The information in this preliminary pricing supplement is not complete and may be changed. A registration statement relating to these securities has been filed with the Securities and Exchange Commission. This preliminary pricing supplement and the accompanying product supplement, underlying supplement, prospectus supplement and prospectus are not an offer to sell these securities, nor are they soliciting an offer to buy these securities, in any state where the offer or sale is not permitted. SUBJECT TO COMPLETION, DATED OCTOBER 15, 2020 | |

| Citigroup Global Markets Holdings Inc. | October----, 2020 Medium-Term Senior Notes, Series N Pricing Supplement No. 2020-USNCH5693 Filed Pursuant to Rule 424(b)(2) |

| Registration Statement Nos. 333-224495 and 333-224495-03 | |

Equity Linked Securities Linked to the Worst Performing of the S&P 500® Index and the Nasdaq-100 Index® Due October 20, 2021

| ▪ | The securities offered by this pricing supplement are unsecured debt securities issued by Citigroup Global Markets Holdings Inc. and guaranteed by Citigroup Inc. The securities offer periodic coupon payments at an annualized rate that is generally higher than the yield on our conventional debt securities of the same maturity. In exchange for this higher yield, you must be willing to accept the risk that, if a downside event (as described below) occurs, the value of what you receive at maturity may be significantly less than the stated principal amount of your securities. The risk will depend solely on the performance of the worst performing of the underlyings specified below. |

| ▪ | You will be subject to risks associated with each of the underlyings and will be negatively affected by adverse movements in any one of the underlyings. Although you will have downside exposure to the worst performing underlying, you will not receive dividends with respect to any underlying or participate in any appreciation of any underlying. |

| ▪ | Investors in the securities must be willing to accept (i) an investment that may have limited or no liquidity and (ii) the risk of not receiving any payments due under the securities if we and Citigroup Inc. default on our obligations. All payments on the securities are subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc. |

| KEY TERMS | |

| Issuer: | Citigroup Global Markets Holdings Inc., a wholly owned subsidiary of Citigroup Inc. |

| Guarantee: | All payments due on the securities are fully and unconditionally guaranteed by Citigroup Inc. |

| Underlyings: | Underlying | Initial underlying value* | Downside threshold value** |

| S&P 500® Index | 3,488.67 | 2,790.936 | |

| Nasdaq-100 Index® | 11,985.36 | 9,588.288 | |

* For each underlying, its closing value on the strike date ** For each underlying, 80% of its initial underlying value | |||

| Stated principal amount: | $1,000 per security |

| Strike date: | October 14, 2020 |

| Pricing date: | October 15, 2020 |

| Issue date: | October 20, 2020 |

| Valuation date: | October 15, 2021, subject to postponement if such date is not a scheduled trading day or certain market disruption events occur |

| Maturity date: | October 20, 2021 |

| Coupon payment dates: | November 20, 2020, December 21, 2020, January 20, 2021, February 22, 2021, March 22, 2021, April 20, 2021, May 20, 2021, June 21, 2021, July 20, 2021, August 20, 2021, September 20, 2021 and the maturity date |

| Coupon payments: | On each coupon payment date, the securities will pay a coupon equal to 0.5333% of the stated principal amount of the securities (equivalent to a coupon rate of approximately 6.40% per annum) |

| Payment at maturity: | For each $1,000 stated principal amount security you hold at maturity, you will receive the final coupon payment plus: ▪ If a downside event does not occur: $1,000 ▪ If a downside event occurs: $1,000 + [$1,000 × the buffer rate × (the underlying return of the worst performing underlying + the buffer percentage)] If a downside event occurs, which means that the worst performing underlying has depreciated from its initial underlying value by more than the buffer percentage, you will lose more than 1% of the stated principal amount of your securities at maturity for every 1% by which that depreciation exceeds the buffer percentage. Accordingly, the lower the final underlying value of the worst performing underlying, the less benefit you will receive from the buffer. |

| Downside event: | A downside event will occur if the final underlying value of the worst performing underlying is less than its downside threshold value |

| Buffer percentage: | 20% |

| Buffer rate: | The initial underlying value of the worst performing underlying divided by its downside threshold value, which is 125% |

| Listing: | The securities will not be listed on any securities exchange |

| Underwriter: | Citigroup Global Markets Inc. (“CGMI”), an affiliate of the issuer, acting as principal |

| Underwriting fee and issue price: | Issue price(1) | Underwriting fee(2) | Proceeds to issuer |

| Per security: | $1,000 | — | $1,000 |

| Total: | $ | — | $ |

(Key Terms continued on next page)

(1) Citigroup Global Markets Holdings Inc. currently expects that the estimated value of the securities on the pricing date will be at least $945.00 per security, which will be less than the issue price. The estimated value of the securities is based on CGMI’s proprietary pricing models and our internal funding rate. It is not an indication of actual profit to CGMI or other of our affiliates, nor is it an indication of the price, if any, at which CGMI or any other person may be willing to buy the securities from you at any time after issuance. See “Valuation of the Securities” in this pricing supplement.

(2) For more information on the distribution of the securities, see “Supplemental Plan of Distribution” in this pricing supplement. CGMI and its affiliates may profit from expected hedging activity related to this offering, even if the value of the securities declines. See “Use of Proceeds and Hedging” in the accompanying prospectus.

Investing in the securities involves risks not associated with an investment in conventional debt securities. See “Summary Risk Factors” beginning on page PS-5.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities or determined that this pricing supplement and the accompanying product supplement, underlying supplement, prospectus supplement and prospectus are truthful or complete. Any representation to the contrary is a criminal offense. You should read this pricing supplement together with the accompanying product supplement, underlying supplement, prospectus supplement and prospectus, which can be accessed via the hyperlinks below:

Product Supplement No. EA-02-08 dated February 15, 2019 Underlying Supplement No. 8 dated February 21, 2019

Prospectus Supplement and Prospectus each dated May 14, 2018

The securities are not bank deposits and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency, nor are they obligations of, or guaranteed by, a bank.

| Citigroup Global Markets Holdings Inc. |

| KEY TERMS (continued) | |

| Final underlying value: | For each underlying, its closing value on the valuation date |

| Worst performing underlying: | The underlying with the lowest underlying return |

| Underlying return: | For each underlying, (i) its final underlying value minus its initial underlying value, divided by (ii) its initial underlying value |

| CUSIP / ISIN: | 17328WWW4 / US17328WWW45 |

Additional Information

General. The terms of the securities are set forth in the accompanying product supplement, prospectus supplement and prospectus, as supplemented by this pricing supplement. The accompanying product supplement, prospectus supplement and prospectus contain important disclosures that are not repeated in this pricing supplement. For example, the accompanying product supplement contains important information about how the closing value of each underlying will be determined and about adjustments that may be made to the terms of the securities upon the occurrence of market disruption events and other specified events with respect to each underlying. The accompanying underlying supplement contains information about each underlying that is not repeated in this pricing supplement. It is important that you read the accompanying product supplement, underlying supplement, prospectus supplement and prospectus together with this pricing supplement in deciding whether to invest in the securities. Certain terms used but not defined in this pricing supplement are defined in the accompanying product supplement.

