| Citigroup Global Markets Holdings Inc. | December 19, 2023 Medium-Term Senior Notes, Series N Pricing Supplement No. 2023-USNCH19886 Filed Pursuant to Rule 424(b)(2) Registration Statement Nos. 333-270327 and 333-270327-01 |

Floating Rate Notes Due December 21, 2063

| · | The notes will pay interest at a floating rate based on SOFR (compounded daily during the relevant observation period) plus the floating rate spread specified below, subject to a minimum interest rate of 0.00%. Interest payments on the notes will vary and may be paid at a rate as low as 0.00% per annum. |

| · | You may request that we repurchase your notes on an annual basis (i.e., once every twelve months) beginning approximately four years after the original issue date, subject to your compliance with the minimum repurchase amount, the procedural requirements and the other limitations set forth under “Key Terms” on page PS-2 and in “Annex A—Supplemental Terms of Notes—Early Repurchase” of this pricing supplement. You will receive less than your principal amount if you request that we repurchase your notes on any repurchase date on or prior to December 21, 2032 |

| · | The notes are unsecured and unsubordinated debt securities issued by Citigroup Global Markets Holdings Inc. and guaranteed by Citigroup Inc. All payments on the notes are subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc. |

| · | It is important for you to consider the information contained in this pricing supplement together with the information contained in the accompanying prospectus supplement and prospectus. The description of the notes below supplements, and to the extent inconsistent with replaces, the description of the general terms of the notes set forth in the accompanying prospectus supplement and prospectus. |

| KEY TERMS | |||

| Issuer: | Citigroup Global Markets Holdings Inc., a wholly owned subsidiary of Citigroup Inc. | ||

| Guarantee: | All payments due on the notes are fully and unconditionally guaranteed by Citigroup Inc. | ||

| Stated principal amount: | $1,000 per note | ||

| Pricing date: | December 19, 2023 | ||

| Original issue date: | December 21, 2023 | ||

| Maturity date: | December 21, 2063. If the maturity date is not a business day, then such date will be postponed to the next succeeding business day. | ||

| Principal due at maturity: | Full principal amount due at maturity | ||

| Payment at maturity: | Unless earlier repurchased, $1,000 per note plus any accrued and unpaid interest | ||

| Interest rate per annum: | For each interest period, the notes will bear interest at a floating rate per annum equal to SOFR (compounded daily over the relevant observation period as described under “Determination of SOFR” below) plus a spread of 0.10% (the “floating rate spread”), subject to a minimum interest rate of 0.00% per annum for any interest period | ||

| Interest period: | Each period from, and including, an interest payment date (or, in the case of the first interest period, the original issue date) to, but excluding, the next succeeding interest payment date. | ||

| Observation period: | For each interest period, the period from, and including, the date two U.S. government securities business days preceding the first date in such interest period to, but excluding, the date two U.S. government securities business days preceding the interest payment date for such interest period. The observation period will not be adjusted if any interest payment date is postponed. | ||

| Interest payment dates: | The 21st day of each March, June, September and December, commencing on March 21, 2024 and ending on the maturity date or, if applicable, the applicable repurchase date. In the event that any interest payment date is not a business day, then such date will be postponed to the next succeeding business day. | ||

| Day count convention: | See “Determination of Interest Payments” in this pricing supplement. | ||

| Business day: | Any weekday that is not a legal holiday in New York City and is not a day on which banking institutions in New York City are authorized or required by law or regulation to be closed and is a U.S. government securities business day. | ||

| U.S. government securities business day: | Any day except for a Saturday, a Sunday or a day on which the Securities Industry and Financial Markets Association recommends that the fixed income departments of its members be closed for the entire day for purposes of trading in U.S. government securities | ||

| Business day convention: | Following | ||

| CUSIP / ISIN: | 17291TWR5 / US17291TWR57 | ||

| Listing: | The notes will not be listed on any securities exchange and, accordingly, may have limited or no market liquidity. | ||

| Underwriter: | Citigroup Global Markets Inc. (“CGMI”), an affiliate of the issuer, acting as principal. See “General Information—Supplemental information regarding plan of distribution; conflicts of interest” in this pricing supplement. | ||

| Underwriting fee and issue price: | Issue price | Underwriting fee(1) | Proceeds to issuer(2) |

| Per note: | $1,000 | $10 | $990 |

| Total: | $7,995,000 | $79,950 | $7,915,050 |

(Key Terms continued on next page)

(1) CGMI, an affiliate of Citigroup Global Markets Holdings Inc. and the underwriter of the sale of the notes, is acting as principal and will receive an underwriting fee of up to $10 for each $1,000 note sold in this offering. The total underwriting fee and proceeds to issuer in the table above give effect to the actual total underwriting fee. Selected dealers not affiliated with CGMI will receive a selling concession of up to $10 for each note they sell. See “General Information—Fees and selling concessions” in this pricing supplement. In addition to the underwriting fee, CGMI and its affiliates may profit from hedging activity related to this offering, even if the value of the notes declines. See “Use of Proceeds and Hedging” in the accompanying prospectus.

(2) The per note proceeds to issuer indicated above represent the minimum per note proceeds to issuer for any note, assuming the maximum per note underwriting fee. As noted above, the underwriting fee is variable.

Investing in the notes involves risks not associated with an investment in conventional fixed rate debt securities. See “Risk Factors” beginning on page PS-3.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the notes or determined that this pricing supplement and the accompanying prospectus supplement and prospectus are truthful or complete. Any representation to the contrary is a criminal offense.

You should read this pricing supplement together with the accompanying prospectus supplement and prospectus, which can be accessed via the hyperlink below:

Prospectus Supplement and Prospectus each dated March 7, 2023

The notes are not bank deposits and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency, nor are they obligations of, or guaranteed by, a bank.

The issuer is not affiliated with the Federal Reserve Bank of New York. The Federal Reserve Bank of New York does not sanction, endorse, or recommend any products or services offered by the issuer.

| Citigroup Global Markets Holdings Inc. |

| KEY TERMS (continued) | |

| Early repurchase: | You may request that we repurchase all or any portion of your notes on any repurchase date on or after December 21, 2027 (the “initial repurchase date”) by following the procedures described under “Annex A—Supplemental Terms of Notes—Early Repurchase,” which will include us receiving a repurchase notice by no later than 4:00 p.m., New York City time, fifteen business days prior to the relevant repurchase date. If you fail to comply with these procedures, your notice will be deemed ineffective. To exercise the early repurchase right, you must submit notes for repurchase having an aggregate stated principal amount equal to the minimum repurchase amount of $100,000 or an integral multiple of $1,000 in excess thereof. |

| Repurchase amount: | Upon early repurchase, you will receive for each $1,000 stated principal amount note, on the applicable repurchase date, a cash “repurchase amount” equal to the following amount, as applicable, plus any accrued and unpaid interest: |

| Repurchase dates occurring: | ||

| From and including December 21, 2027 to and including December 21, 2029 | $980 | |

| From and including December 21, 2030 to and including December 21, 2032 | $990 | |

| From and including December 21, 2033 to but excluding the maturity date | $1,000 |

You may request that we repurchase your notes on an annual basis (i.e., once every twelve months) on or after the initial repurchase date, subject to your compliance with the minimum repurchase amount, the procedural requirements and the other limitations set forth herein and under “Annex A—Supplemental Terms of Notes—Early Repurchase.” You will receive less than your stated principal amount per note if you request that we repurchase your notes on any repurchase date on or prior to December 21, 2032.

