UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-05476

LORD ABBETT GLOBAL FUND, INC.

(Exact name of Registrant as specified in charter)

90 Hudson Street, Jersey City, New Jersey 07302-3973

(Address of principal executive offices) (Zip code)

Lawrence B. Stoller, Esq.

Vice President, Secretary, and Chief Legal Officer

90 Hudson Street, Jersey City, New Jersey 07302-3973

(Name and address of agent for service)

Registrant’s telephone number, including area code: (888) 522-2388

Date of fiscal year end: 12/31

Date of reporting period: 12/31/2022

Item 1: Report(s) to Shareholders.

LORD ABBETT

ANNUAL REPORT

Lord Abbett

Emerging Markets Bond Fund

Emerging Markets Corporate Debt Fund

Global Bond Fund

For the fiscal year ended December 31, 2022

Table of Contents

Lord Abbett Emerging Markets Bond Fund, Lord Abbett Emerging Markets Corporate Debt Fund, and Lord Abbett Global Bond Fund

Annual Report

For the fiscal year ended December 31, 2022

From left to right: James L.L. Tullis, Independent Chair of the Lord Abbett Funds and Douglas B. Sieg, Director, President and Chief Executive Officer of the Lord Abbett Funds. | | Dear Shareholders: We are pleased to provide you with this overview of the performance of the Funds for the fiscal year ended December 31, 2022. On this page and the following pages, we discuss the major factors that influenced fiscal year performance. For detailed and timely information about the Funds, please visit our website at www.lordabbett.com, where you can also access the quarterly commentaries that provide updates on each Fund’s performance and other portfolio related updates. Thank you for investing in Lord Abbett mutual funds. We value the trust that you place in us and look forward to serving your investment needs in the years to come. Best regards,

Douglas B. Sieg

Director, President and Chief Executive Officer |

Lord Abbett Emerging Markets Bond Fund

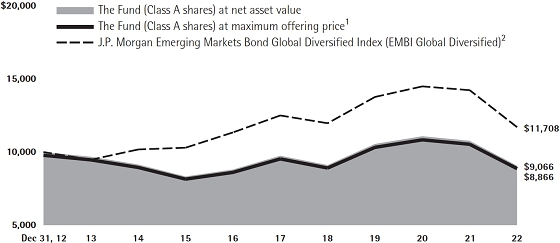

For the fiscal year ended December 31, 2022, the Emerging Markets Bond Fund returned -15.83%, reflecting performance at the net asset value (“NAV”) of Class A shares, with all distributions reinvested, compared to its benchmark, the J.P. Morgan Emerging Markets Bond Global DiversifiedIndex1, which returned -17.78% during the same period.

Over the last twelve months, U.S. dollar-denominated emerging markets sovereign debt (as represented by the J.P.

Morgan Emerging Markets Bond Index Global Diversified1) underperformed U.S. fixed income markets (as represented by the Bloomberg U.S. Aggregate Bond Index2), which returned -13.01%.

At the start of 2022, prospects for emerging markets (EM) debt appeared positive due to an encouraging global growth outlook, an anticipated moderation of supply chain pressures and the continued reopening of developing economies. However, numerous headwinds emerged throughout the period, as inflation expectations began accelerating, leading to

1

increasingly tighter monetary policy by many central banks; an unexpected geopolitical crisis in Ukraine intensified inflationary pressures; and fears of a global growth slowdown emerged.

At the beginning of the period, growing inflationary pressures along with the corresponding tightening of monetary conditions globally was one of the dominant forces impacting emerging market debt. With Consumer Price Index (CPI) readings across developed and emerging economies coming in at higher-than-expected levels at the start of the year, the U.S. Federal Reserve (the Fed) initiated a rate hike of 25 basis points (bps) in March, the first increase to their target Federal Funds Rate since 2018. The Fed continued to increase rates over the next six Federal Open Market Committee (FOMC) meetings to close the year with the target Federal Funds Rate in the 4.25% to 4.50% range. This amounted to the fastest annual pace of rate increases by the Fed since the 1980s. Numerous EM central banks were already well into rate hiking cycles by the time the Fed started tightening monetary policy and many carried out a more aggressive tightening of monetary policy than markets anticipated over the period. Throughout the year, market participants fixated on elevated core yields, the significant appreciation of the U.S. Dollar and how this would impact financing conditions in the developing world as well as global growth.

Despite tightening monetary conditions, inflationary pressures persisted throughout much of the period. The sustained price increases benefitted net commodity-exporting countries,

mainly in Latin America, the Middle East and parts of Africa, at the expense of countries more reliant on imports, particularly in parts of Asia and select regions in Eastern Europe. These price increases came at a time of significantly constrained fiscal budgets for certain countries, limiting the respective governments’ ability to alleviate cost burdens. However, by the back half of the year, commodity prices fell off their highs, most notably in industrial metals and energy, which relieved some pressure among net-importing countries.

In late February, the unexpected invasion of Ukraine by Russian forces significantly dampened sentiment for emerging market debt and added to global inflationary pressures as various commodity prices, particularly in energy and food, appreciated significantly, and anxieties heightened over additional supply chain disruptions. This led to a reduction in expectations for global economic growth and an increase in fears of a stagflationary environment. Local economies closely tied to the region were affected immediately and Russia experienced severe negative economic consequences, with its capital markets largely shutting down and the ban of many of the country’s banks from global payment systems.

While some expected the war to be short lived, the conflict was still ongoing by the end of the year. In the third quarter, Russia intensified efforts against Ukraine with a partial mobilization and announced it would not be resuming a majority of gas exports to Europe, worrying investors about the implications to European industrial production.

2

In the latter half of the year, many investors shifted focus to the potential for a global growth slowdown, given more restrictive financial conditions and continuing troubles in China, among other factors. After a disappointing second quarter GDP release for China in early July, the Chinese government’s supportive signaling somewhat quelled investor worries. However, growth prospects trended lower in the third quarter amid further lockdowns in various Chinese cities after a resurgence of the Covid-19 virus and continued deterioration of the country’s Real Estate sector. Lower economic activity from China, the world’s second-largest economy, a reduction in global trade volumes, and a general economic slowdown in developed countries worried market participants about the spillover effects into the emerging markets.

The deteriorating fundamental backdrop has brought clear differentiation within the emerging markets. Various countries with high energy exports remained in a strong position due to above-average energy prices and many larger EM economies with more robust fiscal reserves were less affected by worsening economic conditions. Conversely, economies reliant on manufacturing of more cyclical goods and those with higher debt levels appeared more vulnerable.

2022 marked the worst year for emerging market sovereign bonds1 since the Global Financial Crisis (GFC) of 2008 and the asset class sold off throughout much of the period, despite rebounding somewhat in November after a better-than-expected U.S. CPI report. Investment grade bonds3 underperformed high yield bonds4 over the period given the higher quality segment’s

longer duration. Similarly, longer-term bonds materially underperformed shorter-term bonds. Given impacts from the Russian invasion, Europe trailed significantly from a regional perspective and Ukraine came in with the worst country performance, while the Middle East outperformed over the period. In terms of technical factors, EM bond funds experienced outflows for much of the period and closed out the year with roughly $87 billion in negative net flows. Supply was more supportive throughout the period, as the year closed out with the lowest level of net issuance since 2008.

In terms of key Fund performance drivers, from a credit quality perspective, security selection within emerging markets high yield sovereign debt was the primary driver of relative outperformance during the period. The Fund’s underweight to, as well as security selection within, investment grade sovereign bonds also contributed to relative returns. One of the primary detractors from relative performance was the Fund’s overweight to various countries’ sovereign bonds that became more distressed throughout the period, such as Sri Lanka, Egypt and El Salvador.

From a regional perspective, positioning within Eastern Europe significantly contributed to relative performance. Given the unanticipated geopolitical crisis in the region, caused by Russia’s military invasion of Ukraine and the resulting economic fallout to the region, the Fund’s underweight position in the Russian Financial and Sovereign sectors going into the conflict led to a positive impact. Not long after Russia entered Ukraine, the aggressor country experienced severe economic sanctions, significant downgrades

3

to its growth outlook, a flight of foreign capital, and its financial system being disconnected from many parts of the global economy. Our remaining position in various Russian sovereign and corporate bonds became an overweight exposure in the Fund after the indices’ removal of all Russian holdings in March 2022. Later in the year, these positions started to recover from depressed levels due to increased demand from Russian issuers and investors, which also contributed to relative performance. The Fund’s modest exposure to Ukraine dragged on relative returns due to the deep economic contraction caused by the invasion. While relative performance benefitted from being devoid numerous sectors within the country, an allocation to the Consumer sector more than offset these contributions and led to an overall negative impact.

