Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-05601

SEI Institutional International Trust

(Exact name of registrant as specified in charter)

c/o CT Corporation

101 Federal Street

Boston, MA 02110

(Address of principal executive offices) (Zip code)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-342-5734

Date of fiscal year end: September 30, 2009

Date of reporting period: September 30, 2009

Table of Contents

| Item 1. | Reports to Stockholders. |

Table of Contents

SEI Institutional International Trust

Annual Report as of September 30, 2009

International Equity Fund

Emerging Markets Equity Fund

International Fixed Income Fund

Emerging Markets Debt Fund

Table of Contents

| 1 | ||

| 6 | ||

| 29 | ||

| 30 | ||

| 31 | ||

| 33 | ||

| 34 | ||

| 45 | ||

| 46 | ||

| 49 | ||

Board of Trustees Considerations in Approving | 50 | |

| 53 | ||

The Trust files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q within sixty days after the end of the period. The Trust’s Form N-Q is available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Trust uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how a Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-800-DIAL-SEI; and (ii) on the Commission’s website at http://www.sec.gov.

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INTERNATIONAL TRUST — SEPTEMBER 30, 2009

International Equity Fund

I. Objective and Strategy

The International Equity Fund (“the Fund”) seeks to provide long-term capital appreciation by investing in equity securities of foreign companies.

II. Multi-Manager Approach

The Fund uses a multi-manager approach, relying upon a number of sub-advisors with differing investment philosophies to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corporation. The Fund utilized the following sub-advisors as of September 30, 2009: Acadian Asset Management, Inc., AXA Rosenberg Investment Management LLC, Declaration Management & Research LLC, INTECH Investment Management, LLC, McKinley Capital Management, Inc., Principal Global Investors, LLC, Quantitative Management Associates LLC and Wellington Management Company, LLC. For the year ended September 30, 2009, Acadian Asset Management, Inc., Declaration Management & Research LLC, INTECH Investment Management, LLC and Wellington Management Company, LLP were added to the Fund; AllianceBernstein L.P., Record Currency Management Limited and Smith Breeden Associates, Inc. were terminated.

III. Market Commentary

The global economic crisis continued to work its way through major economies such as the U.S., UK, Europe and Japan in the latter half of 2008 and the beginning of 2009. Equity markets were characterized by steep declines, sharp reversals and increased volatility. This was especially apparent in the Financials, Energy and Materials sectors. In early March 2009, global markets began a powerful rally. Strong fiscal and monetary stimulus plans from governments around the world seemed to positively impact the fight against recession. In general, equity markets delivered sizable gains by the end of September; however, continued high unemployment, further potential bank losses and mixed economic results have remained risks to a rapid recovery.

Asia Pacific ex-Japan was the strongest performing region during the year, as it benefited from global credit markets, increasing commodity prices and stronger economic conditions relative to its peers. Japan and Europe lagged with mixed economic data for the fiscal year. The fourth quarter of 2008 and early 2009 were characterized by extreme risk aversion and a preference for more defensive sectors. In contrast, cyclical sectors such as Financials and Materials led the market rally in the second and third quarters of 2009.

IV. Return vs. Benchmark

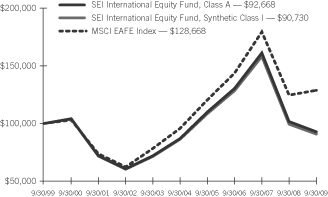

For the year ended September 30, 2009, the Fund underperformed the MSCI EAFE Index (the “Index”), returning (8.73%) versus the Index return of 3.23%.

V. Fund Attribution

Fund performance was primarily driven by stock selection. Holdings in the Financials sector detracted from performance, as the sector experienced dramatic reversals during the year. The Financials sector went from concerns over survival and unprecedented government intervention to a soaring rally by the end of the third quarter 2009. These extreme inflection points in the Financials sector made stock selection difficult. Commodities also experienced significant changes in momentum, which resulted in mixed performance for the Fund’s positions in the Materials sector. Stock selection in Telecommunications and Consumer Staples positively contributed to performance. Regionally, the Fund’s overweight allocation to emerging markets benefitted performance, as emerging markets outpaced developed regions during the time period. Stock selection in Japan and Europe detracted from performance, especially in cyclical sectors such as Financials, Materials and Industrials.

International Equity Fund

AVERAGE ANNUAL TOTAL RETURN1

| One Year Return | Annualized 3 Year Return | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||

| Class A | (8.73)% | (10.75)% | 1.25% | (0.76)% | 2.89% | |||||

| Class I | (8.80)% | (10.93)% | 1.00% | (0.97)% | 2.65% |

Comparison of Change in the Value of a $100,000 Investment in the International Equity Fund, Class A and Class I, versus the Morgan Stanley MSCI EAFE Index

| 1 | For the period ended September 30, 2009. Past performance is no indication of future performance. Class I Shares were offered beginning on January 4, 2002. Class A Shares were offered beginning December 20, 1989. Class I Shares performance for the period prior to January 4, 2002 is performance derived from the performance of the Class A Shares. The performance of Class I Shares may be lower than the performance of Class A Shares because of different distribution fees paid by Class I shareholders. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| SEI Institutional International Trust / Annual Report / September 30, 2009 | 1 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INTERNATIONAL TRUST — SEPTEMBER 30, 2009

Emerging Markets Equity Fund

I. Objective and Strategy

The Emerging Markets Equity Fund (the “Fund”) seeks to provide capital appreciation by investing in emerging-market companies.

II. Multi-Manager Approach

The Fund uses a multi-manager approach, relying upon a number of sub-advisors with differing investment philosophies to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corporation. The Fund utilized the following sub-advisors as of September 30, 2009: AllianceBernstein L.P., Artisan Partners Limited Partnership, AXA Rosenberg Investment Management LLC, PanAgora Asset Management, Inc., Rexiter Capital Management Limited and The Boston Company Asset Management LLC. No manager changes were made during the fiscal year ended September 30, 2009.

III. Market Commentary

Towards the end of 2008, emerging-markets equities witnessed some of the steepest quarterly declines on record. Significant downward pressure on commodities, a slowdown in global demand and investor risk aversion contributed to the negative market performance. However, starting in the first quarter of 2009, emerging markets decoupled from their developed counterparts and soared in the second quarter. Investor exuberance was driven by anticipation that emerging markets would benefit from global stimulus packages, domestic demand and increasing prices in commodity markets. Emerging Asia, especially China, had strong performance, which was generated in part by significant government stimulus. Eastern Europe lagged emerging peers as it struggled to weather the economic crisis.

IV. Return vs. Benchmark

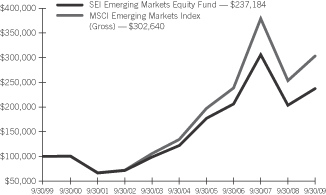

For the year ended September 30, 2009, the Fund underperformed the MSCI Emerging Markets Index (Gross) (the “Index”), returning 16.40% versus the Index return of 19.44%.

V. Fund Attribution

For the fiscal year, the Fund had negative relative performance from stock selection. Stock selection in Consumer Discretionary, especially automobiles and components, was strong. In contrast, the Fund’s underweight allocation to the Financials and Materials sectors ultimately detracted from performance for the fiscal year.

Stock selection in Russia and an allocation to Brazil, which are markets heavily influenced by commodities, posted positive returns for the Fund. However, holdings in Asia and the Pacific Rim detracted the most from Fund performance. In particular, stock selection in India was impaired by negative performance in Information Technology services.

Emerging Markets Equity Fund

AVERAGE ANNUAL TOTAL RETURN1

| One Year Return | Annualized 3 Year Return | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||

| Class A | 16.40% | 4.79% | 14.16% | 9.02% | 5.48% |

Comparison of Change in the Value of a $100,000 Investment in the

Emerging Markets Equity Fund, versus the MSCI Emerging Markets Index (Gross)

| 1 | For the period ended September 30, 2009. Past performance is no indication of future performance. Class A Shares were offered beginning January 17, 1995. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| 2 | SEI Institutional International Trust / Annual Report / September 30, 2009 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INTERNATIONAL TRUST — SEPTEMBER 30, 2009

International Fixed Income Fund

I. Objective and Strategy

The International Fixed Income Fund (“the Fund”) seeks to provide capital appreciation and current income by investing in investment-grade fixed-income securities of foreign government and corporate issuers.

II. Multi-Manager Approach

The Fund uses a multi-manager approach, relying upon a number of sub-advisors with differing investment philosophies to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corporation. The Fund utilized the following sub-advisers as of September 30, 2009: AllianceBernstein L.P., BlackRock Financial Management, Inc., Fidelity International Investment Advisors (UK) Limited, UBS Global Asset Management (Americas) Inc. and Wellington Management Company, LLP. For the year ended September 30, 2009, Wellington Management Company, LLP was added to the Fund; BlackRock Financial Management Inc. and Record Currency Management Limited were terminated.

III. Market Commentary

The fiscal year began with a worldwide economic contraction led by developed markets. Global manufacturing sank to a record low, and orders and inventory also fell rapidly. Spreads widened dramatically as a result of a massive flight to-quality, and liquidity seized up. Central banks around the globe began to coordinate efforts to fight this massive downturn, cutting interest rates and enacting government stimulus plans to provide liquidity to the market. Responses to the crisis were not in vain; during the second half of the fiscal year, the economies of several different countries began a recovery process and global consumption increased. This turnaround sparked a massive rally in early March 2009, as investors increased their risk appetites and funded new investments with cash that had previously been on the sidelines. The third quarter brought about a more tempered view of the situation, as concerns remained regarding global de-leveraging, the health of the financial system and the unwinding of government stimulus. Global labor markets remain under pressure, and global manufacturing activity has recently stalled. Although the period ended with conditions being markedly better than they were last year, we believe it will take some time before normalcy completely returns to the market.

IV. Return vs. Benchmark

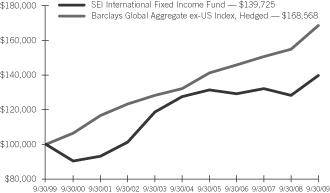

For the year ended September 30, 2009, the Fund slightly underperformed the Barclays Global Aggregate ex-US Index, Hedged, returning 8.85% versus the index return of 8.86%.

V. Fund Attribution

As spreads widened in the fourth quarter of 2008, the Fund’s overweight to Financials detracted from performance. Overweights to commercial mortgage-backed securities (“CMBS”) and mortgage-backed securities (“MBS”) also performed poorly during this period. However, during the early part of 2009, spreads began to tighten, and performance for CMBS and other loans improved. During the second and third quarters of 2009, the Fund benefited from its exposure to Financials, MBS and CMBS, as all of these securities staged massive rallies. Currency management was slightly positive over the fiscal year. An overweight to inflation-linked bonds was also slightly positive for this time period.

