Table of Contents

Filed pursuant to Rule 424(b)(2)

Registration Nos. 333-132370 and 333-132370-01

CALCULATION OF REGISTRATION FEE

Class of securities offered | Aggregate offering price | Amount of registration fee | |||||

Medium-Term Senior Notes, Series D | $ | 14,220,000.00 | $ | 436.55 | (1) | ||

| (1) | The filing fee of $436.55 is calculated in accordance with Rule 457(r) of the Securities Act of 1933. Pursuant to Rule 457(p) under the Securities Act of 1933, the $191,841.18 remaining of the filing fee previously paid with respect to unsold securities that were registered pursuant to a Registration Statement on Form S-3 (No. 333-119615) filed by Citigroup Global Market Holdings Inc., a wholly owned subsidiary of Citigroup Inc., on October 8, 2004 is being carried forward, of which $436.55 is offset against the registration fee due for this offering and of which $191,404.63 remains available for future registration fees. No additional registration fee has been paid with respect to this offering. |

Table of Contents

PRICING SUPPLEMENT NO. 2007-MTNDD187 DATED NOVEMBER 26, 2007

(TO PROSPECTUS SUPPLEMENT DATED APRIL 13, 2006 AND PROSPECTUS DATED MARCH 10, 2006) MEDIUM-TERM NOTES, SERIES D

CITIGROUP FUNDING INC.

Premium mAndatory Callable

Equity-linked secuRitieS

9% Per Annum PACERS Based Upon the

American Depositary Shares of Companhia Vale do Rio Doce

Due June 9, 2009

$10.00 per PACERS

Any Payments Due from Citigroup Funding Inc.

Fully and Unconditionally Guaranteed by Citigroup Inc.

| n | The PACERS will mature on June 9, 2009, unless called earlier by us. |

| n | The PACERS bear interest at the rate of 9% per annum. We will pay interest in cash semi-annually on the ninth day of June and December, commencing on June 9, 2008 up to and including the earlier of (i) any date on which the PACERS are called by us or (ii) maturity. |

| n | We will call the PACERS for cash in an amount equal to the sum of $10 and a mandatory call premium if the closing price of the American Depositary Shares of Companhia Vale do Rio Doce (which we refer to as CVRD depositary shares) on any trading day during each of the three-trading-day periods starting on and including June 2, 2008, December 2, 2008 or June 2, 2009 is greater than or equal to $31.00 (which we refer to as the initial share price). |

| n | If we do not call the PACERS, you will receive at maturity for each PACERS either (1) a certain number of CVRD depositary shares (or if you elect, the cash value of those shares), which we refer to as the share ratio and which is subject to adjustment for a number of dilution events, if the closing price of CVRD depositary shares on any trading day after the date of this pricing supplement, which we refer to as the pricing date, up to and including the third trading day before maturity is less than or equal to $20.15 (approximately 65% of the initial share price) or (2) $10 in cash. The share ratio will equal $10 divided by the initial share price. |

| n | The PACERS are not principal-protected. At maturity you could receive CVRD depositary shares with a value less than your initial investment in the PACERS (or, if you elect, the cash value of those shares in an amount less than $10 per PACERS). |

| n | The PACERS will not be listed on any exchange. |

Investing in the PACERS involves a number of risks. See “Risk Factors Relating to the PACERS” beginning on page PS-7.

The PACERS represent obligations of Citigroup Funding Inc. only. Companhia Vale do Rio Doce is not involved in any way in the offering and has no obligations relating to the PACERS or to the holders of the PACERS.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the PACERS or determined that this pricing supplement and accompanying prospectus supplement and prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per PACERS | Total | |||

Public Offering Price | $10.00 | $14,220,000 | ||

Underwriting Discount | $0.225 | $319,950 | ||

Proceeds to Citigroup Funding Inc. | $9.775 | $13,900,050 |

The agent expects to deliver the PACERS to purchasers on or about November 29, 2007.

| Investment Products | Not FDIC Insured | May Lose Value | No Bank Guarantee |

Table of Contents

What Are the PACERS?

PACERS are callable securities. PACERS’ return, if any, and the amount you will receive at maturity is linked to the closing price of the American Depositary Shares of Companhia Vale do Rio Doce (which we refer to as CVRD depositary shares). We will call the PACERS, in whole, but not in part, only if the closing price of CVRD depositary shares on any trading day during the three-trading-day periods starting on and including June 2, 2008, December 2, 2008 or June 2, 2009 (which we refer to as call determination periods) is greater than or equal to the initial share price of $31.00. The PACERS will not otherwise be called even if the closing price on any other day is greater than or equal to the initial share price of $31.00. If we call the PACERS, you will receive for each PACERS a call price in cash equal to the sum of $10 plus a mandatory call premium. We will provide notice of a call, including the exact payment date, within one business day after the call of the PACERS and will make the payment associated with such call on the earlier of at least three business days after such call or the maturity date. If we call the PACERS during the call determination period beginning on June 2, 2009, we will not provide notice of a call but will pay the call price to you at maturity.

If we do not call the PACERS, you will receive at maturity cash equal to your initial investment of $10 per PACERS, unless the closing price of CVRD depositary shares on any trading day after the pricing date up to and including the third trading day before maturity (which we refer to as the valuation date) is less than or equal to $20.15 (approximately 65% of the initial share price). In this case, you will receive at maturity a certain number of CVRD depositary shares (or, if you elect, the cash value of those shares) the value of which will be directly linked to the change in price of CVRD depositary shares from its closing price on the pricing date, and will likely be less than the amount of your initial investment and could be zero. If we do not call the PACERS, you will not in any case benefit from any increase in the price of CVRD depositary shares or receive an amount at maturity greater than your initial investment unless (1) the closing price of CVRD depositary shares on any trading day after the pricing date up to and including the valuation date is less than or equal to $20.15 (approximately 65% of the initial share price), (2) you do not exercise your cash election right but receive CVRD depositary shares at maturity and (3) at maturity the price of CVRD depositary shares is greater than the initial share price. The PACERS are not principal protected.

The PACERS mature on June 9, 2009, are callable by us semi-annually on any trading day during each call determination period starting on and including June 2, 2008, December 2, 2008 or June 2, 2009, and do not provide for earlier redemption by you. The PACERS are a series of unsecured senior debt securities issued by Citigroup Funding Inc. and any payments due on the PACERS are fully and unconditionally guaranteed by Citigroup Inc. The PACERS will rank equally with all other unsecured and unsubordinated debt of Citigroup Funding and, as a result of the guarantee, any payments due under the PACERS will rank equally with all other unsecured and unsubordinated debt of Citigroup Inc. The return of the principal amount of your investment in the PACERS is not guaranteed.

Each PACERS represents a principal amount of $10. You may transfer the PACERS only in units of $10 and integral multiples of $10. You will not have the right to receive physical certificates evidencing your ownership except under limited circumstances. Instead, we will issue the PACERS in the form of a global certificate, which will be held by the Depository Trust Company or its nominee. Direct and indirect participants in DTC will record beneficial ownership of the PACERS by individual investors. Accountholders in the Euroclear or Clearstream Banking clearance systems may hold beneficial interests in the PACERS through the accounts that these systems maintain with DTC. You should refer to the section “Description of the PACERS — Book-Entry System” in the accompanying prospectus supplement and the section “Description of Debt Securities — Book-Entry Procedures and Settlement” in the accompanying prospectus.

PS-2

Table of Contents

Will I Receive Interest on the PACERS?

The PACERS bear interest at the rate of 9% per annum (to be determined on the pricing date). We will pay cash semi-annually on the ninth day of June and December, (which we refer to as a coupon payment date), commencing on June 9, 2008 up to and including the earlier of (i) any date on which the PACERS are called by us or (ii) maturity.

What Will I Receive if Citigroup Funding Calls the PACERS?

We will call the PACERS, in whole, but not in part, if the closing price of CVRD depositary shares on any trading day during the three-trading-day periods starting on and including June 2, 2008, December 2, 2008 or June 2, 2009 is greater than or equal to the initial share price of $31.00. We refer to the three trading days each six months as a call determination period, and we refer to the trading day on which we call the PACERS, if any, as the call date. If we call the PACERS, you will receive for each PACERS a call price in cash equal to the sum of $10 and a mandatory call premium. The mandatory call premium will equal $0.80 if the PACERS are called during the call determination period beginning on June 2, 2008, $1.60 if the PACERS are called during the call determination period beginning on December 2, 2008 and $2.40 if the PACERS are called during the call determination period beginning on June 2, 2009.

