Exhibit 99.8

Second Quarterly Report

Economic Outlook,

2012/13 Financial Update

&

Six Month Results

April — September 2012

National Library of Canada Cataloguing in Publication Data

British Columbia.

Budget and fiscal plan. — 2002/03/2004/05-

Annual.

Also available on the Internet.

Continues: British Columbia. Ministry of Finance and Corporate Relations. Budget ... reports. ISSN 1207-5841.

ISSN 1705-6071 = Budget and fiscal plan — British Columbia.

1. Budget — British Columbia — Periodicals. 2. British Columbia — Appropriations and expenditures — Periodicals.

I. British Columbia. Ministry of Finance. II. Title.

HJ12.B742 352.48’09711’05 C2003-960048-3

TABLE OF CONTENTS

2012/13 Second Quarterly Report | November 28, 2012 |

| |

Part One: Updated Financial Forecast | |

Introduction | 1 |

Revenue | 2 |

Expense | 4 |

Consolidated Revenue Fund spending | 4 |

Contingencies | 4 |

Spending recovered from third parties | 5 |

Operating transfers to service delivery agencies | 5 |

Service delivery agency spending | 5 |

Government employment (FTEs) | 5 |

Provincial capital spending | 6 |

Provincial debt | 7 |

Risks to the fiscal forecast | 8 |

Supplementary schedules | 8 |

Tables: | |

1.1 | 2012/13 Forecast Update | 1 |

1.2 | 2012/13 Notional Allocations to Contingencies | 4 |

1.3 | 2012/13 Capital Spending Update | 6 |

1.4 | 2012/13 Provincial Debt Update | 7 |

| |

Financial results for the six months Ended September 30, 2012, and 2012/13 full-year forecast | |

1.5 | Operating Statement | 8 |

1.6 | 2012/13 Forecast — Changes from Budget 2012 | 9 |

1.7 | Revenue by Source | 10 |

1.8 | Expense by Ministry, Program and Agency | 11 |

1.9 | Expense by Function | 12 |

1.10 | Material Assumptions — Revenue | 13 |

1.11 | Material Assumptions — Expense | 18 |

1.12 | Full-Time Equivalents | 20 |

1.13 | Capital Spending | 20 |

1.14 | Capital Spending Projects Greater Than $50 Million | 21 |

1.15 | Provincial Debt | 23 |

1.16 | Statement of Financial Position | 24 |

| | | |

Second Quarterly Report 2012/13

Table of Contents

Part Two: Economic Review and Outlook | |

Summary | 25 |

BC Outlook — Economic Forecast Council projections | 25 |

British Columbia economic activity | 26 |

Labour market | 26 |

Consumer spending and housing | 27 |

External trade and commodity markets | 28 |

Risks to the outlook | 29 |

External environment | 30 |

United States | 30 |

Canada | 32 |

Europe | 34 |

China | 35 |

Financial markets | 35 |

| |

Tables: | |

2.1 | British Columbia Economic Indicators | 26 |

2.2 | Private Sector Canadian Interest Rate Forecasts | 36 |

2.3 | Private Sector Exchange Rate Forecasts | 37 |

| |

Topic Box: | |

Provincial Economic Accounts Update | 38 |

Second Quarterly Report 2012/13

ii

PART ONE — UPDATED FINANCIAL FORECAST

2012/13 Second Quarterly Report | November 28, 2012 |

Introduction

Table 1.1 2012/13 Forecast Update

| | | | First | | Second | |

| | Budget | | Quarterly | | Quarterly | |

($ millions) | | 2012 | | Report | | Report | |

Revenue | | 43,101 | | 42,724 | | 42,522 | |

Expense | | (43,869 | ) | (43,956 | ) | (43,956 | ) |

Manage impact of natural gas royalty reductions | | — | | 241 | | 65 | |

Deficit before forecast allowance | | (768 | ) | (991 | ) | (1,369 | ) |

Forecast allowance | | (200 | ) | (150 | ) | (100 | ) |

Deficit | | (968 | ) | (1,141 | ) | (1,469 | ) |

Capital spending: | | | | | | | |

Taxpayer-supported capital spending | | 3,757 | | 3,715 | | 3,744 | |

Self-supported capital spending | | 3,346 | | 3,194 | | 3,207 | |

| | 7,103 | | 6,909 | | 6,951 | |

Provincial Debt: | | | | | | | |

Taxpayer-supported debt | | 38,736 | | 38,679 | | 38,474 | |

Self-supported debt | | 18,667 | | 17,907 | | 17,782 | |

Total debt (including forecast allowance) | | 57,603 | | 56,736 | | 56,356 | |

Taxpayer-supported debt-to-GDP ratio: | | | | | | | |

As previously forecast | | 17.6 | % | 17.4 | % | | |

Impact of Statistics Canada methodology change (1) | | -0.4 | % | -0.3 | % | | |

Restated and second quarter projections | | 17.2 | % | 17.1 | % | 17.0 | % |

| | 2012 | |

Economic Forecast: | | | | | | | |

Real GDP growth | | 1.8 | % | 2.0 | % | 2.0 | % |

Nominal GDP growth | | 3.7 | % | 3.9 | % | 3.9 | % |

(1) See Provincial Accounts topic box on page 38.

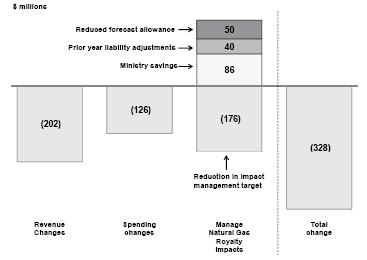

The second quarter fiscal outlook for 2012/13 projects a revised deficit of $1.5 billion. The $328 million deterioration since the first Quarterly Report is primarily due to the delay in the sale of the Little Mountain property.

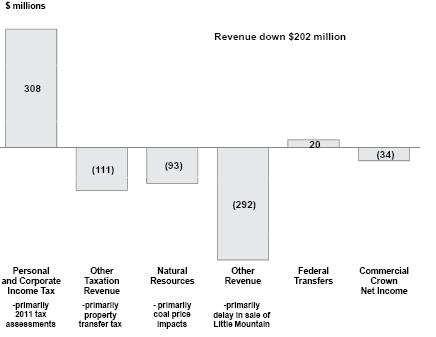

Overall revenue is down $202 million. The impact of the Little Mountain sale delay plus lower income from property transfer tax, natural resources and commercial Crown corporations is partially offset by higher personal and corporate income tax revenue.

Chart 1.1 Operating changes from the first Quarterly Report

Second Quarterly Report 2012/13

Updated Financial Forecast

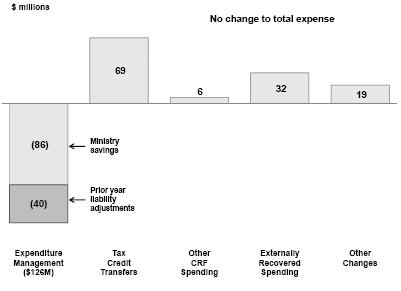

Expenditure management results, including ministry savings and prior year liability adjustments, were offset by higher tax credit transfers, additional spending associated with third party funding and other expense increases. As a result, projected overall government spending for 2012/13 is unchanged since the first Quarterly Report.

The $126 million in expenditure management savings plus a $50 million reduction in the forecast allowance enabled government to achieve $176 million of the $241 million needed to manage the impact of natural gas royalty reductions, leaving $65 million to be found in the remainder of the fiscal year.

Capital spending has increased slightly due to new project approvals and accelerations. Elsewhere in the capital plan, government has achieved $262 million in reduced spending against the capital plan adjustments identified in the first Quarterly Report, leaving $146 million remaining to be found.

Taxpayer-supported debt is down $205 million since the first Quarterly Report, reflecting lower borrowing for operating purposes. As a result the taxpayer-supported debt to GDP ratio is now 17.0 per cent — a 0.1 percentage point reduction from the previous forecast.

Revenue

The 2012/13 revised revenue forecast incorporates year-to-date results for the first six months, updated personal and corporate income tax assessment information from the federal government for 2011 and prior years, and revised forecasts from ministries, the federal government, service delivery agencies and commercial Crown corporations.

Chart 1.2 Main revenue changes from the first Quarterly Report

Second Quarterly Report 2012/13

2

Updated Financial Forecast

Revenue in 2012/13 is projected to be $42.5 billion — $202 million lower than the first Quarterly Report and $579 million below the Budget 2012 forecast. The changes from the first Quarterly Report reflect lower revenue from natural resources, miscellaneous sources and net income from Crown corporations, partly offset by higher revenue from taxation sources and federal government contributions.

Detailed revenue projections are disclosed in Table 1.7, and key assumptions and sensitivities relating to revenue are provided in Table 1.10. Major changes from the first Quarterly Report include:

· Personal income tax revenue is up $283 million including a $151 million prior-year adjustment due to higher 2011 tax assessment reports. Higher 2011 tax assessments result in an improved 2012/13 tax base, increasing the forecast by a further $132 million.

· Corporate income tax revenue is up $25 million mainly due to stronger 2011 tax assessment results.

· Property tax revenue is down $13 million mainly reflecting lower 2012 property assessment results.

· Property transfer tax is down $95 million reflecting the weak housing market in the second quarter. Year to date results indicate annual declines in the average property sale price and the number of transactions.

· Revenue from coal, metals and minerals is down $93 million mainly due to rising mining costs and weaker coal sales reflecting lower coal prices and shipments.

· Forests revenue is up $3 million as higher recoveries and stumpage revenue resulting from improved interior stumpage rates and Crown harvest volumes, are partly offset by reduced border taxes collected under the Softwood Lumber Agreement 2006 and the effects of a higher Canadian dollar.

· Other revenue, comprised of revenue from fees, licenses, investment earnings and other miscellaneous sources, is down $292 million mainly due to the delay in the completion date of the sale of the Little Mountain property.

· Total federal government contributions are expected to be up $20 million mainly due to higher direct transfers to taxpayer supported Crown corporations and the SUCH sector.

· The outlook for commercial Crown corporation net income is $34 million lower than the first Quarterly Report and $90 million lower than budget. The changes from the first Quarterly Report mainly reflect a lower allowed return on deemed equity for BC Hydro (the corporation’s allowed return is based on the pre-tax return of the closest comparative utility regulated by the BC Utilities Commission), higher claims costs incurred by ICBC, and lower gains from the sale of BC Rail assets.

Second Quarterly Report 2012/13

3

Updated Financial Forecast

Expense

There is no change to overall projected government spending in 2012/13 compared to the forecast in the first Quarterly Report, as savings from government’s expenditure management initiative were offset by spending increases in other areas.

Chart 1.3 Main expense changes from the first Quarterly Report

Consolidated Revenue Fund spending

Government’s expenditure management initiative has yielded $86 million in projected ministry savings. As well, a review of accrued liabilities resulted in a $40 million positive adjustment, mainly due to reduction in insurance liabilities in the Insurance and Risk Management Account.

