Table of Contents

Filed pursuant to Rule 424(b)(2)

Registration Nos. 333-132370 and 333-132370-01

CALCULATION OF REGISTRATION FEE

Class of securities offered | Aggregate offering price | Amount of registration fee | |||||

Medium-Term Senior Notes, Series D | $ | 28,000,000.00 | $ | 859.60 | (1) | ||

| (1) | The filing fee of $859.60 is calculated in accordance with Rule 457(r) of the Securities Act of 1933. Pursuant to Rule 457(p) under the Securities Act of 1933, the $191,404.63 remaining of the filing fee previously paid with respect to unsold securities that were registered pursuant to a Registration Statement on Form S-3 (No. 333-119615) filed by Citigroup Global Market Holdings Inc., a wholly owned subsidiary of Citigroup Inc., on October 8, 2004 is being carried forward, of which $859.60 is offset against the registration fee due for this offering and of which $190,545.03 remains available for future registration fees. No additional registration fee has been paid with respect to this offering. |

Table of Contents

Pricing Supplement No. 2007—MTNDD173, Dated November 26, 2007 (To Prospectus Supplement Dated April 13, 2006 and Prospectus Dated March 10, 2006)

US$28,000,000 principal amount

Citigroup Funding Inc.

Medium-Term Notes, Series D

Any Payments Due from Citigroup Funding Inc.

Fully and Unconditionally Guaranteed by Citigroup Inc.

| Notes Based Upon the Gold Price Due November 26, 2008 |

| • | We will not make any payments on the notes prior to maturity. |

| • | The notes will mature on November 26, 2008. You will receive at maturity, for each US$1,000 principal amount of notes you hold, an amount in cash equal to US$970 plus a supplemental return amount, which may be positive or zero and is subject to a cap. The amount you receive at maturity could be less than US$1,000 per note but will be at least US$970 per note. |

| • | The supplemental return amount will be based on the percentage change of the price of unallocated gold bullion, which we refer to as gold, determined by reference to the London PM Fix (as more fully described in this pricing supplement), from the date of this pricing supplement, which we refer to as the pricing date, to the second business day before maturity. |

| • | If the price of gold on the second business day before maturity (which price we refer to as the ending price) is greater than its price on the pricing date (which price we refer to as the starting price), the supplemental return amount will be positive and for each note held at maturity will equal the product of (a) US$1,000 and (b) the percentage increase in the price of gold, provided that the maximum return on your investment in the notes will be limited to 14% per annum. As a result,in no circumstance will the amount you receive at maturity, including principal, be more than US$1,140 per note. |

| • | If the ending price of gold is greater than its starting price and the percentage increase in the price of gold is between 0% and 3%, the amount you receive at maturity will be between US$970 and US$1,000 per note. |

| • | If the ending price of gold is less than or equal to its starting price, the supplemental return amount will be zero. As a result, the amount you receive at maturity will be US$970 per note. |

| • | The notes will be issued in minimum denominations and increments of US$1,000. |

| • | We will not apply to list the notes on any exchange. |

Investing in the notes involves a number of risks. See “Risk Factors Relating to the Notes” beginning on page PS-7.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the notes or determined that this prospectus, prospectus supplement and pricing supplement is truthful or complete. Any representation to the contrary is a criminal offense.

The notes are not deposits or savings accounts but are unsecured debt obligations of Citigroup Funding Inc. The notes are not insured by the Federal Deposit Insurance Corporation or any other governmental agency or instrumentality.

| Per Note | Total | |||||

Public Offering Price | US$ | 1,000.00 | US$ | 28,000,000 | ||

Agent’s Discount | US$ | 0.00 | US$ | 0.00 | ||

Proceeds to Citigroup Funding Inc. | US$ | 1,000.00 | US$ | 28,000,000 | ||

We expect that delivery of the notes will be made against payment therefor on or about November 29, 2007.

| Investment Products | Not FDIC Insured | May Lose Value | No Bank Guarantee |

Table of Contents

This summary includes questions and answers that highlight selected information from the accompanying prospectus and prospectus supplement and this pricing supplement to help you understand the Notes Based Upon the Gold Price Due November 26, 2008. You should carefully read the entire prospectus, prospectus supplement and pricing supplement to understand fully the terms of the notes, as well as the principal tax and other considerations that are important to you in making a decision about whether to invest in the notes. You should, in particular, carefully review the section entitled “Risk Factors Relating to the Notes,” which highlights a number of risks, to determine whether an investment in the notes is appropriate for you. All of the information set forth below is qualified in its entirety by the more detailed explanation set forth elsewhere in this pricing supplement and the accompanying prospectus supplement and prospectus.

What Are the Notes?

The notes are commodity-linked securities issued by Citigroup Funding Inc. that have a maturity of exactly one year. The notes pay an amount at maturity that will depend on the percentage change in the price of gold from the pricing date, to the second business day before maturity, which we refer to as the valuation date. If the percentage change of the price of gold on the valuation date is less than or equal to zero, the payment you receive at maturity will equal 97% of your initial investment in the notes. If the percentage change of the price of gold on the valuation date is greater than zero, the payment you receive at maturity will equal 97% of your initial investment in the notes plus a supplemental return amount, which will be capped as described below. Because the amount you receive at maturity is determined by adding the supplemental return amount to 97%, not 100%, of the principal amount of the notes, the supplemental return amount, if any, will be offset by an amount equal to 3% of the principal amount of the notes, or US$30 per note. Thus,in no circumstance will the return on your investment in the notes be more than 14% per annum, or US$1,140 per note.

The notes mature on November 26, 2008 and do not provide for earlier redemption by you or by us. The notes are a series of unsecured senior debt securities issued by Citigroup Funding. Any payments due on the notes are fully and unconditionally guaranteed by Citigroup Inc., Citigroup Funding’s parent company. The notes will rank equally with all other unsecured and unsubordinated debt of Citigroup Funding, and, as a result of the guarantee, any payments due under the notes will rank equally with all other unsecured and unsubordinated debt of Citigroup Inc.

You may transfer the notes only in minimum denominations and integral multiples of US$1,000. You will not have the right to receive physical certificates evidencing your ownership except under limited circumstances. Instead, we will issue the notes in the form of a global certificate, which will be held by the Depository Trust Company or its nominee. Direct and indirect participants in DTC will record beneficial ownership of the notes by individual investors. Accountholders in the Euroclear or Clearstream clearance systems may hold beneficial interests in the notes through the accounts that each of these systems maintains as a participant in DTC. You should refer to “Description of the Notes—Book-Entry System” in the accompanying prospectus supplement and the section “Description of Debt Securities—Book-Entry Procedures and Settlement” in the accompanying prospectus for further information.

Will I Receive Interest on the Notes?

No. We will not make any periodic payments of interest on the notes or any other payments on the notes until maturity.

What Will I Receive at Maturity of the Notes?

The notes will mature on November 26, 2008. You will receive at maturity, for each US$1,000 principal amount of notes you hold, an amount in cash equal to US$970 plus a supplemental return amount, which may be

PS-2

Table of Contents

positive or zero. Because the supplemental return amount is capped, the maximum amount, including principal, you could receive at maturity is US$1,140 per note.

How Will the Supplemental Return Amount Be Calculated?

The supplemental return amount will be based on the gold price return during the term of notes, provided that the supplemental return amount on the notes will be limited to 17% of the principal amount of the notes.

The gold price return will equal the following fraction, expressed as a percentage:

Ending Price – Starting Price

Starting Price

The starting price equals US$830.00, which was the price of a troy ounce of gold, stated in U.S. dollars, as set by the five members of the London Gold Market Fixing Ltd. during the afternoon session of the twice daily gold price fix which starts at 3:00 p.m. London, England time (the “London PM Fix”) on the pricing date, as reported by Reuters Page “GOFO” or any successor page.

The ending price will equal the London PM Fix of a troy ounce of gold on the valuation date, as reported on Reuters Page “GOFO” or any successor page.

If the gold price return is positive, the supplemental return amount per note will equal the product of (a) US$1,000 and (b) the gold price return, provided that the supplemental return amount on the notes will be limited to 17% of the principal amount of the notes. If the gold price return is between 0% and 3%, the amount you receive at maturity will be between US$970 and US$1,000 per note.

