| |

| |

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

| FORM 10-Q |

| |

| (Mark One) |

| [X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the quarterly period ended March 31, 2008 |

| OR |

| [ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from | | To |

| Commission File Number: 1-9916 |

| |

|

| |

| Freeport-McMoRan Copper & Gold Inc. |

| (Exact name of registrant as specified in its charter) |

| Delaware | 74-2480931 |

| (State or other jurisdiction of | (I.R.S. Employer Identification No.) |

| incorporation or organization) | |

| | |

| One North Central Avenue | |

| Phoenix, AZ | 85004-4414 |

| (Address of principal executive offices) | (Zip Code) |

| |

| (602) 366-8100 |

| (Registrant's telephone number, including area code) |

| |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. R Yes ÿo No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer R Accelerated filer o Non-accelerated filer o Smaller reporting company oÿ

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ÿo Yes R No

On April 30, 2008, there were issued and outstanding 383,219,916 shares of the registrant’s Common Stock, par value $0.10 per share.

FREEPORT-McMoRan COPPER & GOLD INC.

| | |

| | Page |

| 3 |

| | |

| |

| | |

| 3 |

| | |

| 4 |

| | |

| 5 |

| | |

| 6 |

| | |

| 7 |

| | |

| 16 |

| | |

| |

| 17 |

| | |

| 53 |

| | |

| 53 |

| | |

| 53 |

| | |

| 53 |

| | |

| 54 |

| | |

| 54 |

| | |

| 54 |

| | |

| 55 |

| | |

| E-1 |

| | |

FREEPORT-McMoRan COPPER & GOLD INC.

FREEPORT-McMoRan COPPER & GOLD INC.

| | | March 31, | | | December 31, | |

| | | 2008 | | | 2007 | |

| | | (In Millions) | |

| ASSETS | | | | | | | | |

| Current assets: | | | | | | | | |

| Cash and cash equivalents | | $ | 1,831 | | | $ | 1,626 | |

| Trade accounts receivable | | | 1,949 | | | | 1,099 | |

| Other accounts receivable | | | 181 | | | | 196 | |

| Product inventories and materials and supplies, net | | | 2,187 | | | | 2,178 | |

| Mill and leach stockpiles | | | 773 | | | | 707 | |

| Prepaid expenses and other current assets | | | 97 | | | | 97 | |

| Total current assets | | | 7,018 | | | | 5,903 | |

| Property, plant, equipment and development costs, net | | | 25,814 | | | | 25,715 | |

| Goodwill | | | 6,048 | | | | 6,105 | |

| Long-term mill and leach stockpiles | | | 1,153 | | | | 1,106 | |

| Trust assets | | | 599 | | | | 606 | |

| Intangible assets, net | | | 464 | | | | 472 | |

| Other assets and deferred charges | | | 732 | | | | 754 | |

| Total assets | | $ | 41,828 | | | $ | 40,661 | |

| | | | | | | | | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | | | |

| Current liabilities: | | | | | | | | |

| Accounts payable and accrued liabilities | | $ | 2,242 | | | $ | 2,345 | |

| Accrued income taxes | | | 640 | | | | 420 | |

| Current portion of reclamation and environmental liabilities | | | 226 | | | | 263 | |

| Dividends payable | | | 212 | | | | 212 | |

| Current portion of long-term debt and short-term borrowings | | | 36 | | | | 31 | |

| Copper price protection program | | | – | | | | 598 | |

| Total current liabilities | | | 3,356 | | | | 3,869 | |

| Long-term debt, less current portion: | | | | | | | | |

| Senior notes | | | 6,887 | | | | 6,928 | |

| Project financing, equipment loans and other | | | 352 | | | | 252 | |

| Revolving credit facility | | | 296 | | | | – | |

| Total long-term debt, less current portion | | | 7,535 | | | | 7,180 | |

| Deferred income taxes | | | 7,135 | | | | 7,300 | |

| Reclamation and environmental liabilities, less current portion | | | 1,893 | | | | 1,733 | |

| Other liabilities | | | 1,093 | | | | 1,106 | |

| Total liabilities | | | 21,012 | | | | 21,188 | |

| Minority interests in consolidated subsidiaries | | | 1,510 | | | | 1,239 | |

| Stockholders’ equity: | | | | | | | | |

| 5½% Convertible Perpetual Preferred Stock | | | 1,100 | | | | 1,100 | |

| 6¾% Mandatory Convertible Preferred Stock | | | 2,875 | | | | 2,875 | |

| Common stock | | | 50 | | | | 50 | |

| Capital in excess of par value | | | 13,552 | | | | 13,407 | |

| Retained earnings | | | 4,554 | | | | 3,601 | |

| Accumulated other comprehensive income | | | 43 | | | | 42 | |

| Common stock held in treasury | | | (2,868 | ) | | | (2,841 | ) |

| Total stockholders’ equity | | | 19,306 | | | | 18,234 | |

| Total liabilities and stockholders’ equity | | $ | 41,828 | | | $ | 40,661 | |

| | | | | | | | | |

The accompanying notes are an integral part of these consolidated financial statements.

FREEPORT-McMoRan COPPER & GOLD INC.

| | Three Months Ended | |

| | March 31, | |

| | 2008 | | 2007 | |

| | (In Millions, Except Per Share Amounts) | |

| Revenues | $ | 5,672 | | $ | 2,246 | |

| Cost of sales: | | | | | | |

| Production and delivery | | 2,722 | | | 903 | |

| Depreciation, depletion and amortization | | 418 | | | 116 | |

| Total cost of sales | | 3,140 | | | 1,019 | |

| Selling, general and administrative expenses | | 84 | | | 48 | |

| Exploration and research expenses | | 52 | | | 7 | |

| Total costs and expenses | | 3,276 | | | 1,074 | |

| Operating income | | 2,396 | | | 1,172 | |

| Interest expense, net | | (165 | ) | | (52 | ) |

| Losses on early extinguishment of debt | | (6 | ) | | (88 | ) |

| Other income, net | | 2 | | | 24 | |

| Equity in affiliated companies’ net earnings | | 7 | | | 5 | |

| Income from continuing operations before income taxes and minority interests | | 2,234 | | | 1,061 | |

| Provision for income taxes | | (729 | ) | | (458 | ) |

| Minority interests in net income of consolidated subsidiaries | | (319 | ) | | (114 | ) |

| Income from continuing operations | | 1,186 | | | 489 | |

| Income from discontinued operations, net of taxes | | – | | | 4 | |

| Net income | | 1,186 | | | 493 | |

| Preferred dividends | | (64 | ) | | (17 | ) |

| Net income applicable to common stock | $ | 1,122 | | $ | 476 | |

| | | | | | | |

| Basic net income per share of common stock: | | | | | | |

| Continuing operations | $ | 2.93 | | $ | 2.18 | |

| Discontinued operations | | – | | | 0.02 | |

| Basic net income per share of common stock | $ | 2.93 | | $ | 2.20 | |

| | | | | | | |

| Diluted net income per share of common stock: | | | | | | |

| Continuing operations | $ | 2.64 | | $ | 2.00 | |

| Discontinued operations | | – | | | 0.02 | |

| Diluted net income per share of common stock | $ | 2.64 | | $ | 2.02 | |

| | | | | | | |

| Average common shares outstanding: | | | | | | |

| Basic | | 383 | | | 217 | |

| Diluted | | 449 | | | 244 | |

| | | | | | | |

| Dividends declared per share of common stock | $ | 0.4375 | | $ | 0.3125 | |

The accompanying notes are an integral part of these consolidated financial statements.

FREEPORT-McMoRan COPPER & GOLD INC.

| | | Three Months Ended | |

| | | March 31, | |

| | | 2008 | | | 2007 | |

| | | (In Millions) | |

| Cash flow from operating activities: | | | | | | | | |

| Net income | | $ | 1,186 | | | $ | 493 | |

| Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | | | |

| Depreciation, depletion and amortization | | | 418 | | | | 116 | |

| Minority interests in net income of consolidated subsidiaries | | | 319 | | | | 114 | |

| Noncash compensation and benefits | | | 37 | | | | 26 | |

| Unrealized losses on copper price protection program | | | – | | | | 38 | |

| Losses on early extinguishment of debt | | | 6 | | | | 88 | |

| Deferred income taxes | | | (48 | ) | | | (46 | ) |

| Other, net | | | 38 | | | | 42 | |

| (Increases) decreases in working capital, excluding amounts acquired from | | | | | | | | |

| Phelps Dodge: | | | | | | | | |

| Accounts receivable | | | (950 | ) | | | (398 | ) |

| Inventories | | | (81 | ) | | | 81 | |

| Prepaid expenses and other | | | 1 | | | | 1 | |

| Accounts payable and accrued liabilities | | | (527 | ) | | | (30 | ) |

| Accrued income taxes | | | 216 | | | | 144 | |

| Net cash provided by operating activities | | | 615 | | | | 669 | |

| | | | | | | | | |

| Cash flow from investing activities: | | | | | | | | |

| Phelps Dodge capital expenditures | | | (388 | ) | | | (61 | ) |

| PT Freeport Indonesia capital expenditures | | | (115 | ) | | | (74 | ) |

| Other capital expenditures | | | (5 | ) | | | (7 | ) |

| Acquisition of Phelps Dodge, net of cash acquired | | | (1 | ) | | | (13,888 | ) |

