Filed Pursuant to Rule 433

Registration No. 333-223208

October 1, 2019

FREE WRITING PROSPECTUS

(To Prospectus dated February 26, 2018,

Prospectus Supplement dated February 26, 2018 and

Equity Index Underlying Supplement dated February 26, 2018)

Linked to the NYSE FANG+™ Index (the “Reference Asset”)

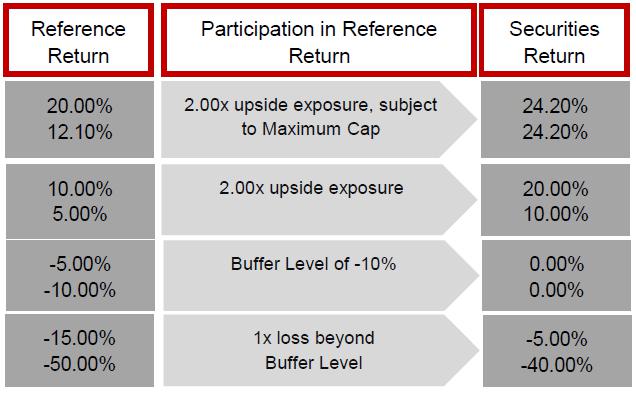

| ► | 2.00x exposure to any positive return of the Reference Asset, subject to a maximum return of at least 24.20% (to be determined on the Pricing Date) |

| ► | Protection from the first 10% of any losses of the Reference Asset |

| ► | Approximately a 2.5 year maturity |

| ► | All payments on the securities are subject to the credit risk of HSBC USA Inc. |

http://uswealth.hsbcnet.com/videos/buffered_accelerated_notes.html

The Buffered Accelerated Market Participation SecuritiesTM(each a “security” and collectively the “securities") offered hereunder will not be listed on any U.S. securities exchange or automated quotation system. The securities will not bear interest.

Neither the U.S. Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the securities or passed upon the accuracy or the adequacy of this document, the accompanying prospectus, prospectus supplement or Equity Index Underlying Supplement. Any representation to the contrary is a criminal offense. We have appointed HSBC Securities (USA) Inc., an affiliate of ours, as the agent for the sale of the securities. HSBC Securities (USA) Inc. will purchase the securities from us for distribution to other registered broker-dealers or will offer the securities directly to investors. In addition, HSBC Securities (USA) Inc. or another of its affiliates or agents may use the pricing supplement to which this free writing prospectus relates in market-making transactions in any securities after their initial sale. Unless we or our agent inform you otherwise in the confirmation of sale, the pricing supplement to which this free writing prospectus relates is being used in a market-making transaction. See “Supplemental Plan of Distribution (Conflicts of Interest)” on page FWP-20 of this document.

Investment in the securities involves certain risks. You should refer to “Risk Factors” beginning on page FWP-7 of this document, page S-1 of the accompanying prospectus supplement and page S-1 of the accompanying Equity Index Underlying Supplement.

The Estimated Initial Value of the securities on the Pricing Date is expected to be between $930.00 and $970.00 per security, which will be less than the price to public. The market value of the securities at any time will reflect many factors and cannot be predicted with accuracy. See “Estimated Initial Value” on page FWP-4 and “Risk Factors” beginning on page FWP-7 of this document for additional information.

| Price to Public | Underwriting Discount(1) | Proceeds to Issuer | |

| Per security | $1,000/ |

(1) HSBC USA Inc. or one of our affiliates may pay varying underwriting discounts of up to 2.75% per $1,000 Principal Amount in connection with the distribution of the securities to other registered broker-dealers. See “Supplemental Plan of Distribution (Conflicts of Interest)” on page FWP-20 of this document.

The Securities:

| Are Not FDIC Insured | Are Not Bank Guaranteed | May Lose Value |

Indicative Terms1

| Principal Amount | $1,000 per security |

| Term | Approximately 2.5 years |

| Reference Asset | The NYSE FANG+™ Index (Ticker: NYFANG) |

| Upside Participation Rate | 200% (2.00x) exposure to any positive Reference Return |

| Maximum Cap | At least 24.20% (to be determined on the Pricing Date) |

| Buffer Level | -10% |

| Reference Return | Final Level – Initial Level Initial Level |

Payment at Maturity per Security | If the Reference Return is greater than zero, you will receive the lesser of: a) $1,000 + ($1,000 × Reference Return × Upside Participation Rate); and b) $1,000 + ($1,000 × Maximum Cap). If the Reference Return is less than or equal to zero but greater than or equal to the Buffer Level: $1,000 (zero return). If the Reference Return is less than the Buffer Level: $1,000 + [$1,000 × (Reference Return + 10%)]. For example, if the Reference Return is -30%, you will suffer a 20% loss and receive 80% of the Principal Amount, subject to the credit risk of HSBC USA, Inc. If the Reference Return is less than the Buffer Level, you will lose some or a significant portion (up to 90%) of your investment. |

| Initial Level | The official Closing Level of the Reference Asset on the Pricing Date |

| Final Level | The official Closing Level of the Reference Asset on the Final Valuation Date |

| Pricing Date | October 28, 2019 |

| Trade Date | October 28, 2019 |

| Original Issue Date | October 31, 2019 |

| Final Valuation Date(2) | April 27, 2022 |

| Maturity Date(2) | May 2, 2022 |

| CUSIP/ISIN | 40435UZF4/US40435UZF47 |

(1)As more fully described on page FWP-4.

(2)Subject to adjustment as described under “Additional Terms of the Notes” in the accompanying Equity Index Underlying Supplement.

The Securities

The securities are designed for investors who believe the Reference Asset will appreciate over the term of the securities. If the Reference Return is below the Buffer Level, then the securities are subject to a 1:1 exposure to any potential decline of the Reference Asset beyond the Buffer Level of -10%.

If the Reference Asset appreciates over the term of the securities, you will realize a return equal to 200% (2.00x) of the Reference Asset appreciation, subject to a Maximum Cap of at least 24.20% (to be determined on the Pricing Date). Should the Reference Asset decline, you will lose 1% of your investment for every 1% decline in the Reference Asset beyond the Buffer Level.

Index Constituents

| Facebook, Inc. |

| Apple Inc. |

| Amazon.com, Inc. |

| Netflix, Inc. |

| Alphabet Inc. |

| Alibaba Group Holding Ltd |

| Baidu, Inc. |

| Nvidia Corporation |

| Tesla, Inc. |

| Twitter, Inc. |

http://uswealth.hsbcnet.com/videos/buffered_accelerated_notes.html

FWP-2

Payoff Example

| The table at right shows the hypothetical payout profile of an investment in the securities reflecting the Upside Participation Rate of 200% (2.00x), reflecting the Buffer Level of -10%, and assuming a Maximum Cap of 24.20%. |  |

Information about the Reference Asset

The Index is an equal-dollar weighted index designed to represent a segment of the technology and consumer discretionary sectors consisting of highly-traded growth stocks of technology and tech-enabled companies. The Index currently has 10 constituents. |  |

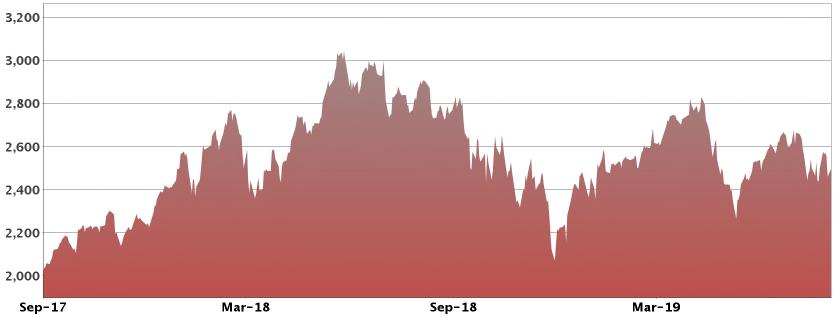

The graph above illustrates the performance of the Reference Asset from September 30, 2017 through September 30, 2019. The closing levels in the graph above were obtained from the Bloomberg Professional® Service. Past performance is not necessarily an indication of future results. For further information on the Reference Asset, please see “Description of the Reference Asset” on page FWP-15 of this document. We have derived all disclosure regarding the Reference Asset from publicly available information. Neither HSBC USA Inc. nor any of its affiliates have undertaken any independent review of, or made any due diligence inquiry with respect to, the publicly available information about the Reference Asset.

