CITIGROUP’S 2007 ANNUAL REPORT ON FORM 10-K

1

THE COMPANY

Citigroup Inc. (Citigroup and, together with its subsidiaries, the Company) is a global diversified financial services holding company whose businesses provide a broad range of financial services to consumer and corporate customers. Citigroup has more than 200 million customer accounts and does business in more than 100 countries. Citigroup was incorporated in 1988 under the laws of the State of Delaware.

The Company is a bank holding company within the meaning of the U.S. Bank Holding Company Act of 1956 registered with, and subject to examination by, the Board of Governors of the Federal Reserve System (FRB). Some of the Company’s subsidiaries are subject to supervision and examination by their respective federal and state authorities. At December 31, 2007, the Company had approximately 147,000 full-time and 13,000 part-time employees in the United States and approximately 227,000 full-time employees outside the United States. The Company has completed

certain strategic business acquisitions and divestitures during the past three years, details of which can be found in Notes 2 and 3 to the Consolidated Financial Statements on pages 122 and 125, respectively.

The principal executive offices of the Company are located at 399 Park Avenue, New York, New York 10043, telephone number 212 559 1000. Additional information about Citigroup is available on the Company’s Web site atwww.citigroup.com. Citigroup’s annual report on Form 10-K, its quarterly reports on Form 10-Q, its current reports on Form 8-K, and all amendments to these reports are available free of charge through the Company’s Web site by clicking on the “Investor Relations” page and selecting “All SEC Filings.” The Securities and Exchange Commission (SEC) Web site contains reports, proxy and information statements, and other information regarding the Company atwww.sec.gov.

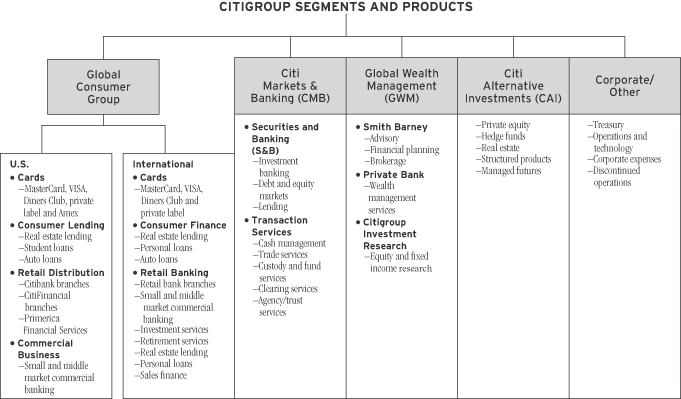

Citigroup is managed along the following segment and product lines:

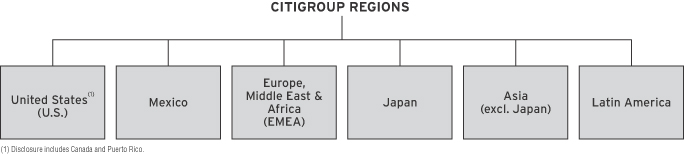

The following are the six regions in which Citigroup operates. The regional results are fully reflected in the product results.

2

| | |

| FIVE-YEAR SUMMARY OF SELECTED FINANCIAL DATA | | Citigroup Inc. and Subsidiaries |

| | | | | | | | | | | | | | | | | | | | |

| In millions of dollars, except per share amounts | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

Revenues, net of interest expense | | $ | 81,698 | | | $ | 89,615 | | | $ | 83,642 | | | $ | 79,635 | | | $ | 71,594 | |

Operating expenses | | | 61,488 | | | | 52,021 | | | | 45,163 | | | | 49,782 | | | | 37,500 | |

Provisions for credit losses and for benefits and claims | | | 18,509 | | | | 7,955 | | | | 9,046 | | | | 7,117 | | | | 8,924 | |

Income from continuing operations before taxes, minority

interest, and cumulative effect of accounting change | | $ | 1,701 | | | $ | 29,639 | | | $ | 29,433 | | | $ | 22,736 | | | $ | 25,170 | |

Provision (benefits) for income taxes | | | (2,201 | ) | | | 8,101 | | | | 9,078 | | | | 6,464 | | | | 7,838 | |

Minority interest, net of taxes | | | 285 | | | | 289 | | | | 549 | | | | 218 | | | | 274 | |

Income from continuing operations before cumulative effect of

accounting change | | $ | 3,617 | | | $ | 21,249 | | | $ | 19,806 | | | $ | 16,054 | | | $ | 17,058 | |

Income from discontinued operations, net of taxes(1) | | | — | | | | 289 | | | | 4,832 | | | | 992 | | | | 795 | |

Cumulative effect of accounting change, net of taxes(2) | | | — | | | | — | | | | (49 | ) | | | — | | | | — | |

Net income | | $ | 3,617 | | | $ | 21,538 | | | $ | 24,589 | | | $ | 17,046 | | | $ | 17,853 | |

Earnings per share | | | | | | | | | | | | | | | | | | | | |

Basic: | | | | | | | | | | | | | | | | | | | | |

Income from continuing operations | | $ | 0.73 | | | $ | 4.33 | | | $ | 3.90 | | | $ | 3.13 | | | $ | 3.34 | |

Net income | | | 0.73 | | | | 4.39 | | | | 4.84 | | | | 3.32 | | | | 3.49 | |

Diluted: | | | | | | | | | | | | | | | | | | | | |

Income from continuing operations | | | 0.72 | | | | 4.25 | | | | 3.82 | | | | 3.07 | | | | 3.27 | |

Net income | | | 0.72 | | | | 4.31 | | | | 4.75 | | | | 3.26 | | | | 3.42 | |

Dividends declared per common share | | | 2.16 | | | | 1.96 | | | | 1.76 | | | | 1.60 | | | | 1.10 | |

At December 31 | | | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 2,187,631 | | | $ | 1,884,318 | | | $ | 1,494,037 | | | $ | 1,484,101 | | | $ | 1,264,032 | |

Total deposits | | | 826,230 | | | | 712,041 | | | | 591,828 | | | | 561,513 | | | | 473,614 | |

Long-term debt | | | 427,112 | | | | 288,494 | | | | 217,499 | | | | 207,910 | | | | 162,702 | |

Mandatorily redeemable securities of subsidiary trusts(3) | | | 23,594 | | | | 9,579 | | | | 6,264 | | | | 6,209 | | | | 6,057 | |

Common stockholders’ equity | | | 113,598 | | | | 118,783 | | | | 111,412 | | | | 108,166 | | | | 96,889 | |

Total stockholders’ equity | | | 113,598 | | | | 119,783 | | | | 112,537 | | | | 109,291 | | | | 98,014 | |

Ratios: | | | | | | | | | | | | | | | | | | | | |

Return on common stockholders’ equity(4) | | | 2.9 | % | | | 18.8 | % | | | 22.3 | % | | | 17.0 | % | | | 19.8 | % |

Return on total stockholders’ equity(4) | | | 3.0 | | | | 18.6 | | | | 22.2 | | | | 16.8 | | | | 19.6 | |

Tier 1 Capital | | | 7.12 | % | | | 8.59 | | | | 8.79 | | | | 8.74 | | | | 8.91 | |

Total Capital | | | 10.70 | | | | 11.65 | | | | 12.02 | | | | 11.85 | | | | 12.04 | |

Leverage(5) | | | 4.03 | | | | 5.16 | | | | 5.35 | | | | 5.20 | | | | 5.56 | |

Common stockholders’ equity to assets | | | 5.19 | % | | | 6.30 | % | | | 7.46 | % | | | 7.29 | % | | | 7.67 | % |

Total stockholders’ equity to assets | | | 5.19 | | | | 6.36 | | | | 7.53 | | | | 7.36 | | | | 7.75 | |

Dividend payout ratio(6) | | | 300.0 | | | | 45.5 | | | | 37.1 | | | | 49.1 | | | | 32.2 | |

Book value per common share | | $ | 22.74 | | | $ | 24.18 | | | $ | 22.37 | | | $ | 20.82 | | | $ | 18.79 | |

Ratio of earnings to fixed charges and preferred stock dividends | | | 1.02 | x | | | 1.51 | x | | | 1.79 | x | | | 2.00 | x | | | 2.41 | x |

| (1) | Discontinued operations for 2003 to 2006 include the operations and associated gain on sale of substantially all of its Asset Management business. The majority of the sale closed on December 1, 2005. Discontinued operations from 2003 to 2006 also include the operations and associated gain on sale of Citigroup’s Travelers Life & Annuity, substantially all of Citigroup’s international insurance business and Citigroup’s Argentine pension business to MetLife Inc. The sale closed on July 1, 2005. See Note 3 to the Consolidated Financial Statements on page 125. |

| (2) | Accounting change of $(49) million in 2005 represents the adoption of Financial Accounting Standards Board (FASB) Interpretation No. 47, “Accounting for Conditional Asset Retirement Obligations, an interpretation of SFAS No. 143, (FIN 47).” |

| (3) | During 2004, the Company deconsolidated the subsidiary issuer trusts in accordance with FIN 46-R. For regulatory capital purposes, these trust securities remain a component of Tier 1 Capital. See “Capital Resources and Liquidity” on page 75. |

| (4) | The return on average common stockholders’ equity is calculated using net income less preferred stock dividends divided by average common stockholders’ equity. The return on total stockholders’ equity is calculated using net income divided by average stockholders’ equity. |

| (5) | Tier 1 Capital divided by adjusted average assets. |

| (6) | Dividends declared per common share as a percentage of net income per diluted share. |

Certain statements in this Annual Report on Form 10-K, including, but not limited to, statements made in “Management’s Discussion and Analysis,” particularly in the “Outlook” sections, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on management’s current

expectations and are subject to uncertainty and changes in circumstances. Actual results may differ materially from those included in these statements due to a variety of factors including, but not limited to, those described under “Risk Factors” on page 38.