If we call the PACERS during one of the call determination periods beginning on June 2, 2008 or December 2, 2008, we will provide notice of a call, including the exact call payment date, within one business day after the call date, and the call payment date will be at least three business days after the call date. If we call the PACERS during the call determination period beginning on June 2, 2009, we will not provide notice of a call but will pay the call price to you at maturity.

The opportunity to fully participate in possible increases in the price of CVRD depositary shares through an investment in the PACERS is limited if we call the PACERS because the return you receive will be limited to the amount of the applicable mandatory call premium and any interest payments on the PACERS.

What Will I Receive at Maturity of the PACERS?

If we call the PACERS during the call determination period beginning on June 2, 2009, at maturity you will receive for each PACERS you hold a call price in cash equal to $12.40, the sum of $10 and the applicable mandatory call premium.

If we do not call the PACERS, at maturity you will receive for each PACERS you hold either:

| • | a number of CVRD depositary shares equal to the share ratio (or, if you elect, the cash value of those shares based on the closing price of CVRD depositary shares on the valuation date), if the closing price of CVRD depositary shares on any trading day after the pricing date up to and including the valuation date is less than or equal to $20.15 (approximately 65% of the initial share price) (any fractional share, if applicable, will be paid in cash), or |

| • | $10 in cash. |

As a result, if we do not call the PACERS and the closing price of CVRD depositary shares on any trading day after the pricing date up to and including the valuation date is less than or equal to approximately 65% of the initial share price, the value of CVRD depositary shares you receive at maturity (or, if you elect, the cash value of those shares) for each PACERS will likely be less than the price paid for each PACERS, and could be zero.

PS-3

Table of Contents

If applicable, you may elect to receive from Citigroup Funding the cash value of the shares you would otherwise receive at maturity by providing notice of your election to your broker, in accordance with your broker’s procedures, so that your broker can irrevocably notify the trustee and paying agent of your election no sooner than 20 business days before maturity and no later than 5 business days before maturity. If you do not elect to receive cash, you will be deemed to have (1) instructed Citigroup Funding to pay the cash value of the number of CVRD depositary shares equal to the share ratio to the stock delivery agent, and (2) instructed the stock delivery agent to purchase for you CVRD depositary shares based on its closing price on the valuation date. If you do not wish to receive CVRD depositary shares at maturity under any circumstances, you should provide notice of your cash election to your broker. You should provide this notice even if the closing price of CVRD depositary shares on any trading day prior to your election has not been less than or equal to $20.15 (approximately 65% of the initial share price). If you elect to receive the cash value of CVRD depositary shares equal to the share ratio you would otherwise be entitled to at maturity, the amount of cash you receive at maturity will be determined based on the closing price of CVRD depositary shares on the valuation date and will be an amount less than $10 per PACERS. This amount will not change from the amount fixed on the valuation date, even if the closing price of CVRD depositary shares changes from the valuation date to maturity. Conversely, if you do not make a cash election and instead receive a number of CVRD depositary shares at maturity equal to the share ratio, the value of those shares at maturity will be different than the value of those shares on the valuation date if the closing price of CVRD depositary shares changes from the valuation date to maturity.

The payment of cash to the stock delivery agent by Citigroup Funding pursuant to your deemed instruction will fully satisfy Citigroup Funding’s obligation to you under the PACERS, and the stock delivery agent will then be obligated to purchase CVRD depositary shares for you based on the closing price on the valuation date. Citigroup Global Markets has agreed to act as stock delivery agent for the PACERS.

The initial share price equals $31.00, the closing price of CVRD depositary shares on the pricing date.

The share ratio equals 0.32258, $10 divided by the initial share price.

Where Can I Find Examples of Hypothetical Amounts Payable at Call or at Maturity?

For a table and graphs setting forth hypothetical amounts you could receive upon a call of the PACERS or at maturity, see “Description of the PACERS — Amounts Payable at Call or Maturity — Hypothetical Examples” in this pricing supplement.

What Are CVRD Depositary Shares?

“CVRD depositary shares” refers to the American Depositary Shares of Companhia Vale do Rio Doce, each of which represents one common share of CVRD and is evidenced by one American Depositary Receipt. Each CVRD depositary share has been deposited and is held, on behalf of the holders of CVRD American Depositary Receipts, by the custodian for the depositary, and/or such other firm or corporation as the depositary may appoint. While the market for the common shares of CVRD is on the São Paulo Stock Exchange in Brazil and while trading in that market is based on the Brazilian real, CVRD depositary shares trade in U.S. dollars on the New York Stock Exchange under the symbol “RIO.”

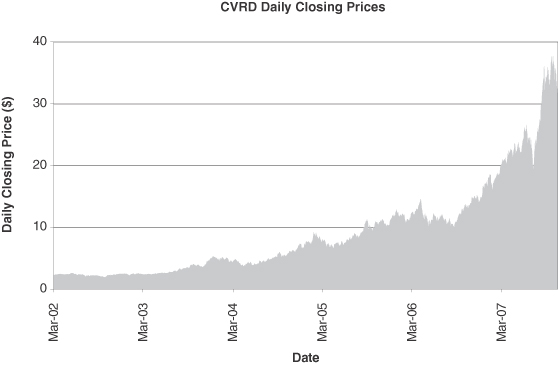

How Have CVRD Depositary Shares Performed Historically?

We have provided a graph showing the daily closing price of CVRD depositary shares, as reported on the New York Stock Exchange from March 21, 2002 to November 26, 2007 and a table showing the high and low sale prices for CVRD depositary shares and the dividends paid on such shares for each quarter since the first quarter of 2002. You can find this graph and table in the section “Historical Data on CVRD Depositary Shares.” in this pricing supplement. We have provided this historical information to help you evaluate the behavior of

PS-4

Table of Contents

CVRD depositary shares in recent years. However, past performance is not indicative of how CVRD depositary shares will perform in the future. You should also refer to the section “Risk Factors Relating to the PACERS — The Historical Performance of CVRD Depositary Shares Is Not an Indication of the Future Performance of CVRD Depositary Shares” in this pricing supplement.

What Are the United States Federal Income Tax Consequences of Investing in the PACERS?

In purchasing a PACERS, you agree with Citigroup Funding that you and Citigroup Funding intend to treat a PACERS for U.S. federal income tax purposes as a derivative financial instrument providing for the future purchase of, or payment based on the value of, CVRD depositary shares. Under this treatment, if you hold the PACERS until they mature and, if not called, you elect to receive cash at maturity, you will recognize capital gain or loss equal to the difference between the amount of cash received and your purchase price for the PACERS. If you receive CVRD depositary shares at maturity of the PACERS, you should not expect to recognize any gain or loss on the receipt of CVRD depositary shares, and your tax basis in CVRD depositary shares generally will equal your purchase price for the PACERS. Upon the mandatory redemption of the PACERS for cash prior to or at maturity, or the sale or other taxable disposition of a PACERS, you generally will recognize capital gain or loss equal to the difference, if any, between the amount of cash received as a result of such mandatory redemption, sale or other taxable disposition and your tax basis in the PACERS. Any such gain or loss generally will be long-term capital gain or loss if you have held the PACERS for more than one year at the time of disposition. Due to the absence of authority as to the proper characterization of the PACERS, no assurance can be given that the Internal Revenue Service (“IRS”) will accept, or that a court will uphold, the characterization and tax treatment described above, and alternative treatments of the PACERS could result in less favorable U.S. federal income tax consequences to you, including a requirement to accrue income on a current basis. In addition, there is no assurance that the IRS will agree with the agreed-to characterization and tax treatment of the receipt of CVRD depositary shares by you at maturity of the PACERS and you may be required by the IRS to recognize gain on the receipt of the CVRD depositary shares. You should refer to the section “Certain United States Federal Income Tax Considerations” in this pricing supplement for more information.

Will the PACERS Be Listed on a Stock Exchange?

No. The PACERS will not be listed on any exchange. There is currently no secondary market for the PACERS. Even if a secondary market does develop, it may not be liquid and may not continue for the term of the PACERS. Although Citigroup Global Markets intends to create a market in the PACERS, it is not obligated to do so.