If the gold price return is zero or negative, the supplemental return amount per note will be zero.

If the London PM Fix of gold price on the valuation date is not reported on Reuters Page “GOFO” or any successor page but is otherwise published by the London Gold Market Fixing Ltd., the price of gold on that date will be determined by reference to the London PM Fix of gold price published by the London Gold Market Fixing Ltd. If no London PM Fix of gold price is available on the valuation date because of a market disruption event or otherwise, the price of gold on that date, unless deferred by the calculation agent as described below, will be the arithmetic mean, as determined by the calculation agent, of the spot price of a troy ounce of gold at 3:00 p.m. London, England time on the relevant date obtained from as many dealers in gold (which may include Citigroup Global Markets Inc. or any of our other affiliates), but not exceeding three such dealers, as will make such price available to the calculation agent. The determination of the price of gold by the calculation agent in the event of a market disruption event may be deferred by the calculation agent for up to five consecutive business days on which a market disruption event is occurring, but not past the business day prior to maturity.

For more specific information about the “supplemental return amount,” the “gold price return” and the determination of a “business day” and a “market disruption event,” please see “Description of the Notes—Supplemental Return Amount” in this pricing supplement.

Where Can I Find Examples of Hypothetical Maturity Payments?

For examples of hypothetical maturity payments, see “Description of the Notes—Hypothetical Maturity Payment Examples” in this pricing supplement.

PS-3

Table of Contents

What Will I Receive if I Sell the Notes Prior to Maturity?

If you choose to sell your notes before maturity, you are not guaranteed to receive 97% of the principal amount of the notes you sell. You should refer to the sections “Risk Factors Relating to the Notes —No Principal Protection Unless You Hold the Notes to Maturity,” “—The Price at Which You Will Be Able to Sell Your Notes Prior to Maturity Will Depend on a Number of Factors and May Be Substantially Less Than the Amount You Originally Invest” and “—You May Not Be Able to Sell Your Notes if an Active Trading Market for the Notes Does Not Develop” in this pricing supplement for further information. You will receive at least 97% of the principal amount of your notes only if you hold the notes at maturity.

Who Publishes the London PM Fix of Gold Price and What Does it Measure?

Unless otherwise stated, all information on the London PM Fix of gold price provided in this pricing supplement is derived from the London Gold Market Fixing Ltd. or other publicly available sources. The London PM Fix of gold price is set by the five members of the London Gold Market Fixing Ltd. during the afternoon session of the twice daily gold price fix which starts at 3:00 p.m. London, England time. During each session, orders are placed either with one of the five fixing members or with another bullion dealer who will then be in contact with a fixing member during the fixing. The fixing members net-off all orders when communicating their individual net interest at the fixing. The fix begins with the fixing chairman suggesting a “trying price,” reflecting the market price prevailing at the opening of the fix. This is relayed by the fixing members to their dealing rooms, which have direct communication with all interested parties. Any market participant may enter the fixing process at any time, or adjust or withdraw its order. The gold price is adjusted up or down until all the buy and sell orders are matched, at which time the price is declared fixed. All fixing orders are transacted on the basis of this fixed price, which is instantly relayed to the market through various media. As of November 26, 2007, the five members of the London Gold Market Fixing Ltd. were The Bank of Nova Scotia – ScotiaMocatta, HSBC, Deutsche Bank AG London, Société Générale Corporate & Investment Banking and Barclays Bank.

Please note that an investment in the notes does not entitle you to any ownership or other interest in gold.

How Has the Price of Gold Performed Historically?

We have provided a table showing the high and low prices of gold for each quarterly period since January 2002 and a graph showing the daily prices of gold from January 2, 1997 through November 26, 2007. You can find the table and the graph in the section “Description of the Gold Price—Historical Data on the Gold Price” in this pricing supplement. We have provided this historical information to help you evaluate the behavior of the price of gold in recent years. However, past performance is not indicative of how the price of gold will perform in the future. You should also refer to the section “Risk Factors Relating to the Notes—The Historical Performance of the Gold Price Is Not an Indication of the Future Performance of the Gold Price” in this pricing supplement.

Can You Tell Me More About the Effect of Citigroup Funding’s Hedging Activity?

We expect to hedge our obligations under the notes through one or more of our affiliates. This hedging activity will likely involve trading in gold or in other instruments, such as options, swaps or futures, based on the price of gold. The costs of maintaining or adjusting this hedging activity could affect the price at which our affiliate Citigroup Global Markets may be willing to purchase your notes in the secondary market. Moreover, this hedging activity may result in us or our affiliates receiving a profit, even if the market value of the notes declines. You should refer to “Risk Factors Relating to the Notes—The Price at Which You Will Be Able to Sell Your Notes Prior to Maturity Will Depend on a Number of Factors and May Be Substantially Less Than the Amount You Originally Invest” in this pricing supplement, “Risk Factors—Citigroup Funding’s Hedging Activity Could Result in a Conflict of Interest” in the accompanying prospectus supplement and “Use of Proceeds and Hedging” in the accompanying prospectus.

PS-4

Table of Contents

Does ERISA Impose Any Limitations on Purchases of the Notes?

Employee benefit plans and other entities the assets of which are subject to the fiduciary responsibility provisions of the Employee Retirement Income Security Act of 1974, as amended, Section 4975 of the Internal Revenue Code of 1986, as amended, or substantially similar federal, state or local laws, including individual retirement accounts, (which we call “Plans”) will be permitted to purchase and hold the notes, provided that each such Plan shall by its purchase be deemed to represent and warrant either that (A)(i) none of Citigroup Global Markets Inc., its affiliates or any employee thereof is a Plan fiduciary that has or exercises any discretionary authority or control with respect to the Plan’s assets used to purchase the notes or renders investment advice with respect to those assets and (ii) the Plan is paying no more than adequate consideration for the notes or (B) its acquisition and holding of the notes is not prohibited by any such provisions or laws or is exempt from any such prohibition. However, individual retirement accounts, individual retirement annuities and Keogh plans, as well as employee benefit plans that permit participants to direct the investment of their accounts, willnot be permitted to purchase or hold the notes if the account, plan or annuity is for the benefit of an employee of Citigroup Global Markets Inc. or a family member and the employee receives any compensation (such as, for example, an addition to bonus) based on the purchase of notes by the account, plan or annuity. Please refer to the section “ERISA Matters” in this pricing supplement for further information.

What Are the U.S. Federal Income Tax Consequences of Investing in the Notes?

Citigroup Funding will treat each note for U.S. federal income tax purposes as a single debt instrument with contingent payments and a maturity of one year, issued by Citigroup Funding. The notes are subject to the timing rules applicable to debt obligations with a maturity of one year or less. There are, however, no rules specifically addressing the U.S. federal income tax treatment of notes with terms identical to those of the notes. Under the rules described above, a U.S. holder generally will be required to recognize income with respect to the notes in accordance with the holder’s method of tax accounting. A cash method U.S. holder generally will not be required to recognize income with respect to the notes until the maturity of the notes. Although there are no specific rules that provide for treatment of accrual method U.S. holders, accrual method U.S. holders generally should not be required to recognize income with respect to the notes prior to the date on which the amount of the contingent payment made with respect to the notes becomes fixed. In addition, any gain recognized by a U.S. holder at maturity of the notes generally will be treated as ordinary income. Any loss on the notes at maturity, or upon sale or other taxable disposition prior to maturity, will be treated as short-term capital loss. You should refer to “Certain United States Federal Income Tax Considerations” in this pricing supplement for more information.

Will the Notes Be Listed on a Stock Exchange?

No. The notes will not be listed on any exchange.

Can You Tell Me More About Citigroup Inc. and Citigroup Funding?

Citigroup Inc. is a diversified global financial services holding company whose businesses provide a broad range of financial services to consumer and corporate customers. Citigroup Funding is a wholly-owned subsidiary of Citigroup Inc. whose business activities consist primarily of providing funds to Citigroup Inc. and its subsidiaries for general corporate purposes.

