Exhibit 99.8

Budget and Fiscal Plan

2009/10 – 2011/12

February 17, 2009

National Library of Canada Cataloguing in Publication Data

British Columbia.

Budget and fiscal plan. — 2002/03/2004/05-

Annual

Also available on the Internet.

Continues: British Columbia. Ministry of Finance and

Corporate Relations. Budget ... reports. ISSN 1207-5841

ISSN 1705-6071 = Budget and fiscal plan — British Columbia.

1. Budget — British Columbia — Periodicals. 2. British

Columbia — Appropriations and expenditures — Periodicals.

I. British Columbia. Ministry of Finance. II. Title.

HJ12.B742 352.48’09711’05 C2003-960048-3

TABLE OF CONTENTS |

|

Budget and Fiscal Plan 2009/10 – 2011/12 | February 17, 2009 |

Attestation by the Secretary to Treasury Board

Summary | 1 |

| |

Part 1: Three-Year Fiscal Plan | |

| |

Introduction | 7 |

Revenue | 13 |

Changes since the first Quarterly Report | 13 |

Budget 2009 Plan | 17 |

Consolidated Revenue Fund Spending | 22 |

Protecting Health Care and Education | 23 |

Sustaining Social Services | 26 |

Supporting Communities and the Environment | 27 |

2010 Olympic and Paralympic Winter Games | 29 |

Administrative and Other Savings | 30 |

Public Service Transformation Fund | 31 |

Service Delivery Agencies | 31 |

Further Efficiencies | 32 |

Full-Time Equivalents | 32 |

Capital Spending | 33 |

Projects over $50 million | 38 |

Provincial Debt | 40 |

Risks to the Fiscal Plan | 43 |

| |

Tables: | |

1.1 | Three-Year Fiscal Plan – Operating Statement | 7 |

1.2 | Three-Year Fiscal Plan Update – Changes from Budget 2008 | 8 |

1.3 | Revenue by Source | 10 |

1.4 | Expense by Ministry, Program and Agency | 11 |

1.5 | Major Factors Underlying Revenue | 17 |

1.6 | Personal Income Tax Revenue | 18 |

1.7 | Corporate Income Tax Revenue | 19 |

1.8 | Social Service Tax Revenue | 19 |

1.9 | Health and Social Transfers | 21 |

1.10 | Sustaining Social Services | 26 |

1.11 | Supporting Communities and the Environment | 28 |

1.12 | Olympics Funding | 29 |

1.13 | Managing Down Expenses | 30 |

1.14 | Administrative Spending – Change from 2008/09 | 31 |

1.15 | Full-Time Equivalents (FTEs) – Changes from Budget 2008 | 32 |

1.16 | Capital Spending | 34 |

1.17 | Provincial Transportation Investments | 35 |

1.18 | Capital Expenditure Projects Greater Than $50 million | 39 |

1.19 | Provincial Debt Summary | 40 |

1.20 | Reconciliation of Summary Results to Provincial Debt Changes | 42 |

1.21 | Provincial Financing | 43 |

1.22 | Key Fiscal Sensitivities | 44 |

1.23 | Notional Allocations to Contingencies | 46 |

Budget and Fiscal Plan – 2009/10 to 2011/12

Topic Boxes: | |

Presentation of Provincial Government Debt | 50 |

The Port Mann Bridge / Highway 1 Project | 52 |

British Columbia’s Strong Foundation | 53 |

| |

Part 2: Tax Measures | |

| |

Tax Measures — Supplementary Information | 64 |

October 22 and November 1, 2008 Measures | 64 |

Budget 2009 Measures | 66 |

| |

Tables: | |

2.1 | Summary of Tax Measures | 63 |

2.2 | British Columbia Personal Income Tax Cut – Impact on Taxpayers | 65 |

2.3 | Commission Rates | 65 |

| | |

Topic Box: | |

Revenue Neutral Carbon Tax | 72 |

| |

Part 3: British Columbia Economic Review and Outlook | |

| |

Summary | 75 |

Recent Developments | 76 |

The Outlook for the External Environment | 78 |

United States | 78 |

Canada | 81 |

Other Economies | 83 |

Financial Markets | 84 |

Interest Rates | 84 |

Exchange Rate | 86 |

The British Columbia Economic Outlook | 87 |

Labour Market | 88 |

Domestic Demand | 88 |

Business and Government | 90 |

External Trade and Commodity Markets | 91 |

Inflation | 92 |

Risks to the Economic Outlook | 93 |

| |

Tables: | |

3.1 | British Columbia Economic Indicators | 76 |

3.2 | Ministry of Finance Economic Forecast: Key Assumptions | 84 |

3.3 | Private Sector Canadian Three Month Treasury Bill Interest Rate Forecasts | 85 |

3.4 | Private Sector Canadian 10-year Government Bond Interest Rate Forecasts | 85 |

3.5 | Private Sector Exchange Rate Forecasts | 86 |

3.6 | British Columbia Economic Outlook | 87 |

3.7 | Ministry of Finance Economic Forecast: Key Economic Indicators | 87 |

3.8 | British Columbia Economic Review | 94 |

3.9.1 | Gross Domestic Product: British Columbia | 95 |

3.9.2 | Components of Nominal Income and Expenditure | 96 |

3.9.3 | Labour Market Indicators | 96 |

3.9.4 | Major Economic Assumptions | 97 |

| | |

Topic Box: | |

The Economic Forecast Council, 2009 | 98 |

Economic Downturns in BC since 1980 | 104 |

Budget and Fiscal Plan – 2009/10 to 2011/12

ii

Part 4: 2008/09 Revised Financial Forecast (Third Quarterly Report) | |

| |

2008/09 Fiscal Year in Review | 107 |

Changes since the Second Quarterly Report | 109 |

2008/09 Priority Spending | 109 |

2008/09 Notional Contingencies Allocations | 111 |

Capital Spending and Provincial Debt | 112 |

| |

Tables: | |

4.1 | Budget 2008 and Quarterly Updates | 107 |

4.2 | 2008/09 Forecast Update | 108 |

4.3 | 2008/09 Priority Initiatives (Operating) | 110 |

4.4 | 2008/09 Priority Initiatives (Capital) | 111 |

4.5 | 2008/09 Notional Allocations to Contingencies | 112 |

4.6 | 2008/09 Capital Spending Update | 112 |

4.7 | 2008/09 Provincial Debt Update | 113 |

4.8 | 2008/09 Operating Statement | 114 |

4.9 | 2008/09 Revenue by Source | 114 |

4.10 | 2008/09 Expense by Function | 115 |

4.11 | 2008/09 Expense by Ministry, Program and Agency | 116 |

4.12 | 2008/09 Capital Spending | 117 |

4.13 | 2008/09 Provincial Debt | 118 |

4.14 | 2008/09 Statement of Financial Position | 119 |

| | |

Appendices | 121 |

Budget and Fiscal Plan – 2009/10 to 2011/12

iii

| | February 17, 2009 |

As required by Section 7(d) of the Budget Transparency and Accountability Act (BTAA), and Section 4(a)(v) of the Carbon Tax Act, I am confirming that the Budget and Fiscal Plan contains the following elements:

· The fiscal and economic forecasts for 2009/10 and the next two years, which are detailed in Parts 1 and 3 of the Budget and Fiscal Plan.

· All material economic, demographic, taxation, accounting policy and other assumptions underlying the 2009/10 economic, revenue, expenditure, surplus and debt forecasts are also disclosed. In particular:

· The capital plan includes $2 billion for accelerated infrastructure projects, based on the assumption that the federal government will contribute $1 billion from federal infrastructure programs announced in the January 27 federal budget;

· The Port Mann Bridge has not been included in the fiscal plan as final agreement has not been reached with the Connect BC Development Group, and accounting treatment has not been finalized. The implications are discussed further in the topic box on the Port Mann Bridge found on page 52 of the Budget and Fiscal Plan;

· The Province is assumed to reach an agreement with the federal government over the funding of Olympic security part of which will require a one-time payment to the federal government before the end of 2008/09;

· Unlike recent years, there are no forecast allowances included in the fiscal plan and government will be managing risks to the fiscal plan through expenditure management and use of the contingency vote;

· Most of the wage agreements reached in the last round of public sector negotiations expire by the end of 2009/10. No funding is included in the fiscal plan for the next round; and

· Further savings of $250 million are to be identified and achieved by 2011/12.

· The report on the advice received from the Minister’s Economic Forecast Council, which was last updated on January 9, on the economic growth outlook for British Columbia, including the range of forecasts for 2009 and 2010.

· The major areas of risk to the plan known at this time are disclosed in the risks section in Part 1 starting at page 43 of the Budget and Fiscal Plan, and in the material assumptions tables in the Appendix.

· A carbon tax report for 2008/09 and a carbon tax plan for 2009/10 to 2011/12 and corresponding material assumptions. These can be are found in the Revenue Neutral Carbon Tax topic box at the end of Part 2: Tax Measures (page 72).

Three-year aggregate financial plans for health authorities, school districts, and universities and colleges have been compiled by the Ministries of Health Services, Education, and Advanced Education and Labour Market Development based on funding included in respective ministry budgets. Individual plans for health authorities and post-secondary institutions, including strategies for managing spending pressures, will be subsequently developed and reflected in the updated fiscal plan in the first Quarterly Report.

The accounting policies followed in the Budget and Fiscal Plan comply, in all material respects, with generally accepted accounting principles (GAAP) for senior governments.

I would like to thank staff in government ministries and agencies for their contribution to this document. During a time of significant uncertainty, I would like to especially recognize the commitment of staff in the Ministry of Finance, whose teamwork and skills were put to the test this year and whose passion was essential to the timely and professional completion of this budget.

