Annual Report

Franklin Gold and Precious Metals Fund

Your Fund’s Goals and Main Investments: Franklin Gold and Precious Metals Fund seeks capital appreciation, with current income as its secondary goal, by investing at least 80% of its net assets in securities of gold and precious metals operation companies.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. Please visit franklintempleton.com or call (800) 342-5236 for most recent month-end performance.

We are pleased to bring you Franklin Gold and Precious Metals Fund’s annual report for the fiscal year ended July 31, 2011.

Performance Overview

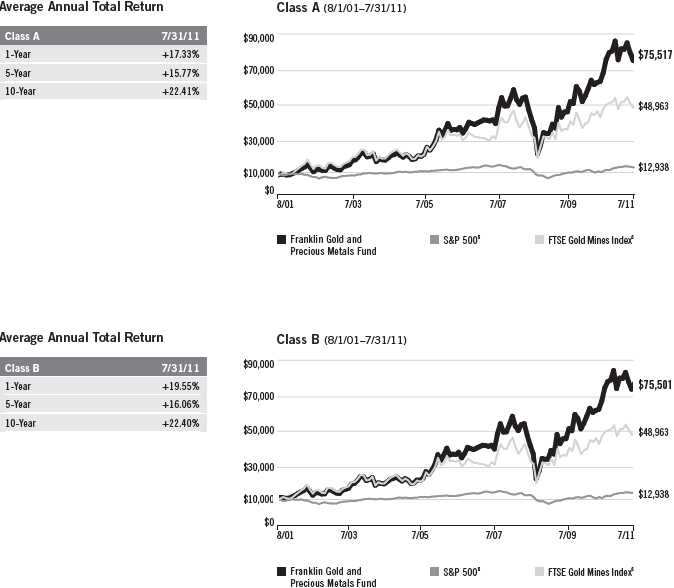

Franklin Gold and Precious Metals Fund – Class A delivered a +24.47% cumulative total return for the 12 months ended July 31, 2011. The Fund outperformed the +19.65% total return of the Standard & Poor’s® 500 Index, which is a broad measure of U.S. stock performance.1 For the same period, the Fund also outperformed the +17.18% price return of the sector-specific FTSE® Gold Mines (All Mines) Index, which comprises companies whose principal activity is gold mining.1 You can find the Fund’s long-term performance data in the Performance Summary beginning on page 11.

Economic and Market Overview

The global economy expanded despite geopolitical and inflationary pressures during the 12-month period ended July 31, 2011. The growth rate was uneven, with emerging economies growing faster than developed economies. Global manufacturing and service sector growth slowed as high commodity prices reduced purchasing power. At period-end, while the U.S. manufacturing sector grew at the slowest rate in two years, U.S. non-manufacturing output grew at the fastest rate in four months and drove global service sector growth.

1. Source: © 2011 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. STANDARD & POOR’S®, S&P® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC. Standard & Poor’s does not sponsor, endorse, sell or promote any S&P index-based product. FTSE® is a trademark of London Stock Exchange Plc and The Financial Times Limited. The indexes are unmanaged; the Standard & Poor’s 500 Index includes reinvested dividends. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

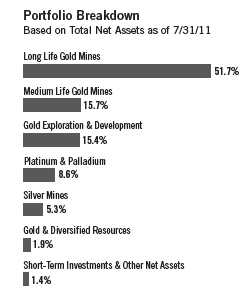

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 22.

Annual Report | 3

The U.S. financial system continued to heal, but the country still faced persistent unemployment, housing market weakness and massive debt. The U.S. Federal Reserve Board (Fed) cut its growth forecast for the world’s largest economy as manufacturing growth slowed globally. Some observers attributed the slow growth to Japan’s earthquake and its aftermath, high commodity prices and a fading inventory restocking cycle. Monetary policy tightening in most parts of the world also inhibited growth and cooled the commodities rally. Inflation rose across much of the world but stayed relatively contained in the U.S. While many central banks raised interest rates to control inflation, the Fed maintained its accommodative monetary policy and undertook a second round of quantitative easing that ended on June 30. Subsequently, the Fed continued to purchase Treasuries with proceeds from maturing debt in an effort to support economic growth.

Corporate profit strength and favorable economic prospects in some regions of the world supported equities. Global stock markets posted strong returns during the 12-month period, but positive momentum from the first nine months of the period waned as investors weathered oil supply disruptions due to revolutions and civil unrest in the Middle East and North Africa as well as the multiple crises triggered by Japan’s earthquake and tsunami. Also weighing on investor sentiment were sovereign debt worries and credit downgrades in Europe and, at period-end, the political stalemate in raising the U.S. debt ceiling by August 2, 2011, and the possibility of a U.S. debt default and credit downgrade.

Shortly after the reporting period ended, the U.S. raised its debt ceiling and avoided default. However, independent credit rating agency Standard & Poor’s (S&P) lowered the U.S. long-term rating to AA+ from AAA, citing political risks and rising debt. Extreme volatility roiled global markets as investors considered the possibility of another recession. The Fed on August 9 announced it would keep the federal funds target rate at 0.00% to 0.25% until mid-2013 to promote ongoing economic recovery. Despite political and economic head-winds, the U.S. economy continued to recover albeit at a slower pace than some anticipated.

Precious Metals Sector Overview

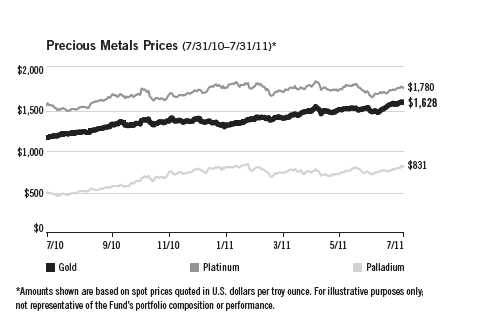

Prices for the four primary precious metals increased significantly — in gold’s case to record highs — as interest in hard assets continued to grow through July 31, 2011, and investors grew increasingly nervous about other asset classes. Attesting to gold’s rising popularity, gold investors bought about 18 million

4 | Annual Report

ounces during July 2011 alone, or roughly twice the total amount purchased in the preceding six months.2 Chinese buyers were the most active as they amassed gold jewelry, coins and bars at such a fast pace they surpassed India as the world’s number one gold buyer during the first quarter of 2011 (accounting for 25% of investment demand for gold, versus India’s 23% share).3

Gold enjoyed a nearly uninterrupted increase in value during a 12-month period fraught with equity market volatility and widespread economic uncertainty, particularly in the U.S. and Europe where policymakers sought budgeting maneuvers and longer term fiscal austerity in attempts to solve record-breaking government deficits. In response, individuals, institutional investors and government central banks all increased their gold holdings as demand for alternatives to U.S. dollars and euros took off. Gold prices began the Fund’s fiscal year at their lowest point ($1,181 per troy ounce) before spiking $447 an ounce to end the period at a new nominal record high of $1,628, for a gain of nearly 37%. Gold’s allure as a classic “safe haven” investment dulled only in January, May and June 2011, when the metal fell mildly and temporarily out of favor. Adjusted for inflation, gold prices at period-end were still lower than in 1980, when they peaked at the present-day equivalent of just under $2,500 per ounce.4 As gold appeared headed for its 11th consecutive annual gain in 2011, its popularity remained untarnished

2. Source: Commodity Futures Trading Commission.

3. Source: World Gold Council.

4. Source: © The Financial Times Ltd., 8/8/11.

Annual Report | 5

despite historically high prices because investors feared the U.S. government would continue to pursue policies — notably zero-percent interest rates and massive fiscal deficits — that could further debase the dollar and spark untenable levels of inflation. In fact, these conditions contributed to the U.S. dollar’s 9.45% decline in value versus the currencies of its major trading partners over the reporting period, adding another key support to gold.5

While gold posted solid gains, many gold companies’ share prices lagged the metal’s advance, particularly in the latter half of the reporting period. This occurred despite solid balance sheets and improved cash generation industry-wide resulting from higher realized gold prices. In fact, gold-related stocks, which generally show a high correlation to gold prices, showed little correlation during the first seven months of 2011. A possible reason for this performance included investor fear that increased cost pressures could make it difficult for gold companies to translate higher gold prices into improved earnings. The mining industry is a large energy consumer, so rising oil prices through April drove up costs and pressured profit margins. The industry also announced significant increases in capital expenditures for new projects due to difficulties in finding skilled engineers and escalating equipment costs. Meanwhile, mining exploration and production operations faced increased geopolitical risk, the threat of rising taxes and environmental resistance to mining.

Widespread risk aversion also contributed to rising silver prices, allowing it to far outpace gold and other precious metals. Overall, silver’s sharp rally from $18 per ounce on July 31, 2010, to its intra-period peak of more than $48 on April 28, 2011, was deemed slightly excessive by traders as it neared an all-time high, triggering a descent to roughly $40 by period-end. Nonetheless, the price for an ounce of silver, supported as an alternative currency with industrial demand underpinnings (particularly for consumer electronics), skyrocketed more than 121% during the Fund’s fiscal year.

Bullish momentum also underpinned double-digit price increases for industrially linked platinum and palladium. Platinum touched an intra-period high of $1,873 per ounce at the end of April (for reference, its record high above $2,200 occurred in March 2008), while in late February palladium jumped to $857 per ounce, the costliest level in almost 10 years (its all-time high was $1,125 in January 2001). Both metals were generally range-bound for the last few months of the Fund’s fiscal year as previously robust global manufacturing activity began to cool. Despite retreating from their peak levels, platinum returned 13.2% for the 12-month period (ending at $1,781 per ounce), while palladium rose an outsized 67.1% even though its per-ounce spot price declined

5. Source: Federal Reserve H10 Report.

6 | Annual Report

to $831 by period-end. These metals are commonly used in jewelry and as catalysts to clean vehicle exhaust. Toward period-end, palladium was in the midst of its biggest shortage in three decades as supplies from mines and warehouses have dwindled. Producers found it challenging to keep up with demand because investment in new mines slowed during the financial crisis and had yet to fully ramp up by period-end.