An overweight to, as well as selection within, the Middle East also contributed to relative performance. Most notably, exposure to the sovereign debt of Saudi Arabia and the United Arab Emirates led to a positive impact on relative returns. Saudi Arabia’s strong position in the global energy market drove relative outperformance given the increased demand and elevated prices for oil and gas. As a result, the country’s gross domestic product grew at the highest level in over a decade, with much of this growth driven by the Oil sector.

The primary detractor from relative performance from a regional perspective was the Fund’s positioning in Latin America, primarily within Ecuador and Colombia. An overweight to Ecuador’s sovereign bonds detracted from relative performance as deteriorating economic conditions within the

country as well as elevated political instability led to headwinds. However, we believe the country stands to benefit from being a net exporter of energy in the current environment and, in our view, its fundamental position is stronger than what’s reflected by market pricing. An overweight to Columbia’s government debt also dragged on relative returns, as the country’s fiscal and current account deficits have weighed on the country’s financial position.

More generally, the Fund’s underweight to various distressed credits across the developing world led to a positive impact on relative returns, particularly in Pakistan, Zambia and Lebanon. For instance, Pakistan’s sovereign bonds significantly underperformed over the period and finished the year at extremely depressed prices due to numerous headwinds, including current account pressures, domestic political issues, a high debt burden, natural disasters, power disruptions and food shortages.

Lord Abbett Emerging Markets Corporate Debt Fund

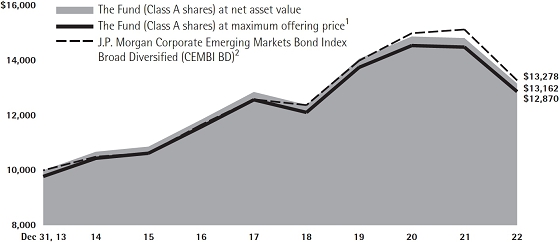

For the fiscal year ended December 31, 2022, the Emerging Markets Corporate Debt Fund returned -11.19%, reflecting performance at the net asset value (“NAV”) of Class A shares, with all distributions reinvested, compared to its benchmark, the J.P. Morgan Corporate Emerging Markets Bond Index Broad Diversified5, which returned -12.26% during the same period.

Over the last twelve months, U.S. dollar-denominated emerging markets corporate debt (as represented by the J.P.

4

Morgan Corporate Emerging Markets Bond Index Broad Diversified1) outperformed U.S. fixed income markets (as represented by the Bloomberg U.S. Aggregate Bond Index2), which returned -13.01%.

At the start of 2022, prospects for emerging markets (EM) debt appeared positive due to an encouraging global growth outlook, an anticipated moderation of supply chain pressures and the continued reopening of developing economies. However, numerous headwinds emerged throughout the period, as inflation expectations began accelerating, leading to increasingly tighter monetary policy by many central banks; an unexpected geopolitical crisis in Ukraine intensified inflationary pressures; and fears of a global growth slowdown emerged.

At the beginning of the period, growing inflationary pressures along with the corresponding tightening of monetary conditions globally was one of the dominant forces impacting emerging market debt. With Consumer Price Index (CPI) readings across developed and emerging economies coming in at higher-than-expected levels at the start of the year, the U.S. Federal Reserve (the Fed) initiated a rate hike of 25 basis points (bps) in March, the first increase to their target Federal Funds Rate since 2018. The Fed continued to increase rates over the next six Federal Open Market Committee (FOMC) meetings to close the year with the target Federal Funds Rate in the 4.25% to 4.50% range. This amounted to the fastest annual pace of rate increases by the Fed since the 1980s. Numerous EM central banks were already

well into rate hiking cycles by the time the Fed started tightening monetary policy and many carried out a more aggressive tightening of monetary policy than markets anticipated over the period. Throughout the year, market participants fixated on elevated core yields, the significant appreciation of the U.S. Dollar and how this would impact financing conditions in the developing world as well as global growth.

Despite tightening monetary conditions, inflationary pressures persisted throughout much of the period. The sustained price increases benefitted net commodity-exporting countries, mainly in Latin America, the Middle East and parts of Africa, at the expense of countries more reliant on imports, particularly in parts of Asia and select regions in Eastern Europe. These price increases came at a time of significantly constrained fiscal budgets for certain countries, limiting the respective governments’ ability to alleviate cost burdens. However, by the back half of the year, commodity prices fell off their highs, most notably in industrial metals and energy, which relieved some pressure among net-importing countries.

In late February, the unexpected invasion of Ukraine by Russian forces significantly dampened sentiment for emerging market debt and added to global inflationary pressures as various commodity prices, particularly in energy and food, appreciated significantly, and anxieties heightened over additional supply chain disruptions. This led to a reduction in expectations for global economic growth and an increase in fears of a stagflationary

5

environment. Local economies closely tied to the region were affected immediately and Russia experienced severe negative economic consequences, with its capital markets largely shutting down and the ban of many of the country’s banks from global payment systems.

While some expected the war to be short lived, the conflict was still ongoing by the end of the year. In the third quarter, Russia intensified efforts against Ukraine with a partial mobilization and announced it would not be resuming a majority of gas exports to Europe, worrying investors about the implications to European industrial production.

In the latter half of the year, many investors shifted focus to the potential for a global growth slowdown, given more restrictive financial conditions and continuing troubles in China, among other factors. After a disappointing second quarter GDP release for China in early July, the Chinese government’s supportive signaling somewhat quelled investor worries. However, growth prospects trended lower in the third quarter amid further lockdowns in various Chinese cities after a resurgence of the Covid-19 virus and continued deterioration of the country’s Real Estate sector. Lower economic activity from China, the world’s second-largest economy, a reduction in global trade volumes, and a general economic slowdown in developed countries worried market participants about the spillover effects into the emerging markets.

The deteriorating fundamental backdrop has brought clear differentiation within the emerging markets. Various countries with high energy exports remained in a strong position due to above-average energy prices and many larger EM economies with more robust fiscal reserves were less affected by worsening economic conditions. Conversely, economies reliant on manufacturing of more cyclical goods and those with higher debt levels appeared more vulnerable.

2022 marked the worst year for emerging market corporate bonds1 since the Global Financial Crisis (GFC) of 2008 and the asset class sold off throughout much of the period, despite rebounding somewhat in November after a better-than-expected U.S. CPI report. Investment grade bonds3 underperformed high yield bonds4 over the period given the higher quality segment’s longer duration. Similarly, longer-term bonds materially underperformed shorter-term bonds. The Financial sector led over the period while the Metals & Mining and Oil & Gas segments underperformed. Given impacts from the Russian invasion, Europe trailed significantly from a regional perspective and Ukraine came in with the worst country performance, while Africa outperformed over the period. In terms of technical factors, EM bond funds experienced outflows for much of the period and closed out the year with roughly $87 billion in negative net flows. Supply was more supportive throughout the period, as the year closed out with the lowest level of net issuance since 2008.

6

In terms of key drivers of Fund performance, from a credit quality perspective, security selection within emerging markets high yield corporate debt was the primary driver of relative outperformance during the period. The Fund’s underweight to, as well as security selection within, investment grade corporate bonds also contributed to relative returns. Additionally, selection of various commodity-producing firms led to a positive impact on relative performance given heightened prices and strong demand. Rates positioning dragged modestly on relative performance, primarily due to the Fund’s slightly longer duration in the first half of the year as yields rose significantly with rising inflation pressures and tightening monetary conditions.

From a regional perspective, positioning within Eastern Europe significantly contributed to relative performance. Given the unanticipated geopolitical crisis in the region, caused by Russia’s military invasion of Ukraine and the resulting economic fallout to the region, the Fund’s underweight position in Russia going into the conflict led to a positive impact. Not long after Russia entered Ukraine, the aggressor country experienced severe economic sanctions, significant downgrades to its growth outlook, a flight of foreign capital and its financial system being disconnected from many parts of the global economy. Our remaining position in various Russian corporate bonds became an overweight exposure in the Fund after the indices’ removal of all Russian holdings in

March 2022. Later in the year, these positions started to recover from depressed levels due to increased demand from Russian issuers and investors, which also contributed to relative performance.

The Fund’s modest exposure to Ukraine dragged on relative performance due to the deep economic contraction caused by the invasion. While the Fund benefitted from being void numerous sectors within the country, the relative performance drag from an allocation to the Consumer sector more than offset these contributions and led to an overall negative impact. Also, within Eastern Europe, the Fund’s exposure to Turkey modestly contributed to relative returns, primarily due to an overweight to a Turkish state-owned bank, as prices recovered throughout the second half of 2022.

