Exhibit 99.1

Exhibit 99.1

Leading the Way in Electricity SM

EDISON INTERNATIONAL®

Business Update

March 2009

March 16, 2009

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Forward-Looking Statements

Statements contained in this presentation about future performance, including, without limitation, earnings, asset and rate base growth, load growth, capital investments, and other statements that are not purely historical, are forward-looking statements. These forward-looking statements reflect our current expectations; however, such statements involve risks and uncertainties. Actual results could differ materially from current expectations. Important factors that could cause different results are discussed under the headings “Risk Factors” and “Management’s Discussion and Analysis” in Edison International’s 2008 Form 10-K and other reports filed with the Securities and Exchange Commission are available on our website: www.edisoninvestor.com. These forward-looking statements represent our expectations only as of the date of this presentation, and Edison International assumes no duty to update them to reflect new information, events or circumstances.

March 16, 2009

EDISON INTERNATIONAL®

Value Drivers

Southern California Edison (SCE)

Rate base growth of 10-13% (CAGR)

3-year Cost of Capital mechanism (11.5% ROCE)

Decoupled CPUC revenue model

Pass through mechanisms for fuel and purchased power, pensions

Growth options: transmission, utility owned generation, Edison SmartConnectTM

Strong financial position

Strong public policy support

Leading the Way in Electricity SM

Edison Mission Group (EMG)

Option for commodity cycle upside or improving reserve margins

Renewables growth opportunities

5,000 MW wind pipeline

Solar development program

Current stable financial condition

No significant bond maturities until 2013

Structurally separate from EIX/SCE

Disciplined approach to coal fleet environmental investments

Flexible business platform

March 16, 2009

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Southern California Edison (SCE)

March 16, 2009

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

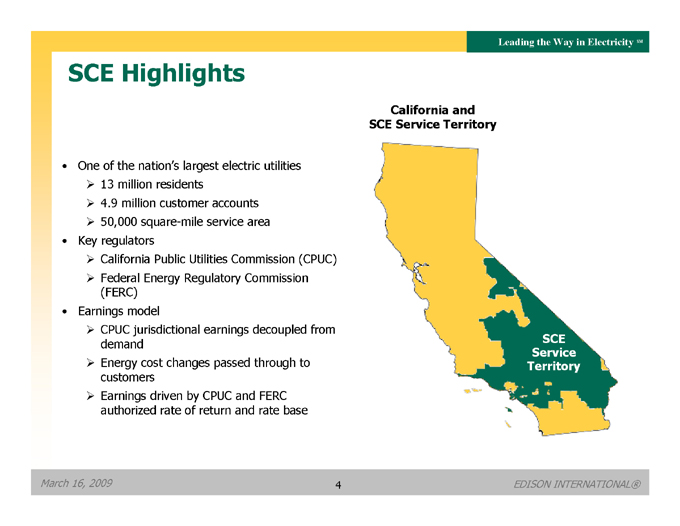

SCE Highlights

California and

SCE Service Territory

One of the nation’s largest electric utilities

13 million residents

4.9 million customer accounts

50,000 square-mile service area

Key regulators

California Public Utilities Commission (CPUC)

Federal Energy Regulatory Commission (FERC)

Earnings model

CPUC jurisdictional earnings decoupled from demand

Energy cost changes passed through to customers

Earnings driven by CPUC and FERC authorized rate of return and rate base

SCE Service Territory

March 16, 2009

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

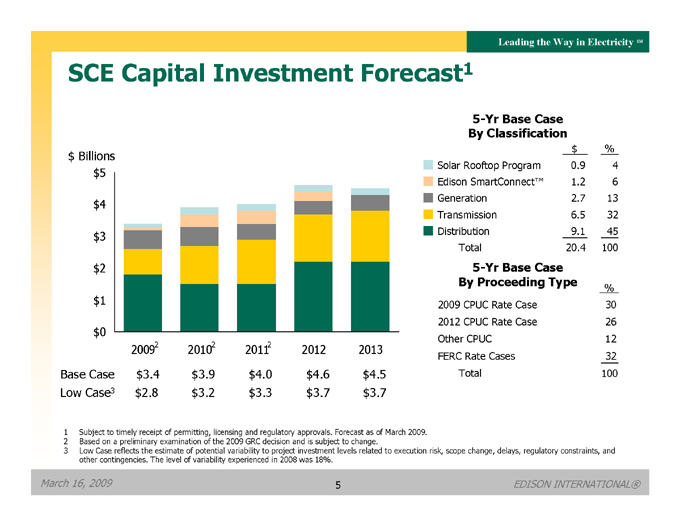

SCE Capital Investment Forecast1

5-Yr Base Case By Classification

$ Billions $5 $4 $3 $2 $1 $0 20092 20102 20112 2012 2013

Base Case $3.4 $3.9 $4.0 $4.6 $4.5

Low Case3 $2.8 $3.2 $3.3 $3.7 $3.7

$ %

Solar Rooftop Program 0.9 4

Edison SmartConnect™ 1.2 6

Generation 2.7 13

Transmission

6.5 32

Distribution 9.1 45

Total 20.4 100

5-Yr Base Case By Proceeding Type

%

2009 CPUC Rate Case 30

2012 CPUC Rate Case 26

Other CPUC 12

FERC Rate Cases 32

Total 100

1 Subject to timely receipt of permitting, licensing and regulatory approvals. Forecast as of March 2009.

2 Based on a preliminary examination of the 2009 GRC decision and is subject to change.

3 Low Case reflects the estimate of potential variability to project investment levels related to execution risk, scope change, delays, regulatory constraints, and other contingencies. The level of variability experienced in 2008 was 18%.

March 16, 2009

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

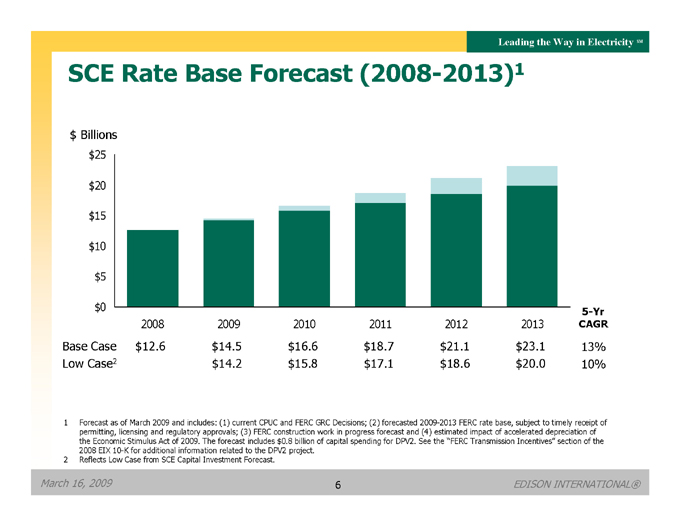

SCE Rate Base Forecast (2008-2013)1

$ Billions

$25

$20 $15 $10 $5 $0

5-Yr CAGR

2008 2009 2010 2011 2012 2013

Base Case $12.6 $14.5 $16.6 $18.7 $21.1 $23.1 13%

Low Case2 $14.2 $15.8 $17.1 $18.6 $20.0 10%

1 Forecast as of March 2009 and includes: (1) current CPUC and FERC GRC Decisions; (2) forecasted 2009-2013 FERC rate base, subject to timely receipt of permitting, licensing and regulatory approvals; (3) FERC construction work in progress forecast and (4) estimated impact of accelerated depreciation of the Economic Stimulus Act of 2009. The forecast includes $0.8 billion of capital spending for DPV2. See the “FERC Transmission Incentives” section of the 2008 EIX 10-K for additional information related to the DPV2 project.