Tax credit transfers were up $69 million as a consequence of the improvement in 2011 personal income tax assessments. Other CRF spending changes reflect higher emergency program flood-related and direct fire costs, partially offset by a reduction in debt servicing costs.

Contingencies

The notional allocations to the Contingencies vote are unchanged from the first Quarterly Report.

Table 1.2 2012/13 Notional Allocations to Contingencies

| | | | | | | | Q2 | |

| | | | First | | Second | | change | |

| | Budget | | Quarterly | | Quarterly | | from | |

($ millions) | | 2012 | | Report | | Report | | budget | |

2010 Sports and Arts Legacy | | 20 | | 20 | | 20 | | — | |

Climate Action and clean energy initiatives | | 40 | | 40 | | 40 | | — | |

Community Living BC anticipated caseload increases | | 12 | | 12 | | 12 | | — | |

Elections BC event-related funding | | 36 | | 15 | | 15 | | (21 | ) |

Subtotal notional allocations | | 108 | | 87 | | 87 | | (21 | ) |

Reserved for unforeseen pressures related to litigation, caseload, natural disasters, and other contingent items | | 192 | | 213 | | 213 | | 21 | |

Total contingencies | | 300 | | 300 | | 300 | | — | |

Second Quarterly Report 2012/13

4

Updated Financial Forecast

Government continues to face a variety of pressures over the three years of the plan which ministries and agencies will work to manage within existing budgets, with additional funding provided from the Contingencies vote as necessary.

Spending recovered from third parties

Spending funded by recoveries from third parties is projected to increase by $32 million in 2012/13 compared to the first Quarterly Report. The changes reflect:

· increased healthcare related cost recoveries (up $22 million), mainly associated with the medical service plan premiums collections;

· increased spending of gaming proceeds from the BC Lottery Corporation (up $6 million); and

· increased general government recoveries, including direct fire fighting (up $4 million).

The above spending changes are offset by an equal increase in revenue, and as a result have no net impact on the fiscal forecast.

Operating transfers to service delivery agencies

Operating transfers to service delivery agencies are forecasted to be $11 million higher in 2012/13 compared to the first Quarterly Report.

Service delivery agency spending

Service delivery agency spending is forecast to increase by $30 million in 2012/13 compared to the first Quarterly Report.

· School district spending is forecast to be $4 million higher due to an upward adjustment to estimated salary and benefit costs.

· Post secondary institution spending projections are unchanged from the first Quarterly Report.

· Health authority and hospital society spending is forecast to be up $24 million in 2012/13, reflecting the projected volume increases in the healthcare services delivered by these organizations on behalf of government. This spending increase is projected to be funded by additional provincial grants and own-source revenue.

· Other service delivery agency spending is projected to increase by $2 million in 2012/13 reflecting mostly higher spending on low income housing.

Detailed expense projections are disclosed in Table 1.8. Key spending assumptions and sensitivities are provided in Table 1.11.

Government employment (FTEs)

The projection of government employment for 2012/13 is unchanged from the first Quarterly Report. Further details on FTEs are provided in Appendix Table 1.12.

Second Quarterly Report 2012/13

5

Updated Financial Forecast

Provincial capital spending

Total capital spending is projected to be $7.0 billion in 2012/13 — $42 million higher than the first Quarterly Report but $152 million lower than budget.

Table 1.3 2012/13 Capital Spending Update

| | ($ millions) | |

2012/13 capital spending — Budget 2012 Fiscal Plan (February 21, 2012) | | 7,103 | | | | 7,103 | |

2012/13 capital spending — first Quarterly Report (September 13, 2012) | | | | 6,909 | | | |

| | Q1 | | Q2 | | Total | |

| | Update | | Update | | Changes | |

Taxpayer-supported changes: | | | | | | | |

Project approvals since Budget 2012 | | 91 | | 22 | | 113 | |

Additional externally funded capital spending by post-secondary institutions | | 53 | | 7 | | 60 | |

Project scheduling changes | | 222 | | (262 | ) | (40 | ) |

Capital planning adjustments | | (408 | ) | 262 | | (146 | ) |

Total taxpayer-supported | | (42 | ) | 29 | | (13 | ) |

Self-supported changes: | | | | | | | |

BC Hydro — mainly scheduling shift on Dawson Creek/Chetwynd and Northwest transmission line projects | | (165 | ) | — | | (165 | ) |

Transportation Investment Corp. — timing of capital spending for Port Mann Bridge/Highway 1 | | 20 | | 15 | | 35 | |

Other | | (7 | ) | (2 | ) | (9 | ) |

Total self-supported | | (152 | ) | 13 | | (139 | ) |

Total changes | | (194 | ) | 42 | | (152 | ) |

2012/13 capital spending — first Quarterly Report | | 6,909 | | | | | |

2012/13 capital spending — second Quarterly Report | | | | 6,951 | | 6,951 | |

Taxpayer-supported capital spending is projected to be $3.7 billion — $29 million higher than the first Quarterly Report. The changes include additional allocations for school district and health facility maintenance programs, additional investments in highway rehabilitation programs, and higher than expected spending on self-funded university projects.

The updated forecast also reflects $262 million in project scheduling changes to meet government’s capital planning adjustment target of $408 million, leaving $146 million to be realized over the remainder of the fiscal year.

Self-supported capital spending is projected to be $3.2 billion — $13 million higher than the first Quarterly Report but $139 million lower than budget. The changes from the first Quarterly Report mainly reflects the timing of capital spending on the Port Mann Bridge/Highway 1 project.

Details on capital spending are shown in Table 1.13, and capital spending projects with provincial contributions greater than $50 million are presented in Table 1.14.

Second Quarterly Report 2012/13

6

Updated Financial Forecast

Provincial debt

The provincial debt, including a $100 million forecast allowance, is projected to total $56.4 billion at March 31, 2013 — $380 million lower than the projection in the first Quarterly Report.

Table 1.4 2012/13 Provincial Debt Update

| | ($ millions) | |

2012/13 provincial debt — Budget 2012 Fiscal Plan (February 21, 2012) | | 57,603 | | | | 57,603 | |

2012/13 provincial debt — first Quarterly Report (September 13, 2012) | | | | 56,736 | | | |

| | Q1 | | Q2 | | Total | |

| | Update | | Update | | Changes | |

Taxpayer-supported changes: | | | | | | | |

Government operating: | | | | | | | |

– bonus bid cash proceeds | | 233 | | (9 | ) | 224 | |

– other CRF operating results | | (44 | ) | (196 | ) | (240 | ) |

Total operating debt changes | | 189 | | (205 | ) | (16 | ) |

Capital debt: | | | | | | | |

– lower spending in 2011/12 | | (217 | ) | — | | (217 | ) |

– other capital spending impacts | | 235 | | (171 | ) | 64 | |

– reduced provincial financing from capital planning adjustments | | (264 | ) | 171 | | (93 | ) |

Total capital debt changes | | (246 | ) | — | | (246 | ) |

Total taxpayer-supported | | (57 | ) | (205 | ) | (262 | ) |

Self-supported changes: | | | | | | | |

BC Hydro – mainly impact of working capital and lower capital spending projections | | (663 | ) | (196 | ) | (859 | ) |

Transportation Investment Corporation – impact of working capital changes | | (77 | ) | 18 | | (59 | ) |

Other changes | | (20 | ) | 53 | | 33 | |

Total self-supported | | (760 | ) | (125 | ) | (885 | ) |

Forecast allowance changes: | | | | | | | |

Adjustment to forecast allowance | | (50 | ) | (50 | ) | (100 | ) |

Total changes | | (867 | ) | (380 | ) | (1,247 | ) |

2012/13 provincial debt – first Quarterly Report | | 56,736 | | | | | |

2012/13 provincial debt – second Quarterly Report | | | | 56,356 | | 56,356 | |

Taxpayer-supported debt is projected at $38.5 billion — a $205 million decrease compared to the first Quarterly Report projection. The reduction is mainly due to an improved CRF cash position (related to bonus bid proceeds) and lower working capital requirements. The taxpayer-supported debt to GDP ratio forecast is projected to be 17.0 per cent — a 0.1 percentage point improvement from the first Quarterly Report.

The projected self-supported debt balance of $17.8 billion at March 31, 2013 is $125 million lower than the projection in the first Quarterly Report. Increased funding from internal sources has lowered financing requirements for capital infrastructure investments.

Total provincial debt includes a $100 million borrowing allowance to mirror the operating statement forecast allowance. This allowance is down $50 million from the first Quarterly Report as the risks to the forecast will have a reduced impact midway through the fiscal year.

Details on provincial debt are shown in Table 1.15.

Second Quarterly Report 2012/13

7

Updated Financial Forecast

Risks to the fiscal forecast

There are a number of risks and pressures to the fiscal plan, including slower than expected economic growth in our trading partners resulting in lower demand for BC’s exports, and continuing instability in financial markets brought about by the European sovereign debt crisis.

Revenues in British Columbia can be volatile, largely due to the influence of the cyclical nature of the natural resource sector in the economy. Changes in energy or commodity prices, such as natural gas and lumber, may have a significant effect on revenue and the fiscal forecast.

The spending forecast contained in the fiscal plan is based on ministry and service delivery agency plans and strategies. Changes to planning assumptions, such as utilization or demand rates for government services in the health care, education, or community social services sectors, represent the main spending risks.

These risks are covered by the $300 million Contingencies vote and the $100 million forecast allowance.

Supplementary schedules

The following tables provide the financial results for the six months ended September 30, 2012, and the 2012/13 full-year forecast.