Depending on market conditions, including changes in interest rates, it is possible that the value of the notes in the secondary market at any time may be greater than the repurchase amount. Accordingly, prior to exercising the early repurchase right described above, you should contact the broker or other entity through which the notes are held to determine whether a sale of the notes in the secondary market may result in greater proceeds than the repurchase amount. |

| Repurchase dates: | $980 repurchase amount December 21, 2027 December 21, 2028 December 21, 2029 | $990 repurchase amount December 21, 2030 December 21, 2031 December 21, 2032 | $1,000 repurchase amount December 21, 2033 December 21, 2034 December 21, 2035 December 21, 2036 December 21, 2037 December 21, 2038 December 21, 2039 December 21, 2040 December 21, 2041 December 21, 2042 December 21, 2043 December 21, 2044 December 21, 2045 December 21, 2046 December 21, 2047 December 21, 2048 December 21, 2049 December 21, 2050 December 21, 2051 December 21, 2052 December 21, 2053 December 21, 2054 December 21, 2055 December 21, 2056 December 21, 2057 December 21, 2058 December 21, 2059 December 21, 2060 December 21, 2061 December 21, 2062 |

| If any repurchase date is not a business day, then the payment required to be made on that repurchase date will be made on the next succeeding business day with the same force and effect as if made on that repurchase date. No additional interest will accrue as a result of delayed payment. | |

| Repurchase notice: | A repurchase notice substantially in the form of the repurchase notice set forth in Annex B to this pricing supplement |

| PS-2 |

| Citigroup Global Markets Holdings Inc. |

Risk Factors

The following is a non-exhaustive list of certain key risk factors for investors in the notes. You should read the risk factors below together with the risk factors included in the accompanying prospectus supplement and in the documents incorporated by reference in the accompanying prospectus, including Citigroup Inc.’s most recent Annual Report on Form 10-K and any subsequent Quarterly Reports on Form 10-Q, which describe risks relating to the business of Citigroup Inc. more generally. We also urge you to consult your investment, legal, tax, accounting and other advisers in connection with your investment in the notes.

| § | The amount of interest payable on the notes will vary. The notes differ from conventional fixed-rate debt securities in that the interest payable on the notes will vary based on the level of SOFR and may be as low as 0.00%. |

| § | The yield on the notes may be lower than the yield on a conventional fixed-rate debt security of ours of comparable maturity. The interest rate applicable to the notes will vary based on the level of SOFR, and may be as low as 0.00% on each interest payment date. As a result, the effective yield on your notes may be less than that which would be payable on a conventional fixed-rate debt security of ours (guaranteed by Citigroup Inc.) of comparable maturity. |

| § | The notes may be riskier than an investment with a shorter term. The notes have a relatively long term to maturity. Accordingly, if you do not own a sufficient principal amount of notes to satisfy the minimum repurchase amount in connection with an exercise of the early repurchase right, you will be subject to heightened risks as compared to an investment in notes with a shorter term because you will be subject to those risks for a longer period of time. For example, because of the longer time horizon of the notes, you will be subject to greater risk that we and Citigroup Inc. may default on our obligations under the notes at some point prior to maturity. In addition, you will be subject to greater interest rate risk. If SOFR fails to increase significantly from current levels, you may be holding a long-dated security with a yield that is lower than you might achieve on other investments, including our fixed rate debt securities of the same maturity. The relatively long term of the notes means that it may be a considerable length of time before you would be able to redeploy your funds to a higher yielding investment. Moreover, the value of a longer-dated note is typically less than the value of an otherwise comparable note with a shorter term, so that, if you were to desire to sell the notes prior to maturity in order to invest in a better performing alternative investment, you may not be able to do so except at a substantial loss. |

| § | If you request that we repurchase your notes on any repurchase date on or prior to December 21, 2032, you will receive less than the stated principal amount of your notes. The repurchase amount for any repurchase date from and including December 21, 2027 to and including December 21, 2029 is equal to $980 and the repurchase amount for any repurchase date from and including December 21, 2030 to and including December 21, 2032 is equal to $990 for each $1,000 stated principal amount note, plus any accrued and unpaid interest. As a result, if you request that we repurchase your notes on any repurchase date on or prior to December 21, 2032, you will receive less than the stated principal amount of your notes upon an early repurchase. |

| § | There are restrictions on your ability to request that we repurchase your notes. To request that we repurchase your notes, you must submit at least the minimum repurchase amount of $100,000 in stated principal amount of your notes. You may not exercise the early repurchase right prior to December 21, 2027, and thereafter you may exercise the early repurchase right only once every twelve months. In addition, if you elect to exercise your early repurchase right, your request that we repurchase your notes is only valid if we receive your repurchase notice by no later than 4:00 p.m., New York City time, fifteen business days prior to the relevant repurchase date and if you follow the procedures described under “Annex A—Supplemental Terms of Notes—Early Repurchase” and we or our affiliates acknowledge receipt of the repurchase notice that same day. If we do not receive that repurchase notice or we or our affiliates do not acknowledge receipt of that notice, your repurchase request will not be effective and we will not be required to repurchase your notes on the corresponding repurchase date. Because of the timing requirements of the repurchase notice, settlement of the repurchase will be prolonged when compared to a sale and settlement in a secondary market sale transaction. As your request that we repurchase your notes is irrevocable, this will subject you to market risk in the event the market fluctuates after we receive your request. |

| § | The notes are subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc., and any actual or perceived changes to the creditworthiness of either entity may adversely affect the value of the notes. You are subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc. If Citigroup Global Markets Holdings Inc. defaults on its obligations under the notes and Citigroup Inc. defaults on its guarantee obligations, your investment would be at risk and you could lose some or all of your investment. As a result, the value of the notes will be affected by changes in the market’s view of the creditworthiness of Citigroup Global Markets Holdings Inc. or Citigroup Inc. Any decline, or anticipated decline in the credit ratings of either entity, or any increase or anticipated increase in the credit spreads of either entity, is likely to adversely affect the value of the notes. |