2 Reflects Low Case from SCE Capital Investment Forecast.

March 16, 2009

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

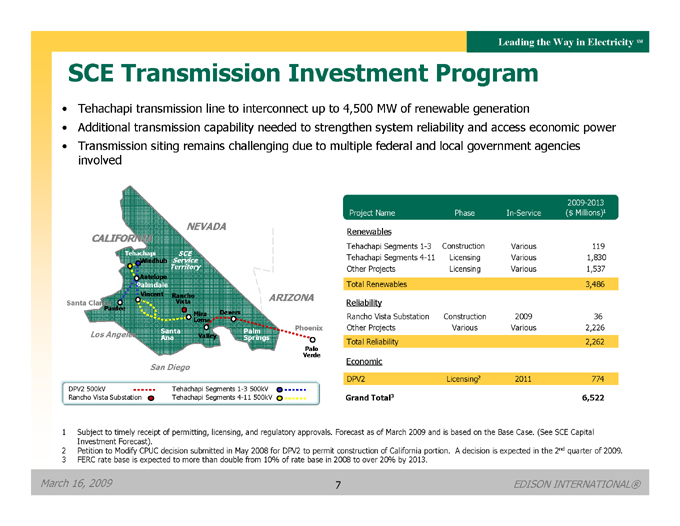

SCE Transmission Investment Program

Tehachapi transmission line to interconnect up to 4,500 MW of renewable generation

Additional transmission capability needed to strengthen system reliability and access economic power

Transmission siting remains challenging due to multiple federal and local government agencies involved

NEVADA CALIFORNIA

Tehachapi Service SCE

Windhub

Territory

Antelope Palmdale

Vincent Rancho ARIZONA Santa Clarita Vista Pardee Mira Devers Loma Santa Palm Phoenix

Los Angeles Ana Valley Springs

Verde Palo

San Diego

DPV2 500kV Tehachapi Segments 1-3 500kV Rancho Vista Substation Tehachapi Segments 4-11 500kV

Project Name

Phase

In-Service

2009-2013 ($ Millions)1

Renewables

Tehachapi Segments 1-3

Construction

Various

119

Tehachapi Segments 4-11

Licensing

Various

1,830

Other Projects

Licensing

Various

1,537

Total Renewables

3,486

Reliability

Rancho Vista Substation

Construction

2009

36

Other Projects

Various

Various

2,226

Total Reliability

2,262

Economic

DPV2

Licensing2

2011

774

Grand Total3

6,522

1 Subject to timely receipt of permitting, licensing, and regulatory approvals. Forecast as of March 2009 and is based on the Base Case. (See SCE Capital Investment Forecast).

2 Petition to Modify CPUC decision submitted in May 2008 for DPV2 to permit construction of California portion. A decision is expected in the 2nd quarter of 2009.

3 FERC rate base is expected to more than double from 10% of rate base in 2008 to over 20% by 2013.

March 16, 2009

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

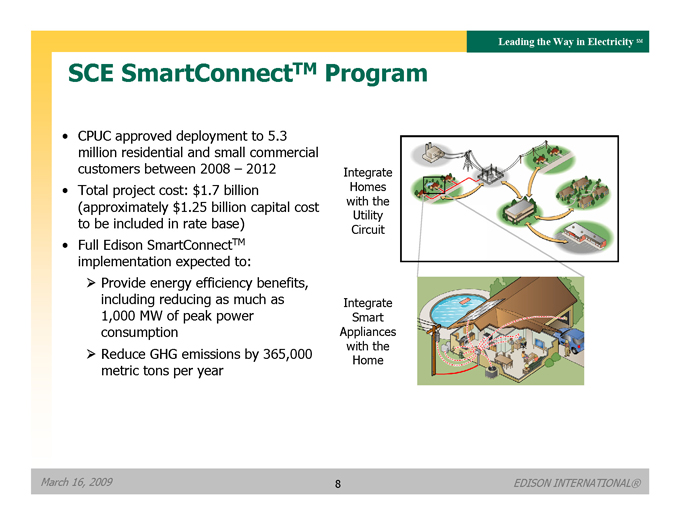

SCE SmartConnectTM Program

Integrate Homes with the Utility Circuit

Integrate Smart Appliances with the Home

CPUC approved deployment to 5.3 million residential and small commercial customers between 2008 – 2012

Total project cost: $1.7 billion (approximately $1.25 billion capital cost to be included in rate base)

Full Edison SmartConnectTM implementation expected to:

Provide energy efficiency benefits, including reducing as much as 1,000 MW of peak power consumption

Reduce GHG emissions by 365,000 metric tons per year

March 16, 2009

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

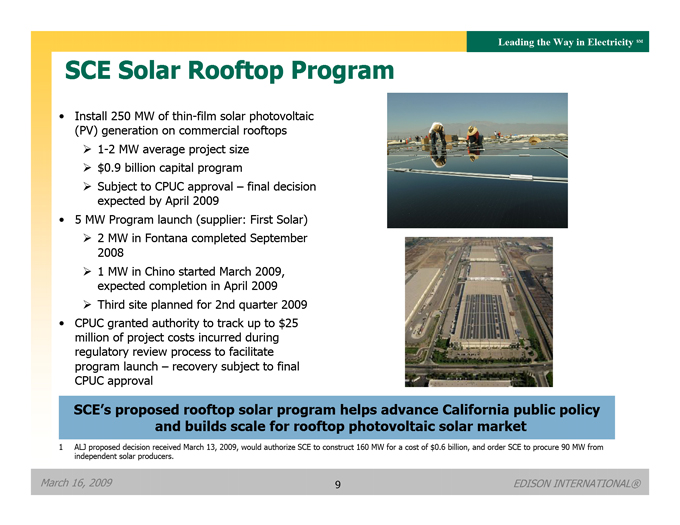

SCE Solar Rooftop Program

Install 250 MW of thin-film solar photovoltaic (PV) generation on commercial rooftops

1-2 MW average project size

$0.9 billion capital program

Subject to CPUC approval – final decision expected by April 2009

5 MW Program launch (supplier: First Solar)

2 MW in Fontana completed September 2008

1 MW in Chino started March 2009, expected completion in April 2009

Third site planned for 2nd quarter 2009

CPUC granted authority to track up to $25 million of project costs incurred during regulatory review process to facilitate program launch – recovery subject to final CPUC approval

SCE’s proposed rooftop solar program helps advance California public policy and builds scale for rooftop photovoltaic solar market

1 ALJ proposed decision received March 13, 2009, would authorize SCE to construct 160 MW for a cost of $0.6 billion, and order SCE to procure 90 MW from independent solar producers.