International Fixed Income Fund

AVERAGE ANNUAL TOTAL RETURN1

| One Year Return | Annualized 3 Year Return | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||

| Class A | 8.85% | 2.65% | 1.85% | 3.40% | 4.59% |

Comparison of Change in the Value of a $100,000 Investment in the International Fixed Income Fund, versus the Barclays Global Aggregate ex-U.S. Index, Hedged

| 1 | For the period ended September 30, 2009. Past performance is no indication of future performance. Class A Shares were offered beginning September 1, 1993. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| SEI Institutional International Trust / Annual Report / September 30, 2009 | 3 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INTERNATIONAL TRUST — SEPTEMBER 30, 2009

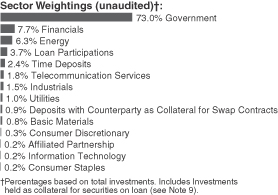

Emerging Markets Debt Fund

I. Objective and Strategy

The Emerging Markets Debt Fund (the “Fund”) invests in U.S.-dollar-denominated debt securities of government, government-rated and corporate issuers of emerging-market countries, as well as entities organized to restructure the outstanding debt of such issuers, with the goal of maximizing total return.

II. Multi-Manager Approach

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment philosophies to manage portions of the Fund’s portfolio under the general supervision of SEI Investments Management Corporation. The Fund utilized the following sub-advisers as of September 30, 2009: Ashmore Investment Management Limited, ING Investment Management Advisors, B.V. and Stone Harbor Investment Partners LP. There were no manager changes made during the fiscal year.

III. Market Commentary

There was upward momentum in emerging-markets debt as an asset class over the fiscal year, as investor risk appetite drove returns higher. With spreads reaching 900 basis points during the peak of the financial crisis, investors fled from lower-quality assets such as emerging-markets debt and moved to higher-quality assets. However, as risk in emerging markets appeared to be overpriced and spread valuations widened to a six-year high, asset prices began to climb and investor sentiment slowly improved. Additionally, market support came from the International Monetary Fund (“IMF”), which became active in lending financial support to nations in financial distress and providing much-needed liquidity to the market. Decreased financing costs resulted in a surge of new issuance from higher-quality sovereigns and corporates, followed by mid-to lower-quality countries and credits. Probably the most significant impact on emerging markets was when world leaders at the G-20 summit pledged over $1.1 trillion of additional resources to the IMF to help support the global economy. As countries slowly climbed out of recession, investor risk appetite continued to increase and inflows into emerging-market assets began to rise, providing further support.

The global economic downturn’s negative impact on emerging markets was immediate, as issuance came to a halt at the beginning

of the fiscal year. Ecuador voluntarily defaulted on its interest payments in the fourth quarter of 2008, sending additional shockwaves through the asset class. Emerging-markets debt also experienced significant investor outflows during the first half of the period, and it wasn’t until the global rally began in March that sentiment slowly began to return and technicals turned positive due to increased issuance. After delivering several downgrades to emerging nations, credit-rating agencies reversed the trend in the third quarter of 2009 and issued five upgrades and only one downgrade due to the stability of emerging economies and their ability to avoid the significant deterioration experienced in the developed world. Continued IMF support, rising commodity prices, supportive levels of reserves and a plethora of front-loaded rate cuts helped emerging economies return to equilibrium, bringing the value of the asset class to levels witnessed prior to the collapse of Lehman Brothers. Even the corporate bond sector of emerging markets, which was expected to struggle given its significant amount of leverage, was able to outperform external debt, which is owed to creditors outside the country, for the period. Gross-domestic-product growth for emerging markets during the fiscal year beat that of the developed world, and we believe emerging markets will lead the global recovery into 2010.

IV. Return vs. Benchmark

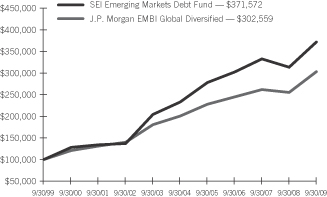

For the year ended September 30, 2009, the Fund underperformed the J.P. Morgan EMBI Global Diversified Index (the “Index”) returning 18.62% versus the Index return of 18.69%.

V. Fund Attribution

During the period, the Fund added to relative performance in Brazil through an overweight as well as security selection to local-currency-denominated assets. The real was one of the stronger performing currencies in emerging markets versus the dollar, and Brazil continues to benefit from strong fundamentals, an improving banking system and rising domestic demand. Security selection in Venezuela benefited performance as bonds were supported by higher oil prices and expectations from market participants that President Chavez would hold true to his plans to reform the broader economy. Ecuador’s choice to default on its issuance caused bonds to plummet, and our underweight position added to performance.

| 4 | SEI Institutional International Trust / Annual Report / September 30, 2009 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI INSTITUTIONAL INTERNATIONAL TRUST — SEPTEMBER 30, 2009

Emerging Markets Debt Fund (Concluded)

The Fund’s overweight to off-benchmark corporate debt hurt performance. Prices dropped on concerns that the corporate sector would struggle to meet refinancing needs and that depreciating currencies would make it more costly to service outstanding debt. Security selection in Russia, especially the banking sector, detracted from performance as the country experienced investor outflows and witnessed a 40% reduction in its international reserves to help prop up a depreciating ruble. Security selection in Mexico subtracted from relative performance as the country experienced significant fiscal deterioration due to its high correlation with the U.S. economy, which struggled for the better part of the period. A shift in the political landscape has created uncertainty over the country’s fiscal position, and a decrease in oil production at PEMEX, the country’s state-run oil company, negatively impacted government revenues.

Emerging Markets Debt Fund

AVERAGE ANNUAL TOTAL RETURN1

| One Year Return | Annualized 3 Year Return | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||

| Class A | 18.62% | 7.16% | 9.80% | 14.03% | 10.52% |

Comparison of Change in the Value of a $100,000 Investment in the Emerging Markets Debt Fund, versus the J.P. Morgan EMBI Global Diversified Index

| 1 | For the period ended September 30, 2009. Past performance is no indication of future performance. Class A Shares were offered beginning June 26, 1997. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| SEI Institutional International Trust / Annual Report / September 30, 2009 | 5 |

Table of Contents

SUMMARY SCHEDULE OF INVESTMENTS

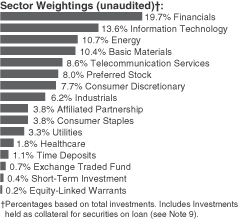

International Equity Fund

September 30, 2009

| Description | Percentage of Net Assets (%) | Shares | Market Value ($ Thousands) | |||||||

COMMON STOCK — 88.8% |

| |||||||||

Argentina — 0.0% |

| |||||||||

Other Securities | 0.0 | % | $ | 575 | ||||||

Australia — 4.9% | ||||||||||

BHP Billiton | 0.7 | 430,742 | 14,343 | |||||||

Other Securities | 4.2 | 85,818 | ||||||||

| 100,161 | ||||||||||

Austria — 0.2% | ||||||||||

Other Securities | 0.2 | 4,824 | ||||||||

Belgium — 1.2% | ||||||||||

Other Securities | 1.2 | 24,496 | ||||||||

Brazil — 0.5% | ||||||||||

Other Securities | 0.5 | 10,941 | ||||||||

Canada — 1.6% | ||||||||||

Other Securities | 1.6 | 31,992 | ||||||||

Chile — 0.1% | ||||||||||

Banco Santander Chile ADR | 0.1 | 23,200 | 1,335 | |||||||

Other Securities | 0.0 | 291 | ||||||||

| 1,626 | ||||||||||

China — 0.8% | ||||||||||

Other Securities | 0.8 | 15,786 | ||||||||

Cyprus — 0.0% | ||||||||||

Other Securities | 0.0 | 229 | ||||||||

Denmark — 0.8% | ||||||||||

Other Securities | 0.8 | 16,423 | ||||||||

| Description | Percentage of Net Assets (%) | Shares | Market Value ($ Thousands) | |||||||

Finland — 0.7% | ||||||||||

Other Securities | 0.7 | % | $ | 15,273 | ||||||

France — 6.8% | ||||||||||

BNP Paribas (A) | 0.7 | 180,227 | 14,384 | |||||||

Sanofi-Aventis | 1.2 | 336,731 | 24,684 | |||||||

Societe Generale | 0.6 | 156,768 | 12,603 | |||||||

Total (A) | 0.7 | 224,102 | 13,301 | |||||||

Other Securities | 3.6 | 75,381 | ||||||||

| 140,353 | ||||||||||

Germany — 6.6% | ||||||||||

Allianz | 0.6 | 95,443 | 11,910 | |||||||

Bayer | 0.5 | 158,633 | 10,979 | |||||||

Deutsche Bank | 0.5 | 123,995 | 9,505 | |||||||

E.ON | 0.4 | 215,684 | 9,137 | |||||||

Siemens | 0.8 | 179,896 | 16,640 | |||||||

Other Securities | 3.8 | 78,597 | ||||||||

| 136,768 | ||||||||||

Greece — 0.7% | ||||||||||

Other Securities | 0.7 | 14,748 | ||||||||

Hong Kong — 3.2% |

| |||||||||

Hang Seng Bank | 0.1 | 92,400 | 1,332 | |||||||

Sun Hung Kai Properties | 0.6 | 857,000 | 12,628 | |||||||

Other Securities | 2.5 | 51,897 | ||||||||

| 65,857 | ||||||||||

India — 0.7% | ||||||||||

Other Securities | 0.7 | 13,713 | ||||||||

Indonesia — 0.1% |

| |||||||||

Other Securities | 0.1 | 2,405 | ||||||||

Ireland — 0.3% | ||||||||||

Other Securities | 0.3 | 6,191 | ||||||||

Israel — 0.3% | ||||||||||

Other Securities | 0.3 | 7,107 | ||||||||

Italy — 2.6% | ||||||||||

Enel | 0.5 | 1,586,211 | 10,057 | |||||||

Other Securities | 2.1 | 44,129 | ||||||||

| 54,186 | ||||||||||

Japan — 18.6% | ||||||||||

Astellas Pharma | 0.4 | 197,500 | 8,140 | |||||||

Canon | 0.7 | 350,800 | 14,222 | |||||||

East Japan Railway | 0.4 | 120,500 | 8,694 | |||||||

Honda Motor | 0.8 | 541,900 | 16,735 | |||||||

Mitsubishi | 0.6 | 622,300 | 12,622 | |||||||

| 6 | SEI Institutional International Trust / Annual Report / September 30, 2009 |

Table of Contents

| Description | Percentage of Net Assets (%) | Shares | Market Value ($ Thousands) | |||||||