| § | The notes will not be listed on any securities exchange and you may not be able to sell them prior to maturity. The notes will not be listed on any securities exchange. Therefore, there may be little or no secondary market for the notes. CGMI currently intends to make a secondary market in relation to the notes and to provide an indicative bid price for the notes on a daily basis. Any indicative bid price for the notes provided by CGMI will be determined in CGMI’s sole discretion, taking into account prevailing market conditions and other relevant factors, and will not be a representation by CGMI that the notes can be sold at that price or at all. CGMI may suspend or terminate making a market and providing indicative bid prices without notice, at any time and for any reason. If CGMI suspends or terminates making a market, there may be no secondary market at all for the notes because it is likely that CGMI will be the only broker-dealer that is willing to buy your notes prior to maturity. Accordingly, except to the extent the early repurchase right is available, an investor must be prepared to hold the notes until maturity. |

| PS-3 |

| Citigroup Global Markets Holdings Inc. |

| § | Immediately following issuance, any secondary market bid price provided by CGMI, and the value that will be indicated on any brokerage account statements prepared by CGMI or its affiliates, will reflect a temporary upward adjustment. The amount of this temporary upward adjustment will steadily decline to zero over the temporary adjustment period. See “General Information—Temporary adjustment period” in this pricing supplement. |

| § | Secondary market sales of the notes may result in a loss of principal. You will be entitled to receive at least the full stated principal amount of your notes, subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc., only if you hold the notes to maturity or to a repurchase date occurring on or after December 21, 2033. If you are able to sell your notes in the secondary market prior to maturity, you are likely to receive less than the stated principal amount of the notes. |

| § | The inclusion of underwriting fees and projected profit from hedging in the issue price is likely to adversely affect secondary market prices. Assuming no changes in market conditions or other relevant factors, the price, if any, at which CGMI may be willing to purchase the notes in secondary market transactions will likely be lower than the issue price since the issue price of the notes includes, and secondary market prices are likely to exclude, underwriting fees paid with respect to the notes, as well as the cost of hedging our obligations under the notes. The cost of hedging includes the projected profit that our affiliates may realize in consideration for assuming the risks inherent in managing the hedging transactions. The secondary market prices for the notes are also likely to be reduced by the costs of unwinding the related hedging transactions. Our affiliates may realize a profit from the hedging activity even if the value of the notes declines. In addition, any secondary market prices for the notes may differ from values determined by pricing models used by CGMI, as a result of dealer discounts, mark-ups or other transaction costs. |

| § | The price at which you may be able to sell your notes prior to maturity will depend on a number of factors and may be substantially less than the amount you originally invest. A number of factors will influence the value of the notes in any secondary market that may develop and the price at which CGMI may be willing to purchase the notes in any such secondary market, including: the level and volatility of SOFR, interest rates in the market, the time remaining to maturity of the notes, changes in CGMI’s estimation of the value of the early repurchase right, hedging activities by our affiliates, fees and projected hedging fees and profits and any actual or anticipated changes in the credit ratings, financial condition and results of either Citigroup Global Markets Holdings Inc. or Citigroup Inc. The value of the notes will vary and is likely to be less than the issue price at any time prior to maturity, and sale of the notes prior to maturity may result in a loss. |

| § | The calculation agent, which is an affiliate of the issuer, will make determinations with respect to the notes. Citibank, N.A., the calculation agent for the notes, is an affiliate of ours. As calculation agent, Citibank, N.A. will determine, among other things, the level of SOFR and will calculate the interest payable to you on each interest payment date. Any of these determinations or calculations made by Citibank, N.A. in its capacity as calculation agent, including with respect to the calculation of the level of SOFR in the event of the unavailability of the level of SOFR, may adversely affect the amount of one or more interest payments to you. |

| § | Hedging and trading activity by us and our affiliates could result in a conflict of interest. One or more of our affiliates have entered into hedging transactions. This hedging activity involves trading in instruments, such as options, swaps or futures, based upon SOFR. This hedging activity may present a conflict between your interest in the notes and the interests our affiliates have in executing, maintaining and adjusting their hedge transactions because it could affect the price at which our affiliate CGMI may be willing to purchase your notes in the secondary market. Because hedging our obligations under the notes involves risk and may be influenced by a number of factors, it is possible that our affiliates may profit from the hedging activity, even if the value of the notes declines. |

| § | SOFR is a relatively new market index and as the related market continues to develop, there may be an adverse effect on the return on or value of the notes. The Federal Reserve Bank of New York (the “NY Federal Reserve”) began to publish SOFR in April 2018. Although the NY Federal Reserve has also begun publishing historical indicative SOFR going back to 2014, such prepublication historical data inherently involves assumptions, estimates and approximations. You should not rely on any historical changes or trends in SOFR as an indicator of the future performance of SOFR. Since the initial publication of SOFR, daily changes in the rate have, on occasion, been more volatile than daily changes in comparable benchmark or market rates. As a result, the return on the notes may fluctuate more than floating rate securities that are linked to less volatile rates. |

The notes likely will have no established trading market when issued, and an established trading market may never develop or may not be very liquid. Market terms for securities indexed to SOFR, such as the spread over the index reflected in interest rate provisions, may evolve over time, and the value of the notes may be lower than those of later-issued SOFR-linked securities as a result. Similarly, if SOFR does not prove to be widely used in securities like the notes, the value of the notes may be lower than those of securities linked to rates that are more widely used. You may not be able to sell the notes at all or may not be able to sell the notes at prices that will provide a yield comparable to similar investments that have a developed secondary market, and may consequently suffer from increased pricing volatility and market risk.

The NY Federal Reserve notes on its publication page for SOFR that use of SOFR is subject to important limitations, indemnification obligations and disclaimers, including that the NY Federal Reserve may alter the methods of calculation, publication schedule, rate revision practices or availability of SOFR at any time without notice. There can be no guarantee that SOFR will not be discontinued or fundamentally altered in a manner that is materially adverse to the interests of investors in the notes. If the manner in which SOFR is calculated is changed or if SOFR is discontinued, that change or discontinuance may result in a reduction or elimination of the amount of interest payable on the notes and a reduction in the value of the notes.

| § | The formula used to determine the interest rate on the notes is relatively new in the market, and as the related market continues to develop there may be an adverse effect on return on or value of the notes. The interest rate on the notes is based on a formula used to calculate a daily compounded SOFR rate, which is relatively new in the market. For each interest |

| PS-4 |

| Citigroup Global Markets Holdings Inc. |

period, the interest rate on the notes is based on a daily compounded SOFR rate calculated using the formula described in “Determination of SOFR” below. This interest rate will not be the SOFR rate published on or for a particular day during such interest period or an average of SOFR rates during such period nor will it be the same as the interest rate on other SOFR-linked notes that use an alternative formula to determine the interest rate. Also, if the SOFR rate for a particular day during an interest period is negative, inclusion of that rate in the calculation will reduce the interest rate for such interest period; provided that in no event will the interest payable on the notes be less than zero.