| Proceeds from the sale of assets and other, net | | | 22 | | | | – | |

| Net cash used in investing activities | | | (487 | ) | | | (14,030 | ) |

| | | | | | | | | |

| Cash flow from financing activities: | | | | | | | | |

| Proceeds from term loans under bank credit facility | | | – | | | | 10,000 | |

| Repayments of term loans under bank credit facility | | | – | | | | (5,618 | ) |

| Net proceeds from sales of senior notes | | | – | | | | 5,880 | |

| Net proceeds from sale of common stock | | | – | | | | 2,816 | |

| Net proceeds from sale of 6¾% Mandatory Convertible Preferred Stock | | | – | | | | 2,803 | |

| Proceeds from revolving credit facility and other debt | | | 473 | | | | 101 | |

| Repayments of revolving credit facility and other debt | | | (118 | ) | | | (48 | ) |

| Cash dividends paid: | | | | | | | | |

| Common stock | | | (169 | ) | | | (63 | ) |

| Preferred stock | | | (64 | ) | | | (15 | ) |

| Minority interests | | | (49 | ) | | | (47 | ) |

| Net payments for exercised stock options | | | (8 | ) | | | (45 | ) |

| Excess tax benefit from exercised stock options | | | 12 | | | | 1 | |

| Bank credit facilities fees and other, net | | | – | | | | (185 | ) |

| Net cash provided by financing activities | | | 77 | | | | 15,580 | |

| | | | | | | | | |

| Net increase in cash and cash equivalents | | | 205 | | | | 2,219 | |

| Cash and cash equivalents at beginning of year | | | 1,626 | | | | 907 | |

| Cash and cash equivalents at end of period | | $ | 1,831 | | | $ | 3,126 | |

The accompanying notes are an integral part of these consolidated financial statements.

FREEPORT-McMoRan COPPER & GOLD INC.

| | | | | | | | | | | | | | | | | | | |

| | | Convertible Perpetual | | Mandatory Convertible | | | | | | | | Accumulated | | Common Stock | | | | |

| | | Preferred Stock | | Preferred Stock | | Common Stock | | | | | | Other | | Held in Treasury | | | | |

| | | Number | | | | Number | | | | Number | | | | Capital in | | | | Compre- | | Number | | | | | | |

| | | of | | At Par | | of | | At Par | | of | | At Par | | Excess of | | Retained | | hensive | | of | | At | | Stockholders’ | |

| | | Shares | | Value | | Shares | | Value | | Shares | | Value | | Par Value | | Earnings | | Income | | Shares | | Cost | | Equity | |

| | | (In Millions) | |

| Balance at December 31, 2007 | | 1 | | $ | 1,100 | | | 29 | | $ | 2,875 | | | 497 | | $ | 50 | | $ | 13,407 | | $ | 3,601 | | $ | 42 | | | 114 | | $ | (2,841 | ) | $ | 18,234 | |

| Exercised stock options, issued | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| restricted stock and other | | – | | | – | | | – | | | – | | | 1 | | | – | | | 114 | | | – | | | – | | | – | | | – | | | 114 | |

| Stock-based compensation costs | | – | | | – | | | – | | | – | | | – | | | – | | | 25 | | | – | | | – | | | – | | | – | | | 25 | |

| Tax benefit for stock option | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| exercises | | – | | | – | | | – | | | – | | | – | | | – | | | 6 | | | – | | | – | | | – | | | – | | | 6 | |

| Tender of shares for exercised | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| stock options and restricted | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| stock | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | 1 | | | (27 | ) | | (27 | ) |

| Dividends on common stock | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | (169 | ) | | – | | | – | | | – | | | (169 | ) |

| Dividends on preferred stock | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | (64 | ) | | – | | | – | | | – | | | (64 | ) |

| Comprehensive income: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net income | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | 1,186 | | | – | | | – | | | – | | | 1,186 | |

| Other comprehensive income, | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| net of taxes: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Defined benefit plans: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Amortization of | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| unrecognized amounts | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | 1 | | | – | | | – | | | 1 | |

| Other comprehensive income | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | 1 | | | – | | | – | | | 1 | |

| Total comprehensive income | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | – | | | 1,187 | |

| Balance at March 31, 2008 | | 1 | | $ | 1,100 | | | 29 | | $ | 2,875 | | | 498 | | $ | 50 | | $ | 13,552 | | $ | 4,554 | | $ | 43 | | | 115 | | $ | (2,868 | ) | $ | 19,306 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

The accompanying notes are an integral part of these consolidated financial statements.

FREEPORT-McMoRan COPPER & GOLD INC.

The accompanying unaudited consolidated financial statements have been prepared in accordance with the instructions to Form 10-Q and do not include all information and disclosures required by generally accepted accounting principles (GAAP) in the United States (U.S.). Therefore, this information should be read in conjunction with Freeport-McMoRan Copper & Gold Inc.’s (FCX) consolidated financial statements and notes contained in its 2007 Annual Report on Form 10-K. The information furnished herein reflects all adjustments which are, in the opinion of management, necessary for a fair statement of the results for the interim periods reported. With the exception of certain adjustments associated with the acquisition of Phelps Dodge Corporation (Phelps Dodge), all such adjustments are, in the opinion of management, of a normal recurring nature. Operating results for the three-month period ended March 31, 2008, are not necessarily indicative of the results that may be expected for the year ending December 31, 2008.

As further discussed in Note 2, on March 19, 2007, FCX completed its acquisition of Phelps Dodge. First-quarter 2007 financial results include Phelps Dodge’s results beginning March 20, 2007. Additionally, Phelps Dodge had an international wire and cable business, Phelps Dodge International Corporation (PDIC), which FCX sold on October 31, 2007. As a result of the sale, Phelps Dodge’s first-quarter 2007 operating results have been restated to remove PDIC from continuing operations and report PDIC as discontinued operations in the consolidated statements of income (see Note 3).

| 2. | ACQUISITION OF PHELPS DODGE |

On March 19, 2007, Phelps Dodge became a wholly owned subsidiary of FCX. The estimated fair value of assets acquired and liabilities assumed and the results of Phelps Dodge’s operations are included in FCX’s consolidated financial statements beginning March 20, 2007.

The acquisition was accounted for under the purchase method as required by Statement of Financial Accounting Standards (SFAS) No. 141, “Business Combinations,” with FCX as the accounting acquirer. In the acquisition, each share of Phelps Dodge common stock was exchanged for 0.67 of a share of FCX common stock and $88.00 in cash. As a result, FCX issued 136.9 million shares and paid $18.0 billion in cash to Phelps Dodge stockholders for total consideration of $25.8 billion.

In accordance with the purchase method of accounting, the purchase price paid was determined at the date of the public announcement of the transaction and was allocated to the assets acquired and liabilities assumed based upon their estimated fair values on the closing date of March 19, 2007. In valuing acquired assets and assumed liabilities, fair values were based on, but were not limited to: quoted market prices, where available; the intent of FCX with respect to whether the assets purchased were to be held, sold or abandoned; expected future cash flows; current replacement cost for similar capacity for certain fixed assets; market rate assumptions for contractual obligations; and appropriate discount rates and growth rates. The excess of the purchase price over the fair value of the net assets acquired has been recorded as goodwill. A decline in copper or molybdenum prices from those used to estimate the fair values of the acquired assets could result in impairment to the carrying amounts assigned to inventories; mill and leach stockpiles; property, plant and equipment; and goodwill. At the date of acquisition of Phelps Dodge, price projections used to value the assets acquired ranged from a near-term price of $2.98 per pound for copper and $26.20 per pound for molybdenum to a long-term average price of $1.20 per pound for copper and $8.00 per pound for molybdenum.

A summary of the final purchase price allocation as of March 19, 2007, follows (in billions):

| | | | | | Purchase | |

| | Historical | | Fair Value | | Price | |

| | Balances | | Adjustments | | Allocation | |

| Cash and cash equivalents | $ | 4.2 | | $ | – | | $ | 4.2 | |

| Inventories, including mill and leach stockpiles | | 0.9 | | | 2.8 | | | 3.7 | |

Property, plant and equipmenta | | 6.0 | | | 16.2 | | | 22.2 | |

| Other assets | | 3.1 | | | 0.2 | | | 3.3 | |

| Allocation to goodwill | | – | | | 6.2 | | | 6.2 | b |

| Total assets | | 14.2 | | | 25.4 | | | 39.6 | |

Deferred income taxes (current and long-term)c | | (0.7 | ) | | (6.3 | ) | | (7.0 | ) |

| Other liabilities | | (4.1 | ) | | (1.5 | ) | | (5.6 | ) |

| Minority interests | | (1.2 | ) | | – | | | (1.2 | ) |

| Total | $ | 8.2 | | $ | 17.6 | | $ | 25.8 | |

| | | | | | | | | | |

| a. | Includes amounts for proven and probable reserves and values assigned to value beyond proven and probable reserves (VBPP). |

| b. | Includes $160 million of goodwill associated with PDIC, which was sold in the fourth quarter of 2007. |

| c. | Deferred income taxes have been recognized based on the difference between the tax basis and the fair values assigned to net assets. |

Goodwill arising from the acquisition of Phelps Dodge was $6.2 billion, which primiarily related to the requirement to recognize a deferred tax liability for the difference between the assigned values and the tax bases of the assets acquired and liabilities assumed in a business combination. FCX allocated goodwill to the individual mines it believes have contributed to the excess purchase price and also included consideration of the mines’ potential for future growth (see Note 10 for the allocation of goodwill to FCX's reportable segments).