What Is the Role of Citigroup Funding’s and Citigroup Inc.’s Affiliates, Citigroup Global Markets Inc. and Citibank, N.A.?

Our affiliate, Citigroup Global Markets Inc. is the agent for the offering and sale of the notes. After the initial offering, Citigroup Global Markets Inc. and/or other of our affiliated dealers currently intend, but are not obligated, to buy and sell the notes to create a secondary market for holders of the notes, and may engage in other activities described in the section “Plan of Distribution” in this pricing supplement, the accompanying prospectus supplement and prospectus. However, neither Citigroup Global Markets Inc. nor any of these affiliates will be obligated to engage in any market-making activities, or continue those activities once it has started them.

PS-5

Table of Contents

Our affiliate, Citibank, N.A., will act as calculation agent for the notes. Potential conflicts of interest may exist between Citibank, N.A. as calculation agent and you as a holder of the notes.

Are There Any Risks Associated With My Investment?

Yes. The notes are subject to a number of risks. Please refer to the section “Risk Factors Relating to the Notes” in this pricing supplement.

PS-6

Table of Contents

RISK FACTORS RELATING TO THE NOTES

An investment in the notes entails significant risks not associated with similar investments in a conventional debt security, including, among other things, fluctuations in the price of gold and other events that are difficult to predict and beyond our control.

You May Lose a Portion of Your Investment if the Price of Gold Declines or Appreciates by Less than 3%

The amount of the maturity payment will depend on the gold price return, which is the percentage change of the price of gold from the pricing date to the valuation date. You will receive at maturity at least the principal amount of the notes you then holdonly if the gold price return is equal to or greater than 3%. If the gold price return is less than 3%, the amount you receive at maturity will be less than the principal amount of your notes and could be as low as US$970 for each note you hold, in which case your investment in the notes will result in a loss. This will be true even if the price of gold exceeds the starting price by more than 3% at one or more times during the term of the notes, but the ending price on the valuation date is less than 103% of the starting price.

The Supplemental Return Amount will be Offset

The amount you receive at maturity will be determined by adding the supplemental return amount, if any, to 97%, not 100%, of the principal amount of the notes. Thus, the supplemental return amount, if any, will be offset by an amount equal to 3% of the principal amount of the notes, or US$30 per note.

Any Appreciation of Your Investment in the Notes Will Be Limited

Because the supplemental return amount on the notes will be capped at 17% of the principal amount of the notes, the maximum amount, including principal, you could receive at maturity is US$1,140 per note. Thus, the notes may provide less opportunity for appreciation than an investment in an instrument directly linked to the price of gold and not subject to a cap.

No Principal Protection Unless You Hold the Notes to Maturity

You will be entitled to receive at least 97% of the principal amount of your notes only if you hold the notes to maturity. The market value of the notes may fluctuate and, because the notes are not fully principal-protected prior to maturity, you may receive less than your initial investment if you sell your notes in the secondary market prior to maturity.

The Yield on the Notes May Be Lower Than the Yield on a Standard Debt Security of Comparable Maturity

The notes do not pay any interest. As a result, if the ending price is less than US$893.74 (an increase of 7.68% from the starting price), the effective yield on your notes will be less than that which would be payable on a conventional fixed-rate, non-callable debt security of Citigroup Funding of comparable maturity.

You Will Not Receive Any Periodic Payments on the Notes

You will not receive any periodic payments of interest or any other periodic payments on the notes.

Gold Prices Are Highly Volatile and Affected by Many Complex Factors

Prices of gold are highly volatile and are affected by numerous factors. These include economic factors, including, among other things, the structure of and confidence in the global monetary system, expectations of the future rate of inflation, the relative strength of, and confidence in, the U.S. dollar (the currency in which the price

PS-7

Table of Contents

of gold is generally quoted), interest rates and gold borrowing and lending rates, and global or regional economic, financial, political, regulatory, judicial or other events. Gold prices may also be affected by industry factors such as industrial and jewelry demand, lending, sales and purchases of gold by the official sector, including central banks and other governmental agencies and multilateral institutions which hold gold, levels of gold production and production costs, and short-term changes in supply and demand because of trading activities in the gold market. It is not possible to predict the aggregate effect of all or any combination of these factors on the price of gold. If these factors result in a decrease in gold prices, it may reduce the amount of the maturity payment and/or the value of the notes in the secondary market.

The Price at Which You Will Be Able to Sell Your Notes Prior to Maturity Will Depend on a Number of Factors and May Be Substantially Less Than the Amount You Originally Invest

We believe that the value of your notes in the secondary market will be affected by the supply of and demand for the notes, the price of gold and a number of other factors. Some of these factors are interrelated in complex ways. As a result, the effect of any one factor may be offset or magnified by the effect of another factor. The following paragraphs describe what we expect to be the impact on the market value of the notes of a change in a specific factor, assuming all other conditions remain constant.

Price of Gold. We expect that the market value of the notes will depend substantially on the changes, if any, in the price of gold from the starting price. However, changes in the gold price may not always be reflected, in full or in part, in the market value of the notes. If you choose to sell your notes when the gold price exceeds its starting price, you may receive substantially less than the amount that would be payable at maturity based on that price because of expectations that the gold price will continue to fluctuate from that time to the time when the ending price of gold is determined. If you choose to sell your notes when the gold price is less than its ending price on the valuation date, you are likely to receive less than the amount you originally invested.

The gold price will be influenced by both the complex and interrelated political, economic, financial and other factors that can affect the markets on which gold is traded. These factors are described in more detail in “—Gold Prices Are Highly Volatile and Affected by Many Complex Factors” above.

Volatility of the Gold Price. Volatility is the term used to describe the size and frequency of market fluctuations. If the expected volatility of the gold price changes during the term of the notes, the market value of the notes may decrease.

Interest Rates. We expect that the market value of the notes will be affected by changes in U.S. interest rates. In general, if U.S. interest rates increase, the market value of the notes may decrease, and if U.S. interest rates decrease, the market value of the notes may increase.

Time Premium or Discount. As a result of a “time premium or discount,” the notes may trade at a value above or below that which would be expected based on the level of interest rates and the gold price the longer the time remaining to maturity. A “time premium or discount” results from expectations concerning the gold price during the period prior to the maturity of the notes. However, as the time remaining to maturity decreases, this time premium or discount may diminish, increasing or decreasing the market value of the notes.

Hedging Activities. Hedging activities related to the notes by one or more of our affiliates will likely involve trading in gold or in other instruments, such as options, swaps or futures, based upon the price of gold. This hedging activity could affect the price of gold and therefore the market value of the notes. It is possible that we or our affiliates may profit from our hedging activity, even if the market value of the notes declines. Profits or loss from this hedging activity could affect the price at which our affiliate Citigroup Global Markets Inc. may be willing to purchase your notes in the secondary market.

PS-8

Table of Contents

Credit Ratings, Financial Condition and Results. Actual or anticipated changes in Citigroup Funding’s financial condition or results or the credit ratings, financial condition or results of Citigroup Inc. may affect the market value of the notes. The notes are subject to the credit risk of Citigroup Inc., the guarantor of any payments due on the notes.

We want you to understand that the impact of one of the factors specified above may offset some or all of any change in the market value of the notes attributable to another factor.

The Historical Performance of the Gold Price Is Not an Indication of the Future Performance of the Gold Price

The historical performance of the gold price, which is included in this pricing supplement, should not be taken as an indication of the future performance of the gold price during the term of the notes. Changes in the gold price will affect the trading price of the notes, but it is impossible to predict whether the gold price will fall or rise.

You Will Not Have Any Rights with Respect to Gold

You will not own or have any beneficial or other legal interest in, and will not be entitled to any rights with respect to, gold. The notes are debt securities issued by Citigroup Funding, not an interest in gold or a futures contract or commodities option based on the price of gold.

You May Not Be Able to Sell Your Notes if an Active Trading Market for the Notes Does Not Develop

The notes have not been and will not be listed on any exchange. There is currently no secondary market for the notes. Citigroup Global Markets and/or other of Citigroup Funding’s affiliated dealers currently intend, but are not obligated, to make a market in the notes. Even if a secondary market does develop, it may not be liquid and may not continue for the term of the notes. If the secondary market for the notes is limited, there may be few buyers should you choose to sell your notes prior to maturity and this may reduce the price you receive.

