UNITED STATES | |||

SECURITIES AND EXCHANGE COMMISSION | |||

Washington, D.C. 20549 | |||

| |||

SCHEDULE 14A | |||

| |||

Proxy Statement Pursuant to Section 14(a) of | |||

| |||

Filed by the Registrant x | |||

| |||

Filed by a Party other than the Registrant o | |||

| |||

Check the appropriate box: | |||

o | Preliminary Proxy Statement | ||

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | ||

o | Definitive Proxy Statement | ||

x | Definitive Additional Materials | ||

o | Soliciting Material under §240.14a-12 | ||

| |||

Walter Energy, Inc. | |||

(Name of Registrant as Specified In Its Charter) | |||

| |||

| |||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | |||

| |||

Payment of Filing Fee (Check the appropriate box): | |||

x | No fee required. | ||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | ||

| (1) | Title of each class of securities to which transaction applies: | |

|

|

| |

| (2) | Aggregate number of securities to which transaction applies: | |

|

|

| |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

|

|

| |

| (4) | Proposed maximum aggregate value of transaction: | |

|

|

| |

| (5) | Total fee paid: | |

|

|

| |

o | Fee paid previously with preliminary materials. | ||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | ||

| (1) | Amount Previously Paid: | |

|

|

| |

| (2) | Form, Schedule or Registration Statement No.: | |

|

|

| |

| (3) | Filing Party: | |

|

|

| |

| (4) | Date Filed: | |

|

|

| |

On April 5, 2013, Walter Energy, Inc. used the following presentation materials in a meeting with Institutional Shareholder Services.

| Well Positioned For Success Investor Presentation April 2013 |

| Forward-Looking & Non-GAAP Statements 2 Except for historical information contained herein, the statements in this release are forward-looking and made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 and may involve a number of risks and uncertainties. Forward-looking statements are based on information available to management at the time, and they involve judgments and estimates. Forward-looking statements include expressions such as "believe," "anticipate," "expect," "estimate," "intend," "may," "plan," "predict," "will," and similar terms and expressions. These forward-looking statements are made based on expectations and beliefs concerning future events affecting us and are subject to various risks, uncertainties and factors relating to our operations and business environment, all of which are difficult to predict and many of which are beyond our control, that could cause our actual results to differ materially from those matters expressed in or implied by these forward-looking statements. The following factors are among those that may cause actual results to differ materially from our forward-looking statements: unfavorable economic, financial and business conditions; the global economic crisis; market conditions beyond our control; prolonged decline in the price of coal; decline in global coal or steel demand; prolonged or dramatic shortages or difficulties in coal production; our customer's refusal to honor or renew contracts; our ability to collect payments from our customers; inherent risks in coal mining such as weather patterns and conditions affecting production, geological conditions, equipment failure and other operational risks associated with mining; title defects preventing us from (or resulting in additional costs for) mining our mineral interests; concentration of our mining operations in limited number of areas; a significant reduction of, or loss of purchases by, our largest customers; unavailability of cost-effective transportation for our coal; availability, performance and costs of railroad, barge, truck and other transportation; disruptions or delays at the port facilities we use; risks associated with our reclamation and mine closure obligations, including failure to obtain or renew surety bonds; significant increase in competitive pressures and foreign currency fluctuations; significant cost increases and delays in the delivery of raw materials, mining equipment and purchased components; availability of adequate skilled employees and other labor relations matters; inaccuracies in our estimates of our coal reserves; estimates concerning economically recoverable coal reserves; greater than anticipated costs incurred for compliance with environmental liabilities or limitations on our abilities to produce or sell coal; our ability to attract and retain key personnel; future regulations that increase our costs or limit our ability to produce coal; new laws and regulations to reduce greenhouse gas emissions that impact the demand for our coal reserves; adverse rulings in current or future litigation; inability to access needed capital; events beyond our control may result in an event of default under one or more of our debt instruments; availability of licenses, permits, and other authorizations may be subject to challenges; risks associated with our reclamation and mine closure obligations; failure to meet project development and expansion targets; risks associated with operating in foreign jurisdictions; risks related to our indebtedness and our ability to generate cash for our financial obligations; downgrade in our credit rating; our ability to identify suitable acquisition candidates to promote growth; our ability to successfully integrate acquisitions; our exposure to indemnification obligations; volatility in the price of our common stock; our ability to pay regular dividends to stockholders; costs related to our post-retirement benefit obligations and workers' compensation obligations; our exposure to litigation; and other risks and uncertainties including those described in our filings with the SEC. Forward-looking statements made by us in this release, or elsewhere, speak only as of the date on which the statements were made. You are advised to read the risk factors in our most recently filed Annual Report on Form 10-K and subsequent filings with the SEC, which are available on our website at www.walterenergy.com and on the SEC's website at www.sec.gov. New risks and uncertainties arise from time to time, and it is impossible for us to predict these events or how they may affect us or our anticipated results. We have no duty to, and do not intend to, update or revise the forward-looking statements in this release, except as may be required by law. In light of these risks and uncertainties, readers should keep in mind that any forward-looking statement made in this press release may not occur. All data presented herein is as of the date of this release unless otherwise noted. We use a number of different financial measures in assessing the overall performance of our business, including measures calculated in accordance with United States generally accepted accounting principles (“GAAP”) and non-GAAP numbers. EBITDA is a financial measure that is not calculated in conformity with GAAP and should be considered supplemental to, and not as a substitute or superior to, financial measures calculated in conformity with GAAP. We believe that EBITDA is a useful measure as some investors and analysts use EBITDA to compare us against other companies and to help analyze our ability to satisfy principal and interest obligations and capital expenditure needs. EBITDA may not be comparable to similarly titled measures used by other companies. |

