FREEPORT-McMoRan COPPER & GOLD INC.

SELECTED FINANCIAL AND OPERATING DATA

| Years Ended December 31, | 2004 | 2003 | 2002 | 2001 | 2000 | ||||||||||

FCXCONSOLIDATED FINANCIAL DATA | (Financial Data in Dollars, Except Average Shares, and in Thousands, Except Per Share Amounts) | ||||||||||||||

| Revenues | $ | 2,371,866 | $ | 2,212,165 | $ | 1,910,462 | $ | 1,838,866 | $ | 1,868,610 | |||||

| Operating income | 703,576 | a | 823,308 | 640,137 | 542,926 | 492,293 | |||||||||

| Net income before cumulative effect of changes in accounting principles | 156,776 | b | 169,812 | c | 130,099 | 76,496 | 39,500 | ||||||||

| Cumulative effect of changes in accounting principles, net | - | (15,593 | )d | (3,049 | )e | - | - | ||||||||

| Net income applicable to common stock | 156,776 | b | 154,219 | c | 127,050 | 76,496 | 39,500 | ||||||||

| Pro forma net income, assuming accounting changes are applied retroactively | 156,776 | b | 169,307 | c, d | 129,635 | 104,847 | 42,610 | ||||||||

| Basic net income per common share | 0.86 | 0.99 | 0.88 | 0.53 | 0.26 | ||||||||||

| Diluted net income per common share: | |||||||||||||||

| Applicable to common stock | 0.85 | b | 0.97 | c, d | 0.87 | 0.53 | 0.26 | ||||||||

| Pro forma, assuming accounting changes are applied retroactively | 0.85 | b | 1.06 | c, d | 0.89 | 0.72 | 0.28 | ||||||||

| Dividends paid per common share | 1.10 | 0.27 | - | - | - | ||||||||||

| Basic average shares outstanding | 182,272 | 155,805 | 144,649 | 143,952 | 153,997 | ||||||||||

| Diluted average shares outstanding | 184,923 | 159,102 | 146,418 | 144,938 | 154,519 | ||||||||||

| At December 31: | |||||||||||||||

| Cash and restricted cash and investments | 551,950 | 498,616 | 115,782 | 149,475 | 7,968 | ||||||||||

| Property, plant, equipment and development costs, net | 3,199,292 | 3,261,697 | 3,320,561 | 3,409,687 | 3,230,564 | ||||||||||

| Total assets | 5,086,995 | 4,718,366 | 4,192,193 | 4,211,929 | 3,950,741 | ||||||||||

| Long-term debt, including current portion and short-term borrowings | 1,951,906 | 2,228,330 | d | 2,038,390 | 2,338,600 | 2,190,025 | |||||||||

| Redeemable preferred stock | - | - | d | 450,003 | 462,504 | 475,005 | |||||||||

| Stockholders’ equity | 1,163,649 | 775,984 | 266,826 | 104,444 | 37,931 | ||||||||||

PT FREEPORT INDONESIA OPERATING DATA, Net of Rio Tinto’s Interest | |||||||||||||||

| Copper (recoverable) | |||||||||||||||

| Production (000s of pounds) | 996,500 | 1,291,600 | 1,524,200 | 1,393,400 | 1,388,100 | ||||||||||

| Production (metric tons) | 452,000 | 585,900 | 691,400 | 632,000 | 629,600 | ||||||||||

| Sales (000s of pounds) | 991,600 | 1,295,600 | 1,522,300 | 1,399,100 | 1,393,700 | ||||||||||

| Sales (metric tons) | 449,800 | 587,700 | 690,500 | 634,600 | 632,200 | ||||||||||

| Average realized price per pound | $1.37 | $0.82 | $0.71 | $0.69 | $0.82 | ||||||||||

| Gold (recoverable ounces) | |||||||||||||||

| Production | 1,456,200 | 2,463,300 | 2,296,800 | 2,634,900 | 1,899,500 | ||||||||||

| Sales | 1,443,000 | 2,469,800 | 2,293,200 | 2,644,800 | 1,921,400 | ||||||||||

| Average realized price per ounce | $412.32 | $366.60 | f | $311.97 | $269.24 | $276.06 | |||||||||

| Silver (recoverable ounces) | |||||||||||||||

| Production | 3,270,700 | 4,112,700 | 4,121,100 | 3,771,500 | 3,542,400 | ||||||||||

| Sales | 3,257,800 | 4,126,700 | 4,116,100 | 3,782,600 | 3,542,300 | ||||||||||

| Average realized price per ounce | $6.10 | $5.15 | $4.66 | $4.80 | $4.98 | ||||||||||

ATLANTIC COPPER OPERATING DATA | |||||||||||||||

| Concentrate and scrap treated (metric tons) | 768,100 | 964,400 | 1,016,700 | 891,100 | 916,300 | ||||||||||

| Anodes | |||||||||||||||

| Production (000s of pounds) | 494,400 | 640,000 | 657,000 | 617,300 | 639,100 | ||||||||||

| Production (metric tons) | 224,300 | 290,300 | 298,000 | 280,000 | 289,900 | ||||||||||

| Sales (000s of pounds) | 36,700 | 97,000 | 101,200 | 87,500 | 80,600 | ||||||||||

| Sales (metric tons) | 16,600 | 44,000 | 45,900 | 39,700 | 36,600 | ||||||||||

| Cathodes | |||||||||||||||

| Production (000s of pounds) | 454,700 | 544,700 | 552,200 | 518,700 | 567,900 | ||||||||||

| Production (metric tons) | 206,200 | 247,100 | 250,500 | 235,300 | 257,600 | ||||||||||

| Sales (including wire rod and wire) | |||||||||||||||

| (000s of pounds) | 479,200 | 546,800 | 556,500 | 549,800 | 562,300 | ||||||||||

| (metric tons) | 217,400 | 248,000 | 252,400 | 249,400 | 255,100 | ||||||||||

| Gold sales in anodes and slimes (ounces) | 316,700 | 929,700 | 813,900 | 831,300 | 605,700 | ||||||||||

Cathode cash production cost per pound before hedgingg | $0.25 | $0.16 | $0.12 | $0.14 | $0.11 | ||||||||||

18

FREEPORT-McMoRan COPPER & GOLD INC. | |||||||||||||||

SELECTED FINANCIAL AND OPERATING DATA | |||||||||||||||

| 2004 | 2003 | 2002 | 2001 | 2000 | |||||||||||

PT SMELTING OPERATING DATA, 25%-Owned by PT Freeport Indonesia | |||||||||||||||

| Concentrate treated (metric tons) | 758,100 | 824,800 | 719,600 | 702,900 | 582,200 | ||||||||||

| Anodes | |||||||||||||||

| Production (000s of pounds) | 466,500 | 545,500 | 465,700 | 479,400 | 383,200 | ||||||||||

| Production (metric tons) | 211,600 | 247,400 | 211,200 | 217,500 | 173,800 | ||||||||||

| Sales (000s of pounds) | 2,300 | 64,600 | 33,000 | 10,100 | 33,100 | ||||||||||

| Sales (metric tons) | 1,000 | 29,300 | 15,000 | 4,600 | 15,000 | ||||||||||

| Cathodes | |||||||||||||||

| Production (000s of pounds) | 464,000 | 492,400 | 424,100 | 468,400 | 349,200 | ||||||||||

| Production (metric tons) | 210,500 | 223,300 | 192,400 | 212,500 | 158,400 | ||||||||||

| Sales (000s of pounds) | 462,900 | 493,500 | 424,100 | 468,800 | 349,700 | ||||||||||

| Sales (metric tons) | 210,000 | 223,800 | 192,400 | 212,600 | 158,600 | ||||||||||

Cathode cash production cost per poundg | $0.12 | $0.10 | $0.14 | $0.12 | $0.13 | ||||||||||

