UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | ||

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the year ended December 31, 2009 | ||

or | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission File Number 001-13711

WALTER ENERGY, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 13-3429953 (IRS Employer Identification No.) | |

4211 W. Boy Scout Boulevard Tampa, Florida (Address of principal executive offices) | 33607 (Zip Code) | |

(813) 871-4811 Registrant's telephone number, including area code: | ||

Securities registered pursuant to Section 12(b) of the Act: | ||

Title of each class | Name of exchange on which registered | |

| Common Stock, par value $0.01 | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act:NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of voting stock held by non-affiliates of the registrant, based on the closing price of the Common Stock on June 30, 2009, the registrant's most recently completed second fiscal quarter, as reported by the New York Stock Exchange, was approximately $1.9 billion.

Number of shares of common stock outstanding as of January 31, 2010: 53,296,211

Documents Incorporated by Reference

Applicable portions of the Proxy Statement for the Annual Meeting of Stockholders of the Company to be held April 21, 2010 are incorporated by reference in Part III of this Form 10-K.

CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS

This report includes statements of our expectations, intentions, plans and beliefs that constitute "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 and are intended to come within the safe harbor protection provided by those sections. These statements, which involve risks and uncertainties, relate to analyses and other information that are based on forecasts of future results and estimates of amounts not yet determinable and may also relate to our future prospects, developments and business strategies. We have used the words "anticipate," "believe," "could," "estimate," "expect," "intend," "may," "plan," "predict," "project," "should" and similar terms and phrases, including references to assumptions, in this report to identify forward-looking statements. These forward-looking statements are made based on expectations and beliefs concerning future events affecting us and are subject to uncertainties and factors relating to our operations and business environment, all of which are difficult to predict and many of which are beyond our control, that could cause our actual results to differ materially from those matters expressed in or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to:

- •

- Deteriorating conditions in the financial markets;

- •

- Global economic crisis;

- •

- Decline in global steel demand;

- •

- Inaccessibility of coal needed for our cokemaking could impair our ability to fill customer orders;

- •

- Prolonged decline in the price of coal;

- •

- Our customers refusal to honor or renew contracts;

- •

- Market conditions beyond our control;

- •

- Title defects preventing us from (or resulting in additional costs for) mining our properties;

- •

- Unavailability of cost-effective transportation for our coal;

- •

- A significant increase in competitive pressures;

- •

- Significant cost increases and delays in the delivery of purchased components;

- •

- Availability of adequate skilled employees and other labor relations matters;

- •

- Greater than anticipated costs incurred for compliance with environmental liabilities;

- •

- Factors beyond our control could impact the accuracy of estimated coal reserves;

- •

- Future regulations could increase our costs or limit our ability to produce coal;

- •

- New laws and regulations to reduce greenhouse gas emissions could adversely impact the demand for our coal reserves;

- •

- Postretirement benefit and pension obligations could be materially higher than estimated if our underlying assumptions are incorrect;

- •

- Greater than expected workers' compensation and medical claims could reduce profitability;

- •

- Adverse rulings in current or future litigation could impact our profitability;

- •

- Inability to access needed capital could limit our ability to operate our business

- •

- A downgrade in our credit rating could adversely impact our costs and expenses;

1

- •

- The anticipated loss of some of our executive officers and other key personnel as a result of the relocation of our corporate offices could harm our business;

- •

- Concentration of our coal and gas producing properties in one area subjects us to risk;

- •

- Our ability to attract and retain key personnel;

- •

- Our ability to identify suitable acquisition candidates to promote growth;

- •

- Volatility in the price of our common stock;

- •

- Our ability to pay regular dividends to stockholders could be restricted;

- •

- Potential suitors could be discouraged by our stockholder rights agreement;

- •

- Our exposure to indemnification obligations;

- •

- A former subsidiary may not be able to satisfy certain obligations to us and we could become liable for certain contingent obligations to them, which could become significant;

- •

- Other factors, including the other factors discussed in Item 1A, "Risk Factors," as updated by any subsequent Form 10-Qs or other documents that are on file with the Securities and Exchange Commission.

You should keep in mind that any forward-looking statement made by us in this Annual Report on Form 10-K or elsewhere speaks only as of the date on which we make it. New risks and uncertainties come up from time to time, and it is impossible for us to predict these events or how they may affect us. We have no duty to, and do not intend to, update or revise the forward-looking statements in this Annual Report on Form 10-K after the date of this Annual Report on Form 10-K, except as may be required by law. In light of these risks and uncertainties, you should keep in mind that any forward-looking statement made in this Annual Report on Form 10-K or elsewhere might not occur.

2

GLOSSARY OF SELECTED MINING TERMS

Ash. Impurities consisting of iron, alumina and other incombustible matter that are contained in coal. Since ash increases the weight of coal, it adds to the cost of handling and can affect the burning characteristics of coal.

Assigned reserves. Coal that is planned to be mined at an operation that is currently operating, currently idled, or for which permits have been submitted and plans are eventually to develop the operation.

Bituminous coal. A common type of coal with moisture content less than 20% by weight and heating value of 10,500 to 14,000 Btus per pound. It is dense and black and often has well-defined bands of bright and dull material.

British thermal unit, or "Btu". A measure of the thermal energy required to raise the temperature of one pound of pure liquid water one degree Fahrenheit at the temperature at which water has its greatest density (39 degrees Fahrenheit).

Coal seam. Coal deposits occur in layers. Each layer is called a "seam."

Coke. A hard, dry carbon substance produced by heating coal to a very high temperature in the absence of air. Coke is used in the manufacture of iron and steel. Its production results in a number of useful by-products.

Compliance coal. Coal which, when burned, emits 1.2 pounds or less of sulfur dioxide per million Btus, as required by Phase II of the Clean Air Act.

Continuous miner. A machine used in underground mining to cut coal from the seam and load onto conveyers or shuttle cars in a continuous operation. In contrast, a conventional mining unit must stop extracting in order to begin loading.

Continuous mining. A form of underground mining that cuts the coal from the seam and loads continuously, thus eliminating the separate cycles of cutting, drilling, shooting and loading.

Hard coking coal. Hard coking coal is a type of metallurgical coal that is a necessary input in the production of strong coke. It is evaluated based on the strength, yield and size distribution of coke produced which is dependent on rank and plastic properties of the coal. Hard coking coals trade at a premium to other coals due to their importance in producing strong coke and as they are of limited resources.

Indicated (Probable) reserves. Reserves for which quantity and grade and/or quality are computed from information similar to that used for proven reserves, but the sites for inspection, sampling and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation.

Industrial coal. Coal generally used as a heat source in the production of lime, cement, or for other industrial uses and is not consideredsteam coal ormetallurgical coal.

Longwall mining. A form of underground mining that employs two rotating drums pulled mechanically back and forth across a long surface of the coal. A hydraulic system supports the roof of the mine while the drum is mining the coal. Chain conveyors move the loosened coal to an underground mine conveyor to transport to the surface. Longwall mining is the most efficient underground mining method in the United States.

Measured (Proven) reserves. Reserves for which: (a) quantity is computed from dimensions revealed in outcrops (part of a rock formation that appears at the surface of the ground), trenches,

3

workings or drill holes; grade and/or quality are computed from the results of detailed sampling; and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well-established.