Citibank, N.A. Is the Calculation Agent, Which Could Result in a Conflict of Interest

Citibank, N.A., which is acting as the calculation agent for the notes, is an affiliate of ours. As a result, Citibank, N.A.’s duties as calculation agent, including with respect to certain determinations and judgments that the calculation agent must make in determining amounts due to you, may conflict with its interest as an affiliate of ours.

PS-9

Table of Contents

The description in this pricing supplement of the particular terms of the notes supplements, and to the extent inconsistent therewith replaces, the descriptions of the general terms and provisions of the debt securities set forth in the accompanying prospectus and prospectus supplement.

General

The Notes Based Upon the Gold Price Due November 26, 2008 (the “Notes”) are commodity-linked securities issued by Citigroup Funding Inc. that have a maturity of exactly one year. The Notes pay an amount at maturity that will depend on the percentage change in the price of gold over the term of the Notes.

If the percentage change of the price of gold from the Pricing Date to the Valuation Date is less than or equal to zero, the payment you receive at maturity will equal 97% of your initial investment in the Notes. If the percentage change of the price of gold from the Pricing Date to the Valuation Date is greater than zero, the payment you receive at maturity will equal 97% of your initial investment in the Notes plus a Supplemental Return Amount, which will be capped as described below. However, because the amount you receive at maturity is determined by adding the Supplemental Return Amount to 97%, not 100%, of the principal amount of the Notes, the Supplemental Return Amount, if any, will be offset by an amount equal to 3% of the principal amount of the Notes, or US$30 per Note. Thus,in no circumstance will the return on your investment in the Notes be more than 14% per annum, or US$1,140 per Note.

The Notes are a series of debt securities issued by Citigroup Funding under the senior debt indenture described in the accompanying prospectus supplement, and prospectus and any payments due under the Notes are fully and unconditionally guaranteed by Citigroup Inc. The aggregate principal amount of Notes issued will be US$28,000,000 (28,000 Notes). The Notes will mature on November 26, 2008, will constitute part of the senior debt of Citigroup Funding, and will rank equally with all other unsecured and unsubordinated debt of Citigroup Funding. As a result of the Citigroup Inc. guarantee, any payments due under the Notes will rank equally with all other unsecured and unsubordinated debt of Citigroup Inc. The Notes will be issued only in fully registered form and in denominations of US$1,000 per Note and integral multiples thereof.

Reference is made to the accompanying prospectus supplement and prospectus for a detailed summary of additional provisions of the Notes and of the senior debt indenture under which the Notes will be issued.

Interest

We will not make any periodic payments of interest on the Notes or any other payments on the Notes until maturity.

Payment at Maturity

The Notes will mature on November 26, 2008. You will receive at maturity, for each US$1,000 principal amount of Notes you hold, an amount in cash equal to US$970 plus a Supplemental Return Amount, which may be positive or zero. Because the Supplemental Return Amount is capped, the maximum amount, including principal, you could receive at maturity is US$1,140 per Note.

Supplemental Return Amount

The Supplemental Return Amount will be based on the Gold Price Return during the term of the Notes and will be calculated as follows:

If the Gold Price Return is positive, the Supplemental Return Amount per Note will equal the product of (a) US$1,000 and (b) the Gold Price Return, provided that the maximum Supplemental Return Amount on the

PS-10

Table of Contents

Notes is limited to 17% of the principal amount of the Notes. If the Gold Price Return is between 0% and 3%, the amount you receive at maturity will be between US$970 and US$1,000 per Note.

If the Gold Price Return is zero or negative, the Supplemental Return Amount per Note will be zero.

The Gold Price Return will equal the following fraction, expressed as a percentage:

Ending Price – Starting Price

Starting Price

The Starting Price equals US$830.00, which was the price of a troy ounce of gold, stated in U.S. dollars, as set by the five members of the London Gold Market Fixing Ltd. during the afternoon session of the twice daily gold price fix which starts at 3:00 p.m. London, England time (the “London PM Fix”) on the Pricing Date, as reported on Reuters Page “GOFO” or any successor page.

The Ending Price will equal the London PM Fix of a troy ounce of gold on the Valuation Date, as reported on Reuters Page “GOFO” or any successor page.

The Pricing Date means November 26, 2007, which is the date of this pricing supplement and the date on which the Notes were priced for initial sale to the public.

The Valuation Date will be the second Business Day before maturity.

If the London PM Fix of gold price on the Valuation Date is not reported on Reuters Page “GOFO” or any successor page but is otherwise published by the London Gold Market Fixing Ltd., the price of gold on that date will be determined by reference to the London PM Fix of gold price published by the London Gold Market Fixing Ltd. If no London PM Fix of gold price is available on the Valuation Date because of a Market Disruption Event or otherwise, the price of gold on that date, unless deferred by the calculation agent as described below, will be the arithmetic mean, as determined by the calculation agent, of the spot price of a troy ounce of gold at 3:00 p.m. London, England time on the relevant date obtained from as many dealers in gold (which may include Citigroup Global Markets Inc. or any of our other affiliates), but not exceeding three such dealers, as will make such price available to the calculation agent. The determination of the price of gold by the calculation agent in the event of a Market Disruption Event may be deferred by the calculation agent for up to five consecutive Business Days on which a Market Disruption Event is occurring, but not past the Business Day prior to maturity.

A Business Day means any day that is not a Saturday, a Sunday or a day on which the securities exchanges or banking institutions or trust companies in the City of New York or in London, England are authorized or obligated by law or executive order to close.

A Market Disruption Event means, as determined by the calculation agent in its sole discretion, the occurrence or existence of any suspension of or limitation imposed on trading (by reason of movements in price exceeding limits permitted by any relevant exchange or market or otherwise) of, or the unavailability through a recognized system of public dissemination of transaction information, for a period longer than two hours, or during the one-half hour period preceding the close of trading, on the applicable exchange or market, of accurate price, volume or related information in respect of (a) gold or (b) any options or futures contracts, or any options on such futures contracts relating to gold on any exchange or market if, in each case, in the determination of the calculation agent, any such suspension, limitation or unavailability is material.

Hypothetical Maturity Payment Examples

The examples below show the hypothetical maturity payments to be made on an investment of US$1,000 principal amount of Notes based on various Ending Prices of gold. The following examples of hypothetical maturity payment calculations are based on the following assumptions:

| • | Principal amount: US$1,000 per Note |

PS-11

Table of Contents

| • | Starting Price: US$750 |

| • | Principal Protection at Maturity: 97% (US$970 per Note) |

| • | Maximum Gold Price Return: 18% of the principal amount per Note |

| • | Maturity: Exactly 1 year |

| • | The Notes are purchased on the issue date and are held through the maturity date. |

The following examples are for purposes of illustration only and would provide different results if different assumptions were applied. The actual maturity payment will depend on the actual Supplemental Return Amount, which, in turn, will depend on the actual Starting Price, Ending Price and maximum Gold Price Return.