Table 1.5 2012/13 Operating Statement

| | Year-to-Date to September 30 | | Full Year | |

| | 2012/13 | | Actual | | 2012/13 | | Actual | |

($ millions) | | Budget | | Actual | | Variance | | 2011/12 | | Budget | | Forecast | | Variance | | 2011/12 | |

Revenue | | 20,680 | | 20,959 | | 279 | | 20,591 | | 43,101 | | 42,522 | | (579 | ) | 41,967 | |

Expense | | (20,896 | ) | (20,311 | ) | 585 | | (21,406 | ) | (43,869 | ) | (43,956 | ) | (87 | ) | (43,807 | ) |

Manage impacts of natural gas royalty reductions | | — | | — | | — | | — | | — | | 65 | | 65 | | — | |

Surplus (deficit) before forecast allowance | | (216 | ) | 648 | | 864 | | (815 | ) | (768 | ) | (1,369 | ) | (601 | ) | (1,840 | ) |

Forecast allowance | | — | | — | | — | | — | | (200 | ) | (100 | ) | 100 | | — | |

Surplus (deficit) | | (216 | ) | 648 | | 864 | | (815 | ) | (968 | ) | (1,469 | ) | (501 | ) | (1,840 | ) |

Accumulated surplus beginning of the year | | 2,016 | | 2,476 | | 460 | | 4,293 | | 2,016 | | 2,434 | | 418 | | 4,274 | |

Accumulated surplus before comprehensive income | | 1,800 | | 3,124 | | 1,324 | | 3,478 | | 1,048 | | 965 | | (83 | ) | 2,434 | |

Accumulated other comprehensive income from self-supported Crown agencies | | 26 | | (29 | ) | (55 | ) | (61 | ) | 52 | | 153 | | 101 | | 23 | |

Accumulated surplus end of period | | 1,826 | | 3,095 | | 1,269 | | 3,417 | | 1,100 | | 1,118 | | 18 | | 2,457 | |

Second Quarterly Report 2012/13

8

Updated Financial Forecast

Table 1.6 2012/13 Forecast — Changes from Budget 2012

| | ($ millions) | |

2012/13 deficit — Budget 2012 Fiscal Plan (February 21, 2012) | | (968 | ) | | | (968 | ) |

2012/13 deficit — first Quarterly Report (September 13, 2012) | | | | (1,141 | ) | | |

| | Q1 | | Q2 | | Total | |

| | Update | | Update | | Changes | |

Revenue changes: | | | | | | | |

Personal income tax – mainly higher 2011 tax assessments | | (16 | ) | 283 | | 267 | |

Corporate income tax – increased federal government installments and higher 2011 tax assessments | | 20 | | 25 | | 45 | |

Property transfer tax – weaker year-to-date results | | — | | (95 | ) | (95 | ) |

Tobacco tax – weaker year-to-date results | | (10 | ) | — | | (10 | ) |

Other tax sources – mainly property and fuel taxes | | (9 | ) | (16 | ) | (25 | ) |

Natural gas royalties – reduced prices and volumes partly offset by savings from lower utilization of royatly and infrastructure programs | | (241 | ) | — | | (241 | ) |

Columbia River Treaty electricity sales – changes in electricity prices | | (33 | ) | 4 | | (29 | ) |

Coal, metals and minerals – mainly higher mining costs and lower prices | | (51 | ) | (93 | ) | (144 | ) |

Forests – mainly changes in stumpage revenue, border tax collections and recoveries | | 10 | | 3 | | 13 | |

Other natural resources – mainly lower Crown land tenures reflecting reduced average bid price and auctioned land base | | (18 | ) | (7 | ) | (25 | ) |

Fees, licenses, investment earnings and miscellaneous sources — mainly due to the delay in the completion date of the sale of the Little Mountain property | | 36 | | (292 | ) | (256 | ) |

Health and social transfers – changes in population share and lower national tax points reflecting lower national personal income tax base | | (65 | ) | (1 | ) | (66 | ) |

Other federal government transfers – mainly higher recoveries and SUCH sector income | | 56 | | 21 | | 77 | |

Commercial Crown agencies operating results: | | | | | | | |

BC Hydro – lower allowed return on deemed equity set by the BC Utilities Commission | | (46 | ) | (8 | ) | (54 | ) |

ICBC – mainly higher claims costs partially offset by higher revenue from premiums and investments | | 14 | | (19 | ) | (5 | ) |

Transportation Investment Corporation – mainly revised tolling framework for the Port Mann Bridge | | (24 | ) | — | | (24 | ) |

Other commercial Crown agencies changes | | — | | (7 | ) | (7 | ) |

Total revenue changes | | (377 | ) | (202 | ) | (579 | ) |

Less: expense increases (decreases): | | | | | | | |

Consolidated Revenue Fund changes: | | | | | | | |

Emergency program flood related costs | | 44 | | (1 | ) | 43 | |

Direct forest fire related costs | | 62 | | 13 | | 75 | |

Ministry savings due to expenditure management | | — | | (86 | ) | (86 | ) |

Prior year liability adjustments | | — | | (40 | ) | (40 | ) |

Management of public debt (net) – reflects lower interest rates and revisions to scheduled borrowing | | (69 | ) | (6 | ) | (75 | ) |

Tax credit transfers changes | | (34 | ) | 69 | | 35 | |

Spending funded by third party recoveries | | 117 | | 32 | | 149 | |

(Increase) decrease in operating transfers to service delivery agencies | | (215 | ) | (11 | ) | (226 | ) |

Changes in spending profile of service delivery agencies: | | | | | | | |

School districts – higher salaries and benefits costs | | 26 | | 4 | | 30 | |

Universities – lower salaries and benefits costs | | 2 | | (9 | ) | (7 | ) |

Colleges – spending related to higher student enrolment | | 14 | | 9 | | 23 | |

Health authorities and hospital societies – increasing demand for healthcare services | | 93 | | 24 | | 117 | |

Other service delivery agencies | | 47 | | 2 | | 49 | |

Total expense increases (decreases) | | 87 | | — | | 87 | |

Subtotal | | (464 | ) | (202 | ) | (666 | ) |

Manage impact of natural gas royalty reductions | | 241 | | (176 | ) | 65 | |

Reduction in forecast allowance | | 50 | | 50 | | 100 | |

Total changes | | (173 | ) | (328 | ) | (501 | ) |

2012/13 deficit – first Quarterly Report | | (1,141 | ) | | | | |

2012/13 deficit – second Quarterly Report | | | | (1,469 | ) | (1,469 | ) |

Second Quarterly Report 2012/13

9

Updated Financial Forecast

Table 1.7 2012/13 Revenue by Source

| | Year-to-Date to September 30 | | Full Year | |

| | 2012/13 | | Actual | | 2012/13 | | Actual | |

($ millions) | | Budget | | Actual | | Variance | | 2011/12 | | Budget | | Forecast | | Variance | | 2011/12 | |

Taxation | | | | | | | | | | | | | | | | | |

Personal income | | 3,255 | | 3,251 | | (4 | ) | 3,123 | | 6,630 | | 6,897 | | 267 | | 6,427 | |

Corporate income | | 976 | | 1,614 | | 638 | | 992 | | 2,266 | | 2,311 | | 45 | | 2,022 | |

Harmonized sales | | 3,021 | | 3,007 | | (14 | ) | 2,886 | | 6,003 | | 6,003 | | — | | 5,779 | |

Other sales (1) | | 49 | | 73 | | 24 | | 91 | | 98 | | 101 | | 3 | | 150 | |

Fuel | | 469 | | 475 | | 6 | | 475 | | 937 | | 929 | | (8 | ) | 928 | |

Carbon | | 501 | | 506 | | 5 | | 419 | | 1,172 | | 1,180 | | 8 | | 959 | |

Tobacco | | 347 | | 329 | | (18 | ) | 336 | | 652 | | 642 | | (10 | ) | 637 | |

Property | | 998 | | 987 | | (11 | ) | 941 | | 2,013 | | 1,985 | | (28 | ) | 1,913 | |

Property transfer | | 512 | | 467 | | (45 | ) | 562 | | 893 | | 798 | | (95 | ) | 944 | |

Other (2) | | 217 | | 221 | | 4 | | 204 | | 424 | | 424 | | — | | 406 | |

| | 10,345 | | 10,930 | | 585 | | 10,029 | | 21,088 | | 21,270 | | 182 | | 20,165 | |

Natural resources | | | | | | | | | | | | | | | | | |

Natural gas royalties | | 187 | | 45 | | (142 | ) | 196 | | 398 | | 157 | | (241 | ) | 339 | |

Forests | | 221 | | 234 | | 13 | | 196 | | 533 | | 546 | | 13 | | 482 | |

Other natural resource (3) | | 1,000 | | 931 | | (69 | ) | 997 | | 2,055 | | 1,857 | | (198 | ) | 1,991 | |

| | 1,408 | | 1,210 | | (198 | ) | 1,389 | | 2,986 | | 2,560 | | (426 | ) | 2,812 | |

Other revenue | | | | | | | | | | | | | | | | | |

Medical Services Plan premiums | | 1,012 | | 1,015 | | 3 | | 951 | | 2,047 | | 2,042 | | (5 | ) | 1,919 | |

Other fees (4) | | 1,288 | | 1,266 | | (22 | ) | 1,271 | | 2,876 | | 2,891 | | 15 | | 2,809 | |

Investment earnings | | 599 | | 519 | | (80 | ) | 585 | | 1,083 | | 1,069 | | (14 | ) | 1,042 | |

Miscellaneous (5) | | 1,301 | | 1,337 | | 36 | | 1,267 | | 3,047 | | 2,795 | | (252 | ) | 2,833 | |

| | 4,200 | | 4,137 | | (63 | ) | 4,074 | | 9,053 | | 8,797 | | (256 | ) | 8,603 | |

Contributions from the federal government | | | | | | | | | | | | | | | | | |

Health and social transfers | | 2,841 | | 2,825 | | (16 | ) | 2,699 | | 5,682 | | 5,616 | | (66 | ) | 5,384 | |

Harmonized sales tax transition payment | | — | | — | | — | | 580 | | — | | — | | — | | 580 | |

Other federal contributions (6) | | 690 | | 658 | | (32 | ) | 693 | | 1,575 | | 1,652 | | 77 | | 1,743 | |

| | 3,531 | | 3,483 | | (48 | ) | 3,972 | | 7,257 | | 7,268 | | 11 | | 7,707 | |

Commercial Crown corporation net income | | | | | | | | | | | | | | | | | |

BC Hydro | | 101 | | 128 | | 27 | | 155 | | 566 | | 512 | | (54 | ) | 558 | |

Liquor Distribution Branch | | 479 | | 486 | | 7 | | 475 | | 906 | | 906 | | — | | 909 | |

BC Lotteries (net of payments to the federal government) | | 556 | | 561 | | 5 | | 547 | | 1,115 | | 1,115 | | — | | 1,099 | |

ICBC | | 63 | | 24 | | (39 | ) | (57 | ) | 146 | | 141 | | (5 | ) | 102 | |

Transportation Investment Corporation (Port Mann) | | (19 | ) | (15 | ) | 4 | | (4 | ) | (48 | ) | (72 | ) | (24 | ) | (17 | ) |

Other | | 16 | | 15 | | (1 | ) | 11 | | 32 | | 25 | | (7 | ) | 29 | |

| | 1,196 | | 1,199 | | 3 | | 1,127 | | 2,717 | | 2,627 | | (90 | ) | 2,680 | |

Total revenue | | 20,680 | | 20,959 | | 279 | | 20,591 | | 43,101 | | 42,522 | | (579 | ) | 41,967 | |

(1) Includes social service tax, continuation of the tax on designated property and hotel room tax.

(2) Corporation capital and insurance premium taxes.

(3) Columbia River Treaty, other energy and minerals, water rental and other resources.

(4) Post-secondary, healthcare-related, motor vehicle, and other fees.

(5) Includes asset dispositions, reimbursements for health care and other services provided to external agencies, and other recoveries.

(6) Includes contributions for health, education, community development, housing and social service programs, and transportation projects.