Metallurgical coal. The various grades of coal suitable for carbonization to make coke for steel manufacture, including hard coking coal (see definition above), semi-soft coking coal (SSCC) and coal used for pulverized coal injection (PCI). Also known as "met" coal, its quality depends on four important criteria: (1) volatility, which affects coke yield; (2) the level of impurities including sulfur and ash, which affect coke quality; (2) composition, which affects coke strength; and (4) other basic characteristics that affect coke oven safety. Met coal typically has a particularly high Btu but low ash and sulfur content.

Nitrogen oxide (NOx). Produced as a gaseous by-product of coal combustion. It is a harmful pollutant that contributes to smog.

Overburden. Layers of earth and rock covering a coal seam. In surface mining operations, overburden is removed prior to coal extraction.

Preparation plant. Usually located on a mine site, although one plant may serve several mines. A preparation plant is a facility for crushing, sizing and washing coal to remove impurities and prepare it for use by a particular customer. The washing process has the added benefit of removing some of the coal's sulfur content.

Recoverable reserves. Tons of mineable coal which can be extracted and marketed after deduction for coal to be left in pillars, etc. and adjusted for reasonable preparation and handling losses.

Reclamation. The process of restoring land and the environment to their original state following mining activities. The process commonly includes "recontouring" or reshaping the land to its approximate original appearance, restoring topsoil and planting native grass and ground covers. Reclamation operations are usually underway before the mining of a particular site is completed. Reclamation is closely regulated by both state and federal law.

Reserve. That part of a mineral deposit that could be economically and legally extracted or produced at the time of the reserve determination.

Roof. The stratum of rock or other mineral above a coal seam; the overhead surface of a coal working place.

Steam coal. Coal used by power plants and industrial steam boilers to produce electricity, steam or both. It generally is lower in Btu heat content and higher in volatile matter than metallurgical coal.

Sulfur. One of the elements present in varying quantities in coal that contributes to environmental degradation when coal is burned. Sulfur dioxide is produced as a gaseous by-product of coal combustion.

Surface mine. A mine in which the coal lies near the surface and can be extracted by removing the covering layer of soil (see "Overburden"). About 67% of total U.S. coal production comes from surface mines.

Tons. A "short" or net ton is equal to 2,000 pounds. A "long" or British ton is equal to 2,240 pounds; a "metric" ton is approximately 2,205 pounds. Unless otherwise indicated, the short ton is the unit of measure referred to in this document. The international standard for quoting price per ton is based on the U.S. dollar per metric ton.

Unassigned reserves. Coal that is likely to be mined in the future, but which is not consideredAssigned reserves.

Underground mine. Also known as a "deep" mine. Usually located several hundred feet or more below the earth's surface, an underground mine's coal is removed mechanically and transferred by shuttle car and conveyor to the surface. Underground mines account for about 33% of annual U.S. coal production.

4

Item 1. Description of Business

Introduction

We are a leading producer and exporter of metallurgical coal for the global steel industry and also produce steam coal, coal bed methane gas ("natural gas"), metallurgical coke and other related products. We trace our roots back to 1946 when Jim Walter began a homebuilding business in Tampa, Florida. Although we were focused on Homebuilding during our early years, we later branched out into many different businesses, including the development, in 1972, of four underground coal mines in the Blue Creek coal seam near Brookwood, Alabama. In 1987 a group of investors formed a new company, subsequently named Walter Industries, Inc. and engineered a leveraged buyout, successfully completed in 1988. In 1997, Walter Industries, Inc. began trading on the New York Stock Exchange. In 2009 we closed our Homebuilding business and spun off our Financing business. Our Homebuilding business was an on-your-lot homebuilder and our Financing business serviced non-conforming instalment notes and loans that were secured by mortgages and liens. With all of our businesses now concentrated in coal and natural gas, we changed our name to Walter Energy, Inc. in April 2009.

Overview

Our primary business, the mining and exporting of hard coking coal for the steel industry, is included in our Underground Mining segment (comprised of Jim Walter Resources, Inc. or "JWR" and Blue Creek Coal Sales, Inc.). JWR, the country's southernmost Appalachian coal producer, mines high quality coal from Alabama's Blue Creek coal seam. JWR's mines are 1,500 to 2,200 feet underground, making them some of the deepest vertical shaft coal mines in North America. Metallurgical coal mined from the Blue Creek seam contains very low sulfur, has strong coking properties and high heat value making it ideally suited to the needs of steel makers as a coking coal and to utilities as a steam coal. In 2009, the Underground Mining segment produced 6.1 million tons of high quality metallurgical coal. Underground Mining has convenient access to the port of Mobile, Alabama through barge and by railroad allowing us to minimize our transportation costs.

Underground Mining also extracts methane gas, principally from the Blue Creek coal seam. Our natural gas business represents one of the most extensive and comprehensive commercial programs for coal seam degasification in the country, producing approximately 19 million cubic feet of gas daily from our 400-plus wells.

Through our Walter Coke segment, we manufacture furnace and foundry coke, collectively referred to as "metallurgical coke." Foundry coke is marketed to iron pipe plants and foundries producing castings. Furnace coke is primarily sold to the domestic steel industry for producing steel in blast furnaces. Walter Coke delivers product to its customers via rail (onsite rail facility), truck and barge.

In our Surface Mining segment, we also mine steam coal for sale to industrial and electric utility markets through our Taft Coal Sales, Tuscaloosa Resources and Walter Minerals subsidiaries.

The financial results of our industry segments is included in Note 16 of "Notes to Consolidated Financial Statements" included in this Form 10-K.

2009 Developments

Spin-off and Merger of Financing Segment On April 17, 2009, we completed the spin-off of our Financing business and the merger of that business with Hanover Capital Mortgage Holdings, Inc. to create Walter Investment Management Corp. ("Walter Investment"), which operates as a publicly traded real estate investment trust. The subsidiaries and assets that Walter Investment owned at the time of the spin-off included all assets of Financing except for those associated with the workers'

5

compensation program and various other run-off insurance programs within Cardem Insurance Co., Ltd. See "Notes to Consolidated Financial Statements" included herein for further information.

Corporate Name Change and Segment Revisions On April 23, 2009, we changed our name from Walter Industries, Inc. to Walter Energy, Inc. ("Walter"). In addition, prior to the first quarter of 2009, our underground and surface coal mining operations were reported together as the Natural Resources segment. Beginning in 2009, we revised our reportable segments to separate the Natural Resources segment into Underground Mining and Surface Mining. Underground Mining includes our underground metallurgical coal operations from the No. 4 and No. 7 mines and our natural gas operations. Surface Mining includes our surface coal mining operations for Tuscaloosa Resources, Inc. ("TRI") and Taft Coal Sales & Associates, Inc. ("Taft") as well as Walter Minerals, Inc. (formerly known as United Land Corporation) results. In addition, during the second quarter of 2009, we changed the name of our metallurgical coke manufacturer from Sloss Industries Corporation to Walter Coke, Inc., ("Walter Coke"). See Note 16 of "Notes to Consolidated Financial Statements" included in this Form 10-K. for segment information.

Share Repurchase Program In 2009, we repurchased $34.2 million or 1.5 million shares of our outstanding stock under our Board of Directors approved $100.0 million share repurchase program. As of December 31, 2009, there was $20.6 million remaining under this program. Purchases are based on liquidity and market conditions. In addition, on April 23, 2009, shareholders voted to grant us the authority to issue 20,000,000 shares of Preferred Stock, par value $.01 per share. No preferred shares have been issued.