Pro Forma Financial Information. The following pro forma information assumes that FCX acquired Phelps Dodge effective January 1, 2007. The most significant adjustments relate to the purchase accounting impacts on the carrying values of acquired metal inventories (including mill and leach stockpiles) and property, plant and equipment using March 19, 2007, metal prices and assumptions (in millions, except per share data):

| | Historical | | | | | |

| | | | | Phelps | | Pro Forma | | Pro Forma | |

| Three months ended March 31, 2007 | FCX | | Dodgea | | Adjustments | | Consolidated | |

| Revenues | $ | 2,246 | | $ | 2,294 | | $ | 30 | | $ | 4,570 | b |

| Operating income | $ | 1,172 | | $ | 793 | | $ | (489 | ) | $ | 1,476 | b,c |

| Income from continuing operations before | | | | | | | | | | | | |

| income taxes and minority interests | $ | 1,061 | | $ | 837 | | $ | (581 | ) | $ | 1,317 | b,c,d,e |

| Net income from continuing operations | | | | | | | | | | | | |

| applicable to common stock | $ | 472 | | $ | 493 | | $ | (427 | ) | $ | 538 | b,c,d,e |

| Diluted net income per share of common | | | | | | | | | | | | |

| stock from continuing operations | $ | 2.00 | | | N/A | | | N/A | | $ | 1.35 | b,c,d,e |

| Diluted weighted-average shares of | | | | | | | | | | | | |

| common stock outstanding | | 244 | | | N/A | | | N/A | | | 446 | f |

| | | | | | | | | | | | | |

| a. | Represents the results of Phelps Dodge’s operations from January 1, 2007, through March 19, 2007. Beginning March 20, 2007, the results of Phelps Dodge’s operations are included in FCX’s consolidated financial statements. |

Additionally, for comparative purposes, the historical Phelps Dodge financial information for first-quarter 2007 represents results from continuing operations, and therefore, excludes the results of PDIC (i.e., discontinued operations).

| b. | Includes charges to revenues for mark-to-market accounting adjustments on the copper price protection program totaling $58 million ($36 million to net income or $0.08 per share) in the first quarter of 2007. Also includes pro forma credits for amortization of acquired intangible liabilities totaling $30 million ($19 million to net income or $0.04 per share). |

| c. | Includes charges associated with the impacts of the increases in the carrying values of acquired metal inventories (including mill and leach stockpiles) and property, plant and equipment, and also includes the amortization of intangible assets and liabilities resulting from the acquisition totaling $755 million ($476 million to net income or $1.07 per share). |

| d. | Excludes net losses on early extinguishment of debt totaling $88 million ($69 million to net income or $0.15 per share) for financing transactions related to the acquisition of Phelps Dodge. |

| e. | Includes interest expense from the debt issued in connection with the acquisition of Phelps Dodge totaling $186 million ($145 million to net income or $0.33 per share). Also includes accretion on the fair value of environmental liabilities resulting from the acquisition totaling $24 million ($19 million to net income or $0.04 per share). |

| f. | Estimated pro forma diluted weighted-average shares of common stock outstanding for the three months ended March 31, 2007, follows (in millions): |

| Average number of basic shares of FCX common stock | | | |

| outstanding prior to the acquisition of Phelps Dodge | | 197 | |

| Shares of FCX common stock issued in the acquisition | | 137 | |

| Sale of shares of FCX common stock | | 47 | |

| Assumed conversion of Mandatory Convertible Preferred Stock | | 39 | |

| Assumed conversion of other dilutive securities | | 26 | |

| Pro forma weighted-average shares of FCX common stock outstanding | | 446 | |

| | | | |

The above pro forma consolidated information has been prepared for illustrative purposes only and is not intended to be indicative of the results that would actually have occurred, or the results expected in future periods, had the events reflected herein occurred on the dates indicated.

| 3. | DISCONTINUED OPERATIONS |

On October 31, 2007, FCX sold its international wire and cable business, PDIC, for $735 million, which resulted in a net loss of $14 million ($9 million to net income) for transaction-related costs. The transaction generated after-tax proceeds of approximately $650 million (net proceeds of $597 million after taxes, transaction-related costs and PDIC cash).

As a result of the sale, the operating results of PDIC have been removed from continuing operations in the consolidated statements of income. Selected financial information related to discontinued operations for the period March 20, 2007, through March 31, 2007, follows (in millions):

| Revenues | $ | 57 | |

| Operating income | | 7 | |

| Provision for income taxes | | 2 | |

| Income from discontinued operations | | 4 | |

| | | | |

| 4. | PENSION AND POSTRETIREMENT BENEFITS |

The components of net periodic benefit cost for pension and postretirement benefits (first-quarter 2007 included Phelps Dodge’s plans for the period March 20, 2007, through March 31, 2007) follow (in millions):

| | | Three Months Ended | |

| | | March 31, | |

| | | 2008 | | 2007 | |

| Service cost | | $ | 9 | | $ | 2 | |

| Interest cost | | | 27 | | | 6 | |

| Expected return on plan assets | | | (32 | ) | | (4 | ) |

| Amortization of prior service cost | | | 2 | | | 1 | |

| Net periodic benefit cost | | $ | 6 | | $ | 5 | |

| | | | | | | | |

The increase in service and interest costs and the expected return on plan assets resulted primarily from the impact of Phelps Dodge for a full three months in first-quarter 2008 compared with only 12 days in first-quarter 2007.

FCX’s basic net income per share of common stock was calculated by dividing net income applicable to common stock by the weighted-average shares of common stock outstanding during the period. The following is a reconciliation of net income and weighted-average shares of common stock outstanding for purposes of calculating diluted net income per share (in millions, except per share amounts):

| | | Three Months Ended | |

| | | March 31, | |

| | | 2008 | | 2007 | |

| Income from continuing operations | | $ | 1,186 | | $ | 489 | |

| Preferred dividends | | | (64 | ) | | (17 | ) |

| Income from continuing operations applicable to common stock | | | 1,122 | | | 472 | |

| Plus income impact of assumed conversion of: | | | | | | | |

| 6¾% Mandatory Convertible Preferred Stock | | | 49 | | | 2 | |

| 5½% Convertible Perpetual Preferred Stock | | | 15 | | | 15 | |

| Diluted net income from continuing operations applicable to common stock | | | 1,186 | | | 489 | |

| Income from discontinued operations | | | – | | | 4 | |

| Diluted net income applicable to common stock | | $ | 1,186 | | $ | 493 | |

| | | | | | | | |

| Weighted-average shares of common stock outstanding: | | | 383 | | | 217 | |

| Add stock issuable upon conversion, exercise or vesting of: | | | | | | | |

| 6¾% Mandatory Convertible Preferred Stock | | | 39 | | | 2 | |

| 5½% Convertible Perpetual Preferred Stock | | | 23 | | | 23 | |

| Dilutive stock options | | | 2 | | | 1 | |

| Restricted stock | | | 2 | | | 1 | |

| Weighted-average shares of common stock outstanding for purposes of | | | | | | | |

| calculating diluted net income per share | | | 449 | | | 244 | |

| | | | | | | | |

| Diluted net income per share of common stock: | | | | | | | |

| Continuing operations | | $ | 2.64 | | $ | 2.00 | |

| Discontinued operations | | | – | | | 0.02 | |

| Diluted net income per share of common stock | | $ | 2.64 | | $ | 2.02 | |

| | | | | | | | |

Outstanding stock options with exercise prices greater than the average market price of FCX’s common stock during the period are excluded from the computation of diluted net income per share of common stock. FCX’s convertible instruments are also excluded when including the conversion of these instruments increases reported diluted net income per share. No amounts were excluded for first-quarter 2008. Excluded amounts

were approximately one million stock options with a weighted-average exercise price of $63.76 in first-quarter 2007.

| 6. | INVENTORIES, AND MILL AND LEACH STOCKPILES |

The components of inventories follow (in millions):

| | | March 31, | | December 31, | |

| | | 2008 | | 2007 | |

| Mining Operations: | | | | | | | |

| Raw materials | | $ | 32 | | $ | 1 | |

| Work-in-process | | | 77 | | | 71 | |

Finished goodsa | | | 794 | | | 898 | |

| Atlantic Copper: | | | | | | | |

| Raw materials (concentrates) | | | 139 | | | 164 | |

| Work-in-process | | | 237 | | | 220 | |

| Finished goods | | | 17 | | | 6 | |

| Total product inventories | | | 1,296 | | | 1,360 | |

Total materials and supplies, netb | | | 891 | | | 818 | |

| Total inventories | | $ | 2,187 | | $ | 2,178 | |

| | | | | | | | |

| a. | Primarily includes concentrates and cathodes. |

| b. | Materials and supplies inventory is net of obsolescence reserves totaling $17 million at March 31, 2008, and $16 million at December 31, 2007. |

The following is a detail of mill and leach stockpiles (in millions):

| | | March 31, | | December 31, | |

| | | 2008 | | 2007 | |

| Current: | | | | | | | |

| Mill stockpiles | | $ | 4 | | $ | 6 | |

| Leach stockpiles | | | 769 | | | 701 | |

| Total current mill and leach stockpiles | | $ | 773 | | $ | 707 | |

| | | | | | | | |

Long-terma: | | | | | | | |

| Mill stockpiles | | $ | 279 | | $ | 248 | |

| Leach stockpiles | | | 874 | | | 858 | |

| Total long-term mill and leach stockpiles | | $ | 1,153 | | $ | 1,106 | |

| | | | | | | | |

| a. | Metals in stockpiles not expected to be recovered within the next 12 months. |

FCX’s first-quarter 2008 income tax provision from continuing operations resulted from taxes on international operations ($579 million) and U.S. taxes ($150 million). The difference between FCX’s consolidated effective income tax rate of approximately 33 percent for first-quarter 2008 and the U.S. federal statutory rate of 35 percent primarily was attributable to a U.S. benefit for percentage depletion and an international tax rate differential, partially offset by withholding taxes on earnings from Indonesia and South America mining operations and a U.S. foreign tax credit limitation.