Hypothetical | Hypothetical Gold Price Return (without cap)(1) | Hypothetical (with cap)(2) | Hypothetical Supplemental Return Amount per Note(3) | Hypothetical Maturity Payment per Note(4) | Hypothetical Return on the Notes | |||||

US$375.00 | -50.000% | -50.000% | US$0.00 | US$970.00 | -3.000% | |||||

$400.00 | -46.667% | -46.667% | $0.00 | $970.00 | -3.000% | |||||

$425.00 | -43.333% | -43.333% | $0.00 | $970.00 | -3.000% | |||||

$450.00 | -40.000% | -40.000% | $0.00 | $970.00 | -3.000% | |||||

$475.00 | -36.667% | -36.667% | $0.00 | $970.00 | -3.000% | |||||

$500.00 | -33.333% | -33.333% | $0.00 | $970.00 | -3.000% | |||||

$525.00 | -30.000% | -30.000% | $0.00 | $970.00 | -3.000% | |||||

$550.00 | -26.667% | -26.667% | $0.00 | $970.00 | -3.000% | |||||

$575.00 | -23.333% | -23.333% | $0.00 | $970.00 | -3.000% | |||||

$600.00 | -20.000% | -20.000% | $0.00 | $970.00 | -3.000% | |||||

$625.00 | -16.667% | -16.667% | $0.00 | $970.00 | -3.000% | |||||

$650.00 | -13.333% | -13.333% | $0.00 | $970.00 | -3.000% | |||||

$675.00 | -10.000% | -10.000% | $0.00 | $970.00 | -3.000% | |||||

$700.00 | -6.667% | -6.667% | $0.00 | $970.00 | -3.000% | |||||

$725.00 | -3.333% | -3.333% | $0.00 | $970.00 | -3.000% | |||||

$750.00 | 0.000% | 0.000% | $0.00 | $970.00 | -3.000% | |||||

$775.00 | 3.333% | 3.333% | $33.33 | $1,003.33 | 0.333% | |||||

$800.00 | 6.667% | 6.667% | $66.67 | $1,036.67 | 3.667% | |||||

$825.00 | 10.000% | 10.000% | $100.00 | $1,070.00 | 7.000% | |||||

$850.00 | 13.333% | 13.333% | $133.33 | $1,103.33 | 10.333% | |||||

$875.00 | 16.667% | 16.667% | $166.67 | $1,136.67 | 13.667% | |||||

$900.00 | 20.000% | 18.000% | $180.00 | $1,150.00 | 15.000% | |||||

$925.00 | 23.333% | 18.000% | $180.00 | $1,150.00 | 15.000% | |||||

$950.00 | 26.667% | 18.000% | $180.00 | $1,150.00 | 15.000% | |||||

$975.00 | 30.000% | 18.000% | $180.00 | $1,150.00 | 15.000% | |||||

$1,000.00 | 33.333% | 18.000% | $180.00 | $1,150.00 | 15.000% | |||||

$1,025.00 | 36.667% | 18.000% | $180.00 | $1,150.00 | 15.000% | |||||

$1,050.00 | 40.000% | 18.000% | $180.00 | $1,150.00 | 15.000% | |||||

$1,075.00 | 43.333% | 18.000% | $180.00 | $1,150.00 | 15.000% | |||||

$1,100.00 | 46.667% | 18.000% | $180.00 | $1,150.00 | 15.000% | |||||

$1,125.00 | 50.000% | 18.000% | $180.00 | $1,150.00 | 15.000% |

| (1) | Hypothetical Gold Price Return = (Hypothetical Ending Gold Price – Hypothetical Starting Gold Price) / Hypothetical Starting Gold Price |

| (2) | Capped Hypothetical Gold Price Return = (Hypothetical Ending Gold Price – Hypothetical Starting Gold Price) / Hypothetical Starting Gold Price, provided that the Hypothetical Gold Price Return will not be greater than 18% per annum |

PS-12

Table of Contents

| (3) | If the Hypothetical Gold Price Return is greater than 0%, the Hypothetical Supplemental Return Amount = US$1,000 x Hypothetical Gold Price Return |

| If the Hypothetical Gold Price Return is less than or equal to 0%, the Hypothetical Supplemental Return Amount = US$0 |

(4) | Hypothetical Maturity Payment per Note = US$970 + Hypothetical Supplemental Return Amount |

Redemption at the Option of the Holder; Defeasance

The Notes are not subject to redemption at the option of any holder prior to maturity and are not subject to the defeasance provisions described in the accompanying prospectus under “Description of Debt Securities—Defeasance.”

Default Interest Rate

In case of default in payment at maturity of the Notes, the Notes shall bear interest, payable upon demand of the beneficial owners of the Notes in accordance with the terms of the Notes, from and after the maturity date through the date when payment of the unpaid amount has been made or duly provided for, at the rate of 5% per annum on the unpaid amount due. If default interest is required to be calculated for a period of less than one year, it will be calculated on the basis of the actual number of days elapsed and a 360-day year consisting of twelve 30-day months.

Paying Agent and Trustee

Citibank, N.A. will serve as paying agent and registrar for the Notes and will also hold the global security representing the Notes as custodian for DTC. The Bank of New York, as successor trustee under an indenture dated as of June 1, 2005, will serve as trustee for the Notes.

Calculation Agent

The calculation agent for the Notes will be Citibank, N.A. All determinations made by the calculation agent will be at the sole discretion of the calculation agent and will, in the absence of manifest error, be conclusive for all purposes and binding on Citigroup Funding, Citigroup Inc. and the holders of the Notes. Because the calculation agent is an affiliate of Citigroup Funding and Citigroup Inc., potential conflicts of interest may exist between the calculation agent and the holders of the Notes, including with respect to certain determinations and judgments that the calculation agent must make in determining amounts due to holders of the Notes. Citibank, N.A. is obligated to carry out its duties and functions as calculation agent in good faith and using its reasonable judgment.

PS-13

Table of Contents

General

The Supplemental Return Amount, if any, will be determined by reference to the price of a troy ounce of gold generally known as the London PM Fix. We have derived all information regarding the London PM Fix of gold price from publicly available sources without independent verification. Such information reflects the policies of, and is subject to change without notice by, the London Gold Market Fixing Ltd. We make no representation or warranty as to the accuracy or completeness of such information.

The London PM Fix of gold price is set by the five members of the London Gold Market Fixing Ltd. during the afternoon session of the twice daily gold price fix which starts at 3:00 p.m. London, England time. During each session, orders are placed either with one of the five fixing members or with another bullion dealer who will then be in contact with a fixing member during the fixing. The fixing members net-off all orders when communicating their individual net interest at the fixing. The fix begins with the fixing chairman suggesting a “trying price,” reflecting the market price prevailing at the opening of the fix. This is relayed by the fixing members to their dealing rooms, which have direct communication with all interested parties. Any market participant may enter the fixing process at any time, or adjust or withdraw its order. The gold price is adjusted up or down until all the buy and sell orders are matched, at which time the price is declared fixed. All fixing orders are transacted on the basis of this fixed price, which is instantly relayed to the market through various media. As of November 26, 2007, the five members of the London Gold Market Fixing Ltd. were The Bank of Nova Scotia— ScotiaMocatta, HSBC, Deutsche Bank AG London, Société Générale Corporate & Investment Banking and Barclays Bank.

Disclaimer

The Notes are not sponsored, endorsed, sold or promoted by the London Gold Market Fixing Ltd. or by any member thereof. The London Gold Market Fixing Ltd. makes no representation or warranty, express or implied, to the purchasers of the Notes or any member of the public regarding the advisability of investing in securities generally or in the Notes particularly or the ability of the London gold price fixings to track general market performance of gold price. The London Gold Market Fixing Ltd. has no relationship to Citigroup Funding and London gold price fixings are determined without regard to any of Citigroup Funding or the Notes. The London Gold Market Fixing Ltd. has no obligation to take the needs of Citigroup Funding or the owners of the Notes into consideration in determining London gold price fixings. The London Gold Market Fixing Ltd. is not responsible for and has not participated in the determination of the timing of, prices at, or quantities of the Notes to be issued or in the determination or calculation of the equation by which the Notes are to be converted into cash. The London Gold Market Fixing Ltd. has no obligation or liability in connection with the administration, marketing or trading of the Notes.