Positioning in Asia benefitted relative performance as well, primarily driven by the Fund’s underweight to numerous Gaming issuers within Macau over the first three quarters of the year. Many of these firms experienced severe drops in top line revenue with a resurgence of Covid-19 and the corresponding lockdowns in the region that depressed casinos’ customer volumes. However, by the fourth quarter, we began adding to this segment due to our expectations of a potential reopening in China, and by the close of the year, the Fund was overweight the Gaming segment. This led to relative outperformance given the rally of many Gaming issuers in the fourth quarter with the easing of Covid restrictions by the Chinese government. Additionally, the Fund’s underweight to the Philippines

7

Utility sector contributed to relative returns, given the high sensitivity of many bonds within the segment to rising global yields.

Within the Middle East, an overweight to, as well as selection within various Gulf Cooperation Council countries led to a positive impact on relative performance. In particular, the Fund’s exposure to the Energy sector within Oman, Qatar and the United Arab Emirates led to relative outperformance as various issuers benefitted from elevated energy prices and a positive supply & demand dynamic throughout much of the year. More specifically, energy prices were supported by increased demand with various parts of the emerging markets and developing world reopening and starting to recover from the pandemic while supply was constrained for much of the period, partly due to the European Union’s ban on Russian oil imports post invasion.

The primary detractor from relative performance from a regional perspective was the Fund’s overweight to Central and Western Asia, particularly within Kazakhstan, which experienced growth headwinds given a disruption to its oil pipelines due to the geopolitical crisis between Ukraine and Russia.

Lord Abbett Global Bond Fund

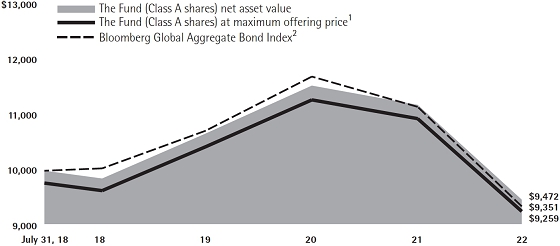

For the fiscal year ended December 31, 2022, the Fund returned -15.44%, reflecting performance at the net asset value (NAV) of Class A shares with all distributions reinvested, compared to its benchmark, the

Bloomberg Global Aggregate Bond Index,6 which returned -16.25%.

The twelve-month period ending December 31, 2022, introduced meaningful headwinds for U.S. markets that led to selloffs in virtually all asset classes. The major risks over the period were inflationary pressures, which reached multi-decade highs, and the most rapid pace of interest rate hikes implemented in history by the U.S. Federal Reserve (Fed). Rates spiked across the U.S. yield curve as a result, with U.S. Treasury yields at almost all maturities reaching their highest levels in years. Other notable challenges for markets included supply chain dislocations and labor shortages influenced in part by the Omicron variant of COVID-19, as well as escalating geopolitical tensions headlined by Russia’s invasion of Ukraine.

The surge in rates over the year caused softness in both major fixed income and equity indices. Equities fared the worst amid the sell-off, with the S&P 5007 returning -18.11% and experiencing its worst year since the Global Financial Crisis (GFC). The tech-heavy NASDAQ8 also logged its worst year since 2008, declining -32.54% as growth-related stocks in semiconductor and software sectors suffered in the face of inflationary pressures. Within fixed income, higher rates caused underperformance in longer duration bonds. These included U.S. Treasuries9 and investment grade bonds10 which returned -12.46% and -15.76% over the period, respectively. However, high yield bond11 and leveraged loan12 indexes outperformed the investment grade index for the period because of their lower

8

duration profiles. Notably, high yield bonds and leveraged loans returned -11.21% and -1.06%, respectively, outperforming higher quality bonds despite recessionary fears in the U.S. economy contributing to wider spreads. Leveraged loans in particular were able to significantly outperform relative to other assets given their insulation from rate volatility due to their floating-rate coupons.

Inflationary concerns began to take focus towards the end of 2021 before becoming a dominant storyline in 2022. Headline consumer price index (CPI) readings had hovered a little above 5% year-over-year for most of 2021, which led investors to question whether this period of rising prices would be more persistent than originally thought. This debate intensified in the beginning of the year as inflation readings continued to climb throughout the first half of 2022, with CPI peaking at 9.1% year-over-year in June. The surge in prices was due primarily to an imbalance between supply and demand dynamics across multiple industries, including energy, food, and used cars.

Inflationary pressures throughout the period were most evident in energy costs, which rose more than 30% year-over-year by the end of June. The Energy sector, which had been subject to rising consumer demand as global economies reopened from lockdowns induced by COVID-19, faced added friction with Russia’s invasion of Ukraine as Russia had been a large exporter of oil and certain minerals. Various sanctions were instilled on Russia from Western nations in response to their aggression towards Ukraine, which contributed to surging prices. Crude oil

specifically reached over $100 per barrel, the highest value since 2014.

The Fed pivoted towards a much more hawkish stance on monetary policy during the period given the surge in inflation. After remaining mostly consistent in its messaging around expectations that price pressures would be transitory, elevated and more persistent inflation pressures caused the Fed to move the target federal funds rate into more restrictive territory. This resulted in a 25-basis point (bps) hike in the federal funds rate at the March Federal Open Market Committee (FOMC) meeting, the first hike in more than three years. Five additional rate hikes followed in the succeeding months, one of 50 bps, and four consecutive hikes of 75 bps and an additional one of 50 bps as inflation prints continued to come mostly in hotter than expected, resulting in a federal funds rate at a range of 4.25%-4.50% by the end of 2022. Bond yields shot up amid this aggressive policy, leading to a bearish curve flattening and ultimately periods of significant yield curve inversion, with the spread between the 2-year and 10-year Treasury yields hitting its most negative level in more than 40 years.

Key macroeconomic indicators trended lower throughout the period. Most notably, the U.S. reported real GDP decline of -1.6% in the first quarter of 2022 and -0.9% in the second quarter before returning to growth in the third quarter. Worries of an impending recession resulted in consumer sentiment dropping to levels worse than during the height of the COVID-19 pandemic and the GFC of 2008.

9

Despite rising recessionary signs, select bright spots in the U.S. economy supported the idea that a potential recession would be shallow. One of the most positive developments seemed to be the traction behind the peak inflation narrative, which gained momentum in the fourth quarter from lower-than-expected CPI prints in both October and November. In addition, energy prices retracted from their multi-year highs, rent prices began to stabilize, and wage growth showed signs of softening. Job growth also remained strong in the period, and the U.S. national unemployment rate continued to hover around pre-COVID lows. Companies also cited relatively stable demand in both second and third quarter earnings seasons as consumers remained resilient despite higher prices. Separately, labor shortages eased, and supply chain frictions moderated, providing added benefits for companies managing generally higher input costs.

For the twelve-month period ended December 31 2022, the Fund’s underweight position to duration versus the benchmark was the largest contributor to relative performance as yields rose and interest rate sensitive bonds were negatively affected.

1 The J.P. Morgan Emerging Markets Bond Global Diversified Index is a uniquely-weighted version of the J.P. Morgan Emerging Markets Bond Index Global (EMBI Global). It limits the weights of those index countries with larger debt stocks by only including specified portions of these countries’ eligible current face amounts of debt outstanding. The countries covered in the EMBI Global Diversified are identical to those covered by the EMBI Global.

Also contributing to relative performance was an off-benchmark allocation to ABS. The short-term, high quality ABS allocation outperformed the benchmark over the period as the sector was better insulated against rising interest rates than other fixed income sectors with longer duration profiles.

Another contributor to relative performance over the period was an underweight to sovereign debt. Sovereign debt was challenged by higher interest rates and a stronger U.S. dollar.

The largest detractor from relative performance over the period was an overweight to both U.S. and non-U.S developed high yield credit. High yield credit underperformed the Fund’s benchmark on a duration-adjusted basis, as investors weighed the risks of owning lower quality companies amid rising interest rates and higher financing costs amid less supportive central bank policies.

Also detracting from relative performance was security selection within investment-grade corporate credit.

The Fund portfolios are actively managed and, therefore, holdings and the weightings of a particular issuer or particular sector as a percentage of portfolio assets are subject to change. Sectors may include many industries.

2 The Bloomberg U.S. Aggregate Bond Index is an index of U.S dollar-denominated, investment-grade U.S. government and corporate securities, and mortgage pass-through securities, and asset-backed securities. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and an investor cannot invest directly in an index.