Can You Tell Me More About Citigroup Inc. and Citigroup Funding?

Citigroup Inc. is a diversified global financial services holding company whose businesses provide a broad range of financial services to consumer and corporate customers. Citigroup Funding is a wholly-owned subsidiary of Citigroup Inc. whose business activities consist primarily of providing funds to Citigroup Inc. and its subsidiaries for general corporate purposes.

What Is the Role of Citigroup Funding’s and Citigroup Inc.’s Affiliate, Citigroup Global Markets?

Our affiliate, Citigroup Global Markets, is the agent for the offering and sale of the PACERS and is expected to receive compensation for activities and services provided in connection with the offering. After the initial offering, Citigroup Global Markets and/or other of our broker-dealer affiliates intend to buy and sell the PACERS to create a secondary market for holders of the PACERS, and may engage in other activities described in the section “Plan of Distribution” in this pricing supplement, the accompanying prospectus supplement and

PS-5

Table of Contents

prospectus. However, neither Citigroup Global Markets nor any of these affiliates will be obligated to engage in any market-making activities, or continue such activities once it has started them. Citigroup Global Markets will also act as calculation agent for the PACERS. Potential conflicts of interest may exist between Citigroup Global Markets and you as holder of the PACERS.

Can You Tell Me More About the Effect of Citigroup Funding’s Hedging Activity?

We expect to hedge our obligations under the PACERS through one or more of our affiliates. This hedging activity will likely involve trading in CVRD depositary shares or the common shares of CVRD, or in other instruments, such as options, swaps or futures, based upon CVRD depositary shares or the common shares of CVRD. This hedging activity could affect the market price of CVRD depositary shares and therefore the market value of the PACERS. The costs of maintaining or adjusting this hedging activity could also affect the price at which our affiliate Citigroup Global Markets may be willing to purchase your PACERS in the secondary market. Moreover, this hedging activity may result in us or our affiliates receiving a profit, even if the market value of the PACERS declines. You should refer to “Risk Factors Relating to the PACERS — The Price at Which You Will Be Able to Sell Your PACERS Prior to Maturity Will Depend on a Number of Factors and May Be Substantially Less Than the Amount You Originally Invest” in this pricing supplement, “Risk Factors — Citigroup Funding’s Hedging Activity Could Result in a Conflict of Interest” in the accompanying prospectus supplement and “Use of Proceeds and Hedging” in the accompanying prospectus.

Does ERISA Impose Any Limitations on Purchases of the PACERS?

Employee benefit plans and other entities the assets of which are subject to the fiduciary responsibility provisions of the Employee Retirement Income Security Act of 1974, as amended, Section 4975 of the Internal Revenue Code of 1986, as amended, or substantially similar federal, state or local laws, including individual retirement accounts, (which we call “Plans”) will be permitted to purchase and hold the PACERS, provided that each such Plan shall by its purchase be deemed to represent and warrant either that (A)(i) none of Citigroup Global Markets, its affiliates or any employee thereof is a Plan fiduciary that has or exercises any discretionary authority or control with respect to the Plan’s assets used to purchase the PACERS or renders investment advice with respect to those assets and (ii) the Plan is paying no more than adequate consideration for the PACERS or (B) its acquisition and holding of the PACERS is not prohibited by any such provisions or laws or is exempt from any such prohibition. However, individual retirement accounts, individual retirement annuities and Keogh plans, as well as employee benefit plans that permit participants to direct the investment of their accounts, willnot be permitted to purchase or hold the PACERS if the account, plan or annuity is for the benefit of an employee of Citigroup Global Markets or a family member and the employee receives any compensation (such as, for example, an addition to bonus) based on the purchase of PACERS by the account, plan or annuity. Please refer to the section “ERISA Matters” in this pricing supplement for further information.

Are There Any Risks Associated with My Investment in the PACERS?

Yes, the PACERS are subject to a number of risks. Please refer to the section “Risk Factors Relating to the PACERS” in this pricing supplement.

PS-6

Table of Contents

RISK FACTORS RELATING TO THE PACERS

Because the terms of the PACERS differ from those of conventional debt securities in that, unless the PACERS are called by us, the amount you receive at maturity will be based on the closing price of CVRD depositary shares on any trading day after the pricing date up to and including the valuation date, an investment in the PACERS entails significant risks not associated with similar investments in conventional debt securities, including, among other things, fluctuations in the price of CVRD depositary shares and other events that are difficult to predict and beyond our control.

Your Investment in the PACERS May Result in a Loss if the Closing Price of CVRD Depositary Shares Declines

If we do not call the PACERS, the amount you receive at maturity will depend on the closing price of CVRD depositary shares on any trading day after the pricing date up to and including the valuation date. As a result, the amount you receive at maturity may be less than the amount you paid for your PACERS. If we do not call the PACERS and (i) on any trading day after the pricing date up to and including the valuation date the closing price of CVRD depositary shares is less than or equal to $20.15 (approximately 65% of the initial share price), and (ii) at maturity (or the valuation date if you elect to receive cash value of CVRD depositary shares) the price of CVRD depositary shares is less than the initial share price, then the value of CVRD depositary shares you receive at maturity (or, if you elect, the cash value of those Shares on the valuation date) will be less than the price paid for each PACERS, and could be zero, in which case your investment in the PACERS will result in a loss, except to the extent of any interest payments on the PACERS. If we do not call the PACERS, this will be true even if the closing price of CVRD depositary shares exceeds the initial share price at one or more times after the pricing date but is less than or equal to approximately 65% of the initial share price on any trading day after the pricing date up to and including the valuation date and the price of CVRD depositary shares at maturity (or the closing price on the valuation date if you elect to receive the cash value of CVRD depositary shares) is less than the initial share price.

The PACERS Have a Mandatory Call Feature Which Limits the Potential Appreciation of Your Investment

We will call the PACERS if the closing price of CVRD depositary shares on any trading day during the three call determination periods beginning on June 2, 2008, December 2, 2008 or June 2, 2009 is greater than or equal to the initial share price. If we call the PACERS, you will receive a call price in cash equal to $10 plus a mandatory call premium. The opportunity to participate in possible increases in the closing price of CVRD depositary shares through an investment in the PACERS is limited because the return you receive if we call the PACERS will be limited to the amount of the applicable mandatory call premium and any interest payments on the PACERS. Therefore, your return on the PACERS may be less than your return on a similar security that was directly linked to CVRD depositary shares and allowed you to participate more fully in the appreciation of the price of CVRD depositary shares.

The Yield on the PACERS May Be Lower Than the Yield on a Standard Debt Security of Comparable Maturity

The PACERS bear interest at the rate of 9% per annum. As a result, if we do not call the PACERS, (and regardless of whether the closing price of CVRD depositary shares on any trading day after the pricing date up to and including the valuation date is less than or equal to $20.15 (approximately 65% of the initial share price) the effective yield on the PACERS may be less than that which would be payable on a conventional fixed-rate, non-callable debt security of Citigroup Funding of comparable maturity.

PS-7

Table of Contents

You May Not Be Able to Sell Your PACERS if an Active Trading Market for the PACERS Does Not Develop

The PACERS will not be listed on any exchange. There is currently no secondary market for the PACERS. Citigroup Global Markets currently intends, but is not obligated, to make a market in the PACERS. Even if a secondary market does develop, it may not be liquid and may not continue for the term of the PACERS. If the secondary market for the PACERS is limited, there may be few buyers should you choose to sell your PACERS prior to maturity and this may reduce the price you receive.

The Price at Which You Will Be Able to Sell Your PACERS Prior to Maturity Will Depend on a Number of Factors and May Be Substantially Less Than the Amount You Originally Invest

We believe that the value of your PACERS in the secondary market will be affected by the supply of and demand for the PACERS, the price of CVRD depositary shares and a number of other factors. Some of these factors are interrelated in complex ways. As a result, the effect of any one factor may be offset or magnified by the effect of another factor. The following paragraphs describe what we expect to be the impact on the market value of the PACERS of a change in a specific factor, assuming all other conditions remain constant.

