Exhibit 99.2

Leading the Way in Electricity SM

Fourth Quarter 2009 Financial Teleconference

March 1, 2010 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Forward-Looking Statements

Statements contained in this presentation about future performance, including, without limitation, earnings, asset and rate base growth, load growth, capital investments, and other statements that are not purely historical, are forward-looking statements. These forward-looking statements reflect our current expectations; however, such statements involve risks and uncertainties. Actual results could differ materially from current expectations. These forward-looking statements represent our expectations only as of the date of this presentation, and Edison International assumes no duty to update them to reflect new information, events or circumstances. Important factors that could cause different results are discussed under the headings “Risk Factors,” and “Management’s Discussion and Analysis” in Edison International’s 2009 Form 10-K, and other reports filed with the Securities and Exchange Commission, which are available on our website: www.edisoninvestor.com. These filings also provide additional information on historical and other factual data contained in this presentation.

March 1, 2010 1 EDISON INTERNATIONAL®

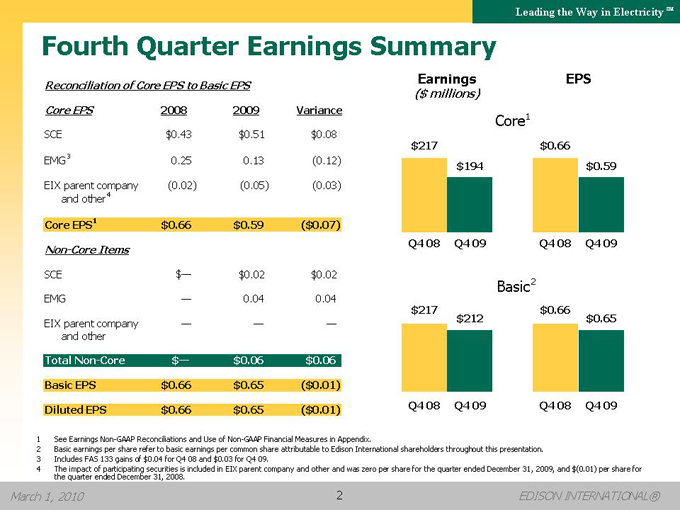

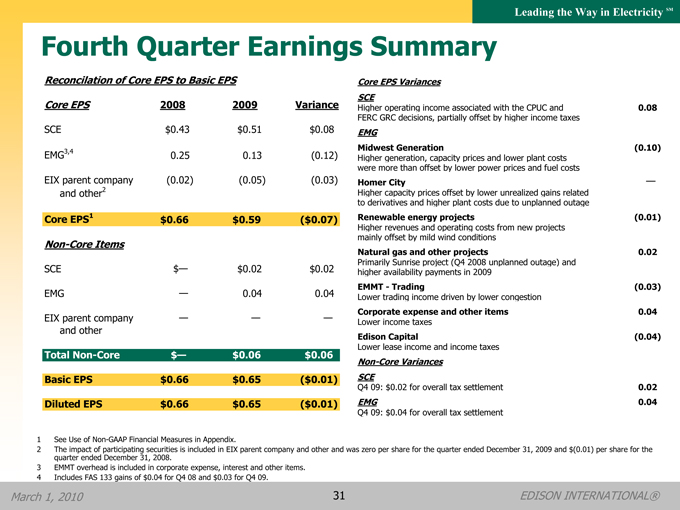

Fourth Quarter Earnings Summary

Reconciliation of Core EPS to Basic EPS

Core EPS

2008

2009

Variance

SCE

$0.43

$0.51

$0.08

EMG3

0.25

0.13

(0.12)

EIX parent company and other4

(0.02)

(0.05)

(0.03)

Core EPS1

$0.66

$0.59

($0.07)

Non-Core Items

SCE

$—

$0.02

$0.02

EMG

—

0.04

0.04

EIX parent company and other

—

—

—

Total Non-Core

$—

$0.06

$0.06

Basic EPS

$0.66

$0.65

($0.01)

Diluted EPS

$0.66

$0.65

($0.01)

Earnings ($ millions)

EPS

Core1

$217 $0.66 $194 $0.59

Q4 08 Q4 09 Q4 08 Q4 09

Basic2

$217 $0.66 $212 $0.65

Q4 08 Q4 09 Q4 08 Q4 09

1 See Earnings Non-GAAP Reconciliations and Use of Non-GAAP Financial Measures in Appendix.

2 Basic earnings per share refer to basic earnings per common share attributable to Edison International shareholders throughout this presentation.

3 Includes FAS 133 gains of $0.04 for Q4 08 and $0.03 for Q4 09.

4 The impact of participating securities is included in EIX parent company and other and was zero per share for the quarter ended December 31, 2009, and $(0.01) per share for the quarter ended December 31, 2008.

March 1, 2010 2 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

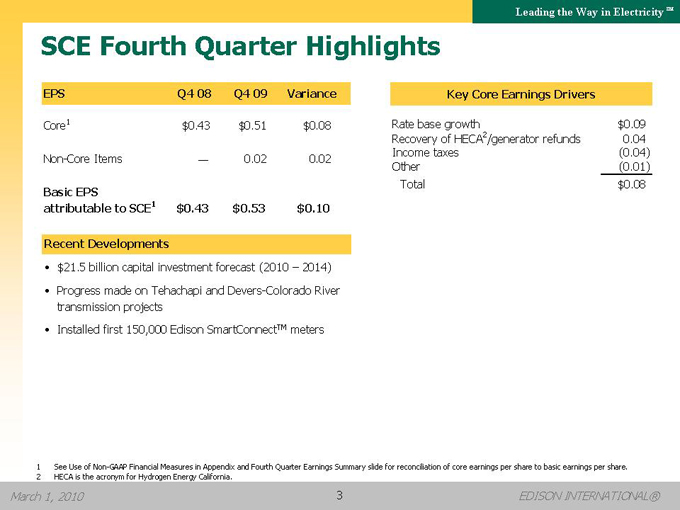

SCE Fourth Quarter Highlights

EPS

Q4 08

Q4 09

Variance

Core1

$0.43

$0.51

$0.08

Non-Core Items

—

0.02

0.02

Basic EPSattributable to SCE1

$0.43

$0.53

$0.10

Recent Developments

• $21.5 billion capital investment forecast (2010 – 2014)

• Progress made on Tehachapi and Devers-Colorado River transmission projects

• Installed first 150,000 Edison SmartConnectTM meters

Key Core Earnings Drivers

Rate base growth

$0.09

Recovery of HECA/generator refunds2

0.04

Income taxes

(0.04)

Other

(0.01)

Total

$0.08

1 See Use of Non-GAAP Financial Measures in Appendix and Fourth Quarter Earnings Summary slide for reconciliation of core earnings per share to basic earnings per share.

2 HECA is the acronym for Hydrogen Energy California.

March 1, 2010 3 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

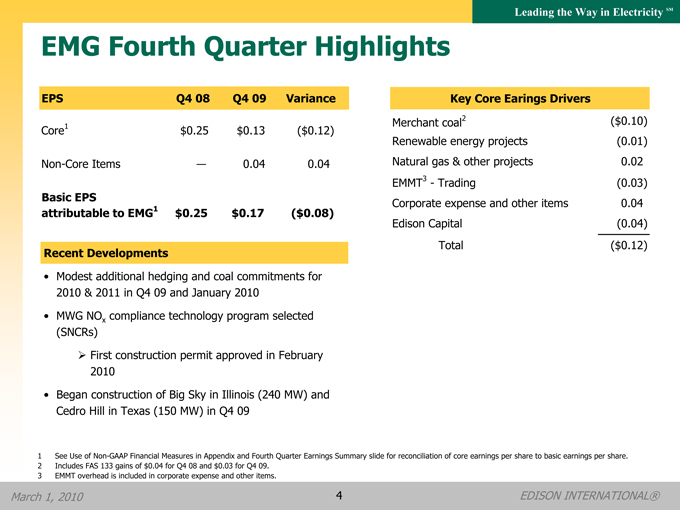

EMG Fourth Quarter Highlights

EPS

Q4 08

Q4 09

Variance

Core1

$0.25

$0.13

($0.12)

Non-Core Items

—

0.04

0.04

Basic EPSattributable to EMG1

$0.25

$0.17

($0.08)

Recent Developments

• Modest additional hedging and coal commitments for 2010 & 2011 in Q4 09 and January 2010

• MWG NOx compliance technology program selected (SNCRs)

?First construction permit approved in February 2010

• Began construction of Big Sky in Illinois (240 MW) and Cedro Hill in Texas (150 MW) in Q4 09

Key Core Earings Drivers

Merchant coal2

($0.10)

Renewable energy projects

(0.01)

Natural gas & other projects

0.02

EMMT3—Trading

(0.03)

Corporate expense and other items

0.04

Edison Capital

(0.04)

Total

($0.12)

1 See Use of Non-GAAP Financial Measures in Appendix and Fourth Quarter Earnings Summary slide for reconciliation of core earnings per share to basic earnings per share.

