The information in this preliminary pricing supplement is not complete and may be changed. This preliminary pricing supplement, the accompanying product supplement, underlying supplement, prospectus supplement and prospectus are not an offer to sell these securities, nor are they soliciting an offer to buy these securities, in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED APRIL 2, 2021

Filed Pursuant to Rule 424(b)(2)

Registration Statement Nos. 333-224495 and 333-224495-03

April-----, 2021 Medium-Term Senior Notes, Series N Pricing Supplement No. 2021-USNCH7228 to Product Supplement No. EA-02-08 |  |

Citigroup Global Markets Holdings Inc. All Payments Due from Citigroup Global Markets Holdings Inc. Fully and Unconditionally Guaranteed by Citigroup Inc. |

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 |

| n | Linked to the Energy Select Sector SPDR® Fund (the “underlying”) | |

| n | Unlike ordinary debt securities, the securities do not pay interest or repay a fixed amount of principal at maturity. Instead, the securities provide for a payment at maturity that may be greater than, equal to or less than the stated principal amount of the securities, depending on the performance of the underlying from the initial underlying value to the final underlying value, subject to the maximum return at maturity. The payment at maturity will reflect the following terms: | |

| n | If the value of the underlying increases, you will receive the stated principal amount plus 200% participation in the upside performance of the underlying, subject to a maximum total return at maturity of 24% to 28% (the “maximum return at maturity”) (to be determined on the pricing date) of the stated principal amount | |

| n | If the value of the underlying decreases, but the decrease is not more than 15.00% (the “buffer percentage”), you will be repaid the stated principal amount | |

| n | If the value of the underlying decreases by more than the buffer percentage, you will receive less than the stated principal amount and have 1-to-1 downside exposure to the decrease in the value of the underlying in excess of the buffer percentage | |

| n | Investors may lose up to 85.00% of the stated principal amount | |

| n | All payments on the securities are subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc.; if Citigroup Global Markets Holdings Inc. and Citigroup Inc. default on their obligations, you could lose some or all of your investment | |

| n | No periodic interest payments or dividends | |

| n | The securities will not be listed on any securities exchange and, accordingly, may have limited or no liquidity. You should not invest in the securities unless you are willing to hold them to maturity. | |

The securities have complex features and investing in the securities involves risks not associated with an investment in conventional debt securities. See “Summary Risk Factors” beginning on page PS-7, “Risk Factors Relating to the Securities” beginning on page EA-7 of the accompanying product supplement and “Risk Factors” beginning on page S-1 of the accompanying prospectus supplement.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the securities or determined that this pricing supplement or the accompanying product supplement, underlying supplement, prospectus supplement and prospectus are truthful or complete. Any representation to the contrary is a criminal offense.

The securities are unsecured debt obligations issued by Citigroup Global Markets Holdings Inc. and guaranteed by Citigroup Inc. All payments due on the securities are subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc. None of Wells Fargo Securities, LLC (“Wells Fargo”) or any of its affiliates will have any liability to the purchasers of the securities in the event Citigroup Global Markets Holdings Inc. defaults on its obligations under the securities and Citigroup Inc. defaults on its guarantee obligations. The securities are not bank deposits and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency, nor are they obligations of, or guaranteed by, a bank.

| Per Security | Total | |

| Public Offering Price(1) | $1,000.00 | $ |

| Maximum Underwriting Discount and Commission(2)(3) | $31.50 | $ |

| Proceeds to Citigroup Global Markets Holdings Inc.(2) | $968.50 | $ |

(1) Citigroup Global Markets Holdings Inc. currently expects that the estimated value of the securities on the pricing date will be at least $900.00 per security, which will be less than the public offering price. The estimated value of the securities is based on Citigroup Global Market Inc.’s (“CGMI”) proprietary pricing models and our internal funding rate. It is not an indication of actual profit to CGMI or other of our affiliates, nor is it an indication of the price, if any, at which any person may be willing to buy the securities from you at any time after issuance. See “Valuation of the Securities” in this pricing supplement.

(2) CGMI, an affiliate of Citigroup Global Markets Holdings Inc., as the lead agent for the offering, expects to sell the securities to Wells Fargo, as agent. Wells Fargo will receive an underwriting discount and commission of up to 3.15% ($31.50) for each security it sells. Wells Fargo will pay selected dealers, which may include Wells Fargo Advisors (“WFA”) (the trade name of the retail brokerage business of its affiliates, Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC), a fixed selling commission of 1.75% ($17.50) for each security they sell. In addition to the selling commission allowed to WFA, Wells Fargo will pay $0.75 per security of the underwriting discount and commission to WFA as a distribution expense fee for each security sold by WFA. The total underwriting discount and commission and proceeds to Citigroup Global Markets Holdings Inc. shown above give effect to the actual underwriting discount and commission provided for the sale of the securities. See “Supplemental Plan of Distribution” below and “Use of Proceeds and Hedging” in the accompanying prospectus for further information regarding how we have hedged our obligations under the securities.

(3) In respect of certain securities sold in this offering, CGMI may pay a fee of up to $1.00 per security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the securities to other securities dealers.

| Citigroup Global Markets Inc. | Wells Fargo Securities |

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 |  |

| Terms of the Securities | |

| Underlying: | The Energy Select Sector SPDR® Fund |

| Issuer: | Citigroup Global Markets Holdings Inc., a wholly owned subsidiary of Citigroup Inc. |

| Guarantee: | All payments due on the securities are fully and unconditionally guaranteed by Citigroup Inc. |

| Stated Principal Amount: | $1,000 per security. References in this pricing supplement to a “security” are to a security with a stated principal amount of $1,000. |

| Pricing Date: | April 30, 2021* |

| Issue Date: | May 5, 2021* |

| Valuation Date: | April 28, 2023, subject to postponement if such date is not a trading day or certain market disruption events occur.* See “Additional Terms of the Securities.” |

| Maturity Date: | May 5, 2023. If the valuation date is postponed, the stated maturity date will be the later of (i) May 5, 2023 and (ii) three business days after the valuation date as postponed.* See “Additional Terms of the Securities.” |

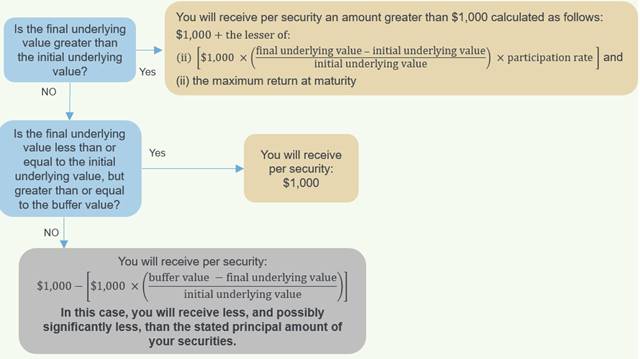

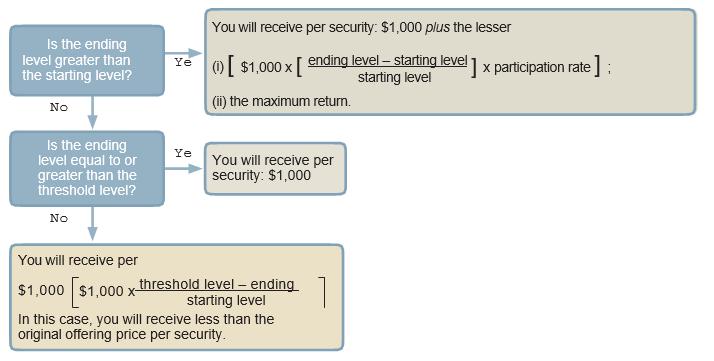

For each $1,000 stated principal amount security you hold at maturity:

