00008312592023FYfalse7.1259.56.125http://fasb.org/us-gaap/2024#Liabilitieshttp://fasb.org/us-gaap/2024#Liabilitieshttp://fasb.org/us-gaap/2024#Liabilitieshttp://www.fcx.com/20241231#EnvironmentalAndAssetRetirementObligationsCurrenthttp://www.fcx.com/20241231#EnvironmentalAndAssetRetirementObligationsCurrenthttp://www.fcx.com/20241231#EnvironmentalAndAssetRetirementObligationsCurrenthttp://www.fcx.com/20241231#EnvironmentalAndAssetRetirementObligationsNoncurrenthttp://www.fcx.com/20241231#EnvironmentalAndAssetRetirementObligationsNoncurrenthttp://www.fcx.com/20241231#EnvironmentalAndAssetRetirementObligationsNoncurrenthttp://fasb.org/us-gaap/2024#PropertyPlantAndEquipmentNethttp://fasb.org/us-gaap/2024#PropertyPlantAndEquipmentNethttp://fasb.org/us-gaap/2024#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2024#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2024#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2024#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2024#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2024#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2024#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2024#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2024#AccountsReceivableNetCurrenthttp://fasb.org/us-gaap/2024#AccountsReceivableNetCurrenthttp://fasb.org/us-gaap/2024#AccountsReceivableNetCurrenthttp://fasb.org/us-gaap/2024#AccountsReceivableNetCurrenthttp://fasb.org/us-gaap/2024#OtherAssetsCurrenthttp://fasb.org/us-gaap/2024#OtherAssetsCurrenthttp://fasb.org/us-gaap/2024#OtherAssetsCurrenthttp://fasb.org/us-gaap/2024#OtherAssetsCurrenthttp://fasb.org/us-gaap/2024#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2024#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2024#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2024#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2024#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2024#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2024#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2024#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2024#OtherAssetsCurrenthttp://fasb.org/us-gaap/2024#OtherAssetsCurrenthttp://fasb.org/us-gaap/2024#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2024#OtherAssetsNoncurrent

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark one)

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2024

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-11307-01

Freeport-McMoRan Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 74-2480931 |

| (State or other jurisdiction of | | (I.R.S. Employer Identification No.) |

| incorporation or organization) | | |

| | | | | | | | | | | | | | | | | | | | |

| 333 North Central Avenue | | | | |

| Phoenix | | Arizona | | | | 85004-2189 |

| (Address of principal executive offices) | | | | (Zip Code) |

(602) 366-8100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, par value $0.10 per share | FCX | The New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act ☑ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☑ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☑ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☑ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ☑ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☑ No

The aggregate market value of common stock held by non-affiliates of the registrant was $69.5 billion on June 30, 2024.

Common stock issued and outstanding was 1,437,073,006 shares on January 31, 2025.

DOCUMENTS INCORPORATED BY REFERENCE

| | |

| Portions of the registrant’s proxy statement for its 2025 annual meeting of stockholders are incorporated by reference into Part III of this report. |

Freeport-McMoRan Inc.

| | | | | |

| TABLE OF CONTENTS |

| | |

| | Page |

| |

| |

| |

| |

| |

| |

| |

| |

| | |

| |

| |

| |

| Item 6. Reserved | |

| |

| |

| |

| |

| |

| |

| |

| | |

| |

| |

| |

| |

| |

| |

| |

| | |

| |

| |

| |

| |

| |

| | |

| |

| | |

| |

| |

| |

PART I

Items 1. and 2. Business and Properties.

All of our periodic reports filed with the United States (U.S.) Securities and Exchange Commission (SEC) pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, are available, free of charge, through our website, fcx.com, including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports. These reports and amendments are available through our website as soon as reasonably practicable after we electronically file or furnish such material to the SEC. Our website is for information only and the contents of our website or information connected thereto are not incorporated in, or otherwise to be regarded as part of, this Form 10-K.

References to “we,” “us” and “our” refer to Freeport-McMoRan Inc. (FCX) and its consolidated subsidiaries. References to “Notes” refer to the Notes to Consolidated Financial Statements included herein (refer to Item 8.), and references to “MD&A” refer to Management’s Discussion and Analysis of Financial Condition and Results of Operations and Quantitative and Qualitative Disclosures About Market Risk included herein (refer to Items 7. and 7A.). The following discussions include forward-looking statements that are not guarantees of future performance and actual results may differ materially (refer to Item 1A. “Risk Factors” and “Cautionary Statement” in MD&A for further discussion).

GENERAL

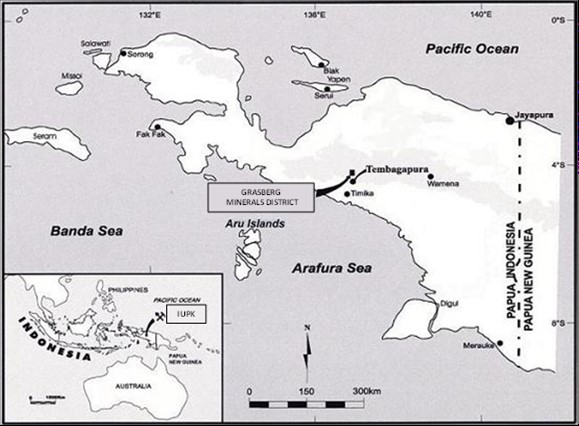

We are a leading international metals company with the objective of being foremost in copper. Headquartered in Phoenix, Arizona, we operate large, long-lived, geographically diverse assets with significant proven and probable mineral reserves of copper, gold and molybdenum. We are one of the world’s largest publicly traded copper producers. Our portfolio of assets includes the Grasberg minerals district in Indonesia, one of the world’s largest copper and gold deposits; and significant operations in North America and South America, including the large-scale Morenci minerals district in Arizona and the Cerro Verde operation in Peru.

Our results for 2024 reflect solid execution of our operating plans and we are committed to enhancing productivity, managing costs and capital and advancing opportunities for long-term profitable growth and value creation. We believe the actions we have taken in recent years to strengthen our balance sheet and maintain flexible organic growth options will allow us to continue to execute our business plans, and reliably and responsibly generate cash flows to pursue value-enhancing organic growth options and return cash to shareholders.

We believe that we have a high-quality portfolio of long-lived copper assets positioned to generate long-term value, and we remain focused on executing our operating and investment plans. Our underground mining operations at the Grasberg minerals district in Indonesia continue to perform well, with copper production increasing in each of the past three years. During 2024, construction of PT Freeport Indonesia’s (PT-FI) new smelter and precious metals refinery (PMR) (collectively, PT-FI’s new downstream processing facilities) in Eastern Java, Indonesia were completed and as part of start-up activities, PT-FI commenced gold production from the PMR in December 2024. In October 2024, during start-up activities of the new smelter, a fire occurred requiring a temporary suspension of smelting operations to complete repairs. PT-FI expects repairs to be completed by mid-2025 and ramp-up to full capacity to be achieved by year-end 2025.

We are progressing initiatives across our North America and South America operations by incorporating new applications, technologies and data analytics to our leaching processes. Incremental copper production from these initiatives totaled 214 million pounds in 2024, compared with a total of 144 million pounds in 2023. We have projects underway to apply recent operational enhancements to our leaching processes on a larger scale and are testing new innovative technology applications that we believe have the potential for significant increases in recoverable metal from leach stockpiles beyond the current run rate.

We believe we benefit from significant copper reserves and resources with embedded growth options, an experienced team and exposure to markets with a favorable fundamental outlook.

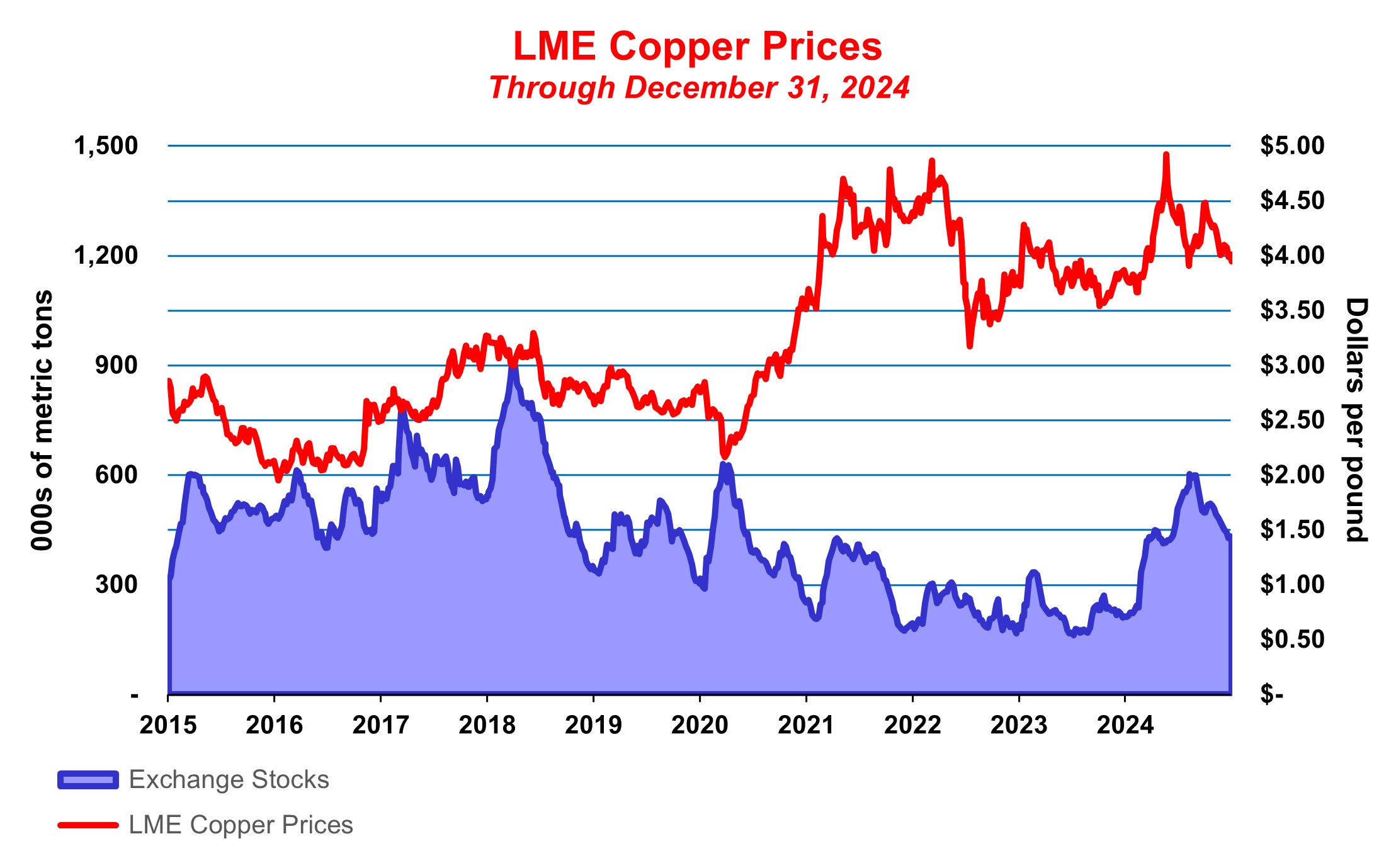

For the year 2024, the London Metal Exchange (LME) copper settlement prices averaged $4.15 per pound (ranging from a low of $3.67 per pound to a high of $4.92 per pound) and closed at $3.95 per pound on December 31, 2024. We believe fundamentals for copper are favorable with growing demand supported by copper’s critical role in the global transition to renewable power, electric vehicles and other carbon-reduction initiatives, continued urbanization in developing countries, data centers and artificial intelligence developments and growing connectivity globally.