FWP-3

HSBC USA Inc.

Buffered Accelerated Market Participation Securities

Linked to the NYSE FANG+™ Index

This document relates to a single offering of Buffered Accelerated Market Participation SecuritiesTM. The securities will have the terms described in this document and the accompanying prospectus, prospectus supplement and Equity Index Underlying Supplement. If the terms of the securities offered hereby are inconsistent with those described in the accompanying prospectus, prospectus supplement or Equity Index Underlying Supplement, the terms described in this document shall control.You should be willing to forgo interest and dividend payments during the term of the securities and, if the Reference Return is less than the Buffer Level, lose some or a significant portion (up to 90%) of your principal.

This document relates to an offering of securities linked to the performance of the NYSE FANG+™Index (the “Reference Asset”). The purchaser of a security will acquire a senior unsecured debt security of HSBC USA Inc. linked to the Reference Asset as described below. The following key terms relate to the offering of securities:

| Issuer: | HSBC USA Inc. |

| Principal Amount: | $1,000 per security |

| Reference Asset: | The NYSE FANG+™ Index (Ticker: NYFANG) |

| Trade Date: | October 28, 2019 |

| Pricing Date: | October 28, 2019 |

| Original Issue Date: | October 31, 2019 |

| Final Valuation Date: | April 27, 2022,subject to adjustment as described under “Additional Terms of the Notes—Valuation Dates” in the accompanying Equity Index Underlying Supplement. |

| Maturity Date: | 3 business days after the Final Valuation Date, which is expected to be May 2, 2022. The Maturity Date is subject to adjustment as described under “Additional Terms of the Notes—Coupon Payment Dates, Call Payment Dates and Maturity Date” in the accompanying Equity Index Underlying Supplement. |

| Upside Participation Rate: | 200% (2.00x) |

| Payment at Maturity: | On the Maturity Date, for each security, we will pay you the Final Settlement Value. |

| Reference Return: | The quotient, expressed as a percentage, calculated as follows: |

Final Level – Initial Level Initial Level | |

| Final Settlement Value: | If the Reference Return is greater than zero,you will receive a cash payment on the Maturity Date, per $1,000 Principal Amount, equal to the lesser of:

(a) $1,000 + ($1,000 × Reference Return × Upside Participation Rate); and

(b) $1,000 + ($1,000 × Maximum Cap).

If the Reference Return is less than or equal to zero but greater than or equal to the Buffer Level, you will receive $1,000 per $1,000 Principal Amount (zero return).

If the Reference Return is less than the Buffer Level, you will receive a cash payment on the Maturity Date, per $1,000 Principal Amount, calculated as follows:

$1,000 + [$1,000 × (Reference Return + 10%)].

Under these circumstances, you will lose 1% of the Principal Amount of your securities for each percentage point that the Reference Return is below the Buffer Level. For example, if the Reference Return is -30%, you will suffer a 20% loss and receive 80% of the Principal Amount, subject to the credit risk of HSBC.If the Reference Return is less than the Buffer Level, you will lose some or a significant portion (up to 90%) of your investment. |

| Buffer Level: | -10% |

| Maximum Cap: | At least 24.20% (to be determined on the Pricing Date). |

| Initial Level: | The Official Closing Level of the Reference Asset on the Pricing Date. |

| Final Level: | The Official Closing Level of the Reference Asset on the Final Valuation Date. |

| Form of Securities: | Book-Entry |

| Listing: | The securities will not be listed on any U.S. securities exchange or quotation system. |

| CUSIP/ISIN: | 40435UZF4/US40435UZF47 |

| Estimated Initial Value: | The Estimated Initial Value of the securities will be less than the price you pay to purchase the securities. The Estimated Initial Value does not represent a minimum price at which we or any of our affiliates would be willing to purchase your securities in the secondary market, if any, at any time. The Estimated Initial Value will be calculated on the Pricing Date. See “Risk Factors — The Estimated Initial Value of the securities, which will be determined by us on the Pricing Date, will be less than the price to public and may differ from the market value of the securities in the secondary market, if any.” |

The Trade Date, the Pricing Date and the other dates set forth above are subject to change, and will be set forth in the pricing supplement relating to the securities.

FWP-4

GENERAL

This document relates to an offering of securities linked to the Reference Asset. The purchaser of a security will acquire a senior unsecured debt security of HSBC USA Inc. We reserve the right to withdraw, cancel or modify this offering and to reject orders in whole or in part. Although the offering of securities relates to the Reference Asset, you should not construe that fact as a recommendation as to the merits of acquiring an investment linked to the Reference Asset or any component security included in the Reference Asset or as to the suitability of an investment in the securities.

You should read this document together with the prospectus dated February 26, 2018, the prospectus supplement dated February 26, 2018 and the Equity Index Underlying Supplement dated February 26, 2018. If the terms of the securities offered hereby are inconsistent with those described in the accompanying prospectus, prospectus supplement or Equity Index Underlying Supplement, the terms described in this document shall control. You should carefully consider, among other things, the matters set forth in “Risk Factors” beginning on page FWP-7 of this document, page S-1 of the prospectus supplement and page S-1 of the Equity Index Underlying Supplement, as the securities involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the securities. As used herein, references to the “Issuer”, “HSBC”, “we”, “us” and “our” are to HSBC USA Inc.

HSBC has filed a registration statement (including a prospectus, prospectus supplement and Equity Index Underlying Supplement) with the SEC for the offering to which this document relates. Before you invest, you should read the prospectus, prospectus supplement and Equity Index Underlying Supplement in that registration statement and other documents HSBC has filed with the SEC for more complete information about HSBC and this offering. You may get these documents for free by visiting EDGAR on the SEC’s web site at www.sec.gov. Alternatively, HSBC Securities (USA) Inc. or any dealer participating in this offering will arrange to send you the prospectus, prospectus supplement and Equity Index Underlying Supplement if you request them by calling toll-free 1-866-811-8049.

You may also obtain:

| 4 | The Equity Index Underlying Supplement at:https://www.sec.gov/Archives/edgar/data/83246/000114420418010782/tv486722_424b2.htm |

| 4 | The prospectus supplement at:https://www.sec.gov/Archives/edgar/data/83246/000114420418010762/tv486944_424b2.htm |

| 4 | The prospectus at:https://www.sec.gov/Archives/edgar/data/83246/000114420418010720/tv487083_424b3.htm |

We are using this document to solicit from you an offer to purchase the securities. You may revoke your offer to purchase the securities at any time prior to the time at which we accept your offer by notifying HSBC Securities (USA) Inc. We reserve the right to change the terms of, or reject any offer to purchase, the securities prior to their issuance. In the event of any material changes to the terms of the securities, we will notify you.

PAYMENT AT MATURITY

On the Maturity Date, for each security you hold, we will pay you the Final Settlement Value, which is an amount in cash, as described below:

If the Reference Return is greater than zero, you will receive a cash payment on the Maturity Date, per $1,000 Principal Amount, equal to the lesser of:

(a) $1,000 + ($1,000 × Reference Return × Upside Participation Rate); and

(b) $1,000 + ($1,000 × Maximum Cap*).

*At least 24.20% (to be determined on the Pricing Date)

If the Reference Return is less than or equal to zero but greater than or equal to the Buffer Level, you will receive $1,000 per $1,000 Principal Amount (zero return).

