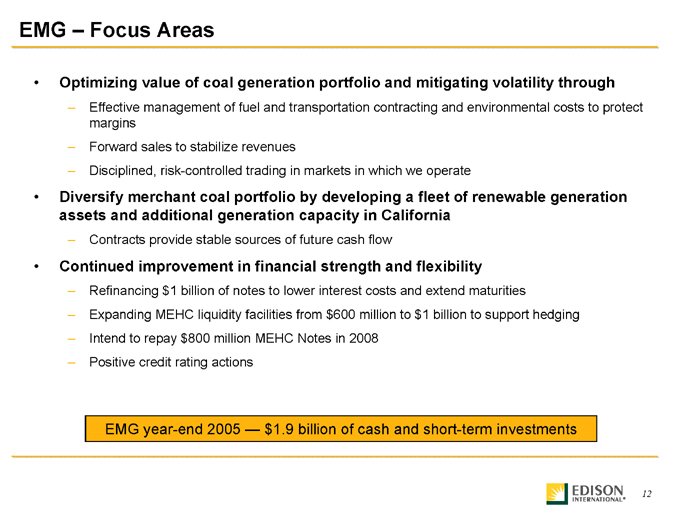

EMG – Focus Areas

Optimizing value of coal generation portfolio and mitigating volatility through

Effective management of fuel and transportation contracting and environmental costs to protect margins

Forward sales to stabilize revenues

Disciplined, risk-controlled trading in markets in which we operate

Diversify merchant coal portfolio by developing a fleet of renewable generation assets and additional generation capacity in California

Contracts provide stable sources of future cash flow

Continued improvement in financial strength and flexibility

Refinancing $1 billion of notes to lower interest costs and extend maturities

Expanding MEHC liquidity facilities from $600 million to $1 billion to support hedging Intend to repay $800 million MEHC Notes in 2008 Positive credit rating actions

EMG year-end 2005 — $1.9 billion of cash and short-term investments

12

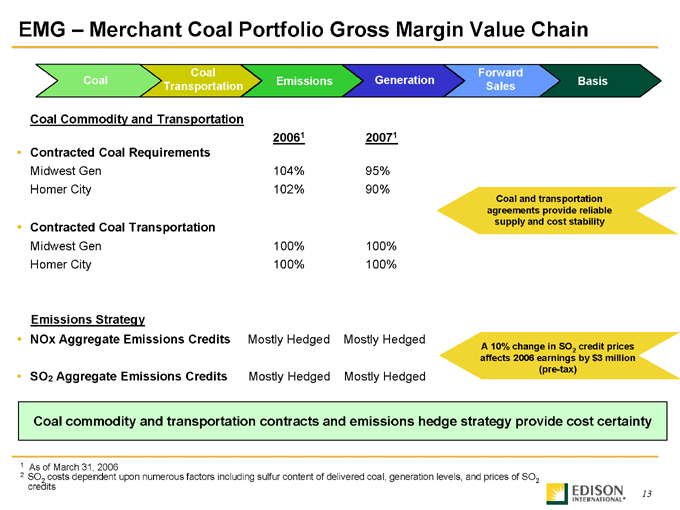

EMG – Merchant Coal Portfolio Gross Margin Value Chain

Coal |

| Coal Transportation Emissions Generation Forward Sales Basis |

Coal |

| Commodity and Transportation |

20061 |

| 20071 |

Contracted |

| Coal Requirements |

Midwest |

| Gen 104% 95% |

Homer |

| City 102% 90% |

Contracted |

| Coal Transportation |

Midwest |

| Gen 100% 100% |

Homer |

| City 100% 100% |

Emissions |

| Strategy |

NOx |

| Aggregate Emissions Credits Mostly Hedged Mostly Hedged |

SO2 |

| Aggregate Emissions Credits Mostly Hedged Mostly Hedged |

Coal and transportation agreements provide reliable supply and cost stability

A 10% change in SO2 credit prices

affects 2006 earnings by $3 million (pre-tax)

Coal commodity and transportation contracts and emissions hedge strategy provide cost certainty