March 16, 2009

9

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Edison Mission Group (EMG)

March 16, 2009

10

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

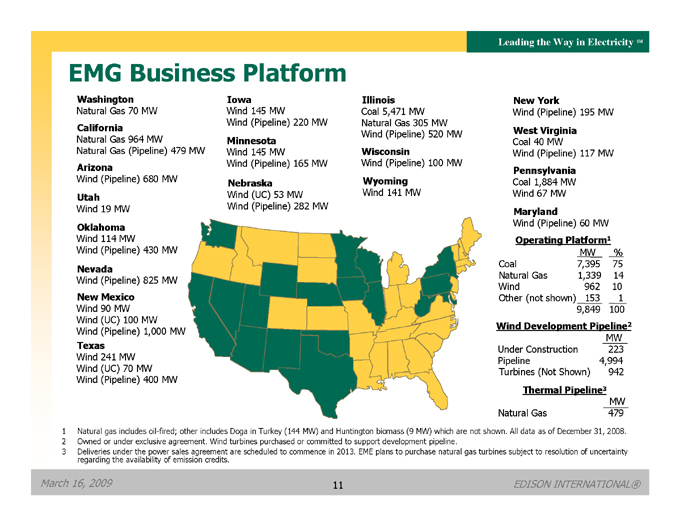

EMG Business Platform

Washington

Natural Gas 70 MW

California

Natural Gas 964 MW

Natural Gas (Pipeline) 479 MW

Arizona

Wind (Pipeline) 680 MW

Utah

Wind 19 MW

Oklahoma

Wind 114 MW

Wind (Pipeline) 430 MW

Nevada

Wind (Pipeline) 825 MW

New Mexico

Wind 90 MW

Wind (UC) 100 MW

Wind (Pipeline) 1,000 MW

Texas

Wind 241 MW

Wind (UC) 70 MW

Wind (Pipeline) 400 MW

Iowa

Wind 145 MW

Wind (Pipeline) 220 MW

Minnesota

Wind 145 MW

Wind (Pipeline) 165 MW

Nebraska

Wind (UC) 53 MW

Wind (Pipeline) 282 MW

Illinois

Coal 5,471 MW

Natural Gas 305 MW

Wind (Pipeline) 520 MW

Wisconsin

Wind (Pipeline) 100 MW

Wyoming

Wind 141 MW

New York

Wind (Pipeline) 195 MW

West Virginia

Coal 40 MW

Wind (Pipeline) 117 MW

Pennsylvania

Coal 1,884 MW

Wind 67 MW

Maryland

Wind (Pipeline) 60 MW

Operating Platform1

MW

%

Coal

7,395

75

Natural Gas

1,339

14

Wind

962

10

Other (not shown)

153

1

9,849

100

Wind Development Pipeline2

MW

Under Construction

223

Pipeline

4,994

Turbines (Not Shown)

942

Thermal Pipeline3

MW

Natural Gas

479

| | 1 | | Natural gas includes oil-fired; other includes Doga in Turkey (144 MW) and Huntington biomass (9 MW) which are not shown. All data as of December 31, 2008. |

| | 2 | | Owned or under exclusive agreement. Wind turbines purchased or committed to support development pipeline. |

| | 3 | | Deliveries under the power sales agreement are scheduled to commence in 2013. EME plans to purchase natural gas turbines subject to resolution of uncertainty regarding the availability of emission credits. |

March 16, 2009

11

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

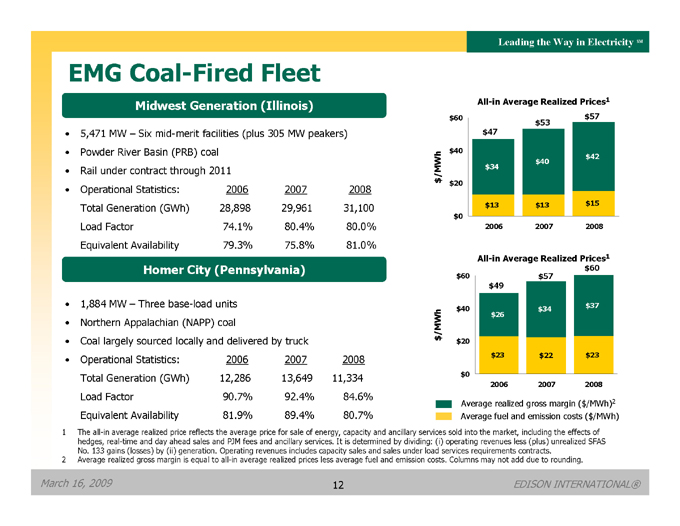

EMG Coal-Fired Fleet

Midwest Generation (Illinois) All-in Average Realized Prices1

• 5,471 MW – Six mid-merit facilities (plus 305 MW peakers)

• Powder River Basin (PRB) coal

• Rail under contract through 2011

$60 $57 $53

$47

$40 $42

$40

$/MWh $34

$20

$13 $13 $15

$0

2006 2007 2008

All-in Average Realized Prices1

$60

$60 $57

$49

Homer City (Pennsylvania)

• Operational Statistics:

2006

2007

2008

Total Generation (GWh)

28,898

29,961

31,100

Load Factor

74.1%

80.4%

80.0%

Equivalent Availability

79.3%

75.8%

81.0%

• 1,884 MW – Three base-load units

• Northern Appalachian (NAPP) coal

• Coal largely sourced locally and delivered by truck

$40 $34 $37

$26

$/MWh

$20

$23 $22 $23

$0 2006 2007 2008

Average realized gross margin ($/MWh)2

Average fuel and emission costs ($/MWh)

• Operational Statistics:

2006

2007

2008

Total Generation (GWh)

12,286

13,649

11,334

Load Factor

90.7%

92.4%

84.6%

Equivalent Availability

81.9%

89.4%

80.7%

1 The all-in average realized price reflects the average price for sale of energy, capacity and ancillary services sold into the market, including the effects of hedges, real-time and day ahead sales and PJM fees and ancillary services. It is determined by dividing: (i) operating revenues less (plus) unrealized SFAS No. 133 gains (losses) by (ii) generation. Operating revenues includes capacity sales and sales under load services requirements contracts.

2 Average realized gross margin is equal to all-in average realized prices less average fuel and emission costs. Columns may not add due to rounding.

March 16, 2009

12

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

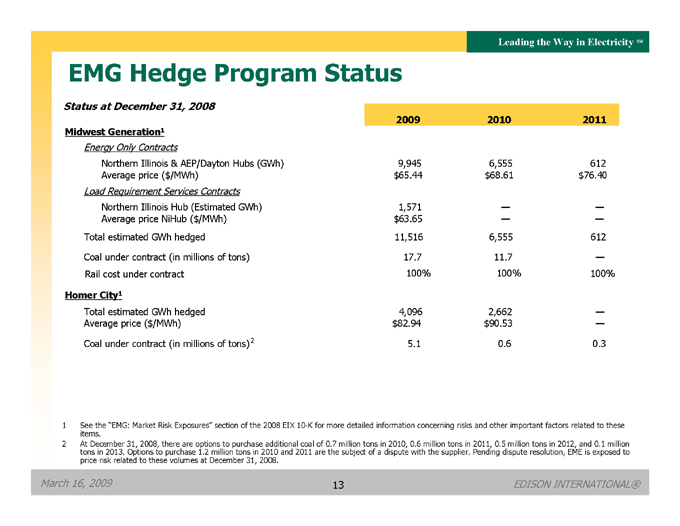

EMG Hedge Program Status

Status at December 31, 2008

2009

2010

2011

Midwest Generation1

Energy Only Contracts

Northern Illinois & AEP/Dayton Hubs (GWh)

9,945

6,555

612

Average price ($/MWh)

$65.44

$68.61

$76.40

Load Requirement Services Contracts

Northern Illinois Hub (Estimated GWh)

1,571

—

—

Average price NiHub ($/MWh)

$63.65

—

—

Total estimated GWh hedged

11,516

6,555

612

Coal under contract (in millions of tons)

17.7

11.7

—

Rail cost under contract

100%

100%

100%

Homer City1

Total estimated GWh hedged

4,096

2,662

—

Average price ($/MWh)

$82.94

$90.53

—

Coal under contract (in millions of tons) 2

5.1

0.6

0.3

1 See the “EMG: Market Risk Exposures” section of the 2008 EIX 10-K for more detailed information concerning risks and other important factors related to these items.

