| | |

| UNITED STATES

SECURITIES AND EXCHANGE COMMISSION |

| | |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| | |

| Investment Company Act file number: | (811-05452) |

| | |

| Exact name of registrant as specified in charter: | Putnam Premier Income Trust |

| | |

| Address of principal executive offices: | 100 Federal Street, Boston, Massachusetts 02110 |

| | |

| Name and address of agent for service: | Stephen Tate, Vice President

100 Federal Street

Boston, Massachusetts 02110 |

| | |

| Copy to: | Bryan Chegwidden, Esq.

Ropes & Gray LLP

1211 Avenue of the Americas

New York, New York 10036 |

| | |

| | James E. Thomas, Esq.

Ropes & Gray LLP

800 Boylston Street

Boston, Massachusetts 02199 |

| | |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| | |

| Date of fiscal year end: | July 31, 2023 |

| | |

| Date of reporting period: | August 1, 2022 – July 31, 2023 |

| | |

|

Item 1. Report to Stockholders: | |

| | |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: | |

Putnam

Premier Income

Trust

Annual report

7 | 31 | 23

Message from the Trustees

September 11, 2023

Dear Fellow Shareholder:

Stocks have generally advanced through much of 2023. Innovations in technology have attracted strong investor interest, helping that sector rebound and lead the market higher. More broadly, international markets are generally performing well, even though the reopening of China’s economy lacked the dynamism many had anticipated.

Bond markets have been more uneven, with some areas gaining and others down moderately. The U.S. Federal Reserve has continued to lift interest rates, but at a more gradual pace than in 2022. U.S. inflation has eased, while the country’s economic growth has remained positive. Against this backdrop, investors are weighing the impact of high borrowing costs, stress in the banking system, and a weaker housing market.

As active managers, your investment team continues to research attractive opportunities for your fund while monitoring risks. This report offers an update on their efforts.

Thank you for investing with Putnam.

Data are historical. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and net asset value (NAV) will fluctuate, and you may have a gain or a loss when you sell your shares. Performance assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart are at NAV. See below and pages 9–10 for additional performance information, including fund returns at market price. Index and Lipper results should be compared with fund performance at NAV.

All Bloomberg indices are provided by Bloomberg Index Services Limited.

Lipper peer group median is provided by Lipper, a Refinitiv company.

* The fund’s primary benchmark, the ICE BofA U.S. Treasury Bill Index, was introduced on 6/30/92, which post-dates the inception of the fund.

This comparison shows your fund’s performance in the context of broad market indexes for the 12 months ended 7/31/23. See above and pages 9–10 for additional fund performance information. Index descriptions can be found on page 18.

All Bloomberg indices are provided by Bloomberg Index Services Limited.

Please describe investing conditions during the 12-month reporting period.

Bond markets were challenged by persistent inflation, central bank tightening, and recessionary fears during the period. In March 2023, a banking crisis caused by the failure of three U.S. regional banks also weighed on investor sentiment. Action by policymakers helped to limit contagion across the financial system.

As U.S. inflation declined, the U.S. Federal Reserve began to reduce the size and pace of its interest-rate hikes in December 2022. Even with this moderation, the federal funds rate climbed to a 22-year high of 5.25%–5.50% at period-end. U.S. home prices, which enjoyed rapid price appreciation during the pandemic, began to soften. Consumer spending weakened but remained positive. A strong labor market helped keep the U.S. economy in expansion, which boosted investor confidence.

Credit spreads widened early in the period and began to tighten as investor sentiment improved. [Spreads are the yield advantage credit-sensitive bonds offer over comparable-maturity U.S. Treasuries. Bond prices rise as yield spreads tighten and decline as spreads widen.] The yield on the benchmark

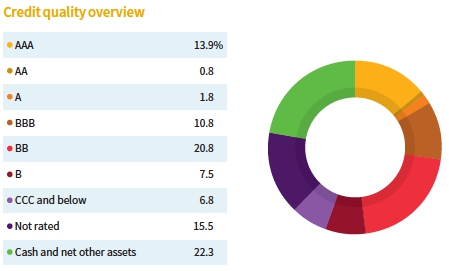

Credit qualities are shown as a percentage of the fund’s net assets as of 7/31/23. A bond rated BBB or higher (A-3 or higher, for short-term debt) is considered investment grade. This chart reflects the highest security rating provided by one or more of Standard & Poor’s, Moody’s, and Fitch. Ratings and portfolio credit quality will vary over time. Due to rounding, percentages may not equal 100%.

Cash and net other assets, if any, represent the market value weights of cash, derivatives, and short-term securities in the portfolio. The fund itself has not been rated by an independent rating agency.

This table shows the fund’s top holdings across three key sectors and the percentage of the fund’s net assets that each represented as of 7/31/23. Short-term investments, to-be-announced commitments, and derivatives, if any, are excluded. Holdings may vary over time.

10-year U.S. Treasury began the period at 2.67% and reached a high of 4.25% in October 2022 before ending the period at 3.97%.

How did the fund perform for the 12-month reporting period?

The fund returned 0.39% at net asset value, underperforming its primary benchmark, the ICE BofA U.S. Treasury Bill Index, which returned 3.94%, and the median return of its Lipper peer group, which returned 6.35%. The fund outperformed its secondary benchmark, the Bloomberg Government Bond Index, which returned –3.93%.

Which strategies detracted from fund performance during the reporting period?

Term structure risk strategies were the largest detractors from fund performance. The period was marked by higher yields and an inverted yield curve, which happens when yields on longer-term bonds fall below those of shorter-term bonds. These conditions negatively impacted the fund, which is positioned with a structural positive duration that has settled around four years. Our structural duration positioning and discretionary relative value strategies drove the fund’s underperformance relative to its primary, cash benchmark.

Currency risk strategies modestly detracted from fund performance. This strategy employs a hedge of safe-haven currencies that typically do well in risk-averse investing environments. We held a long position to the U.S. dollar, Japanese yen, and Swiss franc versus the remaining G10 currencies [the top 10 most traded currencies in the world]. During the period, the Japanese yen weakened, the Swiss franc strengthened, and the U.S. dollar fluctuated relative to all G10 currencies, which led to the strategies’ underperformance.

What strategies helped fund performance during the reporting period?

Corporate credit strategies were the fund’s largest contributors, led by high-yield bonds and convertibles. High-yield spreads tightened by approximately 100 basis points from the start of 2023 to period-end, as measured by the JPMorgan Developed High Yield Index. Prepayment risk strategies, led by our mortgage basis positioning, also were additive. We shifted to a long basis positioning in late 2022, which was beneficial as the mortgage basis significantly tightened. The fund’s long mortgage basis positioning is a strategy that capitalizes on the difference between longer-term U.S. Treasury yields and the interest rates on 30-year home mortgages.

Our agency interest-only securities, emerging market [EM] risk strategies, and exposure to residential mortgage credit, led by our seasoned credit risk transfer [CRT] holdings, also helped results. CRTs performed well as they continued to be tendered by issuers and received some upgrades by rating agencies.

How did you use derivatives during the reporting period?

We used CMBX credit default swaps to hedge the fund’s commercial mortgage-backed securities [CMBS] credit and market risks, and to gain access to specific areas of the market.