• If the final underlying value is greater than the initial underlying value:

$1,000 plus the lesser of:

| |

| (i) $1,000 × | final underlying value – initial underlying value initial underlying value

| × participation rate; and | ||

| (ii) the maximum return at maturity | ||||

Payment at Maturity:

| • If the final underlying value is less than or equal to the initial underlying value, but greater than or equal to the buffer value: $1,000; or

• If the final underlying value is less than the buffer value:

$1,000 minus:

|

| $1,000 × | buffer value – final underlying value initial underlying value

|

| If the final underlying value is less than the buffer value, you will receive less, and possibly significantly less, than the $1,000 stated principal amount per security at maturity. | |

| Participation Rate: | 200% |

| Maximum Return at Maturity: | $240 to $280 per security (24% to 28% of the stated principal amount), to be determined on the pricing date. Because of the maximum return at maturity, the payment at maturity will not exceed $1,240 to $1,280 per security. |

| Buffer Value: | $ , 85.00% of the initial underlying value |

| Buffer Percentage: | 15.00% |

| Initial Underlying Value: | The closing value of the underlying on the pricing date |

| Final Underlying Value: | The closing value of the underlying on the valuation date |

| Underlying Return: | (final underlying value – initial underlying value) / initial underlying value |

| Calculation Agent: | CGMI |

| Denominations: | $1,000 and any integral multiple of $1,000 |

| CUSIP / ISIN: | 17329F4W1 / US17329F4W10 |

* Expected. To the extent that the issuer makes any change to the expected pricing date or expected issue date, the valuation date and maturity date may also be changed in the issuer’s discretion to ensure that the term of the securities remains the same.

PS-2

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

| Terms of the Securities |

The terms of the securities are set forth in the accompanying product supplement, prospectus supplement and prospectus, as supplemented by this pricing supplement. The accompanying product supplement, underlying supplement, prospectus supplement and prospectus contain important disclosures that are not repeated in this pricing supplement. For example, the accompanying product supplement contains important information about how the closing value of the underlying will be determined and other specified events with respect to the underlying. The accompanying underlying supplement contains information about the underlying that is not repeated in this pricing supplement. It is important that you read the accompanying product supplement, underlying supplement, prospectus supplement and prospectus together with this pricing supplement in deciding whether to invest in the securities. Certain terms used but not defined in this pricing supplement are defined in the accompanying product supplement.

When we refer to “we,” “us” and “our” in this pricing supplement, we refer only to Citigroup Global Market Holdings Inc. and not to any of its affiliates, including Citigroup Inc.

You may access the product supplement, underlying supplement and prospectus supplement and prospectus on the SEC website www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| • | Product Supplement No. EA-02-08 dated February 15, 2019: |

https://www.sec.gov/Archives/edgar/data/200245/000095010319002039/dp102379_424b2-psea0208par.htm

| • | Underlying Supplement No. 9 dated October 30, 2020: |

https://www.sec.gov/Archives/edgar/data/200245/000095010320021127/dp139820_424b2-us9.htm

| • | Prospectus Supplement and Prospectus, each dated May 14, 2018: |

https://www.sec.gov/Archives/edgar/data/200245/000119312518162183/d583728d424b2.htm

Prospectus. The first sentence of “Description of Debt Securities— Events of Default and Defaults” in the accompanying prospectus shall be amended to read in its entirety as follows:

Events of default under the indenture are:

| • | failure of Citigroup Global Markets Holdings or Citigroup to pay required interest on any debt security of such series for 30 days; | ||

| • | failure of Citigroup Global Markets Holdings or Citigroup to pay principal, other than a scheduled installment payment to a sinking fund, on any debt security of such series for 30 days; | ||

| • | failure of Citigroup Global Markets Holdings or Citigroup to make any required scheduled installment payment to a sinking fund for 30 days on debt securities of such series; | ||

| • | failure of Citigroup Global Markets Holdings to perform for 90 days after notice any other covenant in the indenture applicable to it other than a covenant included in the indenture solely for the benefit of a series of debt securities other than such series; and | ||

| • | certain events of bankruptcy or insolvency of Citigroup Global Markets Holdings, whether voluntary or not (Section 6.01). |

PS-3

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

| Investor Considerations |

We have designed the securities for investors who:

| · | seek 200% leveraged exposure to the positive performance of the underlying if the final underlying value is greater than the initial underlying value, subject to the maximum return at maturity; |

| · | desire to limit the downside exposure to the underlying through the buffer percentage; |

| · | understand that if the final underlying value is less than the initial underlying value by more than the buffer percentage, they will receive less, and possibly significantly less, than the stated principal amount per security at maturity; |

| · | are willing to forgo interest payments on the securities and dividends on the underlying; and |

| · | are willing to hold the securities to maturity. |

The securities are not designed for, and may not be a suitable investment for, investors who:

| · | seek a liquid investment or are unable or unwilling to hold the securities to maturity; |

| · | are unwilling to accept the risk that the value of the underlying may decrease by more than the buffer percentage from the initial underlying value to the final underlying value; |

| · | seek uncapped exposure to the upside performance of the underlying; |

| · | seek full return of the stated principal amount of the securities at maturity; |

| · | seek current income; |

| · | are unwilling to purchase securities with an estimated value as of the pricing date that is lower than the public offering price and that may be as low as the lower estimated value set forth on the cover page; |

| · | are unwilling to accept the risk of exposure to the energy sector; |

| · | seek exposure to the underlying but are unwilling to accept the risk/return trade-offs inherent in the payment at maturity for the securities; |

| · | are unwilling to accept the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc.; or |

| · | prefer the lower risk of fixed income investments with comparable maturities issued by companies with comparable credit ratings. |

PS-4

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

| Determining Payment at Maturity |

On the maturity date, you will receive a cash payment per security (the payment at maturity) calculated as follows:

PS-5

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

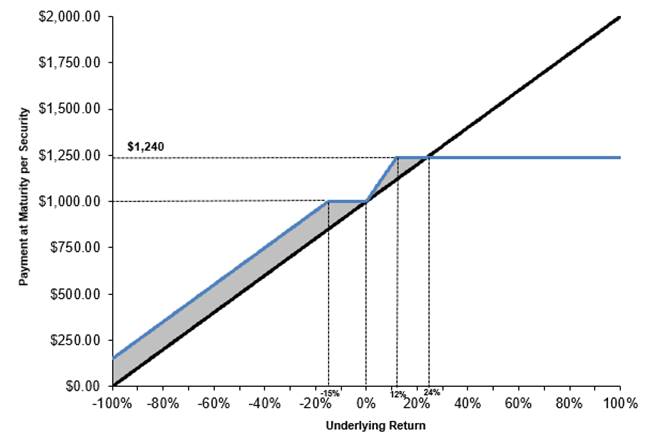

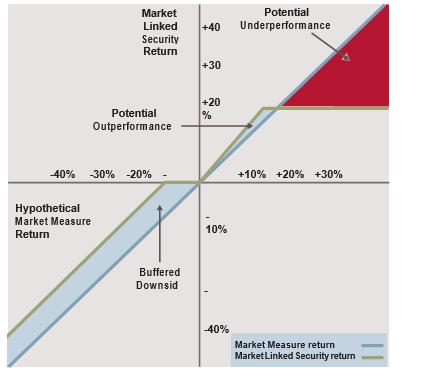

| Hypothetical Payout Profile |

The diagram below illustrates your payment at maturity for a range of hypothetical underlying returns. The diagram assumes that the maximum return at maturity will be set at the lowest value indicated in “Terms of the Securities” above. The actual maximum return at maturity will be determined on the pricing date. Your actual return will depend on the actual final underlying value, the actual maximum return at maturity and whether you hold your securities to maturity.