Investment Strategy

We believe that investing in gold and other precious metals offers an excellent opportunity for diversification in an attractive asset class over the long term. We like companies with multiple mines, attractive production profiles, strong reserve bases and active exploration programs that can drive future reserve and production growth. While the sector can be volatile, especially over the short term, precious metals, such as gold, can be attractive because they are hard assets not tied to any particular country or financial system.

Manager’s Discussion

Given the high-price environment discussed above, merger and acquisition activity continued at a brisk pace during the 12 months under review. Newcrest Mining successfully closed its acquisition of Lihir Gold in October 2010. The combined entity created the world’s third-largest gold company by market capitalization, and the company’s stock continued to be the Fund’s largest holding as of period-end. During the period, Kinross Gold acquired Red Back Mining, taking control of the Tasiast mine in Mauritania where the mineral inventory has grown to more than 21 million ounces through an aggressive exploration campaign. Elsewhere, Goldcorp continued its asset restructuring by acquiring Andean Minerals, which had an attractive high-grade development project in Argentina. Anatolia Minerals announced a merger with Avoca Resources to create a new middle-capitalization mining company with key assets in Turkey and Australia. In a move that was met with market disapproval, Barrick Gold acquired Equinox Minerals, which operated a large copper mine in Zambia and a copper and gold development project in Saudi Arabia. Newmont Mining bought Frontier Gold, giving the company a new gold development opportunity in Nevada.

In this environment, most of the Fund’s investments appreciated in value during its fiscal year, adding to its solid long-term track record. As gold soared to all-time highs, most of our holdings in gold-mining companies followed suit until pricing momentum for gold-related stocks faded in January. Toward period-end, many gold company stocks continued to trade below levels reached in December 2010 despite significantly higher gold prices.

Annual Report | 7

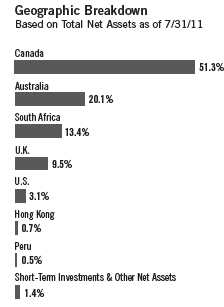

Key Fund contributors from the group included Newcrest Mining, whose shares were supported by its successful acquisition of Lihir Gold, establishing Newcrest as one of the world’s largest gold mining companies. Newcrest operates mines in Australia, Papua New Guinea, Indonesia and Ivory Coast, creating what we believe is an excellent base of production and cash flow to fund its pipeline of potentially attractive growth projects.

Our position in Nevsun Resources also delivered strong returns and significantly aided the Fund’s overall results. Nevsun successfully commissioned the gold circuit of the Bisha Mine in Eritrea, Africa, in the first half of 2011. The Bisha project is a high-grade gold, copper and zinc deposit that has received continuous support from the Eritrean government, which granted Nevsun’s mining license in January 2008. The project is positioned to become the first modern-day mine in this northeast African country. Plans are for the Bisha Mine to be a low-cost gold producer for its first two years and a low-cost, high-grade copper and zinc producer for its remaining 13-year mine life. Nevsun management also believed that further resource potential existed at depth and from nearby discoveries within the company’s licensed areas.

Centerra Gold was another significant contributor to Fund performance. Its share price climbed in response to strong operating results at the company’s Kumtor mine in Kyrgyzstan and diminishing concern over the political changes that took place there in 2010.

Our investment in U.K.-based Fresnillo also appreciated meaningfully during the year as investors sought companies that could benefit from skyrocketing silver and gold prices. The company focuses primarily on silver mining throughout Mexico but also produces significant amounts of gold. Its assets include five operating mines and further development projects elsewhere in the region. Fresnillo has produced nearly 370,000 ounces of gold and more than 38 million ounces of silver annually, making it one of the world’s largest silver producers. With low costs and higher silver prices, Fresnillo enjoyed some of the industry’s biggest margins.

Despite the Fund’s outperformance of its benchmark indexes, some holdings declined in value. For example, shares of Impala Platinum Holdings, a South African mining company and the world’s second-largest platinum producer, declined as prices for industrially linked metals such as platinum and palladium (which Impala also produces) declined in the latter half of the fiscal year. This occurred largely in response to lowered economic growth estimates across much of the developed world, potentially reducing industrial and consumer demand for both metals’ end products. Concerns over escalating wages and

8 | Annual Report

power costs and increased debate about mine nationalization in South Africa also weighed on share price performance. Anglo American Platinum, another South African miner, was similarly affected and fell in price.

Shares in East Asia Minerals plummeted during the period as the negative impact from a disappointing initial resources estimate for its Miwah gold and silver project in Indonesia was compounded by the company’s decision to undertake a complex strategy to split its assets into four separate companies.

Our investment in Centamin Egypt, an Australia-based company whose principal asset is the Sukari gold mine in Egypt’s Eastern Desert near the Red Sea, also lost value during the year under review. Shares of Centamin performed poorly as political upheaval and pending government reforms remained contentious through July 2011. Although the mine was able to operate through much of the turmoil in Egypt given its relatively remote location, the company experienced delays with blasting, which negatively affected production in 2011.

Primero Mining, a Canada-based precious metals producer with operations in Mexico and Australia, was another detractor within the Fund’s portfolio. The company’s share price declined as high silver prices created a drag on earnings given the structure of a silver sales agreement with Silver Wheaton. In July, Northgate Minerals announced plans to merge with Primero to form a new mid-tier gold producer, combining Northgate’s Young-Davidson development project in Ontario, Canada, with Primero’s existing operations.

It is important to recognize the effect of currency movements on the Fund’s performance. In general, if the value of the U.S. dollar increases compared with a foreign currency, an investment traded in that foreign currency will decrease in value because it will be worth fewer U.S. dollars. This can have a negative effect on Fund performance. Conversely, when the U.S. dollar weakens in relation to a foreign currency, an investment traded in that foreign currency will increase in value, which can contribute to Fund performance. For the 12 months ended July 31, 2011, the U.S. dollar fell in value relative to most currencies. As a result, the Fund benefited from a currency gain given its predominant investment in securities with non-U.S. currency exposure. However, one cannot expect the same result in future periods. An offsetting factor to the direct currency impact on Fund performance was the fact that many gold companies operate mines with costs in foreign currencies, while revenue from the sale of gold is generally in U.S. dollars. Therefore, the U.S. dollar’s decline resulted in higher U.S. dollar operating costs, which tended to have a negative effect on local stock prices.

Annual Report | 9

10 | Annual Report

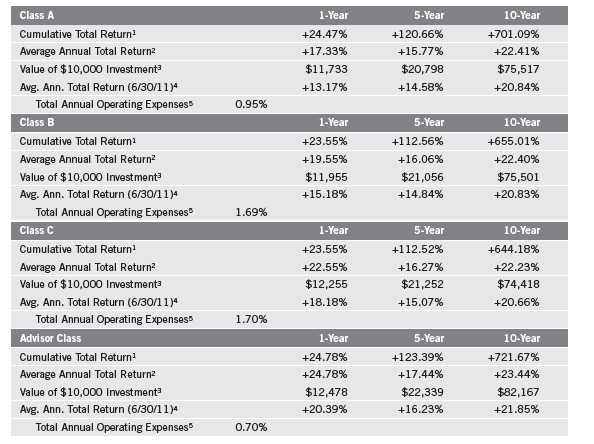

Performance Summary as of 7/31/11

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table and graphs do not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

Annual Report | 11

Performance Summary (continued)

Performance

Cumulative total return excludes sales charges. Average annual total returns and value of $10,000 investment include maximum sales charges. Class A: 5.75% maximum initial sales charge; Class B: contingent deferred sales charge (CDSC) declining from 4% to 1% over six years, and eliminated thereafter; Class C: 1% CDSC in first year only; Advisor Class: no sales charges.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

12 | Annual Report

Performance Summary (continued)

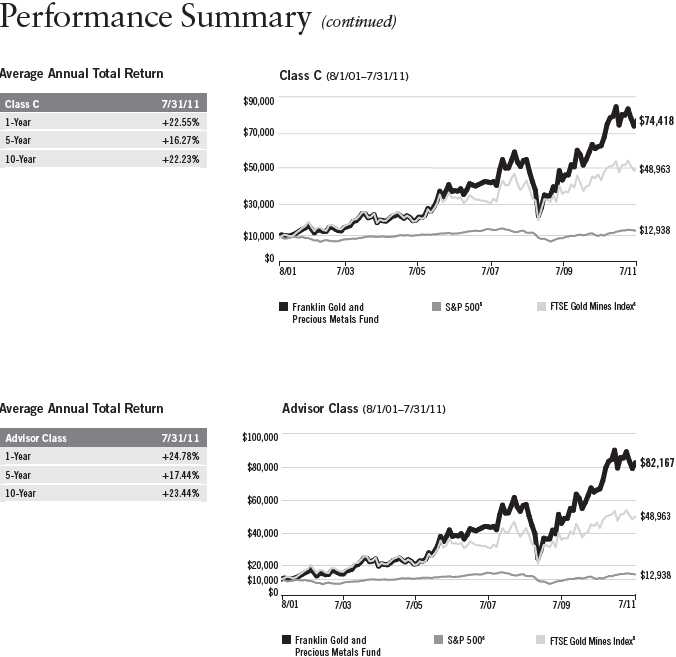

Total Return Index Comparison for a Hypothetical $10,000 Investment

Total return represents the change in value of an investment over the periods shown. It includes any current, applicable, maximum sales charge, Fund expenses, account fees and reinvested distributions. The indexes are unmanaged, differ from the Fund in composition and do not pay management fees or expenses. One cannot invest directly in an index.

