Exhibit 99.1

2006 Analyst Day Event

Realizing Our Dream

Forward Looking Statements

Statements used in this presentation that relate to future plans, events, financial

results or performance are forward-looking statements that are subject to certain

risks and uncertainties including, among others, such factors as our ability to

continue to successfully execute our strategic initiatives and growth strategy; the

efficiency and effectiveness of our advertising and marketing programs; consumer

acceptance of our products, new product offerings and brand image; our ability to

execute our retail store distribution strategy; our ability to execute our wholesale

distribution strategy; our ability to maintain cost-effective sales, production and

delivery of our products; inflationary pressures caused by rising fuel and

commodity costs; the impact of outstanding litigation claims, including the potential

impact of any adverse publicity; competitive trends in the bedding industry;

uncertainties arising from general economic conditions, consumer confidence and

global events, as well as the risk factors listed from time to time in the company’s

filings with the SEC, including the company’s Annual Report on Form 10-K and

other periodic reports filed with the SEC.

1

Chairman and Chief Executive Officer

Bill McLaughlin

Reinvented a commodity product,

dramatically enhancing quality and service…

Built a vertically integrated supply chain to

ensure consistent quality…

Focused on company-owned stores to deliver

a distinctive retail experience…

Created a brand experience worthy of a

premium price

Starbucks’ Story

3

Old line industry leaders, highly recognizable

brand names, but not strong brand

Premium price of mass market products

Huge markets, growth only in premium

segments

Strong gross margins

Growth accelerated by word of mouth

Strong management teams

Industry skepticism high in early years

Other Similarities

4

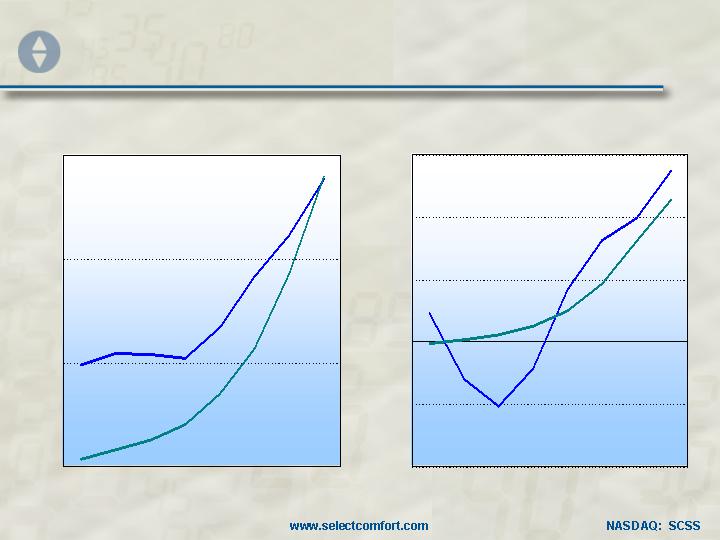

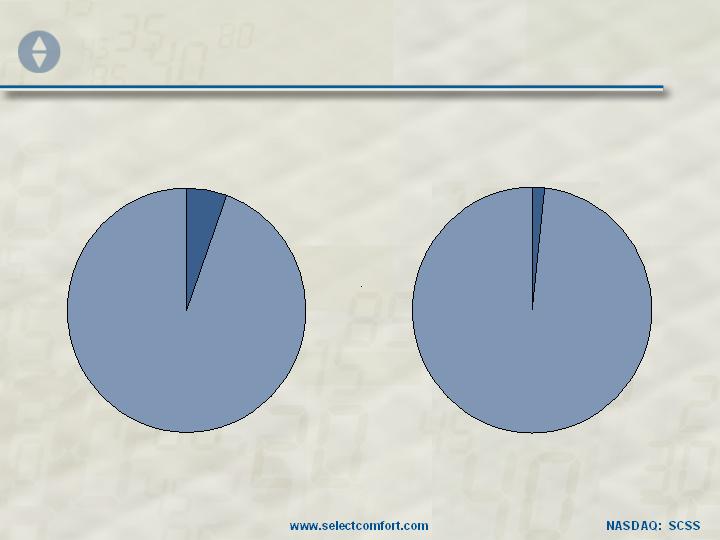

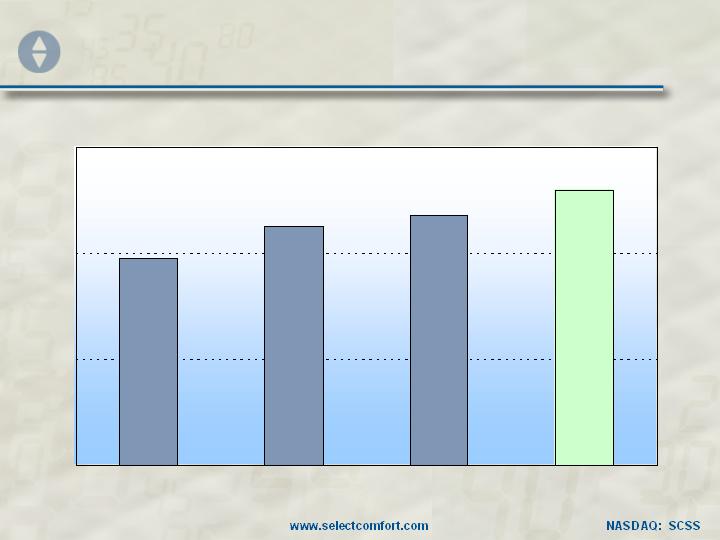

Similar Financial Performance

Net Operating Profit

($ in millions)

$75

$(50)

0

1996

2005

Revenue

($ in millions)

$750

0

SBUX 1989

SCSS 1998

SBUX

SCSS

1996

2005

SBUX 1989

SCSS 1998

SBUX

SCSS

5

SBUX Circa ’96 Closely

Resembles SCSS Circa ‘05

SBUX

SCSS

1996

2005

698

691

57

69

42

44

11%

37%

~3%

~6%

Sales

Operating Income

Net Income

ROE

U.S. Market Share

6

Essentially the Same Story!

