Exhibit 99.1

Business Update

August 2006

Forward-Looking Statement

This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements reflect Edison

International’s current expectations and projections about future events based on Edison International’s knowledge of present facts and circumstances and assumptions about future

events and include any statement that does not directly relate to a historical or current fact. In this presentation and elsewhere, the words “expects,” “believes,” “anticipates,”

“estimates,” “projects,” “intends,” “plans,” “probable,” “may,” “will,” “could,” “would,” “should,” and variations of such words and similar expressions, or discussions of strategy or of

plans, are intended to identify forward-looking statements. Such statements necessarily involve risks and uncertainties that could cause actual results to differ materially from those

anticipated. Some of the risks, uncertainties and other important factors that could cause results to differ, or that otherwise could impact Edison International or its subsidiaries,

include but are not limited to:

• the ability of Edison International to meet its financial obligations and to pay dividends on its common stock if its subsidiaries are unable to pay dividends;

• the ability of Southern California Edison (SCE) to recover its costs in a timely manner from its customers through regulated rates;

• decisions and other actions by the California Public Utilities Commission (CPUC) and other regulatory authorities and delays in regulatory actions;

• market risks affecting SCE’s energy procurement activities;

• access to capital markets and the cost of capital;

• changes in interest rates, rates of inflation and foreign exchange rates;

• governmental, statutory, regulatory or administrative changes or initiatives affecting the electricity industry, including the market structure rules applicable to each market

and environmental regulations that could require additional expenditures or otherwise affect the cost and manner of doing business;

• risks associated with operating nuclear and other power generating facilities, including operating risks, nuclear fuel storage, equipment failure, availability, heat rate and

output;

• the availability of labor, equipment and materials;

• the ability to obtain sufficient insurance, including insurance relating to SCE’s nuclear facilities;

• effects of legal proceedings, changes in or interpretations of tax laws, rates or policies, and changes in accounting standards;

• supply and demand for electric capacity and energy, and the resulting prices and dispatch volumes, in the wholesale markets to which MEHC generating units have

access;

• the cost and availability of coal, natural gas, and fuel oil, nuclear fuel, and associated transportation;

• the cost and availability of emission credits or allowances for emission credits;

• transmission congestion in and to each market area and the resulting differences in prices between delivery points;

• the ability to provide sufficient collateral in support of hedging activities and purchased power and fuel;

• the extent of additional supplies of capacity, energy and ancillary services from current competitors or new market entrants, including the development of new generation

facilities and technologies;

• the difficulty of predicting wholesale prices, transmission congestion, energy demand, and other activities in the complex and volatile markets in which MEHC and its

subsidiaries participate;

• general political, economic and business conditions;

• weather conditions, natural disasters and other unforeseen events; and

• changes in the fair value of investments and other assets accounted for using fair value accounting.

Additional information about risks and uncertainties, including more detail about the factors described above, is contained in Edison International’s reports filed with the Securities and Exchange Commission. Readers are urged to read such reports and carefully consider the risks, uncertainties and other factors that affect Edison International’s business.

Readers also should review future reports filed by Edison International with the Securities and Exchange Commission. The information contained in this presentation is subject to change without notice. Forward-looking statements speak only as of the date they are made and Edison International is not obligated to publicly update or revise forward-looking statements.

1

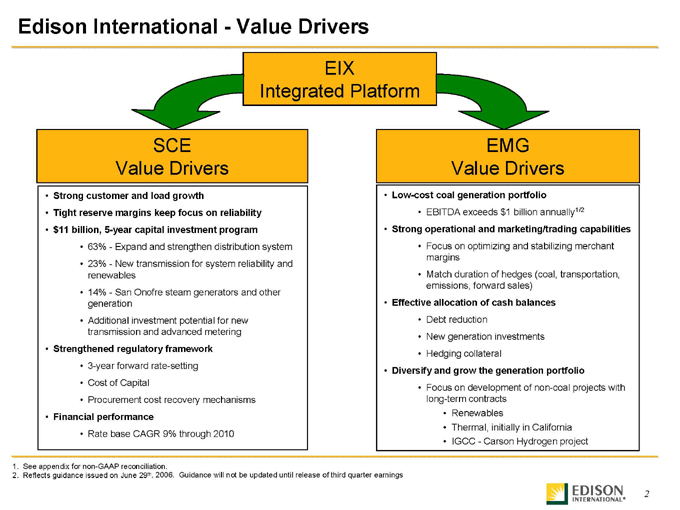

Edison International—Value Drivers

EIX

Integrated Platform

SCE

Value Drivers

Strong customer and load growth

• Tight reserve margins keep focus on reliability

• $11 billion, 5-year capital investment program

• 63%—Expand and strengthen distribution system

• 23%—New transmission for system reliability and

renewables

• 14%—San Onofre steam generators and other

generation

• Additional investment potential for new

transmission and advanced metering

• Strengthened regulatory framework

• 3-year forward rate-setting

• Cost of Capital

• Procurement cost recovery mechanisms

• Financial performance

• Rate base CAGR 9% through 2010

EMG

Value Drivers

• Low-cost coal generation portfolio

• EBITDA exceeds $1 billion annually1/2

• Strong operational and marketing/trading capabilities

• Focus on optimizing and stabilizing merchant

margins

• Match duration of hedges (coal, transportation,

emissions, forward sales)

• Effective allocation of cash balances

• Debt reduction

• New generation investments

• Hedging collateral

• Diversify and grow the generation portfolio

• Focus on development of non-coal projects with

long-term contracts

• Renewables

• Thermal, initially in California

• IGCC—Carson Hydrogen project

1. See appendix for non-GAAP reconciliation.

2. Reflects guidance issued on June 29th, 2006. Guidance will not be updated until release of third quarter earnings

2

System

Growth

Capital

Investment

Execution Regulatory

Framework

Dependable

Earnings

Southern California Edison (SCE)

Capital

Investment

3

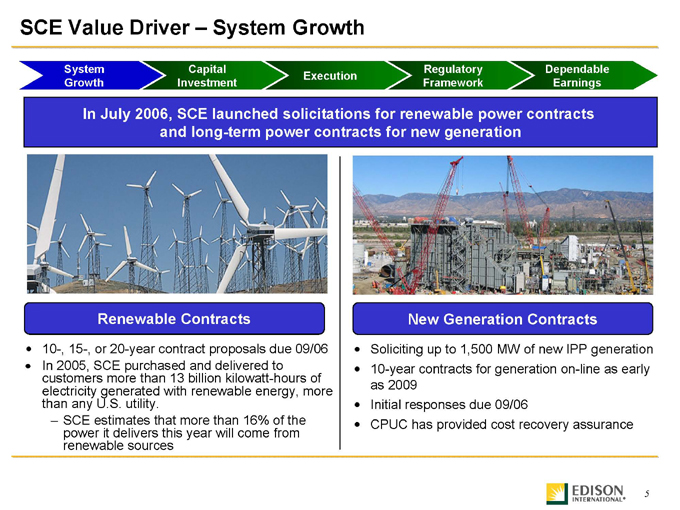

SCE Value Driver – System Growth

System

Growth

Capital

Investment

Execution Regulatory

Framework

Dependable

Earnings

Strong customer and load growth keeps statewide focus on the need to

expand and strengthen the utility infrastructure

SCE Growth 1

88,321 83,979

77,437

73,204

63,463 63,021

50,000

60,000

70,000

80,000

90,000

2001 2002 2003 2004 2005 2006

New Meter Connections

Peak Demand

10,000

14,000

18,000

22,000

26,000

17,890 18,821

20,136 20,762

21,934 22,889

2001 2002 2003 2004 2005 2006

SCE’s service territory has

– 4 of the 10 fastest growing counties in

the nation 2

– 5 of the 25 fastest growing cities in the

nation 3

• New meter connections

– Expect to exceed 88,000 in 2006

– 360,000 meters added in the past 5

years

• Peak demand

– In July 2006 Peak Demand reached

22,889 MW

• 4.4% growth from 2005 peak

• 10.2% higher than 2004 peak

1. 2006 figures projected for full-year.