1 |

| As of March 31, 2006 |

2 SO2 costs dependent upon numerous factors including sulfur content of delivered coal, generation levels, and prices of SO2

credits

13

EMG—Merchant Coal Portfolio Gross Margin Value Chain

Coal |

| Coal Transportation Emissions Generation Forward Sales Basis |

Midwest Gen

EAF and CF

100% 80% 60% 40% 20% 0%

2003 2004 2005 YTD 20061

9%

8% 7%

6%

EFOR

5% 4%

3%

2% 1%

0%

EAF

Capacity Factor

EFOR

EAF and CF

Homer City

100% 80% 60% 40% 20% 0%

2 |

|

2003 2004 2005 YTD 20061

25% 20% 15% EFOR

10% 5% 0%

EAF

Capacity Factor

EFOR

Forecast |

| Generation 2006 2007 |

Midwest |

| Gen (TWh) 28.9 29.1 |

Homer |

| City (TWh) 13.0 13.9 |

Superior performance and operational excellence promote availability during highest margin periods

1 |

| YTD through March 31, 2006 |

2 |

| Equivalent Forced Outage Rate (EFOR) increase due to Homer City Unit 3 extended outage |

14

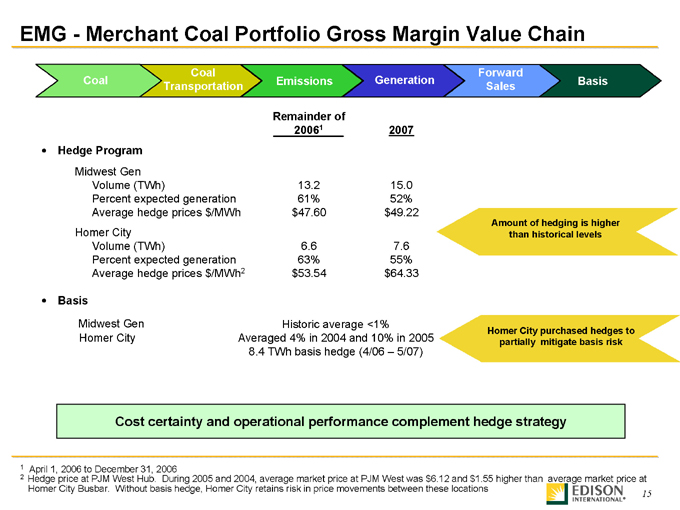

EMG—Merchant Coal Portfolio Gross Margin Value Chain

Coal |

| Coal Transportation Emissions Generation Forward Sales Basis |

Remainder |

| of |

20061 |

| 2007 |

Hedge |

| Program |

Midwest |

| Gen |

Volume |

| (TWh) 13.2 15.0 |

Percent |

| expected generation 61% 52% |

Average |

| hedge prices $/MWh $47.60 $49.22 |

Homer |

| City |

Volume |

| (TWh) 6.6 7.6 |

Percent |

| expected generation 63% 55% |

Average |

| hedge prices $/MWh2 $53.54 $64.33 |

Basis |

|

Midwest |

| Gen Historic average <1% |

Homer |

| City Averaged 4% in 2004 and 10% in 2005 |

8.4 |

| TWh basis hedge (4/06 – 5/07) |

Amount of hedging is higher than historical levels

Homer City purchased hedges to partially mitigate basis risk

Cost certainty and operational performance complement hedge strategy

1 |

| April 1, 2006 to December 31, 2006 |

2 Hedge price at PJM West Hub. During 2005 and 2004, average market price at PJM West was $6.12 and $1.55 higher than average market price at

Homer City Busbar. Without basis hedge, Homer City retains risk in price movements between these locations

15

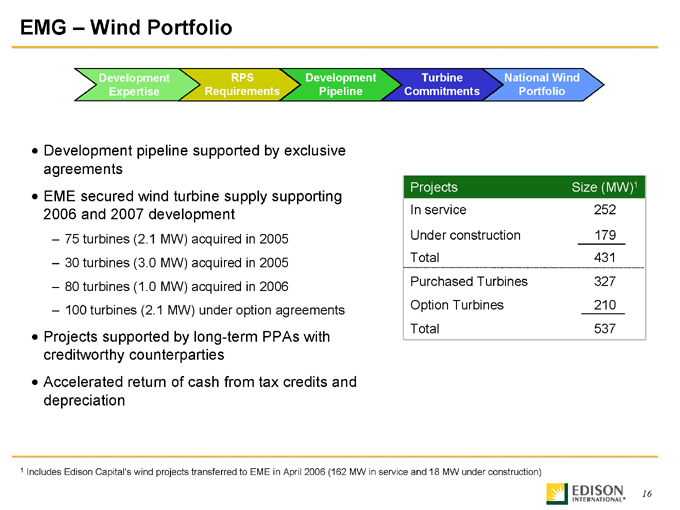

EMG – Wind Portfolio

Development |

| RPS Development Turbine National Wind |

Expertise |

| Requirements Pipeline Commitments Portfolio |

Development pipeline supported by exclusive agreements EME secured wind turbine supply supporting 2006 and 2007 development