Prospectus. The first sentence of “Description of Debt Securities—Events of Default and Defaults” in the accompanying prospectus shall be amended to read in its entirety as follows:

Events of default under the indenture are:

| · | failure of Citigroup Global Markets Holdings or Citigroup to pay required interest on any debt security of such series for 30 days; |

| · | failure of Citigroup Global Markets Holdings or Citigroup to pay principal, other than a scheduled installment payment to a sinking fund, on any debt security of such series for 30 days; |

| · | failure of Citigroup Global Markets Holdings or Citigroup to make any required scheduled installment payment to a sinking fund for 30 days on debt securities of such series; |

| · | failure of Citigroup Global Markets Holdings to perform for 90 days after notice any other covenant in the indenture applicable to it other than a covenant included in the indenture solely for the benefit of a series of debt securities other than such series; and |

| · | certain events of bankruptcy or insolvency of Citigroup Global Markets Holdings, whether voluntary or not (Section 6.01). |

| PS-2 |

| Citigroup Global Markets Holdings Inc. |

Hypothetical Examples of the Payment at Maturity on the Securities

The table below indicates what your payment at maturity would be for various hypothetical underlying returns of the worst performing underlying. Your actual payment at maturity will depend on the actual final underlying value of the worst performing underlying.

| Hypothetical Underlying Return of Worst Performing Underlying | Hypothetical Payment at Maturity(1) |

| 50.00% | $1,005.333 |

| 20.00% | $1,005.333 |

| 10.00% | $1,005.333 |

| 0.00% | $1,005.333 |

| -10.00% | $1,005.333 |

| -20.00% | $1,005.333 |

| -20.01% | $1,005.208 |

| -30.00% | $880.333 |

| -40.00% | $755.333 |

| -50.00% | $630.333 |

| -60.00% | $505.333 |

| -70.00% | $380.333 |

| -80.00% | $255.333 |

| -90.00% | $130.333 |

| -100.00% | $5.333 |

(1) Includes final coupon payment. Each security has a stated principal amount of $1,000.00.

The examples below illustrate how to determine the payment at maturity on the securities, assuming the various hypothetical final underlying values indicated below. The outcomes illustrated below are not exhaustive, and your actual payment at maturity on the securities may differ from any example illustrated below.

The examples below are based on the following hypothetical values and do not reflect the actual initial underlying values or downside threshold values of the underlyings. For the actual initial underlying value and downside threshold value of each underlying, see the cover page of this pricing supplement. We have used these hypothetical values, rather than the actual values, to simplify the calculations and aid understanding of how the securities work. However, you should understand that the actual payments on the securities will be calculated based on the actual initial underlying value and downside threshold value of each underlying, and not the hypothetical values indicated below.

| Underlying | Hypothetical initial underlying value | Hypothetical downside threshold value |

| S&P 500® Index | 100 | 80 (80% of its hypothetical initial underlying value) |

| Nasdaq-100 Index® | 100 | 80 (80% of its hypothetical initial underlying value) |

The hypothetical examples below illustrate the calculation of the payment at maturity on the securities, assuming that the final underlying values of the underlyings are as indicated below.

| Hypothetical final underlying value of S&P 500® Index | Hypothetical final underlying value of Nasdaq-100 Index® | Hypothetical payment at maturity per $1,000 security | |

| Example 1 | 130 (underlying return = (130 – 100) / 100 = 30%) | 120 (underlying return = (120 – 100) / 100 = 20%) | $1,005.333 |

| Example 2 | 70 (underlying return = (70 – 100) / 100 = -30%) | 90 (underlying return = (90 – 100) / 100 = -10%) | $880.333 |

| Example 3 | 140 (underlying return = (140 – 100) / 100 = 40%) | 30 (underlying return = (30 – 100) / 100 = -70%) | $380.333 |

| PS-3 |

| Citigroup Global Markets Holdings Inc. |

Example 1: In this example, the Nasdaq-100 Index® has the lowest underlying return and, therefore, is the worst performing underlying. In this scenario, the final underlying value of the worst performing underlying is greater than its downside threshold value and, as a result, a downside event does not occur. Accordingly, at maturity, you would receive the $1,000 stated principal amount of the securities plus the final coupon payment. You would not participate in the appreciation of any of the underlyings.

Example 2: In this example, the S&P 500® Index has the lowest underlying return and, therefore, is the worst performing underlying. In this scenario, the final underlying value of the worst performing underlying is less than its downside threshold value and, as a result, a downside event occurs. Accordingly, at maturity, you would receive a payment per security calculated as follows:

Payment at maturity = $1,000 + [$1,000 × the buffer rate × (the underlying return of the worst performing underlying + the buffer percentage)] + the final coupon payment

= $1,000 + [$1,000 × 125% × (-30% + 20%)] + $5.333

= $1,000 + [$1,000 × 125% × (-10%)] + $5.333

= $1,000 + -$125.00 + $5.333

= $880.333

In this scenario, because the final underlying value of the worst performing underlying is less than its downside threshold value, you would lose a portion of your investment in the securities. Your payment at maturity (excluding the final coupon payment) would reflect a loss of more than 1% (based on the buffer rate) of the stated principal amount of your securities for every 1% by which the depreciation of the worst performing underlying has exceeded the buffer percentage.

Example 3: In this example, the Nasdaq-100 Index® has the lowest underlying return and, therefore, is the worst performing underlying. In this scenario, the final underlying value of the worst performing underlying is less than its downside threshold value and, as a result, a downside event occurs. Accordingly, at maturity, you would receive a payment per security calculated as follows:

Payment at maturity = $1,000 + [$1,000 × the buffer rate × (the underlying return of the worst performing underlying + the buffer percentage)] + the final coupon payment

= $1,000 + [$1,000 × 125% × (-70% + 20%)] + $5.333

= $1,000 + [$1,000 × 125% × (-50%)] + $5.333

= $1,000 + -$625 + $5.333

= $380.333

In this scenario, because the final underlying value of the worst performing underlying is less than its downside threshold value, you would lose a portion of your investment in the securities. Your payment at maturity (excluding the final coupon payment) would reflect a loss of more than 1% (based on the buffer rate) of the stated principal amount of your securities for every 1% by which the depreciation of the worst performing underlying has exceeded the buffer percentage. A comparison of this example with the previous example illustrates the diminishing benefit of the buffer the lower the final underlying value of the worst performing underlying.

| PS-4 |

| Citigroup Global Markets Holdings Inc. |

Summary Risk Factors

An investment in the securities is significantly riskier than an investment in conventional debt securities. The securities are subject to all of the risks associated with an investment in our conventional debt securities (guaranteed by Citigroup Inc.), including the risk that we and Citigroup Inc. may default on our obligations under the securities, and are also subject to risks associated with each underlying. Accordingly, the securities are suitable only for investors who are capable of understanding the complexities and risks of the securities. You should consult your own financial, tax and legal advisors as to the risks of an investment in the securities and the suitability of the securities in light of your particular circumstances.