FCX’s first-quarter 2007 income tax provision from continuing operations resulted from taxes on earnings at international operations ($504 million), partially offset by a tax benefit from losses in the U.S. ($46 million). The first-quarter 2007 income tax provision primarily related to the operations of PT Freeport Indonesia and also included $31 million associated with Phelps Dodge’s earnings for the 12-day period ending March 31, 2007. The difference between FCX’s consolidated effective income tax rate of approximately 43 percent for first-

quarter 2007 and the U.S. federal statutory rate of 35 percent primarily was attributable to withholding taxes incurred in connection with earnings from Indonesia mining operations.

Interest expense excludes capitalized interest of $22 million in first-quarter 2008 and $7 million in first-quarter 2007.

| 9. | NEW ACCOUNTING STANDARDS |

Fair Value Measurements. In September 2006, the Financial Accounting Standards Board (FASB) issued SFAS No. 157, “Fair Value Measurements,” which provides enhanced guidance for using fair value to measure assets and liabilities. SFAS No. 157 does not require any new fair value measurements under U.S. GAAP but rather establishes a common definition of fair value, provides a framework for measuring fair value under U.S. GAAP and expands disclosure requirements about fair value measurements. In February 2008, FASB issued FSP FAS 157-2, which delays the effective date of SFAS No. 157 for nonfinancial assets or liabilities that are not required or permitted to be measured at fair value on a recurring basis to fiscal years beginning after November 15, 2008, and interim periods within those years. Effective January 1, 2008, FCX adopted SFAS No. 157 for financial assets and liabilities recognized at fair value on a recurring basis. This partial adoption of SFAS No. 157 did not have a material impact on our financial reporting and disclosures as FCX’s financial assets are measured using quoted market prices, or Level 1 inputs. FCX is currently evaluating the impact that the adoption of SFAS No. 157 will have on its financial reporting and disclosures for pension and postretirement related financial assets and nonfinancial assets or liabilities not valued on a recurring basis (at least annually).

Disclosures about Derivative Instruments and Hedging Activities. In March 2008, FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging Activities – an amendment of FASB Statement No. 133.” SFAS No. 161 amends the disclosure requirements for derivative instruments and hedging activities contained in SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities.” Under SFAS No 161, entities are required to provide enhanced disclosures about (i) how and why an entity uses derivative instruments, (ii) how derivative instruments and related hedged items are accounted for under SFAS No. 133 and related interpretations and (iii) how derivative instruments and related hedged items affect an entity’s financial position, financial performance and cash flows. SFAS No. 161 is effective for fiscal years and interim periods beginning after November 15, 2008, with early application encouraged. SFAS No. 161 encourages, but does not require disclosure for earlier periods presented for comparative purposes at initial adoption. The adoption of SFAS No. 161 will not affect FCX’s accounting for derivative financial instruments; however, FCX is currently evaluating the impact on its related disclosures.

FCX has a regional approach to the management of its mining operations. FCX has organized its mining operations geographically into three primary operating divisions – North America mining, South America mining and Indonesia mining. Notwithstanding this geographic structure, FCX internally reports information on a mine by mine basis. Therefore, in accordance with SFAS No. 131, “Disclosures about Segments of an Enterprise and Related Information,” FCX concluded that its operating segments include individual mines. Operating segments that meet SFAS No. 131 thresholds are reportable segments. FCX has revised its segment disclosures for first-quarter 2007 to conform with current year presentation. Further discussion of the reportable segments included in FCX’s primary operating divisions, as well as FCX’s other reportable segment – Atlantic Copper Smelting & Refining, follows.

North America Mining. North America mining operations are comprised of copper operations from mining through rod production, molybdenum operations from mining through conversion to chemical and metallurgical products, and the marketing and sale of both product lines. FCX has six operating copper mines in North America – Morenci, Bagdad, Sierrita and Safford in Arizona and Chino and Tyrone in New Mexico, as well as one operating molybdenum mine – Henderson in Colorado. The North America mining division includes the Morenci copper mine, Rod & Refining operations and Molybdenum operations as reportable segments.

Morenci. The Morenci open-pit mine, located in southeastern Arizona, primarily produces copper cathodes and copper concentrates. In addition to copper, the Morenci mine produces molybdenum concentrates as a by-product. FCX owns an 85 percent undivided interest in Morenci via an unincorporated joint venture.

Rod & Refining. The Rod & Refining segment consists of copper conversion facilities, including a refinery, rod mills and a specialty copper products facility. This segment processes copper produced at FCX’s North America mines and purchased copper into copper anode, cathode, rod and custom copper shapes. At times this segment refines copper and produces copper rod and shapes for customers on a toll basis. Toll arrangements require the tolling customer to deliver appropriate copper-bearing material to FCX’s facilities for processing into a product that is returned to the customer, who pays FCX for processing its material into the specified products.

Molybdenum. The Molybdenum segment includes FCX’s wholly owned Henderson molybdenum mine in Colorado, related conversion facilities and a technology center. The Henderson underground mine produces high-purity, chemical-grade molybdenum concentrates, which are typically further processed into value-added molybdenum chemical products. This segment is an integrated producer of molybdenum, with mining, roasting and processing facilities that produce high-purity, molybdenum-based chemicals, molybdenum metal powder and metallurgical products, which are sold to customers around the world. This segment also includes a sales company that purchases molybdenum from Henderson and FCX’s North America and South America copper mines and sells it to third parties. In addition, at times this segment roasts and/or processes material on a toll basis. Toll arrangements require the tolling customer to deliver appropriate molybdenum-bearing material to FCX’s facilities for processing into a product that is returned to the customer, who pays FCX for processing its material into the specified products. This segment also includes a technology center whose primary activity is developing new engineered products and applications.

The Molybdenum segment also includes FCX’s wholly owned Climax molybdenum mine in Colorado, which has been on care-and-maintenance status since 1995. In December 2007, FCX announced a $500 million project to restart the Climax mine with start up expected in 2010.

Other North America Mining Operations. Other North America mining operations include FCX’s other operating southwestern U.S. copper mines – Bagdad, Sierrita, Safford, Chino and Tyrone. In addition to copper, the Bagdad, Sierrita and Chino mines produce molybdenum, gold and silver, and the Sierrita mine also produces rhenium. Other North America mining operations also include the Miami copper mine, which FCX is undertaking a project to restart; the Miami smelter, which processes our North America concentrates and provides a significant source of sulfuric acid for the various North America leaching operations; and a sales company, which functions as an agent to purchase and sell copper from the North America mines and the Rod & Refining operations and also purchases and sells any copper not sold by the South America mines to third parties.

South America Mining. FCX has four operating copper mines in South America – Cerro Verde in Peru, and Candelaria, Ojos del Salado and El Abra in Chile. These operations include open-pit and underground mining, sulfide ore concentrating, leaching, solution extraction and electrowinning (SX/EW). The South America mining division includes the Cerro Verde copper mine as a reportable segment.

Cerro Verde. The Cerro Verde open-pit copper mine, located near Arequipa, Peru, produces copper cathodes and copper concentrates. In addition to copper, the Cerro Verde mine produces molybdenum concentrates. FCX owns a 53.56 percent interest in Cerro Verde.

Other South America Mining Operations. Other South America mining operations include FCX’s Chilean copper mines – Candelaria, Ojos del Salado and El Abra – which include open-pit and underground mining, sulfide ore concentrating, leaching and SX/EW operations. In addition to copper, the Candelaria and Ojos del Salado mines produce gold and silver. FCX owns an 80 percent interest in both the Candelaria and Ojos del Salado mines, and owns a 51 percent interest in the El Abra mine.

Indonesia Mining. Indonesia mining includes PT Freeport Indonesia’s Grasberg copper and gold mining operations and PT Puncakjaya Power’s power-generating operations (after eliminations with PT Freeport Indonesia). FCX owns 90.64 percent of PT Freeport Indonesia, including 9.36 percent owned through PT Indocopper Investama, and the remaining 9.36 percent is owned by the Government of Indonesia. In 1996, FCX established an unincorporated joint venture with Rio Tinto, which covers PT Freeport Indonesia’s mining operations in Block A and gives Rio Tinto, through 2021, a 40 percent interest in certain assets and future production exceeding specified annual amounts of copper, gold and silver. After 2021, Rio Tinto will have a 40 percent interest in all production from Block A.

Atlantic Copper Smelting & Refining. Atlantic Copper, FCX’s wholly owned smelting unit in Spain, smelts and refines copper concentrates and markets refined copper and precious metals in slimes.