Annual Report | 13

14 | Annual Report

Performance Summary (continued)

Endnotes

Investing in a nondiversified fund involves the risk of greater price fluctuation than a more diversified portfolio. Also, the Fund concentrates in the precious metals sector, which involves fluctuations in the price of gold and other precious metals and increased susceptibility to adverse economic and regulatory developments affecting the sector. In addition, the Fund is subject to the risks of currency fluctuation and political uncertainty associated with foreign investing. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. The Fund may also invest in smaller companies, which can be particularly sensitive to changing economic conditions, and their prospects for growth are less certain than those of larger, more established companies. The manager applies various techniques and analyses in making investment decisions for the Fund, but there can be no guarantee that these decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

| |

Class B: Class C: | These shares have higher annual fees and expenses than Class A shares. Prior to 1/1/04, these shares were offered with an initial sales charge; thus actual total returns would have differed. These shares have higher annual fees and expenses than Class A shares. |

Advisor Class: | Shares are available to certain eligible investors as described in the prospectus. |

1. Cumulative total return represents the change in value of an investment over the periods indicated.

2. Average annual total return represents the average annual change in value of an investment over the periods indicated. 3. These figures represent the value of a hypothetical $10,000 investment in the Fund over the periods indicated.

4. In accordance with SEC rules, we provide standardized average annual total return information through the latest calendar quarter.

5. Figures are as stated in the Fund’s prospectus current as of the date of this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

6. Source: © 2011 Morningstar. The S&P 500 is a market capitalization-weighted index of 500 stocks designed to measure total U.S. equity market performance and includes reinvested dividends. The FTSE Gold Mines Index is a free float-weighted index that comprises companies whose principal activity is gold mining. This is a price-only index and does not include dividends.

Annual Report | 15

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| | If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| | If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

16 | Annual Report

Your Fund’s Expenses (continued)

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

| | | | | | |

| | | Beginning Account | | Ending Account | | Expenses Paid During |

| Class A | | Value 2/1/11 | | Value 7/31/11 | | Period* 2/1/11–7/31/11 |

| Actual | $ | 1,000 | $ | 1,041.10 | $ | 4.81 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,020.08 | $ | 4.76 |

| Class B | | | | | | |

| Actual | $ | 1,000 | $ | 1,037.50 | $ | 8.59 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,016.36 | $ | 8.50 |

| Class C | | | | | | |

| Actual | $ | 1,000 | $ | 1,037.40 | $ | 8.59 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,016.36 | $ | 8.50 |

| Advisor Class | | | | | | |

| Actual | $ | 1,000 | $ | 1,042.40 | $ | 3.54 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,021.32 | $ | 3.51 |

*Expenses are calculated using the most recent six month expense ratio, annualized for each class (A: 0.95%; B: 1.70%; C: 1.70%; and Advisor: 0.70%), multiplied by the average account value over the period, multiplied by 181/365 to reflect the one-half year period.

Annual Report | 17

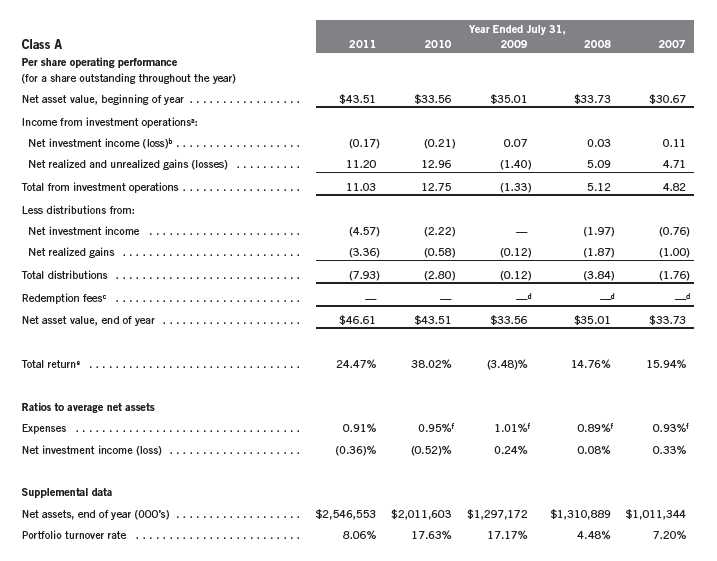

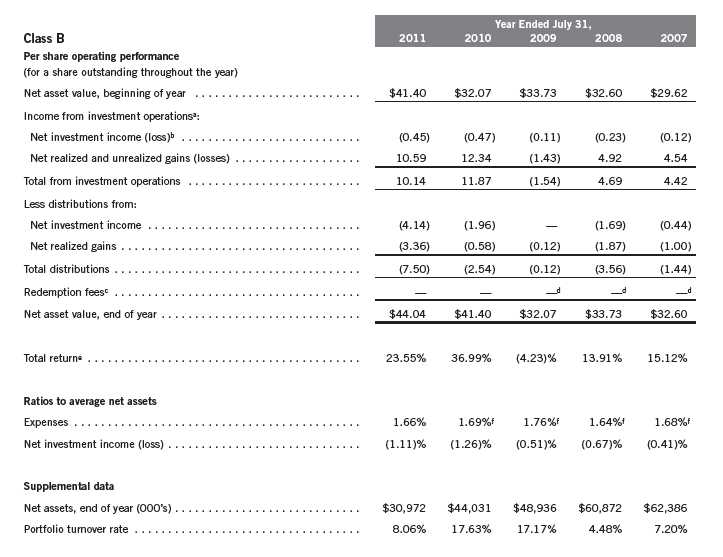

Franklin Gold and Precious Metals Fund

Financial Highlights

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of

the Fund shares in relation to income earned and/or fluctuating market value of the investments of the Fund.

bBased on average daily shares outstanding.

cEffective September 1, 2008, the redemption fee was eliminated.

dAmount rounds to less than $0.01 per share.

eTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable.

fBenefit of expense reduction rounds to less than 0.01%.

18 | The accompanying notes are an integral part of these financial statements. | Annual Report

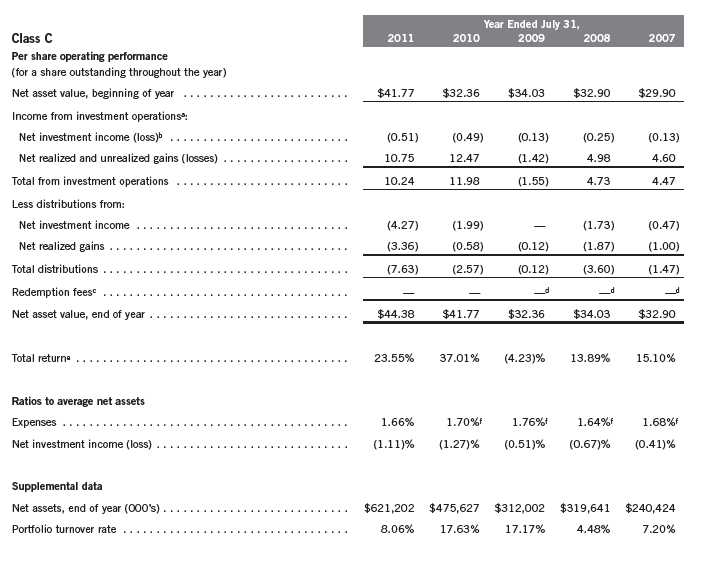

Franklin Gold and Precious Metals Fund

Financial Highlights (continued)

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of

the Fund shares in relation to income earned and/or fluctuating market value of the investments of the Fund.

bBased on average daily shares outstanding.

cEffective September 1, 2008, the redemption fee was eliminated.

dAmount rounds to less than $0.01 per share.

eTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable.

fBenefit of expense reduction rounds to less than 0.01%.

Annual Report | The accompanying notes are an integral part of these financial statements. | 19

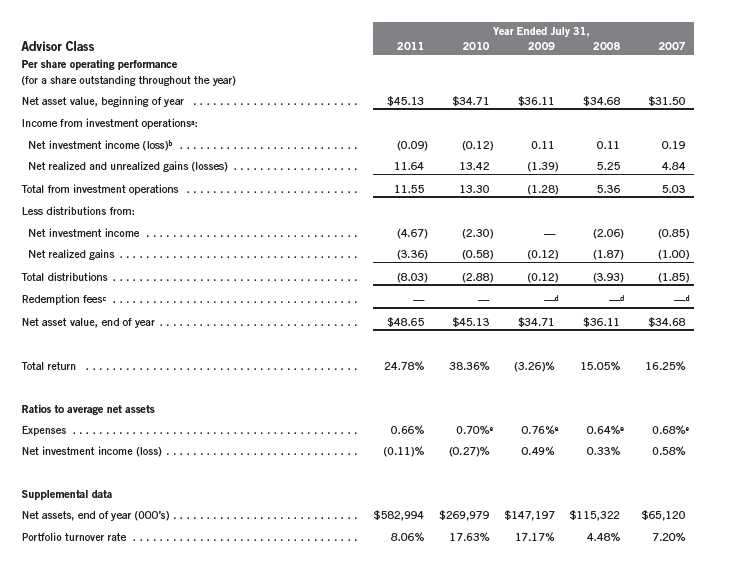

Franklin Gold and Precious Metals Fund

Financial Highlights (continued)

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of

the Fund shares in relation to income earned and/or fluctuating market value of the investments of the Fund.

bBased on average daily shares outstanding.

cEffective September 1, 2008, the redemption fee was eliminated.

dAmount rounds to less than $0.01 per share.

eTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable.

fBenefit of expense reduction rounds to less than 0.01%.

20 | The accompanying notes are an integral part of these financial statements. | Annual Report

Franklin Gold and Precious Metals Fund

Financial Highlights (continued)

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of

the Fund shares in relation to income earned and/or fluctuating market value of the investments of the Fund.

bBased on average daily shares outstanding.

cEffective September 1, 2008, the redemption fee was eliminated.

dAmount rounds to less than $0.01 per share.

eBenefit of expense reduction rounds to less than 0.01%.

