BUDGET AND FISCAL PLAN

2019/20 – 2021/22

February 19, 2019

National Library of Canada Cataloguing in Publication Data

British Columbia.

Budget and fiscal plan. — 2002/03/2004/05-

Annual

Also available on the Internet.

Continues: British Columbia. Ministry of Finance and

Corporate Relations. Budget … reports. ISSN 1207-5841

ISSN 1705-6071 = Budget and fiscal plan — British Columbia.

1. Budget — British Columbia — Periodicals. 2. British

Columbia — Appropriations and expenditures — Periodicals.

I. British Columbia. Ministry of Finance. II. Title.

HJ12.B742 352.48’09711’05 C2003-960048-3

BUDGET AND FISCAL PLAN 2019/20 to 2021/22

February 19, 2019 | TABLE OF CONTENTS |

Attestation by the Secretary to Treasury Board | |

| |

Summary | 1 |

| |

Part 1: Three Year Fiscal Plan | |

Introduction | 7 |

Expense | 8 |

| Consolidated Revenue Fund Spending | 8 |

| | Making Life More Affordable | 8 |

| | Enhancing Services that People Count On | 13 |

| | Building a Strong and Sustainable Economy | 16 |

| Analysis for Equity and Fairness (GBA+) | 24 |

| BC Public Service | 24 |

| Recovered Expenses | 26 |

| Operating Transfers | 26 |

| Service Delivery Agency Spending | 27 |

Revenue | 30 |

| Major Revenue Sources | 32 |

Capital Spending | 38 |

| Taxpayer-Supported Capital Spending | 38 |

| Self-Supported Capital Spending | 45 |

| Projects Over $50 Million | 46 |

Provincial Debt | 51 |

Risks to the Fiscal Plan | 54 |

| |

Tables: | | | |

| 1.1 | Three Year Fiscal Plan | 7 |

| 1.2 | Creating More Opportunities for People to Get Ahead | 8 |

| 1.3 | BC Child Opportunity Benefit | 8 |

| 1.4 | Homes for B.C. | 11 |

| 1.5 | Investing in Health Care and Education | 14 |

| 1.6 | Enhancing Supports | 15 |

| 1.7 | Improving Access to Justice and Public Safety | 15 |

| 1.8 | CleanBC - Operating, Capital and Contingencies Allocations | 17 |

| 1.9 | Reconciliation with First Nations | 19 |

| 1.10 | Securing Resources for Tomorrow | 19 |

| 1.11 | Investing in Higher Education and the Workforce | 20 |

| 1.12 | Investing in Communities | 22 |

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

i

TABLE OF CONTENTS

| 1.13 | Sustainable Economic Development | 23 |

| 1.14 | Revenue by Source | 28 |

| 1.15 | Expense by Ministry, Program and Agency | 29 |

| 1.16 | Comparison of Major Factors Underlying Revenue | 31 |

| 1.17 | Personal Income Tax Revenue | 32 |

| 1.18 | Corporate Income Tax Revenue | 32 |

| 1.19 | Sales Tax Revenue | 33 |

| 1.20 | Federal Government Contributions | 36 |

| 1.21 | Capital Spending | 38 |

| 1.22 | Provincial Transportation Investments | 44 |

| 1.23 | Capital Expenditure Projects Greater Than $50 Million | 47 |

| 1.24 | Provincial Debt Summary | 52 |

| 1.25 | Provincial Borrowing Requirements | 53 |

| 1.26 | Reconciliation of Summary Results to Provincial Debt Changes | 53 |

| 1.27 | Key Fiscal Sensitivities | 54 |

| | | |

Part 2: Tax Measures | |

Tax Measures — Supplementary Information | 60 |

Tables: | |

| 2.1 | Summary of Tax Measures | 59 |

| | | |

Part 3: British Columbia Economic Review and Outlook | |

Summary | 67 |

British Columbia Economic Activity and Outlook | 67 |

| Labour Market | 68 |

| Consumer Spending and Housing | 69 |

| Business and Government | 71 |

| External Trade and Commodity Markets | 72 |

| Demographics | 74 |

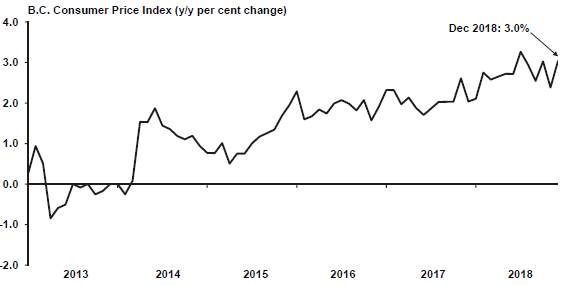

| Inflation | 74 |

Risks to the Economic Outlook | 75 |

External Outlook | 75 |

| United States | 75 |

| Canada | 78 |

| Asia | 80 |

| Europe | 80 |

Financial Markets | 81 |

| Interest Rates | 81 |

| Exchange Rate | 83 |

| | | |

Tables: | |

| 3.1 | British Columbia Economic Indicators | 68 |

| 3.2 | U.S. Real GDP Forecast: Consensus versus Ministry of Finance | 77 |

| 3.3 | Canadian Real GDP Forecast: Consensus versus Ministry of Finance | 79 |

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

ii

TABLE OF CONTENTS

| 3.4 | Private Sector Canadian Interest Rate Forecasts | 82 |

| 3.5 | Private Sector Exchange Rate Forecasts | 83 |

| 3.6.1 | Gross Domestic Product (GDP): British Columbia | 84 |

| 3.6.2 | Selected Nominal Income and Other Indicators: British Columbia | 85 |

| 3.6.3 | Labour Market Indicators: British Columbia | 85 |

| 3.6.4 | Major Economic Assumptions | 86 |

| | | |

Topic Box: | |

| The Economic Forecast Council, Budget 2019 | 87 |

| | | |

Part 4: 2018/19 Updated Financial Forecast (Third Quarterly Report) | |

Introduction | 91 |

Revenue | 93 |

Expense | 93 |

2018/19 Supplementary Estimates | 94 |

Contingencies | 95 |

Government Employment (FTEs) | 95 |

Provincial Capital Spending | 95 |

Provincial Debt | 97 |

Risks to the Fiscal Forecast | 98 |

Supplementary Schedules | 98 |

Tables: | |

| 4.1 | 2018/19 Forecast Update | 91 |

| 4.2 | 2018/19 Financial Forecast Changes | 92 |

| 4.3 | 2018/19 Supplementary Estimates | 94 |

| 4.4 | 2018/19 Capital Spending Update | 96 |

| 4.5 | 2018/19 Provincial Debt Update | 97 |

| 4.6 | 2018/19 Operating Statement | 98 |

| 4.7 | 2018/19 Revenue by Source | 99 |

| 4.8 | 2018/19 Expense by Ministry, Program and Agency | 100 |

| 4.9 | 2018/19 Expense by Function | 101 |

| 4.10 | 2018/19 Capital Spending | 102 |

| 4.11 | 2018/19 Provincial Debt | 103 |

| 4.12 | 2018/19 Statement of Financial Position | 104 |

| | | |

Appendix | 105 |

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

iii

| February 19, 2019 |

As required by Section 7(1)(d) of the Budget Transparency and Accountability Act, I confirm that Budget 2019 contains the following elements:

· Fiscal forecasts for 2019/20 to 2021/22 (provided in Part 1) and economic forecasts for 2019 to 2023 (provided in Part 3).

· A report on the advice received from the Economic Forecast Council (EFC) in November 2018 (updated in January 2019) on the economic growth outlook for British Columbia, including a range of forecasts for 2019 and 2020 (see Part 3, page 87).

· Material economic, demographic, fiscal, accounting policy and other assumptions and risks underlying Budget 2019 economic and fiscal forecasts. In particular:

· The economic forecast reflects strong, stable economic growth for British Columbia amidst ongoing global economic uncertainty. In recognition of downside risks, the economic projections assumed in Budget 2019 are prudent relative to the average of the forecasts provided by the Economic Forecast Council.

· Consistent with past practice, the economic forecast does not incorporate fiscal policy measures announced in the current budget (Budget 2019), due to the timing of decisions. These budget policy measures will be incorporated into the economic outlook in the updated forecast included in the First Quarterly Report.

· Personal and corporate income tax revenue forecasts include the preliminary 2017 income tax assessments and the corporate income tax revenue forecast is based on projections for national corporate taxable income provided by the federal government.

· Natural gas royalty forecasts continue to adopt a lower natural gas price forecast compared to the private sector average in order to maintain prudence against volatility.

· Ministry budgets include base increases for the costs arising from the fourth and final Economic Stability Dividend payable under the current Economic Stability Mandate. Budget 2019 provides ministry base budget increases over the three-year fiscal plan period to fund all ratified collective agreements reached to date under the Sustainable Services Negotiating Mandate. Budget 2019 also includes centralized funding to assist with the anticipated costs of concluding the remaining agreements consistent with the Sustainable Services Negotiating Mandate.

· The fiscal plan includes three-year financial projections for school districts, post-secondary institutions and health authorities, based on plans submitted by those entities to the Ministries of Education, Advanced Education, Skills and Training, and Health, respectively, and for the other service delivery agencies and the commercial Crown corporations.