If the Reference Return is less than the Buffer Level, you will receive a cash payment on the Maturity Date, per $1,000 Principal Amount, calculated as follows:

$1,000 + [$1,000 × (Reference Return + 10%)].

Under these circumstances, you will lose 1% of the Principal Amount of your securities for each percentage point that the Reference Return is below the Buffer Level. For example, if the Reference Return is -30%, you will suffer a 20% loss and receive 80% of the Principal Amount, subject to the credit risk of HSBC.You should be aware that if the Reference Return is less than the Buffer Level, you will lose some or a significant portion (up to 90%) of your investment.

FWP-5

Interest

The securities will not pay interest.

Calculation Agent

We or one of our affiliates will act as calculation agent with respect to the securities.

Reference Sponsor

ICE Data Indices, LLC is the reference sponsor.

INVESTOR SUITABILITY

The securities may be suitable for you if:

| 4 | You seek an investment with an enhanced return linked to the potential positive performance of the Reference Asset and you believe the level of the Reference Asset will increase over the term of the securities. |

| 4 | You understand, and are comfortable with, the risks of investing in securities linked to an index with only 10 constituents, and the other risks relating to the Reference Asset as described under “Risk Factors.” |

| 4 | You are willing to invest in the securities based on the Maximum Cap of at least 24.20% (to be determined on the Pricing Date), which may limit your return at maturity. |

| 4 | You are willing to make an investment that is exposed to the negative Reference Return on a 1-to-1 basis for each percentage point that the Reference Return is below the Buffer Level of -10%. |

| 4 | You are willing to forgo dividends or other distributions paid to holders of the stocks included in the Reference Asset. |

| 4 | You are willing to accept the risk and return profile of the securities versus a conventional debt security with a comparable maturity issued by HSBC or another issuer with a similar credit rating. |

| 4 | You do not seek current income from your investment. |

| 4 | You do not seek an investment for which there is an active secondary market. |

| 4 | You are willing to hold the securities to maturity. |

| 4 | You are comfortable with the creditworthiness of HSBC, as Issuer of the securities. |

The securities may not be suitable for you if:

| 4 | You believe the Reference Return will be negative or that the Reference Return will not be sufficiently positive to provide you with your desired return. |

| 4 | You do not understand, and are not comfortable with, the risks of investing in securities linked to an index with only 10 constituents, and the other risks relating to the Reference Asset as described under “Risk Factors.” |

| 4 | You are unwilling to invest in the securities based on the Maximum Cap of at least 24.20% (to be determined on the Pricing Date), which may limit your return at maturity. |

| 4 | You are unwilling to make an investment that is exposed to the negative Reference Return on a 1-to-1 basis for each percentage point that the Reference Return is below the Buffer Level of -10%. |

| 4 | You seek an investment that provides full return of principal. |

| 4 | You prefer the lower risk, and therefore accept the potentially lower returns, of conventional debt securities with comparable maturities issued by HSBC or another issuer with a similar credit rating. |

| 4 | You prefer to receive the dividends or other distributions paid to holders of the stocks included in the Reference Asset. |

| 4 | You seek current income from your investment. |

| 4 | You seek an investment for which there will be an active secondary market. |

| 4 | You are unable or unwilling to hold the securities to maturity. |

| 4 | You are not willing or are unable to assume the credit risk associated with HSBC, as Issuer of the securities. |

FWP-6

RISK FACTORS

We urge you to read the section “Risk Factors” beginning on page S-1 of the accompanying prospectus supplement and page S-1 of the accompanying Equity Index Underlying Supplement. Investing in the securities is not equivalent to investing directly in any of the stocks included in the Reference Asset. You should understand the risks of investing in the securities and should reach an investment decision only after careful consideration, with your advisors, of the suitability of the securities in light of your particular financial circumstances and the information set forth in this document and the accompanying, prospectus, prospectus supplement and Equity Index Underlying Supplement.

In addition to the risks discussed below, you should review “Risk Factors” in the accompanying prospectus supplement and Equity Index Underlying Supplement including the explanation of risks relating to the securities described in the following sections:

| 4 | “— Risks Relating to All Note Issuances” in the prospectus supplement; and |

| 4 | “— General Risks Related to Indices” in the Equity Index Underlying Supplement. |

You will be subject to significant risks not associated with conventional fixed-rate or floating-rate debt securities.

Your investment in the securities may result in a loss.

You will be exposed to the decline in the Final Level from the Initial Level beyond the Buffer Level of -10%. Accordingly, if the Reference Return is less than the Buffer Level of -10%, your Payment at Maturity will be less than the Principal Amount of your securities. You will lose some or a significant portion (up to 90%) of your investment at maturity if the Reference Return is less than the Buffer Level.

The appreciation on the securities is limited by the Maximum Cap.

You will not participate in any appreciation in the level of the Reference Asset (as multiplied by the Upside Participation Rate) beyond the Maximum Cap of at least 24.20% (to be determined on the Pricing Date). You will not receive a return on the securities greater than the Maximum Cap.

The amount payable on the securities is not linked to the level of the Reference Asset at any time other than on the Final Valuation Date.

The Final Level will be based on the Official Closing Level of the Reference Asset on the Final Valuation Date, subject to postponement for non-trading days and certain market disruption events. Even if the level of the Reference Asset appreciates during the term of the securities other than on the Final Valuation Date but then decreases on the Final Valuation Date to a level that is less than the Initial Level, the Payment at Maturity may be less, and may be significantly less, than it would have been had the Payment at Maturity been linked to the level of the Reference Asset prior to such decrease. Although the actual level of the Reference Asset on the Maturity Date or at other times during the term of the securities may be higher than the Final Level, the Payment at Maturity will be based solely on the Official Closing Level of the Reference Asset on the Final Valuation Date.

Credit risk of HSBC USA Inc.

The securities are senior unsecured debt obligations of the Issuer, HSBC, and are not, either directly or indirectly, an obligation of any third party. As further described in the accompanying prospectus supplement and prospectus, the securities will rank on par with all of the other unsecured and unsubordinated debt obligations of HSBC, except such obligations as may be preferred by operation of law. Any payment to be made on the securities, including any return of principal at maturity, depends on the ability of HSBC to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of HSBC may affect the market value of the securities and, in the event HSBC were to default on its obligations, you may not receive the amounts owed to you under the terms of the securities.

The securities will not bear interest.

As a holder of the securities, you will not receive interest payments.

Changes that affect the Reference Asset will affect the market value of the securities and the amount you will receive at maturity.

The policies of the reference sponsor of the Reference Asset concerning additions, deletions and substitutions of the constituents comprising the Reference Asset and the manner in which the reference sponsor takes account of certain changes affecting those constituents included in the Reference Asset may affect the level of the Reference Asset. The policies of the reference sponsor with respect to the calculation of the Reference Asset could also affect the level of the Reference Asset. The reference sponsor may discontinue or suspend calculation or dissemination of the Reference Asset. Any such actions could affect the value of the securities and the return on the securities.

FWP-7

The securities are not insured or guaranteed by any governmental agency of the United States or any other jurisdiction.

The securities are not deposit liabilities or other obligations of a bank and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency or program of the United States or any other jurisdiction. An investment in the securities is subject to the credit risk of HSBC, and in the event that HSBC is unable to pay its obligations as they become due, you may not receive the full Payment at Maturity of the securities.

The Estimated Initial Value of the securities, which will be determined by us on the Pricing Date, will be less than the price to public and may differ from the market value of the securities in the secondary market, if any.