| Disclaimer 3 Important Additional Information On March 8, 2013, Walter Energy filed with the Securities and Exchange Commission (“SEC”), a definitive proxy statement (as it may be amended or supplemented, the “Proxy Statement”) concerning the proposals to be presented at Walter Energy’s 2013 Annual Meeting of Stockholders in connection with the solicitation of proxies from Walter Energy’s stockholders. The Proxy Statement contains important information about Walter Energy and the 2013 Annual Meeting. In addition, Walter Energy files annual, quarterly and special reports, proxy statements and other information with the SEC. INVESTORS AND STOCKHOLDERS ARE STRONGLY URGED TO READ THE PROXY STATEMENT AND ACCOMPANYING PROXY CARD AND OTHER DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT WALTER ENERGY AND THE PROPOSALS TO BE PRESENTED AT THE 2013 ANNUAL MEETING. These documents are available free of charge at the SEC’s website (www.sec.gov) or from Walter Energy at our investor relations website (www.investorrelations.walterenergy.com). The contents of the websites referenced herein are not deemed to be incorporated by reference into the Proxy Statement. Certain Information Regarding Participants Walter Energy, its directors and certain of its officers may be deemed to be participants in the solicitation of Walter Energy’s stockholders in connection with its 2013 Annual Meeting. Information regarding the names, affiliations and direct and indirect interests (by security holdings or otherwise) of these persons is found in the Proxy Statement for the 2013 Annual Meeting, which is filed with the SEC. Additional information regarding these persons can also be found in other documents filed by Walter Energy with the SEC. Stockholders are able to obtain a free copy of the Proxy Statement and other documents filed by Walter Energy with the SEC from the sources listed above. |

| Review of Contents 4 Walter Energy – A History of Value Creation Business Footprint and Overview Creation of a Pure-Play Met Coal Company History of Strong Performance Throughout The Economic Cycle History of Diligent Return of Capital to Shareholders Decisive Actions Have Well Positioned Walter Energy for Market Recovery Experienced Management Team that Is Driving Shareholder Value Strong Operational Results Disciplined Growth with a Focus on Profitability Significant Growth Opportunities In Place Strengthened Balance Sheet Provides Platform for Growth and Delivering Value Highly Experienced and Engaged Board Balance of Historical Insights and Fresh Perspectives 40% of Board Added in Last 2 Years Extensive Mining, Executive and Large Cap Public Company Experience Audley is Seeking Effective Control with a Flawed Slate and Flawed Plan Audley Capital is Seeking Effective Control with Five Out of Nine Independent Board Seats Dissident Nominees Do Not Have the Right Experience or Expertise Proposals Either Restate Walter Energy’s Established Strategy or Demonstrate a Flawed Understanding of Our Business and Would Destroy Shareholder Value |

| Walter Energy – A Summary Overview 5 Value Proposition Key Facts 2009 2012 Total Met Coal Production 5.4 MMt 11.7 MMt Revenue $1.0 B $2.4 B Adj. EBITDA $275 M $412 M Underground Reserve Life 15-17 years 30+ years #1 “Pure-Play” Metallurgical Coal Company High Quality, Premium Product with 30+ Year Reserve Life Diversified Sales and Geographic Mix Advantaged Access to Atlantic and Pacific Markets Low Cost Asset Base in Stable and Secure Geographies Alabama, U.S. West Virginia, U.S. British Columbia, Canada Wales, U.K. “Walter is the best way to gain exposure to upward coking coal price momentum. The company offers pure play exposure to coking coal... offers better risk-reward and downside protection due to its lower cost position and premium mix” – Morgan Stanley, February 19, 2013 |

| Walter Industries – 2005 6 2005 Sales by Segment In 2005, Walter Was a Diversified Conglomerate With Only 2 Significant Coal Mines in Alabama “The spin-out [of MWA] has moved Walter Industries one step closer to becoming a “pure-play” coal company. The separation also simplifies the operating structure, and should allow for an unlocking of ‘shareholder value’ across the remaining assets. Next up will be the final disposition of the Homebuilding and Finance assets” - Brean Murray Carret & Co., December 18, 2006 Spun off in 2006: Homebuilding Closed & Financing Business Spun off in 2009: Natural Resources (Mining) 27% Mueller Water Products 46% Homebuilding & Finance 22% Other 5% |