Annual Report | The accompanying notes are an integral part of these financial statements. | 21

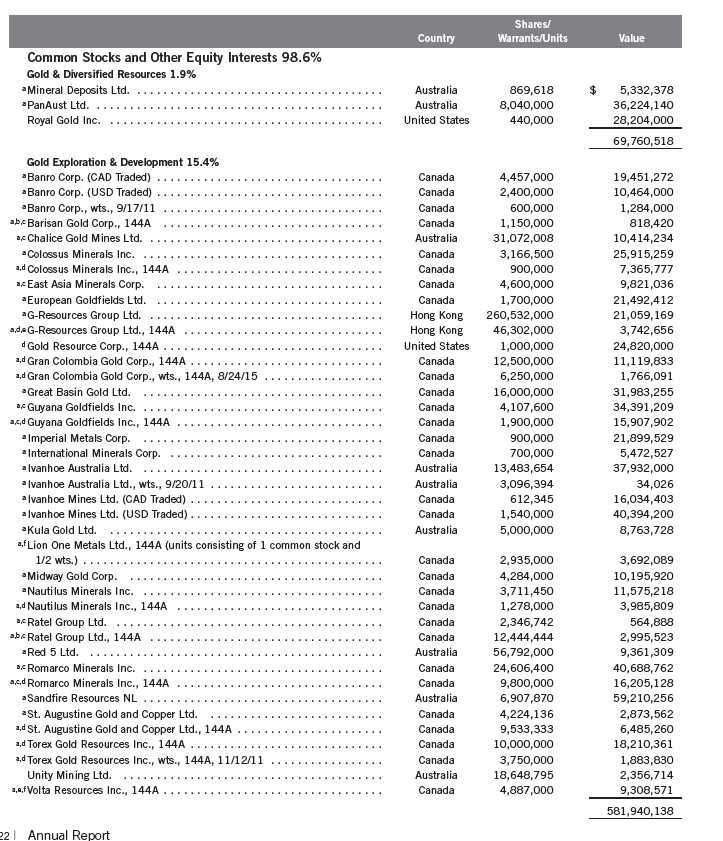

Franklin Gold and Precious Metals Fund

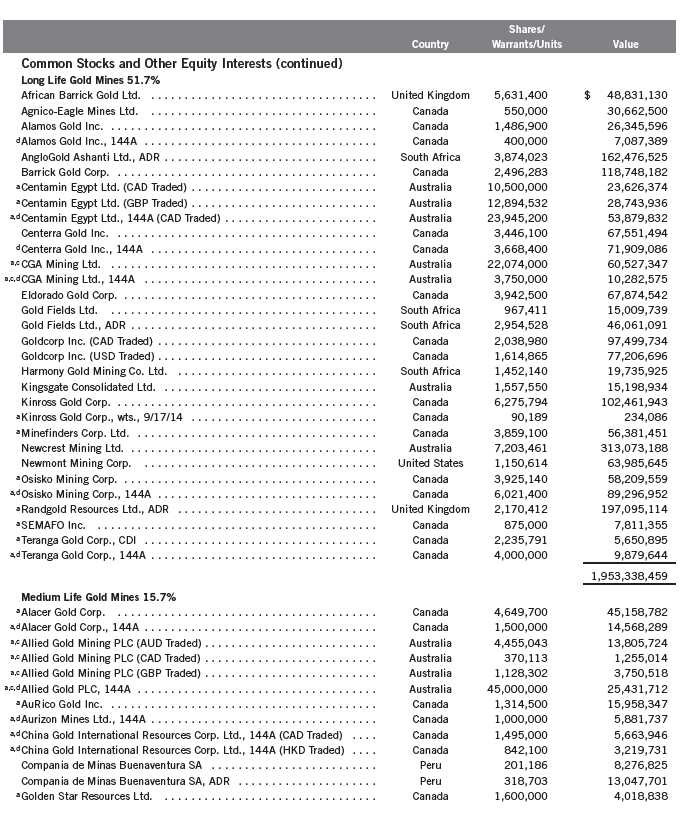

Statement of Investments, July 31, 2011

Franklin Gold and Precious Metals Fund

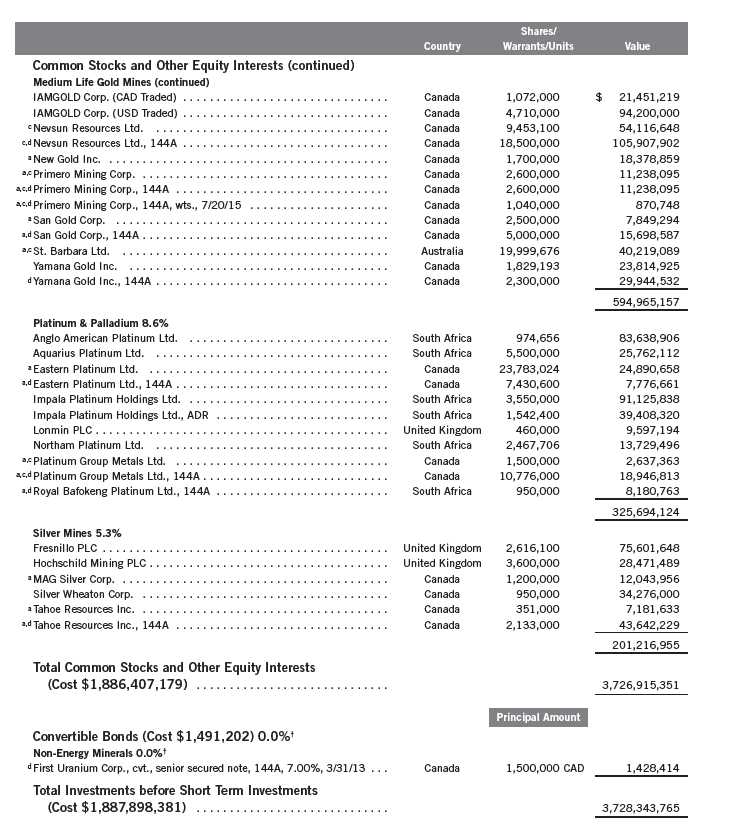

Statement of Investments, July 31, 2011 (continued)

Annual Report | 23

Franklin Gold and Precious Metals Fund

Statement of Investments, July 31, 2011 (continued)

24 | Annual Report

Annual Report | The accompanying notes are an integral part of these financial statements. | 25

Franklin Gold and Precious Metals Fund

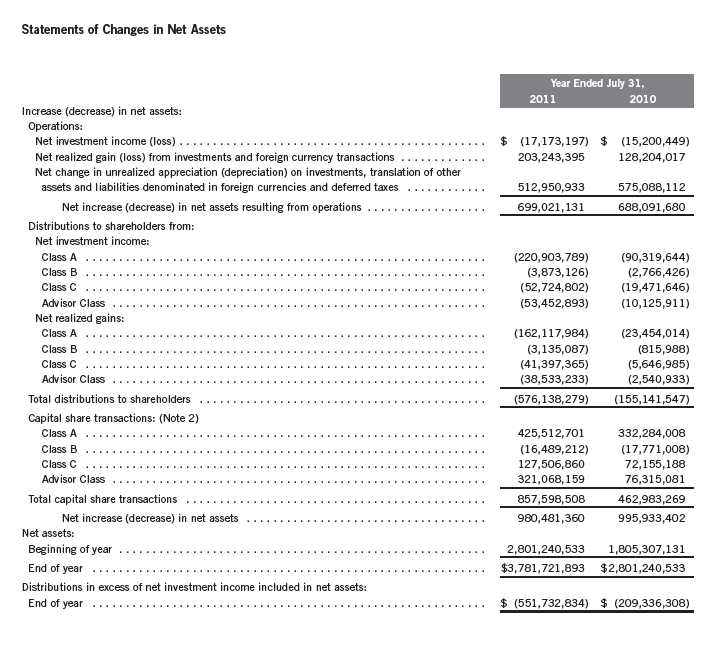

Financial Statements

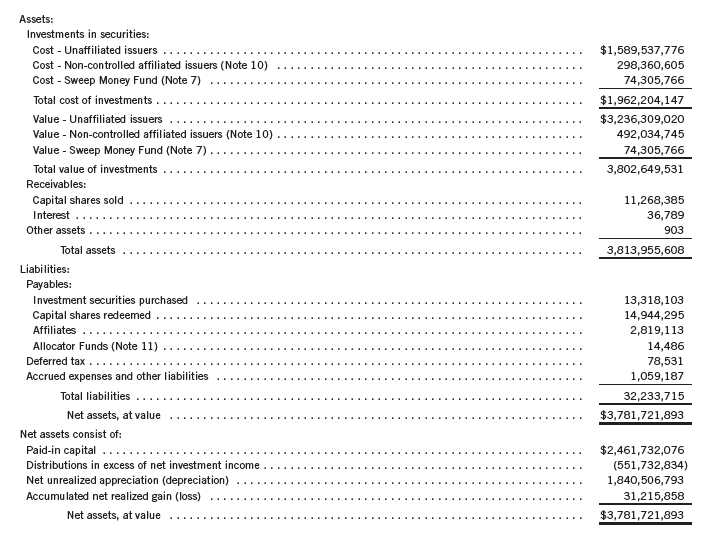

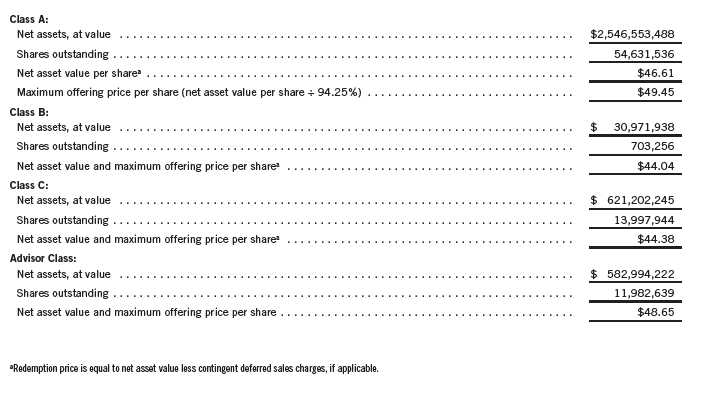

Statement of Assets and Liabilities

July 31, 2011

26 | The accompanying notes are an integral part of these financial statements. | Annual Report

Franklin Gold and Precious Metals Fund

Financial Statements (continued)

Statement of Assets and Liabilities (continued)

July 31, 2011

Annual Report | The accompanying notes are an integral part of these financial statements. | 27

Franklin Gold and Precious Metals Fund

Financial Statements (continued)