PT FREEPORT INDONESIA, 100% Aggregate Operating Data | |||||||||||||||

| Ore milled (metric tons per day) | 185,100 | 203,000 | 235,600 | 237,800 | 223,500 | ||||||||||

| Average ore grade | |||||||||||||||

| Copper (percent) | .87 | 1.09 | 1.14 | 1.00 | 1.07 | ||||||||||

| Gold (grams per metric ton) | .88 | 1.54 | 1.24 | 1.41 | 1.10 | ||||||||||

| Gold (ounce per metric ton) | .028 | .050 | .040 | .045 | .035 | ||||||||||

| Silver (grams per metric ton) | 3.85 | 4.03 | 3.60 | 3.20 | 2.97 | ||||||||||

| Silver (ounce per metric ton) | .124 | .130 | .116 | .103 | .095 | ||||||||||

| Recovery rates (percent) | |||||||||||||||

| Copper | 88.6 | 89.0 | 88.5 | 86.9 | 88.2 | ||||||||||

| Gold | 81.8 | 87.3 | 88.4 | 89.5 | 84.3 | ||||||||||

| Silver | 56.8 | 61.3 | 61.3 | 59.0 | 60.0 | ||||||||||

| Copper (recoverable) | |||||||||||||||

| Production (000s of pounds) | 1,098,600 | 1,522,900 | 1,839,000 | 1,594,200 | 1,636,700 | ||||||||||

| Production (metric tons) | 498,300 | 690,800 | 834,200 | 723,100 | 742,400 | ||||||||||

| Sales (000s of pounds) | 1,092,700 | 1,527,700 | 1,836,800 | 1,600,900 | 1,643,500 | ||||||||||

| Sales (metric tons) | 495,600 | 693,000 | 833,200 | 726,200 | 745,500 | ||||||||||

| Gold (recoverable ounces) | |||||||||||||||

| Production | 1,536,600 | 3,163,900 | 2,938,800 | 3,488,100 | 2,362,600 | ||||||||||

| Sales | 1,523,600 | 3,171,500 | 2,934,000 | 3,498,300 | 2,387,300 | ||||||||||

| Silver (recoverable ounces) | |||||||||||||||

| Production | 3,873,800 | 4,978,600 | 4,922,900 | 4,264,300 | 3,833,200 | ||||||||||

| Sales | 3,857,500 | 4,994,000 | 4,916,000 | 4,280,400 | 3,847,700 | ||||||||||

The selected consolidated financial data shown above is derived from our audited consolidated financial statements. These historical results are not necessarily indicative of results that you can expect for any future period. You should read this data in conjunction with management’s discussion and analysis and our full consolidated financial statements and notes thereto contained in this annual report.

| a. | Includes a $95.0 million gain on insurance settlement related to the fourth-quarter 2003 slippage and debris flow events at the Grasberg open pit and a $12.0 million charge related to Atlantic Copper’s workforce reduction plan. |

| b. | Includes a $48.8 million ($0.26 per share) gain on insurance settlement related to the fourth-quarter 2003 slippage and debris flow events at the Grasberg open pit; a $20.4 million ($0.11 per share) gain from the sale of a parcel of land in Arizona held by an FCX joint venture; a $7.5 million ($0.04 per share) gain from Atlantic Copper’s sale of its wire rod and wire assets; a $12.0 million ($0.06 per share) charge related to Atlantic Copper’s workforce reduction plan; $13.8 million ($0.07 per share) of losses on early extinguishment and conversion of debt; and a $6.3 million ($0.03 per share) gain on reduction of interest expense for conversion of debt. |

| c. | Includes losses on early extinguishment and conversion of debt totaling $31.9 million ($0.20 per share). |

| d. | Effective January 1, 2003, we adopted Statement of Financial Accounting Standards (SFAS) No. 143, “Accounting for Asset Retirement Obligations,” and recorded a $9.1 million ($0.06 per share) cumulative effect gain. Effective July 1, 2003, we adopted SFAS No. 150, “Accounting for Certain Financial Instruments with Characteristics of both Liabilities and Equity,” and recorded a $24.7 million ($0.16 per share) cumulative effect charge. Our mandatorily redeemable preferred stock was classified as debt effective July 1, 2003. SFAS No. 150 does not allow restatement of prior periods. |

| e. | Effective January 1, 2002, we changed our methodology used in the determination of depreciation associated with PT Freeport Indonesia’s mining and milling life-of-mine assets. |

| f. | Amount was $357.61 before hedging gain resulting from redemption of FCX’s Gold-Denominated Preferred Stock. |

| g. | For a reconciliation of cathode cash production costs per pound to production costs applicable to sales reported in FCX’s consolidated financial statements refer to “Product Revenues and Production Costs” in “Management’s Discussion and Analysis.” |

19

FREEPORT-McMoRan COPPER & GOLD INC.

MANAGEMENT'S DISCUSSION AND ANALYSIS

OVERVIEW

In management’s discussion and analysis, “we,” “us” and “our” refer to Freeport-McMoRan Copper & Gold Inc. (FCX) and its consolidated subsidiaries. References to “aggregate” amounts mean the total of our share and Rio Tinto plc’s share as our joint venture partner. The results of operations reported and summarized below are not necessarily indicative of future operating results. The following discussion should be read together with our consolidated financial statements and the related notes.

We have one of the world’s largest copper and gold mining and production operations in terms of reserves and production. We are also one of the lowest-cost copper producers in the world, after taking into account credits for related gold and silver production. Our principal asset is the Grasberg minerals district, which contains the largest single gold reserve and the second-largest copper reserves of any mine in the world.

We operate through our majority-owned subsidiaries, PT Freeport Indonesia and PT Puncakjaya Power (Puncakjaya Power), and through Atlantic Copper, S.A. (Atlantic Copper) and PT Irja Eastern Minerals (Eastern Minerals), our principal wholly owned subsidiaries. We acquired an 85.7 percent ownership in Puncakjaya Power in 2003. Puncakjaya Power’s sole business is to supply power to PT Freeport Indonesia’s operations (see Note 2 of “Notes to Consolidated Financial Statements”). Atlantic Copper’s operations are in Spain and involve the smelting and refining of copper concentrates and the marketing of refined copper products and precious metals in slimes. PT Freeport Indonesia owns a 25 percent interest in PT Smelting, an Indonesian company which operates a copper smelter and refinery in Gresik, Indonesia. Eastern Minerals conducts mineral exploration activities (which are currently suspended) in Papua, Indonesia.

PT Freeport Indonesia, our principal operating subsidiary, operates under an agreement, called a Contract of Work, with the Government of Indonesia. The Contract of Work allows us to conduct exploration, mining and production activities in a 24,700-acre area called Block A located in Papua, Indonesia. Under the Contract of Work, PT Freeport Indonesia also conducts exploration activities (which are currently suspended,but are under review for resumption) in an approximate 500,000-acre area called Block B in Papua. All of our proven and probable mineral reserves and current mining operations are located in Block A. Eastern Minerals holds an additional Contract of Work originally covering a 2.5-million-acre area. Under the terms of Eastern Minerals’ Contract of Work, we have already relinquished 1.3 million acres and must relinquish an additional 0.6 million acres at the end of the three-year exploration period, which can be extended by the Government of Indonesia for as much as two additional years.

In addition to the PT Freeport Indonesia and Eastern Minerals exploration acreage, we have the right to conduct other mineral exploration activities in Papua pursuant to a joint venture through PT Nabire Bakti Mining. Field exploration activities outside of our current mining operations in Block A have been suspended in recent years because of safety and security issues and regulatory uncertainty relating to a possible conflict between our mining and exploration rights in certain forest areas and an Indonesian Forestry law enacted in 1999 prohibiting open-pit mining in forest preservation areas. Recent Indonesian legislation permits open-pit mining in PT Freeport Indonesia’s Block B area, subject to certain requirements. We are currently assessing these requirements and security issues. The timing for our resumption of exploration activities in our Contract of Work areas outside of Block A depends on the resolution of these matters.

We own 90.64 percent of PT Freeport Indonesia, of which 9.36 percent is owned through our wholly owned subsidiary, PT Indocopper Investama. The Government of Indonesia owns the remaining 9.36 percent of PT Freeport Indonesia.In July 2004, we received a request from the Indonesian Department of Energy and Mineral Resources that we offer to sell to Indonesian nationals shares in PT Indocopper Investama at fair market value. In response to this request and in view of the potential benefits of having additional Indonesian ownership in our project, we have agreed to consider a potential sale of an interest in PT Indocopper Investama at fair market value. Neither our Contract of Work nor Indonesian law requires us to divest any portion of our ownership interest in PT Freeport Indonesia or PT Indocopper Investama.

Joint Ventures with Rio Tinto plc (Rio Tinto)

In 1996, we established joint ventures with Rio Tinto, an international mining company with headquarters in London, England. One joint venture covers PT Freeport Indonesia’s mining operations in Block A and gives Rio Tinto, through 2021, a 40 percent interest in certain assets and future production exceeding specified annual amounts of copper, gold and silver in Block A and, after 2021, a 40 percent interest in all production from Block A. The agreement provides for adjustments to the specified annual metal sharing amounts upon the occurrence of certain events that cause an extended interruption in production to occur, including events such as the fourth-quarter 2003 Grasberg open-pit slippage and debris flow.

Operating, nonexpansion capital and administrative costs are shared proportionately between PT Freeport Indonesia and Rio Tinto based on the ratio of (a) the incremental revenues from production from our expansion completed in 1998 to (b) total revenues from production from Block A, including production from PT Freeport Indonesia’s previously

20

existing reserves. PT Freeport Indonesia receives 100 percent of the cash flow from specified annual amounts of copper, gold and silver through 2021, calculated by reference to its proven and probable reserves as of December 31, 1994, and 60 percent of all remaining cash flow. As noted above, the specified annual amounts of copper, gold and silver attributable 100 percent to PT Freeport Indonesia are adjusted upon the occurrence of certain events. As a result of the Grasberg slippage and debris flow events, the 2004 specified amounts attributable 100 percent to PT Freeport Indonesia were reduced by 178 million pounds for copper and 280,000 ounces for gold. Pursuant to an agreement with Rio Tinto, these reductions are expected to be offset by increases in the specified amounts attributable 100 percent to PT Freeport Indonesia totaling 111 million pounds for copper and 175,000 ounces for gold in 2005, and 67 million pounds for copper and 105,000 ounces for gold in 2021.

