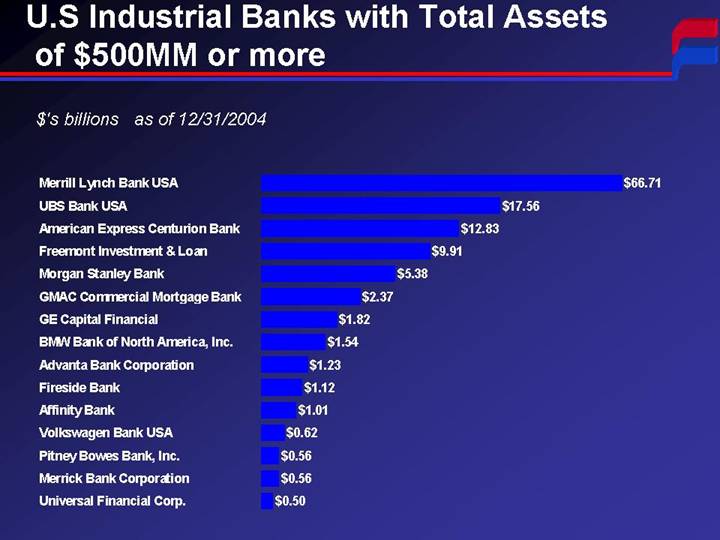

Searchable text section of graphics shown above

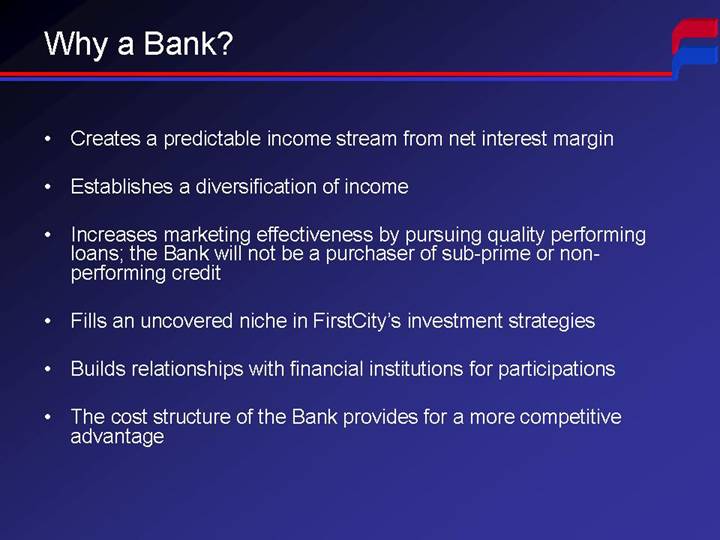

Why a Bank?

• Creates a predictable income stream from net interest margin

• Establishes a diversification of income

• Increases marketing effectiveness by pursuing quality performing loans; the Bank will not be a purchaser of sub-prime or non-performing credit

• Fills an uncovered niche in FirstCity’s investment strategies

• Builds relationships with financial institutions for participations

• The cost structure of the Bank provides for a more competitive advantage

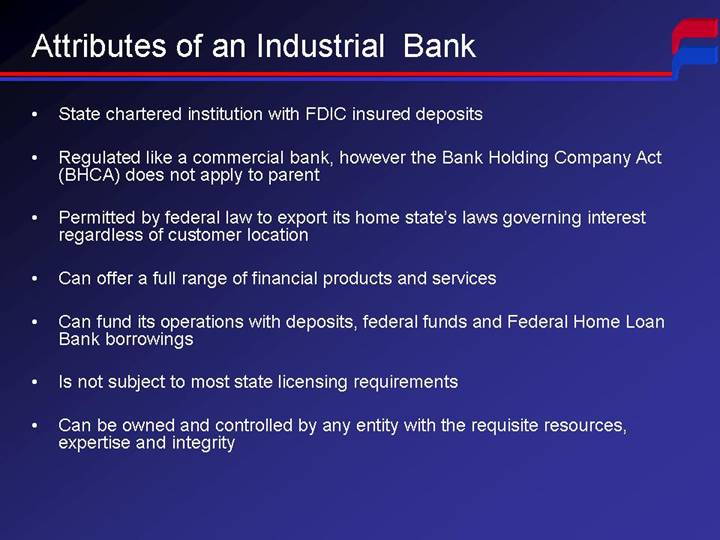

Attributes of an Industrial Bank

• State chartered institution with FDIC insured deposits

• Regulated like a commercial bank, however the Bank Holding Company Act (BHCA) does not apply to parent

• Permitted by federal law to export its home state’s laws governing interest regardless of customer location