| Board Engineered the Evolution of Walter Energy into a Focused, Pure-Play Metallurgical Coal Mining Company 7 Long Track Record of Unlocking Value for Shareholders – 127% Return Since Mueller Water Spin-Off (1) Spun-off Mueller Water 2011 2010 2009 2006 Walter Energy first positioned itself as a pure play metallurgical coal producer with the spinoff of a number of unrelated business units, including the homebuilding business and the financing business” - Scotia Capital, June 8, 2011 Closed Jim Walter Homes, spun-off Walter Investment Management Western Coal acquisition finalized; Acquired mineral leases from Chevron Mining to create the Blue Creek Mine opportunity Entered into an agreement to acquire Western Coal, providing Walter with operating, geographic and customer diversification; Acquired Mobile River Terminal and HighMount Natural Gas Assets Note: (!) Walter shareholders received an ~75% ownership in Mueller Water Products on 14-Dec-06. Growth in market capitalizations reflects the pro-rata change to Walter shareholders. Return is as of February 15, 2013, the unaffected date prior to Audley press release on February 19, 2013 |

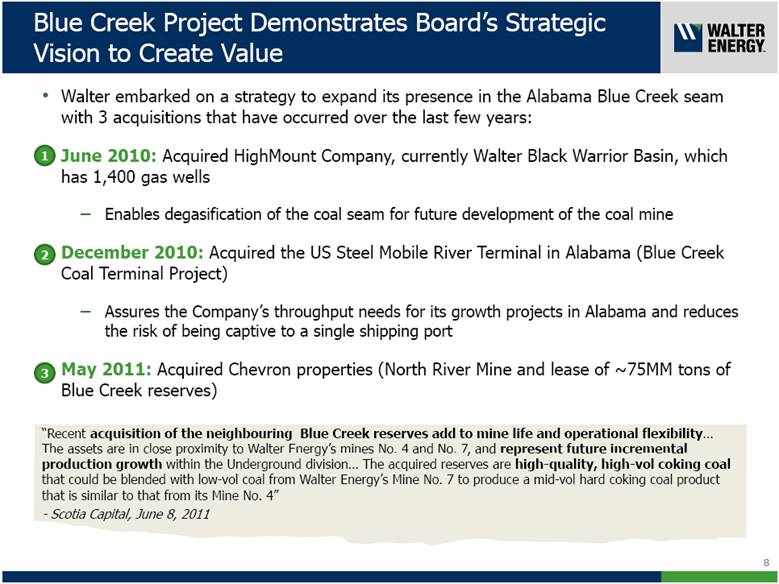

| 8 Blue Creek Project Demonstrates Board’s Strategic Vision to Create Value “Recent acquisition of the neighbouring Blue Creek reserves add to mine life and operational flexibility... The assets are in close proximity to Walter Energy’s mines No. 4 and No. 7, and represent future incremental production growth within the Underground division... The acquired reserves are high-quality, high-vol coking coal that could be blended with low-vol coal from Walter Energy’s Mine No. 7 to produce a mid-vol hard coking coal product that is similar to that from its Mine No. 4” - Scotia Capital, June 8, 2011 Walter embarked on a strategy to expand its presence in the Alabama Blue Creek seam with 3 acquisitions that have occurred over the last few years: June 2010: Acquired HighMount Company, currently Walter Black Warrior Basin, which has 1,400 gas wells Enables degasification of the coal seam for future development of the coal mine December 2010: Acquired the US Steel Mobile River Terminal in Alabama (Blue Creek Coal Terminal Project) Assures the Company’s throughput needs for its growth projects in Alabama and reduces the risk of being captive to a single shipping port May 2011: Acquired Chevron properties (North River Mine and lease of ~75MM tons of Blue Creek reserves) 1 2 3 |

| Walter’s Board Has Transformed Walter into a Leading, Pure-Play Metallurgical Coal Company 9 2012 Coal Production by Mine Diversified Asset Base with 15 Mines in 3 Countries Increased Met Production & Coal Reserves (MMt) 2005 Top Global Met Coal Producer Street Views of Walter’s Transformation “Since the Western merger, Walter has diversified its asset base with access to both the Pacific and Atlantic basins and remains a large, liquid met coal play with about 85% of revenues coming from met coal sales” - BMO Capital Markets, September 8, 2011 “The incorporation of Western Coal into the company adds geographic, endmarket, and operational diversification to Walter Energy, including a unique ability to cost-effectively deliver to both Atlantic and Pacific markets” - Scotia Capital, June 8, 2011 “WLT + WTN = met coal powerhouse WLT-WTN combo creates 5th largest global met coal supplier and leading met ‘pure play’” - Deutsche Bank, March 24, 2011 0 4 8 12 Met Production 5.2 11.7 0 100 200 300 400 Reserves 130 401 |