The following is a summary of certain key risk factors for investors in the securities. You should read this summary together with the more detailed description of risks relating to an investment in the securities contained in the section “Risk Factors Relating to the Securities” beginning on page EA-7 in the accompanying product supplement. You should also carefully read the risk factors included in the accompanying prospectus supplement and in the documents incorporated by reference in the accompanying prospectus, including Citigroup Inc.’s most recent Annual Report on Form 10-K and any subsequent Quarterly Reports on Form 10-Q, which describe risks relating to the business of Citigroup Inc. more generally.

| ▪ | You may lose some or all of your investment. Unlike conventional debt securities, the securities do not provide for the repayment of the stated principal amount at maturity in all circumstances. If a downside event occurs, which means that the worst performing underlying has depreciated from its initial underlying value by more than the buffer percentage, you will lose more than 1% of the stated principal amount of your securities for every 1% by which that depreciation exceeds the buffer percentage. You should understand that any decline in the final underlying value of the worst performing underlying beyond the buffer percentage will result in a magnified loss to your investment based on the buffer rate, which will progressively offset any protection that the buffer percentage would offer. The lower the final underlying value of the worst performing underlying, the less benefit you will receive from the buffer. There is no minimum payment at maturity on the securities (excluding the final coupon payment), and you may lose up to all of your investment. |

| ▪ | The initial underlying values, which have been set on the strike date, may be higher than the closing values of the underlyings on the pricing date. If the closing values of the underlyings on the pricing date are less than the initial underlying values that were set on the strike date, the terms of the securities may be less favorable to you than the terms of an alternative investment that may be available to you that offers a similar payout as the securities but with the initial underlying values set on the pricing date. |

| ▪ | The securities will be adversely affected by volatility in the closing values of the underlyings. The more volatile the closing values of the underlyings, the more likely it is that a downside event will occur and that you will not receive the full stated principal amount of your securities at maturity. In general, the higher the coupon on the securities, the greater the expected likelihood as of the pricing date that a downside event will occur and, as a result, that you will incur a significant loss at maturity. |

| ▪ | Higher coupon payment rates are associated with greater risk. The securities offer coupon payments at a per annum rate that is higher than the rate we would pay on conventional debt securities of the same maturity. In exchange for this higher coupon payment rate, investors in the securities will be subject to significantly greater risk than investors in our conventional debt securities, including the risk that you may lose a significant portion, and up to all, of your investment at maturity (excluding the final coupon payment). The volatility of and the correlation between the underlyings are important factors affecting these risks. In general, the higher the expected volatility of the underlyings, and the lower the expected correlation between the underlyings, the greater the coupon payment rate on the securities. However, higher expected volatility and lower expected correlation would also represent a greater expected likelihood as of the pricing date that the final underlying value of the worst performing underlying will be less than its downside threshold value, such that you will not be repaid the stated principal amount of your securities at maturity. |

| ▪ | The securities are subject to heightened risk because they have multiple underlyings. The securities are more risky than similar investments that may be available with only one underlying. With multiple underlyings, there is a greater chance that any one underlying will perform poorly, adversely affecting your return on the securities. |

| ▪ | The securities are subject to the risks of each of the underlyings and will be negatively affected if any one underlying performs poorly. You are subject to risks associated with each of the underlyings. If any one underlying performs poorly, you will be negatively affected. The securities are not linked to a basket composed of the underlyings, where the blended performance of the underlyings would be better than the performance of the worst performing underlying alone. Instead, you are subject to the full risks of whichever of the underlyings is the worst performing underlying. |

| ▪ | You will not benefit in any way from the performance of any better performing underlying. The return on the securities depends solely on the performance of the worst performing underlying, and you will not benefit in any way from the performance of any better performing underlying. The securities may underperform a similar investment in all of the underlyings or a similar alternative investment linked to a basket composed of the underlyings, since in either such case the performance of any better performing underlying would be blended with the performance of the worst performing underlying, resulting in a better return than the return of the worst performing underlying. |

| ▪ | You will be subject to risks relating to the relationship between the underlyings. It is preferable from your perspective for the underlyings to be correlated with each other, in the sense that their closing values tend to increase or decrease at similar times and by similar magnitudes. By investing in the securities, you assume the risk that the underlyings will not exhibit this relationship. The less correlated the underlyings, the more likely it is that any one of the underlyings will perform poorly over the term of the |

| PS-5 |

| Citigroup Global Markets Holdings Inc. |

securities. All that is necessary for the securities to perform poorly is for one of the underlyings to perform poorly. It is impossible to predict what the relationship between the underlyings will be over the term of the securities. The underlyings differ in significant ways and, therefore, may not be correlated with each other.

| ▪ | The securities offer downside exposure to the worst performing underlying, but no upside exposure to any underlying. You will not participate in any appreciation in the value of any underlying over the term of the securities. Consequently, your return on the securities will be limited to the coupon payments and may be significantly less than the return on any underlying over the term of the securities. In addition, as an investor in the securities, you will not receive any dividends or other distributions or have any other rights with respect to any of the underlyings. |

| ▪ | The performance of the securities will depend on the closing values of the underlyings solely on the valuation date, which makes the securities particularly sensitive to volatility in the closing values of the underlyings on or near the valuation date. What you receive at maturity will depend solely on the closing value of the worst performing underlying on the valuation date, and not on any other day during the term of the securities. Because the performance of the securities depends on the closing values of the underlyings on a limited number of dates, the securities will be particularly sensitive to volatility in the closing values of the underlyings on or near the valuation date. You should understand that the closing value of each underlying has historically been highly volatile. |

| ▪ | The securities are subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc. If we default on our obligations under the securities and Citigroup Inc. defaults on its guarantee obligations, you may not receive anything owed to you under the securities. |

| ▪ | The securities will not be listed on any securities exchange and you may not be able to sell them prior to maturity. The securities will not be listed on any securities exchange. Therefore, there may be little or no secondary market for the securities. CGMI currently intends to make a secondary market in relation to the securities and to provide an indicative bid price for the securities on a daily basis. Any indicative bid price for the securities provided by CGMI will be determined in CGMI’s sole discretion, taking into account prevailing market conditions and other relevant factors, and will not be a representation by CGMI that the securities can be sold at that price, or at all. CGMI may suspend or terminate making a market and providing indicative bid prices without notice, at any time and for any reason. If CGMI suspends or terminates making a market, there may be no secondary market at all for the securities because it is likely that CGMI will be the only broker-dealer that is willing to buy your securities prior to maturity. Accordingly, an investor must be prepared to hold the securities until maturity. |