Investors in the securities will not receive any dividends with respect to the underlying. The diagram below does not show any effect of lost dividend yield over the term of the securities. See “Summary Risk Factors—You Will Not Receive Dividends Or Have Any Other Rights With Respect To The Underlying” below.

| n The Securities | n The Underlying |

PS-6

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

| Summary Risk Factors |

An investment in the securities is significantly riskier than an investment in conventional debt securities. The securities are subject to all of the risks associated with an investment in our conventional debt securities (guaranteed by Citigroup Inc.), including the risk that we and Citigroup Inc. may default on our obligations under the securities, and are also subject to risks associated with the underlying. Accordingly, the securities are suitable only for investors who are capable of understanding the complexities and risks of the securities. You should consult your own financial, tax and legal advisors as to the risks of an investment in the securities and the suitability of the securities in light of your particular circumstances.

The following is a summary of certain key risk factors for investors in the securities. You should read this summary together with the more detailed description of risks relating to an investment in the securities contained in the section “Risk Factors Relating to the Securities” beginning on page EA-7 in the accompanying product supplement. You should also carefully read the risk factors included in the accompanying prospectus supplement and in the documents incorporated by reference in the accompanying prospectus, including Citigroup Inc.’s most recent Annual Report on Form 10-K and any subsequent Quarterly Reports on Form 10-Q, which describe risks relating to the business of Citigroup Inc. more generally.

Citigroup Inc. will release quarterly earnings on April 15, 2021, which is during the marketing period and prior to pricing date of these securities.

You May Lose A Significant Portion Of Your Investment.

Unlike conventional debt securities, the securities do not repay a fixed amount of principal at maturity. Instead, your payment at maturity will depend on the performance of the underlying. If the underlying depreciates by more than the buffer percentage such that the final underlying value is less than the buffer value, you will lose 1% of the stated principal amount of the securities for every 1% by which that depreciation exceeds the buffer percentage.

The Securities Do Not Pay Interest.

Unlike conventional debt securities, the securities do not pay interest or any other amounts prior to maturity. You should not invest in the securities if you seek current income during the term of the securities.

Your Potential Return On The Securities Is Limited.

Your potential total return on the securities at maturity is limited to the maximum return at maturity. Your return on the securities will not exceed the maximum return at maturity, even if the underlying appreciates by significantly more than the maximum return at maturity. If the underlying appreciates by more than the maximum return at maturity, the securities will underperform an alternative investment providing 1-to-1 exposure to the performance of the underlying. When lost dividends are taken into account, the securities may underperform an alternative investment providing 1-to-1 exposure to the performance of the underlying and a pass-through of dividends even if the underlying appreciates by less than the maximum return at maturity. Furthermore, the effect of the participation rate will be progressively reduced for all final underlying values exceeding the final underlying value at which the maximum return at maturity is reached.

You Will Not Receive Dividends Or Have Any Other Rights With Respect To The Underlying.

You will not receive any dividends with respect to the underlying. This lost dividend yield may be significant over the term of the securities. The payment scenarios described in this pricing supplement do not show any effect of lost dividend yield over the term of the securities. In addition, you will not have voting rights or any other rights with respect to the underlying.

Your Payment At Maturity Depends On The Value Of The Underlying On A Single Day.

Because your payment at maturity depends on the value of the underlying solely on the valuation date, you are subject to the risk that the value of the underlying on that day may be lower, and possibly significantly lower, than on one or more other dates during the term of the securities. If you had invested in another instrument linked to the underlying that you could sell for full value at a time selected by you, or if the payment at maturity were based on an average of values of the underlying, you might have achieved better returns.

The Securities Are Subject To The Credit Risk Of Citigroup Global Markets Holdings Inc. And Citigroup Inc.

If we default on our obligations under the securities and Citigroup Inc. defaults on its guarantee obligations, you may not receive anything owed to you under the securities.

PS-7

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

The Securities Will Not Be Listed On Any Securities Exchange And You May Not Be Able To Sell Them Prior To Maturity.

The securities will not be listed on any securities exchange. Therefore, there may be little or no secondary market for the securities. We have been advised that Wells Fargo currently intends to make a secondary market in relation to the securities. However, Wells Fargo may suspend or terminate making a market without notice, at any time and for any reason. If Wells Fargo suspends or terminates making a market, there may be no secondary market at all for the securities because it is likely that Wells Fargo will be the only broker-dealer that is willing to buy your securities prior to maturity. Accordingly, an investor must be prepared to hold the securities until maturity.

The Estimated Value Of The Securities On The Pricing Date, Based On CGMI’s Proprietary Pricing Models And Our Internal Funding Rate, Is Less Than The Public Offering Price.

The difference is attributable to certain costs associated with selling, structuring and hedging the securities that are included in the public offering price. These costs include (i) any selling concessions or other fees paid in connection with the offering of the securities, (ii) hedging and other costs incurred by us and our affiliates in connection with the offering of the securities and (iii) the expected profit (which may be more or less than actual profit) to CGMI or other of our affiliates and/or Wells Fargo or its affiliates in connection with hedging our obligations under the securities. These costs adversely affect the economic terms of the securities because, if they were lower, the economic terms of the securities would be more favorable to you. The economic terms of the securities are also likely to be adversely affected by the use of our internal funding rate, rather than our secondary market rate, to price the securities. See “The Estimated Value Of The Securities Would Be Lower If It Were Calculated Based On Our Secondary Market Rate” below.

The Estimated Value Of The Securities Was Determined For Us By Our Affiliate Using Proprietary Pricing Models.

CGMI derived the estimated value disclosed on the cover page of this pricing supplement from its proprietary pricing models. In doing so, it may have made discretionary judgments about the inputs to its models, such as the volatility of the underlying, the dividend yield on the underlying and interest rates. CGMI’s views on these inputs may differ from your or others’ views, and as an underwriter in this offering, CGMI’s interests may conflict with yours. Both the models and the inputs to the models may prove to be wrong and therefore not an accurate reflection of the value of the securities. Moreover, the estimated value of the securities set forth on the cover page of this pricing supplement may differ from the value that we or our affiliates may determine for the securities for other purposes, including for accounting purposes. You should not invest in the securities because of the estimated value of the securities. Instead, you should be willing to hold the securities to maturity irrespective of the initial estimated value.

The Estimated Value Of The Securities Would Be Lower If It Were Calculated Based On Wells Fargo’s Determination of The Secondary Market Rate With Respect To Us.

The estimated value of the securities included in this pricing supplement is calculated based on our internal funding rate, which is the rate at which we are willing to borrow funds through the issuance of the securities. We expect that our internal funding rate is generally lower than Wells Fargo’s determination of the secondary market rate with respect to us, which is the rate that we expect Wells Fargo will use in determining the value of the securities for purposes of any purchases of the securities from you in the secondary market. If the estimated value included in this pricing supplement were based on Wells Fargo’s determination of the secondary market rate with respect to us, rather than our internal funding rate, it would likely be lower. We determine our internal funding rate based on factors such as the costs associated with the securities, which are generally higher than the costs associated with conventional debt securities, and our liquidity needs and preferences. Our internal funding rate is not an interest rate that is payable on the securities.