Price of CVRD Depositary Shares. We expect that the market value of the PACERS will depend substantially on the amount, if any, by which the price of CVRD depositary shares changes from the initial share price of $31.00. However, changes in the price of CVRD depositary shares may not always be reflected, in full or in part, in the market value of the PACERS. If you choose to sell your PACERS when the price of CVRD depositary shares exceeds the initial share price, you may receive substantially less than the amount that would be payable at maturity or upon a call based on that price because of expectations that the price of CVRD depositary shares will continue to fluctuate between that time and the time when the amount you will receive at maturity or upon a call is determined. In addition, significant increases in the value of CVRD depositary shares are not likely to be reflected in the trading price of the PACERS because we will call the PACERS on the earliest of the three call determination periods beginning on June 2, 2008, December 2, 2008 or June 2, 2009 for a mandatory call premium of $0.80, $1.60 or $2.40, respectively, if the closing price of CVRD depositary shares on any closing day during any of the call determination periods is greater than or equal to the initial share price. If you choose to sell your PACERS when the price of CVRD depositary shares is below the initial share price, you may receive less than the amount you originally invested.

The price of CVRD depositary shares will be influenced by CVRD’s results of operations and by complex and interrelated political, economic, financial and other factors that can affect the capital markets generally and the market segment of which CVRD is a part. Citigroup Funding’s hedging activities, the issuance of securities similar to the PACERS and other trading activities by Citigroup Funding, its affiliates and other market participants can also affect the price of CVRD depositary shares.

Volatility of CVRD Depositary Shares. Volatility is the term used to describe the size and frequency of market fluctuations. If the expected volatility of CVRD depositary shares changes during the term of the PACERS, the market value of the PACERS may decrease.

Mandatory Call Feature. The possibility that the PACERS may be called during one of the call determination periods occurring every six months is likely to limit their value. If the PACERS did not include a mandatory call feature, we expect their value would be significantly different.

Events Involving CVRD. General economic conditions and earnings results of CVRD and real or anticipated changes in those conditions or results, as well as events in Brazil, may affect the value of CVRD depositary shares and the market value of the PACERS. In addition, if the dividend yield on CVRD depositary shares increases, we expect that the value of the PACERS may decrease because the value of any shares or cash you will receive at maturity will not reflect the value of such dividend payments.

PS-8

Table of Contents

Interest Rates. We expect that the market value of the PACERS will be affected by changes in U.S. interest rates. In general, if U.S. interest rates increase, the market value of the PACERS may decrease, and if U.S. interest rates decrease, the market value of the PACERS may increase.

Time Premium or Discount. As a result of a “time premium or discount,” the PACERS may trade at a value above or below that which would be expected based on the level of interest rates and the price of CVRD depositary shares the longer the time remaining to maturity. A “time premium or discount” results from expectations concerning the price of CVRD depositary shares during the period prior to the maturity of the PACERS. However, as the time remaining to maturity decreases, this time premium or discount may diminish, increasing or decreasing the market value of the PACERS.

Hedging Activities. Hedging activities related to the PACERS by us or one or more of our affiliates will likely involve trading in CVRD depositary shares or the common shares of CVRD, or in other instruments, such as options, swaps or futures, based upon CVRD depositary shares or the common shares of CVRD. This hedging activity could affect the market price of CVRD depositary shares and therefore the market value of the PACERS. It is possible that we or our affiliates may profit from our hedging activity, even if the market value of the PACERS declines. Profits or losses from this hedging activity could affect the price at which our affiliate Citigroup Global Markets may be willing to purchase your PACERS in the secondary market.

Credit Ratings, Financial Condition and Results. Actual or anticipated changes in Citigroup Funding’s financial condition or results or the credit ratings, financial condition, or results of Citigroup Inc. may affect the market value of the PACERS. The PACERS are subject to the credit risk of Citigroup Inc., the guarantor of any payments due on the PACERS.

We want you to understand that the impact of one of the factors specified above may offset some or all of any change in the market value of the PACERS attributable to another factor.

The Value of CVRD Depositary Shares May Not Completely Track the Value of the Common Shares of CVRD

Although the trading characteristics and valuations of CVRD depositary shares will usually mirror the characteristics and valuations of the underlying common shares of CVRD, the value of CVRD depositary shares may not completely track the value of the underlying common shares of CVRD. Active trading volume and efficient pricing on the São Paulo Stock Exchange for the underlying common shares of CVRD will usually, but not necessarily, indicate similar characteristics in respect of CVRD depositary shares. Because of the size of the offering of CVRD depositary shares outside Brazil and/or other factors that have limited or increased the float of certain American Depositary Shares, the liquidity of CVRD depositary shares may be less than or greater than that of the underlying common shares of CVRD. In addition, the terms and conditions of depositary facilities may result in less liquidity or lower market value of CVRD depositary shares than for the underlying common shares of CVRD. Since holders of CVRD depositary shares may surrender the American Depositary Shares in order to take delivery of and trade the underlying common shares of CVRD, a characteristic that allows investors in American Depositary Shares to take advantage of price differentials between different markets, a market for the underlying common shares of CVRD that is not liquid will generally result in an illiquid market for the CVRD depositary shares.

The price of CVRD depositary shares is quoted in U.S. dollars. Thus, the starting values and ending values of CVRD depositary shares will be expressed in U.S. dollars and the maturity payment on the PACERS will be made in U.S. dollars. However, you should be aware that a depreciation of the value of the currencies in which the underlying common shares of CVRD are traded versus the U.S. dollar may reduce the trading price of CVRD depositary shares (and thus the trading price of and the maturity payment on the PACERS).

PS-9

Table of Contents

The Trading Price of CVRD Depositary Shares and the PACERS Will Be Affected by Conditions in the Brazilian Securities Markets

Although the market price of CVRD depositary shares is not directly tied to the trading price of the underlying common shares of CVRD in Brazil, the trading price of CVRD depositary shares is expected generally to track the U.S. dollar value of the Brazilian real trading price of the underlying common shares of CVRD on the São Paulo Stock Exchange. This means that the trading value of CVRD depositary shares is expected to be affected by the U.S. dollar/Brazilian real exchange rate and by factors affecting the São Paulo Stock Exchange.

Investments in securities linked to the value of Brazilian equity securities involve certain risks. The Brazilian markets may be more volatile than U.S. or other securities markets and may be affected by market developments in different ways than U.S. or other securities markets. Also, there is generally less publicly available information about Brazilian companies than about U.S. companies, and Brazilian companies are subject to accounting, auditing and financial reporting standards and requirements that differ from those applicable to U.S. companies.

Securities prices in Brazil are subject to political, economic, financial and social factors that apply in Brazil. These factors, which could negatively affect the Brazilian securities markets, include the possibility of recent or future changes in local or Brazil-wide political leadership and economic and fiscal policies, the possible imposition of, or changes in, currency exchange laws or other laws or restrictions applicable to such companies or investments in Brazilian equity securities and the possibility of fluctuations in the rate of exchange between currencies. Moreover, the Brazilian economy may differ favorably or unfavorably from the U.S. economy in such respects as growth of gross national product, rate of inflation, capital investment, resources and self-sufficiency.

The São Paulo Stock Exchange is relatively small and illiquid compared to stock exchanges in major financial centers and a small number of issuers represent a disproportionately large percentage of market capitalization and trading volume. A liquid trading market for the common shares of CVRD may not continue or expand. A limited trading market may impair the ability of a holder of CVRD depositary shares to sell the common shares of CVRD obtained upon withdrawal of such shares of the American Depositary Shares facility in the amount and at the price and time such holder desires, and could increase the volatility of the price of CVRD depositary shares.

The Historical Performance of CVRD Depositary Shares Is Not an Indication of the Future Performance of CVRD Depositary Shares

The historical performance of CVRD depositary shares, which is included in this pricing supplement, should not be taken as an indication of the future performance of CVRD depositary shares during the term of the PACERS. Changes in the price of CVRD depositary shares will affect the value of the PACERS, but it is impossible to predict whether the price of CVRD depositary shares will rise or fall.