| ▪ | The estimated value of the securities on the pricing date, based on CGMI’s proprietary pricing models and our internal funding rate, is less than the issue price. The difference is attributable to certain costs associated with selling, structuring and hedging the securities that are included in the issue price. These costs include (i) any selling concessions or other fees paid in connection with the offering of the securities, (ii) hedging and other costs incurred by us and our affiliates in connection with the offering of the securities and (iii) the expected profit (which may be more or less than actual profit) to CGMI or other of our affiliates in connection with hedging our obligations under the securities. These costs adversely affect the economic terms of the securities because, if they were lower, the economic terms of the securities would be more favorable to you. The economic terms of the securities are also likely to be adversely affected by the use of our internal funding rate, rather than our secondary market rate, to price the securities. See “The estimated value of the securities would be lower if it were calculated based on our secondary market rate” below. |

| ▪ | The estimated value of the securities was determined for us by our affiliate using proprietary pricing models. CGMI derived the estimated value disclosed on the cover page of this pricing supplement from its proprietary pricing models. In doing so, it may have made discretionary judgments about the inputs to its models, such as the volatility of, and correlation between, the closing values of the underlyings, the dividend yields on the underlyings and interest rates. CGMI’s views on these inputs may differ from your or others’ views, and as an underwriter in this offering, CGMI’s interests may conflict with yours. Both the models and the inputs to the models may prove to be wrong and therefore not an accurate reflection of the value of the securities. Moreover, the estimated value of the securities set forth on the cover page of this pricing supplement may differ from the value that we or our affiliates may determine for the securities for other purposes, including for accounting purposes. You should not invest in the securities because of the estimated value of the securities. Instead, you should be willing to hold the securities to maturity irrespective of the initial estimated value. |

| ▪ | The estimated value of the securities would be lower if it were calculated based on our secondary market rate. The estimated value of the securities included in this pricing supplement is calculated based on our internal funding rate, which is the rate at which we are willing to borrow funds through the issuance of the securities. Our internal funding rate is generally lower than our secondary market rate, which is the rate that CGMI will use in determining the value of the securities for purposes of any purchases of the securities from you in the secondary market. If the estimated value included in this pricing supplement were based on our secondary market rate, rather than our internal funding rate, it would likely be lower. We determine our internal funding rate based on factors such as the costs associated with the securities, which are generally higher than the costs associated with conventional debt securities, and our liquidity needs and preferences. Our internal funding rate is not an interest rate that is payable on the securities. |

Because there is not an active market for traded instruments referencing our outstanding debt obligations, CGMI determines our secondary market rate based on the market price of traded instruments referencing the debt obligations of Citigroup Inc., our parent company and the guarantor of all payments due on the securities, but subject to adjustments that CGMI makes in its sole

| PS-6 |

| Citigroup Global Markets Holdings Inc. |

discretion. As a result, our secondary market rate is not a market-determined measure of our creditworthiness, but rather reflects the market’s perception of our parent company’s creditworthiness as adjusted for discretionary factors such as CGMI’s preferences with respect to purchasing the securities prior to maturity.

| ▪ | The estimated value of the securities is not an indication of the price, if any, at which CGMI or any other person may be willing to buy the securities from you in the secondary market. Any such secondary market price will fluctuate over the term of the securities based on the market and other factors described in the next risk factor. Moreover, unlike the estimated value included in this pricing supplement, any value of the securities determined for purposes of a secondary market transaction will be based on our secondary market rate, which will likely result in a lower value for the securities than if our internal funding rate were used. In addition, any secondary market price for the securities will be reduced by a bid-ask spread, which may vary depending on the aggregate stated principal amount of the securities to be purchased in the secondary market transaction, and the expected cost of unwinding related hedging transactions. As a result, it is likely that any secondary market price for the securities will be less than the issue price. |

| ▪ | The value of the securities prior to maturity will fluctuate based on many unpredictable factors. The value of your securities prior to maturity will fluctuate based on the closing values of the underlyings, the volatility of, and correlation between, the closing values of the underlyings, dividend yields on the underlyings, interest rates generally, the time remaining to maturity and our and Citigroup Inc.’s creditworthiness, as reflected in our secondary market rate, among other factors described under “Risk Factors Relating to the Securities—Risk Factors Relating to All Securities—The value of your securities prior to maturity will fluctuate based on many unpredictable factors” in the accompanying product supplement. Changes in the closing values of the underlyings may not result in a comparable change in the value of your securities. You should understand that the value of your securities at any time prior to maturity may be significantly less than the issue price. |

| ▪ | Immediately following issuance, any secondary market bid price provided by CGMI, and the value that will be indicated on any brokerage account statements prepared by CGMI or its affiliates, will reflect a temporary upward adjustment. The amount of this temporary upward adjustment will steadily decline to zero over the temporary adjustment period. See “Valuation of the Securities” in this pricing supplement. |

| ▪ | Our offering of the securities is not a recommendation of any underlying. The fact that we are offering the securities does not mean that we believe that investing in an instrument linked to the underlyings is likely to achieve favorable returns. In fact, as we are part of a global financial institution, our affiliates may have positions (including short positions) in the underlyings or in instruments related to the underlyings, and may publish research or express opinions, that in each case are inconsistent with an investment linked to the underlyings. These and other activities of our affiliates may affect the closing values of the underlyings in a way that negatively affects the value of and your return on the securities. |

| ▪ | The closing value of an underlying may be adversely affected by our or our affiliates’ hedging and other trading activities. We expect to hedge our obligations under the securities through CGMI or other of our affiliates, who may take positions in the underlyings or in financial instruments related to the underlyings and may adjust such positions during the term of the securities. Our affiliates also take positions in the underlyings or in financial instruments related to the underlyings on a regular basis (taking long or short positions or both), for their accounts, for other accounts under their management or to facilitate transactions on behalf of customers. These activities could affect the closing values of the underlyings in a way that negatively affects the value of and your return on the securities. They could also result in substantial returns for us or our affiliates while the value of the securities declines. |

| ▪ | We and our affiliates may have economic interests that are adverse to yours as a result of our affiliates’ business activities. Our affiliates engage in business activities with a wide range of companies. These activities include extending loans, making and facilitating investments, underwriting securities offerings and providing advisory services. These activities could involve or affect the underlyings in a way that negatively affects the value of and your return on the securities. They could also result in substantial returns for us or our affiliates while the value of the securities declines. In addition, in the course of this business, we or our affiliates may acquire non-public information, which will not be disclosed to you. |

| ▪ | The calculation agent, which is an affiliate of ours, will make important determinations with respect to the securities. If certain events occur during the term of the securities, such as market disruption events and other events with respect to an underlying, CGMI, as calculation agent, will be required to make discretionary judgments that could significantly affect your return on the securities. In making these judgments, the calculation agent’s interests as an affiliate of ours could be adverse to your interests as a holder of the securities. See “Risk Factors Relating to the Securities—Risk Factors Relating to All Securities—The calculation agent, which is an affiliate of ours, will make important determinations with respect to the securities” in the accompanying product supplement. |

| ▪ | Changes that affect the underlyings may affect the value of your securities. The sponsors of the underlyings may at any time make methodological changes or other changes in the manner in which they operate that could affect the values of the underlyings. We are not affiliated with any such underlying sponsor and, accordingly, we have no control over any changes any such sponsor may make. Such changes could adversely affect the performance of the underlyings and the value of and your return on the securities. |

| ▪ | The U.S. federal tax consequences of an investment in the securities are unclear. There is no direct legal authority as to the proper U.S. federal tax treatment of the securities, and we do not intend to request a ruling from the Internal Revenue Service (the |

| PS-7 |

| Citigroup Global Markets Holdings Inc. |

“IRS”). Consequently, significant aspects of the tax treatment of the securities are uncertain, and the IRS or a court might not agree with the treatment described herein. If the IRS were successful in asserting an alternative treatment, the tax consequences of ownership and disposition of the securities might be materially and adversely affected. As described below under “United States Federal Tax Considerations,” the U.S. Treasury Department and the IRS have requested comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar financial instruments and have indicated that such transactions may be the subject of future regulations or other guidance. In addition, members of Congress have proposed legislative changes to the tax treatment of derivative contracts. Any legislation, Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the securities, possibly with retroactive effect.