3

MANAGEMENT’S DISCUSSION AND ANALYSIS

2007 IN SUMMARY

There were a number of highlights in 2007, including record performance of our International Consumer, Global Wealth Management andTransaction Services business segments.

These positives, however, were offset by disappointing results in our Markets & Banking business, which was significantly affected by write-downs related to direct subprime exposures, including CDOs, leveraged lending, and by significantly higher credit costs in our U.S. Consumer business. In 2007, Citigroup earned $3.6 billion from continuing operations on revenues of $81.7 billion. Income and EPS were both down 83% from 2006 levels.

Customer volume growth was strong, with average loans up 17%, average deposits up 20% and average interest-earning assets up 29% from year-ago levels.International Cards purchase sales were up 37%, whileU.S. Cardssales were up 8%. In Global Wealth Management, client assets under fee-based management were up 27%. Branch activity included the opening or acquisition of 712 new branches during 2007 (510 internationally and 202 in the U.S.). We also completed several strategic acquisitions or investments (including Nikko Cordial, Egg, Quilter, GFU, Grupo Cuscatlan, ATD, and Akbank), which were designed to strengthen our franchises.

Revenues of $81.7 billion decreased 9% from 2006, primarily driven by significantly lower revenues in CMB due to write-downs related to subprime CDOs and leveraged lending. Revenues outside of CMB grew 14%. Our international operations recorded revenue growth of 15% in 2007, including a 28% increase in International Consumer and a $1.8 billion increase in International GWM, partially offset by a 9% decrease in International CMB.

Net interest revenue grew 19% from 2006, reflecting volume increases across all products. Net interest margin in 2007 was 2.45%, down 21 basis points from 2006, as higher funding costs exceeded the Company’s actions to better manage interest earning assets and reduce low-yielding asset balances, and increased ownership in Nikko Cordial (see the discussion of net interest margin on page 70). Non-interest revenue decreased 31% from 2006, primarily reflecting subprime write-downs. Securities and Banking finished the year ranked #1 in equity underwriting and #2 in completed mergers and acquisitions activity.

Operating expenses increased 18% from the previous year primarily driven by the impact of acquisitions, increased business volumes, charges related to the structural expense initiative and the impact of foreign exchange.

Our equity capital base and trust preferred securities grew to $137.2 billion at December 31, 2007. Stockholders’ equity decreased by $6.2 billion during 2007 to $113.6 billion, which included the distribution of $10.7 billion in dividends to common shareholders. Citigroup maintained its “well-capitalized” position with a Tier 1 Capital Ratio of 7.12% at December 31, 2007. Return on common equity was 2.9% for 2007.

During December 2007 and January 2008 we raised over $30 billion to strengthen our capital base. See page 75 for a discussion of our pro forma year-end capital ratios.

On January 14, 2008, the Board decreased the quarterly dividend on the Company’s common stock to $0.32 per share. This new dividend level will allow the Company to reinvest in growth opportunities and properly position the Company for both favorable and unfavorable economic conditions.

Credit costs increased $10.6 billion from year-ago levels, driven by an increase in NCLs of $3.1 billion and a net charge of $7.5 billion to build loan loss reserves.

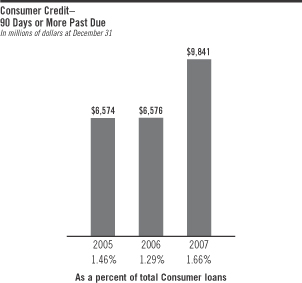

U.S. Consumer credit costs increased $7.1 billion from year-ago levels, driven by a change in estimate of loan losses, increased NCLs and net builds to loan loss reserves. The increases were due to a weakening in credit indicators and sharply higher delinquencies on first and second mortgages related to the deterioration in the U.S. housing market. The NCL ratio increased 27 basis points to 1.46%.

International Consumer credit costs increased $2.3 billion, reflecting a change in estimate of loan losses, along with volume growth and credit weakness in certain countries, the impact of recent acquisitions, and the increase of NCLs in Japan Consumer Finance due to grey zone issues.

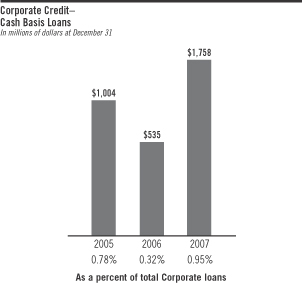

Markets & Banking credit costs increased $1.0 billion, driven by higher NCLs associated with subprime-related direct exposures. Corporate cash-basis loans increased $1.2 billion from year-ago levels to $1.8 billion.

The Company recorded an income tax benefit for 2007, resulting from the significant amount of consolidated pretax lossesinthe Company’s S&Band U.S. Consumer Lendingbusinesses and the tax benefits of permanent differences.

On November 4, 2007, Charles Prince, Chairman and Chief Executive Officer, elected to retire from Citigroup. Robert Rubin served as Chairman between November 4 and December 11. On December 11, 2007, the Board appointed Vikram Pandit as CEO and Sir Win Bischoff as Chairman.

4

OUTLOOK FOR 2008

We enter the challenging environment of 2008 after a disappointing 2007. We are focused on establishing stability for our Company and developing opportunities for enduring growth. We have a stronger capital structure in place and are working to establish a mix of assets and businesses that maximize returns to shareholders.

Business Reviews

We are currently conducting business reviews through all of our franchises. The possible outcomes from these reviews include the focus on establishing stability for our Company; repositioning of low-return, non-strategic assets that do not support our growth strategy; redirection of capital to higher-return opportunities to drive shareholder value in the future; and streamlining certain businesses.

Our Goals in 2008

| • | | Our main goal is capital allocation excellence and we are aggressively building a new risk management culture. Our goal is to have the best risk management in the industry, transforming it into a key competitive advantage that will drive bottom-line results. |

| • | | Strong expense management and the ability to execute productively against our plans are core to our priorities. Our re-engineering and expense management program is designed to make Citigroup more efficient. |

| • | | Another priority is to make financial matters better and easier for our clients in every way that we can. Financial markets are becoming more and more complex, encouraging a deepening interdependency between Citigroup and our clients. |

| • | | We intend to leverage the benefits of emerging technology to respond more quickly, communicate more effectively, simplify transactions, and innovate faster, thus serving our global clients better. |

| • | | We are focused on managing our talent more effectively by rewarding demonstrated performance and by putting the right people in the right positions. |

Economic Environment

As a worldwide business, Citigroup’s financial results are closely tied to the global economic environment. There is a risk of a U.S. and/or global downturn in 2008. A U.S-led economic downturn could negatively impact other markets and economies around the world and could restrict the Company’s growth opportunities internationally. Should economic conditions further deteriorate, the Company could see revenue reductions across its businesses and increased costs of credit. In addition, continuing deterioration of the U.S. or global real estate markets could adversely impact the Company’s revenues, including additional write-downs of subprime and other exposures, additional write-downs of leveraged loan commitments and cost of credit, including increased credit losses in mortgage-related and other activities. Further adverse rating actions by credit rating agencies in respect of structured credit products or other credit-related exposures, or of monoline insurers could result in revenue reductions in those or similar securities. See “Risk Factors” on page 38 for a further discussion of risks.

Credit Costs and Income Taxes

Credit costs in U.S. Consumer are expected to increase across most portfolios due to deterioration in the U.S. housing market, as well as higher levels of unemployment and bankruptcy filings.