The Volatility of the Price of CVRD Depositary Shares May Result in Delivery of CVRD Depositary Shares at Maturity

Historically, the price of CVRD depositary shares has been volatile. From March 21, 2002 to November 26, 2007, the closing price of CVRD depositary shares has been as low as $1.81 per share and as high as $38.32 per share. As a result, on more than one occasion from April 5, 2007 to November 26, 2007, the closing price of CVRD depositary shares has been less than 65% of its closing price of $31.00 on November 26, 2007. If we do not call the PACERS, whether you receive an amount at maturity in cash equal to the amount of your initial investment in the PACERS or a number of CVRD depositary shares (or, if you elect, the cash value of those shares) with a value less than your initial investment depends upon the closing price of CVRD depositary shares on any trading day during the term of the PACERS. The volatility of the price of CVRD depositary shares may

PS-10

Table of Contents

result in your receiving at maturity a number of CVRD depositary shares (or, if you elect, the cash value of those shares) with a value less than your initial investment in the PACERS, which will result in a loss, except to the extent of any interest payments on the PACERS.

You Will Have No Rights Against CVRD Unless and Until You Receive Any CVRD Depositary Shares at Maturity

You will have no rights against CVRD unless and until you receive CVRD depositary shares at maturity, even though:

| • | you will receive CVRD depositary shares at maturity under some circumstances; and |

| • | the market value of the PACERS is expected to depend primarily on the price of CVRD depositary shares. |

CVRD is not in any way involved in this offering and has no obligations relating to the PACERS or to holders of the PACERS. In addition, you will have no voting rights and will receive no dividends or other distributions with respect to CVRD depositary shares unless and until you receive CVRD depositary shares at maturity, if applicable.

The Trading Price of CVRD Depositary Shares and the PACERS May Be Reduced if CVRD Ceases to Be Subject to SEC Reporting Requirements

CVRD is currently subject to the reporting requirements of the Securities and Exchange Commission and publicly files reports and other information on the SEC website. In the event that CVRD ceases to be subject to these reporting requirements, pricing information for the PACERS may be more difficult to obtain and the value, trading price and liquidity of CVRD depositary shares and the PACERS may be reduced.

The Amount You Receive at Maturity May Be Reduced Under Some Circumstances if CVRD Depositary Shares are Diluted Because this Amount Will Not Be Adjusted for All Events that Dilute CVRD Depositary Shares

The amount you receive at maturity is subject to adjustment for a number of events arising from share splits and combinations, share dividends or other distributions, a number of other actions of CVRD that modify its capital structure and a number of other transactions involving CVRD as well as for the liquidation, dissolution or winding up of CVRD. You should refer to the section “Description of the PACERS — Dilution Adjustments,” in this pricing supplement. The amount you receive at maturity, if applicable, will not be adjusted for other events that may adversely affect the price of CVRD depositary shares, such as offerings of the common shares of CVRD for cash or in connection with acquisitions. Because of the relationship of the amount you receive at maturity to the price of CVRD depositary shares, these other events may reduce the amount you receive at maturity on the PACERS.

The Market Value of the PACERS May Be Affected by Purchases and Sales of CVRD Depositary Shares or Derivative Instruments Related to CVRD Depositary Shares by Affiliates of Citigroup Funding

Citigroup Funding’s affiliates, including Citigroup Global Markets, may from time to time buy or sell CVRD depositary shares or derivative instruments relating to CVRD depositary shares or the common shares of CVRD for their own accounts in connection with their normal business practices. These transactions could affect the price of CVRD depositary shares and therefore the market value of the PACERS.

PS-11

Table of Contents

Citigroup Global Markets, an Affiliate of Citigroup Funding and Citigroup Inc., Is the Calculation Agent, Which Could Result in a Conflict of Interest

Citigroup Global Markets, which is acting as the calculation agent for the PACERS, is an affiliate of ours. As a result, Citigroup Global Markets’ duties as calculation agent, including with respect to making certain determinations and judgments that the calculation agent must make in determining amounts due to you, may conflict with its interest as an affiliate of ours.

The United States Federal Income Tax Consequences of the PACERS Are Uncertain

No statutory, judicial or administrative authority directly addresses the characterization of the PACERS or instruments similar to the PACERS for U.S. federal income tax purposes. As a result, significant aspects of the U.S. federal income tax consequences of an investment in the PACERS are not certain. No ruling is being requested from the Internal Revenue Service with respect to the PACERS and no assurance can be given that the Internal Revenue Service will agree with the conclusions expressed under “Certain United States Federal Income Tax Considerations” in this pricing supplement.

PS-12

Table of Contents

The following description of the particular terms of the PACERS supplements, and to the extent inconsistent therewith replaces, the description of the general terms and provisions of the debt securities set forth in the accompanying prospectus supplement and prospectus.

General

Premium mAndatory Callable Equity-linked secuRitieS (PACERSSM) Based Upon the American Depositary Shares of Companhia Vale do Rio Doce (“CVRD Depositary Shares”) are callable securities. PACERS’ return, if any, and the amount you receive at maturity is linked to the Closing Price of CVRD Depositary Shares. We will call the PACERS, in whole, but not in part, only if the Closing Price of CVRD Depositary Shares on any Trading Day during the three-Trading-Day periods starting on and including June 2, 2008, December 2, 2008 or June 2, 2009 is greater than or equal to the Initial Share Price of $31.00. The PACERS will not be called even if the Closing Price on any other day is greater than or equal to the Initial Share Price. If we call the PACERS, you will receive for each PACERS a Call Price in cash equal to the sum of $10 plus a Mandatory Call Premium. If we call the PACERS during one of the call determination periods beginning on June 2, 2008 or December 2, 2008, we will provide notice of a call, including the exact payment date, within one business day after the call of the PACERS and will make the payment associated with such call on the earlier of at least three business days after such call. If we call the PACERS during the call determination period beginning on June 2, 2009, we will not provide notice of a call but will pay the call price to you at maturity.

If we do not call the PACERS, you will receive at maturity cash equal to your initial investment of $10 per PACERS, unless the Closing Price of CVRD Depositary Shares on any Trading Day after the Pricing Date up to and including the Valuation Date is less than or equal to $20.15 (approximately 65% of the Initial Share Price). In this case, you will receive at maturity a number of CVRD Depositary Shares (or, if you elect, the cash value of those shares) the value of which will be directly linked to the change in price of CVRD Depositary Shares from its Closing Price on the Pricing Date, and will likely be less than the amount of your initial investment and could be zero. If we do not call the PACERS, you will not in any case benefit from any increase in the price of CVRD Depositary Shares or receive an amount at maturity greater than your initial investment unless (1) the Closing Price of CVRD Depositary Shares on any Trading Day after the Pricing Date up to and including the Valuation Date is less than or equal to $20.15 (approximately 65% of the Initial Share Price), (2) you do not exercise your cash election right but receive CVRD Depositary Shares at maturity and (3) at maturity the price of CVRD Depositary Shares is greater than the Initial Share Price. PACERS are not principal protected.

The PACERS are a series of debt securities issued under the senior debt indenture described in the accompanying prospectus, any payments due on which are fully and unconditionally guaranteed by Citigroup Inc. The aggregate principal amount of PACERS issued will be $14,220,000 (1,422,000 PACERS). The PACERS will mature on June 9, 2009, unless called earlier by us, will constitute part of the senior debt of Citigroup Funding and will rank equally with all other unsecured and unsubordinated debt of Citigroup Funding. As a result of the Citigroup Inc. guarantee, any payments due under the PACERS will rank equally with all other unsecured and unsubordinated debt of Citigroup Inc. The return of the principal amount of your investment in the PACERS is not guaranteed. The PACERS will be issued only in fully registered form and in denominations of $10 per PACERS and integral multiples thereof.

Reference is made to the accompanying prospectus supplement and prospectus for a detailed summary of additional provisions of the PACERS and of the senior debt indenture under which the PACERS will be issued.

Interest

The PACERS bear interest at the rate of 9% per annum. We will pay interest in cash semi-annually on the ninth day of June and December (each a Coupon Payment Date), commencing on June 9, 2008 up to and including the earlier of (i) any date on which the PACERS are called by us or (ii) maturity. Interest will be

PS-13

Table of Contents

computed on the basis of a 360-day year of twelve 30-day months. The coupon payment will be payable to the persons in whose names the PACERS are registered at the close of business on the third Business Day preceding the Coupon Payment Date. If the Coupon Payment Date falls on a day that is not a Business Day, the coupon payment to be made on that Coupon Payment Date will be made on the next succeeding Business Day with the same force and effect as if made on that Coupon Payment Date, and no additional interest will accrue as a result of such delayed payment.