Under our joint venture arrangements, Rio Tinto has a 40 percent interest in PT Freeport Indonesia’s Contract of Work and in Eastern Minerals’ Contract of Work. Rio Tinto also has the option to participate in 40 percent of any of our other future exploration projects in Papua. Rio Tinto has elected to participate in 40 percent of our interest and cost in the PT Nabire Bakti exploration joint venture covering approximately 0.5 million acres contiguous to Block B and one of Eastern Minerals’ blocks.

Outlook

In 2004, our sales volumes of copper and gold totaled 1.0 billion pounds of copper and 1.44 million ounces of gold. Our 2004 copper and gold sales volumes were lower than those reported for the last several years because of recovery efforts from the fourth-quarter 2003 slippage and debris flow events at the Grasberg open pit.

Following the October 9, 2003, slippage event and the December 12, 2003, debris flow in a section of the Grasberg open pit, PT Freeport Indonesia accelerated the removal of overburden and mined low grade ore prior to restoring safe access to higher-grade ore areas and resuming normal milling rates in June 2004. Average ore grades improved in the second half of 2004 and are expected to be significantly higher for 2005, compared with 2004. Annual sales are expected to approximate 1.5 billion pounds of copper and 2.9 million ounces of gold in 2005, increases of 50 percent for copper and 100 percent for gold compared with 2004. Assuming average copper prices of $1.35 per pound and average gold prices of $420 per ounce, consolidated operating cash flows in 2005 are expected to exceed $1.1 billion. The impact on our annual cash flow for each $0.10 per pound change in copper prices would approximate $75 million, including the effects of price changes on royalty costs and treatment charges, and for each $25 per ounce change in gold prices would approximate $36 million.

Average annual sales volumes over the next five years (2005 to 2009) are expected to approximate 1.36 billion pounds of copper and 2.2 million ounces of gold. Based on these estimates of average annual sales volumes over the next five years and copper prices of approximately $1.35 per pound and gold prices of approximately $420 per ounce, the impact on our annual cash flow for each $0.10 per pound change in copper prices would approximate $70 million, including the effects of price changes on royalty costs and treatment charges, and for each $25 per ounce change in gold prices would approximate $28 million.

Copper and Gold Markets

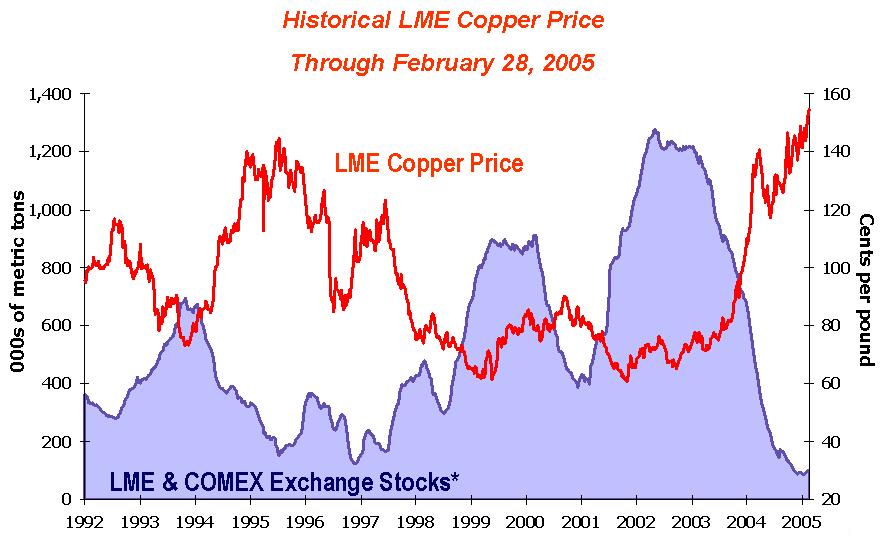

* Excludes Shanghai stocks, producer, consumer and merchant stocks.

The graph above presents London Metal Exchange (LME) copper prices and reported stocks of copper at the LME and New York Commodity Exchange (COMEX) through February 28, 2005. Copper markets have reflected strong demand from China, which has become the world’s largest consumer of copper, stronger U.S. industrial demand for copper and limited incremental supplies from mine production. Global demand for copper exceeded global production during 2003 and 2004, resulting in a significant decline in available inventories, with LME and COMEX inventories declining to levels of less than 100,000 metric tons, less than 10 percent of the available stocks at the beginning of 2003. Copper prices rose sharply beginning in mid-2003 and continued to increase in 2004, with prices ranging from $1.06 per pound to a multi-year high of $1.49 per pound in 2004. Copper prices have remained strong in early 2005 and the LME spot price closed at $1.54 per pound on February 28, 2005. As a result of low inventory levels, expectations of continued strong demand and limited supplies, the outlook for copper markets in 2005 is positive. Market analysts expect copper demand to exceed supply in the first half of 2005, with a possibility of a balance between refined copper supply and demand in the second half of the year. Future copper prices will be determined by demand from China, economic performance in the U.S. and other industrialized countries, the timing of the development of new supplies of copper, production levels of mines and copper smelters and other factors. We consider the underlying supply and demand conditions in the global copper markets to be positive for our company.

21

The positive market environment and investor sentiment toward gold continued during 2004 with gold prices ranging from $374 to $456 per ounce, supported by a weak U.S. dollar reflecting large U.S. deficits, ongoing geopolitical strife and terrorism concerns, growing investment demand for gold and actions by gold producers to reduce hedge positions. Gold prices averaged $410 per ounce in 2004. Recent movements in gold prices have closely followed movements in the U.S. dollar against other currencies and most analysts anticipate that a weak U.S. dollar will continue to support gold prices. The London gold price closed at approximately $435 per ounce on February 28, 2005.

As shown in the graphs above, world metal prices for copper have fluctuated during the period from 1992 through February 2005 from a low of approximately $0.60 per pound in 2001 to a high of approximately $1.54 per pound on February 28, 2005, and world gold prices have fluctuated during the period from 1998 through February 2005 from a low of approximately $250 per ounce in 1999 to a high of approximately $456 per ounce in 2004. Copper and gold prices are affected by numerous factors beyond our control as described further in our Form 10-K for the year ended December 31, 2004.

CRITICAL ACCOUNTING ESTIMATES

Management’s discussion and analysis of our financial condition and results of operations are based on our consolidated financial statements, which have been prepared in conformity with accounting principles generally accepted in the United States. The preparation of these statements requires that we make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses. We base these estimates on historical experience and on assumptions that we consider reasonable under the circumstances; however, reported results could differ from those based on the current estimates under different assumptions or conditions. The areas requiring the use of management’s estimates are discussed in Note 1 of “Notes to Consolidated Financial Statements” under the subheading “Use of Estimates.” Management has reviewed the following discussion of its development and selection of critical accounting estimates with the Audit Committee of our Board of Directors.

| · | Depreciation and Amortization - As discussed in Note 1 of “Notes to Consolidated Financial Statements,” we depreciate our mining and milling assets using the unit-of-production method based on our estimates of our proven and probable recoverable copper reserves. We have other assets that we depreciate on a straight-line basis over their estimated useful lives. Our estimates of proven and probable recoverable copper reserves and of the useful lives of our straight-line assets impact our depreciation and amortization expense. These estimates affect both our “mining and exploration” and “smelting and refining” segments. |

Effective January 1, 2002, we changed our method of computing depreciation for PT Freeport Indonesia’s mining and milling life-of-mine assets. See Note 1 of “Notes to Consolidated Financial Statements” for a discussion of this change. The cumulative effect of this change through December 31, 2001, as reflected in our 2002 results, reduced net income by $3.0 million ($0.02 per share), net of taxes and minority interest sharing.

The accounting estimates related to depreciation and amortization are critical accounting estimates because (1) the determination of copper reserves involves uncertainties with respect to the ultimate geology of our reserves and the assumptions used in determining the economic feasibility of mining those reserves, including estimated copper and gold prices and costs of conducting future mining activities, and (2) changes in estimated proven and probable recoverable copper reserves and useful asset lives can have a material impact on net income. We perform annual assessments of our existing assets, including a review of asset costs and depreciable lives, in connection with the review of mine operating and development plans. When we determine that assigned asset lives do not reflect the expected remaining period of benefit, we make prospective changes to those depreciable lives.

There are a number of uncertainties inherent in estimating quantities of reserves, including many factors beyond our control. Ore reserves estimates are based upon engineering evaluations of samplings of drill holes and other openings. Our estimates of proven and probable recoverable reserves are prepared by our employees and reviewed and verified by independent experts in mining, geology and reserve determination. As of December 31, 2004, aggregate proven and probable recoverable copper reserves totaled 56.2 billion pounds and PT Freeport Indonesia’s estimated share totaled 40.5 billion pounds.