Credit costs are expected to increase across all international businesses as their growing portfolios season or mature, and may be affected by economic and credit conditions in the U.S. and around the world.

The impact of changes to consumer lending laws enacted in 2006, as well as deteriorating consumer credit conditions will increase credit costs in the Japan Consumer Finance business.

While corporate loan default rates are near historic lows, they are projected to increase in 2008. Classified loan exposures are on a rising trend and credit markets are difficult. These credit markets negatively affect a wide range of products, including auction rate securities, credit default swaps and the leveraged loan syndication market.

The 2008 effective tax rate is expected to return to a normalized rate depending on pretax income levels and geographic mix of earnings.

A detailed review and outlook for each of our business segments are included in the discussions that follow, and the risks are more fully discussed on pages 38 to 65.

5

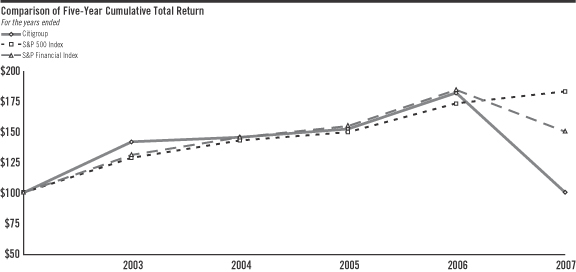

Comparison of Five-Year Cumulative Total Return

The following graph compares the cumulative total return on Citigroup’s common stock with the S&P 500 Index and the S&P Financial Index over the five-year period extending through December 31, 2007. The graph

assumes that $100 was invested on December 31, 2002 in Citigroup’s common stock, the S&P 500 Index and the S&P Financial Index and that all dividends were reinvested.

| | | | | | | | | |

| DECEMBER 31 | | CITIGROUP | | S&P 500 INDEX | | S&P FINANCIAL INDEX |

| 2003 | | $ | 141.58 | | $ | 128.68 | | $ | 131.03 |

| 2004 | | | 145.44 | | | 142.69 | | | 145.32 |

| 2005 | | | 152.17 | | | 149.68 | | | 154.66 |

| 2006 | | | 181.92 | | | 173.32 | | | 184.33 |

| 2007 | | | 100.58 | | | 182.84 | | | 149.99 |

6

EVENTS IN 2007

ITEMS IMPACTING THE SECURITIES AND BANKING BUSINESS

Losses on Subprime-Related Direct Exposures

During the second half of 2007, the Company’sSecurities and Banking (S&B) business recorded unrealized losses of $19.6 billion pretax, net of hedges, on subprime-related direct exposures.

The Company’s remaining $37.3 billion in U.S. subprime net direct exposure inS&B at December 31, 2007 consisted of (a) approximately $8.0 billion of subprime-related exposures in its lending and structuring business and (b) approximately $29.3 billion of net exposures to the super senior tranches of collateralized debt obligations, which are collateralized by asset-backed securities, derivatives on asset-backed securities or both. See “Exposure to Real Estate” on page 48 for a further discussion.

Write-Downs on Highly Leveraged Loans and Commitments

During the second half of 2007, Citigroup recorded write-downs of approximately $1.5 billion pretax, net of underwriting fees, on funded and unfunded highly leveraged finance commitments in theS&B business. Of this amount, approximately $1.1 billion related to debt underwriting activities and $381 million related to lending activities. Write-downs were recorded on all highly leveraged finance commitments where there was value impairment, regardless of the expected funding date. See “Highly Leveraged Funding Commitments” on page 96 for a further discussion.

CREDIT, RESTRUCTURING AND INCOME TAXES

Credit Reserves

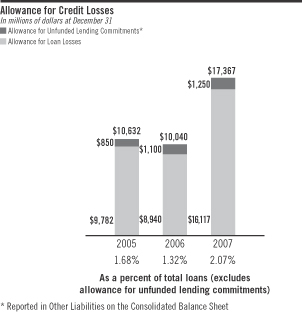

During 2007, the Company recorded a net build of $7.1 billion to its credit reserves, which included an increase in the allowance for unfunded lending commitments of $150 million. The build consisted of $6.3 billion in Global Consumer ($5.0 billion in U.S. Consumer and $1.3 billion in International Consumer), $100 million in Global Wealth Management and $715 million in Markets & Banking.

The $5.0 billion build in U.S. Consumer reflected a weakening of leading credit indicators including delinquencies on first and second mortgages and deterioration in the housing market (approximately $3.0 billion), a downturn in other economic trends including unemployment and GDP, as well as the impact of housing market deterioration, affecting all other portfolios ($1.3 billion), and a change in the estimate of loan losses inherent in the portfolio, but not yet visible in delinquency statistics (approximately $700 million).

The $1.3 billion build in International Consumer included a change in estimate of loan losses inherent in the portfolio but not yet visible in delinquency statistics (approximately $600 million), along with volume growth and credit deterioration in certain countries. With the exception of Mexico, Japan and India, the International Consumer credit environment remained generally stable.

The build of $715 million in Markets & Banking primarily reflected a slight weakening in overall portfolio credit quality, as well as loan loss reserves for specific counterparties. The loan loss reserves for specific counterparties include $327 million for subprime-related direct exposures.

During 2007, the Company changed its estimate of loan losses inherent in the Global Consumer portfolio that were not yet visible in delinquency statistics. The changes in estimate were accounted for prospectively in accordance with FASB Statement No. 154, “Accounting Changes and Error Corrections” (SFAS 154).For the quarter ended March 31, 2007, the change in estimate decreased the Company’s pretax net income by approximately $170 million, or $0.02 per diluted share. For the quarter ended June 30, 2007, the change in estimate decreased the Company’s pretax net income by $240 million, or $0.03 per diluted share. For the quarter ended September 30, 2007, the change in estimate decreased the Company’s pretax net income by approximately $900 million, or $0.11 per diluted share.

Structural Expense Review

In 2007, the Company completed a review of its structural expense base in a Company-wide effort to create a more streamlined organization, reduce expense growth, and provide investment funds for future growth initiatives.

As a result of the review, a pretax restructuring charge of $1.4 billion ($871 million after-tax) was recorded in Corporate/Other during the first quarter of 2007. Additional charges of $200 million were recognized later in 2007. Separate from the restructuring charge, additional implementation costs of approximately $100 million pretax were recorded throughout 2007.

7

Because these charges are a Company-wide initiative, they are reflected in Corporate/Other.

See Note 10 on page 138 for additional information.

In addition, during 2007 several businesses took on their own re-engineering initiatives to further reduce expenses beyond this Company-wide review. These additional initiatives resulted in total repositioning charges of $539 million pretax. These charges, which were incurred by Markets & Banking for $438 million, Global Consumer for $35 million and Global Wealth Management for $67 million, are included in each of these business groups’ 2007 results.

Income Taxes

The Company recorded an income tax benefit for 2007. The effective tax rate (benefit) of (129)% primarily resulted from the pretax losses in the Company’sS&BandU.S. Consumer Lending businesses (the U.S. is a higher tax jurisdiction). In addition, the tax benefits of permanent differences, including the tax benefit for not providing U.S. income taxes on the earnings of certain foreign subsidiaries that are indefinitely invested, favorably affected the Company’s effective tax rate.

The Company’s effective tax rate on continuing operations of 27.3% in 2006 included a $598 million benefit from the resolution of the Federal Tax Audit and a $237 million benefit from the resolution of the New York Tax Audits.

CAI’S STRUCTURED INVESTMENT VEHICLES (SIVs)

On December 13, 2007, Citigroup announced its decision to commit, not legally required, to provide a support facility that would resolve uncertainties regarding senior debt repayment facing the Citi-advised Structured Investment Vehicles (SIVs). As a result of the Company’s commitment, Citigroup included the SIVs’ assets and liabilities in its Consolidated Balance Sheet as of December 31, 2007. This resulted in an increase of assets of $59 billion. On February 12, 2008, Citigroup finalized the terms of the support facility, which takes the form of a commitment to provide mezzanine capital to the SIV vehicles in the event the market value of their capital notes approaches zero.

RECENTLY ANNOUNCED FINANCIAL ACTIONS TO ENHANCE CITIGROUP’S CAPITAL BASE

During the fourth quarter of 2007 and the first quarter of 2008, the Company raised approximately $30 billion of qualifying Tier 1 Capital. These transactions include the issuance of convertible preferred and straight (non-convertible) preferred securities, equity units and enhanced trust-preferred securities. In addition, Citigroup purchased the Nikko Cordial shares that it did not already own, by issuing 175 million Citigroup common shares (approximately $4.4 billion based on the exchange terms) in exchange for those Nikko Cordial shares.