Additionally, market terms for notes linked to SOFR may evolve over time, and the value of the notes may be lower than those of later-issued SOFR-linked securities as a result. Similarly, if the formula to calculate daily compounded SOFR for the notes does not prove to be widely used in other securities like the notes, the trading price of the notes may be lower than those of securities having a formula more widely used. You may not be able to sell the notes at all or may not be able to sell the notes at prices that will provide a yield comparable to similar investments that have a developed secondary market, and may consequently suffer from increased pricing volatility and market risk.

The NY Federal Reserve (or a successor), as administrator of SOFR, may also make methodological or other changes that could change the value of SOFR, including changes related to the method by which SOFR is calculated, eligibility criteria applicable to the transactions used to calculate SOFR, or timing related to the publication of SOFR. In addition, the administrator may alter, discontinue or suspend calculation or dissemination of SOFR (in which case a fallback method of determining interest rates on the notes will apply). The administrator has no obligation to consider the interests of holders of notes when calculating, adjusting, converting, revising or discontinuing SOFR.

| § | The interest rate on the notes will be determined using alternative methods if SOFR is no longer available, and that may have an adverse effect on the return on and value of the notes. The terms of the notes provide that if a benchmark transition event and its related benchmark replacement date occur with respect to SOFR, the interest rate payable on the notes will be determined using the next-available benchmark replacement. As described above, these replacement rates and spreads may be selected or formulated by (i) the relevant governmental body (such as the Alternative Reference Rates Committee of the NY Federal Reserve) (ii) the International Swaps and Derivatives Association, Inc. or (iii) in certain circumstances, Citigroup (or one of its affiliates). In addition, the terms of the notes expressly authorize Citigroup (or one of its affiliates) to make benchmark replacement conforming changes with respect to, among other things, the determination of interest periods and the timing and frequency of determining rates and making payments of interest. The interests of Citigroup (or its affiliate) in making the determinations described above may be adverse to your interests as a holder of the notes. |

The application of a benchmark replacement and benchmark replacement adjustment, and any implementation of benchmark replacement conforming changes, or any implementation of a substitute, successor or alternative reference rate could result in adverse consequences to the interest rate payable on the notes, which could adversely affect the return on, value of and market for the notes. Further, there is no assurance that the characteristics of any substitute, successor or alternative reference rate or benchmark replacement will be similar to SOFR or the then-current benchmark that it is replacing, or that any benchmark replacement will produce the economic equivalent of SOFR or the then-current benchmark that it is replacing.

| § | We or our subsidiaries or affiliates may publish research that could affect the market value of the notes. We or our subsidiaries or affiliates may, at present or in the future, publish research reports with respect to movements in interest rates generally, or the LIBOR transition or SOFR specifically. This research is modified from time to time without notice and may express opinions or provide recommendations that are inconsistent with purchasing or holding the notes. Any of these activities may affect the market value of the notes. |

| § | You will have no rights against the publisher of SOFR. You will have no rights against the publisher of SOFR even though the amount you receive on each interest payment date will depend upon the level of SOFR. The publisher of SOFR is not in any way involved in this offering and has no obligations relating to the notes or the holders of the notes. |

| General Information | |

| Temporary adjustment period: | For a period of approximately six months following issuance of the notes, the price, if any, at which CGMI would be willing to buy the notes from investors, and the value that will be indicated for the notes on any brokerage account statements prepared by CGMI or its affiliates (which value CGMI may also publish through one or more financial information vendors), will reflect a temporary upward adjustment from the price or value that would otherwise be determined. This temporary upward adjustment represents a portion of the hedging profit expected to be realized by CGMI or its affiliates over the term of the notes. The amount of this temporary upward adjustment will decline to zero on a straight-line basis over the six-month temporary adjustment period. However, CGMI is not obligated to buy the notes from investors at any time. See “Risk Factors—The notes will not be listed on any securities exchange and you may not be able to sell them prior to maturity.” |

| PS-5 |

| Citigroup Global Markets Holdings Inc. |

| U.S. federal income tax considerations: | In the opinion of our counsel, Davis Polk & Wardwell LLP, the notes should be treated as “variable rate debt instruments” for U.S. federal income tax purposes. Under this treatment, stated interest on the notes will be taxable to a U.S. Holder (as defined in the accompanying prospectus supplement) as ordinary interest income at the time it accrues or is received in accordance with the U.S. Holder’s method of tax accounting.

Upon the sale or other taxable disposition of a note, a U.S. Holder generally will recognize capital gain or loss equal to the difference between the amount realized on the disposition (other than any amount attributable to accrued interest, which will be treated as a payment of interest) and the U.S. Holder’s adjusted tax basis in the note. A U.S. Holder’s adjusted tax basis in a note generally will equal the cost of the note to the U.S. Holder. Such gain or loss generally will be long-term capital gain or loss if the U.S. Holder has held the note for more than one year at the time of disposition.

Subject to the discussion in “United States Federal Tax Considerations” in the accompanying prospectus supplement, under current law Non-U.S. Holders (as defined in the accompanying prospectus supplement) generally will not be subject to U.S. federal withholding or income tax with respect to interest paid on and amounts received on the sale, exchange or retirement of the notes if they comply with applicable certification requirements. Special rules apply to Non-U.S. Holders whose income on the notes is effectively connected with the conduct of a U.S. trade or business or who are individuals present in the United States for 183 days or more in a taxable year.

You should read the section entitled “United States Federal Tax Considerations” in the accompanying prospectus supplement. The preceding discussion, when read in combination with that section, constitutes the full opinion of Davis Polk & Wardwell LLP regarding the material U.S. federal tax consequences of owning and disposing of the notes. It does not address the potential consequences of an investment in the notes for the tax treatment of your other investments or transactions.

You should also consult your tax adviser regarding all aspects of the U.S. federal tax consequences of an investment in the notes and any tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction. |

| Notes used as qualified replacement property: | Prospective investors seeking to treat the notes as “qualified replacement property” for purposes of Section 1042 of the Internal Revenue Code of 1986, as amended (the “Code”), should be aware that Section 1042 requires the issuer to meet certain requirements in order for the notes to constitute qualified replacement property. In general, qualified replacement property is a security issued by a domestic operating corporation that did not, for the taxable year preceding the taxable year in which such security was purchased, have “passive investment income” in excess of 25 percent of the gross receipts of such corporation for such preceding taxable year (the “passive income test”). For purposes of the passive income test, where the issuing corporation is in control of one or more corporations or such issuing corporation is controlled by one or more other corporations, all such corporations are treated as one corporation (the “affiliated group”) when computing the amount of passive investment income under Section 1042.