2 Includes FAS 133 gains of $0.04 for Q4 08 and $0.03 for Q4 09.

3 EMMT overhead is included in corporate expense and other items.

March 1, 2010 4 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

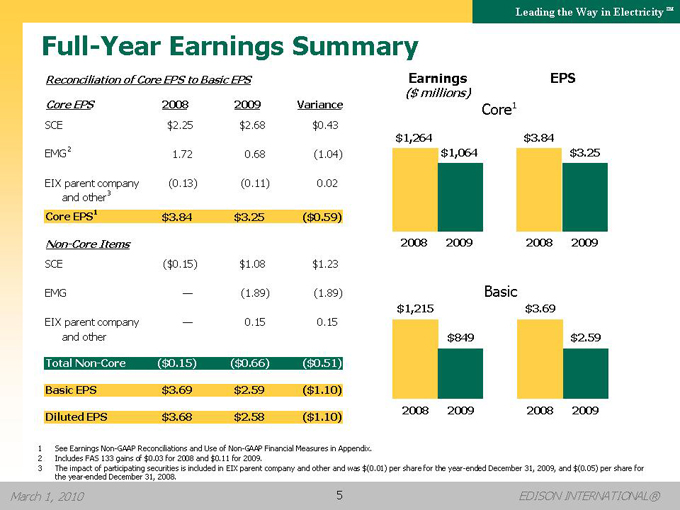

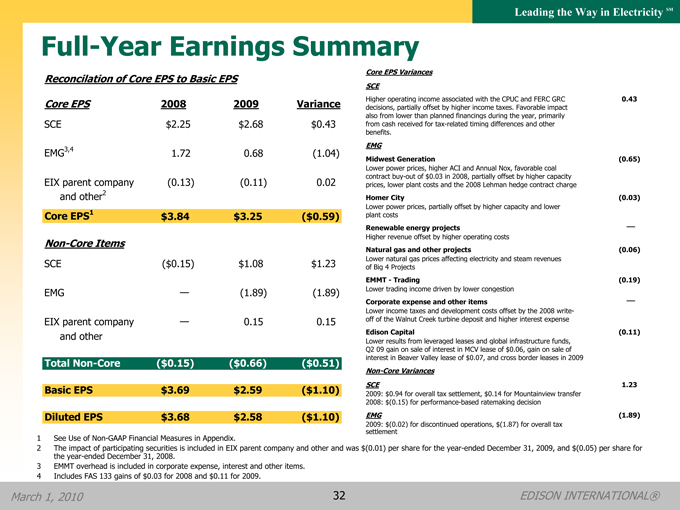

Full-Year Earnings Summary

Reconciliation of Core EPS to Basic EPS

Core EPS

2008

2009

Variance

SCE

$2.25

$2.68

$0.43

EMG2

1.72

0.68

(1.04)

EIX parent company and other3

(0.13)

(0.11)

0.02

Core EPS1

$3.84

$3.25

($0.59)

Non-Core Items

SCE

($0.15)

$1.08

$1.23

EMG

—

(1.89)

(1.89)

EIX parent company and other

—

0.15

0.15

Total Non-Core

($0.15)

($0.66)

($0.51)

Basic EPS

$3.69

$2.59

($1.10)

Diluted EPS

$3.68

$2.58

($1.10)

Earnings EPS

($ millions)

Core1

$1,264 $3.84 $1,064 $3.25

2008 2009 2008 2009

Basic

$1,215 $3.69

$849 $2.59

2008 2009 2008 2009

1 | | See Earnings Non-GAAP Reconciliations and Use of Non-GAAP Financial Measures in Appendix. |

2 | | Includes FAS 133 gains of $0.03 for 2008 and $0.11 for 2009. |

3 | | The impact of participating securities is included in EIX parent company and other and was $(0.01) per share for the year-ended December 31, 2009, and $(0.05) per share for the year-ended December 31, 2008. |

March 1, 2010 5 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

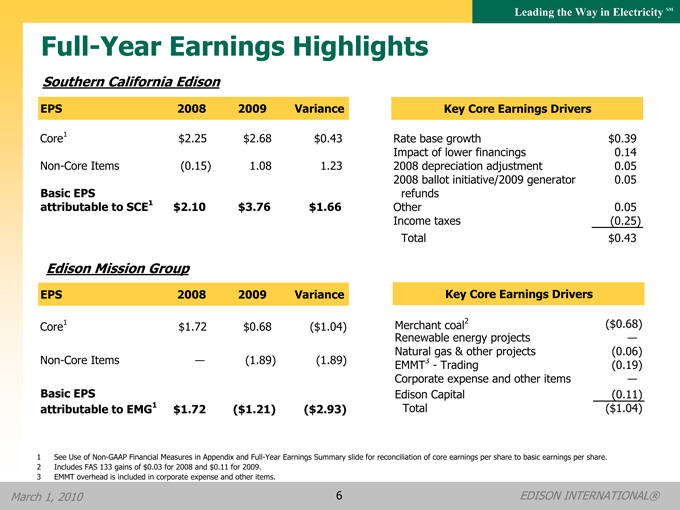

Full-Year Earnings Highlights

Southern California Edison

EPS

2008

2009

Variance

Core1

$2.25

$2.68

$0.43

Non-Core Items

(0.15)

1.08

1.23

Basic EPSattributable to SCE1

$2.10

$3.76

$1.66

Edison Mission Group

EPS

2008

2009

Variance

Core1

$1.72

$0.68

($1.04)

Non-Core Items

—

(1.89)

(1.89)

Basic EPSattributable to EMG1

$1.72

($1.21)

($2.93)

Key Core Earnings Drivers

Rate base growth

$0.39

Impact of lower financings

0.14

2008 depreciation adjustment

0.05

2008 ballot initiative/2009 generator

0.05

refunds

Other

0.05

Income taxes

(0.25)

Total

$0.43

Key Core Earnings Drivers

Merchant coal2

($0.68)

Renewable energy projects

—

Natural gas & other projects

(0.06)

EMMT3—Trading

(0.19)

Corporate expense and other items

—

Edison Capital

(0.11)

Total

($1.04)

1 See Use of Non-GAAP Financial Measures in Appendix and Full-Year Earnings Summary slide for reconciliation of core earnings per share to basic earnings per share.

2 Includes FAS 133 gains of $0.03 for 2008 and $0.11 for 2009.

3 EMMT overhead is included in corporate expense and other items.

March 1, 2010 6 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

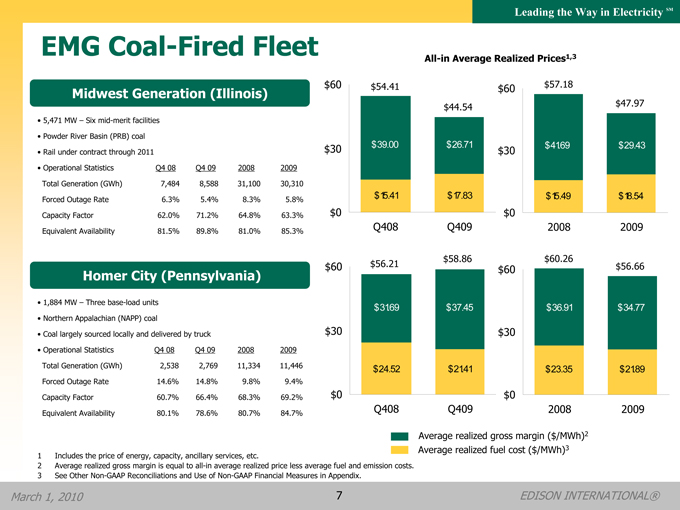

EMG Coal-Fired Fleet

Midwest Generation (Illinois)

• 5,471 MW – Six mid-merit facilities

• Powder River Basin (PRB) coal

• Rail under contract through 2011

• Operational Statistics

Q4 08

Q4 09

2008

2009

Total Generation (GWh)

7,484

8,588

31,100

30,310

Forced Outage Rate

6.3%

5.4%

8.3%

5.8%

Capacity Factor

62.0%

71.2%

64.8%

63.3%

Equivalent Availability

81.5%

89.8%

81.0%

85.3%

Homer City (Pennsylvania)

• 1,884 MW – Three base-load units

• Northern Appalachian (NAPP) coal

• Coal largely sourced locally and delivered by truck

• Operational Statistics

Q4 08

Q4 09

2008

2009

Total Generation (GWh)

2,538

2,769

11,334

11,446

Forced Outage Rate

14.6%

14.8%

9.8%

9.4%

Capacity Factor

60.7%

66.4%

68.3%

69.2%

Equivalent Availability

80.1%

78.6%

80.7%

84.7%

All-in Average Realized Prices1,3

$60 $54.41 $60 $57.18

$44.54 $47.97

$30 $39.00 $26.71 $41 .69 $29.43 $30

$15.41 $17.83 $15.49 $18.54

$0 $0

Q408 Q409 2008 2009

$58.86 $60.26

$60 $56.21 $56.66 $60

$31 .69 $37.45 $36.91 $34.77

$30 $30

$24.52 $21 .41 $23.35 $21 .89

$0 $0

Q408 Q409 2008 2009

Average realized gross margin ($/MWh)2 Average realized fuel cost ($/MWh)3

1 | | Includes the price of energy, capacity, ancillary services, etc. |

2 | | Average realized gross margin is equal to all-in average realized price less average fuel and emission costs. |

3 | | See Other Non-GAAP Reconciliations and Use of Non-GAAP Financial Measures in Appendix. |

March 1, 2010 7 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

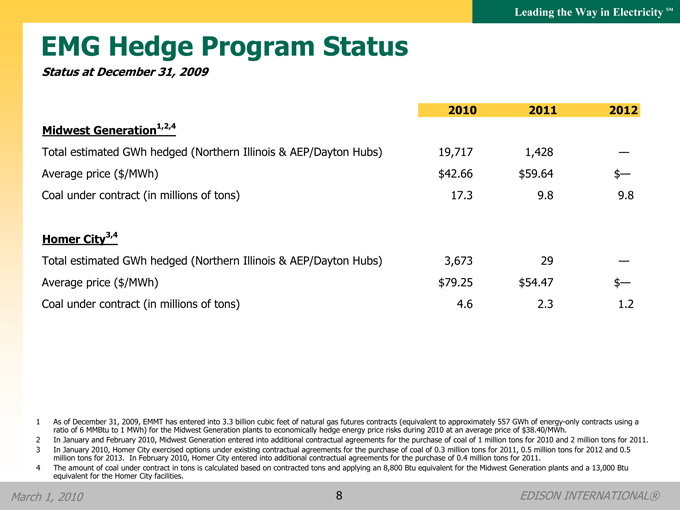

EMG Hedge Program Status

Status at December 31, 2009

Midwest Generation1,2,4

Total estimated GWh hedged (Northern Illinois & AEP/Dayton Hubs) Average price ($/MWh) Coal under contract (in millions of tons)

Homer City3,4

Total estimated GWh hedged (Northern Illinois & AEP/Dayton Hubs) Average price ($/MWh) Coal under contract (in millions of tons)

2010

2011

2012

19,717

1,428

—

$42.66

$59.64

$—

17.3

9.8

9.8

3,673

29

—

$79.25

$54.47

$—

4.6

2.3

1.2

1 As of December 31, 2009, EMMT has entered into 3.3 billion cubic feet of natural gas futures contracts (equivalent to approximately 557 GWh of energy-only contracts using a ratio of 6 MMBtu to 1 MWh) for the Midwest Generation plants to economically hedge energy price risks during 2010 at an average price of $38.40/MWh.