3 Investment Grade Bonds segment of the EMBI Global Diversified

10

4 High Yield Bonds segment of the EMBI Global Diversified

5 The J.P. Morgan Corporate Emerging Markets Bond Index Broad Diversified (CEMBI BD) is a market capitalization weighted index that tracks total returns of U.S. dollar denominated debt instruments issued by corporate entities in emerging markets countries. The Index limits the current face amount allocations of the bonds in the CEMBI Broad by constraining the total face amount outstanding for countries with larger debt stocks.

6 The Bloomberg Global Aggregate Bond Index is a broad-based measure of the global investment-grade, fixed-income markets. The three major components of this index are the U.S. Aggregate, the Pan-European Aggregate, and the Asian-Pacific Aggregate Indexes. The index also includes euro dollar and euro/yen corporate bonds, Canadian government securities, and U.S. dollar investment-grade 144A securities.

7 The S&P 500® Index is widely regarded as the standard for measuring large cap U.S. stock market performance and includes a representative sample of leading companies in leading industries.

8 The Nasdaq Composite Index is the market capitalization-weighted index of over 2,500 common equities listed on the Nasdaq stock exchange.

9 As represented by the U.S. Treasury component of the Bloomberg U.S. Government Index as of 12/31/2022.

10 As represented by the Bloomberg US Corp Investment Grade Index as of 12/31/2022.

11 As represented by the ICE BofA U.S. High Yield Constrained Index as of 12/31/2022.

12 As represented by the Credit Suisse Leveraged Loan Index as of 12/31/2022.

Unless otherwise specified, indexes reflect total return, with all dividends reinvested. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

Important Performance and Other Information

Performance data quoted in the following pages reflect past performance and are no guarantee of

future results. Current performance may be higher or lower than the performance quoted. The investment return and principal value of an investment in the Funds will fluctuate so that shares, on any given day or when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by calling Lord Abbett at 888-522-2388 or referring to www.lordabbett.com.

Except where noted, comparative Fund performance does not account for the deduction of sales charges and would be different if sales charges were included. Each Fund offers classes of shares with distinct pricing options. For a full description of the differences in pricing alternatives, please see each Fund’s prospectus.

During certain periods shown, expense waivers and reimbursements were in place. Without such expense waivers and reimbursements, the Funds’ returns would have been lower.

The annual commentary above discusses the views of the Funds’ management and various portfolio holdings of the Funds as of December 31, 2022. These views and portfolio holdings may have changed after this date. Information provided in the commentary is not a recommendation to buy or sell securities. Because the Funds’ portfolios are actively managed and may change significantly, the Funds may no longer own the securities described above or may have otherwise changed their positions in the securities. For more recent information about the Funds’ portfolio holdings, please visit www.lordabbett.com.

A Note about Risk: See Notes to Financial Statements for a discussion of investment risks. For a more detailed discussion of the risks associated with each Fund, please see each Fund’s prospectus.

Mutual funds are not insured by the FDIC, are not deposits or other obligations of, or guaranteed by, banks, and are subject to investment risks including possible loss of principal amount invested.

11

Emerging Markets Bond Fund

Investment Comparison

Below is a comparison of a $10,000 investment in Class A shares with the same investment in the J.P. Morgan Emerging Markets Bond Global Diversified Index (EMBI Global Diversified), assuming reinvestment of all dividends and distributions. The performance of the other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursement of expenses, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns at Maximum Applicable

Sales Charge for the Periods Ended December 31, 2022 |

| | | 1 Year | | 5 Years | | 10 Years | | Life of Class | |

| Class A3 | | -17.66% | | -1.87% | | -1.20% | | – | |

| Class C4 | | -17.06% | | -2.02% | | -1.58% | | – | |

| Class F5 | | -15.45% | | -1.22% | | -0.81% | | – | |

| Class F36 | | -15.48% | | -1.20% | | – | | -0.12% | |

| Class I5 | | -15.49% | | -1.20% | | -0.75% | | – | |

| Class R35 | | -15.92% | | -1.69% | | -1.23% | | – | |

| Class R47 | | -15.71% | | -1.49% | | – | | 0.20% | |

| Class R57 | | -15.47% | | -1.18% | | – | | 0.49% | |

| Class R67 | | -15.48% | | -1.19% | | – | | 0.51% | |

1 Reflects the deduction of the maximum initial sales charge of 2.25%.

2 Performance for the unmanaged index does not reflect any fees or expenses. The performance of the index is not necessarily representative of the Fund’s performance.

3 Total return, which is the percentage change in net asset value, after deduction of the maximum initial sales charge of 2.25% applicable to Class A shares, with all dividends and distributions reinvested for the periods shown ending December 31,

2022, is calculated using the SEC-required uniform method to compute such return.

4 The 1% CDSC for Class C shares normally applies before the first anniversary of the purchase date. Performance for other periods is at net asset value.

5 Performance is at net asset value.

6 Commenced operations and performance for the Class began on April 4, 2017. Performance is at net asset value.

7 Commenced operations and performance for the Class began on June 30, 2015. Performance is at net asset value.

12

Emerging Markets Corporate Debt Fund

Investment Comparison

Below is a comparison of a $10,000 investment in Class A shares with the same investment in the J.P. Morgan Corporate Emerging Markets Bond Index Broad Diversified (CEMBI BD), assuming reinvestment of all dividends and distributions. The performance of the other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursement of expenses, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns at Maximum Applicable

Sales Charge for the Periods Ended December 31, 2022

| | | 1 Year | | 5 Years | | Life of Class | |

| Class A3 | | -13.20% | | 0.01% | | 2.84% | |

| Class C4 | | -12.58% | | -0.15% | | 2.42% | |

| Class F5 | | -11.09% | | 0.57% | | 3.20% | |

| Class F36 | | -10.88% | | 0.83% | | 1.62% | |

| Class I5 | | -11.02% | | 0.65% | | 3.29% | |

| Class R35 | | -11.45% | | 0.27% | | 3.08% | |

| Class R47 | | -11.24% | | 0.43% | | 2.37% | |

| Class R57 | | -11.00% | | 0.68% | | 2.62% | |

| Class R67 | | -10.86% | | 0.85% | | 2.77% | |

1 Reflects the deduction of the maximum initial sales charge of 2.25%.

2 Performance for the unmanaged index does not reflect any fees or expenses. The performance of the index is not necessarily representative of the Fund’s performance.

3 Class A shares commenced operations on December 6, 2013 and performance for the Class began on December 31, 2013. Total return, which is the percentage change in net asset value, after deduction of the maximum initial sales charge of 2.25% applicable to Class A shares, with all dividends and distributions reinvested for the period shown ended December 31, 2022, is calculated using the SEC-required uniform method to compare such return.

4 Class C shares commenced operations on December 6, 2013 and performance for the Class began on December 31, 2013. The 1% CDSC for Class C normally applies before the first anniversary of the purchase date. Performance for other periods is at net asset value.

5 Commenced operations on December 6, 2013 and performance for the Class began on December 31, 2013. Performance is at net asset value.

6 Commenced operations and performance for the Class began on April 4, 2017. Performance is at net asset value.

7 Commenced operations and performance for the Class began on June 30, 2015. Performance is at net asset value.

13

Global Bond Fund

Investment Comparison

Below is a comparison of a $10,000 investment in Class A shares with the same investment in the Bloomberg Global Aggregate Bond Index, assuming reinvestment of all dividends and distributions. The performance of the other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursement of expenses, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns at Maximum Applicable

Sales Charge for the Periods Ended December 31, 2022

| | | 1 Year | | Life of Class |

| Class A3 | | -17.38% | | -1.73% |

| Class C4 | | -16.79% | | -1.88% |

| Class F5 | | -15.36% | | -1.02% |

| Class F35 | | -15.26% | | -0.96% |

| Class I5 | | -15.27% | | -1.02% |

| Class R35 | | -15.70% | | -1.52% |

| Class R45 | | -15.57% | | -1.27% |

| Class R55 | | -15.27% | | -1.02% |

| Class R65 | | -15.27% | | -0.96% |

1 Reflects the deduction of the maximum initial sales charge of 2.25%.

2 Performance for the unmanaged index does not reflect any fees or expenses. The performance of the index is not necessarily representative of the Fund’s performance.

3 Class A shares commenced operations on July 26, 2018 and performance for the Class began on July 31, 2018. Total return, which is the percentage change in net asset value, after deduction of the maximum initial sales charge of 2.25% applicable to Class A shares, with all distributions reinvested for the periods shown

ending December 31, 2022, is calculated using the SEC-required uniform method to compute such return.

4 Class C shares commenced operations on July 26, 2018 and performance for the Class began on July 31, 2018. The 1% CDSC for Class C shares normally applies before the first anniversary of the purchase date. Performance for other periods is at net asset value.