As described below under “United States Federal Tax Considerations,” in connection with any information reporting requirements we may have in respect of the securities under applicable law, we intend to treat a portion of each coupon payment as attributable to interest and the remainder to option premium. However, in light of the uncertain treatment of the securities, it is possible that other persons having withholding or information reporting responsibility in respect of the securities may treat a security differently, for instance, by treating the entire coupon payment as ordinary income at the time received or accrued by a holder and/or treating some or all of each coupon payment made to a non-U.S. investor on a security as subject to withholding tax at a rate of 30%. Moreover, it is possible that in the future we may determine that we should withhold at a rate of 30% on coupon payments made to a non-U.S. investor on the securities. If withholding applies to the securities, we will not be required to pay any additional amounts with respect to amounts so withheld.

Non-U.S. Holders should also review the section entitled “United States Federal Tax Considerations—Tax Consequences to Non-U.S. Holders—Possible Withholding Under Section 871(m) of the Code” regarding the risk of withholding in respect of “dividend equivalents” on the securities.

You should review carefully the section of this pricing supplement entitled “United States Federal Tax Considerations.” You should also consult your tax adviser regarding the U.S. federal tax consequences of an investment in the securities, as well as tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

| PS-8 |

| Citigroup Global Markets Holdings Inc. |

Information About the S&P 500® Index

The S&P 500® Index consists of the common stocks of 500 issuers selected to provide a performance benchmark for the large capitalization segment of the U.S. equity markets. It is calculated and maintained by S&P Dow Jones Indices LLC.

Please refer to the section “Equity Index Descriptions—The S&P U.S. Indices—The S&P 500® Index” in the accompanying underlying supplement for additional information.

We have derived all information regarding the S&P 500® Index from publicly available information and have not independently verified any information regarding the S&P 500® Index. This pricing supplement relates only to the securities and not to the S&P 500® Index. We make no representation as to the performance of the S&P 500® Index over the term of the securities.

The securities represent obligations of Citigroup Global Markets Holdings Inc. (guaranteed by Citigroup Inc.) only. The sponsor of the S&P 500® Index is not involved in any way in this offering and has no obligation relating to the securities or to holders of the securities.

Historical Information

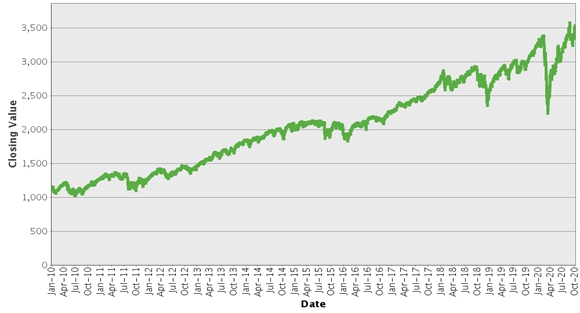

The closing value of the S&P 500® Index on October 14, 2020 was 3,488.67.

The graph below shows the closing value of the S&P 500® Index for each day such value was available from January 4, 2010 to October 14, 2020. We obtained the closing values from Bloomberg L.P., without independent verification. You should not take the historical closing values as an indication of future performance.

S&P 500® Index – Historical Closing Values January 4, 2010 to October 14, 2020 |

|

| PS-9 |

| Citigroup Global Markets Holdings Inc. |

Information About the Nasdaq-100 Index®

The Nasdaq-100 Index® is a modified market capitalization-weighted index of stocks of the 100 largest non-financial companies listed on the Nasdaq Stock Market. All stocks included in the Nasdaq-100 Index® are traded on a major U.S. exchange. The Nasdaq-100 Index® was developed by the Nasdaq Stock Market, Inc. and is calculated, maintained and published by Nasdaq, Inc.

Please refer to the section “Equity Index Descriptions—The Nasdaq-100 Index®” in the accompanying underlying supplement for additional information.

We have derived all information regarding the Nasdaq-100 Index® from publicly available information and have not independently verified any information regarding the Nasdaq-100 Index®. This pricing supplement relates only to the securities and not to the Nasdaq-100 Index®. We make no representation as to the performance of the Nasdaq-100 Index® over the term of the securities.

The securities represent obligations of Citigroup Global Markets Holdings Inc. (guaranteed by Citigroup Inc.) only. The sponsor of the Nasdaq-100 Index® is not involved in any way in this offering and has no obligation relating to the securities or to holders of the securities.

Historical Information

The closing value of the Nasdaq-100 Index® on October 14, 2020 was 11,985.36.

The graph below shows the closing value of the Nasdaq-100 Index® for each day such value was available from January 4, 2010 to October 14, 2020. We obtained the closing values from Bloomberg L.P., without independent verification. You should not take the historical closing values as an indication of future performance.

Nasdaq-100 Index® – Historical Closing Values January 4, 2010 to October 14, 2020 |

|

| PS-10 |

| Citigroup Global Markets Holdings Inc. |

United States Federal Tax Considerations

You should note that, other than the discussion under “United States Federal Tax Considerations—Tax Consequences to U.S. Holders—Possible Taxable Event” regarding the possible assumption of the securities by Citigroup Inc., the discussion under the section called “United States Federal Tax Considerations” in the accompanying product supplement generally does not apply to the securities issued under this pricing supplement and is superseded by the following discussion.

The following is a discussion of the material U.S. federal income and certain estate tax consequences of the ownership and disposition of the securities. It applies to you only if you are an initial holder of a security that purchases the security for cash at its stated principal amount, and holds the security as a capital asset within the meaning of Section 1221 of the Code.

This discussion does not address all of the tax consequences that may be relevant to you in light of your particular circumstances or if you are a holder subject to special rules, such as:

· a financial institution;

· a dealer or trader subject to a mark-to-market method of tax accounting with respect to the securities;

· a person holding the securities as part of a “straddle” or conversion transaction or one who enters into a “constructive sale” with respect to a security;

· a U.S. Holder (as defined below) whose functional currency is not the U.S. dollar;

· an entity classified as a partnership for U.S. federal income tax purposes;

· a regulated investment company;

· a tax-exempt entity, including an “individual retirement account” or “Roth IRA”; or

· an investor subject to special tax accounting rules under Section 451(b) of the Code.