Because there is not an active market for traded instruments referencing our outstanding debt obligations, Wells Fargo may determine the secondary market rate with respect to us for purposes of any purchase of the securities from you in the secondary market based on the market price of traded instruments referencing the debt obligations of Citigroup Inc., our parent company and the guarantor of all payments due on the securities, but subject to adjustments that Wells Fargo may deem appropriate.

The Estimated Value Of The Securities Is Not An Indication Of The Price, If Any, At Which Any Person May Be Willing To Buy The Securities From You In The Secondary Market.

Any such secondary market price will fluctuate over the term of the securities based on the market and other factors described in the next risk factor. Moreover, unlike the estimated value included in this pricing supplement, we expect that any value of the securities determined for purposes of a secondary market transaction will be based on Wells Fargo’s determination of the secondary market rate with respect to us, which will likely result in a lower value for the securities than if our internal funding rate were used. In addition, we expect that any secondary market price for the securities will be reduced by a bid-ask spread, which may vary depending on the

PS-8

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

aggregate stated principal amount of the securities to be purchased in the secondary market transaction, and may be reduced by the expected cost of unwinding related hedging transactions. As a result, it is likely that any secondary market price for the securities will be less than the public offering price.

The Value Of The Securities Prior To Maturity Will Fluctuate Based On Many Unpredictable Factors.

The value of your securities prior to maturity will fluctuate based on the closing value of the underlying, the volatility of the closing value of the underlying, the dividend yield on the underlying, interest rates generally, the time remaining to maturity and our and Citigroup Inc.’s creditworthiness, as reflected in our secondary market rate, among other factors described under “Risk Factors Relating to the Securities—Risk Factors Relating to All Securities—The value of your securities prior to maturity will fluctuate based on many unpredictable factors” in the accompanying product supplement. Changes in the value of the underlying may not result in a comparable change in the value of your securities. You should understand that the value of your securities at any time prior to maturity may be significantly less than the public offering price.

We Have Been Advised That, Immediately Following Issuance, Any Secondary Market Bid Price Provided By Wells Fargo, And The Value That Will Be Indicated On Any Brokerage Account Statements Prepared By Wells Fargo Or Its Affiliates, Will Reflect A Temporary Upward Adjustment.

The amount of this temporary upward adjustment will steadily decline to zero over the temporary adjustment period. See “Valuation of the Securities” in this pricing supplement.

The Energy Select Sector SPDR® Fund Is Subject To Concentrated Risks Associated With The Energy Sector.

The stocks included in the index underlying the Energy Select Sector SPDR® Fund and that are generally tracked by the Energy Select Sector SPDR® Fund are stocks of companies whose primary business is directly associated with the energy sector, including the following two sub-sectors: (i) oil, gas and consumable fuels and (ii) energy equipment and services. Because the securities are linked to the performance of the Energy Select Sector SPDR® Fund, an investment in the securities exposes investors to concentrated risks associated with investments in the energy sector.

Energy companies develop and produce crude oil and natural gas and/or provide drilling and other energy resources production and distribution related services. Stock prices for these types of companies are mainly affected by the business, financial and operating conditions of the particular company, as well as changes in prices for oil, gas and other types of fuels, which in turn largely depend on supply and demand for various energy products and services. Some of the factors that may influence supply and demand for energy products and services include: general economic conditions and growth rates; weather conditions; the cost of exploring for, producing and delivering oil and gas; technological advances affecting energy efficiency and energy consumption; the ability of the Organization of Petroleum Exporting Countries (OPEC) to set and maintain production levels of oil; currency fluctuations; inflation; natural disasters; civil unrest, acts of sabotage or terrorism; and other regional or global events. The profitability of energy companies may also be adversely affected by existing and future laws, regulations, government actions and other legal requirements relating to protection of the environment, health and safety matters and others that may increase the costs of conducting their business or may reduce or delay available business opportunities. Increased supply or weak demand for energy products and services, as well as various developments leading to higher costs of doing business or missed business opportunities, would adversely impact the performance of companies in the energy sector. The value of the securities may be subject to greater volatility and be more adversely affected by a single economic, political or regulatory occurrence affecting the energy sector or one of the sub-sectors of the energy sector than a different investment linked to securities of a more broadly diversified group of issuers.

Our Offering Of The Securities Is Not A Recommendation Of The Underlying.

The fact that we are offering the securities does not mean that we or Wells Fargo or its affiliates believe that investing in an instrument linked to the underlying is likely to achieve favorable returns. In fact, as we and Wells Fargo and its affiliates are each part of respective global financial institutions, our affiliates and affiliates of Wells Fargo may have positions (including short positions) in the underlying or in instruments related to the underlying, and may publish research or express opinions, that in each case are inconsistent with an investment linked to the underlying. These and other activities of our affiliates or of Wells Fargo or its affiliates may affect the closing value of the underlying in a way that negatively affects the value of and your return on the securities.

The Closing Value Of The Underlying May Be Adversely Affected By Our Or Our Affiliates’, Or By Wells Fargo And Its Affiliates’, Hedging And Other Trading Activities.

We expect to hedge our obligations under the securities through CGMI or other of our affiliates and/or Wells Fargo or its affiliates, who may take positions in the underlying or in financial instruments related to the underlying and may adjust such positions during the

PS-9

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

term of the securities. Our affiliates and Wells Fargo and its affiliates may also take positions in the underlying or in financial instruments related to the underlying on a regular basis (taking long or short positions or both), for their accounts, for other accounts under their management or to facilitate transactions on behalf of customers. These activities could affect the closing value of the underlying in a way that negatively affects the value of and your return on the securities. They could also result in substantial returns for us or our affiliates or Wells Fargo and its affiliates while the value of the securities declines.

We And Our Affiliates And Wells Fargo And Its Affiliates May Have Economic Interests That Are Adverse To Yours As A Result Of Our And Their Respective Business Activities.

Our affiliates and Wells Fargo and its affiliates engage in business activities with a wide range of companies. These activities include extending loans, making and facilitating investments, underwriting securities offerings and providing advisory services. These activities could involve or affect the underlying in a way that negatively affects the value of and your return on the securities. They could also result in substantial returns for us or our affiliates or Wells Fargo or its affiliates while the value of the securities declines. In addition, in the course of this business, we or our affiliates or Wells Fargo or its affiliates may acquire non-public information, which will not be disclosed to you.

The Calculation Agent, Which Is An Affiliate Of Ours, Will Make Important Determinations With Respect To The Securities.

If certain events occur during the term of the securities, such as market disruption events and other events with respect to the underlying, CGMI, as calculation agent, will be required to make discretionary judgments that could significantly affect your return on the securities. In making these judgments, the calculation agent’s interests as an affiliate of ours could be adverse to your interests as a holder of the securities. See “Risk Factors Relating to the Securities—Risk Factors Relating to All Securities—The calculation agent, which is an affiliate of ours, will make important determinations with respect to the securities” in the accompanying product supplement.

Even If The Underlying Pays A Dividend That It Identifies As Special Or Extraordinary, No Adjustment Will Be Required Under The Securities For That Dividend Unless It Meets The Criteria Specified In The Accompanying Product Supplement.