2 In January and February 2010, Midwest Generation entered into additional contractual agreements for the purchase of coal of 1 million tons for 2010 and 2 million tons for 2011.

3 In January 2010, Homer City exercised options under existing contractual agreements for the purchase of coal of 0.3 million tons for 2011, 0.5 million tons for 2012 and 0.5 million tons for 2013. In February 2010, Homer City entered into additional contractual agreements for the purchase of 0.4 million tons for 2011.

4 The amount of coal under contract in tons is calculated based on contracted tons and applying an 8,800 Btu equivalent for the Midwest Generation plants and a 13,000 Btu equivalent for the Homer City facilities.

March 1, 2010 8 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

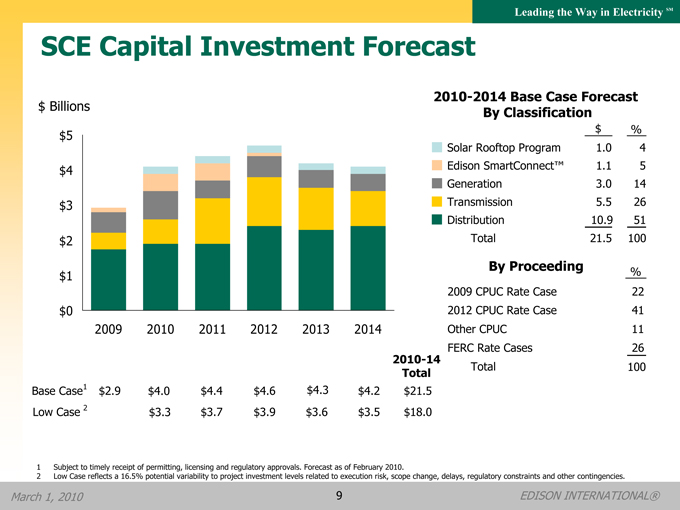

SCE Capital Investment Forecast

$ Billions $5

$4 $3 $2 $1 $0

2009 2010 2011 2012 2013 2014

2010-2014 Base Case Forecast By Classification

$

%

Solar Rooftop Program

1.0

4

Edison SmartConnect™

1.1

5

Generation

3.0

14

Transmission

5.5

26

Distribution

10.9

51

Total

21.5

100

By Proceeding

%

2009

CPUC Rate Case

22

2012

CPUC Rate Case

41

Other CPUC

11

FERC Rate Cases

26

Total

100

2010-14

Total

Base Case1

$2.9

$4.0

$4.4

$4.6

$4.3

$4.2

$21.5

Low Case 2

$3.3

$3.7

$3.9

$3.6

$3.5

$18.0

1 | | Subject to timely receipt of permitting, licensing and regulatory approvals. Forecast as of February 2010. |

2 | | Low Case reflects a 16.5% potential variability to project investment levels related to execution risk, scope change, delays, regulatory constraints and other contingencies. |

March 1, 2010 9 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

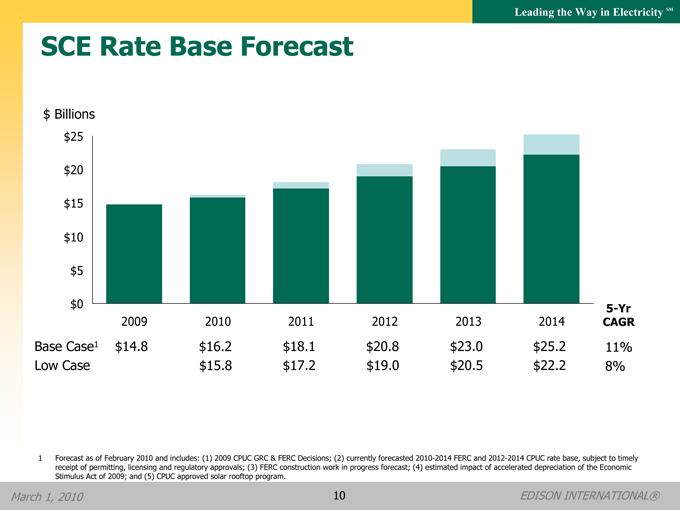

SCE Rate Base Forecast

$ Billions $25

$20 $15 $10 $5 $0

5-Yr

2009

2010

2011

2012

2013

2014

CAGR

Base Case1

$14.8

$16.2

$18.1

$20.8

$23.0

$25.2

11%

Low Case

$15.8

$17.2

$19.0

$20.5

$22.2

8%

1 Forecast as of February 2010 and includes: (1) 2009 CPUC GRC & FERC Decisions; (2) currently forecasted 2010-2014 FERC and 2012-2014 CPUC rate base, subject to timely receipt of permitting, licensing and regulatory approvals; (3) FERC construction work in progress forecast; (4) estimated impact of accelerated depreciation of the Economic Stimulus Act of 2009; and (5) CPUC approved solar rooftop program.

March 1, 2010 10 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

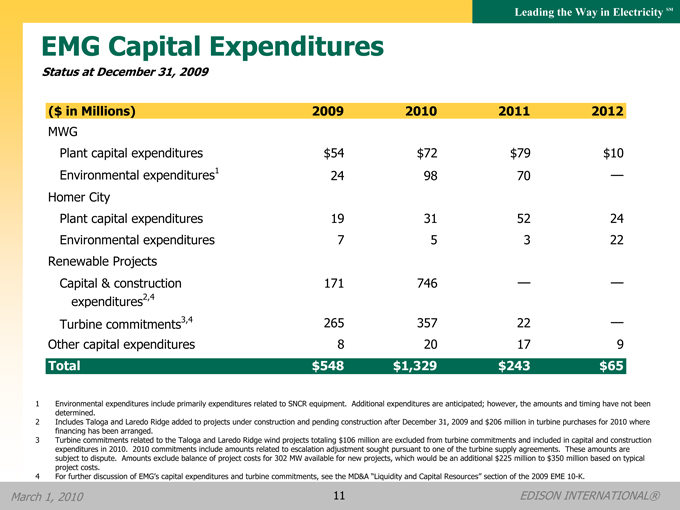

EMG Capital Expenditures

Status at December 31, 2009

($ in Millions)

2009

2010

2011

2012

MWG

Plant capital expenditures

$54

$72

$79

$10

Environmental expenditures1

24

98

70

—

Homer City

Plant capital expenditures

19

31

52

24

Environmental expenditures

7

5

3

22

Renewable Projects

Capital & construction

171

746

—

—

expenditures2,4

Turbine commitments3,4

265

357

22

—

Other capital expenditures

8

20

17

9

Total

$548

$1,329

$243

$65

1 Environmental expenditures include primarily expenditures related to SNCR equipment. Additional expenditures are anticipated; however, the amounts and timing have not been determined.

2 Includes Taloga and Laredo Ridge added to projects under construction and pending construction after December 31, 2009 and $206 million in turbine purchases for 2010 where financing has been arranged.

3 Turbine commitments related to the Taloga and Laredo Ridge wind projects totaling $106 million are excluded from turbine commitments and included in capital and construction expenditures in 2010. 2010 commitments include amounts related to escalation adjustment sought pursuant to one of the turbine supply agreements. These amounts are subject to dispute. Amounts exclude balance of project costs for 302 MW available for new projects, which would be an additional $225 million to $350 million based on typical project costs.

4 For further discussion of EMG’s capital expenditures and turbine commitments, see the MD&A “Liquidity and Capital Resources” section of the 2009 EME 10-K.

March 1, 2010 11 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

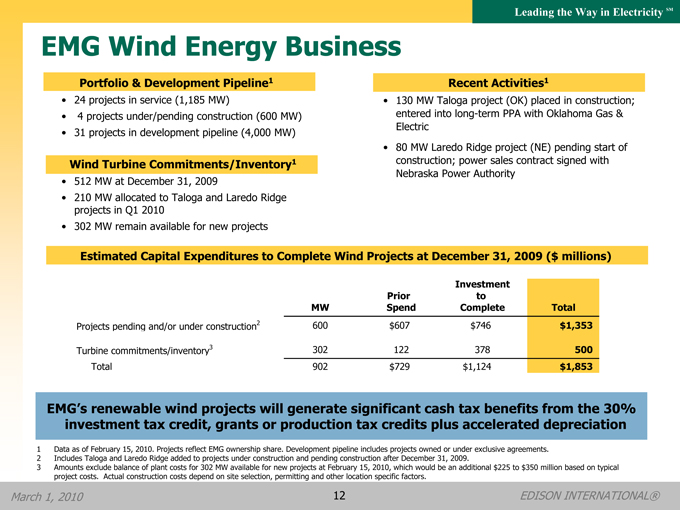

EMG Wind Energy Business

Portfolio & Development Pipeline1

• 24 projects in service (1,185 MW)

• | | 4 projects under/pending construction (600 MW) |

• 31 projects in development pipeline (4,000 MW)

Wind Turbine Commitments/Inventory1

• 512 MW at December 31, 2009

• 210 MW allocated to Taloga and Laredo Ridge projects in Q1 2010

• 302 MW remain available for new projects

Recent Activities1

130 MW Taloga project (OK) placed in construction; entered into long-term PPA with Oklahoma Gas & Electric

80 MW Laredo Ridge project (NE) pending start of construction; power sales contract signed with Nebraska Power Authority

Estimated Capital Expenditures to Complete Wind Projects at December 31, 2009 ($ millions)

MW

Prior Spend

Investment to Complete

Total

Projects pending and/or under construction2

600

$607

$746

$1,353

Turbine commitments/inventory3

302

122

378

500

Total

902

$729

$1,124

$1,853

EMG’s renewable wind projects will generate significant cash tax benefits from the 30% investment tax credit, grants or production tax credits plus accelerated depreciation

1 Data as of February 15, 2010. Projects reflect EMG ownership share. Development pipeline includes projects owned or under exclusive agreements.