The Company reported a Tier 1 Capital ratio of 7.12% and a Tangible Common Equity (TCE) as a percent of Risk Weighted Managed Assets (RWMA) ratio of 5.6% at December 31, 2007. On a pro forma basis, after giving effect to the issuance of the new securities referred to above (and including the common shares issued in connection with the Nikko Cordial transaction), the Company’s December 31, 2007 Tier 1 Capital ratio would be approximately 8.8% and its TCE/RWMA would be approximately 6.9%. See “Capital Resources and Liquidity” on page 75 for further details.

Lowering the Company’s Quarterly Dividend to $0.32 Per Share

On January 14, 2008 the Board declared a quarterly dividend on the Company’s common stock of $0.32 per share, which was paid on February 22, 2008, to stockholders of record on February 4, 2008. This action would result in a reduction in the dividend level of approximately $4.4 billion from the previous year. This new dividend level will allow the Company to reinvest in growth opportunities and properly position the Company for both favorable and unfavorable economic conditions. The Board is responsible for setting dividend levels and declaring dividends.

STRATEGIC ACQUISITIONS

U.S.

Acquisition of ABN AMRO Mortgage Group

In 2007, Citigroup acquired ABN AMRO Mortgage Group (AAMG), a subsidiary of LaSalle Bank Corporation and ABN AMRO Bank N.V. AAMG is a national originator and servicer of prime residential mortgage loans. As part of this acquisition, Citigroup purchased approximately $12 billion in assets, including $3 billion of mortgage servicing rights, which resulted in the addition of approximately 1.5 million servicing customers. Results for AAMG are included within Citigroup’sU.S. Consumer Lendingbusiness from March 1, 2007 forward.

Acquisition of Old Lane Partners, L.P.

In 2007, the Company completed the acquisition of Old Lane Partners, L.P. and Old Lane Partners, GP, LLC (Old Lane). Old Lane is the manager of a global, multi-strategy hedge fund and a private equity fund with total assets under management and private equity commitments of approximately $4.5 billion. Results for Old Lane are included within Citi Alternative Investments (CAI), Citigroup’s integrated alternative investments platform, from July 2, 2007 forward.

8

Acquisition of Bisys

In 2007, the Company completed its acquisition of Bisys Group, Inc. (Bisys) for $1.47 billion in cash. In addition, Bisys’ shareholders received $18.2 million in the form of a special dividend paid by Bisys simultaneously. Citigroup completed the sale of the Retirement and Insurance Services Divisions of Bisys to affiliates of J.C. Flowers & Co. LLC, making the net cost of the transaction to Citigroup approximately $800 million. Citigroup retained the Fund Services and Alternative Investment services businesses of Bisys, which provides administrative services for hedge funds, mutual funds and private equity funds. Results for Bisys are included within Citigroup’sTransaction Services business from August 1, 2007 forward.

Acquisition of Automated Trading Desk

In 2007, Citigroup completed its acquisition of Automated Trading Desk (ATD), a leader in electronic market making and proprietary trading, for approximately $680 million ($102.6 million in cash and approximately 11.17 million shares of Citigroup common stock). ATD operates as a unit of Citigroup’s Global Equities business, adding a network of broker-dealer customers to Citigroup’s diverse base of institutional, broker-dealer and retail customers. Results for ATD are included within Citigroup’sSecurities and Banking business from October 3, 2007 forward.

Japan

Nikko Cordial

Citigroup began consolidating Nikko Cordial’s financial results and the related minority interest under the equity method of accounting on May 9, 2007, when Nikko Cordial became a 61%-owned subsidiary. Citigroup later increased its ownership stake in Nikko Cordial to approximately 68%. Nikko Cordial results are included within Citigroup’sSecurities and Banking,Smith Barney and International Consumer businesses.

On January 29, 2008, Citigroup completed the acquisition of the remaining Nikko Cordial shares that it did not already own, by issuing 175 million Citigroup common shares (approximately $4.4 billion based on the exchange terms) in exchange for those Nikko Cordial shares. The share exchange was completed following the listing of Citigroup’s common shares on the Tokyo Stock Exchange on November 5, 2007.

Latin America

Acquisition of Grupo Financiero Uno

In 2007, Citigroup completed its acquisition of Grupo Financiero Uno (GFU), the largest credit card issuer in Central America, and its affiliates.

The acquisition of GFU, with $2.2 billion in assets, expands the presence of Citigroup’s Latin America consumer franchise, enhances its credit card business in the region and establishes a platform for regional growth in Consumer Finance and Retail Banking. GFU has more than one million retail clients and operates a distribution network of 75 branches and more than 100 mini-branches and points of sale. The results for GFU are included within Citigroup’sInternational Cards and International Retail Bankingbusinesses from March 5, 2007 forward.

Acquisition of Grupo Cuscatlan

In 2007, Citigroup completed the acquisition of the subsidiaries of Grupo Cuscatlan for $1.51 billion ($755 million in cash and 14.2 million shares of Citigroup common stock) from Corporacion UBC Internacional S.A. Grupo Cuscatlan is one of the leading financial groups in Central America, with assets of $5.4 billion, loans of $3.5 billion, and deposits of $3.4 billion. Grupo Cuscatlan has operations in El Salvador, Guatemala, Costa Rica, Honduras and Panama. The results of Grupo Cuscatlan are included from May 11, 2007 forward and are recorded inInternational Retail Banking.

Agreement to Establish Partnership with Quiñenco– Banco de Chile

In 2007, Citigroup and Quiñenco entered into a definitive agreement to establish a strategic partnership that combines Citigroup operations in Chile with Banco de Chile’s local banking franchise to create a banking and financial services institution with approximately 20% market share of the Chilean banking industry. The transaction closed on January 1, 2008.

Under the agreement, Citigroup contributed Citigroup’s Chilean operations and other assets, and acquired an approximate 32.96% stake in LQIF, a wholly owned subsidiary of Quiñenco that controls Banco de Chile, and is accounted for under the equity method of accounting. As part of the overall transaction, Citigroup also acquired the U.S. branches of Banco de Chile for approximately $130 million. Citigroup has entered into an agreement to acquire an additional 17.04% stake in LQIF for approximately $1 billion within three years. The new partnership calls for active participation by Citigroup in the management of Banco de Chile including board representation at both LQIF and Banco de Chile.

Asia

Acquisition of Bank of Overseas Chinese

In 2007, Citigroup completed its acquisition of Bank of Overseas Chinese (BOOC) in Taiwan for approximately $427 million. BOOC offers a broad suite of corporate banking, consumer and wealth management products and services to more than one million clients through 55 branches in Taiwan. This transaction will strengthen Citigroup’s presence in Asia, making it the largest international bank and 13th largest by total assets among all domestic Taiwan banks. Results for BOOC are included in Citigroup’sInternational Retail Banking,International Cards andSecurities and Banking businesses from December 1, 2007 forward.

9

EMEA

Acquisition of Quilter

In 2007, the Company completed the acquisition of Quilter, a U.K. wealth advisory firm with over $10.9 billion of assets under management, from Morgan Stanley. Quilter has more than 18,000 clients and 300 staff located in 10 offices throughout the U.K., Ireland and the Channel Islands. Quilter’s results are included in Citigroup’sSmith Barney business from March 1, 2007 forward.

Acquisition of Egg

In 2007, Citigroup completed its acquisition of Egg Banking plc (Egg), one of the U.K.’s leading online financial services providers, from Prudential PLC for approximately $1.39 billion. Egg offers various financial products and services including online payment and account aggregation services, credit cards, personal loans, savings accounts, mortgages, insurance and investments. Results for Egg are included in Citigroup’sInternational Cards and International Retail Banking businesses from May 1, 2007 forward.

Purchase of 20% Equity Interest in Akbank

In 2007, Citigroup completed its purchase of a 20% equity interest in Akbank for approximately $3.1 billion and is accounted for under the equity method of accounting. Akbank, the second-largest privately owned bank by assets in Turkey, is a premier, full-service retail, commercial, corporate and private bank.

Sabanci Holding, a 34% owner of Akbank shares, and its subsidiaries have granted Citigroup a right of first refusal or first offer over the sale of any of their Akbank shares in the future. Subject to certain exceptions, including purchases from Sabanci Holding and its subsidiaries, Citigroup has otherwise agreed not to increase its percentage ownership in Akbank.