Select Comfort’s Story

Reinvented a commodity product, dramatically

enhancing quality and service…

Focused on company-owned stores to deliver

a distinctive retail experience…

Built a vertically integrated supply chain to

ensure consistent quality…

Created a brand experience worthy of a

premium price

7

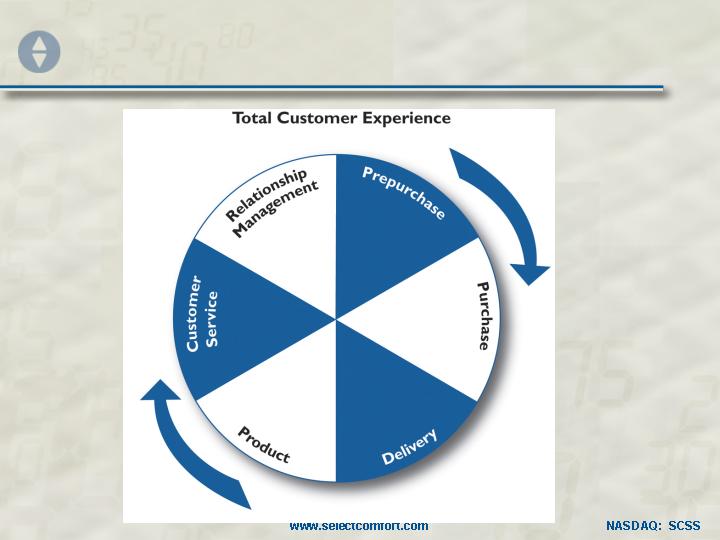

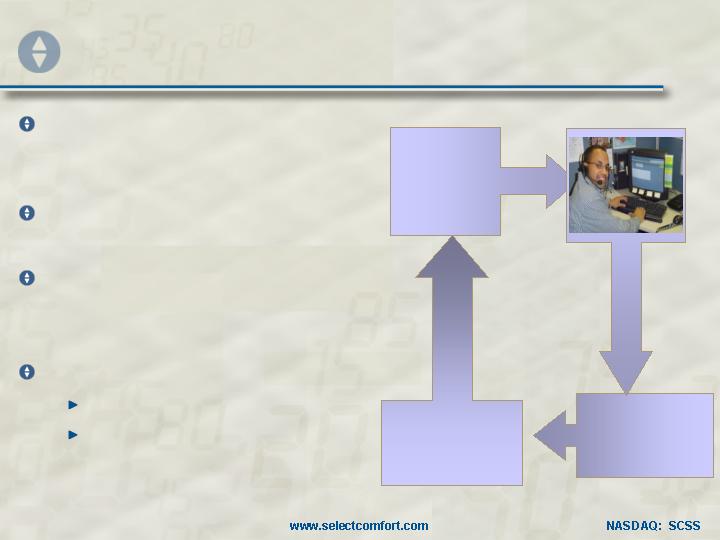

Consumer Loyalty Experience

8

Starts with Differentiated

Product/Service

9

Why Our Business Model?