We used bond futures and interest-rate swaps to take tactical positions along the yield curve, and to hedge the risk associated with the fund’s yield curve positioning. We also employed interest-rate swaps to gain exposure to interest rates in various countries. We utilized options to hedge duration and convexity, to isolate the prepayment risk associated with our holdings of collateralized mortgage obligations, and to help manage overall portfolio downside risk. We used total return swaps as a hedging tool and to help manage the portfolio’s sector exposure and inflation risk. In addition, we used currency forward contracts to hedge the portfolio’s

exposure to non-U.S. currencies and to gain exposure to various currencies.

What are your current views on the various sectors in which the fund invests?

Corporate fundamentals have been strong year to date. We do not believe a recession is imminent given the absence of further stress in the financial sector. We believe the economy may slow or experience a mild recession in calendar 2024. We expect market technicals [supply/demand metrics] will be influenced by broader risk appetite in the near term. We believe valuations are still somewhat attractive, especially among high-yield bonds and lower-dollar prices. Credit spreads are pricing in a continued increase in defaults along with slower growth, but they do not signal a harsh recession, in our view.

High inflation, central bank tightening, slowing growth, and tighter credit conditions remain considerable headwinds to fundamentals and market technicals, in our view. We believe we are nearing a point when the Fed’s interest-rate hiking cycle will start to wind down. We are monitoring industry and company fundamentals, the health of balance sheets, the generation and use of free cash flow, and the resiliency of credit to slow economic growth.

The broad commercial real estate market is facing meaningful headwinds and increased risks, in our view. The risk of recession remains a concern as the Fed continues to combat inflation by raising the cost of risk-free capital. We believe some of these risks already have been priced in to the CMBS market, which experienced significant spread widening in calendar 2022. In our view, the most attractive relative value opportunities will require detailed analysis and security selection. We expect greater return dispersion across the market in the near term, which we believe underscores the importance of rigorous loan-level analysis to uncover relative value. We favor shorter spread duration assets, including seasoned mezzanine tranches on deals with high-quality collateral. We believe these deals are attractively valued and provide insulation from losses, even in deep recessionary scenarios.

Within residential mortgage credit, U.S. homeowner balance sheets are well positioned, in our view. Homeowners who locked in ultra-low mortgage rates have been benefiting from rapid home price appreciation in recent years. We believe the risk of a housing or economic correction that would cause widespread defaults and delinquencies is low. Based on this view, supply is unlikely to grow from distressed home sales. Given our cautious macro and housing outlooks, we favor higher-quality bonds with shorter spread durations. We also prefer bonds with seasoned collateral that we believe can withstand home price declines due to significant built-up home equity.

Our intermediate outlook for EM is cautious, although we believe recession risks and inflation risks are declining. China’s economic reopening in late calendar 2022 has been disappointing, challenging the idea of a sustained recovery, in our view. However, the global growth outlook doesn’t appear to be as challenging as we anticipated earlier this year. We expect to see some monetary policy adjustments if a severe economic slowdown materializes. We believe central banks will be somewhat constrained based on continued inflationary pressures.

Regardless of the policy path, we continue to believe higher-grade EM names are overvalued in the current environment. We see the risks of recession and inflation declining, which we believe should be supportive of EM over the near term. Distressed names appear to be rich given current market dynamics. As such, we expect a bit more downside within the next three to nine months, but timing remains a

challenge. We prefer to stay beta neutral and seek relative value opportunities, remaining very selective in our high-yield risk exposure.

We expect prepayment speeds will be stable going forward. We believe the sector can provide good protection against a potential recession. Macro volatility in interest rates can hinder performance, but we expect volatility will decline. We believe many prepayment-sensitive assets offer an attractive risk-adjusted return at current price levels and significant upside potential if rates stabilize and volatility declines.

Our selection efforts span a variety of collateral types that we believe are attractively priced based on anticipated prepayment speeds. We have a neutral to slightly long mortgage basis positioning. Uncertainty related to banks’ willingness to buy mortgages remains a focus. However, we are encouraged by robust sales of the FDIC’s mortgage holdings. We remain tactical and will actively trade the basis as new information emerges and events occur.

As of July 31, 2023, what is the team’s outlook?

In the near term, we expect uncertainty to remain high and market volatility to persist. The strength of the U.S. labor market will keep Fed policy hawkish, in our view. That said, the labor market is very sensitive to inflation and interest-rate changes. The fund maintains a position at the lower end of the risk spectrum with lower spread duration across credit sectors.

What were the fund’s distributions during the period?

The fund’s distributions are fixed at a targeted rate. The targeted rate is not expected to vary with each distribution, but may change from time to time. During the last fiscal year, the fund made monthly distributions totaling $0.312 per share from August 2022 to July 2023, which were characterized as $0.260756 per share of net investment income and $0.051244 per share of return of capital.

Distributions of capital decrease the fund’s total assets and total assets per share and, therefore, could have the effect of increasing the fund’s expense ratio. In general, the policy of fixing the fund’s distributions at a targeted rate does not affect the fund’s investment strategy. However, in order to make these distributions, on occasion the fund may have to sell portfolio securities at a less than opportune time.

[Please see the Distributions to shareholders note on page 90 for more information on fund distributions.]

Thanks for your time and for bringing us up to date, Mike.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. Disclosures provide only a summary of certain changes that have occurred in the past fiscal period, which may not reflect all of the changes that have occurred since an investor purchased the fund. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future.

Current and future portfolio holdings are subject to risk. Statements in the Q&A concerning the fund’s performance or portfolio composition relative to those of the fund’s Lipper peer group may reference information produced by Lipper Inc. or through a third party.

CLOSED-END FUNDS OFFER DISTINCTIVE CHARACTERISTICS

Closed-end funds have some key characteristics that you should understand as you consider your portfolio strategies.

More assets at work Closed-end funds are typically fixed pools of capital that do not need to hold cash in connection with sales and redemptions, allowing the funds to keep more assets actively invested.

Traded like stocks Closed-end fund shares are traded on stock exchanges.

They have a market price A closed-end fund has a per-share net asset value (NAV) and a market price, which is how much you pay when you buy shares of the fund, and how much you receive when you sell them.

When looking at a closed-end fund’s performance, you will usually see that the NAV and the market price differ. The market price can be influenced by several factors that cause it to vary from the NAV, including fund distributions, changes in supply and demand for the fund’s shares, changing market conditions, and investor perceptions of the fund or its investment manager.

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended July 31, 2023, the end of its most recent fiscal year. In accordance with regulatory requirements for closed-end funds, we also include performance information as of the most recent calendar quarter-end. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return, net asset value, and market price will fluctuate, and you may have a gain or a loss when you sell your shares.

Annualized fund performance Total return for periods ended 7/31/23

| | | | | |

| | Life of fund | | | | |

| | (since 2/29/88) | 10 years | 5 years | 3 years | 1 year |

| Net asset value | 5.75% | 2.10% | –0.07% | –0.17% | 0.39% |

| Market price | 5.87 | 3.31 | 0.54 | –0.95 | 2.08 |

Performance assumes reinvestment of distributions and does not account for taxes.

Performance includes the deduction of management fees and administrative expenses.