OTHER ITEMS

Sale of MasterCard Shares

In 2007, the Company recorded a $367 million after-tax gain ($581 million pretax) on the sale of approximately 4.9 million MasterCard Class B shares that had been received by Citigroup as a part of the MasterCard Initial Public Offering (IPO) completed in June 2006. The gain was recorded in the following businesses:

| | | | | | | | | | | | |

| In millions of dollars | | 2007

Pretax

total | | 2007 After-tax total | | 2006

Pretax

total | | 2006 After-tax total |

U.S. Cards | | $ | 394 | | $ | 250 | | $ | 59 | | $ | 37 |

U.S. Retail Distribution | | | 55 | | | 33 | | | 7 | | | 5 |

International Cards | | | 72 | | | 46 | | | 35 | | | 22 |

International Retail Banking | | | 41 | | | 26 | | | 20 | | | 13 |

Markets & Banking | | | 19 | | | 12 | | | 2 | | | 1 |

Total | | $ | 581 | | $ | 367 | | $ | 123 | | $ | 78 |

Redecard IPO

In 2007, Citigroup (a 31.9% shareholder in Redecard S.A., the only merchant acquiring company for MasterCard in Brazil) sold approximately 48.8 million Redecard shares in connection with Redecard’s IPO in Brazil. Following the sale of these shares, Citigroup retained approximately 23.9% ownership in Redecard. An after-tax gain of approximately $469 million ($729 million pretax) was recorded in Citigroup’s 2007 financial results in theInternational Cards business.

Visa Restructuring and Litigation Matters

In 2007, Visa USA, Visa International and Visa Canada were merged into Visa Inc. (Visa). As a result of that reorganization, Citigroup recorded a $534 million (pretax) gain on its holdings of Visa International shares primarily recognized in theInternational Consumer business, which are carried on Citigroup’s balance sheet at the new cost basis. In addition, Citigroup recorded a $306 million (pretax) charge related to certain of Visa USA’s litigation matters primarily recognized in the U.S. Consumer business.

Both the Visa-related gain and charge are subject to change, depending on the timing and success of Visa’s planned IPO and other factors. For example, in connection with its upcoming planned IPO, Visa has announced plans to withhold, on a pro rata basis, shares to be distributed to its USA member banks (including Citigroup), which would be used to fund an escrow account to satisfy certain of Visa USA’s litigation matters. Such a withholding could enable Citigroup to release portions of its $306 million reserve.

Sale of Simplex Investment Advisors Inc. Shares

In 2007, Nikko Cordial sold all of its shares of Simplex Investment Advisors Inc. (SIA) for an after-tax gain of $106 million ($313 million pretax), which was recorded inInternational Retail Banking. Nikko Cordial held 42.5% of SIA.

10

ACCOUNTING CHANGES

Adoption of SFAS 157–Fair Value Measurements

The Company elected to early-adopt SFAS No. 157, “Fair Value Measurements” (SFAS 157), as of January 1, 2007. SFAS 157 defines fair value, expands disclosure requirements around fair value and specifies a hierarchy of valuation techniques based on whether the inputs to those valuation techniques are observable or unobservable. Observable inputs reflect market data obtained from independent sources, while unobservable inputs reflect the Company’s market assumptions. These two types of inputs create the following fair value hierarchy:

| • | | Level 1–Quoted prices foridentical instruments in active markets. |

| • | | Level 2–Quoted prices forsimilar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets. |

| • | | Level 3–Valuations derived from valuation techniques in which one or more significant inputs or significant value drivers are unobservable. |

This hierarchy requires the Company to use observable market data, when available, and to minimize the use of unobservable inputs when determining fair value.

For some products or in certain market conditions, observable inputs may not be available. For example, during the market dislocations that occurred in the second half of 2007, certain markets became illiquid, and some key inputs used in valuing certain exposures were unobservable. When and if these markets are liquid, the valuation of these exposures will use the related observable inputs available at that time from these markets.

Under SFAS 157, Citigroup is required to take into account its own credit risk when measuring the fair value of derivative positions as well as other liabilities for which fair value accounting has been elected under SFAS 155, “Accounting for Certain Hybrid Financial Instruments” (SFAS 155) and SFAS 159, after taking into consideration the effects of credit-risk mitigants. The adoption of SFAS 157 has also resulted in some other changes to the valuation techniques used by Citigroup when determining the fair value of derivatives, most notably changes to the way that the probability of default of a counterparty is factored in, and the elimination of a derivative valuation adjustment which is no longer necessary under SFAS 157. The cumulative effect at January 1, 2007 of making these changes was a gain of $250 million after-tax ($402 million pretax), or $0.05 per diluted share, which was recorded in the 2007 first quarter earnings within theSecurities and Banking business.

SFAS 157 also precludes the use of block discounts for instruments traded in an active market, which were previously applied to large holdings of publicly traded equity securities, and requires the recognition of trade-date gains related to certain derivative trades that use unobservable inputs in determining their fair value. Previous accounting guidance allowed the use

of block discounts in certain circumstances and prohibited the recognition of day-one gains on certain derivative trades when determining the fair value of instruments not traded in an active market. The cumulative effect of these changes resulted in an increase to January 1, 2007 retained earnings of $75 million.

Adoption of SFAS 159–Fair Value Option

In conjunction with the adoption of SFAS 157, the Company early-adopted SFAS 159, “The Fair Value Option for Financial Assets and Financial Liabilities” (SFAS 159), as of January 1, 2007. SFAS 159 provides an option on an instrument-by-instrument basis for most financial assets and liabilities to be reported at fair value with changes in fair value reported in earnings. After the initial adoption, the election is made at the time of the acquisition of a financial asset, financial liability, or a firm commitment, and it may not be revoked. SFAS 159 provides an opportunity to mitigate volatility in reported earnings that resulted prior to its adoption from being required to apply fair value accounting to certain economic hedges (e.g., derivatives) while having to measure the assets and liabilities being economically hedged using an accounting method other than fair value.

Under the SFAS 159 transition provisions, the Company elected to apply fair value accounting to certain financial instruments held at January 1, 2007 with future changes in value reported in earnings. The adoption of SFAS 159 resulted in an after-tax decrease to January 1, 2007 retained earnings of $99 million ($157 million pretax).

See Note 26 to the Consolidated Financial Statements on page 167 for additional information.

SUBSEQUENT EVENT

On February 20, 2008, the Company entered into a $500 million credit facility with the Falcon multi-strategy fixed income funds (the “Funds”) managed by Citigroup Alternative Investments. As a result of providing this facility, the Company became the primary beneficiary of the Funds and will include the Funds’ assets and liabilities in its Consolidated Balance Sheet commencing on February 20, 2008. The consolidation of the Funds will increase Citigroup’s assets and liabilities by approximately $10 billion.

11

EVENTS IN 2006

Strategic Investment and Cooperation Agreement with Guangdong Development Bank

In 2006, a Citigroup-led consortium acquired an 85.6% stake in Guangdong Development Bank (“GDB”). Citigroup’s share is 20% of GDB and its investment of approximately $725 million is accounted for under the equity method of accounting.

Sale of Avantel

In 2006, Citigroup sold its investment in Avantel, a leading long-distance telecom service provider inMexico, to AXTEL. The transaction resulted in an after-tax gain of $145 million ($234 million pretax) in the 2006 fourth quarter. The investment in Avantel was initially acquired by Citigroup as part of its acquisition of Banamex in 2001 and was subsequently increased with the purchase of an additional stake in 2005.

Repositioning of the Japan Consumer Finance Business

In 2007, Citigroup announced that it would reposition its consumer finance business inJapan. This decision resulted from changes in the operating environment in the consumer finance business inJapan, and the passage on December 13, 2006, of changes toJapan’s consumer lending laws. The change in law will lower the interest rates permissible on new consumer finance loans by 2010.

In 2006, the Company recorded a $375 million after-tax ($581 million pretax) charge to increase reserves for estimated losses resulting from customer refund settlements in the business. This charge was recorded as a reduction to interest revenue on loans. The Company also recorded a $40 million after-tax ($60 million pretax) repositioning charge for costs associated with closing approximately 270 branches and 100 automated loan machines.

Finalizing the 2005 Sale of Asset Management Business

In 2005, the Company sold substantially all of its Asset Management Business to Legg Mason Inc. (Legg Mason) in exchange for Legg Mason’s broker-dealer and capital markets businesses, $2.298 billion of Legg Mason’s common and preferred shares (valued as of the closing date), and $500 million in cash. This cash was obtained via a lending facility provided by Citigroup’s lending business. The transaction did not include Citigroup’s asset management business inMexico, its retirement services business inLatin America (both of which are included inInternational Retail Banking) or its interest in the CitiStreet joint venture (which is included inSmith Barney). The total value of the transaction at the time of closing was approximately $4.369 billion, resulting in an after-tax gain for Citigroup of approximately $2.082 billion ($3.404 billion pretax), which was reported in discontinued operations.