If an entity that is classified as a partnership for U.S. federal income tax purposes holds the securities, the U.S. federal income tax treatment of a partner will generally depend on the status of the partner and the activities of the partnership. If you are a partnership holding the securities or a partner in such a partnership, you should consult your tax adviser as to the particular U.S. federal tax consequences of holding and disposing of the securities to you.

This discussion is based on the Code, administrative pronouncements, judicial decisions and final, temporary and proposed Treasury regulations, all as of the date of this pricing supplement, changes to any of which may affect the tax consequences described herein, possibly with retroactive effect. This discussion does not address the effects of any applicable state, local or non-U.S. tax laws or the potential application of the Medicare contribution tax. You should consult your tax adviser about the application of U.S. federal tax laws to your particular situation (including the possibility of alternative treatments of the securities), as well as any tax consequences arising under the laws of any state, local or non-U.S. jurisdiction.

Tax Treatment of the Securities

Due to the absence of statutory, judicial or administrative authorities that directly address the U.S. federal tax treatment of the securities or similar instruments, there is substantial uncertainty regarding the U.S. federal tax consequences of an investment in the securities. In connection with any information reporting requirements we may have in respect of the securities under applicable law, we intend (in the absence of an administrative determination or judicial ruling to the contrary) to treat each security for U.S. federal income tax purposes as a unit comprising (i) an option written by you that, if exercised, requires you to pay us an amount equal to the Deposit (as defined below) in exchange for a cash payment from us based on the underlying return of the least performing underlying (the “Put Option”) and (ii) a deposit with us of a fixed amount of cash equal to the stated principal amount of the security to secure your potential obligation under the Put Option (the “Deposit”). In the opinion of our counsel, Davis Polk & Wardwell LLP, this treatment of the securities is reasonable under current law; however, our counsel has advised us that due to the lack of any controlling legal authority it is unable to conclude affirmatively that this treatment is more likely than not to be upheld, and that alternative treatments are possible. Moreover, our counsel’s opinion is based on market conditions as of the date of this preliminary pricing supplement and is subject to confirmation on the pricing date. Under this treatment:

· a portion of each coupon payment made with respect to a security will be attributable to interest on the Deposit; and

· the remainder will represent option premium attributable to your grant of the Put Option (with respect to each coupon payment received and, collectively, all coupon payments received, “Put Premium”).

| PS-11 |

| Citigroup Global Markets Holdings Inc. |

We will specify in the final pricing supplement the portion of each coupon payment that we will allocate to interest on the Deposit and to Put Premium, respectively.

We do not plan to request a ruling from the IRS, and the IRS or a court might not agree with this treatment. Accordingly, you should consult your tax adviser regarding the U.S. federal tax consequences of an investment in the securities. Unless otherwise stated, the following discussion is based on the treatment of each security as a Put Option and a Deposit.

Tax Consequences to U.S. Holders

This section applies only to U.S. Holders. You are a “U.S. Holder” if for U.S. federal income tax purposes you are a beneficial owner of a security that is:

· a citizen or individual resident of the United States;

· a corporation, or other entity taxable as a corporation, created or organized in or under the laws of the United States, any state thereof or the District of Columbia; or

· an estate or trust the income of which is subject to U.S. federal income taxation regardless of its source.

Coupon Payments. We intend to treat interest paid with respect to the Deposit as ordinary interest income that is taxable to you at the time it accrues or is received, in accordance with your method of tax accounting. The Put Premium should not be taken into account until retirement or earlier sale or exchange of the security.

Sale or Exchange Prior to Retirement. Upon a sale or exchange of a security prior to retirement, you should apportion the amount realized between the Deposit and the Put Option based on their respective values on the date of sale or exchange. If the value of the Put Option is negative, you should be treated as having made a payment of such negative value to the purchaser in exchange for the purchaser’s assumption of the Put Option, in which case a corresponding amount should be added to the amount realized in respect of the Deposit.

You should recognize gain or loss with respect to the Deposit in an amount equal to the difference between (i) the amount realized that is apportioned to the Deposit and (ii) your basis in the Deposit (i.e., the price you paid to acquire the security plus any amounts previously accrued into income but not yet paid). Any loss should be treated as short-term capital loss. Any gain should be treated as ordinary interest income to the extent of the amount of any accrued but unpaid discount on the Deposit not yet taken into income and any remaining gain should be treated as short-term capital gain.

You should recognize gain or loss in respect of the Put Option in an amount equal to the total Put Premium you previously received, decreased by the amount deemed to be paid by you, or increased by the amount deemed to be paid to you, in exchange for the purchaser’s assumption of the Put Option. This gain or loss should be short-term capital gain or loss.

Tax Treatment at Retirement. The coupon payment received upon retirement will be treated as described above under “Coupon Payments.”

If a security is retired for its stated principal amount (without taking into account any coupon payment), the Put Option should be deemed to have expired unexercised, in which case you should recognize short-term capital gain in an amount equal to the sum of all payments of Put Premium received, including the Put Premium received upon retirement.

At maturity, if you receive an amount of cash, not counting the final coupon payment, that is different from the stated principal amount, the Put Option should be deemed to have been exercised and you should be deemed to have applied the Deposit toward the cash settlement of the Put Option. In that case, you should recognise short-term capital gain or loss with respect to the Put Option in an amount equal to the difference between (i) the sum of the total Put Premium received (including the Put Premium received at maturity) and the cash you receive at maturity, excluding the final coupon payment, and (ii) the Deposit.

Possible Taxable Event. In the event of a designation of a successor underlying, it is possible that the securities could be treated, in whole or part, as terminated and reissued for U.S. federal income tax purposes. In such a case, you might be required to recognize gain or loss (subject to the possible application of the wash sale rules) with respect to the securities.

Possible Alternative Tax Treatments of an Investment in the Securities

Alternative U.S. federal income tax treatments of the securities are possible that, if applied, could materially and adversely affect the timing and/or character of income, gain or loss with respect to the securities. A security could be treated as a debt instrument issued by us, in which case the timing and character of taxable income with respect to coupon payments on the securities would differ from that described herein and all or a portion of any gain you realize would generally be treated as ordinary income. In addition, you could be subject to special reporting requirements if any loss exceeded certain thresholds. Under other possible treatments, the entire coupon on the securities might either be (i) treated as income to you at the time received or accrued or (ii) not accounted for separately as

| PS-12 |

| Citigroup Global Markets Holdings Inc. |

giving rise to income to you until the sale, exchange or retirement of the securities. You should consult your tax adviser regarding these issues.

Other possible U.S. federal income tax treatments of the securities are possible that could also affect the timing and character of income or loss with respect to the securities. In addition, the U.S. Treasury Department and the IRS have requested comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar financial instruments and have indicated that such transactions may be the subject of future regulations or other guidance. In addition, members of Congress have proposed legislative changes to the tax treatment of derivative contracts. Any legislation, Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the securities, possibly with retroactive effect. You should consult your tax adviser regarding the U.S. federal income tax consequences of an investment in the securities.