Debt Amendment On September 3, 2009, we amended the 2005 Walter Credit Agreement ("Credit Agreement") to extend the maturity date for our Revolving Credit Facility ("Revolver") from October 4, 2010 to July 2, 2012 and amend the size of the Revolver to $300.0 million that, subject to certain conditions, can be increased to $425.0 million. See Management's Discussion and Analysis for further information.

The Coal Industry

Coal is one of the most available and important energy sources in the world, providing approximately 26% of the world's primary energy needs according to the World Coal Institute ("WCI"). Per the WCI, the most significant uses for coal are for electricity generation, steel production, cement manufacturing and as a liquid fuel. According to the WCI, approximately 41% of the world's electricity is generated from coal and this level is expected to increase to 44% by 2030. During 2008, coal was used to generate approximately 49% of the electricity in the United States according to the International Energy Agency ("IEA").

Approximately 66% of global steel is produced in Basic Oxygen Furnaces according to the WCI. After metallurgical coal is converted to coke it is used in blast furnaces to smelt iron ore which is subsequently used to produce steel. Steel is critical to everyday life. For example, it is used in cars, buildings, trains, ships, bridges, medical equipment and refrigerators. Metallurgical coal is critical in making coke for steel manufacturing due to its characteristics: lower volatility, lower sulfur and ash content and favorable coking characteristics (higher coke strength). Additionally, metallurgical coal has a higher Btu value. A significant amount of steel is also produced in Electric Arc Furnaces, a process in which a large percentage of the electricity is generated from coal-fired power stations.

Coal is mined in more than 50 countries in the world and used in more than 70 countries. Coal's appeal is that it is readily available from a wide variety of sources, its prices have been lower and more stable than oil and gas prices, and it is likely to remain the most affordable fuel for power generation in many developing and industrialized nations for several decades per the WCI. By contrast, at current

6

production levels, proven coal reserves are estimated to last 122 years while oil and gas reserves are estimated to last approximately 42 and 60 years, respectively. The top five coal producing countries in the world are China, the United States, India, Australia and Russia. The largest exporters of coal in 2008 were Australia, Indonesia and Russia (the U.S. is 5th) according to the WCI. The leading exporters of metallurgical coal for coking, per the WCI, are Australia, the United States and Indonesia. Because coking (metallurgical) coal is more expensive than steam coal, exporters are able to afford the high freight rates involved in exporting coking coal worldwide.

Coal Characteristics

Coal is generally classified by end use as either metallurgical coal or steam coal. Sulfur, ash and moisture content as well as coking characteristics are key attributes in grading metallurgical coal while heat value, ash and sulfur content are important variables in rating steam coal. We currently mine, process, market and transport coal with the characteristics described below.

Sulfur Content (metallurgical and steam coal): Although sulfur content can differ from seam to seam, our metallurgical sulfur content ranges from 0.65% to 0.8%, a low value which is preferred by customers. Coal produces undesirable sulfur dioxide when it burns, the amount of which depends on the concentration of sulfur in the coal as well as the chemical composition.

Ash and Moisture (metallurgical and steam coal): Ash residue is what remains after the combustion of coal. Low ash is desirable because businesses must dispose of ash after the coal is used. High moisture content decreases the heat value of the coal which is undesirable and increases the coal's weight which is also negative because higher weight increases transportation charges. Our metallurgical coal has a 9% ash rating which is desirable.

Coking Characteristics (metallurgical coal): Two important coking characteristics are coke strength and volatility. Measuring the expansion and contraction of coal when heated determines the strength of coke that could be produced from the coal. When coal is heated in the absence of air, the loss in mass less moisture is volatility. Volatility of metallurgical coal is used to determine the percentage of coal that becomes coke. This measure is known as coke yield. A low volatility results in a higher coke yield. Our metallurgical coal has both a high rating for coke strength as well as a low measure of volatility.

Description of Our Business

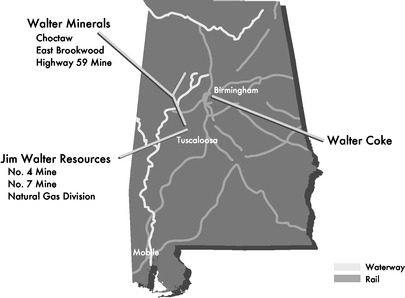

We operate our business through three principal business segments-Underground Mining, Surface Mining and Walter Coke. Our industry segment financial information is included in Note 16 of "Notes to Consolidated Financial Statements" included herein. During 2009, we actively operated five mines. We operate two metallurgical coal mines in Southern Appalachia's Blue Creek coal seam, the No. 7 Mine (which includes No. 7 East) and the No. 4 Mine, both operated by Underground Mining, and three steam coal mines operated by Surface Mining, TRI's East Brookwood Mine, Walter Minerals' Highway 59 Mine and Taft's Choctaw Mine. The following map provides our Underground Mining, Surface Mining, and Walter Coke locations as of December 31, 2009. For a comprehensive summary of all of our coal properties and of our coal reserves and production levels, see the tables summarizing our coal reserves and production in "Item 2. Description of Property" in this Form 10-K.

7

Underground Mining

Our principal business segment, comprising more than 80% of our revenue and operating income, is our Underground Mining segment. Underground Mining includes the operations of our JWR subsidiary. Underground Mining is headquartered in Brookwood, Alabama and currently has approximately 140.4 million tons of recoverable reserves from our mines located in west central Alabama between the cities of Birmingham and Tuscaloosa. Operating at about 2,000 feet below the surface, the No. 4 and No. 7 mines are some of the deepest underground coal mines in North America. We extract coal primarily from Alabama's Blue Creek and Mary Lee seams, which contain high-quality bituminous coal. Blue Creek coal offers high coking strength with low coking pressure, low sulfur and low-to-medium ash content with high Btu values that can be sold either as metallurgical coal (used to produce coke) or as compliance steam coal (used by electric utilities because it meets current environmental compliance specifications).

The coal from JWR's Mines No. 4 and 7 is currently sold as a high quality low- and mid-vol metallurgical coal. JWR has more than 1,400 active employees. At forecasted production levels, we estimate the current reserves to have a 15 to 17 year life. Mines No. 4 and No.7 are located near Brookwood, Alabama, and are serviced by CSX rail. Both mines have access to our barge load out facility on the Black Warrior River. Service via both rail and barge culminates in delivery to the Port of Mobile, whereby shipments are delivered to our international customers via ocean vessels. More than 97% of the metallurgical coal sales in our Underground Mining segment are sales to international customers. The coal producer is responsible for transporting the coal from the mine to the export coal-loading facility. Export coal is usually sold at the loading port, with the buyer responsible for further transportation to their plant.

Since potential customers may choose a metallurgical coal supplier in large part based on transportation costs, this is a critical issue. We have the advantage of having our mines conveniently located near both barge load out facilities and railroad transportation (CSX rail) with direct access to the Port of Mobile, minimizing our transportation costs.

Approximately 80% of JWR's metallurgical coal is mined using longwall extraction technology with development support from continuous miners. Underground mining with longwall technology drives greater production efficiency, improved safety, higher coal recovery and lower production costs. Historically, JWR has operated one longwall mining system in each mine for primary production and four to six continuous miner sections in each mine for the development of mains and longwall panel

8

entries. As discussed in previous periods, we invested in our Mine No. 7 East Expansion such that the No. 7 mine now operates two longwall mining systems. JWR's optimal operating plan is a longwall/continuous miner production ratio of approximately 80% / 20%. By utilizing longwall mining, our full year 2009 production costs for metallurgical coal averaged $61.12 per ton.