| 10 Challenges High costs of production at legacy Western mines Depressed met coal prices have squeezed margins of higher cost mines SG&A cost control despite need to maintain multi-jurisdictional footprint Unforeseeable geological issues at Alabama mines Management turnover post-transaction Significant debt on balance sheet entering a downcycle pricing environment Actions Leadership is Successfully Addressing the Challenges Faced by Walter Since the Western Acquisition Walter Is Now Well Positioned to Capitalize on the Market Rebound Transitioned from contractor to owner-operated mines and reduced Canadian cash costs of production 40% from Q4 2011 to Q4 2012 with initiatives to further reduce costs underway Idled Willow Creek mine and reduced production at lower margin mines, including Brule Reduced SG&A costs by $32.5MM in 2012 with public commitment to further reductions Effectively worked through geological issues at Mine No. 7 Assembled best-in-class management team; Strong board and leadership team now in-place Company has successfully reduced term debt, enhanced liquidity and extended its maturity profile |

| Track Record of Delivering Strong Long-Term Shareholder Returns 11 Walter Total Shareholder Returns vs. US Coal Peers (1) (%) WLT Total Shareholder Returns Relative to US Peer Median (5) Shareholder Returns Have Outperformed Walter’s Peer Group Notes: (1) Represents total shareholder return assuming all dividends reinvested (2) From February 15 to March 29, 2013 (3) As of February 15, 2013, unaffected date prior to Audley press release on February 19, 2013 (4) Includes Mueller spin-off (5) US Coal Peers include Arch Coal, Alpha Natural Resources, Peabody Energy, Cloud Peak, CONSOL Energy and James River Coal Company (6) The MSCI Metals & Mining Index used by Audley does not include any companies which mine only coal; Index includes diversified miners, gold, aluminum, and other companies (3)(4) (3) (3) (3) (3) (2) Walter Energy has outperformed its U.S. coal peers across various time frames and through multiple industry cycles Walter is a pure-play metallurgical coal company and should be compared to other U.S. coal companies not global metals and mining indices(6) Recent share price pressures are industry-wide Source: CapitalIQ (20.0) 0.0 20.0 40.0 60.0 80.0 100.0 Since Audley Announcement YTD Last 1 Year Last 3 Years Last 5 Years Last 10 Years (14.3) 15.0 (0.7) 8.0 68.8 524.7 |

| Jul-08 Apr-11 Peak Dec-08 Apr-13 From Trough to Trough and Peak to Peak, Walter’s Board Has Created Value 12 Trough 29% 98% 2007 – 2009 Cycle Hard Coking Coal Price ($ / metric ton) Source: Wood Mackenzie, Bloomberg Walter Share Price 2010 – 2012 Cycle 2007 – 2009 2010 - 2012 Cycle Cycle Jul. 2008 share price: $109.77 Apr. 2011 share price: $141.17 Apr. 2013 share price: $24.15 Dec. 2008 share price: $12.20 Peak Trough 0 90 180 270 360 450 2007 2008 2009 2010 2011 2013 0 40 80 120 160 12.20 109.77 24.15 141.17 |

| Note: As of February 15, 2013 13 Source: CapitallQ Current Dividend Yield (1) (%) Consistent and growing dividend Increased dividend per share >300% over the past 10 years Maintained dividend throughout industry cycles Dividend yield consistent with U.S. coal peers Walter’s Annual Dividend Per Share Over Time ($) Responsible Return of Capital to Shareholders 0.0 1.0 2.0 3.0 Arch CONSOL Peabody Walter Alpha Cloud Peak James River 2.0 1.5 1.4 1.3 0.0 0.0 0.0 0.00 0.25 0.50 0.75 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 0.12 0.13 0.16 0.16 0.20 0.30 0.40 0.48 0.50 0.50 |

| 14 Source: Wood Mackenzie and CRU Total Seaborne Metallurgical Coal Demand LV PCI SSCC +54% Cyclical Downturn of Met Coal Market Is Poised for a Turnaround Wood Mackenzie Predicts Significant Growth of Met Coal Demand “...the worst of the downturn in the metallurgical coal market is over ...there is increasing evidence that steel production is likely to be marginally higher in 2013 compared with in 2012 in the key seaborne markets” – Morgan Stanley, January 24, 2013 “We are encouraged by recent spot price moves for export hard coking and PCI coal prices above the 1Q13 benchmark levels, and believe Walter as a near pure play in metallurgical coal would be a top beneficiary on a further price recovery beyond the depressed 4Q12-1Q13 levels” - Stifel Nicolaus, February 25, 2013 0 100 200 300 400 500 2012 2015 2020 2025 149 167 202 222 58 67 87 95 38 42 54 61 245 277 344 377 |

| 5. Strengthen Balance Sheet and Increase Financial Flexibility Strategic Initiatives to Position Walter to Capitalize on the Recovery of the Met Coal Market 15 1. Safety Is Our First Priority 2. Assemble and Leverage Best-in-Class Management 3. Increase Profitable, High Quality Met Coal Production 4. Reduce Costs and Manage Capital Spending Carefully |

