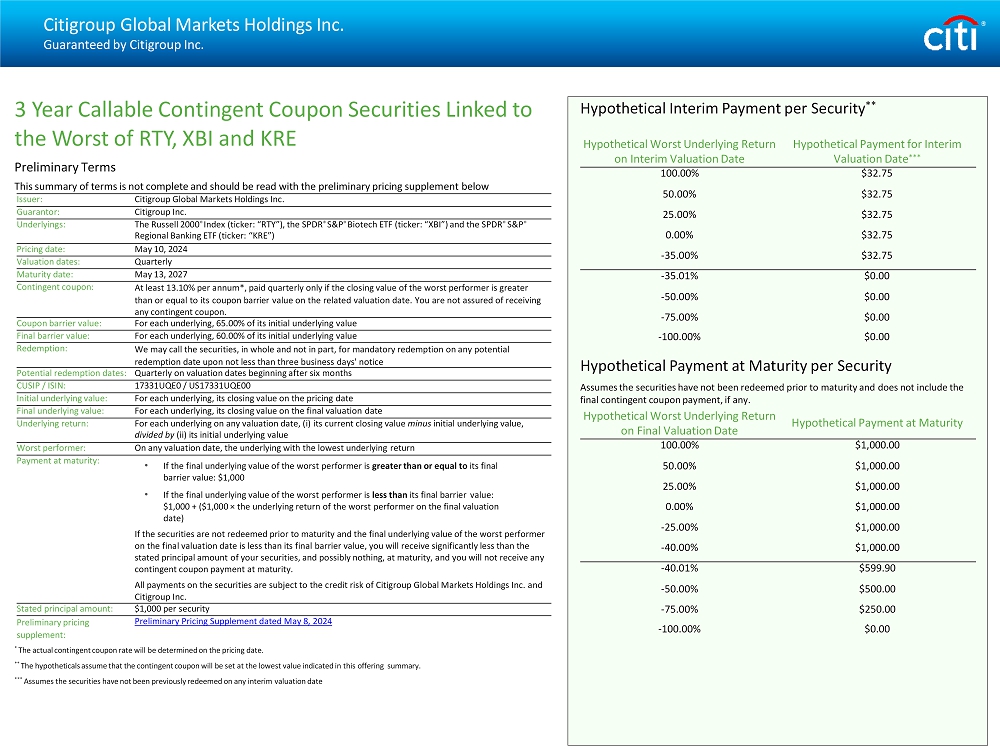

Citigroup Global Markets Holdings Inc. Guaranteed by Citigroup Inc. 3 Year Callable Contingent Coupon Securities Linked to the Worst of RTY, XBI and KRE Preliminary Terms This summary of terms is not complete and should be read with the preliminary pricing supplement below Citigroup Global Markets Holdings Inc. Issuer: Citigroup Inc. Guarantor: The Russell 2000 ® Index (ticker: “RTY”), the SPDR ® S&P ® Biotech ETF (ticker: “XBI”) and the SPDR ® S&P ® Regional Banking ETF (ticker: “KRE”) Underlyings: May 10, 2024 Pricing date: Quarterly Valuation dates: May 13, 2027 Maturity date: At least 13.10% per annum*, paid quarterly only if the closing value of the worst performer is greater than or equal to its coupon barrier value on the related valuation date. You are not assured of receiving any contingent coupon. Contingent coupon: For each underlying, 65.00% of its initial underlying value Coupon barrier value: For each underlying, 60.00% of its initial underlying value Final barrier value: We may call the securities, in whole and not in part, for mandatory redemption on any potential redemption date upon not less than three business days' notice Redemption: Quarterly on valuation dates beginning after six months Potential redemption dates: 17331UQE0 / US17331UQE00 CUSIP / ISIN: For each underlying, its closing value on the pricing date Initial underlying value: For each underlying, its closing value on the final valuation date Final underlying value: For each underlying on any valuation date, (i) its current closing value minus initial underlying value, divided by (ii) its initial underlying value Underlying return: On any valuation date, the underlying with the lowest underlying return Worst performer: • If the final underlying value of the worst performer is greater than or equal to its final barrier value: $1,000 • If the final underlying value of the worst performer is less than its final barrier value: $1,000 + ($1,000 п the underlying return of the worst performer on the final valuation date) If the securities are not redeemed prior to maturity and the final underlying value of the worst performer on the final valuation date is less than its final barrier value, you will receive significantly less than the stated principal amount of your securities, and possibly nothing, at maturity, and you will not receive any contingent coupon payment at maturity. All payments on the securities are subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc. Payment at maturity: $1,000 per security Stated principal amount: Preliminary Pricing Supplement dated May 8, 2024 Preliminary pricing supplement: * The actual contingent coupon rate will be determined on the pricing date. ** The hypotheticals assume that the contingent coupon will be set at the lowest value indicated in this offering summary. *** Assumes the securities have not been previously redeemed on any interim valuation date Hypothetical Interim Payment per Security ** Hypothetical Payment for Interim Valuation Date *** Hypothetical Worst Underlying Return on Interim Valuation Date $32.75 100.00% $32.75 50.00% $32.75 25.00% $32.75 0.00% $32.75 - 35.00% $0.00 - 35.01% $0.00 - 50.00% $0.00 - 75.00% $0.00 - 100.00% Hypothetical Payment at Maturity per Security Assumes the securities have not been redeemed prior to maturity and does not include the final contingent coupon payment, if any. Hypothetical Payment at Maturity Hypothetical Worst Underlying Return on Final Valuation Date $1,000.00 100.00% $1,000.00 50.00% $1,000.00 25.00% $1,000.00 0.00% $1,000.00 - 25.00% $1,000.00 - 40.00% $599.90 - 40.01% $500.00 - 50.00% $250.00 - 75.00% $0.00 - 100.00%