Nippon Telegraph & Telephone | 0.5 | % | 221,800 | $ | 10,305 | |||||

Nissan Motor | 0.4 | 1,213,900 | 8,230 | |||||||

Sumitomo Mitsui Financial Group (A) | 0.4 | 236,800 | 8,278 | |||||||

Toyota Motor | 0.4 | 224,100 | 8,935 | |||||||

Other Securities | 14.0 | 287,867 | ||||||||

| 384,028 | ||||||||||

Jersey — 0.0% | ||||||||||

Other Securities | 0.0 | 799 | ||||||||

Malta — 0.0% | ||||||||||

Other Securities | 0.0 | — | ||||||||

Mauritius — 0.1% | ||||||||||

Other Securities | 0.1 | 975 | ||||||||

Mexico — 0.0% | ||||||||||

Other Securities | 0.0 | 271 | ||||||||

Netherlands — 4.5% |

| |||||||||

Royal Dutch Shell, Cl A | 1.0 | 756,178 | 21,597 | |||||||

Royal Dutch Shell, Cl B | 0.5 | 386,633 | 10,735 | |||||||

Unilever | 0.5 | 381,815 | 10,992 | |||||||

Other Securities | 2.5 | 48,707 | ||||||||

| 92,031 | ||||||||||

New Zealand — 0.1% |

| |||||||||

Other Securities | 0.1 | 2,669 | ||||||||

Norway — 0.7% | ||||||||||

Other Securities | 0.7 | 14,681 | ||||||||

Papua New Guinea — 0.0% |

| |||||||||

Other Securities | 0.0 | 552 | ||||||||

Portugal — 0.5% |

| |||||||||

Other Securities | 0.5 | 9,471 | ||||||||

Russia — 0.4% |

| |||||||||

Other Securities | 0.4 | 8,719 | ||||||||

Singapore — 1.4% |

| |||||||||

Wilmar International (A) | 0.4 | 1,844,000 | 8,271 | |||||||

Other Securities | 1.0 | 20,183 | ||||||||

| 28,454 | ||||||||||

South Africa — 0.2% |

| |||||||||

Other Securities | 0.2 | 3,054 | ||||||||

South Korea — 0.2% |

| |||||||||

Other Securities | 0.2 | 4,150 | ||||||||

Spain — 3.8% |

| |||||||||

Banco Bilbao Vizcaya Argentaria (A) | 0.5 | 566,652 | 10,047 | |||||||

| Description | Percentage of Net Assets (%) | Shares/ Face Amount (Thousands) (1) | Market Value ($ Thousands) | |||||||

Banco Santander Central Hispano | 0.9 | % | 1,188,325 | $ | 19,107 | |||||

Telefonica (A) | 1.3 | 955,149 | 26,324 | |||||||

Other Securities | 1.1 | 22,413 | ||||||||

| 77,891 | ||||||||||

Sweden — 1.6% |

| |||||||||

Other Securities | 1.6 | 33,172 | ||||||||

Switzerland — 7.6% |

| |||||||||

Credit Suisse Group | 0.9 | 318,180 | 17,632 | |||||||

Nestle | 1.3 | 640,927 | 27,276 | |||||||

Novartis | 1.1 | 438,826 | 21,928 | |||||||

Roche Holding | 0.8 | 98,060 | 15,829 | |||||||

UBS | 0.4 | 458,387 | 8,380 | |||||||

Xstrata | 0.5 | 620,018 | 9,148 | |||||||

Zurich Financial Services | 0.7 | 56,710 | 13,472 | |||||||

Other Securities | 1.9 | 42,814 | ||||||||

| 156,479 | ||||||||||

Taiwan — 0.8% |

| |||||||||

Other Securities | 0.8 | 15,621 | ||||||||

Turkey — 0.1% |

| |||||||||

Other Securities | 0.1 | 2,477 | ||||||||

United Kingdom — 15.6% |

| |||||||||

AstraZeneca | 0.9 | 394,014 | 17,670 | |||||||

Barclays | 0.6 | 1,988,437 | 11,767 | |||||||

BG Group | 0.4 | 484,545 | 8,424 | |||||||

BHP Billiton | 0.6 | 451,274 | 12,327 | |||||||

BP | 1.4 | 3,285,633 | 29,060 | |||||||

British American Tobacco | 0.7 | 435,903 | 13,685 | |||||||

GlaxoSmithKline | 0.6 | 668,037 | 13,136 | |||||||

HSBC Holdings | 1.1 | 2,006,864 | 22,981 | |||||||

Rio Tinto | 0.5 | 218,036 | 9,306 | |||||||

Standard Chartered | 0.8 | 672,608 | 16,588 | |||||||

Vodafone Group | 0.9 | 7,916,006 | 17,750 | |||||||

Other Securities | 7.1 | 148,392 | ||||||||

| 321,086 | ||||||||||

United States — 0.5% |

| |||||||||

Other Securities | 0.5 | 10,043 | ||||||||

Total Common Stock | 1,830,277 | |||||||||

MORTGAGE-BACKED SECURITIES — 3.7% | ||||||||||

Agency Mortgage-Backed Obligations — 1.8% | ||||||||||

FNMA | ||||||||||

6.000%, 07/01/37 | 0.0 | 869 | 919 | |||||||

FNMA 15 Year TBA | ||||||||||

6.000%, 10/20/21 | 0.2 | 4,000 | 4,260 | |||||||

| SEI Institutional International Trust / Annual Report / September 30, 2009 | 7 |

Table of Contents

SUMMARY SCHEDULE OF INVESTMENTS

International Equity Fund (Continued)

September 30, 2009

| Description | Percentage of Net Assets (%) | Face Amount (Thousands) (1)/ Shares | Market Value ($ Thousands) | |||||||

FNMA 30 Year TBA | ||||||||||

6.500%, 10/01/37 | 0.6 | % | 10,650 | $ | 11,382 | |||||

6.000%, 10/01/37 | 0.6 | 12,100 | 12,765 | |||||||

FNMA ARM | ||||||||||

5.128%, 10/01/35 (D) | 0.1 | 1,319 | 1,376 | |||||||

4.504%, 05/01/35 (D) | 0.1 | 1,027 | 1,067 | |||||||

FNMA CMO STRIPS, Ser 369, Cl 1, IO | ||||||||||

5.000%, 03/01/36 | 0.0 | 1,283 | 168 | |||||||

Other Securities | 0.2 | 4,734 | ||||||||

| 36,671 | ||||||||||

Non-Agency Mortgage-Backed Obligations — 1.9% | ||||||||||

Other Securities | 1.9 | 39,393 | ||||||||

Total Mortgage-Backed Securities |

| 76,064 | ||||||||

ASSET-BACKED SECURITIES — 1.4% | ||||||||||

Automotive — 0.3% | ||||||||||

Other Securities | 0.3 | 5,090 | ||||||||

Credit Card — 0.7% | ||||||||||

Other Securities | 0.7 | 15,228 | ||||||||

Mortgage-Related — 0.4% |

| |||||||||

Other Securities | 0.4 | 8,418 | ||||||||

Total Asset-Backed Securities | 28,736 | |||||||||

PREFERRED STOCK — 0.5% | ||||||||||

Brazil — 0.4% | ||||||||||

Other Securities | 0.4 | 7,787 | ||||||||

France — 0.0% | ||||||||||

Other Securities | 0.0 | 497 | ||||||||

Germany — 0.1% |

| |||||||||

Other Securities | 0.1 | 2,603 | ||||||||

Total Preferred Stock | 10,887 | |||||||||

CORPORATE OBLIGATION — 0.1% | ||||||||||

United States — 0.1% | ||||||||||

Other Securities | 0.1 | 914 | ||||||||

Total Corporate Obligation | 914 | |||||||||

| Description | Percentage of Net Assets (%) | Shares/ Face Amount (Thousands) (1) | Market Value ($ Thousands) | |||||||

WARRANTS — 0.0% | ||||||||||

Italy — 0.0% | ||||||||||

Other Securities | 0.0 | % | $ | 7 | ||||||

Singapore — 0.0% |

| |||||||||

Other Securities | 0.0 | 30 | ||||||||

Total Warrants | 37 | |||||||||

RIGHTS — 0.0% |

| |||||||||

Australia — 0.0% |

| |||||||||

Other Securities | 0.0 | 33 | ||||||||

Belgium — 0.0% |

| |||||||||

Other Securities | 0.0 | — | ||||||||

France — 0.0% |

| |||||||||

Other Securities | 0.0 | 396 | ||||||||

Hong Kong — 0.0% |

| |||||||||

Other Securities | 0.0 | 77 | ||||||||

Sweden — 0.0% |

| |||||||||

Other Securities | 0.0 | 97 | ||||||||

Total Rights | 603 | |||||||||

CASH EQUIVALENT — 3.9% | ||||||||||

United States — 3.9% |

| |||||||||

SEI Daily Income Trust, Prime Obligation Fund, Cl A, 0.110%†* | 3.9 | 80,443,128 | 80,443 | |||||||

Total Cash Equivalent | ||||||||||

U.S. TREASURY OBLIGATIONS — 0.7% | ||||||||||

U.S. Treasury Bills | ||||||||||

0.233%, 12/03/09 (B) (C) | 0.6 | 12,364 | 12,362 | |||||||

Other Obligations | 0.1 | 2,350 | ||||||||

Total U.S. Treasury Obligations | 14,712 | |||||||||

AFFILIATED PARTNERSHIP — 7.9% | ||||||||||

United States — 7.9% |

| |||||||||

SEI Liquidity Fund, L.P., 0.400%†* (D) | 7.9 | 165,342,282 | 163,007 | |||||||

Total Affiliated Partnership | 163,007 | |||||||||

| 8 | SEI Institutional International Trust / Annual Report / September 30, 2009 |

Table of Contents

| Description | Percentage of Net Assets (%) | Face Amount (Thousands) (1) | Market Value ($ Thousands) | |||||||||

TIME DEPOSITS — 2.0% | ||||||||||||

United States — 2.0% |

| |||||||||||

Brown Brothers Harriman | ||||||||||||

5.950%, 10/01/09 | 0.0 | % | ZAR | 3 | $ | — | ||||||

2.174%, 10/01/09 | 0.0 | AUD | 531 | 469 | ||||||||

1.500%, 10/01/09 | 0.0 | NZD | 100 | 72 | ||||||||

0.382%, 10/01/09 | 0.0 | NOK | 185 | 32 | ||||||||

0.125%, 10/01/09 | 0.0 | EUR | 85 | 124 | ||||||||

0.100%, 10/01/09 | 0.0 | DKK | 3,539 | 695 | ||||||||

0.088%, 10/01/09 | 0.0 | GBP | 321 | 513 | ||||||||

0.060%, 10/01/09 | 0.0 | CAD | 3 | 2 | ||||||||

0.030%, 10/01/09 | 1.9 | 38,281 | 38,281 | |||||||||

0.020%, 10/01/09 | 0.0 | CHF | 454 | 438 | ||||||||

0.010%, 10/01/09 | 0.0 | HKD | 693 | 89 | ||||||||

0.010%, 10/01/09 | 0.1 | JPY | 71,757 | 801 | ||||||||

0.010%, 10/01/09 | 0.0 | SEK | 1,438 | 206 | ||||||||

0.005%, 10/01/09 | 0.0 | SGD | 53 | 38 | ||||||||

Total Time Deposits | 41,760 | |||||||||||

Total Investments — 109.0% | $ | 2,247,440 | ||||||||||

A summary of the outstanding forward foreign currency contracts held by the Fund at September 30, 2009, is as follows:

| Settlement Date | Currency to Deliver (Thousands) | Currency to Receive (Thousands) | Unrealized Appreciation (Depreciation) ($ Thousands) | |||||||||