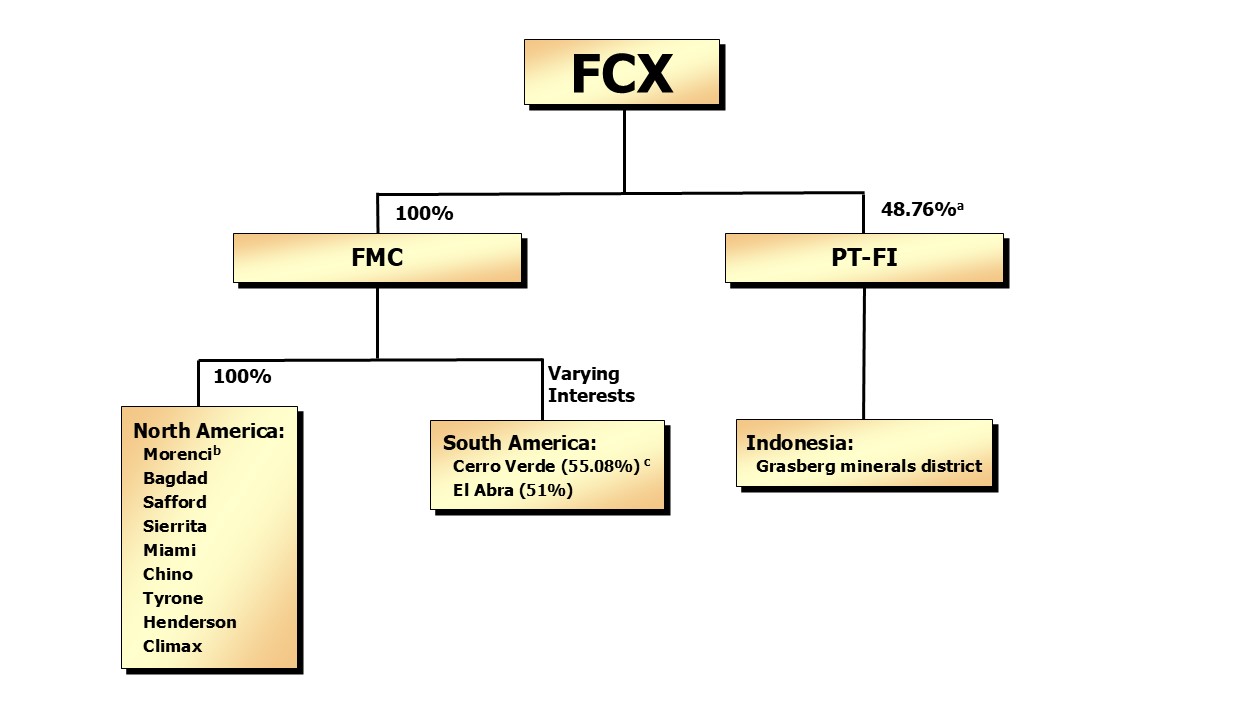

Following are our ownership interests at December 31, 2024, in operating mines through our consolidated subsidiaries, Freeport Minerals Corporation (FMC) and PT-FI:

a.Refer to Note 2 for discussion of our conclusion to consolidate PT-FI.

b.FMC has a 72% undivided interest in Morenci via an unincorporated joint venture. Refer to Note 2 for further discussion.

c.FMC’s interest in Cerro Verde is 55.08%, and prior to September 2024 was 53.56%.

Following is the allocation of our estimated consolidated recoverable proven and probable mineral reserves at December 31, 2024, by geographic location (refer to “Operations” and “Mineral Reserves” for further discussion):

| | | | | | | | | | | | | | | | | | | | |

| Copper | | Gold | | Molybdenum | |

| North America | 43 | % | | 3 | % | | 79 | % | a |

| South America | 29 | | | — | | | 21 | | |

| Indonesia | 28 | | | 97 | | | — | | |

| 100 | % | | 100 | % | | 100 | % | |

a.Our North America copper mines contain 61% of our estimated consolidated recoverable proven and probable molybdenum reserves, and our Henderson and Climax molybdenum mines contain 18%.

In North America, we manage seven copper operations – Morenci, Bagdad, Safford (including Lone Star), Sierrita and Miami in Arizona, and Chino and Tyrone in New Mexico, and two molybdenum mines – Henderson and Climax in Colorado. We also operate a copper smelter in Miami, Arizona. In addition to copper, certain of our North America copper mines also produce molybdenum concentrate, gold and silver.

In South America, we manage two copper operations – Cerro Verde in Peru and El Abra in Chile. In addition to copper, the Cerro Verde mine also produces molybdenum concentrate and silver.

In Indonesia, PT-FI operates in the Grasberg minerals district. In addition to copper, the Grasberg minerals district also produces gold and silver. Upon completion and full ramp-up of PT-FI’s new downstream processing facilities, PT-FI will be a fully integrated producer of refined copper and gold.

Following is the allocation of our consolidated copper, gold and molybdenum production for the year 2024 by geographic location (refer to “Operations” and MD&A for further information):

| | | | | | | | | | | | | | | | | | | | |

| Copper | | Gold | | Molybdenum | |

| North America | 29 | % | | 1 | % | | 75 | % | a |

| South America | 28 | | | — | | | 25 | | |

| Indonesia | 43 | | | 99 | | | — | | |

| 100 | % | | 100 | % | | 100 | % | |

a.Our North America copper mines produced 38% of our consolidated molybdenum production, and our Henderson and Climax molybdenum mines produced 37%.

Copper production from three of our mines (the Morenci mine in North America, the Cerro Verde mine in Peru and the Grasberg minerals district in Indonesia) together totaled 77% of our consolidated copper production in 2024.

The geographic locations of our operating mines are shown on the world map below.

COPPER, GOLD AND MOLYBDENUM

The following provides a summary of our primary natural resources – copper, gold and molybdenum. Refer to MD&A for further discussion of historical and current market prices of these commodities and Item 1A. “Risk Factors” for discussion of factors that can cause price fluctuations.

Copper

Copper is an internationally traded commodity, and its prices are determined by the major metals exchanges – the LME, Commodity Exchange Inc. (COMEX) and Shanghai Futures Exchange. Prices on these exchanges generally reflect the worldwide balance of copper supply and demand, and can be volatile and cyclical.

In general, demand for copper reflects the rate of underlying world economic growth, particularly in industrial production and construction. According to a 2024 report from Wood Mackenzie, a widely followed independent metals market consultant, copper’s end-use markets (and their estimated shares of total consumption) are electrical applications (29%), construction (25%), consumer products (21%), transportation (14%) and industrial machinery (11%). We believe copper will continue to be essential in these basic uses as well as contribute significantly to new technologies for clean energy and advancement in communications, including the global transition to renewable

power, electric vehicles and other carbon-reduction initiatives, continued urbanization in developing countries, data centers and artificial intelligence developments and growing connectivity globally. Examples of areas we believe will require additional copper in the future include: (i) high efficiency motors, which consume up to 75% more copper than a standard motor; (ii) electric vehicles, which consume up to four times the amount of copper in terms of weight compared to vehicles of similar size with an internal combustion engine, and require copper-intensive charging station infrastructure to refuel; and (iii) renewable energy such as wind and solar, which consume four to five times the amount of copper compared to traditional fossil fuel generated power.

Gold

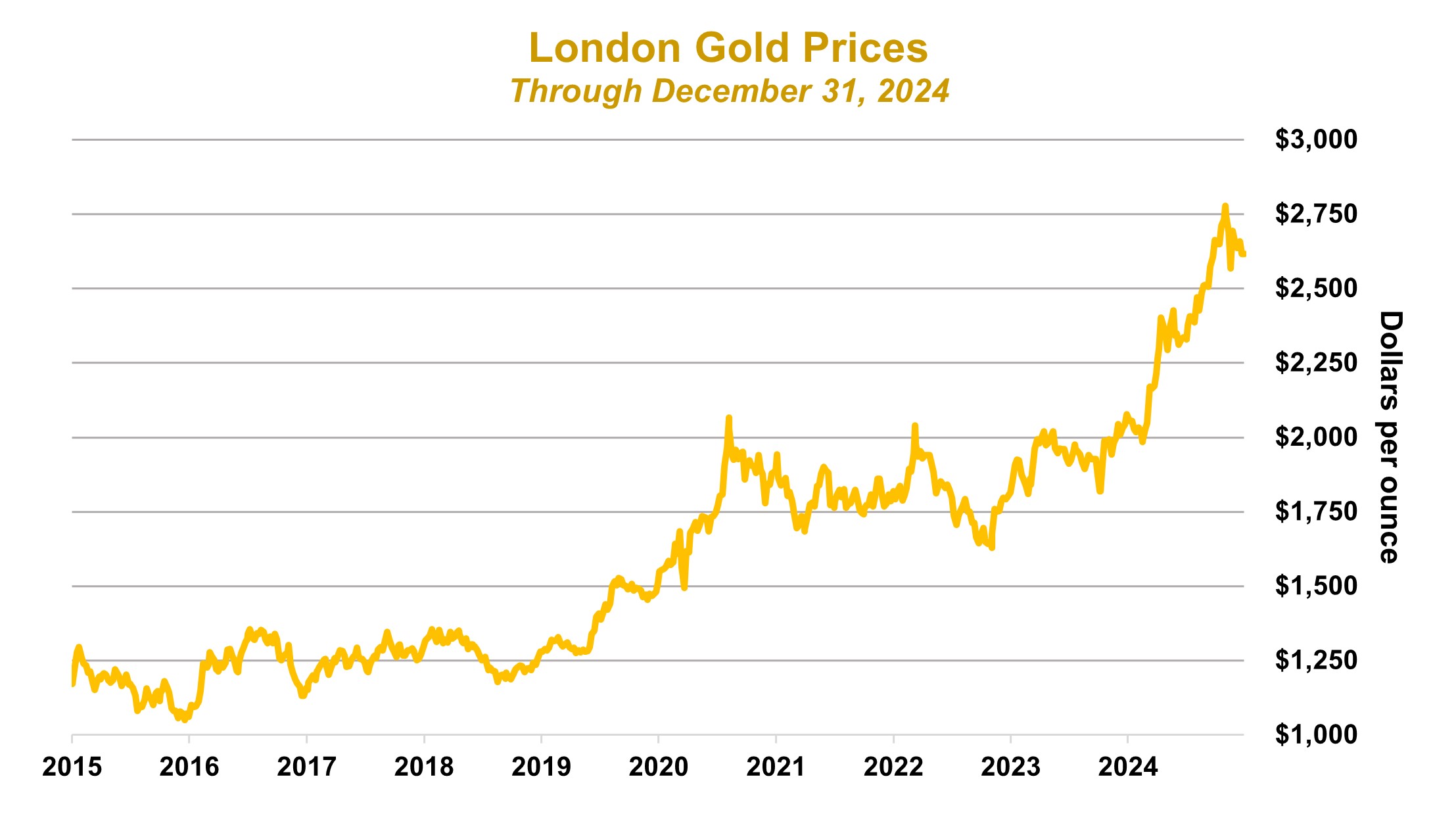

Gold is used for jewelry, coinage and bullion as well as various industrial and electronic applications. Gold can be readily sold on numerous markets throughout the world. Benchmark prices are generally based on London Bullion Market Association (London) quotations.