· The financial results of the Insurance Corporation of British Columbia are a key risk to government’s fiscal plan.

· Fiscal prudence totals $1.25 billion in 2019/20, $700 million in 2020/21, and $700 million in 2021/22, being the sum of the Contingencies vote and the forecast allowance in each fiscal year. Government’s economic and fiscal prudence measures generally have resulted in government exceeding its budget targets.

To the best of my knowledge, the three-year fiscal plan contained in Budget 2019 conforms to the standards and guidelines of generally accepted accounting principles for senior governments as outlined in Note 1 of the 2017/18 Public Accounts.

I would like to recognize staff in government ministries and agencies for their contribution to this document. I would especially like to acknowledge staff in the Ministry of Finance, whose professionalism, commitment and expertise were essential to the completion of this budget and fiscal plan.

| /s/ Heather Wood |

| Heather Wood |

| Associate Deputy Minister and Secretary to Treasury Board |

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

SUMMARY | BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

| | Updated | | Budget | | | | | |

| | Forecast | | Estimate | | Plan | | Plan | |

($ millions) | | 2018/19 | | 2019/20 | | 2020/21 | | 2021/22 | |

Revenue | | 56,636 | | 59,047 | | 60,038 | | 62,458 | |

Expense | | (55,762 | ) | (58,273 | ) | (59,451 | ) | (61,573 | ) |

Forecast allowance | | (500 | ) | (500 | ) | (300 | ) | (300 | ) |

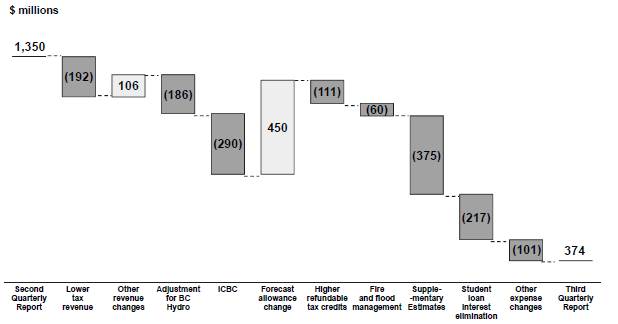

Surplus | | 374 | | 274 | | 287 | | 585 | |

| | | | | | | | | |

Capital spending: | | | | | | | | | |

Taxpayer-supported capital spending | | 4,771 | | 6,340 | | 6,837 | | 6,911 | |

Self-supported capital spending | | 4,192 | | 4,274 | | 3,333 | | 3,361 | |

| | 8,963 | | 10,614 | | 10,170 | | 10,272 | |

Provincial Debt: | | | | | | | | | |

Taxpayer-supported debt | | 43,957 | | 46,384 | | 50,454 | | 53,986 | |

Self-supported debt | | 23,459 | | 25,664 | | 26,905 | | 28,090 | |

Total debt (including forecast allowance) | | 67,916 | | 72,548 | | 77,659 | | 82,376 | |

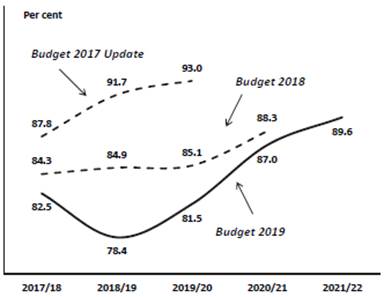

Taxpayer-supported debt to GDP ratio | | 14.9 | % | 15.0 | % | 15.7 | % | 16.1 | % |

Taxpayer-supported debt to revenue ratio | | 78.4 | % | 81.5 | % | 87.0 | % | 89.6 | % |

| | 2018 | | 2019 | | 2020 | | 2021 | |

Economic Forecast: | | | | | | | | | |

Real GDP growth | | 2.2 | % | 2.4 | % | 2.3 | % | 2.1 | % |

Nominal GDP growth | | 4.6 | % | 4.4 | % | 4.3 | % | 4.0 | % |

Making Life Better

Budget 2019 takes action to make life better for British Columbians. It includes priority investments to meet government’s three commitments to British Columbians: making life more affordable, enhancing services that people count on, and building a strong and sustainable economy that works for everyone.

Budget 2019 fulfills government’s commitment to eliminate Medical Services Plan (MSP) premiums and makes investments in key priorities: creating more opportunities for people to get ahead, CleanBC, reconciliation with First Nations, child care, housing and homelessness, and mental health services. Each year of the fiscal plan is balanced, with surpluses of $274 million in 2019/20, $287 million in 2020/21, and $585 million in 2021/22.

Making Life More Affordable

Government is launching a comprehensive $860 million investment over the fiscal plan that lays the groundwork to make sure every

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

1

SUMMARY

person can reach their full potential, with another $263 million investment in 2018/19. Budget 2019 introduces the BC Child Opportunity Benefit, income and disability assistance increases, student loan interest elimination, and other initiatives to make life better for people in British Columbia. This is in addition to fulfilling government’s commitment to eliminate MSP premiums, and investments in housing and child care.

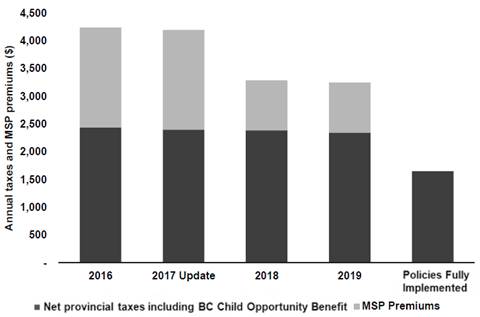

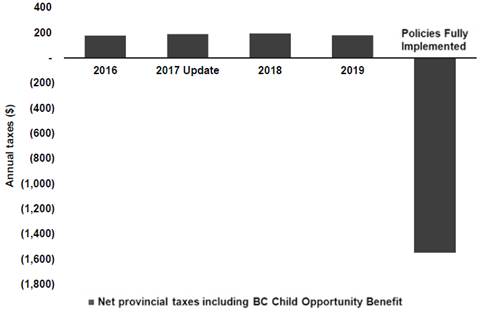

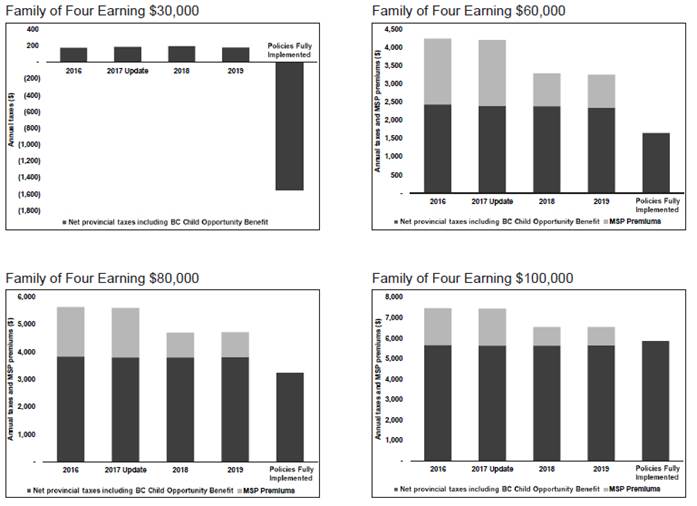

The new BC Child Opportunity Benefit will provide families with children under 18 with up to $1,600 per year for the first child, up to $2,600 per year for families with two children, and up to $3,400 per year for families with three children. In total, the benefit will provide $380 million a year for B.C. families. This new benefit, combined with the elimination of MSP premiums, will provide a significant reduction in the tax burden for lower- and middle-income families with children; a family of four earning $60,000 will see their net provincial taxes reduced by more than $2,500 per year.

Net Provincial Taxes Since Budget 2016

Family of Four Earning $60,000

Net Provincial Taxes Since Budget 2016

Family of Four Earning $30,000

Government is also eliminating interest on British Columbia student loans. This $318 million investment over fours years beginning in 2018/19 will help make post-secondary education more affordable. The typical undergraduate borrower graduates with $11,200 in British Columbia student loan debt, and will save an estimated $2,300 in interest over a 10-year repayment period.

In addition to the BC Child Opportunity Benefit, actions to address poverty include increases to income and disability assistance rates of $50 per month, for a total increase of $150 per month since Budget 2017 Update. Changes to the BC Employment Assistance Program will remove barriers to accessing assistance, such as helping clients obtain personal identification and removing restrictions on vehicle ownership.

Budget 2019 provides additional funding for housing affordability and a provincial homelessness action plan, building on the most significant provincial investment in housing ever in Budget 2018.

Services People Count On

To improve health care and patient outcomes, Budget 2019 invests $1.3 billion to enhance services for families, women and children, and coverage for additional drugs under PharmaCare. This investment also continues to support the initiatives introduced in Budget 2018, which increased access to team-based primary care and expanded seniors’ care services. To ensure British Columbians can continue to access quality health care services in the future, Budget 2019 provides $5 million to help train the health care professionals of tomorrow, including nurse practitioners, sonographers, health care assistants, and specialty nurses.

Budget 2019 also includes $74 million over three years to support new, integrated services that address mental health and addictions for children, youth and young adults, and improvements in access to quality care.