10/1/09-10/21/09 | JPY | 3,376,515 | USD | 36,750 | $ | (971 | ) | |||||

10/1/09-10/21/09 | USD | 37,114 | JPY | 3,376,515 | 607 | |||||||

10/2/09-10/21/09 | AUD | 53,713 | USD | 46,813 | (506 | ) | ||||||

10/2/09-10/21/09 | CAD | 25,266 | USD | 23,760 | 214 | |||||||

10/5/09-10/21/09 | HKD | 313,704 | USD | 40,483 | — | |||||||

10/5/09-10/21/09 | USD | 76,835 | GBP | 46,440 | (2,575 | ) | ||||||

10/6/09-10/21/09 | USD | 46,832 | AUD | 53,682 | 460 | |||||||

10/21/09 | AUD | 2,537 | CHF | 2,100 | (210 | ) | ||||||

10/21/09 | CHF | 2,100 | AUD | 2,568 | 238 | |||||||

10/21/09 | CHF | 4,400 | GBP | 2,560 | (148 | ) | ||||||

10/21/09 | CHF | 9,218 | USD | 8,708 | (179 | ) | ||||||

10/21/09 | GBP | 2,569 | CHF | 4,400 | 134 | |||||||

10/21/09 | MXP | 3,461 | USD | 261 | 6 | |||||||

10/21/09 | NOK | 9,412 | USD | 1,610 | (12 | ) | ||||||

10/21/09 | SEK | 92,083 | USD | 13,486 | 313 | |||||||

10/21/09 | SGD | 2,711 | USD | 1,918 | (6 | ) | ||||||

10/21/09 | USD | 23,614 | CAD | 25,266 | (68 | ) | ||||||

10/21/09 | USD | 8,787 | CHF | 9,218 | 99 | |||||||

10/21/09 | USD | 76,695 | EUR | 52,051 | (619 | ) | ||||||

10/21/09 | USD | 40,484 | HKD | 313,704 | (1 | ) | ||||||

10/21/09 | USD | 260 | MXP | 3,461 | (4 | ) | ||||||

10/21/09 | USD | 391 | NZD | 542 | 1 | |||||||

10/21/09 | USD | 13,435 | SEK | 92,083 | (261 | ) | ||||||

10/21/09 | USD | 1,920 | SGD | 2,711 | 4 | |||||||

10/21/09 | USD | 1,592 | ZAR | 11,915 | (24 | ) | ||||||

10/21/09 | ZAR | 11,915 | USD | 1,616 | 48 | |||||||

10/21/09-11/20/09 | EUR | 52,083 | USD | 77,049 | 928 | |||||||

10/21/09-11/20/09 | GBP | 2,448 | JPY | 378,000 | 310 | |||||||

10/21/09-11/20/09 | GBP | 1,204 | SGD | 2,800 | 62 | |||||||

10/21/09-11/20/09 | GBP | 46,576 | USD | 76,063 | 1,585 | |||||||

10/21/09-11/20/09 | JPY | 378,000 | GBP | 2,570 | (115 | ) | ||||||

10/21/09-11/20/09 | JPY | 189,000 | NZD | 3,263 | 243 | |||||||

10/21/09-11/20/09 | NZD | 3,147 | JPY | 189,000 | (159 | ) | ||||||

10/21/09-11/20/09 | NZD | 659 | USD | 460 | (16 | ) | ||||||

| Settlement Date | Currency to Deliver (Thousands) | Currency to Receive (Thousands) | Unrealized Appreciation (Depreciation) ($ Thousands) | |||||||||

10/21/09-11/20/09 | SGD | 2,800 | GBP | 1,227 | $ | (26 | ) | |||||

10/21/09-11/20/09 | USD | 1,629 | NOK | 9,526 | 12 | |||||||

11/20/09 | CHF | 2,100 | EUR | 1,391 | 7 | |||||||

11/20/09 | CHF | 1,000 | NOK | 5,854 | 43 | |||||||

11/20/09 | EUR | 1,393 | CHF | 2,100 | (10 | ) | ||||||

11/20/09 | EUR | 1,397 | JPY | 188,000 | 59 | |||||||

11/20/09 | JPY | 188,000 | EUR | 1,431 | (10 | ) | ||||||

11/20/09 | NOK | 5,968 | CHF | 1,000 | (63 | ) | ||||||

| $ | (610 | ) | ||||||||||

A summary of the open futures contracts held by the Fund at September 30, 2009, is as follows:

| Type of Contract | Number of Contracts Long (Short) | Expiration Date | Unrealized Appreciation (Depreciation) ($ Thousands) | ||||||

DJ Euro Stoxx 50 Index | 932 | Dec-2009 | $ | 494 | |||||

FTSE 100 Index | 278 | Dec-2009 | 520 | ||||||

Hang Seng Index | 16 | Oct-2009 | 7 | ||||||

MSCI EAFE Index E-MINI | 88 | Dec-2009 | 133 | ||||||

Nikkei 225 Index | 20 | Dec-2009 | (24 | ) | |||||

SPI 200 Index | 66 | Dec-2009 | 220 | ||||||

Topix Index | 244 | Dec-2009 | (1,094 | ) | |||||

U.S. 10-Year Treasury Note | (14 | ) | Dec-2009 | (20 | ) | ||||

U.S. 5-Year Treasury Note | (14 | ) | Dec-2009 | (13 | ) | ||||

| $ | 223 | ||||||||

For the year ended September 30, 2009, The total amount of all open futures contracts, as presented in the table above, are representative of the volume of activity for this derivative type during the period.

| SEI Institutional International Trust / Annual Report / September 30, 2009 | 9 |

Table of Contents

SUMMARY SCHEDULE OF INVESTMENTS

International Equity Fund (Concluded)

September 30, 2009

A summary of outstanding swap agreements held by the Fund at September 30, 2009, is as follows:

| Total Return Swap | ||||||||||||||

| Counterparty | Reference Entity/Obligation | Fund Pays | Fund Receives | Termination Date | Notional Amount (Thousands) | Net Unrealized Depreciation ($ Thousands) | ||||||||

| Morgan Stanley | MSCI Daily TR Net EAFE USD Market Index | 3-Month LIBOR | Price Return | 01/13/10 | 95,310 | $ | (1,341 | ) | ||||||

| Credit Default Swaps | ||||||||||||||

| Counterparty | Reference Entity/Obligation | Buy/Sell Protection | (Pays)/ Receives Rate | Termination Date | Notional Amount (Thousands) | Net Unrealized Appreciation ($ Thousands) | ||||||||

| Bank of America | Radian Group Inc., 7.750%, 06/01/11 | BUY | (0.39 | ) | 12/20/13 | 2,500 | $ | 920 | ||||||

| JPMorgan Chase Bank | Radian Group Inc., 7.750%, 06/01/11 | BUY | (0.39 | ) | 12/20/13 | 2,500 | 921 | |||||||

| $ | 1,841 | |||||||||||||

The following is a summary of the inputs used as of September 30, 2009 in valuing the Fund’s investments carried at value ($ Thousands):

| Investments in Securities | Level 1 | Level 2 | Level 3 | Total | ||||||||

Common Stock | $ | 1,830,277 | $ | — | $ | — | $ | 1,830,277 | ||||

Mortgage-Backed Securities | — | 76,064 | — | 76,064 | ||||||||

Asset-Backed Securities | — | 28,736 | — | 28,736 | ||||||||

Preferred Stock | 10,887 | — | — | 10,887 | ||||||||

Corporate Obligation | — | 914 | — | 914 | ||||||||

Warrants | 37 | — | — | 37 | ||||||||

Rights | — | 603 | — | 603 | ||||||||

Cash Equivalent | 80,443 | — | — | 80,443 | ||||||||

U.S. Treasury Obligations | — | 14,712 | — | 14,712 | ||||||||

Affiliated Partnership | — | 163,007 | — | 163,007 | ||||||||

Time Deposits | — | 41,760 | — | 41,760 | ||||||||

Total Investments in Securities | $ | 1,921,644 | $ | 325,796 | $ | — | $ | 2,247,440 | ||||

| Other Financial Instruments* | Level 1 | Level 2 | Level 3 | Total | ||||||||||

Futures | $ | 223 | $ | — | $ | — | $ | 223 | ||||||

Forwards | — | (610 | ) | — | (610 | ) | ||||||||

Credit Default Swaps | — | 1,841 | — | 1,841 | ||||||||||

Total Return Swaps | — | (1,341 | ) | — | (1,341 | ) | ||||||||

Total Other Financial Instruments | $ | 223 | $ | (110 | ) | $ | — | $ | 113 | |||||

| * | Other Financial Instruments are valued at unrealized appreciation/depreciation. |

For more information on valuation inputs, see Note 2 — Significant Accounting Policies in Notes to Financial Statements.

The accompanying notes are an integral part of the financial statements.

Percentages are based on a Net Assets of $2,061,808 ($ Thousands).

| * | Rate shown is the 7-day effective yield as of September 30, 2009. |

| (1) | In U.S. dollars unless otherwise indicated. |

| † | Affiliated security. |

| (A) | This security or a partial position of this security is on loan at September 30, 2009. The total market value of securities on loan at September 30, 2009 was $155,229 ($ Thousands) (See Note 9). |

| (B) | Zero coupon security. The rate reported on the Summary Schedule of Investments is the effective yield at time of purchase. |

| (C) | Security, or portion thereof, has been pledged as collateral on open futures contracts. |

| (D) | This security was purchased with cash collateral held from securities on loan (see Note 9). The total value of such securities as of September 30, 2009 was $163,007 ($ Thousands). |

ARM — Adjustable Rate Mortgage

AUD — Australian Dollar

CAD — Canadian Dollar

CHF — Swiss Franc

Cl — Class

CMO — Collateralized Mortgage Obligation

DKK — Danish Krone

EAFE — Europe, Australasia and Far East

EUR — Euro

FNMA — Federal National Mortgage Association

GBP — British Pound Sterling

HKD — Hong Kong Dollar

IO — Interest Only

JPY — Japanese Yen

LIBOR — London Interbank Offered Rate

L.P. — Limited Partnership

MSCI — Morgan Stanley Capital International

MXP — Mexican Peso

NOK — Norwegian Krone

NZD — New Zealand Dollar

SEK — Swedish Krona

SER — Series

SGD — Singapore Dollar

STRIPS — Separate Trading of Registered Interest and Principal of Securities

TBA — To Be Announced

USD — U.S. Dollar

ZAR — South African Rand

Amounts designated as “—” are $O or have been rounded to $O.