| Consistently Improving Safety Performance Strong Commitment to Safety Total Reportable Injury Rates (21)% (15)% (26)% 16 Reportable Injury Rates Have Decreased 26% Year-over-Year Injury Rates Have Decreased Each of the Past 3 Years (50)% Source: Company Filings 2009 2010 2011 2012 |

| 17 Jan-2012 - Earl Doppelt (SVP, General Counsel and Secretary): Served as the senior legal officer of several multi-national companies, including The Nielsen Corporation (formerly VNU), ACNielsen Corporation, The Dun & Bradstreet Corporation and Paramount Communications. Has more than 30 years of legal experience. Jul-2012 - William Harvey (CFO): Served as SVP and CFO of Resolute Forest Products Inc. (formerly AbitibiBowater Inc.). Previously served as CFO of Bowater and played a major role in the 2007 merger of Abitibi-Consolidated and Bowater. Sep-2011 - Walter Scheller (CEO / Director): Served as President and Chief Operating Officer of Jim Walter Resources. Previously served as Group Executive and SVP - Strategic Operations at Peabody and VP - Operations at Consol Energy. Assembled World-Class Leadership Team Management May-2012 – Mike Madden (SVP, Chief Commercial Officer): Served as SVP, Sales and Marketing since February 2010 and VP, Marketing, Transportation, and Quality Control since 1997 for the Company's primary subsidiary, Jim Walter Resources. Apr-2012 – Thomas Lynch (SVP, Human Resources): Mr. Lynch has over 25 years of experience in Human Resources including labor and employee relations, performance management, recruitment and retention. Previously served as VP, Human Resources for NRG Energy, Inc. |

| Assembled World-Class Leadership Team (cont’d) 18 Jan-2012 - Daniel Cartwright (President of Canadian Operations): Served as VP, Underground Mining Operations since July 2011. Has more than 38 years of mining experience at Peabody and Shell Mining Company. Jan-2012 - Richard Donnelly (President of Jim Walter Resources): Served as VP Engineering at Jim Walter Resources since March 2003. Started his career with the Company in 1977. Operations Mar-2012 – Carol Farrell (President, Walter Coke): Served as Executive Vice President of Walter Coke and Walter Minerals. Started her career with the Company in 1981. Mar-2012 – Charles Stewart (SVP, Project Development): Served as the President and Chief Operating Officer of Walter Coke and Walter Minerals. Started his career with the Company in 1978. Apr-2012 – Dan Stickel (President, West Virginia Operations): Prior to the acquisition of Western Coal, served as President and CEO of West Virginia and US Operations under Cambrian Mining and Western Coal Corporation. Has more than 33 years of mining experience including US Steel Mining, Arch Coal and Drummond Company. |

| Achieved Record Met Coal Production 19 US Canada / UK 2013 Target Source: Company Filings Notes: Inclusive of an ~200K favorable impact from the re-alignment of methodology of accounting for production between the US and Canada performed in the second quarter 2012 Ability to increase production to 15MMt in 2013 as market conditions warrant Increased Metallurgical Coal Production 35% in 2012 Ability to Increase Production in 2013 to 15MMt as Market Conditions Warrant 5-Year Met Coal Production (MMt) +35% (Capacity (2)) (1) 0.0 3.0 6.0 9.0 12.0 15.0 18.0 2009 2010 2011 2012 2013 Target 6.0 7.0 11.5-13.0 Target 2.7 4.7 5.5 6.0 8.7 11.7 15.0 |

| Curtailed Production When Conditions Warranted Achieved Profitable Growth While Reducing Output at Lower Margin Mines 20 Source: Company Filings Jun-11: Idled Gauley Eagle underground mine Nov-11: Idled Aberpergwm underground mine in South Wales Mar-12: Curtailed Maple underground mine in West Virginia as well as production at Brule Jun-12: Idled Gauley Eagle surface mine Nov-12: Idled development work at Aberpergwm mine Mar-13: Accelerated closure of North River (thermal) mine in Alabama and idled Willow Creek mine in British Columbia Existing Leadership Has History of Taking Decisive Action “We Applaud the Company’s Decision to Idle Willow Creek ... this signals a willingness to take action and could foreshadow future closures should other CAD operations struggle with profitability...” – UBS, March 22, 2013 “We are supportive of Walter Energy announced production cutback of higher cost Canadian and US thermal coal mines. While its higher quality Alabama operations should find support as expected pricing recovers, we believe leaving some of its Canadian product in the ground appears appropriate” – Sterne Agee, March 22, 2013 “We view the Willow Creek mine closure as much more material, as it provides evidence that management is appropriately focused on profitability” – Goldman Sachs, March 22, 2013 |