In longwall mining, mechanized shearers are used to cut and remove the coal from long rectangular blocks of medium or thick seams. After the coal is removed, it drops onto a chain conveyor, which moves it to a second conveyor that will ultimately take the coal to the surface. Temporary hydraulic-powered roof supports hold up the roof throughout the extraction process. This method of mining has proven to be more efficient than other mining methods, with a recovery rate of nearly 45 percent, but the equipment is more expensive than other conventional mining methods and cannot be used in all geological circumstances. In longwall mining, only the main tunnels are bolted. Most of the longwall panel is allowed to collapse behind the shields (which hold the roof as coal is excavated).

Included in Underground Mining is our natural gas operation which is also headquartered in Brookwood, Alabama. This operation extracts and sells natural gas from the coal seams owned or leased by JWR, primarily through Black Warrior Methane Corp., an equal ownership joint venture with El Paso Production Co., a subsidiary of El Paso Corporation. The original motivation for the joint venture was to increase safety in JWR's Blue Creek mines by reducing natural gas concentrations with wells drilled in conjunction with the mining operations. There were approximately 400 wells producing approximately 6.1 billion cubic feet of natural gas in 2009. JWR also operates a wholly owned low quality gas ("LQG") facility. The degasification operation has improved mining operations and safety by reducing methane gas levels in the mines, and has been a profitable operation. We expect production of natural gas to be 6.0 to 6.3 billion cubic feet in 2010.

Surface Mining

We are currently operating three surface mines in Alabama with planned production for 2010 of approximately 1.3 million to 1.4 million tons of coal. We mine steam and industrial coal principally for the industrial and electric utility markets. Our coal mines are convenient to our barge load out facility as well as two rail load out facilities. Our steam and industrial coal business currently represents approximately 10% of our total revenues.

Taft's Choctaw Mine The Choctaw Mine is located near Parrish in Walker County, Alabama and has an onsite rail facility serviced by Norfolk Southern rail. Access to Highway 269 provides delivery access to local customers via truck. The Choctaw Mine is a surface mine that primarily produces steam and industrial coal. Taft is able to blend coal to meet utility and industrial customers' needs.

TRI's East Brookwood and Highway 59 Mines TRI's East Brookwood and Highway 59 mines are located in Tuscaloosa County near Brookwood, Alabama. They both have access to our barge load out facility on the Black Warrior River. The East Brookwood and Highway 59 mines are surface mines that produce steam and industrial coal. Approximately half of TRI's coal is delivered via barges to a local power company. The remainder is delivered to customers via truck. As with Taft, TRI is able to blend coal to meet industrial utility customers' requirements.

We also own two mines that are ready for operation and will be placed in service when market conditions permit. Taft's Reid School Mine is located in Blount County, Alabama and will have access to Highway 79 for delivery to local customers via truck. Walter Mineral's Flat Top Mine is located in Adamsville, Alabama near Highway 78 where coal will be delivered to local customers via truck.

9

Coal Preparation and Blending

All of our coal mines are located in Alabama and we have coal preparation and blending facilities convenient to each of our mines. Using our facilities, we are able to efficiently blend our coal to meet our customers' specifications.

Marketing, Sales and Customers

Coal prices are impacted by many factors and differ substantially by region. Factors impacting coal prices include the overall economy, the demand for electricity, the demand for steel, location, the market, quality and type of coal, mine operation costs and the cost of alternative fuels. The major factors influencing our business are the economy and the demand for steel. Our high quality Blue Creek coal is rated among the highest quality coals in the world and is preferred as a base coal in our customers' blends. Our marketing strategy is to focus on international markets mostly in Europe and South America where we have a significant transportation cost advantage and where our coal is in high demand.

During 2009, approximately 59% of our hard coking coal shipments were to customers in Europe and approximately 26% to South America. We are the largest U.S. supplier of hard coking coal into South America. Further, we focus on long-term customer relationships where we have a competitive advantage. We sell most of our metallurgical coal under fixed price supply contracts, usually with a one year term, running principally from April through March or from July through June. Some sales of metallurgical coal can, however, occur in the spot market as dictated by available supply and market demand.

During 2009, our Underground Mining segment's two largest customers represented approximately 17% and 16% of the Underground Mining segment's sales. Even in this challenging economy we believe that the loss of these customers would not have a material adverse effect on our results of operations as the loss of volume from these customers would be replaced with sales to other existing or new customers due to the demand for our metallurgical coal. Our outlook on the long-term prospects for growth and related demand for our product is very strong.

Our Surface Mining segment markets its steam and industrial coal to customers in the United States, generally under long term contracts. Our customers for steam coal are electric utility and industrial customers.

Our sales backlog of fixed-priced, fixed-quantity contracts was approximately 4.1 million tons as of December 31, 2009, which includes sales of both metallurgical and steam coal. This tonnage is expected to be delivered in 2010.

Trade Names, Trademarks and Patents

The names of each of our subsidiaries are well established in the respective markets they serve. Management believes that customer recognition of such trade names is of significant importance. Our subsidiaries have numerous patents and trademarks. Management does not believe, however, that any one such patent or trademark is material to our individual segments or to the business as a whole.

Competition

Substantially all of our metallurgical coal sales are exported. Our major competitors are businesses that sell into our core business areas of Europe and South America. In both Europe and South America, we primarily compete with producers of premium coking coal from Australia, Canada and North America. The principal areas in which we compete are coal prices at the port of shipment, coal quality and characteristics, customer relationships and the reliability of supply. The demand for our metallurgical coal is significantly dependent on the general economy and the worldwide demand for steel. Although there are significant challenges in this current difficult economy, we believe that we have competitive strengths in our business areas that provide us with distinct competitive advantages.

10

We have a premium product. Blue Creek Coal is recognized to be among the highest quality coals in the world. Its characteristics are very low sulfur, low ash and low volatility. These strong coking properties and high heat value make it ideally suited for steel makers as a coking coal and to utilities as a steam coal.

We have a significant transportation advantage in shipping to our customers. Our principal mines in Brookwood, Alabama are serviced by CSX rail. We also have access to our barge load out facility on the Black Warrior River. Service via rail or barge is a relatively short distance to the Port of Mobile. Since customers for our coal are primarily in Europe and South America we are able to ship our coal quickly and at a relatively favorable cost.

We are a low-cost producer making our coal competitive on a delivered basis. We primarily use longwall mining for our metallurgical coal, recognized as the most efficient underground mining method in the United States. We have invested in expanded longwall mining in our Mine No. 7 East expansion, which has added to our annual production capacity. We expect to increase annual production capacity from 6.0 million tons in 2009, increasing annually to an estimated 9.5 million tons of annual capacity achievable in 2012. With the East expansion, Mine No. 7 is the largest producer of low-vol metallurgical coal in the United States. By increasing our longwall mining capabilities, the cost per ton to mine our metallurgical coal has been reduced.

We maintain excellent relationships with our customers. Customers want good products, delivered on a timely basis at a fair price. Having a premium product and with our production and transportation efficiencies, we are able to deliver a premium product at a competitive price on a timely basis. As a result, we have maintained excellent relationships with our customers over many years.