Comparative annualized index returns For periods ended 7/31/23

| | | | | |

| | Life of fund | | | | |

| | (since 2/29/88) | 10 years | 5 years | 3 years | 1 year |

| ICE BofA U.S. Treasury | | | | | |

| Bill Index | —* | 1.04% | 1.61% | 1.37% | 3.94% |

| Bloomberg Government | | | | | |

| Bond Index | 4.95% | 0.94 | 0.48 | –5.17 | –3.93 |

| Lipper General Bond | | | | | |

| Funds (closed-end) | | | | | |

| category median† | 6.97 | 4.53 | 3.24 | 3.57 | 6.35 |

Index and Lipper results should be compared with fund performance at net asset value. Lipper calculates performance differently than the closed-end funds it ranks, due to varying methods for determining a fund’s monthly reinvestment net asset value.

All Bloomberg indices are provided by Bloomberg Index Services Limited.

Lipper peer group median is provided by Lipper, a Refinitiv company.

* The fund’s primary benchmark, the ICE BofA U.S. Treasury Bill Index, was introduced on 6/30/92, which post-dates the inception of the fund.

† Over the 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 7/31/23, there were 65, 50, 40, 24, and 4 funds, respectively, in this Lipper category.

Past performance does not indicate future results.

Fund price and distribution information For the 12-month period ended 7/31/23

| | |

| Distributions | |

| Number | 12 |

| Income | $0.260756 |

| Capital gains | — |

| Return of capital* | 0.051244 |

| Total | $0.312000 |

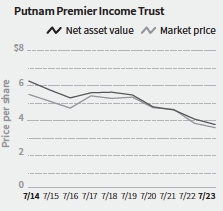

| Share value | NAV | Market price |

| 7/31/22 | $4.12 | $3.89 |

| 7/31/23 | 3.82 | 3.65 |

| Current dividend rate† | 8.17% | 8.55% |

The classification of distributions, if any, is an estimate. Final distribution information will appear on your year-end tax forms.

* See page 101.

† Most recent distribution, including any return of capital and excluding capital gains, annualized and divided by NAV or market price at period-end.

Annualized fund performance as of most recent calendar quarter

Total return for periods ended 6/30/23

| | | | | |

| | Life of fund | | | | |

| | (since 2/29/88) | 10 years | 5 years | 3 years | 1 year |

| Net asset value | 5.74% | 2.12% | –0.11% | –0.09% | 1.58% |

| Market price | 5.75 | 2.71 | –0.16 | –2.13 | 0.70 |

See the discussion following the fund performance table on page 9 for information about the calculation of fund performance.

Information about the fund’s goal, investment strategies, principal risks, and fundamental investment policies

Goal

The goal of the fund is to seek high current income consistent with the preservation of capital by allocating its investments among the U.S. government sector, high yield sector and international sector of the fixed-income securities market.

The fund’s main investment strategies and related risks

This section contains detail regarding the fund’s main investment strategies and the related risks you face as a fund shareholder. It is important to keep in mind that risk and reward generally go hand in hand; the higher the potential reward, the greater the risk.

We pursue the fund’s goal by investing mainly in assignments of and participations in fixed and floating rate bank loans, bonds, securitized debt instruments (such as residential mortgage-backed securities and commercial mortgage-backed securities), and other obligations of companies and governments worldwide that are either investment-grade or below-investment-grade in quality (sometimes referred to as “junk bonds”), that have intermediate- to long-term maturities (three years or longer), and that are from multiple sectors. The fund currently has significant investment exposure to residential and commercial mortgage-backed investments. We may consider, among other factors, credit, interest rate and prepayment risks, as well as general market conditions, when deciding whether to buy or sell investments. We typically use to a significant extent derivatives, such as futures, options, certain foreign currency transactions and swap contracts, for hedging and non-hedging purposes and to obtain leverage.

The fund currently has significant investment exposure to CMBS, which are also subject to risks associated with the commercial real estate markets and the servicing of mortgage loans secured by commercial properties. During periods of difficult economic conditions, delinquencies and losses on CMBS in particular generally increase, including as a result of the effects of those conditions on commercial real estate markets, the ability of commercial tenants to make loan payments, and the ability of a property to attract and retain commercial tenants. The fund achieves exposure to CMBS via CMBX, an index that references a basket of CMBS.

• Foreign investments. We consider any securities issued by a foreign government or a supranational organization (such as the World Bank) or denominated in a foreign currency to be securities of a foreign issuer. In addition, we consider an issuer to be a foreign issuer if we determine that (i) the issuer is headquartered or organized outside the United States, (ii) the issuer’s securities trade in a market outside the United States, (iii) the issuer derives a majority of its revenues or profits outside the United States, or (iv) the issuer is significantly exposed to the economic fortunes and risks of regions outside the United States. Foreign investments involve certain special risks, including:

— Unfavorable changes in currency exchange rates: Foreign investments are typically issued and traded in foreign currencies. As a result, their values may be affected by changes in exchange rates between foreign currencies and the U.S. dollar.

— Political and economic developments: Foreign investments may be subject to the risks of seizure by a foreign government, direct or indirect impact of sovereign debt default, imposition of economic sanctions, tariffs, trade restrictions, currency restrictions or similar actions (or retaliatory measures taken in response to such actions), and tax increases.

— Unreliable or untimely information: There may be less information publicly available about a foreign company than about most publicly-traded U.S. companies, and foreign companies are usually not subject to accounting, auditing and financial reporting standards and practices as stringent as those in the United States. Foreign securities may trade on markets that are closed when U.S. markets are open. As a result, accurate pricing information based on foreign market prices may not always be available.

— Limited legal recourse: Legal remedies for investors may be more limited than the remedies available in the United States.

— Limited markets: Certain foreign investments may be less liquid (harder to buy and sell) and more volatile than most U.S. investments, which means we may at times be unable to sell these foreign investments at desirable prices. In addition, there may be limited or no markets for bonds of issuers that become distressed. For the same reason, we

may at times find it difficult to value the fund’s foreign investments.

— Trading practices: Brokerage commissions and other fees are generally higher for foreign investments than for U.S. investments. The procedures and rules governing foreign transactions and custody may also involve delays in payment, delivery or recovery of money or investments.

— Sovereign issuers: The willingness and ability of sovereign issuers to pay principal and interest on government securities depends on various economic factors, including the issuer’s balance of payments, overall debt level, and cash flow from tax or other revenues. In addition, there may be no legal recourse for investors in the event of default by a sovereign government.

The risks of foreign investments are typically increased in countries with less developed markets, which are sometimes referred to as emerging markets. Emerging markets may have less developed economies and legal and regulatory systems and may be susceptible to greater political and economic instability than developed foreign markets. Countries with emerging markets are also more likely to experience high levels of inflation, or currency devaluation, and investments in emerging markets may be more volatile and less liquid than investments in developed markets. For these and other reasons, investments in emerging markets are often considered speculative.

Certain risks related to foreign investments may also apply to some extent to U.S.- traded investments that are denominated in foreign currencies, investments in U.S. companies that are traded in foreign markets, or investments in U.S. companies that have significant foreign operations.