Tax Consequences to Non-U.S. Holders

This section applies only to Non-U.S. Holders. You are a “Non-U.S. Holder” if you are a beneficial owner of a security that is, for U.S. federal income tax purposes:

· an individual who is classified as a nonresident alien;

· a foreign corporation; or

· a foreign trust or estate.

You are not a Non-U.S. Holder for the purposes of this discussion if you are (i) an individual who is present in the United States for 183 days or more in the taxable year of disposition or (ii) a former citizen or resident of the United States. If you are or may become such a person during the period in which you hold a security, you should consult your tax adviser regarding the U.S. federal tax consequences of an investment in the securities to you.

Subject to the discussions below regarding Section 871(m) and “FATCA,” under current law, you generally should not be subject to U.S. federal withholding or income tax in respect of payments on the securities or amounts received on the sale, exchange or retirement of the securities, provided that (i) income in respect of the securities is not effectively connected with your conduct of a trade or business in the United States, and (ii) you provide to the applicable withholding agent an appropriate IRS Form W-8 certifying under penalties of perjury that you are not a U.S. person.

If you are engaged in a U.S. trade or business, and if income from the securities is effectively connected with the conduct of that trade or business, you generally will be subject to regular U.S. federal income tax with respect to that income in the same manner as if you were a U.S. Holder, unless an applicable income tax treaty provides otherwise. If you are a Non-U.S. Holder to which this paragraph may apply, you should consult your tax adviser regarding other U.S. tax consequences of the ownership and disposition of the securities. If you are a corporation, you should also consider the potential application of a 30% (or lower treaty rate) branch profits tax.

As described above under “—Tax Consequences to U.S. Holders—Possible Alternative Tax Treatments of an Investment in the Securities” alternative tax treatments could apply to the securities, in which case the tax consequences to you could be materially and adversely affected. In addition, potential legislative or regulatory changes to the tax treatment of the securities could adversely impact your consequences of an investment in the securities.

Possible Withholding Under Section 871(m) of the Code. Section 871(m) of the Code and Treasury regulations promulgated thereunder (“Section 871(m)”) generally impose a 30% withholding tax on dividend equivalents paid or deemed paid to Non-U.S. Holders with respect to certain financial instruments linked to U.S. equities (“U.S. Underlying Equities”) or indices that include U.S. Underlying Equities. Section 871(m) generally applies to instruments that substantially replicate the economic performance of one or more U.S. Underlying Equities, as determined based on tests set forth in the applicable Treasury regulations. However, the regulations, as modified by an IRS notice, exempt financial instruments issued prior to January 1, 2023 that do not have a “delta” of one. Based on the terms of the securities and representations provided by us as of the date of this preliminary pricing supplement, our counsel is of the opinion that the securities should not be treated as transactions that have a “delta” of one within the meaning of the regulations with respect to any U.S. Underlying Equity and, therefore, should not be subject to withholding tax under Section 871(m). However, the final determination regarding the treatment of the securities under Section 871(m) will be made as of the pricing date for the securities, and it is possible that the securities will be subject to withholding under Section 871(m) based on the circumstances of that date.

A determination that the securities are not subject to Section 871(m) is not binding on the IRS, and the IRS may disagree with this treatment. Moreover, Section 871(m) is complex and its application may depend on your particular circumstances, including your other transactions. You should consult your tax adviser regarding the potential application of Section 871(m) to the securities.

While we currently do not intend to withhold on payments on the securities to Non-U.S. Holders (subject to the certification requirement described above, the discussion above regarding Section 871(m) and the discussion below regarding “FATCA”), in light of the uncertain treatment of the securities other persons having withholding or information reporting responsibility in

| PS-13 |

| Citigroup Global Markets Holdings Inc. |

respect of the securities may treat some or all of each coupon payment on a security as subject to withholding tax at a rate of 30%. Moreover, it is possible that in the future we may determine that we should withhold at a rate of 30% on coupon payments on the securities. We will not be required to pay any additional amounts with respect to amounts withheld.

U.S. Federal Estate Tax

If you are an individual Non-U.S. Holder, or an entity the property of which is potentially includible in such an individual’s gross estate for U.S. federal estate tax purposes (for example, a trust funded by such an individual and with respect to which the individual has retained certain interests or powers), you should note that, absent an applicable treaty exemption, a security may be treated as U.S.-situs property subject to U.S. federal estate tax. If you are such an individual or entity, you should consult your tax adviser regarding the U.S. federal estate tax consequences of an investment in the securities.

Information Reporting and Backup Withholding

Amounts paid on the securities, and payment of the proceeds of a sale, exchange or other taxable disposition of the securities, may be subject to information reporting and, if you fail to provide certain identifying information (such as an accurate taxpayer identification number if you are a U.S. Holder) or meet certain other conditions, may also be subject to backup withholding at the rate specified in the Code. If you are a Non-U.S. Holder that provides the applicable withholding agent with an appropriate IRS Form W-8, you will generally establish an exemption from backup withholding. Amounts withheld under the backup withholding rules are not additional taxes and may be refunded or credited against your U.S. federal income tax liability, provided the relevant information is timely furnished to the IRS.

FATCA

Legislation commonly referred to as “FATCA” generally imposes a withholding tax of 30% on payments to certain non-U.S. entities (including financial intermediaries) with respect to certain financial instruments, unless various U.S. information reporting and due diligence requirements have been satisfied. An intergovernmental agreement between the United States and the non-U.S. entity’s jurisdiction may modify these requirements. This legislation generally applies to certain financial instruments that are treated as paying U.S.-source interest, dividend equivalents or other U.S.-source “fixed or determinable annual or periodical” income (“FDAP income”). Withholding (if applicable) applies to payments of U.S.-source FDAP income. While existing Treasury regulations would also require withholding on payments of gross proceeds of the disposition (including upon retirement) of certain financial instruments treated as providing for U.S.-source interest or dividends, the U.S. Treasury Department has indicated in subsequent proposed regulations its intent to eliminate this requirement. The U.S. Treasury Department has indicated that taxpayers may rely on these proposed regulations pending their finalization. Although the application of the FATCA rules to the securities is not entirely clear because the U.S. federal income tax treatment of the securities is unclear, it would be prudent to assume that a withholding agent will treat the securities as subject to the withholding rules under FATCA. If withholding applies to the securities, we will not be required to pay any additional amounts with respect to amounts withheld. You should consult your tax adviser regarding the potential application of FATCA to the securities.

The preceding discussion, when read in conjunction with “United States Federal Tax Considerations—Tax Consequences to U.S. Holders—Possible Taxable Event” in the accompanying product supplement, constitutes the full opinion of Davis Polk & Wardwell LLP regarding the material U.S. federal tax consequences of owning and disposing of the securities.

You should consult your tax adviser regarding all aspects of the U.S. federal income and estate tax consequences of an investment in the securities, and any tax consequences arising under the laws of any state, local or foreign taxing jurisdiction.

Supplemental Plan of Distribution

CGMI, an affiliate of Citigroup Global Markets Holdings Inc. and the underwriter of the sale of the securities, is acting as principal and will not receive any underwriting fee for any securities sold in this offering.