We have a strong balance sheet to meet unknown issues that may arise. With the uncertain economy it is important to maintain access to credit and liquidity. We have a minimal amount of funded debt and zero borrowings under our revolving credit facility. Operationally, our cash flow is very strong and we expect to maintain this strong financial profile

We are able to purchase and blend coal to the customer's specifications. In order to provide the customer exactly what he needs at the lowest possible price, we are able to blend our high quality coal to meet the customer's energy needs at an affordable price.

Environmental and Other Regulatory Matters

Our businesses are subject to numerous federal, state and local laws and regulations with respect to matters such as permitting and licensing requirements, employee health and safety, reclamation and restoration of property and protection of the environment. Environmental laws and regulations include, but are not limited to, the federal Clean Air Act ("CAA") and its state counterpart with respect to air emissions; the Clean Water Act ("CWA") and its state counterpart with respect to water discharges; the Resource Conservation and Recovery Act ("RCRA") and its state counterparts with respect to solid and hazardous waste generation, treatment, storage and disposal; as well as the regulation of underground storage tanks; and the Comprehensive Environmental Response, Compensation and Liability Act ("CERCLA") and its state counterpart with respect to releases, threatened releases, and remediation of hazardous substances. Other environmental laws and regulations require reporting, even though the impact of that reporting is unknown. Compliance with these laws and regulations may be costly and time-consuming and may delay commencement or continuation of exploration or production at our operations. These laws are constantly evolving and becoming increasingly stringent. The ultimate impact of complying with existing laws and regulations is not always clearly known or determinable due in part to the fact that certain implementing regulations for these environmental laws have not yet been promulgated and in certain instances are undergoing revision. These laws and regulations, particularly

11

new legislative or administrative proposals (or judicial interpretations of existing laws and regulations) related to the protection of the environment, could result in substantially increased capital, operating and compliance costs and have a material adverse effect on our operations and/or our customers' ability to use our products.

We strive to conduct our mining, natural gas and coke operations in compliance with all applicable federal, state and local laws and regulations. However, due in part to the extensive and comprehensive regulatory requirements, along with changing interpretations of these requirements, violations occur from time to time in our industry and at our operations. In recent years, expenditures for regulatory or environmental obligations have been mainly for safety or process changes, although certainly some expenditures continue to be made at several facilities to comply with ongoing monitoring or investigation obligations. To the extent these expenditures, as with all costs, are not ultimately reflected in the prices of our products and services, operating results will be reduced. We believe that our major North American competitors are confronted by substantially similar conditions and thus do not believe that our relative position with regard to such competitors is materially affected by the impact of environmental laws and regulations. However, the costs and operating restrictions necessary for compliance with environmental laws and regulations may have an adverse effect on our competitive position with regard to foreign producers and operators who may not be required to undertake equivalent costs in their operations. In addition, the specific impact on each competitor may vary depending on a number of factors, including the age and location of its operating facilities, applicable state legislation and its production methods.

Permitting and Approvals

Numerous governmental permits and approvals are required for mining operations. We are required to prepare and present to federal, state or local authorities data pertaining to the effect or impact that any proposed exploration for or production of coal may have upon the environment, the public and our employees. In addition, we must also submit a comprehensive plan for mining and restoring, upon the completion of mining operations, the mined property to its prior condition, productive use or other permitted condition. The requirements are costly and time-consuming and may delay commencement or continuation of exploration or production at our operations. Typically we submit our necessary mining permit applications several months, or even years, before we anticipate mining a new area.

Our coking operations are subject to numerous regulatory permits and approvals, including air and water permits. These permits subject us to monitoring and reporting requirements. We typically submit our necessary permit renewal applications several months prior to expiration.

Applications for permits or permit renewals at our mining and coking operations are subject to public comment and may be subject to litigation from third parties seeking to deny issuance of a permit or to overturn the agency's grant of the permit application, which may also delay commencement or continuation of our mining and coking operations. Further, regulations provide that applications for certain permits or permit modifications can be delayed, refused or revoked if an officer, director or a stockholder with a 10% or greater interest in the entity is affiliated with or is in a position to control another entity that has outstanding permit violations. In the current regulatory environment, we anticipate approvals will take even longer than previously experienced, and some permits may not be issued at all. Significant delays in obtaining, or denial of, permits could have a material adverse effect on our business.

Mine Health and Safety

Stringent health and safety standards have been in effect since Congress enacted the Coal Mine Health and Safety Act of 1969. The Federal Mine Safety and Health Act of 1977 significantly expanded

12

the enforcement of safety and health standards and imposed safety and health standards on all aspects of mining operations. Regulations are comprehensive and affect numerous aspects of mining operations, including training of mine personnel, mining procedures, blasting, the equipment used in mining operations and other matters. The Federal Mine Safety and Health Administration ("MSHA") monitors compliance with these federal laws and regulations and can impose under recently enacted regulations maximum penalties of up to $220,000 for certain violations, as well as closure of mines. In addition, certain portions of the Coal Mine Safety and Health Act of 1969 and the Federal Mine Safety and Health Act of 1977, as amended, require payments of benefits to disabled coal miners with black lung disease and to certain survivors of miners who die from black lung disease.

Underground mining accidents involving fatalities in 2006 received national attention and prompted responses at the federal and state levels that have resulted in increased scrutiny of current safety practices and procedures in the mining industry. On June 15, 2006, Congress passed the federal Mine Improvement and New Emergency Response Act of 2006 (the "MINER Act"). Implementation of the specific requirements is currently underway. The implementation of these new requirements has caused us and will cause us to incur substantial additional costs which will impact our operating costs. The additional requirements of the MINER Act and implementing federal regulations include, among other things, expanded emergency response plans, providing additional quantities of breathable air for emergencies, installation of refuge chambers in underground coal mines, installation of two-way communications and tracking systems for underground coal mines, new standards for sealing mined out areas of underground coal mines, more available mine rescue teams and enhanced training for emergencies.

On January 25, 2006, an Alabama circuit judge ordered the Alabama governor and legislature to take action to ensure the safety of Alabama's mineworkers. On February 2, 2010, Alabama Senate Bill 362 was proposed and read to the Senate's Business and Labor Committee. The bill purports to extensively revise and modernize the Alabama Coal Mine Safety Law of 1975 to comply with federal law to enhance mining safety. While many of the proposed changes track the federal MINER Act, the proposed bill and its supplemental provisions go beyond current federal law.

Most aspects of mine operations are subject to extensive regulation. While mine safety and health regulation has a significant effect on our operating costs, our U.S. competitors are subject to the same degree of regulation. However, pending legislation at the state level could result in differing operating costs than our competitors.

Workers' Compensation and Black Lung

We are self-insured for workers' compensation benefits for work-related injuries. Workers' compensation liabilities, including those related to claims incurred but not reported, are recorded principally using annual valuations based on discounted future expected payments using historical data of the division or combined insurance industry data when historical data is limited. In addition, certain of our subsidiaries are responsible for medical and disability benefits for black lung disease under the Federal Coal Mine Health and Safety Act of 1969 and the Federal Mine Safety and Health Act of 1977, as amended, and is self-insured against black lung related claims. We perform periodic evaluations of our black lung liability, using assumptions regarding rates of successful claims, discount factors, benefit increases and mortality rates, among others. See "Item 7. Management's Discussion and Analysis of Results of Operations and Financial Condition."