Citigroup Global Markets Holdings Inc. Guaranteed by Citigroup Inc. Selected Risk Considerations • You may lose a significant portion or all of your investment. Unlike conventional debt securities, the securities do not provide for the repayment of the stated principal amount at maturity in all circumstances. If the securities are not redeemed prior to maturity, your payment at maturity will depend on the final underlying value of the worst performer on the final valuation date. If the final underlying value of the worst performer on the final valuation date is less than its final barrier value, you will lose 1% of the stated principal amount of your securities for every 1% by which the worst performer on the final valuation date has declined from its initial underlying value. There is no minimum payment at maturity on the securities, and you may lose up to all of your investment. • You will not receive any contingent coupon following any valuation date on which the closing value of the worst performer on that valuation date is less than its coupon barrier value. • We may redeem the securities at our option, which will limit your ability to receive the contingent coupon payments. • The securities are subject to heightened risk because they have multiple underlyings. • The return on the securities depends solely on the performance of the worst performer. As a result, the securities are subject to the risks of each of the underlyings and will be negatively affected if any one underlying performs poorly. • You will be subject to risks relating to the relationship between the underlyings. The less correlated the underlyings, the more likely it is that any one of the underlyings will perform poorly over the term of the securities. All that is necessary for the securities to perform poorly is for one of the underlyings to perform poorly. • The securities offer downside exposure, but no upside exposure, to the underlyings. • The securities are particularly sensitive to the volatility of the closing values of the underlyings on or near the valuation dates. • The securities are subject to the credit risk of Citigroup Global Markets Holdings Inc. and Citigroup Inc. If Citigroup Global Markets Holdings Inc. defaults on its obligations under the securities and Citigroup Inc. defaults on its guarantee obligations, you may not receive anything owed to you under the securities. • The securities will not be listed on any securities exchange and you may not be able to sell them prior to maturity. • The estimated value of the securities on the pricing date will be less than the issue price. For more information about the estimated value of the securities, see the accompanying preliminary pricing supplement. • The value of the securities prior to maturity will fluctuate based on many unpredictable factors. • The Russell 2000 ® Index is subject to risks associated with small capitalization stocks. • The SPDR ® S&P ® Biotech ETF is subject to risks associated with investing in the biotechnology sector. • The SPDR ® S&P ® Regional Banking ETF is subject to concentrated risks associated with the banking industry. • The issuer and its affiliates may have conflicts of interest with you. • The U.S. federal tax consequences of an investment in the securities are unclear. The above summary of selected risks does not describe all of the risks associated with an investment in the securities. You should read the accompanying preliminary pricing supplement and product supplement for a more complete description of risks relating to the securities. Additional Information Citigroup Global Markets Holdings Inc. and Citigroup Inc. have filed registration statements (including the accompanying preliminary pricing supplement, product supplement, underlying supplement, prospectus supplement and prospectus) with the Securities and Exchange Commission (“SEC”) for the offering to which this communication relates. Before you invest, you should read the accompanying preliminary pricing supplement, product supplement, underlying supplement, prospectus supplement and prospectus in those registration statements (File Nos. 333 - 270327 and 333 - 270327 - 01) and the other documents Citigroup Global Markets Holdings Inc. and Citigroup Inc. have filed with the SEC for more complete information about Citigroup Global Markets Holdings Inc., Citigroup Inc. and this offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, you can request these documents by calling toll - free 1 - 800 - 831 - 9146. Filed pursuant to Rule 433 This offering summary does not contain all of the material information an investor should consider before investing in the securities. This offering summary is not for distribution in isolation and must be read together with the accompanying preliminary pricing supplement and the other documents referred to therein, which can be accessed via the link on the first page.