2 At December 31, 2008, there are options to purchase additional coal of 0.7 million tons in 2010, 0.6 million tons in 2011, 0.5 million tons in 2012, and 0.1 million tons in 2013. Options to purchase 1.2 million tons in 2010 and 2011 are the subject of a dispute with the supplier. Pending dispute resolution, EME is exposed to price risk related to these volumes at December 31, 2008.

March 16, 2009

13

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

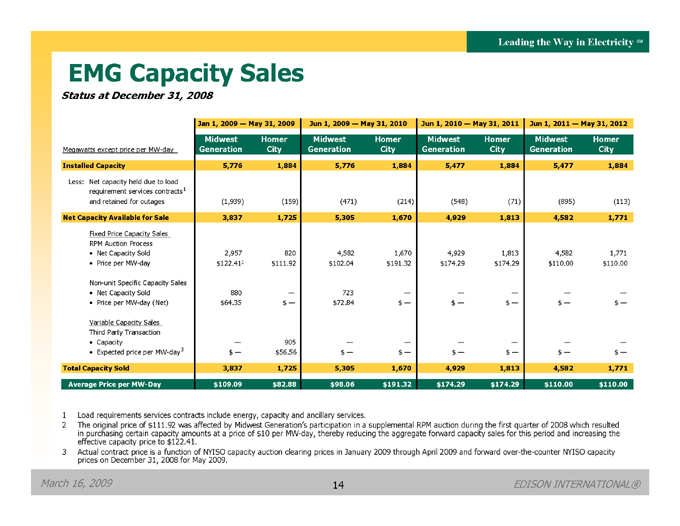

EMG Capacity Sales

Status at December 31, 2008

Jan 1, 2009 — May 31, 2009

Jun 1, 2009 — May 31, 2010

Jun 1, 2010 — May 31, 2011

Jun 1, 2011 — May 31, 2012

Megawatts except price per MW-day

Midwest Generation

Homer City

Midwest Generation

Homer City

Midwest Generation

Homer City

Midwest Generation

Homer City

Installed Capacity

5,776

1,884

5,776

1,884

5,477

1,884

5,477

1,884

Less: Net capacity held due to load requirement services contracts1 and retained for outages

(1,939)

(159)

(471)

(214)

(548)

(71)

(895)

(113)

Net Capacity Available for Sale

3,837

1,725

5,305

1,670

4,929

1,813

4,582

1,771

Fixed Price Capacity Sales

RPM Auction Process

Net Capacity Sold

2,957

820

4,582

1,670

4,929

1,813

4,582

1,771

Price per MW-day

$122.412

$111.92

$102.04

$191.32

$174.29

$174.29

$110.00

$110.00

Non-unit Specific Capacity Sales

Net Capacity Sold

880

—

723

—

—

—

—

—

Price per MW-day (Net)

$64.35

$—

$72.84

$—

$—

$—

$—

$—

Variable Capacity Sales

Third Party Transaction

Capacity

—

905

—

—

—

—

—

—

Expected price per MW-day 3

$—

$56.56

$—

$—

$—

$—

$—

$—

Total Capacity Sold

3,837

1,725

5,305

1,670

4,929

1,813

4,582

1,771

Average Price per MW-Day

$109.09

$82.88

$98.06

$191.32

$174.29

$174.29

$110.00

$110.00

1 Load requirements services contracts include energy, capacity and ancillary services.

2 The original price of $111.92 was affected by Midwest Generation’s participation in a supplemental RPM auction during the first quarter of 2008 which resulted in purchasing certain capacity amounts at a price of $10 per MW-day, thereby reducing the aggregate forward capacity sales for this period and increasing the effective capacity price to $122.41.

3 Actual contract price is a function of NYISO capacity auction clearing prices in January 2009 through April 2009 and forward over-the-counter NYISO capacity prices on December 31, 2008 for May 2009.

March 16, 2009

14

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

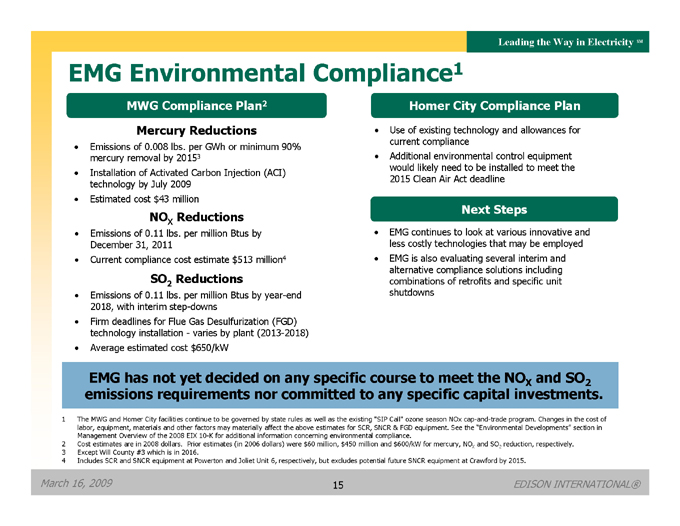

EMG Environmental Compliance1

MWG Compliance Plan2 Mercury Reductions

Emissions of 0.008 lbs. per GWh or minimum 90% mercury removal by 20153

Installation of Activated Carbon Injection (ACI) technology by July 2009

Estimated cost $43 million

NOX Reductions

Emissions of 0.11 lbs. per million Btus by December 31, 2011

Current compliance cost estimate $513 million4

SO2 Reductions

Emissions of 0.11 lbs. per million Btus by year-end 2018, with interim step-downs

Firm deadlines for Flue Gas Desulfurization (FGD) technology installation - varies by plant (2013-2018)

Average estimated cost $650/kW

Homer City Compliance Plan

Use of existing technology and allowances for current compliance

Additional environmental control equipment would likely need to be installed to meet the 2015 Clean Air Act deadline

Next Steps

EMG continues to look at various innovative and less costly technologies that may be employed

EMG is also evaluating several interim and alternative compliance solutions including combinations of retrofits and specific unit shutdowns

EMG has not yet decided on any specific course to meet the NOX and SO2 emissions requirements nor committed to any specific capital investments.

1 The MWG and Homer City facilities continue to be governed by state rules as well as the existing “SIP Call” ozone season NOx cap-and-trade program. Changes in the cost of labor, equipment, materials and other factors may materially affect the above estimates for SCR, SNCR & FGD equipment. See the “Environmental Developments” section in Management Overview of the 2008 EIX 10-K for additional information concerning environmental compliance.

2 Cost estimates are in 2008 dollars. Prior estimates (in 2006 dollars) were $60 million, $450 million and $600/kW for mercury, NOX and SO2 reduction, respectively.

3 Except Will County #3 which is in 2016.

4 Includes SCR and SNCR equipment at Powerton and Joliet Unit 6, respectively, but excludes potential future SNCR equipment at Crawford by 2015.