Surface Mining Control and Reclamation Act

The Surface Mining Control and Reclamation Act of 1977 ("SMCRA"), requires that comprehensive environmental protection and reclamation standards be met during the course of and following completion of mining activities. Permits for all mining operations must be obtained from the

13

Federal Office of Surface Mining Reclamation and Enforcement or, where state regulatory agencies have adopted federally approved state programs under the Act, the appropriate state regulatory authority. In Alabama, the Alabama Surface Mining Commission reviews and approves SMCRA permits.

SMCRA permit provisions include requirements for coal prospecting, mine plan development, topsoil removal, storage and replacement, selective handling of overburden materials, mine pit backfilling and grading, subsidence control for underground mines, surface drainage control, mine drainage and mine discharge control and treatment and revegetation. These requirements seek to limit the adverse impacts of coal mining and more restrictive requirements may be adopted from time to time.

Before a SMCRA permit is issued, a mine operator must submit a bond or otherwise secure the performance of reclamation obligations. The Abandoned Mine Land Fund, which is part of SMCRA, requires a fee on all coal produced. The proceeds are used to reclaim mine lands closed or abandoned prior to 1977. On December 7, 2006, the Abandoned Mine Land Program was extended for 15 years.

SMCRA stipulates compliance with many other major environmental statutes, including: the Clean Air Act, the Clean Water Act, the Resource Conservation and Recovery Act, and the Comprehensive Environmental Response, Compensation and Liability Act.

We accrue for the costs of final mine closure. Estimates of our total reclamation and mine-closing liabilities are based upon permit requirements and our experience. The amounts recorded are dependent upon a number of variables, including the estimated future retirement costs, estimated proven reserves, assumptions involving profit margins, inflation rates, and the assumed credit-adjusted risk-free interest rates. Furthermore, these obligations are unfunded. If these accruals are insufficient or our liability in a particular year is greater than currently anticipated, our future operating results could be adversely affected. At December 31, 2009, we have accrued $19.5 million for our asset retirement obligations, most of which will be incurred at our underground mining operations at the end of the mines' life.

Surety Bonds/Financial Assurance

We use surety bonds, trusts and letters of credit to provide financial assurance for certain transactions and business activities. Federal and state laws require us to obtain surety bonds to secure payment of certain long-term obligations, including mine closure or reclamation costs and other miscellaneous obligations. The bonds are renewable on a yearly basis.

Surety bond costs have increased in recent years while the market terms of such bonds have generally become more unfavorable. In addition, the number of companies willing to issue surety bonds has decreased. Bonding companies also require posting of collateral, typically in the form of letters of credit, to secure the surety bonds. As of December 31, 2009, we had outstanding surety bonds and collateral with parties for post-mining reclamation totaling $35.0 million, plus $8.9 million for miscellaneous purposes. As of December 31, 2009, we maintained letters of credit totaling $30.4 million to secure surety bonds plus $7.9 million in other forms of collateral to satisfy reclamation obligations.

Climate Change

Global climate change continues to attract considerable public and scientific attention with widespread concern about the impacts of human activity, especially the emission of greenhouse gases ("GHGs"), such as carbon dioxide and methane. Combustion of fossil fuels, such as the coal and methane gas we produce, results in the creation of carbon dioxide that is currently emitted into the atmosphere by coal and gas end-users. Further, some of our operations, such as coal mining and coke production, directly emit GHGs. Laws and regulations governing emissions of GHGs have been

14

adopted by foreign governments, including the European Union and member countries, individual states in the United States, and regional governmental authorities. Further, numerous proposals also have been made and are likely to continue to be made at the international, national, regional, and state levels of government that are intended to limit emissions of GHGs by enforceable requirements and voluntary measures. In addition, the United States and over 160 other nations are signatories to the 1992 Framework Convention on Climate Change, which is intended to limit emissions of GHGs. In December 1997, in Kyoto, Japan, the signatories to the convention established a binding set of emission targets for developed nations. Although the specific emission targets vary from country to country, the United States would have been required to reduce emissions to 93% of 1990 levels from 2008 through 2012. Although the United States has not ratified the Kyoto agreement and is not bound by its emission targets, the United States is participating in international discussions to develop a treaty or other agreement to require reductions in GHG emissions after 2012 and has signed the Copenhagen Accord, which includes a non-binding commitment to reduce GHG emissions.

In April 2009, in response to a 2007 U.S. Supreme Court decision, EPA proposed findings that emissions of GHGs from motor vehicles are contributing to air pollution which, in turn, is endangering the public health and welfare. These proposed findings (which were made final in December 2009) set in motion the process for EPA to regulate GHGs from mobile sources, which in turn may result in regulation of GHGs from stationary sources under the Clean Air Act. EPA's findings focus on six GHGs, including carbon dioxide and nitrous oxide (which are emitted from coal combustion) and methane (which is emitted from coal beds). Although EPA has stated a preference that GHG reduction be based on new federal legislation rather than through agency regulation pursuant to the existing Clean Air Act, EPA is nonetheless taking steps to regulate many sources of GHGs without further legislation (see Clean Air Act below). It is difficult to predict reliably how such regulation will develop and when or whether it will take effect, as EPA's recently finalized findings that underpin such regulation are the subject of a number of lawsuits. Also, bills have been introduced in Congress that would, if enacted, prevent EPA from regulating GHGs under the Clean Air Act.

The U.S. House of Representatives has passed a bill that would regulate GHG emissions through a "cap and trade" system and related programs, which generally would require emitters of GHGs to purchase or otherwise obtain allowances to emit GHGs. Similar bills have been proposed in the U.S. Senate. However, it is uncertain whether Congress will enact "cap and trade" or other legislation to address climate change and, if it does, when it will occur and what it will require.

Coalbed methane must be expelled from our underground coal mines for mining safety reasons. Our gas operations extract coalbed methane from our underground coal mines prior to mining. With the exception of some coalbed methane which is vented into the atmosphere when the coal is mined, the methane is captured. If regulation of GHG emissions does not exempt the release of coalbed methane, we may have to curtail coal production, pay higher taxes, or incur costs to purchase credits that allow us to continue operations as they now exist at our underground coal mines. The amount of coalbed methane we capture is recorded, on a voluntary basis, with the U.S Department of Energy. We have recorded the amounts we have captured since 1992. In addition, Jim Walter Resources, Inc is registered as an Offsets Provider of credits with the Chicago Climate Exchange ("CCX"), an international rules-based GHG emission reduction, audit, registry and trading program based in the U.S. As a member, Jim Walter Resources,Inc. reports, on behalf of the mining, cokemaking and natural gas businesses (collectively, "Jim Walter Resources") to the CCX and has agreed to reduce emissions a minimum of 1% per year from its allocated annual emissions allowance, or baseline, and further committed to reduce its emissions a minimum of 6% below its baseline by the year 2010. Members who reduce beyond their targets have surplus allowances to sell or bank on the CCX. As of December 31, 2009, Jim Walter Resources had a total of 27,670 carbon financial instruments ("CFI") registered on the CCX as a result of carbon recapture, consisting of 5,858 exchange allowances and 21,812 exchange offsets. A CFI is equal to 100 metric tons of carbon dioxide credits available for use or sale on the

15

CCX. In addition, in 2009, Jim Walter Resources partnered with Biothermica Technologies to capture and mitigate the methane that is vented into the atmosphere as a result of the mining process. This project resulted in the listing of the project with the Climate Action Reserve on February 2, 2010, a national offsets program working to ensure integrity, transparency and financial value in the U.S. carbon market by establishing regulatory-quality standards for the development, quantification and verification of GHG emissions reduction projects in North America. If regulation of GHGs does not give us credit for capturing methane that would otherwise be released into the atmosphere at our coal mines, any value associated with our historical or future credits would be reduced or eliminated.