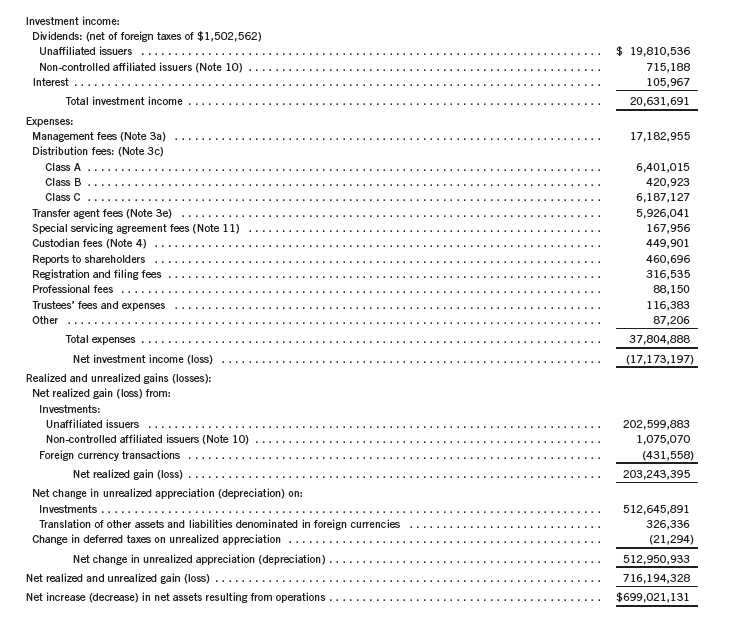

Statement of Operations

for the year ended July 31, 2011

28 | The accompanying notes are an integral part of these financial statements. | Annual Report

Franklin Gold and Precious Metals Fund

Financial Statements (continued)

Annual Report | The accompanying notes are an integral part of these financial statements. | 29

Franklin Gold and Precious Metals Fund

Notes to Financial Statements

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Franklin Gold and Precious Metals Fund (Fund) is registered under the Investment Company Act of 1940, as amended, (1940 Act) as an open-end investment company. The Fund offers four classes of shares: Class A, Class B, Class C, and Advisor Class. Each class of shares differs by its initial sales load, contingent deferred sales charges, distribution fees, voting rights on matters affecting a single class and its exchange privilege.

The following summarizes the Fund’s significant accounting policies.

a. Financial Instrument Valuation

The Fund’s investments in securities and other financial instruments are carried at fair value daily. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants on the measurement date. Under procedures approved by the Fund’s Board of Trustees, the Fund may utilize independent pricing services, quotations from securities and financial instrument dealers, and other market sources to determine fair value.

Equity securities listed on an exchange or on the NASDAQ National Market System are valued at the last quoted sale price or the official closing price of the day, respectively. Foreign equity securities are valued as of the close of trading on the foreign stock exchange on which the security is primarily traded, or the NYSE, whichever is earlier. The value is then converted into its U.S. dollar equivalent at the foreign exchange rate in effect at the close of the NYSE on the day that the value of the security is determined. Over-the-counter securities are valued within the range of the most recent quoted bid and ask prices. Securities that trade in multiple markets or on multiple exchanges are valued according to the broadest and most representative market. Certain equity securities are valued based upon fundamental characteristics or relationships to similar securities. Investments in open-end mutual funds are valued at the closing net asset value.

Debt securities generally trade in the over-the-counter market rather than on a securities exchange. The Fund’s pricing services use multiple valuation techniques to determine fair value. In instances where sufficient market activity exists, the pricing services may utilize a market-based approach through which quotes from market makers are used to determine fair value. In instances where sufficient market activity may not exist or is limited, the pricing services also utilize proprietary valuation models which may consider market characteristics such as benchmark yield curves, option-adjusted spreads, credit spreads, estimated default rates, coupon rates, anticipated timing of principal repayments, underlying collateral, and other unique security features in order to estimate the relevant cash flows, which are then discounted to calculate the fair value. Securities denominated in a foreign currency are converted into their U.S. dollar equivalent at the foreign exchange rate in effect at the close of the NYSE on the date that the values of the foreign debt securities are determined.

30 | Annual Report

Franklin Gold and Precious Metals Fund

Notes to Financial Statements (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| a. | Financial Instrument Valuation (continued) |

The Fund has procedures to determine the fair value of securities and other financial instruments for which market prices are not readily available or which may not be reliably priced. Under these procedures, the Fund primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. The Fund may also use an income-based valuation approach in which the anticipated future cash flows of the investment are discounted to calculate fair value. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. Due to the inherent uncertainty of valuations of such investments, the fair values may differ significantly from the values that would have been used had an active market existed.

Trading in securities on foreign securities stock exchanges and over-the-counter markets may be completed before the daily close of business on the NYSE. Occasionally, events occur between the time at which trading in a foreign security is completed and the close of the NYSE that might call into question the reliability of the value of a portfolio security held by the Fund. As a result, differences may arise between the value of the Fund’s portfolio securities as determined at the foreign market close and the latest indications of value at the close of the NYSE. In order to minimize the potential for these differences, the investment manager monitors price movements following the close of trading in foreign stock markets through a series of country specific market proxies (such as baskets of American Depositary Receipts, futures contracts and exchange traded funds). These price movements are measured against established trigger thresholds for each specific market proxy to assist in determining if an event has occurred that may call into question the reliability of the values of the foreign securities held by the Fund. If such an event occurs, the securities may be valued using fair value procedures, which may include the use of independent pricing services.

b. Foreign Currency Translation

Portfolio securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars based on the exchange rate of such currencies against U.S. dollars on the date of valuation. The Fund may enter into foreign currency exchange contracts to facilitate transactions denominated in a foreign currency. Purchases and sales of securities, income and expense items denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transaction date. Portfolio securities and assets and liabilities denominated in foreign currencies contain risks that those currencies will decline in value relative to the U.S. dollar. Occasionally, events may impact the availability or reliability of foreign exchange rates used to convert the U.S. dollar equivalent value. If such an event occurs, the foreign exchange rate will be valued at fair value using procedures established and approved by the Fund’s Board of Trustees.

Annual Report | 31

Franklin Gold and Precious Metals Fund

Notes to Financial Statements (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| b. | Foreign Currency Translation (continued) |

The Fund does not separately report the effect of changes in foreign exchange rates from changes in market prices on securities held. Such changes are included in net realized and unrealized gain or loss from investments on the Statement of Operations.

Realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions and the difference between the recorded amounts of dividends, interest, and foreign withholding taxes and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in foreign exchange rates on foreign denominated assets and liabilities other than investments in securities held at the end of the reporting period.

c. Securities Purchased on a Delayed Delivery Basis

The Fund purchases securities on a delayed delivery basis, with payment and delivery scheduled for a future date. These transactions are subject to market fluctuations and are subject to the risk that the value at delivery may be more or less than the trade date purchase price. Although the Fund will generally purchase these securities with the intention of holding the securities, it may sell the securities before the settlement date. Sufficient assets have been segregated for these securities.

d. Income and Deferred Taxes

It is the Fund’s policy to qualify as a regulated investment company under the Internal Revenue Code. The Fund intends to distribute to shareholders substantially all of its taxable income and net realized gains to relieve it from federal income and excise taxes. As a result, no provision for U.S. federal income taxes is required. The Fund files U.S. income tax returns as well as tax returns in certain other jurisdictions. The Fund records a provision for taxes in its financial statements including penalties and interest, if any, for a tax position taken on a tax return (or expected to be taken) when it fails to meet the more likely than not (a greater than 50% probability) threshold and based on the technical merits, the tax position may not be sustained upon examination by the tax authorities. As of July 31, 2011, and for all open tax years, the Fund has determined that no provision for income tax is required in the Fund’s financial statements. Open tax years are those that remain subject to examination and are based on each tax jurisdiction statute of limitation.

The Fund may be subject to foreign taxation related to income received, capital gains on the sale of securities and certain foreign currency transactions in the foreign jurisdictions in which it invests. Foreign taxes, if any, are recorded based on the tax regulations and rates that exist in the foreign markets in which the Fund invests. When a capital gain tax is determined to apply the Fund records an estimated deferred tax liability for unrealized gains on these securities in an amount that would be payable if the securities were disposed of on the valuation date.

32 | Annual Report

Franklin Gold and Precious Metals Fund

Notes to Financial Statements (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| e. | Security Transactions, Investment Income, Expenses and Distributions |

Security transactions are accounted for on trade date. Realized gains and losses on security transactions are determined on a specific identification basis. Interest income and estimated expenses are accrued daily. Dividend income is recorded on the ex-dividend date except that certain dividends from foreign securities are recognized as soon as the Fund is notified of the ex-dividend date. Distributions to shareholders are recorded on the ex-dividend date and are determined according to income tax regulations (tax basis). Distributable earnings determined on a tax basis may differ from earnings recorded in accordance with accounting principles generally accepted in the United States of America. These differences may be permanent or temporary. Permanent differences are reclassified among capital accounts to reflect their tax character. These reclassifications have no impact on net assets or the results of operations. Temporary differences are not reclassified, as they may reverse in subsequent periods.

Realized and unrealized gains and losses and net investment income, not including class specific expenses, are allocated daily to each class of shares based upon the relative proportion of net assets of each class. Differences in per share distributions, by class, are generally due to differences in class specific expenses.

f. Accounting Estimates

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

g. Guarantees and Indemnifications

Under the Trust’s organizational documents, its officers and trustees are indemnified by the Trust against certain liabilities arising out of the performance of their duties to the Trust. Additionally, in the normal course of business, the Trust, on behalf of the Fund, enters into contracts with service providers that contain general indemnification clauses. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred. Currently, the Trust expects the risk of loss to be remote.