The Estimated Initial Value of the securities will be calculated by us on the Pricing Date and will be less than the price to public. The Estimated Initial Value will reflect our internal funding rate, which is the borrowing rate we pay to issue market-linked securities, as well as the mid-market value of the embedded derivatives in the securities. This internal funding rate is typically lower than the rate we would use when we issue conventional fixed or floating rate debt securities. As a result of the difference between our internal funding rate and the rate we would use when we issue conventional fixed or floating rate debt securities, the Estimated Initial Value of the securities may be lower if it were based on the prices at which our fixed or floating rate debt securities trade in the secondary market. In addition, if we were to use the rate we use for our conventional fixed or floating rate debt issuances, we would expect the economic terms of the securities to be more favorable to you. We will determine the value of the embedded derivatives in the securities by reference to our or our affiliates’ internal pricing models. These pricing models consider certain assumptions and variables, which can include volatility and interest rates. Different pricing models and assumptions could provide valuations for the securities that are different from our Estimated Initial Value. These pricing models rely in part on certain forecasts about future events, which may prove to be incorrect. The Estimated Initial Value does not represent a minimum price at which we or any of our affiliates would be willing to purchase your securities in the secondary market (if any exists) at any time.

The price of your securities in the secondary market, if any, immediately after the Pricing Date will be less than the price to public.

The price to public takes into account certain costs. These costs, which will be used or retained by us or one of our affiliates, include the underwriting discount, our affiliates’ projected hedging profits (which may or may not be realized) for assuming risks inherent in hedging our obligations under the securities and the costs associated with structuring and hedging our obligations under the securities. If you were to sell your securities in the secondary market, if any, the price you would receive for your securities may be less than the price you paid for them because secondary market prices will not take into account these costs. The price of your securities in the secondary market, if any, at any time after issuance will vary based on many factors, including the level of the Reference Asset and changes in market conditions, and cannot be predicted with accuracy. The securities are not designed to be short-term trading instruments, and you should, therefore, be able and willing to hold the securities to maturity. Any sale of the securities prior to maturity could result in a loss to you.

If we were to repurchase your securities immediately after the Original Issue Date, the price you receive may be higher than the Estimated Initial Value of the securities.

Assuming that all relevant factors remain constant after the Original Issue Date, the price at which HSBC Securities (USA) Inc. may initially buy or sell the securities in the secondary market, if any, and the value that may initially be used for customer account statements, if any, may exceed the Estimated Initial Value on the Pricing Date for a temporary period expected to be approximately 6 months after the Original Issue Date. This temporary price difference may exist because, in our discretion, we may elect to effectively reimburse to investors a portion of the estimated cost of hedging our obligations under the securities and other costs in connection with the securities that we will no longer expect to incur over the term of the securities. We will make such discretionary election and determine this temporary reimbursement period on the basis of a number of factors, including the tenor of the securities and any agreement we may have with the distributors of the securities. The amount of our estimated costs which we effectively reimburse to investors in this way may not be allocated ratably throughout the reimbursement period, and we may discontinue such reimbursement at any time or revise the duration of the reimbursement period after the Original Issue Date of the securities based on changes in market conditions and other factors that cannot be predicted.

The securities lack liquidity.

The securities will not be listed on any securities exchange. HSBC Securities (USA) Inc. is not required to offer to purchase the securities in the secondary market, if any exists. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the securities easily. Because other dealers are not likely to make a secondary market for the securities, the price at which you may be able to trade your securities is likely to depend on the price, if any, at which HSBC Securities (USA) Inc. is willing to buy the securities.

Potential conflicts of interest may exist.

An affiliate of HSBC has a minority equity interest in the owner of an electronic platform, through which we may make available certain structured investments offering materials. HSBC and its affiliates play a variety of roles in connection with the issuance of the securities,

FWP-8

including acting as calculation agent and hedging our obligations under the securities. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the securities. We will not have any obligation to consider your interests as a holder of the securities in taking any action that might affect the value of your securities.

Uncertain tax treatment.

For a discussion of the U.S. federal income tax consequences of your investment in a security, please see the discussion under “U.S. Federal Income Tax Considerations” herein and the discussion under “U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement.

The Reference Asset has limited actual historical information.

The Reference Asset was launched on September 26, 2017. Because the Reference Asset is of recent origin and limited actual historical performance data exists with respect to it, your investment in the securities may involve a greater risk than investing in securities linked to an index with a more established record of performance.

The historical performance of the Reference Asset should not be taken as an indication of its future performance. While the trading prices of the Index’s constituents (the “Index constituents”) will determine the Official Closing Level, it is impossible to predict whether the Official Closing Level will fall or rise. Trading prices of the Index constituents will be influenced by the complex and interrelated economic, financial, regulatory, geographic, judicial, tax, political and other factors that can affect the capital markets generally and the equity trading markets on which the Index constituents are traded, and by various circumstances that can influence the prices of the Index constituents. Due to the small number of Index constituents, the level of the Reference Asset may be materially affected by changes in the level of a small number of Index constituents, or even one Index constituent.

ICE Data Indices, LLC, as the Index Calculation Agent, may adjust the Reference Asset in a way that may affect its level, and the Index Calculation Agent has no obligation to consider your interests.

ICE Data Indices, LLC, as the Index Calculation Agent, Index Sponsor and Index Administrator, is responsible for calculating and maintaining the Reference Asset. The Index Sponsor can add, delete or substitute an Index constituent or make other methodological changes that could change the Official Closing Level. The Index Sponsor will determine, for example, which companies have an appropriate business for inclusion in the Reference Asset. Changes to the Index constituents may affect the Reference Asset, as a newly added equity security may perform significantly better or worse than the Index constituent or constituents it replaces. Additionally, the Index Sponsor may alter, discontinue or suspend calculation or dissemination of the Reference Asset. Any of these actions could adversely affect the value of the securities. As Index Calculation Agent, Index Sponsor and Index Administrator, ICE Data Indices, LLC has no obligation to consider your interests in calculating or revising the Reference Asset. See “Description of the Reference Asset.”

As discussed above, the Reference Asset was launched recently. The Index Sponsor has indicated that it expects to monitor the composition of the Reference Asset over time, including through discussions with market participants, in order to determine whether any changes to the Reference Asset or its components are necessary or appropriate. Because the Reference Asset currently has only 10 components, any additions to or deletions from the Reference Asset could have a significant impact on future levels of the Reference Asset.

HSBC and its affiliates have no affiliation with ICE Data Indices, LLC and are not responsible for any of their public disclosure of information.

HSBC and its affiliates are not affiliated with ICE Data Indices, LLC, as the Index Calculation Agent, Index Sponsor and Index Administrator (except for licensing arrangements discussed under “Description of the Reference Asset”) and have no ability to control or predict its actions, including any errors in or discontinuation of public disclosure regarding methods or policies relating to the calculation of the Reference Asset. If the Index Sponsor discontinues or suspends the calculation of the Reference Asset, it may become difficult to determine the market value of the securities and the payment at maturity, call or upon early redemption. The Calculation Agent may designate a successor index in its sole discretion. If the Calculation Agent determines in its sole discretion that no successor index comparable to the Reference Asset exists, the payment you receive at maturity, call or upon early redemption will be determined by the Calculation Agent in its sole discretion. See “Specific Terms of the Notes — Market Disruption Events” and “— Calculation Agent.” The Index Sponsor is not involved in the offer of the securities in any way and has no obligation to consider your interest as an owner of the securities in taking any actions that might affect the market value of your securities.

ICE Data Indices, LLC, as the Index Calculation Agent, Index Sponsor and Index Administrator is not involved in the offering of the securities in any way and it does not have any obligation of any sort with respect to your securities. ICE Data Indices, LLC, as Index Calculation Agent, Index Sponsor and Index Administrator does not have any obligation to take your interests into consideration for any reason, including when taking any actions that might affect the value of the securities.

We have derived the information about ICE Data Indices, LLC and the Reference Asset from publicly available information, without independent verification. Neither we nor any of our affiliates have undertaken any independent review of the publicly available

FWP-9

information about ICE Data Indices, LLC, as the Index Calculation Agent, Index Sponsor and Index Administrator or the Reference Asset contained in this document. You, as an investor in the securities, should make your own independent investigation into the ICE Data Indices, LLC, as the Index Calculation Agent, Index Sponsor and Index Administrator and the Reference Asset.