• Can offer a full range of financial products and services

• Can fund its operations with deposits, federal funds and Federal Home Loan Bank borrowings

• Is not subject to most state licensing requirements

• Can be owned and controlled by any entity with the requisite resources, expertise and integrity

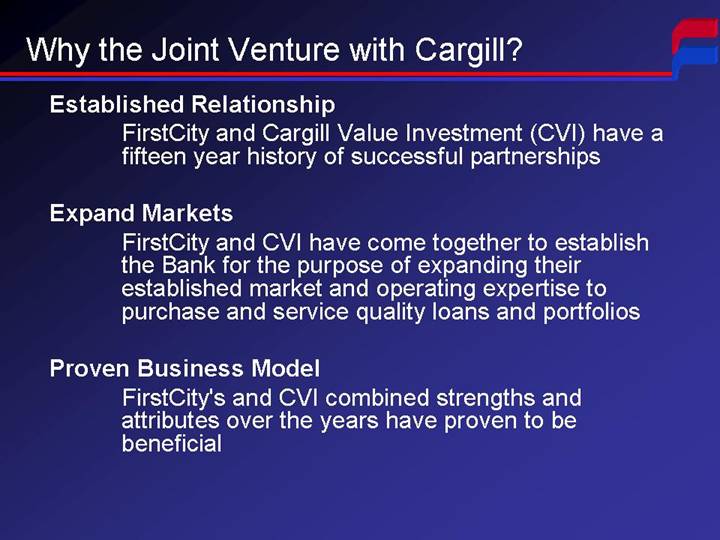

Why the Joint Venture with Cargill?

Established Relationship

FirstCity and Cargill Value Investment (CVI) have a fifteen year history of successful partnerships

Expand Markets

FirstCity and CVI have come together to establish the Bank for the purpose of expanding their established market and operating expertise to purchase and service quality loans and portfolios

Proven Business Model

FirstCity’s and CVI combined strengths and attributes over the years have proven to be beneficial

American Pioneer Bank Business Model

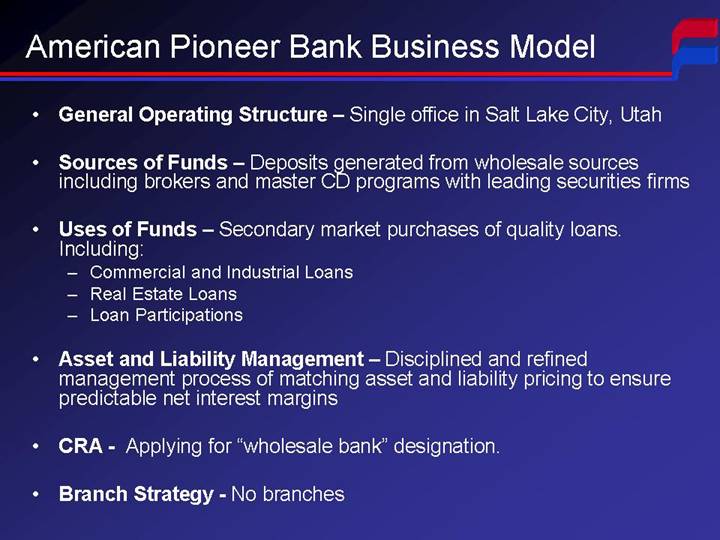

• General Operating Structure – Single office in Salt Lake City, Utah

• Sources of Funds – Deposits generated from wholesale sources including brokers and master CD programs with leading securities firms

• Uses of Funds – Secondary market purchases of quality loans. Including:

• Commercial and Industrial Loans

• Real Estate Loans

• Loan Participations

• Asset and Liability Management – Disciplined and refined management process of matching asset and liability pricing to ensure predictable net interest margins

• CRA - Applying for “wholesale bank” designation.

• Branch Strategy - No branches

Bank Structure and Organization

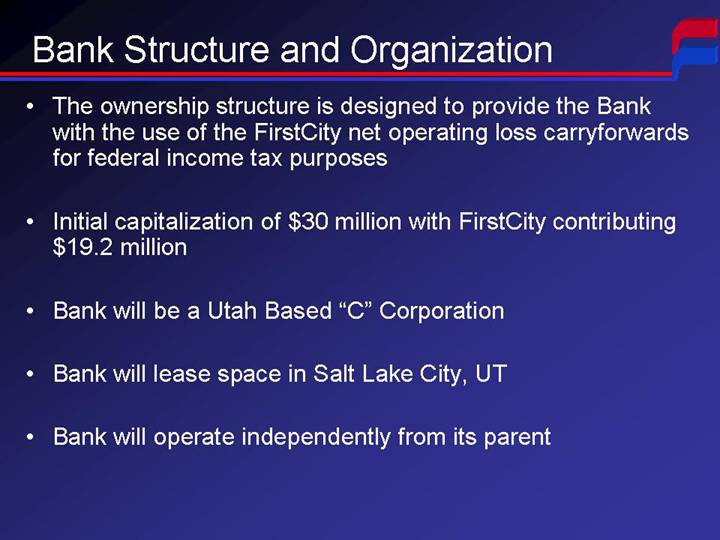

• The ownership structure is designed to provide the Bank with the use of the FirstCity net operating loss carryforwards for federal income tax purposes