Other. Intersegment sales by the Indonesia and South America mines are based on similar arms-length transactions with third parties at the time of the sale. Intersegment sales of any individual mine may not be reflective of the actual prices ultimately realized because of a variety of factors, including additional processing, timing of sales to unaffiliated customers and transportation premiums.

FCX allocates certain operating costs, expenses and capital to the operating divisions and individual segments. However, not all costs and expenses applicable to a mine or operation are allocated. All federal and state income taxes are recorded and managed at the corporate level with the exception of foreign income taxes, which are generally recorded and managed at the applicable mine or operation. Accordingly, the following segment information reflects management determinations that may not be indicative of what the actual financial performance of each operating division or segment would be if it was an independent entity.

Business Segments

| (In Millions) | North America | | South America | | Indonesia | | | | | | | |

| | | | | | | | | Other | | Total | | | | Other | | Total | | | | Atlantic | | Corporate, | | | |

| | | | | | | | | North | | North | | | | South | | South | | | | Copper | | Other & | | | |

| | | | | Rod & | | Molyb- | | America | | America | | Cerro | | America | | America | | | | Smelting | | Elimi- | | FCX | |

| First-Quarter 2008 | Morenci | | Refining | | denum | | Mining | | Mining | | Verde | | Mining | | Mining | | Grasberg | | & Refining | | nations | | Total | |

| Revenues: | | | | | | | | | | | | | | | | | | | | | | | | | |

| Unaffiliated customers | $ | 50 | | $ | 1,680 | | $ | 719 | | $ | 823 | | $ | 3,272 | | $ | 462 | | $ | 503 | | $ | 965 | | $ | 887 | a | $ | 665 | | $ | (117 | ) | $ | 5,672 | |

| Intersegment | | 541 | | 8 | | – | | (548 | ) | 1 | | 253 | | 375 | | 628 | | 165 | | – | | (794 | ) | – | |

Production and deliveryb | | 272 | | 1,676 | | 460 | | (270 | ) | 2,138 | | 162 | | 270 | | 432 | | 399 | | 651 | | (898 | ) | 2,722 | |

Depreciation, depletion and amortizationb | | 81 | | 2 | | 39 | | 105 | | 227 | | 43 | | 87 | | 130 | | 45 | | 9 | | 7 | | 418 | |

| Exploration and research expenses | | – | | – | | – | | – | | – | | – | | – | | – | | – | | – | | 52 | | 52 | |

| Selling, general and administrative expenses | | – | | – | | 6 | | 4 | | 10 | | – | | – | | – | | 37 | | 8 | | 29 | | 84 | |

Operating income (loss)b | | 238 | | 10 | | 214 | | 436 | | 898 | | 510 | | 521 | | 1,031 | | 571 | | (3 | ) | (101 | ) | 2,396 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest expense, net | | 1 | | 1 | | – | | 10 | | 12 | | 1 | | – | | 1 | | 1 | | 4 | | 147 | | 165 | |

| Provision for income taxes | | – | | – | | – | | – | | – | | 173 | | 160 | | 333 | | 239 | | – | | 157 | | 729 | |

| Goodwill | | 1,912 | | – | | 703 | | 2,299 | | 4,914 | | 763 | | 366 | | 1,129 | | – | | – | | 5 | | 6,048 | |

| Total assets at March 31, 2008 | | 6,932 | | 604 | | 4,179 | | 12,746 | | 24,461 | | 5,464 | | 4,833 | | 10,297 | | 3,932 | | 994 | | 2,144 | | 41,828 | |

| Capital expenditures | | 77 | | 3 | | 12 | | 83 | | 175 | | 17 | | 46 | | 63 | | 115 | | 5 | | 150 | | 508 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| First-Quarter 2007 | | | | | | | | | | | | | | | | | | | | | | | | | |

| Revenues: | | | | | | | | | | | | | | | | | | | | | | | | | |

| Unaffiliated customers | | – | | 206 | | 52 | | 61 | | 319 | | 14 | | 126 | | 140 | | 1,332 | a | 454 | | 1 | | 2,246 | |

| Intersegment | | 21 | | 2 | | – | | (23 | ) | – | | 97 | | 25 | | 122 | | 377 | | – | | (499 | ) | – | |

Production and deliveryb | | 29 | | 206 | | 52 | | 40 | | 327 | | 44 | | 72 | | 116 | | 323 | | 427 | | (290 | ) | 903 | |

Depreciation, depletion and amortizationb | | 5 | | – | | 3 | | 6 | | 14 | | 9 | | 19 | | 28 | | 59 | | 10 | | 5 | | 116 | |

| Exploration and research expenses | | – | | – | | – | | – | | – | | – | | – | | – | | – | | – | | 7 | | 7 | |

| Selling, general and administrative expenses | | – | | – | | – | | 1 | | 1 | | – | | – | | – | | 44 | | 4 | | (1 | ) | 48 | |

Operating income (loss)b | | (13 | ) | 2 | | (3 | ) | (9 | ) | (23 | ) | 58 | | 60 | | 118 | | 1,283 | | 13 | | (219 | ) | 1,172 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest expense, net | | – | | – | | – | | – | | – | | – | | – | | – | | 4 | | 7 | | 41 | | 52 | |

| Provision for income taxes | | – | | – | | – | | – | | – | | 22 | | 19 | | 41 | | 462 | | – | | (45 | ) | 458 | |

| Total assets at March 31, 2007 | | 4,775 | | 631 | | 1,918 | | 8,705 | | 16,029 | | 4,011 | | 4,491 | | 8,502 | | 4,549 | | 1,075 | | 11,279 | c | 41,434 | |

| Capital expenditures | | 15 | | 1 | | 2 | | 35 | | 53 | | 1 | | 1 | | 2 | | 74 | | 7 | | 6 | | 142 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| a. | Includes PT Freeport Indonesia’s sales to PT Smelting totaling $464 million in first-quarter 2008 and $584 million in first-quarter 2007. |

| b. | The following tables summarize the impact of purchase accounting fair value adjustments on first-quarters 2008 and 2007 operating income (loss) primarily associated with the impacts of the increases in the carrying values of Phelps Dodge’s metals inventories (including mill and leach stockpiles) and property, plant and equipment: |

| First-Quarter 2008 | | | | | | | | | | | | | | | | | | | | | | | | | |

| Production and delivery | $ | (18 | ) | $ | – | | $ | (14 | ) | $ | (15 | ) | $ | (47 | ) | $ | (9 | ) | $ | (16 | ) | $ | (25 | ) | N/A | | N/A | | $ | – | | $ | (72 | ) |

| Depreciation, depletion and amortization | | (47 | ) | – | | (34 | ) | (55 | ) | (136 | ) | (21 | ) | (49 | ) | (70 | ) | N/A | | N/A | | (1 | ) | (207 | ) |

| Reduction of operating income | $ | (65 | ) | $ | – | | $ | (48 | ) | $ | (70 | ) | $ | (183 | ) | $ | (30 | ) | $ | (65 | ) | $ | (95 | ) | N/A | | N/A | | $ | (1 | ) | $ | (279 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| First-Quarter 2007 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Production and delivery | $ | (16 | ) | $ | – | | $ | (13 | ) | $ | (19 | ) | $ | (48 | ) | $ | (20 | ) | $ | (28 | ) | $ | (48 | ) | N/A | | N/A | | $ | – | | $ | (96 | ) |

| Depreciation, depletion and amortization | | (3 | ) | – | | (2 | ) | (1 | ) | (6 | ) | (6 | ) | (15 | ) | (21 | ) | N/A | | N/A | | (1 | ) | (28 | ) |

| Reduction of operating income | $ | (19 | ) | $ | – | | $ | (15 | ) | $ | (20 | ) | $ | (54 | ) | $ | (26 | ) | $ | (43 | ) | $ | (69 | ) | N/A | | N/A | | $ | (1 | ) | $ | (124 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| c. | Includes preliminary goodwill of $6.9 billion, which had not yet been allocated to reporting units, and also includes assets of $1.1 billion associated with discontinued operations (see Note 3). |

TO THE BOARD OF DIRECTORS AND STOCKHOLDERS OF

FREEPORT-McMoRan COPPER & GOLD INC.

We have reviewed the condensed consolidated balance sheet of Freeport-McMoRan Copper & Gold Inc. as of March 31, 2008, the related consolidated statements of income and cash flows for the three-month periods ended March 31, 2008 and 2007, and the related consolidated statement of stockholders’ equity for the three-month period ended March 31, 2008. These financial statements are the responsibility of the Company’s management.

We conducted our review in accordance with the standards of the Public Company Accounting Oversight Board (United States). A review of interim financial information consists principally of applying analytical procedures and making inquiries of persons responsible for financial and accounting matters. It is substantially less in scope than an audit conducted in accordance with the standards of the Public Company Accounting Oversight Board, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Accordingly, we do not express such an opinion.

Based on our review, we are not aware of any material modifications that should be made to the condensed consolidated financial statements referred to above for them to be in conformity with U.S. generally accepted accounting principles.