PS-14

Table of Contents

Historical Data on the Gold Price

The following table sets forth, for each of the quarterly periods indicated, the high and low London PM Fix of a troy ounce of gold, as reported by Bloomberg. These historical data on the price of gold are not indicative of the future performance of the price of gold or what the value of the Notes may be. Any historical upward or downward trend in the price of gold during any period set forth below is not an indication that the price of gold is more or less likely to increase or decrease at any time during the term of the Notes.

| High | Low | |||||

2002 | ||||||

Quarter | ||||||

First | US$ | 304.30 | US$ | 277.75 | ||

Second | 327.05 | 297.75 | ||||

Third | 326.30 | 302.25 | ||||

Fourth | 349.30 | 310.75 | ||||

2003 | ||||||

Quarter | ||||||

First | 382.10 | 329.45 | ||||

Second | 371.40 | 319.90 | ||||

Third | 390.70 | 342.50 | ||||

Fourth | 416.25 | 370.25 | ||||

2004 | ||||||

Quarter | ||||||

First | 425.50 | 390.50 | ||||

Second | 427.25 | 375.00 | ||||

Third | 415.65 | 387.30 | ||||

Fourth | 454.20 | 411.25 | ||||

2005 | ||||||

Quarter | ||||||

First | 443.70 | 411.10 | ||||

Second | 440.55 | 414.45 | ||||

Third | 473.25 | 418.35 | ||||

Fourth | 536.50 | 456.50 | ||||

2006 | ||||||

Quarter | ||||||

First | 584.00 | 524.75 | ||||

Second | 725.00 | 567.00 | ||||

Third | 663.25 | 573.60 | ||||

Fourth | 648.75 | 560.75 | ||||

2007 | ||||||

Quarter | ||||||

First | 685.75 | 608.40 | ||||

Second | 691.40 | 642.10 | ||||

Third | 743.00 | 648.75 | ||||

Fourth (through November 26) | 841.10 | 725.50 | ||||

The London PM Fix of a troy ounce of gold on November 26, 2007, as reported on Reuters Page “GOFO,” was US$830.00.

PS-15

Table of Contents

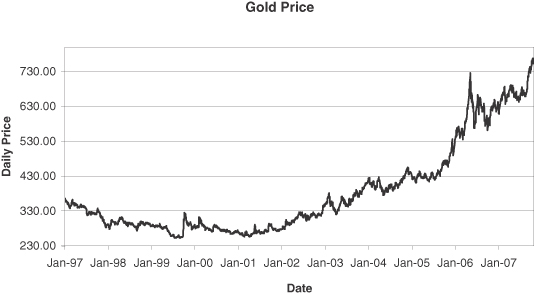

The following graph illustrates the historical performance of the prices of a troy ounce of gold based on London PM Fix thereof, as reported by Bloomberg, from January 2, 1997 through November 26, 2007. Past movements of gold price are not indicative of future prices of gold. Any historical upward or downward trend in the price of gold during any period set forth below is not an indication that the price of gold is more or less likely to increase or decrease at any time during the term of the Notes.

PS-16

Table of Contents

CERTAIN UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS

The following is a summary of certain U.S. federal income tax considerations that may be relevant to a beneficial owner of a Note that is a citizen or resident of the United States or a domestic corporation or otherwise subject to U.S. federal income tax on a net income basis in respect of a Note (a “U.S. Holder”). All references to “holders” (including U.S. Holders) are to beneficial owners of the Notes. This summary is based on U.S. federal income tax laws, regulations, rulings and decisions in effect as of the date of this pricing supplement, all of which are subject to change at any time (possibly with retroactive effect).

This summary addresses the U.S. federal income tax consequences to U.S. Holders who are initial holders of the Notes and who will hold the Notes as capital assets. This summary does not address all aspects of U.S. federal income taxation that may be relevant to a particular holder in light of its individual investment circumstances or to certain types of holders subject to special treatment under the U.S. federal income tax laws, such as dealers in securities or foreign currency, financial institutions, insurance companies, tax-exempt organizations or taxpayers holding the Notes as part of a “straddle,” “hedge,” “conversion transaction,” “synthetic security” or other integrated investment, or persons whose functional currency is not the U.S. dollar. Moreover, the effect of any applicable state, local or foreign tax laws is not discussed.

Investors should consult their own tax advisors in determining the tax consequences to them of holding the Notes, including the application to their particular situation of the U.S. federal income tax considerations discussed below.

Tax Characterization of the Notes

Citigroup Funding will treat each Note for U.S. federal income tax purposes as a single debt instrument with a contingent payment determined by reference to the percentage change in the gold price and a maturity of one year, issued by Citigroup Funding. Each holder, by accepting a Note, agrees to this characterization of the Note. The remainder of this summary assumes such characterization of each Note and the holder’s agreement thereto.

United States Holders

The Notes are subject to special rules applicable to debt obligations with a maturity of one year or less. Under these rules, a U.S. Holder using the cash method of accounting generally will include amounts in income with respect to the Supplemental Return Amount at the time that such payment is received. U.S. Holders using an accrual method of accounting generally are required to accrue original issue discount with respect to a Note. The rules applicable to short-term debt obligations do not, however, address how to accrue income with respect to a future contingent payment such as the Supplemental Return Amount that will be paid at maturity. Moreover, while there are special U.S. federal income tax rules applicable to debt instruments with one or more contingent payments that require U.S. Holders to accrue interest income using a specified methodology, those rules do not apply to short-term taxable debt obligations. Taxpayers using an accrual method of accounting generally are not required to include amounts in income until all the events have occurred that fix the right to receive the income and the amount of the income can be determined with reasonable accuracy. Accordingly, although no assurance can be given that the Internal Revenue Service (the “IRS”) will accept, or that a court will uphold, the following tax treatment, under the rules described above a U.S. Holder using the accrual method of accounting should not be required to include amounts in income in respect of the Supplemental Return Amount prior to the date on which the amount of such payment becomes fixed. Under this treatment, a U.S. Holder will recognize ordinary income in respect to the Supplemental Return Amount to the extent that the amount payable to the Holder at maturity exceeds $1,000, or capital loss to the extent that the maturity payment is less than the Holder’s basis in the Notes. A U.S. Holder’s tax basis in the Notes generally will equal the cost of the Notes to such holder.

Upon a sale or exchange of the Notes prior to maturity, a U.S. Holder generally will recognize gain or loss equal to the difference between the amount realized and the Holder’s tax basis in the Notes. The rules applicable

PS-17

Table of Contents

to short-term debt obligations do not address the proper characterization of any gain realized upon disposition of obligations such as the Notes prior to maturity. Generally, gain on disposition of a short-term note issued by a corporation is treated as ordinary income to the extent of accrued original issue discount not previously taken into account, and otherwise as short-term capital gain. Accordingly, under the rules generally applicable, and assuming that a U.S. Holder is not required to accrue any amounts in respect of the Supplemental Return Amount prior to the time when that Amount is paid or fixed, a gain on the disposition of the Notes prior to maturity would be treated as short-term capital gain. A U.S. Holder should note, however, that the IRS may seek to characterize any gain on disposition as ordinary income, particularly if the Holder disposes of the Note close to maturity. Any loss on the Notes will be treated as short-term capital loss.

Information Reporting and Backup Withholding. Information returns may be required to be filed with the IRS relating to payments made to a particular U.S. Holder of Notes. In addition, U.S. Holders may be subject to backup withholding tax on such payments if they do not provide their taxpayer identification numbers in the manner required, fail to certify that they are not subject to backup withholding tax, or otherwise fail to comply with applicable backup withholding tax rules. U.S. Holders may also be subject to information reporting and backup withholding tax with respect to the proceeds from a sale, exchange, retirement or other taxable disposition of the Notes.

Non-United States Holders

The following is a summary of certain U.S. federal income tax consequences that will apply to Non-U.S. Holders of the Notes. The term “Non-U.S. Holder” means a beneficial owner of a Note that is a foreign corporation or nonresident alien.

Non-U.S. Holders should consult their own tax advisors to determine the U.S. federal, state and local and any foreign tax consequences that may be relevant to them.

Payment with Respect to the Notes. All payments on the Notes made to a Non-U.S. Holder, and any gain realized on a sale, exchange or redemption of the Notes, will be exempt from U.S. income and withholding tax, provided that:

(i) such Non-U.S. Holder does not own, actually or constructively, 10 percent or more of the total combined voting power of all classes of the Citigroup Funding’s stock entitled to vote, and is not a controlled foreign corporation related, directly or indirectly, to Citigroup Funding through stock ownership;

(ii) the beneficial owner of a Note certifies on IRS Form W-8BEN (or successor form), under penalties of perjury, that it is not a U.S. person and provides its name and address or otherwise satisfies applicable documentation requirements; and

(iii) such payments and gains are not effectively connected with the conduct by such Non-U.S. Holder to a trade or business in the United States.