2. LA, Riverside, San Bernardino and Orange counties. US Census Bureau data, in terms of population increase between 2000 and 2005.

3. Moreno Valley, Rancho Cucamonga, Irvine, Lancaster and Fontana. US Census Bureau data, in terms of population increase between 2004 and 2005.

4 |

|

SCE Value Driver – System Growth

Capital

Investment

System

Growth Execution Regulatory

Framework

Dependable

Earnings

In July 2006, SCE launched solicitations for renewable power contracts

and long-term power contracts for new generation

Renewable Contracts

• 10-, 15-, or 20-year contract proposals due 09/06

??In 2005, SCE purchased and delivered to

customers more than 13 billion kilowatt-hours of

electricity generated with renewable energy, more

than any U.S. utility.

??SCE estimates that more than 16% of the

power it delivers this year will come from

renewable sources

New Generation Contracts

Soliciting up to 1,500 MW of new IPP generation

• 10-year contracts for generation on-line as early

as 2009

• Initial responses due 09/06

• CPUC has provided cost recovery assurance

5

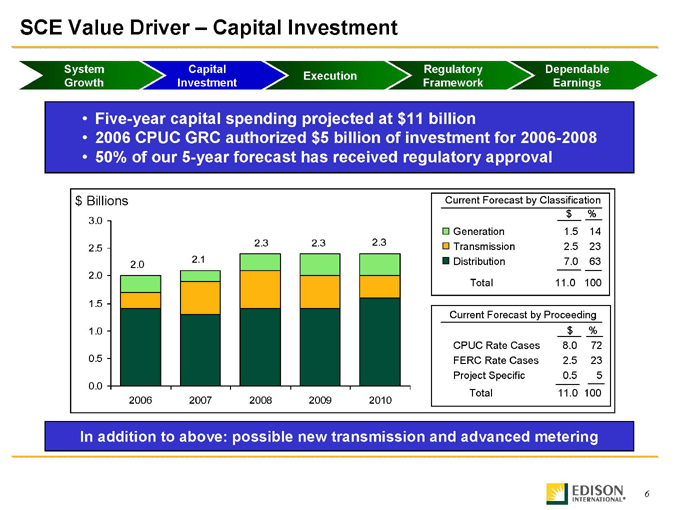

SCE Value Driver – Capital Investment

2.3 2.3 2.3

2.1 2.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2006 2007 2008 2009 2010

Current Forecast by Classification

$ %

Current Forecast by Proceeding

$ Billions

$ %

Generation 1.5 14

Transmission 2.5 23

Distribution 7.0 63

CPUC Rate Cases 8.0 72

FERC Rate Cases 2.5 23

Project Specific 0.5 5

Total 11.0 100

Total 11.0 100

• Five-year capital spending projected at $11 billion

• 2006 CPUC GRC authorized $5 billion of investment for 2006-2008

• 50% of our 5-year forecast has received regulatory approval

In addition to above: possible new transmission and advanced metering

Capital

Investment

System

Growth Execution Regulatory

Framework

Dependable

Earnings

Five-year capital spending projected at $11 billion

• 2006 CPUC GRC authorized $5 billion of investment for 2006-2008

• 50% of our 5-year forecast has received regulatory approval

6

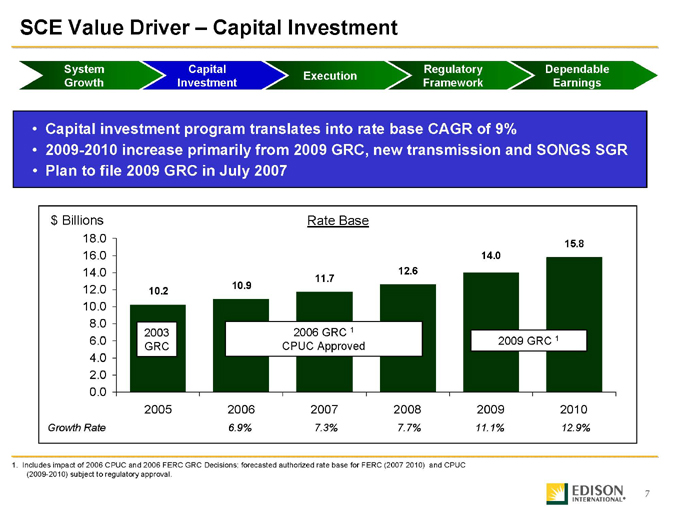

SCE Value Driver – Capital Investment

• Capital investment program translates into rate base CAGR of 9%

• 2009-2010 increase primarily from 2009 GRC, new transmission and SONGS SGR

• Plan to file 2009 GRC in July 2007

1. Includes impact of 2006 CPUC and 2006 FERC GRC Decisions; forecasted authorized rate base for FERC (2007 2010) and CPUC

(2009-2010) subject to regulatory approval.

14.0

15.8

12.6

11.7 10.9 10.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

2005 2006 2007 2008 2009 2010

2003

GRC

2006 GRC 1

CPUC Approved 2009 GRC 1

Growth Rate 6.9% 7.3% 7.7% 11.1% 12.9%

$ Billions Rate Base

Capital

Investment

System

Growth Execution Regulatory

Framework

Dependable

Earnings

7

8

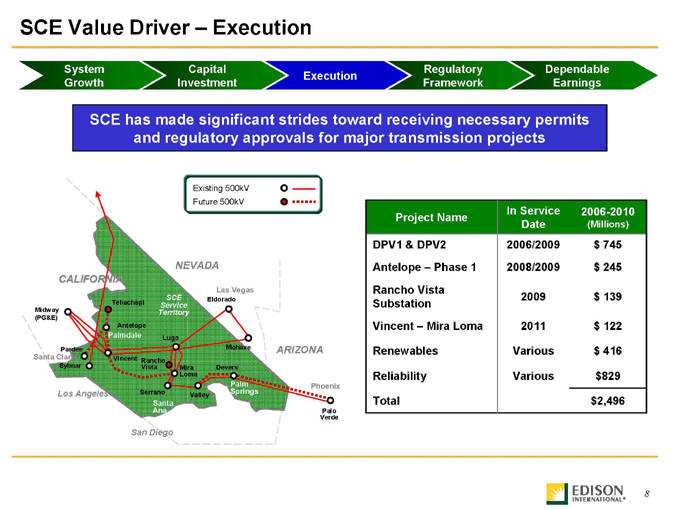

SCE Value Driver – Execution

SCE has made significant strides toward receiving necessary permits

and regulatory approvals for major transmission projects

$829 Various Reliability

$2,496 Total

$ 416 Various Renewables

$ 122 2011 Vincent – Mira Loma

$ 745 2006/2009 DPV1 & DPV2

$ 139

$ 245

2006-2010

(Millions)

2008/2009 Antelope – Phase 1

2009 Rancho Vista

Substation

In Service

Date Project Name

Las Vegas

Existing 500kV

Future 500kV

Midway

(PG&E)