See “Plan of Distribution; Conflicts of Interest” in the accompanying product supplement and “Plan of Distribution” in each of the accompanying prospectus supplement and prospectus for additional information.

Valuation of the Securities

CGMI calculated the estimated value of the securities set forth on the cover page of this pricing supplement based on proprietary pricing models. CGMI’s proprietary pricing models generated an estimated value for the securities by estimating the value of a hypothetical package of financial instruments that would replicate the payout on the securities, which consists of a fixed-income bond (the “bond component”) and one or more derivative instruments underlying the economic terms of the securities (the “derivative component”). CGMI calculated the estimated value of the bond component using a discount rate based on our internal funding rate. CGMI calculated the estimated value of the derivative component based on a proprietary derivative-pricing model, which generated a theoretical price for the instruments that constitute the derivative component based on various inputs, including the factors described under “Summary Risk Factors—The value of the securities prior to maturity will fluctuate based on many unpredictable factors” in this

| PS-14 |

| Citigroup Global Markets Holdings Inc. |

pricing supplement, but not including our or Citigroup Inc.’s creditworthiness. These inputs may be market-observable or may be based on assumptions made by CGMI in its discretionary judgment.

The estimated value of the securities is a function of the terms of the securities and the inputs to CGMI’s proprietary pricing models. As of the date of this preliminary pricing supplement, it is uncertain what the estimated value of the securities will be on the pricing date because it is uncertain what the values of the inputs to CGMI’s proprietary pricing models will be on the pricing date.

For a period of approximately three months following issuance of the securities, the price, if any, at which CGMI would be willing to buy the securities from investors, and the value that will be indicated for the securities on any brokerage account statements prepared by CGMI or its affiliates (which value CGMI may also publish through one or more financial information vendors), will reflect a temporary upward adjustment from the price or value that would otherwise be determined. This temporary upward adjustment represents a portion of the hedging profit expected to be realized by CGMI or its affiliates over the term of the securities. The amount of this temporary upward adjustment will decline to zero on a straight-line basis over the three-month temporary adjustment period. However, CGMI is not obligated to buy the securities from investors at any time. See “Summary Risk Factors—The securities will not be listed on any securities exchange and you may not be able to sell them prior to maturity.”

Certain Selling Restrictions

Hong Kong Special Administrative Region

The contents of this pricing supplement and the accompanying product supplement, underlying supplement, prospectus supplement and prospectus have not been reviewed by any regulatory authority in the Hong Kong Special Administrative Region of the People’s Republic of China (“Hong Kong”). Investors are advised to exercise caution in relation to the offer. If investors are in any doubt about any of the contents of this pricing supplement and the accompanying product supplement, underlying supplement, prospectus supplement and prospectus, they should obtain independent professional advice.

The securities have not been offered or sold and will not be offered or sold in Hong Kong by means of any document, other than

| (i) | to persons whose ordinary business is to buy or sell shares or debentures (whether as principal or agent); or |

| (ii) | to “professional investors” as defined in the Securities and Futures Ordinance (Cap. 571) of Hong Kong (the “Securities and Futures Ordinance”) and any rules made under that Ordinance; or |

| (iii) | in other circumstances which do not result in the document being a “prospectus” as defined in the Companies Ordinance (Cap. 32) of Hong Kong or which do not constitute an offer to the public within the meaning of that Ordinance; and |

There is no advertisement, invitation or document relating to the securities which is directed at, or the contents of which are likely to be accessed or read by, the public of Hong Kong (except if permitted to do so under the securities laws of Hong Kong) other than with respect to securities which are or are intended to be disposed of only to persons outside Hong Kong or only to “professional investors” as defined in the Securities and Futures Ordinance and any rules made under that Ordinance.

Non-insured Product: These securities are not insured by any governmental agency. These securities are not bank deposits and are not covered by the Hong Kong Deposit Protection Scheme.

Singapore

This pricing supplement and the accompanying product supplement, underlying supplement, prospectus supplement and prospectus have not been registered as a prospectus with the Monetary Authority of Singapore, and the securities will be offered pursuant to exemptions under the Securities and Futures Act, Chapter 289 of Singapore (the “Securities and Futures Act”). Accordingly, the securities may not be offered or sold or made the subject of an invitation for subscription or purchase nor may this pricing supplement or any other document or material in connection with the offer or sale or invitation for subscription or purchase of any securities be circulated or distributed, whether directly or indirectly, to any person in Singapore other than (a) to an institutional investor pursuant to Section 274 of the Securities and Futures Act, (b) to a relevant person under Section 275(1) of the Securities and Futures Act or to any person pursuant to Section 275(1A) of the Securities and Futures Act and in accordance with the conditions specified in Section 275 of the Securities and Futures Act, or (c) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the Securities and Futures Act. Where the securities are subscribed or purchased under Section 275 of the Securities and Futures Act by a relevant person which is:

| (a) | a corporation (which is not an accredited investor (as defined in Section 4A of the Securities and Futures Act)) the sole business of which is to hold investments and the entire share capital of which is owned by one or more individuals, each of whom is an accredited investor; or |

| (b) | a trust (where the trustee is not an accredited investor) whose sole purpose is to hold investments and each beneficiary is an individual who is an accredited investor, securities (as defined in Section 239(1) of the Securities and Futures Act) of that corporation or the beneficiaries’ rights and interests (howsoever described) in that trust shall not be transferable for 6 months after that corporation or that trust has acquired the relevant securities pursuant to an offer under Section 275 of the Securities and Futures Act except: |

| PS-15 |

| Citigroup Global Markets Holdings Inc. |

| (i) | to an institutional investor or to a relevant person defined in Section 275(2) of the Securities and Futures Act or to any person arising from an offer referred to in Section 275(1A) or Section 276(4)(i)(B) of the Securities and Futures Act; or |

| (ii) | where no consideration is or will be given for the transfer; or |

| (iii) | where the transfer is by operation of law; or |

| (iv) | pursuant to Section 276(7) of the Securities and Futures Act; or |

| (v) | as specified in Regulation 32 of the Securities and Futures (Offers of Investments) (Shares and Debentures) Regulations 2005 of Singapore. |

Any securities referred to herein may not be registered with any regulator, regulatory body or similar organization or institution in any jurisdiction.

The securities are Specified Investment Products (as defined in the Notice on Recommendations on Investment Products and Notice on the Sale of Investment Product issued by the Monetary Authority of Singapore on 28 July 2011) that is neither listed nor quoted on a securities market or a futures market.

Non-insured Product: These securities are not insured by any governmental agency. These securities are not bank deposits. These securities are not insured products subject to the provisions of the Deposit Insurance and Policy Owners’ Protection Schemes Act 2011 of Singapore and are not eligible for deposit insurance coverage under the Deposit Insurance Scheme.

Contact

Clients may contact their local brokerage representative. Third-party distributors may contact Citi Structured Investment Sales at (212) 723-7005.

© 2020 Citigroup Global Markets Inc. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

| PS-16 |