Concurrent with this sale, the Company sold Legg Mason’s capital markets business to Stifel Financial Corp. (The transactions described in the above two paragraphs are referred to as the “Sale of the Asset Management Business.”)

With the receipt of Legg Mason’s broker-dealer business, the Company added 1,226 financial advisors in 124 branch offices to its Global Wealth Management business.

During March 2006, the Company sold 10.3 million shares of Legg Mason stock through an underwritten public offering. The net sale proceeds of $1.258 billion resulted in a pretax gain of $24 million for the Company.

In September 2006, the Company received from Legg Mason the final closing adjustment payment related to this sale. This payment resulted in an additional after-tax gain of $51 million ($83 million pretax), recorded in discontinued operations.

Additional information can be found in Note 3 to the Consolidated Financial Statements on page 125.

RESOLUTION OF TAX AUDITS

New York State and New York City

In 2006, Citigroup reached a settlement agreement with the New York State and New York City taxing authorities regarding various tax liabilities for the years 1998 – 2005 (referred to above and hereinafter as the “resolution of the New York Tax Audits”).

For the third quarter of 2006, the Company released $254 million from its tax contingency reserves, which resulted in increases of $237 million in after-tax Income from continuing operations and $17 million in after-tax Income from discontinued operations.

Federal

In 2006, the Company received a notice from the Internal Revenue Service (IRS) that they had concluded the tax audit for the years 1999 through 2002 (referred to above and hereinafter as the “resolution of the Federal Tax Audit”). For the 2006 first quarter, the Company released a total of $657 million from its tax contingency reserves related to the resolution of the Federal Tax Audit.

The following table summarizes the 2006 tax benefits, by business, from the resolution of the New York Tax Audits and Federal Tax Audit:

| | | | | | | | | |

| In millions of dollars | | New York City

and New York

State Audits | | Federal Audit | | Total |

Global Consumer | | $ | 79 | | $ | 290 | | $ | 369 |

Markets & Banking | | | 116 | | | 176 | | | 292 |

Global Wealth Management | | | 34 | | | 13 | | | 47 |

Alternative Investments | | | — | | | 58 | | | 58 |

Corporate/Other | | | 8 | | | 61 | | | 69 |

Continuing Operations | | $ | 237 | | $ | 598 | | $ | 835 |

Discontinued Operations | | $ | 17 | | $ | 59 | | $ | 76 |

Total | | $ | 254 | | $ | 657 | | $ | 911 |

12

Finalizing the 2005 Sale of Travelers Life & Annuity

In 2005, the Company sold Citigroup’s Travelers Life & Annuity and substantially all of Citigroup’s international insurance businesses to MetLife. The businesses sold were the primary vehicles through which Citigroup engaged in the Life Insurance and Annuities business. This transaction encompassed Travelers Life & Annuity’s U.S. businesses and its international operations, other than Citigroup’s life insurance business inMexico (which is now included withinInternational Retail Banking). (This transaction is referred to hereinafter as the “Sale of the Life Insurance and Annuities Business”.)

At closing, Citigroup received $1.0 billion in MetLife equity securities and $10.830 billion in cash, which resulted in an after-tax gain of approximately $2.120 billion ($3.386 billion pretax), which was included in discontinued operations.

During 2006, Citigroup recognized an $85 million after-tax gain from the sale of MetLife shares. This gain was reported within Income from continuing operations in the Alternative Investments business.

In July 2006, the Company received the final closing adjustment payment related to this sale, resulting in an after-tax gain of $75 million ($115 million pretax), which was recorded in discontinued operations.

Additional information can be found in Note 3 to the Consolidated Financial Statements on page 125.

Sale of Upstate New York Branches

In 2006, Citigroup sold the Upstate New York Financial Center Network, consisting of 21 branches in Rochester, N.Y. and Buffalo, N.Y. to M&T Bank (referred to hereinafter as the “Sale of New York Branches”). Citigroup received a premium on deposit balances of approximately $1 billion. An after-tax gain of $92 million ($163 million pretax) was recognized in 2006.

Acquisition of Federated Credit Card Portfolio and Credit Card Agreement With Federated Department Stores (Macy’s)

In 2005, Citigroup announced a long-term agreement with Federated Department Stores, Inc. (Macy’s) under which the companies partner to acquire and manage approximately $6.2 billion of Macy’s credit card receivables, including existing and new accounts, executed in three phases.

For the first phase, which closed in October 2005, Citigroup acquired Macy’s receivables under management, totaling approximately $3.3 billion. For the second phase, which closed in May 2006, additional Macy’s receivables totaling approximately $1.9 billion were transferred to Citigroup from the previous provider. For the final phase, in July 2006, Citigroup acquired the approximately $1.0 billion credit card receivable portfolio of The May Department Stores Company (May), which merged with Macy’s.

Citigroup paid a premium of approximately 11.5% to acquire these portfolios. The multi-year agreement also provides Macy’s the ability to participate in the portfolio performance, based on credit sales and certain other performance metrics.

The Macy’s and May credit card portfolios comprised a total of approximately 17 million active accounts.

Consolidation of Brazil’s CrediCard

In 2006, Citigroup and Banco Itau dissolved their joint venture in CrediCard, a Brazilian consumer credit card business. In accordance with the dissolution agreement, Banco Itau received half of CrediCard’s assets and customer accounts in exchange for its 50% ownership, leaving Citigroup as the sole owner of CrediCard.

Adoption of the Accounting for Share-Based Payments

In 2006, the Company adopted Statement of Financial Accounting Standards (SFAS) No. 123 (revised 2004), “Share-Based Payment” (SFAS 123(R)), which replaced the existing SFAS 123 and superseded Accounting Principles Board (APB) 25. SFAS 123(R) requires companies to measure and record compensation expense for stock options and other share-based payments based on the instruments’ fair value, reduced by expected forfeitures.

In adopting this standard, the Company conformed to recent accounting guidance that requires restricted or deferred stock awards issued to retirement-eligible employees who meet certain age and service requirements to be either expensed on the grant date or accrued over a service period prior to the grant date. This charge consisted of $398 million after-tax ($648 million pretax) for the immediate expensing of awards granted to retirement-eligible employees in January 2006.

The following table summarizes the SFAS 123(R) impact, by segment, on the 2006 first quarter pretax compensation expense for stock awards granted to retirement-eligible employees in January 2006:

| | |

| In millions of dollars | | 2006 first quarter |

Global Consumer | | $121 |

Markets & Banking | | 354 |

Global Wealth Management | | 145 |

Alternative Investments | | 7 |

Corporate/Other | | 21 |

Total | | $648 |

Additional information can be found in Notes 1 and 8 to the Consolidated Financial Statements on pages 111 and 129, respectively.

Credit Reserves

In 2006, the Company recorded a net release/utilization of its credit reserves of $356 million, consisting of a net release/utilization of $626 million in Global Consumer and a net build of $270 million in CMB. The net release/utilization in Global Consumer was primarily due to lower bankruptcy filings, a stable credit environment in the U.S. Consumer portfolio and International portfolio and a release of approximately $200 million related to Hurricane Katrina. Partially offsetting the net releases were builds inMexico, primarily driven by target market expansion in Cards, Taiwan, due to the impact of industry-wide credit conditions in Cards, andJapan, related to the changes in the consumer lending environment. Developments in 2007 have led to a significant build in reserves in Global Consumer in 2007, as described above.

The net build of $270 million in CMB was primarily composed of $261 million inSecurities and Banking, which included a $232 million reserve increase for unfunded lending commitments during the year. The net build reflected growth in loans and unfunded commitments and a change in credit rating of certain counterparties in certain industries.

13

EVENTS IN 2005

Change in EMEA Consumer Write-off Policy

Prior to the third quarter of 2005, certain Western European consumer portfolios were granted an exception to Citigroup’s global write-off policy. The exception extended the write-off period from the standard 120-day policy for personal installment loans, and was granted because of the higher recovery rates experienced in these portfolios. During 2005, Citigroup observed lower actual recovery rates, stemming primarily from a change in bankruptcy and wage garnishment laws in Germany and, as a result, rescinded the exception to the global standard. The net charge was $332 million ($490 million pretax) resulting from the recording of $1.153 billion of write-offs and a corresponding utilization of $663 million of reserves in the third quarter of 2005.

Hurricane Katrina

In 2005, the Company recorded a $222 million after-tax charge ($357 million pretax) for the estimated probable losses incurred from Hurricane Katrina. This charge consisted primarily of additional credit costs inU.S. Cards,U.S. Commercial Business, U.S. Consumer LendingandU.S. Retail Distribution businesses, based on total credit exposures of approximately $3.6 billion in the Federal Emergency Management Agency (FEMA) Individual Assistance designated areas. This charge did not include an after-tax estimate of $75 million ($109 million pretax) for fees and interest due from related customers that were waived during 2005. These reserves were utilized or released in subsequent years.