5 Commenced operations on July 26, 2018 and performance for the Class began on July 31, 2018. Performance is at net asset value.

14

Expense Example

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments (these charges vary among the share classes); and (2) ongoing costs, including management fees; distribution and service (12b-1) fees (these charges vary among the share classes); and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in each Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2022 through December 31, 2022).

Actual Expenses

For each class of each Fund, the first line of the table on the following pages provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading titled “Expenses Paid During Period 7/1/22 – 12/31/22” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each class of each Fund, the second line of the table on the following pages provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

15

Emerging Markets Bond Fund

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† | |

| | | 7/1/22 | | 12/31/22 | | 7/1/22 -

12/31/22 | |

| Class A | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,038.60 | | | | $ | 4.98 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,020.32 | | | | $ | 4.94 | | |

| Class C | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,037.70 | | | | $ | 8.32 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,017.04 | | | | $ | 8.24 | | |

| Class F | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,042.20 | | | | $ | 3.96 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,021.32 | | | | $ | 3.92 | | |

| Class F3 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,042.40 | | | | $ | 3.91 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,021.37 | | | | $ | 3.87 | | |

| Class I | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,042.30 | | | | $ | 3.96 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,021.32 | | | | $ | 3.92 | | |

| Class R3 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,039.70 | | | | $ | 6.53 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,018.80 | | | | $ | 6.46 | | |

| Class R4 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,041.00 | | | | $ | 5.25 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,020.06 | | | | $ | 5.19 | | |

| Class R5 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,042.40 | | | | $ | 3.91 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,021.37 | | | | $ | 3.87 | | |

| Class R6 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,042.40 | | | | $ | 3.91 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,021.37 | | | | $ | 3.87 | | |

| † | For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (0.97% for Class A, 1.62% for Class C, 0.77% for Class F, 0.76% for Class F3, 0.77% for Class I, 1.27% for Class R3, 1.02% for Class R4, 0.76% for Class R5 and 0.76% for Class R6) multiplied by the average account value over the period, multiplied by 184/365 (to reflect one-half year period). |

16

Portfolio Holdings Presented by Sector

December 31, 2022

| Sector* | | %** |

| Basic Materials | | 0.88% | |

| Communications | | 0.76% | |

| Consumer Non-Cyclical | | 1.24% | |

| Energy | | 16.72% | |

| Financial | | 4.25% | |

| Industrial | | 0.34% | |

| Utilities | | 5.98% | |

| U.S. Government | | 69.32% | |

| Repurchase Agreements | | 0.51% | |

| Total | | 100.00% | |

| * | | A sector may comprise several industries. |

| ** | | Represents percent of total investments, which excludes derivatives. |

17

Emerging Markets Corporate Debt Fund

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† | |

| | | 7/1/22 | | 12/31/22 | | 7/1/22 -

12/31/22 | |

| Class A | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,037.00 | | | | $ | 5.39 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,019.91 | | | | $ | 5.35 | | |

| Class C | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,034.60 | | | | $ | 8.56 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,016.79 | | | | $ | 8.49 | | |

| Class F | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,038.30 | | | | $ | 4.88 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,020.42 | | | | $ | 4.84 | | |

| Class F3 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,038.80 | | | | $ | 3.65 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,021.63 | | | | $ | 3.62 | | |

| Class I | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,038.90 | | | | $ | 4.37 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,020.92 | | | | $ | 4.33 | | |

| Class R3 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,036.30 | | | | $ | 6.93 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,018.40 | | | | $ | 6.87 | | |

| Class R4 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,037.60 | | | | $ | 5.65 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,019.66 | | | | $ | 5.60 | | |

| Class R5 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,038.10 | | | | $ | 4.37 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,020.92 | | | | $ | 4.33 | | |

| Class R6 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,039.60 | | | | $ | 3.65 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,021.63 | | | | $ | 3.62 | | |

| † | For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (1.05% for Class A, 1.67% for Class C, 0.95% for Class F, 0.71% for Class F3, 0.85% for Class I, 1.35% for Class R3, 1.10% for Class R4, 0.85% for Class R5 and 0.71% for Class R6) multiplied by the average account value over the period, multiplied by 184/365 (to reflect one-half year period). |

18

Portfolio Holdings Presented by Sector

December 31, 2022

| Sector* | | %** |

| Basic Material | | 13.31% | |

| Communications | | 8.14% | |

| Consumer Cyclical | | 5.35% | |

| Consumer Non Cyclical | | 6.34% | |

| Diversified | | 1.24% | |

| Energy | | 22.95% | |

| Financial | | 21.53% | |

| Foreign Government | | 1.35% | |

| Industrial | | 2.48% | |

| Technology | | 3.10% | |

| U.S. Government | | 3.05% | |

| Utilities | | 10.84% | |

| Repurchase Agreements | | 0.32% | |

| Total | | 100.00% | |

| * | | A sector may comprise several industries. |

| ** | | Represents percent of total investments, which excludes derivatives. |

19

Global Bond Fund

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† | |

| | | 7/1/22 | | 12/31/22 | | 7/1/22 -

12/31/22 | |

| Class A | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,001.70 | | | | $ | 3.94 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,021.27 | | | | $ | 3.97 | | |

| Class C | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 998.60 | | | | $ | 7.05 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,018.15 | | | | $ | 7.12 | | |

| Class F | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,002.70 | | | | $ | 2.93 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,022.28 | | | | $ | 2.96 | | |

| Class F3 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,002.70 | | | | $ | 2.88 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,022.33 | | | | $ | 2.91 | | |

| Class I | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,002.70 | | | | $ | 2.93 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,022.28 | | | | $ | 2.96 | | |

| Class R3 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,000.20 | | | | $ | 5.44 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,019.76 | | | | $ | 5.50 | | |

| Class R4 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,001.40 | | | | $ | 4.19 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,021.02 | | | | $ | 4.23 | | |

| Class R5 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,002.70 | | | | $ | 2.93 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,022.28 | | | | $ | 2.96 | | |

| Class R6 | | | | | | | | | | | | | | | | |

| Actual | | | $ | 1,000.00 | | | | $ | 1,002.70 | | | | $ | 2.88 | | |

| Hypothetical (5% Return Before Expenses) | | | $ | 1,000.00 | | | | $ | 1,022.33 | | | | $ | 2.91 | | |

| † | For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (0.78% for Class A, 1.40% for Class C, 0.58% for Class F, 0.57% for Class F3, 0.58% for Class I, 1.08% for Class R3, 0.83% for Class R4, 0.58% for Class R5 and 0.57% for Class R6) multiplied by the average account value over the period, multiplied by 184/365 (to reflect one-half year period). |

20

Portfolio Holdings Presented by Sector

December 31, 2022

| Sector* | | %** |

| Asset Backed Securities | | 7.70% | |

| Basic Material | | 1.82% | |

| Communications | | 6.77% | |

| Consumer Cyclical | | 4.65% | |

| Consumer Non Cyclical | | 8.68% | |

| Energy | | 7.39% | |

| Financial | | 16.68% | |

| Foreign Government | | 16.84% | |

| Industrial | | 6.02% | |

| Mortgage Backed Securities | | 9.52% | |

| Municipal | | 0.39% | |

| Technology | | 1.51% | |

| U.S. Government | | 3.76% | |

| Utilities | | 5.22% | |

| Repurchase Agreements | | 3.05% | |

| Total | | 100.00% | |

| * | | A sector may comprise several industries. |

| ** | | Represents percent of total investments, which excludes derivatives. |

21

Schedule of Investments

EMERGING MARKETS BOND FUND December 31, 2022

| Investments | | | Interest

Rate | | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| LONG-TERM INVESTMENTS 97.57% | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| CORPORATE BONDS 30.65% | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Bahrain 0.46% | | | | | | | | | | | | | | |

| Oil & Gas | | | | | | | | | | | | | | |

| Oil and Gas Holding Co. BSCC (The) | | | 7.625% | | | 11/7/2024 | | $ | 550,000 | | | $ | 560,686 | |

| | | | | | | | | | | | | | | |

| Brazil 1.48% | | | | | | | | | | | | | | |

| Banks 1.07% | | | | | | | | | | | | | | |

| Banco do Brasil SA† | | | 3.25% | | | 9/30/2026 | | | 850,000 | | | | 783,513 | |

| Itau Unibanco Holding SA† | | | 4.50%

(5 Yr. Treasury CMT + 2.82% | )# | | 11/21/2029 | | | 550,000 | | | | 527,398 | |

| | | | | | | | | | | | | | 1,310,911 | |

| Media 0.41% | | | | | | | | | | | | | | |

| Globo Comunicacao e Participacoes SA† | | | 4.875% | | | 1/22/2030 | | | 600,000 | | | | 503,585 | |