Second Quarterly Report 2012/13

10

Updated Financial Forecast

Table 1.8 2012/13 Expense by Ministry, Program and Agency (1)

| | Year-to-Date to September 30 | | Full Year | |

| | 2012/13 | | Actual | | 2012/13 | | Actual | |

($ millions) | | Budget | | Actual | | Variance | | 2011/12 (2) | | Budget | | Forecast | | Variance | | 2011/12 (2) | |

Office of the Premier | | 4 | | 4 | | — | | 5 | | 9 | | 9 | | — | | 9 | |

Aboriginal Relations and Reconciliation | | 40 | | 36 | | (4 | ) | 40 | | 80 | | 80 | | — | | 92 | |

Advanced Education, Innovation and Technology | | 964 | | 955 | | (9 | ) | 961 | | 1,981 | | 1,981 | | — | | 1,977 | |

Agriculture | | 40 | | 42 | | 2 | | 43 | | 66 | | 66 | | — | | 74 | |

Children and Family Development | | 656 | | 644 | | (12 | ) | 652 | | 1,333 | | 1,331 | | (2 | ) | 1,332 | |

Citizens’ Services and Open Government | | 276 | | 243 | | (33 | ) | 266 | | 533 | | 532 | | (1 | ) | 562 | |

Community, Sport and Cultural Development | | 202 | | 184 | | (18 | ) | 182 | | 311 | | 311 | | — | | 404 | |

Education | | 2,723 | | 2,681 | | (42 | ) | 2,694 | | 5,315 | | 5,315 | | — | | 5,264 | |

Energy, Mines and Natural Gas | | 219 | | 250 | | 31 | | 205 | | 449 | | 449 | | — | | 453 | |

Environment | | 59 | | 60 | | 1 | | 60 | | 129 | | 128 | | (1 | ) | 143 | |

Finance | | 97 | | 73 | | (24 | ) | 53 | | 173 | | 172 | | (1 | ) | 189 | |

Forests, Lands and Natural Resource Operations | | 304 | | 326 | | 22 | | 289 | | 602 | | 671 | | 69 | | 562 | |

Health | | 7,971 | | 7,835 | | (136 | ) | 7,555 | | 16,180 | | 16,115 | | (65 | ) | 15,567 | |

Jobs, Tourism and Skills Training | | 109 | | 122 | | 13 | | 91 | | 232 | | 230 | | (2 | ) | 261 | |

Justice | | 552 | | 553 | | 1 | | 536 | | 1,110 | | 1,149 | | 39 | | 1,174 | |

Social Development | | 1,218 | | 1,190 | | (28 | ) | 1,207 | | 2,457 | | 2,456 | | (1 | ) | 2,427 | |

Transportation and Infrastructure | | 400 | | 398 | | (2 | ) | 371 | | 807 | | 804 | | (3 | ) | 807 | |

Total ministries and Office of the Premier | | 15,834 | | 15,596 | | (238 | ) | 15,210 | | 31,767 | | 31,799 | | 32 | | 31,297 | |

Management of public funds and debt | | 645 | | 594 | | (51 | ) | 632 | | 1,287 | | 1,212 | | (75 | ) | 1,238 | |

Contingencies | | 150 | | 2 | | (148 | ) | — | | 300 | | 300 | | — | | 22 | |

Funding for capital expenditures | | 340 | | 299 | | (41 | ) | 497 | | 1,062 | | 1,070 | | 8 | | 1,182 | |

Refundable tax credit transfers | | 527 | | 527 | | — | | 436 | | 1,091 | | 1,126 | | 35 | | 969 | |

Legislative and other appropriations | | 62 | | 54 | | (8 | ) | 62 | | 124 | | 124 | | — | | 132 | |

Subtotal | | 17,558 | | 17,072 | | (486 | ) | 16,837 | | 35,631 | | 35,631 | | — | | 34,840 | |

Liability for reimbursement of HST transition funding | | — | | — | | — | | 1,599 | | — | | — | | — | | 1,599 | |

Prior year liability adjustments | | — | | — | | — | | — | | — | | (40 | ) | (40 | ) | (99 | ) |

Consolidated revenue fund expense | | 17,558 | | 17,072 | | (486 | ) | 18,436 | | 35,631 | | 35,591 | | (40 | ) | 36,340 | |

Expenses recovered from external entities | | 1,256 | | 1,231 | | (25 | ) | 1,225 | | 2,756 | | 2,905 | | 149 | | 2,689 | |

Funding provided to service delivery agencies | | (10,424 | ) | (10,484 | ) | (60 | ) | (10,460 | ) | (21,127 | ) | (21,361 | ) | (234 | ) | (21,199 | ) |

Total direct program spending | | 8,389 | | 7,819 | | (570 | ) | 9,201 | | 17,260 | | 17,135 | | (125 | ) | 17,830 | |

Service delivery agency expense | | | | | | | | | | | | | | | | | |

School districts | | 2,457 | | 2,428 | | (29 | ) | 2,427 | | 5,569 | | 5,599 | | 30 | | 5,500 | |

Universities | | 1,963 | | 1,881 | | (82 | ) | 1,845 | | 4,050 | | 4,043 | | (7 | ) | 3,807 | |

Colleges and institutes | | 516 | | 519 | | 3 | | 516 | | 1,095 | | 1,118 | | 23 | | 1,095 | |

Health authorities and hospital societies | | 5,961 | | 6,042 | | 81 | | 5,810 | | 12,431 | | 12,548 | | 117 | | 12,116 | |

Other service delivery agencies | | 1,609 | | 1,622 | | 13 | | 1,607 | | 3,464 | | 3,513 | | 49 | | 3,459 | |

| | 12,507 | | 12,492 | | (15 | ) | 12,205 | | 26,609 | | 26,821 | | 212 | | 25,977 | |

Total expense | | 20,896 | | 20,311 | | (585 | ) | 21,406 | | 43,869 | | 43,956 | | 87 | | 43,807 | |

(1) Reflects government’s organization that was in effect at September 30, 2012.

(2) Restated to reflect government’s current accounting policies.

Second Quarterly Report 2012/13

11

Updated Financial Forecast

Table 1.9 2012/13 Expense By Function

| | Year-to-Date to September 30 | | Full Year | |

| | 2012/13 | | Actual | | 2012/13 | | Actual | |

($ millions) | | Budget | | Actual | | Variance | | 2011/12 (1) | | Budget | | Forecast | | Variance | | 2011/12 (1) | |

Health: | | | | | | | | | | | | | | | | | |

Medical Services Plan | | 1,991 | | 1,970 | | (21 | ) | 1,930 | | 4,162 | | 4,181 | | 19 | | 4,004 | |

Pharmacare | | 592 | | 570 | | (22 | ) | 571 | | 1,210 | | 1,162 | | (48 | ) | 1,147 | |

Regional services | | 5,740 | | 5,635 | | (105 | ) | 5,434 | | 11,840 | | 11,839 | | (1 | ) | 11,255 | |

Other healthcare expenses (2) | | 344 | | 341 | | (3 | ) | 304 | | 758 | | 799 | | 41 | | 642 | |

| | 8,667 | | 8,516 | | (151 | ) | 8,239 | | 17,970 | | 17,981 | | 11 | | 17,048 | |

Education: | | | | | | | | | | | | | | | | | |

Elementary and secondary | | 2,560 | | 2,538 | | (22 | ) | 2,530 | | 5,973 | | 5,983 | | 10 | | 5,885 | |

Post-secondary | | 2,437 | | 2,372 | | (65 | ) | 2,303 | | 5,204 | | 5,239 | | 35 | | 4,917 | |

Other education expenses (3) | | 281 | | 174 | | (107 | ) | 225 | | 584 | | 574 | | (10 | ) | 436 | |

| | 5,278 | | 5,084 | | (194 | ) | 5,058 | | 11,761 | | 11,796 | | 35 | | 11,238 | |

Social services: | | | | | | | | | | | | | | | | | |

Social assistance (2),(3) | | 877 | | 774 | | (103 | ) | 880 | | 1,545 | | 1,563 | | 18 | | 1,550 | |

Child welfare (2) | | 522 | | 534 | | 12 | | 548 | | 1,060 | | 1,062 | | 2 | | 1,112 | |

Low income tax credit transfers | | 239 | | 255 | | 16 | | 233 | | 523 | | 533 | | 10 | | 509 | |

Community living and other services | | 315 | | 373 | | 58 | | 255 | | 800 | | 785 | | (15 | ) | 769 | |

| | 1,953 | | 1,936 | | (17 | ) | 1,916 | | 3,928 | | 3,943 | | 15 | | 3,940 | |

Protection of persons and property | | 619 | | 686 | | 67 | | 678 | | 1,380 | | 1,425 | | 45 | | 1,512 | |

Transportation | | 773 | | 763 | | (10 | ) | 721 | | 1,655 | | 1,663 | | 8 | | 1,544 | |

Natural resources and economic development | | 877 | | 893 | | 16 | | 921 | | 1,792 | | 1,891 | | 99 | | 1,881 | |

Other | | 633 | | 663 | | 30 | | 649 | | 1,360 | | 1,355 | | (5 | ) | 1,394 | |

Contingencies | | 150 | | 2 | | (148 | ) | — | | 300 | | 300 | | — | | 22 | |

General government | | 716 | | 589 | | (127 | ) | 2,050 | | 1,207 | | 1,173 | | (34 | ) | 2,845 | |

Debt servicing | | 1,230 | | 1,179 | | (51 | ) | 1,174 | | 2,516 | | 2,429 | | (87 | ) | 2,383 | |

Total expense | | 20,896 | | 20,311 | | (585 | ) | 21,406 | | 43,869 | | 43,956 | | 87 | | 43,807 | |

(1) Restated to reflect government’s current organization and accounting policies.

(2) Payments for healthcare services by the Ministry of Social Development and the Ministry of Children and Family Development made on behalf of their clients are reported in the Health function.

(3) Payments for training costs by the Ministry of Social Development made on behalf of its clients are reported in the Education function.

