Exhibit 99.1

Leading the Way in Electricity SM

Business Update

May-June 2008

May 23, 2008

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Forward-Looking Statements

Statements contained in this presentation about future performance, including, without limitation, earnings, asset and rate base growth, load growth, capital investments, and other statements that are not purely historical, are forward-looking statements. These forward-looking statements reflect our current expectations; however, such statements involve risks and uncertainties. Actual results could differ materially from current expectations. Important factors that could cause different results are discussed under the headings “Risk Factors” and “Management’s Discussion and Analysis” in Edison International’s 2007 Form 10-K and other reports filed with the Securities and Exchange Commission are available on our website: www.edisoninvestor.com. These forward-looking statements represent our expectations only as of the date of this presentation, and Edison International assumes no duty to update them to reflect new information, events or circumstances.

May 23, 2008

1

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

What’s New Since Our April Update

Updated Information

• 1Q 2008 results and forward looking forecasts as appropriate

• Regulatory matters (p. 19, 33)

Additional Topics

• Renewable transmission planning (p. 20)

• Electronic technology solutions to meet the climate change challenge (p. 21)

• Shareholder value proposition (p. 31)

May 23, 2008

2

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Strategic Overview

May 23, 2008

3

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

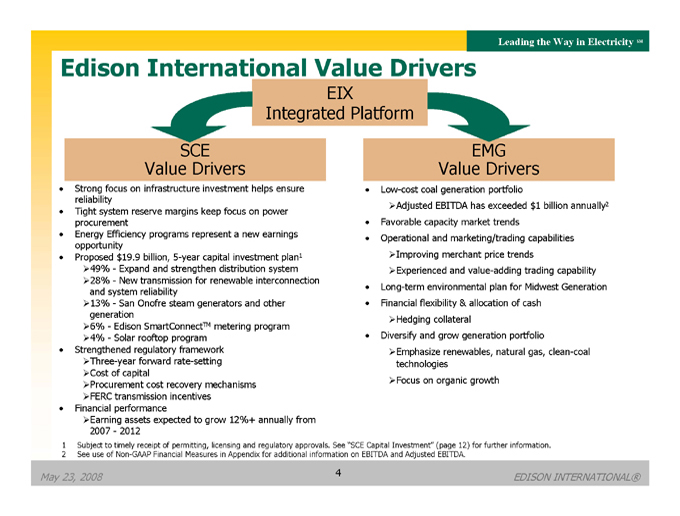

Edison International Value Drivers

EIX Integrated Platform

SCE Value Drivers

Strong focus on infrastructure investment helps ensure reliability Tight system reserve margins keep focus on power procurement Energy Efficiency programs represent a new earnings opportunity Proposed $19.9 billion, 5-year capital investment plan1

49%—Expand and strengthen distribution system

28%—New transmission for renewable interconnection and system reliability

13%—San Onofre steam generators and other generation

6%—Edison SmartConnectTM metering program

4%—Solar rooftop program Strengthened regulatory framework

Three-year forward rate-setting

Cost of capital

Procurement cost recovery mechanisms

FERC transmission incentives Financial performance

Earning assets expected to grow 12%+ annually from 2007—2012

EMG Value Drivers

Low-cost coal generation portfolio

Adjusted EBITDA has exceeded $1 billion annually2 Favorable capacity market trends Operational and marketing/trading capabilities

Improving merchant price trends

Experienced and value-adding trading capability Long-term environmental plan for Midwest Generation Financial flexibility & allocation of cash

Hedging collateral

Diversify and grow generation portfolio

Emphasize renewables, natural gas, clean-coal technologies

Focus on organic growth

1 Subject to timely receipt of permitting, licensing and regulatory approvals. See “SCE Capital Investment” (page 12) for further information.

2 See use of Non-GAAP Financial Measures in Appendix for additional information on EBITDA and Adjusted EBITDA.

May 23, 2008

4

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

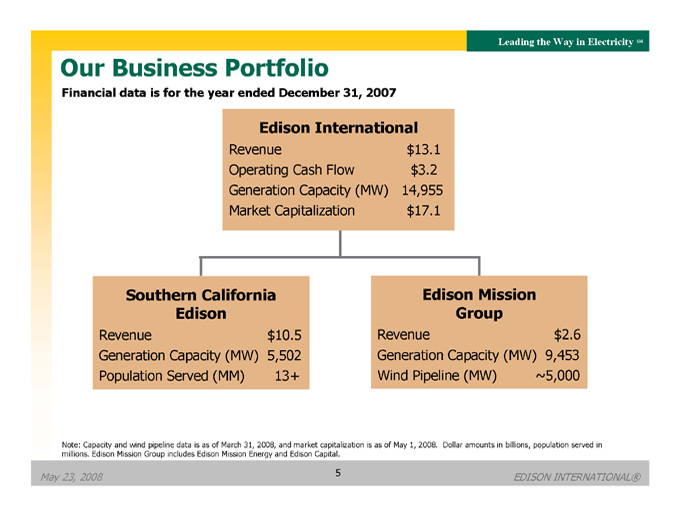

Our Business Portfolio

Financial data is for the year ended December 31, 2007

Edison International

Revenue $13.1 Operating Cash Flow $3.2 Generation Capacity (MW) 14,955 Market Capitalization $17.1

Southern California Edison

Revenue $10.5 Generation Capacity (MW) 5,502 Population Served (MM) 13+

Edison Mission Group

Revenue $2.6 Generation Capacity (MW) 9,453 Wind Pipeline (MW) ~5,000

Note: Capacity and wind pipeline data is as of March 31, 2008, and market capitalization is as of May 1, 2008. Dollar amounts in billions, population served in millions. Edison Mission Group includes Edison Mission Energy and Edison Capital.

May 23, 2008

5

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

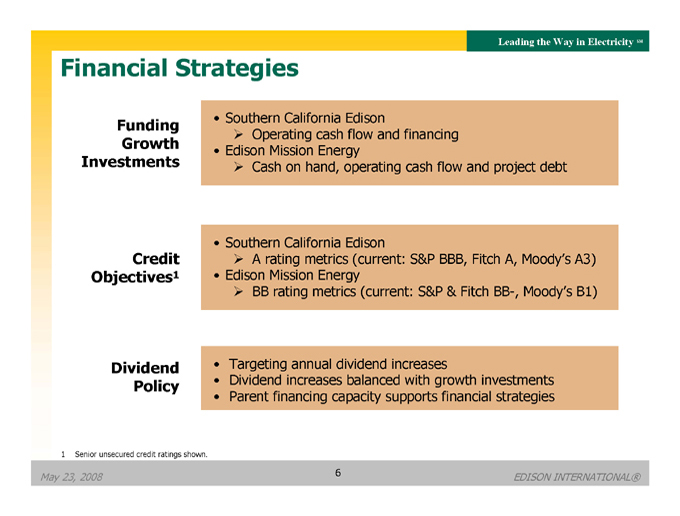

Financial Strategies

Funding Growth Investments

Southern California Edison

Operating cash flow and financing

Edison Mission Energy

Cash on hand, operating cash flow and project debt

Credit Objectives1

Southern California Edison

A rating metrics (current: S&P BBB, Fitch A, Moody’s A3)

Edison Mission Energy

BB rating metrics (current: S&P & Fitch BB-, Moody’s B1)

Dividend Policy

Targeting annual dividend increases

Dividend increases balanced with growth investments Parent financing capacity supports financial strategies

1 Senior unsecured credit ratings shown.

May 23, 2008

6

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

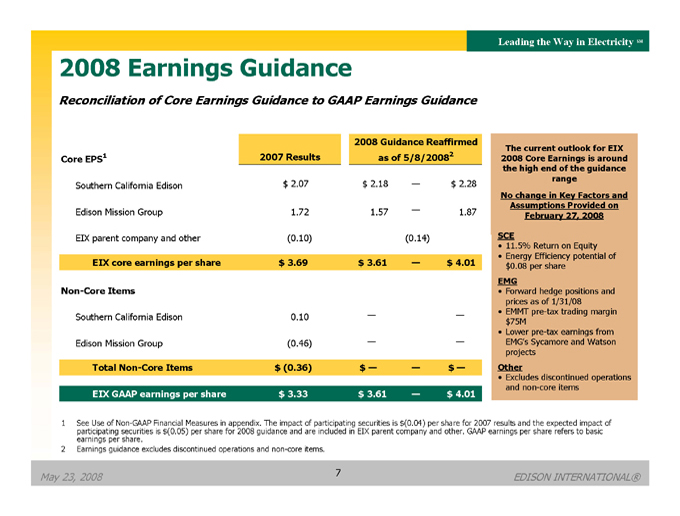

2008 Earnings Guidance

Reconciliation of Core Earnings Guidance to GAAP Earnings Guidance

2008 Guidance Reaffirmed Core EPS1 2007 Results as of 5/8/20082

Southern California Edison $ 2.07 $ 2.18 — $ 2.28 Edison Mission Group 1.72 1.57 — 1.87 EIX parent company and other (0.10) (0.14)

EIX core earnings per share $ 3.69 $ 3.61 — $ 4.01

Non-Core Items

Southern California Edison 0.10 — —

Edison Mission Group (0.46) — —

Total Non-Core Items $ (0.36) $ — — $ —

EIX GAAP earnings per share $ 3.33 $ 3.61 — $ 4.01

The current outlook for EIX 2008 Core Earnings is around the high end of the guidance range No change in Key Factors and Assumptions Provided on February 27, 2008

SCE

11.5% Return on Equity

Energy Efficiency potential of $0.08 per share

EMG

Forward hedge positions and prices as of 1/31/08

EMMT pre-tax trading margin $75M

Lower pre-tax earnings from EMG’s Sycamore and Watson projects

Other

• Excludes discontinued operations and non-core items

1 See Use of Non-GAAP Financial Measures in appendix. The impact of participating securities is $(0.04) per share for 2007 results and the expected impact of participating securities is $(0.05) per share for 2008 guidance and are included in EIX parent company and other. GAAP earnings per share refers to basic earnings per share.