CALIFORNIA

Los Angeles

Sylmar

Lugo

Mohave

Palo

Verde

Vincent

ARIZONA

San Diego

NEVADA

Eldorado

Pardee

Tehachapi

Antelope

Palmdale

Santa

Ana

SCE

Service

Territory

Phoenix

Santa Clarita

Serrano Valley

Mira

Loma

Devers

Rancho

Vista

Palm

Springs

Capital

Investment

System

Growth Execution Regulatory

Framework

Dependable

Earnings

9

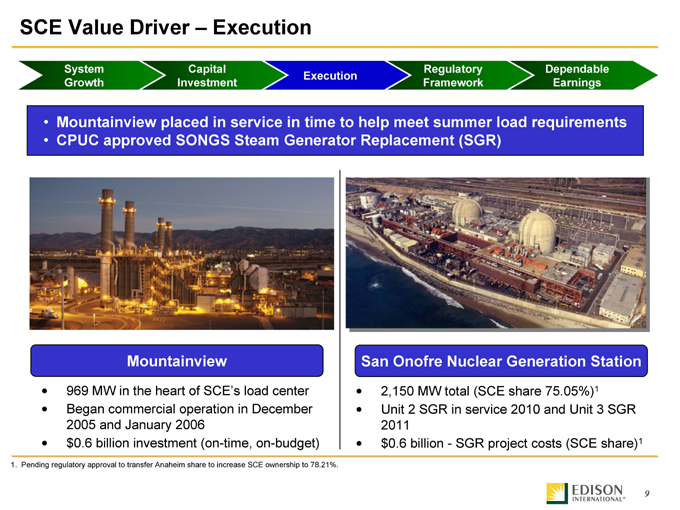

SCE Value Driver – Execution

San Onofre Nuclear Generation Station Mountainview

• Mountainview placed in service in time to help meet summer load requirements

• CPUC approved SONGS Steam Generator Replacement (SGR)

• 969 MW in the heart of SCE’s load center

• Began commercial operation in December

2005 and January 2006

• $0.6 billion investment (on-time, on-budget)

• 2,150 MW total (SCE share 75.05%)1

• Unit 2 SGR in service 2010 and Unit 3 SGR

2011

• $0.6 billion—SGR project costs (SCE share)1

1. Pending regulatory approval to transfer Anaheim share to increase SCE ownership to 78.21%.

Capital

Investment

System

Growth Execution Regulatory

Framework

Dependable

Earnings

10

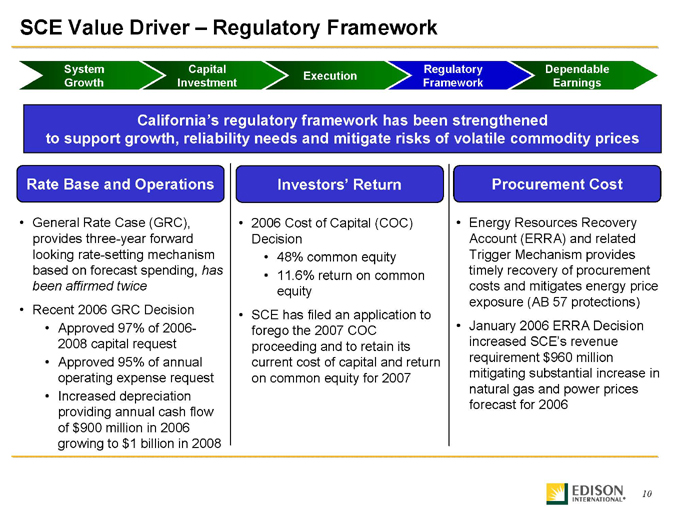

SCE Value Driver – Regulatory Framework

California’s regulatory framework has been strengthened

to support growth, reliability needs and mitigate risks of volatile commodity prices

• 2006 Cost of Capital (COC)

Decision

• 48% common equity

• 11.6% return on common

equity

• SCE has filed an application to

forego the 2007 COC

proceeding and to retain its

current cost of capital and return

on common equity for 2007

Investors’ Return

• General Rate Case (GRC),

provides three-year forward

looking rate-setting mechanism

based on forecast spending, has

been affirmed twice

• Recent 2006 GRC Decision

• Approved 97% of 2006-

2008 capital request

• Approved 95% of annual

operating expense request

• Increased depreciation

providing annual cash flow

of $900 million in 2006

growing to $1 billion in 2008

Rate Base and Operations

• Energy Resources Recovery

Account (ERRA) and related

Trigger Mechanism provides

timely recovery of procurement

costs and mitigates energy price

exposure (AB 57 protections)

• January 2006 ERRA Decision

increased SCE’s revenue

requirement $960 million

mitigating substantial increase in

natural gas and power prices

forecast for 2006

Procurement Cost

Capital

Investment

System

Growth Execution Regulatory

Framework

Dependable

Earnings

11

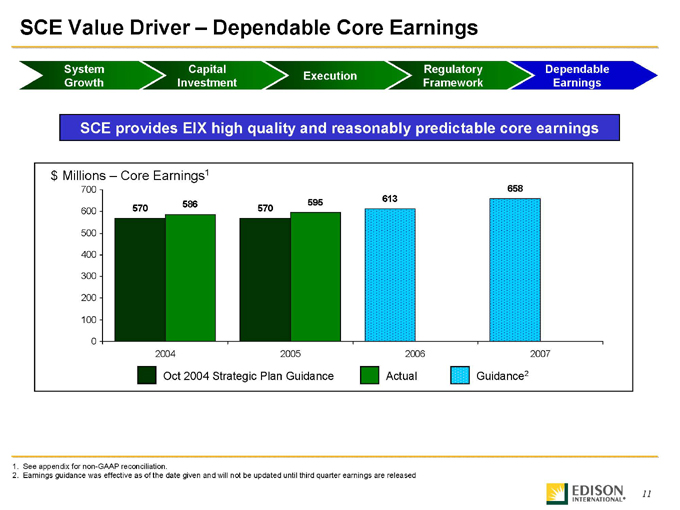

SCE Value Driver – Dependable Core Earnings

570 570

613

658

586 595

0

100

200

300

400

500

600

700

2004 2005 2006 2007

$ Millions – Core Earnings1

Oct 2004 Strategic Plan Guidance Actual Guidance2

SCE provides EIX high quality and reasonably predictable core earnings

1. See appendix for non-GAAP reconciliation.

2. Earnings guidance was effective as of the date given and will not be updated until third quarter earnings are released

Capital

Investment

System

Growth Execution Regulatory

Framework

Dependable

Earnings

12

Edison Mission Group (EMG)

Operational/Marketing/

Trading Capabilities

Low-Cost

Coal

Cash

Position

Growth

Opportunities

13

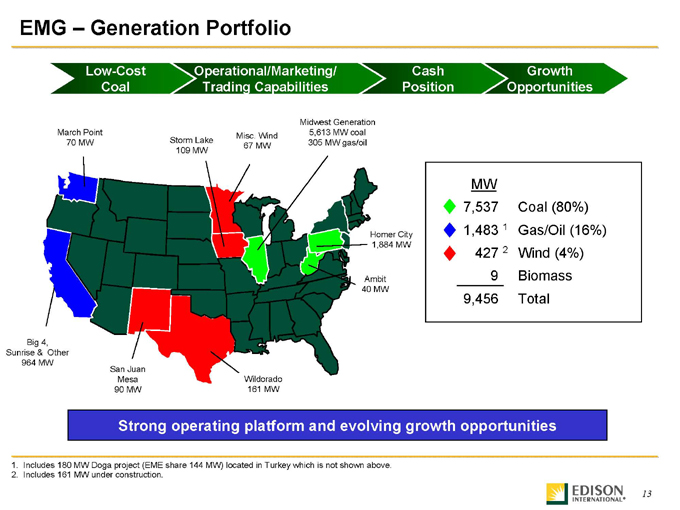

EMG – Generation Portfolio

Wildorado

161 MW

Homer City

1,884 MW

Midwest Generation

5,613 MW coal

305 MW gas/oil

March Point

70 MW

Big 4,

Sunrise & Other

964 MW

San Juan

Mesa

90 MW

Storm Lake

109 MW

Misc. Wind

67 MW

Ambit

40 MW

Strong operating platform and evolving growth opportunities

Operational/Marketing/

Trading Capabilities

Low-Cost

Coal

Cash

Position

Growth

Opportunities

MW

7,537 Coal (80%)