75 turbines (2.1 MW) acquired in 2005 30 turbines (3.0 MW) acquired in 2005 80 turbines (1.0 MW) acquired in 2006

100 turbines (2.1 MW) under option agreements

Projects supported by long-term PPAs with creditworthy counterparties Accelerated return of cash from tax credits and depreciation

Projects |

| Size (MW)1 |

In |

| service 252 |

Under |

| construction 179 |

Total |

| 431 |

Purchased |

| Turbines 327 |

Option |

| Turbines 210 |

Total |

| 537 |

1 Includes Edison Capital’s wind projects transferred to EME in April 2006 (162 MW in service and 18 MW under construction)

16

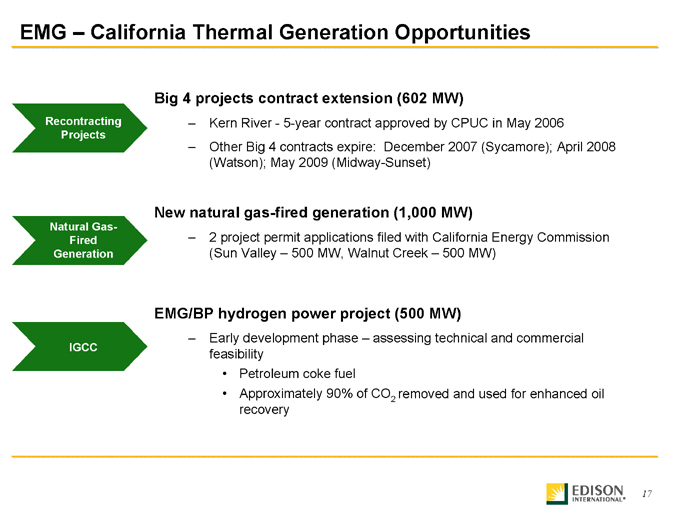

EMG – California Thermal Generation Opportunities

Recontracting Projects

Big 4 projects contract extension (602 MW)

Kern River—5-year contract approved by CPUC in May 2006

Other Big 4 contracts expire: December 2007 (Sycamore); April 2008 (Watson); May 2009 (Midway-Sunset)

Natural Gas-Fired Generation

New natural gas-fired generation (1,000 MW)

2 |

| project permit applications filed with California Energy Commission (Sun Valley – 500 MW, Walnut Creek – 500 MW) |

IGCC

EMG/BP hydrogen power project (500 MW)

Early development phase – assessing technical and commercial feasibility

Petroleum coke fuel

Approximately 90% of CO2 removed and used for enhanced oil

recovery

17

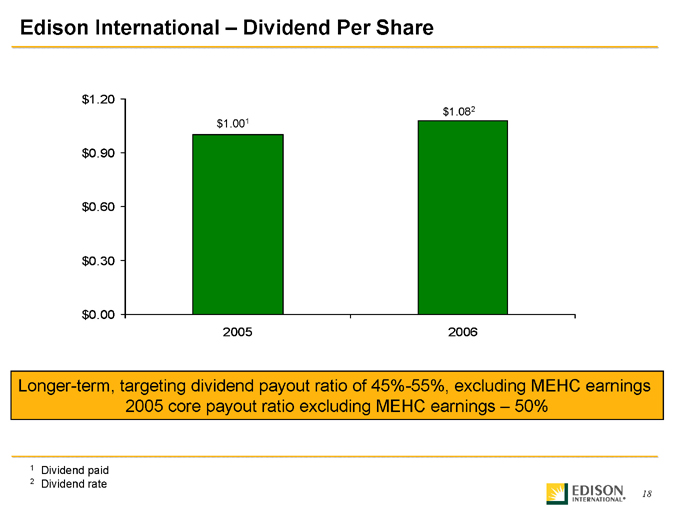

Edison International – Dividend Per Share $1.20 $0.90 $0.60 $0.30 $0.00 $1.001 $1.082