• Interest rate risk. The values of bonds and other debt instruments usually rise and fall in response to changes in interest rates. Interest rates can change in response to the supply and demand for credit, government and/or central bank monetary policy and action, inflation rates, and other factors. Declining interest rates generally result in an increase in the value of existing debt instruments, and rising interest rates generally result in a decrease in the value of existing debt instruments. Changes in a debt instrument’s value usually will not affect the amount of interest income paid to the fund but will affect the value of the fund’s shares. Interest rate risk is generally greater for investments with longer maturities.

Some investments give the issuer the option to call or redeem an investment before its maturity date. If an issuer calls or redeems an investment during a time of declining interest rates, we might have to reinvest the proceeds in an investment offering a lower yield, and, therefore, the fund might not benefit from any increase in value as a result of declining interest rates.

• Credit risk. Investors normally expect to be compensated in proportion to the risk they are assuming. Thus, debt of issuers with poor credit prospects usually offers higher yields than debt of issuers with more secure credit. Higher-rated investments generally have lower credit risk.

Investments rated below BBB or its equivalent are below investment-grade in quality (sometimes referred to as “junk bonds”). This rating reflects a greater possibility that the issuers may be unable to make timely payments of interest and principal and thus default. If a default occurs, or is perceived as likely to occur, the value of the investment will usually be more volatile and could decrease. The value of a debt instrument may also be affected by changes in, or perceptions of, the financial condition of the issuer, borrower, counterparty, or other entity, or underlying collateral or assets, or changes in, or perceptions of, specific or general market, economic, industry, political, regulatory, geopolitical, environmental, public health, and other conditions. A default or expected default could also make it difficult for us to sell the investment at a price approximating the value we had previously placed on it. Lower-rated debt usually has a more limited market than higher-rated debt, which may at times make it difficult for us to buy or sell certain debt instruments or to establish their fair values. Credit risk is generally greater for zero-coupon bonds and other investments that are issued at less than their face value and that are required to make interest payments only at maturity rather than at intervals during the life of the investment.

Credit ratings are based largely on the issuer’s historical financial condition and the rating agencies’ investment analysis at the time of rating. The rating assigned to any particular investment does not necessarily reflect the issuer’s current financial condition and does not reflect an assessment of the investment’s volatility or liquidity. Although we consider credit ratings in making investment decisions, we perform our own investment analysis and do not rely only on ratings assigned by the rating agencies. Our success in achieving the fund’s goal may depend more on our own credit analysis when we buy lower-rated debt than when we buy investment-grade debt. We may have to participate in legal proceedings involving

the issuer. This could increase the fund’s operating expenses and decrease its net asset value.

Although investment-grade investments generally have lower credit risk, they may share some of the risks of lower-rated investments. U.S. government investments generally have the least credit risk but are not completely free of credit risk. While some investments, such as U.S. Treasury obligations and Ginnie Mae certificates, are backed by the full faith and credit of the U.S. government, others are backed only by the credit of the issuer. Mortgage-backed securities may be subject to the risk that underlying borrowers will be unable to meet their obligations.

Bond investments may be more susceptible to downgrades or defaults during economic downturns or other periods of economic stress, which can significantly strain the financial resources of debt issuers, including the issuers of the bonds in which the fund invests (or has exposure to). This may make it less likely that those issuers can meet their financial obligations when due and may adversely impact the value of their bonds, which could negatively impact the performance of the fund. It is difficult to predict the level of financial stress and duration of such stress issuers may experience.

• Prepayment risk. Traditional debt investments typically pay a fixed rate of interest until maturity, when the entire principal amount is due. In contrast, payments on securitized debt instruments, including mortgage-backed and asset-backed investments, typically include both interest and partial payment of principal. Principal may also be prepaid voluntarily or as a result of refinancing or foreclosure. We may have to invest the proceeds from prepaid investments in other investments with less attractive terms and yields.

Compared to debt that cannot be prepaid, mortgage-backed investments are less likely to increase in value during periods of declining interest rates and have a higher risk of decline in value during periods of rising interest rates. These investments may increase the volatility of the fund. Some mortgage-backed investments receive only the interest portion or the principal portion of payments on the underlying mortgages. The yields and values of these investments are extremely sensitive to changes in interest rates and in the rate of principal payments on the underlying mortgages. The market for these investments may be volatile and limited, which may make them difficult to buy or sell. Asset-backed securities are structured like mortgage-backed securities, but instead of mortgage loans or interests in mortgage loans, the underlying assets may include such items as motor vehicle installment sales or installment loan contracts, leases of various types of real and personal property and receivables from credit card agreements. Asset-backed securities are subject to risks similar to those of mortgage-backed securities.

• Derivatives. We may engage to a significant extent in a variety of transactions involving derivatives, such as to-be-announced (TBA) commitments, futures, options and swaptions on mortgage-backed securities and indices, forward contracts, certain foreign currency transactions, credit default, total return and interest rate swap contracts, including to obtain or adjust exposure to commercial and residential mortgage-backed instruments.

Derivatives are financial instruments whose value depends upon, or is derived from, the value of something else, such as one or more underlying investments, pools of investments, indexes or currencies. We may make use of “short” derivatives positions, the values of which typically move in the opposite direction from the price of the underlying investment, pool of investments, index or currency. We may use derivatives for hedging and non-hedging purposes and to obtain leverage. For example, we may use derivatives to increase or decrease the fund’s exposure to long- or short-term interest rates (in the United States or abroad), increase or decrease the fund’s exposure to inflation, adjust the term of the fund’s U.S. Treasury security exposure, adjust the fund’s positioning on the yield curve (a line that plots interest rates of bonds having equal credit quality but differing maturity dates) or to take tactical positions along the yield curve or to a particular currency or group of currencies, or as a substitute for a direct investment in the securities of one or more issuers. The fund may also use derivatives to isolate prepayment risk associated with the fund’s holdings of collateralized mortgage obligations. However, we may also choose not to use derivatives based on our evaluation of market conditions or the availability of suitable derivatives. Investments in derivatives may be applied toward meeting a requirement to invest in a particular kind of investment if the derivatives have economic characteristics similar to that investment.

Derivatives involve special risks and may result in losses. The successful use of derivatives depends on our ability to manage these sophisticated instruments. Some derivatives are “leveraged,”

which means they provide the fund with investment exposure greater than the value of the fund’s investment in the derivatives. As a result, these derivatives may magnify or otherwise increase investment losses to the fund. The risk of loss from certain short derivatives positions is theoretically unlimited. The value of derivatives may move in unexpected ways due to unanticipated market movements, the use of leverage, imperfect correlation between the derivative instrument and the reference asset or other factors, especially in unusual market conditions, and volatility in the value of derivatives could adversely impact the fund’s returns, obligations, and exposures.

Other risks arise from the potential inability to terminate or sell derivatives positions. Derivatives may be subject the fund to liquidity risk due to the fund’s obligation to make payments of margin, collateral, or settlement payments to counterparties. A liquid secondary market may not always exist for the fund’s derivative positions. In fact, certain over-the-counter instruments (investments not traded on an exchange) may not be liquid. Over-the-counter instruments also involve the risk that the other party to the derivative transaction may not be willing or able to meet its obligations with respect to the derivative transaction. The risk of a party failing to meet its obligations may increase if the fund has significant exposure to that counterparty. Derivative transactions may also be subject to operational risk, including due to documentation and settlement issues, system failures, inadequate controls and human error, and legal risk due to insufficient documentation, insufficient capacity or authority of a counterparty, or issues with respect to the legality or enforceability of the derivative contract.