22

These estimates involve assumptions regarding future copper and gold prices, the geology of our mines, the mining methods we use and the related costs we incur to develop and mine our reserves. Changes in these assumptions could result in material adjustments to our reserve estimates, which could result in changes to unit-of-production depreciation and amortization expense in future periods, with corresponding adjustments to net income. If aggregate estimated copper reserves were 10 percent higher or lower at December 31, 2004, we estimate that our annual depreciation expense for 2005 would change by approximately $14 million, changing net income by approximately $7 million. Although some degree of variability is expected, we believe the extent of our technical data and operating experience - specifically as it relates to our Grasberg open-pit mine, which we have been mining for 15 years - mitigates the potential for significant changes in reserve estimates, especially as compared with mines that are undeveloped or newly developed.

As discussed in Note 1 of “Notes to Consolidated Financial Statements,” we review and evaluate our long-lived assets for impairment when events or changes in circumstances indicate that the related carrying amounts may not be recoverable. Changes to our estimates of proven and probable recoverable copper and gold reserves could have an impact on our assessment of asset impairment. However, we believe it is unlikely that revisions to our estimates of proven and probable recoverable copper and gold reserves would give rise to an impairment of our assets because of the significant size of our reserves in relation to our asset carrying values.

| · | Deferred Mining Costs - Mining costs are charged to operations as incurred. However, because of the configuration and location of the Grasberg ore body and the location and extent of surrounding overburden, the ratio of overburden to ore is much higher in the initial mining of the pit than in later years. As a result, surface mining costs associated with overburden removal at PT Freeport Indonesia’s Grasberg open-pit mine that are estimated to relate to future production are initially deferredwhen the ratio of actual overburden removed to ore mined exceeds the estimated average ratio of overburden to ore over the life of the Grasberg open-pit mine. Those deferred costs are subsequently charged to operating costs when the ratio of actual overburden removed to ore mined falls below the estimated average ratio of overburden removed to ore mined over the life of the Grasberg open-pit mine.We use the proven and probable ore reserves for the Grasberg open pit disclosed in the notes to our consolidated financial statements to calculate the estimated average ratio of overburden to ore over the life of the mine. |

The deferred mining cost method is used by some companies in the metals mining industry; however, industry practice varies. The Emerging Issues Task Force of the Financial Accounting Standards Board (FASB) currently is evaluating this issue. The deferred mining cost method matches the cost of production with the sale of the related metal from the open pit by assigning each metric ton of ore removed an equivalent amount of overburden tonnage, thereby averaging overburden removal costs over the life of the mine. The mining costs capitalized in inventory and the amounts charged to cost of goods sold do not represent the actual costs incurred to mine the ore in any given period. If we were to charge all mining costs to expense when incurred, including all overburden removal costs, as some mining companies do, there would be greater volatility in our period-to-period results of operations.

The application of the deferred mining cost method has resulted in an asset on our balance sheets (“Deferred Mining Costs”), which based on current mine plans, is estimated to continue to increase through about 2010. Subsequently,thesecosts are expected to begin to amortize as a charge to production and delivery costs until they are fully amortized at the end of the open pit’s life, which is estimated to be in approximately 2015. This is because PT Freeport Indonesia expects to mine higher than average amounts of overburden through 2010 and less than average thereafter. Deferred mining costs totaled $220.4 million at December 31, 2004, and $142.6 million at December 31, 2003. Additions to deferred mining costs are classified as increases in deferred mining costs in operating activities in our consolidated statements of cash flows and totaled $77.8 million in 2004, $64.4 million in 2003 and $30.6 million in 2002. We evaluate the recoverability of our deferred mining costs in conjunction with our evaluation of the recoverability of our mining assets. The Grasberg mine is currently our only producing open-pit mine.

The estimated average ratio of overburden to ore over the life of the Grasberg open pit used in our deferred mining costs calculation is a critical accounting estimate because (1) it is susceptible to change from period to period because it requires management to make assumptions about future mining activities and (2) changes could materially affect net income. Our mine plan is derived from a model that takes into consideration available geological data and determines the most efficient and cost-effective method of accessing the economic reserves. Significant assumptions underlying our mine plan include the amount of total overburden and ore we expect to move in a given

23

In the fourth quarter of 2004, PT Freeport Indonesia changed its life-of-mine overburden-to-ore ratio to 2.4 to 1 based on a recently completed annual assessment. PT Freeport Indonesia’s estimated life-of-mine overburden-to-ore ratio averaged 2.3 to 1 in 2004, 2.0 to 1 in 2003 and 1.8 to 1 in 2002. PT Freeport Indonesia’s geologists and engineers reassess the overburden-to-ore ratio and the remaining life of the Grasberg open-pit mine at least annually, and we reflect any changes in our estimates prospectively beginning in the quarter of change. We expect the estimated life-of-mine overburden-to-ore ratio to average 2.4 to 1 for 2005. The increases in the ratio over the last several years primarily relate to changes in the cutoff grade at the open pit caused by a reassessment of the optimal milling rate at our mill facilities including a greater proportional contribution to our total ore processed from our underground Deep Ore Zone mine.

If the life-of-mine overburden-to-ore ratio was 2.4 to 1, as in the fourth quarter of 2004, instead of the 2.2 to 1 ratio used through September 30, 2004, we estimate our deferral of mining costs for 2004 would have been $11.0 million lower and net income would have been $5.6 million ($0.03 per share) lower.

| · | Reclamation and Closure Costs - Our mining operations involve activities that have a significant effect on the surrounding area. Our reclamation and closure costs primarily involve treatment of acidic water (also known as acid rock drainage) created by overburden, reclamation and revegetation of a large area in the lowlands of Papua where mill tailings are deposited, reclamation of overburden stockpiles and decommissioning of operating assets. Through December 31, 2002, we had accrued $29.2 million for estimated closure and reclamation costs on a unit-of-production basis over our total estimated proven and probable recoverable copper reserves. For a discussion of the assumptions that we make to estimate proven and probable recoverable reserves, see “Depreciation and Amortization” above. |

Effective January 1, 2003, we adopted Statement of Financial Accounting Standards (SFAS) No. 143, “Accounting for Asset Retirement Obligations” (see Note 1 of “Notes to Consolidated Financial Statements”). SFAS No. 143 requires that we record the fair value of our estimated asset retirement obligations in the period incurred, with the cumulative effect of adopting SFAS No. 143 as of January 1, 2003, for all existing asset retirement obligations, asset retirement costs and related accumulated depreciation required to be reflected in earnings as a separate line item. The accounting estimates related to reclamation and closure costs are critical accounting estimates because (1) we will not incur most of these costs for a number of years, requiring us to make estimates over a long period; (2) reclamation and closure laws and regulations could change in the future or circumstances affecting our operations could change, either of which could result in significant changes to our current plans; (3) calculating the fair value of our asset retirement obligations in accordance with SFAS No. 143 requires management to assign probabilities to projected cash flows, to make long-term assumptions about inflation rates, to determine our credit-adjusted, risk-free interest rates and to determine market risk premiums that are appropriate for our operations; and (4) given the magnitude of our estimated reclamation and closure costs, changes in any or all of these estimates could have a material impact on net income.

In 2002, we engaged an independent environmental consulting and auditing firm to assist in estimating PT Freeport Indonesia’s aggregate asset retirement obligations, and worked with other consultants in estimating Atlantic Copper’s asset retirement obligations. We estimated these obligations using an expected cash flow approach, in which multiple cash flow scenarios were used to reflect a range of possible outcomes. We estimated these aggregate obligations to be approximately $120 million for PT Freeport Indonesia and $17 million for Atlantic Copper. To calculate the fair value of these obligations, we applied an estimated long-term inflation rate of 2.5 percent, except for Indonesian rupiah-denominated labor costs with respect to PT Freeport Indonesia’s obligations, for which an estimated inflation rate of 9.0 percent was applied. The projected cash flows were discounted at our estimated credit-adjusted, risk-free interest rates which ranged from 9.4 percent to 12.6 percent for the corresponding time periods over which these costs would be incurred. The inflation rates and discount rates we used to calculate the fair value of PT Freeport Indonesia’s asset retirement obligation are critical factors in the calculation of future value and discounted

24

present value costs. An increase of one percent in the inflation rates used results in an approximate 17 percent increase in the discounted present value costs. A decrease of one percent in the discount rates used has a similar effect resulting in an approximate 16 percent increase in the discounted present value costs. After discounting the projected cash flows, a market risk premium of 10 percent was applied to the total to reflect what a third party might require to assume these asset retirement obligations. The market risk premium was based on market-based estimates of rates that a third party would have to pay to insure its exposure to possible future increases in the value of these obligations.

At January 1, 2003, we estimated the fair value of our aggregate asset retirement obligations to be $28.5 million. We recorded the fair value of these obligations and the related additional assets as of January 1, 2003. The net difference between our previously recorded reclamation and closure cost liability and the amounts estimated under SFAS No. 143, after taxes and minority interest, resulted in a gain of $9.1 million (after reduction by $8.5 million for taxes and minority interest sharing), $0.06 per share on a diluted basis, which was recognized as a cumulative effect adjustment for a change in accounting principle. As a result of adopting SFAS No. 143, we expect our future depreciation and amortization expense to be lower and our production costs to be higher, with no significant net impact on earnings for the near term.