In general, an adjustment will not be made under the terms of the securities for any cash dividend paid by the underlying unless the amount of the dividend per share, together with any other dividends paid in the same quarter, exceeds the dividend paid per share in the most recent quarter by an amount equal to at least 10% of the closing value of the underlying on the date of declaration of the dividend. Any dividend will reduce the closing value of the underlying by the amount of the dividend per share. If the underlying pays any dividend for which an adjustment is not made under the terms of the securities, holders of the securities will be adversely affected. See “Description of the Securities—Certain Additional Terms for Securities Linked to an Underlying Company or an Underlying ETF—Dilution and Reorganization Adjustments—Certain Extraordinary Cash Dividends” in the accompanying product supplement.

The Securities Will Not Be Adjusted For All Events That May Have A Dilutive Effect On Or Otherwise Adversely Affect The Closing Value Of The Underlying.

For example, we will not make any adjustment for ordinary dividends or extraordinary dividends that do not meet the criteria described above, partial tender offers or additional underlying share issuances. Moreover, the adjustments we do make may not fully offset the dilutive or adverse effect of the particular event. Investors in the securities may be adversely affected by such an event in a circumstance in which a direct holder of the underlying shares would not.

The Securities May Become Linked To An Underlying Other Than The Original Underlying Upon The Occurrence Of A Reorganization Event Or Upon The Delisting Of The Underlying Shares.

For example, if the underlying enters into a merger agreement that provides for holders of the underlying shares to receive shares of another entity and such shares are marketable securities, the closing value of the underlying following consummation of the merger will be based on the value of such other shares. Additionally, if the underlying shares are delisted, the calculation agent may select a successor underlying. See “Description of the Securities—Certain Additional Terms for Securities Linked to an Underlying Company or an Underlying ETF” in the accompanying product supplement.

The Value And Performance Of The Underlying Shares May Not Completely Track The Performance Of The Underlying Index That The Underlying Seeks To Track Or The Net Asset Value Per Share Of The Underlying.

The underlying does not fully replicate the underlying index that it seeks to track and may hold securities different from those included in its underlying index. In addition, the performance of the underlying will reflect additional transaction costs and fees that are not included in the calculation of its underlying index. All of these factors may lead to a lack of correlation between the performance of the underlying and its underlying index. In addition, corporate actions with respect to the equity securities held by the

PS-10

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

underlying (such as mergers and spin-offs) may impact the variance between the performance of the underlying and its underlying index. Finally, because the underlying shares are traded on an exchange and are subject to market supply and investor demand, the closing value of the underlying may differ from the net asset value per share of the underlying.

During periods of market volatility, securities included in the underlying’s underlying index may be unavailable in the secondary market, market participants may be unable to calculate accurately the net asset value per share of the underlying and the liquidity of the underlying may be adversely affected. This kind of market volatility may also disrupt the ability of market participants to create and redeem shares of the underlying. Further, market volatility may adversely affect, sometimes materially, the price at which market participants are willing to buy and sell the underlying shares. As a result, under these circumstances, the closing value of the underlying may vary substantially from the net asset value per share of the underlying. For all of the foregoing reasons, the performance of the underlying may not correlate with the performance of its underlying index and/or its net asset value per share, which could materially and adversely affect the value of the securities and/or reduce your return on the securities.

Changes That Affect The Underlying May Affect The Value Of Your Securities.

The sponsor of the underlying may at any time make methodological changes or other changes in the manner in which it operates that could affect the value of the underlying. We are not affiliated with the underlying sponsor and, accordingly, we have no control over any changes such sponsor may make. Such changes could adversely affect the performance of the underlying and the value of and your return on the securities.

The Stated Maturity Date May Be Postponed If The Valuation Date is Postponed.

The valuation date will be postponed if the originally scheduled valuation date is not a trading day or if the calculation agent determines that a market disruption event has occurred or is continuing on the valuation date. If such a postponement occurs, the stated maturity date will be the later of (i) the initial stated maturity date and (ii) three business days after the valuation date as postponed.

The U.S. Federal Tax Consequences Of An Investment In The Securities Are Unclear.

There is no direct legal authority regarding the proper U.S. federal tax treatment of the securities, and we do not plan to request a ruling from the Internal Revenue Service (the “IRS”). Consequently, significant aspects of the tax treatment of the securities are uncertain, and the IRS or a court might not agree with the treatment of the securities as prepaid forward contracts. If the IRS were successful in asserting an alternative treatment of the securities, the tax consequences of the ownership and disposition of the securities might be materially and adversely affected. Even if the treatment of the securities as prepaid forward contracts is respected, a security may be treated as a “constructive ownership transaction,” with potentially adverse consequences described below under “United States Federal Tax Considerations.” Moreover, future legislation, Treasury regulations or IRS guidance could adversely affect the U.S. federal tax treatment of the securities, possibly retroactively.

If you are a non-U.S. investor, you should review the discussion of withholding tax issues in “United States Federal Tax Considerations—Non-U.S. Holders” below.

You should read carefully the discussion under “United States Federal Tax Considerations” and “Risk Factors Relating to the Securities” in the accompanying product supplement and “United States Federal Tax Considerations” in this pricing supplement. You should also consult your tax adviser regarding the U.S. federal tax consequences of an investment in the securities, as well as tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

PS-11

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

| Hypothetical Returns |

The table below is based on a range of hypothetical underlying returns and illustrates:

| • | the hypothetical underlying return; |

| • | the hypothetical payment at maturity per security; and |

| • | the hypothetical total pre-tax rate of return. |

The table below is based on a hypothetical initial underlying value of 100 and does not reflect the actual initial underlying value. The table below assumes that the maximum return at maturity will be set at the lowest value indicated in “Terms of the Securities” above. The actual maximum return at maturity will be determined on the pricing date.

Hypothetical final underlying value | Hypothetical underlying return

| Hypothetical payment at maturity per security | Hypothetical total pre-tax rate of return |

| $200.00 | 100.00% | $1,240.00 | 24.00% |

| $175.00 | 75.00% | $1,240.00 | 24.00% |

| $150.00 | 50.00% | $1,240.00 | 24.00% |

| $140.00 | 40.00% | $1,240.00 | 24.00% |

| $130.00 | 30.00% | $1,240.00 | 24.00% |

| $120.00 | 20.00% | $1,240.00 | 24.00% |

| $110.00 | 10.00% | $1,200.00 | 20.00% |

| $105.00 | 5.00% | $1,100.00 | 10.00% |

| $100.00 | 0.00% | $1,000.00 | 0.00% |

| $95.00 | -5.00% | $1,000.00 | 0.00% |

| $90.00 | -10.00% | $1,000.00 | 0.00% |

| $85.00 | -15.00% | $1,000.00 | 0.00% |

| $84.99 | -15.01% | $999.90 | -0.01% |

| $80.00 | -20.00% | $950.00 | -5.00% |

| $70.00 | -30.00% | $850.00 | -15.00% |

| $60.00 | -40.00% | $750.00 | -25.00% |

| $50.00 | -50.00% | $650.00 | -35.00% |

| $25.00 | -75.00% | $400.00 | -60.00% |

| $0.00 | -100.00% | $150.00 | -85.00% |

The above figures are for purposes of illustration only and may have been rounded for ease of analysis.