Chris Trumpy

Deputy Minister and

Secretary to Treasury Board

Ministry of

Finance | | Office of the

Deputy Minister | | Mailing Address:

PO Box 9417 Stn Prov Govt

Victoria BC V8W 9V1

www.gov.bc.ca/fin | | Location Address:

Room 109

617 Government Street

Victoria BC |

Summary: BUDGET AND FISCAL PLAN — 2009/10 to 2011/12

| | 2008/09 | | Budget | | | | | |

($ millions) | | Budget | | Updated

Forecast | | Estimate

2009/10 | | Plan

2010/11 | | Plan

2011/12 | |

Revenue | | 38,490 | | 38,455 | | 38,812 | | 39,795 | | 41,182 | |

Expense | | (37,690 | ) | (38,405 | ) | (39,307 | ) | (40,040 | ) | (41,182 | ) |

Surplus (Deficit) before forecast allowance | | 800 | | 50 | | (495 | ) | (245 | ) | — | |

Forecast allowance | | (750 | ) | — | | — | | — | | — | |

Surplus (Deficit) | | 50 | | 50 | | (495 | ) | (245 | ) | — | |

Capital spending: | | | | | | | | | | | |

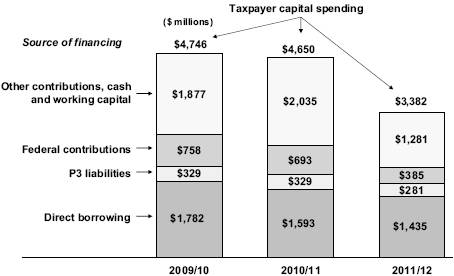

Taxpayer-supported capital spending | | 3,859 | | 4,133 | | 4,746 | | 4,650 | | 3,382 | |

Total capital spending | | 5,766 | | 5,951 | | 6,945 | | 7,155 | | 5,924 | |

Provincial Debt: | | | | | | | | | | | |

Government direct operating debt | | 7,408 | | 6,437 | | 6,847 | | 7,104 | | 7,074 | |

Taxpayer-supported debt | | 27,741 | | 27,692 | | 30,213 | | 32,392 | | 34,078 | |

Total debt | | 37,741 | | 37,487 | | 40,471 | | 44,203 | | 47,215 | |

Government direct operating debt-to-GDP ratio | | 3.7 | % | 3.2 | % | 3.5 | % | 3.4 | % | 3.3 | % |

Taxpayer-supported debt-to-GDP ratio | | 14.0 | % | 13.8 | % | 15.2 | % | 15.7 | % | 15.8 | % |

Total debt-to GDP ratio | | 19.0 | % | 18.7 | % | 20.4 | % | 21.4 | % | 21.8 | % |

Protecting Public Services

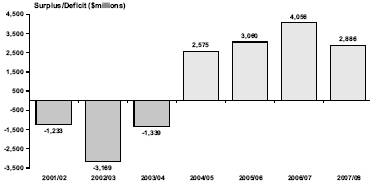

Budget 2009 projects deficits of $495 million in 2009/10 and $245 million in 2010/11, returning to a balanced budget by 2011/12.

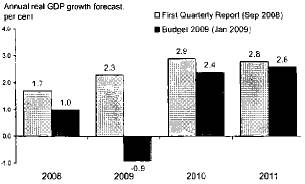

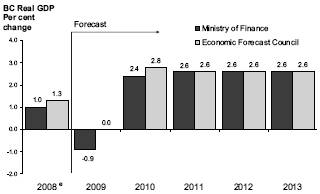

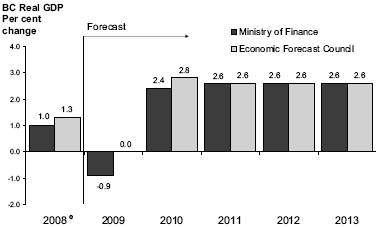

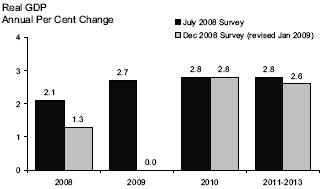

The fiscal plan is based on the Ministry of Finance economic forecast that projects real economic growth of minus 0.9 per cent for 2009, recovering to 2.4 per cent in 2010 and 2.6 per cent in 2011. The economic outlook is a significant reversal of expectations at the time of the 2008/09 first Quarterly Report, particularly in 2009.

Government’s economic forecast lowered from the first Quarterly Report

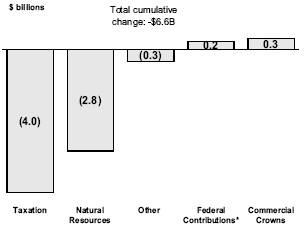

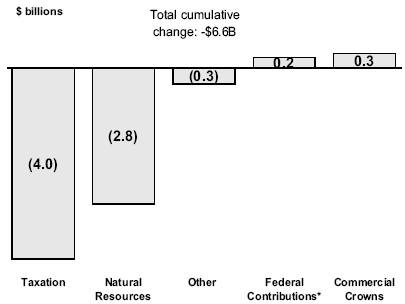

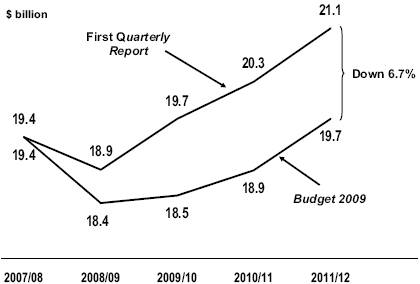

The economic downturn resulted in a reduction of $6.6 billion in revenue over the fiscal plan period since the September Budget Consultation Paper. This loss will be partially offset by $870 million in federal funding that comes with transfer of responsibilities under the Labour Market Development Agreement that provides training for British Columbians seeking employment, resulting in a net decrease in revenue of $5.8 billion.

3-Year cumulative change in revenue since the first Quarterly Report

* Excludes $870 million in funding for the LMDA transfer

Overall, spending is projected to increase by $2.8 billion over the fiscal plan period. This includes spending associated with the Labour Market Development Agreement. Excluding the agreement, projected spending represents an average annual growth of 2.2 per cent. By achieving $1.9 billion of savings, government is able to maintain services during the economic downturn while providing additional spending in key areas.

Budget and Fiscal Plan – 2009/10 to 2011/12

Summary

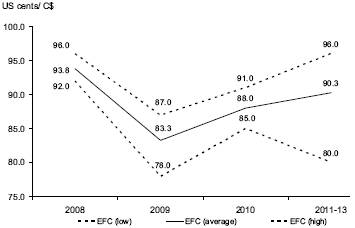

Domestic Economy Contracts

BC’s economic forecast for 2009 reflects the sharp US and global economic slowdown, moderating domestic demand, as well as instability in global financial and commodity markets.

In the medium term, BC’s economy is expected to return closer to historical levels of growth, due primarily to an anticipated recovery of US demand (particularly in the housing sector) and a gradual rise in commodity prices.

BC’s economy to rebound in 2010

(e): estimate

Note: the EFC provided an average forecast for 2011 to 2013 on January 9, 2009

Indicators of economic performance through most of 2008 confirm that British Columbia’s economy slowed considerably in the latter half of the year. On the domestic side, monthly retail sales and housing starts declined significantly since July. The employment situation has also weakened in recent months, with the unemployment rate climbing by 1.6 per cent from July to January.

On the trade side, the value of manufacturing shipments fell steadily through most of 2008 due mainly to reduced demand for BC’s forest products from the troubled US economy. However, total exports from BC increased year-to-date to November 2008, driven by high energy prices pushing up the value of energy exports.

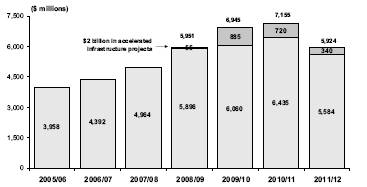

Infrastructure Program

Budget 2009 continues government’s commitment to an infrastructure spending plan that includes the acceleration of a number of new projects in order to keep British Columbians working and help stimulate the economy.

Infrastructure spending on transit, roads, schools, hospitals, post secondary facilities, electrical generation, transmission and distribution projects and other capital assets totals $20 billion over the three year period of the fiscal plan.

The capital plan includes $2 billion for accelerated infrastructure projects and assumes federal contributions of $1.0 billion, from infrastructure stimulus funds announced in the federal budget on January 27, 2009.

Construction investments of $10.6 billion are also included in the Province’s capital plan (i.e. excluding information technology projects, land purchases, and vehicle purchases).

An additional $1.4 billion in local infrastructure projects is being built in partnership with local governments and the federal government.

These investments are estimated to generate 88,000 direct construction jobs over the next three years.

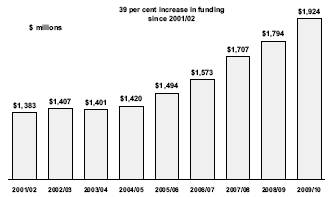

Healthcare funding increases

* Before $120 million Supplementary Estimates

Protecting Healthcare and Education

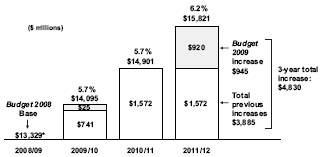

Budget 2009 confirms government’s commitment to health care and provides an additional $920 million for the Ministry of Health Services and health authorities in 2011/12, for an annual 6 per cent increase in funding for the third year of the fiscal plan. This funding is in addition to $3.9 billion over 3 years allocated previously in Budget 2008.

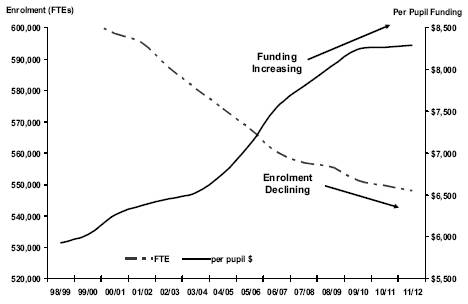

Budget 2009 maintains operating grant funding to school districts at previously announced funding levels. Despite enrolment declines over the next 3 years, the total budget for K-12 education continues to increase, resulting in higher levels of per pupil funding at the school district level.

Budget and Fiscal Plan – 2009/10 to 2011/12

2

Summary

Per pupil funding rises while student enrolment drops

Budget 2009 also increases access to post-secondary education and training throughout the province by providing $244 million over three years in new operating funding, including $228 million to post-secondary institutions and $16 million to support immigrant workers over three years.

Post-secondary funding increases

Sustaining Social Services

Budget 2009 ensures that programs and services that enhance the quality of life for British Columbians in need are protected, and provides $381 million over four years to:

· maintain previous funding commitments that implement new and expanded measures to help break the cycle of homelessness and support low income seniors and families;

· support priority programs and services for families and communities to care for and protect vulnerable children and youth;

· support programs and services to adults with developmental disabilities and their families, including continued access to community living services such as respite care, residential placements and life skills training; and

· provide additional support to individuals and families who experience difficulty in paying for their basic living necessities and will require income assistance.

Sustaining Social Services

($ millions) | | 4-year

Total (1) | |

Acquisition of social housing | | 30 | |

Children and Families | | | |

– Supporting families and children in care | | 47 | |

– Child care subsidies | | 25 | |

– Supporting children with special needs | | 38 | |

Subtotal | | 110 | |

Supporting adults with developmental disabilities | | 73 | |

Income assistance for individuals and families in need | | 110 | |

Policing and victim support | | 58 | |

Total | | 381 | |

(1) See page 26 for further information.