2 Includes Taloga and Laredo Ridge added to projects under construction and pending construction after December 31, 2009.

3 Amounts exclude balance of plant costs for 302 MW available for new projects at February 15, 2010, which would be an additional $225 to $350 million based on typical project costs. Actual construction costs depend on site selection, permitting and other location specific factors.

March 1, 2010 12 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

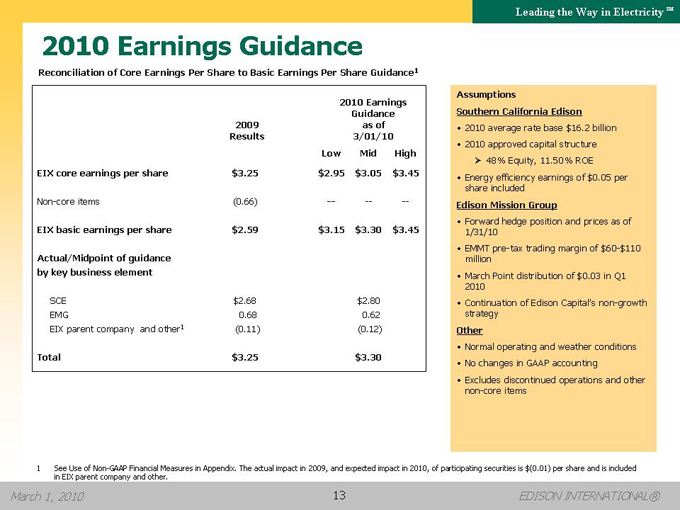

2010 Earnings Guidance

Reconciliation of Core Earnings Per Share to Basic Earnings Per Share Guidance1

2009 Results

2010 Earnings Guidance as of 3/01/10

Low

Mid

High

EIX core earnings per share

$3.25

$2.95

$3.05

$3.45

Non-core items

(0.66)

—

—

—

EIX basic earnings per share

$2.59

$3.15

$3.30

$3.45

Actual/Midpoint of guidance by key business element

SCE

$2.68

$2.80

EMG

0.68

0.62

EIX parent company and other1

(0.11)

(0.12)

Total

$3.25

$3.30

Assumptions

Southern California Edison

• 2010 average rate base $16.2 billion

• 2010 approved capital structure

??48% Equity, 11.50% ROE

• Energy efficiency earnings of $0.05 per share included

Edison Mission Group

• Forward hedge position and prices as of 1/31/10

• Increased plant outage activity at MWG

• March Point distribution of $0.03 in Q1 2010

• Continuation of Edison Capital’s non-growth strategy

Other

• Normal operating and weather conditions

• No changes in GAAP accounting

• Excludes discontinued operations and other non-core items

1 See Use of Non-GAAP Financial Measures in Appendix. The actual impact in 2009, and expected impact in 2010, of participating securities is $(0.01) per share and is included in EIX parent company and other.

March 1, 2010 13 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

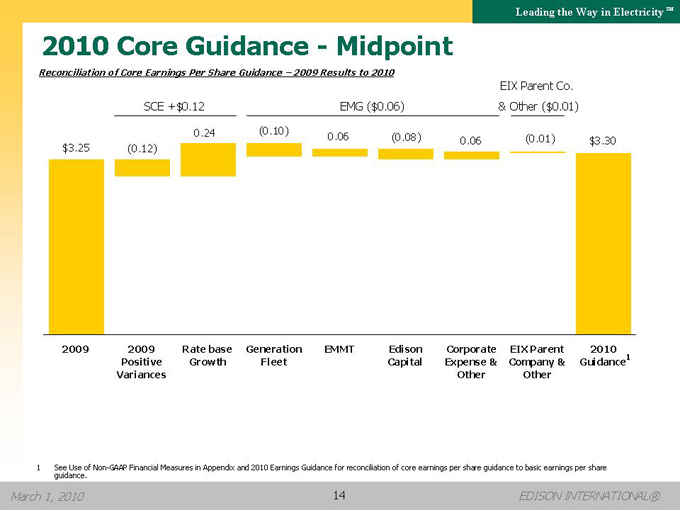

2010 Core Guidance—Midpoint

Reconciliation of Core Earnings Per Share Guidance – 2009 Results to 2010

SCE +$0.12

EMG ($0.06)

& Other ($0.01)

EIX Parent Co.

0.24

(0.10)

0.06

(0.08)

0.06

(0.01)

$3.30

$3.25

(0.12)

2009

2009 Positive Variances

Rate base Growth

Generation Fleet

EMMT

Edison Capital

Corporate Expense & Other

EIX Parent Company & Other

2010 Guidance1

1 See Use of Non-GAAP Financial Measures in Appendix and 2010 Earnings Guidance for reconciliation of core earnings per share guidance to basic earnings per share guidance.

March 1, 2010 14 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

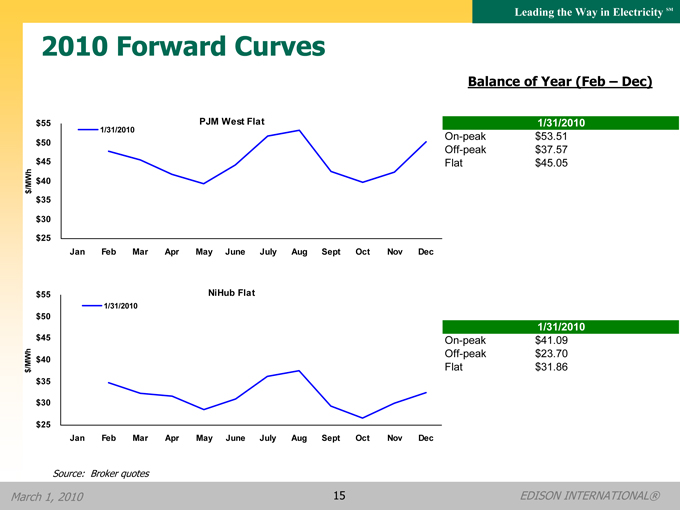

2010 Forward Curves

$55

$50

$45 /MWh $40 $ $35

$30

$25

PJM West Flat 1/31/2010

Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec

$55

$50

$45 /MWh $40 $ $35

$30

$25

NiHub Flat 1/31/2010

Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec

Balance of Year (Feb – Dec)

1/31/2010

On-peak

$53.51

Off-peak

$37.57

Flat

$45.05

1/31/2010

On-peak

$41.09

Off-peak

$23.70

Flat

$31.86

Source: Broker quotes

March 1, 2010 15 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Appendix

March 1, 2010 16 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Delivering Superior and Sustained Value

Edison International

Southern California Edison

Edison Mission Group

A diversified and flexible platform best positions EIX in an industry undergoing unprecedented change Leverage regulated and competitive businesses Positioned for long-term earnings and dividend growth

Balance electric reliability, rates and public policy needs to assure long-term sustainable growth Focus on grid reliability and transmission investments Establish foundation for technology investments Decoupled regulatory model mitigates demand and fuel cost risks

Diversify generation platform by growing renewables business Create value by resolving environmental compliance issues Effectively manage merchant coal margins

Our key operating principles emphasize financial discipline, superior execution and innovative solutions to the challenges of today and tomorrow

March 1, 2010 17 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

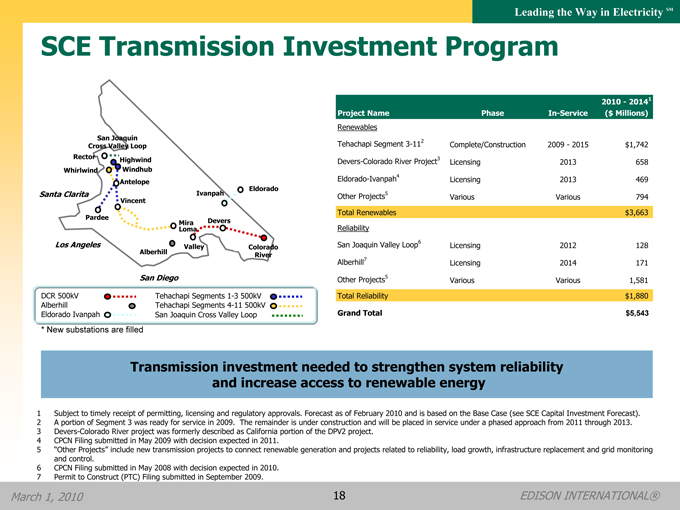

SCE Transmission Investment Program

San Joaquin

Cross Valley Loop

Rector

Highwind

Whirlwind

Windhub

Antelope

Santa Clarita

Ivanpah

Eldorado

Vincent

Pardee

MiraLoma Devers

Los Angeles

Valley

Colorado

Alberhill

River

San Diego

DCR 500kV

Tehachapi Segments 1-3 500kV

Alberhill

Tehachapi Segments 4-11 500kV

Eldorado Ivanpah

San Joaquin Cross Valley Loop

* New substations are filled

Project Name

Phase

In-Service

2010 - 20141 ($ Millions)

Renewables

Tehachapi Segment 3-112

Complete/Construction

2009 - 2015

$1,742

Devers-Colorado River Project3

Licensing

2013

658

Eldorado-Ivanpah4

Licensing

2013

469

Other Projects5

Various

Various

794

Total Renewables

$3,663

Reliability

San Joaquin Valley Loop6

Licensing

2012

128

Alberhill7

Licensing

2014

171

Other Projects5

Various

Various

1,581

Total Reliability

$1,880

Grand Total

$5,543

Transmission investment needed to strengthen system reliability and increase access to renewable energy

1 Subject to timely receipt of permitting, licensing and regulatory approvals. Forecast as of February 2010 and is based on the Base Case (see SCE Capital Investment Forecast).

2 A portion of Segment 3 was ready for service in 2009. The remainder is under construction and will be placed in service under a phased approach from 2011 through 2013.