Depending on their requirements, additional laws or regulations regarding GHG emissions or other actions to limit GHG emissions could result in fuel switching, from coal or, to a lesser degree, natural gas to other fuel sources. Alternative fuels (non-fossil fuels) could become more attractive than coal or, to a lesser degree, natural gas in order to reduce GHG emissions. This could result in a reduction in the demand for our coal and, to a lesser degree, our natural gas, and, therefore, our revenues, as well as reduce the value of our reserves (although fuel switching could increase demand for our natural gas, which emits less GHG when burned than an equivalent quantity of coal). The anticipation of such requirements could also lead to reduced demand for some of our products. Additional GHG laws or regulations could also increase our costs, such as those to produce natural gas and manufacture coke. Although the potential impacts on us of additional climate change regulation are difficult to reliably quantify, they could be material.

Clean Air Act

The federal Clean Air Act ("CAA") and comparable state laws that regulate air emissions affect coal mining and coking operations both directly and indirectly. Direct impacts on coal mining may occur through permitting requirements and/or emission control requirements relating to particulate matter, such as fugitive dust, or fine particulate matter measuring 2.5 micrometers in diameter or smaller. The Clean Air Act indirectly affects our mining operations and directly affects our cokemaking operations by extensively regulating the air emissions of sulfur dioxide, nitrogen oxides, mercury and other compounds emitted by coal-fired utilities, steel manufacturers and coke ovens. As described below, proposed regulations would also subject GHG emissions to regulation under the Clean Air Act.

The CAA requires, among other things, the regulation of hazardous air pollutants through the development and promulgation of Maximum Achievable Control Technology ("MACT") Standards. The EPA has developed various industry-specific MACT standards pursuant to this requirement. The CAA requires EPA to promulgate regulations establishing emission standards for each category of Hazardous Air Pollutants. EPA must also conduct risk assessments on each source category that is already subject to MACT standards and determine if additional standards are needed to reduce residual risks.

Our cokemaking facilities are subject to certain MACT standards and NESHAPS (National Emissions Standards for Hazardous Air Pollutants). Relative to MACT, these standards apply to pushing, quenching, and under-firing stacks and went into effect in April 2006. The Boiler MACT was withdrawn in recent years but is still under consideration by EPA. Concerning NESHAPS, the standards include Coke Oven NESHAPS (1993), Benzene NESHAPS and Benzene Waste NESHAPS, which were also enacted in the early 1990's. EPA is required to make a risk-based determination for pushing and quenching emissions and determine whether additional emissions reductions are necessary from this process by 2011. EPA has yet to publish or propose any residual risk standards from these operations; therefore, the impact cannot be estimated at this time. The portion of NESHAP which applies to coke ovens addresses emissions from charging, coke oven battery tops, and coke oven doors. With regard to this standard, Walter Coke chose the LAER (Lowest Achievable Emissions Rate) track, and therefore is not required to comply with residual risk until 2020. Since the scope of future changes is relatively uncertain, the magnitude of the impact of these anticipated changes cannot be estimated at this time.

16

The CAA also requires EPA to develop and implement National Ambient Air Quality Standards or NAAQS for criteria pollutants, which include, among others, particulate matter. In 1997, EPA established 24-hour and annual standards for fine particles that are less than 2.5 micrometers in size or PM2.5 and in 2006, EPA tightened the 24-hour standard but retained the annual standard. States are required to demonstrate compliance with the fine particle standard by April 2010, with a possible extension to April 2015. EPA designated certain counties in which we operate as "nonattainment" and "unclassified/attainment" for the 2006 PM2.5 fine particle standard. State Implementation Plans for the 2006 standard are expected to be due in early 2013, with attainment demonstrations with the 2006 standard expected to be made thereafter. It is anticipated that EPA's fine particle programs could result in significant costs to us; however, it is impossible to estimate the magnitude of these costs at this time as state and federal agencies are still developing regulations for the programs and implementation could be as late as 2019.

The EPA has initiated a regional haze program designed to protect and improve visibility at and around national parks, national wilderness areas and international parks. This program may result in additional emissions restrictions from new coal-fired power plants whose operation may impair visibility at and around federally protected areas. This program may also require certain existing coal-fired power plants to install additional control measures designed to limit haze-causing emissions, such as sulfur dioxide, nitrogen oxides, volatile organic chemicals and particulate matter. In addition, there are currently certain bills before Congress that would cut mercury emissions by 90 percent from coal-fired power plants and tighten national limits on emissions of sulfur dioxide (SO2) and nitrogen oxides (NOx). These bills, and others such as acid rain regulations, could affect the future market for coal.

EPA's finding concerning GHG endangerment of public health and welfare (see the discussion on Climate Change) may lead to regulation of GHG emissions from stationary sources under the Clean Air Act. In connection with that finding, EPA has also proposed a tailoring rule which would set emission thresholds for GHG regulation under EPA's current Clean Air Act stationary source permitting requirements. Once finalized, this rule may draw legal challenges, as EPA's endangerment finding has. Accordingly, the impact of such regulation on us cannot be reliably estimated at this time, although it could be material.

Clean Water Act

The federal Clean Water Act ("CWA") and corresponding state laws affect our operations by imposing restrictions on discharges of wastewater into creeks and streams. These restrictions, more often than not, require us to pre-treat the wastewater prior to discharging it. Permits requiring regular monitoring and compliance with effluent limitations and reporting requirements govern the discharge of pollutants into regulated waters. Our mining and cokemaking operations maintain water discharge permits as required under the National Pollutant Discharge Elimination System program of the CWA, and conduct its operations to be in compliance with such permits. We believe we have obtained all permits required under the Clean Water Act and corresponding state laws and are in substantial compliance with such permits. However, new requirements under the Clean Water Act and corresponding state laws may cause us to incur significant additional costs that could adversely affect our operating results.

Resource Conservation and Recovery Act

The Resource Conservation and Recovery Act ("RCRA") and corresponding state laws establish standards for the management of solid and hazardous wastes generated at our various facilities. Besides affecting current waste disposal practices, RCRA also addresses the environmental effects of certain past hazardous waste treatment, storage and disposal. In addition, RCRA also requires certain of our facilities to evaluate and respond to any past release, or threatened release, of a hazardous substance that may pose a risk to human health or the environment.

17

RCRA may affect coal mining operations by establishing requirements for the proper management, handling, transportation and disposal of solid and hazardous wastes. Currently, certain coal mine wastes, such as earth and rock covering a mineral deposit (commonly referred to as overburden) and coal cleaning wastes, are exempted from hazardous waste management under RCRA. Any change or reclassification of this exemption could significantly increase our coal mining costs.

Our cokemaking operation is in the study phase of a RCRA corrective action program. Until the studies are complete, we are unable to determine the cleanup or remediation that may be required and are unable to estimate the total cost of any such remediation activities. For additional information regarding significant enforcement actions, capital expenditures and costs of compliance, see "Item 3. Legal Proceedings" and Environmental Matters under "Note 14- Commitments and Contingencies."