Annual Report | 33

Franklin Gold and Precious Metals Fund

Notes to Financial Statements (continued)

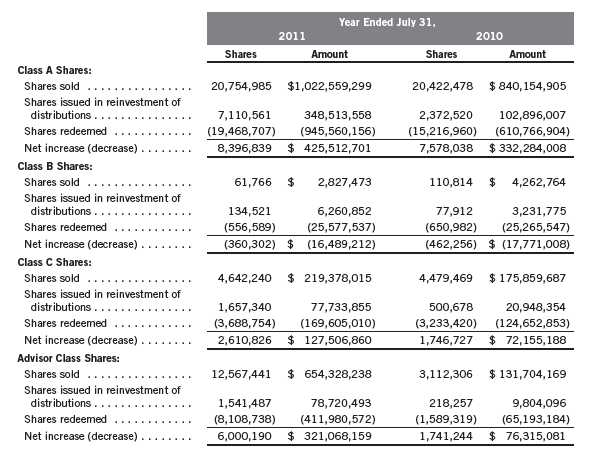

2. SHARES OF BENEFICIAL INTEREST

At July 31, 2011, there were an unlimited number of shares authorized (without par value).

Transactions in the Fund’s shares were as follows:

3. TRANSACTIONS WITH AFFILIATES

Franklin Resources, Inc. is the holding company for various subsidiaries that together are referred to as Franklin Templeton Investments. Certain officers and trustees of the Fund are also officers and/or directors of the following subsidiaries:

34 | Annual Report

Franklin Gold and Precious Metals Fund

Notes to Financial Statements (continued)

| 3. | TRANSACTIONS WITH AFFILIATES (continued) |

| a. | Management Fees |

The Fund pays an investment management fee to Advisers based on the month-end net assets of the Fund as follows:

| | |

| Annualized Fee Rate | | Net Assets |

| 0.625 | % | Up to and including $100 million |

| 0.500 | % | Over $100 million, up to and including $250 million |

| 0.450 | % | Over $250 million, up to and including $7.5 billion |

| 0.440 | % | Over $7.5 billion, up to and including $10 billion |

| 0.430 | % | Over $10 billion, up to and including $12.5 billion |

| 0.420 | % | Over $12.5 billion, up to and including $15 billion |

| 0.400 | % | In excess of $15 billion |

b. Administrative Fees

Under an agreement with Advisers, FT Services provides administrative services to the Fund. The fee is paid by Advisers based on average daily net assets, and is not an additional expense of the Fund.

c. Distribution Fees

The Fund’s Board of Trustees has adopted distribution plans for each share class, with the exception of Advisor Class shares, pursuant to Rule 12b-1 under the 1940 Act. Under the Fund’s Class A reimbursement distribution plan, the Fund reimburses Distributors for costs incurred in connection with the servicing, sale and distribution of the Fund’s shares up to the maximum annual plan rate. Under the Class A reimbursement distribution plan, costs exceeding the maximum for the current plan year cannot be reimbursed in subsequent periods.

In addition, under the Fund’s Class B and C compensation distribution plans, the Fund pays Distributors for costs incurred in connection with the servicing, sale and distribution of the Fund’s shares up to the maximum annual plan rate for each class.

The maximum annual plan rates, based on the average daily net assets, for each class, are as follows:

d. Sales Charges/Underwriting Agreements

Front-end sales charges and contingent deferred sales charges (CDSC) do not represent expenses of the Fund. These charges are deducted from the proceeds of sales of Fund shares prior to investment or from redemption proceeds prior to remittance, as applicable. Distributors has

Annual Report | 35

Franklin Gold and Precious Metals Fund

Notes to Financial Statements (continued)

3. TRANSACTIONS WITH AFFILIATES (continued) d. Sales Charges/Underwriting Agreements (continued)

advised the Fund of the following commission transactions related to the sales and redemptions of the Fund’s shares for the year:

e. Transfer Agent Fees

For the year ended July 31, 2011, the Fund paid transfer agent fees of $5,926,041, of which $3,514,844 was retained by Investor Services.

4. EXPENSE OFFSET ARRANGEMENT

The Fund has entered into an arrangement with its custodian whereby credits realized as a result of uninvested cash balances are used to reduce a portion of the Fund’s custodian expenses. During the year ended July 31, 2011, there were no credits earned.

5. INCOME TAXES

For tax purposes, realized currency losses occurring subsequent to October 31, may be deferred and treated as occurring on the first day of the following fiscal year. At July 31, 2011, the Fund deferred realized currency losses and ordinary income losses of $487,694 and $17,584,738, respectively.

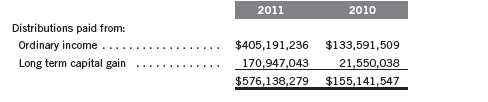

The tax character of distributions paid during the years ended July 31, 2011 and 2010, was as follows:

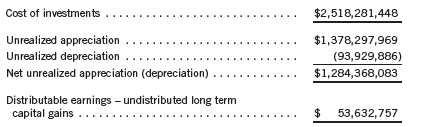

At July 31, 2011, the cost of investments, net unrealized appreciation (depreciation), and undistributed long term capital gains for income tax purposes were as follows:

36 | Annual Report

Franklin Gold and Precious Metals Fund

Notes to Financial Statements (continued)

5. INCOME TAXES (continued)

Differences between income and/or capital gains as determined on a book basis and a tax basis are primarily due to differing treatment of passive foreign investment company shares, which impacted the characterization of the distributions.

6. INVESTMENT TRANSACTIONS

Purchases and sales of investments (excluding short term securities) for the year ended July 31, 2011, aggregated $655,416,560 and $292,111,172, respectively.

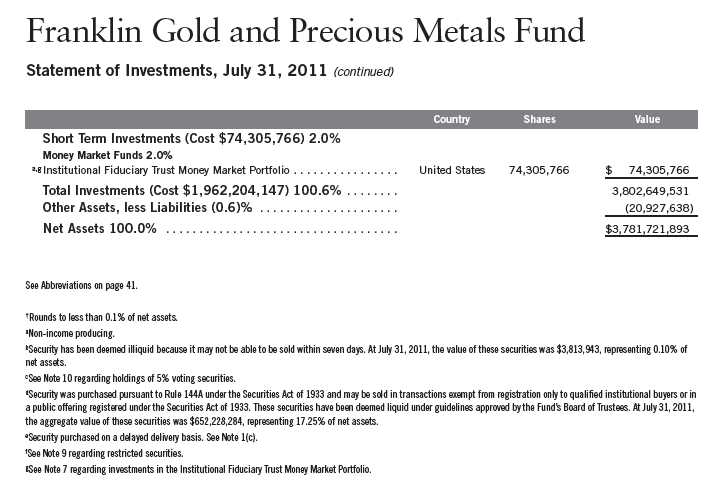

7. INVESTMENTS IN INSTITUTIONAL FIDUCIARY TRUST MONEY MARKET PORTFOLIO

The Fund invests in the Institutional Fiduciary Trust Money Market Portfolio (Sweep Money Fund), an open-end investment company managed by Advisers. Management fees paid by the Fund are reduced on assets invested in the Sweep Money Fund, in an amount not to exceed the management and administrative fees paid by the Sweep Money Fund.

8. CONCENTRATION OF RISK

Investing in foreign securities may include certain risks and considerations not typically associated with investing in U.S. securities, such as fluctuating currency values and changing local and regional economic, political and social conditions, which may result in greater market volatility. In addition, certain foreign securities may not be as liquid as U.S. securities.

9. RESTRICTED SECURITIES

The Fund invests in securities that are restricted under the Securities Act of 1933 (1933 Act) or which are subject to legal, contractual, or other agreed upon restrictions on resale. Restricted securities are often purchased in private placement transactions, and cannot be sold without prior registration unless the sale is pursuant to an exemption under the 1933 Act. Disposal of these securities may require greater effort and expense, and prompt sale at an acceptable price may be difficult. The Fund may have registration rights for restricted securities. The issuer generally incurs all registration costs.

At July 31, 2011, the Fund held investments in restricted securities, excluding certain securities exempt from registration under the 1933 Act deemed to be liquid, as follows:

Annual Report | 37

Franklin Gold and Precious Metals Fund

Notes to Financial Statements (continued)

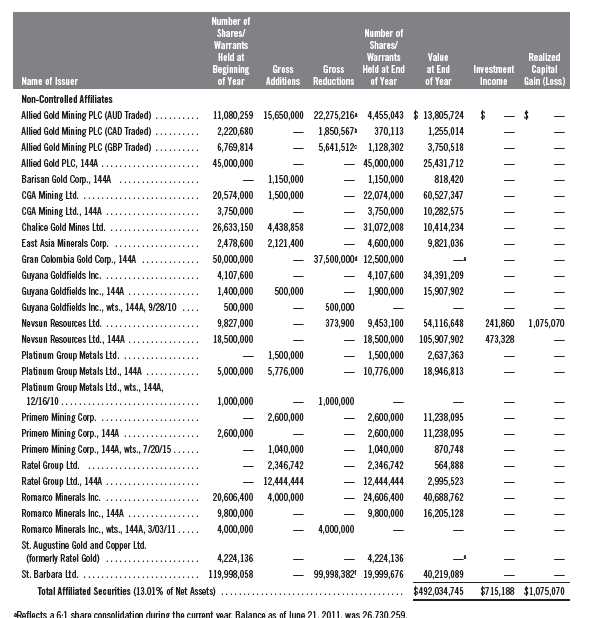

10. HOLDINGS OF 5% VOTING SECURITIES OF PORTFOLIO COMPANIES

The 1940 Act defines “affiliated companies” to include investments in portfolio companies in which a fund owns 5% or more of the outstanding voting securities. Investments in “affiliated companies” for the Fund for the year ended July 31, 2011, were as shown below.

bReflects a 6:1 share consolidation during the current year. Balance as of June 30, 2011, was 2,220,680. cReflects a 6:1 share consolidation during the current year. Balance as of June 30, 2011, was 6,769,814. dReflects a 4:1 share consolidation during the current year. Balance as of November 11, 2010, was 50,000,000. eAs of July 31, 2011, no longer an affiliate. fReflects a 6:1 share consolidation during the current year. Balance as of November 22, 2010, was 119,998,058.