The effect of adopting SFAS No. 143 was to increase net income by approximately $1 million, $0.01 per share for 2003. Had we followed SFAS No. 143 during 2002, net income would have increased by approximately $0.5 million or less than $0.01 per share.

At December 31, 2004 and 2003, PT Freeport Indonesia revised its estimates for (1) changes in the projected timing of certain reclamation costs because of the slippage and debris flow events in the Grasberg open pit, (2) changes in certain cost estimates, and (3) additional asset retirement obligations incurred during 2003. We estimated PT Freeport Indonesia’s aggregate asset retirement obligations to be about $149 million at December 31, 2004, and $130 million at December 31, 2003. An analysis of PT Freeport Indonesia’s discounted asset retirement obligation follows (in millions):

| 2004 | 2003 | |||||

| Asset retirement obligation at beginning of year | $ | 25.7 | $ | 27.9 | ||

| Accretion expense | 2.8 | 2.7 | ||||

| Revisions for changes in estimates | (6.5 | ) | (4.3 | ) | ||

| Liabilities incurred | - | 0.6 | ||||

| Liabilities settled | - | (1.2 | ) | |||

| Asset retirement obligation at end of year | $ | 22.0 | $ | 25.7 | ||

The expected deferral of certain costs was the primary change in estimates that caused the decline in the obligation balance over the last two years. These changesreduced the related asset balance and are not expected to have a material impact on future net income.

CONSOLIDATED RESULTS OF OPERATIONS

Consolidated revenues include PT Freeport Indonesia’s sale of copper concentrates, which also contain significant quantities of gold and silver, and the sale by Atlantic Copper of copper anodes, cathodes, wire and wire rod, and gold in anodes and slimes. Consolidated revenues and net income vary significantly with fluctuations in the market prices of copper and gold and other factors. PT Freeport Indonesia’s intercompany sales to Atlantic Copper are eliminated in consolidation. Consolidated revenues were $2.4 billion for 2004, compared with $2.2 billion for 2003, reflecting significantly higher copper and gold prices partly offset by lower- grade ore and reduced mill throughput as PT Freeport Indonesia accelerated the removal of overburden and mined low-grade ore prior to restoring safe access to the higher-grade ore areas in its Grasberg open-pit mine following the fourth-quarter 2003 slippage and debris flow events (see “Mining and Exploration Operations - PT Freeport Indonesia Operating Results”). Atlantic Copper’s 2004 revenues were adversely affected by its scheduled major maintenance turnaround (see “Smelting and Refining Operations - Atlantic Copper Operating Results”) partly offset by higher copper and gold prices. Consolidated revenues in 2003 benefited from higher copper and gold price realizations and higher gold sales volumes, partly offset by lower copper sales volumes when compared with 2002 revenues of $1.9 billion.

Consolidated production and delivery costs were higher in 2004 at $1,450.3 million compared with $1,071.3 million for 2003 and $938.5 million for 2002. The increase in 2004 was primarily because of higher costs of concentrate purchases at Atlantic Copper caused by higher metals prices, higher production costs at PT Freeport Indonesia and the costs of Atlantic Copper’s smelter turnaround. Production and delivery costs in 2003 were higher than in 2002 primarily because of higher concentrates costs at Atlantic Copper caused by the increase in copper and gold prices during the year. Consolidated depreciation and amortization expense was $206.4 million in 2004, $230.8 million in 2003 and $260.4 million in 2002. Depreciation and amortization expense decreased each year during the last three years primarily because a large portion of our depreciation is calculated on a unit-of-production basis and our copper sales volumes at PT Freeport Indonesia declined each year.

Exploration expenses increased to $8.7 million in 2004, from $6.4 million in 2003 and $3.1 million in 2002, reflecting increased exploration drilling in Block A. Our 2004 drilling

25

efforts resulted in additions to our proven and probable reserves as of December 31, 2004 (see “Exploration and Reserves”). All approved exploration costs in the joint venture areas with Rio Tinto are generally shared 60 percent by us and 40 percent by Rio Tinto. The FCX/Rio Tinto joint ventures’ 2005 exploration budgets total approximately $21 million ($15 million for our share).

Consolidated general and administrative expenses increased to $89.9 million in 2004 from $80.3 million in 2003. General and administrative expenses for 2004 include a $2.2 million charge for Atlantic Copper’s workforce reduction plan (see “Smelting and Refining Operations”). The cost of our outstanding stock appreciation rights varies with the price of our common stock price, resulting in increases in general and administrative expenses totaling $0.5 million in 2004 and $7.3 million in 2003. Our parent company charges PT Freeport Indonesia for the in-the-money value of exercised employee stock options. These charges are eliminated in consolidation; however, PT Freeport Indonesia shares these charges with Rio Tinto and Rio Tinto’s reimbursements reduce our consolidated general and administrative expenses. General and administrative expenses are net of Rio Tinto’s share of joint venture reimbursements for employee stock option exercises, which reduced general and administrative expenses by $7.0 million in 2004 and $11.3 million in 2003. In addition, in accordance with our joint venture agreement, Rio Tinto’s percentage share of general and administrative expenses in 2004 was lower because of lower metal sales volumes. Estimated general and administrative expenses for 2005 are expected to approximate the 2004 level before consideration of the new accounting rules for share-based payments discussed in “New Accounting Standards.”

General and administrative expenses increased by $12.0 million to $80.3 million in 2003 from $68.3 million in 2002. The increase relates to charges for costs associated with stock appreciation rights caused by an increase in our stock price, higher compensation and other costs. As a percentage of revenues, general and administrative expenses were 3.8 percent in 2004 and 3.6 percent in 2003 and 2002.

PT Freeport Indonesia maintains property damage and business interruption insurance related to its operations. In December 2004, we entered into an insurance settlement agreement and settled all claims that arose from the fourth-quarter 2003 slippage and debris flow events in the Grasberg open-pit mine.Our insurers agreed to pay us an aggregate of $125.0 million, inclusive of interest and the $20.0 million paid to us in the third quarter of 2004, in connection with our claims.After considering our joint venture partner’s interest in the proceeds, PT Freeport Indonesia’s share of proceeds totaled $95.0 million. As a result of the settlement, we recorded in our Consolidated Statements of Income an $87.0 million gain on insurance settlement for the business interruption recovery and an $8.0 million gain to production costs for the property loss recovery for a net gain of $48.8 million ($0.26 per share), after taxes and minority interest sharing, in 2004.

Total consolidated interest cost (before capitalization) was $151.0 million in 2004, $200.0 million in 2003 and $183.4 million in 2002. Interest costs decreased in 2004 primarily because we reduced average debt levels, including early conversions in 2003 and 2004 of all of the $603.8 million of our 8¼% Convertible Senior Notes into 42.2 million shares of common stock (see Note 5 of “Notes to Consolidated Financial Statements” and “Capital Resources and Liquidity - Financing Activities”). Interest cost increased in 2003 compared to 2002, primarily because of higher average interest rates for our senior notes issued in early 2003 and higher average annual debt levels. Our interest cost for 2005 is expected to be about the same as 2004 unless we elect to prepay certain long-term debt. Capitalized interest totaled $2.9 million in 2004, $3.0 million in 2003 and $12.2 million in 2002. The reduction in capitalized interest in 2003 compared to 2002 reflects the completion of initial development activities at the Deep Ore Zone underground mine in early 2003.

Losses on early extinguishment and conversion of debt in 2004 ($14.0 million) and 2003 ($34.6 million) primarily resulted from the early conversions of our 8¼% Convertible Senior Notes. Gains on sales of assets totaled $28.8 million in 2004 as a result of two transactions. In November 2004, a joint venture in which we own a 50 percent interest completed the sale to a real estate developer of a parcel of land in Arizona where the joint venture previously was engaged in a copper mining research project. Our share of the net proceeds from the sale resulted in a gain of $21.3 million ($20.4 million to net income or $0.11 per share). In December 2004, Atlantic Copper completed a sale of its wire rod and wire assets for $18.3 million cash and recorded a gain of $7.5 million ($7.5 million to net income or $0.04 per share).

Other income (expense) includes the impact of translating into U.S. dollars Atlantic Copper’s net euro-denominated liabilities, primarily its retiree pension obligations. Changes in the U.S. dollar/euro exchange rate require us to adjust the dollar value of our net euro-denominated liabilities and record the adjustment in earnings. Exchange rate effects on our net income from euro-denominated liabilities were losses of $1.6 million in 2004, $13.6 million in 2003 and $11.9 million in 2002. The losses reflect a stronger euro in relation to the U.S. dollar (see “Disclosures About Market Risks”). Other expenses in 2003 also include a $5.6 million ($3.7 million

26

to net income or $0.02 per share) charge associated with the amended FCX and PT Freeport Indonesia credit facility (see “Capital Resources and Liquidity - Financing Activities”) and interest income of $5.9 million in 2004, $8.9 million in 2003 and $4.8 million in 2002.