The Index Calculation Agent may, in its sole discretion, discontinue the public disclosure of the intraday and Official Closing Level of the Index.

The Index Calculation Agent is under no obligation to continue to calculate the intraday Official Closing Level of the Reference Asset, or to calculate similar values for any successor index.

The Reference Asset lacks diversification and is vulnerable to fluctuations in the technology and consumer discretionary industries.

All of the stocks included in the Reference Asset are issued by companies whose primary lines of business are in the technology and consumer discretionary industries. As a result, the stocks that will determine the performance of the Reference Asset and hence, the value of the securities, are concentrated in two industries and vulnerable to events affecting those industries. Although an investment in the securities will not give holders any ownership or other direct interests in the Index constituents, the return on an investment in the securities will be subject to certain risks, including those described below, associated with a direct equity investment in companies in the technology and consumer discretionary industries. Accordingly, by investing in the securities, you will not benefit from the diversification which could result from an investment linked to companies that operate in multiple sectors. The Reference Asset is also subject to the risk that large-capitalization stocks may underperform other segments of the equity market or the equity market as a whole. Larger, more established companies may be unable to respond quickly to new competitive challenges such as changes in technology and may not be able to attain the high growth rate of smaller companies, especially during extended periods of economic expansion.

The Reference Asset currently includes constituents in the following categories:

| · | Information Technology Sector Risk. The information technology sector includes companies engaged in internet software and services, technology hardware and storage peripherals, electronic equipment instruments and components, and semiconductors and semiconductor equipment. Information technology companies face intense competition, both domestically and internationally, which may have an adverse effect on profit margins. Information technology companies may have limited product lines, markets, financial resources or personnel. The products of information technology companies may face rapid product obsolescence due to technological developments and frequent new product introduction, unpredictable changes in growth rates and competition for the services of qualified personnel. Failure to introduce new products, develop and maintain a loyal customer base, or achieve general market acceptance for their products could have a material adverse effect on a company’s business. Companies in the information technology sector are heavily dependent on intellectual property and the loss of patent, copyright and trademark protections may adversely affect the profitability of these companies. |

| · | Internet Company Risk. Many internet-related companies have incurred large losses since their inception and may continue to incur large losses in the hope of capturing market share and generating future revenues. Accordingly, many such companies expect to incur significant operating losses for the foreseeable future, and may never be profitable. The markets in which many internet companies compete face rapidly evolving industry standards, frequent new service and product announcements, introductions and enhancements, and changing customer demands. The failure of an internet company to adapt to such changes could have a material adverse effect on the company’s business. Additionally, the widespread adoption of new internet, networking, telecommunications technologies, or other technological changes, could require substantial expenditures by an internet company to modify or adapt its services or infrastructure, which could have a material adverse effect on an internet company’s business. |

| · | Semiconductor Company Risk. Competitive pressures may have a significant effect on the financial condition of semiconductor companies and, as product cycles shorten and manufacturing capacity increases, these companies may become increasingly subject to aggressive pricing, which hampers profitability. Reduced demand for end-user products, under-utilization of manufacturing capacity, and other factors could adversely impact the operating results of companies in the semiconductor sector. Semiconductor companies typically face high capital costs and may be heavily dependent on intellectual property rights. The semiconductor sector is highly cyclical, which may cause the operating results of many semiconductor companies to vary significantly. The stock prices of companies in the semiconductor sector have been and likely will continue to be extremely volatile. |

| · | Software Industry Risk. The software industry can be significantly affected by intense competition, aggressive pricing, technological innovations, and product obsolescence. Companies in the software industry are subject to significant competitive pressures, such as aggressive pricing, new market entrants, competition for market share, short product cycles due to an accelerated rate of technological developments and the potential for limited earnings and/or falling profit margins. These |

FWP-10

| companies also face the risks that new services, equipment or technologies will not be accepted by consumers and businesses or will become rapidly obsolete. These factors can affect the profitability of these companies and, as a result, the value of their securities. Also, patent protection is integral to the success of many companies in this industry, and profitability can be affected materially by, among other things, the cost of obtaining (or failing to obtain) patent approvals, the cost of litigating patent infringement and the loss of patent protection for products (which significantly increases pricing pressures and can materially reduce profitability with respect to such products). In addition, many software companies have limited operating histories. Prices of these companies’ securities historically have been more volatile than other securities, especially over the short term. | ||

| · | Internet Information Provider Company Risk. Internet information provider companies provide internet navigation services and reference guide information and publish, provide or present proprietary advertising and/or third party content. These companies often derive a large portion of their revenues from advertising, and a reduction in spending by or loss of advertisers could seriously harm their business. This business is rapidly evolving and intensely competitive, and is subject to changing technologies, shifting user needs, and frequent introductions of new products and services. The research and development of new, technologically advanced products is a complex and uncertain process requiring high levels of innovation and investment, as well as the accurate anticipation of technology, market trends and consumer needs. The number of people who access the internet is increasing dramatically and a failure to attract and retain a substantial number of these users to a company’s products and services or to develop products and technologies that are more compatible with alternative devices, could adversely affect operating results. Concerns regarding a company’s products, services or processes that may compromise the privacy of users or other privacy related matters, even if unfounded, could damage a company’s reputation and adversely affect operating results. |

| · | Catalog and Mail Order House Company Risk. Catalog and mail order house companies may be exposed to significant inventory risks that may adversely affect operating results due to, among other factors: seasonality, new product launches, rapid changes in product cycles and pricing, defective merchandise, changes in consumer demand and consumer spending patterns, or changes in consumer tastes with respect to products. Demand for products can change significantly between the time inventory or components are ordered and the date of sale. The acquisition of certain types of inventory or components may require significant lead-time and prepayment and they may not be returnable. Failure to adequately predict customer demand or otherwise optimize and operate distribution centers could result in excess or insufficient inventory or distribution capacity, result in increased costs, impairment charges, or both. The business of catalog and mail order house companies can be highly seasonal and failure to stock or restock popular products in sufficient amounts during high demand periods could significantly affect revenue and future growth. Increased website traffic during peak periods could cause system interruptions which may reduce the volume of goods sold and the attractiveness of a company’s products and services. |

A limited number of Index constituents may affect the Official Closing Level, and the Reference Asset is not necessarily representative of its focus industry.

Each of the Index constituents represents 10% of the weight of the Reference Asset as of each quarterly rebalancing date (based on the 10 Index constituents as of the date of this document). Any reduction in the market price of any of those stocks is likely to have a substantial adverse impact on the Official Closing Level and the value of the securities. Due to the small number of Index constituents, those Index constituents and the Reference Asset itself may not necessarily follow the price movements of the entire technology and consumer discretionary industries. If the Index constituents decline in value, the Reference Asset will also decline in value, even if common stock prices of other companies in the technology and consumer discretionary industries generally increase in value. Giving effect to leverage, negative changes in the performance of one Index constituent will be magnified and have a material adverse effect on the value of the securities.

An Index constituent may be replaced upon the occurrence of certain adverse events.

An exchange may delist an Index constituent. Procedures have been established by the Index Sponsor to address such an event. Because there are only 10 Index constituents as of the date of this document, there can be no assurance that the replacement or delisting of the Index constituents, or any other force majeure event, will not have an adverse or distortive effect on the Official Closing Level or the manner in which it is calculated and, therefore, may have any adverse impact on the value of the securities. An Index constituent may also be removed from the Reference Asset, as described under “Description of the Reference Asset.”

The Reference Asset uses a proprietary selection methodology, which may not select the constituent issuers in the same manner as would other index providers or market participants.

Using a proprietary methodology discussed below, the Reference Asset seeks to identify constituent issuers that exhibit characteristics of highly-traded, high-growth technology and internet/media stocks. When selecting future constituent issuers, the Index Sponsor will focus on distinguishing between traditional technology and service companies and newer, innovative, technology-utilizing companies. There can be no assurances that the proprietary methodology used to identify constituent issuers eligible for inclusion in the Reference

FWP-11

Asset will be successful. The Index Sponsor’s methodology, to some extent, involves subjective judgments, and there can be no assurance that any or all constituent issuers included in the Reference Asset would be selected by other market participants using a similar selection process. See “Description of the Reference Asset—Index Constituent Selection.”