“Business Day” means any day that is not a Saturday, a Sunday, or a day on which securities exchanges or banking institutions or trust companies in the City of New York are authorized or obligated by law or executive order to close.

Mandatory Call Feature

We will call the PACERS, in whole, but not in part, if the Closing Price of CVRD Depositary Shares on any Trading Day during the three-Trading-Day periods starting on and including June 2, 2008, December 2, 2008 or June 2, 2009 is greater than or equal to the Initial Share Price. We refer to the three Trading Days each six months as a Call Determination Period, and we refer to the Trading Day within a Call Determination Period on which we call the PACERS, if any, as the Call Date. If we call the PACERS, you will receive for each PACERS a Call Price in cash equal to the sum of $10 and a Mandatory Call Premium. The Mandatory Call Premium will equal $0.80 if the PACERS are called during the Call Determination Period beginning on June 2, 2008, $1.60 if the PACERS are called during the Call Determination Period beginning on December 2, 2008 and $2.40, if the PACERS are called during the Call Determination Period beginning on June 2, 2009.

If we call the PACERS during one of the Call Determination Periods beginning on June 2, 2008 or December 2, 2008 we will provide notice of a call, including the exact call payment date, within one business day after the Call Date, and the call payment date will be at least three business days after the Call Date. If we call the PACERS during the Call Determination Period beginning on June 2, 2009, we will not provide notice of a call but will pay the Call Price to you at maturity.

The opportunity to participate in possible increases in the price of CVRD Depositary Shares through an investment in the PACERS is limited if we call the PACERS because the amount you receive will be limited to the Call Price.

So long as the PACERS are represented by global securities and are held on behalf of DTC, call notices and other notices will be given by delivery to DTC. If the PACERS are no longer represented by global securities or are not held on behalf of DTC, call notices and other notices will be published in a leading daily newspaper in the City of New York, which is expected to beThe Wall Street Journal.

Payment at Maturity

If we call the PACERS during the Call Determination Period beginning on June 2, 2009, at maturity you will receive for each PACERS you hold a Call Price in cash equal to $12.40, the sum of $10 and the applicable Mandatory Call Premium.

If we do not call the PACERS, they will mature on June 9, 2009. At maturity, you will receive for each PACERS an amount described below.

PS-14

Table of Contents

Determination of the Amount to be Received at Maturity

If not previously called, at maturity you will receive for each $10 principal amount of PACERS either:

| • | a number of CVRD Depositary Shares equal to the Share Ratio (or, if you elect, the cash value of those shares based on the Closing Price of CVRD Depositary Shares on the Valuation Date), if the Closing Price of CVRD Depositary Shares on any Trading Day after the Pricing Date up to and including the Valuation Date is less than or equal to $20.15 (approximately 65% of the Initial Share Price) (any fractional share will be paid in cash), which we refer to as the “Downside Trigger Price,” or |

| • | $10 in cash. |

As a result, if we do not call the PACERS and the Closing Price of CVRD Depositary Shares on any Trading Day after the Pricing Date up to and including the Valuation Date is less than or equal to the Downside Trigger Price, the value of CVRD Depositary Shares you receive at maturity (or, if you elect, the cash value of those shares) for each PACERS will always be less than the price paid for each PACERS, and could be zero.

You may elect to receive from Citigroup Funding the cash value of the shares you would otherwise receive at maturity by providing notice of your election to your broker, in accordance with your broker’s procedures, so that your broker can irrevocably notify the trustee and paying agent of your election no sooner than 20 business days before maturity and no later than 5 business days before maturity. If you do not elect to receive cash, you will be deemed to have (1) instructed Citigroup Funding to pay the cash value of the number of CVRD Depositary Shares equal to the Share Ratio to the stock delivery agent, and (2) instructed the stock delivery agent to purchase for you CVRD Depositary Shares based on its Closing Price on the Valuation Date. If you do not wish to receive CVRD Depositary Shares at maturity under any circumstances, you should provide notice of your cash election to your broker. You should provide this notice even if the Closing Price of CVRD Depositary Shares at any time prior to your election has not been less than or equal to $20.15 (approximately 65% of the Initial Share Price). If you elect to receive the cash value of CVRD Depositary Shares equal to the Share Ratio you would otherwise be entitled to at maturity, the amount of cash you receive at maturity will be determined based on the Closing Price of CVRD Depositary Shares on the Valuation Date and will be an amount less than $10 per PACERS. This amount will not change from the amount fixed on the Valuation Date, even if the Closing Price of CVRD Depositary Shares changes from the Valuation Date to maturity. Conversely, if you do not make a cash election and instead receive a number of CVRD Depositary Shares at maturity equal to the Share Ratio, the value of those shares at maturity will be different from the value of those shares on the Valuation Date if the Closing Price of CVRD Depositary Shares changes from the Valuation Date to maturity.

The payment of cash to the stock delivery agent by Citigroup Funding pursuant to your deemed instruction will fully satisfy Citigroup Funding’s obligation to you under the PACERS, and the stock delivery agent will then be obligated to purchase CVRD Depositary Shares for you based on the Closing Price on the Valuation Date. Citigroup Global Markets has agreed to act as stock delivery agent for the PACERS.

In lieu of any fractional share that you would otherwise receive in respect of any PACERS, at maturity you will receive an amount in cash equal to the value of such fractional share. The number of full CVRD Depositary Shares, and any cash in lieu of a fractional share, to be delivered at maturity, or any cash amount if elected, to each holder will be calculated based on the aggregate number of PACERS held by each holder.

The “Initial Share Price” equals $31.00, the Closing Price of CVRD Depositary Shares on the Pricing Date.

The “Pricing Date” means November 26 the date of this pricing supplement and the date on which the PACERS were priced for initial sale to the public.

The “Valuation Date” means the third Trading Day before maturity.

PS-15

Table of Contents

The “Share Ratio” equals 0.32258, $10 divided by the Initial Share Price.

A “Market Disruption Event” means, as determined by the calculation agent in its sole discretion, the occurrence or existence of any suspension of or limitation imposed on trading (by reason of movements in price exceeding limits permitted by any exchange or market or otherwise) of, or the unavailability, through a recognized system of public dissemination of transaction information, for a period longer than two hours, or during the one-half hour period preceding the close of trading, on the applicable exchange or market, of accurate price, volume or related information in respect of (1) CVRD Depositary Shares or the common shares of CVRD (or any other security for which a Closing Price must be determined) on any exchange or market, or (2) any options contracts or futures contracts relating to CVRD Depositary Shares or the common shares of CVRD (or other relevant security), or any options on such futures contracts, on any exchange or market if, in each case, in the determination of the calculation agent, any such suspension, limitation or unavailability is material.

A “Trading Day” means a day, as determined by the calculation agent, on which trading is generally conducted (or was scheduled to have been generally conducted, but for the occurrence of a Market Disruption Event) on the New York Stock Exchange, the American Stock Exchange, the Nasdaq National Market, the Chicago Mercantile Exchange and the Chicago Board Options Exchange, and in the over-the-counter market for equity securities in the United States, or in the case of a security traded on one or more non-U.S. securities exchanges or markets, on the principal non-U.S. securities exchange or market for such security.