PS-12

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

| Hypothetical Examples |

The examples below illustrate how to determine the payment at maturity on the securities, assuming the various hypothetical final underlying values indicated below. The examples are solely for illustrative purposes, do not show all possible outcomes and are not a prediction of what the actual payment at maturity on the securities will be. The actual payment at maturity will depend on the actual final underlying value.

The examples below are based on a hypothetical initial underlying value of 100, rather than the actual initial underlying value. For the actual initial underlying value, see “Terms of the Securities” above. We have used this hypothetical value, rather than the actual value, to simplify the calculations and aid understanding of how the securities work. However, you should understand that the actual payment at maturity on the securities will be calculated based on the actual initial underlying value, and not the hypothetical value indicated below. The examples below assume that the maximum return at maturity will be set at the lowest value indicated in “Terms of the Securities” above. The actual maximum return at maturity will be determined on the pricing date.

Example 1—Upside Scenario A. The hypothetical final underlying value is 105 (a 5% increase from the initial underlying value), which is greater than the initial underlying value.

Payment at maturity per security = $1,000 plus the lesser of:

(i) $1,000 × final underlying value – initial underlying value × participation rate and (ii) the maximum return at maturity

initial underlying value

= $1,000 + the lesser of : (i) ($1,000 × 105 – 100 × participation rate) and (ii) $240

100

= $1,000 + the lesser of: (i) ($1,000 × 5% × 200%) and (ii) $240

= $1,000 + the lesser of (i) $100 and (ii) $240

= $1,100

Because the underlying appreciated from the initial underlying value to the hypothetical final underlying value, you would receive a total return at maturity equal to the upside performance of the underlying multiplied by the participation rate, which in this case is less than the maximum return at maturity.

Example 2—Upside Scenario B. The hypothetical final underlying value is 150 (a 50% increase from the initial underlying value), which is greater than the initial underlying value.

Payment at maturity per security = $1,000 plus the lesser of:

(i) $1,000 × final underlying value – initial underlying value × participation rate and (ii) the maximum return at maturity

initial underlying value

= $1,000 + the lesser of : (i) ($1,000 × 150 – 100 × participation rate) and (ii) $240

100

= $1,000 + the lesser of: (i) ($1,000 × 50% × 200%) and (ii) $240

= $1,000 + the lesser of (i) $1,000 and (ii) $240

= $1,240

Because the underlying appreciated from the initial underlying value to the hypothetical final underlying value and the upside performance of the underlying multiplied by the participation rate exceeds the maximum return at maturity, your total return at maturity would be limited to the maximum return at maturity in this case. In this scenario, an investment in the securities would underperform a hypothetical alternative investment providing 1-to-1 exposure to the appreciation of the underlying without a maximum return.

PS-13

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

Example 3—Par Scenario. The hypothetical final underlying value is 95 (a 5% decrease from the initial underlying value), which is less than the initial underlying value but greater than the buffer value.

Payment at maturity per security = $1,000

Because the hypothetical final underlying value is less than the initial underlying value but greater than the buffer value, you would be repaid the stated principal amount of your securities at maturity but would not receive any positive return on your investment.

Example 4—Downside Scenario. The hypothetical final underlying value is 50 (a 50% decrease from the initial underlying value), which is less than the buffer value.

Payment at maturity per security = $1,000 - ($1,000 × buffer value – final underlying value )

initial underlying value

= $1,000 – ($1,000 × 85 – 50)

100

= $1,000 - ($1,000 × 35%)

= $1,000 - $350

= $650

Because the underlying depreciated from the initial underlying value to the hypothetical final underlying value by more than the buffer percentage, such that the hypothetical final underlying value is less than the buffer value, your payment at maturity in this scenario would reflect 1-to-1 exposure to the negative performance of the underlying beyond the buffer percentage.

PS-14

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

| Additional Terms of the Securities |

The following provisions supersede the provisions in the product supplement to the extent that they are inconsistent from those provisions.

Certain Definitions

The “closing value” of the underlying on any date is the closing price of its underlying shares on such date, subject to adjustment as provided in the accompanying product supplement. The “underlying shares” of the underlying are its shares that are traded on a U.S. national securities exchange on the pricing date. Please see the accompanying product supplement for more information.

A “trading day” means a day, as determined by the calculation agent, on which the relevant stock exchange and each related futures or options exchange with respect to the underlying or any successor thereto, if applicable, are scheduled to be open for trading for their respective regular trading sessions.

The “relevant stock exchange” for the underlying means the primary exchange or quotation system on which shares (or other applicable securities) of the underlying are traded, as determined by the calculation agent.

The “related futures or options exchange” for the underlying means an exchange or quotation system where trading has a material effect (as determined by the calculation agent) on the overall market for futures or options contracts relating to the underlying.

Postponement of the Valuation Date

If the scheduled valuation date is not a trading day, the valuation date will be postponed to the next succeeding day that is a trading day. The valuation date is also subject to postponement due to the occurrence of a market disruption event. See “—Market Disruption Events.”

Market Disruption Events

A “market disruption event” with respect to the underlying means any of the following events as determined by the calculation agent in its sole discretion:

| (A) | The occurrence or existence of a material suspension of or limitation imposed on trading by the relevant stock exchange or otherwise relating to the shares (or other applicable securities) of the underlying or any successor underlying on the relevant stock exchange at any time during the one-hour period that ends at the close of trading on that day, whether by reason of movements in price exceeding limits permitted by that relevant stock exchange or otherwise. |

| (B) | The occurrence or existence of a material suspension of or limitation imposed on trading by any related futures or options exchange or otherwise in futures or options contracts relating to the shares (or other applicable securities) of the underlying or any successor underlying on any related futures or options exchange at any time during the one-hour period that ends at the close of trading on that day, whether by reason of movements in price exceeding limits permitted by the related futures or options exchange or otherwise. |

| (C) | The occurrence or existence of any event, other than an early closure, that materially disrupts or impairs the ability of market participants in general to effect transactions in, or obtain market values for, shares (or other applicable securities) of the underlying or any successor underlying on the relevant stock exchange at any time during the one-hour period that ends at the close of trading on that day. |

| (D) | The occurrence or existence of any event, other than an early closure, that materially disrupts or impairs the ability of market participants in general to effect transactions in, or obtain market values for, futures or options contracts relating to shares (or other applicable securities) of the underlying or any successor underlying on any related futures or options exchange at any time during the one-hour period that ends at the close of trading on that day. |

| (E) | The closure of the relevant stock exchange or any related futures or options exchange with respect to the underlying or any successor underlying prior to its scheduled closing time unless the earlier closing time is announced by the relevant stock |

PS-15

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

exchange or related futures or options exchange, as applicable, at least one hour prior to the earlier of (1) the actual closing time for the regular trading session on such relevant stock exchange or related futures or options exchange, as applicable, and (2) the submission deadline for orders to be entered into the relevant stock exchange or related futures or options exchange, as applicable, system for execution at the close of trading on that day.

| (F) | The relevant stock exchange or any related futures or options exchange with respect to the underlying or any successor underlying fails to open for trading during its regular trading session. |

For purposes of determining whether a market disruption event has occurred with respect to the underlying:

| (1) | “close of trading” means the scheduled closing time of the relevant stock exchange with respect to the underlying or any successor underlying; and |

| (2) | the “scheduled closing time” of the relevant stock exchange or any related futures or options exchange on any trading day for the underlying or any successor underlying means the scheduled weekday closing time of such relevant stock exchange or related futures or options exchange on such trading day, without regard to after hours or any other trading outside the regular trading session hours. |

If a market disruption event occurs or is continuing on the valuation date, then the valuation date will be postponed to the first succeeding trading day on which a market disruption event has not occurred and is not continuing; however, if such first succeeding trading day has not occurred as of the eighth trading day after the originally scheduled valuation date, that eighth trading day shall be deemed to be the valuation date. If the valuation date has been postponed eight trading days after the originally scheduled valuation date and a market disruption event occurs or is continuing on such eighth trading day, the calculation agent will determine the closing value of the underlying on such eighth trading day based on its good faith estimate of the value of the underlying shares of the underlying as of the close of trading on such eighth trading day.