• Floating rate loans. Floating rate loans are debt obligations with interest rates that adjust or “float” periodically (normally on a monthly or quarterly basis) based on a generally recognized base rate, such as the London Inter-Bank Offered Rate or the prime rate offered by one or more major U.S. banks. While most floating rate loans are below-investment-grade in quality, many also are senior in rank in the event of bankruptcy to most other securities of the borrower, such as common stock or public bonds. Floating rate loans are also normally secured by specific collateral or assets of the borrower so that the holders of the loans will have a priority claim on those assets in the event of default or bankruptcy of the issuer.

Floating rate loans generally are less sensitive to interest rate changes than obligations with fixed interest rates but may decline in value if their interest rates do not rise as much, or as quickly, as interest rates in general. Conversely, floating rate instruments will not generally increase in value if interest rates decline. Changes in interest rates will also affect the amount of interest income the fund earns on its floating rate investments. Most floating rate loans allow for prepayment of principal without penalty. If a borrower prepays a loan, we might have to reinvest the proceeds in an investment that may have lower yields than the yield on the prepaid loan or might not be able to take advantage of potential gains from increases in the credit quality of the issuer.

The value of collateral, if any, securing a floating rate loan can decline, and may be insufficient to meet the borrower’s obligations or difficult to liquidate. In addition, the fund’s access to collateral may be limited by bankruptcy or other insolvency proceedings. Floating rate loans may not be fully collateralized and may decline in value. Loans may not be considered “securities,” and it is possible that the fund may not be entitled to rely on anti-fraud and other protections under the federal securities laws when it purchases loans.

Although the market for the types of floating rate loans in which the fund invests has become increasingly liquid over time, this market is still developing, and there can be no assurance that adverse developments with respect to this market or particular borrowers will not prevent the fund from selling these loans at their market values when we consider such a sale desirable. In addition, the settlement period (the period between the execution of the trade and the delivery of cash to the purchaser) for floating rate loan transactions may be significantly longer than the settlement period for other investments, and in some cases longer than seven days. Requirements to obtain consent of borrower and/or agent can delay or impede the fund’s ability to sell the floating rate loans and can adversely affect the price that can be obtained. It is possible that sale proceeds from floating rate loan transactions will not be available to meet redemption obligations.

• Liquidity and illiquid investments. We may invest the fund’s assets in illiquid investments, which may be considered speculative, and which may be difficult to sell. The sale of many of these investments is prohibited or limited by law or contract. Some investments may be difficult to value for purposes of determining the fund’s net asset value. Certain other investments may not have an active trading market due to adverse market, economic, industry, political, regulatory, geopolitical, environmental, public health, and other conditions, including

investors trying to sell large quantities of a particular investment or type of investment, or lack of market makers or other buyers for a particular investment or type of investment. Commercial mortgage-backed securities may be less liquid and exhibit greater price volatility than other types of mortgage- or asset-backed securities. We may not be able to sell the fund’s illiquid investments when we consider it desirable to do so, or we may be able to sell them only at less than their value.

• Focused investment risk. Focusing investments in sectors and industries with high positive correlations to one another creates additional risk. The fund currently has significant investment exposure to private issuers of residential and commercial mortgage-backed securities and mortgage-backed securities issued or guaranteed by the U.S. government or its agencies or instrumentalities, which makes the fund’s net asset value more susceptible to economic, market, political and other developments affecting the residential and commercial real estate markets and the servicing of mortgage loans secured by real estate properties. Factors affecting the residential and commercial real estate markets include the supply and demand of real property in particular markets, changes in the availability, terms and costs of mortgages, changes in tenants’ ability to make loan payments, changes in zoning laws and eminent domain practices, the impact of environmental laws, delays in completion of construction, changes in real estate values, changes in property taxes, levels of occupancy, adequacy of rent to cover operating expenses, changes in government regulations, and local and regional market conditions. Some of these factors may vary greatly by geographic location. The value of these investments also may be affected by changes in interest rates and social and economic trends. Mortgage-backed securities are subject to the risk of fluctuations in income from underlying real estate assets, prepayments, extensions, and defaults by borrowers.

Because the fund currently has significant investment exposure to commercial mortgage-backed securities, the fund may be particularly susceptible to adverse developments affecting those securities. Commercial mortgage-backed securities include securities that reflect an interest in, or are secured by, mortgage loans on commercial real property, such as industrial and warehouse properties, office buildings, retail space and shopping malls, cooperative apartments, hotels and motels, nursing homes, hospitals and senior living centers. Many of the risks of investing in commercial mortgage-backed securities reflect the risks of investing in the real estate securing the underlying mortgage loans. During periods of difficult economic conditions (including periods of significant disruptions to business operations, supply chains, and customer activity and lower consumer demand for goods and services), delinquencies and losses on commercial real estate generally increase, including as a result of the effects of those conditions on commercial real estate markets, the ability of commercial tenants to make loan payments, and the ability of a property to attract and retain commercial tenants. The risk of defaults on residential mortgage-backed securities is generally higher in the case of mortgage-backed investments that include non-qualified mortgages. Litigation with respect to the representations and warranties given in connection with the issuance of mortgage-backed securities can be an important consideration in investing in such securities, and the outcome of any such litigation could significantly impact the value of the fund’s mortgage-backed investments.

• Market risk. The value of investments in the fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons, including general economic, political or financial market conditions; investor sentiment and market perceptions (including perceptions about monetary policy, interest rates, inflation or the risk of default); government actions (including protectionist measures, intervention in the financial markets or other regulation, and changes in fiscal, monetary or tax policies); geopolitical events or changes (including natural disasters, terrorism and war); outbreaks of infectious illnesses or other widespread public health issues (including epidemics and pandemics); and factors related to a specific issuer, asset class, geography, industry or sector. Foreign financial markets have their own market risks, and they may be more or less volatile than U.S. markets and may move in different directions. During a general downturn in financial markets, multiple asset classes may decline in value simultaneously. These and other factors may lead to increased volatility and reduced liquidity in the fund’s portfolio holdings. These risks may be exacerbated during economic downturns or other periods of economic stress.

The Covid-19 pandemic and efforts to contain its spread have resulted in, among other effects, significant market volatility, exchange trading suspensions and closures, declines in global financial markets, higher default rates, significant changes in fiscal and monetary policies, and economic downturns and

recessions. The effects of the Covid-19 pandemic have negatively affected, and may continue to negatively affect, the global economy, the economies of the United States and other individual countries, the financial performance of individual issuers, sectors, industries, asset classes, and markets, and the value, volatility, and liquidity of particular securities and other assets. The effects of the Covid-19 pandemic also are likely to exacerbate other risks that apply to the fund, which could negatively impact the fund’s performance and lead to losses on your investment in the fund. The duration of the Covid-19 pandemic and its effects cannot be determined with certainty.