• Initial capitalization of $30 million with FirstCity contributing $19.2 million

• Bank will be a Utah Based “C” Corporation

• Bank will lease space in Salt Lake City, UT

• Bank will operate independently from its parent

Relationship Between Bank and Parent

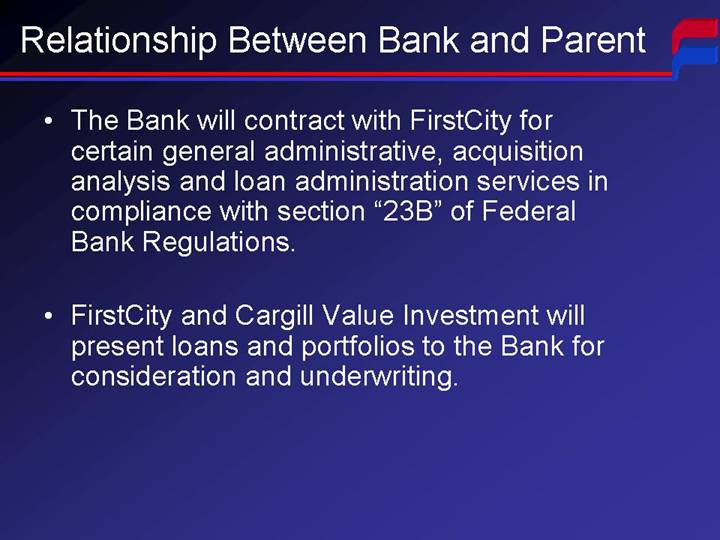

• The Bank will contract with FirstCity for certain general administrative, acquisition analysis and loan administration services in compliance with section “23B” of Federal Bank Regulations.

• FirstCity and Cargill Value Investment will present loans and portfolios to the Bank for consideration and underwriting.