Budget 2019 invests over $550 million to ensure schools have the resources they need to support student learning. This investment will enable

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

2

SUMMARY

more teacher and education assistant hiring, which means more professionals in the classroom ensuring children have the support they need to succeed.

In addition to eliminating interest on provincial student loans, Budget 2019 invests $44 million more to help British Columbians develop the skills they need to succeed by removing barriers to access training. This investment also supports the B.C. labour force to meet the growing demands of employers and ensures that employment standards keep up with the changing needs of our labour force.

Building a Strong and Sustainable Economy

CleanBC

Through the CleanBC plan, government is reducing climate pollution by investing in cleaner transportation, energy efficient homes and buildings, clean energy strategies with Indigenous and remote communities, waste diversion and cleaner industry. Budget 2019 includes more than $679 million over the fiscal plan for CleanBC initiatives. This investment is supplemented by enhancements to the Climate Action Tax Credit totalling $223 million over three years, bringing government’s overall commitment to over $902 million.

Reconciliation with First Nations

To support Government’s commitment to reconciliation with First Nations, Budget 2019 commits to a historic revenue-sharing agreement with First Nations of B.C., with payments estimated at $297 million over three years and $3 billion over the next 25 years. This will enable First Nations to determine and invest in community priorities to support strong healthy communities and services to make life better for families.

Budget 2019 provides significant funding to support Indigenous families and children, by increasing support payments for the Extended Family Program and for foster parents caring for children.

Enhancing Business Competitiveness

B.C. is joining with the federal government to support business competitiveness in the face of ongoing global developments. B.C. will contribute over $800 million over the fiscal plan for investment incentives in capital assets, such as buildings, machinery and equipment. This will make it more attractive to invest in assets that drive business growth and free up capital that can be used to create more good, well-paying jobs for British Columbians.

Economic Outlook

An average of six private-sector forecasters expect B.C.’s economic growth to rank at the top of the provincial rankings in both 2019 and 2020.

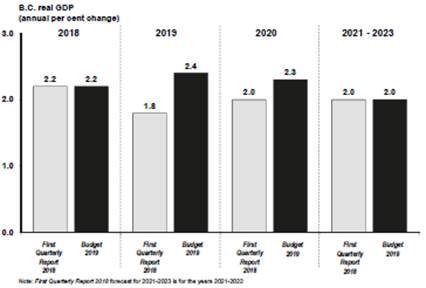

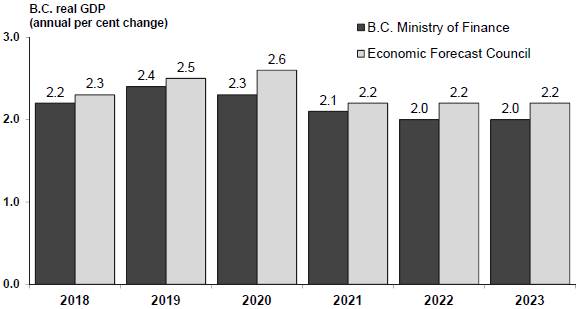

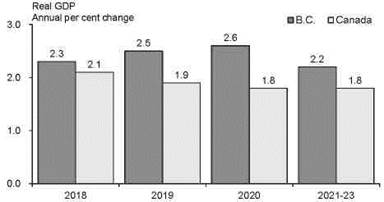

The Budget 2019 estimate for B.C. real GDP growth in 2018 remains unchanged from the projection in the First Quarterly Report 2018 at 2.2 per cent. Employment and exports performed better than expected and investment was positive, with some moderation in housing activity and consumer spending through the year. The Budget 2019 forecast for B.C. real GDP growth has increased from 1.8 per cent to 2.4 per cent in 2019 and from 2.0 per cent to 2.3 per cent in 2020, compared to the First Quarterly Report 2018. The changes partly reflect recent developments regarding the Canada-United States-Mexico Agreement (CUSMA) and the final investment decision on the LNG Canada project. The economic growth outlook for 2021 is 2.1 per cent, followed by 2.0 per cent in both 2022 and 2023, in line with previous expectations.

British Columbia’s Economic Outlook

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

3

SUMMARY

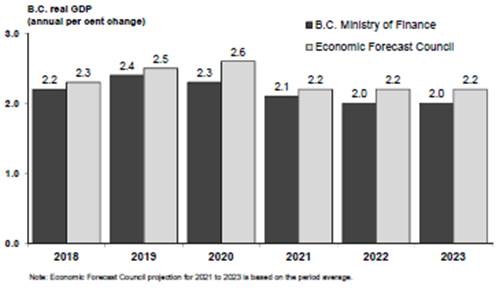

The Budget 2019 forecast for B.C. real GDP growth is below the outlook provided by the Economic Forecast Council. This is one of the levels of prudence built into the fiscal plan.

Prudent Economic Forecast

The main upside risks to the economic outlook include less domestic monetary policy tightening, a weaker Canadian dollar, and a more resilient US economy. The main downside risks include uncertainty regarding global trade policy, weakening global economic activity, lower commodity prices, as well as ongoing economic challenges in Asia and the euro zone.

Capital Investments

Budget 2019 makes new capital commitments in the health, transportation and education sectors. Taxpayer-supported infrastructure spending on hospitals, schools, post-secondary facilities, transit, and roads is forecast to be $20.1 billion, the highest level ever, over the three-year fiscal plan.

Self-supported capital spending is expected to total $11.0 billion over three years, relating primarily to power generation and transmission projects.

Debt Affordability

Debt affordability metrics have improved since Budget 2018 due to better operating results in 2017/18 and 2018/19. Capital debt requirements are partially mitigated by the elimination of the operating debt in 2018/19, which allows for government operating cash surplus to be directed towards funding capital spending.

Debt to GDP

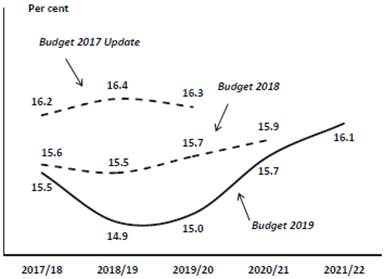

The taxpayer-supported debt-to-GDP ratio is forecast to be 16.1 per cent by 2021/22. Taxpayer-supported debt-to-revenue remains within a reasonable range over the fiscal plan period at below 90 per cent.

Debt to Revenue

Total taxpayer-supported debt is projected to increase by $10 billion over the three-year period, reaching $54 billion by 2021/22.

Risks to the Fiscal Plan

In addition to the risks to the economic outlook, the main risks to the government’s fiscal plan include:

· financial results of the Insurance Corporation of British Columbia which may continue to reflect accident and claims cost trends observed in 2018/19;

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

4

SUMMARY

· potential changes to federal government allocations for health and social transfers and cost-sharing agreements, as well as impacts on provincial income taxes arising from federal government tax policy changes; and

· increased demands for government services, such as health care, children and family services, and income assistance.

In addition, changes in the timing of capital project spending may reduce borrowing requirements and debt needed to fund capital investments in the near term.

To mitigate the risks to the fiscal plan, government incorporates four main levels of prudence in its projections:

· government has included forecast allowances throughout the three-year period: $500 million in 2019/20, $300 million in 2020/21, and $300 million in 2021/22 to guard against volatility, including revenue changes;

· the fiscal plan includes a Contingencies vote allocation of $750 million in 2019/20, and $400 million per year in 2020/21 and 2021/22, to help manage unexpected pressures and fund priority initiatives;

· the Budget 2019 outlook for B.C.’s real GDP growth is lower than the outlook provided by the Economic Forecast Council (0.1 percentage point lower in 2019, 0.3 percentage points lower in 2020, 0.1 percentage point lower in 2021, and 0.2 percentage points lower in 2022 and 2023); and

· the natural gas revenue forecast incorporates additional prudence by using a price forecast that is lower than the average of private sector forecasts.

Conclusion

Budget 2019 takes action to make life better for British Columbians by fulfilling government’s commitment to eliminate Medical Services Plan premiums and making investments in initiatives that will create opportunities for people to get ahead, CleanBC, reconciliation with First Nations, child care and housing, and mental health services. Priority investments meet government’s three commitments to British Columbians: making life more affordable, enhancing services that people count on, and building a strong and sustainable economy that works for everyone.

Each year of the fiscal plan is balanced, with surpluses of $274 million in 2019/20, $287 million in 2020/21, and $585 million in 2021/22.