• ESG considerations. Although ESG considerations do not represent a primary focus of the fund, we expect to integrate environmental, social, or governance (“ESG”) considerations into our fundamental research process and investment decision-making for the fund, where we consider them material and relevant, and where data is available. We believe that ESG considerations, like other, more traditional subjects of investment analysis such as credit, interest rate, prepayment and liquidity risks, as well as general market conditions, have the potential to impact financial risk and investment returns. We believe that ESG considerations are best analyzed in combination with traditional fundamental considerations, including a company’s industry, geography, and strategic position or the fundamentals of a securitized product and its underlying assets. With respect to securitized products, we may evaluate ESG considerations related to the originator, servicers and other relevant parties. We also consider ESG factors when evaluating sovereign debt, including both current ESG metrics and goals and progress by the sovereign issuer with respect to ESG considerations. When considering ESG factors for all asset classes, we use company or issuer disclosures, public data sources, and independent third-party data (where available) as inputs into our analytical processes. With respect to certain fund holdings, such as holdings of securitized investments, data on material ESG considerations may be limited. Because fixed income investments generally represent a promise to pay principal and interest by an issuer, and not an ownership interest, and may involve complex structures, ESG-related investment considerations may have a more limited impact on risk and return (or may have an impact over a different investment time horizon) relative to other asset classes, and this may be particularly true for shorter-term investments. The consideration of ESG factors as part of the fund’s investment process does not mean that the fund pursues a specific “ESG” or “sustainable” investment strategy, and we may make investment decisions for the fund other than on the basis of relevant ESG considerations.

• Management and operational risk. The fund is actively managed, and its performance will reflect, in part, our ability to make investment decisions that seek to achieve the fund’s investment objective. There is no guarantee that the investment techniques, analyses, or judgments that we apply in making investment decisions for the fund will produce the intended outcome or that the investments we select for the fund will perform as well as other securities that were not selected for the fund. As a result, the fund may underperform its benchmark or other funds with a similar investment goal and may realize losses. In addition, we, or the fund’s other service providers, may experience disruptions or operating errors that could negatively impact the fund. Although service providers may have operational risk management policies and procedures and take appropriate precautions to avoid and mitigate risks that could lead to disruptions and operating errors, it may not be possible to identify all of the operational risks that may affect the fund or to develop processes and controls to completely eliminate or mitigate their occurrence or effects.

• Other investments. In addition to the main investment strategies described above, the fund may make other types of investments, such as investments in asset-backed, hybrid and structured bonds and notes, preferred securities that would be characterized as debt securities under applicable accounting standards and tax laws, and assignments of and participations in fixed and floating rate loans. The fund may also invest in cash or cash equivalents, including money market instruments or short-term instruments such as commercial paper, bank obligations (e.g., certificates of deposit and bankers’ acceptances), repurchase agreements, and U.S. Treasury bills or other government obligations. The fund may also from time to time invest all or a portion of its cash balances in money market and/or short-term bond funds advised by Putnam Management or its affiliates. The percentage of the fund invested in cash and cash equivalents and such money market and short-term bond funds is expected to vary over time and will depend on various factors, including market conditions, purchase and redemption activity by fund shareholders, and our assessment of the cash level that is appropriate to allow the fund to pursue investment opportunities as they arise. Large cash positions

may dampen performance and may prevent the fund from achieving its goal. The fund may also loan portfolio securities to earn income.

• Temporary defensive strategies. In response to adverse market, economic, political or other conditions, we may take temporary defensive positions, such as investing some or all of the fund’s assets in cash and cash equivalents, that differ from the fund’s usual investment strategies. However, we may choose not to use these temporary defensive strategies for a variety of reasons, even in very volatile market conditions. If we do employ these strategies, the fund may miss out on investment opportunities, and may not achieve its goal. Additionally, while temporary defensive strategies are mainly designed to limit losses, they may not work as intended.

• Changes in policies. The Trustees may change the fund’s goal, investment strategies and other policies without shareholder approval, except in circumstances in which shareholder approval is specifically required by law (such as changes to fundamental investment policies) or where a shareholder approval requirement was specifically disclosed in the fund’s prospectus, statement of additional information or shareholder report and is otherwise still in effect.

The fund’s fundamental investment policies

The fund has adopted the following investment restrictions which may not be changed without the affirmative vote of a “majority of the outstanding voting securities” of the fund (which is defined in the Investment Company Act of 1940, as amended, (the “1940 Act”) to mean the affirmative vote of the lesser of (1) more than 50% of the outstanding shares of the fund, or (2) 67% or more of the shares present at a meeting if more than 50% of the outstanding shares of the fund are represented at the meeting in person or by proxy). The fund may not:

1. Borrow money or issue senior securities (as defined in the 1940 Act), except as permitted by (i) the 1940 Act, (ii) the rules or regulations promulgated by the Securities and Exchange Commission under the 1940 Act or (iii) any applicable exemption from the provisions of the 1940 Act.

2. Underwrite securities issued by other persons except to the extent that, in connection with the disposition of its portfolio investments, it may be deemed to be an underwriter under the federal securities laws.

3. Purchase or sell real estate, although it may purchase securities of issuers which deal in real estate, securities which are secured by interests in real estate, and securities representing interests in real estate, and it may acquire and dispose of real estate or interests in real estate acquired through the exercise of its rights as a holder of debt obligations secured by real estate or interests therein.

4. Purchase or sell commodities or commodity contracts, except that the fund may purchase and sell financial futures contracts and options and may enter into foreign exchange contracts and other financial transactions not involving physical commodities.

5. Make loans, except by purchase of debt obligations in which the fund may invest consistent with its investment policies (including without limitation debt obligations issued by other Putnam funds), by entering into repurchase agreements or by lending its portfolio securities.

6. With respect to 50% of its total assets, invest in securities of any issuer if, immediately after such investment, more than 5% of the total assets of the fund (taken at current value) would be invested in the securities of such issuer; provided that this limitation does not apply to obligations issued or guaranteed as to interest or principal by the U.S. Government or its agencies or instrumentalities.

7. With respect to 50% of its total assets, acquire more than 10% of the outstanding voting securities of any issuer.

8. Invest more than 25% of the value of its total assets in any one industry. (Securities of the U.S. Government, its agencies or instrumentalities, or of any foreign government, its agencies or instrumentalities, securities of supranational entities, and securities backed by the credit of a governmental entity are not considered to represent industries.)

Comparative index definitions

Bloomberg Government Bond Index is an unmanaged index of U.S. Treasury and government agency bonds.

Bloomberg U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed income securities.

CMBX Index is an unmanaged index that tracks the performance of a basket of commercial mortgage-backed securities issued in a particular year.

ICE BofA (Intercontinental Exchange Bank of America) U.S. Treasury Bill Index is an unmanaged index that tracks the performance of U.S. dollar-denominated U.S. Treasury bills publicly issued in the U.S. domestic market. Qualifying securities must have a remaining term of at least one month to final maturity and a minimum amount outstanding of $1 billion.

JPMorgan Developed High Yield Index is an unmanaged index of high-yield fixed income securities issued in developed countries.

S&P 500® Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approve or endorse this material, or guarantee the accuracy or completeness of any information herein, or make any warranty, express or implied, as to the results to be obtained therefrom, and to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

ICE Data Indices, LLC (“ICE BofA”), used with permission. ICE BofA permits use of the ICE BofA indices and related data on an “as is” basis; makes no warranties regarding same; does not guarantee the suitability, quality, accuracy, timeliness, and/or completeness of the ICE BofA indices or any data included in, related to, or derived therefrom; assumes no liability in connection with the use of the foregoing; and does not sponsor, endorse, or recommend Putnam Investments, or any of its products or services.