2005

2006

Longer-term, targeting dividend payout ratio of 45%-55%, excluding MEHC earnings 2005 core payout ratio excluding MEHC earnings – 50%

1 |

| Dividend paid |

2 |

| Dividend rate |

18

Appendix

19

Edison International – Organizational Structure (1)

Edison International

Credit Rating (2) BBB / Baa3

Total |

| Assets $34.7 B |

Generation |

| (3) 14,441 MW |

Edison Mission Group

Southern California Edison

Credit Rating (2) BBB+ / A3

Operating |

| Statistics: |

Total |

| Assets $24.8 B |

Customers |

| 4.8 M |

Total |

| Debt (4) 5.5 B |

Mission Energy Holding Company

Credit Rating (2) B- / B2

B+ / Ba3 (EME)

Operating |

| Statistics: |

Total |

| Assets $6.7 B |

Total |

| MWs Owned (3) 9,227 |

Coal |

| Generation MWs 7,537 |

Total |

| Debt (4) $4.0 B |

Edison Capital

Credit Rating (2) BB+ / Ba1

Operating |

| Statistics: |

Total |

| Assets $3.6 B |

Total |

| MWs Owned (3) 180 |

Total |

| Investments $2.7 B |

Total |

| Debt (4) $0.3 B |

1) As of March 31, 2006.

2) Represents S&P and Moody’s ratings: SCE and MEHC Senior Secured debt, EC Senior Unsecured debt, and EME corporate as of May 15, 2006; EIX corporate credit rating (S&P) and Senior Unsecured shelf rating (Moody’s) as of May 15, 2006.

3) Includes 179 MW under construction; 161 MW at MEHC & 18 MW at Edison Capital.

4) Includes short-term, long-term, and current portion of long-term debt; non-recourse debt; and intercompany debt of $27 million, $78 million and $75 million at SCE, MEHC and Edison Capital respectively.

20

Appendix

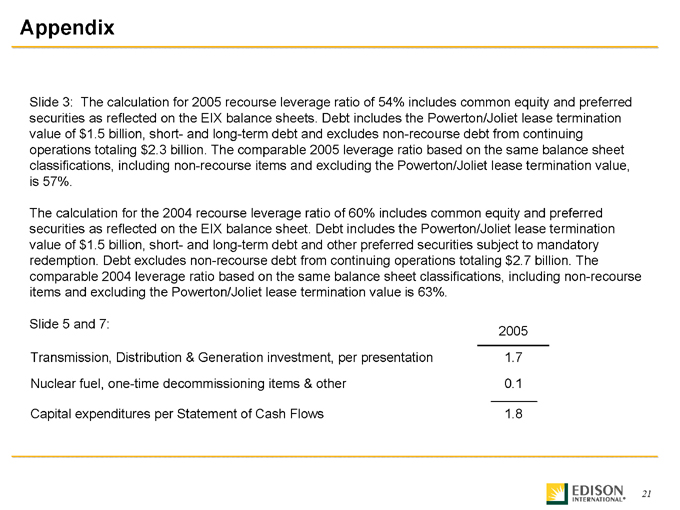

Slide 3: The calculation for 2005 recourse leverage ratio of 54% includes common equity and preferred securities as reflected on the EIX balance sheets. Debt includes the Powerton/Joliet lease termination value of $1.5 billion, short- and long-term debt and excludes non-recourse debt from continuing operations totaling $2.3 billion. The comparable 2005 leverage ratio based on the same balance sheet classifications, including non-recourse items and excluding the Powerton/Joliet lease termination value, is 57%.

The calculation for the 2004 recourse leverage ratio of 60% includes common equity and preferred securities as reflected on the EIX balance sheet. Debt includes the Powerton/Joliet lease termination value of $1.5 billion, short- and long-term debt and other preferred securities subject to mandatory redemption. Debt excludes non-recourse debt from continuing operations totaling $2.7 billion. The comparable 2004 leverage ratio based on the same balance sheet classifications, including non-recourse items and excluding the Powerton/Joliet lease termination value is 63%.