| Total Brazil | | | | | | | | | | | | | 1,814,496 | |

| | | | | | | | | | | | | | | |

| Chile 1.64% | | | | | | | | | | | | | | |

| Chemicals 0.23% | | | | | | | | | | | | | | |

| Sociedad Quimica y Minera de Chile SA† | | | 3.50% | | | 9/10/2051 | | | 380,000 | | | | 280,205 | |

| Electric 0.31% | | | | | | | | | | | | | | |

| Alfa Desarrollo SpA† | | | 4.55% | | | 9/27/2051 | | | 498,177 | | | | 379,435 | |

| Mining 0.41% | | | | | | | | | | | | | | |

| Corp. Nacional del Cobre de Chile† | | | 3.00% | | | 9/30/2029 | | | 575,000 | | | | 503,286 | |

| Oil & Gas 0.69% | | | | | | | | | | | | | | |

| Empresa Nacional del Petroleo† | | | 3.45% | | | 9/16/2031 | | | 1,000,000 | | | | 844,436 | |

| Total Chile | | | | | | | | | | | | | 2,007,362 | |

| | | | | | | | | | | | | | | |

| China 0.79% | | | | | | | | | | | | | | |

| Internet 0.34% | | | | | | | | | | | | | | |

| Prosus NV† | | | 3.832% | | | 2/8/2051 | | | 675,000 | | | | 410,158 | |

| Investment Companies 0.45% | | | | | | | | | | | | | | |

| Huarong Finance 2019 Co. Ltd. | | | 3.375% | | | 2/24/2030 | | | 270,000 | | | | 206,070 | |

| Huarong Finance 2019 Co. Ltd. | | | 5.824%

(3 Mo. LIBOR + 1.13% | ) | | 2/24/2023 | | | 350,000 | | | | 348,895 | |

| | | | | | | | | | | | | | 554,965 | |

| Total China | | | | | | | | | | | | | 965,123 | |

| | | | | | | | | | | | | | | |

| Colombia 0.63% | | | | | | | | | | | | | | |

| Oil & Gas 0.36% | | | | | | | | | | | | | | |

| Ecopetrol SA | | | 5.875% | | | 11/2/2051 | | | 650,000 | | | | 438,095 | |

| 22 | See Notes to Financial Statements. |

Schedule of Investments (continued)

EMERGING MARKETS BOND FUND December 31, 2022

| Investments | | | Interest

Rate | | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Colombia (continued) | | | | | | | | | | | | | | |

| Pipelines 0.27% | | | | | | | | | | | | | | |

| AI Candelaria Spain SA† | | | 5.75% | | | 6/15/2033 | | $ | 437,000 | | | $ | 333,029 | |

| Total Colombia | | | | | | | | | | | | | 771,124 | |

| | | | | | | | | | | | | | | |

| India 1.27% | | | | | | | | | | | | | | |

| Commercial Services 0.30% | | | | | | | | | | | | | | |

| Adani Ports & Special Economic Zone Ltd.† | | | 3.10% | | | 2/2/2031 | | | 500,000 | | | | 367,527 | |

| Oil & Gas 0.63% | | | | | | | | | | | | | | |

| Reliance Industries Ltd.† | | | 2.875% | | | 1/12/2032 | | | 950,000 | | | | 771,083 | |

| Transportation 0.34% | | | | | | | | | | | | | | |

| Indian Railway Finance Corp. Ltd. | | | 2.80% | | | 2/10/2031 | | | 500,000 | | | | 411,060 | |

| Total India | | | | | | | | | | | | | 1,549,670 | |

| | | | | | | | | | | | | | | |

| Indonesia 2.98% | | | | | | | | | | | | | | |

| Coal 0.40% | | | | | | | | | | | | | | |

| Indika Energy Capital IV Pte Ltd. | | | 8.25% | | | 10/22/2025 | | | 500,000 | | | | 494,724 | |

| Electric 1.46% | | | | | | | | | | | | | | |

| Perusahaan Perseroan Persero PT | | | | | | | | | | | | | | |

| Perusahaan Listrik Negara† | | | 3.00% | | | 6/30/2030 | | | 600,000 | | | | 493,223 | |

| Perusahaan Perseroan Persero PT | | | | | | | | | | | | | | |

| Perusahaan Listrik Negara† | | | 4.00% | | | 6/30/2050 | | | 560,000 | | | | 401,798 | |

| Perusahaan Perseroan Persero PT | | | | | | | | | | | | | | |

| Perusahaan Listrik Negara† | | | 4.125% | | | 5/15/2027 | | | 930,000 | | | | 894,934 | |

| | | | | | | | | | | | | | 1,789,955 | |

| Oil & Gas 1.12% | | | | | | | | | | | | | | |

| Pertamina Persero PT† | | | 3.10% | | | 1/21/2030 | | | 900,000 | | | | 785,346 | |

| Pertamina Persero PT† | | | 5.625% | | | 5/20/2043 | | | 630,000 | | | | 580,347 | |

| | | | | | | | | | | | | | 1,365,693 | |

| Total Indonesia | | | | | | | | | | | | | 3,650,372 | |

| | | | | | | | | | | | | | | |

| Israel 0.73% | | | | | | | | | | | | | | |

| Banks | | | | | | | | | | | | | | |

| Bank Hapoalim BM† | | | 3.255%

(5 Yr. Treasury CMT + 2.16% | )# | | 1/21/2032 | | | 480,000 | | | | 415,075 | |

| Bank Leumi Le-Israel BM† | | | 3.275%

(5 Yr. Treasury CMT + 1.63% | )# | | 1/29/2031 | | | 200,000 | | | | 177,921 | |

| Bank Leumi Le-Israel BM† | | | 5.125% | | | 7/27/2027 | | | 300,000 | | | | 298,363 | |

| Total Israel | | | | | | | | | | | | | 891,359 | |

| | See Notes to Financial Statements. | 23 |

Schedule of Investments (continued)

EMERGING MARKETS BOND FUND December 31, 2022

| Investments | | | Interest

Rate | | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Kazakhstan 1.88% | | | | | | | | | | | | |

| Oil & Gas 1.06% | | | | | | | | | | | | | | |

| KazMunayGas National Co. JSC† | | | 4.75% | | | 4/19/2027 | | $ | 700,000 | | | $ | 647,850 | |

| KazMunayGas National Co. JSC† | | | 6.375% | | | 10/24/2048 | | | 300,000 | | | | 248,921 | |

| Tengizchevroil Finance Co. International Ltd.† | | | 3.25% | | | 8/15/2030 | | | 560,000 | | | | 401,615 | |

| | | | | | | | | | | | | | 1,298,386 | |

| Pipelines 0.82% | | | | | | | | | | | | | | |

| KazTransGas JSC† | | | 4.375% | | | 9/26/2027 | | | 1,100,000 | | | | 996,831 | |

| Total Kazakhstan | | | | | | | | | | | | | 2,295,217 | |

| | | | | | | | | | | | | | | |

| Kuwait 0.38% | | | | | | | | | | | | | | |

| Banks | | | | | | | | | | | | | | |

| NBK Tier 1 Financing 2 Ltd.† | | | 4.50%

(6 Yr. Treasury CMT + 2.83% | )# | | – | (a) | | 500,000 | | | | 460,329 | |

| | | | | | | | | | | | | | | |

| Malaysia 2.13% | | | | | | | | | | | | | | |

| Oil & Gas | | | | | | | | | | | | | | |

| Petronas Capital Ltd.† | | | 2.48% | | | 1/28/2032 | | | 1,000,000 | | | | 829,105 | |

| Petronas Capital Ltd.† | | | 3.404% | | | 4/28/2061 | | | 1,300,000 | | | | 902,763 | |

| Petronas Energy Canada Ltd.† | | | 2.112% | | | 3/23/2028 | | | 1,000,000 | | | | 875,790 | |

| Total Malaysia | | | | | | | | | | | | | 2,607,658 | |

| | | | | | | | | | | | | | | |

| Mexico 4.13% | | | | | | | | | | | | | | |

| Banks 0.29% | | | | | | | | | | | | | | |

| Banco Nacional de Comercio Exterior SNC† | | 2.72%

(5 Yr. Treasury CMT + 2.00% | )# | | 8/11/2031 | | | 420,000 | | | | 351,931 | |

| Electric 0.83% | | | | | | | | | | | | | | |

| Comision Federal de Electricidad† | | | 3.348% | | | 2/9/2031 | | | 625,000 | | | | 490,688 | |

| Comision Federal de Electricidad† | | | 4.677% | | | 2/9/2051 | | | 800,000 | | | | 524,440 | |

| | | | | | | | | | | | | | 1,015,128 | |

| Oil & Gas 3.01% | | | | | | | | | | | | | | |

| Petroleos Mexicanos | | | 5.35% | | | 2/12/2028 | | | 1,250,000 | | | | 1,054,731 | |

| Petroleos Mexicanos | | | 6.50% | | | 6/2/2041 | | | 1,175,000 | | | | 767,422 | |

| Petroleos Mexicanos | | | 6.70% | | | 2/16/2032 | | | 1,652,000 | | | | 1,300,458 | |

| Petroleos Mexicanos | | | 6.75% | | | 9/21/2047 | | | 880,000 | | | | 563,449 | |

| | | | | | | | | | | | | | 3,686,060 | |

| Total Mexico | | | | | | | | | | | | | 5,053,119 | |

| | | | | | | | | | | | | | | |

| Morocco 0.22% | | | | | | | | | | | | | | |

| Chemicals | | | | | | | | | | | | | | |

| OCP SA† | | | 5.125% | | | 6/23/2051 | | | 350,000 | | | | 267,010 | |

| 24 | See Notes to Financial Statements. |

Schedule of Investments (continued)