2 Earnings guidance excludes discontinued operations and non-core items.

May 23, 2008

7

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Southern California Edison (SCE)

An Investor-Owned Electric Utility

May 23, 2008

8

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

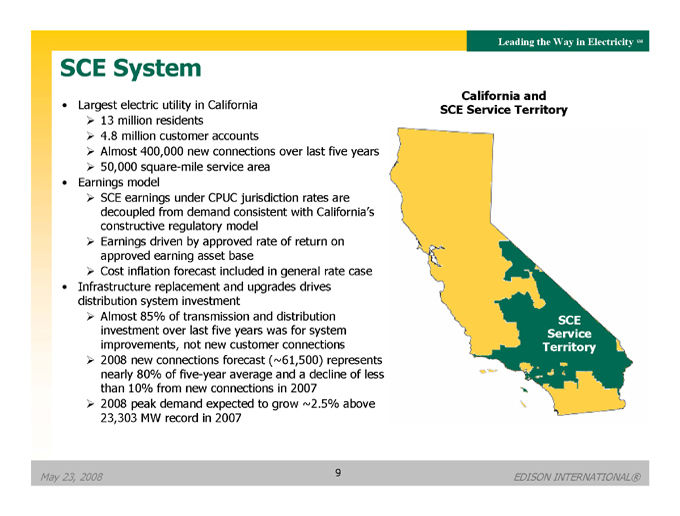

SCE System

Largest electric utility in California

13 million residents

4.8 million customer accounts

Almost 400,000 new connections over last five years

50,000 square-mile service area

Earnings model

SCE earnings under CPUC jurisdiction rates are decoupled from demand consistent with California’s constructive regulatory model

Earnings driven by approved rate of return on approved earning asset base

Cost inflation forecast included in general rate case

Infrastructure replacement and upgrades drives distribution system investment

Almost 85% of transmission and distribution investment over last five years was for system improvements, not new customer connections

2008 new connections forecast (~61,500) represents nearly 80% of five-year average and a decline of less than 10% from new connections in 2007

2008 peak demand expected to grow ~2.5% above 23,303 MW record in 2007

California and SCE Service Territory

SCE Service Territory

May 23, 2008

9

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

SCE Long-Term Resource Objectives

SCE Distribution System Supply and Demand Balance (MW)

Power Resource Needs

Supply Objectives

New Renewables

Other Projects Underway

1,874

830

4,176

1,339

319

Increased

Demand

Requirement1

Potential

Retirements

Anticipated

New

Generation

New Demand-

Side Resources

Potential Need

by 20152

System

Reliability

Price

Stability

Environmental

Considerations

Balance Objectives

• Energy efficiency

• Demand response

• Renewable resources

• Distributed generation

• Clean fossil fuel generation

Load growth, retirements, and renewable mandates drive power resource needs

• ~6,700 MW new resources required

• ~1,350 MW new generation contracts awarded March 2008

1 Relative to 2007; data as of February 2008, includes planning reserve margin (PRM) of 15%. Source: 2006 SCE Long-Term Procurement Plan Final Decision; CEC November Load Forecast.

2 This number is without DPV2.

May 23, 2008

10

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

SCE Renewable Energy Goals

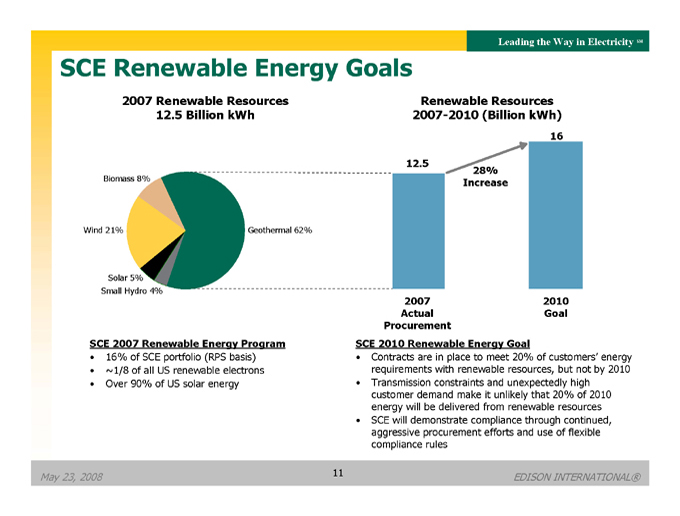

2007 Renewable Resources 12.5 Billion kWh

Biomass 8%

Wind 21%

Geothermal 62%

Solar 5% Small Hydro 4%

SCE 2007 Renewable Energy Program

• 16% of SCE portfolio (RPS basis)

• ~1/8 of all US renewable electrons

• Over 90% of US solar energy

Renewable Resources 2007-2010 (Billion kWh)

12.5

2007 Actual Procurement

28% Increase

16 2010 Goal

SCE 2010 Renewable Energy Goal

• Contracts are in place to meet 20% of customers’ energy requirements with renewable resources, but not by 2010

• Transmission constraints and unexpectedly high customer demand make it unlikely that 20% of 2010 energy will be delivered from renewable resources

• SCE will demonstrate compliance through continued, aggressive procurement efforts and use of flexible compliance rules

May 23, 2008

11

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

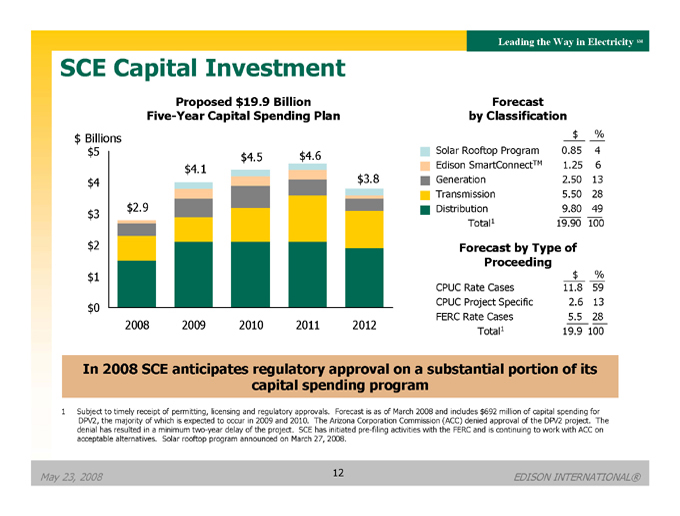

SCE Capital Investment

Proposed $19.9 Billion Five-Year Capital Spending Plan

$ Billions

$5

$4

$3

$2

$1

$0 $2.9

$4.1

$4.5

$4.6

$3.8

2008

2009

2010

2011

2012

Forecast by Classification

$ % Solar Rooftop Program 0.85 4

Edison SmartConnectTM 1.25 6

Generation 2.50 13

Transmission 5.50 28

Distribution 9.80 49 Total1 19.90 100

Forecast by Type of Proceeding

$ % CPUC Rate Cases 11.8 59

CPUC Project Specific 2.6 13

FERC Rate Cases 5.5 28

Total1 19.9 100

In 2008 SCE anticipates regulatory approval on a substantial portion of its capital spending program

1 Subject to timely receipt of permitting, licensing and regulatory approvals. Forecast is as of March 2008 and includes $692 million of capital spending for DPV2, the majority of which is expected to occur in 2009 and 2010. The Arizona Corporation Commission (ACC) denied approval of the DPV2 project. The denial has resulted in a minimum two-year delay of the project. SCE has initiated pre-filing activities with the FERC and is continuing to work with ACC on acceptable alternatives. Solar rooftop program announced on March 27, 2008.

May 23, 2008

12

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

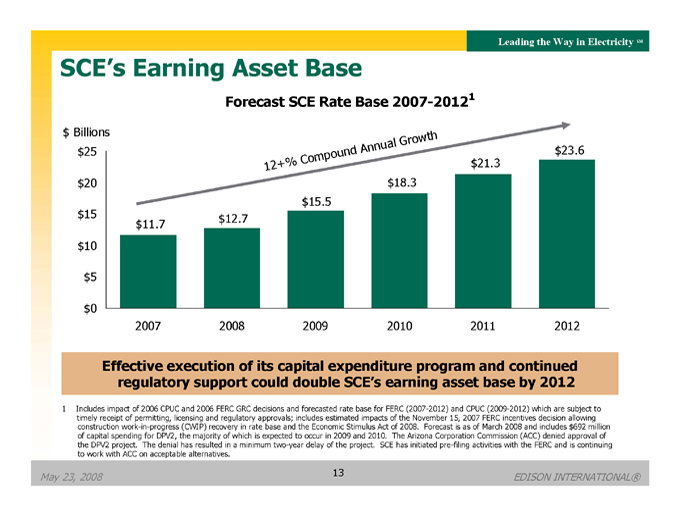

SCE’s Earning Asset Base

Forecast SCE Rate Base 2007-20121

$ Billions

$25

$20

$15

$10

$5

$0

12+% Compound Annual Growth

$11.7

$12.7

$15.5

$18.3

$21.3

$23.6

2007

2008

2009

2010

2011

2012

Effective execution of its capital expenditure program and continued regulatory support could double SCE’s earning asset base by 2012

1 Includes impact of 2006 CPUC and 2006 FERC GRC decisions and forecasted rate base for FERC (2007-2012) and CPUC (2009-2012) which are subject to timely receipt of permitting, licensing and regulatory approvals; includes estimated impacts of the November 15, 2007 FERC incentives decision allowing construction work-in-progress (CWIP) recovery in rate base and the Economic Stimulus Act of 2008. Forecast is as of March 2008 and includes $692 million of capital spending for DPV2, the majority of which is expected to occur in 2009 and 2010. The Arizona Corporation Commission (ACC) denied approval of the DPV2 project. The denial has resulted in a minimum two-year delay of the project. SCE has initiated pre-filing activities with the FERC and is continuing to work with ACC on acceptable alternatives.