Citigroup Global Markets Holdings Inc. believes that less than 25 percent of its affiliated group’s gross receipts was passive investment income for the taxable year ending December 31, 2022. In making this determination, we have made certain assumptions and used procedures which we believe are reasonable. Accordingly, Citigroup Global Markets Holdings Inc., as issuer, is of the view that the notes should qualify as “qualified replacement property.” Citigroup Global Markets Holdings Inc. cannot give any assurance as to whether its affiliated group will continue to meet the passive income test. It is, in addition, possible that the Internal Revenue Service may disagree with the manner in which Citigroup Global Markets Holdings Inc. has calculated the affiliated group’s gross receipts (including the characterization thereof) and passive investment income and the conclusions reached herein.

The notes are securities with no established trading market. No assurance can be given as to whether a trading market for the notes will develop or as to the liquidity of a trading market for the notes. The availability and liquidity of a trading market for the notes will also be affected by the degree to which purchasers treat the notes as qualified replacement property.

|

| PS-6 |

| Citigroup Global Markets Holdings Inc. |

| Trustee: | The Bank of New York Mellon (as trustee under an indenture dated March 8, 2016) will serve as trustee for the notes. |

| Use of proceeds and hedging: | The net proceeds received from the sale of the notes will be used for general corporate purposes and, in part, in connection with hedging our obligations under the notes through one or more of our affiliates.

Hedging activities related to the notes by one or more of our affiliates involves trading in one or more instruments, such as options, swaps and/or futures, based on SOFR and/or taking positions in any other available securities or instruments that we may wish to use in connection with such hedging and may include adjustments to such positions during the term of the notes. It is possible that our affiliates may profit from this hedging activity, even if the value of the notes declines. Profit or loss from this hedging activity could affect the price at which Citigroup Global Markets Holdings Inc.’s affiliate, CGMI, may be willing to purchase your notes in the secondary market. For further information on our use of proceeds and hedging, see “Use of Proceeds and Hedging” in the accompanying prospectus.

|

| ERISA and IRA purchase considerations: | Please refer to “Benefit Plan Investor Considerations” in the accompanying prospectus supplement for important information for investors that are ERISA or other benefit plans or whose underlying assets include assets of such plans. |

| Fees and selling concessions: | CGMI, an affiliate of Citigroup Global Markets Holdings Inc. and the underwriter of the sale of the notes, is acting as principal and will receive an underwriting fee of up to $10 for each note sold in this offering. The actual underwriting fee will be equal to up to $10 for each note sold by CGMI directly to the public and will otherwise be equal to the selling concession provided to selected dealers, as described in this paragraph. CGMI will pay selected dealers not affiliated with CGMI a selling concession of up to $10 for each note they sell.

Additionally, it is possible that CGMI and its affiliates may profit from hedging activity related to this offering, even if the value of the notes declines. You should refer to “Risk Factors” above and the section “Use of Proceeds and Hedging” in the accompanying prospectus. |

| Supplemental information regarding plan of distribution; conflicts of interest: | The terms and conditions set forth in the Amended and Restated Global Selling Agency Agreement dated April 7, 2017 among Citigroup Global Markets Holdings Inc., Citigroup Inc. and the agents named therein, including CGMI, govern the sale and purchase of the notes.

The notes will not be listed on any securities exchange.

In order to hedge its obligations under the notes, Citigroup Global Markets Holdings Inc. has entered into one or more swaps or other derivatives transactions with one or more of its affiliates. You should refer to the sections “Risk Factors—Hedging and trading activity by us or our affiliates could result in a conflict of interest,” and “General Information—Use of proceeds and hedging” in this pricing supplement and the section “Use of Proceeds and Hedging” in the accompanying prospectus.

See “Plan of Distribution; Conflicts of Interest” in the accompanying prospectus supplement for more information. |

| Calculation agent: | Citibank, N.A., an affiliate of Citigroup Global Markets Holdings Inc., will serve as calculation agent for the notes. All determinations made by the calculation agent will be at the sole discretion of the calculation agent and will, in the absence of manifest error, be conclusive for all purposes and binding on Citigroup Global Markets Holdings Inc., Citigroup Inc. and the holders of the notes. Citibank, N.A. is obligated to carry out its duties and functions as calculation agent in good faith and using its reasonable judgment. |

| Paying agent: | Citibank, N.A. will serve as paying agent and registrar and will also hold the global security representing the notes as custodian for The Depository Trust Company (“DTC”). |

| Contact: | Clients may contact their local brokerage representative. Third party distributors may contact Citi Structured Investment Sales at (212) 723-7005. |

We encourage you to also read the accompanying prospectus supplement and prospectus, which can be accessed via the hyperlink on the cover page of this pricing supplement.

Determination of Interest Payments

On each interest payment date, the amount of each interest payment will equal (i) the stated principal amount of the notes multiplied by the interest rate in effect during the applicable interest period, multiplied by (ii) the quotient of the actual number of calendar days in

| PS-7 |

| Citigroup Global Markets Holdings Inc. |

such Interest Period divided by 360; provided that in no event will the interest payment be less than zero. The interest rate applicable to each interest period will be equal to the accrued interest compounding factor (as defined under “Determination of SOFR” below) plus the floating rate spread.

Determination of SOFR

For the purposes of calculating interest with respect to any interest period:

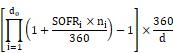

“Accrued interest compounding factor” means, for the observation period corresponding to such interest period, the result of the following formula:

where:

“d0”, for any observation period, is the number of U.S. government securities business days in the relevant observation period.

“i” is a series of whole numbers from one to d0, each representing the relevant U.S. government securities business days in chronological order from, and including, the first U.S. government securities business day in the relevant observation period.

“SOFRi”, for any day “i” in the relevant observation period, is a reference rate equal to SOFR in respect of that day.

“ni”, for any day “i” in the relevant observation period, is the number of calendar days from, and including, such U.S. government securities business day “i” to, but excluding, the following U.S. government securities business day.

“d” is the number of calendar days in the relevant observation period.

“SOFR” means, with respect to any day, the rate determined by the calculation agent in accordance with the following provisions:

| (1) | the Secured Overnight Financing Rate for trades made on such day that appears at approximately 3:00 p.m. (New York City time) on the NY Federal Reserve’s website on the U.S. government securities business day immediately following such U.S. government securities business day; or |

| (2) | if the rate specified in (1) above does not so appear, unless a benchmark transition event and its related benchmark replacement date have occurred as described in (3) below, the Secured Overnight Financing Rate published on the NY Federal Reserve’s website for the first preceding U.S. government securities business day for which the Secured Overnight Financing Rate was published on the NY Federal Reserve’s website; or |

| (3) | if a benchmark transition event and its related benchmark replacement date have occurred prior to the relevant interest payment date, the calculation agent will use the benchmark replacement to determine the rate and for all other purposes relating to the notes. |

In connection with the SOFR definition above, the following definitions apply:

“Benchmark” means, initially, SOFR; provided that if a benchmark transition event and its related benchmark replacement date have occurred with respect to SOFR or the then-current benchmark, then “benchmark” means the applicable benchmark replacement.