38 | Annual Report

Franklin Gold and Precious Metals Fund

Notes to Financial Statements (continued)

11. SPECIAL SERVICING AGREEMENT

The Fund, which is an eligible underlying investment of one or more of the Franklin Templeton Fund Allocator Series Funds (Allocator Funds), participates in a Special Servicing Agreement (SSA) with the Allocator Funds and certain service providers of the Fund and the Allocator Funds. Under the SSA, the Fund may pay a portion of the Allocator Funds’ expenses (other than any asset allocation, administrative, and distribution fees) to the extent such payments are less than the amount of the benefits realized or expected to be realized by the Fund (e.g., due to reduced costs associated with servicing accounts) from the investment in the Fund by the Allocator Funds. The Allocator Funds are either managed by Advisers or administered by FT Services, affiliates of the Fund. For the year ended July 31, 2011, the Fund was held by one or more of the Allocator Funds and the amount of expenses borne by the Fund is noted in the Statement of Operations. At July 31, 2011, 3.07% of the Fund’s outstanding shares was held by one or more of the Allocator Funds.

12. CREDIT FACILITY

The Fund, together with other U.S. registered and foreign investment funds (collectively, Borrowers), managed by Franklin Templeton Investments, are borrowers in a joint syndicated senior unsecured credit facility totaling $750 million (Global Credit Facility) which matures on January 20, 2012. This Global Credit Facility provides a source of funds to the Borrowers for temporary and emergency purposes, including the ability to meet future unanticipated or unusually large redemption requests.

Under the terms of the Global Credit Facility, the Fund shall, in addition to interest charged on any borrowings made by the Fund and other costs incurred by the Fund, pay its share of fees and expenses incurred in connection with the implementation and maintenance of the Global Credit Facility, based upon its relative share of the aggregate net assets of all of the Borrowers, including an annual commitment fee of 0.08% based upon the unused portion of the Global Credit Facility, which is reflected in other expenses on the Statement of Operations. During the year ended July 31, 2011, the Fund did not use the Global Credit Facility.

13. FAIR VALUE MEASUREMENTS

The Fund follows a fair value hierarchy that distinguishes between market data obtained from independent sources (observable inputs) and the Fund’s own market assumptions (unobservable inputs). These inputs are used in determining the value of the Fund’s investments and are summarized in the following fair value hierarchy:

- Level 1 – quoted prices in active markets for identical securities

- Level 2 – other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speed, credit risk, etc.)

- Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

Annual Report | 39

Franklin Gold and Precious Metals Fund

Notes to Financial Statements (continued)

13. FAIR VALUE MEASUREMENTS (continued)

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities.

For movements between the levels within the fair value hierarchy, the Fund has adopted a policy of recognizing the transfers as of the date of the underlying event which caused the movement.

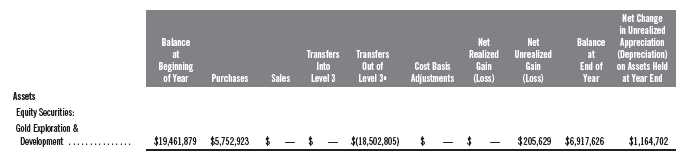

The following is a summary of the inputs used as of July 31, 2011, in valuing the Fund’s assets carried at fair value:

At July 31, 2011, the reconciliation of assets in which significant unobservable inputs (Level 3) were used in determining fair value, is as follows:

aThe investment was transferred out of Level 3 as a result of the availability of a quoted price in an active market for identical securities.

40 | Annual Report

Franklin Gold and Precious Metals Fund

Notes to Financial Statements (continued)

14. NEW ACCOUNTING PRONOUNCEMENTS

In May 2011, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2011-04, Fair Value Measurement (Topic 820): Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs. The amendments in the ASU will improve the comparability of fair value measurements presented and disclosed in financial statements prepared in accordance with U.S. GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards) and include new guidance for certain fair value measurement principles and disclosure requirements. The ASU is effective for interim and annual periods beginning after December 15, 2011. The Fund is currently evaluating the impact, if any, of applying this provision.

15. SUBSEQUENT EVENTS

The Fund has evaluated subsequent events through the issuance of the financial statements and determined that no events have occurred that require disclosure.

Annual Report | 41

Franklin Gold and Precious Metals Fund

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of Franklin Gold and Precious Metals Fund

In our opinion, the accompanying statement of assets and liabilities, including the statement of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Franklin Gold and Precious Metals Fund (the “Fund”) at July 31, 2011, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at July 31, 2011 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

San Francisco, California

September 19, 2011

42 | Annual Report

Franklin Gold and Precious Metals Fund

Tax Designation (unaudited)

Under Section 852(b)(3)(C) of the Internal Revenue Code (Code), the Fund designates the maximum amount allowable but no less than $170,947,043 as a long term capital gain dividend for the fiscal year ended July 31, 2011.

Under Section 871(k)(2)(C) of the Code, the Fund designates the maximum amount allowable but no less than $74,236,626 as a short term capital gain dividend for purposes of the tax imposed under Section 871(a)(1)(A) of the Code for the fiscal year ended July 31, 2011.

Under Section 854(b)(2) of the Code, the Fund designates the maximum amount allowable but no less than $44,264,915 as qualified dividends for purposes of the maximum rate under Section 1(h)(11) of the Code for the fiscal year ended July 31, 2011. Distributions, including qualified dividend income, paid during calendar year 2011 will be reported to shareholders on Form 1099-DIV in January 2012. Shareholders are advised to check with their tax advisors for information on the treatment of these amounts on their individual income tax returns.

Annual Report | 43

Franklin Gold and Precious Metals Fund

Board Members and Officers

The name, year of birth and address of the officers and board members, as well as their affiliations, positions held with the Fund, principal occupations during the past five years and number of portfolios overseen in the Franklin Templeton Investments fund complex are shown below. Generally, each board member serves until that person’s successor is elected and qualified.

| | | | |

| Independent Board Members | | | |

| |

| | | | Number of Portfolios in | |

| Name, Year of Birth | | Length of | Fund Complex Overseen | |

| and Address | Position | Time Served | by Board Member* | Other Directorships Held |

| Harris J. Ashton (1932) | Trustee | Since 1982 | 131 | Bar-S Foods (meat packing company) |

| One Franklin Parkway | | | | (1981-2010). |

| San Mateo, CA 94403-1906 | | | | |

Principal Occupation During Past 5 Years:

Director of various companies; and formerly, Director, RBC Holdings, Inc. (bank holding company) (until 2002); and President, Chief Executive Officer and Chairman of the Board, General Host Corporation (nursery and craft centers) (until 1998).

| | | | |

| Sam Ginn (1937) | Trustee | Since 2007 | 107 | ICO Global Communications |

| One Franklin Parkway | | | | (Holdings) Limited (satellite company) |

| San Mateo, CA 94403-1906 | | | | (2006-2010), Chevron Corporation |

| | | | | (global energy company) (1989-2009), |

| | | | | Hewlett-Packard Company (technology |

| | | | | company) (1996-2002), Safeway, Inc. |

| | | | | (grocery retailer) (1991-1998) and |

| | | | | TransAmerica Corporation (insurance |

| | | | | company) (1989-1999). |

Principal Occupation During Past 5 Years:

Private investor; and formerly, Chairman of the Board, Vodafone AirTouch, PLC (wireless company); Chairman of the Board and Chief Executive Officer, AirTouch Communications (cellular communications) (1993-1998) and Pacific Telesis Group (telephone holding company) (1988-1994).

| | | | |

| Edith E. Holiday (1952) | Trustee | Since 2003 | 131 | Hess Corporation (exploration and |

| One Franklin Parkway | | | | refining of oil and gas), H.J. Heinz |

| San Mateo, CA 94403-1906 | | | | Company (processed foods and allied |

| | | | | products), RTI International Metals, |

| | | | | Inc. (manufacture and distribution of |

| | | | | titanium), Canadian National Railway |

| | | | | (railroad) and White Mountains |

| | | | | Insurance Group, Ltd. (holding |

| | | | | company). |

Principal Occupation During Past 5 Years:

Director or Trustee of various companies and trusts; and formerly, Assistant to the President of the United States and Secretary of the Cabinet (1990-1993); General Counsel to the United States Treasury Department (1989-1990); and Counselor to the Secretary and Assistant Secretary for Public Affairs and Public Liaison – United States Treasury Department (1988-1989).

44 | Annual Report

| | | | |

| | | | Number of Portfolios in | |

| Name, Year of Birth | | Length of | Fund Complex Overseen | |

| and Address | Position | Time Served | by Board Member* | Other Directorships Held |

| J. Michael Luttig (1954) | Trustee | Since 2009 | 131 | Boeing Capital Corporation (aircraft |

| One Franklin Parkway | | | | financing). |

| San Mateo, CA 94403-1906 | | | | |

Principal Occupation During Past 5 Years:

Executive Vice President, General Counsel and member of Executive Council, The Boeing Company; and formerly, Federal Appeals Court Judge, U.S. Court of Appeals for the Fourth Circuit (1991-2006).

| | | | |

| Frank A. Olson (1932) | Trustee | Since 2005 | 131 | Hess Corporation (exploration and |

| One Franklin Parkway | | | | refining of oil and gas). |

| San Mateo, CA 94403-1906 | | | | |

Principal Occupation During Past 5 Years:

Chairman Emeritus, The Hertz Corporation (car rental) (since 2000) (Chairman of the Board (1980-2000) and Chief Executive Officer (1977-1999)); and formerly, Chairman of the Board, President and Chief Executive Officer, UAL Corporation (airlines).

| | | | |

| Larry D. Thompson (1945) | Trustee | Since 2007 | 139 | Cbeyond, Inc. (business commu- |

| One Franklin Parkway | | | | nications provider), The Southern |

| San Mateo, CA 94403-1906 | | | | Company (energy company) and |

| | | | | The Washington Post Company |

| | | | | (education and media organization). |

Principal Occupation During Past 5 Years:

John A. Sibley Professor of Corporate and Business Law, University of Georgia School of Law (2011); and formerly, Senior Vice President –Government Affairs, General Counsel and Secretary, PepsiCo, Inc. (consumer products) (2004-May 2011); Director, Delta Airlines (aviation) (2003-2005) and Providian Financial Corp. (credit card provider) (1997-2001); Senior Fellow of The Brookings Institution (2003-2004); Visiting Professor, University of Georgia School of Law (2004); and Deputy Attorney General, U.S. Department of Justice (2001-2003).