Differentiated Product that’s Complex

Air Control System

Chambers

Sewing

Daily Use

10-20 Years

Marketing and Sales Challenge

Consumers—low interest, long purchase cycle, skeptical

Selling—longer process, more Q&A, confidence

High Cost of Customer Acquisition—“Razor Blade” for Leverage

Referral

Repeat

Accessories

Total Experience of Customer Satisfaction

10

Business Model

Industry

Select Comfort

Brand

Sell

Make

Deliver

Service

Relationship

Mfg 1

Mfg 2

Mfg 3

Retail 3

Retail 2

Retail 1

Retail

Mfg

Delivery

Service

Customer

Customer

11

Awareness

Distribution

Innovation

Leverage

People

&

Systems

Expand

Strategies

12

Awareness

Distribution

Innovation

Leverage

People

&

Systems

Expand

Strategies/Competitive Advantages

1. Product Design

2. Brand

3. Quality, Cost,

Flexibility, Service

5. Balance Sheet and

Cash

4. Controlled

Distribution

6. People & Culture

13

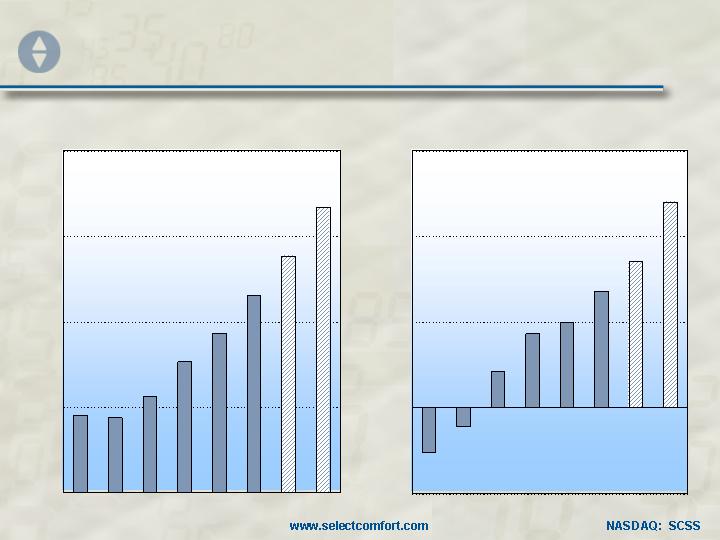

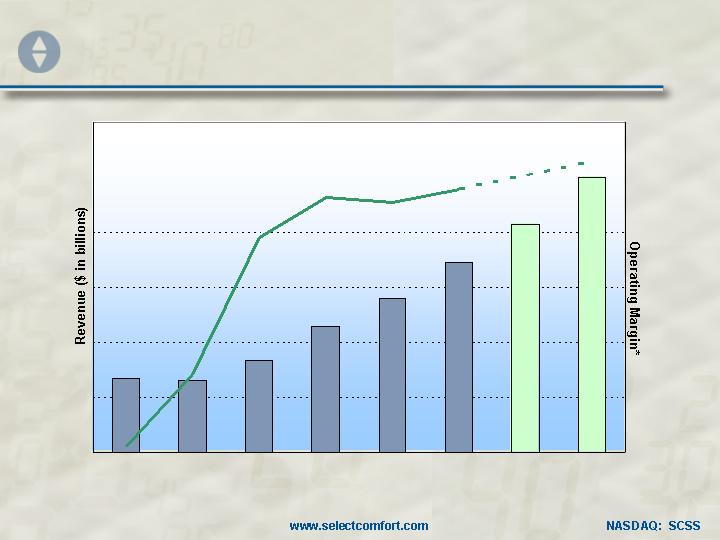

Realizing Our Dream

Revenue

($ in billions)

$1.2

0

$150

$(50)

0

Net Operating Profit

($ in millions)

2000

2007E

2000

2007E

2005

2005

14

Doug

Awareness

Keith

Distribution

Doug

Innovation

Kathy

Leverage

People

&

Systems

Expand

Agenda

15

Awareness

Distribution

Innovation

Leverage

People

&

Systems

Expand

16

SVP, Chief Marketing Officer

Doug Collier