“Benchmark replacement” means the first alternative set forth in the order below that can be determined by Citigroup (or one of its affiliates) as of the benchmark replacement date:

| (1) | the sum of: (a) the alternate rate of interest that has been selected or recommended by the relevant governmental body as the replacement for the then-current benchmark for the applicable corresponding tenor and (b) the benchmark replacement adjustment; or |

| (2) | the sum of: (a) the ISDA fallback rate and (b) the benchmark replacement adjustment; or |

| (3) | the sum of: (a) the alternate rate of interest that has been selected by Citigroup (or one of its affiliates) as the replacement for the then-current benchmark for the applicable corresponding tenor giving due consideration to any industry-accepted rate of interest as a replacement for the then-current benchmark for U.S. dollar-denominated floating rate notes at such time and (b) the benchmark replacement adjustment. |

“Benchmark replacement adjustment” means the first alternative set forth in the order below that can be determined by Citigroup (or one of its affiliates) as of the benchmark replacement date:

| (1) | the spread adjustment, or method for calculating or determining such spread adjustment, (which may be a positive or negative value or zero) that has been selected or recommended by the relevant governmental body for the applicable unadjusted benchmark replacement; |

| (2) | if the applicable unadjusted benchmark replacement is equivalent to the ISDA fallback rate, then the ISDA fallback adjustment; |

| (3) | the spread adjustment (which may be a positive or negative value or zero) that has been selected by Citigroup (or one of its affiliates) giving due consideration to any industry-accepted spread adjustment, or method for calculating or determining such |

| PS-8 |

| Citigroup Global Markets Holdings Inc. |

spread adjustment, for the replacement of the then-current benchmark with the applicable unadjusted benchmark replacement for U.S. dollar-denominated floating rate notes at such time.

“Benchmark replacement conforming changes” means, with respect to any benchmark replacement, any technical, administrative or operational changes that Citigroup (or one of its affiliates) decides may be appropriate to reflect the adoption of such benchmark replacement in a manner substantially consistent with market practice (or, if Citigroup (or such affiliate) decides that adoption of any portion of such market practice is not administratively feasible or if Citigroup (or such affiliate) determines that no market practice for use of the benchmark replacement exists, in such other manner as Citigroup (or such affiliate) determines is reasonably necessary).

“Benchmark replacement date” means the earliest to occur of the following events with respect to the then-current benchmark:

| (1) | in the case of clause (1) or (2) of the definition of “benchmark transition event,” the later of (a) the date of the public statement or publication of information referenced therein and (b) the date on which the administrator of the benchmark permanently or indefinitely ceases to provide the benchmark; or |

| (2) | in the case of clause (3) of the definition of “benchmark transition event,” the date of the public statement or publication of information referenced therein. |

For the avoidance of doubt, if the event giving rise to the benchmark replacement date occurs on the same day as, but earlier than, the reference time in respect of any determination, the benchmark replacement date will be deemed to have occurred prior to the reference time for such determination.

“Benchmark transition event” means the occurrence of one or more of the following events with respect to the then-current Benchmark:

| (1) | a public statement or publication of information by or on behalf of the administrator of the benchmark announcing that such administrator has ceased or will cease to provide the benchmark, permanently or indefinitely, provided that, at the time of such statement or publication, there is no successor administrator that will continue to provide the benchmark; |

| (2) | a public statement or publication of information by the regulatory supervisor for the administrator of the benchmark, the central bank for the currency of the benchmark, an insolvency official with jurisdiction over the administrator for the benchmark, a resolution authority with jurisdiction over the administrator for the benchmark or a court or an entity with similar insolvency or resolution authority over the administrator for the benchmark, which states that the administrator of the benchmark has ceased or will cease to provide the benchmark permanently or indefinitely, provided that, at the time of such statement or publication, there is no successor administrator that will continue to provide the benchmark; or |

| (3) | a public statement or publication of information by the regulatory supervisor for the administrator of the benchmark announcing that the benchmark is no longer representative. |

“Corresponding tenor” with respect to a benchmark replacement means a tenor (including overnight) having approximately the same length (disregarding business day adjustment) as the applicable tenor for the then-current benchmark.

“ISDA” means the International Swaps and Derivatives Association, Inc. or any successor thereto.

“ISDA definitions” means the 2006 ISDA Definitions published by ISDA, as amended or supplemented from time to time, or any successor definitional booklet for interest rate derivatives published from time to time.

“ISDA fallback adjustment” means the spread adjustment (which may be a positive or negative value or zero) that would apply for derivatives transactions referencing the ISDA definitions to be determined upon the occurrence of an index cessation event with respect to the benchmark for the applicable tenor.

“ISDA fallback rate” means the rate that would apply for derivatives transactions referencing the ISDA definitions to be effective upon the occurrence of an index cessation date with respect to the benchmark for the applicable tenor excluding the applicable ISDA fallback adjustment.

“NY Federal Reserve” means the Federal Reserve Bank of New York.

“NY Federal Reserve’s website” means the website of the NY Federal Reserve, currently at http://www.newyorkfed.org, or any successor website of the NY Federal Reserve or the website of any successor administrator of the Secured Overnight Financing Rate.

“Reference time” with respect to any determination of the benchmark means the time determined by Citigroup (or one of its affiliates) in accordance with the benchmark replacement conforming changes.

“Relevant governmental body” means the Federal Reserve Board and/or the NY Federal Reserve, or a committee officially endorsed or convened by the Federal Reserve Board and/or the NY Federal Reserve or any successor thereto.

“Unadjusted benchmark replacement” means the benchmark replacement excluding the benchmark replacement adjustment.

| PS-9 |

| Citigroup Global Markets Holdings Inc. |

About SOFR

SOFR is published by the NY Federal Reserve and is intended to be a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities. The NY Federal Reserve reports that SOFR includes all trades in the Broad General Collateral Rate, plus bilateral Treasury repurchase agreement (“repo”) transactions cleared through the delivery-versus-payment service offered by the Fixed Income Clearing Corporation (the “FICC”), a subsidiary of The Depository Trust & Clearing Corporation (“DTCC”). SOFR is filtered by the NY Federal Reserve to remove a portion of the foregoing transactions considered to be “specials”. According to the NY Federal Reserve, “specials” are repos for specific-issue collateral which take place at cash-lending rates below those for general collateral repos because cash providers are willing to accept a lesser return on their cash in order to obtain a particular security.

The NY Federal Reserve reports that SOFR is calculated as a volume-weighted median of transaction-level tri-party repo data collected from The Bank of New York Mellon, which currently acts as the clearing bank for the tri-party repo market, as well as General Collateral Finance Repo transaction data and data on bilateral Treasury repo transactions cleared through the FICC’s delivery-versus-payment service. The NY Federal Reserve notes that it obtains information from DTCC Solutions LLC, an affiliate of DTCC.