The Summary Schedule of Investments does not reflect the complete portfolio holdings. It includes the Fund’s 50 largest holdings and each investment in any issuer that exceeds 1% of the Fund’s net assets. “Other Securities” represent all issues not required to be disclosed under the rules adopted by the U.S. Securities and Exchange Commission (“SEC”). Footnotes above may apply to securities that are included in “other securities.” For further detail, the complete schedule of portfolio holdings is available (i) without charge, upon request, by calling (800) 342-5734; and (ii) on the SEC’s website at http://www.sec.gov.

| 10 | SEI Institutional International Trust / Annual Report / September 30, 2009 |

Table of Contents

SUMMARY SCHEDULE OF INVESTMENTS

Emerging Markets Equity Fund

September 30, 2009

| Description | Percentage of Net Assets (%) | Shares | Market Value ($ Thousands) | |||||

COMMON STOCK — 86.7% | ||||||||

Argentina — 0.4% | ||||||||

Other Securities | 0.4 | % | $ | 3,323 | ||||

Brazil — 7.8% | ||||||||

Banco do Brasil | 0.3 | 161,654 | 2,848 | |||||

Centrais Eletricas Brasileiras | 0.1 | 54,180 | 838 | |||||

Cia de Saneamento Basico do Estado de Sao Paulo | 0.2 | 101,469 | 1,920 | |||||

Cia de Saneamento Basico do Estado de Sao Paulo ADR | 0.0 | 610 | 23 | |||||

Itau Unibanco Holding ADR | 0.6 | 287,329 | 5,790 | |||||

Petroleo Brasileiro | 0.9 | 347,229 | 7,936 | |||||

Petroleo Brasileiro ADR | 0.3 | 49,934 | 2,292 | |||||

Redecard | 0.4 | 239,703 | 3,685 | |||||

Usinas Siderurgicas de Minas Gerais | 0.4 | 142,800 | 3,647 | |||||

Vale | 0.3 | 136,800 | 3,157 | |||||

Vale ADR, Cl B | 0.6 | 252,970 | 5,851 | |||||

Other Securities | 3.7 | 33,374 | ||||||

| 71,361 | ||||||||

Chile — 1.2% | ||||||||

Enersis ADR | 0.4 | 205,191 | 3,786 | |||||

Other Securities | 0.8 | 7,429 | ||||||

| 11,215 | ||||||||

China — 9.6% | ||||||||

Bank of China | 0.8 | 14,479,000 | 7,622 | |||||

China Citic Bank | 0.1 | 1,009,000 | 665 | |||||

China Construction Bank | 1.3 | 15,222,250 | 12,158 | |||||

China Shenhua Energy | 0.0 | 36,000 | 157 | |||||

Industrial & Commercial Bank of China (A) | 1.2 | 14,633,000 | 11,027 | |||||

| Description | Percentage of Net Assets (%) | Shares | Market Value ($ Thousands) | |||||

PetroChina | 0.4 | % | 3,469,023 | $ | 3,921 | |||

PetroChina ADR | 0.1 | 11,290 | 1,284 | |||||

Other Securities | 5.7 | 51,382 | ||||||

| 88,216 | ||||||||

Czech Republic — 0.5% | ||||||||

Other Securities | 0.5 | 4,550 | ||||||

Egypt — 0.4% | ||||||||

Other Securities | 0.4 | 4,074 | ||||||

Hong Kong — 6.2% | ||||||||

China Foods | 0.0 | 148,000 | 102 | |||||

China Mobile | 1.5 | 1,453,715 | 14,181 | |||||

China Mobile ADR | 0.3 | 48,070 | 2,361 | |||||

China Overseas Land & Investment | 0.2 | 806,800 | 1,745 | |||||

China Resources Power Holdings | 0.2 | 734,800 | 1,708 | |||||

CNOOC | 0.7 | 4,828,448 | 6,492 | |||||

CNOOC ADR | 0.1 | 3,510 | 475 | |||||

CNPC Hong Kong | 0.1 | 1,172,836 | 929 | |||||

Industrial and Commercial Bank of China Asia | 0.1 | 293,000 | 663 | |||||

Other Securities | 3.0 | 28,139 | ||||||

| 56,795 | ||||||||

Hungary — 0.2% | ||||||||

Other Securities | 0.2 | 1,535 | ||||||

India — 6.9% | ||||||||

Tata Consultancy Services | 0.5 | 336,788 | 4,348 | |||||

Other Securities | 6.4 | 59,121 | ||||||

| 63,469 | ||||||||

Indonesia — 1.7% | ||||||||

Bank Mandiri | 0.4 | 7,908,592 | 3,846 | |||||

Telekomunikasi Indonesia | 0.4 | 4,293,100 | 3,842 | |||||

Other Securities | 0.9 | 8,232 | ||||||

| 15,920 | ||||||||

Israel — 1.7% | ||||||||

Teva Pharmaceutical Industries | 0.4 | 73,554 | 3,683 | |||||

Teva Pharmaceutical Industries ADR | 0.5 | 84,356 | 4,265 | |||||

Other Securities | 0.8 | 7,631 | ||||||

| 15,579 | ||||||||

Kazakhstan — 0.2% |

| |||||||

Other Securities | 0.2 | % | 1,873 | |||||

| SEI Institutional International Trust / Annual Report / September 30, 2009 | 11 |

Table of Contents

SUMMARY SCHEDULE OF INVESTMENTS

Emerging Markets Equity Fund (Continued)

September 30, 2009

| Description | Percentage of Net Assets (%) | Shares | Market Value ($ Thousands) | |||||

Malaysia — 1.9% | ||||||||

Malayan Banking | 0.4 | % | 1,851,067 | $ | 3,557 | |||

Other Securities | 1.5 | 14,019 | ||||||

| 17,576 | ||||||||

Mexico — 4.1% | ||||||||

America Movil, Ser L | 0.6 | 2,408,459 | 5,270 | |||||

America Movil ADR, Ser L | 0.7 | 147,706 | 6,474 | |||||

Other Securities | 2.8 | 26,173 | ||||||

| 37,917 | ||||||||

Netherlands — 0.1% |

| |||||||

Other Securities | 0.1 | 1,042 | ||||||

Pakistan — 0.1% | ||||||||

Other Securities | 0.1 | 1,189 | ||||||

Panama — 0.1% | ||||||||

Other Securities | 0.1 | 1,174 | ||||||

Peru — 0.2% | ||||||||

Other Securities | 0.2 | 1,973 | ||||||

Philippines — 0.4% | ||||||||

Other Securities | 0.4 | 3,360 | ||||||

Poland — 0.7% | ||||||||

Other Securities | 0.7 | 6,382 | ||||||

Russia — 6.0% | ||||||||

Lukoil ADR | 1.3 | 217,888 | 11,951 | |||||

Lukoil OAO ADR | 0.2 | 37,300 | 2,022 | |||||

OAO Gazprom ADR | 1.8 | 722,532 | 16,799 | |||||

Rosneft Oil GDR | 0.5 | 658,529 | 4,952 | |||||

Other Securities | 2.2 | 18,950 | ||||||

| 54,674 | ||||||||

South Africa — 6.8% | ||||||||

ABSA Group | 0.3 | 150,030 | 2,376 | |||||

FirstRand | 0.4 | 1,869,984 | 4,074 | |||||

Gold Fields | 0.4 | 271,744 | 3,640 | |||||

MTN Group | 0.7 | 390,818 | 6,300 | |||||

Sasol | 0.5 | 116,007 | 4,323 | |||||

Other Securities | 4.5 | 41,314 | ||||||

| 62,027 | ||||||||

South Korea — 12.9% | ||||||||

Hyundai Motor | 0.5 | 46,878 | 4,436 | |||||

Korea Electric Power | 0.4 | 122,970 | 3,736 | |||||

LG | 0.3 | 41,054 | 2,753 | |||||

LG Electronics | 0.7 | 58,280 | 6,208 | |||||

LG Philips LCD | 0.5 | 170,970 | 4,919 | |||||

POSCO | 0.7 | 15,149 | 6,262 | |||||

| Description | Percentage of Net Assets (%) | Shares | Market Value ($ Thousands) | |||||

Samsung Electronics | 3.2 | % | 42,310 | $ | 29,266 | |||

Shinhan Financial Group | 0.9 | 203,930 | 8,135 | |||||

Other Securities | 5.7 | 52,374 | ||||||

| 118,089 | ||||||||

Sweden — 0.1% | ||||||||

Other Securities | 0.1 | 996 | ||||||

Taiwan — 10.9% | ||||||||

Chinatrust Financial Holding | 0.5 | 6,844,862 | 4,439 | |||||

Compal Electronics | 0.6 | 4,376,281 | 5,098 | |||||

HON HAI Precision Industry | 1.4 | 3,247,934 | 13,033 | |||||

MediaTek | 0.8 | 458,023 | 7,637 | |||||

Taiwan Fertilizer | 0.4 | 1,007,000 | 3,602 | |||||

Taiwan Semiconductor Manufacturing | 1.4 | 6,509,456 | 13,060 | |||||

Taiwan Semiconductor Manufacturing ADR | 0.2 | 164,386 | 1,802 | |||||

United Microelectronics | 0.6 | 11,392,312 | 5,581 | |||||

Other Securities | 5.0 | 45,599 | ||||||

| 99,851 | ||||||||

Thailand — 2.7% | ||||||||

Other Securities | 2.7 | 24,249 | ||||||

Turkey — 2.6% | ||||||||

Tupras Turkiye Petrol Rafine | 0.4 | 235,733 | 3,902 | |||||

Other Securities | 2.2 | 19,559 | ||||||

| 23,461 | ||||||||

United Arab Emirates — 0.0% | ||||||||

Other Securities | 0.0 | 16 | ||||||

United Kingdom — 0.3% | ||||||||

Other Securities | 0.3 | 2,932 | ||||||

Total Common Stock | 794,818 | |||||||

PREFERRED STOCK — 8.1% | ||||||||

Brazil — 8.1% | ||||||||

Centrais Eletricas Brasileiras | 0.2 | 112,246 | 1,566 | |||||

Investimentos Itau | 0.6 | 917,435 | 5,520 | |||||

Itau Unibanco Holding | 0.6 | 263,562 | 5,296 | |||||

Petroleo Brasileiro | 1.3 | 596,442 | 11,680 | |||||

Petroleo Brasileiro Sponsored ADR, Cl A | 1.5 | 351,510 | 13,818 | |||||

Vale, Cl A | 0.7 | 322,331 | 6,625 | |||||

Vale ADR, Cl B | 0.4 | 183,376 | 3,761 | |||||

Other Securities | 2.8 | 26,113 | ||||||

Total Preferred Stock | 74,379 | |||||||

| 12 | SEI Institutional International Trust / Annual Report / September 30, 2009 |

Table of Contents

| Description | Percentage of Net Assets (%) | Shares/ Face Amount | Market Value ($ Thousands) | |||||

DEBENTURE BOND — 0.0% | ||||||||

Brazil — 0.0% | ||||||||

Vale, Ser 1997 | ||||||||

0.000%, 09/30/49* | 0.0 | % | 8 | $ | — | |||

Total Debenture Bond | — | |||||||

EQUITY-LINKED WARRANTS — 0.1% | ||||||||

Russia — 0.1% | ||||||||

Other Securities | 0.1 | 769 | ||||||

United Arab Emirates — 0.0% | ||||||||

Other Securities | 0.0 | 564 | ||||||

Total Equity-Linked Warrants | 1,333 | |||||||

EXCHANGE TRADED FUND — 0.7% | ||||||||

United States — 0.7% | ||||||||

iShares MSCI Emerging Markets Index Fund | 0.7 | 165,068 | 6,423 | |||||

Total Exchange Traded Fund | 6,423 | |||||||

CASH EQUIVALENT — 0.4% | ||||||||

United States — 0.4% | ||||||||

SEI Daily Income Trust, Prime Obligation Fund, Cl A, 0.110%†** | 0.4 | 3,454,719 | 3,455 | |||||