United States Bankruptcy Legislation

In 2005, the Bankruptcy Reform Act (the Act) became effective. The Act imposed a means test to determine if people who file for Chapter 7 bankruptcy earn more than the median income in their state and could repay at least $6,000 of unsecured debt over five years. Bankruptcy filers who meet this test are required to enter into a repayment plan under Chapter 13, instead of canceling their debt entirely under Chapter 7. As a result of these more stringent guidelines, bankruptcy claims accelerated prior to the effective date. The incremental bankruptcy losses over the Company’s estimated baseline in 2005 that was attributable to the Act inU.S. Cards business was approximately $970 million on a managed basis ($550 million in the Company’s on-balance-sheet portfolio and $420 million in the securitized portfolio). In addition, theU.S. Retail Distribution business incurred incremental bankruptcy losses of approximately $90 million during 2005.

Bank and Credit Card Customer Rewards Costs

In 2005, the Company conformed its global policy approach for the accounting of rewards costs for bank and credit card customers. Conforming the global policy resulted in the write-off of $354 million after-tax ($565 million pretax) of unamortized deferred rewards costs. Previously, accounting practices for these costs varied across the Company.

The revised policy requires all businesses to recognize rewards costs as incurred.

Sale of Nikko Cordial Stake

During 2005, Citigroup reduced its stake in Nikko Cordial from approximately 11.2% to 4.9%, which resulted in an after-tax gain of $248 million ($386 million pretax).

Sale of the Merchant Acquiring Businesses

In 2005, Citigroup sold its European merchant acquiring business to EuroConex for $127 million. This transaction resulted in a $62 million after-tax gain ($98 million pretax).

In 2005, Citigroup sold its U.S. merchant acquiring business, Citigroup Payment Service Inc., to First Data Corporation for $70 million, resulting in a $41 million after-tax gain ($61 million pretax).

Homeland Investment Act Benefit

The Company’s 2005 full-year results from continuing operations include a $198 million tax benefit from the Homeland Investment Act provision of the American Jobs Creation Act of 2004, net of the impact of remitting income earned in 2005 and prior years that would otherwise have been indefinitely invested overseas. The amount of dividends that were repatriated relating to this benefit was approximately $3.2 billion.

Copelco Litigation Settlement

In 2000, Citigroup purchased Copelco Capital, Inc., a leasing business, from Itochu International Inc. and III Holding Inc. (formerly known as Copelco Financial Services Group, Inc., collectively referred to herein as “Itochu”) for $666 million. During 2001, Citigroup filed a lawsuit asserting breach of representations and warranties, among other causes of action, under the Stock Purchase Agreement entered into between Citigroup and Itochu in March 2000. During the third quarter of 2005, Citigroup and Itochu signed a settlement agreement that mutually released all claims, and under which Itochu paid Citigroup $185 million, which was recorded in pretax income.

Mexico Value Added Tax (VAT) Refund

In 2005, Citigroup Mexico received a $182 million refund of VAT taxes from the Mexican government related to the 2003 and 2004 tax years as a result of a Mexico Supreme Court ruling. The refund was recorded as a reduction of $140 million (pretax) in Other operating expense and $42 million (pretax) in Other revenue.

Settlement of Enron Class Action Litigation

As described in the “Legal Proceedings” discussion on page 195, in 2005, Citigroup settled class action litigation brought on behalf of purchasers of Enron securities.

Settlement of the Securities and Exchange Commission’s Transfer Agent Investigation

In 2005, the Company settled an investigation by the Securities and Exchange Commission (SEC) into matters relating to arrangements between certainSmith Barney mutual funds (the Funds), an affiliated transfer agent, and an unaffiliated sub-transfer agent.

Under the terms of the settlement, Citigroup paid a total of $208 million, consisting of $128 million in disgorgement and $80 million in penalties. These funds, less $24 million already credited to the Funds, have been paid to the U.S. Treasury and will be distributed pursuant to a distribution plan prepared by Citigroup and to be approved by the SEC. The terms of the settlement had been fully reserved by Citigroup in prior periods.

14

Merger of Bank Holding Companies

In 2005, Citigroup merged its two intermediate bank holding companies, Citigroup Holdings Company and Citicorp, into Citigroup Inc. Coinciding with this merger, Citigroup assumed all existing indebtedness and outstanding guarantees of Citicorp. See Note 28 on page 176.

Repositioning Charges

The Company recorded a $272 million after-tax ($435 million pretax) charge in 2005 for repositioning costs. The repositioning charges were predominantly severance-related costs recorded in CMB ($151 million after-tax) and in Global Consumer ($95 million after-tax). These repositioning actions were consistent with the Company’s objectives of controlling expenses while continuing to invest in growth opportunities.

Resolution of Glendale Litigation

During 2005, the Company recorded a $72 million after-tax gain ($114 million pretax) following the resolution ofGlendale Federal Bank v. United States, an action brought by Glendale Federal Bank.

Acquisition of First American Bank

In 2005, Citigroup completed the acquisition of First American Bank in Texas (FAB). The transaction established Citigroup’s retail branch presence in Texas, giving Citigroup 106 branches, $4.2 billion in assets and approximately 120,000 new customers in the state at the time of the transaction’s closing. The results of FAB are included in the Consolidated Financial Statements from March 2005 forward.

Divestiture of the Manufactured Housing Loan Portfolio

In 2005, Citigroup completed the sale of its manufactured housing loan portfolio, consisting of $1.4 billion in loans, to 21st Mortgage Corp. The Company recognized a $109 million after-tax loss ($157 million pretax) in the divestiture.

Divestiture of CitiCapital’s Transportation Finance Business

In 2005, the Company completed the sale of CitiCapital’s Transportation Finance Business based in Dallas and Toronto to GE Commercial Finance for total cash consideration of approximately $4.6 billion. The sale resulted in an after-tax gain of $111 million ($161 million pretax).

Shutdown of the Private Bank in Japan and Related Charge and Other Activities in Japan

On September 29, 2005, the Company officially closed itsPrivate Bank business inJapan.

In September 2004, the Financial Services Agency of Japan (FSA) issued an administrative order against Citibank Japan. This order included a requirement that Citigroup exit all private banking operations inJapan by September 30, 2005. In connection with this required exit, the Company established a $400 million ($244 million after-tax) reserve (the Exit Plan Charge) during 2004.

On October 25, 2004, Citigroup announced its decision to wind down Cititrust and Banking Corporation (Cititrust), a licensed trust bank inJapan, after concluding that there were internal control, compliance and governance issues in that subsidiary. On April 22, 2005, the FSA issued an administrative order requiring Cititrust to suspend from engaging in all new trust business in 2005. Cititrust closed all customer accounts in 2005.

15

SIGNIFICANT ACCOUNTING POLICIES AND SIGNIFICANT ESTIMATES

The Notes to the Consolidated Financial Statements on page 111 contain a summary of the Company’s significant accounting policies, including a discussion of recently issued accounting pronouncements. These policies, as well as estimates made by management, are integral to the presentation of the Company’s financial condition. It is important to note that they require management to make difficult, complex or subjective judgments and estimates, at times, regarding matters that are inherently uncertain. Management has discussed each of these significant accounting policies, the related estimates and its judgments with the Audit and Risk Management Committee of the Board of Directors. Additional information about these policies can be found in Note 1 to the Consolidated Financial Statements on page 111.

Valuations of Financial Instruments

The Company holds fixed income and equity securities, derivatives, retained interests in securitizations, investments in private equity and other financial instruments. In addition, the Company purchases securities under agreements to resell and sells securities under agreements to repurchase. The Company holds its investments, trading assets and liabilities, and resale and repurchase agreements on the balance sheet to meet customer needs, to manage liquidity needs and interest rate risks, and for proprietary trading and private equity investing.

Substantially all of these assets and liabilities are reflected at fair value on the Company’s balance sheet. In addition, certain loans, short-term borrowings, long-term debt and deposits as well as certain securities borrowed and loaned positions that are collateralized with cash are carried at fair value. In total, approximately 38.9% and 35.2% of assets, and 23.1% and 8.9% of liabilities, are accounted for at fair value as of December 31, 2007 and 2006, respectively. The increase is driven by the election of the fair value option as permitted under SFAS 159 for certain assets and liabilities, including securities purchased under agreements to resell and securities sold under agreements to repurchase, as well as certain structured and non-structured liabilities.