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

5

PART 1 | THREE YEAR FISCAL PLAN

Table 1.1 Three Year Fiscal Plan

| | Updated | | Budget | | | | | |

| | Forecast | | Estimate | | Plan | | Plan | |

($ millions) | | 2018/19 | | 2019/20 | | 2020/21 | | 2021/22 | |

Revenue | | 56,636 | | 59,047 | | 60,038 | | 62,458 | |

Expense | | (55,762 | ) | (58,273 | ) | (59,451 | ) | (61,573 | ) |

Forecast allowance | | (500 | ) | (500 | ) | (300 | ) | (300 | ) |

Surplus | | 374 | | 274 | | 287 | | 585 | |

Capital spending: | | | | | | | | | |

Taxpayer-supported capital spending | | 4,771 | | 6,340 | | 6,837 | | 6,911 | |

Self-supported capital spending | | 4,192 | | 4,274 | | 3,333 | | 3,361 | |

| | 8,963 | | 10,614 | | 10,170 | | 10,272 | |

Provincial Debt: | | | | | | | | | |

Taxpayer-supported debt | | 43,957 | | 46,384 | | 50,454 | | 53,986 | |

Self-supported debt | | 23,459 | | 25,664 | | 26,905 | | 28,090 | |

Total debt (including forecast allowance) | | 67,916 | | 72,548 | | 77,659 | | 82,376 | |

Taxpayer-supported debt to GDP ratio | | 14.9 | % | 15.0 | % | 15.7 | % | 16.1 | % |

Taxpayer-supported debt to revenue ratio | | 78.4 | % | 81.5 | % | 87.0 | % | 89.6 | % |

Introduction

Budget 2019 takes action to make life better for British Columbians. It includes priority investments to meet government’s three commitments to British Columbians: making life more affordable, enhancing services that people count on, and building a strong and sustainable economy that works for everyone. These measures are funded by improved revenues from existing sources. Each year of the fiscal plan is balanced, with surpluses of $274 million in 2019/20, $287 million in 2020/21, and $585 million in 2021/22.

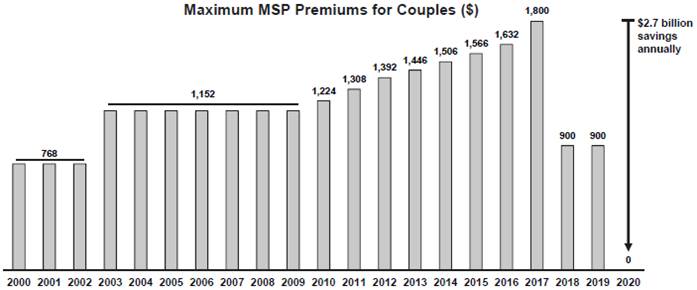

In Budget 2019, government is moving ahead with the full elimination of Medical Services Plan premiums, saving individuals up to $900 a year, and families up to $1,800 a year, for a total reduction of $2.7 billion. In addition, Budget 2019 introduces the new BC Child Opportunity Benefit, a historic investment that provides $380 million for B.C. families. This new benefit, combined with the elimination of MSP premiums, will provide a significant reduction in the tax burden for lower- and middle-income families with children.

The new operating funding initiatives are discussed in the Expense section starting on the next page. Details on the forecasts for the Province’s revenue sources are provided in the Revenue section, starting on page 30. The Capital investments section is on page 38, followed by the Debt section on page 51, and a discussion on the risks to the fiscal plan on page 54.

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

7

THREE YEAR FISCAL PLAN

Expense

Consolidated Revenue Fund Spending

Making Life More Affordable

Creating More Opportunities for People to Get Ahead

Budget 2019 introduces a range of measures to help make sure every British Columbian can reach their full potential. In addition to fulfilling government’s commitment to eliminate MSP premiums and building on previous commitments to improve housing affordability and affordable child care, Budget 2019 introduces several new initiatives.

Table 1.2 Creating More Opportunities for People to Get Ahead

($ millions) | | 2019/20 | | 2020/21 | | 2021/22 | | Total | |

BC Child Opportunity Benefit | | — | | 125 | | 250 | | 375 | |

Student Loan Interest Elimination | | 31 | | 31 | | 31 | | 93 | |

Increase to Income and Disability Assistance Rates and Enhancements | | 98 | | 103 | | 106 | | 307 | |

Increase Support Payments for Children in EFP/PAA | | 6 | | 6 | | 6 | | 18 | |

Increase Support Payments for Children of Foster Parents | | 16 | | 16 | | 16 | | 48 | |

Ensure Children in Care Benefit from Provincial Tax Benefits | | — | | 6 | | 13 | | 19 | |

Total in fiscal plan period | | 151 | | 287 | | 422 | | 860 | |

Student Loan Interest Elimination — Write-Down in 2018/19 | | | | | | | | 225 | |

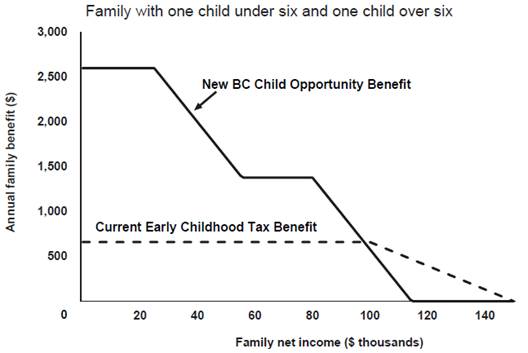

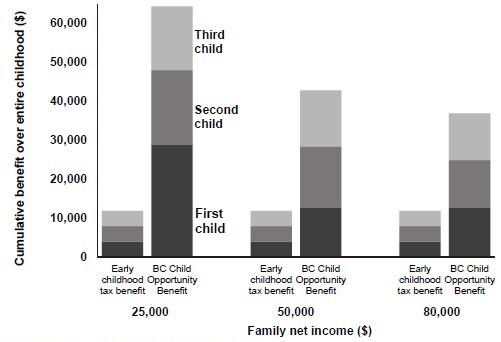

BC Child Opportunity Benefit: The new BC Child Opportunity Benefit will provide families with children under 18 with up to $1,600 per year for the first child, up to $2,600 per year for families with two children, and up to $3,400 per year for families with three children. The BC Child Opportunity Benefit supports families with children under 18, whereas the early childhood tax benefit only applied to children under age 6. This means the new benefit will provide significantly more support for children over their entire childhood. The table below illustrates how the new benefit will provide more support for children.

Effective October 1, 2020, a new BC Child Opportunity Benefit will be combined with the early childhood tax benefit into a single new benefit. The new refundable tax credit provides $380 million annually to B.C. families with children under the age of 18. Budget 2019 includes incremental funding of $125 million in 2020/21 and $250 million in 2021/22 to support the transition from the early childhood tax benefit to the BC Child Opportunity Benefit. Further details of this new tax benefit are provided in Part 2: Tax Measures.

Table 1.3 - BC Child Opportunity Benefit

| | Maximum Annual Benefit | | Maximum Benefit over

Entire Childhood* | |

| | Existing

Benefit | | New

BC Child

Opportunity Benefit | | Existing

Benefit | | New

BC Child

Opportunity Benefit | |

One Child | | $ | 660 | | $ | 1,600 | | $ | 3,960 | | $ | 28,800 | |

Two Children | | $ | 1,320 | | $ | 2,600 | | $ | 7,920 | | $ | 48,000 | |

Three Children | | $ | 1,980 | | $ | 3,400 | | $ | 11,880 | | $ | 64,400 | |

* Calculation assumes each child is born two years apart.

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

8

THREE YEAR FISCAL PLAN

Chart 1.1 Net Provincial Taxes Since Budget 2016

This new benefit, combined with the elimination of MSP premiums, will provide a significant reduction in the tax burden for lower- and middle-income families with children.

Student Loan Interest Elimination: To make education more affordable, Government is eliminating interest charges on B.C. student loans. As of February 19, 2019, interest will no longer accrue on new and existing student loans provided through the British Columbia Student Loan Program (previously, interest was charged at the prime rate). Government is investing a total of $318 million in 2018/19 and over the fiscal plan period to implement these changes. Borrowers will collectively save an estimated $22 million in interest payments on these loans in 2019/20.

The average undergraduate borrower has $11,200 in British Columbia student loan debt upon graduation and total federal and provincial student loan debt totaling $28,000. Eliminating interest on the provincial portion will save this borrower an estimated $2,300 over the 10-year repayment period.

Income Assistance and Disability Assistance Increases and Improvements: To help the province’s most vulnerable pay for essential needs, Budget 2019 provides $307 million over the fiscal plan to increase income assistance and disability assistance rates and enhance the BC Employment and Assistance Program. Effective April 1, 2019, income and disability assistance rates will increase by $50 per month. When taken together with

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

9

THREE YEAR FISCAL PLAN

an increase provided in Budget 2017 Update, the rate for a single individual on income assistance will have increased by a total of 25 per cent, and by 15 per cent for a single individual on disability assistance.

Enhancements to the BC Employment Assistance Program will remove barriers to accessing assistance, especially for youth, those with mental health and addictions issues, and persons with disabilities. These enhancements will include:

· removing requirements that make it harder for older adults, youth, and persons with mental health issues to access the program;

· helping clients obtain personal identification so they can access income assistance, essential services, and overcome personal barriers to securing housing and employment;

· aligning the definition of spouse to other benefit programs in order to ensure fairness in the level of support couples receive; and

· extending the shelter rate to those paying room and board to a family member.

Government has already doubled the crisis food supplement from $20 per person, per month to $40 per person, per month and increased the crisis utility supplement. Budget 2019 provides further enhancements to the BC Employment Assistance Program, which are part of the homelessness action plan (see page 11).

Supporting Children in Care: Importantly, Budget 2019 provides $18 million over three years to support children who are placed in the care of extended family caregivers and adoptive parents. Support payments for the Extended Family Program, which help to cover the cost of basic necessities such as food, clothing and shelter, will increase by approximately 75 per cent, and for the Post-Adoption Assistance program by 15 per cent, benefiting almost 2,500 children.