Total Cash Equivalent | 3,455 | |||||||

AFFILIATED PARTNERSHIP — 3.9% | ||||||||

United States — 3.9% | ||||||||

SEI Liquidity Fund, L.P., | ||||||||

0.400%†** (B) | 3.9 | 36,294,960 | 35,307 | |||||

Total Affiliated Partnership | 35,307 | |||||||

TIME DEPOSITS — 1.1% | ||||||||

United States — 1.1% | ||||||||

Brown Brothers Harriman | ||||||||

5.950%, 10/01/09 | 0.0 | ZAR 3,094 | 408 | |||||

0.125%, 10/01/09 | 0.0 | EUR 76 | 111 | |||||

0.088%, 10/01/09 | 0.0 | GBP 6 | 10 | |||||

0.030%, 10/01/09 | 1.0 | 9,451 | 9,451 | |||||

| Description | Percentage of | Face Amount (Thousands) (1) | Market Value ($ Thousands) | |||||

0.010%, 10/01/09 | 0.1 | % | HKD 4,162 | $ | 537 | |||

0.005%, 10/01/09 | 0.0 | SGD 2 | 2 | |||||

Total Time Deposits | 10,519 | |||||||

Total Investments — 101.0% | $ | 926,234 | ||||||

Percentages are based on a Net Assets of $916,780 ($ Thousands).

| * | Non-Income producing security. |

| ** | Rate shown is the 7-day effective yield as of September 30, 2009. |

| (1) | In U.S. dollars unless otherwise indicated. |

| † | Affiliated security. |

| (A) | This security or a partial position of this security is on loan at September 30, 2009. The total market value of securities on loan at September 30, 2009 was $34,648 ($ Thousands) (See Note 9). |

| (B) | This security was purchased with cash collateral held from securities on loan (see Note 9). The total value of such securities as of September 30, 2009 was $35,307 ($ Thousands). |

ADR — American Depositary Receipt

Cl — Class

EUR — Euro

GBP — British Pound Sterling

GDR — Global Depositary Receipt

HKD — Hong Kong Dollar

L.P. — Limited Partnership

MSCI — Morgan Stanley Capital International

Ser — Series

SGD — Singapore Dollar

USD — U.S. Dollar

ZAR — South African Rand

Amounts designated as “—” are $O or have been rounded to $O.

The Summary Schedule of Investments does not reflect the complete portfolio holdings. It includes the Fund’s 50 largest holdings and each investment in any issuer that exceeds 1% of the Fund’s net assets. “Other Securities” represent all issues not required to be disclosed under the rules adopted by the U.S. Securities and Exchange Commission (“SEC”). Footnotes above may apply to securities that are included in “Other Securities.” For further detail, the complete schedule of portfolio holdings is available (i) without charge, upon request, by calling (800) 342-5734; and (ii) on the SEC’s website at http://www.sec.gov.

The following is a summary of the inputs used as of September 30, 2009 in valuing the Fund’s investments carried at value ($ Thousands):

| Investments in Securities | Level 1 | Level 2 | Level 3 | Total | ||||||||

Common Stock | $ | 794,811 | $ | — | $ | 7 | $ | 794,818 | ||||

Preferred Stock | 74,379 | — | — | 74,379 | ||||||||

Debenture Bond | — | — | — | — | ||||||||

Equity-Linked Warrants | — | 1,333 | — | 1,333 | ||||||||

Exchange Traded Fund | 6,423 | — | — | 6,423 | ||||||||

Cash Equivalent | 3,455 | — | — | 3,455 | ||||||||

Affiliated Partnership | — | 35,307 | — | 35,307 | ||||||||

Time Deposits | — | 10,519 | — | 10,519 | ||||||||

Total Investments in Securities | $ | 879,068 | $ | 47,159 | $ | 7 | $ | 926,234 | ||||

| SEI Institutional International Trust / Annual Report / September 30, 2009 | 13 |

Table of Contents

SUMMARY SCHEDULE OF INVESTMENTS

Emerging Markets Equity Fund (Concluded)

September 30, 2009

The following is a reconciliation of the investments is which significant unobservable inputs (Level 3) were used in determining value ($ Thousands):

| Common Stock | |||

Beginning balance as of October 1, 2008 | $ | — | |

Accrued discounts/premiums | — | ||

Realized gain/(loss) | — | ||

Change in unrealized appreciation/(depreciation) | — | ||

Net purchases/sales | — | ||

Net transfer in and/or out of Level 3 | 7 | ||

Ending balance as of September 30, 2009 | $ | 7 | |

| Changes in unrealized gains/(losses) included in earnings related to securities still held at reporting date. | $ | — | |

For more information on valuation inputs, see Note 2 — Significant Accounting Policies in Notes to Financial Statements.

The accompanying notes are an integral part of the financial statements.

| 14 | SEI Institutional International Trust / Annual Report / September 30, 2009 |

Table of Contents

SUMMARY SCHEDULE OF INVESTMENTS

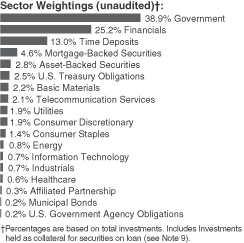

International Fixed Income Fund

September 30, 2009

| Description | Percentage of Net Assets (%) | Face Amount (Thousands) (1) | Market Value ($ Thousands) | |||||||

GLOBAL BONDS — 73.2% |

| |||||||||

Australia — 1.6% | ||||||||||

Other Securities | 1.6 | % | $ | 8,720 | ||||||

Austria — 0.1% | ||||||||||

Other Securities | 0.1 | 616 | ||||||||

Belgium — 1.6% | ||||||||||

Kingdom of Belgium, Ser 31 | ||||||||||

5.500%, 03/28/28 | 0.9 | 2,872 | 4,871 | |||||||

Kingdom of Belgium, Ser 48 | ||||||||||

4.000%, 03/28/22 | 0.6 | 2,100 | 3,089 | |||||||

Other Securities | 0.2 | 819 | ||||||||

| 8,779 | ||||||||||

Brazil — 0.5% | ||||||||||

Federal Republic of Brazil | ||||||||||

12.500%, 01/05/16 | 0.3 | 3,080 | 1,899 | |||||||

Other Securities | 0.2 | 863 | ||||||||

| 2,762 | ||||||||||

Canada — 3.8% | ||||||||||

Export Development Canada MTN | ||||||||||

2.375%, 03/19/12 | 0.2 | 800 | 817 | |||||||

Government of Canada | ||||||||||

5.000%, 06/01/14 | 0.2 | 1,000 | 1,035 | |||||||

5.000%, 06/01/37 | 0.9 | 4,200 | 4,679 | |||||||

4.250%, 06/01/18 | 0.3 | 1,525 | 1,538 | |||||||

3.750%, 06/01/19 | 0.1 | 630 | 608 | |||||||

3.750%, 06/01/12 | 0.9 | 4,960 | 4,863 | |||||||

Province of Ontario Canada | ||||||||||

4.200%, 03/08/18 | 0.3 | 1,950 | 1,885 | |||||||

Other Securities | 0.9 | 5,216 | ||||||||

| 20,641 | ||||||||||

| Description | Percentage of Net Assets (%) | Face Amount (Thousands) (1) | Market Value ($ Thousands) | |||||||

Chile — 0.1% | ||||||||||

Other Securities | 0.1 | % | $ | 662 | ||||||

Colombia — 0.1% | ||||||||||

Other Securities | 0.1 | 260 | ||||||||

Denmark — 1.7% | ||||||||||

Dong Energy MTN | ||||||||||

4.875%, 05/07/14 | 0.0 | 100 | 153 | |||||||

Kingdom of Denmark MTN | ||||||||||

4.000%, 11/15/12 | 0.8 | 20,391 | 4,198 | |||||||

4.000%, 11/15/17 | 0.2 | 4,450 | 912 | |||||||

3.125%, 03/17/14 | 0.1 | 500 | 748 | |||||||

Other Securities | 0.6 | 3,158 | ||||||||

| 9,169 | ||||||||||

France — 5.6% | ||||||||||

EDF MTN | ||||||||||

6.875%, 12/12/22 | 0.1 | 300 | 561 | |||||||

6.125%, 06/02/34 | 0.0 | 100 | 182 | |||||||

Government of France | ||||||||||

4.750%, 04/25/35 | 0.7 | 2,465 | 3,970 | |||||||

4.250%, 04/25/19 | 1.3 | 4,670 | 7,260 | |||||||

3.750%, 10/25/19 | 0.0 | 100 | 149 | |||||||

3.750%, 04/25/21 | 0.6 | 2,300 | 3,379 | |||||||

3.500%, 04/25/15 | 0.2 | 535 | 813 | |||||||

Other Securities | 2.7 | 13,551 | ||||||||

| 29,865 | ||||||||||

Germany — 9.1% | ||||||||||

Bundesrepublik Deutschland, | ||||||||||

5.000%, 01/04/12 | 0.1 | 500 | 788 | |||||||

Bundesrepublik Deutschland, | ||||||||||

4.750%, 07/04/34 | 0.7 | 2,460 | 3,991 | |||||||

4.250%, 01/04/14 | 0.4 | 1,425 | 2,249 | |||||||

Bundesrepublik Deutschland, | ||||||||||

3.750%, 01/04/17 | 1.0 | 3,600 | 5,554 | |||||||

Bundesrepublik Deutschland, | ||||||||||

4.250%, 07/04/39 | 1.1 | 3,740 | 5,764 | |||||||

4.000%, 01/04/18 | 0.4 | 1,260 | 1,963 | |||||||

Bundesrepublik Deutschland, | ||||||||||

4.750%, 07/04/40 | 1.9 | 6,255 | 10,421 | |||||||

Bundesrepublik Deutschland, | ||||||||||

3.500%, 07/04/19 | 1.2 | 4,331 | 6,476 | |||||||

| SEI Institutional International Trust / Annual Report / September 30, 2009 | 15 |

Table of Contents

SUMMARY SCHEDULE OF INVESTMENTS

International Fixed Income Fund (Continued)

September 30, 2009

| Description | Percentage of Net Assets (%) | Face Amount (Thousands) (1) | Market Value ($ Thousands) | |||||||