| 21 Board and Management are Creating Value for the Long-Term Source: Company Filings 11.5-13.0 Significant Growth Opportunities in Place as Market Recovers 20.0+ Willow Creek Restart when there is visibility of sustained improvement in met coal price 19.0MM metric tons of reserves Capacity to produce 1.8 Mtpa Blue Creek Estimated mine life of 40 to 45 years of high quality metallurgical coal Secured over $500MM in Alabama state tax abatements Current capital commitments remain modest 74.9MM metric tons of reserves Belcourt-Saxon 50/50 joint venture with Anglo-American Pre-feasibility project with large resource base Metallurgical Coal Production (MMt) |

| 22 Source: Company Filings Wolverine Brule Willow Creek ($ / ton) ($ / ton) ($ / ton) (45%) (43%) Decreasing Total Cost of Production per Metric Ton per Product (35%) Canadian Coal Cost of Production per Metric Ton Decreasing Total Met ($ / ton) (21%) Hard Coking Coal ($ / ton) (9%) LV PCI ($ / ton) (39%) Cash Costs Have Decreased Significantly Since Current Walter Management Team Put in Place 150 83 50 100 150 200 250 Q4 2011 Q4 2012 195 111 50 100 150 200 250 Q4 2011 Q4 2012 50 100 150 200 250 Q4 2011 Q4 2012 119 95 50 100 150 200 250 Q4 2011 Q4 2012 96 87 50 100 150 200 250 Q4 2011 Q4 2012 204 125 50 100 150 200 250 Q4 2011 Q4 2012 223 145 |

| 23 2012 Total SG&A ($MM) Total SG&A Increase / (Reduction) 2011-2012 ($MM) #1 in SG&A Cost Reduction Leading U.S. Peers in SG&A Reduction SG&A Is Low Relative to Our Peers Despite Inclusion of Mine Level Overhead Costs (1) Source: Company Filings Notes: Alpha Natural Resources includes pro forma $164MM merger adjustment for the acquisition of Massey Energy 0 100 200 300 400 Peabody Energy Alpha Natural Resources CONSOL Energy Arch Coal Walter Energy James River Cloud Peak 269 210 148 134 133 60 55 (45.0) (30.0) (15.0) 0.0 15.0 30.0 45.0 Arch Coal Cloud Peak James River Peabody Energy Alpha Natural Resources CONSOL Energy Walter Energy 15.2 3.5 2.8 0.6 (19.9) (27.4) (32.3) |

| Disciplined Approach to SG&A Expenses and Capital Deployment 24 Recent Accomplishments / Initiatives SG&A 2011 – 2013E ($MM) SG&A Decreased by $32.3MM (19%) Year-Over-Year Downsized Canadian Headquarters Implemented Company-wide ERP (19)% (10)% Source: Company Filings Capex 2011 – 2013E ($MM) (44)% (6)% Tightened Capital Spending in 2012 2013 Capex Target of $220MM Continued Focus on Blue Creek Project 0 45 90 135 180 225 2011 2012 2013 Target 166 133 120 0 100 200 300 400 500 2011 2012 2013 Target 415 392 220 |

| Continued Strengthening of the Balance Sheet Financially Positioning the Company for Long-term Success An Extended Maturity and Liquidity Profile Combined with an Attractive Cost of Debt Has Strengthened Walter’s Balance Sheet 25 Increased liquidity and eliminated near term maturities Increased liquidity by $415MM in the form of cash on the balance sheet and revolver pay-down Reduced near-term maturities of secured debt by $722MM Extended maturity profile with no material debt obligations until 2015 Attractive cost of debt in-line with U.S. coal peers Total debt target of $1B “Operational restructuring is credit positive; upsized bond offering improves Walter’s liquidity position... we expect Walter to hold the cash on the balance sheet for liquidity purposes. We view this use of cash as prudent given the state of metallurgical coal markets” – Moody’s Investors Service, March 25, 2013 Ba3 / BB Ba1 / BB+ B1 / B+ B1 / B+ Ba3 / BB- Caa1 / CCC B2 / B+ Note: CLD – Cloud Peak Energy, CNX – CONSOL Energy, ACI – Arch Coal, WLT – Walter Energy, BTU – Peabody Energy, JRCC – James River Coal, ANR – Alpha Natural Resources Attractive Weighted Average Cost of Debt(1) (%) Credit Ratings: 10 8 6 4 2 0 8.4 7.9 7.1 6.7 5.6 5.5 5.3 CLD CNX ACI WLT BTU JRCC ANR |

| 1. Safety Is Our First Priority 26% Improvement in Reportable Injury Rate 2. Assemble and Leverage Best-in-Class Management 5 Additions to the Executive Leadership Team 3. Increase Profitable, High Quality Met Coal Production 35% Increase in Met Coal Production ~2 MMt Curtailment from Lower Margin Mines 4. Reduce Costs and Manage Capital Spending Carefully 21% Reduction in Met Cash Cost of Production (Q4 Y-o-Y) 19% Decrease in SG&A 5. Strengthen Balance Sheet and Increase Financial Flexibility $722MM in Repayments of Near-Term Debt Maturities $415MM Increase in Available Liquidity 26 Walter Has Made Significant Progress on Its Strategy |