March 16, 2009

15

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

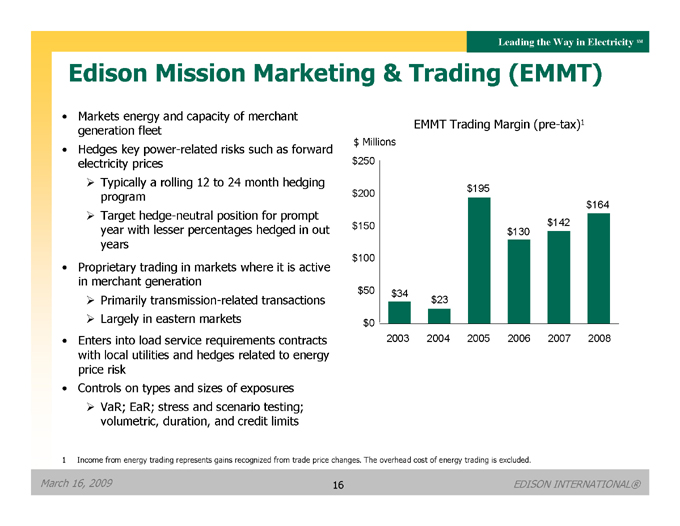

Edison Mission Marketing & Trading (EMMT)

Markets energy and capacity of merchant generation fleet

Hedges key power-related risks such as forward electricity prices

Typically a rolling 12 to 24 month hedging program

Target hedge-neutral position for prompt year with lesser percentages hedged in out years

Proprietary trading in markets where it is active in merchant generation

Primarily transmission-related transactions

Largely in eastern markets

Enters into load service requirements contracts with local utilities and hedges related to energy price risk

Controls on types and sizes of exposures

VaR; EaR; stress and scenario testing; volumetric, duration, and credit limits

EMMT Trading Margin (pre-tax)1 $ Millions $250

$195 $200 $164 $150 $130 $142 $100

$50 $34 $23 $0

2003 2004 2005 2006 2007 2008

1 | | Income from energy trading represents gains recognized from trade price changes. The overhead cost of energy trading is excluded. |

March 16, 2009

16

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

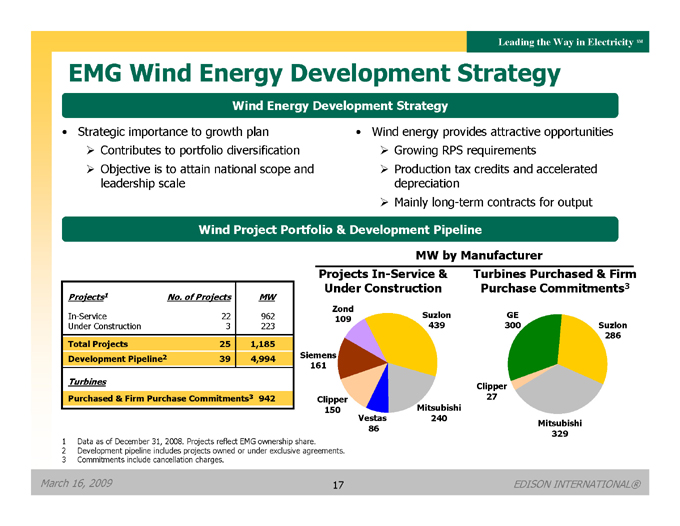

EMG Wind Energy Development Strategy

Wind Energy Development Strategy

Strategic importance to growth plan

Contributes to portfolio diversification

Objective is to attain national scope and leadership scale

Wind energy provides attractive opportunities

Growing RPS requirements

Production tax credits and accelerated depreciation

Mainly long-term contracts for output

Wind Project Portfolio & Development Pipeline

MW by Manufacturer

Projects In-Service & Under Construction

Turbines Purchased & Firm Purchase Commitments3

Projects1

No. of Projects

MW

In-Service

22

962

Under Construction

3

223

Total Projects

25

1,185

Development Pipeline2

39

4,994

Turbines

Purchased & Firm Purchase Commitments3 942

Zond

109

Suzlon

GE

439

300

Suzlon

286

Siemens

161

Clipper

27

Clipper

150

Mitsubishi

240

Vestas

86

Mitsubishi

329

1 Data as of December 31, 2008. Projects reflect EMG ownership share.

2 Development pipeline includes projects owned or under exclusive agreements.

3 Commitments include cancellation charges.

March 16, 2009

17

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

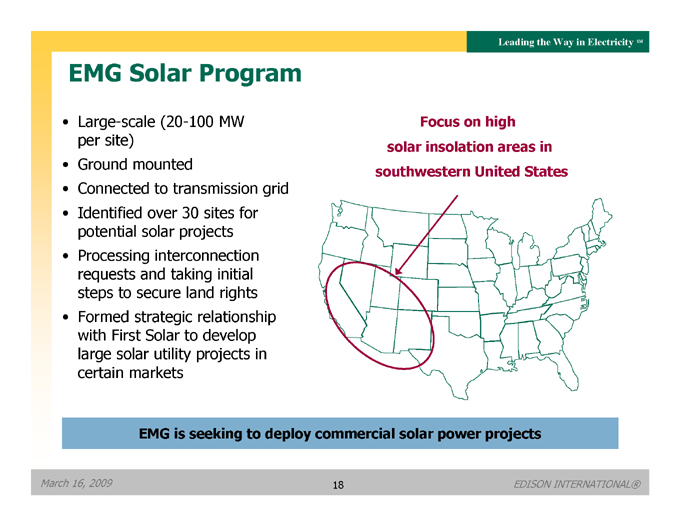

EMG Solar Program

• Large-scale (20-100 MW per site)

• Ground mounted

• Connected to transmission grid

• Identified over 30 sites for potential solar projects

• Processing interconnection requests and taking initial steps to secure land rights

• Formed strategic relationship with First Solar to develop large solar utility projects in certain markets

Focus on high

solar insolation areas in

southwestern United States

EMG is seeking to deploy commercial solar power projects

March 16, 2009

18

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

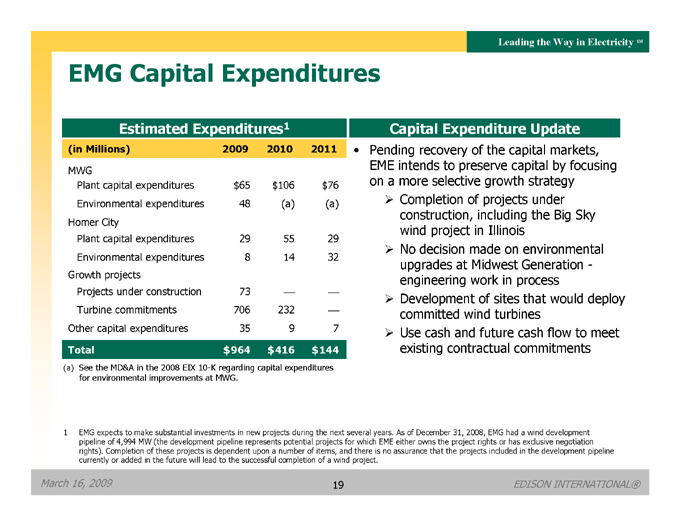

EMG Capital Expenditures

Estimated Expenditures1

(in Millions)

2009

2010

2011

MWG

Plant capital expenditures

$65

$106

$76

Environmental expenditures

48

(a)

(a)

Homer City

Plant capital expenditures

29

55

29

Environmental expenditures

8

14

32

Growth projects

Projects under construction

73

—

—

Turbine commitments

706

232

—

Other capital expenditures

35

9

7

Total

$964

$416

$144

(a) See the MD&A in the 2008 EIX 10-K regarding capital expenditures for environmental improvements at MWG.