The Reference Asset seeks to identify constituent issuers that exhibit characteristics of highly-traded stocks.

The Reference Asset seeks to identify constituent issuers that exhibit characteristics of highly-traded, high-growth technology and internet/media stocks. Highly-traded stocks may be more susceptible to periods of over-valuation followed by “corrections” or rapid decreases in share price and may also be more sensitive to general market fluctuations or shocks. Consequently, the price of the constituents, and therefore the level of the Reference Asset, may decrease more rapidly during periods of market stress than other less highly-traded constituents or indices.

We are not currently affiliated with any of the constituent issuers.

We are not currently affiliated with any of the constituent issuers. As a result, we have no ability, nor expect to have the ability in the future, to control the actions of such constituent issuers, including actions that could affect the value of the Index constituents or the value of your securities, and we are not responsible for any disclosure made by any other company. None of the money you pay us will go to any of the constituent issuers represented in the Reference Asset and none of the constituent issuers will be involved in the offering of the securities in any way. The constituent issuers will not have any obligation to consider your interests as a holder of the securities in taking any corporate actions that might affect the value of your securities. In the event we become affiliated with any of the constituent issuers, we will have no obligation to consider your interests as a holder of the securities in taking any action with respect to such constituent issuer that might affect the value of your securities.

FWP-12

ILLUSTRATIVE EXAMPLES

The following table and examples are provided for illustrative purposes only and are hypothetical. They do not purport to be representative of every possible scenario concerning increases or decreases in the level of the Reference Asset relative to its Initial Level. We cannot predict the Final Level. The assumptions we have made in connection with the illustrations set forth below may not reflect actual events, and the hypothetical Initial Level used in the table and examples below is not expected to be the actual Initial Level of the Reference Asset. You should not take this illustration or these examples as an indication or assurance of the expected performance of the Reference Asset or the return on your securities.The Final Settlement Value may be less than the amount that you would have received from a conventional debt security with the same stated maturity, including such a security issued by HSBC. The numbers appearing in the table below and following examples have been rounded for ease of analysis.

The table below illustrates the Payment at Maturity on a $1,000 investment in the securities for a hypothetical range of Reference Returns from -100% to +100%. The following results are based solely on the assumptions outlined below. The “Hypothetical Return on the Securities” as used below is the number, expressed as a percentage, that results from comparing the Final Settlement Value per $1,000 Principal Amount to $1,000. The potential returns described here assume that your securities are held to maturity. You should consider carefully whether the securities are suitable to your investment goals. The following table and examples assume the following:

| 4 | Principal Amount: | $1,000 |

| 4 | Hypothetical Initial Level*: | 1,000.00 |

| 4 | Upside Participation Rate: | 200% |

| 4 | Hypothetical Maximum Cap*: | 24.20% |

| 4 | Buffer Level: | -10% |

*The actual Initial Level and Maximum Cap will be determined on the Pricing Date.

Hypothetical Final Level | Hypothetical Reference Return | Hypothetical Final Settlement Value | Hypothetical Return on the Securities |

| 2,000.00 | 100.000% | $1,242.00 | 24.20% |

| 1,800.00 | 80.000% | $1,242.00 | 24.20% |

| 1,600.00 | 60.000% | $1,242.00 | 24.20% |

| 1,400.00 | 40.000% | $1,242.00 | 24.20% |

| 1,300.00 | 30.000% | $1,242.00 | 24.20% |

| 1,200.00 | 20.000% | $1,242.00 | 24.20% |

| 1,121.00 | 12.100% | $1,242.00 | 24.20% |

| 1,100.00 | 10.000% | $1,200.00 | 20.00% |

| 1,050.00 | 5.000% | $1,100.00 | 10.00% |

| 1,020.00 | 2.000% | $1,040.00 | 4.00% |

| 1,010.00 | 1.000% | $1,020.00 | 2.00% |

| 1,000.00 | 0.000% | $1,000.00 | 0.00% |

| 990.00 | -1.000% | $1,000.00 | 0.00% |

| 980.00 | -2.000% | $1,000.00 | 0.00% |

| 950.00 | -5.000% | $1,000.00 | 0.00% |

| 900.00 | -10.000% | $1,000.00 | 0.00% |

| 800.00 | -20.000% | $900.00 | -10.00% |

| 700.00 | -30.000% | $800.00 | -20.00% |

| 600.00 | -40.000% | $700.00 | -30.00% |

| 200.00 | -80.000% | $300.00 | -80.00% |

| 0.00 | -100.000% | $100.00 | -90.00% |

FWP-13

The following examples indicate how the Final Settlement Value would be calculated with respect to a hypothetical $1,000 investment in the securities.

Example 1: The level of the Reference Asset increases from the Initial Level of 1,000.00 to a Final Level of 1,050.00.

| Reference Return: | 5.00% |

| Final Settlement Value: | $1,100.00 |

Because the Reference Return is positive, and the Reference Return multiplied by the Upside Participation Rate is less than the hypothetical Maximum Cap, the Final Settlement Value would be $1,100.00 per $1,000 Principal Amount, calculated as follows:

$1,000 + ($1,000 × Reference Return × Upside Participation Rate)

= $1,000 + ($1,000 × 5.00% × 200%)

= $1,100.00

Example 1 shows that you will receive the return of your principal investment plus a return equal to the Reference Return multiplied by the Upside Participation Rate when the Reference Asset appreciates and such Reference Return multiplied by the Upside Participation Rate doesnot exceed the hypothetical Maximum Cap.

Example 2: The level of the Reference Asset increases from the Initial Level of 1,000.00 to a Final Level of 1,200.00.

| Reference Return: | 20.00% |

| Final Settlement Value: | $1,242.00 |

Because the Reference Return is positive, and the Reference Return multiplied by the Upside Participation Rate is greater than the hypothetical Maximum Cap, the Final Settlement Value would be $1,242.00 per $1,000 Principal Amount, calculated as follows:

$1,000 + ($1,000 × Maximum Cap)

= $1,000 + ($1,000 × 24.20%)

= $1,242.00

Example 2 shows that you will receive the return of your principal investment plus a return equal to the hypothetical Maximum Cap when the Reference Return is positive and such Reference Return multiplied by the Upside Participation Rate exceeds the hypothetical Maximum Cap.

Example 3: The level of the Reference Asset decreases from the Initial Level of 1,000.00 to a Final Level of 920.00.

| Reference Return: | -8.00% |

| Final Settlement Value: | $1,000.00 |

Because the Reference Return is less than zero but greater than the Buffer Level of -10%, the Final Settlement Value would be $1,000.00 per $1,000 Principal Amount (a zero return).

Example 4: The level of the Reference Asset decreases from the Initial Level of 1,000.00 to a Final Level of 700.00.

| Reference Return: | -30.00% |

| Final Settlement Value: | $800.00 |

Because the Reference Return is less than the Buffer Level of -10%, the Final Settlement Value would be $800.00 per $1,000 Principal Amount, calculated as follows:

$1,000 + [$1,000 × (Reference Return + 10%)]

= $1,000 + [$1,000 × (-30.00% + 10%)]

= $800.00

Example 4 shows that you are exposed on a 1-to-1 basis to declines in the level of the Reference Asset beyond the Buffer Level of -10%.You will lose some or a significant portion (up to 90%) of your investment.