| 27 “Walter remains the ‘go-to’ met story in the U.S. in an improving met coal environment” – BMO, February 20, 2013 “WLT remains our top pick in the coal space. We see a potential entry point ahead of a near-term pick up in met coal prices and improved execution in 2013. In addition, we view this week’s earnings announcement as the last near-term overhang” – Morgan Stanley, February 19, 2013 Walter Is Well Positioned to Capitalize on the Market Rebound and Continue to Create Long-Term Shareholder Value “WLT is our preferred vehicle for exposure to improving met coal markets. Based on stabilizing global steel production and more balanced supply, we project a rebound in coking coal in 2013. As a pure play with a high-quality product, we view WLT as the preferred vehicle to gain exposure to this rebound. The company maintains a strong liquidity position of $445MM, and improved profitability from rising prices in tandem with focused unit cost reductions should help it deleverage and improve its capital composition” – Dahlman Rose, February 22, 2013 The Research Community Sees Significant Upside in Our Business Strategy “Walter Energy offers investors pure North American metallurgical coal exposure and the highest leverage to metallurgical coal prices in our coverage universe” – RBC, March 6, 2013 “WLT deserves to trade closer to its historical average multiple because of some operational/financial/strategic progress made with the recent closure of its more marginal mines thermal and international met coal mines and increased liquidity following last week's debt issuance” – Goldman Sachs, March 31, 2013 |

| Independent and Highly Qualified Board 28 Of Walter’s Board Members: 4 have been added in the last 2 years 5 have financial, operational, or director level experience at other mining companies 7 have CEO or CFO-level experience at companies other than Walter 9 are independent, the other is the CEO |

| Walter Has an Outstanding Board with a Fresh Perspective 40% of the Board Renewed in Last 2 Years 29 Member Profile Former senior general partner of KKR Chairman and Managing Principal at MVC Capital Outstanding Directors Exchange’s Outstanding Director of the Year in 2007 Director of CNO Financial Group, IDEX Corporation, Mueller Water Products and MVC Capital Former CFO, general partner and Vice Chairman of Deloitte & Touche Director of Mueller Water Products Certified Public Accountant EVP, CFO and a principal owner of Sachs Electric Company Served for 15 years in various executive capacities for Arch Coal, including as CFO Certified Public Accountant Former Chairman of and CEO of AirTran Director of Air Canada and Mueller Water Products Former Interim CEO of Walter Jerry Kolb Environmental Comm.3 (C) Audit Committee (M) Patrick Kriegshauser Audit Committee (C) Compensation Comm.1 (M) Joseph Leonard Audit Committee (M) Executive Comm. (M) Michael Tokarz Compensation Comm.1 (M) Executive Comm. (M) Nominating Comm.2 (M) Member Profile Chairman of the Board, Emeritus and former Chairman and CEO of Flowserve Corporation Former senior executive at Phelps Dodge Director of Dover Corporation and Mueller Water Products. Former director of Belden, Inc. Outstanding Directors Exchange’s Outstanding Director of the Year in 2008 Bernard Rethore Nominating Comm.2 (C) Executive Comm. (M) Former President of Ford Motor Credit North America and Vice President of Ford Motor Company President and CEO of AJ Wagner & Associates, a multi-industry business consulting organization A.J. Wagner Compensation Comm.1 (C) Environmental Comm. (M) Appointed the Company's Chief Executive Officer in September 2011 Joined Walter Energy from Peabody Energy, where he served as Senior Vice President-Strategic Operations Walter Scheller CEO Executive Comm. (M) New Additions in Last 2 Years 30 years of management experience in a variety of international and domestic roles at Bestfoods and its predecessors Director of CNO Financial Group. Former director of AXA, Del Monte, Pactiv and Royal Dutch Shell Mary “Nina” Henderson Former CEO of two coal companies. Former executive at Billiton, Deutsche Morgan Grenfell and Barclays Bank Director of Ncondezi Coal Company and Gemfields PLC Graham Mascall Environmental Comm.3 (M) Conway Director for the Clarkson Centre for Business Ethics and Board Effectiveness at the University of Toronto’s Rotman School of Management Director of FirstService Corp. Former Managing Director of the Canadian Coalition for Good Governance, and also a former board member of Bank of Montreal. Former Chairman of Inmet Mining David Beatty Compensation Comm.1 (M) Nominating Comm.2 (M) Notes: (M) = Member, (C) = Chairman Compensation and Human Resource Committee Nominating and Corporate Governance Committee Environmental, Health and Safety Committee |

| Audley’s Nominees Lack the Qualifications and Experience to be Suitable Director Candidates 30 The Nominating and Corporate Governance Committee of the Board: Evaluates the composition of the Board continually and has an established process for reviewing potential director candidates Nominated Nina Henderson as a director in February 2013 following such a review Reviewed Audley’s nominees in detail and concluded that, individually and collectively, the nominees do not possess the experience or expertise to qualify as director candidates for Walter’s Board(1) Note: Please refer to Walter Energy’s letter to shareholders dated 25-Mar-2013. http://www.sec.gov/ Archives/edgar/ data/837173/ 000104746913003273 /a2213995zdefa14a.htm Audley’s Nominees Do Not Have the Experience, Expertise or Professional Credibility to Qualify as a Director Candidate for Walter’s Board |