May 23, 2008

13

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

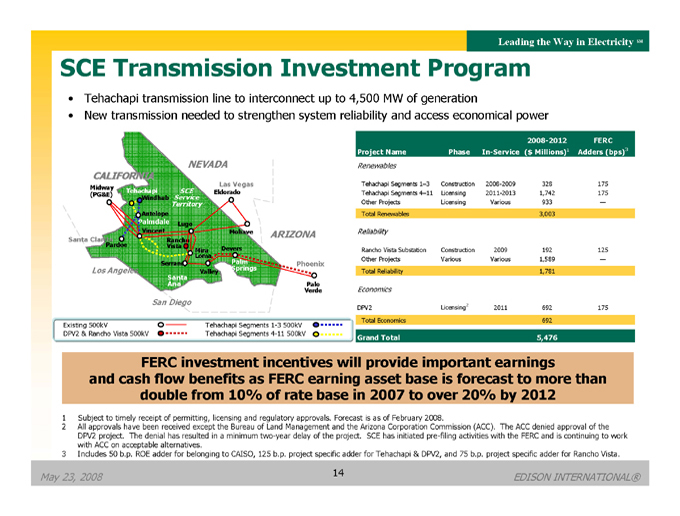

SCE Transmission Investment Program

• Tehachapi transmission line to interconnect up to 4,500 MW of generation

• New transmission needed to strengthen system reliability and access economical power

NEVADA CALIFORNIA

Las Vegas

Midway

Tehachapi SCE Eldorado

(PG&E) Service

Windhub

Territory

Antelope

Palmdale Lugo

Vincent Mohave ARIZONA

Santa Clarita Rancho Pardee Vista

Mira Devers Loma

Serrano Palm Phoenix

Los Angeles Springs

Valley

Santa

Ana Palo Verde

Existing 500kV Tehachapi Segments 1-3 500kV DPV2 & Rancho Vista 500kV Tehachapi Segments 4-11 500kV

2008-2012 FERC

Project Name Phase In-Service ($ Millions)1 Adders (bps)3

Renewables

Tehachapi Segments 1–3 Construction 2008-2009 328 175

Tehachapi Segments 4–11 Licensing 2011-2013 1,742 175

Other Projects Licensing Various 933 —

Total Renewables 3,003

Reliability

Rancho Vista Substation Construction 2009 192 125

Other Projects Various Various 1,589 —

Total Reliability 1,781

Economics

DPV2 Licensing2 2011 692 175

Total Economics 692

Grand Total 5,476

FERC investment incentives will provide important earnings and cash flow benefits as FERC earning asset base is forecast to more than double from 10% of rate base in 2007 to over 20% by 2012

1 Subject to timely receipt of permitting, licensing and regulatory approvals. Forecast is as of February 2008.

2 All approvals have been received except the Bureau of Land Management and the Arizona Corporation Commission (ACC). The ACC denied approval of the DPV2 project. The denial has resulted in a minimum two-year delay of the project. SCE has initiated pre-filing activities with the FERC and is continuing to work with ACC on acceptable alternatives.

3 Includes 50 b.p. ROE adder for belonging to CAISO, 125 b.p. project specific adder for Tehachapi & DPV2, and 75 b.p. project specific adder for Rancho Vista.

May 23, 2008

14

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

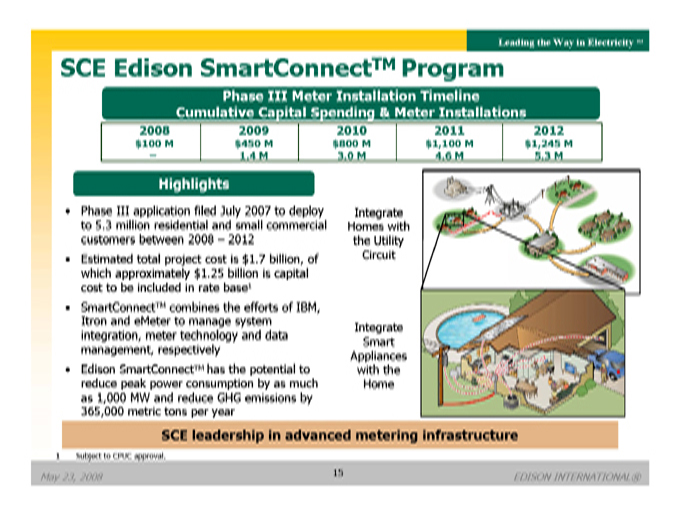

SCE Edison SmartConnectTM Program

Phase III Meter Installation Timeline

Cumulative Capital Spending & Meter Installations

2008 2009 2010 2011 2012

$100 M $450 M $800 M $1,100 M $1,245 M

– 1.4 M 3.0 M 4.6 M 5.3 M

Highlights

• Phase III application filed July 2007 to deploy

to 5.3 million residential and small commercial

customers between 2008 – 2012

• Estimated total project cost is $1.7 billion, of

which approximately $ 1.25 billion is capital

cost to be included in rate base 1

• SmartConnectTM combines the efforts of IBM,

Itron and eMeter to manage system

integration, meter technology and data

management, respectively

• Edison SmartConnectTM has the potential to

reduce peak power consumption by as much

as 1,000 MW and reduce GHG emissions by

365,000 metric tons per year

Integrate Homes with the Utility Circuit

Integrate Smart Appliances with the Home

SCE leadership in advanced metering infrastructure

1 Subject to CPUC approval.

May 23, 2008

15

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

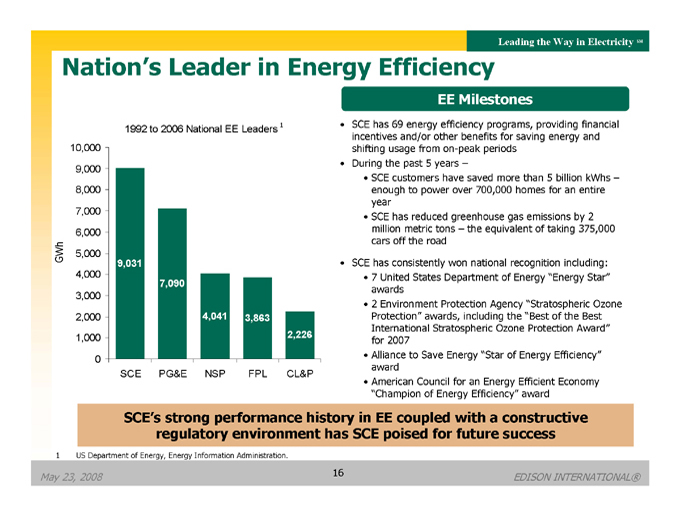

Nation’s Leader in Energy Efficiency

1992 to 2006 National EE Leaders 1

10,000

9,000 8,000 7,000 6,000 5,000 4,000 3,000 2,000 1,000 0

9,031

7,090

4,041

3,863

2,226

SCE

PG&E

NSP

FPL

EE Milestones

• SCE has 69 energy efficiency programs, providing financial incentives and/or other benefits for saving energy and shifting usage from on-peak periods

• During the past 5 years –

• SCE customers have saved more than 5 billion kWhs –enough to power over 700,000 homes for an entire year

• SCE has reduced greenhouse gas emissions by 2 million metric tons – the equivalent of taking 375,000 cars off the road

• SCE has consistently won national recognition including:

• 7 United States Department of Energy “Energy Star” awards

• 2 Environment Protection Agency “Stratospheric Ozone Protection” awards, including the “Best of the Best International Stratospheric Ozone Protection Award” for 2007

• Alliance to Save Energy “Star of Energy Efficiency” award

• American Council for an Energy Efficient Economy “Champion of Energy Efficiency” award

SCE’s strong performance history in EE coupled with a constructive regulatory environment has SCE poised for future success

1 US Department of Energy, Energy Information Administration.

May 23, 2008

16

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

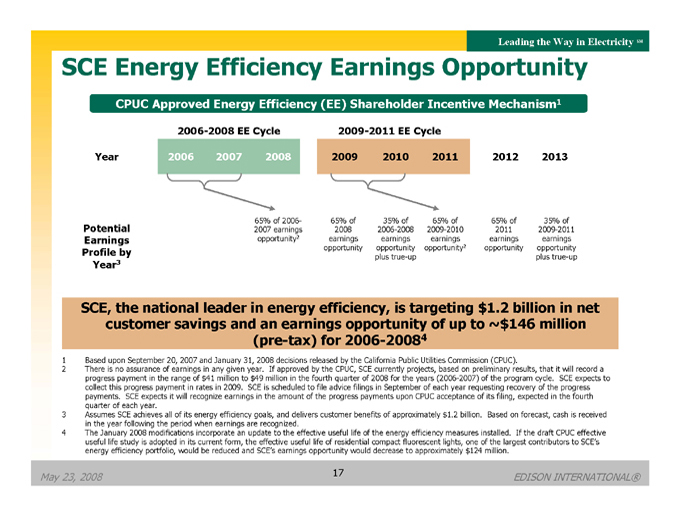

SCE Energy Efficiency Earnings Opportunity

CPUC Approved Energy Efficiency (EE) Shareholder Incentive Mechanism1

Year Potential Earnings Profile by Year3 2006-2008 EE Cycle 2006 2007 2008 2009-2011 EE Cycle

2009

2010

2011

2012

2013

65% of 2006- 65% of 35% of 65% of 65% of 35% of 2007 earnings 2008 2006-2008 2009-2010 2011 2009-2011 opportunity2 earnings earnings earnings earnings earnings opportunity opportunity opportunity2 opportunity opportunity plus true-up plus true-up

SCE, the national leader in energy efficiency, is targeting $1.2 billion in net customer savings and an earnings opportunity of up to ~$146 million (pre-tax) for 2006-20084

1 Based upon September 20, 2007 and January 31, 2008 decisions released by the California Public Utilities Commission (CPUC).