3 Devers-Colorado River project was formerly described as California portion of the DPV2 project.

4 CPCN Filing submitted in May 2009 with decision expected in 2011.

5 “Other Projects” include new transmission projects to connect renewable generation and projects related to reliability, load growth, infrastructure replacement and grid monitoring and control.

6 CPCN Filing submitted in May 2008 with decision expected in 2010.

7 Permit to Construct (PTC) Filing submitted in September 2009.

March 1, 2010 18 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

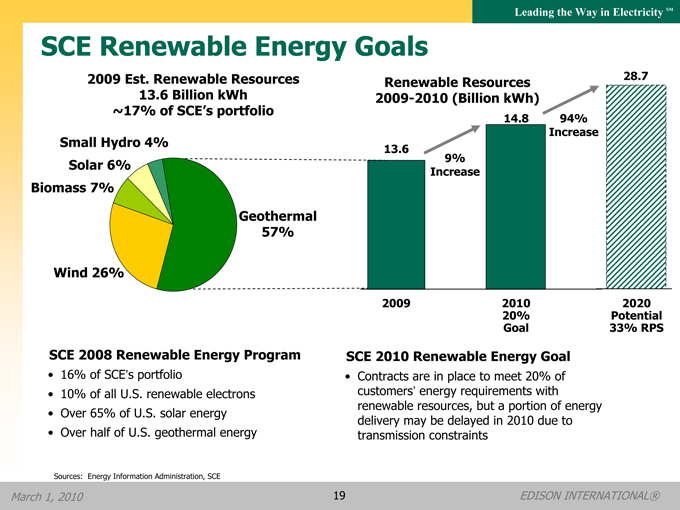

SCE Renewable Energy Goals

2009 Est. Renewable Resources 13.6 Billion kWh ~17% of SCE’s portfolio

Small Hydro 4% Solar 6% Biomass 7%

Geothermal 57%

Wind 26%

Renewable Resources 28.7 2009-2010 (Billion kWh)

28.7

13.6

9% Increase

14.8 94% Increase

2009

2010 20% Goal

2020 Potential 33% RPS

SCE 2008 Renewable Energy Program

• 16% of SCE’s portfolio

• 10% of all U.S. renewable electrons

• Over 65% of U.S. solar energy

• Over half of U.S. geothermal energy

SCE 2010 Renewable Energy Goal

• Contracts are in place to meet 20% of customers’ energy requirements with renewable resources, but a portion of energy delivery may be delayed in 2010 due to transmission constraints

Sources: Energy Information Administration, SCE

March 1, 2010 19 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

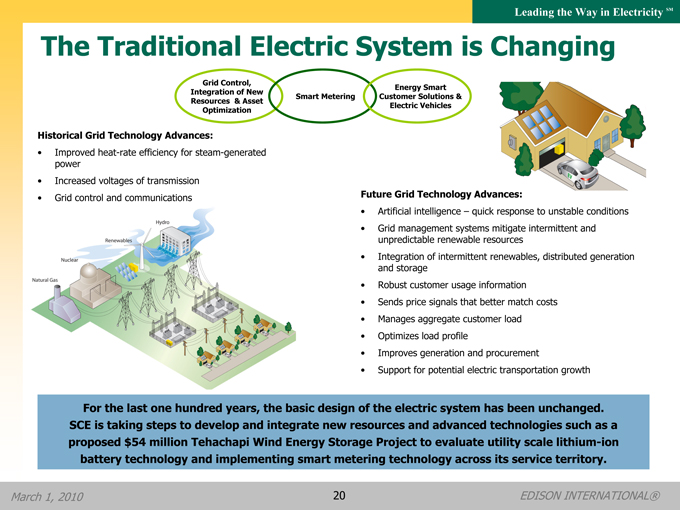

The Traditional Electric System is Changing

Grid Control, Integration of New Resources & Asset Optimization

Smart Metering

Energy Smart Customer Solutions & Electric Vehicles

Historical Grid Technology Advances:

• Improved heat-rate efficiency for steam-generated power

• Increased voltages of transmission

• Grid control and communications

Future Grid Technology Advances:

• Artificial intelligence – quick response to unstable conditions

• Grid management systems mitigate intermittent and unpredictable renewable resources

• Integration of intermittent renewables, distributed generation and storage

• Robust customer usage information

• Sends price signals that better match costs

• Manages aggregate customer load

• Optimizes load profile

• Improves generation and procurement

• Support for potential electric transportation growth

For the last one hundred years, the basic design of the electric system has been unchanged. SCE is taking steps to develop and integrate new resources and advanced technologies such as a proposed $54 million Tehachapi Wind Energy Storage Project to evaluate utility scale lithium-ion battery technology and implementing smart metering technology across its service territory.

March 1, 2010 20 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

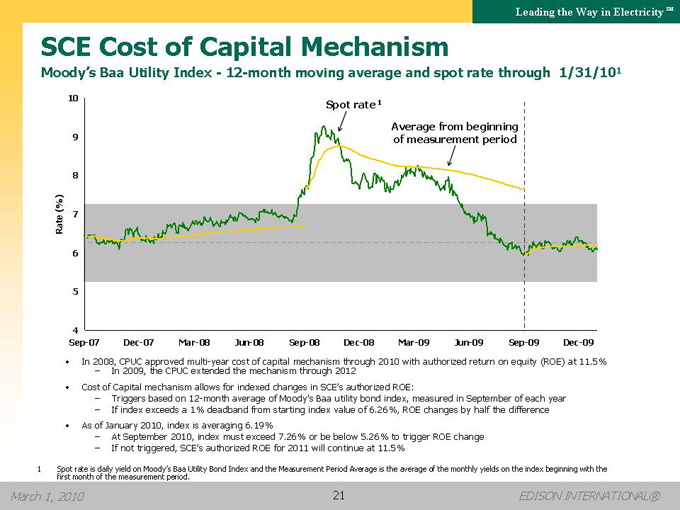

SCE Cost of Capital Mechanism

Moody’s Baa Utility Index - 12-month moving average and spot rate through 1/31/101

10

9

(%) 7 Rate 6

Spot rate

Average from beginning of measurement period

Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09

• In 2008, – In CPUC 2009, approved the CPUC multi extended -year cost the mechanism of capital mechanism through 2012 through 2010 with authorized return on equity (ROE) at 11.5%

• Cost of Capital mechanism allows for indexed changes in SCE’s authorized ROE:

– Triggers based on 12-month average of Moody’s Baa utility bond index, measured in September of each year

– If index exceeds a 1% deadband from starting index value of 6.26%, ROE changes by half the difference

• As of January 2010, index is averaging 6.19%

– At September 2010, index must exceed 7.26% or be below 5.26% to trigger ROE change

– If not triggered, SCE’s authorized ROE for 2011 will continue at 11.5%

1 Spot rate is daily yield on Moody’s Baa Utility Bond Index and the Measurement Period Average is the average of the monthly yields on the index beginning with the first month of the measurement period.

March 1, 2010 21 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

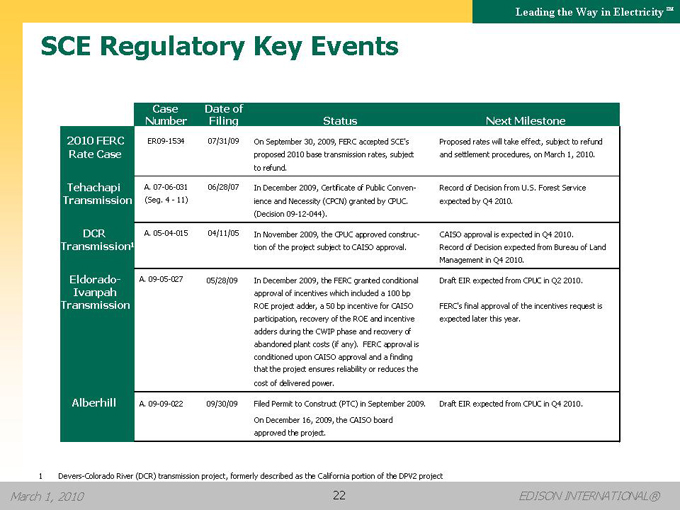

SCE Regulatory Key Events

Case Number

Date of Filing

Status

Next Milestone

2010 FERC Rate Case

ER09-1534

07/31/09

On September 30, 2009, FERC accepted SCE’s proposed 2010 base transmission rates, subject to refund.

Proposed rates will take effect, subject to refund and settlement procedures, on March 1, 2010.

Tehachapi Transmission

A. 07-06-031 (Seg. 4 - 11)

06/28/07

In December 2009, Certificate of Public Conven- ience and Necessity (CPCN) granted by CPUC. (Decision 09-12-044).

Record of Decision from U.S. Forest Service expected by Q4 2010.

DCR Transmission1

A.05— A.05-04— 015

04/11/05

In November 2009, the CPUC approved construc- tion of the project subject to CAISO approval.

CAISO approval is expected in Q4 2010. Record of Decision expected from Bureau of Land Management in Q4 2010.

Eldorado- Ivanpah Transmission1 Transmission

A.09— A.09-05— 027

05/28/09

In December 2009, the FERC granted conditional approval of incentives which included a 100 bp ROE project adder, a 50 bp incentive for CAISO participation, recovery of the ROE and incentive adders during the CWIP phase and recovery of abandoned plant costs (if any). FERC approval is conditioned upon CAISO approval and a finding that the project ensures reliability or reduces the cost of delivered power.

Draft EIR expected from CPUC in Q2 2010. FERC’s final approval of the incentives request is expected later this year.

Alberhill

A.09— A.09-09— 022

09/30/09

Filed Permit to Construct (PTC) in September 2009. On December 16, 2009, the CAISO board approved the project.

Draft EIR expected from CPUC in Q4 2010.