Slide |

| 5 and 7: |

2005

Transmission, |

| Distribution & Generation investment, per presentation 1.7 |

Nuclear |

| fuel, one-time decommissioning items & other 0.1 |

Capital |

| expenditures per Statement of Cash Flows 1.8 |

21

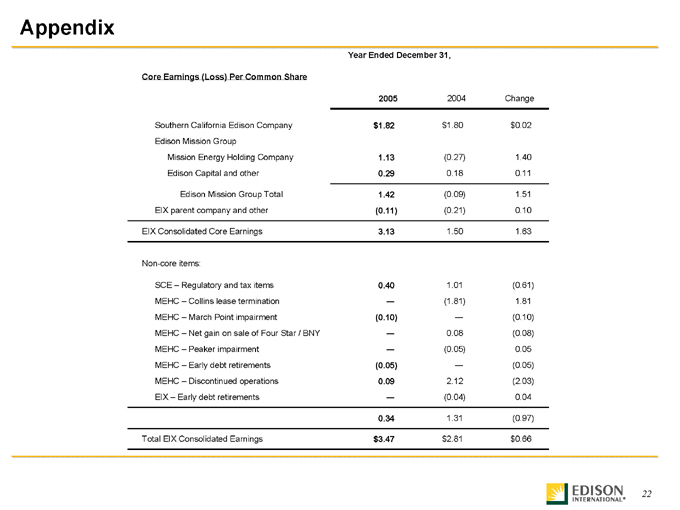

Appendix

Year |

| Ended December 31, |

Core |

| Earnings (Loss) Per Common Share |

2005 |

| 2004 Change |

Southern |

| California Edison Company $1.82 $1.80 $0.02 |

Edison |

| Mission Group |

Mission |

| Energy Holding Company 1.13 (0.27) 1.40 |

Edison |

| Capital and other 0.29 0.18 0.11 |

Edison |

| Mission Group Total 1.42 (0.09) 1.51 |

EIX |

| parent company and other (0.11) (0.21) 0.10 |

EIX |

| Consolidated Core Earnings 3.13 1.50 1.63 |

Non-core |

| items: |

SCE |

| – Regulatory and tax items 0.40 1.01 (0.61) |

MEHC |

| – Collins lease termination ? (1.81) 1.81 |

MEHC |

| – March Point impairment (0.10) ? (0.10) |

MEHC |

| – Net gain on sale of Four Star / BNY ? 0.08 (0.08) |

MEHC |

| – Peaker impairment ? (0.05) 0.05 |

MEHC |

| – Early debt retirements (0.05) ? (0.05) |

MEHC |

| – Discontinued operations 0.09 2.12 (2.03) |

EIX |

| – Early debt retirements ? (0.04) 0.04 |

0.34 |

| 1.31 (0.97) |

Total |

| EIX Consolidated Earnings $3.47 $2.81 $0.66 |

22

Appendix

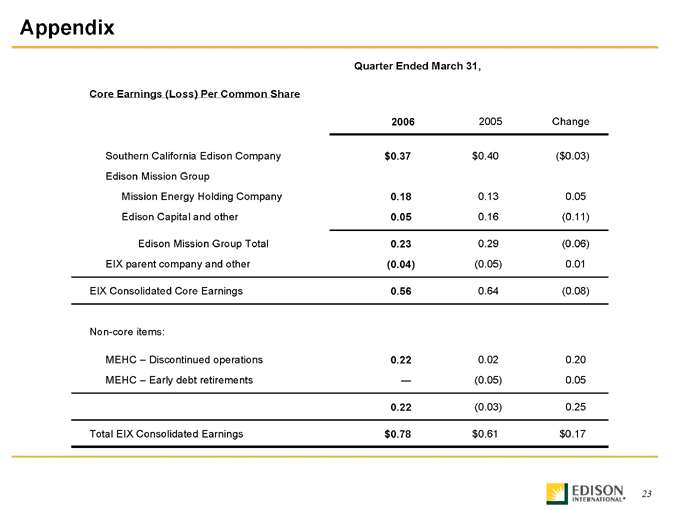

Quarter Ended March 31,

Core |

| Earnings (Loss) Per Common Share |

2006 |

| 2005 Change |

Southern |

| California Edison Company $0.37 $0.40 ($0.03) |

Edison |

| Mission Group |

Mission |

| Energy Holding Company 0.18 0.13 0.05 |