Molybdenum

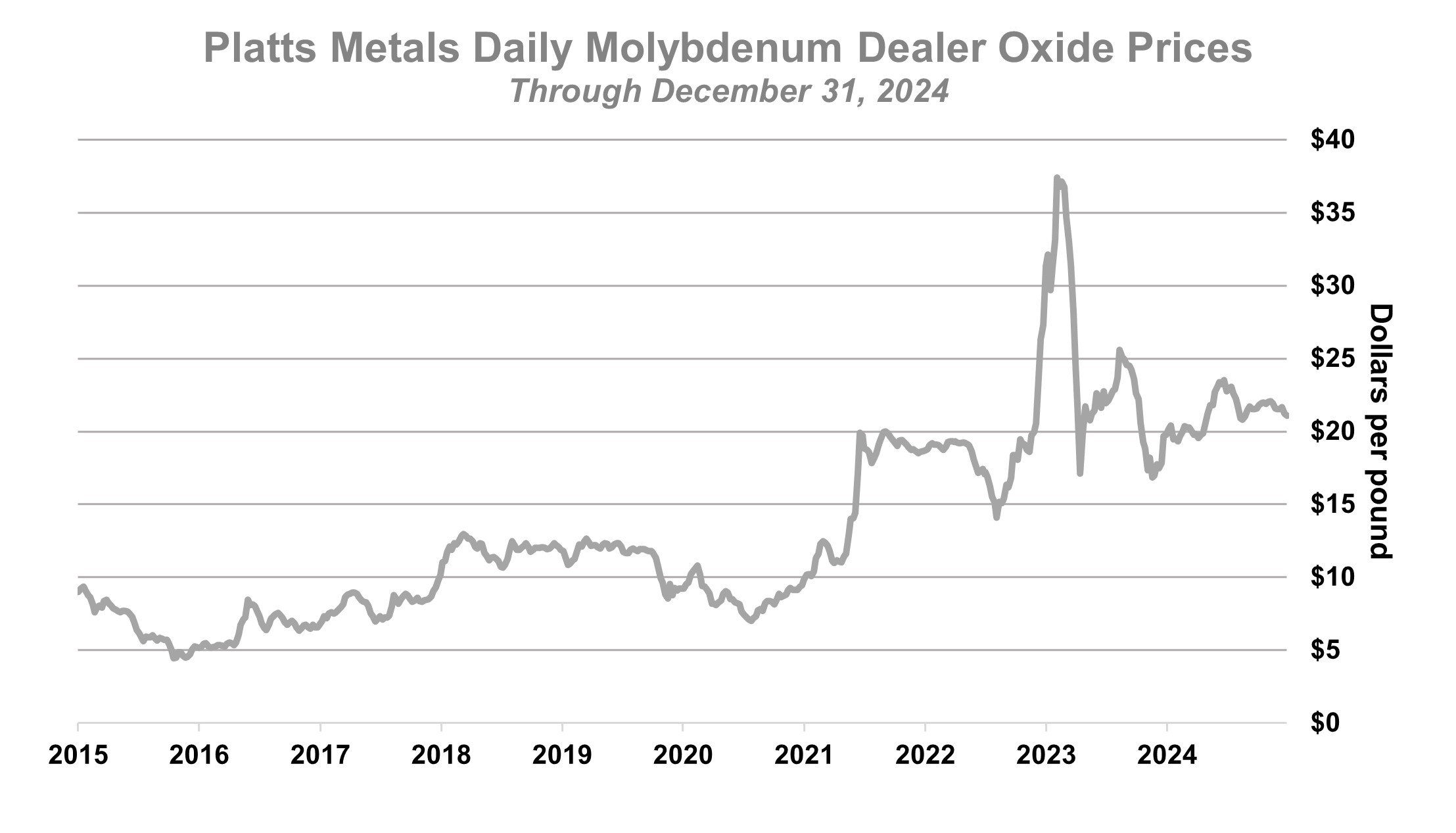

Molybdenum is a key alloying element in steel and the raw material for several chemical-grade products used in catalysts, lubrication, smoke suppression, corrosion inhibition and pigmentation. Molybdenum-based chemicals are used to produce high-purity molybdenum metal used in electronics such as flat-panel displays and in super alloys used in aerospace. Like copper, demand for molybdenum is positively impacted by new technologies for clean energy. Reference prices for molybdenum are available in several publications, but generally based on Platts Metals Daily.

PRODUCTS AND SALES

Our consolidated revenues for 2024 primarily included sales of copper (74%), gold (17%) and molybdenum (7%). For the three years ended December 31, 2024, the only customers that accounted for 10% or more of our consolidated revenues were Mitsubishi Materials Corporation (MMC), PT-FI’s joint venture partner in PT Smelting (PT-FI’s 66%-owned copper smelter and refinery), in 2024 and PT Smelting in 2022. Beginning January 1, 2023, PT-FI’s commercial arrangement with PT Smelting changed to a tolling arrangement so there were no further sales from PT-FI to PT Smelting (refer to Note 2 for further discussion) during 2023 and 2024. Refer to Note 14 for a summary of our consolidated revenues by product and geographic area, and revenues and operating income (loss) by business segment.

Copper Products

We are one of the world’s leading producers of copper concentrate, cathode and continuous cast copper rod. During 2024, 45% of our mined copper was sold in concentrate, 34% as cathode and 21% as rod. The copper ore from our mines is generally processed either by smelting and refining or by solution extraction and electrowinning (SX/EW) as described below.

Copper Concentrate. We produce copper concentrate at six of our mines in which mined ore is crushed and treated to produce a copper concentrate with copper content of approximately 20% to 30%. In North America, copper concentrate is produced at the Morenci, Bagdad, Sierrita and Chino mines, and a significant portion is shipped to our Miami smelter in Arizona for further processing. Copper concentrate is also produced at the Cerro Verde mine in Peru and the Grasberg minerals district in Indonesia. Historically, copper concentrate produced in the Grasberg minerals district has been shipped to PT Smelting in Indonesia, Atlantic Copper in Spain and third-party smelters outside of Indonesia. Once PT-FI’s new smelter is fully operational, all of Grasberg’s copper concentrate is expected to be processed within Indonesia.

Copper Cathode. We produce copper cathode at our electrolytic refinery located in El Paso, Texas, and at nine of our mines.

SX/EW cathode is produced from the Morenci, Bagdad, Safford, Sierrita, Miami, Chino and Tyrone mines in North America, and from the Cerro Verde and El Abra mines in South America. For ore subject to the SX/EW process, the ore is placed on stockpiles and copper is extracted from the ore by dissolving it with a weak sulfuric acid solution. The copper content of the solution is increased in two additional SX stages, and then the copper-bearing solution undergoes an EW process to produce cathode that is, on average, 99.99% copper. Our copper cathode is used as the raw material input for copper rod, brass mill products and for other uses.

Copper cathode is also produced at Atlantic Copper (our wholly owned copper smelting and refining unit in Spain) and PT Smelting. Copper concentrate is smelted (i.e., subjected to extreme heat) to produce copper anode, which

weighs between 700 and 900 pounds and has an average copper content of 99.5%. We operate a copper smelter in Miami, Arizona that produces copper anode. The anode is further treated by electrolytic refining to produce copper cathode, which weighs between 100 and 350 pounds and has an average copper content of 99.99%. Refer to “Smelting Facilities and Other Mining Properties” for further discussion of PT-FI’s new downstream processing facilities, Atlantic Copper, PT Smelting and the Miami smelter.

Continuous Cast Copper Rod. We manufacture continuous cast copper rod at our facilities in El Paso, Texas and Miami, Arizona, primarily using copper cathode produced at our North America copper mines.

Copper Sales

North America. The majority of the copper produced at our North America copper mines and refined in our El Paso, Texas refinery is consumed at our rod plants to produce copper rod, which is then sold to wire and cable manufacturers. The remainder of our North America copper production is sold in the form of copper cathode or copper concentrate under U.S. dollar-denominated annual contracts. Generally, copper cathode is sold to rod, brass or tube fabricators. Cathode and rod contract prices are generally based on the prevailing COMEX monthly average settlement price for the month of shipment and include a premium.

South America. Production from our South America operations is sold as copper concentrate or copper cathode under U.S. dollar-denominated, annual and multi-year contracts. During 2024, our South America operations sold 74% of their copper production in concentrate and 26% as cathode.

Substantially all of our South America copper concentrate and cathode sales contracts provide final copper pricing in a specified future month (generally one to four months from the shipment date) primarily based on quoted LME monthly average settlement copper prices. Revenues from our South America concentrate sales are recorded net of royalties and treatment charges (i.e., fees paid to smelters that are generally negotiated annually). In addition, because a portion of the metals contained in copper concentrate is unrecoverable from the smelting process, revenues from our South America concentrate sales are also recorded net of allowances for unrecoverable metals, which are a negotiated term of the contracts and vary by customer.

Indonesia. PT-FI has historically sold its production in the form of copper concentrate, which contains significant quantities of gold and silver, primarily under U.S. dollar-denominated, long-term contracts. PT-FI sells a small amount of copper concentrate in the spot market. Following the full ramp-up of PT-FI’s new downstream processing facilities, PT-FI’s mining and smelting operations will be fully integrated and copper sales will be in the form of copper cathodes.

Beginning in 2023, PT-FI’s commercial arrangement with PT Smelting changed to a tolling arrangement so there were no further sales from PT-FI to PT Smelting during 2023 and 2024. Under this arrangement, PT-FI pays PT Smelting a tolling fee to smelt and refine its concentrate and PT-FI retains title to all products for sale to third parties. PT-FI’s sale of copper cathodes under the tolling arrangement are priced in the month of shipment and are not subject to provisional pricing.

During 2024, PT-FI sold 56% of its copper production in concentrate and 44% as cathode.

Substantially all of PT-FI’s copper concentrate sales contracts provide final pricing in a specified future month (generally one to four months from the shipment date) primarily based on quoted LME monthly average settlement copper prices. Revenues from PT-FI’s concentrate sales are recorded net of royalties, export duties, treatment charges and allowances for unrecoverable metals. Revenues from PT-FI’s cathode sales are recorded net of royalties.

Refer to Item 1A. “Risk Factors,” “Operations – Indonesia” in MD&A and Notes 10 and 11 for a discussion of Indonesia regulatory matters, including those related to export licenses, export duties and export proceeds.

Gold Products and Sales

We produce gold almost exclusively from our mines in the Grasberg minerals district. The gold we produce is primarily sold as a component of our copper concentrate or in anode slimes, which are a product of the smelting and refining process. Gold generally is priced at the average London price for a specified month near the month of shipment. Revenues from gold sold as a component of our copper concentrate are recorded net of treatment charges, royalties, export duties and allowances for unrecoverable metals. Revenues from gold sold in anode slimes are recorded net of royalties and refining charges. As part of start-up activities, PT-FI commenced gold production from its new PMR in December 2024. We began selling gold bars produced by the PMR in February 2025 and the related revenues are recorded net of royalties.

Molybdenum Products and Sales

According to Wood Mackenzie, we are the world’s largest producer of molybdenum and molybdenum-based chemicals. In addition to production from the Henderson and Climax molybdenum mines, we produce molybdenum concentrate at certain of our North America copper mines and our Cerro Verde copper mine in Peru. The majority of our molybdenum concentrate is processed in our own conversion facilities. Our molybdenum sales are primarily priced based on the average published Platts Metals Daily prices for the month prior to the month of shipment.

GOVERNMENTAL REGULATIONS

Our operations are subject to a broad range of laws and regulations imposed by governments and regulatory bodies, both in the U.S. and internationally. These laws and regulations touch all aspects of our operations, the most significant of which include how we extract, process and explore for minerals and how we conduct our business, including laws and regulations governing matters such as mining rights, environmental and reclamation matters, climate change, occupational health and safety, and human rights. Compliance with these laws and regulations requires expenditures for the implementation, operation and maintenance of systems and programs, but has not had and is not expected to have a material adverse effect on our expenditures, results of operations or competitive position. We continuously monitor and strive to maintain compliance with changes in laws and regulations that impact our business.