1 Devers-Colorado River (DCR) transmission project, formerly described as the California portion of the DPV2 project

March 1, 2010 22 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

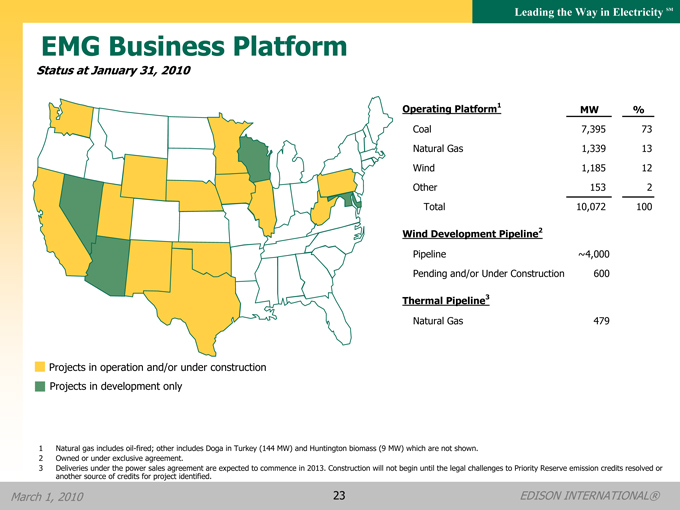

EMG Business Platform

Status at January 31, 2010

Projects in operation and/or under construction Projects in development only

Operating Platform1

MW

%

Coal

7,395

73

Natural Gas

1,339

13

Wind

1,185

12

Other

153

2

Total

10,072

100

Wind Development Pipeline2

Pipeline

~4,000

Pending and/or Under Construction

600

Thermal Pipeline3

Natural Gas

479

1 | | Natural gas includes oil-fired; other includes Doga in Turkey (144 MW) and Huntington biomass (9 MW) which are not shown. |

2 | | Owned or under exclusive agreement. |

3 | | Deliveries under the power sales agreement are expected to commence in 2013. Construction will not begin until the legal challenges to Priority Reserve emission credits resolved or another source of credits for project identified. |

March 1, 2010 23 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

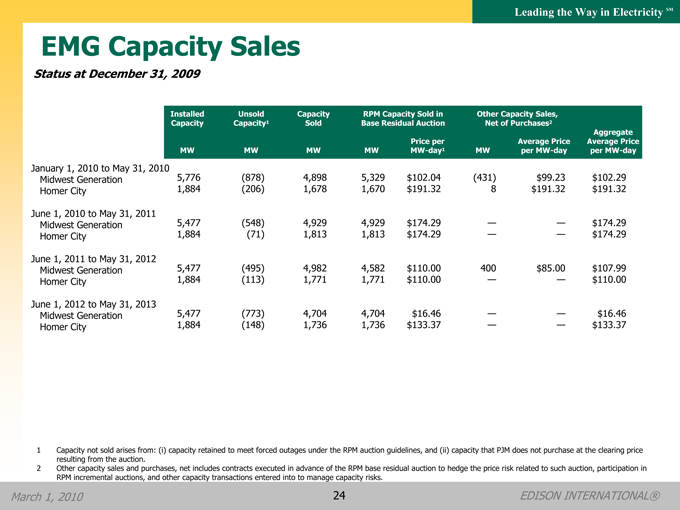

EMG Capacity Sales

Status at December 31, 2009

Installed Capacity

Unsold Capacity1

Capacity Sold

RPM Capacity Sold in Base Residual Auction

Other Capacity Sales, Net of Purchases2

MW

MW

MW

MW

Price per MW-day1

MW

Average Price per MW-day

Aggregate Average Price per MW-day

January 1, 2010 to May 31, 2010

Midwest Generation

5,776

(878)

4,898

5,329

$102.04

(431)

$99.23

$102.29

Homer City

1,884

(206)

1,678

1,670

$191.32

8

$191.32

$191.32

June 1, 2010 to May 31, 2011

Midwest Generation

5,477

(548)

4,929

4,929

$174.29

—

—

$174.29

Homer City

1,884

(71)

1,813

1,813

$174.29

—

—

$174.29

June 1, 2011 to May 31, 2012

Midwest Generation

5,477

(495)

4,982

4,582

$110.00

400

$85.00

$107.99

Homer City

1,884

(113)

1,771

1,771

$110.00

—

—

$110.00

June 1, 2012 to May 31, 2013

Midwest Generation

5,477

(773)

4,704

4,704

$16.46

—

—

$16.46

Homer City

1,884

(148)

1,736

1,736

$133.37

—

—

$133.37

1 Capacity not sold arises from: (i) capacity retained to meet forced outages under the RPM auction guidelines, and (ii) capacity that PJM does not purchase at the clearing price resulting from the auction.

2 Other capacity sales and purchases, net includes contracts executed in advance of the RPM base residual auction to hedge the price risk related to such auction, participation in RPM incremental auctions, and other capacity transactions entered into to manage capacity risks.

March 1, 2010 24 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

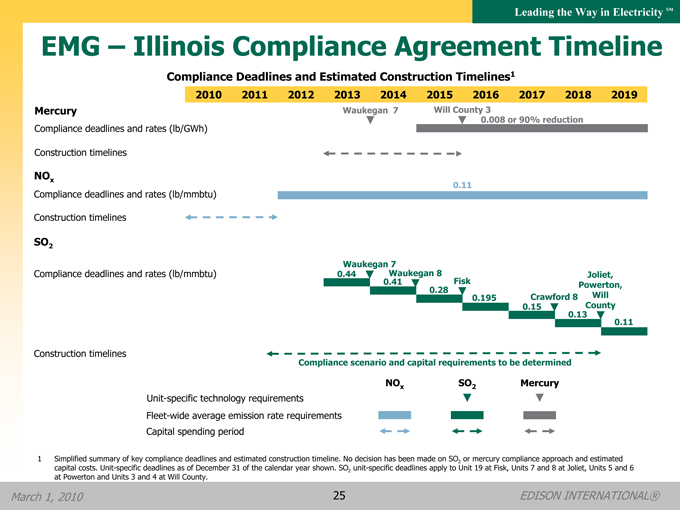

EMG – Illinois Compliance Agreement Timeline

Compliance Deadlines and Estimated Construction Timelines1

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Mercury

Waukegan 7

Will County 3

0.008 or 90% reduction

Compliance deadlines and rates (lb/GWh)

Construction timelines

NOx

0.11

Compliance deadlines and rates (lb/mmbtu)

Construction timelines

SO2

Waukegan 7

Compliance deadlines and rates (lb/mmbtu)

0.44

Waukegan 8

Joliet,

0.41

Fisk

Powerton,

0.28

0.195

Crawford 8

Will

0.15

County

0.13

0.11

Construction timelines Compliance scenario and capital requirements to be determined

Unit-specific technology requirements

Fleet-wide average emission rate requirements Capital spending period

NOx SO2 Mercury

1 Simplified summary of key compliance deadlines and estimated construction timeline. No decision has been made on SO2 or mercury compliance approach and estimated capital costs. Unit-specific deadlines as of December 31 of the calendar year shown. SO2 unit-specific deadlines apply to Unit 19 at Fisk, Units 7 and 8 at Joliet, Units 5 and 6 at Powerton and Units 3 and 4 at Will County.

March 1, 2010 25 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

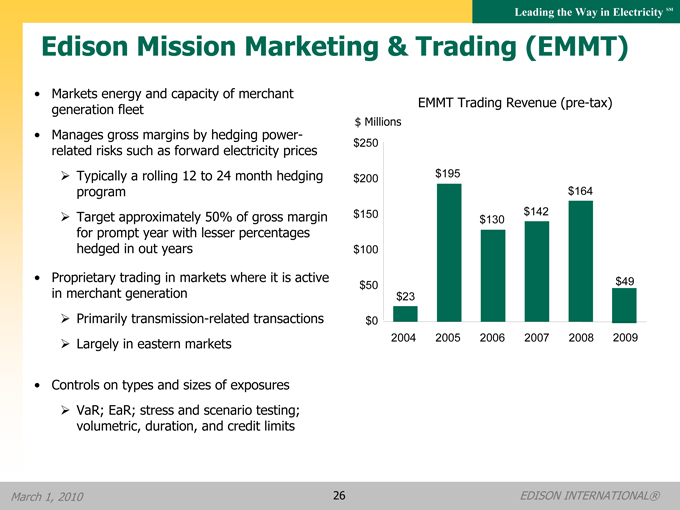

Edison Mission Marketing & Trading (EMMT)

• Markets energy and capacity of merchant generation fleet

• Manages gross margins by hedging power-related risks such as forward electricity prices

?Typically a rolling 12 to 24 month hedging program

?Target approximately 50% of gross margin for prompt year with lesser percentages hedged in out years

• Proprietary trading in markets where it is active in merchant generation

?Primarily transmission-related transactions

?Largely in eastern markets

• Controls on types and sizes of exposures

?VaR; EaR; stress and scenario testing; volumetric, duration, and credit limits

EMMT Trading Revenue (pre-tax)

$ Millions

$250

$200

$195

$164

$150

$142

$130

$100

$50

$49

$23

$0

2004

2005

2006

2007

2008

2009

March 1, 2010 26 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

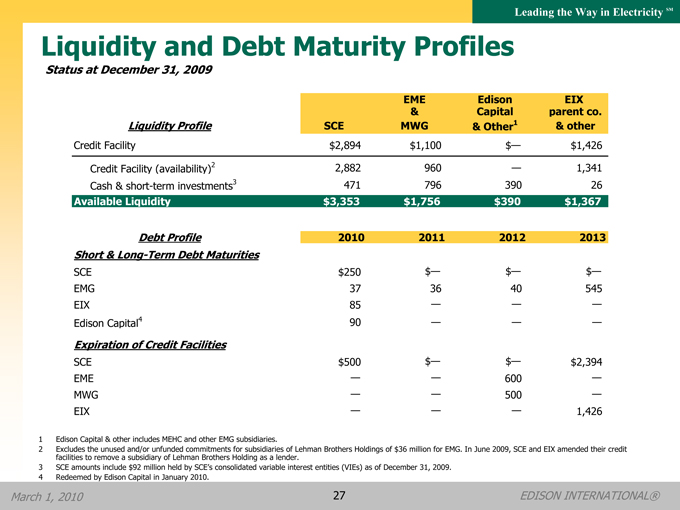

Liquidity and Debt Maturity Profiles

Status at December 31, 2009

Liquidity Profile

SCE

EME & MWG

Edison Capital & Other1

EIX parent co. & other

Credit Facility

$2,894

$1,100

$—

$1,426

Credit Facility (availability)2

2,882

960

—

1,341

Cash & short-term investments3

471

796

390

26

Available Liquidity

$3,353

$1,756

$390

$1,367

Debt Profile

2010

2011

2012

2013

Short & Long-Term Debt Maturities

SCE

$250

$—

$—

$—

EMG

37

36

40

545

EIX

85

—

—

—

Edison Capital4

90

—

—

—

Expiration of Credit Facilities

SCE

$500

$—

$—

$2,394

EME

—

—

600

—

MWG

—

—

500

—

EIX

—

—

—

1,426

1 Edison Capital & other includes MEHC and other EMG subsidiaries.

2 Excludes the unused and/or unfunded commitments for subsidiaries of Lehman Brothers Holdings of $36 million for EMG. In June 2009, SCE and EIX amended their credit facilities to remove a subsidiary of Lehman Brothers Holding as a lender.