2 There is no assurance of earnings in any given year. If approved by the CPUC, SCE currently projects, based on preliminary results, that it will record a progress payment in the range of $41 million to $49 million in the fourth quarter of 2008 for the years (2006-2007) of the program cycle. SCE expects to collect this progress payment in rates in 2009. SCE is scheduled to file advice filings in September of each year requesting recovery of the progress payments. SCE expects it will recognize earnings in the amount of the progress payments upon CPUC acceptance of its filing, expected in the fourth quarter of each year.

3 Assumes SCE achieves all of its energy efficiency goals, and delivers customer benefits of approximately $1.2 billion. Based on forecast, cash is received in the year following the period when earnings are recognized.

4 The January 2008 modifications incorporate an update to the effective useful life of the energy efficiency measures installed. If the draft CPUC effective useful life study is adopted in its current form, the effective useful life of residential compact fluorescent lights, one of the largest contributors to SCE’s energy efficiency portfolio, would be reduced and SCE’s earnings opportunity would decrease to approximately $124 million.

May 23, 2008

17

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

SCE Solar Rooftop Program

• Install 250 MW of solar photovoltaic generation on leased commercial rooftops

– 1-2 MW average installations target significant cost economies of scale

– May seek future authority to expand to 500 MW program

•$ 875 million capital spending program1

– 100 b.p. premium for utility-owned renewable generation (SCE’s CPUC-approved return on equity is 11.5% for 2008)

• SCE has requested authority to recover costs incurred during regulatory approval process to facilitate a 2008 program launch

• Operating costs would be recovered through a balancing account with after-the-fact reasonableness review until included in base rates as part of general rate cases

SCE’s proposed rooftop solar program will help advance California public policy and help build scale for the large rooftop photovoltaic solar market

1 Subject to CPUC approval. Direct capital forecast in 2008 dollars (2008-2013).

May 23, 2008

18

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

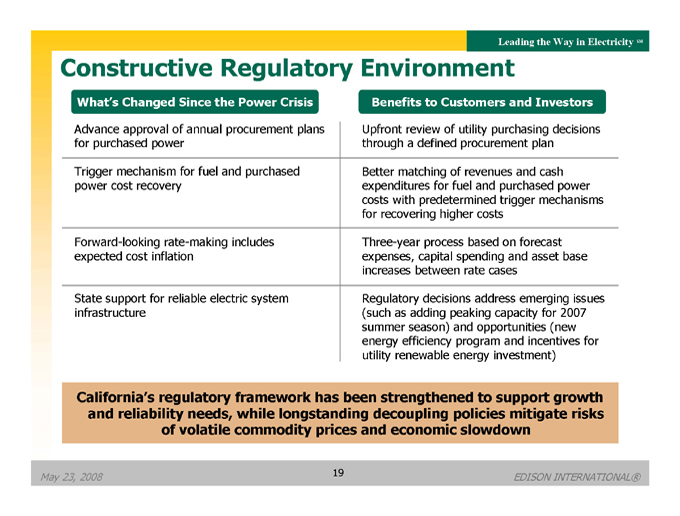

Constructive Regulatory Environment

What’s Changed Since the Power Crisis

Advance approval of annual procurement plans for purchased power

Trigger mechanism for fuel and purchased power cost recovery

Forward-looking rate-making includes expected cost inflation

State support for reliable electric system infrastructure

Benefits to Customers and Investors

Upfront review of utility purchasing decisions through a defined procurement plan

Better matching of revenues and cash expenditures for fuel and purchased power costs with predetermined trigger mechanisms for recovering higher costs

Three-year process based on forecast expenses, capital spending and asset base increases between rate cases

Regulatory decisions address emerging issues (such as adding peaking capacity for 2007 summer season) and opportunities (new energy efficiency program and incentives for utility renewable energy investment)

California’s regulatory framework has been strengthened to support growth and reliability needs, while longstanding decoupling policies mitigate risks of volatile commodity prices and economic slowdown

May 23, 2008

19

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

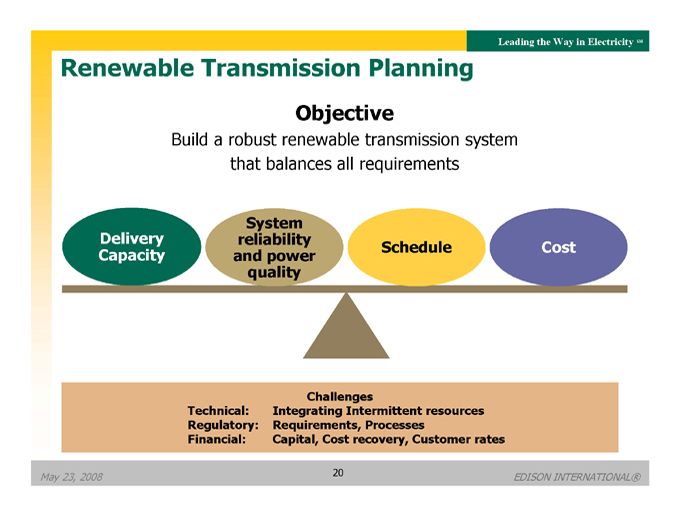

Renewable Transmission Planning

Objective

Build a robust renewable transmission system that balances all requirements

Delivery Capacity

System reliability and power quality

Schedule

Cost

Challenges

Technical: Integrating Intermittent resources Regulatory: Requirements, Processes Financial: Capital, Cost recovery, Customer rates

May 23, 2008

EDISON INTERNATIONAL®

20

Leading the Way in Electricity SM

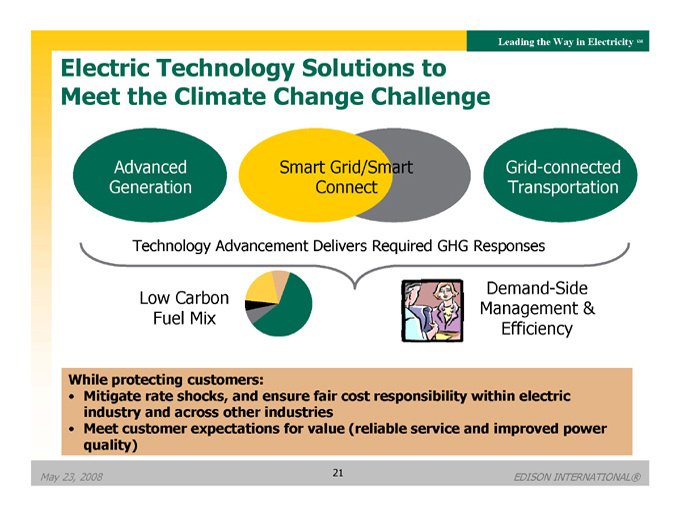

Electric Technology Solutions to Meet the Climate Change Challenge

Advanced Generation

Smart Grid/Smart Connect

Grid-connected Transportation

Technology Advancement Delivers Required GHG Responses

Low Carbon Fuel Mix

Demand-Side Management & Efficiency

While protecting customers:

• Mitigate rate shocks, and ensure fair cost responsibility within electric industry and across other industries

• Meet customer expectations for value (reliable service and improved power quality)

May 23, 2008

EDISON INTERNATIONAL®

21

Leading the Way in Electricity SM

Edison Mission Group (EMG)

A Competitive Power Generation Company

May 23, 2008

EDISON INTERNATIONAL®

22

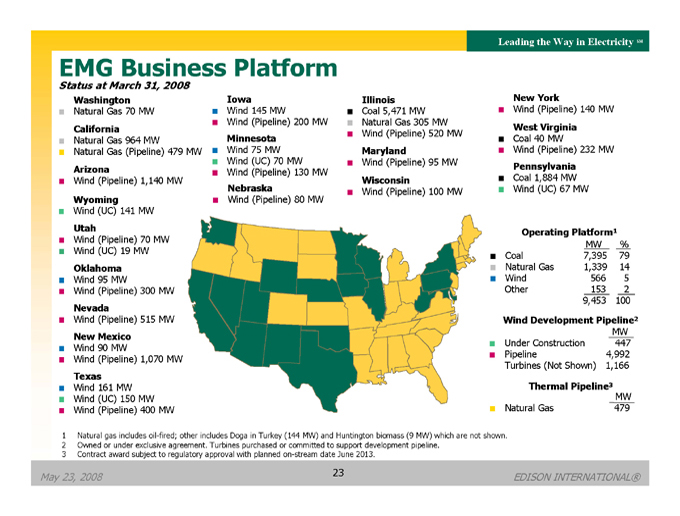

Leading the Way in Electricity SM EMG Business Platform

Status at March 31, 2008 Washington

Natural Gas 70 MW California

Natural Gas 964 MW

Natural Gas (Pipeline) 479 MW Arizona

Wind (Pipeline) 1,140 MW Wyoming

Wind (UC) 141 MW Utah

Wind (Pipeline) 70 MW Wind (UC) 19 MW Oklahoma

Wind 95 MW

Wind (Pipeline) 300 MW Nevada

Wind (Pipeline) 515 MW New Mexico

Wind 90 MW

Wind (Pipeline) 1,070 MW Texas

Wind 161 MW Wind (UC) 150 MW Wind (Pipeline) 400 MW Iowa

Wind 145 MW

Wind (Pipeline) 200 MW Minnesota

Wind 75 MW Wind (UC) 70 MW Wind (Pipeline) 130 MW Nebraska

Wind (Pipeline) 80 MW Illinois

Coal 5,471 MW Natural Gas 305 MW Wind (Pipeline) 520 MW Maryland

Wind (Pipeline) 95 MW Wisconsin

Wind (Pipeline) 100 MW New York

Wind (Pipeline) 140 MW West Virginia Coal 40 MW

Wind (Pipeline) 232 MW Pennsylvania Coal 1,884 MW Wind (UC) 67 MW

Operating Platform1 MW % Coal 7,395 79 Natural Gas 1,339 14 Wind 566 5 Other 153 2 9,453 100

Wind Development Pipeline2 MW Under Construction 447 Pipeline 4,992 Turbines (Not Shown) 1,166 Thermal Pipeline3

MW Natural Gas 479

1 Natural gas includes oil-fired; other includes Doga in Turkey (144 MW) and Huntington biomass (9 MW) which are not shown.