Supporting Communities and the Environment

Budget 2009 provides $479 million over four years, to support economic activity in communities throughout the province during the economic downturn, maintain BC as a leader in environmental protection and funds initiatives to support local government priorities and provide greater flexibility to address immediate needs including community safety.

Supporting Communities and the Environment

($ millions) | | 4-year

Total (1) | |

Supporting Communities | | | |

– Improving access for shale gas development | | 6 | |

– Improvements for rural resource roads | | 20 | |

– Community economic development | | 30 | |

– Towns for Tomorrow: cost shared community infrastructure | | 50 | |

– Local transportation projects to accelerate job creation | | 20 | |

– Bulkley-Nechako / Kitimal-Stikine Regional District grants | | 3 | |

– Internet connectivity for rural communities | | 5 | |

– Peace River Regional District infrastructure | | 9 | |

– Local government priorities, including community safety | | 151 | |

Subtotal | | 294 | |

Targeted Measures | | | |

– Michael Smith Foundation for health research | | 15 | |

– Provincial Transit Plan additional operating funding | | 59 | |

Subtotal | | 74 | |

Continued Environmental Leadership | | | |

– Carbon tax rebates for local government | | 15 | |

– Extending the ICE fund for green technology advancements | | 75 | |

– Planning for Capital Regional District water treatment facility | | 2 | |

– Trees for Tomorrow: planting trees in public places | | 11 | |

– BC portion of the Hydrogen Highway | | 8 | |

Subtotal | | 111 | |

Total | | 479 | |

(1) See page 28 for further information.

Budget and Fiscal Plan – 2009/10 to 2011/12

3

Summary

Tax Measures

On October 22, 2008, government announced economic stimulus measures including the accelerated personal income tax cuts and small business tax relief. The 3 per cent reduction in the rates for the two lowest income tax brackets, combined with the 2 per cent reduction in Budget 2008, provides a $211 million reduction in 2008 taxes for British Columbians to help stimulate the economy.

Government also introduced a temporary property tax deferment program for homeowners who are experiencing financial hardship due to current economic conditions.

Administrative Efficiencies

Government is managing down expenses in order to protect health care, education and social service programs. Significant savings in administrative and other discretionary spending will be achieved, and some government programs will be streamlined.

Budget 2009 reallocates $1.9 billion in administrative and other savings over 3 years to health care, education and social service programs as well as to support other priority programs that provide public services.

Administrative Spending – Change from 2008/09

| | 2008/09 | | 2009/10 | | $ | | % | |

($ millions) | | Estimates | | Estimates | | Change | | Change | |

Expense category: | | | | | | | | | |

– Boards, commissions and courts (fees and expenses) | | 11 | | 10 | | (1 | ) | -5 | % |

– Public servant travel | | 74 | | 58 | | (16 | ) | -22 | % |

– Professional services | | 769 | | 592 | | (177 | ) | -23 | % |

– Office and business expenses | | 116 | | 106 | | (10 | ) | -8 | % |

– Informational advertising and publications | | 30 | | 7 | | (23 | ) | -76 | % |

– Operating equipment and vehicles | | 135 | | 123 | | (12 | ) | -9 | % |

– Transfers — grants (discretionary) | | 826 | | 768 | | (58 | ) | -7 | % |

Total savings | | 1,961 | | 1,664 | | (297 | ) | -15 | % |

Government has also established a Transformation Fund within the Public Service Agency. The fund will be used to strategically invest in priority job streams and targeted recruitment, and to fund opportunities where the approach to work can be re-tooled to deliver quality services to citizens with fewer staff.

In addition, government will continue to review its operations to achieve a further $250 million in annual efficiencies by the end of 2011/12.

Return to Balanced Budgets by 2011/12

Government maintains its practice of strong fiscal management by requiring the budget to be balanced by the third year of the fiscal plan. In addition, the exemption to the balanced budget legislation requires government to use any future year end surpluses to eliminate direct operating debt, prohibiting Supplementary Estimates until the direct operating debt is eliminated.

BC will return to balanced budgets in 2011/12

Debt Remains Affordable

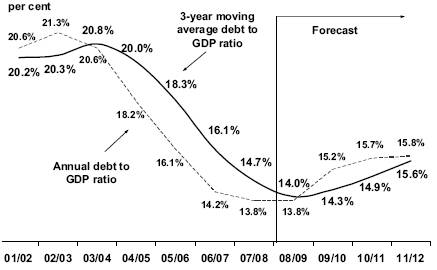

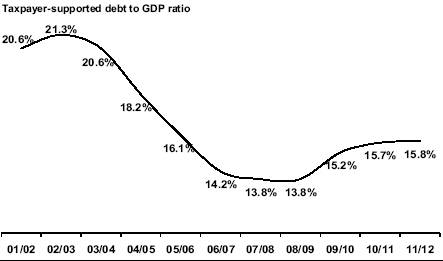

Significant progress has been made in reducing the taxpayer supported debt burden over the past five years. The taxpayer-supported debt to GDP ratio has declined from 21.3 per cent in 2002/03 to 13.8 per cent by 2008/09, a 35 per cent reduction. Due to significant infrastructure investments and weaker economic growth, the taxpayer-supported debt to GDP ratio is forecast to increase from 13.8 per cent in 2008/09 to 15.8 per cent in 2011/12. Debt remains affordable, despite the global economic downturn.

Taxpayer-supported debt burden remains low

Budget and Fiscal Plan – 2009/10 to 2011/12

4

Summary

Risks to the Fiscal Plan

The main risks to the government fiscal plan on the economic side include a protracted period of low economic growth in the US, reduced global demand for BC’s exports, continuing turmoil in global financial markets, and further weakening of domestic demand. Other risks include exchange rate movements or changes in natural gas, lumber or other commodity markets, as well as service demand pressures on the expenditure side.

No funding is included in the fiscal plan for the next round of public sector wage negotiations.

As the agreement has not been finalized, the fiscal implications of the Port Mann Bridge/ Highway 1 project, which will be funded from tolls, are not included in Budget 2009.

Other major risks to the fiscal plan stem from changes in factors that government does not directly control. These include:

· Assumptions underlying revenue and Crown corporation and agency forecasts such as economic factors, commodity prices and weather conditions.

· Utilization rates for government services such as health care, children and family services, and income assistance.

· The outcome of litigation, arbitrations, and negotiations with third parties.

· Potential changes to federal transfer allocations, cost-sharing agreements with the federal government and impacts on the provincial income tax bases arising from federal tax policy and budget changes. The impact of the recent federal income tax reductions on the economy was not anticipated when the economic forecast was finalized.

The fiscal plan includes contingencies of $385 million in 2009/10, $300 million in 2010/11 and $250 million in 2011/12 to help ensure the fiscal targets are met.

Conclusion

In summary, Budget 2009:

· provides a $2.0 billion accelerated infrastructure program to keep people at work in the construction sector over the next three years;

· protects public services and provides additional funding for health care, education and social services;

· reduces administrative and other costs and returns to balanced budgets by 2011/12; and

· keeps debt affordable.

Budget and Fiscal Plan – 2009/10 to 2011/12

5

Part 1: THREE-YEAR FISCAL PLAN

Table 1.1 Three-Year Fiscal Plan – Operating Statement

| | 2008/09 | | Budget | | | | | |

| | | | Updated | | Estimate | | Plan | | Plan | |

($ millions) | | Budget | | Forecast | | 2009/10 | | 2010/11 | | 2011/12 | |

Taxpayer-supported programs and agencies: | | | | | | | | | | | |

Revenue | | 38,490 | | 38,455 | | 38,812 | | 39,795 | | 41,182 | |

Expense | | (37,690 | ) | (38,405 | ) | (39,307 | ) | (40,040 | ) | (41,182 | ) |

Surplus (deficit) before forecast allowance | | 800 | | 50 | | (495 | ) | (245 | ) | — | |

Forecast allowance | | (750 | ) | — | | — | | — | | — | |

Surplus (deficit) | | 50 | | 50 | | (495 | ) | (245 | ) | — | |

Introduction

Budget 2009 reflects government’s response to the recent unprecedented drop in provincial revenues resulting from the global economic downturn. Despite economic stimulus measures and a comprehensive review of government operations to achieve administrative cost savings, revenue weakness has required the government to suspend its balanced budget legislation for a period of two years in order to protect vital health care, education and social services.

Budget 2009 projects deficits of $495 million in 2009/10 and $245 million in 2010/11. Nonetheless, government maintains its practice of strong fiscal management by requiring the budget to be balanced by the third year of the fiscal plan. In addition, the exemption to the balanced budget legislation requires government to use any future year end surpluses to eliminate direct operating debt, prohibiting Supplementary Estimates until the direct operating debt is eliminated.

The fiscal plan is based on the Ministry of Finance economic forecast that projects real economic growth of minus 0.9 per cent for 2009, recovering to 2.4 per cent in 2010 and 2.6 per cent in 2011. The Ministry of Finance’s outlook for 2009 is significantly lower than the outlook provided by the Economic Forecast Council. This greater-than-normal level of prudence recognizes the potential for further forecast downgrades by the private sector due to continuing economic and financial turmoil in global markets. The economic outlook is a significant reversal of expectations at the time of the 2008/09 first Quarterly Report, particularly in 2009. Full details of the economic forecast are found in Part 3: British Columbia Economic Review and Outlook.

The economic downturn resulted in a reduction of $6.6 billion in revenue over the fiscal plan period since the September Budget Consultation Paper. This loss was partially offset by $870 million in federal funding that comes with transfer of responsibilities under the Labour Market Development Agreement that provides training for British Columbians seeking employment, resulting in a net decrease in revenue of $5.8 billion as shown in Table 1.2.

Government is managing down expenses in order to protect health care, education and social service programs. Significant savings in administrative and other discretionary spending will be achieved, and some government programs will be streamlined. Budget 2009 reallocates $1.9 billion in administrative and other savings over 3 years to health care, education and social service programs as well as to support other priority programs that provide public services.