1,483 1 Gas/Oil (16%)

427 2 Wind (4%)

9 Biomass

9,456 Total

1. Includes 180 MW Doga project (EME share 144 MW) located in Turkey which is not shown above.

2. Includes 161 MW under construction.

14

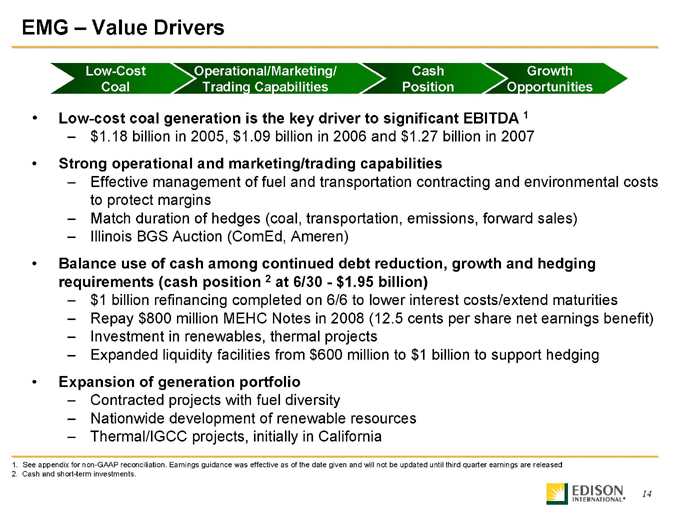

• Low-cost coal generation is the key driver to significant EBITDA 1

– $1.18 billion in 2005, $1.09 billion in 2006 and $1.27 billion in 2007

• Strong operational and marketing/trading capabilities

– Effective management of fuel and transportation contracting and environmental costs

to protect margins

– Match duration of hedges (coal, transportation, emissions, forward sales)

– Illinois BGS Auction (ComEd, Ameren)

• Balance use of cash among continued debt reduction, growth and hedging

requirements (cash position 2 at 6/30—$1.95 billion)

– $1 billion refinancing completed on 6/6 to lower interest costs/extend maturities

– Repay $800 million MEHC Notes in 2008 (12.5 cents per share net earnings benefit)

– Investment in renewables, thermal projects

– Expanded liquidity facilities from $600 million to $1 billion to support hedging

• Expansion of generation portfolio

– Contracted projects with fuel diversity

– Nationwide development of renewable resources

– Thermal/IGCC projects, initially in California

EMG – Value Drivers

1. See appendix for non-GAAP reconciliation. Earnings guidance was effective as of the date given and will not be updated until third quarter earnings are released

Operational/Marketing/

Trading Capabilities

Low-Cost

Coal

Cash

Position

Growth

Opportunities

2. Cash and short-term investments.

15

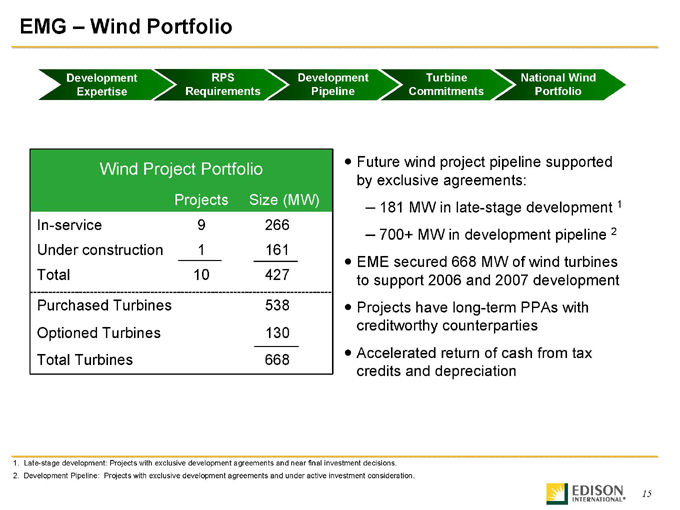

EMG – Wind Portfolio

• Future wind project pipeline supported

by exclusive agreements:

– 181 MW in late-stage development 1

– 700+ MW in development pipeline 2

• EME secured 668 MW of wind turbines

to support 2006 and 2007 development

• Projects have long-term PPAs with

creditworthy counterparties

• Accelerated return of cash from tax

credits and depreciation

RPS

Requirements

Development

Expertise

Development

Pipeline

Turbine

Commitments

National Wind

Portfolio

1. Late-stage development: Projects with exclusive development agreements and near final investment decisions.

2. Development Pipeline: Projects with exclusive development agreements and under active investment consideration.

130 Optioned Turbines

668 Total Turbines

538 Purchased Turbines

427 10 Total

161 1 Under construction

266 9 In-service

Size (MW) Projects

Wind Project Portfolio

16

EMG – California Thermal Generation Opportunities

Natural Gas-

Fired

Generation

Recontracting

Projects

IGCC

• Big 4 projects contract extension (602 MW)

– Kern River—5-year market-rate contract approved by

CPUC in May 2006

– Other Big 4 contracts expire: December 2007

(Sycamore); April 2008 (Watson); May 2009 (Midway-

Sunset)

• New natural gas-fired generation (1,000 MW)

– 2 project permit applications filed with California Energy

Commission (Sun Valley – 500 MW, Walnut Creek – 500

MW)

– Intend to bid into SCE RFO (Sept 2006)

• EMG/BP hydrogen power project (500 MW)

– Conducting engineering studies

• Petroleum coke fuel with approximately 90% of CO2 removed

and used for enhanced oil recovery

• Submitted DOE application for gasification tax credits

17

Year to Date Performance

through June 30, 2006

Balance Sheet

Strength Performance Growth Dividends Shareholder

Returns

18

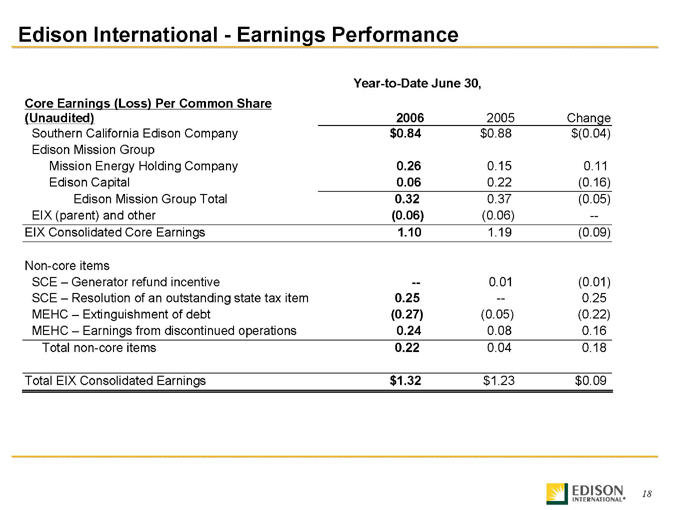

Edison International—Earnings Performance

Year-to-Date June 30,

Core Earnings (Loss) Per Common Share

(Unaudited)

2006 2005 Change

Southern California Edison Company $0.84 $0.88 $(0.04)

Edison Mission Group

Mission Energy Holding Company 0.26 0.15 0.11

Edison Capital 0.06 0.22 (0.16)

Edison Mission Group Total 0.32 0.37 (0.05)

EIX (parent) and other (0.06) (0.06) —

EIX Consolidated Core Earnings 1.10 1.19 (0.09)

Non-core items

SCE – Generator refund incentive — 0.01 (0.01)