2 Owned or under exclusive agreement. Turbines purchased or committed to support development pipeline.

3 Contract award subject to regulatory approval with planned on-stream date June 2013.

May 23, 2008

EDISON INTERNATIONAL®

23

Leading the Way in Electricity SM

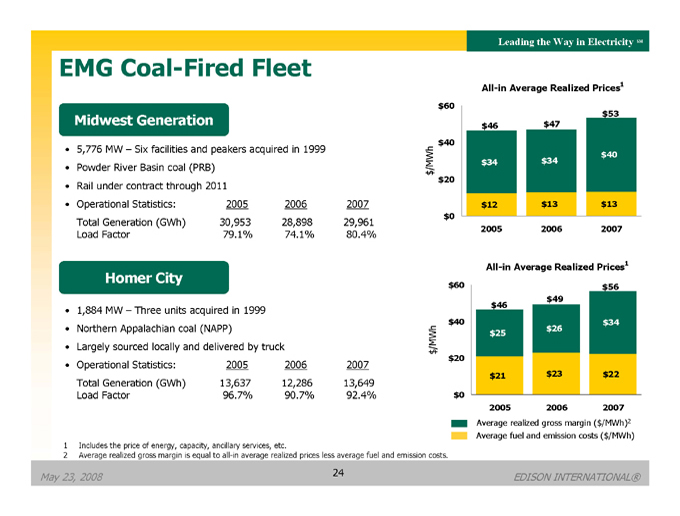

EMG Coal-Fired Fleet

Midwest Generation

5,776 MW – Six facilities and peakers acquired in 1999 Powder River Basin coal (PRB) Rail under contract through 2011

Operational Statistics: 2005 2006 2007 Total Generation (GWh) 30,953 28,898 29,961 Load Factor 79.1% 74.1% 80.4%

Homer City

• 1,884 MW – Three units acquired in 1999

• Northern Appalachian coal (NAPP)

• Largely sourced locally and delivered by truck

• Operational Statistics: 2005 2006 2007 Total Generation (GWh) 13,637 12,286 13,649 Load Factor 96.7% 90.7% 92.4%

All-in Average Realized Prices1

$/MWh $60 $40 $20 $0 $46 $34 $12 $47 $34 $13 $53 $40 $13

2005 2006 2007

All-in Average Realized Prices1

$/MWh $60 $40 $20 $0 $46 $25 $21 $49 $26 $23 $56 $34 $22

2005 2006 2007

Average realized gross margin ($/MWh)2 Average fuel and emission costs ($/MWh)

1 Includes the price of energy, capacity, ancillary services, etc.

2 Average realized gross margin is equal to all-in average realized prices less average fuel and emission costs.

May 23, 2008

24

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

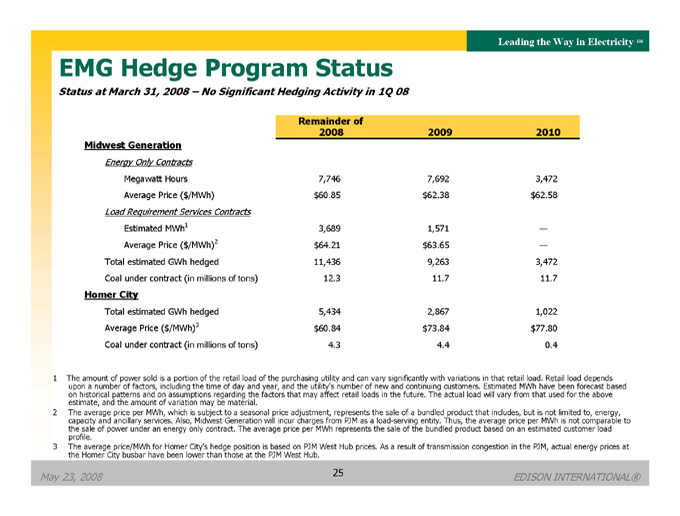

EMG Hedge Program Status

Status at March 31, 2008 – No Significant Hedging Activity in 1Q 08

Remainder of

2008 2009 2010

Midwest Generation

Energy Only Contracts

Megawatt Hours 7,746 7,692 3,472

Average Price ($/MWh) $ 60.85 $ 62.38 $ 62.58

Load Requirement Services Contracts

Estimated MWh1 3,689 1,571 —

Average Price ($/MWh)2 $ 64.21 $ 63.65 —

Total estimated GWh hedged 11,436 9,263 3,472

Coal under contract (in millions of tons) 12.3 11.7 11.7

Homer City

Total estimated GWh hedged 5,434 2,867 1,022

Average Price ($ /MWh)3 $ 60.84 $ 73.84 $ 77.80

Coal under contract ( in millions of tons) 4.3 4.4 0.4

1 The amount of power sold is a portion of the retail load of the purchasing utility and can vary significantly with variations in that retail load. Retail load depends upon a number of factors, including the time of day and year, and the utility’s number of new and continuing customers. Estimated MWh have been forecast based on historical patterns and on assumptions regarding the factors that may affect retail loads in the future. The actual load will vary from that used for the above estimate, and the amount of variation may be material.

2 The average price per MWh, which is subject to a seasonal price adjustment, represents the sale of a bundled product that includes, but is not limited to, energy, capacity and ancillary services. Also, Midwest Generation will incur charges from PJM as a load-serving entity. Thus, the average price per MWh is not comparable to the sale of power under an energy only contract. The average price per MWh represents the sale of the bundled product based on an estimated customer load profile.

3 The average price/MWh for Homer City’s hedge position is based on PJM West Hub prices. As a result of transmission congestion in the PJM, actual energy prices at the Homer City busbar have been lower than those at the PJM West Hub.

May 23, 2008

EDISON INTERNATIONAL®

25

Leading the Way in Electricity SM

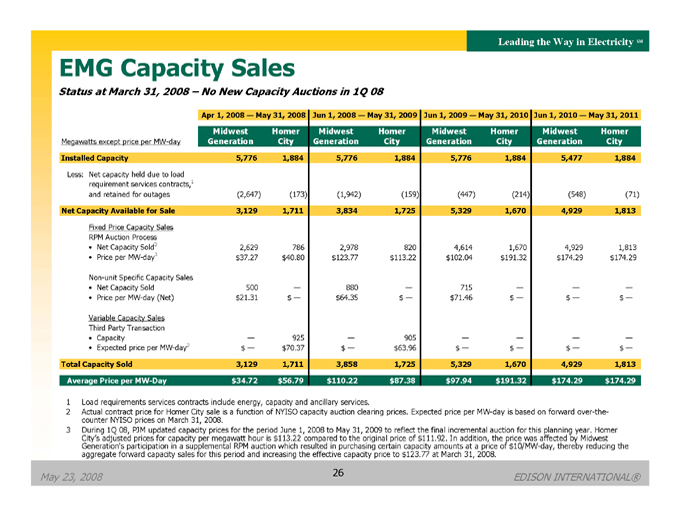

EMG Capacity Sales

Status at March 31, 2008 – No New Capacity Auctions in 1Q 08

Apr 1, 2008 — May 31, 2008 Jun 1, 2008 — May 31, 2009 Jun 1, 2009 — May 31, 2010 Jun 1, 2010 — May 31, 2011

Midwest Homer Midwest Homer Midwest Homer Midwest Homer

Megawatts except price per MW-day Generation City Generation City Generation City Generation City

Installed Capacity 5,776 1,884 5,776 1,884 5,776 1,884 5,477 1,884

Less: Net capacity held due to load requirement services contracts,1

and retained for outages (2,647) (173) (1,942) (159) (447) (214) (548) (71)

Net Capacity Available for Sale 3,129 1,711 3,834 1,725 5,329 1,670 4,929 1,813

Fixed Price Capacity Sales RPM Auction Process

• Net Capacity Sold3 2,629 786 2,978 820 4,614 1,670 4,929 1,813

• Price per MW-day3 $ 37.27 $ 40.80 $ 123.77 $ 113.22 $ 102.04 $ 191.32 $ 174.29 $ 174.29

Non-unit Specific Capacity Sales

• Net Capacity Sold 500 — 880 — 715 — — —

• Price per MW-day (Net) $ 21.31 $ — $ 64.35 $ — $ 71.46 $ — $ — $ —

Variable Capacity Sales Third Party Transaction

• Capacity — 925 — 905 — — — —

• Expected price per MW-day2 $ — $ 70.37 $ — $ 63.96 $ — $ — $ — $ —

Total Capacity Sold 3,129 1,711 3,858 1,725 5,329 1,670 4,929 1,813

Average Price per MW-Day $ 34.72 $ 56.79 $ 110.22 $ 87.38 $ 97.94 $ 191.32 $ 174.29 $ 174.29

1 Load requirements services contracts include energy, capacity and ancillary services.

2 Actual contract price for Homer City sale is a function of NYISO capacity auction clearing prices. Expected price per MW-day is based on forward over-the-counter NYISO prices on March 31, 2008.