Mining Rights

We conduct our mining and exploration activities pursuant to concessions granted by, or under contracts with, the host government in the countries where we operate. These countries include, among others, the U.S., Peru, Chile and Indonesia. Mining rights include our license to operate and involve our payment of applicable taxes and royalties to the host governments. The concessions and contracts are subject to the political risks associated with the host countries. For information about mining rights, governmental agreements, licenses to operate, and tax regulations and related matters refer to “Operations” below, Item 1A. “Risk Factors” and Notes 2, 9, 10 and 11.

Environmental Matters

Our operations are subject to extensive and complex environmental laws and regulations governing the generation, storage, treatment, transportation and disposal of hazardous substances; solid waste disposal; air emissions; wastewater discharges; remediation, restoration and reclamation of environmental contamination, including mine closures and reclamation; protection of endangered and threatened species and designation of critical habitats; and other related matters. In addition, we must obtain regulatory permits and approvals to start, continue and expand operations. As a mining company, compliance with environmental, health and safety laws and regulations is an integral and costly part of our business. We conduct our operations in a manner that aims to protect public health and the environment. We believe our operations follow applicable laws and regulations in all material respects, and we have internal company policies that in some instances go beyond compliance with such laws and regulations.

At December 31, 2024, we had $2.0 billion recorded in our consolidated balance sheet for environmental obligations and $3.7 billion recorded for asset retirement obligations. We incurred environmental capital expenditures and other environmental costs (including our joint venture partners’ shares) to comply with applicable environmental laws and regulations that affect our operations totaling $0.6 billion in 2024, $0.5 billion in 2023 and $0.4 billion in 2022, and we expect to incur approximately $0.6 billion in 2025. The timing and amounts of estimated payments could change as a result of changes in regulatory requirements, changes in scope and costs of reclamation activities, the settlement of environmental matters and the rate at which actual spending occurs on continuing matters.

For information about environmental laws and regulations at our global operations, including legal proceedings and related costs, and reclamation matters, see below as well as Item 1A. “Risk Factors,” Item 3 “Legal Proceedings” and Notes 1, 10 and 11.

United States. There are a number of federal and state environmental laws and regulations that apply to our properties and may affect our operations. Laws such as the Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended (CERCLA) and similar state laws may expose us to joint and several liability for environmental damages caused by our operations, or by previous owners or operators of properties we acquired or are currently operating or at sites where we previously sent materials for processing, recycling or disposal. Other federal and comparable state environmental laws have affected, or could in the future affect, us including, but not limited to, the Resource Conservation and Recovery Act, the Clean Air Act and the National Environmental Policy Act. We have substantial obligations for environmental remediation on mining properties previously owned or operated by FMC and certain of its affiliates.

Our operations are subject to state regulations governing mine closures and reclamation. Closure plans are required to be updated every six years in Arizona and every five years in New Mexico and Colorado. We are also required by U.S. federal and state laws and regulations to provide financial assurance sufficient to allow a third party to implement approved closure and reclamation plans for our mining properties if we are unable to do so. Most of our financial assurance obligations are imposed by state laws that vary significantly by jurisdiction, depending on how each state regulates land use and groundwater quality. The U.S. Environmental Protection Agency (EPA) and state agencies may also require financial assurance for investigation and remediation actions that are required under settlements of enforcement actions under CERCLA or similar state laws.

Regulations have been, and may in the future be, considered at various governmental levels to increase financial responsibility requirements both for mine closure and reclamation. Further, there has been consideration of reforms to federal mining laws, including enhancement of laws, regulations and policies governing financial assurance, which if ever enacted, may be applicable to us.

Our U.S. mining operations are also subject to regulations under the Endangered Species Act (ESA) that are intended to protect species listed by the Department of the Interior’s Fish & Wildlife Service (FWS) as endangered or threatened, along with critical habitat designated by FWS for these listed species. The ESA may affect the ability of landowners, including us, to obtain federal permits or authorizations needed for expansion of our operations, and may also affect our ability to obtain, retain or deliver water to some operations.

New or revised environmental regulatory requirements are frequently proposed, many of which result in substantially increased costs for our business, including those regarding financial assurance discussed above and in Item 1A. “Risk Factors.” For example, in May 2024, EPA amended its rule establishing standards for hazardous air pollutant emissions from primary copper smelters. This final rule will impact our Miami, Arizona smelter operations, which process a significant portion of the copper concentrate produced by our North America copper mines. We are evaluating processes and equipment modifications and the costs involved, which could be significant in connection with the revised rule requirements. Our appeal of EPA’s final rule to the Court of Appeals for the District of Columbia Circuit is suspended pending resolution of several petitions for reconsideration to the EPA filed by us and other parties.

EPA and state agencies continue to consider regulations for man-made organic compounds that could be present in soil, groundwater and surface water at our existing and former operations. These regulations may include drinking water standards, hazardous waste requirements, and hazardous substance designations for Perfluorooctanesulfonic and Perfluorooctanoic acids. In January 2024, EPA announced through guidance that, effective immediately, it lowered the recommended screening levels for investigation and cleanup of lead in residential soils, and in January 2025, EPA published its final toxicological assessment for inorganic arsenic, which may be used to calculate cleanup levels at state and federal remediation sites and may lead to regulatory guidance, rulemaking and other regulatory activities. We are working with state agencies to understand possible ramifications of this guidance to our projects. This EPA guidance and future changes to EPA’s lead and arsenic cleanup levels could result in increases to our environmental reserves for ongoing residential property cleanup projects near former smelter sites.

In 2023, EPA and the U.S. Army Corps of Engineers issued a final rule to amend the final revised definition of the “waters of the United States.” Although future court decisions may further affect the scope of the final rule and legal challenges have already been successful, we may need federal authorization under the Clean Water Act to expand some of our operations.

Peru. The General Environmental Law (Law No. 28611) establishes the main environmental guidelines and principles applicable in Peru. Pursuant to the General Environmental Law, Ministry of Energy and Mines (MINEM) issued national environmental regulations, which have gradually replaced prior guidelines governing governmental agencies’ environmental competencies. The Environmental Evaluation and Oversight Agency has the authority to inspect mining operations and fine companies that fail to comply with prescribed environmental regulations and their approved environmental assessments.

Cerro Verde is subject to regulation under the Mine Closure Law administered by MINEM. Under the closure regulations, mines must submit a closure plan that includes the reclamation methods, closure cost estimates, methods of control and verification, closure and post-closure plans, and financial assurance. In compliance with the requirement for five-year updates, Cerro Verde submitted its updated closure plan and cost estimates and received approval from MINEM in December 2023.

The Cerro Verde mine has developed and continues to implement detailed, comprehensive mine waste and tailings management programs to meet the applicable Peru waste regulations and our environmental management practices. These programs incorporate commitments included in the Environmental and Social Impact Studies and the engineer of record designs for the specific cases of tailings storage facilities and certain leach pad stockpiles. For any future projects, including for existing facilities, Cerro Verde also may be required by MINEM or the National Environmental Certification Service for Sustainable Investments to incur additional costs to comply with the requirements of new regulations that provide for the adequacy of the transportation and final disposal of tailings.

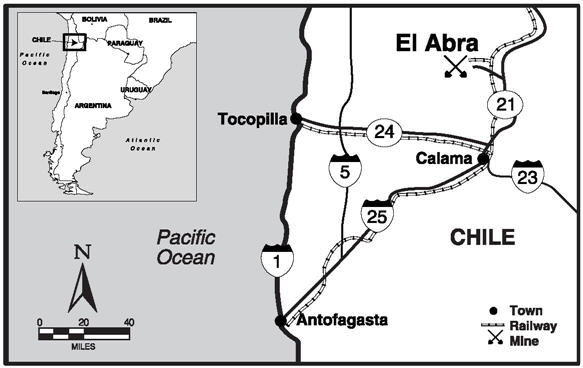

Chile. El Abra is subject to regulation under the Mine Closure Law administered by the Chile Mining and Geology Agency. In compliance with the requirement for five-year updates, El Abra is working to submit an updated plan with closure cost estimates in the second half of 2025.

Indonesia. PT-FI holds multiple permits from national, provincial, and regency regulatory agencies, including groundwater use permits, effluent and air discharge permits, solid and hazardous waste storage and management permits and protection of forest borrow-to-use permits. Where permits have specific terms, renewal applications are made to the relevant regulatory authority as required, prior to the end of the permit term.

In December 2018, Indonesia’s Ministry of Environment and Forestry (MOEF) issued a revised environmental permit to PT-FI to address certain operational activities that it alleged were inconsistent with earlier studies. PT-FI and the MOEF also established a new framework known as the Tailings Management Roadmap for continuous improvement in environmental practices at PT-FI’s operations, including initiatives to potentially increase tailings retention and to evaluate large scale beneficial uses of tailings within Indonesia. The third-party expert nominated by MOEF to perform the framework evaluation submitted its report to the MOEF in June 2021. In 2024, PT-FI continued to work with MOEF on the Tailings Management Roadmap objectives, including further reduction of non-tailings sediment entering the tailings management area, construction of bamboo and geotube structures in the estuary portion of the tailings management area to increase sedimentation and reduce erosion, as well as continue pursuing additional beneficial uses of tailings in infrastructure and other projects. In October 2024, MOEF approved the next phase of the Tailings Management Roadmap, which extends from 2025 to 2030 and continues activities from the initial period with additional programs and studies for continuous improvement in tailings management.

In 2020, PT-FI initiated a new environmental impact analysis (called an Analisis Mengenai Dampak Lingkungan or AMDAL) in preparation for the proposed activities associated with the transition from Grasberg surface mine to underground operations, and PT-FI completed the approval requirements of the AMDAL covering all support activities for the underground transition in 2023. In December 2023, PT-FI received technical approval for its tailings management activities. In 2024, the MOEF approved an addendum to the AMDAL that covers activities associated with the conversion of PT-FI’s power plant from coal-fired to liquefied natural gas (LNG). Permitting related to the conversion to LNG continues to progress.

A detailed mine closure plan and five-year reclamation plan have been approved by Indonesia regulators as required by Indonesia law. The mine closure plan is reviewed annually and required reclamation bonds are in place. In 2019, PT-FI completed and received approval on an updated mine closure plan to reflect Grasberg minerals district production operations until 2041 and PT-FI will be required to fund the next mine closure guarantee in 2025. PT-FI’s most recent five-year reclamation plan covering 2022 through 2026 was approved in early 2022. In the future, additional approval will be required for the diversion of the Aghawagon/Otomona River out of the tailings management area at the end of the mine life.

Climate

In many of the jurisdictions in which we or our customers operate, governmental bodies are increasingly enacting legislation and regulations in response to the potential impacts of climate change, including:

•As a result of the 2015 Paris Agreement, a number of governments, including Peru, Indonesia and Chile, have pledged “Nationally Determined Contributions” to control and reduce greenhouse gas emissions (GHG).

•Several states in the U.S., including Colorado and New Mexico, have advanced goals reducing or eliminating fossil fuel-based energy production and use.

•Carbon tax legislation also has been adopted in jurisdictions where we operate, including Indonesia, Chile and the European Union (EU). Starting in 2025, PT-FI's coal-fired power plant will be subject to a carbon emissions trade system based on reported emissions submitted to the regulators in early 2026. Refer to “Operations – Indonesia” below for discussion of PT-FI’s plans to transition its existing energy source from coal to natural gas.

Regulations that affect us also may include mandated corporate climate-related reporting, including:

•The SEC’s new climate-related disclosure rules, which are being challenged in federal courts.

•The EU’s Corporate Sustainability Reporting Directive, which requires in scope entities to provide detailed reporting on climate change and other sustainability topics.