Second Quarterly Report 2012/13

12

Updated Financial Forecast

Table 1.10 2012/13 Material Assumptions – Revenue

| | | | 1st | | 2nd | | | |

Revenue Source and Assumptions | | Budget | | Quarter | | Quarter | | | |

($ millions unless otherwise specified) | | 2012 | | Forecast | | Forecast | | 2012/13 Sensitivities | |

Personal income tax | | $ | 6,630 | | $ | 6,614 | | $ | 6,897 | | | |

Current calendar year assumptions | | | | | | | | | |

Personal income growth | | 3.7 | % | 3.5 | % | 3.5 | % | +/- 1% change in 2012 BC personal income growth equals +/- $50 to $100 million | |

Labour income growth | | 3.6 | % | 3.2 | % | 3.2 | % | |

Tax base growth | | 3.7 | % | 3.5 | % | 3.5 | % | |

Average tax yield | | 4.88 | % | 4.88 | % | 4.92 | % | |

Current-year tax | | $ | 6,273 | | $ | 6,264 | | $ | 6,418 | | +/- 1% change in 2011 BC personal or taxable income growth equals +/- $50 to $100 million one-time effect (prior-year adjustment) and could result in an additional +/-$55 to $75 million base change in 2012/13 | |

BC Tax Reduction | | $ | -111 | | $ | -111 | | $ | -107 | | |

Non-Refundable BC tax credits | | $ | -47 | | $ | -47 | | $ | -48 | | |

Policy neutral elasticity * | | 1.2 | | 1.2 | | 1.2 | | |

Fiscal year assumptions | | | | | | | | |

Prior-year adjustment | | | | | | $ | 151 | | |

| | | | | | | | | |

| | 2011 Assumptions | | | |

2011 Tax-year | | | | | | | | | |

Personal income growth | | 3.7 | % | 4.1 | % | 4.1 | % | | |

Tax base growth | | 3.0 | % | 3.0 | % | 4.7 | % | | |

Average 2011 tax yield | | 4.84 | % | 4.84 | % | 4.88 | % | | |

2011 tax | | $ | 6,006 | | $ | 6,006 | | $ | 6,155 | | | |

BC Tax Reduction | | $ | -109 | | $ | -109 | | $ | -105 | | | |

Non-Refundable BC tax credits | | $ | -43 | | $ | -43 | | $ | -51 | | | |

Policy neutral elasticity * | | 1.0 | | 0.9 | | 1.5 | | | |

* Ratio of annual per cent change in current-year revenue to annual per cent change in personal income (calendar year).

Corporate income tax | | $ | 2,266 | | $ | 2,286 | | $ | 2,311 | | | |

Components of revenue (fiscal year) | | | | | | | | | |

Advance instalments | | $ | 2,305 | | $ | 2,325 | | $ | 2,339 | | | |

International Business Activity Act refunds | | $ | -20 | | $ | -20 | | $ | -20 | | | |

Prior-year adjustment | | $ | -19 | | $ | -19 | | $ | -8 | | | |

Current calendar year assumptions | | | | | | | | | |

National tax base ($ billions) | | $ | 245.9 | | $ | 249.1 | | $ | 248.8 | | +/ - 1% change in the 2012 national tax base equals +/- $20 to $30 million | |

BC instalment share of national tax base | | 11.8 | % | 11.8 | % | 11.8 | % | |

Effective tax rates (general/small business) | | 10.0 / 2.5 | | 10.0 / 2.5 | | 10.0 / 2.5 | | |

BC tax base growth (post federal measures) | | 4.8 | % | 4.5 | % | 4.5 | % | | |

BC corporate profits growth | | 3.5 | % | 4.4 | % | 4.4 | % | +/ - 1% change in the 2011 BC tax base equals +/- $20 to $30 million in 2012/13 | |

Non-Refundable BC tax credits | | $ | -76 | | $ | -76 | | $ | -77 | | |

| | | | | | | | |

| | | | | | | | | |

| | 2011 Assumptions | | | |

2011 Tax-year | | | | | | | | | |

BC tax base growth | | 10.5 | % | 10.7 | % | 12.1 | % | | |

BC corporate profits growth | | 10.6 | % | 13.4 | % | 13.4 | % | | |

Gross 2011 tax | | $ | 1,939 | | $ | 1,939 | | $ | 1,963 | | | |

Prior-year adjustments | | $ | -19 | | $ | -19 | | $ | -8 | | | |

Prior years losses/gains (included in above) | | $ | 0 | | $ | 0 | | $ | -25 | | | |

Non-Refundable BC tax credits | | $ | -71 | | $ | -71 | | $ | -58 | | | |

Revenue is recorded on a cash basis. Due to lags in the federal collection and instalment systems, changes to the BC corporate profits and tax base forecasts affect revenue in the succeeding year. The 2012/13 instalments from the federal government reflect 9 months of payments related to the 2012 tax year (paid during Apr-Sept 2012) and one-third of 2013 payments as reflected in the Tax Collection Agreement amended in Summer 2012. Instalments for the 2012 (2013) tax year are based on BC’s share of the national tax base for the 2010 (2011) tax year and a forecast of the 2012 (2013) national tax base. BC’s share of the 2010 national tax base was 11.8%, based on tax assessments as of December 31, 2011. Cash adjustments for any under/over payments from the federal government in respect of 2011 will be received/paid on March 28, 2013.

Second Quarterly Report 2012/13

13

Updated Financial Forecast

Table 1.10 2012/13 Material Assumptions – Revenue (continued)

| | | | 1st | | 2nd | | | |

Revenue Source and Assumptions | | Budget | | Quarter | | Quarter | | | |

($ millions unless otherwise specified) | | 2012 | | Forecast | | Forecast | | 2012/13 Sensitivities | |

Harmonized sales tax | | $ | 6,003 | | $ | 6,003 | | $ | 6,003 | | | |

Calendar Year | | | | | | | | +/- 1% change in consumer expenditure growth equals up to +/- $35 million | |

Nominal consumer expenditure | | 4.3 | % | 4.3 | % | 4.3 | % | |

Nominal residential investment | | 2.8 | % | 4.4 | % | 4.4 | % | |

Above two bases represent about 84% of the total base | | | | | | | | |

HST Rebates (% rebate of the provincial portion of the HST paid) | | | | | | | | +/- 1% change in residential construction growth equals up to +/- $15 million | |

Municipalities | | 75 | % | 75 | % | 75 | % | |

Charities and non-profit organizations | | 57 | % | 57 | % | 57 | % | |

New housing (up to $42,500) | | 71.43 | % | 71.43 | % | 71.43 | % | |

School authorities | | 87 | % | 87 | % | 87 | % | |

Universities and public colleges | | 75 | % | 75 | % | 75 | % | |

Hospital authorities | | 58 | % | 58 | % | 58 | % | | |

Components of revenue | | | | | | | | | |

Gross | | $ | 7,527 | | $ | 7,527 | | $ | 7,535 | | | |

Input tax credit denial (temporary) | | $ | 145 | | $ | 119 | | $ | 119 | | | |

Rebates: | | | | | | | | | |

· Point of sale | | $ | (372 | ) | $ | (366 | ) | $ | (374 | ) | | |

· Municipalities, charities & non profit organizations | | $ | (315 | ) | $ | (322 | ) | $ | (322 | ) | | |

· SUCH sector | | $ | (218 | ) | $ | (222 | ) | $ | (222 | ) | | |

· New housing | | $ | (552 | ) | $ | (516 | ) | $ | (516 | ) | | |

· Residential energy use | | $ | (212 | ) | $ | (217 | ) | $ | (217 | ) | | |

Other sales taxes | | $ | 98 | | $ | 101 | | $ | 101 | | | |

Tax on designated property (12% rate) | | $ | 98 | | $ | 101 | | $ | 101 | | | |

Fuel and carbon taxes | | $ | 2,109 | | $ | 2,112 | | $ | 2,109 | | | |

Calendar Year | | | | | | | | | |

Real GDP | | 1.8 | % | 2.0 | % | 2.0 | % | | |

Gasoline volumes | | 0.0 | % | 0.0 | % | 0.0 | % | | |

Diesel volumes | | 2.0 | % | 2.0 | % | 2.0 | % | | |

Natural gas volumes | | 2.0 | % | 2.0 | % | 2.0 | % | | |

Carbon tax rates (July 1) | | | | | | | | | |

Carbon dioxide equivalent emissions ($/tonne) | | $ | 30 | | $ | 30 | | $ | 30 | | | |

Natural gas (cents/gigajoule) | | 148.98¢ | | 148.98¢ | | 148.98¢ | | | |

Gasoline (cents/litre) | | 6.67¢ | | 6.67¢ | | 6.67¢ | | | |

Light fuel oil (cents/litre) | | 7.67¢ | | 7.67¢ | | 7.67¢ | | | |

Carbon tax revenue | | $ | 1,172 | | $ | 1,180 | | $ | 1,180 | | | |

Carbon tax rates change on July 1 | | | | | | | | | |

Components of fuel tax revenue | | | | | | | | | |

Consolidated Revenue Fund | | $ | 491 | | $ | 486 | | $ | 486 | | | |

BC Transit | | $ | 11 | | $ | 11 | | $ | 11 | | | |

BC Transportation Financing Authority | | $ | 435 | | $ | 435 | | $ | 432 | | | |

| | $ | 937 | | $ | 932 | | $ | 929 | | | |

| | | | | | | | | |

Property taxes | | $ | 2,013 | | $ | 1,998 | | $ | 1,985 | | | |

Calendar Year | | | | | | | | | |

BC Consumer Price Index | | 1.9 | % | 1.9 | % | 1.9 | % | +/- 1% change in new construction and inflation equals up to +/- $5 million in residential property taxation revenue | |

Housing starts | | 24,978 | | 26,000 | | 26,000 | | |

Home owner grants (fiscal year) | | $ | -799 | | $ | -804 | | $ | -804 | | |

Components of revenue | | | | | | | | |

Residential (net of home owner grants) | | $ | 704 | | $ | 696 | | $ | 689 | | | |

Non-residential | | $ | 1,030 | | $ | 1,026 | | $ | 1,025 | | +/- 1% change in new construction and inflation equals up to +/- $5 million in non-residential property taxation revenue | |

Rural area | | $ | 92 | | $ | 91 | | $ | 91 | |

Police | | $ | 30 | | $ | 30 | | $ | 30 | |

BC Assessment Authority | | $ | 79 | | $ | 79 | | $ | 79 | |

BC Transit | | $ | 78 | | $ | 76 | | $ | 71 | |

Second Quarterly Report 2012/13

14

Updated Financial Forecast

Table 1.10 2012/13 Material Assumptions – Revenue (continued)

| | | | 1st | | 2nd | | | |

Revenue Source and Assumptions | | Budget | | Quarter | | Quarter | | | |

($ millions unless otherwise specified) | | 2012 | | Forecast | | Forecast | | 2012/13 Sensitivities | |

Other taxes | | $ | 1,969 | | $ | 1,959 | | $ | 1,864 | | | |

Calendar Year | | | | | | | | | |

Population | | 1.1 | % | 0.7 | % | 0.7 | % | | |

BC Consumer Price Index | | 1.9 | % | 1.9 | % | 1.9 | % | | |

BC housing starts | | -5.4 | % | -1.5 | % | -1.5 | % | | |

Real GDP | | 1.8 | % | 2.0 | % | 2.0 | % | | |

Nominal GDP | | 3.7 | % | 3.9 | % | 3.9 | % | | |

Components of revenue | | | | | | | | | |

Property transfer | | $ | 893 | | $ | 893 | | $ | 798 | | | |

Tobacco | | $ | 652 | | $ | 642 | | $ | 642 | | | |

Insurance premium | | $ | 424 | | $ | 424 | | $ | 424 | | | |

Energy, sales of Crown land tenures, metals, minerals and other | | $ | 1,973 | | $ | 1,629 | | $ | 1,532 | | | |