3 During 1Q 08, PJM updated capacity prices for the period June 1, 2008 to May 31, 2009 to reflect the final incremental auction for this planning year. Homer City’s adjusted prices for capacity per megawatt hour is $113.22 compared to the original price of $111.92. In addition, the price was affected by Midwest Generation’s participation in a supplemental RPM auction which resulted in purchasing certain capacity amounts at a price of $10/MW-day, thereby reducing the aggregate forward capacity sales for this period and increasing the effective capacity price to $123.77 at March 31, 2008.

May 23, 2008

EDISON INTERNATIONAL®

26

Leading the Way in Electricity SM

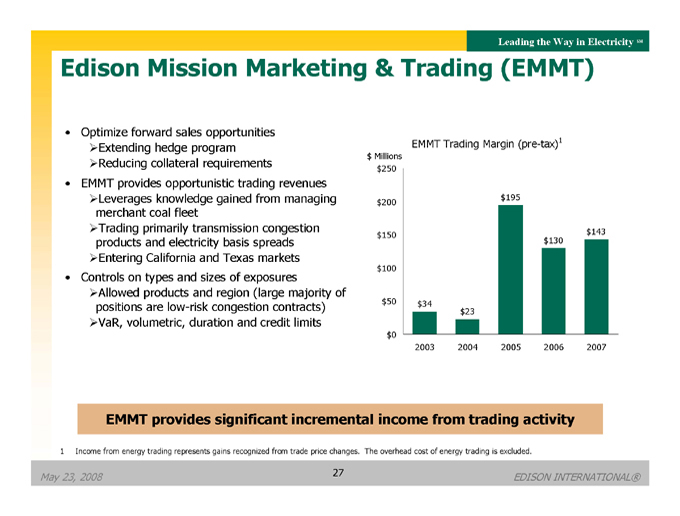

Edison Mission Marketing & Trading (EMMT)

• Optimize forward sales opportunities

Extending hedge program

Reducing collateral requirements

• EMMT provides opportunistic trading revenues

Leverages knowledge gained from managing merchant coal fleet

Trading primarily transmission congestion products and electricity basis spreads

Entering California and Texas markets

• Controls on types and sizes of exposures

Allowed products and region (large majority of positions are low-risk congestion contracts)

VaR, volumetric, duration and credit limits

EMMT Trading Margin (pre-tax)1

$ Millions

$250 $200 $150 $100 $50 $0 $34 $23 $195 $130 $143

2003 2004 2005 2006 2007

EMMT provides significant incremental income from trading activity

1 Income from energy trading represents gains recognized from trade price changes. The overhead cost of energy trading is excluded. May 23, 2008

EDISON INTERNATIONAL®

27

Leading the Way in Electricity SM

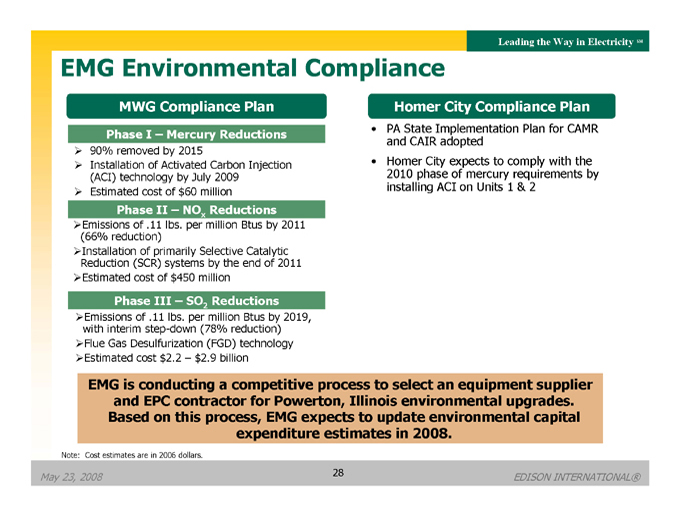

EMG Environmental Compliance

MWG Compliance Plan

Phase I – Mercury Reductions

90% removed by 2015

Installation of Activated Carbon Injection (ACI) technology by July 2009

Estimated cost of $60 million

Phase II – NOx Reductions

Emissions of .11 lbs. per million Btus by 2011 (66% reduction)

Installation of primarily Selective Catalytic Reduction (SCR) systems by the end of 2011

Estimated cost of $450 million

Phase III – SO2 Reductions

Emissions of .11 lbs. per million Btus by 2019, with interim step-down (78% reduction)

Flue Gas Desulfurization (FGD) technology

Estimated cost $2.2 – $2.9 billion

Homer City Compliance Plan

PA State Implementation Plan for CAMR and CAIR adopted Homer City expects to comply with the 2010 phase of mercury requirements by installing ACI on Units 1 & 2

EMG is conducting a competitive process to select an equipment supplier and EPC contractor for Powerton, Illinois environmental upgrades.

Based on this process, EMG expects to update environmental capital expenditure estimates in 2008.

Note: Cost estimates are in 2006 dollars.

May 23, 2008

EDISON INTERNATIONAL®

28

Leading the Way in Electricity SM

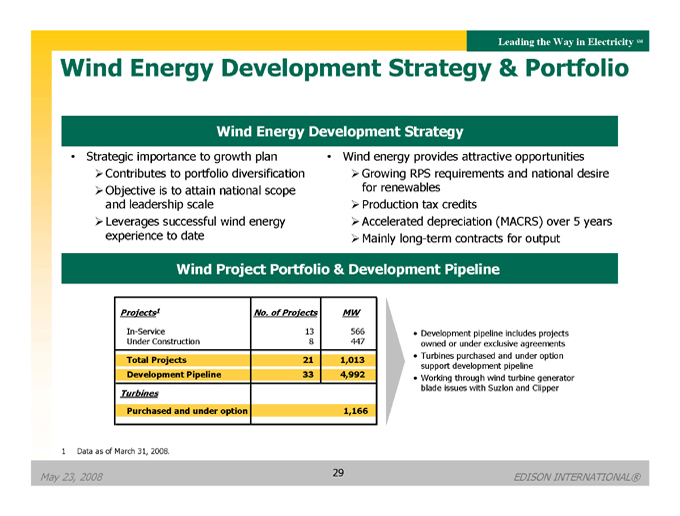

Wind Energy Development Strategy & Portfolio

Wind Energy Development Strategy

• Strategic importance to growth plan

Contributes to portfolio diversification

Objective is to attain national scope and leadership scale

Leverages successful wind energy experience to date

Wind energy provides attractive opportunities

Growing RPS requirements and national desire for renewables

Production tax credits

Accelerated depreciation (MACRS) over 5 years

Mainly long-term contracts for output

Wind Project Portfolio & Development Pipeline

Projects1 No. of Projects MW

In-Service 13 566

Under Construction 8 447

Total Projects 21 1,013

Development Pipeline 33 4,992

Turbines

Purchased and under option 1,166

• Development pipeline includes projects owned or under exclusive agreements

• Turbines purchased and under option support development pipeline

• Working through wind turbine generator blade issues with Suzlon and Clipper

1 Data as of March 31, 2008.

May 23, 2008

EDISON INTERNATIONAL®

29

Leading the Way in Electricity SM

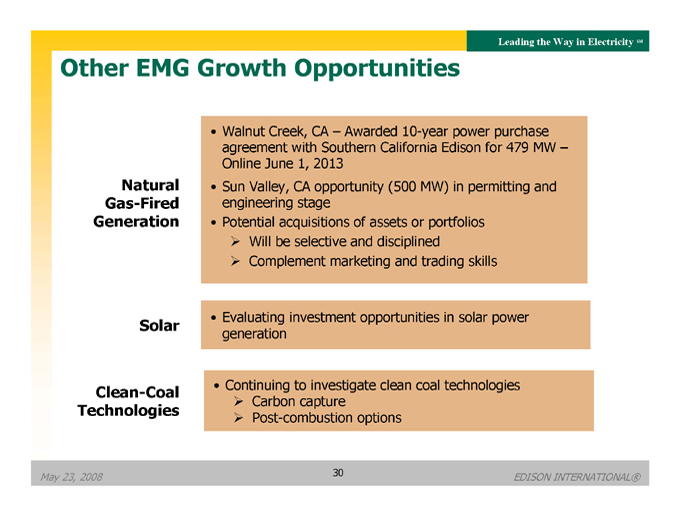

Other EMG Growth Opportunities

Natural Gas-Fired Generation

• Walnut Creek, CA – Awarded 10-year power purchase agreement with Southern California Edison for 479 MW – Online June 1, 2013

Sun Valley, CA opportunity (500 MW) in permitting and engineering stage

Potential acquisitions of assets or portfolios

Will be selective and disciplined

Complement marketing and trading skills

Solar

Evaluating investment opportunities in solar power generation

Clean-Coal Technologies

Continuing to investigate clean coal technologies

Carbon capture

Post-combustion options

May 23, 2008

30

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Our Shareholder Value Proposition

• Attractive business portfolio and growth opportunities

• Southern California Edison

Demonstrated need for utility infrastructure investments

Among the best domestic electric utility growth platforms

Leadership in environmental and alternative energy programs (energy efficiency, renewable energy, advanced technologies)

• Edison Mission Group

Favorable market conditions for unregulated generation portfolio

Strong growth pipeline led by renewable investments

• Commitment to long-term shareholder value creation

• Incentive compensation and stock ownership guidelines consistent with shareholder interests