When available, the Company generally uses quoted market prices to determine fair value, and classifies such items within Level 1 of the fair value hierarchy. If quoted market prices are not available, fair value is based upon internally developed valuation models that use, where possible, current market-based or independently sourced market parameters, such as interest rates, currency rates, option volatilities, etc. More than 800 models are used across Citigroup. Where a model is internally developed and used to price a significant product, it is subject to validation and testing by independent personnel. Such models are often based on a discounted cash flow analysis.

Items valued using such internally generated valuation techniques are classified according to the lowest level input or value driver that is significant to the valuation. Thus, an item may be classified in Level 3 even though there may be some significant inputs that are readily observable.

As seen during the second half of 2007, the credit crisis has caused some markets to become illiquid, thus reducing the availability of certain observable data used by the Company’s valuation techniques. When or if the

liquidity returns to these markets, the valuations will revert to using the related observable inputs in verifying internally calculated values.

With the Company’s early adoption of SFAS 157 and SFAS 159 as of January 1, 2007, the following specific changes were made in the valuation of the Company’s financial assets and liabilities:

| | (i) | Amendments to the way that the probability of default of a counterparty is factored into the valuation of derivative positions and inclusion for the first time of the impact of Citigroup’s own-credit risk on the valuation of derivatives and other liabilities measured at fair value; |

| | (ii) | Elimination of the derivatives portfolio servicing adjustment which is no longer necessary under SFAS 157; |

| | (iii) | Block discounts for large holdings of publicly traded equity securities were discontinued; and |

| | (iv) | Trade-date gains related to certain derivatives using unobservable inputs were recognized immediately, superseding the previous guidance, which prohibited the recognition of these day-one gains. |

The cumulative effect of these changes totaled $325 million after-tax. $250 million, which related to the first two items above and was recorded as an increase in the current year’s earnings. The remaining $75 million, related to items (iii) and (iv) above and was recorded as an increase to January 1, 2007 opening Retained earnings.

Changes in the valuation of the trading assets and liabilities, as well as all other assets (excluding available-for-sale securities) and liabilities, carried at fair value, are recorded in the Consolidated Statement of Income. Changes in the valuation of available-for-sale securities generally are recorded in Accumulated other comprehensive income, which is a component of stockholders’ equity on the Consolidated Balance Sheet. A full description of the Company’s related policies and procedures can be found in Notes 1, 26 and 27 to the Consolidated Financial Statements on pages 111, 167 and 176, respectively.

Key Controls over Fair-Value Measurement

The Company’s processes include a number of key controls that are designed to ensure that fair value is measured appropriately. Such controls include a model validation policy requiring that valuation models be validated by qualified personnel independent from those who created the models and escalation procedures to ensure that valuations using unverifiable inputs are identified and monitored on a regular basis by senior management.

Allowance for Credit Losses

Management provides reserves for an estimate of probable losses inherent in the funded loan portfolio on the balance sheet in the form of an allowance for loan losses. In addition, management has established and maintains reserves for the potential credit losses related to the Company’s off-balance- sheet exposures of unfunded lending commitments, including standby letters of credit and guarantees. These reserves are established in accordance with Citigroup’s Loan Loss Reserve Policies, as approved by the Audit and Risk Management Committee of the Company’s Board of Directors. The

16

Company’s Chief Risk Officer and Chief Financial Officer review the adequacy of the credit loss reserves each quarter with representatives from the Risk and Finance staffs for each applicable business area.

During these reviews, the above-mentioned representatives covering the business area having classifiably managed portfolios (that is, portfolios where internal credit-risk ratings are assigned, which are primarily Markets & Banking, Global Consumer’s commercial lending businesses, and Global Wealth Management) present recommended reserve balances for their funded and unfunded lending portfolios along with supporting quantitative and qualitative data. The quantitative data include:

| • | | Estimated probable losses for non-performing, non-homogeneous exposures within a business line’s classifiably managed portfolio. Consideration is given to all available evidence when determining this estimate including, as appropriate: (i) the present value of expected future cash flows discounted at the loan’s contractual effective rate; (ii) the borrower’s overall financial condition, resources and payment record; and (iii) the prospects for support from financially responsible guarantors or the realizable value of any collateral. |

| • | | Statistically calculated losses inherent in the classifiably managed portfolio for performing and de minimis non-performing exposures. The calculation is based upon: (i) Citigroup’s internal system of credit-risk ratings, which are analogous to the risk ratings of the major rating agencies; (ii) the Corporate portfolio database; and (iii) historical default and loss data, including rating agency information regarding default rates from 1983 to 2006, and internal data, dating to the early 1970s, on severity of losses in the event of default. |

| • | | Additional adjustments include: (i) statistically calculated estimates to cover the historical fluctuation of the default rates over the credit cycle, the historical variability of loss severity among defaulted loans, and the degree to which there are large obligor concentrations in the global portfolio; and (ii) adjustments made for specifically known items, such as current environmental factors and credit trends. |

In addition, representatives from both the Risk Management and Finance staffs that cover business areas which have delinquency-managed portfolios containing smaller homogeneous loans (primarily Global Consumer’s non-commercial lending areas) present their recommended reserve balances based upon leading credit indicators including delinquencies on first and second mortgages and deterioration in the housing market, a downturn in other economic trends including unemployment and GDP, changes in the portfolio size, and a change in the estimated loan losses inherent in the portfolio but not yet visible in the delinquencies (change in estimate of loan losses). This methodology is applied separately for each individual product within each different geographic region in which these portfolios exist.

This evaluation process is subject to numerous estimates and judgments. The frequency of default, risk ratings, loss recovery rates, the size and diversity of individual large credits, and the ability of borrowers with foreign currency obligations to obtain the foreign currency necessary for orderly debt servicing, among other things, are all taken into account during this review. Changes in these estimates could have a direct impact on the credit costs in any quarter and could result in a change in the allowance. Changes to the reserve flow through the income statement on the lines “provision for loan losses” and “provision for unfunded lending commitments.” For a further description of the loan loss reserve and related accounts, see Notes 1 and 18 to the Consolidated Financial Statements on pages 111 and 147, respectively.

Securitizations

The Company securitizes a number of different asset classes as a means of strengthening its balance sheet and to access competitive financing rates in the market. Under these securitization programs, assets are sold into a trust and used as collateral by the trust as a means of obtaining financing. The cash flows from assets in the trust service the corresponding trust securities. If the structure of the trust meets certain accounting guidelines, trust assets are treated as sold and no longer reflected as assets of the Company. If these guidelines are not met, the assets continue to be recorded as the Company’s assets, with the financing activity recorded as liabilities on Citigroup’s balance sheet.

The Financial Accounting Standards Board (FASB) is currently working on amendments to the accounting standards governing asset transfers and securitization accounting. Upon completion of these standards, the Company will need to re-evaluate its accounting and disclosures. The SEC has requested that FASB complete its deliberations by the end of 2008. Due to the FASB’s ongoing deliberations, the Company is unable to accurately determine the effect of future amendments at this time.

The Company assists its clients in securitizing their financial assets and also packages and securitizes financial assets purchased in the financial markets. The Company may also provide administrative, asset management, underwriting, liquidity facilities and/or other services to the resulting securitization entities, and may continue to service some of these financial assets.

A complete description of the Company’s accounting for securitized assets can be found in “Off-Balance-Sheet Arrangements” on page 85 and in Notes 1 and 23 to the Consolidated Financial Statements on pages 111 and 156, respectively.

Income Taxes

The Company is subject to the income tax laws of the U.S., its states and municipalities and those of the foreign jurisdictions in which the Company operates. These tax laws are complex and subject to different interpretations by the taxpayer and the relevant governmental taxing authorities. In establishing a provision for income tax expense, the Company must make judgments and interpretations about the application of these inherently complex tax laws. The Company must also make estimates about when in the future certain items will affect taxable income in the various tax jurisdictions, both domestic and foreign.

Disputes over interpretations of the tax laws may be subject to review/adjudication by the court systems of the various tax jurisdictions or may be settled with the taxing authority upon examination or audit.

The Company implemented FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes” (FIN 48), on January 1, 2007, which sets out a consistent framework to determine the appropriate level of tax reserves to maintain for uncertain tax positions. See Note 11 to the Consolidated Financial Statements on page 139.

17

The Company treats interest and penalties on income taxes as a component of income tax expense.

Deferred taxes are recorded for the future consequences of events that have been recognized for financial statements or tax returns, based upon enacted tax laws and rates. Deferred tax assets are recognized subject to management’s judgment that realization is more likely than not.

See Note 11 to the Consolidated Financial Statements on page 139 for a further description of the Company’s provision and related income tax assets and liabilities.

Legal Reserves