SCE – Resolution of an outstanding state tax item 0.25 — 0.25

MEHC – Extinguishment of debt (0.27) (0.05) (0.22)

MEHC – Earnings from discontinued operations 0.24 0.08 0.16

Total non-core items 0.22 0.04 0.18

Total EIX Consolidated Earnings $1.32 $1.23 $0.09

19

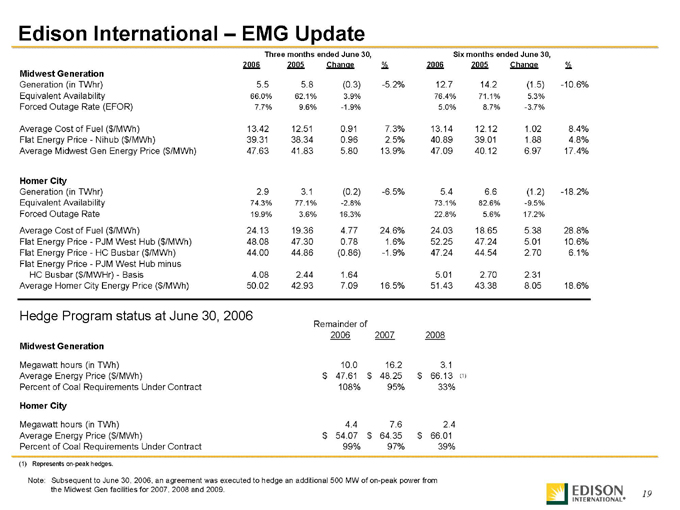

Three months ended June 30, Six months ended June 30,

2006 2005 Change % 2006 2005 Change %

Midwest Generation

Generation (in TWhr) 5.5 5.8 (0.3) -5.2% 12.7 14.2 (1.5) -10.6%

Equivalent Availability 66.0% 62.1% 3.9% 76.4% 71.1% 5.3%

Forced Outage Rate (EFOR) 7.7% 9.6% -1.9% 5.0% 8.7% -3.7%

Average Cost of Fuel ($/MWh) 13.42 12.51 0.91 7.3% 13.14 12.12 1.02 8.4%

Flat Energy Price—Nihub ($/MWh) 39.31 38.34 0.96 2.5% 40.89 39.01 1.88 4.8%

Average Midwest Gen Energy Price ($/MWh) 47.63 41.83 5.80 13.9% 47.09 40.12 6.97 17.4%

Homer City

Generation (in TWhr) 2.9 3.1 (0.2) -6.5% 5.4 6.6 (1.2) -18.2%

Equivalent Availability 74.3% 77.1% -2.8% 73.1% 82.6% -9.5%

Forced Outage Rate 19.9% 3.6% 16.3% 22.8% 5.6% 17.2%

Average Cost of Fuel ($/MWh) 24.13 19.36 4.77 24.6% 24.03 18.65 5.38 28.8%

Flat Energy Price—PJM West Hub ($/MWh) 48.08 47.30 0.78 1.6% 52.25 47.24 5.01 10.6%

Flat Energy Price—HC Busbar ($/MWh) 44.00 44.86 (0.86) -1.9% 47.24 44.54 2.70 6.1%

Flat Energy Price—PJM West Hub minus

HC Busbar ($/MWHr)—Basis 4.08 2.44 1.64 5.01 2.70 2.31

Average Homer City Energy Price ($/MWh) 50.02 42.93 7.09 16.5% 51.43 43.38 8.05 18.6%

Hedge Program status at June 30, 2006

Remainder of

2006 2007 2008

Midwest Generation

Megawatt hours (in TWh) 10.0 16.2 3.1

Average Energy Price ($/MWh) 47.61 $ 48.25 $ 66.13 $ (1)

Percent of Coal Requirements Under Contract 108% 95% 33%

Homer City

Megawatt hours (in TWh) 4.4 7.6 2.4

Average Energy Price ($/MWh) 54.07 $ 64.35 $ 66.01 $

Percent of Coal Requirements Under Contract 99% 97% 39%

(1) |

| Represents on-peak hedges. |

Note: Subsequent to June 30, 2006, an agreement was executed to hedge an additional 500 MW of on-peak power from

the Midwest Gen facilities for 2007, 2008 and 2009.

Edison International – EMG Update

Hedge Program status at June 30, 2006

20

Guidance

as of June 29th, 2006

Balance Sheet

Strength Performance Growth Dividends Shareholder

Returns

21

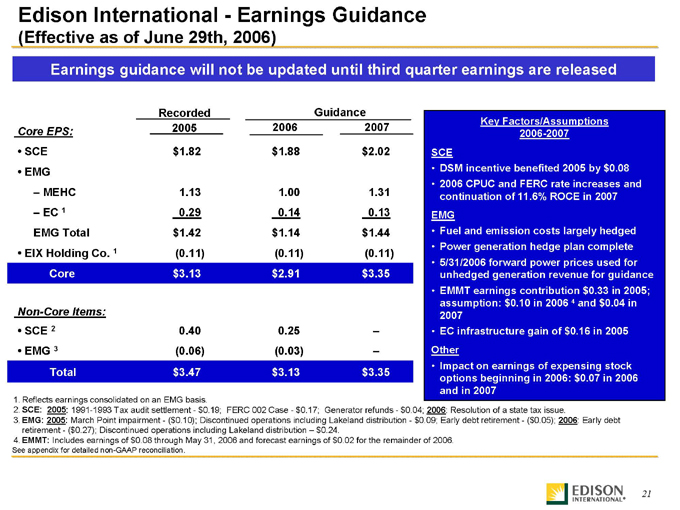

Edison International—Earnings Guidance

(Effective as of June 29th, 2006)

Guidance

2006 2007 Core EPS:

$3.35 $3.13 $3.47 Total

$1.44 $1.14 $1.42 EMG Total

– 0.25 0.40

Non-Core Items:

• SCE 2

– (0.03) (0.06) • EMG 3

$3.35 $2.91 $3.13 Core

(0.11) (0.11) (0.11) • EIX Holding Co. 1

0.13 0.14 0.29 – EC 1

1.31 1.00 1.13 – MEHC

• EMG

$2.02 $1.88 $1.82 • SCE

Recorded

2005 Key Factors/Assumptions

2006-2007

SCE

• DSM incentive benefited 2005 by $0.08

• 2006 CPUC and FERC rate increases and

continuation of 11.6% ROCE in 2007

EMG

• Fuel and emission costs largely hedged

• Power generation hedge plan complete

• 5/31/2006 forward power prices used for

unhedged generation revenue for guidance

• EMMT earnings contribution $0.33 in 2005;

assumption: $0.10 in 2006 4 and $0.04 in

2007

• EC infrastructure gain of $0.16 in 2005

Other

• Impact on earnings of expensing stock

options beginning in 2006: $0.07 in 2006

and in 2007

1. Reflects earnings consolidated on an EMG basis.

2. SCE: 2005: 1991-1993 Tax audit settlement—$0.19; FERC 002 Case—$0.17; Generator refunds—$0.04; 2006: Resolution of a state tax issue.

3. EMG: 2005: March Point impairment—($0.10); Discontinued operations including Lakeland distribution—$0.09; Early debt retirement—($0.05); 2006: Early debt

retirement—($0.27); Discontinued operations including Lakeland distribution – $0.24.

4. EMMT: Includes earnings of $0.08 through May 31, 2006 and forecast earnings of $0.02 for the remainder of 2006.

See appendix for detailed non-GAAP reconciliation.