Lipper, a Refinitiv company, is a third-party industry-ranking entity that ranks funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category medians reflect performance trends for funds within a category.

Other information for shareholders

Important notice regarding share repurchase program

In September 2022, the Trustees of your fund approved the renewal of a share repurchase program that had been in effect since 2005. This renewal allows your fund to repurchase, in the 365 days beginning October 1, 2022, up to 10% of the fund’s common shares outstanding as of September 30, 2022.

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single notice of internet availability, or a single printed copy, of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2023, are available in the Individual Investors section of putnam.com and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT within 60 days of the end of such fiscal quarter. Shareholders may obtain the fund’s Form N-PORT on the SEC’s website at www.sec.gov.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam funds. As of July 31, 2023, Putnam employees had approximately $504,000,000 and the Trustees had approximately $70,000,000 invested in Putnam funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

Important notice regarding Putnam’s privacy policy

In order to conduct business with our shareholders, we must obtain certain personal information such as account holders’ names, addresses, Social Security numbers, and dates of birth. Using this information, we are able to maintain accurate records of accounts and transactions.

It is our policy to protect the confidentiality of our shareholder information, whether or not a shareholder currently owns shares of our funds. In particular, it is our policy not to sell information about you or your accounts to outside marketing firms. We have safeguards in place designed to prevent unauthorized access to our computer systems and procedures to protect personal information from unauthorized use.

Under certain circumstances, we must share account information with outside vendors who provide services to us, such as mailings and proxy solicitations. In these cases, the service providers enter into confidentiality agreements with us, and we provide only the information necessary to process transactions and perform other services related to your account. Finally, it is our policy to share account information with your financial representative, if you’ve listed one on your Putnam account.

Summary of Putnam closed-end funds’ amended and restated dividend reinvestment plans

Putnam Managed Municipal Income Trust, Putnam Master Intermediate Income Trust, Putnam Municipal Opportunities Trust and Putnam Premier Income Trust (each, a “Fund” and collectively, the “Funds”) each offer a dividend reinvestment plan (each, a “Plan” and collectively, the “Plans”). If you participate in a Plan, all income dividends and capital gain distributions are automatically reinvested in Fund shares by the Fund’s agent, Putnam Investor Services, Inc. (the “Agent”). If you are not participating in a Plan, every month you will receive all dividends and other distributions in cash, paid by check and mailed directly to you or your intermediary.

Upon a purchase (or, where applicable, upon registration of transfer on the shareholder records of a Fund) of shares of a Fund by a registered shareholder, each such shareholder will be deemed to have elected to participate in that Fund’s Plan. Each such shareholder will have all distributions by a Fund automatically reinvested in additional shares, unless such shareholder elects to terminate participation in a Plan by instructing the Agent to pay future distributions in cash. Shareholders who were not participants in a Plan as of January 31, 2010, will continue to receive distributions in cash but may enroll in a Plan at any time by contacting the Agent.

If you participate in a Fund’s Plan, the Agent will automatically reinvest subsequent distributions, and the Agent will send you a confirmation in the mail telling you how many additional shares were issued to your account.

To change your enrollment status or to request additional information about the Plans, you may contact the Agent either in writing, at P.O. Box 8383, Boston, MA 02266-8383, or by telephone at 1-800-225-1581 during normal East Coast business hours.

How you acquire additional shares through a Plan If the market price per share for your Fund’s shares (plus estimated brokerage commissions) is greater than or equal to their net asset value per share on the payment date for a distribution, you will be issued shares of the Fund at a value equal to the higher of the net asset value per share on that date or 95% of the market price per share on that date.

If the market price per share for your Fund’s shares (plus estimated brokerage commissions) is less than their net asset value per share on the payment date for a distribution, the Agent will buy Fund shares for participating accounts in the open market. The Agent will aggregate open-market purchases on behalf of all participants, and the average price (including brokerage commissions) of all shares purchased by the Agent will be the price per share allocable to each participant. The Agent will generally complete these open-market purchases within five business days following the payment date. If, before the Agent has completed open-market purchases, the market price per share (plus estimated brokerage commissions) rises to exceed the net asset value per share on the payment date, then the purchase price may exceed the net asset value per share, potentially resulting in the acquisition of fewer shares than if the distribution had been paid in newly issued shares.

How to withdraw from a Plan Participants may withdraw from a Fund’s Plan at any time by notifying the Agent, either in writing or by telephone. Such withdrawal will be effective immediately if notice is received by the Agent with sufficient time prior to any distribution record date; otherwise, such withdrawal will be effective with respect to any subsequent distribution following notice of withdrawal. There is no penalty for withdrawing from or not participating in a Plan.

Plan administration The Agent will credit all shares acquired for a participant under a Plan to the account in which the participant’s common shares are held. Each participant will

be sent reasonably promptly a confirmation by the Agent of each acquisition made for his or her account.

About brokerage fees Each participant pays a proportionate share of any brokerage commissions incurred if the Agent purchases additional shares on the open market, in accordance with the Plans. There are no brokerage charges applied to shares issued directly by the Funds under the Plans.

About taxes and Plan amendments Reinvesting dividend and capital gain distributions in shares of the Funds does not relieve you of tax obligations, which are the same as if you had received cash distributions. The Agent supplies tax information to you and to the IRS annually. Each Fund reserves the right to amend or terminate its Plan upon 30 days’ written notice. However, the Agent may assign its rights, and delegate its duties, to a successor agent with the prior consent of a Fund and without prior notice to Plan participants.

If your shares are held in a broker or nominee name If your shares are held in the name of a broker or nominee offering a dividend reinvestment service, consult your broker or nominee to ensure that an appropriate election is made on your behalf. If the broker or nominee holding your shares does not provide a reinvestment service, you may need to register your shares in your own name in order to participate in a Plan.

In the case of record shareholders such as banks, brokers or nominees that hold shares for others who are the beneficial owners of such shares, the Agent will administer the Plan on the basis of the number of shares certified by the record shareholder as representing the total amount registered in such shareholder’s name and held for the account of beneficial owners who are to participate in the Plan.

Trustee approval of management contracts

Consideration of your fund’s new and interim management and sub-management contracts

At their meeting on June 23, 2023, the Board of Trustees of your fund, including all of the Trustees who are not “interested persons” (as this term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”)) of the Putnam mutual funds, closed-end funds and exchange-traded funds (collectively, the “funds”) (the “Independent Trustees”) approved, subject to approval by your fund’s shareholders, a new management contract with Putnam Investment Management (“Putnam Management”) and a new sub-management contract between Putnam Management and its affiliate, Putnam Investments Limited (“PIL”) (collectively, the “New Management Contracts”). The Trustees considered the proposed New Management Contracts in connection with the planned acquisition of Putnam U.S. Holdings I, LLC (“Putnam Holdings”) by a subsidiary of Franklin Resources, Inc. (“Franklin Templeton”). The Trustees considered that, on May 31, 2023, Franklin Templeton and Great-West Lifeco Inc., the parent company of Putnam Holdings, announced that they had entered into a definitive agreement for a subsidiary of Franklin Templeton to acquire Putnam Holdings in a stock and cash transaction (the “Transaction”). The Trustees noted that Putnam Holdings was the parent company of Putnam Management and PIL. The Trustees were advised that the Transaction would result in a “change of control” of Putnam Management and PIL and would cause your fund’s current Management Contract with Putnam Management and Sub-Management Contract with PIL (collectively, the “Current Management Contracts”) to terminate in accordance with the 1940 Act. The Trustees considered that the New Management Contracts would take effect upon the closing of the Transaction, which was expected to occur in the fourth quarter of 2023.