3 SCE amounts include $92 million held by SCE’s consolidated variable interest entities (VIEs) as of December 31, 2009.

4 Redeemed by Edison Capital in January 2010.

March 1, 2010 27 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

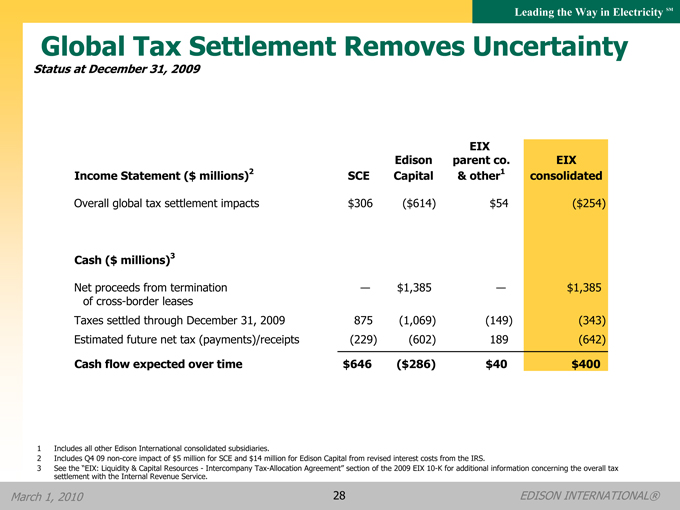

Global Tax Settlement Removes Uncertainty

Status at December 31, 2009

Income Statement ($ millions)2

SCE

Edison Capital

EIX parent co. & other1

EIX consolidated

Overall global tax settlement impacts

$306

($614)

$54

($254)

Cash ($ millions)3

Net proceeds from termination

—

$1,385

—

$1,385

of cross-border leases

Taxes settled through December 31, 2009

875

(1,069)

(149)

(343)

Estimated future net tax (payments)/receipts

(229)

(602)

189

(642)

Cash flow expected over time

$646

($286)

$40

$400

1 Includes all other Edison International consolidated subsidiaries.

2 Includes Q4 09 non-core impact of $5 million for SCE and $14 million for Edison Capital from revised interest costs from the IRS.

3 See the “EIX: Liquidity & Capital Resources—Intercompany Tax-Allocation Agreement” section of the 2009 EIX 10-K for additional information concerning the overall tax settlement with the Internal Revenue Service.

March 1, 2010 28 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

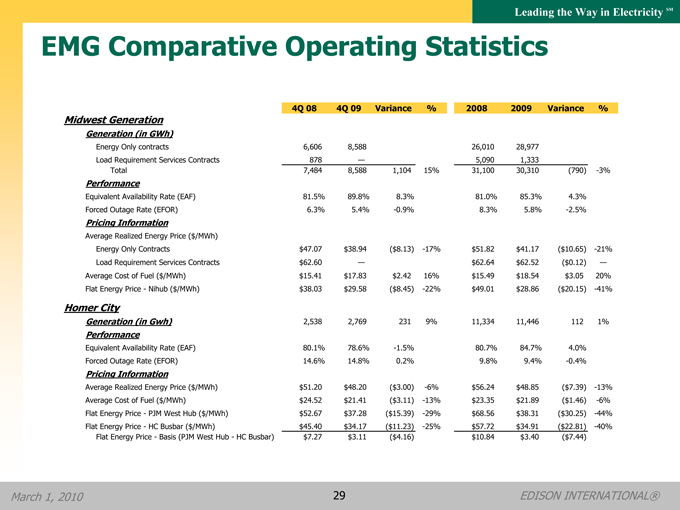

EMG Comparative Operating Statistics

4Q 08

4Q 09

Variance

%

2008

2009

Variance

% Midwest Generation

Generation (in GWh)

Energy Only contracts

6,606

8,588

26,010

28,977

Load Requirement Services Contracts

878

—

5,090

1,333

Total

7,484

8,588

1,104

15%

31,100

30,310

(790)

-3%

Performance

Equivalent Availability Rate (EAF)

81.5%

89.8%

8.3%

81.0%

85.3%

4.3%

Forced Outage Rate (EFOR)

6.3%

5.4%

-0.9%

8.3%

5.8%

-2.5%

Pricing Information

Average Realized Energy Price ($/MWh)

Energy Only Contracts

$47.07

$38.94

($8.13)

-17%

$51.82

$41.17

($10.65)

-21%

Load Requirement Services Contracts

$62.60

—

$62.64

$62.52

($0.12)

—

Average Cost of Fuel ($/MWh)

$15.41

$17.83

$2.42

16%

$15.49

$18.54

$3.05

20%

Flat Energy Price—Nihub ($/MWh)

$38.03

$29.58

($8.45)

-22%

$49.01

$28.86

($20.15)

-41%

Homer City

Generation (in Gwh)

2,538

2,769

231

9%

11,334

11,446

112

1%

Performance

Equivalent Availability Rate (EAF)

80.1%

78.6%

-1.5%

80.7%

84.7%

4.0%

Forced Outage Rate (EFOR)

14.6%

14.8%

0.2%

9.8%

9.4%

-0.4%

Pricing Information

Average Realized Energy Price ($/MWh)

$51.20

$48.20

($3.00)

-6%

$56.24

$48.85

($7.39)

-13%

Average Cost of Fuel ($/MWh)

$24.52

$21.41

($3.11)

-13%

$23.35

$21.89

($1.46)

-6%

Flat Energy Price—PJM West Hub ($/MWh)

$52.67

$37.28

($15.39)

-29%

$68.56

$38.31

($30.25)

-44%

Flat Energy Price—HC Busbar ($/MWh)

$45.40

$34.17

($11.23)

-25%

$57.72

$34.91

($22.81)

-40%

Flat Energy Price—Basis (PJM West Hub—HC Busbar)

$7.27

$3.11

($4.16)

$10.84

$3.40

($7.44)

March 1, 2010 29 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

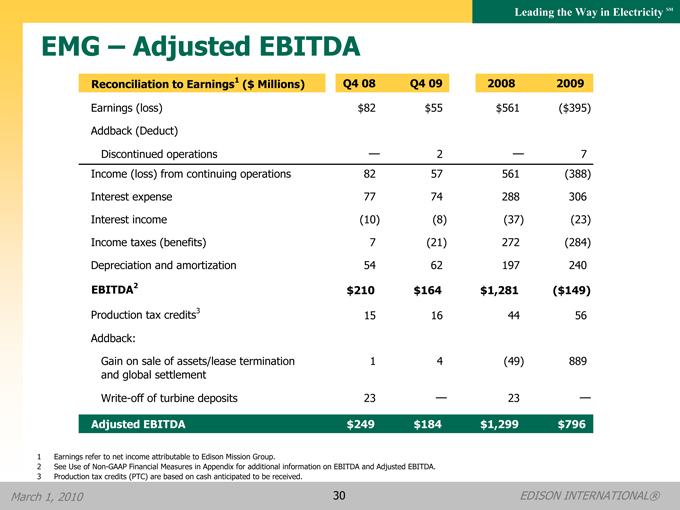

EMG – Adjusted EBITDA

Reconciliation to Earnings1 ($ Millions)

Q4 08

Q4 09

2008

2009

Earnings (loss)

$82

$55

$561

($395)

Addback (Deduct)

Discontinued operations

—

2

—

7

Income (loss) from continuing operations

82

57

561

(388)

Interest expense

77

74

288

306

Interest income

(10)

(8)

(37)

(23)

Income taxes (benefits)

7

(21)

272

(284)

Depreciation and amortization

54

62

197

240

EBITDA2

$210

$164

$1,281

($149)

Production tax credits3

15

16

44

56

Addback:

Gain on sale of assets/lease termination

1

4

(49)

889

and global settlement

Write-off of turbine deposits

23

—

23

—

Adjusted EBITDA

$249

$184

$1,299

$796

1 Earnings refer to net income attributable to Edison Mission Group.

2 See Use of Non-GAAP Financial Measures in Appendix for additional information on EBITDA and Adjusted EBITDA.

3 Production tax credits (PTC) are based on cash anticipated to be received.

March 1, 2010 30 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Fourth Quarter Earnings Summary

Reconcilation of Core EPS to Basic EPS

Core EPS

2008

2009

Variance

SCE

$0.43

$0.51

$0.08

EMG3,4

0.25

0.13

(0.12)

EIX parent company

(0.02)

(0.05)

(0.03)

and other2

Core EPS1

$0.66

$0.59

($0.07)

Non-Core Items

SCE

$—

$0.02

$0.02

EMG

—

0.04

0.04

EIX parent company and other

—

—

—

Total Non-Core

$—

$0.06

$0.06

Basic EPS

$0.66

$0.65

($0.01)

Diluted EPS

$0.66

$0.65

($0.01)

Core EPS Variances

SCE

Higher operating income associated with the CPUC and

0.08

FERC GRC decisions, partially offset by higher income taxes

EMG

Midwest Generation

(0.10)

Higher generation, capacity prices and lower plant costs were more than offset by lower power prices and fuel costs

Homer City

—

Higher capacity prices offset by lower unrealized gains related to derivatives and higher plant costs due to unplanned outage

Renewable energy projects

(0.01)

Higher revenues and operating costs from new projects mainly offset by mild wind conditions

Natural gas and other projects

0.02

Primarily Sunrise project (Q4 2008 unplanned outage) and higher availability payments in 2009

EMMT—Trading

(0.03)

Lower trading income driven by lower congestion

Corporate expense and other items

0.04

Lower income taxes

Edison Capital

(0.04)

Lower lease income and income taxes

Non-Core Variances

SCE

Q4 09: $0.02 for overall tax settlement

0.02

EMG

0.04

Q4 09: $0.04 for overall tax settlement

1 See Use of Non-GAAP Financial Measures in Appendix.

2 The impact of participating securities is included in EIX parent company and other and was zero per share for the quarter ended December 31, 2009 and $(0.01) per share for the quarter ended December 31, 2008.