If a Non-U.S. Holder of the Notes is engaged in a trade or business in the United States, and if interest on the Notes is effectively connected with the conduct of such trade or business, the Non-U.S. Holder, although exempt from the withholding tax discussed in the preceding paragraphs, generally will be subject to regular U.S. federal income tax on interest and on any gain realized on the sale, exchange or redemption of the Notes in the same manner as if it were a U.S. Holder. In lieu of the certificate described in clause (ii) of the second preceding paragraph, such a Non-U.S. Holder will be required to provide to the withholding agent a properly executed IRS Form W-8ECI (or successor form) in order to claim an exemption from withholding tax.

Information Reporting and Backup Withholding. In general, a Non-U.S. Holder will not be subject to backup withholding and information reporting with respect to payments made with respect to the Notes if such Non-U.S. Holder has provided Citigroup Funding with an IRS Form W-8BEN described above and Citigroup

PS-18

Table of Contents

Funding does not have actual knowledge or reason to know that such Non-U.S. Holder is a U.S. person. In addition, no backup withholding will be required regarding the proceeds of the sale of the Notes made within the United States or conducted through certain U.S. financial intermediaries if the payor receives the statement described above and does not have actual knowledge or reason to know that the Non-U.S. Holder is a U.S. person or the Non-U.S. Holder otherwise establishes an exemption.

U.S. Federal Estate Tax.A Note beneficially owned by an individual who at the time of death is a Non-U.S. Holder should not be subject to U.S. federal estate tax.

PS-19

Table of Contents

The terms and conditions set forth in the Global Selling Agency Agreement dated April 20, 2006 among Citigroup Funding, Citigroup Inc. and the agents named therein, including Citigroup Global Markets Inc., govern the sale and purchase of the Notes.

Citigroup Global Markets, as principal, has agreed to purchase from Citigroup Funding, and Citigroup Funding has agreed to sell to Citigroup Global Markets, US$28,000,000 principal amount of Notes (28,000 Notes), any payments due on which are fully and unconditionally guaranteed by Citigroup Inc. Citigroup Global Markets proposes to offer some of the Notes directly to the public at market prices prevailing at the time of sale or at prices otherwise negotiated and some of the Notes to certain dealers, including Citicorp Financial Services Corp., Citigroup Global Markets Singapore Pte. Ltd. and Citigroup Global Markets Asia Limited, broker-dealers affiliated with Citigroup Global Markets, at the public offering price less a concession of $6.00 per Note. Citigroup Global Markets may allow, and these dealers may reallow, a concession of $6.00 per Note on sales to certain other dealers. In addition, Financial Advisors employed by Smith Barney, the broker-dealer division of Citigroup Global Markets, will receive a fixed sales commission of $6.00 per Note for each Note they sell. If all of the Notes are not sold at the initial offering price, Citigroup Global Markets may change the public offering price and other selling terms.

The Notes will not be listed on any exchange.

In order to hedge its obligations under the Notes, Citigroup Funding expects to enter into one or more swaps or other derivatives transactions with one or more of its affiliates. You should refer to the section “Risk Factor Relating to the Notes—The Price at Which You Will Be Able to Sell Your Notes Prior to Maturity Will Depend on a Number of Factors and May Be Substantially Less Than the Amount You Originally Invest” in this pricing supplement, “Risk Factors—Citigroup Funding’s Hedging Activity Could Result in a Conflict of Interest” in the accompanying prospectus supplement and the section “Use of Proceeds and Hedging” in the accompanying prospectus.

Citigroup Global Markets is an affiliate of Citigroup Funding. Accordingly, the offering will conform to the requirements set forth in Rule 2720 of the Conduct Rules of the National Association of Securities Dealers. Client accounts over which Citigroup Inc. or its affiliates have investment discretion are not permitted to purchase the Notes, either directly or indirectly.

To the extent the offer of any Notes is made in any Member State of the European Economic Area that has implemented the European Council Directive 2003/71/EC (such Directive, together with any applicable implementing measures in the relevant home Member State under such Directive, the “Prospectus Directive”) before the date of publication of a valid prospectus in relation to the Notes which has been approved by the competent authority in that Member State in accordance with the Prospectus Directive (or, where appropriate, published in accordance with the Prospectus Directive and notified to the competent authority in that Member State in accordance with the Prospectus Directive), the offer (including any offer pursuant to this document) is only addressed to qualified investors in that Member State within the meaning of the Prospectus Directive or has been or will be made otherwise in circumstances that do not require the Citigroup Funding to publish a prospectus pursuant to the Prospectus Directive.

This document is only being distributed to and is only directed at (i) persons who are outside the United Kingdom or (ii) to investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) or (iii) high net worth entities, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order (all such persons together being referred to as “relevant persons”). The Notes will only be available to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire such Notes will be engaged in only with, relevant persons. Any person who is not a relevant person should not act or rely on this document or any of its contents.

PS-20

Table of Contents

The Notes are being offered globally for sale in the United States, Europe, Asia and elsewhere where it is lawful to make such offers.

Purchasers of the Notes may be required to pay stamp taxes and other charges in accordance with the laws and practices of the country of purchase in addition to the issue price set forth on the cover page of this document.

The agent or dealer has agreed that it will not offer, sell or deliver any of the Notes, directly or indirectly, or distribute this pricing supplement or the accompanying prospectus supplement or prospectus or any other offering material relating to the Notes, in or from any jurisdiction, except when to the best knowledge and belief of the agent or dealer it is permitted under applicable laws and regulations. In so doing, the agent or dealer will not impose any additional obligations on Citigroup Funding.

The agent or dealer has represented and agreed that:

| • | in relation to each Member State of the European Economic Area which has implemented the Prospectus Directive (each, a “Relevant Member State”), with effect from and including the date on which the Prospectus Directive is implemented in that Relevant Member State (“Relevant Implementation Date”) it has not made and will not make an offer of Notes to the public in that Relevant Member State prior to the publication of a prospectus in relation to the Notes which has been approved by the competent authority in that Relevant Member State or, where appropriate, approved in another Relevant Member State and notified to the competent authority in that Relevant Member State, all in accordance with the Prospectus Directive, except that it may, with effect from and including the Relevant Implementation Date, make an offer of Notes to the public in that Relevant Member State at any time: |

| (a) | to legal entities which are authorized or regulated to operate in the financial markets or, if not so authorized or regulated, whose corporate purpose is solely to invest in securities; |

| (b) | to any legal entity which has two or more of (1) an average of at least 250 employees during the last financial year; (2) a total balance sheet of more than €43,000,000 and (3) an annual net turnover of more than €50,000,000, as shown in its last annual or consolidated accounts; or |

| (c) | in any other circumstances which do not require the publication by the issuer of a prospectus pursuant to Article 3 of the Prospectus Directive. |

| For the purposes of this provision, the expression an “offer of Notes to the public” in relation to any Notes in any Relevant Member State means the communication in any form and by any means of sufficient information on the terms of the offer and the Notes to be offered so as to enable an investor to decide to purchase or subscribe the Notes, as the same may be varied in that Member State by any measure implementing the Prospectus Directive in that Member State; |

| • | it has only communicated or caused to be communicated and will only communicate or cause to be communicated an invitation or inducement to engage in investment activity (within the meaning of Section 21 of the Financial Services and Markets Act 2000 (the “FSMA”)) received by it in connection with the issue or sale of the Notes in circumstances in which Section 21(1) of the FSMA does not apply to Citigroup Funding or Citigroup Inc.; |

| • | it has complied and will comply with all applicable provisions of the FSMA with respect to anything done by it in relation to the Notes in, from or otherwise involving the United Kingdom; |

| • | it will not offer or sell any Notes directly or indirectly in Japan or to, or for the benefit of, any Japanese person or to others, for re-offering or re-sale directly or indirectly in Japan or to any Japanese person except under circumstances which will result in compliance with all applicable laws, regulations and guidelines promulgated by the relevant governmental and regulatory authorities in effect at the relevant time. For purposes of this paragraph, “Japanese person” means any person resident in Japan, including any corporation or other entity organized under the laws of Japan; |