Natural gas price | | | | | | | | +/- $0.50 change in the natural gas price equals +/- $72 to $110 million. | |

Plant inlet, $Cdn/gigajoule | | $ | 2.52 | | $ | 1.41 | | $ | 1.42 | | |

Sumas, $US/ MMBtu | | $ | 3.88 | | $ | 2.99 | | $ | 3.10 | | |

Natural gas production volumes (petajoules) | | 1,648 | | 1,496 | | 1,468 | | Sensitivities can vary significantly especially at lower prices. | |

Annual per cent change | | 12.8 | % | 4.0 | % | 2.0 | % | |

| | | | | | | | | | | | |

Oil price ($US/bbl at Cushing, Ok) | | $ | 97.07 | | $ | 93.99 | | $ | 92.70 | | +/- 1% change in natural gas volumes equals +/- $2 million on natural gas royalties +/- 1 cent change in the exchange rate equals +/- $2 million on natural gas royalties | |

| | | | | | | | |

Auctioned land base (000 hectares) | | 245 | | 94 | | 124 | | |

Average bid price/hectare ($) | | $ | 1,200 | | $ | 650 | | $ | 563 | | |

Cash sales of Crown land tenures | | $ | 294 | | $ | 61 | | $ | 70 | | |

Metallurgical coal price ($US/tonne, fob west coast) | | $ | 218 | | $ | 218 | | $ | 183 | | |

Copper price ($US/lb) | | $ | 3.68 | | $ | 3.49 | | $ | 3.54 | | |

Annual electricity volumes set by treaty (million mega-watt hours) | | 4.3 | | 4.3 | | 4.3 | | | |

Mid-Columbia electricity price ($US/mega-watt hour) | | $ | 32 | | $ | 25 | | $ | 26 | | +/- 10% change in the average Mid- | |

Exchange rate (US¢/ Cdn$, calendar year) | | 96.6 | | 98.7 | | 100.4 | | Columbia electricity price equals +/- $10 million | |

Components of revenue | | | | | | | | | |

Natural gas royalties | | $ | 398 | | $ | 157 | | $ | 157 | | | |

Bonus bids, fees and rentals | | $ | 882 | | $ | 865 | | $ | 866 | | Based on a recommendation from the Auditor General to be consistent with generally accepted accounting principles, bonus bid revenue recognition reflects nine-year deferral of cash receipts from the sale of Crown land tenures |

Petroleum royalties | | $ | 105 | | $ | 108 | | $ | 103 | |

Columbia River Treaty electricity sales | | $ | 125 | | $ | 92 | | $ | 96 | |

Coal | | $ | 341 | | $ | 309 | | $ | 215 | |

Minerals, metals and other | | $ | 74 | | $ | 55 | | $ | 56 | |

Oil and Gas Commission fees and levies | | $ | 48 | | $ | 43 | | $ | 39 | |

Royalty programs and infrastructure credits | | | | | | | |

Summer drilling | | $ | -25 | | $ | -17 | | $ | -29 | |

Deep drilling | | $ | -122 | | $ | -101 | | $ | -123 | |

Road and pipeline infrastructure | | $ | -188 | | $ | -42 | | $ | -31 | |

Total | | $ | -335 | | $ | -160 | | $ | -183 | |

Implicit average natural gas royalty rate | | 9.5 | % | 7.4 | % | 7.5 | % |

Royalty program (marginal, low productivity and ultra marginal drilling) adjustments reflect reduced royalty rates.

Natural gas royalties incorporate royalty programs and Treasury Board approved infrastructure credits.

Second Quarterly Report 2012/13

15

Updated Financial Forecast

Table 1.10 2012/13 Material Assumptions – Revenue (continued)

| | | | 1st | | 2nd | | | |

Revenue Source and Assumptions | | Budget | | Quarter | | Quarter | | | |

($ millions unless otherwise specified) | | 2012 | | Forecast | | Forecast | | 2012/13 Sensitivities | |

Forests | | $ | 533 | | $ | 543 | | $ | 546 | | | |

Prices (calendar year average) | | | | | | | | +/- US$50 change in SPF price equals +/- $25 to $50 million | |

SPF 2x4 ($US/1000 bd ft) | | $ | 260 | | $ | 284 | | | 289 | | |

Random Lengths Composite ($US/thousand board feet) | | $ | 295 | | $ | 319 | | $ | 316 | | | |

Pulp ($US/tonne) | | $ | 838 | | $ | 832 | | $ | 816 | | +/- US$50 change in pulp price equals +/-$5 to $10 million +/- Cdn$10 change in average log price equals +/-$10 to $20 million | |

Coastal log ($Cdn/cubic metre) | | | | | | | | |

(Vancouver Log Market, fiscal year) | | $ | 73 | | $ | 78 | | $ | 79 | | |

| | | | | | | | |

Fiscal Year Trade Assumptions | | | | | | | | |

Export tax rate (effective rate) | | 11.3 | % | 10.4 | % | 10.0 | % | |

Lumber shipments and consumption (billion board feet) | | | | | | | | +/- 1 cent change in exchange rate equals +/- $5 to $10 million on stumpage revenue +/- 10% change in Interior harvest volumes equals | |

U.S. lumber consumption | | 33.1 | | 34.1 | | 35.9 | | |

BC surge trigger volumes | | 7.0 | | 7.2 | | 7.6 | | |

BC lumber exports to US | | 5.1 | | 5.4 | | 5.6 | | |

| | | | | | | | |

Crown harvest volumes (million cubic metres) | | | | | | | | |

Interior | | 50.8 | | 50.8 | | 51.7 | | +/- $10 to $15 million | |

Coast | | 14.2 | | 14.2 | | 14.3 | | +/- 10% change in Coastal harvest volumes equals +/- $3 to $6 million | |

Total | | 65.0 | | 65.0 | | 66.0 | | |

BC Timber Sales (included in above) | | 11.8 | | 10.5 | | 10.5 | | |

Components of revenue | | | | | | | | The above sensitivities relate to stumpage revenue only. Depending on market conditions, changes in stumpage revenues may be offset by changes in border tax revenues. | |

Tenures | | $ | 186 | | $ | 179 | | $ | 196 | | |

BC Timber Sales | | $ | 178 | | $ | 178 | | $ | 178 | | |

Federal border tax (SLA 2006) | | $ | 128 | | $ | 139 | | $ | 123 | | |

Logging tax | | $ | 15 | | $ | 15 | | $ | 15 | | |

Other CRF revenue | | $ | 16 | | $ | 15 | | $ | 15 | | |

Recoveries | | $ | 10 | | $ | 17 | | $ | 19 | | |

Other natural resources | | $ | 480 | | $ | 481 | | $ | 482 | | | |

Components of revenue | | | | | | | | | |

Water rental and licences* | | $ | 411 | | $ | 412 | | $ | 412 | | | |

Recoveries | | $ | 49 | | $ | 49 | | $ | 49 | | | |

Angling and hunting permits and licences | | $ | 13 | | $ | 13 | | $ | 13 | | | |

Recoveries | | $ | 7 | | $ | 7 | | $ | 8 | | | |

* BC Hydro rate increases are indexed to Consumer Price Index.

| | | | | | | | | |

Other revenue | | $ | 9,053 | | $ | 9,089 | | $ | 8,797 | | | |

Components of revenue | | | | | | | | | |

Fees and licences | | | | | | | | | |

Consolidated Revenue Fund | | $ | 2,811 | | $ | 2,776 | | $ | 2,789 | | | |

Medical Services Plan premiums | | $ | 1,991 | | $ | 1,956 | | $ | 1,966 | | | |

Motor vehicle licences and permits | | $ | 485 | | $ | 487 | | $ | 485 | | | |

Other Consolidated revenue fund | | $ | 335 | | $ | 333 | | $ | 338 | | | |

Recoveries | | $ | 223 | | $ | 235 | | $ | 225 | | | |

MSP recoveries | | $ | 56 | | $ | 87 | | $ | 76 | | | |

Other recoveries | | $ | 167 | | $ | 148 | | $ | 149 | | | |

Crown corporations and agencies | | $ | 105 | | $ | 104 | | $ | 101 | | | |

Other service delivery agencies | | $ | 1,784 | | $ | 1,812 | | $ | 1,818 | | | |

Post-secondary education fees | | $ | 1,318 | | $ | 1,332 | | $ | 1,336 | | | |

Other health-care related fees | | $ | 318 | | $ | 326 | | $ | 328 | | | |

School Districts | | $ | 148 | | $ | 154 | | $ | 154 | | | |

Investment earnings | | | | | | | | | |

Consolidated Revenue Fund | | $ | 65 | | $ | 65 | | $ | 65 | | | |

Fiscal agency loans & sinking funds earnings | | $ | 854 | | $ | 838 | | $ | 839 | | | |

Crown corporations and agencies | | $ | 36 | | $ | 33 | | $ | 33 | | | |

Other service delivery agencies | | $ | 128 | | $ | 145 | | $ | 132 | | | |

Sales of goods and services | | $ | 889 | | $ | 926 | | $ | 930 | | | |

Miscellaneous | | | | | | | | | |

Consolidated Revenue Fund | | $ | 203 | | $ | 212 | | $ | 221 | | | |

Recoveries | | $ | 501 | | $ | 556 | | $ | 571 | | | |

Crown corporations and agencies | | $ | 371 | | $ | 362 | | $ | 51 | | | |

Other service delivery agencies | | $ | 1,083 | | $ | 1,025 | | $ | 1,022 | | | |

Second Quarterly Report 2012/13

16

Updated Financial Forecast

Table 1.10 2012/13 Material Assumptions – Revenue (continued)

| | | | 1st | | 2nd | | | |

Revenue Source and Assumptions | | Budget | | Quarter | | Quarter | | | |

($ millions unless otherwise specified) | | 2012 | | Forecast | | Forecast | | 2012/13 Sensitivities | |

Health and social transfers | | $ | 5,682 | | $ | 5,617 | | $ | 5,616 | | | |

National Cash Transfers | | | | | | | | | |

Canada Health Transfer (CHT) | | $ | 28,569 | | $ | 28,569 | | $ | 28,569 | | | |

Wait Times Reduction Transfer (WTRT) | | $ | 250 | | $ | 250 | | $ | 250 | | +/- 0.1% change in BC’s | |

Canada Social Transfer (CST) | | $ | 11,859 | | $ | 11,859 | | $ | 11,859 | | population share equals | |

BC share of national population (June 1) | | 13.28 | % | 13.22 | % | 13.26 | % | +/- $50 to $55 million | |