• Edison people committed to excellence in safety and customer service

May 23, 2008

EDISON INTERNATIONAL®

31

Leading the Way in Electricity SM

Appendix

May 23, 2008

32

EDISON INTERNATIONAL®

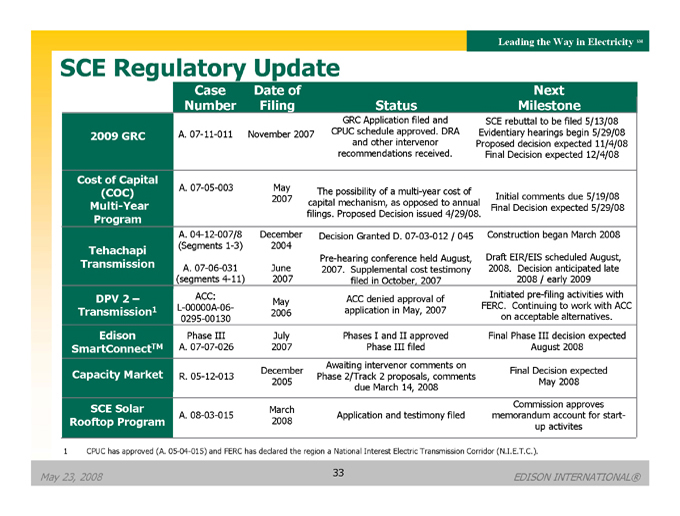

Leading the Way in Electricity SM SCE Regulatory Update Case Date of Next Number Filing Status Milestone

GRC Application filed and SCE rebuttal to be filed 5/13/08

2009 GRC A. 07-11-011 November 2007 CPUC schedule approved. DRA Evidentiary hearings begin 5/29/08

and other intervenor Proposed decision expected 11/4/08

recommendations received. Final Decision expected 12/4/08 Cost of Capital

(COC) A. 07-05-003 May The possibility of a multi-year cost of 2007 Initial comments due 5/19/08

Multi-Year capital mechanism, as opposed to annual Final Decision expected 5/29/08

Program filings. Proposed Decision issued 4/29/08.

A. 04-12-007/8 December Decision Granted D. 07-03-012 / 045 Construction began March 2008

Tehachapi (Segments 1-3) 2004 Pre-hearing conference held August, Draft EIR/EIS scheduled August,

Transmission A. 07-06-031 June 2008. Decision anticipated late 2007. Supplemental cost testimony

(segments 4-11) 2007 filed in October, 2007 2008 / early 2009

DPV 2 – ACC: ACC denied approval of Initiated pre-filing activities with May FERC. Continuing to work with ACC

Transmission1 L-00000A-06- application in May, 2007 2006 on acceptable alternatives. 0295-00130

Edison Phase III July Phases I and II approved Final Phase III decision expected

SmartConnectTM A. 07-07-026 2007 Phase III filed August 2008 Awaiting intervenor comments on

Capacity Market December Final Decision expected

R. 05-12-013 Phase 2/Track 2 proposals, comments 2005 May 2008 due March 14, 2008

SCE Solar Commission approves

March

A. 08-03-015 Application and testimony filed memorandum account for start-

Rooftop Program 2008

up activites

1 CPUC has approved (A. 05-04-015) and FERC has declared the region a National Interest Electric Transmission Corridor (N.I.E.T.C.).

May 23, 2008

33

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

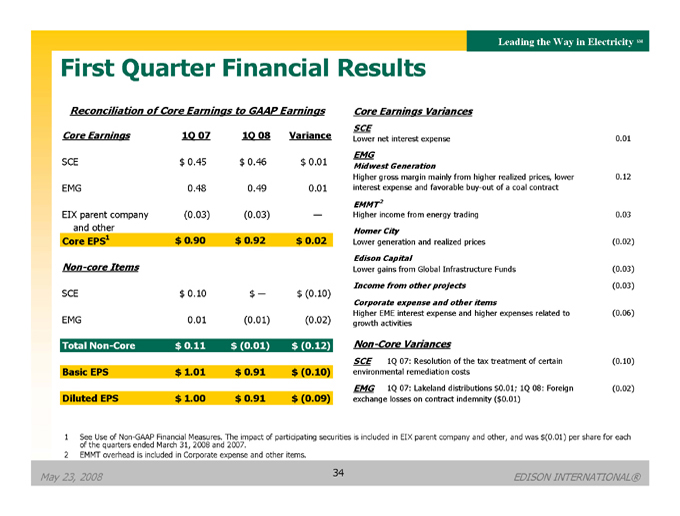

First Quarter Financial Results

Reconciliation of Core Earnings to GAAP Earnings

Core Earnings 1Q 07 1Q 08 Variance

SCE $ 0.45 $ 0.46 $ 0.01

EMG 0.48 0.49 0.01

EIX parent company (0.03) (0.03) — and other

Core EPS1 $ 0.90 $ 0.92 $ 0.02

Non-core Items

SCE $ 0.10 $ — $ (0.10)

EMG 0.01 (0.01) (0.02)

Total Non-Core $ 0.11 $ (0.01) $ (0.12)

Basic EPS $ 1.01 $ 0.91 $ (0.10)

Diluted EPS $ 1.00 $ 0.91 $ (0.09)

Core Earnings Variances SCE

Lower net interest expense 0.01 EMG

Midwest Generation

Higher gross margin mainly from higher realized prices, lower 0.12

interest expense and favorable buy-out of a coal contract EMMT2

Higher income from energy trading 0.03 Homer City

Lower generation and realized prices (0.02) Edison Capital

Lower gains from Global Infrastructure Funds (0.03)

Income from other projects (0.03) Corporate expense and other items

Higher EME interest expense and higher expenses related to (0.06) growth activities Non-Core Variances

SCE 1Q 07: Resolution of the tax treatment of certain (0.10)

environmental remediation costs

EMG 1Q 07: Lakeland distributions $ 0.01; 1Q 08: Foreign (0.02)

exchange losses on contract indemnity ($ 0.01)

1 See Use of Non-GAAP Financial Measures. The impact of participating securities is included in EIX parent company and other, and was $(0.01) per share for each of the quarters ended March 31, 2008 and 2007.

2 EMMT overhead is included in Corporate expense and other items.

May 23, 2008

EDISON INTERNATIONAL®

34

Leading the Way in Electricity SM

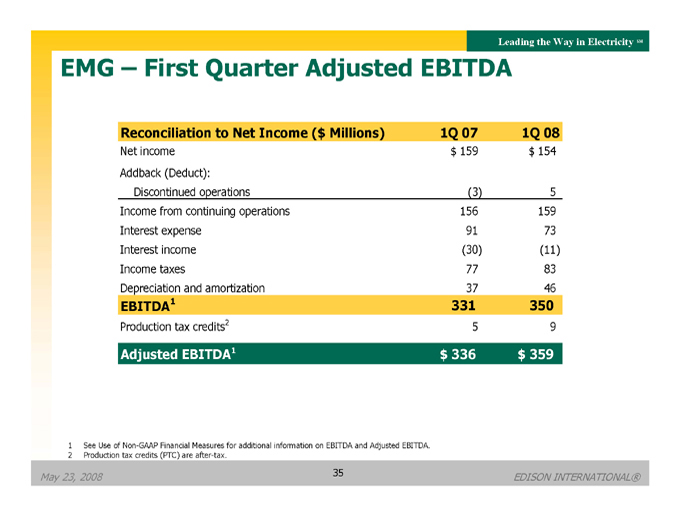

EMG – First Quarter Adjusted EBITDA

Reconciliation to Net Income ($Millions) 1Q 07 1Q 08

Net income $159 $154

Addback (Deduct):

Discontinued operations (3) 5

Income from continuing operations 156 159

Interest expense 91 73

Interest income (30) (11)

Income taxes 77 83

Depreciation and amortization 37 46

EBITDA1 331 350

Production tax credits2 5 9

Adjusted EBITDA1 $336 $359

1 See Use of Non-GAAP Financial Measures for additional information on EBITDA and Adjusted EBITDA.

2 Production tax credits (PTC) are after-tax.

May 23, 2008

35

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

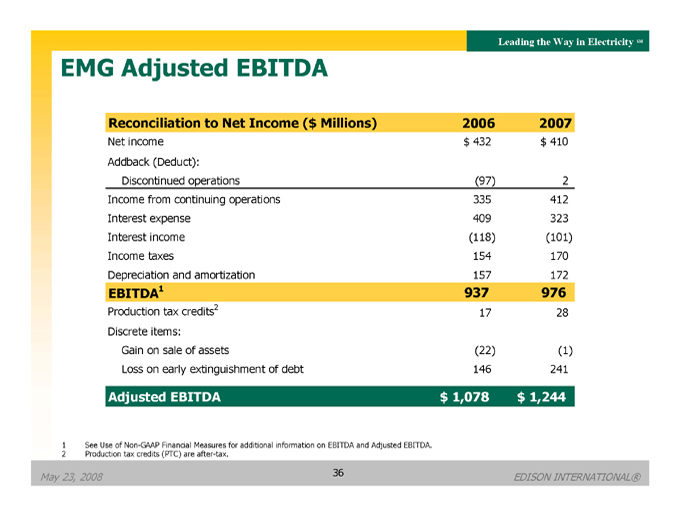

EMG Adjusted EBITDA

Reconciliation to Net Income ($Millions) 2006 2007

Net income $432 $410

Addback (Deduct):

Discontinued operations (97) 2

Income from continuing operations 335 412

Interest expense 409 323

Interest income (118) (101)

Income taxes 154 170

Depreciation and amortization 157 172

EBITDA1 937 976

Production tax credits2 17 28

Discrete items:

Gain on sale of assets (22) (1)