PS-21

Table of Contents

| • | it is aware of the fact that no securities prospectus (Wertpapierprospekt) under the German Securities Prospectus Act (Wertpapierprospektgesetz, the “Prospectus Act”) has been or will be published in respect of the Notes in the Federal Republic of Germany and that it will comply with the Prospectus Act and all other laws and regulations applicable in the Federal Republic of Germany governing the issue, offering and sale of the Notes; and |

| • | no Notes have been offered or sold and will be offered or sold, directly or indirectly, to the public in France except to qualified investors (investisseurs qualifiés) and/or to a limited circle of investors (cercle restreint d’investisseurs) acting for their own account as defined in article L. 411-2 of the French Code Monétaire et Financier and applicable regulations thereunder; and that the direct or indirect resale to the public in France of any Notes acquired by any qualified investors (investisseurs qualifiés) and/or any investors belonging to a limited circle of investors (cercle restreint d’investisseurs) may be made only as provided by articles L. 412-1 and L. 621-8 of the French Code of Monétaire et Financier and applicable regulations thereunder; and that none of the pricing supplement, the prospectus supplement, the prospectus or any other offering materials relating to the Notes has been released, issued or distributed to the public in France except to qualified investors (investisseurs qualifiés) and/or to a limited circle of investors (cercle restreint d’investisseurs) mentioned above. |

This document has not been registered as a prospectus with the Monetary Authority of Singapore under the Securities and Futures Act, Chapter 289 of the Singapore Statutes (the “Securities and Futures Act” or the “Act”). Accordingly, neither this document nor any other document or material in connection with the offer or sale, or invitation for subscription or purchase, of the Notes may be circulated or distributed, nor may the Notes be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to the public or any member of the public in Singapore other than in circumstances where the registration of a prospectus is not required and thus only (1) to an institutional investor or other person falling within section 274 of the Securities and Futures Act, (2) to a “relevant person” (as defined in section 275 of the Securities and Futures Act) or to any person pursuant to section 275(1A) of the Securities and Futures Act and in accordance with the conditions specified in section 275 of the Securities and Futures Act, or (3) pursuant to, and in accordance with the conditions of, any other applicable provision of the Securities and Futures Act. No person receiving a copy of this document may treat the same as constituting any invitation to him/her, unless in the relevant territory such an invitation could be lawfully made to him/her without compliance with any registration or other legal requirements or where such registration or other legal requirements have been satisfied. Each of the following relevant persons specified in Section 275 of the Securities and Futures Act who has subscribed for or purchased Notes, namely a person who is:

| (a) | a corporation (which is not an accredited investor) the sole business of which is to hold investments and the entire share capital of which is owned by one or more individuals, each of whom is an accredited investor, or |

| (b) | a trust (where the trustee is not an accredited investor) whose sole purpose is to hold investments and of which each beneficiary is an individual who is an accredited investor, |

should note that securities of that corporation or the beneficiaries’ rights and interest in that trust may not be transferred for 6 months after that corporation or that trust has acquired the Notes under Section 275 of the Securities and Futures Act pursuant to an offer made in reliance on an exemption under Section 275 of the Securities and Futures Act unless:

| (i) | the transfer is made only to institutional investors, or relevant persons as defined in Section 275(2) of the Act, or arises from an offer referred to in Section 275(1A) of the Act (in the case of a corporation) or in accordance with Section 276(4)(i)(B) of the Act (in the case of a trust) |

| (ii) | no consideration is or will be given for the transfer; or |

| (iii) | the transfer is by operation of law. |

PS-22

Table of Contents

WARNING TO INVESTORS IN HONG KONG ONLY: The contents of this document have not been reviewed by any regulatory authority in Hong Kong. Investors are advised to exercise caution in relation to the offer. If investors are in any doubt about any of the contents of this document, they should obtain independent professional advice.

This offer of Notes is not being made in Hong Kong, by means of any document, other than (1) to persons whose ordinary business it is to buy or sell shares or debentures (whether as principal or agent); (2) to “professional investors” within the meaning of the Securities and Futures Ordinance (Cap. 571) of Hong Kong (the “SFO”) and any rules made under the SFO; or (3) in other circumstances which do not result in the document being a “prospectus” as defined in the Companies Ordinance (Cap. 32) of Hong Kong (the “CO”) or which do not constitute an offer to the public within the meaning of the CO.

There is no advertisement, invitation or document relating to the Notes, which is directed at, or the contents of which are likely to be accessed or read by, the public in Hong Kong (except if permitted to do so under the laws of Hong Kong) other than with respect to Notes which are or are intended to be disposed of only to persons outside Hong Kong or only to the persons or in the circumstances described in the preceding paragraph.

Each purchaser of the Notes or any interest therein will be deemed to have represented and warranted on each day from and including the date of its purchase or other acquisition of the Notes through and including the date of disposition of such Notes that either:

| (a) | it is not (i) an employee benefit plan subject to the fiduciary responsibility provisions of ERISA, (ii) an entity with respect to which part or all of its assets constitute assets of any such employee benefit plan by reason of C.F.R. 2510.3-101 or otherwise, (iii) a plan described in Section 4975(e)(1) of the Internal Revenue Code of 1986, as amended (the “Code”) (for example, individual retirement accounts, individual retirement annuities or Keogh plans), or (iv) a government or other plan subject to federal, state or local law substantially similar to the fiduciary responsibility provisions of ERISA or Section 4975 of the Code (such law, provisions and Section, collectively, a “Prohibited Transaction Provision” and (i), (ii), (iii) and (iv), collectively, “Plans”); or |

| (b) | if it is a Plan, either (A)(i) none of Citigroup Global Markets Inc., its affiliates or any employee thereof is a Plan fiduciary that has or exercises any discretionary authority or control with respect to the Plan’s assets used to purchase the Notes or renders investment advice with respect to those assets, and (ii) the Plan is paying no more than adequate consideration for the Notes or (B) its acquisition and holding of the Notes is not prohibited by a Prohibited Transaction Provision or is exempt therefrom. |

The above representations and warranties are in lieu of the representations and warranties described in the section “ERISA Matters” in the accompanying prospectus supplement. Please also refer to the section “ERISA Matters” in the accompanying prospectus.

PS-23

Table of Contents

You should rely only on the information contained or incorporated by reference in this pricing supplement and the accompanying prospectus supplement and prospectus. We are not making an offer of these securities in any state where the offer is not permitted. You should not assume that the information contained or incorporated by reference in this pricing supplement, prospectus supplement or prospectus is accurate as of any date other than the date on the front of such document.

| Page | ||

| Pricing Supplement | ||

| PS-2 | ||

| PS-7 | ||

| PS-10 | ||

| PS-14 | ||

| PS-17 | ||

| PS-20 | ||

| PS-23 | ||

| Prospectus Supplement | ||

Risk Factors | S-3 | |

Important Currency Information | S-6 | |

Description of the Notes | S-7 | |

Certain United States Federal Income Tax Considerations | S-33 | |

Plan of Distribution | S-40 | |

ERISA Matters | S-41 | |

| Prospectus | ||

Prospectus Summary | 1 | |

Forward-Looking Statements | 6 | |

Citigroup Inc. | 6 | |

Citigroup Funding Inc. | 6 | |

Use of Proceeds and Hedging | 7 | |

European Monetary Union | 8 | |

Description of Debt Securities | 8 | |

Description of Index Warrants | 21 | |

Description of Debt Security and Index Warrant Units | 24 | |

Limitations on Issuances in Bearer Form | 25 | |

Plan of Distribution | 26 | |

ERISA Matters | 29 | |

Legal Matters | 29 | |

Experts | 29 | |

Citigroup Funding Inc.

Medium-Term Notes, Series D

US$28,000,000 principal amount

Notes Based Upon the Gold Price

Due November 26, 2008

(US$1,000 Principal Amount per Note)

Any Payments Due from Citigroup Funding Inc.

Fully and Unconditionally Guaranteed

by Citigroup Inc.

Pricing Supplement

November 26, 2007

(Including Prospectus Supplement dated

April 13, 2006 and Prospectus dated

March 10, 2006)