Chief Marketing Officer

Doug Collier

17

Agenda

Market Opportunity

Strong Starting Platform

Opportunities to Enhance and Advance

18

The Size of Our Opportunity

5.5%

1.6%

2005E U.S. Mattress Industry

Source: International Sleep Products Association (ISPA) and company information.

Wholesale

$6.3 billion

Units

22 million

19

2002

2005E

The Size of Our Opportunity

75%

40%

$500+ Price Point Segment - Queen Sets

69%

Source: International Sleep Products Association (ISPA) and company information.

20

2005E

2010E

The Size of Our Opportunity

$35B

$40B

0

U.S. Mattress

U.S. Bedding Accessories

Int’l Mattress

Estimated Retail Market

Source: International Sleep Products Association (ISPA), CSIL Milano and company information.

21

Situation in 2000

Low awareness…

number one barrier to

growth

Air bed had negative

connotations…and not

proprietary

Dominated by company’s

direct-marketing heritage

22

Our Marketing Model

Broad appeal of Sleep

Number® concept and

advertising campaign

Focus on unique product

feature of personalized

comfort

Message strongly integrated

across all brand touchpoints

Major investment in media

to drive awareness

23

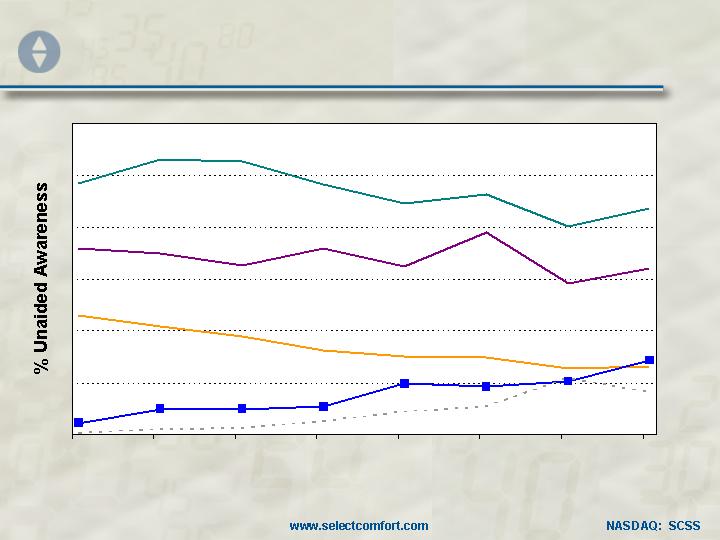

National Unaided Brand Awareness

Jan-02

Jul-02

Jan-03

Jul-03

Jan-04

Jul-04

Jan-05

Jul-05

Sealy

Sealy

Simmons

SCSS

TPX

Source: Third-party research.