Budget and Fiscal Plan – 2009/10 to 2011/12

7

Three-Year Fiscal Plan

Table 1.2 Three-Year Fiscal Plan Update – Changes from Budget 2008

($ millions) | | 2008/09 | | 2009/10 | | 2010/11 | | 2011/12 | |

| | | | | | | | | |

Budget 2008 Fiscal Plan Surplus (February 19, 2008) | | 50 | | 150 | | 150 | | 150 | |

Budget 2009 Consultation Paper – available revenue | | 970 | | 1,015 | | 385 | | 1,500 | |

Updated fiscal plan before revenue changes and spending initiatives | | 1,020 | | 1,165 | | 535 | | 1,650 | |

Revenue changes: | | | | | | | | | |

Personal income tax: | | | | | | | | | |

Personal income tax – prior year adjustment | | (94 | ) | — | | — | | — | |

Personal income tax | | (285 | ) | (363 | ) | (325 | ) | (116 | ) |

Corporate income tax | | 311 | | (122 | ) | (244 | ) | (363 | ) |

Social service tax | | (234 | ) | (363 | ) | (421 | ) | (460 | ) |

Carbon tax | | (38 | ) | (85 | ) | (126 | ) | (175 | ) |

Property tax | | (24 | ) | (73 | ) | (122 | ) | (183 | ) |

Property transfer tax | | (165 | ) | (175 | ) | (100 | ) | (70 | ) |

Other tax sources | | 4 | | (20 | ) | (47 | ) | (43 | ) |

Forests | | (103 | ) | (226 | ) | (158 | ) | (269 | ) |

Natural gas royalties | | (356 | ) | (553 | ) | (346 | ) | (145 | ) |

Other energy, metals and minerals | | (214 | ) | (433 | ) | (363 | ) | (301 | ) |

Other fees and licenses | | (101 | ) | (13 | ) | (66 | ) | (73 | ) |

Investment earnings | | (76 | ) | (40 | ) | (25 | ) | 63 | |

Health and social transfers | | 49 | | 61 | | 6 | | (34 | ) |

Labour Market Development Agreement | | 48 | | 290 | | 290 | | 290 | |

Other federal transfers | | (24 | ) | 59 | | 67 | | 70 | |

Other taxpayer-supported revenue | | (55 | ) | (88 | ) | (112 | ) | (23 | ) |

Commercial Crown agencies operating results: | | | | | | | | | |

BC Hydro – mainly increase in allowed return on equity | | (4 | ) | 41 | | 37 | | 43 | |

Liquor Distribution Branch – mainly increased product sales | | 13 | | 33 | | 44 | | 58 | |

ICBC – mainly lower claims costs and operating efficiencies partially offset by lower premium and investment revenue | | 131 | | 13 | | 1 | | 38 | |

BC Railway Company – mainly delay in surplus property sales | | (25 | ) | (5 | ) | 21 | | (1 | ) |

Other commercial Crown agencies changes | | 4 | | 9 | | 4 | | (19 | ) |

Total revenue changes | | (1,238 | ) | (2,053 | ) | (1,985 | ) | (1,713 | ) |

Forecast allowance updates | | 750 | | 675 | | 675 | | 675 | |

Less : expense increases (decreases): | | | | | | | | | |

| | | | | | | | | |

Strategic priorities: | | | | | | | | | |

Healthcare (Chart 1.13) | | 120 | | 25 | | — | | 920 | |

Post-secondary education | | — | | 71 | | 86 | | 87 | |

Sustaining social services (Table 1.10) | | 30 | | 119 | | 127 | | 105 | |

Supporting communities and the environment (Table 1.11) | | 213 | | 104 | | 63 | | 99 | |

Public service transformation | | — | | 50 | | 25 | | — | |

Administrative and other savings | | — | | (589 | ) | (650 | ) | (631 | ) |

Labour Market Development Agreement | | 48 | | 290 | | 290 | | 290 | |

Adjust contingencies | | 125 | | (5 | ) | (100 | ) | (150 | ) |

Remove allocation for future wage increases | | — | | — | | (400 | ) | (400 | ) |

Debt servicing (including MOPD) | | (23 | ) | (64 | ) | (5 | ) | 160 | |

Additional expense recovered from external sources | | 22 | | 36 | | — | | 63 | |

Impact of transportation investment plan and infrastructure spending | | 22 | | 66 | | 109 | | 390 | |

Ministry year-end savings redirected to priorities | | (123 | ) | — | | — | | — | |

Other spending changes | | 48 | | 179 | | 50 | | (71 | ) |

Further efficiencies | | — | | — | | (125 | ) | (250 | ) |

Total expense increases (decreases) | | 482 | | 282 | | (530 | ) | 612 | |

Budget 2009 Updated Fiscal Plan Surplus (Deficit) | | 50 | | (495 | ) | (245 | ) | — | |

Budget and Fiscal Plan – 2009/10 to 2011/12

8

Three-Year Fiscal Plan

Chart 1.1 Revenue and spending trends

Overall, spending is projected to increase by $2.8 billion over the fiscal plan period. This includes spending associated with the Labour Market Development Agreement. Excluding the agreement, projected spending represents an average annual growth of 2.2 per cent, slightly higher than inflation. This will enable government to maintain services during the economic downturn while providing additional spending in key areas.

In 2008/09, ministry savings and a reduced forecast allowance have enabled government to allocate $622 million to priority initiatives, primarily to address the impact of the economic downturn. Government intends to introduce Supplementary Estimates to obtain the necessary legislative appropriations to fund these initiatives. (See Part 4: 2008/09 Revised Financial Forecast (third Quarterly Report) for further details).

Budget 2009 continues government’s commitment to an infrastructure spending plan that includes the acceleration of a number of new projects in order to keep British Columbians working and help stimulate the economy. Infrastructure spending on transit, roads, schools, hospitals, post secondary facilities, electrical generation, transmission and distribution projects and other capital assets totals $20 billion over the three year period of the fiscal plan. The capital plan includes $2 billion for accelerated infrastructure projects and assumes federal contributions of $1.0 billion from infrastructure stimulus funds announced in the federal budget on January 27, 2009. More information on the three-year capital spending plan is found on page 33.

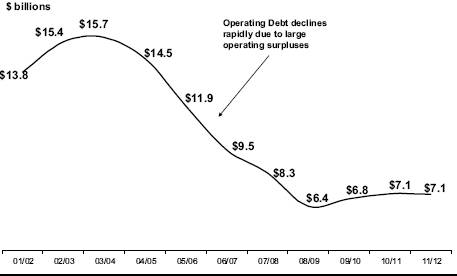

Since peaking in 2003/04, government has made significant progress in reducing taxpayer-supported debt, including the operating debt. Taxpayer-supported debt has declined from $30.0 billion in 2003/04 to $27.7 billion by 2008/09. Operating debt has been reduced by 59 per cent from a peak of $15.7 billion in 2003/04 to $6.4 billion in 2008/09. These reductions allow government the flexibility to address the current economic challenges, while keeping debt affordable.

Budget and Fiscal Plan – 2009/10 to 2011/12

9

Three-Year Fiscal Plan

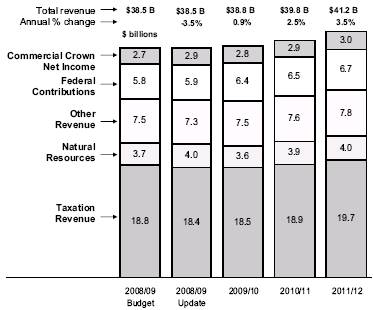

Table 1.3 Revenue by Source

| | 2008/09 | | Budget | | | | | |

($ millions) | | Budget | | Revised

Forecast | | Estimate

2009/10 | | Plan

2010/11 | | Plan

2011/12 | |

Taxation revenue | | | | | | | | | | | |

Personal income | | 6,700 | | 6,219 | | 6,562 | | 6,942 | | 7,366 | |

Corporate income | | 1,343 | | 2,037 | | 1,529 | | 1,072 | | 923 | |

Social service | | 5,284 | | 4,998 | | 5,087 | | 5,299 | | 5,533 | |

Fuel | | 957 | | 912 | | 914 | | 920 | | 928 | |

Carbon | | 338 | | 300 | | 546 | | 754 | | 968 | |

Tobacco | | 705 | | 713 | | 687 | | 687 | | 687 | |

Property | | 1,861 | | 1,840 | | 1,881 | | 1,936 | | 1,967 | |

Property transfer | | 1,020 | | 735 | | 685 | | 720 | | 750 | |

Other (1) | | 601 | | 610 | | 594 | | 553 | | 570 | |

| | 18,809 | | 18,364 | | 18,485 | | 18,883 | | 19,692 | |

Natural resource revenue | | | | | | | | | | | |

Natural gas royalties | | 1,165 | | 1,376 | | 1,014 | | 1,156 | | 1,281 | |

Forests | | 952 | | 587 | | 609 | | 707 | | 700 | |

Other resource (2) | | 1,606 | | 2,048 | | 2,007 | | 2,046 | | 2,030 | |

| | 3,723 | | 4,011 | | 3,630 | | 3,909 | | 4,011 | |

Other revenue | | | | | | | | | | | |

Medical Services Plan premiums | | 1,571 | | 1,577 | | 1,591 | | 1,613 | | 1,635 | |

Other fees (3) | | 2,505 | | 2,430 | | 2,518 | | 2,501 | | 2,519 | |

Investment earnings | | 884 | | 839 | | 918 | | 1,005 | | 1,095 | |

Miscellaneous (4) | | 2,509 | | 2,474 | | 2,475 | | 2,503 | | 2,562 | |

| | 7,469 | | 7,320 | | 7,502 | | 7,622 | | 7,811 | |

Contributions from the federal government | | | | | | | | | | | |

Health and social transfers | | 4,794 | | 4,693 | | 4,910 | | 5,110 | | 5,316 | |

Other federal contributions (5) | | 1,015 | | 1,223 | | 1,460 | | 1,408 | | 1,396 | |

| | 5,809 | | 5,916 | | 6,370 | | 6,518 | | 6,712 | |

Commercial Crown corporation net income | | | | | | | | | | | |

BC Hydro | | 358 | | 357 | | 452 | | 493 | | 542 | |

Liquor Distribution Branch | | 854 | | 867 | | 896 | | 918 | | 938 | |

BC Lotteries (net of payments to federal government) | | 1,101 | | 1,101 | | 1,154 | | 1,198 | | 1,228 | |

ICBC (6) | | 272 | | 459 | | 260 | | 192 | | 217 | |

Other | | 95 | | 60 | | 63 | | 62 | | 31 | |

| | 2,680 | | 2,844 | | 2,825 | | 2,863 | | 2,956 | |

Total revenue | | 38,490 | | 38,455 | | 38,812 | | 39,795 | | 41,182 | |

(1) Corporation capital, insurance premium and hotel room taxes.

(2) Columbia River Treaty, other energy and minerals, water rental and other resources.