PT Freeport Indonesia’s Contract of Work provides for a 35 percent corporate income tax rate. PT Indocopper Investama pays a 30 percent corporate income tax on dividends it receives from its 9.36 percent ownership in PT Freeport Indonesia. In addition, the tax treaty between Indonesia and the United States provides for a withholding tax rate of 10 percent on dividends and interest that PT Freeport Indonesia and PT Indocopper Investama pay to their parent company, FCX. We also incurred a U.S. alternative minimum tax at a rate of two percent based primarily on consolidated income, net of smelting and refining results. As a result of the enactment of the American Jobs Creation Act of 2004, the 90 percent limitation on the use of foreign tax credits to offset the U.S. federal alternative minimum tax liability has been repealed effective January 1, 2005. Based on current projections, we expect that the removal of this limitation will significantly reduce our U.S. federal taxes beginning in 2005. Our U.S. federal alternative minimum tax liability totaled $8.2 million in 2004, $9.3 million in 2003 and $8.2 million in 2002. We currently record no income taxes at Atlantic Copper, which is subject to taxation in Spain, because it has not generated significant taxable income in recent years and has substantial tax loss carryforwards for which we have provided no financial statement benefit. We receive no consolidated tax benefit from these losses because they cannot be used to offset PT Freeport Indonesia’s profits in Indonesia.

Parent company costs consist primarily of interest, depreciation and amortization, and general and administrative expenses. We receive minimal tax benefit from these costs, including interest expense, primarily because our parent company generates no taxable income from U.S. sources. As a result, our provision for income taxes as a percentage of our consolidated income before income taxes and minority interests will vary as PT Freeport Indonesia’s income changes absent changes in Atlantic Copper and parent company costs. The provision for income taxes as a percentage of consolidated income before income taxes and minority interests totaled 58 percent for 2004 and 2003 and 55 percent for 2002. Summaries of the approximate significant components of the calculation of our consolidated provision for income taxes are shown below (in thousands, except percentages).

| Years Ended December 31, | |||||||||

| 2004 | 2003 | 2002 | |||||||

Mining and exploration segment operating incomea | $ | 832,112 | $ | 850,253 | $ | 692,634 | |||

| Mining and exploration segment interest expense, net | (22,209 | ) | (44,861 | ) | (71,424 | ) | |||

| Intercompany operating profit (deferred) recognized | (24,683 | ) | 13,828 | (28,807 | ) | ||||

| Income before taxes | 785,220 | 819,220 | 592,403 | ||||||

| Indonesian corporate income tax rate (35%) plus U.S. alternative minimum tax rate (2%) | 37 | % | 37 | % | 37 | % | |||

| Corporate income taxes | 290,531 | 303,111 | 219,189 | ||||||

| Approximate PT Freeport Indonesia net income | 494,689 | 516,109 | 373,214 | ||||||

| Withholding tax on FCX’s equity share | 9.064 | % | 9.064 | % | 9.064 | % | |||

| Withholding taxes | 44,839 | 46,780 | 33,828 | ||||||

| Other, net | (4,690 | ) | (11,838 | ) | (7,499 | ) | |||

| FCX consolidated provision for income taxes | $ | 330,680 | $ | 338,053 | $ | 245,518 | $ | ||

| FCX consolidated effective tax rate | 58 | % | 58 | % | 55 | % | |||

| a. | Excludes charges for FCX stock option exercises, which are eliminated in consolidation, totaling $87.3 million in 2004, $57.8 million in 2003 and $5.5 million in 2002. |

We have two operating segments: “mining and exploration” and “smelting and refining.” The mining and exploration segment consists of our Indonesian activities including PT Freeport Indonesia’s copper and gold mining operations, Puncakjaya Power’s power generating operations (after eliminations with PT Freeport Indonesia) and our Indonesian exploration activities, including those of Eastern Minerals. The smelting and refining segment includes Atlantic Copper’s operations in Spain and PT Freeport Indonesia’s equity investment in PT Smelting. Summary comparative operating income (loss) data by segment follow (in millions):

27

| Years Ended December 31, | ||||||||||

| 2004 | 2003 | 2002 | ||||||||

Mining and explorationa | $ | 744.8 | $ | 792.5 | $ | 687.2 | ||||

| Smelting and refining | (83.5 | ) | (21.8 | ) | 2.6 | |||||

Intercompany eliminations and othera, b | 42.3 | 52.6 | (49.7 | ) | ||||||

| FCX operating income | $ | 703.6 | $ | 823.3 | $ | 640.1 | ||||

| a. | Includes charges to the mining and exploration segment for FCX stock option exercises, which are eliminated in consolidation, totaling $87.3 million in 2004, $57.8 million in 2003 and $5.5 million in 2002. |

| b. | We defer recognizing profits on PT Freeport Indonesia’s sales to Atlantic Copper and on 25 percent of PT Freeport Indonesia’s sales to PT Smelting until their sales of final products to third parties. Changes in the amount of these deferred profits impacted operating income by $(24.7) million in 2004, $13.8 million in 2003 and $(28.8) million in 2002. Our consolidated earnings fluctuate depending on the timing and prices of these sales. At December 31, 2004, our deferred profits to be recognized in future periods’ operating income totaled $80.9 million, $41.6 million to net income, after taxes and minority interest sharing. |

MINING AND EXPLORATIONOPERATIONS

A summary of changes in PT Freeport Indonesia’s revenues follows (in millions):

| 2004 | 2003 | |||||

| PT Freeport Indonesia revenues - prior year | $ | 1,744.6 | $ | 1,519.0 | ||

| Price realizations: | ||||||

| Copper | 545.4 | 146.4 | ||||

| Gold | 66.0 | 134.9 | ||||

| Sales volumes: | ||||||

| Copper | (249.0 | ) | (160.1 | ) | ||

| Gold | (376.4 | ) | 55.1 | |||

| Adjustments, primarily for copper pricing on prior year open sales | 4.9 | 0.6 | ||||

| Treatment charges, royalties and other | 11.1 | 48.7 | ||||

| PT Freeport Indonesia revenues - current year | $ | 1,746.6 | $ | 1,744.6 | ||

PT Freeport Indonesia, Gross Profit Per Pound of Copper, before intercompany profit eliminations (cents):

| Years Ended December 31, | |||||||

| 2004 | 2003 | 2002 | |||||

| Average realized price | 136.9 | 81.9 | 70.6 | ||||

| Production costs: | |||||||

| Site production and delivery, before reclamation, noncash and nonrecurring costs (credits) shown below | 77.1 | a | 47.6 | a | 36.0 | a | |

| Gold and silver credits | (62.2 | ) | (69.8 | ) | (48.2 | ) | |

| Treatment charges | 20.4 | 17.9 | 18.3 | ||||

| Royalty on metals | 4.4 | 2.0 | 1.6 | ||||

| Net cash production costs (credits) | 39.7 | (2.3 | ) | 7.7 | |||

| Depreciation and amortization | 17.0 | 14.7 | 14.4 | ||||

| Reclamation, noncash and nonrecurring costs (credits) | (0.4 | )b | 1.2 | b | 0.5 | ||

| Total production costs | 56.3 | 13.6 | 22.6 | ||||

| Adjustments, primarily for copper pricing on prior year open sales and gold/silver hedging | 1.9 | 2.8 | 0.9 | ||||

| Gross profit per pound of copper, before intercompany profit eliminations | 82.5 | 71.1 | 48.9 | ||||

| a. | Net of deferred mining costs totaling $77.8 million (7.8 cents per pound) in 2004, $64.4 million (5.0 cents per pound) in 2003 and $30.6 million (2.0 cents per pound) in 2002. |

| b. | Includes a gain on insurance settlement totaling $8.0 million (0.8 cents per pound) in 2004 and equipment losses of $8.4 million (0.7 cents per pound) in 2003 related to the fourth-quarter 2003 Grasberg pit events. |

Net cash production costs (credits) per pound of copper is a measure intended to provide investors with information about the cash generating capacity of our mining operations expressed on a basis relating to its primary metal product, copper. PT Freeport Indonesia uses this measure for the same purpose and for monitoring operating performance by its mining operations. This information differs from measures of performance determined in accordance with generally accepted accounting principles and should not be considered in isolation or as a substitute for measures of performance determined in accordance with generally accepted accounting principles. This measure is presented by other copper and gold mining companies, although our

28

measures may not be comparable to similarly titled measures reported by other companies. For a reconciliation of cash production costs per pound to production and delivery costs applicable to sales reported in our consolidated financial statements, see “PT Freeport Indonesia Product Revenues and Net Cash Production Costs” under “Product Revenues and Production Costs.”