Capital Expenditure Update

Pending recovery of the capital markets, EME intends to preserve capital by focusing on a more selective growth strategy

Completion of projects under construction, including the Big Sky wind project in Illinois

No decision made on environmental upgrades at Midwest Generation - engineering work in process

Development of sites that would deploy committed wind turbines

Use cash and future cash flow to meet existing contractual commitments

1 EMG expects to make substantial investments in new projects during the next several years. As of December 31, 2008, EMG had a wind development pipeline of 4,994 MW (the development pipeline represents potential projects for which EME either owns the project rights or has exclusive negotiation rights). Completion of these projects is dependent upon a number of items, and there is no assurance that the projects included in the development pipeline currently or added in the future will lead to the successful completion of a wind project.

March 16, 2009

19

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

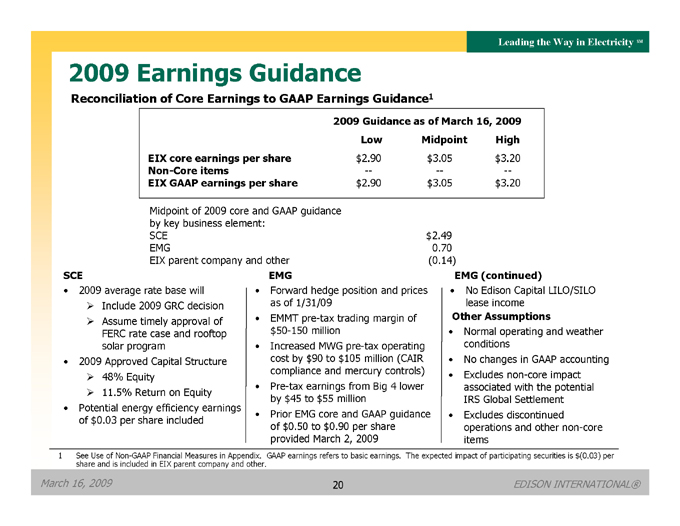

2009 Earnings Guidance

Reconciliation of Core Earnings to GAAP Earnings Guidance1

2009 Guidance as of March 16, 2009

Low

Midpoint

High

EIX core earnings per share

$2.90

$3.05

$3.20

Non-Core items

—

—

—

EIX GAAP earnings per share

$2.90

$3.05

$3.20

Midpoint of 2009 core and GAAP guidance by key business element:

SCE

$2.49

EMG

0.70

EIX parent company and other

(0.14)

SCE

• 2009 average rate base will

Include 2009 GRC decision

Assume timely approval of FERC rate case and rooftop solar program

• 2009 Approved Capital Structure

48% Equity

11.5% Return on Equity

• Potential energy efficiency earnings of $0.03 per share included

EMG

• Forward hedge position and prices as of 1/31/09

• EMMT pre-tax trading margin of

$50-150 million

• Increased MWG pre-tax operating cost by $90 to $105 million (CAIR compliance and mercury controls)

• Pre-tax earnings from Big 4 lower by $45 to $55 million

• Prior EMG core and GAAP guidance of $0.50 to $0.90 per share provided March 2, 2009

EMG (continued)

• No Edison Capital LILO/SILO lease income

Other Assumptions

• Normal operating and weather conditions

• No changes in GAAP accounting

• Excludes non-core impact associated with the potential IRS Global Settlement

• Excludes discontinued operations and other non-core items

1 See Use of Non-GAAP Financial Measures in Appendix. GAAP earnings refers to basic earnings. The expected impact of participating securities is $(0.03) per share and is included in EIX parent company and other.

March 16, 2009

20

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Appendix

March 16, 2009

21

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

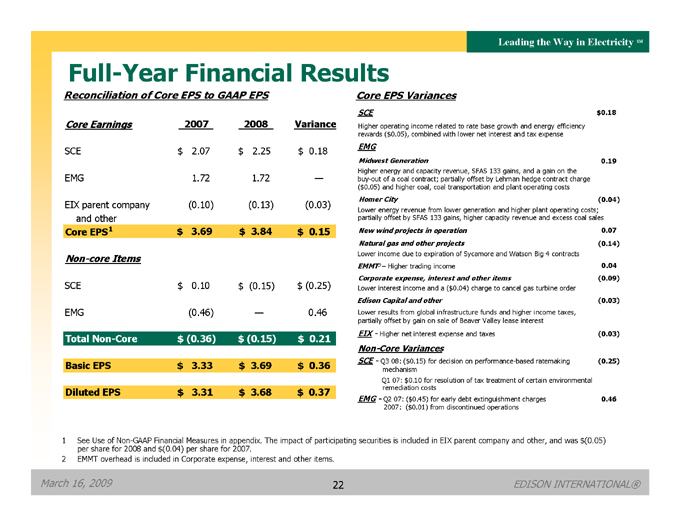

Full-Year Financial Results

Reconciliation of Core EPS to GAAP EPS

Core Earnings

2007

2008

Variance

SCE

$2.07

$2.25

$0.18

EMG

1.72

1.72

—

EIX parent company and other

(0.10)

(0.13)

(0.03)

Core EPS 1

$3.69

$3.84

$0.15

Non-core Items

SCE

$0.10

$(0.15)

$(0.25)

EMG

(0.46)

—

0.46

Total Non-Core

$(0.36)

$(0.15)

$0.21

Basic EPS

$3.33

$3.69

$0.36

Diluted EPS

$3.31

$3.68

$0.37

Core EPS Variances

SCE

$0.18

Higher operating income related to rate base growth and energy efficiency rewards ($0.05), combined with lower net interest and tax expense

EMG

Midwest Generation

0.19

Higher energy and capacity revenue, SFAS 133 gains, and a gain on the buy-out of a coal contract; partially offset by Lehman hedge contract charge

($0.05) and higher coal, coal transportation and plant operating costs

Homer City

(0.04)

Lower energy revenue from lower generation and higher plant operating costs; partially offset by SFAS 133 gains, higher capacity revenue and excess coal sales

New wind projects in operation

0.07

Natural gas and other projects

(0.14)

Lower income due to expiration of Sycamore and Watson Big 4 contracts

EMMT2 – Higher trading income

0.04

Corporate expense, interest and other items

(0.09)

Lower interest income and a ($0.04) charge to cancel gas turbine order

Edison Capital and other

(0.03)

Lower results from global infrastructure funds and higher income taxes, partially offset by gain on sale of Beaver Valley lease interest

EIX - Higher net interest expense and taxes

(0.03)

Non-Core Variances

SCE - Q3 08: ($0.15) for decision on performance-based ratemaking mechanism

(0.25)

Q1 07: $0.10 for resolution of tax treatment of certain environmental remediation costs

EMG - Q2 07: ($0.45) for early debt extinguishment charges

0.46

2007: ($0.01) from discontinued operations

1 See Use of Non-GAAP Financial Measures in appendix. The impact of participating securities is included in EIX parent company and other, and was $(0.05) per share for 2008 and $(0.04) per share for 2007.