Earnings guidance will not be updated until third quarter earnings are released

22

Coal Transp. Coal Emissions Generation Forward

Sales Basis

10% Price Increase Sensitivities

(pre-tax impact)

($ million)

1. Full-year 2006.

2. Coal contracts based on expected burn and contracted deliveries without regard to inventory levels.

3. As of May 31, 2006, excludes transportation.

4. Fuel costs, excluding emissions, includes coal and coal transportation costs, natural gas and oil used for startup and limestone cost.

See Assumptions Detail in appendix for additional information.

($ million)

($ million)

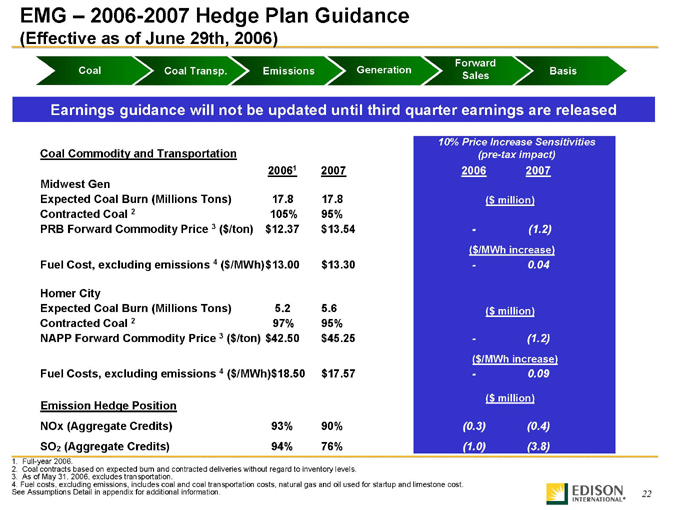

EMG – 2006-2007 Hedge Plan Guidance

(Effective as of June 29th, 2006)

Coal Commodity and Transportation

20061 2007 2006 2007

Midwest Gen

Expected Coal Burn (Millions Tons) 17.8 17.8

Contracted Coal 2 105% 95%

PRB Forward Commodity Price 3 ($/ton) $12.37 $13.54—(1.2)

($/MWh increase)

Fuel Cost, excluding emissions 4 ($/MWh)$13.00 $13.30—0.04

Homer City

Expected Coal Burn (Millions Tons) 5.2 5.6

Contracted Coal 2 97% 95%

NAPP Forward Commodity Price 3 ($/ton) $42.50 $45.25—(1.2)

($/MWh increase)

Fuel Costs, excluding emissions 4 ($/MWh)$18.50 $17.57—0.09

Emission Hedge Position

NOx (Aggregate Credits) 93% 90% (0.3) (0.4)

SO2 (Aggregate Credits) 94% 76% (1.0) (3.8)

Earnings guidance will not be updated until third quarter earnings are released

23

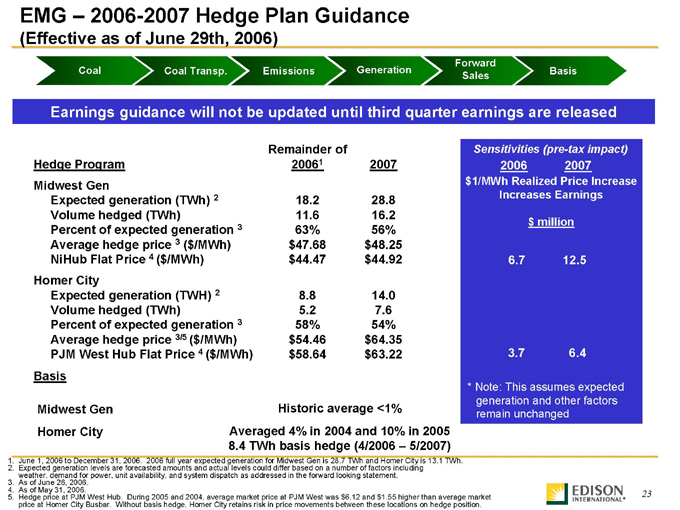

14.0

7.6

54%

$64.35

$63.22

28.8

16.2

56%

$48.25

$44.92

2007

Remainder of

20061 Hedge Program

8.8

5.2

58%

$54.46

$58.64

Homer City

Expected generation (TWH) 2

Volume hedged (TWh)

Percent of expected generation 3

Average hedge price 3/5 ($/MWh)

PJM West Hub Flat Price 4 ($/MWh)

Basis

18.2

11.6

63%

$47.68

$44.47

Midwest Gen

Expected generation (TWh) 2

Volume hedged (TWh)

Percent of expected generation 3

Average hedge price 3 ($/MWh)

NiHub Flat Price 4 ($/MWh)

Midwest Gen

Homer City

1. June 1, 2006 to December 31, 2006. 2006 full year expected generation for Midwest Gen is 28.7 TWh and Homer City is 13.1 TWh.

2. Expected generation levels are forecasted amounts and actual levels could differ based on a number of factors including

weather, demand for power, unit availability, and system dispatch as addressed in the forward looking statement.

3. As of June 26, 2006.

4. As of May 31, 2006.

5. Hedge price at PJM West Hub. During 2005 and 2004, average market price at PJM West was $6.12 and $1.55 higher than average market

price at Homer City Busbar. Without basis hedge, Homer City retains risk in price movements between these locations on hedge position.

Historic average <1%

Averaged 4% in 2004 and 10% in 2005

8.4 TWh basis hedge (4/2006 – 5/2007)

2006 2007

$1/MWh Realized Price Increase

Increases Earnings

$ million

6.7 12.5

3.7 6.4

Sensitivities (pre-tax impact)

Coal Transp. Coal Emissions Generation Forward

Sales Basis

EMG – 2006-2007 Hedge Plan Guidance

(Effective as of June 29th, 2006)

* |

| Note: This assumes expected |

generation and other factors

remain unchanged

Earnings guidance will not be updated until third quarter earnings are released

24

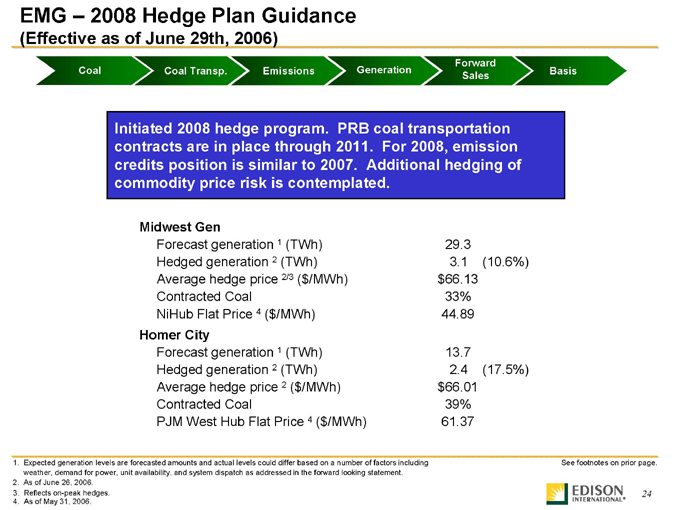

Midwest Gen

Forecast generation 1 (TWh) 29.3

Hedged generation 2 (TWh) 3.1 (10.6%)

Average hedge price 2/3 ($/MWh) $66.13

Contracted Coal 33%

NiHub Flat Price 4 ($/MWh) 44.89

Homer City

Forecast generation 1 (TWh) 13.7

Hedged generation 2 (TWh) 2.4 (17.5%)

Average hedge price 2 ($/MWh) $66.01

Contracted Coal 39%

PJM West Hub Flat Price 4 ($/MWh) 61.37

Initiated 2008 hedge program. PRB coal transportation

contracts are in place through 2011. For 2008, emission

credits position is similar to 2007. Additional hedging of

commodity price risk is contemplated.

2. As of June 26, 2006.

3. Reflects on-peak hedges.

See footnotes on prior page.