•The EU’s Corporate Sustainability Due Diligence Directive which will require in scope entities to identify, assess and address various social and environmental topics.

•California’s Climate Corporate Data Accountability Act and Climate-Related Financial Risk Act, which are being challenged in federal courts, and Voluntary Carbon Market Disclosures Act, which were enacted in 2023. Legislation similar to California’s is also under consideration in other states.

While it is not yet possible to reasonably estimate the nature, extent, timing and cost or other impacts of any future carbon pricing mechanisms, mandatory disclosures, other climate change regulatory programs or future legislative action that may be enacted, we anticipate that we will dedicate more resources and incur more costs to comply and remediate in response to legislative or regulatory changes.

For information about the risks posed by the potential impacts of climate change and related regulations, refer to Item 1A. “Risk Factors.”

Health and Safety

Our highest priority is the health, safety and well-being of our employees and contractors. We also work to promote our safety-first values with our suppliers and in the communities where we operate. We believe health and safety considerations are integral to, and fundamental for, all other functions in our organization, and we understand the health and safety of our workforce is critical to our operational efficiency and long-term success. We are subject to extensive U.S. and international regulation of worker health and safety, including the requirements of the U.S. Occupational Safety and Health Act and similar laws of other jurisdictions. For example, in the U.S., the operation of our mines is subject to regulation by the U.S. Mine Safety and Health Administration (MSHA) under the Federal Mine Safety and Health Act of 1977 (Mine Act). MSHA inspects our mines on a regular basis and issues citations and orders when it believes a violation has occurred under the Mine Act. In 2024, MSHA enacted the Safety Program for Surface Mobile Equipment regulation and finalized a new regulation, which reduces permissible exposure limits of respirable crystalline silica effective April 2026. Our compliance with these or any other new health and safety regulations could increase our mining costs. If we were found to be in violation of these regulations we could face penalties or restrictions that may materially and adversely affect our operations.

Additionally, in the U.S., various state agencies have concurrent jurisdiction arising under state law that regulate worker health and safety in both our industrial facilities and mines. If regulatory inspections result in an alleged violation, we may be subject to fines and penalties and, in instances of alleged significant violations, our mining operations or industrial facilities could be subject to temporary or extended closures. Refer to Exhibit 95.1 to this Form 10-K for additional information regarding certain orders and citations issued by MSHA for our operations during the year ended December 31, 2024. For information about health and safety, refer to “Human Capital” below and Item 4. “Mine Safety Disclosures.”

Human Rights

We are dedicated to the recognition, respect and promotion of human rights wherever we do business. We are committed to respecting the rights of all people, including our employees, business partners, community members and others who potentially may be impacted by our business activities. We take this obligation seriously in all aspects of our business, and we expect the same of our business partners.

For information about human rights, refer to “Community and Human Rights” below.

COMPETITION

The top 10 producers of copper comprise approximately 40% of total worldwide mined copper production. Based on Wood Mackenzie’s December 2024 estimates, we ranked third among those producers for the year 2024, with approximately 6% of estimated total worldwide mined copper production based on net equity ownership. We believe our competitive position is based on the size, quality and grade of our ore bodies and our ability to manage costs compared with other producers. We have a diverse portfolio of mining operations with varying ore grades and cost structures. Our costs are driven by the location, grade and nature of our ore bodies, and the level of input costs, including energy, labor and equipment. The metals markets are cyclical, and we believe our ability to maintain our competitive position over the long term is based on our ability to acquire and develop quality deposits (including the expansion of deposits at our existing mine sites); recruit, retain, develop and advance a skilled workforce; and to manage our costs.

OPERATIONS

Responsible Production

We demonstrate our responsible production performance through the Copper Mark, a comprehensive assurance framework developed specifically for the copper industry, and recently extended to other metals including molybdenum. To achieve the Copper Mark, each site is required to complete an independent external assurance process to assess conformance with various environmental, social and governance criteria. Awarded sites must be revalidated every three years. We have achieved, and are committed to maintaining, the Copper Mark and/or Molybdenum Mark, as applicable, at all of our operating sites globally.

We are also a founding member of the International Council on Mining & Metals (ICMM), an organization dedicated to a safe, fair and sustainable mining and metals industry, aiming continuously to strengthen performance across the global mining and metals industry. As a member company, we are required to implement the 10 Mining Principles which define good environmental, social and governance practices, and associated position statements, while also meeting 39 performance expectations.

Tailings Management

We dedicate substantial financial resources and internal and external technical resources to pursue the safe management of our tailings facilities and to reduce or eliminate the number of and potential consequences of credible failure modes. Our tailings management and stewardship program, which involves qualified external engineers of record and periodic oversight by an independent tailings review board and our tailings stewardship team, conform with the tailings governance framework on preventing catastrophic failure of tailings storage facilities adopted by the ICMM. Further, our tailings management policy outlines our continued commitment to managing our tailings responsibly and effectively across our sites globally. As an ICMM member and in accordance with our commitment in our tailings management policy, we also have implemented the Global Industry Standard on Tailings Management (the Tailings Standard) for all tailings storage facilities with “Extreme” or “Very High” potential consequences based on “credible failure modes” and are committed to implementing the Tailings Standard by August 2025 for all other tailing storage facilities that have not been deemed “Safely Closed” (each as defined in the Tailings Standard). We believe we have the financial capacity to meet current estimated lifecycle costs, including estimated closure, post-closure and reclamation obligations associated with our tailings storage facilities. We continue to enhance our existing practices to strengthen the design, operation and closure of tailings storage facilities in an effort to reduce the risk of severe or catastrophic failure of those facilities.

Refer to Item 1A. “Risk Factors” for further discussion of the risks associated with our tailings management.