We have previously audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Freeport-McMoRan Copper & Gold Inc. as of December 31, 2007, and the related consolidated statements of income, cash flows, and stockholders’ equity for the year then ended (not presented herein), and in our report dated February 29, 2008, we expressed an unqualified opinion on those consolidated financial statements and which report included an explanatory paragraph for the Company’s adoption of FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes – an interpretation of FASB Statement No. 109,” effective January 1, 2007; Statement of Financial Accounting Standards (SFAS) No. 123 (revised 2004), “Share-Based Payment,” effective January 1, 2006; Emerging Issues Task Force Issue No. 04-6, “Accounting for Stripping Costs Incurred during Production in the Mining Industry,” effective January 1, 2006; and SFAS No. 158, “Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans, an amendment of FASB Statements No. 87, 88, 106 and 132R,” effective December 31, 2006. In our opinion, the information set forth in the accompanying condensed consolidated balance sheet as of December 31, 2007, is fairly stated, in all material respects, in relation to the consolidated balance sheet from which it has been derived.

ERNST & YOUNG LLP

Phoenix, Arizona

May 6, 2008

OVERVIEW

In Management’s Discussion and Analysis of Financial Condition and Results of Operations, “we,” “us” and “our” refer to Freeport-McMoRan Copper & Gold Inc. (FCX) and its consolidated subsidiaries, including, except as otherwise stated, Phelps Dodge Corporation (Phelps Dodge) and its subsidiaries, which we acquired on March 19, 2007. You should read this discussion in conjunction with our financial statements, the related Management’s Discussion and Analysis of Financial Condition and Results of Operations and the discussion of our “Business and Properties” in our Form 10-K for the year ended December 31, 2007, filed with the Securities and Exchange Commission. The results of operations reported and summarized below are not necessarily indicative of future operating results. In particular, the financial results included for 2007 include the operations of Phelps Dodge for only 12 days, not the full first quarter of 2007 because of the accounting treatment for the acquisition. References to “Notes” are Notes included in our “Notes to Consolidated Financial Statements.” Throughout Management's Discussion and Analysis of Financial Condition and Results of Operations all references to earnings or losses per share are on a diluted basis, unless otherwise noted.

We are one of the world’s largest copper, gold and molybdenum mining companies in terms of reserves and production. One of our principal assets is the Grasberg minerals district in Indonesia, which contains the largest single recoverable copper reserve and the largest single gold reserve of any mine in the world based on the latest available reserve data provided by third-party industry consultants.

On March 19, 2007, we acquired Phelps Dodge, a fully integrated producer of copper and molybdenum, with mines in North and South America and processing capabilities for other by-product minerals, such as gold, silver and rhenium, and several development projects, including Tenke Fungurume in the Democratic Republic of Congo (DRC).

In North America, we have six operating copper mines – Morenci, Bagdad, Sierrita and Safford in Arizona and Chino and Tyrone in New Mexico, as well as one operating molybdenum mine – Henderson in Colorado. In addition, we are restarting the Miami copper mine in Arizona and the Climax molybdenum mine in Colorado. All of these mining operations are wholly owned, except for Morenci. We have an 85 percent undivided interest in Morenci, an unincorporated joint venture. The North America mining operations are operated in an integrated fashion and have long-lived reserves with additional development potential.

In South America, we have four operating copper mines – Cerro Verde in Peru, and Candelaria, Ojos del Salado and El Abra in Chile. We own a 53.56 percent interest in Cerro Verde, an 80 percent interest in both Candelaria and Ojos del Salado and a 51 percent interest in El Abra.

We own 90.64 percent of PT Freeport Indonesia, including 9.36 percent owned through our wholly owned subsidiary, PT Indocopper Investama. The Government of Indonesia owns the remaining 9.36 percent of PT Freeport Indonesia. PT Freeport Indonesia operates under an agreement, called a Contract of Work, with the Government of Indonesia. The Contract of Work allows us to conduct exploration, mining and production activities in a 24,700-acre area called Block A located in Papua, Indonesia. Under the Contract of Work, PT Freeport Indonesia also conducts exploration activities (which had been suspended, but resumed in 2007) in an approximate 500,000-acre area called Block B in Papua. All of PT Freeport Indonesia’s proven and probable mineral reserves and current mining operations, including the Grasberg minerals district, are located in Block A.

We also operate Atlantic Copper S.A. (Atlantic Copper), a wholly owned subsidiary, located in Spain. Atlantic Copper’s operations involve the smelting and refining of copper concentrates and the marketing of refined copper and precious metals in slimes. Additionally, PT Freeport Indonesia owns a 25 percent interest in PT Smelting, an Indonesian company, which operates a copper smelter and refinery in Gresik, Indonesia.

Phelps Dodge also had an international manufacturing division, Phelps Dodge International Corporation (PDIC), which manufactured engineered wire and cable products principally for the global energy sector. On October 31, 2007, we sold PDIC, and as a result, the operating results of PDIC for the 12-day period ended March 31, 2007, have been removed from continuing operations and reported as discontinued operations in the consolidated statements of income.

ACQUISITION OF PHELPS DODGE

Phelps Dodge became our wholly owned subsidiary on March 19, 2007. In the acquisition, each share of Phelps Dodge common stock was exchanged for 0.67 of a share of FCX common stock and $88.00 in cash. As a result, we issued 136.9 million shares and paid $18.0 billion in cash to Phelps Dodge shareholders for total consideration of $25.8 billion. The results of Phelps Dodge’s operations are included in our consolidated financial statements beginning March 20, 2007.

Accounting for the Acquisition. The acquisition of Phelps Dodge was accounted for under the purchase method as required by Statement of Financial Accounting Standards (SFAS) No. 141, “Business Combinations,” with FCX as the accounting acquirer. In accordance with the purchase method of accounting, the purchase price has been allocated to the assets acquired and liabilities assumed based upon their fair values on the acquisition date of March 19, 2007. In valuing acquired assets and assumed liabilities, fair values were based on, but were not limited to: quoted market prices, where available; our intent with respect to whether the assets purchased were to be held, sold or abandoned; expected future cash flows; current replacement cost for similar capacity for certain fixed assets; market rate assumptions for contractual obligations; and appropriate discount rates and growth rates. The excess of the purchase price over the fair value of net tangible and identifiable intangible assets has been recorded as goodwill. At March 31, 2008, the carrying value of goodwill associated with our acquisition of Phelps Dodge totaled approximately $6.0 billion (refer to Note 2 for further discussion of goodwill and to Note 10 for the allocation of goodwill to our reportable segments).

The following table summarizes the impacts of purchase accounting fair value adjustments on first-quarter 2008 and 2007 operating income and income from continuing operations, which are primarily associated with increases in the carrying values of Phelps Dodge’s property, plant and equipment and metal inventories, including mill and leach stockpiles (in millions):

| | First-Quarter | | |

| | 2008 | | 2007a | | |

| Purchase accounting impacts: | | | | | | | |

| Depreciation, depletion and amortization | $ | 207 | | $ | 28 | | |

| Production and delivery costs | | 72 | | | 96 | | |

| Reduction of operating income | $ | 279 | | $ | 124 | | |

| | | | | | | | |

| Reduction of income from continuing operations | $ | 184 | b | $ | 79 | | |

| a. | Represents purchase accounting impacts for the 12-day period ended March 31, 2007. |

| b. | Includes net purchase accounting fair value adjustments related to other non-operating income and expenses of $15 million ($9 million to net income). |