BC health and social transfers revenue | | | | | | | | | |

CHT | | $ | 4,051 | | $ | 4,002 | | $ | 4,007 | | | |

WTRT | | $ | 33 | | $ | 33 | | $ | 33 | | | |

CST | | $ | 1,575 | | $ | 1,568 | | $ | 1,572 | | | |

Prior-year adjustments | | | | $ | -9 | | $ | -19 | | | |

Health deferral | | | | | | | | | |

Diagnostic and Medical Equipment | | $ | 16 | | $ | 16 | | $ | 16 | | | |

Medical Equipment Trust | | $ | 7 | | $ | 7 | | $ | 7 | | | |

Other federal contributions | | $ | 1,575 | | $ | 1,631 | | $ | 1,652 | | | |

Components of revenue | | | | | | | | | |

Other Consolidated Revenue Fund | | $ | 150 | | $ | 149 | | $ | 149 | | | |

Labour Market Development Agreement | | $ | 285 | | $ | 286 | | $ | 285 | | | |

Local Government Services and Transfers | | $ | 33 | | $ | 32 | | $ | 32 | | | |

Canada-BC Co-operation on Immigration | | $ | 120 | | $ | 120 | | $ | 120 | | | |

Labour Market Agreement | | $ | 66 | | $ | 105 | | $ | 105 | | | |

Other recoveries | | $ | 199 | | $ | 210 | | $ | 207 | | | |

Crown corporations and agencies | | $ | 213 | | $ | 211 | | $ | 222 | | | |

Other service delivery agencies | | $ | 509 | | $ | 518 | | $ | 532 | | | |

| | | | | | | | | |

Service delivery agency direct revenue | | $ | 5,769 | | $ | 5,780 | | $ | 5,473 | | | |

School districts | | $ | 481 | | $ | 496 | | $ | 496 | | | |

Post-secondary institutions | | $ | 2,873 | | $ | 2,896 | | $ | 2,881 | | | |

Health authorities and hospital societies | | $ | 801 | | $ | 792 | | $ | 815 | | | |

BC Transportation Financing Authority | | $ | 465 | | $ | 471 | | $ | 467 | | | |

Other service delivery agencies | | $ | 1,149 | | $ | 1,125 | | $ | 814 | | | |

Commercial Crown corporation net income | | $ | 2,717 | | $ | 2,661 | | $ | 2,627 | | | |

BC Hydro | | $ | 566 | | $ | 520 | | $ | 512 | | | |

reservoir water inflows | | 100 | % | 110 | % | 109 | % | +/-1% in hydro generation | |

| | | | | | | | = +/-$5 million | |

mean gas price | | 4.77 | | 2.72 | | 2.85 | | +/-10% = -/+$5 million | |

(Sumas, $US/MMbtu – BC Hydro forecast based on NYMEX forward selling prices) | | | |

electricity prices | | 36.67 | | 20.81 | | 20.65 | | +/-10% change in electricity trade | |

(Mid-C, $US/MWh) | | | | | | | | margins = +/-$20 million | |

allowed return on deemed equity | | 12.75 | % | 11.73 | % | 11.73 | % | +/-1% = +/-$47 to $53 million | |

| | | | | | | | | |

ICBC | | $ | 146 | | $ | 160 | | $ | 141 | | | |

vehicle growth | | + 1.3 | % | + 1.4 | % | + 1.4 | % | +/-1% = +/-$38 million | |

current claims cost percentage change | | + 1.4 | % | + 4.6 | % | + 5.3 | % | +/-1% = -/+$30 million | |

investment return | | 3.4 | % | 3.5 | % | 3.6 | % | +/-1% return = +/-$115 million | |

loss ratio | | 86.4 | % | 86.6 | % | 87.8 | % | | |

Second Quarterly Report 2012/13

17

Updated Financial Forecast

Table 1.11 2012/13 Material Assumptions – Expense

| | | | 1st | | 2nd | | | |

Ministry Programs and Assumptions | | Budget | | Quarter | | Quarter | | | |

($ millions unless otherwise specified) | | 2012 | | Forecast | | Forecast | | Sensitivities 2012/13 | |

Advanced Education, Innovation and Technology | | 1,981 | | 1,981 | | 1,981 | | | |

Student spaces in public institutions (# FTEs) | | 201,307 | | 201,307 | | 201,983 | | The number of student spaces may vary depending on the financial and other policies of post-secondary institutions. | |

Children and Family Development | | 1,333 | | 1,333 | | 1,331 | | | |

Average children-in-care caseload (#) | | 8,070 | | 8,070 | | 8,150 | | Caseload is expected to decline. The child population (age 0 to 18) is projected to start increasing in 2013, potentially decelerating the downward trend. A 1% increase in the cost per case or a 1% increase in the average caseload will affect expenditures by approximately $2.8 million. | |

Average annual residential cost per child in care ($) | | 35,200 | | 35,200 | | 35,200 | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Education | | 5,315 | | 5,315 | | 5,315 | | | |

Enrolment (# of FTEs) | | 556,660 | | 556,660 | | 555,195 | | Enrolment figures are based on BC Stats enrolment trends, to which the Ministry has added forecasts for distributed learning, adult education, and summer learning. | |

School age (K–12) | | 530,220 | | 530,220 | | 530,879 | | |

Distributed Learning (online) | | 12,329 | | 12,329 | | 11,907 | | |

Summer | | 6,117 | | 6,117 | | 6,117 | | |

Adults | | 7,994 | | 7,994 | | 6,292 | | |

| | | | | | | | |

Forests, Lands and Natural Resource Operations | | 602 | | 664 | | 671 | | | |

BC Timber Sales | | 160 | | 160 | | 160 | | Targets can be impacted by changes to actual inventory costs incurred. There is a lag of approximately 2 years between when inventory costs are incurred and when they are expensed. Volume harvested can also impact targets. For example, if volume harvested is less than projected in any year then capitalized expenses will also be reduced in that year. | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Direct Fire Fighting | | 63 | | 125 | | 138 | | Over the past several years, Direct fire fighting costs have ranged from a low of $19 million in 1997 to $382 million in 2009. | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Health | | 16,180 | | 16,180 | | 16,115 | | | |

Pharmacare | | 1,185 | | 1,144 | | 1,115 | | A 1% change in utilization or drug prices affects costs by approximately $10 million. | |

| | | | | | | | |

| | | | | | | | |

Medical Services Plan (MSP) | | 3,895 | | 3,909 | | 3,885 | | A 1% increase in volume of services provided by fee-for-service physicians affects costs by approximately $25 million. | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Regional Services | | 10,859 | | 10,859 | | 10,846 | | | |

Justice | | 1,110 | | 1,154 | | 1,149 | | | |

New cases filed/processed (# for all courts) | | 295,000 | | 295,000 | | 295,000 | | The number of criminal cases proceeded on by the provincial and federal Crown (including appeals to higher courts in BC), the number of civil and family litigation cases, the number of violation tickets disputed, and the number of municipal bylaw tickets disputed which would go to court for resolution. | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | | |

Crown Proceedings Act (CPA) | | 25 | | 25 | | 25 | | The number and size of litigation brought against the province, as well as the effectiveness of mitigation strategies and legal defence. | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | | |

Policing, Victim Services and Corrections | | 569 | | 569 | | 582 | | The volume and severity of criminal activity, the number of inmate beds occupied and the number of offenders under community supervision. | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | | |

Emergency Program Act (EPA) | | 15 | | 59 | | 58 | | The number and severity of natural disasters. | |

Second Quarterly Report 2012/13

18

Updated Financial Forecast

Table 1.11 2012/13 Material Assumptions – Expense (continued )

| | | | 1st | | 2nd | | | |

Ministry Programs and Assumptions | | Budget | | Quarter | | Quarter | | | |

($ millions unless otherwise specified) | | 2012 | | Forecast | | Forecast | | Sensitivities 2012/13 | |

Social Development | | 2,457 | | 2,457 | | 2,456 | | | |

Temporary Assistance annual average caseload (#) | | 55,000 | | 55,000 | | 51,896 | | The expected to work caseload is sensitive to fluctuations in economic and employment trends in the service sector. A 1% change in the Temporary Assistance annual average caseload or average cost per case will affect expenditures by approximately $4.5 million annually. | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Disability Assistance annual average caseload (#) | | 83,000 | | 83,000 | | 84,279 | | The caseload for persons with disabilities is sensitive to the aging of the population and longer life expectancy for individuals with disabilities and significant health issues. A 1% change in the Disability Assistance annual average caseload or average cost per case will affect expenditures by approximately $7.5 million annually. | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Total annual average caseload (#) | | 138,000 | | 138,000 | | 136,175 | | The average cost per case is sensitive to the composition of the caseload, and reported income. | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Adult Community Living: | | | | | | | | | |

Residential Services: | | | | | | | | | |

Average caseload (#) | | 5,536 | | 5,536 | | 5,754 | | The adult community living caseload is sensitive to the pressures of an aging population. A 1% increase in the adult caseload will increase expenditures by approximately $2.4 million. | |

Average cost per client ($) | | 74,800 | | 74,800 | | 70,838 | | |

Day Programs: | | | | | | | | |

Average caseload (#) | | 14,570 | | 14,570 | | 14,661 | | |

Average cost per client ($) | | 18,150 | | 18,150 | | 17,775 | | |

Personal Supports Initiative | | | | | | | | |

Average caseload (#) | | 419 | | 419 | | 415 | | |

Average cost per client ($) | | 23,700 | | 23,700 | | 25,306 | | | |

Tax Transfers | | 1,091 | | 1,057 | | 1,127 | | | |

Personl Income | | 632.3 | | 632.3 | | 622.7 | | | |

| | | | | | | | These tax transfers are now expensed as required under generally accepted accounting principles. Previously for the family bonus was split 50/50 between expense program and as reduction to revenue while all other refundable credits were recorded as reduction to revenue. | |

Family Bonus Program | | 4.5 | | 4.5 | | 4.5 | | |

Low Income Climate Action | | 190.0 | | 190.0 | | 195.0 | | |

Sales Tax / BC HST | | 328.3 | | 328.3 | | 333.3 | | |

Small Business Venture Capital | | 28.0 | | 28.0 | | 23.5 | | |

Other Personal income | | 81.5 | | 81.5 | | 66.4 | | |

Corporate Income | | 459.2 | | 424.8 | | 504.1 | | |

Film and Television | | 70.0 | | 65.0 | | 97.0 | | |

Production Services | | 217.4 | | 201.5 | | 259.5 | | |

Scientific Research & Experimental Development | | 79.2 | | 72.3 | | 72.3 | | | |

Interactive Digital Media | | 37.9 | | 35.0 | | 30.0 | | | |

Other Corporate income | | 54.7 | | 51.0 | | 45.3 | | | |

Management of Public Funds and Debt | | 1,287 | | 1,218 | | 1,212 | | | |

Interest rates for new provincial borrowing: | | | | | | | | Full year impact on MoPD on interest costs of a 1% change in interest rates equals $35.1 million; $100 million increase in debt level equals $1.1 million. | |