PT Freeport Indonesia Operating Results - 2004 Compared with 2003

PT Freeport Indonesia’s 2004 revenues were slightly higher than 2003 revenues, with higher price realizations offset by lower sales volumes. PT Freeport Indonesia reported lower production and sales in 2004, reflecting the mining of lower-grade material and accelerated overburden removal activities following the fourth-quarter 2003 slippage and debris flow events. Copper sales volumes totaled 1.0 billion pounds in 2004, 23 percent lower than the 1.3 billion pounds reported in 2003. Copper price realizations of $1.37 per pound in 2004 were $0.55 per pound higher than the 2003 realizations of $0.82 per pound. Gold sales volumes totaled 1,443,000 ounces in 2004, 42 percent lower than the 2,469,800 ounces reported in 2003. Gold price realizations of $412.32 per ounce in 2004 were $54.71 an ounce higher than the 2003 realizations of $357.61 per ounce, before realized gains related to the redemption of our Gold-Denominated Preferred Stock. Gold realizations were $366.60 per ounce in 2003 after hedging gains from redemption of our Gold-Denominated Preferred Stock.

Treatment charges vary with the volume of metals sold and the price of copper, and royalties vary with the volume of metals sold and the prices of copper and gold. In addition, treatment charges vary based on PT Freeport Indonesia’s customer mix. Market rates for treatment and refining charges increased significantly toward the end of 2004 and are expected to be higher in 2005; however, PT Freeport Indonesia expects its 2005 rates to approximate its 2004 rates because of its customer mix. Total treatment charges for PT Freeport Indonesia in 2004 were lower because of the lower volume of metal sales. Royalty costs totaled $43.5 million in 2004 compared with $26.5 million in 2003, reflecting higher metal prices partly offset by lower sales volumes.

Following the fourth-quarter 2003 Grasberg open-pit slippage and debris flow events, we accelerated the removal of overburden and mined low-grade ore prior to restoring safe access to higher-grade ore areas in the second quarter of 2004 and resuming normal milling rates in June 2004. Mill throughput averaged 185,100 metric tons of ore per day in 2004 and 203,000 metric tons of ore in 2003. Mill throughput, which varies depending on ore types being processed, averaged 229,800 metric tons per day in the fourth quarter of 2004 and is expected to average approximately 235,000 metric tons per day in 2005. Approximate average daily throughput processed at our mill facilities from each of our producing mines follows (metric tons of ore per day):

| Years Ended December 31, | ||||||

| 2004 | 2003 | 2002 | ||||

| Grasberg open pit | 141,500 | 155,700 | 194,500 | |||

| Deep Ore Zone | 43,600 | 40,500 | 21,800 | |||

| Intermediate Ore Zone | - | 6,800 | 19,300 | |||

| Total mill throughput | 185,100 | 203,000 | 235,600 | |||

Production from the Deep Ore Zone (DOZ) underground mine averaged 43,600 metric tons of ore per day, representing 24 percent of total 2004 mill throughput. DOZ operations continue to perform above design capacity of 35,000 metric tons of ore per day. PT Freeport Indonesia is expanding the capacity of the DOZ underground operation to 50,000 metric tons per day with the installation of a second crusher and additional ventilation. PT Freeport Indonesia’s share of capital expenditures for the DOZ expansion in the period 2004 through the projected 2007 ramp-up are expected to approximate $37 million, with $19 million estimated for 2005. The DOZ mine, a block cave operation, is one of the world’s largest underground operations. The Intermediate Ore Zone underground mine was depleted during the third quarter of 2003, producing almost 30 percent more copper and gold throughout its 10-year life than the initial reserve estimates.

Copper ore grades averaged 0.87 percent in 2004, compared with 1.09 percent in 2003. Copper recovery rates were 88.6 percent for 2004, compared with 89.0 percent for 2003. In 2004, gold ore grades averaged 0.88 grams per metric ton (g/t), compared with 1.54 g/t in 2003. Gold recovery rates were 81.8 percent for 2004, compared with 87.3 percent for 2003. The mining of lower grade material resulted in lower 2004 recovery rates. Compared to 2004, ore grades are expected to be higher for 2005 resulting in increased metal production in 2005. Gold recovery rates are expected to improve with the higher ore grades.

Unit net cash production costs, including gold and silver credits, averaged $0.40 per pound of copper during 2004, compared with a net credit of $(0.02) per pound for 2003. Higher unit site production and delivery costs in 2004 reflected significantly lower sales volumes resulting from lower ore grades and the primarily fixed nature of a large portion of PT Freeport Indonesia’s cost structure. In addition, the lower sales volumes resulted in PT Freeport Indonesia being allocated a larger percentage of those fixed costs in 2004 under our joint venture arrangements with Rio Tinto. To a lesser extent, 2004 unit costs were impacted by higher energy costs, increased maintenance costs, the impact of a stronger Australian dollar and increased treatment and refining charge rates caused by higher copper prices and our customer mix.

29

Unit site production and delivery costs in 2004 averaged $0.77 per pound of copper, $0.29 per pound higher than the $0.48 reported in 2003. Unit production and delivery costs are net of deferred mining costs of $0.08 per pound ($77.8 million) for 2004 and $0.05 per pound ($64.4 million) for 2003. The increase in deferred mining costs included the effects of PT Freeport Indonesia’s accelerated overburden removal efforts during 2004. In the fourth quarter of 2004, PT Freeport Indonesia changed its life-of-mine overburden-to-ore ratio to 2.4 to 1 from 2.2 to 1, and in the fourth quarter of 2003 the ratio changed to 2.1 to 1 from 1.9 to 1, as discussed above. The fourth-quarter 2004 change increased 2004 costs by $5.5 million or 0.6 cents per pound. As of December 31, 2004, deferred mining costs totaled $220.4 million compared with $142.6 million at December 31, 2003. See “Critical Accounting Estimates” for a discussion of changes in the estimated life-of-mine overburden-to-ore ratio.

Gold and silver credits were $0.62 per pound for 2004, compared with $0.70 for 2003. The decrease primarily reflects the reduced production and sales of gold during 2004, partly offset by the improved gold realizations.

Unit treatment charges vary with the price of copper, and royalty rates vary with prices of copper and gold. In addition, treatment charges vary based on PT Freeport Indonesia’s customer mix. Royalties of $0.04 per pound were $0.02 per pound above the year-ago period primarily because of higher copper and gold prices. The copper royalty rate payable by PT Freeport Indonesia under its Contract of Work varies from 1.5 percent of copper net revenue at a copper price of $0.90 or less per pound to 3.5 percent at a copper price of $1.10 or more per pound. The Contract of Work royalty rate for gold and silver sales is 1.0 percent. In connection with our fourth concentrator mill expansion completed in 1998, PT Freeport Indonesia agreed to pay the Government of Indonesia additional royalties (royalties not required by the Contract of Work) to provide further support to the local governments and the people of the Indonesian province of Papua. The additional royalties are paid on metal from production from PT Freeport Indonesia’s milling facilities above 200,000 metric tons of ore per day. The additional royalty for copper equals the Contract of Work royalty rate, and for gold and silver equals twice the Contract of Work royalty rates. Therefore, PT Freeport Indonesia’s royalty rate on copper net revenues from production above 200,000 metric tons of ore per day is double the Contract of Work royalty rate, and the royalty rates on gold and silver sales from production above 200,000 metric tons of ore per day are triple the Contract of Work royalty rates. As a result of higher projected copper and gold sales volumes, we expect our 2005 royalty costs to increase compared with 2004 royalty costs of $43.5 million. If copper prices average $1.35 per pound and gold prices average $420 per ounce in 2005, we would expect royalty costs to total approximately $90 million ($0.06 per pound) for 2005. These estimates assume 2005 sales volumes of 1.5 billion pounds of copper and 2.9 million ounces of gold.

Assuming 2005 average prices of $1.35 per pound for copper and $420 per ounce for gold, and copper and gold sales of 1.5 billion pounds and 2.9 million ounces for 2005, PT Freeport Indonesia estimates that its gold credits would essentially offset its cash production costs, resulting in net cash production costs of approximately zero cents per pound for the year 2005. Estimated unit cash costs reflect recent increases in energy costs, a stronger Australian dollar currency and other factors. Net unit cash production costs for 2005 would change by approximately $0.05 per pound for each $25 per ounce change in the average price of gold. Forecasted unit costs are calculated on the same basis as the historical unit costs, which are discussed above and reconciled in “Product Revenues and Production Costs.”

As a result of the lower copper production and sales in 2004, PT Freeport Indonesia’s depreciation rate per pound of copper increased to $0.17 for 2004 compared with $0.15 for 2003. For 2005, PT Freeport Indonesia expects its deprecation rate to decrease to approximately $0.14 per pound, primarily because of higher projected copper production and sales. Because certain assets are depreciated on a straight-line basis, the rate per pound will vary with the level of copper production and sales.

PT Freeport Indonesia Operating Results - 2003 Compared with 2002

PT Freeport Indonesia’s revenues increased by $225.6 million in 2003 from 2002. Both copper and gold price realizations improved during 2003 with copper approximately 15 percent higher at $0.82 per pound and gold approximately 18 percent higher at $366.60 per ounce. Gold revenues include a $22.1 million ($8.99 per ounce) hedging gain from redemption of our Gold-Denominated Preferred Stock. Copper sales volumes declined 15 percent to 1.3 billion pounds in 2003 from 1.5 billion pounds in 2002 because of lower copper ore grades and reduced mill throughput resulting from the fourth-quarter slippage and debris flow events. Gold sales volumes increased 8 percent to 2.5 million ounces in 2003 from 2.3 million ounces in 2002 because of higher gold ore grades partly offset by lower mill throughput. Treatment charges were $46.6 million lower in 2003 compared with 2002 because of lower copper sales volumes and market treatment rates. Royalties were higher at $26.5 million for 2003 compared with $24.5 million for 2002 primarily reflecting higher metals prices.