13%

60%

0%

24

Moving the Model Forward

Compelling

Creative

Media

Investment

Differentiated

Product

In-Store

Experience

Consumer

Loyalty

25

Moving the Model Forward

Compelling

Creative

Media

Investment

Differentiated

Product

In-Store

Experience

Consumer

Loyalty

New Sleep Number®

campaign…leverage across

all touchpoints

New web-site

Communicate store

experience

26

27

Moving the Model Forward

Compelling

Creative

Media

Investment

Differentiated

Product

In-Store

Experience

Consumer

Loyalty

Continue increasing media

investment…efficiently

28

2000

2006E

Media Spending

$120

0

15%

7%

29

Moving the Model Forward

Compelling

Creative

Media

Investment

Differentiated

Product

In-Store

Experience

Consumer

Loyalty

Continue increasing media

investment…efficiently

Increase on-line spending 4X

Increased use of retail

activation tools

30

New Tools – Sunday Inserts

31

Moving the Model Forward

Compelling

Creative

Media

Investment

Differentiated

Product

In-Store

Experience

Consumer

Loyalty

R&D investment up 2X

…build pipeline of

innovation

Accessories growth…new

products, unique features

32

Moving the Model Forward

Compelling

Creative

Media

Investment

Differentiated

Product

In-Store

Experience

Consumer

Loyalty

New in-store and lease line

tools to drive traffic and

brand

Advance store design and

in-store experience

33

Moving the Model Forward

Compelling

Creative

Media

Investment

Differentiated

Product

In-Store

Experience

Consumer

Loyalty

Redesign loyalty program

…drive referrals and repeat

purchase

Consumer insight…refine

and customize message

34

Summary

Strong and Expanding Market Opportunity

Strong Starting Marketing Platform

Opportunities to Enhance and Advance

35

Awareness

Distribution

Innovation

Leverage

People

&

Systems

Expand

Keith Spurgeon

SVP, GM - Consumer Channels

36

Senior Vice President and

General Manager,

Consumer Channels

Keith Spurgeon

37

Integrating Sales and Marketing

Compelling

Creative

Media

Investment

Differentiated

Product

In-Store

Experience

Consumer

Loyalty

Differentiation and Sustainable

Competitive Advantage

Maximize Revenue and

Operating Leverage

Improve Distribution and

Sales Experience

Increase Awareness and

Traffic

38

Advantaged Distribution

Retail

Direct

eCommerce

Retail Partners

Other

Total

Retail Stores - 77%

Direct – 11%

eCommerce – 5%

Retail Partners – 3%

2005 Revenue Mix

Other – 4%

2000-2005

20%

9%

34%

NM

NM

20%

CAGR

39

Advantaged Distribution

Control

Brand

Distribution

Selling Process

Focus

Personnel

Product

Customer Loyalty

Be Where the

Customer is

Lifetime Customer

Relationship

Retail Stores - 77%

Direct – 11%

eCommerce – 5%

Retail Partners – 3%

2005 Revenue Mix

Other – 4%

40

Sustainable Growth

Same Store

New Stores

Retail

Partners

New

Channels

Continued

Organic

Growth

5% - 10%

Annual Store

Count Growth

Increasing

Share of Retail

Partners’

Business

Incremental

Opportunities

41

The Store is the Core

Growing

Revenues

Same Store

Sales

New Stores

Consumer-

Driven Mix

Bedding

Accessories

Compelling

Store Model

2003

2004

2005

2006E

49%

64%

77%

90%

0

8%

14%

20%

Stores >$2M

Stores >$1M

Stores <$1M

450

Stores Open > 12 Months

42

Targeted New Store Economics ($000)

