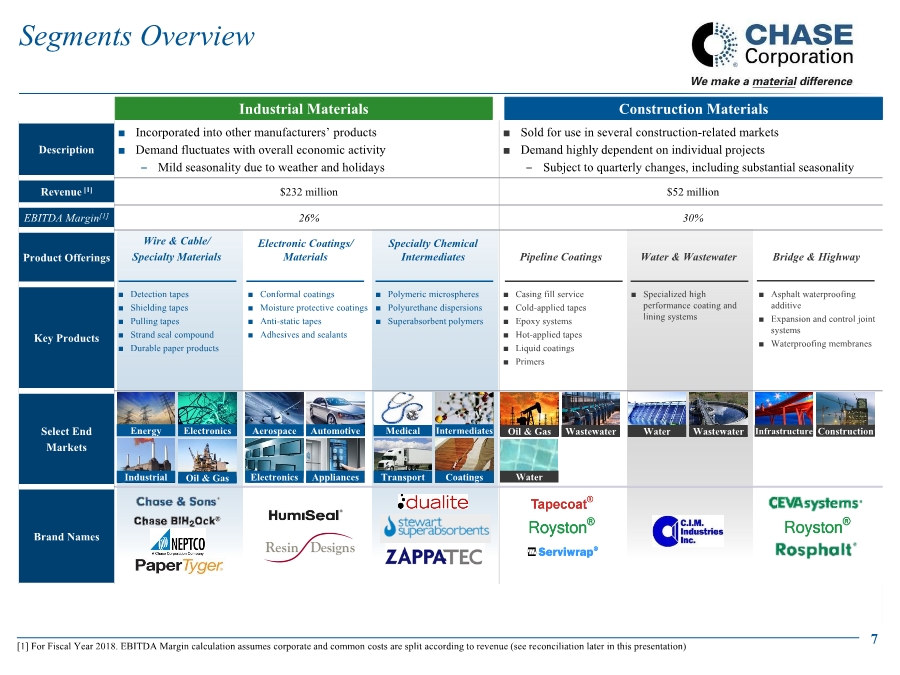

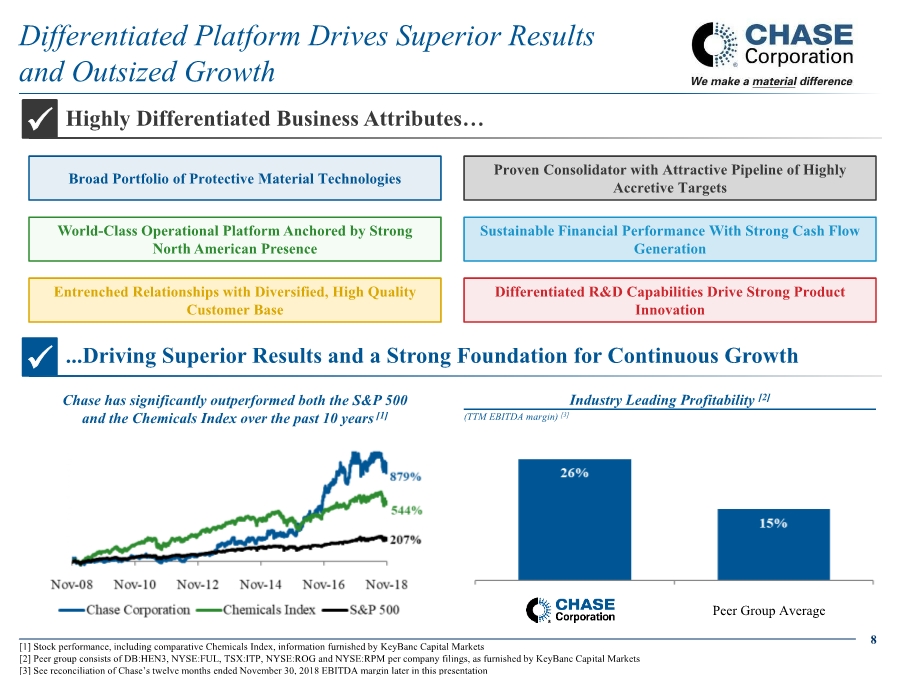

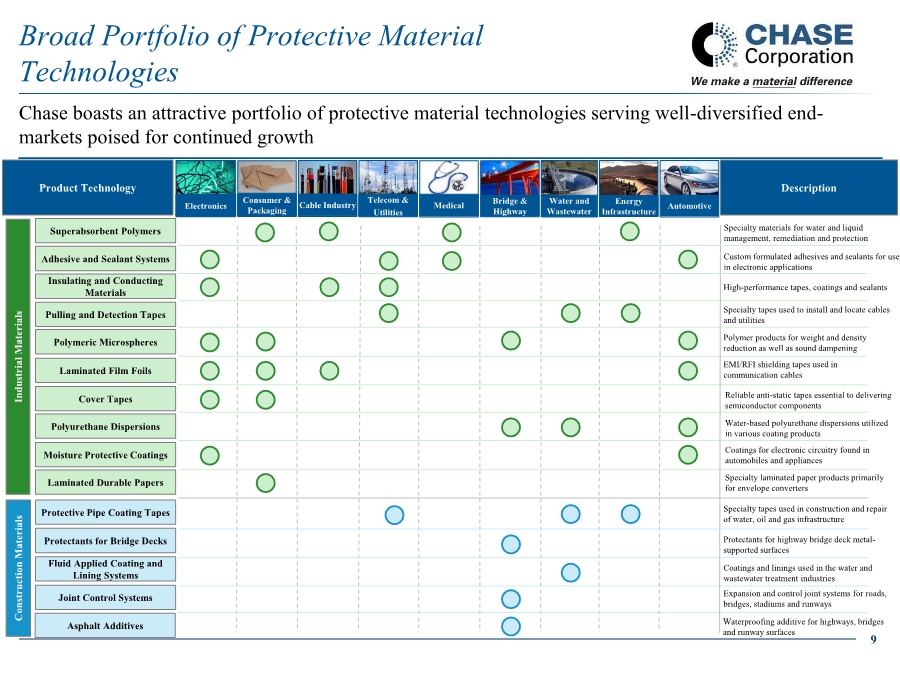

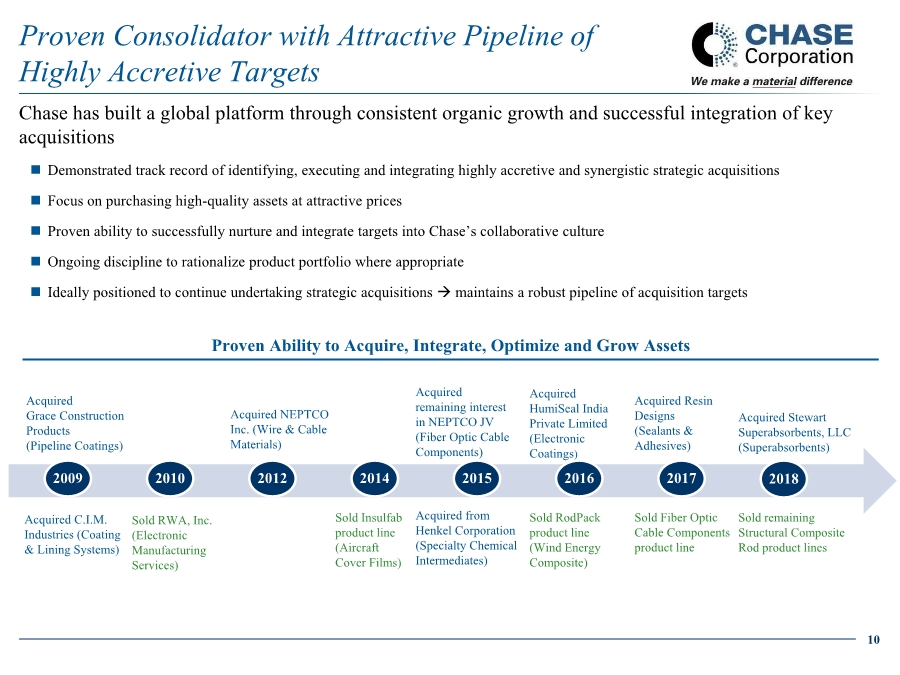

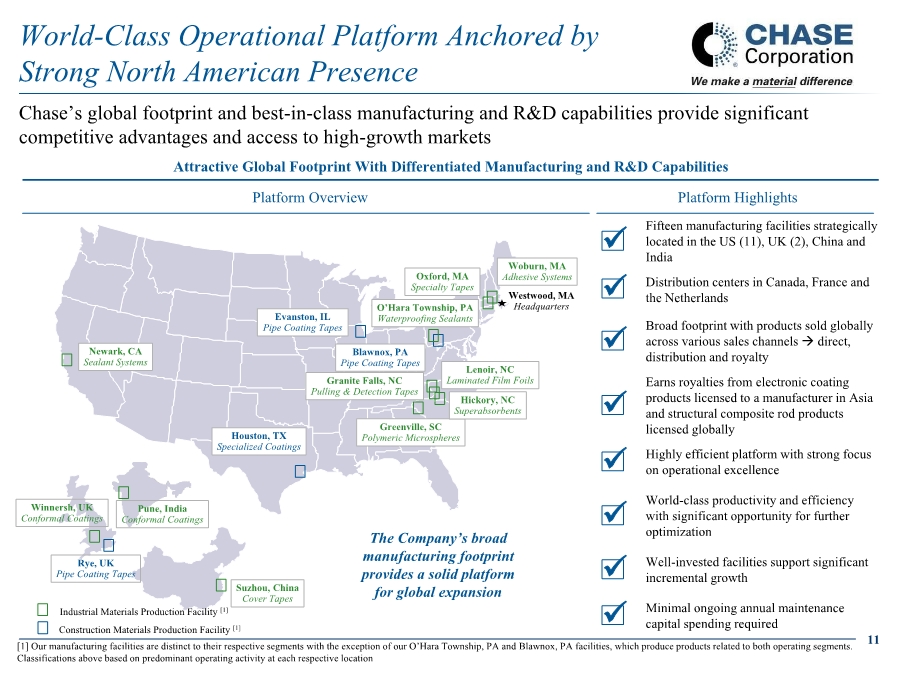

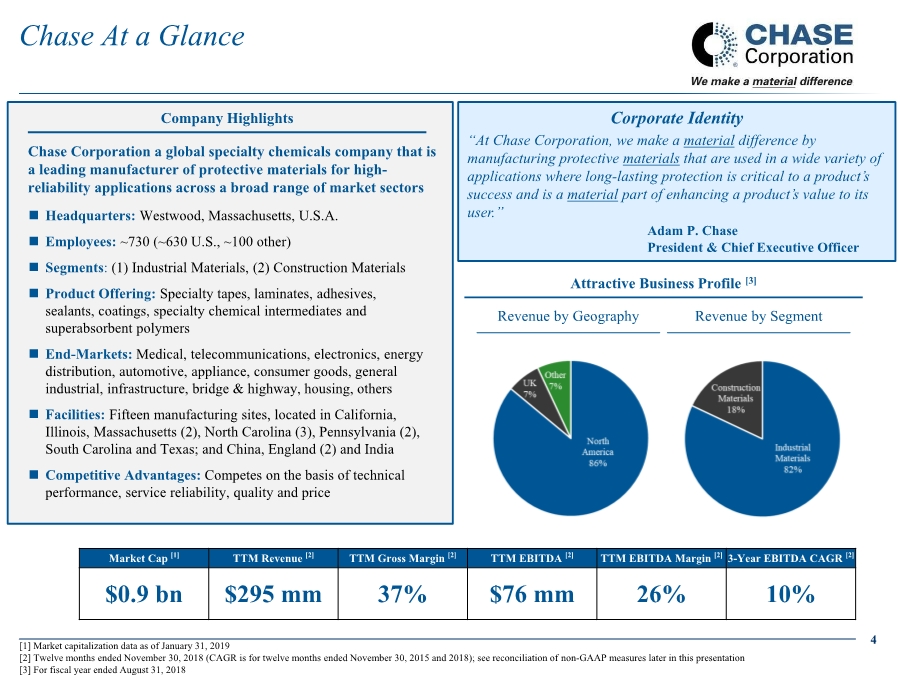

| 4 Chase At a Glance [1] Market capitalization data as of January 31, 2019 [2] Twelve months ended November 30, 2018 (CAGR is for twelve months ended November 30, 2015 and 2018); see reconciliation of non-GAAP measures later in this presentation [3] For fiscal year ended August 31, 2018 Chase Corporation a global specialty chemicals company that is a leading manufacturer of protective materials for high- reliability applications across a