Leveraging of Existing FirstCity Infrastructure

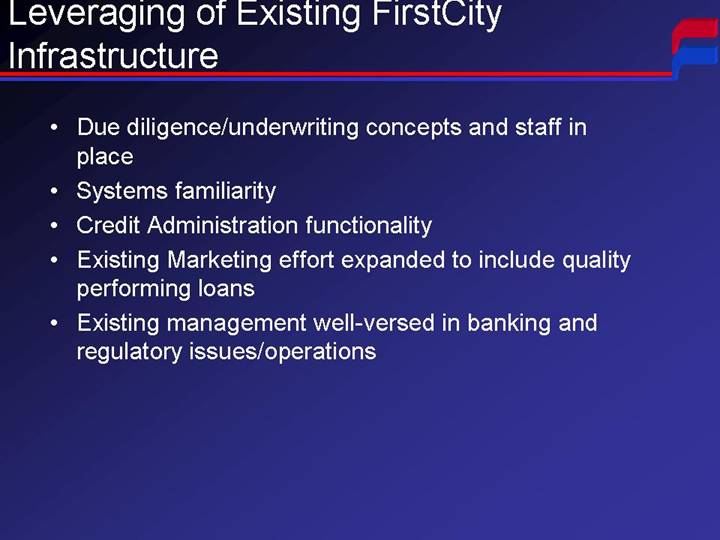

• Due diligence/underwriting concepts and staff in place

• Systems familiarity

• Credit Administration functionality

• Existing Marketing effort expanded to include quality performing loans

• Existing management well-versed in banking and regulatory issues/operations

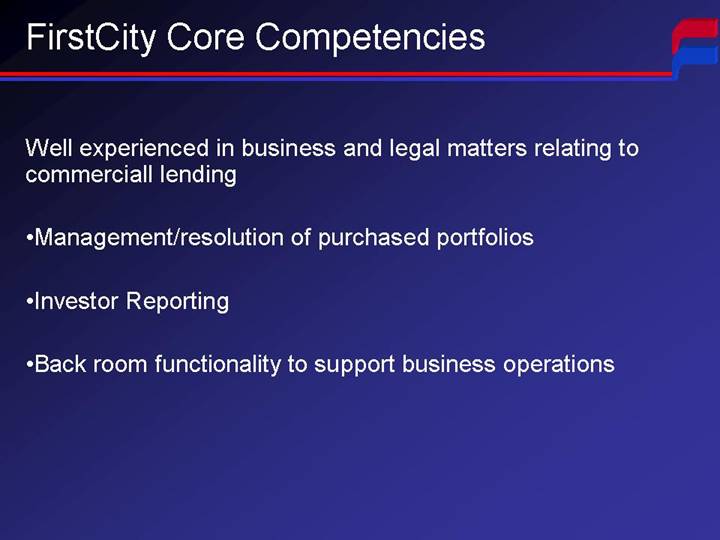

FirstCity Core Competencies

Well experienced in business and legal matters relating to commerciall lending

• Management/resolution of purchased portfolios

• Investor Reporting

• Back room functionality to support business operations

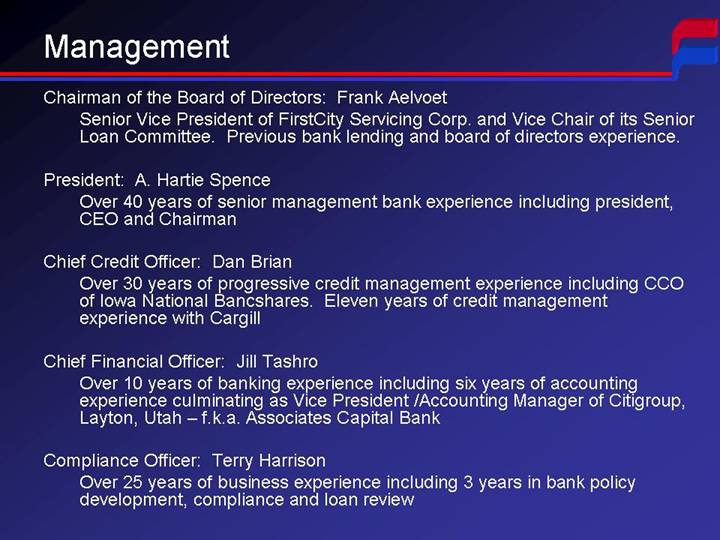

Management

Chairman of the Board of Directors: Frank Aelvoet

Senior Vice President of FirstCity Servicing Corp. and Vice Chair of its Senior Loan Committee. Previous bank lending and board of directors experience.

President: A. Hartie Spence

Over 40 years of senior management bank experience including president, CEO and Chairman

Chief Credit Officer: Dan Brian

Over 30 years of progressive credit management experience including CCO of Iowa National Bancshares. Eleven years of credit management experience with Cargill

Chief Financial Officer: Jill Tashro

Over 10 years of banking experience including six years of accounting experience culminating as Vice President /Accounting Manager of Citigroup, Layton, Utah – f.k.a. Associates Capital Bank

Compliance Officer: Terry Harrison

Over 25 years of business experience including 3 years in bank policy development, compliance and loan review

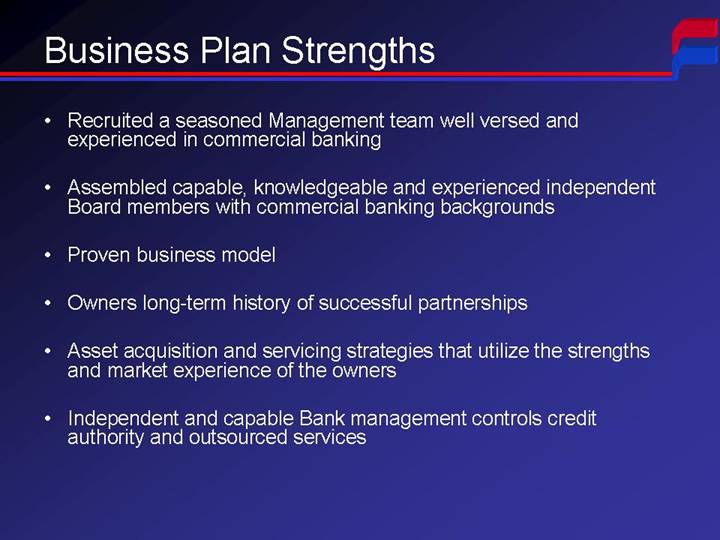

Business Plan Strengths

• Recruited a seasoned Management team well versed and experienced in commercial banking

• Assembled capable, knowledgeable and experienced independent Board members with commercial banking backgrounds

• Proven business model

• Owners long-term history of successful partnerships

• Asset acquisition and servicing strategies that utilize the strengths and market experience of the owners

• Independent and capable Bank management controls credit authority and outsourced services