Delisting, Liquidation or Termination of the Underlying

If the closing value of the underlying is determined by reference to the underlying index as described in the accompanying product supplement in the section “Description of the Securities—Certain Additional Terms for Securities Linked to an Underlying Company or an Underlying ETF—Delisting, Liquidation or Termination of an Underlying ETF”, and at any time the publisher of the underlying index (i) announces that it will make a material change in the formula for or the method of calculating the underlying index or in any other way materially modifies the underlying index (other than a modification prescribed in that formula or method to maintain the underlying index in the event of changes in constituent stock and capitalization and other routine events) or (ii) permanently cancels the underlying index and no successor underlying index is chosen as described in the accompanying product supplement, then the calculation agent will calculate the closing value of the underlying index of the underlying in accordance with the formula last used to calculate such closing value before such event, but using only those securities that were held by the underlying index of the underlying immediately prior to such event without any rebalancing or substitution of such securities following such event. Such value, as calculated by the calculation agent, will be substituted for the relevant value of the underlying index for all purposes. In such event, the calculation agent will make such adjustments, if any, to any level of the underlying index that is used for purposes of the securities as it determines are appropriate in the circumstances.

PS-16

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

| Information About the Energy Select Sector SPDR® Fund |

The Energy Select Sector SPDR® Fund is an exchange-traded fund that seeks to provide investment results that, before expenses, correspond generally to the performance of publicly traded equity securities of companies in the S&P Energy Select Sector Index. The S&P Energy Select Sector Index is intended to provide an indication of the pattern of common stock price movements of companies that are components of the S&P 500® Index and are involved in the development or production of energy. The S&P Energy Select Sector Index includes companies in the following two industries: (i) oil, gas and consumable fuels and (ii) energy equipment and services. The Energy Select Sector SPDR® Fund is managed by the Select Sector SPDR® Trust, a registered investment company. The Select Sector SPDR® Trust consists of numerous separate investment portfolios, including the Energy Select Sector SPDR® Fund.

Information provided to or filed with the SEC by the Select Sector SPDR® Trust pursuant to the Securities Act of 1933, as amended, and the Investment Company Act of 1940, as amended, can be located by reference to SEC file numbers 333-57791 and 811-08837, respectively, through the SEC’s website at http://www.sec.gov. In addition, information may be obtained from other sources including, but not limited to, press releases, newspaper articles and other publicly disseminated documents. The underlying shares of the Energy Select Sector SPDR® Fund trade on the NYSE Arca under the ticker symbol “XLE.”

Please refer to the section “Fund Descriptions—The Select Sector SPDR® Funds” in the accompanying underlying supplement for additional information.

We have derived all information regarding the Energy Select Sector SPDR® Fund from publicly available information and have not independently verified any information regarding the Energy Select Sector SPDR® Fund. This pricing supplement relates only to the securities and not to the Energy Select Sector SPDR® Fund. We make no representation as to the performance of the Energy Select Sector SPDR® Fund over the term of the securities.

The securities represent obligations of Citigroup Global Markets Holdings Inc. (guaranteed by Citigroup Inc.) only. The sponsor of the Energy Select Sector SPDR® Fund is not involved in any way in this offering and has no obligation relating to the securities or to holders of the securities.

Historical Information

The closing value of the Energy Select Sector SPDR® Fund on March 29, 2021 was $49.83.

The graph below shows the closing value of the Energy Select Sector SPDR® Fund for each day such value was available from January 4, 2016 to March 29, 2021. We obtained the closing values from Bloomberg L.P., without independent verification. You should not take historical closing values as an indication of future performance.

PS-17

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

| United States Federal Tax Considerations |

You should read carefully the discussion under “United States Federal Tax Considerations” and “Risk Factors Relating to the Securities” in the accompanying product supplement and “Summary Risk Factors” in this pricing supplement.

In the opinion of our counsel, Davis Polk & Wardwell LLP, a security should be treated as a prepaid forward contract for U.S. federal income tax purposes. By purchasing a security, you agree (in the absence of an administrative determination or judicial ruling to the contrary) to this treatment. There is uncertainty regarding this treatment, and the IRS or a court might not agree with it. Moreover, our counsel’s opinion is based on market conditions as of the date of this preliminary pricing supplement and is subject to confirmation on the pricing date.

Assuming this treatment of the securities is respected and subject to the discussion in “United States Federal Tax Considerations” in the accompanying product supplement, the following U.S. federal income tax consequences should result under current law:

| · | You should not recognize taxable income over the term of the securities prior to maturity, other than pursuant to a sale or exchange. |

| · | Upon a sale or exchange of a security (including retirement at maturity), you should recognize gain or loss equal to the difference between the amount realized and your tax basis in the security. Subject to the discussion below concerning the potential application of the “constructive ownership” rules under Section 1260 of the Code, any gain or loss recognized upon a sale, exchange or retirement of a security should be long-term capital gain or loss if you held the security for more than one year. |

Even if the treatment of the securities as prepaid forward contracts is respected, your purchase of a security may be treated as entry into a “constructive ownership transaction,” within the meaning of Section 1260 of the Code. In that case, all or a portion of any long-term capital gain you would otherwise recognize in respect of your securities would be recharacterized as ordinary income to the extent such gain exceeded the “net underlying long-term capital gain.” Any long-term capital gain recharacterized as ordinary income under Section 1260 would be treated as accruing at a constant rate over the period you held your securities, and you would be subject to an interest charge in respect of the deemed tax liability on the income treated as accruing in prior tax years. Due to the lack of governing authority under Section 1260, our counsel is not able to opine as to whether or how Section 1260 applies to the securities. You should read the section entitled “United States Federal Tax Considerations—Tax Consequences to U.S. Holders—Potential Application of Section 1260 of the Code” in the accompanying product supplement for additional information and consult your tax adviser regarding the potential application of the “constructive ownership” rule.

We do not plan to request a ruling from the IRS regarding the treatment of the securities. An alternative characterization of the securities could materially and adversely affect the tax consequences of ownership and disposition of the securities, including the timing and character of income recognized. In addition, the U.S. Treasury Department and the IRS have requested comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar financial instruments and have indicated that such transactions may be the subject of future regulations or other guidance. Furthermore, members of Congress have proposed legislative changes to the tax treatment of derivative contracts. Any legislation, Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the securities, possibly with retroactive effect. You should consult your tax adviser regarding possible alternative tax treatments of the securities and potential changes in applicable law.

Non-U.S. Holders. Subject to the discussions below and in “United States Federal Tax Considerations” in the accompanying product supplement, if you are a Non-U.S. Holder (as defined in the accompanying product supplement) of the securities, you generally should not be subject to U.S. federal withholding or income tax in respect of any amount paid to you with respect to the securities, provided that (i) income in respect of the securities is not effectively connected with your conduct of a trade or business in the United States, and (ii) you comply with the applicable certification requirements.