The NY Federal Reserve currently publishes SOFR daily on its website. The NY Federal Reserve states on its publication page for SOFR that use of SOFR is subject to important disclaimers, limitations and indemnification obligations, including that the NY Federal Reserve may alter the methods of calculation, publication schedule, rate revision practices or availability of SOFR at any time without notice. Information contained in the publication page for SOFR is not incorporated by reference in, and should not be considered part of, this pricing supplement.

This pricing supplement contains SOFR data and related information posted to the NY Federal Reserve website. This pricing supplement is subject to the Terms of Use posted at newyorkfed.org. The NY Federal Reserve is not responsible for publication of this pricing supplement by Citi, does not sanction or endorse any particular republication, and has no liability for your use. This pricing supplement also describes products or services by reference to SOFR. Citi is not affiliated with the NY Federal Reserve. The NY Federal Reserve does not sanction, endorse, or recommend any products or services offered by Citi.

Historical Information on SOFR

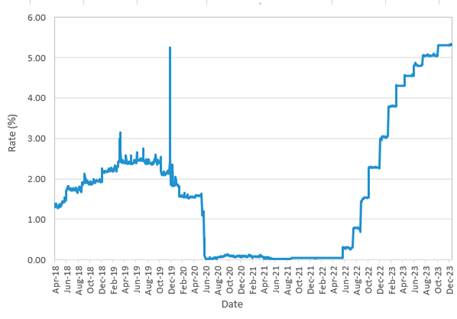

SOFR was 5.31% on December 19, 2023.

The graph below shows the published daily rate for SOFR for each day it was available from April 2, 2018 to December 19, 2023. We obtained the values below from Bloomberg L.P., without independent verification. The values below do not reflect the spread that will be deducted from SOFR in determining the rate at which interest is paid on the notes. You should not take the historical performance of SOFR as an indication of future performance.

The historical rates do not reflect the daily compounding method used to calculate the floating rate at which interest will be payable on the notes.

Historical SOFR April 2, 2018 to December 19, 2023 |

|

| PS-10 |

| Citigroup Global Markets Holdings Inc. |

Certain Selling Restrictions

Prohibition of Sales to EEA Retail Investors

The notes may not be offered, sold or otherwise made available to any retail investor in the European Economic Area. For the purposes of this provision:

| (a) | the expression “retail investor” means a person who is one (or more) of the following: |

| (i) | a retail client as defined in point (11) of Article 4(1) of Directive 2014/65/EU (as amended, “MiFID II”); or |

| (ii) | a customer within the meaning of Directive 2002/92/EC, where that customer would not qualify as a professional client as defined in point (10) of Article 4(1) of MiFID II; or |

| (iii) | not a qualified investor as defined in Directive 2003/71/EC; and |

| (b) | the expression “offer” includes the communication in any form and by any means of sufficient information on the terms of the offer and the notes offered so as to enable an investor to decide to purchase or subscribe the notes. |

Prohibition of Sales to United Kingdom Retail Investors

The notes may not be offered, sold or otherwise made available to any retail investor in the United Kingdom. For the purposes of this provision:

| (a) | the expression “retail investor” means a person who is one (or more) of the following: |

| (i) | a retail client, as defined in point (8) of Article 2 of Regulation (EU) No 2017/565 as it forms part of United Kingdom domestic law by virtue of the European Union (Withdrawal) Act 2018 (the “EUWA”) and the regulations made under the EUWA; or |

| (ii) | a customer within the meaning of the provisions of the Financial Services and Markets Act 2000 (as amended) (the “FSMA”) and any rules or regulations made under the FSMA to implement Directive (EU) 2016/97, where that customer would not qualify as a professional client, as defined in point (8) of Article 2(1) of Regulation (EU) No 600/2014 as it forms part of United Kingdom domestic law by virtue of the EUWA and the regulations made under the EUWA; or |

| (iii) | not a qualified investor as defined in Regulation (3)(e) of the Prospectus Regulation; and |

| (b) | the expression “offer” includes the communication in any form and by any means of sufficient information on the terms of the offer and the notes offered so as to enable an investor to decide to purchase or subscribe the notes. |

| PS-11 |

| Citigroup Global Markets Holdings Inc. |

Validity of the Notes

In the opinion of Davis Polk & Wardwell LLP, as special products counsel to Citigroup Global Markets Holdings Inc., when the notes offered by this pricing supplement have been executed and issued by Citigroup Global Markets Holdings Inc. and authenticated by the trustee pursuant to the indenture, and delivered against payment therefor, such notes and the related guarantee of Citigroup Inc. will be valid and binding obligations of Citigroup Global Markets Holdings Inc. and Citigroup Inc., respectively, enforceable in accordance with their respective terms, subject to applicable bankruptcy, insolvency and similar laws affecting creditors’ rights generally, concepts of reasonableness and equitable principles of general applicability (including, without limitation, concepts of good faith, fair dealing and the lack of bad faith), provided that such counsel expresses no opinion as to the effect of fraudulent conveyance, fraudulent transfer or similar provision of applicable law on the conclusions expressed above. This opinion is given as of the date of this pricing supplement and is limited to the laws of the State of New York, except that such counsel expresses no opinion as to the application of state securities or Blue Sky laws to the notes.

In giving this opinion, Davis Polk & Wardwell LLP has assumed the legal conclusions expressed in the opinions set forth below of Alexia Breuvart, Secretary and General Counsel of Citigroup Global Markets Holdings Inc., and Barbara Politi, Associate General Counsel—Capital Markets of Citigroup Inc. In addition, this opinion is subject to the assumptions set forth in the letter of Davis Polk & Wardwell LLP dated March 7, 2023, which has been filed as an exhibit to a Current Report on Form 8-K filed by Citigroup Inc. on March 8, 2023, that the indenture has been duly authorized, executed and delivered by, and is a valid, binding and enforceable agreement of, the trustee and that none of the terms of the notes nor the issuance and delivery of the notes and the related guarantee, nor the compliance by Citigroup Global Markets Holdings Inc. and Citigroup Inc. with the terms of the notes and the related guarantee respectively, will result in a violation of any provision of any instrument or agreement then binding upon Citigroup Global Markets Holdings Inc. or Citigroup Inc., as applicable, or any restriction imposed by any court or governmental body having jurisdiction over Citigroup Global Markets Holdings Inc. or Citigroup Inc., as applicable.

In the opinion of Alexia Breuvart, Secretary and General Counsel of Citigroup Global Markets Holdings Inc., (i) the terms of the notes offered by this pricing supplement have been duly established under the indenture and the Board of Directors (or a duly authorized committee thereof) of Citigroup Global Markets Holdings Inc. has duly authorized the issuance and sale of such notes and such authorization has not been modified or rescinded; (ii) Citigroup Global Markets Holdings Inc. is validly existing and in good standing under the laws of the State of New York; (iii) the indenture has been duly authorized, executed and delivered by Citigroup Global Markets Holdings Inc.; and (iv) the execution and delivery of such indenture and of the notes offered by this pricing supplement by Citigroup Global Markets Holdings Inc., and the performance by Citigroup Global Markets Holdings Inc. of its obligations thereunder, are within its corporate powers and do not contravene its certificate of incorporation or bylaws or other constitutive documents. This opinion is given as of the date of this pricing supplement and is limited to the laws of the State of New York.