Edison |

| Capital and other 0.05 0.16 (0.11) |

Edison |

| Mission Group Total 0.23 0.29 (0.06) |

EIX |

| parent company and other (0.04) (0.05) 0.01 |

EIX |

| Consolidated Core Earnings 0.56 0.64 (0.08) |

Non-core |

| items: |

MEHC |

| – Discontinued operations 0.22 0.02 0.20 |

MEHC |

| – Early debt retirements ? (0.05) 0.05 |

0.22 |

| (0.03) 0.25 |

Total |

| EIX Consolidated Earnings $0.78 $0.61 $0.17 |

23

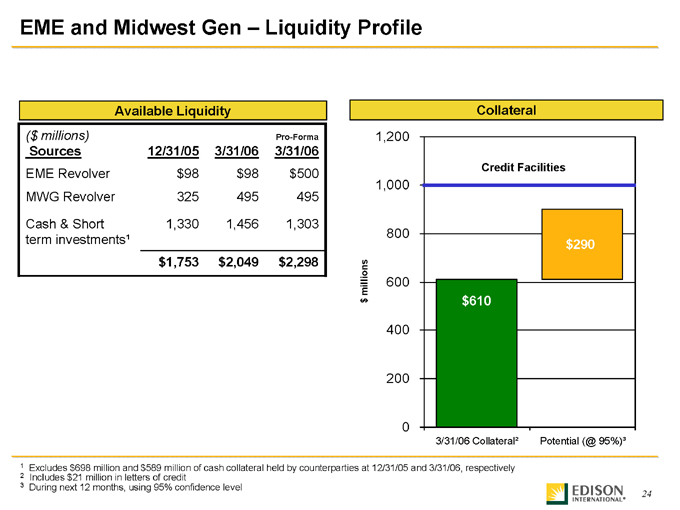

EME and Midwest Gen – Liquidity Profile

Available Liquidity

($millions) |

| Pro-Forma |

Sources |

| 12/31/05 3/31/06 3/31/06 |

EME |

| Revolver $98 $98 $500 |

MWG |

| Revolver 325 495 495 |

Cash |

| & Short 1,330 1,456 1,303 |

term |

| investments¹ |

$1,753 |

| $2,049 $2,298 |

Collateral $ millions

1,200 1,000 800 600 400 200 0

Credit Facilities $610

3/31/06 Collateral² $290

Potential (@ 95%)³

1 Excludes $698 million and $589 million of cash collateral held by counterparties at 12/31/05 and 3/31/06, respectively

2 |

| Includes $21 million in letters of credit |

3 |

| During next 12 months, using 95% confidence level |

24

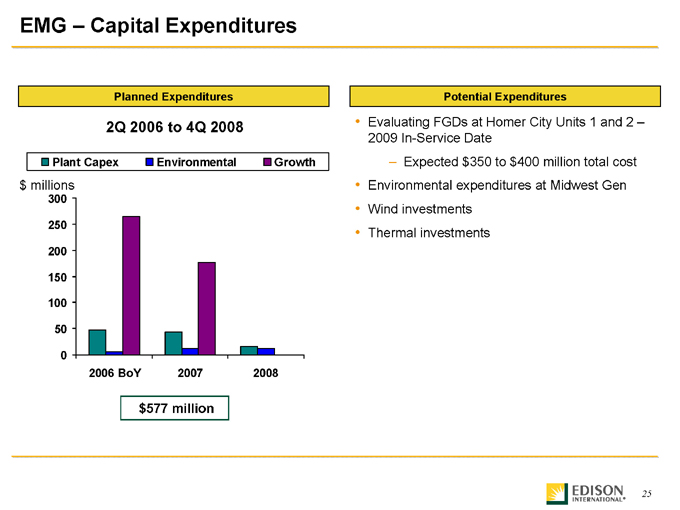

EMG – Capital Expenditures

Planned Expenditures

2Q 2006 to 4Q 2008

Plant Capex

Environmental

Growth $millions

300 250 200 150 100 50 0

2006 BoY 2007 2008

$577 million

Potential Expenditures

Evaluating FGDs at Homer City Units 1 and 2 –2009 In-Service Date

Expected $350 to $400 million total cost

Environmental expenditures at Midwest Gen Wind investments Thermal investments

25