The “Closing Price” of CVRD Depositary Shares (or any other security for which a Closing Price must be determined) on any date of determination will be (1) if the CVRD Depositary Shares or other security is listed on a national securities exchange on that date of determination, the closing sale price or, if no closing sale price is reported, the last reported sale price on that date on the principal national securities exchange on which the CVRD Depositary Shares or other security is listed or admitted to trading, and (2) if the CVRD Depositary Shares or other security is not listed on a national securities exchange on that date of determination, or if the closing sale price or last reported sale price on such exchange is not obtainable (even if the CVRD Depositary Shares or other security is listed or admitted to trading on such exchange), any last reported sale price of the principal trading session on the over-the-counter market on that date as reported on the OTC Bulletin Board, the National Quotation Bureau or a similar organization; provided that if the closing price of CVRD Depositary Shares cannot be determined by the methods described in (1) or (2) above, then the Closing Price will be the closing sale price or, if no closing sale price is reported, the last reported sale price on that date of the common shares of CVRD on the São Paulo Stock Exchange in Brazil, expressed in U.S. dollars as converted from the relevant currency using the 12:00 noon buying rate in New York certified by the New York Federal Reserve Bank for customs purposes on that date, or if this rate is unavailable, such rate as the calculation agent may determine; provided, however that the Closing Price will be determined as described in this paragraph with regard to the number of common shares of CVRD represented by each CVRD Depositary Share at the time the determination of the Closing Price is made, provided further that, if the Closing Price of any other security for which a Closing Price must be determined cannot be determined by the methods described in (1) or (2) above and if the security for which a closing price must be determined is traced on one or more non-U.S. securities exchanges or markets, then the Closing Price of such security will be the closing sale price or, if no closing sale price is reported, the last reported sale price on that date on the principal non-U.S. securities exchange or market on which the security is traded, expressed in U.S. dollars as converted from the relevant currency using the 12:00 noon buying rate in New York certified by the New York Federal Reserve Bank for customs purposes on that date, or if this rate is unavailable, such rate as the calculation agent may determine. The determination of the Closing Price by the calculation agent in the event of a Market Disruption Event may be deferred by the calculation agent for up to five consecutive Trading Days on which a Market Disruption Event is occurring, but not past the third Trading Day prior to maturity. If no sale price is available pursuant to clauses (1) or (2) above or if there is a Market Disruption Event, the Closing Price on any date of determination, unless deferred by the calculation agent as described in the preceding sentence, will be the arithmetic mean, as determined by the calculation agent, of the bid prices of the CVRD Depositary Shares or other security obtained from as many dealers in such CVRD Depositary Shares or other security (which may include Citigroup Global Markets or any

PS-16

Table of Contents

of our other affiliates or subsidiaries), but not exceeding three such dealers, as will make such bid prices available to the calculation agent. The term “OTC Bulletin Board” will include any successor to such service. If the CVRD American Depositary Shares program is terminated or the Closing Price is otherwise calculated by substituting the common shares of CVRD for the CVRD Depositary Shares, the Closing Price of the common shares of CVRD will be substituted for all purposes related to the PACERS including the determination of whether the PACERS are called and calculating the payment at maturity.

Amounts Payable at Call or Maturity — Hypothetical Examples

The examples of hypothetical Call Prices and amounts received at maturity set forth below are intended to illustrate the effect of different Closing Prices of CVRD Depositary Shares on the amount you will receive in respect of the PACERS upon a mandatory call or at maturity. All of the hypothetical examples are based on the following assumptions:

| • | Issue Price: $10.00 per PACERS |

| • | Pricing Date: November 16, 2007 |

| • | Settlement Date: November 21, 2007 |

| • | Valuation Date: May 18, 2009 |

| • | Maturity Date: May 21, 2009 |

| • | Initial Share Price: $36.88 |

| • | Underlying Share price at which a Mandatory Call occurs: $36.88 (100% of the hypothetical Initial Share Price) |

| • | Interest: 8% per annum, payable semi-annually ($.80 per PACERS total) |

| • | Mandatory Call Premium: |

| a. | 6.50%, if called on any Call Date in May 2008 |

| b. | 13.00%, if called on any Call Date in November 2008 |

| c. | 19.50%, if called on any Call Date in May 2009 |

| • | Share Ratio: 0.27115 CVRD Depositary Shares per PACERS |

| • | Annualized dividend yield of CVRD Depositary Shares: 1.05% |

| • | If the PACERS have not been previously called, at maturity, whether you receive CVRD Depositary Shares (or, if you elect, the equivalent cash value) or your initial investment ($10.00 per PACERS) depends on whether the Closing Price of CVRD Depositary Shares has declined by 35% or more (to $23.97 or less, the “Downside Trigger Price”) from the Initial Share Price on any Trading Day after the Pricing Date up to and including the Valuation Date. |

The following examples are for purposes of illustration only and would provide different results if different assumptions were applied. The actual amount you receive at maturity will depend on the Initial Share Price; whether the Closing Price of CVRD Depositary Shares on any Call Date is greater than or equal to the Initial Share Price, causing the PACERS to be called; and if the PACERS are not called, whether the Closing Price of CVRD Depositary Shares on any Trading Day up to and including the Valuation Date has declined by approximately 35% or more from the Initial Share Price causing you to receive a fixed number of CVRD Depositary Shares at maturity (or the cash value of those shares at your election).

Additionally, if you elect to receive the cash value of CVRD Depositary Shares equal to the Share Ratio you would otherwise be entitled to at maturity, the amount of cash you receive at maturity will be determined based

PS-17

Table of Contents

on the Closing Price of CVRD Depositary Shares on the Valuation Date. This amount will not change from the amount fixed on the Valuation Date, even if the Closing Price of CVRD Depositary Shares changes from the Valuation Date to maturity. Conversely, if you do not make a cash election and instead receive a number of CVRD Depositary Shares at maturity equal to the Share Ratio, the value of those shares at maturity will be different than the value of those shares on the Valuation Date if the Closing Price of CVRD Depositary Shares changes from the Valuation Date to maturity.

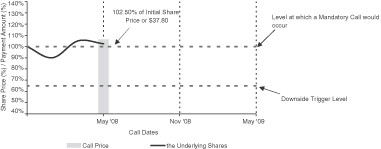

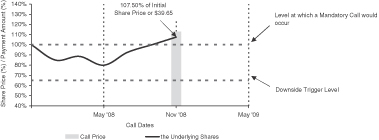

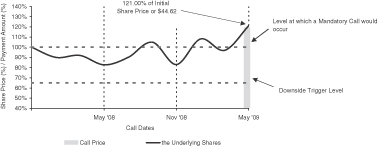

PACERS are Mandatorily Called on any of the Call Dates

The PACERS have not been previously called and the closing price of the Underlying Stock on the relevant Call Date is equal to or greater than $36.88, the price at which a Mandatory Call occurs. The PACERS are consequently called at the applicable Call Price of $10.00 plus the Mandatory Call Premium per PACERS.

a. If the Call Date occurs in May 2008, the Call Price will be $10.00 plus a Mandatory Call Premium of $0.650

Call Price = $10.00 + $0.650 = $10.65 per PACERS |  | |

b. If the Call Date occurs in November 2008, the Call Price will be $10.00 plus a Mandatory Call Premium of $1.300

Call Price = $10.00 + $1.300 = $11.30 per PACERS |  | |

c. If the Call Date occurs in May 2009, the Call Price will be $10.00 plus a Mandatory Call Premium of $1.950

Call Price = $10.00 + $1.950 = $11.95 per PACERS |  | |

PS-18

Table of Contents

d. Even if the Downside Trigger Price has been breached, the PACERS will be called on any Trading Day within any Call Determination Period if the Closing Price of CVRD Depositary Shares on such date is equal to or greater than $36.88, the price at which a Mandatory Call would occur. If the Call Date occurs in May 2009, the Call Price will be $10.00 plus a Mandatory Call Premium of $1.950

Call Price = $10.00 + $1.950 = $11.95 per PACERS |  |

PACERS are not Mandatorily Called on any of the Call Dates and Downside Trigger Price is Not Breached

The PACERS are not called on any of the Call Dates, and the Closing Price of CVRD Depositary Shares is not less than or equal to 65% of the Initial Share Price, or $23.97, at any day from the Pricing Date up to and including the Valuation Date.

Since the Closing Price of CVRD Depositary Shares on any Trading Day after the Pricing Date up to and including the Valuation Date is not less than or equal to $23.97, the amount received at maturity will be $10.00 per PACERS.

Amount received at maturity = $10.00 per PACERS |  |

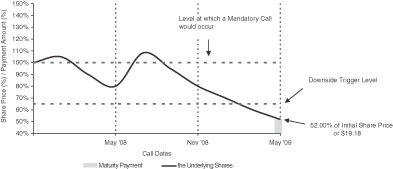

PACERS are not Mandatorily Called on any of the Call Dates and Downside Trigger Price is Breached

The PACERS are not called on any of the Call Dates, and the Closing Price of CVRD Depositary Shares is less than 65% of the Initial Share Price, or $23.97, on any Trading Day from the Pricing Date up to and including the Valuation Date. At maturity you will receive for each PACERS a number of CVRD Depositary Shares equal to the Share Ratio, or 0.27115 shares (or the cash value of those shares at your election).