Bundesschatzanweisungen, | ||||||||||

1.250%, 09/16/11 | 0.9 | % | 3,300 | $ | 4,822 | |||||

KFW | ||||||||||

4.700%, 06/02/37 | 0.3 | CAD | 2,080 | 1,788 | ||||||

3.875%, 01/21/19 | 0.1 | 325 | 487 | |||||||

3.500%, 03/10/14 (A) | 0.3 | 1,675 | 1,743 | |||||||

Other Securities | 0.6 | 3,064 | ||||||||

| 49,110 | ||||||||||

Greece — 0.5% | ||||||||||

Hellenic Republic 30 Year Government Bond | ||||||||||

4.600%, 09/20/40 | 0.5 | 2,000 | 2,657 | |||||||

Hungary — 0.3% | ||||||||||

Other Securities | 0.3 | 1,775 | ||||||||

Ireland — 0.8% | ||||||||||

Other Securities | 0.8 | 4,045 | ||||||||

Italy — 3.8% | ||||||||||

Buoni Poliennali Del Tesoro | ||||||||||

5.750%, 02/01/33 | 1.3 | 4,170 | 6,914 | |||||||

Intesa Sanpaolo MTN | ||||||||||

6.375%, 04/06/10 | 0.6 | 2,150 | 3,203 | |||||||

Italy Buoni Poliennali Del Tesoro | ||||||||||

4.250%, 03/01/20 | 0.1 | 195 | 289 | |||||||

3.500%, 06/01/14 | 0.8 | 2,900 | 4,354 | |||||||

Unicredito Italiano MTN | ||||||||||

4.500%, 09/22/19 | 0.4 | 1,300 | 1,916 | |||||||

Other Securities | 0.7 | 4,020 | ||||||||

| 20,696 | ||||||||||

Japan — 13.5% | ||||||||||

Government of Japan 10 Year Bond, Ser 284 | ||||||||||

1.700%, 12/20/16 | 1.3 | 568,400 | 6,714 | |||||||

Government of Japan 10 Year Bond, Ser 288 | ||||||||||

1.700%, 09/20/17 | 3.8 | 1,729,950 | 20,386 | |||||||

Government of Japan 10 Year Bond, Ser 296 | ||||||||||

1.500%, 09/20/18 | 0.9 | 427,000 | 4,914 | |||||||

Government of Japan 10 Year Bond, Ser 301 | ||||||||||

1.500%, 06/20/19 | 0.5 | 235,300 | 2,685 | |||||||

Government of Japan 15 Year Bond, Ser 35 | ||||||||||

0.410%, 07/20/20 (B) | 0.3 | 170,500 | 1,811 | |||||||

| Description | Percentage of Net Assets (%) | Face Amount (Thousands) (1) | Market Value ($ Thousands) | |||||||

Government of Japan 20 Year Bond, Ser 109 | ||||||||||

1.900%, 03/20/29 | 0.5 | % | 256,000 | $ | 2,799 | |||||

Government of Japan 20 Year Bond, Ser 48 | ||||||||||

2.500%, 12/21/20 | 0.7 | 289,450 | 3,570 | |||||||

Government of Japan 20 Year Bond, Ser 99 | ||||||||||

2.100%, 12/20/27 | 2.3 | 1,075,900 | 12,241 | |||||||

Government of Japan CPI Linked Bond, Ser 13 | ||||||||||

1.300%, 09/10/17 | 0.2 | 111,712 | 1,170 | |||||||

Government of Japan CPI Linked Bond, Ser 15 | ||||||||||

1.400%, 03/10/18 | 0.2 | 92,647 | 974 | |||||||

Government of Japan CPI Linked Bond, Ser 5 | ||||||||||

0.800%, 09/10/15 | 1.0 | 499,982 | 5,208 | |||||||

Japan Finance for Municipal Enterprises | ||||||||||

2.000%, 05/09/16 | 1.2 | 540,000 | 6,363 | |||||||

Other Securities | 0.6 | 3,530 | ||||||||

| 72,365 | ||||||||||

Jersey — 0.1% | ||||||||||

Other Securities | 0.1 | 340 | ||||||||

Mexico — 0.1% | ||||||||||

Other Securities | 0.1 | 789 | ||||||||

Netherlands — 5.5% | ||||||||||

Government of Netherlands | ||||||||||

7.500%, 01/15/23 | 0.8 | 2,228 | 4,497 | |||||||

4.500%, 07/15/17 | 0.4 | 1,500 | 2,379 | |||||||

4.000%, 07/15/16 | 0.5 | 1,700 | 2,628 | |||||||

Rabobank Nederland MTN | ||||||||||

4.125%, 04/04/12 | 0.4 | 1,250 | 1,918 | |||||||

Other Securities | 3.3 | 18,087 | ||||||||

| 29,509 | ||||||||||

New Zealand — 0.1% |

| |||||||||

Other Securities | 0.1 | 492 | ||||||||

Norway — 0.6% | ||||||||||

Other Securities | 0.6 | 3,150 | ||||||||

Peru — 0.2% | ||||||||||

Other Securities | 0.2 | 1,103 | ||||||||

Poland — 0.3% | ||||||||||

Other Securities | 0.3 | 1,652 | ||||||||

Portugal — 0.1% | ||||||||||

Other Securities | 0.1 | 734 | ||||||||

| 16 | SEI Institutional International Trust / Annual Report / September 30, 2009 |

Table of Contents

| Description | Percentage of Net Assets (%) | Face Amount (Thousands) (1) | Market Value ($ Thousands) | ||||||||||

Russia — 0.6% | |||||||||||||

Other Securities | 0.6 | % | $ | 3,288 | |||||||||

Singapore — 0.0% | |||||||||||||

Other Securities | 0.0 | 137 | |||||||||||

South Africa — 0.1% | |||||||||||||

Other Securities | 0.1 | 449 | |||||||||||

Spain — 1.0% | |||||||||||||

Other Securities | 1.0 | 5,114 | |||||||||||

Supra-National — 3.6% | |||||||||||||

European Investment Bank MTN | |||||||||||||

6.000%, 08/14/13 | 0.1 | AUD | 700 | 624 | |||||||||

3.500%, 04/15/16 | 0.7 | 2,525 | 3,761 | ||||||||||

1.400%, 06/20/17 | 2.4 | JPY | 1,138,000 | 12,907 | |||||||||

Other Securities | 0.4 | 2,209 | |||||||||||

| 19,501 | |||||||||||||

Sweden — 1.2% | |||||||||||||

Kingdom of Sweden, | |||||||||||||

4.500%, 08/12/15 | 0.6 | 21,900 | 3,389 | ||||||||||

Other Securities | 0.6 | �� | 3,115 | ||||||||||

| 6,504 | |||||||||||||

Switzerland — 0.9% | |||||||||||||

Other Securities | 0.9 | 4,771 | |||||||||||

United Arab Emirates — 0.1% | |||||||||||||

Other Securities | 0.1 | 605 | |||||||||||

United Kingdom — 7.9% | |||||||||||||

Abbey National Treasury Services MTN | |||||||||||||

4.250%, 04/12/21 | 0.4 | 1,350 | 1,923 | ||||||||||

Anglian Water Services Financing MTN | |||||||||||||

4.625%, 10/07/13 | 0.4 | 1,450 | 2,204 | ||||||||||

Barclays Bank MTN | |||||||||||||

14.000%, 06/15/19 (B) | 0.0 | 100 | 206 | ||||||||||

10.000%, 05/21/21 | 0.1 | 304 | 620 | ||||||||||

6.750%, 01/16/23 (B) | 0.1 | 350 | 564 | ||||||||||

5.000%, 09/22/16 | 0.1 | 330 | 334 | ||||||||||

4.500%, 03/04/19 (B) | 0.0 | 125 | 172 | ||||||||||

Chester Asset Receivables, Ser A | |||||||||||||

6.125%, 10/15/10 | 0.6 | EUR | 2,160 | 3,156 | |||||||||

Royal Bank of Scotland MTN | |||||||||||||

6.934%, 04/09/18 | 0.1 | 300 | 435 | ||||||||||

5.750%, 05/21/14 | 0.1 | 250 | 389 | ||||||||||

| Description | Percentage of Net Assets (%) | Face Amount (Thousands) (1) | Market Value ($ Thousands) | |||||||||

United Kingdom Treasury | ||||||||||||

4.750%, 12/07/38 | 0.2 | % | 665 | $ | 1,183 | |||||||

4.750%, 09/07/15 | 0.3 | 910 | 1,611 | |||||||||

4.500%, 03/07/19 | 0.1 | 195 | 334 | |||||||||

4.500%, 12/07/42 | 0.1 | 335 | 575 | |||||||||

4.250%, 12/07/49 | 0.0 | 85 | 141 | |||||||||

4.250%, 09/07/39 | 0.1 | 325 | 532 | |||||||||

4.000%, 09/07/16 | 0.1 | 350 | 594 | |||||||||

2.250%, 03/07/14 | 0.1 | 355 | 560 | |||||||||

Other Securities | 5.0 | 26,865 | ||||||||||

| 42,398 | ||||||||||||

United States — 7.7% | ||||||||||||

BA Covered Bond Issuer MTN | ||||||||||||

4.125%, 04/05/12 | 0.9 | EUR | 3,100 | 4,622 | ||||||||

Citigroup | ||||||||||||

5.500%, 04/11/13 | 0.2 | 995 | 1,018 | |||||||||

4.750%, 02/10/19 (B) | 0.2 | EUR | 1,000 | 1,198 | ||||||||

4.625%, 08/03/10 | 0.1 | 400 | 409 | |||||||||

4.250%, 02/25/30 (B) | 0.1 | 450 | 454 | |||||||||

Citigroup Funding | ||||||||||||

2.250%, 12/10/12 | 0.1 | 550 | 557 | |||||||||

Other Securities | 6.1 | 33,107 | ||||||||||

| 41,365 | ||||||||||||

Total Global Bonds |

| 394,023 | ||||||||||

MORTGAGE-BACKED SECURITIES — 4.6% | ||||||||||||

Non-Agency Mortgage-Backed Obligation — 4.6% | ||||||||||||

Beluga Master Issuer, | ||||||||||||

1.051%, 04/28/99 (A) | 0.5 | 2,200 | 2,951 | |||||||||

Citigroup Commercial Mortgage Trust, Ser 2007-C6, Cl A4 | ||||||||||||

5.888%, 06/10/17 (A) | 0.2 | 1,140 | 992 | |||||||||

Citigroup Commercial Mortgage Trust, Ser 2008-C7, Cl A4 | ||||||||||||

6.299%, 05/01/38 (A) | 0.1 | 405 | 365 | |||||||||

Citigroup Mortgage Loan Trust, | ||||||||||||

5.110%, 05/25/35 (A) | 0.3 | 2,003 | 1,658 | |||||||||

Gracechurch Mortgage Financing, Ser 2006-1, Cl C3 | ||||||||||||

1.129%, 11/20/56 (A) (B) | 0.0 | 250 | 277 | |||||||||

Gracechurch Mortgage Financing, Ser 2007-1X, Cl 3A2 | ||||||||||||

0.959%, 11/20/56 (A) | 0.5 | 2,000 | 2,836 | |||||||||

| SEI Institutional International Trust / Annual Report / September 30, 2009 | 17 |

Table of Contents

SUMMARY SCHEDULE OF INVESTMENTS

International Fixed Income Fund (Continued)

September 30, 2009

| Description | Percentage of Net Assets (%) | Face Amount (Thousands) (1) | Market Value ($ Thousands) | |||||||||