EMERGING MARKETS BOND FUND December 31, 2022

| Investments | | | Interest

Rate | | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Oman 0.94% | | | | | | | | | | | | |

| Electric | | | | | | | | | | | | |

| OmGrid Funding Ltd.† | | | 5.196% | | | 5/16/2027 | | $ | 1,200,000 | | | $ | 1,154,700 | |

| | | | | | | | | | | | | | | |

| Panama 0.68% | | | | | | | | | | | | | | |

| Banks 0.33% | | | | | | | | | | | | | | |

| Banco Nacional de Panama† | | | 2.50% | | | 8/11/2030 | | | 500,000 | | | | 401,638 | |

| Multi-National 0.35% | | | | | | | | | | | | | | |

| Banco Latinoamericano de Comercio Exterior SA† | | | 2.375% | | | 9/14/2025 | | | 478,000 | | | | 436,997 | |

| Total Panama | | | | | | | | | | | | | 838,635 | |

| | | | | | | | | | | | | | | |

| Paraguay 0.22% | | | | | | | | | | | | | | |

| Banks | | | | | | | | | | | | | | |

| Banco Continental SAECA† | | | 2.75% | | | 12/10/2025 | | | 300,000 | | | | 268,760 | |

| | | | | | | | | | | | | | | |

| Peru 0.44% | | | | | | | | | | | | | | |

| Banks | | | | | | | | | | | | | | |

| Banco Internacional del Peru SAA Interbank† | | | 3.25% | | | 10/4/2026 | | | 590,000 | | | | 537,760 | |

| | | | | | | | | | | | | | | |

| Qatar 1.47% | | | | | | | | | | | | | | |

| Oil & Gas | | | | | | | | | | | | | | |

| Qatar Energy† | | | 2.25% | | | 7/12/2031 | | | 1,500,000 | | | | 1,245,272 | |

| QatarEnergy Trading LLC† | | | 3.30% | | | 7/12/2051 | | | 750,000 | | | | 555,600 | |

| Total Qatar | | | | | | | | | | | | | 1,800,872 | |

| | | | | | | | | | | | | | | |

| Saudi Arabia 1.40% | | | | | | | | | | | | | | |

| Electric 0.42% | | | | | | | | | | | | | | |

| Acwa Power Management and Investments One Ltd.† | | | 5.95% | | | 12/15/2039 | | | 548,900 | | | | 513,496 | |

| Oil & Gas 0.51% | | | | | | | | | | | | | | |

| SAGlobal Sukuk Ltd.† | | | 1.602% | | | 6/17/2026 | | | 240,000 | | | | 214,802 | |

| Saudi Arabian Oil Co. | | | 2.25% | | | 11/24/2030 | | | 300,000 | | | | 247,874 | |

| Saudi Arabian Oil Co.† | | | 3.25% | | | 11/24/2050 | | | 225,000 | | | | 159,094 | |

| | | | | | | | | | | | | | 621,770 | |

| Pipelines 0.47% | | | | | | | | | | | | | | |

| EIG Pearl Holdings Sarl† | | | 3.545% | | | 8/31/2036 | | | 685,000 | | | | 576,518 | |

| Total Saudi Arabia | | | | | | | | | | | | | 1,711,784 | |

| | | | | | | | | | | | | | | |

| South Africa 1.50% | | | | | | | | | | | | | | |

| Electric | | | | | | | | | | | | | | |

| Eskom Holdings SOC Ltd. | | | 6.35% | | | 8/10/2028 | | | 700,000 | | | | 649,775 | |

| Eskom Holdings SOC Ltd.† | | | 7.125% | | | 2/11/2025 | | | 1,300,000 | | | | 1,187,029 | |

| Total South Africa | | | | | | | | | | | | | 1,836,804 | |

| | See Notes to Financial Statements. | 25 |

Schedule of Investments (continued)

EMERGING MARKETS BOND FUND December 31, 2022

| Investments | | | Interest

Rate | | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| South Korea 1.51% | | | | | | | | | | | | | | |

| Electric 0.39% | | | | | | | | | | | | | | |

| Korea East-West Power Co. Ltd.† | | | 3.60% | | | 5/6/2025 | | $ | 495,000 | | | $ | 479,108 | |

| Energy-Alternate Sources 0.40% | | | | | | | | | | | | | | |

| Hanwha Energy USA Holdings Corp.† | | | 4.125% | | | 7/5/2025 | | | 500,000 | | | | 485,479 | |

| Oil & Gas 0.72% | | | | | | | | | | | | | | |

| Korea National Oil Corp.† | | | 2.125% | | | 4/18/2027 | | | 1,000,000 | | | | 882,202 | |

| Total South Korea | | | | | | | | | | | | | 1,846,789 | |

| | | | | | | | | | | | | | | |

| Supranational 0.37% | | | | | | | | | | | | | | |

| Multi-National | | | | | | | | | | | | | | |

| African Export-Import Bank (The)† | | | 2.634% | | | 5/17/2026 | | | 500,000 | | | | 450,000 | |

| | | | | | | | | | | | | | | |

| Thailand 0.64% | | | | | | | | | | | | | | |

| Oil & Gas | | | | | | | | | | | | | | |

| Thaioil Treasury Center Co. Ltd.† | | | 3.50% | | | 10/17/2049 | | | 1,300,000 | | | | 780,769 | |

| | | | | | | | | | | | | | | |

| United Arab Emirates 2.59% | | | | | | | | | | | | | | |

| Commercial Services 0.92% | | | | | | | | | | | | | | |

| DP World Crescent Ltd. | | | 3.875% | | | 7/18/2029 | | | 1,200,000 | | | | 1,125,089 | |

| Energy-Alternate Sources 0.44% | | | | | | | | | | | | | | |

| Sweihan PV Power Co. PJSC† | | | 3.625% | | | 1/31/2049 | | | 665,451 | | | | 536,593 | |

| Investment Companies 0.26% | | | | | | | | | | | | | | |

| MDGH GMTN RSC Ltd.† | | | 5.50% | | | 4/28/2033 | | | 300,000 | | | | 317,842 | |

| Pipelines 0.63% | | | | | | | | | | | | | | |

| Galaxy Pipeline Assets Bidco Ltd.† | | | 3.25% | | | 9/30/2040 | | | 1,000,000 | | | | 777,604 | |

| Sovereign 0.34% | | | | | | | | | | | | | | |

| Finance Department Government of Sharjah | | | 3.625% | | | 3/10/2033 | | | 500,000 | | | | 416,305 | |

| Total United Arab Emirates | | | | | | | | | | | | | 3,173,433 | |

| | | | | | | | | | | | | | | |

| United States 0.17% | | | | | | | | | | | | | | |

| Oil & Gas | | | | | | | | | | | | | | |

| Citgo Holding, Inc.† | | | 9.25% | | | 8/1/2024 | | | 208,000 | | | | 207,944 | |

| Total Corporate Bonds (cost $43,344,531) | | | | | | | | | | | | | 37,501,775 | |

| | | | | | | | | | | | | | | |

| FOREIGN GOVERNMENT OBLIGATIONS 66.92% | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Angola 1.73% | | | | | | | | | | | | | | |

| Angolan Government International Bond | | | 8.75% | | | 4/14/2032 | | | 200,000 | | | | 173,680 | |

| Angolan Government International Bond† | | | 9.125% | | | 11/26/2049 | | | 850,000 | | | | 666,315 | |

| Republic of Angola† | | | 8.25% | | | 5/9/2028 | | | 1,400,000 | | | | 1,280,440 | |

| Total Angola | | | | | | | | | | | | | 2,120,435 | |

| 26 | See Notes to Financial Statements. |

Schedule of Investments (continued)