4. As of May 31, 2006.

Coal Transp. Coal Emissions Generation Forward

Sales Basis

EMG – 2008 Hedge Plan Guidance

(Effective as of June 29th, 2006)

1. Expected generation levels are forecasted amounts and actual levels could differ based on a number of factors including

weather, demand for power, unit availability, and system dispatch as addressed in the forward looking statement.

25

Edison International – Strategic Plan Foundation

• Strong utility

operating in a large

and rapidly growing

service territory

• Competitive power

generation business

with large base of

low-cost coal assets

Organic Growth

• Significant long-term

earnings and cash flow

growth from regulated

investments

• Business flexibility for

future growth

• Upside earnings potential

from competitive

generation investments

Produces Produces

Balance Sheet

Strength Performance Growth Dividends Shareholder

Returns

26

Appendix

27

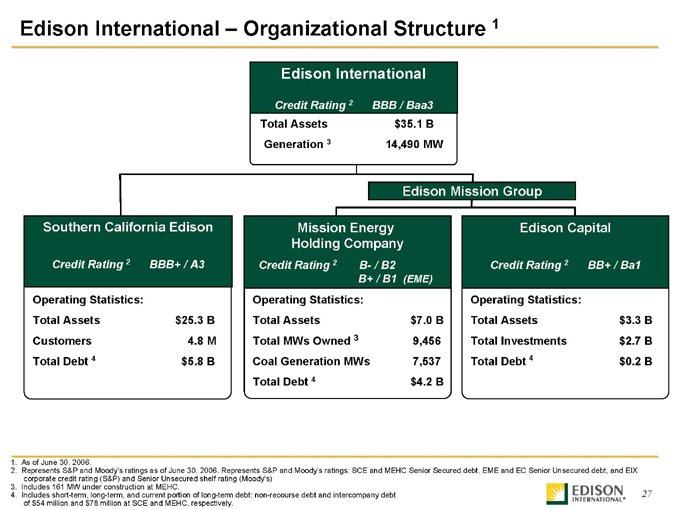

Operating Statistics:

Total Assets $25.3 B

Customers 4.8 M

Total Debt 4 $5.8 B

Total Assets $35.1 B

Generation 3 14,490 MW

Edison International – Organizational Structure 1

Operating Statistics:

Total Assets $3.3 B

Total Investments $2.7 B

Total Debt 4 $0.2 B

Southern California Edison

Credit Rating 2 BBB+ / A3

Operating Statistics:

Total Assets $7.0 B

Total MWs Owned 3 9,456

Coal Generation MWs 7,537

Total Debt 4 $4.2 B

Mission Energy

Holding Company

Credit Rating 2 B- / B2

B+ / B1 (EME)

Edison Capital

Credit Rating 2 BB+ / Ba1

1. As of June 30, 2006.

2. Represents S&P and Moody’s ratings as of June 30, 2006. Represents S&P and Moody’s ratings: SCE and MEHC Senior Secured debt, EME and EC Senior Unsecured debt, and EIX

corporate credit rating (S&P) and Senior Unsecured shelf rating (Moody’s)

3. Includes 161 MW under construction at MEHC.

4. Includes short-term, long-term, and current portion of long-term debt; non-recourse debt and intercompany debt

of $54 million and $78 million at SCE and MEHC, respectively.

Edison International

Credit Rating 2 BBB / Baa3

Edison Mission Group

28

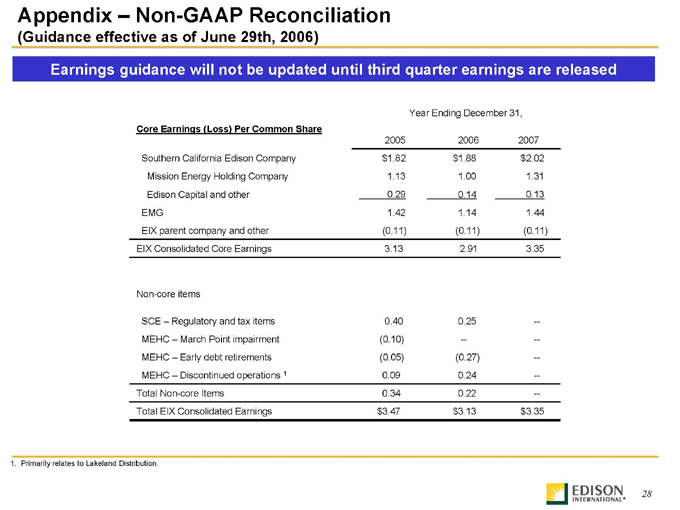

Appendix – Non-GAAP Reconciliation

(Guidance effective as of June 29th, 2006)

1.44 1.14 1.42 EMG

$3.47

0.34

0.09

(0.05)

(0.10)

0.40

3.13

(0.11)

0.29

1.13

$1.82

2005

$3.35 $3.13 Total EIX Consolidated Earnings

— 0.22 Total Non-core Items

— 0.24 MEHC – Discontinued operations 1

— (0.27) MEHC – Early debt retirements

— — MEHC – March Point impairment

— 0.25 SCE – Regulatory and tax items

Non-core items

3.35 2.91 EIX Consolidated Core Earnings

(0.11) (0.11) EIX parent company and other

0.13 0.14 Edison Capital and other

1.31 1.00 Mission Energy Holding Company

$2.02 $1.88 Southern California Edison Company

2007 2006

Core Earnings (Loss) Per Common Share

Year Ending December 31,

1. Primarily relates to Lakeland Distribution.

Earnings guidance will not be updated until third quarter earnings are released

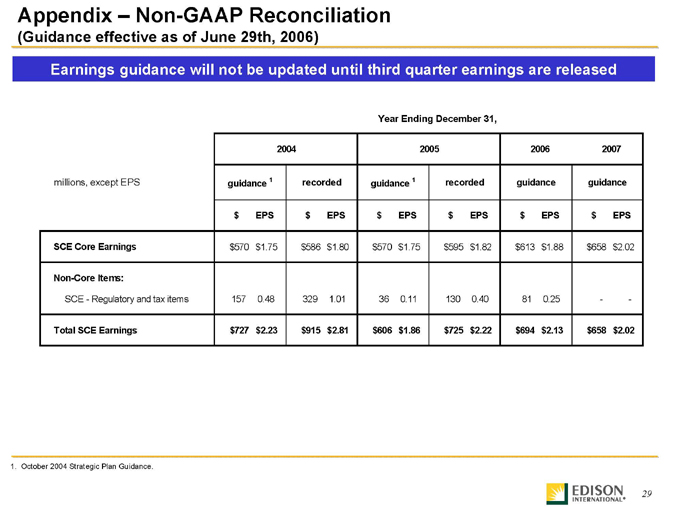

29

2004 2005 2006 2007

millions, except EPS guidance 1 recorded guidance 1 recorded guidance guidance

$ EPS $ EPS $ EPS $ EPS $ EPS $ EPS

SCE Core Earnings $570 $1.75 $586 $1.80 $570 $1.75 $595 $1.82 $613 $1.88 $658 $2.02

Non-Core Items:

SCE—Regulatory and tax items 157 0.48 329 1.01 36 0.11 130 0.40 81 0.25—-

Total SCE Earnings $727 $2.23 $915 $2.81 $606 $1.86 $725 $2.22 $694 $2.13 $658 $2.02

Year Ending December 31,

1. October 2004 Strategic Plan Guidance.

Earnings guidance will not be updated until third quarter earnings are released

Appendix – Non-GAAP Reconciliation

(Guidance effective as of June 29th, 2006)