Even if the Closing Price of CVRD Depositary Shares is greater than $36.88, or the price at which a Mandatory Call occurs, at one or more times on or prior to the Valuation Date, the Closing Price of CVRD Depositary Shares is below $36.88 on all of the Call Dates. Consequently, the PACERS will not be called on any Call Date.

PS-19

Table of Contents

If the Closing Price of CVRD Depositary Shares on any Trading Day from the Pricing Date up to and including the Valuation Date is equal to or less than $23.97, then you will receive at maturity a number of CVRD Depositary Shares equal to the Share Ratio (or the cash value of those Shares at your election). If the Closing Price of CVRD Depositary Shares on the Maturity Date is $19.18 then the market value of CVRD Depositary Shares you will receive, based on such Closing Price, will be $5.20.

Value of CVRD Depositary Shares received at maturity = 0.27115 shares * $19.18 = $5.20 |  |

Summary Chart of Hypothetical Examples

PACERS are Mandatorily Called

| Date on which the PACERS are called | Any Call Date in May 2008 | Any Call Date in November 2008 | Any Call Date in May 2009 (Downside Trigger Not Breached) | Any Call Date in May 2009 (Downside Trigger Breached) | ||||||||||||

Hypothetical Initial Depositary Share Price | $ | 36.88 | $ | 36.88 | $ | 36.88 | $ | 36.88 | ||||||||

Hypothetical lowest Closing Price on or prior to the Valuation Date | $ | 33.19 | $ | 29.50 | $ | 30.54 | $ | 23.23 | ||||||||

Is the hypothetical lowest Closing Price less than or equal to 65% of the Initial Share Price, or $23.97? | No | No | No | Yes | ||||||||||||

Hypothetical minimum price at which a Mandatory Call would occur | $ | 36.88 | $ | 36.88 | $ | 36.88 | $ | 36.88 | ||||||||

Hypothetical Closing Price of the Underlying Depositary Shares on the Call Date | $ | 37.80 | $ | 39.65 | $ | 44.62 | $ | 38.72 | ||||||||

Call Price for the PACERS | $ | 10.65 | $ | 11.30 | $ | 11.95 | $ | 11.95 | ||||||||

Return on CVRD Depositary Shares (excluding any cash dividend payments) | 2.50 | % | 7.50 | % | 21.00 | % | 5.00 | % | ||||||||

Return on the PACERS (excluding fixed coupon payments) | 6.50 | % | 13.00 | % | 19.50 | % | 19.50 | % | ||||||||

Return on CVRD Depositary Shares (including all cash dividend payments) | 3.02 | % | 8.55 | % | 22.58 | % | 6.58 | % | ||||||||

Return on PACERS (including fixed coupon payments) | 10.50 | % | 21.00 | % | 31.50 | % | 31.50 | % | ||||||||

PS-20

Table of Contents

PACERS are not Mandatorily Called

| Downside Trigger Not Breached | Downside Trigger Breached | |||||||

Hypothetical Initial Share Price | $ | 36.88 | $ | 36.88 | ||||

Hypothetical lowest Closing Price on or prior to the Valuation Date | $ | 25.82 | $ | 19.18 | ||||

Is the hypothetical lowest Closing Price less than or equal to 65% of the Initial Share Price, or $23.97? | No | Yes | ||||||

Will 0.27115 (the Hypothetical Share Ratio) CVRD Depositary Shares be delivered at maturity? | No | Yes | ||||||

Hypothetical Closing Price of CVRD Depositary Shares at maturity | $ | 29.50 | $ | 19.18 | ||||

Amount received at maturity (cash or value of CVRD Depositary Shares per PACERS) | $ | 10.00 | $ | 5.20 | ||||

Return on CVRD Depositary Shares (excluding any cash dividend payments) | -20.00 | % | -48.00 | % | ||||

Return on the PACERS (excluding fixed coupon payments) | 0.00 | % | -48.00 | % | ||||

Return on CVRD Depositary Shares (including all cash dividend payments) | -18.43 | % | -46.43 | % | ||||

Return on the PACERS (either in cash or the market value of CVRD Depositary Shares) | 12.00 | % | -36.00 | % | ||||

Dilution Adjustments

The Share Ratio will be subject to adjustment from time to time in certain situations. Any of these adjustments could have an impact on the amount to be paid by Citigroup Funding to you. Citigroup Global Markets, as calculation agent, will be responsible for the effectuation and calculation of any adjustment described herein and will furnish the trustee with notice of any adjustment. All references below to common stock refer to the common shares of CVRD represented by CVRD Depositary Shares.

If CVRD, after the Pricing Date,

(1) pays a share dividend or makes a distribution with respect to its common stock in such shares of common stock (excluding any share dividend or distribution for which the number of shares of common stock paid or distributed is based on a fixed cash equivalent value),

(2) subdivides or splits its outstanding common stock into a greater number of shares,

(3) combines its outstanding common stock into a smaller number of shares, or

(4) issues by reclassification of its common stock any shares of other common stock of CVRD,

then, in each of these cases, the Share Ratio will be multiplied by a dilution adjustment equal to a fraction, the numerator of which will be the number of shares of common stock outstanding immediately after the event, plus, in the case of a reclassification referred to in (4) above, the number of shares of other common stock of CVRD, and the denominator of which will be the number of shares of common stock outstanding immediately before the event. In the event of a reclassification referred to in (4) above as a result of which no common stock is outstanding, the Share Ratio will be determined by reference to the other shares of CVRD issued in the reclassification. The Initial Share Price and the Downside Trigger Price will also be adjusted in that case in the manner described below.

If CVRD, after the Pricing Date, issues, or declares a record date in respect of an issuance of, rights or warrants to all holders of its common stock entitling them to subscribe for or purchase shares of its common stock at a price per share less than the Then-Current Market Price of the common stock, other than rights to purchase common stock pursuant to a plan for the reinvestment of dividends or interest, then, in each case, the Share Ratio will be multiplied by a dilution adjustment equal to a fraction, the numerator of which will be the number of shares of common stock outstanding immediately before the adjustment is effected by reason of the

PS-21

Table of Contents

issuance of such rights or warrants, plus the number of additional shares of common stock offered for subscription or purchase pursuant to the rights or warrants, and the denominator of which will be the number of shares of common stock outstanding immediately before the adjustment is effected by reason of the issuance of the rights or warrants, plus the number of additional shares of common stock which the aggregate offering price of the total number of shares of common stock offered for subscription or purchase pursuant to the rights or warrants would purchase at the Then-Current Market Price of the common stock, which will be determined by multiplying the total number of shares so offered for subscription or purchase by the exercise price of the rights or warrants and dividing the product obtained by the Then-Current Market Price. To the extent that, after the expiration of the rights or warrants, the shares of common stock offered thereby have not been delivered, the Share Ratio will be further adjusted to equal the Share Ratio which would have been in effect had the adjustment for the issuance of the rights or warrants been made upon the basis of delivery of only the number of shares of common stock actually delivered. The Initial Share Price and the Downside Trigger Price will also be adjusted in that case in the manner described below.

If CVRD, after the Pricing Date, declares or pays a dividend or makes a distribution to all holders of the common stock of any class of its capital stock, the capital stock of one or more of its subsidiaries, evidences of its indebtedness or other non-cash assets, excluding any dividends or distributions referred to in the above paragraph, or issues to all holders of its common stock rights or warrants to subscribe for or purchase any of its or one or more of its subsidiaries’ securities, other than rights or warrants referred to in the above paragraph, then, in each of these cases, the Share Ratio will be multiplied by a dilution adjustment equal to a fraction, the numerator of which will be the Then-Current Market Price of one share of common stock, and the denominator of which will be the Then-Current Market Price of one share of common stock, less the fair market value as of the time the adjustment is effected of the portion of the capital shares, assets, evidences of indebtedness, rights or warrants so distributed or issued applicable to one share of the common stock. The Initial Share Price and the Downside Trigger Price will also be adjusted in that case in the manner described below. If any capital stock declared or paid as a dividend or otherwise distributed or issued to all holders of CVRD Depositary Shares consists, in whole or in part, of Marketable Securities, then the fair market value of such Marketable Securities will be determined by the calculation agent by reference to the Closing Price of such capital stock. The fair market value of any other distribution or issuance referred to in this paragraph will be determined by a nationally recognized independent investment banking firm retained for this purpose by Citigroup Funding, whose determination will be final.