Support payments for foster parents, which are similarly intended to cover the cost of basic necessities, such as food, clothing, and shelter, were last increased in April 2009. These support payments will be increased by $179.09 per month, effective April 1, 2019. Budget 2019 provides $16 million annually for this purpose. This change will increase support payments by approximately 20 per cent, and will benefit more than 7,200 vulnerable children.

By providing more funding for Indigenous extended family caregivers, government is responding to recommendations from Indigenous communities and Grand Chief Ed John to keep more Indigenous children with their families rather than taking them into the care of the Province. By providing more funding to foster parents, government is recognizing the important work they do caring for children.

Furthermore, children in the care of the Province have not previously benefited from provincial child tax benefits. Budget 2019 addresses this inequity. To ensure children in care benefit from provincial child tax benefits, the Ministry of Children and Family Development will receive $6 million in 2020/21 and $13 million in 2021/22 for programming that will enrich the lives of these children.

Legal Clinics: To improve access to justice, government is providing funding to continue consultation and development of the Indigenous Justice Strategy and to pilot legal clinics in up to eight communities throughout the province. In partnership with

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

10

THREE YEAR FISCAL PLAN

the Law Foundation of British Columbia, legal clinics will provide access to justice community programs and increase access to legal advice and advocacy.

Homes for B.C.

Government is taking meaningful action to address the significant housing challenges facing British Columbians as a result of increasingly unaffordable house prices and a lack of affordable and market rental housing. Government has committed to building 114,000 units of affordable market rental, non-profit, co-op, supportive and owner-purchased housing in partnership with local governments, the federal government, Indigenous peoples, the non-profit and for-profit sectors, and faith groups.

Budget 2017 Update introduced the initial steps taken to address needed housing supply, which included capital investments of $499 million to help build 1,700 new units of affordable rental housing and 2,000 modular units for housing people who are homeless. Additional funding was also provided to improve landlord and tenant services.

Budget 2018 launched the most significant provincial investment ever made in housing — $7 billion over 10 years. The Province announced investments to build and maintain affordable rental housing, provide supportive housing for at-risk and vulnerable British Columbians, introduce a new student housing program for public post-secondary institutions, and increase support to low-income families and seniors who rent.

Budget 2019 continues to build on government’s historic Budget 2018 housing investments. In addition to Budget 2018 commitments, Budget 2019 provides additional operating funding of $24 million over three years.

To provide greater certainty to housing providers, government is accelerating the payment of $38 million in grants to housing providers in 2018/19. This funding will be used to reduce ongoing borrowing costs to improve the range of affordable market rents.

Table 1.4 Homes for B.C.

($ millions) | | 2018/19 | | 2019/20 | | 2020/21 | | 2021/22 | | Total | |

Incremental Housing Initiatives | | — | | 4 | | 6 | | 14 | | 24 | |

Deepening Affordability of Housing Projects | | 38 | | — | | — | | — | | 38 | |

Homelessness Action Plan | | — | | 5 | | 5 | | 5 | | 15 | |

Total | | 38 | | 9 | | 11 | | 19 | | 77 | |

Budget 2019 also launches a province-wide homelessness action plan. As part of the homelessness action plan, government will:

· Implement a supportive housing response strategy, including building 200 modular units and creating interim and permanent housing options to house people who are homeless or at risk of homelessness. This will bring the total to 2,200 modular units.

· Enhance the BC Employment Assistance program to better support people who are homeless or at risk of homelessness to find stable housing, including:

· increasing the maximum value of assets clients can have prior to receiving assistance;

· removing restrictions on vehicles a client can own to use for day-to-day transportation;

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

11

THREE YEAR FISCAL PLAN

· supporting clients to leave assistance for short-term opportunities by simplifying the re-application process;

· increasing the crisis supplement for shelter; and

· helping clients with security deposits in order to prevent homelessness.

The homelessness action plan will also:

· conduct a provincewide homelessness count in 2020; and

· establish a provincial homelessness co-ordination unit.

To support these initiatives, Budget 2019 provides $15 million in operating funding for the Ministry of Social Development and Poverty Reduction and the Ministry of Municipal Affairs and Housing, as well as $61 million in capital funding for the Ministry of Municipal Affairs and Housing.

To help combat poverty and homelessness, the Ministry of Social Development and Poverty Reduction is also contributing $10 million in 2018/19 for a provincial rent bank. This will provide access to loans for vulnerable families in need of immediate assistance to avoid eviction from their homes. Through this measure, families will be provided protection from falling into homelessness and deep poverty.

Child Care BC

Finding child care is a significant challenge for families in British Columbia. Budget 2018 made a historic $1 billion investment in Child Care BC — government’s plan to bring affordable, accessible, and quality child care to families across the province.

Budget 2018 provided $630 million over three years for two key affordability initiatives: the Affordable Child Care Benefit and Child Care Fee Reduction Initiative. Since September 2018, the new Affordable Child Care Benefit has been helping families by reducing the cost of child care by up to $1,250 per month, per child.

Since April 2018, the Child Care Fee Reduction Initiative has helped lower the cost of licensed child care for families with young children by providing increased funding to child care providers to reduce child care fees by up to $350 per month. The uptake of the fee reduction program by child care providers has been even more successful than anticipated, with an estimated 88 per cent of eligible child care spaces now participating. Budget 2019 provides an additional $9 million annually to support the Child Care Fee Reduction Initiative and associated Child Care Operating Fund program.

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

12

THREE YEAR FISCAL PLAN

Enhancing Services that People Count On

Budget 2019 makes critical investments in services and programs. Significant new investments will improve access to quality health care, support kids in the classroom and ensure our most vulnerable citizens have the supports they need. Budget 2019 provides just over $100 million annually to public-sector employers to support the transition to the Employer Health Tax. In addition, government is committed to ensuring fair and affordable compensation for public-sector employees through freely negotiated collective agreements. As such, Budget 2019 provides funding for the Sustainable Services Negotiating Mandate and the final Economic Stability Dividend.

Investing in Health Care

To improve health services and patient outcomes, Budget 2019 provides more than $1.3 billion over three years to the Ministry of Health. This investment includes supports for the BC Children’s and Women’s hospitals to provide services to women, children, newborns and families. This investment will also support the BC Cancer Agency and provide for new drugs to be covered under PharmaCare. This is in addition to the $3.8 billion that has been provided since Budget 2017 Update for services for seniors across the continuum of health care, expanding team-based care, improving the affordability of prescription drugs for low- and middle-income individuals and families, and addressing other needs in the health-care system.

Government is investing $89 million in 2018/19 in grants to health and life sciences research organizations to strengthen the Province’s competitiveness in attracting and retaining health researchers, and to support research, entrepreneurship and commercialization in life sciences. This provincial contribution is expected to attract over $200 million in external funding toward these research activities to improve health and other outcomes for British Columbians.

Improving Mental Health Services and Responding to the Opioid Overdose Emergency

Budget 2019 provides $74 million over three years to enhance mental health and addictions services for children, youth and young adults. This investment focuses on services to support the health and wellbeing of young children, enhance mental health for those at school age, and expand access for children and youth seeking mental health and addictions services.

Funding will be targeted to begin implementing a coordinated mental health and addictions system for children and youth that will link schools, community services and team-based primary care. This funding will support parent-child social and emotional development programs for young children, school based programs for mental wellness promotion, prevention and early intervention for students at risk or experiencing early signs of mental health or substance use challenges, and specialized service teams comprised of educators, counsellors, mental health practitioners, substance use workers and other professionals to support children, youth and their families.

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

13

THREE YEAR FISCAL PLAN

The investment will also expand the number of “one-stop shop” Foundry centres, which bring mental health, substance use and core health and social services together in a single location so that young people aged 12-25 can find the support they need - both online and in their community.

In addition, more than $30 million over the fiscal plan is provided to increase efforts in responding to the opioid overdose emergency. The funding will be directed to initiatives delivered by BC Emergency Health Services and the BC Centre for Disease Control. This investment will significantly expand programs to meet increased demand for paramedics in rural and remote areas and broaden distribution of life-saving naloxone kits. This new investment is in addition to the total $578 million provided since Budget 2017 Update for the opioid overdose emergency response and initiatives to address mental health and substance use.

These investments are guided by the Ministry of Mental Health and Addictions, and will be delivered by the Ministry of Health and the Ministry of Children and Family Development.

Table 1.5 Investing in Health Care and Education

($ millions) | | 2018/19 | | 2019/20 | | 2020/21 | | 2021/22 | | Total | |

Improving Access to Health Care Services | | — | | 60 | | 60 | | 699 | | 819 | |

Additional Drugs Available Under PharmaCare | | — | | 14 | | 14 | | 14 | | 42 | |

Research and Commercialization in Life Sciences | | 89 | | — | | — | | — | | 89 | |

Improving Mental Health and Addictions Services | | — | | 18 | | 26 | | 30 | | 74 | |

Responding to the Opioid Overdose Emergency | | — | | 10 | | 10 | | 10 | | 30 | |

K-12 Public Schools | | — | | 182 | | 184 | | 184 | | 550 | |

Total | | 89 | | 284 | | 294 | | 937 | | 1,604 | |

Investing in K-12 Education

As K-12 enrolment is projected to continue to grow, Budget 2019 provides an additional $550 million over three years to the Ministry of Education to support public education. Budget 2019 also provides $31 million over three years for independent schools, where enrolment is also growing.