| | | | |

| John B. Wilson (1959) | Lead | Trustee since | 107 | None |

| One Franklin Parkway | Independent | 2006 and Lead | | |

| San Mateo, CA 94403-1906 | Trustee | Independent | | |

| | | Trustee since | | |

| 2008 |

Principal Occupation During Past 5 Years:

President and Founder, Hyannis Port Capital, Inc. (real estate and private equity investing); serves on private and non-profit boards; and formerly, Chief Operating Officer and Executive Vice President, Gap, Inc. (retail) (1996-2000); Chief Financial Officer and Executive Vice President – Finance and Strategy, Staples, Inc. (office supplies) (1992-1996); Senior Vice President – Corporate Planning, Northwest Airlines, Inc. (airlines) (1990-1992); and Vice President and Partner, Bain & Company (consulting firm) (1986-1990).

| | | | | |

| Interested Board Members and Officers | | | |

| |

| |

| | | | | Number of Portfolios in | |

| Name, Year of Birth | | Length of | | Fund Complex Overseen | |

| and Address | Position | Time Served | | by Board Member* | Other Directorships Held |

| **Charles B. Johnson (1933) | Trustee and | Trustee since | | 131 | None |

| One Franklin Parkway | Chairman of | 1976 | and | | |

| San Mateo, CA 94403-1906 | the Board | Chairman of the | | | |

| | | Board since 1993 | | | |

Principal Occupation During Past 5 Years:

Chairman of the Board, Member – Office of the Chairman and Director, Franklin Resources, Inc.; and officer and/or director or trustee, as the case may be, of some of the other subsidiaries of Franklin Resources, Inc. and of 41 of the investment companies in Franklin Templeton Investments.

Annual Report | 45

Annual Report | 47

48 | Annual Report

Franklin Gold and Precious Metals Fund

Shareholder Information

Board Review of Investment Management Agreement

At a meeting held April 19, 2011, the Board of Trustees (Board), including a majority of non-interested or independent Trustees, approved renewal of the investment management agreement for the Fund. In reaching this decision, the Board took into account information furnished throughout the year at regular Board meetings, as well as information prepared specifically in connection with the annual renewal review process. Information furnished and discussed throughout the year included investment performance reports and related financial information for the Fund, as well as periodic reports on expenses, shareholder services, legal, compliance, pricing, brokerage commissions and execution and other services provided by the Investment Manager (Manager) and its affiliates. Information furnished specifically in connection with the renewal process included a report for the Fund prepared by Lipper, Inc. (Lipper), an independent organization, as well as additional material, including a Fund profitability analysis prepared by management. The Lipper report compared the Fund’s investment performance and expenses with those of other mutual funds deemed comparable to the Fund as selected by Lipper. The Fund profitability analysis discussed the profitability to Franklin Templeton Investments from its overall U.S. fund operations, as well as on an individual fund-by-fund basis. Additional material accompanying such profitability analysis included information on a fund-by-fund basis listing portfolio managers and other accounts they manage, as well as information on management fees charged by the Manager and its affiliates to U.S. mutual funds and other accounts, including management’s explanation of differences where relevant. Such material also included a memorandum prepared by management describing project initiatives and capital investments relating to the services provided to the Fund by the Franklin Templeton Investments organization, as well as a memorandum relating to economies of scale and a comparative analysis concerning transfer agent fees charged the Fund.

In considering such materials, the independent Trustees received assistance and advice from and met separately with independent counsel. In approving continuance of the investment management agreement for the Fund, the Board, including a majority of independent Trustees, determined that the existing management fee structure was fair and reasonable and that continuance of the investment management agreement was in the best interests of the Fund and its shareholders. While attention was given to all information furnished, the following discusses some primary factors relevant to the Board’s decision.

NATURE, EXTENT AND QUALITY OF SERVICES. The Board was satisfied with the nature and quality of the overall services provided by the Manager and its affiliates to the Fund and its shareholders. In addition to investment performance and expenses discussed later, the Board’s opinion was based, in part, upon periodic reports furnished it showing that the investment policies and restrictions for the Fund were consistently complied with as well as other reports periodically furnished the Board covering matters such as the compliance of portfolio managers and other management personnel with the code of ethics adopted throughout the Franklin Templeton fund complex, the adherence to fair value pricing procedures established by the Board, and the accuracy of net asset value calculations. The Board also noted the extent of benefits provided Fund shareholders from being part of the Franklin Templeton family of funds, including the right to exchange

Annual Report | 49

Franklin Gold and Precious Metals Fund

Shareholder Information (continued)

Board Review of Investment Management Agreement (continued)

investments between the same class of funds without a sales charge, the ability to reinvest Fund dividends into other funds and the right to combine holdings in other funds to obtain a reduced sales charge. Favorable consideration was given to management’s continuous efforts and expenditures in establishing back-up systems and recovery procedures to function in the event of a natural disaster, it being noted that such systems and procedures had functioned smoothly during the Florida hurricanes and blackouts experienced in previous years. Among other factors taken into account by the Board were the Manager’s best execution trading policies, including a favorable report by an independent portfolio trading analytical firm. Consideration was also given to the experience of the Fund’s portfolio management team, the number of accounts managed and general method of compensation. In this latter respect, the Board noted that a primary factor in management’s determination of a portfolio manager’s bonus compensation was the relative investment performance of the funds he or she managed and that a portion of such bonus was required to be invested in a pre-designated list of funds within such person’s fund management area so as to be aligned with the interests of shareholders. The Board also took into account the quality of transfer agent and shareholder services provided Fund shareholders by an affiliate of the Manager and the continuous enhancements to the Franklin Templeton website. Particular attention was given to management’s conservative approach and diligent risk management procedures, including continuous monitoring of counterparty credit risk and attention given to derivatives and other complex instruments. The Board also took into account, among other things, management’s efforts in establishing a global credit facility for the benefit of the Fund and other accounts managed by Franklin Templeton Investments to provide a source of cash for temporary and emergency purposes or to meet unusual redemption requests as well as the strong financial position of the Manager’s parent company and its commitment to the mutual fund business as evidenced by its subsidization of money market funds.

INVESTMENT PERFORMANCE. The Board placed significant emphasis on the investment performance of the Fund in view of its importance to shareholders. While consideration was given to performance reports and discussions with portfolio managers at Board meetings during the year, particular attention in assessing such performance was given to the Lipper report furnished for the agreement renewal. The Lipper report prepared for the Fund showed the investment performance of its Class A shares during the year ended January 31, 2011, as well as the previous 10 years ended that date in comparison to a performance universe consisting of all retail and institutional precious metal funds as selected by Lipper. On a comparative basis, the Lipper report showed the Fund’s total return for the one-year period to be in the second-highest quintile of the performance universe, and on an annualized basis to be in the highest quintile of such universe for the previous three-year period, the second-highest quintile of such universe for the previous five-year period, and the second-lowest quintile of such universe for the previous 10-year period. The Board was satisfied with such performance, noting that the Fund’s total return for the 10-year period on an annualized basis exceeded 22% as set forth in the Lipper report.

50 | Annual Report

Franklin Gold and Precious Metals Fund

Shareholder Information (continued)

Board Review of Investment Management Agreement (continued)

COMPARATIVE EXPENSES. Consideration was given to a comparative analysis of the management fees and total expense ratio of the Fund compared with those of a group of other funds consisting of eight other funds selected by Lipper as its appropriate Lipper expense group. Lipper expense data is based upon information taken from each fund’s most recent annual report, which reflects historical asset levels that may be quite different from those currently existing, particularly in a period of market volatility. While recognizing such inherent limitation and the fact that expense ratios generally increase as assets decline and decrease as assets grow, the Board believed the independent analysis conducted by Lipper to be an appropriate measure of comparative expenses. In reviewing comparative costs, Lipper provides information on the Fund’s management fee in comparison with the contractual investment management fee that would have been charged by other funds within its Lipper expense group assuming they were similar in size to the Fund, as well as the actual total expense ratio of the Fund in comparison with those of its Lipper expense group. The Lipper contractual investment management fee analysis includes administrative charges as being part of a management fee, and total expenses, for comparative consistency, are shown by Lipper for Fund Class A shares. The results of such expense comparisons showed that both the contractual investment management fee rate for the Fund, as well as its actual total expense ratio, was the least expensive of its Lipper expense group. The Board was satisfied with the management fee and total expenses of the Fund in comparison to its expense group as shown in the Lipper report.

MANAGEMENT PROFITABILITY. The Board also considered the level of profits realized by the Manager and its affiliates in connection with the operation of the Fund. In this respect, the Board reviewed the Fund profitability analysis that addresses the overall profitability of Franklin Templeton’s U.S. fund business, as well as its profits in providing management and other services to each of the individual funds during the 12-month period ended September 30, 2010, being the most recent fiscal year-end for Franklin Resources, Inc., the Manager’s parent. In reviewing the analysis, attention was given to the methodology followed in allocating costs to the Fund, it being recognized that allocation methodologies are inherently subjective and various allocation methodologies may each be reasonable while producing different results. In this respect, the Board noted that, while being continuously refined and reflecting changes in the Manager’s own cost accounting, the allocation methodology was consistent with that followed in profitability report presentations for the Fund made in prior years and that the Fund’s independent registered public accounting firm had been engaged by the Manager to review the reasonableness of the allocation methodologies solely for use by the Fund’s Board in reference to the profitability analysis. In reviewing and discussing such analysis, management discussed with the Board its belief that costs incurred in establishing the infrastructure necessary for the type of mutual fund operations conducted by the Manager and its affiliates may not be fully reflected in the expenses allocated to the Fund in determining its profitability, as well as the fact that the level of profits, to a certain extent, reflected operational cost savings and efficiencies initiated by management. The Board also took into account management’s expenditures in improving shareholder services provided the Fund, as well as the need to meet additional regulatory and compliance requirements resulting from the Sarbanes-Oxley Act and recent

Annual Report | 51

Franklin Gold and Precious Metals Fund

Shareholder Information (continued)

Board Review of Investment Management Agreement (continued)