FWP-14

DESCRIPTION OF THE REFERENCE ASSET

We have derived all information contained in this document regarding the Reference Asset (or the “Index”), including, without limitation, its make-up, performance, method of calculation and changes in its constituents, from publicly available sources. Such information reflects the policies of and is subject to change by ICE Data Indices, LLC (“ICE Data”), which is the Index Sponsor, Index Administrator and Index Calculation Agent. We have not undertaken any independent review or due diligence of such information. The Index Sponsor has no obligation to continue to publish, and may discontinue the publication of, the Index. The description of the Index is summarized from its governing methodology, which is available at www.theice.com/publicdocs/data/NYSE_FANGplus_Index_Methodology.pdf. Neither the methodology nor any other information included on that website is included or incorporated by reference into this document.

Introduction

The Index is an equal-dollar weighted index designed to represent a segment of the technology and consumer discretionary sectors consisting of highly-traded growth stocks of technology and tech-enabled companies such as Facebook, Inc., Apple Inc., Amazon.com, Inc., Netflix, Inc. and Google (Alphabet Inc.). The Index currently has 10 Index constituents, which is the minimum number, but it may have more than 10 Index constituents in the future. The Index was launched on September 26, 2017. As of the date of this document, the Index constituents are Facebook, Inc., Apple Inc., Amazon.com, Inc., Netflix, Inc., Google (Alphabet Inc.), Alibaba Group Holding Limited, Baidu, Inc., Nvidia Corporation, Tesla, Inc. and Twitter, Inc.

Index Universe

The Index universe will consist of all stocks classified as Consumer Discretionary or Technology by the Index Sponsor that are listed on a major U.S. stock exchange, such as the NYSE, Nasdaq or NYSE American. American Depositary Receipts are eligible for inclusion in the Index.

Index Constituent Selection

At each quarterly rebalance, the Index universe will be screened utilizing a proprietary methodology that references, among other factors, sector classification, revenue growth and an analysis of the applicable issuer’s business. The following steps will be executed:

| · | Stocks must have a market capitalization (including all share classes and unlisted shares) of at least $5 billion; |

| · | Stocks must have a trailing six month average daily traded value (ADTV / turnover) of $50 million on the specific listing line; |

| · | The ICE Data Indices Governance Committee (the “Governance Committee”) will oversee a process to select FANG and FANG-related stocks. The FANG stocks include Facebook, Inc., Apple Inc., Amazon.com, Inc., Netflix, Inc., Google (Alphabet Inc.). Other stocks selected for the Index, in addition to satisfying the criteria in the two subparagraphs above, should exhibit characteristics of high-growth technology and internet/media stocks. ICE Data and its Governance Committee will focus on distinguishing between traditional technology and services companies and newer, innovative, technology utilizing companies using, among other factors, sector classification, revenue growth and an analysis of the issuer’s business. |

| · | The final list of companies will be equally weighted based upon the prices and Index market capitalization as of the close of trading on the third Friday of March, June, September, and December. |

Rebalances and Frequency

The general aim of the quarterly rebalance of the Index is to ensure that the selection and weightings of the Index constituents continues to reflect as closely as possible the Index’s objective of representing a segment of the technology and consumer discretionary sectors consisting of the most highly-traded and high-growth technology and internet/media stocks such as Facebook, Inc., Apple Inc., Amazon.com, Inc., Netflix, Inc., Google (Alphabet Inc.).

The Index Administrator reserves the right to, at any time, change the number of stocks comprising the Index by adding or deleting one or more stocks, or replacing one or more stocks contained in the Index with one or more substitute stocks of its choice, if in the Index Administrator’s discretion such addition, deletion or substitution is necessary or appropriate to maintain the quality and/or character of the Index. Any such action would need to be approved by the Governance Committee.

Changes to the Index constituents may occur during a scheduled rebalance and as a result of the removal of an Index constituent. The quarterly Index rebalance becomes effective after the close of the third Friday of March, June, September, and December. The rebalance announcement will be made after the close of the Wednesday preceding that third Friday. The reference date for all company-specific data and information utilized in the rebalancing process will be taken from that same day, with exception of the prices utilized to determine the shares, which will be taken from the third Friday.

FWP-15

Periodical Weighting Adjustment

At quarterly Index rebalances, the Index will be rebalances according to the methodology described above under “—Index Universe” and “—Index Constituent Selection.”

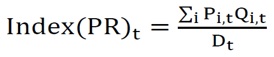

Index Calculation

The Index is calculated on a price return basis. The current Index level would be calculated by dividing the current modified Index market capitalization by the Index divisor. The divisor was determined based on the initial capitalization base of the Index and the base level. The divisor is updated as a result of corporate actions and composition changes. The general formula for the Index is:

Where:

tmeans Index Calculation Datet

Dtmeans the Index divisor on Index Calculation Datet

Pi,tmeans the price of Index constituention Index Calculation Datet

Qi,tmeans the number of shares of Index constituention Index Calculation Datet

Index Calculation Date means a U.S. Business Day where all of the Constituent Exchanges are open.

TheIndex Divisor Dt will be adjusted for corporate actions and any additions, deletions, and share changes for the Index Constituents:

Where:

Dtmeans the Index divisor on Index Calculation Datet

Index(PR)t-1 means the Price Return Index Level from Datet-1

APCi,tmeans the Adjusted Previous Close Price (for corporate actions, and, denominated in the Index Base Currency) of Index Constituention Index Calculation Datet

Qi,tmeans the number of shares of Index constituention Index Calculation Datet

The Base Date for the Index is September 19, 2014, and the Base Level is 1,000.00.

Corporate Actions

General.The Index may be adjusted in order to maintain the continuity of the Index level and the composition. Adjustments take place in reaction to events that occur with Index constituents in order to mitigate or eliminate the effect of that event on Index performance.

Removal of constituents.Any Index constituent deleted from the Index as a result of a corporate action such as a merger, acquisition, spin-off, delisting or bankruptcy will be replaced by a new stock. Thus, the total number of Index constituents in the Index will stay constant. The Governance Committee would select a replacement stock that reflects the Index’s objective and is in line with the rebalancing selection criteria as set forth above under “—Index Universe” and “—Index Constituent Selection.” If an Index constituent is removed and replaced in the Index, the divisor will be adjusted to maintain the Index level.

Mergers and Acquisitions.

| · | Merger or acquisition between Index constituents: In the event a merger or acquisition occurs between Index constituents, the acquired company is deleted and will be replaced by another company. There will be no change made to the acquiring company’s inclusion in the Index. |

| · | Merger or acquisition between an Index constituent and a non-member: A non-member is defined as a company that is not a current Index constituent. A merger or acquisition between an Index constituent and one non-member can take two forms: |

FWP-16

| o | The acquiring company is an Index constituent and the acquired company is not. There will be no action taken as to inclusion in the Index. |

| o | The acquiring company is not an Index constituent, but the acquired company is an Index constituent. The acquired company is removed from the Index and will be replaced by another company. It is possible, but not necessary, that the replacement company selected for the Index will be the acquiring company. |

Suspensions and company distress. Immediately upon an Index constituent filing for bankruptcy, an announcement will be made to remove the stock from the Index effective for the next business day following the bankruptcy. If the stock is trading on an over-the-counter (OTC) market, the last trade or price on that market is utilized as the deletion price on that day.

If the stock does not trade on the relevant exchange between the bankruptcy announcement and the deletion effective date, the stock may be deleted from the Index in that corporate action with a presumed market value of $0.

Price sources. In the event that the trading in shares is suspended or halted, the last known price established during regular daytime trading on the primary exchange will be used. Depending on the particular situation, the Index Administrator may choose to value the security at a price of $0 for purposes of Index calculation and/or Index corporate action. This would be applicable for certain extreme cases such as a company bankruptcy or severe distress when the security is no longer tradeable.

Spin-offs. The closing price of the Index constituent is adjusted by the value of the spin-off, and the shares of the Index constituent will be adjusted to maintain its existing weighting in the Index. The divisor will be adjusted to account for any changes in the overall Index market capitalization. Spun-off companies will not be added into the Index at the time of the event.

Dividends. The Index calculation incorporates regular cash dividends paid on the Index constituents and reinvests those distributions into the Index at the open of the dividend ex-date.