~12 months

Payback

$200+

Store Investment

22%

Profit Margin

$200

First Year Profit

$900

First Year Sales

The Store is the Core

43

The Store is the Core

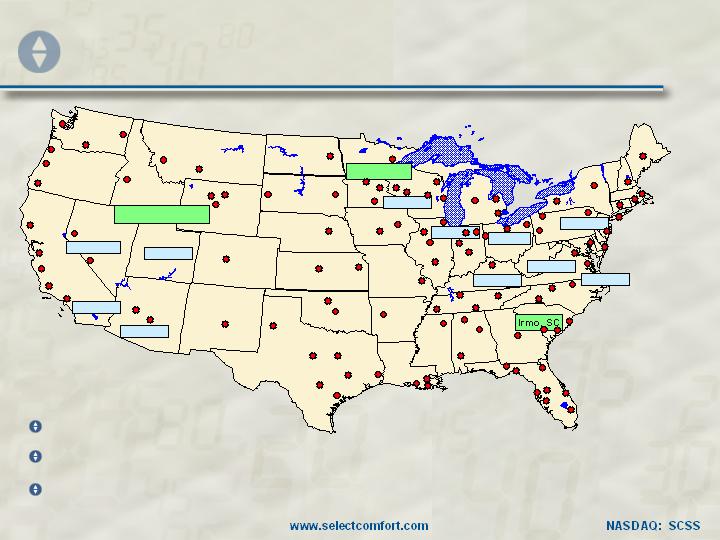

600-650 Stores

Non-Mall

396 Stores

Mall-Based

Locations

Mall-Based

Locations

Non-Mall

44

The Store is the Core

Store Locations

Promotions

People

Compensation & Incentives

In-Store Tools

Store Experience

Retention /

Stability

Traffic /

Higher Conversion

Customer Satisfaction

45

Retail Partner Strategy

Objectives

Principles

Criteria

Preferred Partners

Healthy Back

46

Retail Partner Strategy

Objectives

Leverage

Advertising

Increase Market

Share

First Choice of

Retail Partners

Pre-empt

Competition

Better Bedding

47

Retail Partner Strategy

Objectives

Principles

Semi-Exclusive

Controlled

Program

Incremental

Criteria

Preferred Partners

Sleep Train

48

Retail Partner Strategy

Objectives

Principles

Criteria

Dominant Player

Quality Success

Brand Building

Preferred Partners

Mattress Firm

49

Retail Partner Strategy

Objectives

Principles

Criteria

Preferred Partners

Exclusivity

Brand Strength

Product Quality

Service & Support

Dedicated

Trainers

50

Leading Bedding Retailers

Source: Furniture|Today, Aug. 1, 2005

# Stores

370

318

314

108

Select Comfort

Sleepy’s

Mattress Firm

The Sleep Train

2004

Sales Rank

# 1

# 2

# 3

# 8

51

Integrating Sales and Marketing

Compelling

Creative

Media

Investment

Differentiated

Product

In-Store

Experience

Consumer

Loyalty

Differentiation and Sustainable

Competitive Advantage

Maximize Revenue and

Operating Leverage

Improve Distribution and

Sales Experience

Increase Awareness and

Traffic

52

Awareness

Distribution

Innovation

Leverage

People

&

Systems

Expand

SVP, Global Operations

Kathy Roedel

53

Senior Vice President,

Global Operations

Kathy Roedel

54

Introducing Global Operations

Sourcing

Logistics

Home

Delivery

Customer

Service

Manufacturing

Product

Design

Secret Weapon…

55

Delivering competitive advantage

Driving customer loyalty

Keys to Advantage & Loyalty

Complex product – history and scale

Flexible JIT supply chain – quality, cost, cash

Integrated, company owned Service

People & culture

56

Complex, Differentiated Product

More than a bed…a “sleep system”