Public school funding includes an additional $58 million over three years for the Classroom Enhancement Fund, to reflect the 2016 Supreme Court of Canada decision on class size and composition. A total of $423 million is now allocated annually which has already enabled the hiring of over 4,000 teachers, including 700 special education teachers and 160 more teacher psychologists and counsellors, since 2017.

Enhancing Supports

Income and Disability Assistance and Community Living BC: Budget 2019 ensures continued support for persons receiving income or disability assistance and/or support from Community Living BC. The Ministry of Social Development and Poverty Reduction will receive $44 million over three years to support growth in these programs. Community Living BC provides critical support to over 22,000 adults with developmental disabilities.

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

14

THREE YEAR FISCAL PLAN

Table 1.6 Enhancing Supports

($ millions) | | 2019/20 | | 2020/21 | | 2021/22 | | Total | |

Income and Disability Assistance and Community Living BC | | | | | | | | | |

Income and Disability Assistance | | 2 | | 6 | | 36 | | 44 | |

Increasing Payments for Community Living BC Home Share Provider | | 9 | | 18 | | 18 | | 45 | |

Vulnerable Children and Youth | | | | | | | | | |

Increasing the Benefit Rate and Reducing the Waitlist for Respite | | 6 | | 6 | | 6 | | 18 | |

Improving Residential Care for Children and Youth | | 31 | | 31 | | 31 | | 93 | |

Total | | 48 | | 61 | | 91 | | 200 | |

In addition, payments for Community Living BC home-share providers will increase for the first time since April 2009. These care providers play a vital role in ensuring adults with developmental disabilities are able to live as independently as possible. Budget 2019 provides $45 million over the fiscal plan to increase funding for the home sharing program by 15 per cent.

Supporting Vulnerable Children and Youth: Parents who care for children with special needs on a day-to-day basis will receive more rest and relief. An additional $6 million in annual funding for the Ministry of Children and Family Development will be used to increase the respite benefit amount by 10 per cent and significantly reduce the waitlist for respite services.

In addition, Budget 2019 directly supports children and youth with special needs and vulnerable children living in contracted residential care with $94 million over three years for the Ministry of Children and Family Development. Funding increases will support service levels in the ministry’s autism and medical benefits programs ($11 million annually) and ensure that residential care facilities are prepared to address the needs of individual children and youth ($20 million annually).

Improving Access to Justice and Public Safety

Government is providing funding for programming related to anti-money laundering, cannabis legalization, gun and gang violence, and road safety. Budget 2019 provides the Ministry of Attorney General with $6 million in base funding over the fiscal plan to update equipment, complete mandatory health and safety updates, and fund operating expenses related to capital investments. An additional $3 million is provided over the fiscal plan to support compensation and retention of court clerks, expand capacity at Justice Centres, and modernize IT infrastructure at the Independent Investigations Office.

To support the ongoing operations of the Intersection Safety Camera Red Light program, which targets and tickets unsafe drivers travelling through red lights in intersections across the province, Budget 2019 provides the Ministry of Public Safety and Solicitor General with $6 million over three years. An additional $6 million is provided over the fiscal plan period to maintain service levels in the Crime Victim Assistance Program, which supports victims of violent crime and their families by offsetting financial losses and assisting in recovery.

Table 1.7 Improving Access to Justice and Public Safety

($ millions) | | 2018/19 | | 2019/20 | | 2020/21 | | 2021/22 | | Total | |

Enhancing Capacity in the Justice System | | — | | 2 | | 3 | | 4 | | 9 | |

Intersection Safety Camera Red Light Program | | — | | 2 | | 2 | | 2 | | 6 | |

Crime Victim Assistance Program | | — | | 2 | | 2 | | 2 | | 6 | |

Civil Resolution Tribunal | | 8 | | 8 | | 8 | | 8 | | 32 | |

Total | | 8 | | 14 | | 15 | | 16 | | 53 | |

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

15

THREE YEAR FISCAL PLAN

Following through on government’s commitment to provide a more accessible, timely, and affordable alternative to the traditional court system, Budget 2019 commits $8 million annually to support the Civil Resolution Tribunal. The Civil Resolution Tribunal allows for 24/7 online access to information, early dispute resolution processes, and expedited adjudication by diverting disputes from arbitration and the courts.

These commitments build on funding since Budget 2017 Update. In Budget 2018, government made significant new investments in access to justice initiatives ($26 million over three years) and victim service and violence against women programs ($23 million over four years). In Budget 2017 Update, the Ministry of Public Safety and Solicitor General received $32 million over three years to respond to the fentanyl crisis.

Building a Strong and Sustainable Economy

CleanBC Plan

Budget 2019 includes over $679 million in funding for the CleanBC plan to reduce carbon pollution and promote the use of our clean energy to power B.C.’s economy. This includes $354 million in new program funding and $26 million in capital funding over three years for new initiatives.

In addition to the funding for the specific initiatives detailed below, $299 million is specifically allocated in Contingencies funding over the fiscal plan. This will ensure additional programs currently being developed are fully funded.

This investment is supplemented by enhancements to the Climate Action Tax Credit totalling $223 million over three years, bringing government’s overall commitment to over $902 million.

Cleaner transportation: Budget 2019 includes over $107 million in operating funding to help British Columbians switch to cleaner transportation options, including making zero-emission vehicles more affordable and investing in supporting infrastructure. This funding is allocated as follows:

· $90 million is being provided to the Ministry of Energy, Mines and Petroleum Resources to encourage and accelerate the adoption of zero-emission vehicles in the province. Funding will support a range of initiatives, including:

· $42 million to continue existing point-of-sale incentives for battery electric and hydrogen fuel cell vehicles. This will save British Columbians up to $6,000 on the purchase of a zero-emission vehicle and approximately $1,500 per year in fuel costs;

· $20 million to support the creation of new public fast-charging and hydrogen fueling stations to make it easier to fuel zero-emission vehicles;

· $10 million to offer more incentives for medium- and heavy-duty vehicles, including trucking, port and airport ground equipment, buses, and marine vessels;

· $6 million to support training programs for automotive technicians and electricians, as well as research and commercialization, in the zero-emission vehicle sector;

· $6 million to help light-duty vehicle fleets adopt zero-emission vehicles;

· $5 million for incentives for the installation of home and workplace charging stations; and

· $1 million to support implementation and public outreach.

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

16

THREE YEAR FISCAL PLAN

Table 1.8 CleanBC - Operating, Capital and Contingencies Allocations

($ millions) | | 2019/20 | | 2020/21 | | 2021/22 | | Total | |

CleanBC Operating Funding | | | | | | | | | |

Cleaner Transportation | | 96 | | 6 | | 5 | | 107 | |

Energy Efficient Buildings | | 10 | | 19 | | 29 | | 58 | |

Indigenous and Remote Communities | | 18 | | — | | — | | 18 | |

Climate Strategy Resourcing | | 1 | | 1 | | 1 | | 3 | |

CleanBC Program for Industry | | 56 | | 56 | | 56 | | 168 | |

Total Operating Funding | | 181 | | 82 | | 91 | | 354 | |

| | | | | | | | | |

CleanBC Capital Funding | | | | | | | | | |

Energy Efficient Buildings | | 8 | | 9 | | 9 | | 26 | |

Total Capital Funding | | 8 | | 9 | | 9 | | 26 | |

| | | | | | | | | |

CleanBC Contingencies Funding | | | | | | | | | |

CleanBC Programming Under Development | | 37 | | 87 | | 175 | | 299 | |

Total | | 37 | | 87 | | 175 | | 299 | |

Total Operating, Capital and Contingencies Allocated to CleanBC | | | | | | | | 679 | |

· The Ministry of Energy, Mines and Petroleum Resources will receive $3 million over three years to support the development and implementation of a Zero-Emission Vehicle (ZEV) standard. The standard will require automakers to meet an escalating annual percentage of new light-duty zero-emission vehicle sales, reaching 10 per cent by 2025, 30 per cent by 2030, and 100 per cent by 2040. Complemented by consumer incentive programs offered by the Province, the ZEV standard will help ensure cleaner vehicles are widely available and competitively priced.

· Government is investing over $5 million over three years for battery electric vehicle charging stations at highway rest areas and buildings owned by the Province. Expanding the Province’s charging station network will enable longer-range travel by cleaner vehicles.

· Government is providing $3 million over three years for a new heavy-duty vehicle efficiency program. This program will help businesses reduce their fuel consumption and support the Province in meeting its greenhouse gas (GHG) emission reduction targets.

· $6 million will be provided to initiatives supporting active transportation options, including walking and cycling, over a three-year period.

Energy Efficient Buildings: Budget 2019 provides over $58 million in operating funding in addition to capital funding to make homes and buildings in B.C. more energy efficient. Investments include:

· Expansion of energy-efficiency incentives delivered in partnership with BC Hydro, FortisBC, and BC Housing. These incentives are provided to households and businesses for the installation of high-efficiency heating equipment and building envelope improvements to reduce GHG emissions and reduce energy use. Additional funding of $41 million over three years will supplement the $24 million previously provided by the Province and the federal government, allowing incentives to reach significantly more homes and businesses.