2 EMMT overhead is included in Corporate expense, interest and other items.

March 16, 2009

22

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

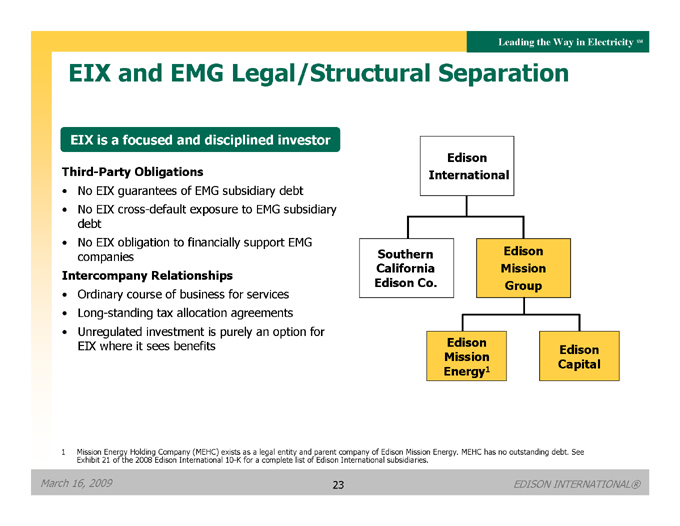

EIX and EMG Legal/Structural Separation

EIX is a focused and disciplined investor

Third-Party Obligations

• No EIX guarantees of EMG subsidiary debt

• No EIX cross-default exposure to EMG subsidiary debt

• No EIX obligation to financially support EMG companies

Intercompany Relationships

• Ordinary course of business for services

• Long-standing tax allocation agreements

• Unregulated investment is purely an option for EIX where it sees benefits

Edison

International

Southern California Edison Co.

Edison Mission Group

Edison Mission Energy1

Edison Capital

1 Mission Energy Holding Company (MEHC) exists as a legal entity and parent company of Edison Mission Energy. MEHC has no outstanding debt. See Exhibit 21 of the 2008 Edison International 10-K for a complete list of Edison International subsidiaries.

March 16, 2009

23

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

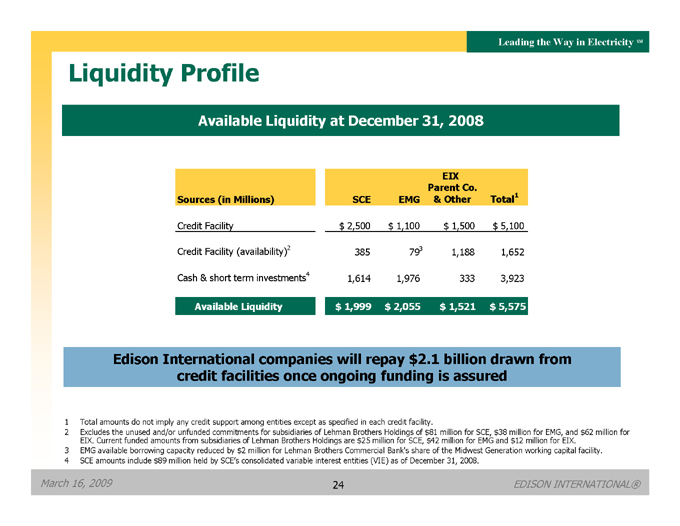

Liquidity Profile

Available Liquidity at December 31, 2008

Sources (in Millions)

SCE

EMG

EIX Parent Co. & Other

Total1

Credit Facility

$2,500

$1,100

$1,500

$5,100

Credit Facility (availability)2

385

793

1,188

1,652

Cash & short term investments4

1,614

1,976

333

3,923

Available Liquidity

$1,999

$2,055

$1,521

$5,575

Edison International companies will repay $2.1 billion drawn from credit facilities once ongoing funding is assured

1 Total amounts do not imply any credit support among entities except as specified in each credit facility.

2 Excludes the unused and/or unfunded commitments for subsidiaries of Lehman Brothers Holdings of $81 million for SCE, $38 million for EMG, and $62 million for EIX. Current funded amounts from subsidiaries of Lehman Brothers Holdings are $25 million for SCE, $42 million for EMG and $12 million for EIX.

3 EMG available borrowing capacity reduced by $2 million for Lehman Brothers Commercial Bank’s share of the Midwest Generation working capital facility.

4 SCE amounts include $89 million held by SCE’s consolidated variable interest entities (VIE) as of December 31, 2008.

March 16, 2009

24

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

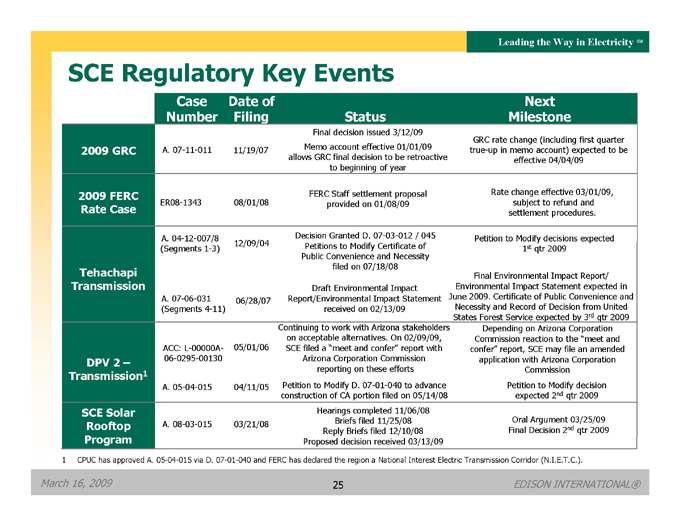

SCE Regulatory Key Events

Case Number

Date of Filing

Status

Next Milestone

2009 GRC

A. 07-11-011

11/19/07

Final decision issued 3/12/09 Memo account effective 01/01/09 allows GRC final decision to be retroactive to beginning of year

GRC rate change (including first quarter true-up in memo account) expected to be effective 04/04/09

2009 FERC Rate Case

ER08-1343

08/01/08

FERC Staff settlement proposal provided on 01/08/09

Rate change effective 03/01/09, subject to refund and settlement procedures.

A. 04-12-007/8 (Segments 1-3)

12/09/04

Decision Granted D. 07-03-012 / 045 Petitions to Modify Certificate of Public Convenience and Necessity filed on 07/18/08

Petition to Modify decisions expected 1st qtr 2009

Tehachapi Transmission

A. 07-06-031 (Segments 4-11)

06/28/07

Draft Environmental Impact Report/Environmental Impact Statement received on 02/13/09

Final Environmental Impact Report/Environmental Impact Statement expected in June 2009. Certificate of Public Convenience and Necessity and Record of Decision from United States Forest Service expected by 3rd qtr 2009

DPV 2 – Transmission1

ACC: L-00000A-06-0295-00130

05/01/06

Continuing to work with Arizona stakeholders on acceptable alternatives. On 02/09/09, SCE filed a “meet and confer” report with Arizona Corporation Commission reporting on these efforts

Depending on Arizona Corporation Commission reaction to the “meet and confer” report, SCE may file an amended application with Arizona Corporation Commission

A. 05-04-015

04/11/05

Petition to Modify D. 07-01-040 to advance construction of CA portion filed on 05/14/08

Petition to Modify decision

expected 2nd qtr 2009

SCE Solar Rooftop Program

A. 08-03-015

03/21/08

Hearings completed 11/06/08 Briefs filed 11/25/08 Reply Briefs filed 12/10/08 Proposed decision received 03/13/09

Oral Argument 03/25/09 Final Decision 2nd qtr 2009

1 CPUC has approved A. 05-04-015 via D. 07-01-040 and FERC has declared the region a National Interest Electric Transmission Corridor (N.I.E.T.C.).