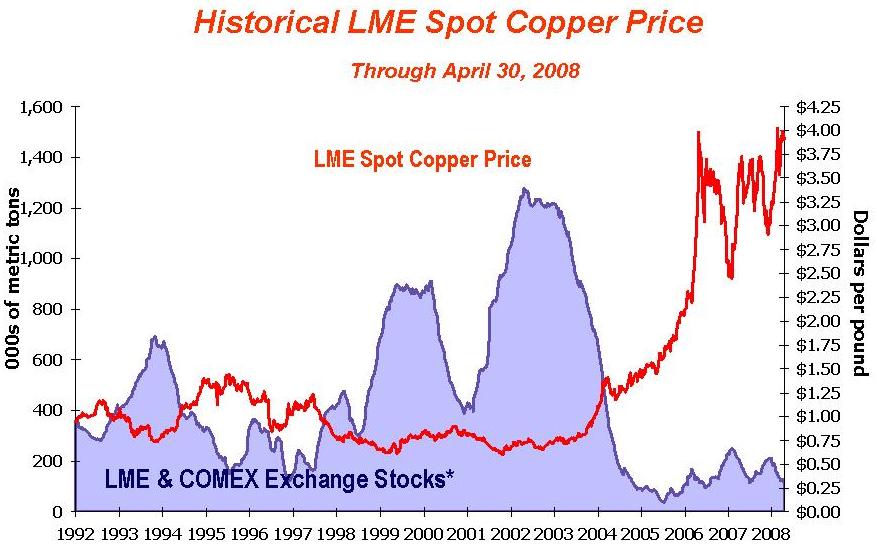

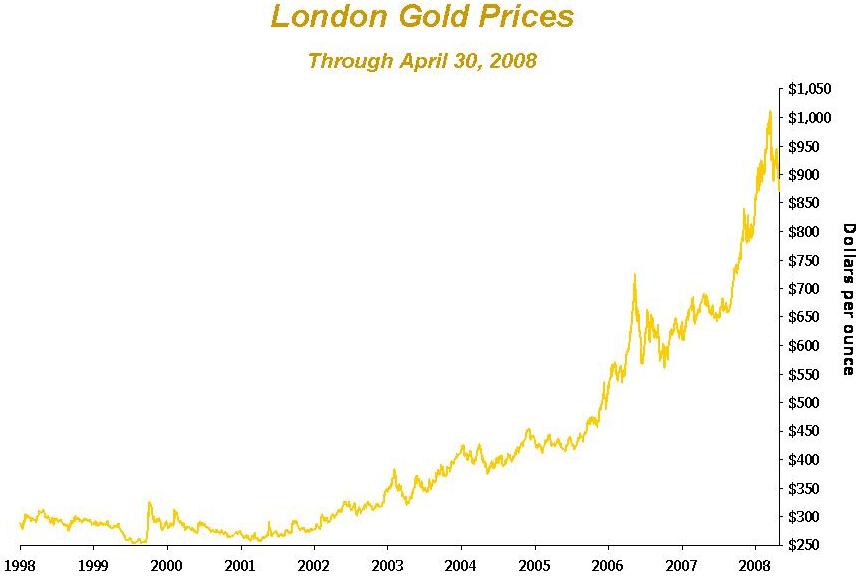

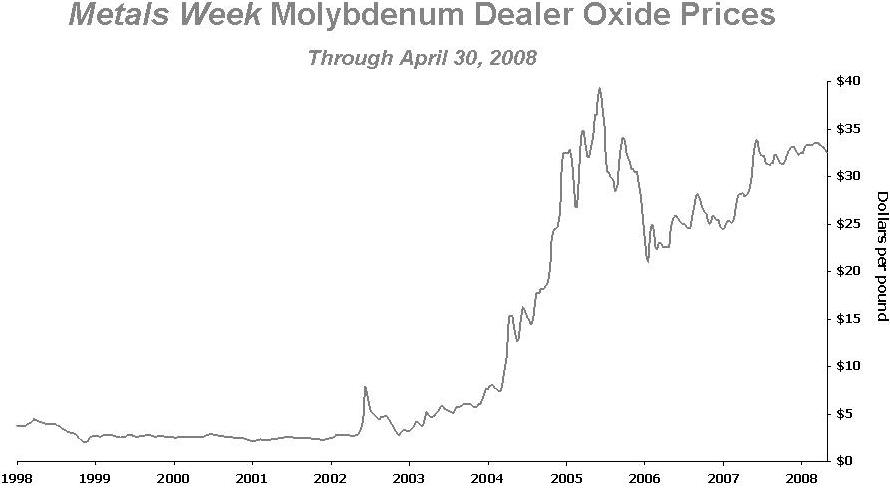

COPPER, GOLD AND MOLYBDENUM MARKETS

The graphs below are intended to illustrate the movements in metals prices during the periods presented. World metal prices for copper have fluctuated significantly from 1992 through April 2008, with the London Metal Exchange (LME) spot copper price varying from a low of $0.60 per pound in 2001 to record highs above $4.00 per pound in March 2008. World gold prices have also fluctuated widely from 1998 through April 2008 from a low of approximately $250 per ounce in 1999 to record highs above $1,000 per ounce in March 2008. During the period from 1998 through April 2008, Metals Week Molybdenum Dealer Oxide prices have ranged from a low of $2.00 per pound in 1998 to a high of $40.00 per pound in 2005. Copper, gold and molybdenum prices are affected by numerous factors beyond our control as described further in our “Risk Factors” contained in Part I, Item 1A of our Form 10-K for the year ended December 31, 2007.

* Excludes Shanghai stocks, producer, consumer and merchant stocks.

The graph above presents LME spot copper prices and reported stocks of copper at the LME and New York Commodity Exchange (COMEX) through April 30, 2008. Since 2003 global demand has exceeded supply, evidenced by the decline in exchange warehouse inventories. Combined LME and COMEX stocks of approximately 123,000 metric tons at March 31, 2008, remain at historically low levels, representing less than three days of global consumption. Disruptions associated with strikes, unrest and other operational issues resulted in low levels of inventory throughout 2006 and 2007. During first-quarter 2008, copper prices were strong, with LME copper prices ranging from $3.02 per pound to record highs above $4.00 per pound and averaging $3.52 per pound. Future copper prices may continue to be volatile and are expected to be influenced by demand from China, economic activity in the United States (U.S.) and other industrialized countries, the timing of the development of new supplies of copper, production levels of mines and copper smelters and the level of direct participation by investors. We consider the current underlying supply and demand conditions in the global copper markets to be positive for our company and continue to pursue opportunities to expand production. The LME spot price closed at $3.93 per pound on April 30, 2008.

Gold prices continue to be supported by increased investment demand for gold, ongoing geopolitical tensions, a weak U.S. dollar, inflationary pressures and reduced mine supply. During first-quarter 2008, gold prices ranged from approximately $847 per ounce to record highs above $1,000 per ounce and averaged approximately $925 per ounce. On April 30, 2008, London gold prices closed at approximately $871 per ounce.

Molybdenum markets have been strong in recent years with growing demand and limited supply. During first-quarter 2008, molybdenum prices ranged from $32.00 per pound to $33.80 per pound and averaged $33.24 per pound. The Metals Week Molybdenum Dealer Oxide price closed at $32.45 per pound on April 28, 2008.

OUTLOOK

Consolidated sales volumes for first-quarter 2008 totaled 911 million pounds of copper, 280 thousand ounces of gold and 20 million pounds of molybdenum, compared with 520 million pounds of copper, 956 thousand ounces of gold and 2 million pounds of molybdenum for first-quarter 2007. Pro forma sales volumes for first-quarter 2007, including Phelps Dodge sales volumes prior to the acquisition, totaled 1.0 billion pounds of copper, 977 thousand ounces of gold and 19 million pounds of molybdenum.

Because of mine sequencing at Grasberg and the ramp up of production at the Safford mine, second-half 2008 production and sales are expected to be higher than the first half of 2008. Approximately 56 percent of projected 2008 copper sales and 64 percent of projected 2008 gold sales are expected in the second half of the year. Projected consolidated sales volumes for the full year 2008 are estimated to be 4.2 billion pounds of copper, 1.4 million ounces of gold and 75 million pounds of molybdenum, including 930 million pounds of copper, 225 thousand ounces of gold and 18 million pounds of molybdenum for second-quarter 2008. Achievement of these sales estimates depends on the achievement of targeted mining rates and expansion plans, the successful operation of production facilities, the impact of weather conditions and other factors. Additionally, sales volumes may vary from these estimates depending on the areas being mined within the Grasberg open pit, with quarterly sales volumes expected to vary significantly. Refer to “Mining Operations” for further discussion of sales volumes at our North America, South America and Indonesia mining operations.

Consolidated revenues, operating cash flows and net income vary significantly with fluctuations in the market prices of copper, gold and molybdenum, sales volumes and other factors. Based on projected consolidated sales volumes (excluding purchased copper and molybdenum) for 2008 and assuming an average price of $3.75 per pound of copper, $900 per ounce of gold and $30 per pound of molybdenum for the remainder of 2008, our consolidated operating cash flow would exceed $6.5 billion in 2008, including net reductions for estimated working capital requirements totaling $1.1 billion. Each $0.20 per pound change in copper prices for the balance of the year would have an approximate $450 million impact on 2008 operating cash flows.

CONSOLIDATED RESULTS

| | First-Quarter | |

| | 2008 | | 2007 | |

Financial Data (in millions, except per share amounts) | | | | | | |

| Revenues | $ | 5,672 | a | $ | 2,246 | a,b |

| Operating income | | 2,396 | a,c | | 1,172 | a,b,c |

Income from continuing operations applicable to common stockd | | 1,122 | c,e | | 472 | b,c,f |

Net income applicable to common stockd | | 1,122 | c,e | | 476 | b,c,f |

Diluted net income per share of common stockg: | | | | | | |

| Continuing operations | $ | 2.64 | | $ | 2.00 | |

| Discontinued operations | | – | | | 0.02 | |

Diluted net income per share of common stockh | $ | 2.64 | c,e | $ | 2.02 | b,c,f |

Diluted average common shares outstandingg,h | | 449 | | | 244 | |

| | | | | | | |

| Operating Data - Sales from Mines, Excluding Sales of Purchased Metal | | | | | | |

| Copper | | | | | | |

| Consolidated share (millions of recoverable pounds) | | 911 | | | 520 | |

| Average realized price per pound | $ | 3.69 | | $ | 3.00 | b |

| Gold | | | | | | |

| Consolidated share (thousands of recoverable ounces) | | 280 | | | 956 | |

| Average realized price per ounce | $ | 932.55 | | $ | 654.63 | |

| Molybdenum | | | | | | |

| Consolidated share (millions of recoverable pounds) | | 20 | | | 2 | |

| Average realized price per pound | $ | 31.67 | | | 23.26 | |

| a. | A summary of revenues and operating income (loss) by operating division, for first-quarter 2008 and 2007 follows (in millions): |

| | First-Quarter 2008 | | | First-Quarter 2007 | |

| | | | Operating | | | | | Operating | |

| | | | Income | | | | | Income | |

| | Revenues | | (Loss) | | | Revenues | | (Loss) | |

| North America mining | $ | 3,273 | | $ | 898 | | | $ | 319 | | $ | (23 | ) |

| South America mining | | 1,593 | | | 1,031 | | | | 262 | | | 118 | |

| Indonesia mining | | 1,052 | | | 571 | | | | 1,709 | | | 1,283 | |

| Atlantic Copper smelting & refining | | 665 | | | (3 | ) | | | 454 | | | 13 | |

| Corporate, other & eliminations | | (911 | ) | | (101 | ) | | | (498 | ) | | (219 | ) |

| Total FCX | $ | 5,672 | | $ | 2,396 | | | $ | 2,246 | | $ | 1,172 | |

Refer to Note 10 for further discussion of our operating divisions.