(3) Post-secondary, healthcare-related, motor vehicle, and other fees.

(4) Includes asset dispositions, reimbursements for health care and other services provided to external agencies, and other recoveries.

(5) Includes contributions for health, education, community development, housing and social service programs, and transportation projects.

(6) The 2008/09 amounts represent ICBC’s projected earnings during government’s fiscal year. On ICBC’s fiscal year basis (December), the outlook for 2008 is: (budget) — $272 million; (forecast) — $498 million. For 2009/10 to 2011/12, the fiscal year and calendar year projections are assumed to be the same.

Budget and Fiscal Plan – 2009/10 to 2011/12

10

Three-year Fiscal Plan

Table 1.4 Expense by Ministry, Program and Agency

| | 2008/09 | | Budget | | | | | |

| | | | Revised | | Estimate | | Plan | | Plan | |

($ millions) | | Budget(1) | | Forecast | | 2009/10 | | 2010/11 | | 2011/12 | |

Office of the Premier | | 14 | | 14 | | 12 | | 12 | | 11 | |

Aboriginal Relations and Reconciliation | | 62 | | 62 | | 51 | | 47 | | 46 | |

Advanced Education and Labour Market Development | | 2,075 | | 2,056 | | 2,260 | | 2,262 | | 2,237 | |

Agriculture and Lands | | 289 | | 249 | | 298 | | 232 | | 230 | |

Attorney General | | 546 | | 546 | | 556 | | 549 | | 534 | |

Children and Family Development | | 1,389 | | 1,389 | | 1,403 | | 1,414 | | 1,414 | |

Community Development | | 238 | | 238 | | 197 | | 182 | | 234 | |

Education | | 5,117 | | 5,115 | | 5,179 | | 5,215 | | 5,231 | |

Energy, Mines and Petroleum Resources | | 73 | | 72 | | 73 | | 50 | | 55 | |

Environment | | 263 | | 251 | | 239 | | 237 | | 234 | |

Finance | | 234 | | 231 | | 153 | | 116 | | 104 | |

Forests and Range | | 806 | | 770 | | 768 | | 692 | | 696 | |

Health Services | | 13,329 | | 13,329 | | 14,095 | | 14,901 | | 15,821 | |

Healthy Living and Sport | | 72 | | 66 | | 71 | | 71 | | 72 | |

Housing and Social Development | | 2,602 | | 2,602 | | 2,641 | | 2,651 | | 2,617 | |

Labour and Citizens’ Services | | 102 | | 102 | | 78 | | 73 | | 64 | |

Public Safety and Solicitor General | | 624 | | 624 | | 647 | | 630 | | 625 | |

Small Business, Technology and Economic Development | | 67 | | 67 | | 85 | | 79 | | 79 | |

Tourism, Culture and the Arts | | 353 | | 349 | | 55 | | 51 | | 51 | |

Transportation and Infrastructure | | 771 | | 771 | | 766 | | 790 | | 844 | |

Total ministries and Office of the Premier | | 29,026 | | 28,903 | | 29,627 | | 30,254 | | 31,199 | |

Management of public funds and debt | | 1,262 | | 1,212 | | 1,200 | | 1,292 | | 1,330 | |

Contingencies | | 342 | | 342 | | 385 | | 300 | | 250 | |

Funding for capital expenditures | | 972 | | 899 | | 1,323 | | 1,347 | | 1,017 | |

Legislative and other appropriations | | 137 | | 137 | | 165 | | 127 | | 125 | |

Subtotal | | 31,739 | | 31,493 | | 32,700 | | 33,320 | | 33,921 | |

Priority spending initiatives | | — | | 622 | | — | | — | | — | |

Consolidated revenue fund total expense | | 31,739 | | 32,115 | | 32,700 | | 33,320 | | 33,921 | |

Expenses recovered from external entities | | 1,892 | | 2,193 | | 2,402 | | 2,385 | | 2,450 | |

Externally-funded service delivery agency expense: | | | | | | | | | | | |

School districts | | 301 | | 268 | | 273 | | 296 | | 329 | |

Post-secondary institutions | | 2,185 | | 2,174 | | 2,176 | | 2,378 | | 2,564 | |

Health authorities and hospital societies | | 427 | | 520 | | 686 | | 653 | | 727 | |

Other service delivery agencies | | 1,146 | | 1,135 | | 1,070 | | 1,133 | | 1,441 | |

| | 4,059 | | 4,097 | | 4,205 | | 4,460 | | 5,061 | |

Subtotal expense | | 37,690 | | 38,405 | | 39,307 | | 40,165 | | 41,432 | |

Further efficiencies | | — | | — | | — | | (125 | ) | (250 | ) |

Total expense | | 37,690 | | 38,405 | | 39,307 | | 40,040 | | 41,182 | |

(1) The 2008/09 budget estimate and revised forecast have been restated to reflect government’s current organization and accounting policies.

Budget and Fiscal Plan – 2009/10 to 2011/12

11

Three-year Fiscal Plan

Taxpayer-supported debt is forecast to increase to $34.1 billion by 2011/12, reflecting the significant infrastructure investments planned over the next three years that will benefit future generations of British Columbians, and the forecast deficits over the next two fiscal years. Total provincial debt, which includes commercial Crown agency debt, is forecast to increase over the next three years to $47.2 billion by 2011/12, primarily reflecting additional investment in improving and expanding British Columbia’s hydro generation assets.

Significant progress has been made in reducing the taxpayer supported debt burden over the past six years. The taxpayer-supported debt to GDP ratio has declined from 21.3 per cent in 2002/03 to 13.8 per cent by 2008/09, a 35 per cent reduction. Due to significant infrastructure investments and weaker economic growth, the taxpayer- supported debt to GDP ratio is forecast to increase from 13.8 per cent in 2008/09 to 15.8 per cent in 2011/12. Debt remains affordable, despite the global economic downturn. Additional information on the debt outlook is found starting on page 40.

Chart 1.2 Taxpayer-supported debt burden remains low

The main risks to the government fiscal plan include a protracted period of low economic growth in the US, reduced global demand for BC’s exports, continuing turmoil in global financial markets, and further weakening of domestic demand. Other risks include exchange rate movements or changes in natural gas, lumber or other commodity markets, as well as service demand pressures on the expenditure side. These and other risks are more fully described starting on page 43.

The fiscal plan includes contingencies of $385 million in 2009/10, $300 million in 2010/11 and $250 million in 2011/12 to help ensure the fiscal targets are met. In addition, government will continue to review its operations to achieve a further $250 million in annual efficiencies by the end of 2011/12. The budget provides no funding for annual wage increases in the next round of public sector bargaining.

The three-year fiscal plan conforms to the standards set by the accounting profession for senior governments in Canada referred to as generally accepted accounting principles or “GAAP”.

Budget and Fiscal Plan – 2009/10 to 2011/12

12

Three-year Fiscal Plan

Revenue

Changes since the first Quarterly Report

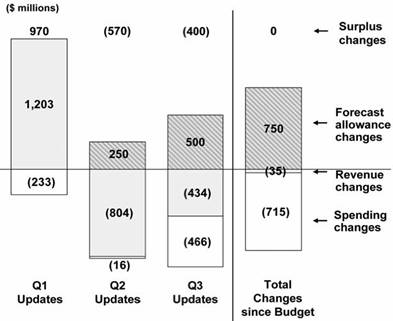

Since the updated fiscal plan released September 12, 2008 in the 2009 Budget Consultation Paper, the revenue forecast has declined $1.2 billion, $2.1 billion, $2.0 billion and $1.7 billion in the four years 2008/09 to 2011/12, respectively. Changes to the 2008/09 revenue forecast are detailed in Part 4: 2008/09 Revised Financial Forecast (third Quarterly Report).

Chart 1.3 Three-year cumulative change in revenue since the first Quarterly Report

* Excludes $870 million in funding for the LMDA transfer

The economic downturn resulted in a reduction of $6.6 billion in revenue over the fiscal plan period since the September Budget Consultation Paper. This loss was partially offset by $870 million in federal funding in support of the Labour Market Development Agreement, resulting in a net decrease in revenue of $5.8 billion. The cumulative $5.8 billion revenue loss over the next three years reflects decreases

Chart 1.4 Nominal GDP changes

Budget and Fiscal Plan – 2009/10 to 2011/12

13

Three-year Fiscal Plan

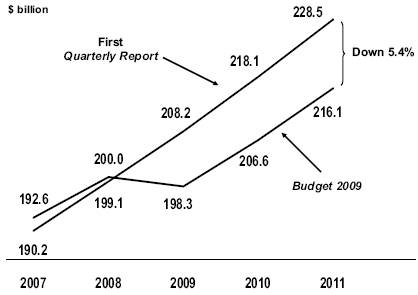

in taxation, natural resource and other revenue sources, partially offset by improvements in federal government transfers and commercial Crown corporation net income. The global economic slowdown combined with the financial market crisis and equity market disruptions have contributed to a significant decline in the BC economic outlook. The level of nominal Gross Domestic Product in 2011 is now projected to be 5.4 per cent lower than forecast in the first Quarterly Report. This loss in economic output, combined with the effects of accelerated tax cuts, results in a $4.0 billion cumulative reduction in taxation revenues over the three years. Weaker economic growth affects virtually all taxation revenue sources and in particular, the cumulative three-year loss from personal income, corporate income, social service, carbon and property transfer tax revenues totals $3.5 billion.

Chart 1.5 Taxation revenue changes

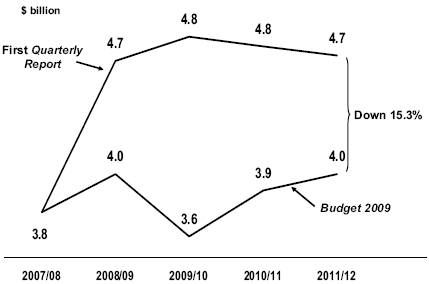

Plunging commodity prices and the fallout in the US housing sector are major contributors to the three-year total loss of $2.8 billion in natural resource revenues.