Alexia Breuvart, or other internal attorneys with whom she has consulted, has examined and is familiar with originals, or copies certified or otherwise identified to her satisfaction, of such corporate records of Citigroup Global Markets Holdings Inc., certificates or documents as she has deemed appropriate as a basis for the opinions expressed above. In such examination, she or such persons has assumed the legal capacity of all natural persons, the genuineness of all signatures (other than those of officers of Citigroup Global Markets Holdings Inc.), the authenticity of all documents submitted to her or such persons as originals, the conformity to original documents of all documents submitted to her or such persons as certified or photostatic copies and the authenticity of the originals of such copies.

In the opinion of Barbara Politi, Associate General Counsel—Capital Markets of Citigroup Inc., (i) the Board of Directors (or a duly authorized committee thereof) of Citigroup Inc. has duly authorized the guarantee of such notes by Citigroup Inc. and such authorization has not been modified or rescinded; (ii) Citigroup Inc. is validly existing and in good standing under the laws of the State of Delaware; (iii) the indenture has been duly authorized, executed and delivered by Citigroup Inc.; and (iv) the execution and delivery of such indenture, and the performance by Citigroup Inc. of its obligations thereunder, are within its corporate powers and do not contravene its certificate of incorporation or bylaws or other constitutive documents. This opinion is given as of the date of this pricing supplement and is limited to the General Corporation Law of the State of Delaware.

Barbara Politi, or other internal attorneys with whom she has consulted, has examined and is familiar with originals, or copies certified or otherwise identified to her satisfaction, of such corporate records of Citigroup Inc., certificates or documents as she has deemed appropriate as a basis for the opinions expressed above. In such examination, she or such persons has assumed the legal capacity of all natural persons, the genuineness of all signatures (other than those of officers of Citigroup Inc.), the authenticity of all documents submitted to her or such persons as originals, the conformity to original documents of all documents submitted to her or such persons as certified or photostatic copies and the authenticity of the originals of such copies.

Additional Information

We reserve the right to withdraw, cancel or modify any offering of the notes and to reject orders in whole or in part prior to their issuance.

© 2023 Citigroup Global Markets Inc. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

| PS-12 |

| Citigroup Global Markets Holdings Inc. |

Annex A

Supplemental Terms of Notes

Early Repurchase

You may submit a request to have us repurchase all or any portion of your notes on any repurchase date during the term of the notes on or after the initial repurchase date, subject to the procedures and terms set forth below. Any repurchase request that we accept in accordance with the procedures and terms set forth below will be irrevocable. To exercise the early repurchase right, you must submit notes for repurchase having an aggregate stated principal amount equal to the minimum repurchase amount of $100,000 or an integral multiple of $1,000 in excess thereof.

To request that we repurchase your notes, you must instruct your broker or other person through which you hold your notes to take the following steps:

| · | Send a notice of repurchase, substantially in the form attached as Annex B to this pricing supplement (a “repurchase notice”), to us via email at cag.us.middle.office@citi.com, with “Floating Rate Notes Due December 21, 2063, CUSIP No. 17291TWR5” as the subject line, by no later than 4:00 p.m., New York City time, fifteen business days prior to the relevant repurchase date. We or our affiliate must acknowledge receipt of the repurchase notice on the same business day for it to be effective, which acknowledgment will be deemed to evidence our acceptance of your repurchase request; |

| · | Instruct your DTC custodian to book a delivery versus payment trade with respect to your notes on the relevant repurchase date at a price equal to the repurchase amount payable upon early repurchase of the notes; and |

| · | Cause your DTC custodian to deliver the trade as booked for settlement via DTC at or prior to 10:00 a.m., New York City time, on the day on which the notes will be repurchased. |

Different brokerage firms may have different deadlines for accepting instructions from their customers. Accordingly, you should consult the brokerage firm through which you own your interest in the notes in respect of those deadlines. If we do not receive your repurchase notice by 4:00 p.m., New York City time, fifteen business days prior to the relevant repurchase date or we (or our affiliates) do not acknowledge receipt of the repurchase notice on the same day, your repurchase notice will not be effective, and we will not repurchase your notes. Once given, a repurchase notice may not be revoked.

The calculation agent will, in its sole discretion, resolve any questions that may arise as to the validity of a repurchase notice and the timing of receipt of a repurchase notice or as to whether and when the required deliveries have been made. Questions about the repurchase requirements should be directed to cag.us.middle.office@citi.com.

| PS-13 |

| Citigroup Global Markets Holdings Inc. |

Annex B

Form of Repurchase Notice

To: Citigroup Global Markets Holdings Inc. – Middle Office

Subject: Floating Rate Notes Due December 21, 2063, CUSIP No. 17291TWR5

Ladies and Gentlemen:

The undersigned holder of Citigroup Global Markets Holdings Inc.’s Medium-Term Senior Notes, Series N, Floating Rate Notes Due December 21, 2063, CUSIP No. 17291TWR5, fully and unconditionally guaranteed by Citigroup Inc. (the “notes”), hereby irrevocably elects to exercise, with respect to the number of the notes indicated below, as of the date hereof, the right to have you repurchase such notes on the repurchase date specified below as described in the pricing supplement dated December 19, 2023 relating to the notes (collectively, the “supplement”). Terms not defined herein have the meanings given to such terms in the supplement.

The undersigned certifies to you that it will (i) instruct its DTC custodian with respect to the notes (specified below) to book a delivery versus payment trade on the relevant repurchase date with respect to the number of notes specified below at a price per $1,000 stated principal amount note determined in the manner described in the supplement, facing DTC 0274 and (ii) cause the DTC custodian to deliver the trade as booked for settlement via DTC at or prior to 10:00 a.m. New York City time on the repurchase date.

Very truly yours,

[NAME OF HOLDER]

Name:

Title:

Telephone:

Fax:

Email:

Number of notes surrendered for repurchase (minimum of $100,000 stated principal amount):

Applicable repurchase date: _________________, 20__*

DTC # (and any relevant sub-account):

Contact Name:

Telephone:

Acknowledgment: I acknowledge that the notes specified above will not be repurchased unless all of the requirements specified in the supplement are satisfied, including the acknowledgment by you or your affiliate of the receipt of this notice on the date hereof.

Questions regarding the repurchase requirements of your notes should be directed to CAG US Middle Office via email at cag.us.middle.office@citi.com.

*Subject to adjustment as described in the supplement.

| PS-14 |