Rights issues and other rights.

In the event of a rights issue, the price is adjusted for the value of the right before the open on the ex-date, and the shares are increased to maintain the Index constituent’s existing weighting within the Index. The adjustment assumes that the rights issue is fully subscribed. The amount of the price adjustment is determined from the terms of the rights issue, including the subscription price, and the price of the underlying security. The Index Administrator shall only enact adjustments if the rights represent a positive value, or are in-the-money, or alternatively, represent or can be converted into a tangible cash value.

Bonus issues, stock splits and reverse stock splits. For bonus issues, stock splits and reverse stock splits, the number of shares included in the Index will be adjusted in accordance with the ratio given in the corporate action. Since the event will also incorporate a corresponding price adjustment and will not change the value of the company included in the Index, the divisor will not be changed because of this.

Changes in number of shares. Changes in the number of shares outstanding, typically due to share repurchases, tenders, or offerings, will not be reflected in the Index.

Index Governance

ICE Data is responsible for the day-to-day management of the Index, including retaining primary responsibility for all aspects of the Index determination process, including implementing appropriate governance and oversight, as required under the International Organization of Securities Commission’s Principles for Financial Benchmarks (the “IOSCO Principles”). The Governance Committee is responsible for helping to ensure ICE Data’s overall compliance with the IOSCO Principles, by performing the Oversight Function which includes overseeing the Index development, design, issuance and operation of the Index, as well as reviewing the control framework. ICE Data is also responsible for decisions regarding the interpretation of the Index methodology and the Governance Committee is responsible for reviewing all rule book modifications and Index constituent changes to ensure that they are made objectively, without bias, and in accordance with applicable law and regulation and ICE Data’s policies and procedures. Consequently, all ICE Data’s and the Governance Committee discussions and decisions are confidential until released to the public.

Cases not covered in the methodology. In cases which are not expressly covered in the methodology, operational adjustments will take place along the lines of the aim of the Index. Operational adjustments may also take place if, in the opinion of the Index Administrator, it is desirable to do so to maintain a fair and orderly market in derivatives on the Index and/or this is in the best interests of the investors in products based on the Index and/or the proper functioning of the markets. Any such modifications described in this paragraph will also be governed by any applicable and outstanding policies and procedures in place by ICE Data at such time.

Methodology changes. The Governance Committee reviews all methodology modifications and Index changes to ensure that they are made objectively, without bias and in accordance with applicable law and regulation and ICE Data’s policies and procedures. The methodology may be supplemented, amended in whole or in part, revised or withdrawn at any time. Supplements, amendments, revisions and withdrawals may also lead to changes in the way the Index is compiled or calculated or affect the Index in another way. Any such modifications described in this paragraph will also be governed by any applicable and outstanding policies and procedures in place by ICE Data at such time.

Dissemination

The Index is calculated from 9:30 a.m. until 6:00 p.m. Eastern Time on those days specified as “Index Business Days,” as that term is defined in the Index methodology. Solely for the purpose of the preceding sentence and not for the purpose of any calculation of the value of the securities, Index Business Days will be classified as days on which the U.S. Equity Markets (NYSE, Nasdaq, and NYSE American) are open for a full or partial day of trading.

FWP-17

Exceptional Market Conditions and Corrections

The Index Administrator retains the right to delay the publication of the opening level of the Index. Furthermore, the Index Administrator retains the right to suspend the publication of the level of the Index if it believes that circumstances prevent the proper calculation of the Index.

If Index constituent prices are cancelled, the Index will not be recalculated unless the Index Administrator decides otherwise.

Commercially reasonable efforts are made to ensure the correctness and validity of data used in real-time Index calculations. If incorrect price or corporate action data affects Index daily highs, lows, or closes, it is corrected retroactively as soon as possible and all revisions are communicated out to the public and market data vendors.

Announcements

Changes to the Index methodology which arise as a result of market feedback, consultations, internal reviews, or otherwise will be communicated by an Index announcement which will be distributed by ICE Data Indices at https://www.theice.com/market-data/indices/equity-indices and NYSE Market Data at https://www.theice.com/market-data/indices/equity-indices/products. The information included in those websites will not be deemed to be included or incorporated by reference in this document.

As a general rule, the announcement periods that are mentioned below will be applied. However, urgently required corporate action treatments, often resulting from late notices from the relevant company or exchange, may require the Index Administrator to deviate from the standard timing.

Inclusion of new Index constituents. The inclusion of new companies in the Index will typically only occur during the quarterly rebalance, although there could be exceptions based on a specific corporate action affecting a current Index constituent during the year. The inclusion of the new company will be announced at least one week before the effective date of the actual inclusion. For example, for the rebalance effective for September 18, 2018, the announcement would have occurred after the close on September 6, 2018.

Removal of Index constituents. Index constituents would be removed from the Index as a result of periodic corporate actions as well as the results of the quarterly rebalance. All removals will be announced at least three trading days before the effective date of the removal. It should be noted that in the case of mergers and acquisitions, every effort will be made to remove the company at some reasonable time ahead of the suspension in trading in the acquired company. There will be certain situations and corporate actions that would require the removal of a company that has already ceased trading. In those cases, the company will be removed from the Index at its last traded price, or, at the discretion of the Index Administrator, at a derived price that most accurately represents its post-suspension value.

Corporate actions. In case of an event that could affect one or more Index constituents, the Index Administrator will inform the market about the intended treatment of the event in the Index shortly after the firm details have become available and have been confirmed. When possible, the corporate action will be announced, even if not all information is known, at least one trading day before the effective date of the action. Once the corporate action has been effectuated, the Index Administrator will confirm the changes in a separate announcement.

Methodology changes. Barring exceptional circumstances, a period of at least two months should pass between the date a proposed methodology change is published and the date it goes into effect. Exceptions can be made if the change is not in conflict with the interests of a “Stakeholder,” which specifically includes external parties that subscribe to the Index data or license it as the basis for an investment product, including, but not limited to, HSBC.

Reviews; publication of new selection. The new composition of the Index, including the companies to be a part of the Index and their corresponding new Index weights, will be announced at least three trading days before the effective date and can be accessed from NYSE Market Data at www.nyse.com/market-data/indices.

FWP-18

Historical Information

Any historical upward or downward trend in value of the Index during any period shown below is not an indication that the value of the Index is more or less likely to increase or decrease at any time during the term of the securities. The historical Index returns do not give an indication of the future performance of the Index. We cannot make any assurance that the future performance of the Index will result in holders of the securities receiving a positive return on their investment.

Historical Performance of the Reference Asset

The following graph sets forth the historical performance of the Reference Asset based on the daily historical closing levels from September 30, 2017 through September 30, 2019. We obtained the closing levels below from the Bloomberg Professional® service. We have not undertaken any independent review of, or made any due diligence inquiry with respect to, the information obtained from the Bloomberg Professional® service.

The historical levels of the Reference Asset should not be taken as an indication of future performance, and no assurance can be given as to the Official Closing Level of the Reference Asset on the Final Valuation Date.

License Agreement

The NYSE FANG+™ Index is a trade mark of ICE Data or its affiliates and has been licensed, along with the Index, for use by HSBC in connection with the securities. Neither HSBC, nor the securities, as applicable, is sponsored, endorsed, sold or promoted by ICE Data. ICE Data makes no representations or warranties regarding the advisability of investing in securities generally, in the securities particularly, or the ability of the Index to track general stock market performance.

ICE DATA, ITS AFFILIATES AND ITS RESPECTIVE THIRD PARTY SUPPLIERS MAKE NO EXPRESS OR IMPLIED WARRANTIES, AND HEREBY EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE WITH RESPECT TO THE INDEX, INDEX VALUES OR ANY DATA INCLUDED THEREIN. IN NO EVENT SHALL ICE DATA HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, DIRECT, INDIRECT, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

FWP-19

EVENTS OF DEFAULT AND ACCELERATION