Short-term | | 1.11 | % | 1.05 | % | 1.08 | % | |

Long-term | | 3.47 | % | 2.86 | % | 2.76 | % | |

CDN/US exchange rate (cents) | | 102.7 | | 101.6 | | 99.3 | | |

| | | | | | | | |

Service delivery agency net spending | | 5,482 | | 5,516 | | 5,460 | | | |

School districts | | 204 | | 228 | | 194 | | | |

Post-secondary institutions | | 2,834 | | 2,855 | | 2,822 | | | |

Health authorities and hospital societies | | 646 | | 705 | | 705 | | | |

BC Transportation Financing Authority | | 946 | | 898 | | 898 | | | |

Other service delivery agencies | | 852 | | 830 | | 841 | | | |

Second Quarterly Report 2012/13

19

Updated Financial Forecast

Table 1.12 2012/13 Full-Time Equivalents (FTEs) (1)

| | 2012/13 | | Actual | |

FTEs | | Budget | | Forecast | | Variance | | 2011/12 (2) | |

Ministries and special offices (consolidated revenue fund) | | 26,891 | | 26,891 | | — | | 27,228 | |

Service delivery agencies (3) | | 4,568 | | 4,568 | | — | | 4,346 | |

Total FTEs | | 31,459 | | 31,459 | | — | | 31,574 | |

(1) Full-time equivalents (FTEs) are a measure of staff employment. FTEs are calculated by dividing the total hours of employment paid for in a given period by the number of hours an individual, full-time person would normally work in that period. This does not equate to the physical number of employees. For example, two half-time employees would equal one FTE, or alternatively, three FTEs may represent two full-time employees who have worked sufficient overtime hours to equal an additional FTE.

(2) The ministry 2011/12 FTE total includes a reduction of about 3,200 FTEs reflecting the shift of BC Ambulance Service oversight from the Ministry of Health to the Provincial Health Services Authority.

(3) Service delivery agency FTE amounts do not include SUCH sector staff employment.

Table 1.13 2012/13 Capital Spending

| | Year-to-Date to September 30 | | Full Year | |

| | 2012/13 | | Actual | | 2012/13 | | Actual | |

($ millions) | | Budget | | Actual | | Variance | | 2011/12 | | Budget | | Forecast | | Variance | | 2011/12 | |

Taxpayer-supported | | | | | | | | | | | | | | | | | |

Education | | | | | | | | | | | | | | | | | |

School districts | | 243 | | 286 | | 43 | | 319 | | 486 | | 517 | | 31 | | 560 | |

Post-secondary institutions | | 344 | | 222 | | (122 | ) | 265 | | 688 | | 791 | | 103 | | 662 | |

Health | | 440 | | 273 | | (167 | ) | 272 | | 879 | | 887 | | 8 | | 732 | |

BC Transportation Financing Authority | | 535 | | 583 | | 49 | | 635 | | 1,069 | | 1,088 | | 19 | | 921 | |

BC Transit | | 45 | | 14 | | (31 | ) | 19 | | 90 | | 61 | | (29 | ) | 37 | |

BC Place redevelopment | | — | | — | | — | | 159 | | — | | 8 | | 8 | | 194 | |

Government operating (ministries) | | 227 | | 68 | | (159 | ) | 86 | | 454 | | 416 | | (38 | ) | 245 | |

Other (1) | | 46 | | 41 | | (5 | ) | 116 | | 91 | | 122 | | 31 | | 221 | |

Capital planning adjustment | | — | | — | | — | | — | | — | | (146 | ) | (146 | ) | — | |

Total taxpayer-supported | | 1,879 | | 1,487 | | (392 | ) | 1,871 | | 3,757 | | 3,744 | | (13 | ) | 3,572 | |

Self-supported | | | | | | | | | | | | | | | | | |

BC Hydro | | 1,132 | | 953 | | (179 | ) | 884 | | 2,361 | | 2,196 | | (165 | ) | 1,917 | |

Columbia River power projects (2) | | 57 | | 56 | | (1 | ) | 61 | | 122 | | 122 | | — | | 108 | |

Transportation Investment Corporation | | | | | | | | | | | | | | | | | |

(Port Mann) | | 362 | | 384 | | 22 | | 417 | | 606 | | 641 | | 35 | | 735 | |

BC Rail | | 7 | | 4 | | (3 | ) | 4 | | 13 | | 11 | | (2 | ) | 9 | |

ICBC | | 39 | | 40 | | 1 | | 47 | | 101 | | 97 | | (4 | ) | 92 | |

BC Lottery Corporation | | 58 | | 43 | | (15 | ) | 38 | | 116 | | 118 | | 2 | | 74 | |

Liquor Distribution Branch | | 13 | | 2 | | (11 | ) | 6 | | 27 | | 22 | | (5 | ) | 19 | |

Total self-supported | | 1,668 | | 1,482 | | (186 | ) | 1,457 | | 3,346 | | 3,207 | | (139 | ) | 2,954 | |

Total capital spending | | 3,547 | | 2,969 | | (578 | ) | 3,328 | | 7,103 | | 6,951 | | (152 | ) | 6,526 | |

(1) Includes BC Housing Management Commission, Provincial Rental Housing Corporation and other service delivery agencies.

(2) Joint ventures of the Columbia Power Corporation and Columbia Basin Trust.

Second Quarterly Report 2012/13

20

Updated Financial Forecast

Table 1.14 Capital Expenditure Projects Greater Than $50 million (1)

Note: Information in bold type denotes changes from the 2012/13 first Quarterly Report released on September 13, 2012.

| | Projected | | Total Costs | | Projected | | Total | | Project Financing | |

| | Completion | | to | | Costs to | | Capital | | Internal/ | | P3 | | Federal | | Other | |

($ millions) | | Date | | Sept 30, 2012 | | Complete | | Costs | | Borrowing | | Liability | | Gov’t | | Contrib’ns | |

Taxpayer-supported | | | | | | | | | | | | | | | | | |

School districts | | | | | | | | | | | | | | | | | |

Revelstoke Elementary and Secondary | | Fall 2012 | | 55 | | 5 | | 60 | | 58 | | — | | — | | 2 | |

Burnaby Central Secondary | | Fall 2012 | | 52 | | 8 | | 60 | | 60 | | — | | — | | — | |

Alberni District Secondary | | Fall 2012 | | 50 | | 8 | | 58 | | 54 | | — | | — | | 4 | |

Southern Okanagan Secondary | | Fall 2013 | | 34 | | 20 | | 54 | | 52 | | — | | — | | 2 | |

Chilliwack Secondary | | Fall 2013 | | 19 | | 39 | | 58 | | 58 | | — | | — | | — | |

Centennial Secondary | | Spring 2015 | | 3 | | 59 | | 62 | | 62 | | — | | — | | — | |

Oak Bay Secondary | | Fall 2015 | | 1 | | 49 | | 50 | | 48 | | — | | — | | 2 | |

Kitsilano Secondary | | Fall 2015 | | 2 | | 56 | | 58 | | 58 | | — | | — | | — | |

Seismic mitigation program | | Spring 2021 | | — | | 1,300 | | 1,300 | | 1,300 | | — | | — | | — | |

Full-day kindergarten | | Winter 2012 | | 121 | | 13 | | 134 | | 134 | | — | | — | | — | |

Total school districts | | | | 337 | | 1,557 | | 1,894 | | 1,884 | | — | | — | | 10 | |

Post-secondary institutions | | | | | | | | | | | | | | | | | |

University of British Columbia | | | | | | | | | | | | | | | | | |

— Pharmaceutical Sciences and Centre for Drug | | | | | | | | | | | | | | | | | |

Research & Development | | Fall 2012 | | 133 | | — | | 133 | | 86 | | — | | 3 | | 44 | |

Health facilities | | | | | | | | | | | | | | | | | |

Victoria Royal Jubilee Hospital — Patient Care Centre | | | | | | | | | | | | | | | | | |

— Direct procurement | | Spring 2013 | | 48 | | 21 | | 69 | | 23 | | — | | — | | 46 | |

— P3 contract | | Spring 2011 | | 280 | | — | | 280 | | — | | 199 | | — | | 81 | |

Fort St. John Hospital and Residential Care (2) | | | | | | | | | | | | | | | | | |

— Direct procurement | | Spring 2012 | | 48 | | 5 | | 53 | | 52 | | — | | — | | 1 | |

— P3 contract | | Spring 2012 | | 249 | | — | | 249 | | 121 | | 33 | | — | | 95 | |

Expansions to Kelowna General and | | | | | | | | | | | | | | | | | |

Vernon Jubilee Hospitals (2) | | | | | | | | | | | | | | | | | |

— Direct procurement | | Spring 2012 | | 38 | | 11 | | 49 | | 25 | | — | | — | | 24 | |

— P3 contract | | Spring 2012 | | 386 | | — | | 386 | | 3 | | 158 | | — | | 225 | |

Northern Cancer Control Strategy | | | | | | | | | | | | | | | | | |

— Direct procurement | | Summer 2013 | | 25 | | 10 | | 35 | | 32 | | — | | — | | 3 | |

— P3 contract | | Summer 2012 | | 67 | | 4 | | 71 | | 54 | | 17 | | — | | — | |

Lions Gate Hospital (Mental Health) | | | | | | | | | | | | | | | | | |

Redevelopment | | Fall 2013 | | 5 | | 57 | | 62 | | 38 | | — | | — | | 24 | |

Surrey Emergency/Critical Care Tower | | | | | | | | | | | | | | | | | |

— Direct procurement | | Summer 2014 | | 47 | | 147 | | 194 | | 174 | | — | | — | | 20 | |

— P3 contract | | Summer 2014 | | 173 | | 145 | | 318 | | 139 | | 179 | | — | | — | |

Lakes District Hospital | | Summer 2015 | | — | | 55 | | 55 | | 46 | | — | | — | | 9 | |

Queen Charlotte/Haida Gwaii Hospital | | Summer 2015 | | — | | 50 | | 50 | | 31 | | — | | — | | 19 | |

North Island Hospitals | | Summer 2017 | | — | | 601 | | 601 | | 365 | | — | | — | | 236 | |

Interior Heart and Surgical Centre | | Spring 2017 | | 79 | | 288 | | 367 | | 217 | | 79 | | — | | 71 | |

Children’s and Women’s Hospital (3) | | Spring 2018 | | 23 | | 657 | | 680 | | 532 | | — | | — | | 148 | |

Total health facilities | | | | 1,468 | | 2,051 | | 3,519 | | 1,852 | | 665 | | — | | 1,002 | |

Transportation | | | | | | | | | | | | | | | | | |

South Fraser Perimeter Road | | | | | | | | | | | | | | | | | |

— Direct procurement | | Summer 2014 | | 934 | | 128 | | 1,062 | | 714 | | — | | 348 | | — | |