Gracechurch Mortgage Financing, Ser 2007-1X, Cl 2D2 | ||||||||||||

1.259%, 11/20/56 (A) (B) | 0.1 | % | 400 | $ | 519 | |||||||

Salomon Brothers Mortgage Securities, Ser 2000-C1, Cl A2 | ||||||||||||

7.520%, 12/18/32 (A) | 0.1 | 630 | 631 | |||||||||

Other Securities | 2.8 | 14,636 | ||||||||||

Total Mortgage-Backed Securities | 24,865 | |||||||||||

CORPORATE OBLIGATIONS — 3.8% | ||||||||||||

United States — 3.8% | ||||||||||||

Other Securities | 3.8 | 20,308 | ||||||||||

Total Corporate Obligations | 20,308 | |||||||||||

ASSET-BACKED SECURITIES — 2.8% | ||||||||||||

Automotive — 0.8% | ||||||||||||

Other Securities | 0.8 | 4,393 | ||||||||||

Credit Card — 0.5% | ||||||||||||

Citibank Credit Card Issuance Trust, | ||||||||||||

5.375%, 04/11/11 | 0.5 | EUR | 1900 | 2,727 | ||||||||

Mortgage-Related — 0.3% |

| |||||||||||

Other Securities | 0.3 | 1,760 | ||||||||||

Other Asset-Backed Securities — 1.2% | ||||||||||||

Lambda Finance, Ser 2005-1X, Cl A2 | ||||||||||||

1.113%, 11/15/29 (A) (B) | 0.2 | 844 | 1,135 | |||||||||

Other Securities | 1.0 | 5,131 | ||||||||||

| 6,266 | ||||||||||||

Total Asset-Backed Securities | 15,146 | |||||||||||

U.S. TREASURY OBLIGATIONS — 2.5% | ||||||||||||

U.S. Treasury Bonds | ||||||||||||

3.500%, 02/15/39 | 0.0 | 75 | 68 | |||||||||

4.250%, 05/15/39 | 0.2 | 960 | 993 | |||||||||

U.S. Treasury Notes | ||||||||||||

1.375%, 04/15/12 | 0.5 | 2,500 | 2,511 | |||||||||

2.000%, 11/30/13 | 0.8 | 4,300 | 4,307 | |||||||||

2.625%, 07/31/14 | 0.1 | 700 | 711 | |||||||||

4.500%, 11/15/15 | 0.2 | 1,100 | 1,213 | |||||||||

2.750%, 02/15/19 | 0.1 | 660 | 630 | |||||||||

| Description | Percentage of Net Assets (%) | Face Amount (Thousands) (1)/ Shares | Market Value ($ Thousands) | |||||||||

U.S. Treasury Inflationary Index Note | ||||||||||||

3.000%, 07/15/12 | 0.6 | % | 2,575 | $ | 3,279 | |||||||

Total U.S. Treasury Obligations (Cost $13,623) ($ Thousands) |

| 13,712 | ||||||||||

U.S. GOVERNMENT AGENCY OBLIGATION — 0.2% | ||||||||||||

Other Securities | 0.2 | 878 | ||||||||||

Total U.S. Government Agency Obligation | 878 | |||||||||||

MUNICIPAL BONDS — 0.2% | ||||||||||||

Other Securities | 0.2 | 1,234 | ||||||||||

Total Municipal Bonds | 1,234 | |||||||||||

TIME DEPOSITS — 13.1% | ||||||||||||

United States — 13.1% | ||||||||||||

Brown Brothers Harriman | ||||||||||||

5.950%, 10/01/09 | 0.0 | ZAR | 45 | 6 | ||||||||

2.174%, 10/01/09 | 0.0 | AUD | 79 | 70 | ||||||||

1.500%, 10/01/09 | 0.0 | NZD | 10 | 7 | ||||||||

0.382%, 10/01/09 | 0.0 | NOK | 5 | 1 | ||||||||

0.125%, 10/01/09 | 0.1 | EUR | 125 | 183 | ||||||||

0.088%, 10/01/09 | 0.1 | GBP | 383 | 613 | ||||||||

0.060%, 10/01/09 | 0.2 | CAD | 1,272 | 1,185 | ||||||||

0.030%, 10/01/09 | 12.6 | 67,494 | 67,495 | |||||||||

0.010%, 10/01/09 | 0.0 | HKD | 2 | — | ||||||||

0.010%, 10/01/09 | 0.1 | JPY | 52,493 | 586 | ||||||||

0.010%, 10/01/09 | 0.0 | SEK | 998 | 143 | ||||||||

0.005%, 10/01/09 | 0.0 | SGD | 1 | — | ||||||||

Total Time Deposits | 70,289 | |||||||||||

AFFILIATED PARTNERSHIP — 0.3% | ||||||||||||

United States — 0.3% | ||||||||||||

SEI Liquidity Fund, L.P., | ||||||||||||

0.400%†* (C) | 0.3 | 1,712,483 | 1,704 | |||||||||

Total Affiliated Partnership | 1,704 | |||||||||||

Total Investments — 100.7% | $ | 542,159 | ||||||||||

| 18 | SEI Institutional International Trust / Annual Report / September 30, 2009 |

Table of Contents

A summary of the outstanding forward foreign currency contracts held by the Fund at September 30, 2009, is as follows:

| Settlement Date | Currency to Deliver (Thousands) | Currency to Receive (Thousands) | Unrealized (Depreciation) | |||||||

10/1/09 | USD | 5,088 | CHF | 5,281 | $ | 2 | ||||

10/1/09-11/9/09 | USD | 23,957 | GBP | 14,920 | (95 | ) | ||||

10/1/09-12/4/09 | CHF | 34,081 | USD | 32,175 | (690 | ) | ||||

10/2/09 | USD | 3,675 | DKK | 18,764 | 9 | |||||

10/6/09 | USD | 733 | MXP | 9,904 | — | |||||

10/6/09 | USD | 1,414 | SEK | 9,887 | — | |||||

10/6/09-10/28/09 | USD | 9,518 | CAD | 10,237 | 21 | |||||

10/6/09-11/5/09 | JPY | 10,117,167 | USD | 109,296 | (3,736 | ) | ||||

10/6/09-11/5/09 | MXP | 19,808 | USD | 1,474 | 11 | |||||

10/6/09-11/5/09 | NOK | 3,278 | USD | 555 | (10 | ) | ||||

10/6/09-11/9/09 | GBP | 39,063 | USD | 63,496 | 1,032 | |||||

10/6/09-11/27/09 | CAD | 63,846 | USD | 58,622 | (882 | ) | ||||

10/6/09-11/27/09 | USD | 120,548 | EUR | 82,496 | 34 | |||||

10/6/09-11/27/09 | USD | 31,237 | JPY | 2,813,453 | 190 | |||||

10/6/09-11/27/09 | USD | 33,576 | NOK | 203,357 | 1,429 | |||||

10/6/09-12/2/09 | SEK | 44,384 | USD | 6,339 | (12 | ) | ||||

10/6/09-12/16/09 | EUR | 246,360 | USD | 357,608 | (2,450 | ) | ||||

10/13/09 | USD | 4,233 | AUD | 5,051 | 220 | |||||

10/19/09 | JPY | 147,033 | KRW | 1,988,696 | 47 | |||||

10/22/09-10/28/09 | DKK | 31,475 | USD | 6,104 | (75 | ) | ||||

10/27/09 | PLN | 2,522 | USD | 876 | 7 | |||||

10/28/09 | AUD | 4,349 | USD | 3,599 | (230 | ) | ||||

11/4/09 | GBP | 512 | EUR | 580 | 29 | |||||

11/17/09 | HUF | 145,058 | USD | 767 | (12 | ) | ||||

11/24/09 | HUF | 158,903 | PLN | 2,425 | (19 | ) | ||||

11/25/09 | EUR | 1,121 | PLN | 4,658 | (37 | ) | ||||

11/27/09 | SEK | 77,404 | EUR | 7,580 | — | |||||

| $ | (5,217 | ) | ||||||||

A summary of the open futures contracts held by the Fund at September 30, 2009, is as follows:

| Type of Contract | Number of Contracts Long (Short) | Expiration Date | Unrealized Appreciation (Depreciation) ($ Thousands) | ||||||

30-Day FED Fund | (1 | ) | Oct-2009 | $ | — | ||||

Australian 10-Year Bond | 5 | Dec-2009 | — | ||||||

Australian 3-Year Bond | 178 | Dec-2009 | (80 | ) | |||||

Canadian 10-Year Bond | 39 | Dec-2009 | 58 | ||||||

Euro-Bobl | 132 | Dec-2009 | 115 | ||||||

Euro-Bund | 27 | Dec-2009 | 11 | ||||||

Euro-Schatz | 36 | Dec-2009 | 33 | ||||||

Japanese 10-Year Bond | 1 | Dec-2009 | 8 | ||||||

Long Gilt 10-Year Bond | 36 | Dec-2009 | 43 | ||||||

U.S. 10-Year Treasury Note | (208 | ) | Dec-2009 | (346 | ) | ||||

U.S. 2-Year Treasury Note | (136 | ) | Dec-2009 | (140 | ) | ||||

U.S. 5-Year Treasury Note | (130 | ) | Dec-2009 | (182 | ) | ||||

U.S. Long Treasury Bond | (54 | ) | Dec-2009 | (117 | ) | ||||

| $ | (597 | ) | |||||||

For the year ended September 30, 2009, the total amount of all open futures contracts, as presented in the table above, are representative of the volume of activity for this derivative type during the period.

| SEI Institutional International Trust / Annual Report / September 30, 2009 | 19 |

Table of Contents

SUMMARY SCHEDULE OF INVESTMENTS

International Fixed Income Fund (Continued)

September 30, 2009

A summary of outstanding swap agreements held by the Fund at September 30, 2009, is as follows:

| Credit Default Swaps | |||||||||||||||||

| Counterparty | Reference Entity/Obligation | Buy/Sell Protection | (Pays)/ Receives Rate | Termination Date | Notional Amount (Thousands) | Net Unrealized Appreciation (Depreciation) ($ Thousands) | |||||||||||

| Deutsche Bank | Wolters Kluwer NV, 5.125% 01/27/14 | BUY | (0.90 | ) | 03/20/14 | EUR | 1,400 | $ | (40 | ) | |||||||

| HSBC | Autozone Inc., 5.500% 11/15/15 | BUY | (1.00 | ) | 03/20/15 | 650 | 3 | ||||||||||

| JPMorgan Chase Bank | iTraxx Europe Crossover Series 9 Version 3 | SELL | 6.50 | 06/20/13 | EUR | (4,800 | ) | 153 | |||||||||

| Morgan Stanley | Prudential Financial 4.500% 07/15/13 | SELL | 5.00 | 09/20/14 | (350 | ) | 45 | ||||||||||

| Morgan Stanley | Spanish Government, 5.500% 07/30/17 | BUY | (1.00 | ) | 09/20/14 | USD | 4,100 | (16 | ) | ||||||||

| $ | 145 | ||||||||||||||||

| Interest Rate Swaps | |||||||||||||

| Counterparty | Fund Pays | Fund Receives | Termination Date | Notional Amount (Thousands) | Net Unrealized Appreciation (Depreciation) ($ Thousands) | ||||||||

| Citigroup | 3.79% | 6-Month GBP LIBOR | 05/19/19 | GBP | 2,500,000 | $ | (7 | ) | |||||

| Deutsche Bank | 6-Month EURIBOR | 4.17% | 03/28/13 | EUR | 7,000,000 | 868 | |||||||

| Deutsche Bank | 4.31% | 6-Month EURIBOR | 04/07/10 | EUR | 6,500,000 | (282 | ) | ||||||