EMERGING MARKETS BOND FUND December 31, 2022

| Investments | | | Interest

Rate | | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Argentina 1.66% | | | | | | | | | | | | |

| Argentine Republic Government International Bond | | | 1.50% | | | 7/9/2035 | | $ | 2,950,000 | | | $ | 755,630 | |

| Argentine Republic Government International Bond | | | 3.50% | | | 7/9/2041 | | | 2,150,000 | | | | 611,867 | |

| Argentine Republic Government International Bond | | | 3.875% | | | 1/9/2038 | | | 2,077,038 | | | | 662,228 | |

| Total Argentina | | | | | | | | | | | | | 2,029,725 | |

| | | | | | | | | | | | | | | |

| Bahrain 2.31% | | | | | | | | | | | | | | |

| Kingdom of Bahrain† | | | 5.45% | | | 9/16/2032 | | | 1,550,000 | | | | 1,373,847 | |

| Kingdom of Bahrain† | | | 6.00% | | | 9/19/2044 | | | 300,000 | | | | 235,225 | |

| Kingdom of Bahrain† | | | 7.00% | | | 1/26/2026 | | | 1,180,000 | | | | 1,212,890 | |

| Total Bahrain | | | | | | | | | | | | | 2,821,962 | |

| | | | | | | | | | | | | | | |

| Bermuda 0.22% | | | | | | | | | | | | | | |

| Bermuda Government International Bond† | | | 2.375% | | | 8/20/2030 | | | 320,000 | | | | 271,532 | |

| | | | | | | | | | | | | | | |

| Brazil 2.22% | | | | | | | | | | | | | | |

| Federal Republic of Brazil | | | 3.75% | | | 9/12/2031 | | | 1,650,000 | | | | 1,390,573 | |

| Federal Republic of Brazil | | | 4.75% | | | 1/14/2050 | | | 1,431,000 | | | | 1,007,161 | |

| Federal Republic of Brazil | | | 5.00% | | | 1/27/2045 | | | 436,000 | | | | 324,450 | |

| Total Brazil | | | | | | | | | | | | | 2,722,184 | |

| | | | | | | | | | | | | | | |

| Cayman Islands 1.36% | | | | | | | | | | | | | | |

| KSA Sukuk Ltd.† | | | 5.268% | | | 10/25/2028 | | | 1,600,000 | | | | 1,665,062 | |

| | | | | | | | | | | | | | | |

| Chile 1.73% | | | | | | | | | | | | | | |

| Chile Government International Bond | | | 2.45% | | | 1/31/2031 | | | 850,000 | | | | 707,351 | |

| Chile Government International Bond | | | 3.10% | | | 5/7/2041 | | | 1,050,000 | | | | 757,929 | |

| Chile Government International Bond | | | 3.50% | | | 1/25/2050 | | | 900,000 | | | | 652,386 | |

| Total Chile | | | | | | | | | | | | | 2,117,666 | |

| | | | | | | | | | | | | | | |

| Colombia 2.80% | | | | | | | | | | | | | | |

| Republic of Colombia | | | 3.00% | | | 1/30/2030 | | | 505,000 | | | | 387,758 | |

| Republic of Colombia | | | 3.25% | | | 4/22/2032 | | | 875,000 | | | | 639,142 | |

| Republic of Colombia | | | 3.875% | | | 4/25/2027 | | | 860,000 | | | | 764,069 | |

| Republic of Colombia | | | 4.125% | | | 5/15/2051 | | | 750,000 | | | | 451,379 | |

| Republic of Colombia | | | 5.00% | | | 6/15/2045 | | | 1,735,000 | | | | 1,186,837 | |

| Total Colombia | | | | | | | | | | | | | 3,429,185 | |

| | | | | | | | | | | | | | | |

| Costa Rica 0.81% | | | | | | | | | | | | | | |

| Costa Rica Government† | | | 5.625% | | | 4/30/2043 | | | 862,000 | | | | 709,294 | |

| Costa Rica Government† | | | 6.125% | | | 2/19/2031 | | | 285,000 | | | | 277,843 | |

| Total Costa Rica | | | | | | | | | | | | | 987,137 | |

| | See Notes to Financial Statements. | 27 |

Schedule of Investments (continued)

EMERGING MARKETS BOND FUND December 31, 2022

| Investments | | | Interest

Rate | | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Dominican Republic 3.33% | | | | | | | | | | | | | | |

| Dominican Republic† | | | 4.50% | | | 1/30/2030 | | $ | 1,200,000 | | | $ | 1,026,083 | |

| Dominican Republic† | | | 5.30% | | | 1/21/2041 | | | 750,000 | | | | 581,530 | |

| Dominican Republic† | | | 5.875% | | | 1/30/2060 | | | 970,000 | | | | 715,055 | |

| Dominican Republic† | | | 5.95% | | | 1/25/2027 | | | 1,225,000 | | | | 1,202,963 | |

| Dominican Republic International Bond† | | | 5.50% | | | 2/22/2029 | | | 600,000 | | | | 554,317 | |

| Total Dominican Republic | | | | | | | | | | | | | 4,079,948 | |

| | | | | | | | | | | | | | | |

| Ecuador 1.93% | | | | | | | | | | | | | | |

| Ecuador Government International Bond† | | | 1.50% | | | 7/31/2040 | | | 1,921,077 | | | | 791,160 | |

| Ecuador Government International Bond† | | | 2.50% | | | 7/31/2035 | | | 1,275,000 | | | | 592,541 | |

| Ecuador Government International Bond† | | | 5.50% | | | 7/31/2030 | | | 1,507,550 | | | | 976,242 | |

| Total Ecuador | | | | | | | | | | | | | 2,359,943 | |

| | | | | | | | | | | | | | | |

| Egypt 2.96% | | | | | | | | | | | | | | |

| Republic of Egypt† | | | 3.875% | | | 2/16/2026 | | | 2,400,000 | | | | 1,987,608 | |

| Republic of Egypt† | | | 7.30% | | | 9/30/2033 | | | 1,000,000 | | | | 712,480 | |

| Republic of Egypt† | | | 7.903% | | | 2/21/2048 | | | 920,000 | | | | 584,669 | |

| Republic of Egypt† | | | 8.75% | | | 9/30/2051 | | | 500,000 | | | | 337,600 | |

| Total Egypt | | | | | | | | | | | | | 3,622,357 | |

| | | | | | | | | | | | | | | |

| El Salvador 0.77% | | | | | | | | | | | | | | |

| El Salvador Government International Bond† | | | 8.25% | | | 4/10/2032 | | | 1,575,000 | | | | 701,233 | |

| Republic of EI Salvador† | | | 6.375% | | | 1/18/2027 | | | 550,000 | | | | 246,125 | |

| Total El Salvador | | | | | | | | | | | | | 947,358 | |

| | | | | | | | | | | | | | | |

| Gabon 0.65% | | | | | | | | | | | | | | |

| Gabon Government International Bond† | | | 7.00% | | | 11/24/2031 | | | 967,000 | | | | 795,261 | |

| | | | | | | | | | | | | | | |

| Ghana 1.10% | | | | | | | | | | | | | | |

| Ghana Government International Bond | | | 8.627% | | | 6/16/2049 | | | 725,000 | | | | 256,382 | |

| Republic of Ghana† | | | 6.375% | | | 2/11/2027 | | | 1,625,000 | | | | 629,736 | |

| Republic of Ghana† | | | 7.625% | | | 5/16/2029 | | | 730,000 | | | | 275,648 | |

| Republic of Ghana† | | | 8.625% | | | 4/7/2034 | | | 500,000 | | | | 182,800 | |

| Total Ghana | | | | | | | | | | | | | 1,344,566 | |

| | | | | | | | | | | | | | | |

| Guatemala 0.95% | | | | | | | | | | | | | | |

| Republic of Guatemala† | | | 4.375% | | | 6/5/2027 | | | 625,000 | | | | 593,773 | |

| Republic of Guatemala† | | | 6.125% | | | 6/1/2050 | | | 600,000 | | | | 566,858 | |

| Total Guatemala | | | | | | | | | | | | | 1,160,631 | |

| | | | | | | | | | | | | | | |

| Indonesia 2.52% | | | | | | | | | | | | | | |

| Indonesia Government International Bond | | | 1.85% | | | 3/12/2031 | | | 1,600,000 | | | | 1,296,429 | |