Overview of Mines

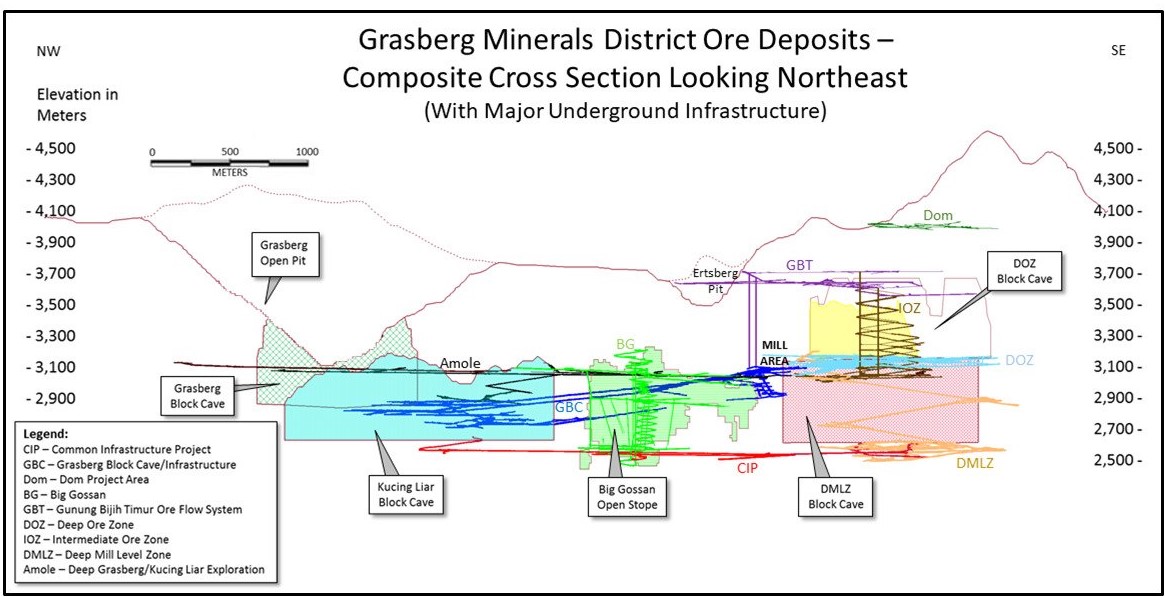

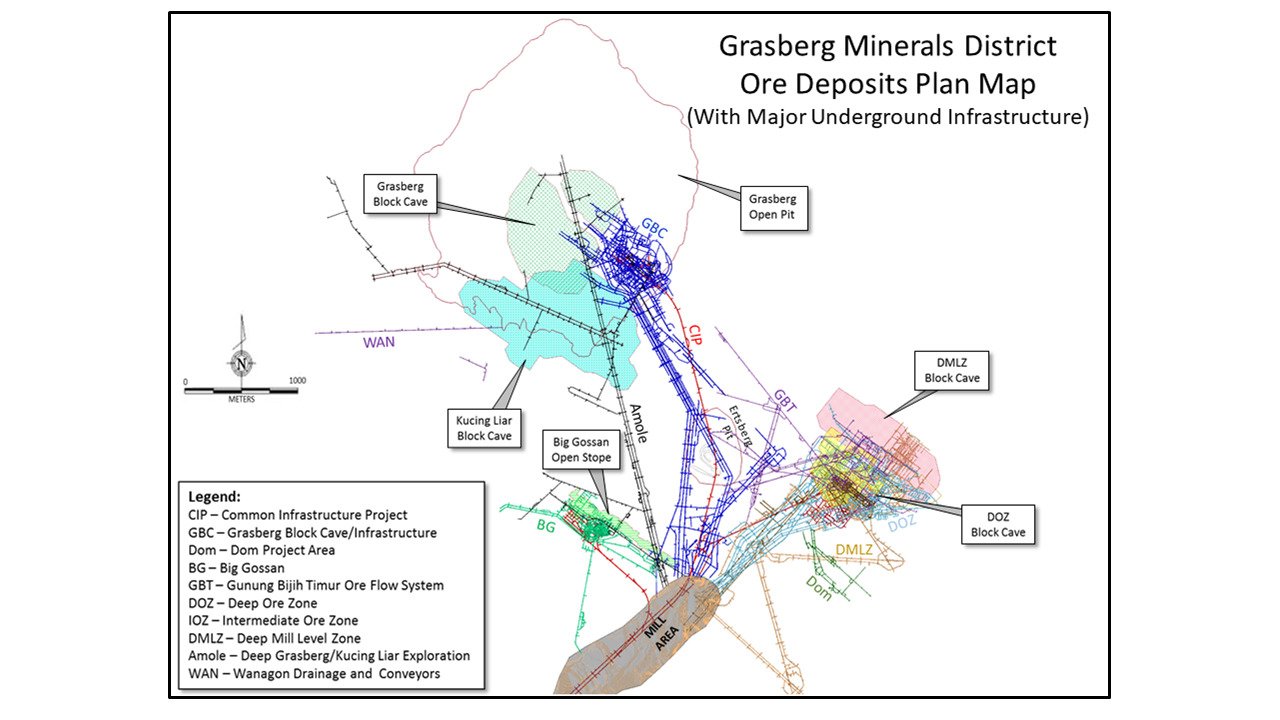

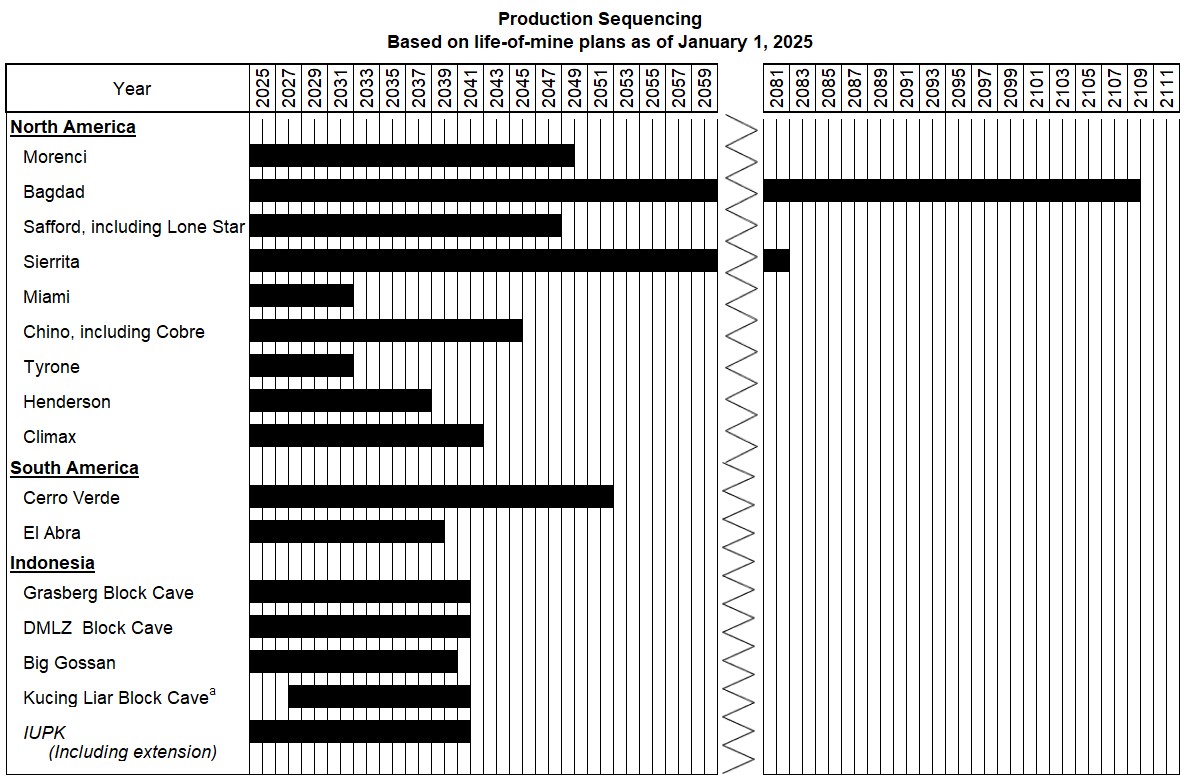

Following are maps and descriptions of our copper and molybdenum mining operations in North America, South America and Indonesia. We consider our material mines, as defined under the disclosure requirements of Subpart 1300 of SEC Regulation S-K, to be the Morenci mine in the U.S., the Cerro Verde mine in Peru and the Grasberg minerals district in Indonesia. Refer to Exhibits 96.1, 96.2 and 96.3 for the Technical Report Summaries that have been prepared for our material mines.

North America

In the U.S., most of the land occupied by our copper and molybdenum mines, concentrators, SX/EW facilities, smelter, refinery, rod mills, molybdenum roasters and processing facilities is owned by us or is located on unpatented mining claims owned by us. Certain portions of our Bagdad, Sierrita, Miami, Chino, Tyrone, Henderson and Climax operations are located on government-owned land and are operated under a Mine Plan of Operations or other use permit. We hold various federal and state permits or leases on government land for purposes incidental to mine operations.

Morenci

We own a 72% undivided interest in Morenci, with the remaining 28% owned by Sumitomo Metal Mining Arizona, Inc. (15%) and SMM Morenci, Inc. (13%). Each partner takes in kind its share of Morenci’s production.

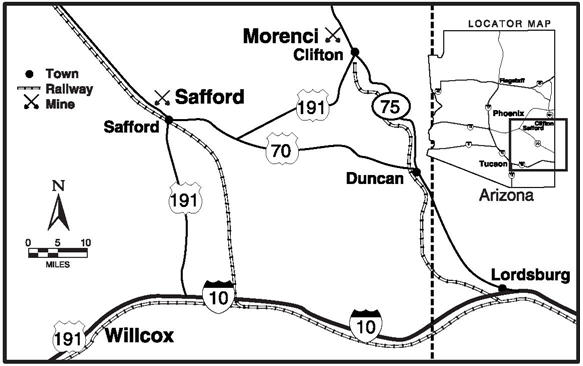

Morenci is an open-pit copper and molybdenum mining complex that has been in continuous operation since 1939 and previously was mined through underground workings. In the 1880s, Phelps Dodge & Company (Phelps Dodge) first invested in the area, and through acquisition, consolidated all mining operations in the area by the 1920s. Phelps Dodge was acquired by FCX in 2007. Morenci is located in Greenlee County, Arizona, approximately 50 miles northeast of Safford on U.S. Highway 191. The property is located at latitude 33.07 degrees north and longitude 109.35 degrees west using the World Geodetic System (WGS) 84 coordinate system. The site is accessible by a paved highway and a railway spur.

The Morenci mine is a porphyry copper deposit that has oxide, secondary sulfide and primary sulfide mineralization. The predominant oxide copper mineral is chrysocolla. Chalcocite is the most important secondary copper sulfide mineral, with chalcopyrite as the dominant primary copper sulfide.

The Morenci operation consists of two concentrators with a milling design capacity of 132,000 metric tons of ore per day, which produce copper and molybdenum concentrate; a 72,500 metric ton-per-day, crushed-ore leach pad and stacking system; a low-grade run-of-mine (ROM) leaching system; four SX plants; and three EW tank houses that produce copper cathode. Total EW tank house capacity is approximately 900 million pounds of copper per year. Morenci’s available mining fleet consists of one hundred and forty-one 235-metric-ton haul trucks loaded by 13 electric shovels with bucket sizes ranging from 47 to 59 cubic meters. Morenci’s mining fleet is capable of moving an average of 785,000 metric tons of material per day. Our share of Morenci’s net property, plant, equipment (PP&E) and mine development costs at December 31, 2024, totaled $2.2 billion.

Morenci’s production, including our joint venture partners’ share, totaled 0.7 billion pounds of copper and 3 million pounds of molybdenum in 2024, 0.8 billion pounds of copper and 3 million pounds of molybdenum in 2023, and 0.9 billion pounds of copper and 4 million pounds of molybdenum in 2022.

Morenci is located in a desert environment with rainfall averaging 13 inches per year. The highest bench elevation is 1,900 meters above sea level and the ultimate pit bottom is expected to have an elevation of 760 meters above sea level. The Morenci operation encompasses approximately 61,700 acres, comprising 51,300 acres of fee lands and 10,400 acres of unpatented mining claims held on public mineral estate and numerous state or federal permits, easements and rights-of-way.

The Morenci operation’s electrical power is supplied by our wholly owned subsidiary, The Morenci Water & Electric Company (MW&E). MW&E sources its generation services through our wholly owned subsidiary, Freeport-McMoRan Copper and Gold Energy Services LLC, through capacity rights at the Luna Energy Facility in Deming, New Mexico, and other power purchase agreements. Although we believe the Morenci operation has sufficient water sources to support current operations, we are a party to litigation that may impact our water right claims or rights to continued use of currently available water supplies, which could adversely affect our water supply for the Morenci operation. Refer to “Governmental Regulations” above, Item 1A. “Risk Factors” and Item 3. “Legal Proceedings” for further discussion.

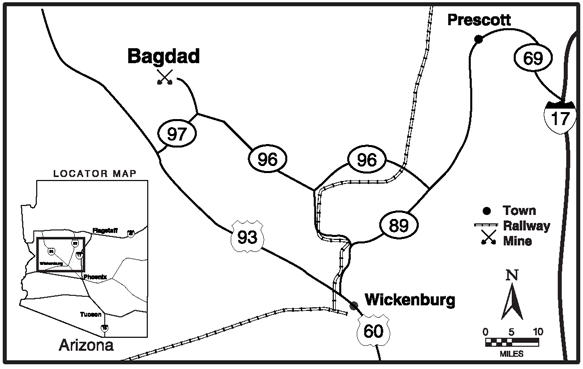

Bagdad

Our wholly owned Bagdad mine is an open-pit copper and molybdenum mining complex that has been in continuous operation since 1945 and prior mining was conducted through underground workings. Bagdad is located in Yavapai County in west-central Arizona, approximately 60 miles west of Prescott and 100 miles northwest of Phoenix. The property can be reached by U.S. Highway 93 to State Route 97 or Arizona Highway 96, which ends at the town of Bagdad. The closest railroad is at Hillside, Arizona, 24 miles southeast on Arizona Highway 96.

The Bagdad mine is a porphyry copper deposit containing both sulfide and oxide mineralization. Chalcopyrite and molybdenite are the dominant primary sulfides and are the primary economic minerals in the mine. Chalcocite is the most common secondary copper sulfide mineral, and the predominant oxide copper minerals are chrysocolla, malachite and azurite.

The Bagdad operation consists of a concentrator with a milling design capacity of 77,100 metric tons of ore per day that produces copper and molybdenum concentrate, a SX/EW plant that can produce approximately 9 million pounds per year of copper cathode from solution generated by low-grade stockpile leaching, and a pressure-leach plant to process molybdenum concentrate. The available mining fleet consists of thirty-eight 235-metric-ton haul trucks loaded by 6 electric shovels and 2 loaders with bucket sizes ranging from 30 to 48 cubic meters, which are capable of moving an average of 236,000 metric tons of material per day. In 2023, we announced a project to convert Bagdad’s fleet of haul trucks to become fully autonomous. The testing of the autonomous fleet is expected to begin in second-quarter 2025 with anticipated project completion by year-end 2025. Bagdad’s net PP&E and mine development costs at December 31, 2024, totaled $1.0 billion.

Bagdad’s production totaled 146 million pounds of copper and 13 million pounds of molybdenum in 2024, 146 million pounds of copper and 10 million pounds of molybdenum in 2023, and 165 million pounds of copper and 9 million pounds of molybdenum in 2022.

We have a potential expansion project to more than double the concentrator capacity of the Bagdad operation in northwest Arizona. Bagdad’s reserve life currently exceeds 80 years and supports an expanded operation. In late 2023, we completed technical and economic studies, which indicate the opportunity to construct new concentrating facilities to increase copper production by 200 to 250 million pounds per year at estimated incremental project

capital costs of approximately $3.5 billion. Expanded operations would provide improved efficiency and reduce unit net cash costs through economies of scale. Project economics indicate that the expansion would require an incentive copper price in the range of $3.50 to $4.00 per pound and approximately three to four years to complete. The decision of whether to proceed and timing of the potential expansion will take into account overall copper market conditions, availability of labor and other factors, including pending conversion of the existing haul truck fleet to autonomous to support long-range plans. In parallel, we are enhancing local infrastructure and advancing activities for expanded tailings infrastructure projects required under long-range plans in order to advance the potential construction timeline. Refer to Item 1A. “Risk Factors” for further discussion.

Bagdad is located in a desert environment with rainfall averaging 15 inches per year. The highest bench elevation is 1,250 meters above sea level and the ultimate pit bottom is expected to be 120 meters above sea level. The Bagdad operation encompasses approximately 53,300 acres, comprising 40,000 acres of fee lands and 13,300 acres of unpatented mining claims held on public mineral estate and numerous state or federal permits, easements and rights-of-ways.

Bagdad receives electrical power from Arizona Public Service Company. We believe the Bagdad operation has sufficient water sources to support current operations.

Safford, including Lone Star

Our wholly owned Safford mine is an open-pit copper mining complex that has been in operation since 2007. Safford is located in Graham County, Arizona, 8 miles north of the town of Safford and 170 miles east of Phoenix. The site is accessible by a paved county road off U.S. Highway 70.

The Safford mine includes three copper deposits that have oxide mineralization overlaying primary copper sulfide mineralization. The predominant oxide copper minerals are chrysocolla and copper-bearing iron oxides with the predominant copper sulfide material being chalcopyrite. The only Safford deposit currently being mined is Lone Star.