| b. | Includes charges to revenues for mark-to-market accounting adjustments on the 2007 copper price protection program totaling $38 million ($23 million to net income or $0.10 per share) and a reduction in average realized copper prices of $0.07 per pound. |

| c. | First-quarter 2008 includes the impact of purchase accounting fair value adjustments associated with the acquisition of Phelps Dodge totaling $279 million to operating income ($175 million to net income or $0.39 per share), and also includes $9 million to net income or $0.02 per share for other non-operating income and expenses. First-quarter 2007 includes impacts totaling $124 million to operating income ($79 million to net income or $0.32 per share). |

| d. | After preferred dividends. |

| e. | Includes a loss on early extinguishment of debt totaling $6 million ($5 million to net income or $0.01 per share) associated with an open-market purchase of our 9.5% Senior Notes. |

| f. | Includes net losses on early extinguishment of debt totaling $88 million ($75 million to net income or $0.31 per share) primarily related to premiums paid and the accelerated recognition of deferred financing costs associated with prepayments of debt. |

| g. | Reflects assumed conversion of our 7% Convertible Senior Notes, 5½% Convertible Perpetual Preferred Stock and 6¾% Mandatory Convertible Preferred Stock. |

| h. | On March 19, 2007, we issued 137 million common shares to acquire Phelps Dodge, and on March 28, 2007, we sold 47 million common shares. Common shares outstanding on March 31, 2008, totaled 383 million. Assuming conversion of the instruments discussed in Note g above and including dilutive stock options and restricted stock units, total common shares outstanding would approximate 449 million at March 31, 2008. |

Revenues

Consolidated revenues include the sales of copper, gold, molybdenum and other metals and metal-related products by our North and South America mining operations, our Indonesia mining operation’s sale of copper concentrates, which also contain significant quantities of gold and silver, and the sale by Atlantic Copper of copper anodes, copper cathodes, and gold in anodes and slimes. Consolidated revenues for first-quarter 2008 were approximately $3.4 billion higher than first-quarter 2007. The increase in revenues reflects higher overall copper and molybdenum sales volumes because of a full three months of activity from Phelps Dodge operations, compared with only 12 days in first-quarter 2007. Higher first-quarter 2008 revenues also reflect higher copper, gold and molybdenum prices. These favorable factors were partly offset by lower copper and gold sales volumes at our Indonesia mining operations associated with mining lower-grade ore during first-quarter 2008 (refer to “Indonesia Mining” for further discussion).

Approximately two-thirds of our copper is sold in concentrate and cathodes and the remaining one-third is sold primarily as rod (principally from our North America operations). Substantially all of our concentrate sales contracts and some of our cathode sales contracts provide final copper pricing in a specified future period (generally one to four months from the shipment date) based on quoted LME or COMEX prices. We ultimately receive market prices based on prices in the specified future period; however, the accounting rules applied to these sales result in changes recorded to revenues until the specified future period. We record revenues and

invoice customers at the time of shipment based on then-current LME or COMEX prices, which results in an embedded derivative on our provisional priced concentrate and cathode sales that is adjusted to fair value through earnings each period until the date of final pricing. To the extent final prices are higher or lower than what was recorded on a provisional basis, an increase or decrease to revenues is recorded each reporting period until the date of final pricing. Accordingly, in times of rising copper prices, our revenues during a quarter benefit from higher prices received for contracts priced at current market rates and also from an increase related to the final pricing of provisionally priced contracts entered into in prior periods; in times of falling copper prices, the opposite occurs.

While first-quarter 2008 LME copper prices averaged $3.52 per pound, our average recorded price of $3.69 per pound was heavily weighted to the applicable forward curve price at the end of the quarter ($3.82 per pound). Approximately half of our consolidated copper sales during first-quarter 2008 were provisionally priced at the time of shipment and are subject to final pricing later in 2008. At December 31, 2007, 402 million pounds of copper (net of minority interests) were provisionally priced at $3.02 per pound. Copper prices increased in first-quarter 2008 resulting in adjustments to these prior period sales that increased consolidated revenues by $294 million ($127 million to net income or $0.28 per share), compared with a decrease of $15 million ($8 million to net income or $0.03 per share) in first-quarter 2007.

At March 31, 2008, our consolidated copper sales included 362 million pounds of copper (net of minority interests) priced at an average of $3.82 per pound and subject to final pricing over the next several months. We estimate that each $0.05 change in the price realized from the March 31, 2008, provisional price recorded would impact our 2008 consolidated revenues by $25 million ($11 million to net income).

On limited past occasions, in response to market conditions, we have entered into copper and gold price protection contracts for a portion of our expected future mine production to mitigate the risk of adverse price fluctuations. Also, in connection with the Phelps Dodge acquisition, FCX assumed the 2007 copper price protection program, which resulted in charges to revenues for first-quarter 2007 totaling $38 million ($23 million to net income or $0.10 per share). The 2007 copper price protection program matured on December 31, 2007, and in January 2008, we made a $598 million payment upon the settlement of contracts. We do not intend to enter into similar hedging programs in the future.

Production and Delivery Costs

Consolidated production and delivery costs for first-quarter 2008 were approximately $1.8 billion higher than first-quarter 2007 reflecting a full three months of costs associated with Phelps Dodge operations, compared with only 12 days in first-quarter 2007. Also impacting first-quarter 2008 production and delivery costs were higher costs of concentrate purchases at Atlantic Copper associated with higher copper and gold prices.

Energy Costs. Energy, including electricity, diesel fuel, coal and natural gas, is a significant portion of our production costs. As a result, we have been negatively impacted by rising energy prices and could continue to be impacted by future energy availability issues and/or additional increases in energy prices. For 2008, we expect energy costs to approximate 25 percent of our production costs.

We own a one-third interest in the Luna Energy Facility (Luna) located near Deming, New Mexico, which became operational in April 2006. Public Service Company of New Mexico (PNM), a subsidiary of PNM Resources, and Tucson Electric Power, a subsidiary of Unisource Energy Corporation, partnered in the purchase of Luna, each owning a one-third interest and each responsible for one-third of the costs and expenses. PNM is the operating partner of the plant. Approximately 190 megawatts, or one-third of the plant’s electricity, is available to satisfy a portion of the electricity demands of our New Mexico and Arizona operations. Electricity in excess of our demand is sold on the wholesale market. This efficient, low-cost plant is expected to continue to stabilize our southwest North America mining operations’ energy costs and increase the reliability of our energy supply.

Cost Structure. We continue to experience increases in our worldwide copper production costs. In addition to energy, costs have been affected by the prices of commodity input costs, royalties and profit sharing arrangements, equipment consumed or used in our operations and labor costs.

Additionally, we are developing large-scale underground operations in Indonesia that are more sensitive to labor costs than our large-scale open pit and mill processing operations. Increasing labor costs without corresponding productivity gains will adversely impact our current and future underground development and operations.

Depreciation, Depletion and Amortization

Consolidated depreciation, depletion and amortization expense of $418 million for first-quarter 2008 was $302 million higher than first-quarter 2007. The increase reflects higher purchase accounting impacts of $179 million related to the increase in the carrying values of acquired property, plant and equipment, and also includes the impact of higher overall copper sales volumes under the unit-of-production method resulting from a full three months of Phelps Dodge operations, compared with only 12 days in first-quarter 2007.

Exploration and Research Expenses

Consolidated exploration and research expenses totaled $52 million for first-quarter 2008, compared with $7 million for first-quarter 2007. The increase in expenditures for first-quarter 2008 primarily reflects a full three months, or $46 million, of exploration and research expenses associated with Phelps Dodge operations, compared with $3 million for the 12-day period ended March 31, 2007. Refer to “Exploration Activities” for further discussion of our exploration activities.

Selling, General and Administrative Expenses

Consolidated selling, general and administrative expenses for first-quarter 2008 were $36 million higher than first-quarter 2007 primarily related to a full three months of expense associated with the Phelps Dodge operations, compared with only 12 days in first-quarter 2007, partly offset by reductions totaling approximately $40 million to adjust 2007 incentive compensation to actual cash and stock-based awards approved by the Corporate Personnel Committee of FCX’s Board of Directors in January 2008.

Interest Expense, Net

Consolidated interest expense (before capitalization) totaled $187 million for first-quarter 2008, compared with $59 million for first-quarter 2007. The increase in first-quarter 2008 primarily relates to a full three months of interest on the debt incurred in connection with the March 19, 2007, acquisition of Phelps Dodge. Additionally, first-quarter 2008 consolidated interest expense includes net purchase accounting impacts of $19 million primarily related to accretion on assumed environmental obligations.

Capitalized interest totaled $22 million for first-quarter 2008, compared with $7 million for first-quarter 2007. Higher capitalized interest for first-quarter 2008 primarily relates to our development projects, including Tenke Fungurume (refer to “Development Projects” for further discussion).

Losses on Early Extinguishment of Debt

During first-quarter 2008, we purchased, in an open market transaction, $33 million of the 9.5% Senior Notes for $46 million, which resulted in a net charge of $6 million ($5 million to net income or $0.01 per share) for early extinguishment of debt.