broad range of market sectors ◼ Headquarters: Westwood, Massachusetts, U.S.A. ◼ Employees: ~730 (~630 U.S., ~100 other) ◼ Segments: (1) Industrial Materials, (2) Construction Materials ◼ Product Offering: Specialty tapes, laminates, adhesives, sealants, coatings, specialty chemical intermediates and superabsorbent polymers ◼ End-Markets: Medical, telecommunications, electronics, energy distribution, automotive, appliance, consumer goods, general industrial, infrastructure, bridge & highway, housing, others ◼ Facilities: Fifteen manufacturing sites, located in California, Illinois, Massachusetts (2), North Carolina (3), Pennsylvania (2), South Carolina and Texas; and China, England (2) and India ◼ Competitive Advantages: Competes on the basis of technical performance, service reliability, quality and price Company Highlights Attractive Business Profile [3] Revenue by Geography Revenue by Segment Corporate Identity “At Chase Corporation, we make a material difference by manufacturing protective materials that are used in a wide variety of applications where long-lasting protection is critical to a product’s success and is a material part of enhancing a product’s value to its user.” Adam P. Chase President & Chief Executive Officer Market Cap [1] TTM Revenue [2] TTM Gross Margin [2] TTM EBITDA [2] TTM EBITDA Margin [2] 3-Year EBITDA CAGR [2] $0.9 bn $295 mm 37% $76 mm 26% 10% |