3 EMMT overhead is included in corporate expense, interest and other items.

4 Includes FAS 133 gains of $0.04 for Q4 08 and $0.03 for Q4 09.

March 1, 2010 31 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Full-Year Earnings Summary

Reconcilation of Core EPS to Basic EPS

Core EPS

2008

2009

Variance

SCE

$2.25

$2.68

$0.43

EMG3,4

1.72

0.68

(1.04)

EIX parent company and other2

(0.13)

(0.11)

0.02

Core EPS1

$3.84

$3.25

($0.59)

Non-Core Items

SCE

($0.15)

$1.08

$1.23

EMG

—

(1.89)

(1.89)

EIX parent company and other

—

0.15

0.15

Total Non-Core

($0.15)

($0.66)

($0.51)

Basic EPS

$3.69

$2.59

($1.10)

Diluted EPS

$3.68

$2.58

($1.10)

Core EPS Variances

SCE

Higher operating income associated with the CPUC and FERC GRC decisions, partially offset by higher income taxes. Favorable impact also from lower than planned financings during the year, primarily from cash received for tax-related timing differences and other benefits.

0.43

EMG

Midwest Generation

(0.65)

Lower power prices, higher ACI and Annual Nox, favorable coal contract buy-out of $0.03 in 2008, partially offset by higher capacity prices, lower plant costs and the 2008 Lehman hedge contract charge

Homer City

(0.03)

Lower power prices, partially offset by higher capacity and lower plant costs

Renewable energy projects

—

Higher revenue offset by higher operating costs

Natural gas and other projects

(0.06)

Lower natural gas prices affecting electricity and steam revenues of Big 4 Projects

EMMT—Trading

(0.19)

Lower trading income driven by lower congestion

Corporate expense and other items

—

Lower income taxes and development costs offset by the 2008 write- off of the Walnut Creek turbine deposit and higher interest expense

Edison Capital

(0.11)

Lower results from leveraged leases and global infrastructure funds, Q2 09 gain on sale of interest in MCV lease of $0.06, gain on sale of interest in Beaver Valley lease of $0.07, and cross border leases in 2009

Non-Core Variances

SCE

1.23

2009: $0.94 for overall tax settlement, $0.14 for Mountainview transfer

2008: $(0.15) for performance-based ratemaking decision

EMG

(1.89)

2009: $(0.02) for discontinued operations, $(1.87) for overall tax settlement

1 | | See Use of Non-GAAP Financial Measures in Appendix. |

2 | | The impact of participating securities is included in EIX parent company and other and was $(0.01) per share for the year-ended December 31, 2009, and $(0.05) per share for the year-ended December 31, 2008. |

3 | | EMMT overhead is included in corporate expense, interest and other items. |

4 | | Includes FAS 133 gains of $0.03 for 2008 and $0.11 for 2009. |

March 1, 2010 32 EDISON INTERNATIONAL®

Lea

Earnings Non-GAAP Reconciliations

Reconciliation of EIX Core Earnings to EIX GAAP Earnings

Earnings (Loss) (in millions)

Quarter Ended December 31,

Year-Ended December 31,

Attributable to Edison International (Unaudited)

2008

2009

2008

2009

Core Earnings1

SCE

$141

$167

$732

$874

EMG

81

42

561

222

EIX parent company and other

(5)

(15)

(29)

(32)

EIX core earnings

$217

$194

$1,264

$1,064

Non-core items

SCE—regulatory items

—

5

(49)

46

Global tax settlement:

SCE

—

—

—

306

EMG

—

14

—

(610)

EIX parent company and other

—

—

—

50

EMG—discontinued operations

—

(1)

—

(7)

Total non-core items

—

$18

($49)

($215)

EIX GAAP Earnings

$217

$212

$1,215

$849

1 See Use of Non-GAAP Financial Measures in Appendix.

March 1, 2010 33 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

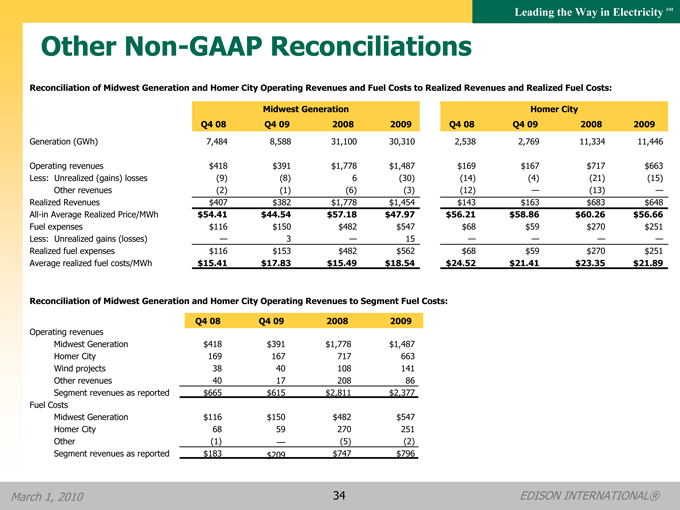

Other Non-GAAP Reconciliations

Reconciliation of Midwest Generation and Homer City Operating Revenues and Fuel Costs to Realized Revenues and Realized Fuel Costs:

Midwest Generation

Homer City

Q4 08

Q4 09

2008

2009

Q4 08

Q4 09

2008

2009

Generation (GWh)

7,484

8,588

31,100

30,310

2,538

2,769

11,334

11,446

Operating revenues

$418

$391

$1,778

$1,487

$169

$167

$717

$663

Less: Unrealized (gains) losses

(9)

(8)

6

(30)

(14)

(4)

(21)

(15)

Other revenues

(2)

(1)

(6)

(3)

(12)

—

(13)

—

Realized Revenues

$407

$382

$1,778

$1,454

$143

$163

$683

$648

All-in Average Realized Price/MWh

$54.41

$44.54

$57.18

$47.97

$56.21

$58.86

$60.26

$56.66

Fuel expenses

$116

$150

$482

$547

$68

$59

$270

$251

Less: Unrealized gains (losses)

—

3

—

15

—

—

—

—

Realized fuel expenses

$116

$153

$482

$562

$68

$59

$270

$251

Average realized fuel costs/MWh

$15.41

$17.83

$15.49

$18.54

$24.52

$21.41

$23.35

$21.89

Reconciliation of Midwest Generation and Homer City Operating Revenues to Segment Fuel Costs:

Q4 08

Q4 09

2008

2009

Operating revenues

Midwest Generation

$418

$391

$1,778

$1,487

Homer City

169

167

717

663

Wind projects

38

40

108

141

Other revenues

40

17

208

86

Segment revenues as reported

$665

$615

$2,811

$2,377

Fuel Costs

Midwest Generation

$116

$150

$482

$547

Homer City

68

59

270

251

Other

(1)

—

(5)

(2)

Segment revenues as reported

$183

$209

$747

$796

March 1, 2010 34 EDISON INTERNATIONAL®

Leading the Way in Electricity SM

Use of Non-GAAP Financial Measures

Edison International’s earnings are prepared in accordance with generally accepted accounting principles used in the United States and represent the company’s earnings as reported to the Securities and Exchange Commission. Our management uses core earnings and earnings per share (EPS) by principal operating subsidiary internally for financial planning and for analysis of performance. We also use core earnings and EPS by principal operating subsidiary when communicating with analysts and investors regarding our earnings results and outlook to facilitate comparisons of the Company’s performance from period to period.

Core earnings is a non-GAAP financial measure and may not be comparable to those of other companies. Core earnings are defined as earnings attributable to common shareholders less income or loss from discontinued operations and income or loss from significant discrete items that management does not consider representative of ongoing earnings. EPS by principal operating subsidiary is based on the principal operating subsidiary net income attributable to the common shareholders of each operating subsidiary, respectively, and Edison International’s weighted average outstanding common shares. The impact of participating securities (vested stock options that earn dividend equivalents that may participate in undistributed earnings with common stock) for each principal operating subsidiary is not material to each principal operating subsidiary’s EPS and is therefore reflected in the results of the Edison International holding company, which we refer to as EIX parent company and other. EIX core EPS and core EPS by principal operating subsidiary are reconciled to basic EPS.

EBITDA is defined as earnings before interest, income taxes, depreciation and amortization. Adjusted EBITDA includes production tax credits from EMG’s wind projects and excludes amounts from gain on the sale of assets, loss on early extinguishment of debt and leases, and impairment of assets and investments. Our management uses Adjusted EBITDA as an important financial measure for evaluating EMG.

The average realized energy price and average realized fuel cost is a non-GAAP performance measure since such statistical measures exclude unrealized gains or losses recorded as operating revenues and unrealized gains or losses recorded as fuel expenses. Management believes that the average realized energy price and average realized fuel cost is more meaningful for investors as it reflects the impact of hedge contracts at the time of actual generation in period-over-period comparisons or as compared to real-time market prices.

A reconciliation of Non-GAAP information to GAAP information, including the impact of participating securities, is included either on the slide where the information appears or on another slide referenced in this presentation.

March 1, 2010 35 EDISON INTERNATIONAL®