Mill throughput from production from PT Freeport Indonesia’s producing mines averaged 203,000 metric tons of ore per day in 2003 and 235,600 metric tons of ore per day in 2002. The lower mill throughput rate during 2003 primarily reflects the

30

impact of the fourth-quarter 2003 open-pit slippage and debris flow events and the subsequent clean-up efforts. At the DOZ underground mine, production averaged 40,500 metric tons of ore per day for 2003, compared with 21,800 metric tons of ore per day for 2002. Production from the Intermediate Ore Zone averaged 6,800 metric tons of ore per day for 2003 and 19,300 metric tons of ore per day for 2002.

PT Freeport Indonesia reported record-low average unit net cash production costs of a net credit of $(0.02) per pound in 2003, compared with $0.08 per pound in 2002. Unit site production and delivery costs in 2003 averaged $0.48 per pound of copper, $0.12 per pound higher than the $0.36 in 2002 primarily because of lower copper sales volumes. Higher mine maintenance costs, stronger Indonesian and Australian currencies and higher energy costs also resulted in higher costs compared with 2002.

Gold credits for 2003 of $0.70 per pound were higher than the gold credits of $0.48 per pound in 2002 primarily because of higher gold sales volumes and prices in 2003. Gold ore grades for 2003 improved by 24 percent to 1.54 grams per metric ton in 2003 from 1.24 grams per metric ton in 2002. As a result of the lower copper production and sales in 2003, PT Freeport Indonesia’s depreciation rate per pound of copper increased to $0.15 for 2003 compared with $0.14 for 2002.

PT Freeport Indonesia Sales Outlook

PT Freeport Indonesia sells its copper concentrates primarily under long-term sales agreements denominated in U.S. dollars, mostly to companies in Asia and Europe and to international trading companies. PT Freeport Indonesia’s share of sales for 2005 is projected to approximate 1.5 billion pounds of copper and 2.9 million ounces of gold, and to average 1.36 billion pounds of copper and 2.2 million ounces of gold annually over the next five years (2005-2009). PT Freeport Indonesia expects its sales for the first quarter of 2005 to approximate 310 million pounds of copper and 520,000 ounces of gold. Also, based on the current mine plan for 2005, PT Freeport Indonesia estimates approximately 54 percent of its copper and 60 percent of its gold will be produced in the second half of 2005. Because of the nature of the Grasberg ore body, the sequencing in mining will cause ore grades to vary from quarter to quarter, particularly for gold.

PT Freeport Indonesia has long-term contracts to provide approximately 60 percent of Atlantic Copper’s copper concentrate requirements at market prices and nearly all of PT Smelting’s copper concentrate requirements. Under the PT Smelting contract, for the first 15 years of PT Smelting’s operations beginning December 1998, the treatment and refining charges on the majority of the concentrate PT Freeport Indonesia provides will not fall below specified minimum rates, subject to renegotiation in 2008. The rate was $0.23 per pound during the period from the commencement of PT Smelting’s operations in 1998 until April 2004, when it declined to a minimum of $0.21 per pound. Market rates, excluding price participation, under long-term contracts settled in late 2004 approximate $0.21 per pound.

Exploration and Reserves

During 2004, net additions and revisions to the aggregate proven and probable reserves at the Grasberg mining complex totaled approximately 141 million metric tons of ore representing increases of 2.9 billion recoverable pounds of copper, 2.2 million recoverable ounces of gold and 18.9 million recoverable ounces of silver. The additions were primarily the result of positive drilling results at the Deep Mill Level Zone ore body, a 146-million-metric-ton ore body. We expect to complete additional engineering studies evaluating drilling results on the western side of the ore body in 2005, which could increase the size of the ore body. Our aggregate exploration budget for 2005, including Rio Tinto’s share, is expected to total approximately $21 million ($15 million for our share) with most of the effort focused on testing the Mill Level Zone and Deep Mill Level Zone deposits to the northwest, expansion of the underground Grasberg resource, and testing reconnaissance targets along the Wanagon and Idenberg fault trends. Net of Rio Tinto’s share, PT Freeport Indonesia’s share of proven and probable recoverable reserves as of December 31, 2004, was 40.5 billion pounds of copper, 46.5 million ounces of gold and 124.5 million ounces of silver. FCX’s equity interest in proven and probable recoverable reserves as of December 31, 2004, was 36.7 billion pounds of copper, 42.1 million ounces of gold and 112.8 million ounces of silver (see Note 13 of “Notes to Consolidated Financial Statements”). PT Freeport Indonesia’s share of reserve additions replaced approximately 175 percent of its 2004 copper production, 90 percent of 2004 gold production and 330 percent of 2004 silver production. Estimated recoverable reserves were assessed using a copper price of $0.85 per pound and a gold price of $270 per ounce. If we adjusted metal prices used in our reserve estimates to the approximate average London spot prices for the past three years ($0.94 per pound of copper and $361 per ounce of gold), the additions to proven and probable reserves would not be material to reported reserves.

The Indonesian government previously approved suspensions of our field exploration activities outside of our current mining operations area, which have been in suspension in recent years due to safety and security issues and regulatory uncertainty relating to a possible conflict between our mining and exploration rights in certain forest areas and an Indonesian Forestry law enacted in 1999 prohibiting open-pit mining in forest preservation areas. The current suspensions were granted for one-year periods ending February 26, 2005, for Block B; March 31, 2005, for PT Nabire

31

Bakti Mining; and November 15, 2004, for Eastern Minerals. Recent Indonesian legislation permits open-pit mining in PT Freeport Indonesia’s Block B area, subject to certain requirements. We are currently assessing these requirements and security issues. The timing for our resumption of exploration activities in our Contract of Work areas outside of Block A depends on the resolution of these matters.

SMELTING AND REFINING OPERATIONS

Our investment in smelters serves an important role in our concentrate marketing strategy. PT Freeport Indonesia generally sells approximately one-half of its concentrate production to its affiliated smelters, Atlantic Copper and PT Smelting, and the remainder to other customers. Treatment charges for smelting and refining copper concentrates represent a cost to PT Freeport Indonesia and income to Atlantic Copper and PT Smelting. Through downstream integration, we are assured placement of a significant portion of our concentrate production. While low smelting and refining charges in recent years adversely affected the operating results of Atlantic Copper, they benefited the operating results of PT Freeport Indonesia’s mining operations, effectively achieving a hedge for these charges. Treatment and refining charge rates are currently increasing. Higher future treatment and refining charges will benefit our smelter operations and adversely affect our mining operations. Taking into account taxes and minority ownership interests, an equivalent change in smelting and refining charge rates would essentially offset in our consolidated operating results.

Atlantic Copper Operating Results

| Years Ended December 31, | |||||||||

| (In Millions) | 2004 | 2003 | 2002 | ||||||

| Gross (loss) profit | $ | (69.4 | ) | $ | (10.7 | ) | $ | 11.2 | |

| Add depreciation and amortization expense | 28.6 | 28.5 | 27.7 | ||||||

| Other | 16.4 | a | 4.6 | 4.5 | |||||

| Cash (deficit) margin | $ | (24.4 | )b | $ | 22.4 | $ | 43.4 | ||

| Operating (loss) income (in millions) | $ | (83.5 | ) | $ | (21.8 | ) | $ | 2.6 | |

| Concentrate and scrap treated (metric tons) | 768,100 | 964,400 | 1,016,700 | ||||||

| Anodes production (000s of pounds) | 494,400 | 640,000 | 657,000 | ||||||

| Treatment rates per pound | $0.16 | $0.16 | $0.17 | ||||||

| Cathodes, wire rod and wire sales (000s of pounds) | 479,200 | 546,800 | 556,500 | ||||||

| Cathode cash production cost per pound before hedging | $0.25 | $0.16 | $0.12 | ||||||

| Gold sales in anodes and slimes (ounces) | 316,700 | 929,700 | 813,900 | ||||||

| a. | Includes a $9.8 million charge for Atlantic Copper’s workforce reduction plan. |

| b. | Includes costs related to Atlantic Copper’s 51-day major maintenance turnaround totaling $27.5 million. |

Atlantic Copper Operating Results - 2004 Compared with 2003

Atlantic Copper completed a 51-day scheduled major maintenance turnaround in May 2004, adversely affecting 2004 results. Atlantic Copper’s operating cash margin was a $24.4 million deficit in 2004, compared with a positive $22.4 million in 2003. The deficit in 2004 was primarily because of Atlantic Copper’s major maintenance turnaround. Major maintenance turnarounds of this duration typically occur approximately every nine years for Atlantic Copper, with significantly shorter-term maintenance turnarounds occurring in the interim.