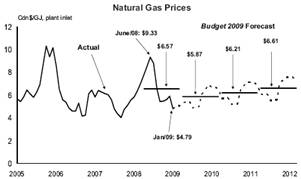

Chart 1.6 Change in natural gas prices

Budget and Fiscal Plan – 2009/10 to 2011/12

14

Three-year Fiscal Plan

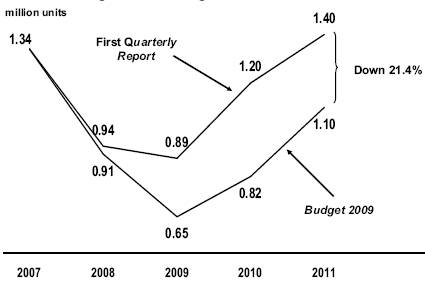

Chart 1.7 Change in US housing starts

Lower natural gas prices, disruptions in capital markets and a reduced expectation of the average bonus bid per hectare result in a $1.5 billion reduction from natural gas royalties and revenue of sales of Crown land tenures over the three years ending 2011/12. Volatility in other commodity markets including lumber, pulp, coal, metals, oil and electricity contribute to a further $1.4 billion revenue decline.

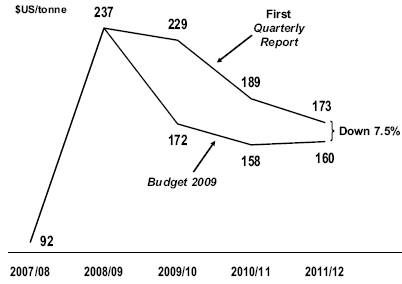

Chart 1.8 Change in coal prices

Budget and Fiscal Plan – 2009/10 to 2011/12

15

Three-year Fiscal Plan

Chart 1.9 Change in natural resource revenue

Excluding the $870 million in support of the Labour Market Development Agreement, the $0.2 billion improvement over the three years from federal government contributions mainly reflects increases in program recoveries from ministries and taxpayer supported Crown corporations. Since these transfers represent both higher revenues and expenses, there is no impact on government’s bottom line. These recoveries include $69 million for additional agricultural programs, $24 million in added support to the Ministry of Children and Family Development and $110 million directed to taxpayer supported Crown agencies.

The three-year $0.3 billion decline in other taxpayer-supported sources includes reduced revenue from the school, university, college and health authority (SUCH) sector and $183 million resulting from decommissioning the Coquihalla highway toll booths.

Higher net incomes from the commercial Crown corporations mainly reflect increased sales from the Liquor Distribution Branch, timing of BC Railway Company asset dispositions and an improved rate of return from BC Hydro.

Budget and Fiscal Plan – 2009/10 to 2011/12

16

Three-Year Fiscal Plan

Table 1.5 Major Factors Underlying Revenue

Calendar Year | | Budget 2009 | | First Quarterly Report | |

Per cent growth unless otherwise indicated | | 2008 | | 2009 | | 2010 | | 2011 | | 2008 | | 2009 | | 2010 | | 2011 | |

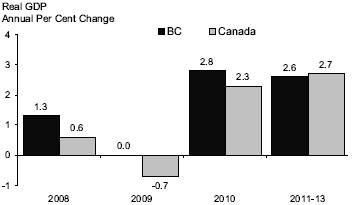

Real GDP | | 1.0 | | -0.9 | | 2.4 | | 2.6 | | 1.7 | | 2.3 | | 2.9 | | 2.8 | |

Nominal GDP | | 3.9 | | -0.9 | | 4.2 | | 4.6 | | 4.7 | | 4.6 | | 4.8 | | 4.8 | |

Personal income | | 5.1 | | 1.7 | | 3.5 | | 4.3 | | 5.5 | | 4.3 | | 4.5 | | 4.5 | |

Corporate profits | | -4.0 | | -24.7 | | 1.5 | | 3.2 | | -1.6 | | 1.7 | | 4.3 | | 4.5 | |

Consumer expenditures | | 3.7 | | 1.9 | | 4.8 | | 4.7 | | 4.8 | | 4.9 | | 5.1 | | 5.0 | |

Consumer expenditures on durable goods | | -5.1 | | 0.3 | | 2.3 | | 2.5 | | -1.0 | | 3.2 | | 2.7 | | 2.8 | |

Business investment | | 4.6 | | -0.5 | | 5.4 | | 4.8 | | 4.6 | | 3.4 | | 5.1 | | 5.6 | |

Retail sales | | 1.5 | | 1.3 | | 4.4 | | 4.4 | | 3.2 | | 4.7 | | 4.9 | | 4.9 | |

Employment | | 2.1 | | -0.5 | | 1.3 | | 1.5 | | 2.5 | | 1.7 | | 1.7 | | 1.6 | |

BC housing starts | | -12.4 | | -25.6 | | 4.9 | | 3.8 | | -5.4 | | -11.2 | | -4.3 | | -1.4 | |

| | | | | | | | | | | | | | | | | |

US housing starts | | -32.7 | | -28.0 | | 25.4 | | 35.0 | | -29.9 | | -5.3 | | 34.8 | | 16.7 | |

SPF 2x4 price ($US/thousand board feet) | | $ | 219 | | $ | 213 | | $ | 250 | | $ | 300 | | $ | 237 | | $ | 250 | | $ | 300 | | $ | 300 | |

Pulp ($US/tonne) | | $ | 851 | | $ | 606 | | $ | 650 | | $ | 700 | | $ | 882 | | $ | 850 | | $ | 825 | | $ | 800 | |

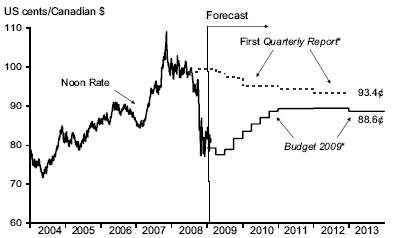

Exchange rate (US cents/Canadian dollar) | | 93.7 | | 79.3 | | 86.2 | | 89.4 | | 99.3 | | 98.2 | | 95.1 | | 94.4 | |

Fiscal Year | | 2008/09 | | 2009/10 | | 2010/11 | | 2011/12 | | 2008/09 | | 2009/10 | | 2010/11 | | 2011/12 | |

Natural gas price ($Cdn/GJ at plant inlet) | | $ | 6.57 | | $ | 5.87 | | $ | 6.21 | | $ | 6.61 | | $ | 7.58 | | $ | 7.27 | | $ | 6.86 | | $ | 6.67 | |

Bonus bids average bid price per hectare ($) | | $ | 3,659 | | $ | 794 | | $ | 954 | | $ | 1,226 | | $ | 4,299 | | $ | 1,010 | | $ | 1,082 | | $ | 1,173 | |

Electricity price ($US/mega-watt hour, Mid-C) | | $ | 61 | | $ | 61 | | $ | 67 | | $ | 67 | | $ | 81 | | $ | 76 | | $ | 74 | | $ | 75 | |

Metallurgical coal price ($US/tonne, fob west coast) | | $ | 237 | | $ | 172 | | $ | 158 | | $ | 160 | | $ | 237 | | $ | 229 | | $ | 189 | | $ | 173 | |

Copper price ($US/lb) | | $ | 2.65 | | $ | 1.73 | | $ | 2.44 | | $ | 2.38 | | $ | 3.56 | | $ | 3.23 | | $ | 2.93 | | $ | 2.58 | |

Crown harvest volumes (million cubic metres) | | 51.0 | | 52.0 | | 55.0 | | 60.0 | | 52.0 | | 54.0 | | 60.0 | | 63.0 | |

Budget 2009 Plan

Government revenue includes the combined revenues of the Consolidated Revenue Fund (CRF), taxpayer-supported Crown agencies, the SUCH sector, and the net income of commercial Crown corporations.

Following growth of 3.4 per cent in 2007/08, revenue is forecast to decline 3.5 per cent to total $38.5 billion in 2008/09. The 2008/09 revised forecast incorporates the impacts of slowing economic growth in 2008; and tax measures introduced in Budget 2007, Budget 2008, and Budget 2009 as well as accelerated tax cuts announced on October 22, 2008 designed to improve competitiveness and reduce costs for families and businesses. The 2008/09 revenue projection also includes the impacts of volatile commodity markets with increasing revenue from natural gas royalties, sales of Crown land tenures and coal production, partially offset by a 46 per cent decline in forest revenue.

In 2009/10, revenue growth of 0.9 per cent reflects a 7.7 per cent increase in federal government contributions and a 2.5 per cent increase in other taxpayer supported revenue sources, partially offset by the impacts of a 0.9 per cent decline in nominal GDP growth, falling natural gas prices and the full-year effect of reducing corporate income tax rates. More than half of the increasing federal government transfers represent additional funding in support of higher expenses under the Labour Market Development Agreement, agricultural programs and taxpayer supported Crown agencies.

Over the next two years as economic growth strengthens and commodity prices rise, due in part to an improving US economic outlook, revenue is expected to average 3.0 per cent annual growth.

Budget and Fiscal Plan – 2009/10 to 2011/12

17

Three-Year Fiscal Plan

Chart 1.10 Revenue forecast

Key assumptions and sensitivities relating to revenue are provided in Appendix Table A10. The major revenue components are:

· Personal income tax – up 5.5 per cent in 2009/10, and rising to 5.8 per cent and 6.1 per cent over the next two years.

Over the four years, revenue includes the effects of $2.6 billion of tax reductions provided to BC residents in the 2007 and 2008 budgets. Adding back the tax measures, base revenue is forecast to average 4.8 per cent annual growth over the next three years, consistent with Budget 2009 projections of personal and labour incomes. For full details on tax initiatives, see Part 2: Tax Measures.

Table 1.6 Personal Income Tax Revenue

($ millions) | | 2008/09 | | 2009/10 | | 2010/11 | | 2011/12 | |

Budget 2009 revenue | | 6,219 | | 6,562 | | 6,942 | | 7,366 | |

Budget 2009 measures – dividend tax credits | | — | | (8 | ) | (32 | ) | (32 | ) |

Budget 2008 measures | | | | | | | | | |

– carbon tax recycling | | 320 | | 365 | | 377 | | 404 | |

– Other measures | | (6 | ) | (41 | ) | (43 | ) | (46 | ) |

Budget 2007measures – tax cuts in 2008 | | 273 | | 282 | | 298 | | 316 | |

Federal government measures | | 11 | | 4 | | 11 | | 11 | |

Prior-year adjustment | | 151 | | — | | — | | — | |

Base personal income tax revenue | | 6,968 | | 7,164 | | 7,553 | | 8,019 | |

Annual growth | | 4.9 | % | 2.8 | % | 5.4 | % | 6.2 | % |

Personal income growth (calendar year) | | 5.1 | % | 1.7 | % | 3.5 | % | 4.3 | % |

Labour income growth (calendar year) | | 5.8 | % | 1.2 | % | 3.8 | % | 5.0 | % |

Elasticity (1) (calendar year basis, policy neutral) | | 1.0 | | 1.3 | | 1.4 | | 1.4 | |

(1) Percent growth in current year tax relative to per cent growth in personal income.