In addition to the New Management Contracts, the Trustees also approved interim management and sub-management contracts with Putnam Management and PIL, respectively (the “Interim Management Contracts”), which would take effect in the event that for any reason shareholder approval of a New Management Contract was not received by the time of the Transaction closing. The Trustees considered that each Interim Management Contract that became effective would remain in effect until shareholders approved the proposed New Management Contract, or until 150 days elapse after the closing of the Transaction, whichever occurred first. The considerations and conclusions discussed in connection with the Trustees’ consideration of the New Management Contracts and the continuance of your fund’s Current Management Contracts also apply to the Trustees’ consideration of the Interim Management Contracts, supplemented by consideration of the terms, nature and reason for any Interim Management Contract.

The Independent Trustees met with their independent legal counsel, as defined in Rule 0 – 1(a)(6) under the 1940 Act (their “independent legal counsel”), and representatives of Putnam Management and its parent company, Power Corporation of Canada, to discuss the potential Transaction, including the timing and structure of the Transaction and its implications for Putnam Management and the funds, during their regular meeting on November 18, 2022, and the full Board of Trustees further discussed these matters with representatives of Putnam Management at its regular meeting on December 15, 2022. At a special meeting on December 20, 2022, the full Board of Trustees met with representatives of Putnam Management, Power Corporation of Canada and Franklin Templeton to further discuss the potential Transaction, including Franklin Templeton’s strategic plans for Putnam Management’s asset management business and the funds, potential sources of synergy between Franklin Templeton and Putnam Management, potential areas of partnership between Power Corporation of Canada and Franklin Templeton, Franklin Templeton’s distribution capabilities, Franklin Templeton’s existing service provider relationships and Franklin Templeton’s recent acquisitions of other asset management firms.

In order to assist the Independent Trustees in their consideration of the New Management Contracts and other anticipated impacts of the Transaction on the funds and their shareholders, independent legal counsel for the Independent Trustees furnished an initial information request to Franklin Templeton (the “Initial Franklin Request”). At a special meeting of the full Board of Trustees held on January 25, 2023, representatives of Franklin Templeton addressed the firm’s responses to the

Initial Franklin Request. At the meeting, representatives of Franklin Templeton discussed, among other things, the business and financial condition of Franklin Templeton and its affiliates, Franklin Templeton’s U.S. registered fund operations, its recent acquisition history, Franklin Templeton’s intentions regarding the operation of Putnam Management and the funds following the completion of the potential Transaction and expected benefits to the funds and Putnam Management that might result from the Transaction.

The Board of Trustees actively monitored developments with respect to the potential Transaction throughout the period leading up to the public announcement of a final sale agreement on May 31, 2023. The Independent Trustees met to discuss these matters at their regular meetings on January 27, April 20 and May 19, 2023. The full Board of Trustees also discussed developments at their regular meeting on February 23, 2023. Following the public announcement of the Transaction on May 31, 2023, independent legal counsel for the Independent Trustees furnished a supplemental information request (the “Supplemental Franklin Request”) to Franklin Templeton. At the Board of Trustees’ regular in-person meeting held on June 22–23, 2023, representatives of Putnam Management and Power Corporation of Canada provided further information regarding, among other matters, the final terms of the Transaction and efforts undertaken to retain Putnam employees. The Contract Committee of the Board of Trustees also met on June 22, 2023 to discuss Franklin Templeton’s responses to the Supplemental Franklin Request. Mr. Reynolds, the only Trustee affiliated with Putnam Management, participated in portions of these meetings to provide the perspective of the Putnam organization, but did not otherwise participate in the deliberations of the Independent Trustees or the Contract Committee regarding the potential Transaction.

After the presentations and after reviewing the written materials provided, the Independent Trustees met at their in-person meeting on June 23, 2023 to consider the New Management Contracts for each fund, proposed to become effective upon the closing of the Transaction, and the filing of a preliminary proxy statement. At this meeting and throughout the process, the Independent Trustees also received advice from their independent legal counsel regarding their responsibilities in evaluating the potential Transaction and the New Management Contracts. The Independent Trustees reviewed the terms of the proposed New Management Contracts and the differences between the New Management Contracts and the Current Management Contracts. They noted that the terms of the proposed New Management Contracts were identical to the Current Management Contracts, except for the effective dates and initial terms.

In considering the approval of the proposed New Management Contracts, the Board of Trustees took into account a number of factors, including:1

(i) Franklin Templeton’s and Putnam Management’s belief that the Transaction would not adversely affect the funds or their shareholders and their belief that the Transaction was likely to result in certain benefits (described below) for the funds and their shareholders;

(ii) That Franklin Templeton did not intend to make any material change in Putnam Management’s senior investment professionals (other than certain changes related to reporting structure and organization of personnel discussed below), including the portfolio managers of the funds, or to the firm’s operating locations as a result of the Transaction;

(iii) That Franklin Templeton intended for Putnam Management’s equity investment professionals to continue to operate largely independently from Franklin Templeton, reporting to Franklin Templeton’s Head of Public Markets following the Transaction;

(iv) That, while Putnam Management’s organizational structure was not expected to change immediately following the Transaction, Franklin Templeton intended to revise Putnam Management’s reporting structure in order to include Putnam Management’s fixed income investment professionals in Franklin Templeton’s fixed income group and to include Putnam Management’s Global Asset Allocation (“GAA”) investment professionals in Franklin Templeton’s investment solutions group, with both Franklin Templeton groups reporting to Franklin Templeton’s Head of Public Markets;

1All subsequent references to Putnam Management describing the Board of Trustees’ considerations should be deemed to include references to PIL as necessary or appropriate in the context.

(v) Franklin Templeton’s expectation that there would not be any changes in the investment objectives, strategies or portfolio holdings of the funds as a result of the Transaction;

(vi) That neither Franklin Templeton nor Putnam Management had any current plans to propose changes to the funds’ existing management fees or expense limitations;

(vii) Franklin Templeton’s and Putnam Management’s representations that, following the Transaction, there was not expected to be any diminution in the nature, quality and extent of services provided to the funds and their shareholders by Putnam Management and PIL, including compliance and other non-advisory services;

(viii) That Franklin Templeton did not currently plan to change the branding of the funds or to change the lineup of funds in connection with the Transaction but would continue to evaluate how best to position the funds in the market;

(ix) The possible benefits accruing to the funds and their shareholders as a result of the Transaction, including:

a. That the scale of Franklin Templeton’s investment operations platform would increase the investment and operational resources available to the funds;

b. That the Putnam open-end funds would benefit from Franklin Templeton’s large retail and institutional global distribution capabilities and significant network of intermediary relationships, which may provide additional opportunities for the funds to increase assets and reduce expenses by spreading expenses over a larger asset base; and