We have commenced pre-feasibility studies in the Lone Star district of Safford to define a potential significant expansion opportunity. Positive drilling conducted in recent years indicates a large, mineralized district with opportunities to pursue a further expansion project. We are expecting to complete these studies in 2026. The decision of whether to proceed and timing of the potential expansion will take into account results of technical and economic studies, overall copper market conditions and other factors.

Safford is a mine-for-leach operation that produces copper cathode. The operation feeds a crushing facility with a design capacity of 103,500 metric tons of ore per day. The crushed ore is delivered to a leach pad by a series of overland and portable conveyors. Leach solutions feed a SX/EW facility with a capacity of 320 million pounds of copper per year. A sulfur burner plant is also in operation at Safford, providing a cost-effective source of sulfuric acid used in SX/EW operations. The available mining fleet consists of fifty-nine 235-metric-ton haul trucks loaded by 7 electric shovels with bucket sizes ranging from 34 to 47 cubic meters, which are capable of moving an average of 408,000 metric tons of material per day. Safford’s net PP&E and mine development costs at December 31, 2024, totaled $1.7 billion.

Safford’s copper production totaled 249 million pounds in 2024, 245 million pounds in 2023 and 285 million pounds in 2022.

Safford is located in a desert environment with rainfall averaging 10 inches per year. The highest bench elevation is 1,783 meters above sea level and the ultimate pit bottom is expected to have an elevation of 716 meters above sea level. The Safford operation encompasses approximately 78,600 acres, comprising 38,000 acres of fee lands and 40,600 acres of unpatented claims held on public mineral estate.

The Safford operation’s electrical power is primarily sourced from Tucson Electric Power Company, Arizona Public Service Company and the Luna Energy facility. Although we believe the Safford operation has sufficient water sources to support current operations, we are a party to litigation that may impact our water right claims or rights to continued use of currently available water supplies, which could adversely affect our water supply for the Safford operation. Refer to “Governmental Regulations” above, Item 1A. “Risk Factors” and Item 3. “Legal Proceedings” for further discussion.

Sierrita

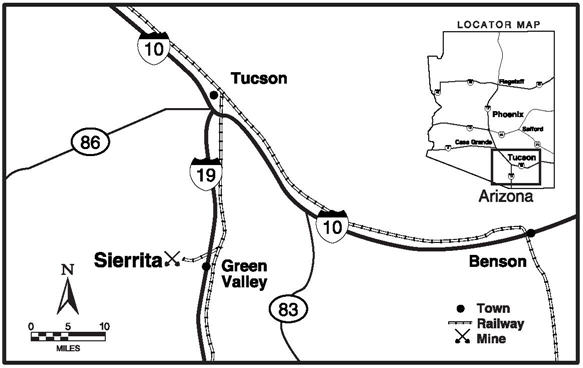

Our wholly owned Sierrita mine is an open-pit copper and molybdenum mining complex that has been in operation since 1959. Sierrita is located in Pima County, Arizona, approximately 20 miles southwest of Tucson and 7 miles west of the town of Green Valley and Interstate Highway 19. The site is accessible by a paved highway and by rail.

The Sierrita mine is a porphyry copper deposit that has oxide, secondary sulfide and primary sulfide mineralization. The predominant oxide copper minerals are malachite, azurite and chrysocolla. Chalcocite is the most important secondary copper sulfide mineral, and chalcopyrite and molybdenite are the dominant primary sulfides.

The Sierrita operation includes a concentrator with a milling design capacity of 100,000 metric tons of ore per day that produces copper and molybdenum concentrate. Sierrita also produces copper from a ROM oxide-leaching system. Cathode copper is plated at the Twin Buttes EW facility, which has a design capacity of approximately 50 million pounds of copper per year. The Sierrita operation also has molybdenum facilities consisting of a leaching circuit, two molybdenum roasters and a packaging facility. The molybdenum facilities process molybdenum concentrate produced by Sierrita, from our other mines and from third-party sources. The available mining fleet consists of twenty-five 235-metric-ton haul trucks loaded by 4 electric shovels with bucket sizes ranging from 34 to 56 cubic meters, which are capable of moving an average of 200,000 metric tons of material per day. Sierrita’s net PP&E and mine development costs at December 31, 2024, totaled $0.9 billion.

Sierrita’s production totaled 165 million pounds of copper and 15 million pounds of molybdenum in 2024, 185 million pounds of copper and 18 million pounds of molybdenum in 2023, and 184 million pounds of copper and 17 million pounds of molybdenum in 2022.

Sierrita is located in a desert environment with rainfall averaging 14 inches per year. The highest bench elevation is 1,387 meters above sea level and the ultimate pit bottom is expected to be 427 meters above sea level. The Sierrita operation, including the adjacent Twin Buttes site, encompasses approximately 47,700 acres, comprising 38,700 acres of fee lands including split estate lands and 9,000 acres of unpatented mining claims held on public mineral estate.

Sierrita receives electrical power through long-term contracts with the Tucson Electric Power Company. Although we believe the Sierrita operation has sufficient water sources to support current operations, we are a party to litigation that may impact our water rights claims or rights to continued use of currently available water supplies, which could

adversely affect our water supply for the Sierrita operation. Refer to “Governmental Regulations” above, Item 1A. “Risk Factors” and Item 3. “Legal Proceedings” for further discussion.

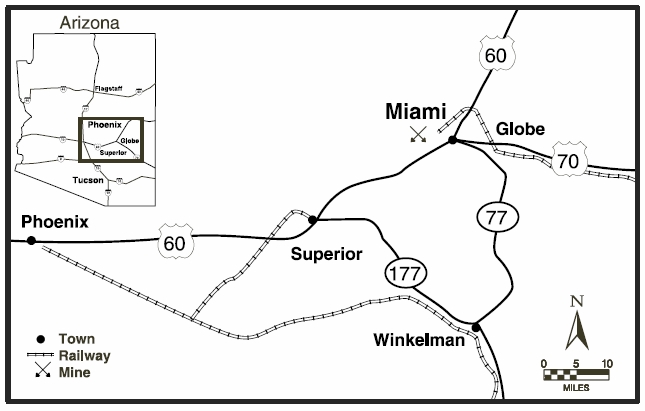

Miami

Our wholly owned Miami mine is an open-pit copper mining complex located in Gila County, Arizona, 90 miles east of Phoenix and 6 miles west of the city of Globe on U.S. Highway 60. The site is accessible by a paved highway and by rail.

The Miami mine is a porphyry copper deposit that has leachable oxide and secondary sulfide mineralization. The predominant oxide copper minerals are chrysocolla, copper-bearing clays, malachite and azurite. Chalcocite and covellite are the most important secondary copper sulfide minerals.

Since about 1915, the Miami mining operation had processed copper ore using both flotation and leaching technologies. The design capacity of the SX/EW plant is 200 million pounds of copper per year. Miami is no longer mining ore, but currently produces copper through leaching material already placed on stockpiles. Miami’s net PP&E and mine development costs at December 31, 2024, totaled $13 million.

Miami’s copper production totaled 9 million pounds in 2024, 12 million pounds in 2023 and 11 million pounds in 2022.

Miami is located in a desert environment with rainfall averaging 18 inches per year. The highest bench elevation is 1,390 meters above sea level and mining advanced the pit bottom to an elevation of 810 meters above sea level. Subsequent sloughing of material into the pit has filled it back to an elevation estimated to be 900 meters above sea level. The Miami operation encompasses approximately 14,800 acres, comprising 10,400 acres of fee lands and 4,400 acres of unpatented mining claims held on public mineral estate.

Miami receives electrical power through long-term contracts with the Salt River Project and natural gas through long-term contracts with El Paso Natural Gas as the transporter. We believe the Miami operation has sufficient water sources to support current operations. Refer to “Governmental Regulations” above and Item 1A. “Risk Factors” for further discussion.

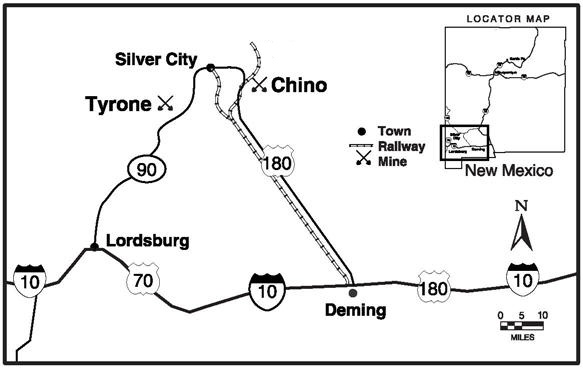

Chino and Tyrone

Chino. Our wholly owned Chino mine is an open-pit copper mining complex that has been in operation since 1910. Chino is located in Grant County, New Mexico, approximately 15 miles east of Silver City, along State Highway 180. The mine is accessible by paved roads and by rail.

The Chino mine is a porphyry copper deposit with adjacent copper skarn deposits. There is leachable oxide, secondary sulfide and millable primary sulfide mineralization. The predominant oxide copper mineral is chrysocolla. Chalcocite is the most important secondary copper sulfide mineral, and chalcopyrite and molybdenite are the dominant primary sulfides.

The Chino operation consists of a concentrator with a milling design capacity of 36,000 metric tons of ore per day that produces copper concentrate, and a 150 million pound-per-year SX/EW plant that produces copper cathode from solution generated by ROM leaching. The available mining fleet consists of twenty 240-metric-ton haul trucks loaded by 3 electric shovels with bucket sizes ranging from 31 to 48 cubic meters, which are capable of moving an average of 180,000 metric tons of material per day. Chino’s net PP&E and mine development costs at December 31, 2024, totaled $0.6 billion.

Chino’s copper production totaled 133 million pounds in 2024, 141 million pounds in 2023 and 130 million pounds in 2022.

Chino is located in a desert environment with rainfall averaging 16 inches per year. The highest bench elevation is 2,250 meters above sea level and the ultimate pit bottom is expected to be 1,508 meters above sea level. The Chino operation encompasses approximately 129,700 acres, comprising 111,900 acres of fee lands and 17,800 acres of unpatented mining claims held on public mineral estate.

Chino receives electrical power from the Luna Energy facility and from the open market. We believe the Chino operation has sufficient water sources to support current operations. Refer to “Governmental Regulations” above and Item 1A. “Risk Factors” for further discussion.

Tyrone. Our wholly owned Tyrone mine is an open-pit copper mining complex and has been in operation since 1967. Tyrone is located in Grant County, New Mexico, 10 miles south of Silver City, along State Highway 90. The site is accessible by paved roads and by rail.

The Tyrone mine is a porphyry copper deposit. Mineralization is predominantly secondary sulfide consisting of chalcocite, with leachable oxide mineralization consisting of chrysocolla.

Copper processing facilities consist of a SX/EW operation with a maximum capacity of approximately 100 million pounds of copper cathode per year. The available mining fleet consists of six 240-metric-ton haul trucks loaded by 1 electric shovel with a bucket size of 47 cubic meters, which is capable of moving an average of 108,000 metric tons of material per day. Tyrone’s net PP&E and mine development costs at December 31, 2024, totaled $0.1 billion.

Tyrone’s copper production totaled 43 million pounds in 2024, 51 million pounds in 2023 and 59 million pounds in 2022.

Tyrone is located in a desert environment with rainfall averaging 16 inches per year. The highest bench elevation is 2,070 meters above sea level and the ultimate pit bottom is expected to have an elevation of 1,475 meters above sea level. The Tyrone operation encompasses approximately 78,500 acres, comprising 65,500 acres of fee lands and 13,000 acres of unpatented mining claims held on public mineral estate.