Budget and Fiscal Plan – 2009/10 to 2011/12

18

Three-Year Fiscal Plan

· Corporate income tax – declining $508 million or 25 per cent in 2009/10 reflecting a slowing economy; the full-year impact of tax cuts implemented in July and December 2008; and a lower settlement payment in respect of prior years. Revenue continues to decline over the next two years due to overpayments from the federal government in 2009 and 2010; and general rate reductions in 2010 and 2011 supporting the 2009/10 Revenue Neutral Carbon Tax Plan. For more details on carbon tax recycling, see the Revenue Neutral Carbon Tax topic box on page 72.

Table 1.7 Corporate Income Tax Revenue

($ millions) | | 2008/09 | | 2009/10 | | 2010/11 | | 2011/12 | |

Advance instalments from the federal government: | | | | | | | | | |

– Payment share | | 10.0 | % | 12.1 | % | 11.7 | % | 10.8 | % |

– Advances | | 1,386 | | 1,302 | | 1,257 | | 1,209 | |

International Financial Activity Act refunds | | (20 | ) | (20 | ) | (20 | ) | (20 | ) |

Prior-year adjustment | | 671 | | 247 | | (165 | ) | (266 | ) |

| | | | | | | | | |

Corporate income tax revenue | | 2,037 | | 1,529 | | 1,072 | | 923 | |

| | | | | | | | | |

Annual per cent growth | | -9.5 | % | -24.9 | % | -29.9 | % | -13.9 | % |

· Social Service tax — after incorporating measures introduced in Budget 2009, annual growth is forecast to average 3.4 per cent over the next three years, lower than recent history and consistent with the revised outlook of consumer and business spending and overall economic growth. For full details on tax initiatives, see Part 2: Tax Measures.

Table 1.8 Social Service Tax Revenue

($ millions) | | 2008/09 | | 2009/10 | | 2010/11 | | 2011/12 | |

Base revenue | | 4,998 | | 5,102 | | 5,317 | | 5,543 | |

Budget 2009 measures | | — | | (15 | ) | (18 | ) | (10 | ) |

Budget 2009 revenue | | 4,998 | | 5,087 | | 5,299 | | 5,533 | |

Annual growth | | -1.5 | % | 1.8 | % | 4.2 | % | 4.4 | % |

Annual per cent change (calendar year) | | | | | |

Personal consumption | | 3.7 | % | 1.9 | % | 4.8 | % | 4.7 | % |

Business investment | | 4.6 | % | -0.5 | % | 5.4 | % | 4.8 | % |

Nominal GDP | | 3.9 | % | -0.9 | % | 4.2 | % | 4.6 | % |

· Carbon tax – as announced in Budget 2008, the carbon tax rate per tonne of CO2-equivalent will increase by $5 each year to $25 per tonne in 2011/12. The forecast assumes that purchased volumes of natural gas will continue to grow by 2.0 per cent while consumption of gasoline is expected to be flat over the next three years. Revenue is expected to increase in line with these higher rates and assumed volume growth. By law, carbon tax revenue is fully returned to taxpayers through tax reductions. For more details on carbon tax recycling, see the Revenue Neutral Carbon Tax topic box on page 72.

· Property tax – revenue is expected to average 2.2 per cent annual growth over the fiscal plan and includes the effects of an Industrial Property Tax Credit for light and major industrial properties announced on October 22, 2008; and other tax measures including the northern and rural homeowner benefit announced in Budget 2009. These tax cuts are included in the 2009/10 Revenue Neutral Carbon Tax Plan. For full details on tax initiatives, see Part 2: Tax Measures.

Budget and Fiscal Plan – 2009/10 to 2011/12

19

Three-Year Fiscal Plan

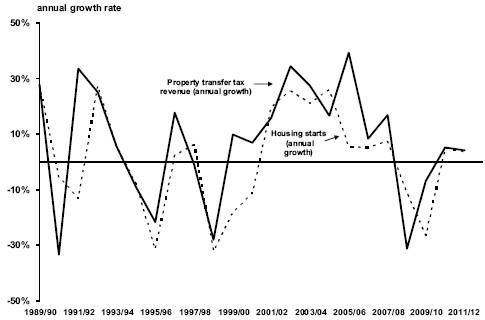

Chart 1.11 Property transfer tax

· Property transfer tax – consistent with the outlook for BC housing starts and expected moderation in the housing market, annual revenue growth is forecast to average 0.7 per cent over the next three years.

· Natural gas royalties – declines 26.3 per cent in 2009/10 due to lower natural gas prices and increasing production from wells qualifying for royalty programs and credits. Over the next two years, revenue is expected to increase as demand and average prices rise with an improving North American economy. The government continues to provide royalty programs and credits to foster industry investment in exploration and development. See Appendix Table A.11 for more details regarding natural gas price forecasts.

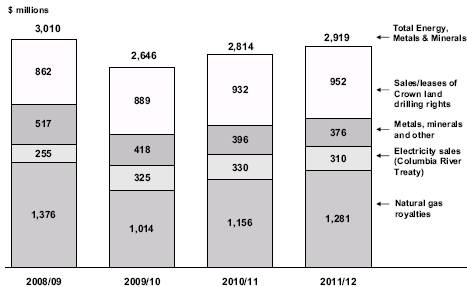

· Other energy, metals and minerals – average annual revenue growth from sales of Crown land tenures is forecast to be 3.4 per cent over the next three years as annual cash sales are recorded as revenue over eight years. Revenue from other

Chart 1.12 Revenue from energy metals and minerals

Budget and Fiscal Plan – 2009/10 to 2011/12

20

Three-Year Fiscal Plan

energy, metals and minerals falls in the next three years due to the effects of commodity prices, production volumes, the exchange rate and higher mining costs.

· Forests – in 2009/10, the impacts of the mountain pine beetle infestation, prevailing weak lumber prices and an anaemic US housing market are expected to continue to result in declining stumpage revenue. This is partially offset by increasing border tax revenues mainly resulting from a one-time $39 million refund to forest companies in 2008/09.

Over the next two years as prices and markets are expected to recover, stumpage revenue increases, partially offset by declining border tax revenues. Revenue is forecast to average 7.2 per cent annual growth, however by 2011/12, forests revenue is still expected to be significantly below recent historical levels.

· Health and social transfers – Over the next three years, revenue is expected to average 4.2 per cent annual growth reflecting national base growth, rising BC population share and incorporating partial protection from the federal government health transfer measures introduced in its recent budget on January 27, 2009.

Table 1.9 Health and Social Transfers

($ millions) | | 2008/09 | | 2009/10 | | 2010/11 | | 2011/12 | |

Canada Health Transfer (CHT) | | 3,168 | | 3,373 | | 3,536 | | 3,719 | |

Wait times | | — | | 33 | | 33 | | 33 | |

Health deferral | | 145 | | 68 | | 53 | | 23 | |

Canada Social Transfer (CST) | | 1,385 | | 1,436 | | 1,488 | | 1,541 | |

Prior-year adjustments | | (5 | ) | — | | — | | — | |

Total health and social transfers | | 4,693 | | 4,910 | | 5,110 | | 5,316 | |

Annual Change | | 79 | | 217 | | 200 | | 206 | |

| | 1.7 | % | 4.6 | % | 4.1 | % | 4.0 | % |

· Other federal contributions

· up $237 million or 19 per cent in 2009/10 mainly due to funding under the Labour Market Development Agreement for which the province administers programs and services previously provided by the federal government, aimed at helping Employment Insurance clients and the unemployed prepare for and obtain employment.

· declining $52 million in 2010/11 mainly reflecting the termination of funding for the Millennium Scholarship program in 2009/10.

Commercial Crown Corporation Net Income

· British Columbia Hydro and Power Authority – BC Hydro’s net income, based on meeting its allowed return on equity, is forecast at $452 million in 2009/10, $493 million in 2010/11 and $542 million in 2011/12 after regulatory account transfers. These transfers are used to mitigate the income risks of key assumptions such as water inflows, market prices and trade income.

The projections reflect increases in energy costs largely due to a greater proportion of requirements being met through imported energy and from new sources of supply generated by independent power producers. These sources result in higher energy costs than from power generated by Heritage resources which are operating at near maximum capacity. Maintenance requirements and additional borrowings for capital asset improvement programs are also increasing financing and amortization

Budget and Fiscal Plan – 2009/10 to 2011/12

21

Three-Year Fiscal Plan

expenses. These costs are driven by the need for major overhauls of ageing infrastructure and to address capacity constraints caused by demand load growth, reliability issues, and escalating construction costs.

While BC Hydro has incorporated rate increases into its projections, the rate increases are subject to approval by the BC Utilities Commission (BCUC) through the revenue requirements application process. In November 2008, BC Hydro filed its Final Argument for rate increases in 2008/09 and 2009/10. BCUC’s decision is expected in early 2009 (see Appendix Table A10 for rate assumptions).

· British Columbia Liquor Distribution Branch (LDB) – LDB’s net income is forecast at $896 million in 2009/10, $918 million in 2010/11 and $938 million in 2011/12. These projections reflect an increasing sales trend for spirits, wine and beer, and cost reductions resulting from operating efficiencies.

· British Columbia Lottery Corporation – BCLC’s net income (after payments to the federal government) is forecast at $1,154 million in 2009/10, $1,198 million in 2010/11 and $1,228 million in 2011/12. These projections reflect continued revenue growth mainly from casinos, community gaming centres and e-Gaming. Revenue from lotteries is also expected to increase, but at a more moderate pace.

A significant portion of provincial income from gaming is redistributed to charities and local governments. In Budget 2009, total distributions of gaming income are projected to increase from $263 million in 2008/09 to $280 million in 2011/12.

· British Columbia Railway Company – BCRC’s net income is forecast at $37 million in 2009, $32 million in 2010 and $0.2 million in 2011 reflecting the completion of surplus property sales at the end of 2010. BCRC will continue to operate the Port Subdivision (Robert’s Bank) as well as invest in the DeltaPort Berth 3 expansion project in support of government’s Pacific gateway and ports strategies.

· Insurance Corporation of British Columbia – ICBC’s net income is forecast at $260 million in 2009, $192 million in 2010 and $217 million in 2011. The projections reflect current assumptions for premiums including the full-year impact of a 3.0 per cent rate decrease on optional insurance, effective on July 1, 2008, and moderate growth in vehicles being insured. The projections also reflect lower investment income as a result of the decline in equity investment markets in 2008 and a return to historical claims trends.