· Energy efficiency upgrades and emissions reduction projects in more than 1,500 government owned and leased buildings. The Ministry of Citizens’ Services is allocated $14 million in operating funding and almost $26 million in capital funding

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

17

THREE YEAR FISCAL PLAN

to support these projects that will reduce energy costs. This investment will create opportunities throughout the province for local businesses, Indigenous peoples, professions and trades to develop building retrofit expertise that can be applied in their communities.

· Development of a net-zero building code applicable to all new buildings by 2032, new standards for alterations to existing buildings, and new energy efficiency standards. To support this work, the Ministry of Municipal Affairs and Housing and the Ministry of Energy, Mines and Petroleum Resources will receive $3 million over three years.

Indigenous and Remote Communities: Budget 2019 includes $18 million for two initiatives with Indigenous and remote communities:

· $15 million will support B.C.’s new Remote Community Clean Energy Strategy, which aims to reduce diesel consumption for electricity generation in remote communities by 80 per cent by 2030. The funding will help remote communities served by B.C.’s 22 largest diesel-powered electricity generation stations to reduce or eliminate diesel generation and replace it with energy from cleaner sources.

· Government is contributing $3 million to the BC Indigenous Clean Energy Initiative, with matching funding from the federal government. The funding supports both on-grid and off-grid Indigenous communities working to advance energy efficiency and clean energy projects for B.C.’s clean energy future.

Climate Strategy Resourcing: To support the implementation and monitoring of the CleanBC plan and the development of new initiatives, $3 million over three years is being provided to the Ministry of Environment and Climate Change Strategy.

Organics Collection and Processing Infrastructure: To reduce greenhouse gas emissions through waste diversion, an initial investment of $1 million over three years is provided to the Ministry of Environment and Climate Change Strategy to develop a program to increase organics collection and processing capacity in communities around the province.

CleanBC Program for Industry: Budget 2019 provides $168 million over three years for the CleanBC program for industry announced in Budget 2018. The program is designed to support large industrial operations, such as pulp and paper mills, natural gas operations and refineries, and large mines in reducing GHG emissions through targeted incentives.

This program will direct a portion of the carbon tax paid by industry to:

· an industrial incentive that reduces carbon-tax cost for operations meeting world leading emissions benchmarks; and,

· a clean industry fund that invests a portion of industrial carbon tax revenue directly into emissions reduction projects.

The fund and the incentive work together as the fund invests in GHG reducing projects, and industrial operations with lower emissions pay less carbon tax and receive larger incentives.

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

18

THREE YEAR FISCAL PLAN

Reconciliation with First Nations

Revenue Sharing: Supporting self-governance and self-determination is a cornerstone of government’s commitment to reconciliation with First Nations. Budget 2019 provides for gaming revenue-sharing payments of $297 million over the three years for First Nations communities. This revenue stream will provide stable, long-term funding estimated at over $3 billion over the next 25 years. First Nations will be able to invest in their community priorities ranging from health and wellness, housing, infrastructure, training, environmental protection and economic development. See page 37 for additional details.

Supporting Indigenous Families and Children: As already noted, Budget 2019 increases support payments for foster parents, ensures children and families in care benefit from provincial tax benefits, and increases support payments for extended family members caring for children. These changes begin to address some of the issues resulting from decades of Indigenous children being brought into the care of the Province. The changes are in support of recommendations from Indigenous communities and Grand Chief Ed John to keep more Indigenous children with their families.

Budget 2019 takes further action to support government’s commitment to reconciliation with Indigenous peoples. The Ministry of Indigenous Relations and Reconciliation is receiving $6 million in funding over three years for new staff to support continued work on treaties and other agreements, environmental stewardship initiatives, and socio-economic development. This builds on an initial investment made in Budget 2018.

Table 1.9 Reconciliation with First Nations

($ millions) | | 2019/20 | | 2020/21 | | 2021/22 | | Total | |

Revenue Sharing | | 197 | | — | | 100 | | 297 | |

Support for Indigenous Reconciliation Work | | 2 | | 2 | | 2 | | 6 | |

Total | | 199 | | 2 | | 102 | | 303 | |

Securing Our Resources for Tomorrow

Coast Forest Revitalization: Budget 2019 provides the Ministry of Forests, Lands, Natural Resource Operations and Rural Development with $10 million over three years to support the Coast Forest Sector Revitalization Initiative. Funding will support the objectives of diversifying forest tenures and manufacturing, increasing domestic timber processing and collaborating and consulting with Indigenous governments, industry committees, and other stakeholders.

Forest Carbon Initiative: Budget 2019 provides the Ministry of Forests, Lands, Natural Resource Operations and Rural Development with funding of $13 million over three years to support the Forest Carbon Initiative which is delivered in partnership with the Forest Enhancement Society of British Columbia and cost-shared with the Government of Canada. Funding targets the reduction of carbon emissions in the forest sector and the capture of carbon through the restoration of forests damaged by disease and wildfire.

Table 1.10 Securing Resources for Tomorrow

($ millions) | | 2018/19 | | 2019/20 | | 2020/21 | | 2021/22 | | Total | |

Coast Forest Sector Revitalization Initiative | | — | | 3 | | 3 | | 4 | | 10 | |

Forest Carbon Initiative | | — | | 3 | | 4 | | 6 | | 13 | |

Fire Management Vote | | — | | 37 | | 37 | | 37 | | 111 | |

Fire Management - Statutory Spending | | 551 | | — | | — | | — | | 551 | |

Total | | 551 | | 43 | | 44 | | 47 | | 685 | |

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

19

THREE YEAR FISCAL PLAN

Wildfire Resiliency: In addition to the $60 million provided in 2018/19 for the Community Resiliency Investment Program, Budget 2019 increases base funding for fire management from $64 million to $101 million per year in recognition of increased wildfire activity in recent years. This will provide for additional wildfire control capacity and increase communication resourcing for community engagement during the wildfire season. Costs above this base amount will continue to be funded through the statutory spending authority provided for under the Wildfire Act and managed within the prudence provided for in the fiscal plan. These investments are incremental to funding provided in Budget 2018 for wildfire resiliency and recovery activities.

Investing in Higher Education and Skills Training

Adult Basic Education and English Language Learning: Budget 2019 provides an additional $18 million over three years to support British Columbians who upgrade their education and skills. The additional funding will increase the total annual budget for these programs to $24 million annually, enabling more people to access basic education and develop skills used to improve their lives.

Increasing Participation in Trades: Budget 2019 provides an additional $3 million over three years to enable the Industry Training Authority to increase hands-on support for apprentices, employers and Indigenous communities to engage with and navigate through the trades training system. The funding will also support the development of a Performance Management Framework, including a system-wide reporting tool to inform and evaluate its initiatives and report on progress toward inclusion of Indigenous peoples as well as women and other equity-seeking groups in skilled trades.

Expanding Access to Health Training Programs: Budget 2019 provides $5 million over three years to train and graduate more health-care providers through public post-secondary institutions in urban, rural, remote and under-served communities. The expansion is targeted to a number of professions that are facing shortages that are impacting the delivery of health care. This funding continues government’s commitments to improve health outcomes and to deliver a patient-centered, integrated system of care across all regions of the province.

Expanding Access to Technology Training Programs: An additional $5 million in annual funding will be provided for post-secondary institution grants in 2021/22 to support technology programming, increasing total annual funding for this program to $41 million.

Table 1.11 Investing in Higher Education and the Workforce

($ millions) | | 2019/20 | | 2020/21 | | 2021/22 | | Total | |

Removing barriers to access skills training | | | | | | | | | |

Adult Basic Education and English Language Learning | | 6 | | 6 | | 6 | | 18 | |

Increasing Participation in Trades | | 1 | | 1 | | 1 | | 3 | |

Investing in the Workforce | | | | | | | | | |

Expanding Access to Health Training Programs | | 1 | | 2 | | 2 | | 5 | |

Expanding Access to Technology Training Programs | | — | | — | | 5 | | 5 | |

Employment Standards Branch Transformation | | 4 | | 5 | | 5 | | 14 | |

Total | | 12 | | 14 | | 19 | | 45 | |

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

20

THREE YEAR FISCAL PLAN

Improving B.C.’s Employment Standards

Budget 2019 provides $14 million over three years to support the transformation of the Employment Standards Branch in the Ministry of Labour, to update employment standards to reflect the changing nature of work and ensure standards are applied fairly and consistently. The funding will also be used to implement the Temporary Foreign Worker Protection Act, and create a registry of licensed foreign worker recruiters and employers seeking to hire temporary foreign workers, which will help protect vulnerable workers from exploitation. This funding is in addition to the $3 million provided in Budget 2018 to initiate planning and begin the transformation of the Employment Standards Branch.

Investing in Communities

Supporting Local Economies

Northern Capital and Planning Grant: Government will provide $100 million in 2018/19 to 26 local governments along the LNG corridor and near Kitimat to help meet their current and future infrastructure needs. The funding will benefit communities in northwest and north-central B.C. to assist with strategic planning and capital investments.

Connecting BC: Connectivity is foundational — it is essential for people, businesses, and government to operate and interact today. Government is investing $50 million in 2018/19 for the Connecting British Columbia program with the intent of leveraging funding from the Canadian Radio-television and Telecommunications Commission’s Broadband Fund. This will help close the gap in high-speed internet access between rural and urban areas. High-speed internet access will be expanded to more than 200 rural and Indigenous communities to enable them to participate in today’s economy.