User Interface - Controls

Service 7 days/week

20 Year Durability

Modularity

Air Control System

57

Salt Lake City UT

Minneapolis

Key Operations Locations

Foundations

Fabric

Foam

Foam

Foam

Foundations

Foundations

Foam

Foundations

Foundations

Foundations

2 Manufacturing Locations + HQ (Partner Fulfillment)

Global & Local Suppliers

Home Delivery thru 100+ cross docks

58

Keys to Advantage & Loyalty

Complex product – history and scale

Flexible JIT supply chain – quality, cost, cash

Integrated, company owned Service

People & culture

59

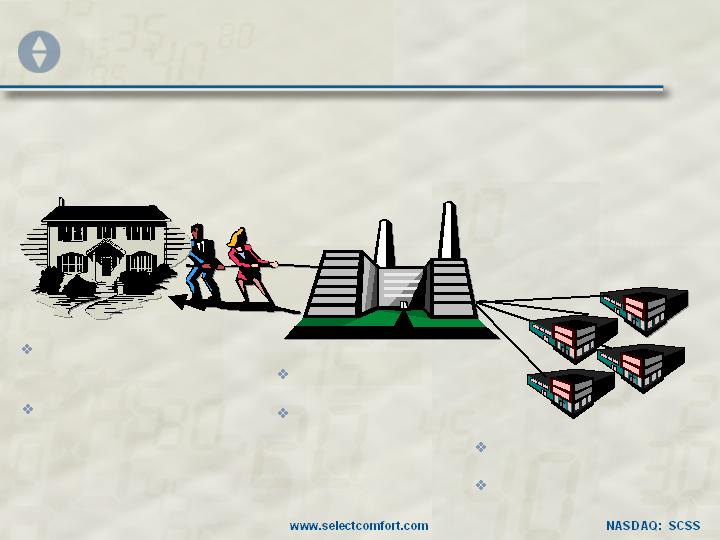

Just In Time – Flexibility & Cash

Select Comfort

Manufacturing

Customer’s

Home

Suppliers

Build to Order

Ship < 48 hours

No warehouse

…no inventory

Short supply lines

Hrs –> Days Raw Mat’l

Customer sees

“out of box” quality

60

Quality…Zero Defect Culture

Designed for manufacture & service-ability

Suppliers… qualified, certified, audited,

selectively exclusive

Mistake Proofed Processes

Quality Built In – “Do / Check”

Rapid Response – daily customer pulse

61

Keys to Advantage & Loyalty

Complex product – history and scale

Flexible JIT supply chain – quality, cost, cash

Integrated, company owned Service

People & culture

62

Select Customer Service

Customer care specialists

…Sleep Number bed owners!

Continuous Improvement

Closed loop process

Rapid response

Zero

Defect

Culture

Customer Data

Root Cause

Analysis

Design & Mfg

Improvements

Great

Customer

Service

All Channels, 7 days/week

Metrics & Incentives

63

Home Delivery Service

Select Comfort controls the entire customer experience

…right into their bedroom!

Centralized Scheduling

White Glove Treatment

Great Feedback

Seals the deal…best

bed buying decision!

64

Product

Design

Productivity

“JIT”

Supply Chain

Flexibility

& Cost

Co.-owned

Service

Faster

Order Delivery

Building on Success

People &

Culture

Even deeper

bench

Refined design for mfg

Six Sigma pilots

Dual sourcing strategy

2010 capacity plan

Pilot new network design

Continuous optimization

Training and staffing

65

Keys to Advantage & Loyalty

Complex product – history and scale

Flexible JIT supply chain – quality, cost, cash

Integrated, company owned Service

People & culture

66

Operations Leadership Team

Kathy Roedel

Global Operations

4/4/05

Joy Grant

Administrative Support

3/31/92

Mark Sponsler

Home Delivery

3/1/05

Darrell Olson

Logistics

11/7/95

Kathleen Graber

Supply Chain

5/31/95

Dave Menssen

Cust. Service

8/3/98

Don Hancock

Mfg – SLC, UT

5/24/99

Ron McCoy

Mfg – Irmo, SC

12/6/04

Todd Dockter

Capacity Programs

1/5/98

Hunter Saklad

Finance

10/1/04

Alix Colehour

Human Resources

8/30/04

Junell Erickson

Info Systems

2/25/02

Justin Revak

Mfg – Mpls, MN

10/2/05

67

Winning Team & Culture

Passion for customers and results

100% bonus participation

Innovation mindset

Community commitment

Proud of accomplishments

Bullish on our future!