Consolidated Revenue Fund Spending

Consolidated Revenue Fund (CRF) spending is forecast to increase from a revised forecast of $32.1 billion in 2008/09 to $33.9 billion by 2011/12 – a 5.6 per cent increase over the three year period.

Budget 2009 protects health care, education and social services on which BC families depend. To address the current economic challenges, Budget 2009 also provides support for communities and protection of the environment.

Government recognizes, and has acted on, the need to cut back in all areas of discretionary spending, just as British Columbia’s businesses and citizens are having to do in these difficult economic times. Budget 2009 achieves significant administrative savings while supporting direct services to the public in health care, education, social supports, and other priority services. A further review of programs throughout the public sector is planned over the next two years to achieve additional savings to again reach a balanced budget by 2011/12.

Budget and Fiscal Plan – 2009/10 to 2011/12

22

Three-Year Fiscal Plan

Protecting Health Care and Education

Health Care

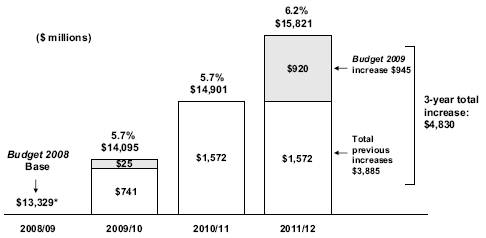

Budget 2009 confirms government’s commitment to health care and provides an additional $920 million for the Ministry of Health Services and health authorities in 2011/12, for an annual 6 per cent increase in funding for the third year of the fiscal plan. This funding is in addition to $3.9 billion over 3 years allocated previously in Budget 2008.

Chart 1.13 Ministry of Health Services budget increases

* Before $120 million Supplementary Estimates

Budget 2009 provides additional funding of $562 million to health authorities in 2011/12, an increase of 6 per cent from 2010/11. Funding for Ministry of Health Services programs including PharmaCare, Medical Services Plan, and Emergency Health Services, increases by $358 million in 2011/12.

Funding for the Ministry of Health Services and health authorities will support growth in beds, increased surgical procedures, improved access to services and new hospital facilities.

The Ministry’s budget includes $25 million in 2009/10 for the Lower Mainland Innovation and Integration Fund (LMIIF) to assist health authorities implement best practices and integrate and coordinate service delivery. This funding is in addition to the $50 million provided for the LMIIF in 2008/09.

To ensure that health services are protected in the current economic environment, the Ministry of Health Services and health authorities will be required to achieve efficiencies and administrative savings beginning in 2009/10. These savings will be re-directed to enhance health services.

· Collectively, health authorities will be required to achieve administrative savings of $25 million per year, approximately 2 per cent of the health authorities’ administration and support services costs. It is expected that a significant portion of these savings can be realized through innovation and lean-design approaches to health care delivery. Every dollar will be redirected to patient care.

Budget and Fiscal Plan – 2009/10 to 2011/12

23

Three-Year Fiscal Plan

· The Ministry will be required to achieve administrative savings of $48 million, of which $35 million will be redirected to health authorities to enhance patient care and the remaining $13 million will be allocated to establish a BC Family Residence Program for family members traveling to regional health centres.

Health spending by function includes all health care-related spending by the Ministry of Health Services and other ministries, including Healthy Living and Sport, Children and Family Development, and Housing and Social Development, as well as other service delivery agencies such as Canadian Blood Services. Health spending by function, on a summary basis, increases to $17.5 billion in 2011/12, up from $12.4 billion in 2005/06, a 41 per cent increase.

Post-Secondary Education

Budget 2009 is consistent with government’s commitment to increase access to post-secondary education and training throughout the province. At a time of global economic slowdown, government recognizes, more than ever, the importance of maintaining funding to this sector.

Budget 2009 provides $244 million in new operating funding, including $228 million to post-secondary institutions and $16 million to support immigrant workers, over three years. The post-secondary portion is comprised of:

· $165 million to further enhance general access to post-secondary educational opportunities in universities and colleges throughout BC.

· $40 million to expand health education programs to address health human resource shortages, including expanding the three-year Bachelor of Science in nursing, medical technology, and pharmacy.

· $23 million, starting in 2010/11, to fulfill the commitment to increase the number of doctors trained to address growing demands on the health care sector.

In recognition of the importance of BC’s industry training and apprenticeship system, government will maintain funding of $105 million per year to the Industry Training Authority for apprenticeship training spaces in public and private training institutions. By the end of 2009/10, government will have funded an additional 7,000 new apprenticeship spaces since 2007/08, allowing more apprentices to take their classroom training and complete their apprenticeships. Since 2001, funding for industry training has increased by 42 per cent and the number of apprentices and trainees in BC has more than doubled to an estimated 45,500 in 2008/09.

Collectively, public post-secondary institutions will be required to achieve administrative savings of $11 million per year. It is expected that these savings will be redirected to education and training within the institutions.

Post-secondary education spending by function, on a summary basis, increases to $4.8 billion in 2011/12, up from $3.9 billion in 2005/06, a 23 per cent increase.

Even during the current economic slowdown, skilled labour shortages remain a critical issue for BC employers. To remain competitive and address skills supply issues, BC must attract and retain a highly skilled workforce from other countries. Moreover, many immigrants face challenges in adapting their knowledge and integrating into the workforce.

Budget and Fiscal Plan – 2009/10 to 2011/12

24

Three-Year Fiscal Plan

Chart 1.14 Post-secondary funding

Budget 2009 includes new investments of $16 million over the next three years beginning in 2009/10 in the following initiatives that remove barriers to employment for BC’s immigrant workforce:

· To continue the Skills Connect for Immigrants and International Qualifications programs and leverage additional federal investments in these areas. Both programs address the barriers to full labour market participation that many immigrants face.

· Skills Connect provides immigrants with personal assessments and career planning to support skills upgrading, language enhancement and workplace experience opportunities in order to overcome barriers to employment.

· The International Qualifications program supports projects that remove systemic barriers that prevent skilled immigrants from finding employment in a career area related to their experience and training. Specific initiatives include strategies to improve recognition of foreign credentials and work-based language training.

On February 20, 2008 Canada and British Columbia signed a new Labour Market Development Agreement (LMDA). The LMDA provides BC with an investment of approximately $290 million annually for Employment Insurance (EI) Part II programs and services, which are designed to provide EI clients with appropriate training and support to help them prepare for, obtain and maintain employment. A separate new labour market agreement (LMA) totaling approximately $66 million per year for the next 5 years for non-EI eligible clients was also signed with the federal government at the same time. These two agreements enable the province to direct funding and programming to support BC’S short and long-term labour market challenges. The ministries of Advanced Education and Labour Market Development, Housing and Social Development and other ministries are working together to implement these agreements.

Stable Funding for K-12 Education

Budget 2009 maintains operating grant funding to school districts at previously announced funding levels. Over the next 3 years, while the total budget for K-12 education increases, enrolment is expected to decline, resulting in increasing levels of per pupil funding at the school district level.

Budget and Fiscal Plan – 2009/10 to 2011/12

25

Three-Year Fiscal Plan

Chart 1.15 Student enrolment and per pupil funding (public schools)

Collectively, school districts will be required to achieve administrative savings of $12 million per year. It is expected that these savings will be redirected to the classroom.

K–12 education spending by function, on a summary basis, increases to $5.8 billion in 2011/12, up from $4.8 billion in 2005/06, a 21 per cent increase.

Sustaining Social Services

Government is committed to ensuring that programs and services that enhance the quality of life for British Columbians in need are protected.

Table 1.10 Sustaining Social Services

($ millions) | | 2008/09 | | 2009/10 | | 2010/11 | | 2011/12 | | Total | |

Acquisition of social housing | | 30 | | — | | — | | — | | 30 | |

Children and Families | | | | | | | | | | | |

– Supporting families and children in care | | — | | 14 | | 13 | | 20 | | 47 | |

– Child care subsidies | | — | | 8 | | 8 | | 9 | | 25 | |

– Supporting children with special needs | | — | | 11 | | 13 | | 14 | | 38 | |

Subtotal | | — | | 33 | | 34 | | 43 | | 110 | |

Supporting adults with developmental disabilities | | — | | 19 | | 27 | | 27 | | 73 | |

Income assistance for individuals and families in need | | — | | 47 | | 47 | | 16 | | 110 | |

Policing and victim support | | — | | 20 | | 19 | | 19 | | 58 | |

Total | | 30 | | 119 | | 127 | | 105 | | 381 | |

Budget 2009 maintains previous funding commitments to implement new and expanded measures to help break the cycle of homelessness and support low income seniors and families. In 2008/09 the province intends to introduce supplementary estimates for $30 million to acquire and renovate rental properties including 4 single room occupancy (SRO) hotels in Vancouver and 4 hotels/motels throughout British Columbia. This new, year-end funding is part of a $36 million initiative to protect and

Budget and Fiscal Plan – 2009/10 to 2011/12

26

Three-Year Fiscal Plan

create housing involving 15 properties and utilizing $6 million in existing funding. In total, the provincial government has protected or created 45 properties since 2001 through multiple initiatives.

Budget 2009 continues to support families and communities to care for and protect vulnerable children and youth, and to support healthy child and family development, by providing $110 million over 3 years for priority programs and services, including:

· $47 million over 3 years to respond to the increasing acuity of needs and rising costs of supporting children in care and for preventative and family support services;

· $25 million over 3 years for the child care subsidy program. The program assists low and middle income families with the cost of child care; and

· $38 million over three years to support children and families with special needs.

Budget 2009 includes an additional $73 million over three years for programs and services to adults with developmental disabilities and their families. This funding will provide for continued access to community living services including respite care, residential placements and life skills training.

During this global economic downturn, more individuals and families will experience difficulty in paying for their basic living necessities and will require income assistance. Budget 2009 provides an additional $110 million over three years to support individuals and families in need of income assistance.

Budget 2009 provides $47 million over 3 years to fund RCMP salary, pension and operating cost increases and $11 million to fund increased costs related to providing financial assistance and benefits to victims and others who are impacted by violent crimes.

Supporting Communities and the Environment

Budget 2009 provides $479 million over four years to support economic activity in communities throughout the province during the economic downturn as well as to maintain BC as a leader in environmental protection.

Targeted new spending includes:

Supporting Communities

· In response to new types of petroleum resource development in North America, the province is investing $6 million over 3 years to support the strategic development of shale and tight gas resources in the northeast area of BC. This expenditure will assist in adding to BC’s natural gas potential.