Tourism, Arts and Culture: Budget 2019 provides a total of $57 million over three years to the Ministry of Tourism, Arts and Culture for the following initiatives:

· $39 million over three years for the Resort Municipality Initiative to fund infrastructure projects that will create jobs and build a strong economy in tourism-oriented communities.

· $3 million over three years for Destination BC to expand promotion of B.C. as a global tourism destination.

· $15 million over three years for the BC Arts Council to further support professional artists and community organizations, bringing the annual budget for BC Arts Council grants to $34 million. A component of this new funding will increase access to make arts more accessible to everyone. This $15 million investment is in addition to the initial $15 million fiscal plan increase for arts grants provided in Budget 2018.

In order to preserve, protect, and provide better access to the human and natural history collections of British Columbia, government is planning for a capital project to modernize and renew the Royal BC Museum.

Budget 2019 provides $18 million in 2019/20 for the Ministry of Municipal Affairs and Housing to facilitate the payments under the Peace River Agreement. Funding provided under this agreement supports planning, programs, asset management and infrastructure investments related to regional economic growth where intensive industrial activities occur outside the boundaries of the region’s municipalities.

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

21

THREE YEAR FISCAL PLAN

Budget 2019 also provides the Ministry of Municipal Affairs and Housing with an opportunity to advance the first grant payment of $62 million to the Capital Regional District in 2019/20 towards the completion of the Core Area Wastewater Treatment Project. The project will provide tertiary wastewater treatment to exceed regulatory standards by December 2020.

Table 1.12 Investing in Communities

($ millions) | | 2018/19 | | 2019/20 | | 2020/21 | | 2021/22 | | Total | |

Supporting Local Economies | | | | | | | | | | | |

Northern Capital and Planning Grant | | 100 | | — | | — | | — | | 100 | |

Connecting BC | | 50 | | — | | — | | — | | 50 | |

Resort Municipality Initiative | | — | | 13 | | 13 | | 13 | | 39 | |

Destination BC - Tourism Market Development | | — | | 1 | | 1 | | 1 | | 3 | |

BC Arts Council - Increased Funding | | — | | 5 | | 5 | | 5 | | 15 | |

Accessible and Safe Transportation Network | | | | | | | | | | | |

Transit Services | | — | | 3 | | 8 | | 10 | | 21 | |

Taxi Modernization and Ride Hailing | | — | | 3 | | 3 | | 3 | | 9 | |

BC Road Network Maintenance | | — | | 13 | | 13 | | 13 | | 39 | |

Commercial Vehicle Safety and Enforcement | | — | | 1 | | 1 | | 1 | | 3 | |

Total | | 150 | | 39 | | 44 | | 46 | | 279 | |

Accessible and Safe Transportation Network

To help individuals access transit services, Budget 2019 adds $21 million over three years to improve conventional bus services in over 30 communities around the province, including improvements to handyDART in both rural and urban settings.

Over three years, $9 million is provided to implement government’s commitments to modernize the taxi industry and enable ride-hailing in B.C. This funding will also enhance vehicle compliance and enforcement activities and support the Passenger Transportation Board in its new role as provincial regulator for passenger-directed vehicles.

Budget 2019 adds $39 million over three years for the maintenance of B.C.’s network of bridges and roads. Continued investment is important to ensuring roads are both safe and efficient at moving goods and people throughout the province, providing related economic benefits to all communities.

A further $3 million over three years is provided to enhance commercial vehicle safety and enforcement in B.C., increasing timely and consistent intervention with carriers.

Sustainable Economic Development

Regulatory Excellence in Mining: Budget 2019 provides the Ministry of Energy, Mines and Petroleum Resources with close to $20 million over three years to fulfill the government’s commitments to improve permitting and increase industry safety by establishing an independent oversight unit. This investment will allow the ministry to hire up to 65 new full-time employees over three years. The ministry will establish a new Mines Health, Safety and Enforcement Division, with an increased number of mines inspectors and a new auditing function; this new division will be separate and independent from a Mines Competitiveness and Authorizations Division. This funding will also provide for the creation of a standing committee to review and update the Health, Safety and Reclamation Code for Mines to ensure it meets current standards and continues to

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

22

THREE YEAR FISCAL PLAN

address the needs of workers, the environment, industry, Indigenous groups and the public. Additional resources are also provided to enhance Indigenous engagement and to improve the co-ordination and predictability of the permitting process to attract increased investment in the province’s mining sector.

Professional Reliance: The Office of the Superintendent of Professional Governance will be established through a nearly $2 million investment over three years. This Office will provide a centralized statutory authority for professional governance oversight to ensure consistency and best practices are applied to the work of natural resource professionals.

Increased Monitoring and Oversight Capacity: Budget 2019 also provides $7 million over three years to the Ministry of Environment and Climate Change Strategy for increased monitoring and oversight activities under the Environmental Management Act. This work will be funded through revenues collected by the Sustainable Environment Fund which receives money from waste discharge fees, provincial sales tax on diapers, pesticide license and permit fees, and other miscellaneous sources.

Environmental Assessment Revitalization: Funding of $9 million is provided in Budget 2019 for implementing the revitalized Environmental Assessment Act, which will focus on enhancing public confidence and participation in the Environmental Assessment process, pursuing reconciliation with Indigenous peoples, and protecting the environment while achieving sustainable project approvals. This funding will allow for new tools and approaches, such as early engagement, seeking consensus with Indigenous peoples, enhanced environmental, social, and economic assessment including gender-based analysis, and modernized compliance and enforcement.

Table 1.13 Sustainable Economic Development

($ millions) | | 2019/20 | | 2020/21 | | 2021/22 | | Total | |

Regulatory Excellence in Mining | | 5 | | 7 | | 8 | | 20 | |

Professional Reliance | | 0.6 | | 0.6 | | 0.6 | | 2 | |

Increased Monitoring and Oversight Capacity | | 2 | | 2 | | 3 | | 7 | |

Environmental Assessment Act Revitalization | | 3 | | 3 | | 3 | | 9 | |

Total | | 10 | | 13 | | 14 | | 37 | |

Strategic Investments with Our Partners

Budget 2019 is accelerating $175 million of grants and other payments to local governments, public libraries and other non-government agencies to provide more certainty for those entities. As a result, there will be corresponding reduced requirements for providing such payments through ministry budgets in 2019/20 and 2020/21.

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

23

THREE YEAR FISCAL PLAN

Analysis for Equity and Fairness (GBA+)

In February 2018, the government of British Columbia committed to advancing gender equality by establishing a Parliamentary Secretary for Gender Equity, reporting to the Minister of Finance. The mandate of the Parliamentary Secretary includes:

· Ensuring government’s commitment to gender equality is reflected in our budgets, policies and programs;

· Acting as the government’s liaison with organizations concerned with gender equality and the advancement of women;

· Co-ordinating cross-ministerial action on gender issues, including but not limited to gendered violence, advancing gender equality and women’s economic empowerment;

· Tracking progress on the National Inquiry into Missing and Murdered Indigenous Women and Girls;

· Promoting gender equity in leadership at senior levels in both the private and public sector.

The Gender Equity Office (GEO) was established in the Ministry of Finance to advance this work across government, including the introduction of Gender-Based Analysis Plus (GBA+) within the BC Public Service. GBA+ is an analytical tool used to assess how diverse groups of people may be impacted by policies, programs and budgets. The “plus” in GBA+ acknowledges that this goes beyond biological (sex) and socio-cultural (gender) differences. It also considers many other identifying factors like Indigeneity, ethnicity, religion, income, geography, age and mental or physical (dis)ability.

The BC Public Service is working to build capacity and understanding throughout government as GBA+ is integrated into policy, program and budget processes, with the goal of facilitating more comprehensive advice to decision-makers, advancing evidence-based policy-making and helping achieve better results for British Columbians.

BC Public Service

Full-time equivalent (FTE) staff utilization in core government ministries is projected to increase from a forecasted 30,750 in 2018/19 to 31,350 FTEs in 2019/20. This is due mainly to increased staffing requirements to implement CleanBC programming, Employment Standards and Temporary Foreign Worker Registry Transformation initiatives, mental health services, coast forest sector revitalization, and independent oversight of mining and other professions. The projected increase in FTEs is also due in part to continued implementation of road safety programs, the Civil Resolution Tribunal, cannabis legalization, commercial vehicle and safety enforcement, and staff to support reconciliation with First Nations.

FTE utilization is projected to increase slightly in 2020/21 due to the continued implementation of these initiatives, before stabilizing in 2021/22.

BUDGET AND FISCAL PLAN - 2019/20 to 2021/22

24

THREE YEAR FISCAL PLAN

Public Sector Compensation: The Economic Stability Mandate and the new Sustainable Services Negotiating Mandate

There are more than 326,000 members covered by 183 collective agreements across the B.C. public sector. The vast majority of these collective agreements expire between April 1 and June 30, 2019. Fiscal 2019/20 marks a transition between the province’s previous five-year (2014-2019) Economic Stability Mandate (ESM) and the new three-year (2019-2022) Sustainable Services Negotiating Mandate (SSNM). Budget 2019 supports the final compensation adjustments pursuant to the ESM as well as the new collective agreements reached under the SSNM.