Tyrone receives electrical power from the Luna Energy facility and from the open market. We believe the Tyrone operation has sufficient water sources to support current operations. Refer to “Governmental Regulations” above and Item 1A. “Risk Factors” for further discussion.

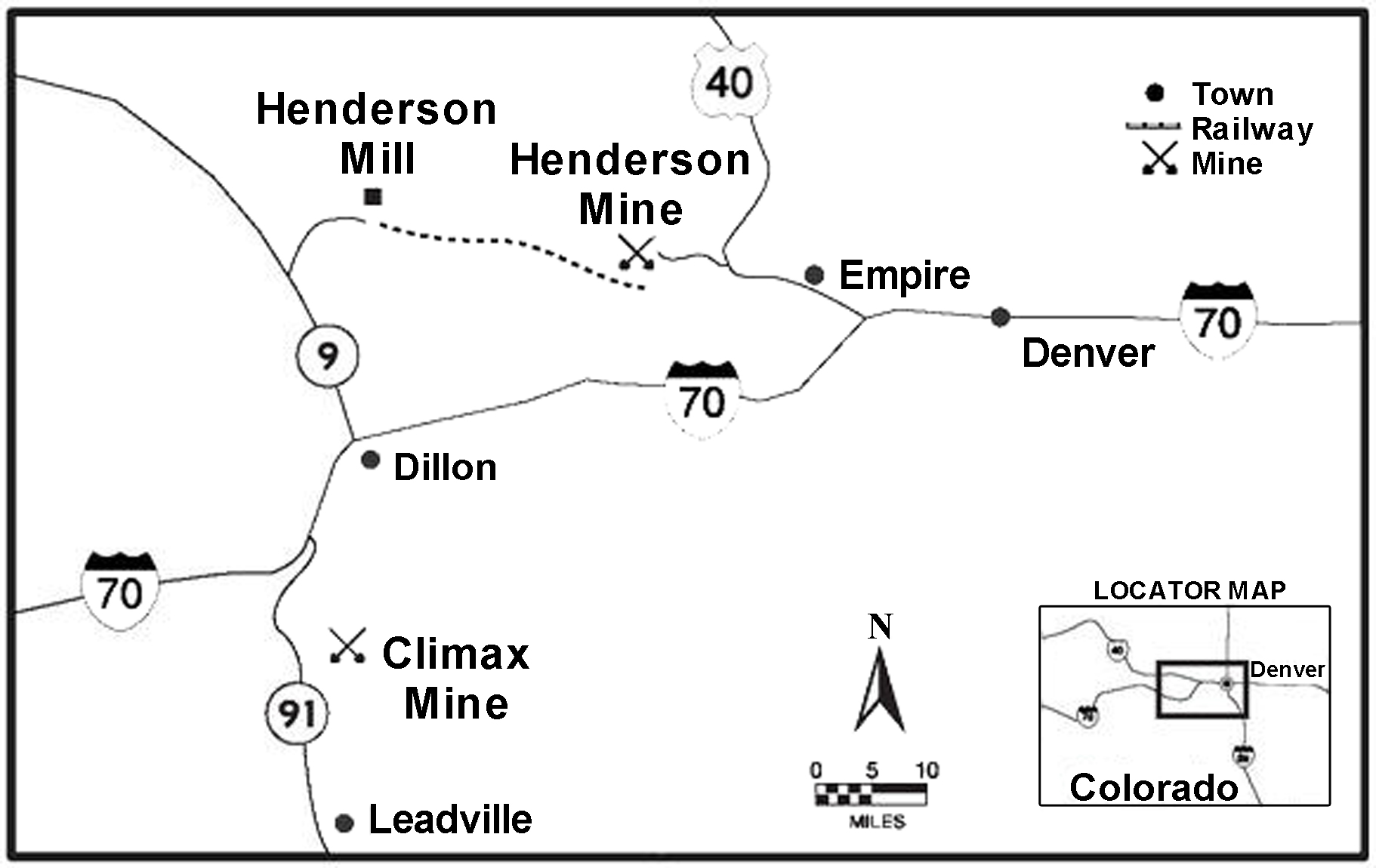

Climax and Henderson

Climax. Our wholly owned Climax mine is an open-pit molybdenum mine that is located 13 miles northeast of Leadville, Colorado, off Colorado State Highway 91 at the top of Fremont Pass. The mine is accessible by paved roads. Climax was placed on care and maintenance status by its previous owner in 1995 and, after being acquired by FMC, began commercial production in 2012.

The Climax ore body is a porphyry molybdenum deposit, with molybdenite as the primary sulfide mineral.

The Climax mine includes a 25,000 metric tons of ore per day mill facility. Climax has the capacity to produce approximately 30 million pounds of molybdenum per year. The majority of the molybdenum concentrate produced is shipped to our Fort Madison, Iowa, processing facility. The available mining fleet consists of thirteen 177-metric-ton haul trucks loaded by 2 hydraulic shovels with bucket sizes of 34 cubic meters, which are capable of moving an average of 90,000 metric tons of material per day. Climax’s net PP&E and mine development costs at December 31, 2024, totaled $1.4 billion.

Climax’s molybdenum production totaled 18 million pounds in 2024, 17 million pounds in 2023 and 21 million pounds in 2022.

The Climax mine is located in a mountainous region. The highest bench elevation is approximately 4,050 meters above sea level and the ultimate pit bottom is expected to have an elevation of approximately 3,100 meters above sea level. This region experiences significant snowfall during the winter months. The Climax operation encompasses approximately 15,100 acres, comprising 14,300 acres of privately owned land and 800 acres of federal claims.

Climax operations receive electrical power through long-term contracts with Xcel Energy and natural gas supply with United Energy Trading (with Xcel as the transporter). We believe the Climax operation has sufficient water sources to support current operations. Refer to “Governmental Regulations” above and Item 1A. “Risk Factors” for further discussion.

Henderson. Our wholly owned Henderson molybdenum mining complex has been in operation since 1976. Henderson is located 42 miles west of Denver, Colorado, off U.S. Highway 40. Nearby communities include the towns of Empire, Georgetown and Idaho Springs. The Henderson mill site is located 15 miles west of the mine and is accessible from Colorado State Highway 9. The Henderson mine and mill are connected by a 10-mile conveyor tunnel under the Continental Divide and an additional 5-mile surface conveyor. The tunnel portal is located 5 miles east of the mill.

The Henderson mine is a porphyry molybdenum deposit, with molybdenite as the primary sulfide mineral.

The Henderson operation consists of a block-cave underground mining complex feeding a concentrator with a design capacity of approximately 32,000 metric tons per day. Henderson has the capacity to produce approximately 15 million pounds of molybdenum per year. The majority of the molybdenum concentrate produced is shipped to our Fort Madison, Iowa, processing facility. The available underground mining equipment fleet consists of fifteen 9-metric-ton load-haul-dump (LHD) units and seven 73-metric-ton haul trucks, which deliver ore to a gyratory crusher feeding a series of 3 overland conveyors to the mill stockpiles. Henderson’s net PP&E and mine development costs at December 31, 2024, totaled $0.3 billion.

Henderson’s molybdenum production totaled 12 million pounds in 2024, 13 million pounds in 2023 and 12 million pounds in 2022.

The Henderson mine is located in a mountainous region with the main access shaft at 3,180 meters above sea level. The main production levels are currently at elevations of 2,200 and 2,350 meters above sea level. This region experiences significant snowfall during the winter months. The Henderson mine and mill operations encompass approximately 17,200 acres, comprising 13,000 acres of fee lands, 4,200 acres of unpatented mining claims held on public mineral estate and a 50-acre easement with the U.S. Forest Service for the surface portion of the conveyor corridor.

Henderson operations receive electrical power through long-term contracts with Xcel Energy and natural gas supply with United Energy Trading (with Xcel Energy as the transporter). We believe the Henderson operation has sufficient water sources to support current operations. Refer to “Governmental Regulations” above and Item 1A. “Risk Factors” for further discussion.

South America

At our operations in South America, mine properties and facilities are controlled through mining claims or concessions under the general mining laws of the relevant country. The claims or concessions are owned or controlled by the operating companies in which we or our subsidiaries have a controlling ownership interest. Roads, power lines and aqueducts are controlled by easements.

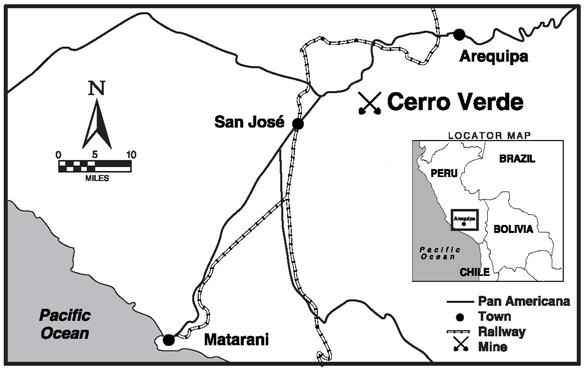

Cerro Verde

In September 2024, we purchased 5.3 million shares of Cerro Verde common stock for $210 million, increasing our ownership interest in Cerro Verde to 55.08% from 53.56%. The remaining 44.92% ownership interest in Cerro Verde is held by SMM Cerro Verde Netherlands B.V. (21.0%), Compañia de Minas Buenaventura S.A.A. (19.58%) and other stockholders whose Cerro Verde shares are publicly traded on the Lima Stock Exchange (4.34%).

Cerro Verde is an open-pit copper and molybdenum mining complex that has been in operation since the 1970s. Cerro Verde is located 20 miles southwest of Arequipa, Peru. Prior to being acquired in 1994 by a predecessor of Phelps Dodge, the mine was previously operated by the Peru government. The property is located at latitude 16.53 degrees south and longitude 71.58 degrees west using the WGS 84 coordinate system. The site is accessible by paved highways. Cerro Verde’s copper cathode and concentrate production that is not sold locally is transported approximately 70 miles by truck and by rail to the Port of Matarani for shipment to international markets. Molybdenum concentrate is transported by truck to either the Ports of Callao or Matarani for shipment.

The Cerro Verde mine is a porphyry copper deposit that has oxide, secondary sulfide and primary sulfide mineralization. The predominant oxide copper minerals are brochantite, chrysocolla, malachite and copper “pitch.” Chalcocite and covellite are the most important secondary copper sulfide minerals. Chalcopyrite and molybdenite are the dominant primary sulfides.

Cerro Verde’s operation includes 2 concentrating facilities with an annual average permitted milling capacity of 409,500 metric tons of ore per day (and the ability to annually treat up to 10% more for a total of 450,450 metric tons of ore per day). As a result of several efficiency initiatives implemented over the past several years, in 2024, Cerro Verde’s 2 concentrators were able to achieve a combined average milling rate of 415,500 metric tons of ore per day in 2024. Cerro Verde also operates a 100,000-metric-ton-per-day ROM leach system coupled with SX/EW leaching facilities, which have a production capacity of approximately 200 million pounds of copper per year.

The available fleet consists of fifty-four 300-metric-ton haul trucks, ninety-one 250-metric-ton haul trucks (8 of which are currently on standby) and 8 leased 380-metric-ton haul trucks loaded by 14 electric shovels with bucket sizes ranging from 33 to 57 cubic meters. This fleet is capable of moving an average of approximately 1,000,000 metric tons of material per day. Cerro Verde’s net PP&E and mine development costs at December 31, 2024, totaled $5.8 billion.

Cerro Verde’s production totaled 0.9 billion pounds of copper and 20 million pounds of molybdenum in 2024, 1.0 billion pounds of copper and 22 million pounds of molybdenum in 2023, and 1.0 billion pounds of copper and 23 million pounds of molybdenum in 2022.