Loss on early extinguishment of debt 146 241

Adjusted EBITDA $1,078 $1,244

1 See Use of Non-GAAP Financial Measures for additional information on EBITDA and Adjusted EBITDA.

2 Production tax credits (PTC) are after-tax.

May 23, 2008

36

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

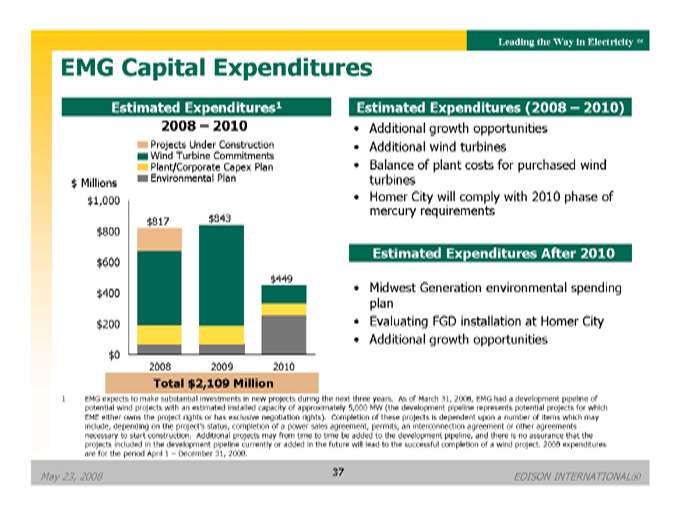

EMG Capital Expenditures

Estimated Expenditures1 2008 – 2010

Projects Under Construction Wind Turbine Commitments Plant/Corporate Capex Plan Environmental Plan

$ Millions $1,000 $800 $600 $400 $200 $0 $817 $843 $449

2008 2009 2010

Total $2,109 Million

Estimated Expenditures (2008 – 2010)

• Additional growth opportunities

• Additional wind turbines

• Balance of plant costs for purchased wind turbines

• Homer City will comply with 2010 phase of mercury requirements

Estimated Expenditures After 2010

• Midwest Generation environmental spending plan

• Evaluating FGD installation at Homer City

• Additional growth opportunities

1 EMG expects to make substantial investments in new projects during the next three years. As of March 31, 2008, EMG had a development pipeline of potential wind projects with an estimated installed capacity of approximately 5,000 MW (the development pipeline represents potential projects for which EME either owns the project rights or has exclusive negotiation rights). Completion of these projects is dependent upon a number of items which may include, depending on the project’s status, completion of a power sales agreement, permits, an interconnection agreement or other agreements necessary to start construction. Additional projects may from time to time be added to the development pipeline, and there is no assurance that the projects included in the development pipeline currently or added in the future will lead to the successful completion of a wind project. 2008 expenditures are for the period April 1 – December 31, 2008.

May 23, 2008

37

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

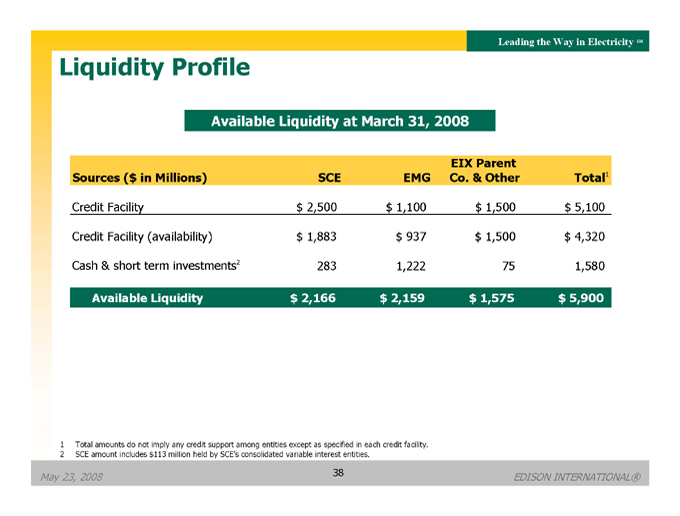

Liquidity Profile

Available Liquidity at March 31, 2008

EIX Parent

Sources ($ in Millions) SCE EMG Co. & Other Total1

Credit Facility $2,500 $1,100 $1,500 $5,100

Credit Facility (availability) $ 1,883 $ 937 $ 1,500 $ 4,320

Cash & short term investments2 283 1,222 75 1,580

Available Liquidity $2,166 $2,159 $1,575 $5,900

1 Total amounts do not imply any credit support among entities except as specified in each credit facility.

2 SCE amount includes $113 million held by SCE’s consolidated variable interest entities.

May 23, 2008

38

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

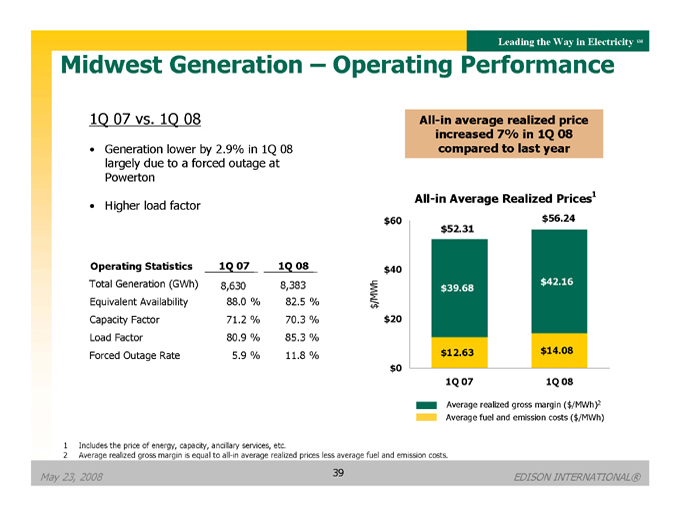

Midwest Generation – Operating Performance

1Q 07 vs. 1Q 08

Generation lower by 2.9% in 1Q 08 largely due to a forced outage at Powerton

Higher load factor

Operating Statistics 1Q 07 1Q 08

Total Generation (GWh) 8,630 8,383 Equivalent Availability 88.0% 82.5% Capacity Factor 71.2% 70.3% Load Factor 80.9% 85.3% Forced Outage Rate 5.9% 11.8%

All-in average realized price increased 7% in 1Q 08 compared to last year

All-in Average Realized Prices1

/MWh $ $20 $60 $40 $0 $52.31 $39.68 $12.63 $56.24 $42.16 $14.08

1Q 08 1Q 07

Average realized gross margin ($/MWh)2 Average fuel and emission costs ($/MWh)

1 Includes the price of energy, capacity, ancillary services, etc.

2 Average realized gross margin is equal to all-in average realized prices less average fuel and emission costs.

May 23, 2008

39

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

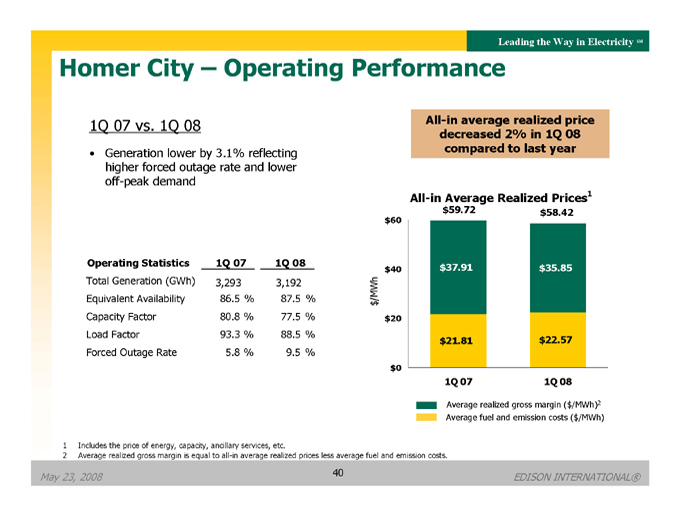

Homer City – Operating Performance

1Q 07 vs. 1Q 08

• Generation lower by 3.1% reflecting higher forced outage rate and lower off-peak demand

Operating Statistics 1Q 07 1Q 08

Total Generation (GWh) 3,293 3,192 Equivalent Availability 86.5% 87.5% Capacity Factor 80.8% 77.5% Load Factor 93.3% 88.5% Forced Outage Rate 5.8% 9.5%

All-in average realized price decreased 2% in 1Q 08 compared to last year

All-in Average Realized Prices1

$/MWh

$60 $40 $20 $0 $59.72 $37.91 $21.81 1Q 07

$58.42 $35.85 $22.57 1Q 08

Average realized gross margin ($/MWh)2 Average fuel and emission costs ($/MWh)

1 Includes the price of energy, capacity, ancillary services, etc.

2 Average realized gross margin is equal to all-in average realized prices less average fuel and emission costs.

May 23, 2008

40

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Use of Non-GAAP Financial Measures

Edison International’s earnings are prepared in accordance with generally accepted accounting principles used in the United States and represent the company’s earnings as reported to the Securities and Exchange Commission. Our management uses core earnings and EPS by principal operating subsidiary internally for financial planning and for analysis of performance. We also use core earnings and EPS by principal operating subsidiary as primary performance measurements when communicating with analysts and investors regarding our earnings results and outlook, as it allows us to more accurately compare the company’s ongoing performance across periods. Core earnings exclude discontinued operations and other non-core items and are reconciled to basic earnings per common share.

EPS by principal operating subsidiary is based on the principal operating subsidiary net income and Edison International’s weighted average outstanding common shares. The impact of participating securities (vested stock options that earn dividend equivalents that may participate in undistributed earnings with common stock) for each principal operating subsidiary is not material to each principal operating subsidiary’s EPS and is therefore reflected in the results of the Edison International holding company, which we refer to as EIX parent company. EPS and core EPS by principal operating subsidiary are reconciled to basic earnings per common share.

EBITDA is defined as earnings before interest, income taxes, depreciation and amortization. Adjusted EBITDA includes production tax credits from EMG’s wind projects and excludes amounts from gain on the sale of assets, loss on early extinguishment of debt and leases, and impairment of assets and investments. Our management uses Adjusted EBITDA as an important financial measure for evaluating EMG.

A reconciliation of Non-GAAP information to GAAP information, including the impact of participating securities, is included either on the slide where the information appears or on another slide referenced in the presentation.

May 23, 2008

41

EDISON INTERNATIONAL®