68

Global Operations

Sourcing

Logistics

Home

Delivery

Customer

Service

Manufacturing

Product

Design

Secret Weapon…

Delivering competitive advantage

Driving customer loyalty

69

Chief Financial Officer

Jim Raabe

70

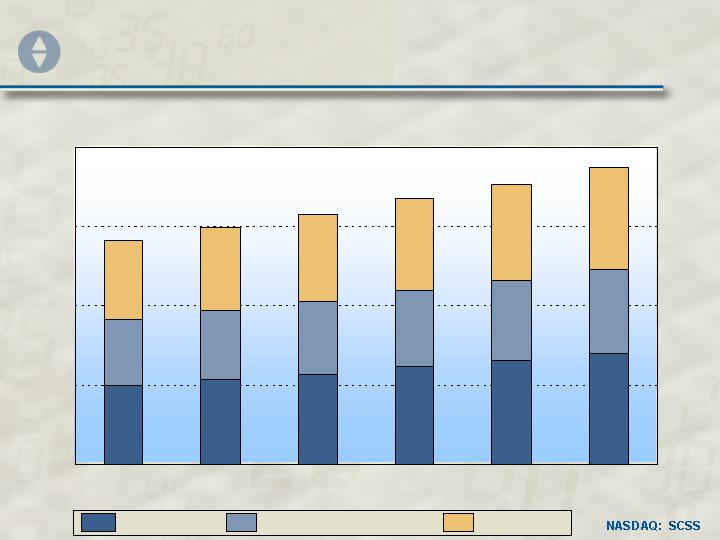

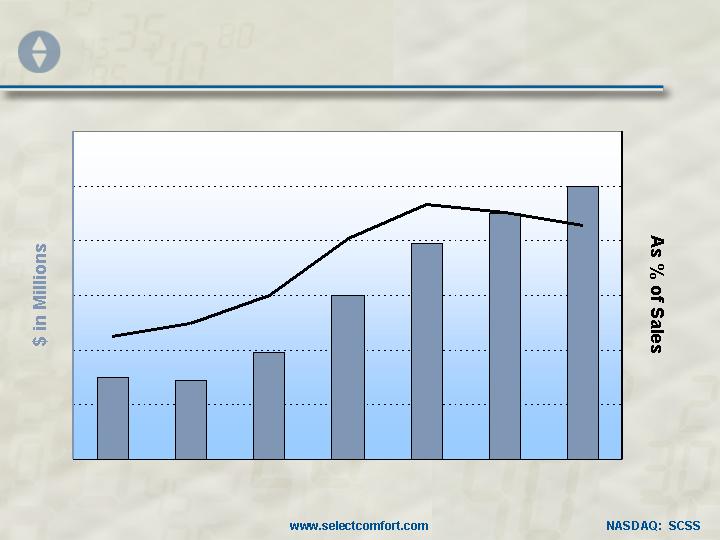

Sustainable Growth

Multiple Sources of Growth

Multiple Sources of Leverage

Internally Funded

71

2000

2001

2002

2003

2004

2005

2006E

2007E

$1.0B

$0

15%

-10%

12%

*Note: Before stock option expense

Realizing Our Dream

72

Multiple Sources of Growth

Operating Margin

G&A

Media

Selling Margin (Ex-Media)

Gross Margin

Sales

Total

Wholesale

Company-

owned

*Including Radisson sales

92%

62%

31%

8%

34%*

26%*

100%

59%

31%

13%

8%

10%

73

Consistent Revenue Growth

+

Hospitality - year 2

Int’l - initial investment

QVC/RV

New Channels

15% - 20%

2 - 3%

100% more doors

10% 20% share of floor

Retail Partner

4 - 6%

45 - 50 Stores

New stores

9 - 11%

7-12% Target

Media + 15%

30 store relocations

e-Commerce/Direct

Same store growth

Consolidated Sales

74

Consistent Margin Growth to ‘07

~ 0.5 ppt

G&A

~ 1.0 ppt

Selling

~ 0.5 ppt

Marketing

- -

Gross Margin

75

Cash from Operations: Funds Growth

2002

2003

2004

2005

2006E

2007E

110

0

Free

Cash

Flow

Capital

76

THANK YOU!

Demonstrated Performance

Proven Strategies

Multiple Sources of Growth

Competitive Advantages

Strong Culture

Depth of Management

77