March 16, 2009

25

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

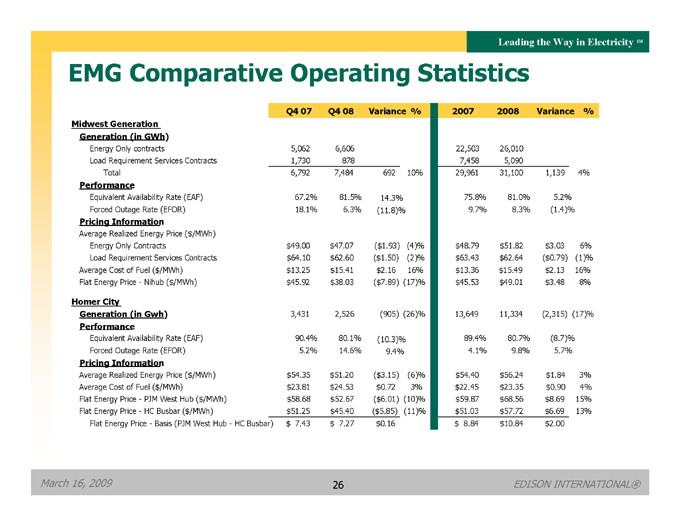

EMG Comparative Operating Statistics

Q4 07

Q4 08

Variance %

2007

2008

Variance

%

Midwest Generation

Generation (in GWh)

Energy Only contracts

5,062

6,606

22,503

26,010

Load Requirement Services Contracts

1,730

878

7,458

5,090

Total

6,792

7,484

692

10%

29,961

31,100

1,139

4%

Performance

Equivalent Availability Rate (EAF)

67.2%

81.5%

14.3%

75.8%

81.0%

5.2%

Forced Outage Rate (EFOR)

18.1%

6.3%

(11.8)%

9.7%

8.3%

(1.4)%

Pricing Information

Average Realized Energy Price ($/MWh)

Energy Only Contracts

$49.00

$47.07

($1.93)

(4)%

$48.79

$51.82

$3.03

6%

Load Requirement Services Contracts

$64.10

$62.60

($1.50)

(2)%

$63.43

$62.64

($0.79)

(1)%

Average Cost of Fuel ($/MWh)

$13.25

$15.41

$2.16

16%

$13.36

$15.49

$2.13

16%

Flat Energy Price - Nihub ($/MWh)

$45.92

$38.03

($7.89)

(17)%

$45.53

$49.01

$3.48

8%

Homer City

Generation (in Gwh)

3,431

2,526

(905)

(26)%

13,649

11,334

(2,315)

(17)%

Performance

Equivalent Availability Rate (EAF)

90.4%

80.1%

(10.3)%

89.4%

80.7%

(8.7)%

Forced Outage Rate (EFOR)

5.2%

14.6%

9.4%

4.1%

9.8%

5.7%

Pricing Information

Average Realized Energy Price ($/MWh)

$54.35

$51.20

($3.15)

(6)%

$54.40

$56.24

$1.84

3%

Average Cost of Fuel ($/MWh)

$23.81

$24.53

$0.72

3%

$22.45

$23.35

$0.90

4%

Flat Energy Price - PJM West Hub ($/MWh)

$58.68

$52.67

($6.01)

(10)%

$59.87

$68.56

$8.69

15%

Flat Energy Price - HC Busbar ($/MWh)

$51.25

$45.40

($5.85)

(11)%

$51.03

$57.72

$6.69

13%

Flat Energy Price - Basis (PJM West Hub - HC Busbar)

$7.43

$7.27

$0.16

$8.84

$10.84

$2.00

March 16, 2009

26

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

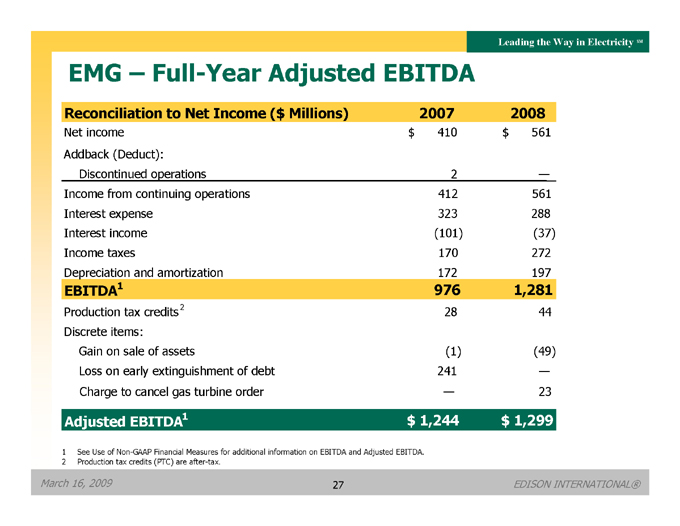

EMG – Full-Year Adjusted EBITDA

Reconciliation to Net Income ($ Millions)

2007

2008

Net income

$410

$561

Addback (Deduct):

Discontinued operations

2

—

Income from continuing operations

412

561

Interest expense

323

288

Interest income

(101)

(37)

Income taxes

170

272

Depreciation and amortization

172

197

EBITDA1

976

1,281

Production tax credits 2

28

44

Discrete items:

Gain on sale of assets

(1)

(49)

Loss on early extinguishment of debt

241

—

Charge to cancel gas turbine order

—

23

Adjusted EBITDA1

$1,244

$1,299

1 See Use of Non-GAAP Financial Measures for additional information on EBITDA and Adjusted EBITDA.

2 Production tax credits (PTC) are after-tax.

March 16, 2009

27

EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Use of Non-GAAP Financial Measures

Edison International’s earnings are prepared in accordance with generally accepted accounting principles used in the United States and represent the company’s earnings as reported to the Securities and Exchange Commission. Our management uses core earnings and EPS by principal operating subsidiary internally for financial planning and for analysis of performance. We also use core earnings and EPS by principal operating subsidiary as primary performance measurements when communicating with analysts and investors regarding our earnings results and outlook, as it allows us to more accurately compare the company’s ongoing performance across periods. Core earnings exclude discontinued operations and other non-core items and are reconciled to basic earnings per common share.

EPS by principal operating subsidiary is based on the principal operating subsidiary net income and Edison International’s weighted average outstanding common shares. The impact of participating securities (vested stock options that earn dividend equivalents that may participate in undistributed earnings with common stock) for each principal operating subsidiary is not material to each principal operating subsidiary’s EPS and is therefore reflected in the results of the Edison International holding company, which we refer to as EIX parent company and other. EPS and core EPS by principal operating subsidiary are reconciled to basic earnings per common share.

EBITDA is defined as earnings before interest, income taxes, depreciation and amortization. Adjusted EBITDA includes production tax credits from EMG’s wind projects and excludes amounts from gain on the sale of assets, loss on early extinguishment of debt and leases, and impairment of assets and investments. EBITDA is the principal financial metric used by the financial community in assessing the relative cash-generation power of companies. Our management uses Adjusted EBITDA as an important financial measure for evaluating EMG.

A reconciliation of Non-GAAP information to GAAP information, including the impact of participating securities, is included either on the slide where the information appears or on another slide referenced in the presentation.

March 16, 2009

28

EDISON INTERNATIONAL®