As discussed under “United States Federal Tax Considerations—Tax Consequences to Non-U.S. Holders” in the accompanying product supplement, Section 871(m) of the Code and Treasury regulations promulgated thereunder (“Section 871(m)”) generally impose a 30% withholding tax on dividend equivalents paid or deemed paid to Non-U.S. Holders with respect to certain financial instruments linked to U.S. equities (“U.S. Underlying Equities”) or indices that include U.S. Underlying Equities. Section 871(m) generally applies to instruments that substantially replicate the economic performance of one or more U.S. Underlying Equities, as determined based on tests set forth in the applicable Treasury regulations. However, the regulations, as modified by an IRS notice, exempt financial instruments issued prior to January 1, 2023 that do not have a “delta” of one. Based on the terms of the securities and representations provided by us as of the date of this preliminary pricing supplement, our counsel is of the opinion that the securities should not be treated as transactions that have a “delta” of one within the meaning of the regulations with respect to any U.S. Underlying Equity and, therefore, should not be subject to withholding tax under Section 871(m). However, the final

PS-18

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

determination regarding the treatment of the securities under Section 871(m) will be made as of the pricing date for the securities, and it is possible that the securities will be subject to withholding tax under Section 871(m) based on the circumstances as of that date.

A determination that the securities are not subject to Section 871(m) is not binding on the IRS, and the IRS may disagree with this treatment. Moreover, Section 871(m) is complex and its application may depend on your particular circumstances, including your other transactions. You should consult your tax adviser regarding the potential application of Section 871(m) to the securities.

If withholding tax applies to the securities, we will not be required to pay any additional amounts with respect to amounts withheld.

You should read the section entitled “United States Federal Tax Considerations” in the accompanying product supplement. The preceding discussion, when read in combination with that section, constitutes the full opinion of Davis Polk & Wardwell LLP regarding the material U.S. federal tax consequences of owning and disposing of the securities.

You should also consult your tax adviser regarding all aspects of the U.S. federal income and estate tax consequences of an investment in the securities and any tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

PS-19

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

| Supplemental Plan of Distribution |

Pursuant to the terms of the Amended and Restated Global Selling Agency Agreement, dated April 7, 2017, CGMI, acting as principal, will purchase the securities from Citigroup Global Markets Holdings Inc. CGMI, as the lead agent for the offering, expects to sell the securities to Wells Fargo, as agent. Wells Fargo will receive an underwriting discount and commission of up to 3.15% ($31.50) for each security it sells. Wells Fargo will pay selected dealers, which may include WFA, a fixed selling commission of 1.75% ($17.50) for each security they sell. In addition to the selling commission allowed to WFA, Wells Fargo will pay $0.75 per security of the underwriting discount and commission to WFA as a distribution expense fee for each security sold by WFA.

In addition, in respect of certain securities sold in this offering, CGMI may pay a fee of up to $1.00 per security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the securities to other securities dealers.

The public offering price of the securities includes the underwriting discount and commission described on the cover page of this pricing supplement and the estimated cost of hedging our obligations under the securities. We expect to hedge our obligations under the securities through affiliated or unaffiliated counterparties, which may include our affiliates or affiliates of Wells Fargo. Our cost of hedging will include the projected profit that such counterparties, which may include our affiliates and affiliates of Wells Fargo, expect to realize in consideration for assuming the risks inherent in hedging our obligations under the securities. Because hedging our obligations entails risks and may be influenced by market forces beyond the control of any counterparty, which may include our affiliates and affiliates of Wells Fargo, such hedging may result in a profit that is more or less than expected, or could result in a loss.

This pricing supplement and the accompanying product supplement, underlying supplement, prospectus supplement and prospectus may be used by Wells Fargo or an affiliate of Wells Fargo in connection with offers and sales related to market-making or other transactions in the securities. Wells Fargo or an affiliate of Wells Fargo may act as principal or agent in such transactions. Such sales will be made at prices related to prevailing market prices at the time of sale or otherwise.

No action has been or will be taken by Citigroup Global Markets Holdings Inc., Wells Fargo or any broker-dealer affiliates of any of them that would permit a public offering of the securities or possession or distribution of this pricing supplement or the accompanying product supplement, underlying supplement, prospectus supplement or prospectus in any jurisdiction, other than the United States, where action for that purpose is required. No offers, sales or deliveries of the securities, or distribution of this pricing supplement, the accompanying product supplement, underlying supplement or prospectus supplement and prospectus, may be made in or from any jurisdiction except in circumstances that will result in compliance with any applicable laws and regulations and will not impose any obligations on Citigroup Global Markets Holdings Inc., Wells Fargo or any broker-dealer affiliates of any of them.

For the following jurisdictions, please note specifically:

Argentina

Citigroup Global Markets Holdings Inc.’s Series N Medium-Term Senior Notes program and the related offer of the securities and the sale of the securities under the terms and conditions provided herein does not constitute a public offering in Argentina. Consequently, no public offering approval has been requested or granted by the Comisión Nacional de Valores, nor has any listing authorization of the securities been requested on any stock market in Argentina.

Brazil

The securities may not be offered or sold to the public in Brazil. Accordingly, this pricing supplement and the accompanying prospectus supplement and prospectus have not been submitted to the Comissão de Valores Mobiliáros for approval. Documents relating to this offering may not be supplied to the public as a public offering in Brazil or be used in connection with any offer for subscription or sale to the public in Brazil.

Chile

The securities have not been registered with the Superintendencia de Valores y Seguros in Chile and may not be offered or sold publicly in Chile. No offer, sales or deliveries of the securities, or distribution of this pricing supplement or the prospectus supplement and prospectus, may be made in or from Chile except in circumstances that will result in compliance with any applicable Chilean laws and regulations.

PS-20

Market Linked Securities—Leveraged Upside Participation to a Cap and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due May 5, 2023 | |

Mexico

The securities have not been registered with the National Registry of Securities maintained by the Mexican National Banking and Securities Commission and may not be offered or sold publicly in Mexico. This pricing supplement and the accompanying prospectus supplement and prospectus may not be publicly distributed in Mexico.

Paraguay

This is a private and personal offering. The securities offered have not been approved by or registered with the National Securities Commission (Comisión Nacional de Valores) and are not part of a public offering as defined by the Paraguayan Securities Law. The information contained herein is for informational and marketing purposes only and should not be taken as an investment advice.

Peru

The securities have not been and will not be registered with the Capital Markets Public Registry of the Capital Markets Superintendence (SMV) nor the Lima Stock Exchange Registry (RBVL) for their public offering in Peru under the Peruvian Capital Markets Law (Law N°861/ Supreme Decree N°093-2002) and the decrees and regulations thereunder.

Consequently, the securities may not be offered or sold, directly or indirectly, nor may this pricing supplement and the accompanying product supplement, prospectus supplement and prospectus or any other offering material relating to the securities be distributed or caused to be distributed in Peru to the general public. The securities may only be offered in a private offering without using mass marketing, which is defined as a marketing strategy utilizing mass distribution and mass media to offer, negotiate or distribute securities to the whole market. Mass media includes newspapers, magazines, radio, television, mail, meetings, social networks, Internet servers located in Peru, and other media or technology platforms.

Taiwan

These securities may be made available outside Taiwan for purchase by Taiwan residents outside Taiwan but may not be offered or sold in Taiwan.

| Valuation of the Securities |