Comprehensive Environmental Response, Compensation and Liability Act

The Comprehensive Environmental Response, Compensation and Liability Act, CERCLA or Superfund, and similar state laws affect our coal mining and coking operations by, among other things, imposing investigation and cleanup requirements for threatened or actual releases of hazardous substances. Under CERCLA, joint and several liability may be imposed on operators, generators, site owners, lessees and others regardless of fault or the legality of the original activity that caused or resulted in the release of the hazardous substances. Although the EPA excludes most wastes generated by coal mining and processing operations from the hazardous waste laws, the universe of materials/wastes governed by CERCLA is broader than "hazardous waste" and such even non-hazardous wastes can, in certain circumstances, contain hazardous substances which, if released into the environment, are governed by CERCLA. Alabama's version of CERCLA mirrors the federal version, with the important difference that there is no joint and several liability—liability is consistent with one's contribution to the contamination. In addition, the disposal, release or spilling of some products used by coal and coking companies in operations, such as chemicals, could trigger the liability provisions of CERCLA or similar state laws because, at that point, they are deemed to be waste and the activity, even though inadvertent, is deemed to constitute disposal or a covered CERCLA release. Thus, we may be subject to liability under CERCLA and similar state laws for properties that 1) we currently own, lease or operate or that 2) we, our predecessors, or former subsidiaries have previously owned, leased or operated, 3) sites to which we, our predecessors or former subsidiaries sent waste materials, or 4) sites at which hazardous substances from our facilities' operations have otherwise come to be located.

Other Environmental Laws

We are required to comply with numerous other federal, state and local environmental laws and regulations in addition to those previously discussed. These additional laws include, for example, the Endangered Species Act, the Safe Drinking Water Act, the Toxic Substance Control Act and the Emergency Planning and Community Right-to-Know Act.

Seasonality

Our primary business is not materially impacted by seasonal fluctuations. Demand for coal is generally more heavily influenced by other factors such as the general economy, interest rates and commodity prices.

Employees

As of December 31, 2009, we employed approximately 2,100 people, of whom approximately 1,300 were hourly workers and 800 were salaried employees. Unions represented approximately 1,300 employees under collective bargaining agreements, of which approximately 1,100 were covered by one contract with the United Mine Workers of America that expires on December 31, 2011.

18

Available Information

We make our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K and amendments thereto available on our website atwww.walterenergy.com without charge as soon as reasonably practical after filing or furnishing these reports to the Securities and Exchange Commission ("SEC"). Additionally, we will also provide, without charge, a copy of our Form 10-K to any shareholder by mail. Requests should be sent to Walter Energy, Inc., Attention: Shareholder Relations, 4211 W. Boy Scout Boulevard, Tampa, Florida 33607. You may read and copy any document the Company files at the SEC's public reference room at 450 Fifth Street, N.W., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room. Our SEC filings are also available to the public from the SEC's website athttp://www.sec.gov.

Continuing unfavorable economic, financial and business conditions may adversely affect our businesses and financial condition.

The financial markets in the United States, Europe, South America and Asia have been experiencing extreme disruption over the last year. As widely reported, these markets have experienced, among other things, extreme volatility in security prices, commodities and currencies; severely diminished liquidity and credit availability, rating downgrades and declining valuations of certain investments. The tightening of credit in financial markets, the inability to access capital markets, the bankruptcy, failure, collapse or sale of various financial institutions and an unprecedented level of intervention from the United States federal government could have a material adverse effect on the demand for our coal, coke and natural gas products and on our sales, pricing and profitability. Continuation or worsening of the current economic conditions, a prolonged global, national or regional economic recession or other similar events could have a material adverse effect on the demand for our products and on our sales, pricing and profitability. We are unable to predict the likely duration and severity of the current disruption in financial markets and adverse economic conditions in the U.S. and other countries and the impact these events may have on our operations and the industry in general.

Our businesses may suffer as a result of a substantial or extended decline in pricing, demand and other factors beyond our control, which could negatively affect our operating results and cash flows.

Our businesses are cyclical and have experienced significant difficulties in the past. Our financial performance depends, in large part, on varying conditions in the international and domestic markets we serve, which fluctuate in response to various factors beyond our control. The prices at which we sell our coal, coke and natural gas are largely dependent on prevailing market prices for those products. We have experienced significant price fluctuations in our coal, coke and natural gas businesses, and we expect that such fluctuations will continue. Demand for and, therefore, the price of, coal, coke and natural gas are driven by a variety of factors such as availability, price, location and quality of competing sources of coal, coke or natural gas, availability of alternative fuels or energy sources, government regulation and economic conditions. In addition, reductions in the demand for metallurgical coal caused by reduced steel production by our customers, increases in the use of substitutes for steel (such as aluminum, composites or plastics) and the use of steel-making technologies that use less or no metallurgical coal can significantly affect our financial results and impede growth. Demand for steam coal is primarily driven by the price of steam coal and natural gas and the consumption patterns of the domestic electric power generation industry, which, in turn, is influenced by demand for electricity and technological developments. We estimate that a 10% decrease in the price of metallurgical coal in 2009 would have resulted in a reduction in pre-tax income of $75.8 million. Demand for natural gas is also affected by storage levels of natural gas in North America and consumption patterns, which can be affected by weather conditions. We estimate that a 10%

19

decrease in the price in natural gas in 2009 would have resulted in a reduction in pre-tax income of approximately $2.6 million in that year, which includes the benefit of hedges. Occasionally we utilize derivative commodity instruments to manage fluctuations in natural gas prices. If we choose not to engage in, or reduce our use of hedging arrangements in the future, we may be more adversely affected by changes in the pricing of these commodities. Currently, we have hedged approximately 24% of our anticipated 2010 natural gas production at an average price of $6.20 per thousand cubic feet.

The failure of our customers to honor or renew contracts could adversely affect our business.

A significant portion of the sales of our coal, coke and natural gas are to long-term customers. The success of our businesses depends on our ability to retain our current clients, renew our existing customer contracts and solicit new customers. Our ability to do so generally depends on a variety of factors, including the quality and price of our products, our ability to market these products effectively, our ability to deliver on a timely basis and the level of competition we face. If current customers do not honor current contract commitments, terminate agreements or exercise force majeure provisions allowing for the temporary suspension of performance, our revenues will be adversely affected. If we are unsuccessful in renewing contracts with our long-term customers and they discontinue purchasing coal, coke or natural gas from us, renew contracts on terms less favorable than in the past, or if we are unable to sell our coal, coke or natural gas to new customers on terms as favorable to us, our revenues could suffer significantly.

Coal mining is subject to inherent risks and is dependent upon many factors and conditions beyond our control, which may cause our profitability and our financial position to decline.

The majority of our coal mining operations are conducted in underground mines and the balance of our operations is surface mining operations. Coal mining is subject to inherent risks and is dependent upon a number of conditions beyond our control that can affect our costs and production schedules at particular mines. These risks and conditions include, but are not limited to:

- •

- variations in geological conditions, such as the thickness of the coal seam and amount of rock embedded in the coal deposit;

- •

- mining, process and equipment or mechanical failures;

- •

- adverse weather and natural disasters, such as heavy rains and flooding;

- •

- environmental hazards, such as subsidence and excess water ingress;

- •

- delays and difficulties in acquiring, maintaining or renewing necessary permits or mining rights; and

- •