30

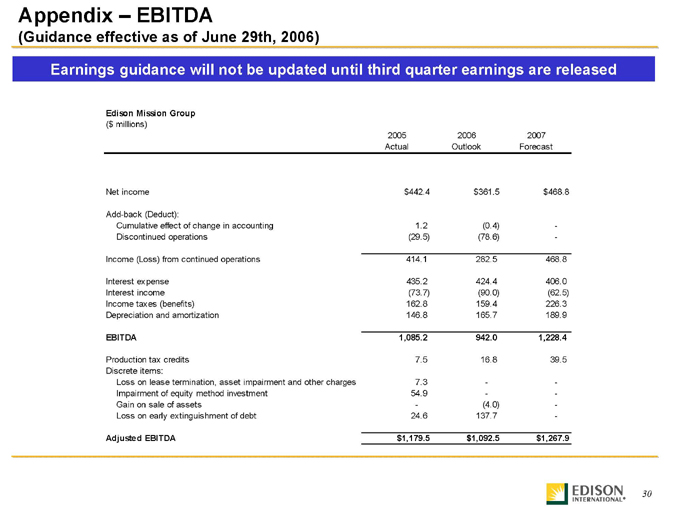

Appendix – EBITDA

(Guidance effective as of June 29th, 2006)

Edison Mission Group

($ millions)

2005 2006 2007

Actual Outlook Forecast

Net income $442.4 $361.5 $468.8

Add-back (Deduct):

Cumulative effect of change in accounting 1.2 (0.4) -

Discontinued operations (29.5) (78.6) -

Income (Loss) from continued operations 414.1 282.5 468.8

Interest expense 435.2 424.4 406.0

Interest income (73.7) (90.0) (62.5)

Income taxes (benefits) 162.8 159.4 226.3

Depreciation and amortization 146.8 165.7 189.9

EBITDA 1,085.2 942.0 1,228.4

Production tax credits 7.5 16.8 39.5

Discrete items:

Loss on lease termination, asset impairment and other charges 7.3—-

Impairment of equity method investment 54.9—-

Gain on sale of assets—(4.0) -

Loss on early extinguishment of debt 24.6 137.7 -

Adjusted EBITDA $1,179.5 $1,092.5 $1,267.9

Earnings guidance will not be updated until third quarter earnings are released

31

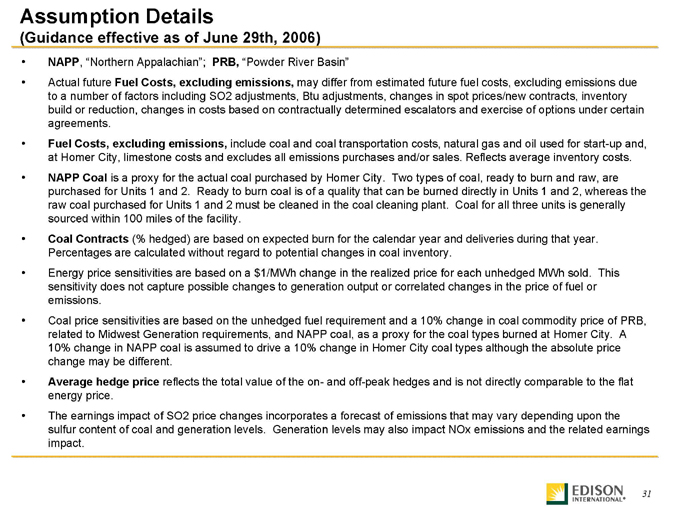

• NAPP, “Northern Appalachian”; PRB, “Powder River Basin”

• Actual future Fuel Costs, excluding emissions, may differ from estimated future fuel costs, excluding emissions due

to a number of factors including SO2 adjustments, Btu adjustments, changes in spot prices/new contracts, inventory

build or reduction, changes in costs based on contractually determined escalators and exercise of options under certain

agreements.

• Fuel Costs, excluding emissions, include coal and coal transportation costs, natural gas and oil used for start-up and,

at Homer City, limestone costs and excludes all emissions purchases and/or sales. Reflects average inventory costs.

• NAPP Coal is a proxy for the actual coal purchased by Homer City. Two types of coal, ready to burn and raw, are

purchased for Units 1 and 2. Ready to burn coal is of a quality that can be burned directly in Units 1 and 2, whereas the

raw coal purchased for Units 1 and 2 must be cleaned in the coal cleaning plant. Coal for all three units is generally

sourced within 100 miles of the facility.

• Coal Contracts (% hedged) are based on expected burn for the calendar year and deliveries during that year.

Percentages are calculated without regard to potential changes in coal inventory.

• Energy price sensitivities are based on a $1/MWh change in the realized price for each unhedged MWh sold. This

sensitivity does not capture possible changes to generation output or correlated changes in the price of fuel or

emissions.

• Coal price sensitivities are based on the unhedged fuel requirement and a 10% change in coal commodity price of PRB,

related to Midwest Generation requirements, and NAPP coal, as a proxy for the coal types burned at Homer City. A

10% change in NAPP coal is assumed to drive a 10% change in Homer City coal types although the absolute price

change may be different.

• Average hedge price reflects the total value of the on- and off-peak hedges and is not directly comparable to the flat

energy price.

• The earnings impact of SO2 price changes incorporates a forecast of emissions that may vary depending upon the

sulfur content of coal and generation levels. Generation levels may also impact NOx emissions and the related earnings

impact.

Assumption Details

(Guidance effective as of June 29th, 2006)

32

EMG – Capital Expenditures

2Q 2006 to 4Q 2008

0

50

100

150

200

250

300

350

400

450

500

2006 BoY 2007 2008 2009

Plant Capex Environmental Growth

$826 Million

• Evaluating FGDs at Homer City Units 1 and 2

• Environmental expenditures at Midwest Gen

• Wind investments

• Thermal investments

Potential Expenditures Planned Expenditures

$ Millions

33

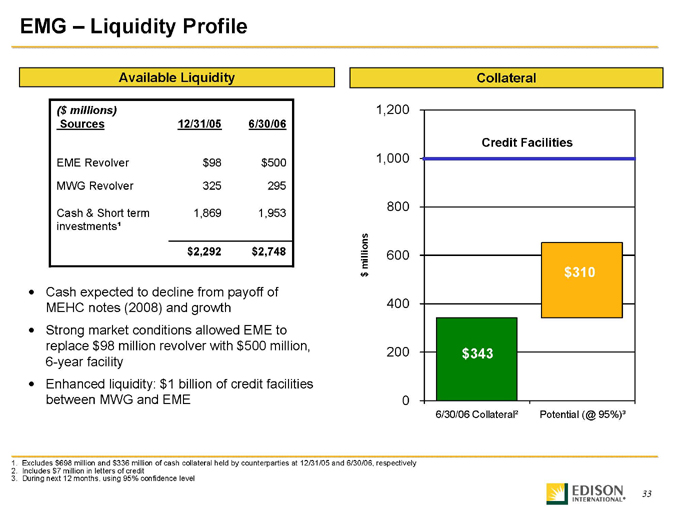

EMG – Liquidity Profile

0

200

400

600

800

1,000

1,200

6/30/06 Collateral² Potential (@ 95%)³

$ millions

$2,748

1,953

295

$500

6/30/06

$2,292

1,869

325

$98

12/31/05

Cash & Short term

investments¹

MWG Revolver

EME Revolver

($ millions)

Sources

Available Liquidity

Credit Facilities

Collateral

1. Excludes $698 million and $336 million of cash collateral held by counterparties at 12/31/05 and 6/30/06, respectively

2. Includes $7 million in letters of credit

3. During next 12 months, using 95% confidence level

$310

$343

• Cash expected to decline from payoff of

MEHC notes (2008) and growth

• Strong market conditions allowed EME to

replace $98 million revolver with $500 million,

6-year facility

• Enhanced liquidity: $1 billion of credit facilities

between MWG and EME