| 31 Walter’s Pre-Existing 1. Strategic Initiatives Safety Is Our First Priority 2. Assemble and Leverage Best-in-Class Management 3. Reduce Costs and Manage Capital Spending Carefully 4. Strengthen Balance Sheet and Increase Financial Flexibility 5. Increase Profitable, High Quality Met Coal Production Audley’s Initial “Proposals” Audley’s Initial “Proposals” Restate Walter’s Pre-Existing Strategic Initiatives... “Stabilize senior management” “Undertake an in-depth review of SG&A and cost control” “Seek to reduce debt” “Improve operational performance and costs of the business” |

| 32 “allowing for the business to ultimately pay dividends” Audley’s Subsequent Proposals Highlight Lack of Understanding of Walter’s Business “Walter Energy could evaluate the tax savings associated with reorganizing the energy assets, in particular profitable thermal coal and natural gas assets, by placing them into a Master Limited Partnership structure” “We understand that there are substantial additional reserves and resources of met coal at both the U.S. and Canadian operations that are not reflected in the current reserve and resource statements” Walter pays a dividend, and has done so for 13 years Walter’s thermal coal and natural gas assets have not been sufficiently cash flow positive in recent times to support the distribution requirements of a public MLP An updated and comprehensive reserve statement is included in Walter’s 2012 10-K that reflects the increases in its reserves US SEC regulation only allows for disclosure of proven and probable mineral reserves. While the Company controls non-reserve mineral deposits, quantifying these amounts conflicts with SEC guidance “Audley Capital is baffled that the Company consistently provides incorrect quarterly earnings guidance to analysts” Walter does not provide quarterly earnings guidance Audley Says But the Reality Is “We believe thermal coal mines as well as UK anthracite mines, should be sold or spun off to enhance value for Company stockholders” These assets have not had sufficient cash flow in recent times to operate as standalone entities .................. |

| 33 “Audley would propose raising off balance sheet financing immediately in order to reduce debt to more acceptable levels... [including] less dilutive methods of raising equity capital, such as a convertible bond issuance” ...And Others Would Be Value Destructive for Shareholders “Solicit a Joint Venture Partner for Blue Creek this new development would benefit from sharing the capex burden with a strong joint venture partner” “We believe that a review of coal marketing arrangements should be undertaken to improve market share, pricing and volumes, and reduce sales and marketing costs” “We believe thermal... coal mines... as well as UK anthracite mines, should be sold or spun off to enhance value for Company stockholders” Off-balance sheet financings reduce the quality of the accounting information and reduce accounting transparency Because the Company has adequate liquidity, issuing any equity or hybrid security would unnecessarily dilute shareholders Walter will maintain a disciplined approach to capital spending. Blue Creek’s current capital needs are modest; the Company would consider partnerships as necessary so as not to erode shareholder value Walter sells its production in the most efficient manner (directly to customers) and achieves benchmark pricing for the majority of its products . A review of our marketing strategy is therefore unwarranted and would only result in incremental costs. Third party commentary supports our position: Walter has already publicly announced that it is open to divesting non-core assets on terms that would enhance shareholder value. It is difficult to achieve fair value for these assets at the trough of the cycle Audley Says ...But the Reality Is “Evaluating the merits of accelerating the development of the Wolverine properties to increase hard coking coal production to 3mpta + with a joint venture partner” Walter has grown production by 35% year-over-year and has the current capacity to further grow production should market conditions warrant, without having to share the upside with a third party “But the marketing issue, particularly, struck me as one in which a broader point should be made – the strongest U.S. metallurgical coals are best placed to the closest customer base. Walter’s marketing group is envied of much of the industry and knows extremely well where its high-quality coal will earn the best return” – Coal & Energy, Market Commentary by Jim Thompson, 26-Mar-2013 |

| 34 “... We have serious doubts about what Audley Capital will be able to accomplish given the complex geology of WLT's assets, the macro forces that drive the company's earnings, and the current status/mindset of most of the logical buyers (the global diversified miners)” – BB&T, February 21, 2013 “ ... we perceive shortcomings in Audley’s proposal (the fund’s likely minor position in the company, tarnished relationship with Walter Energy, lack of communication with Walter prior to its notice of intent, and insider trading accusations towards one of the proposed board members)...” – Brean Capital, LLC, February 20, 2013 “Audley’s move probably highlights investor frustration with the stock’s fall from the $141.17 high to a $28.46 low prior to recovering to yesterday’s $39.96 close. However, it’s worth noting that the stock has held up reasonably well compared with the other coal equities. WLT actually outperformed the coal index until mid 2012” – JPMorgan, February 20, 2013 Analysts Also Question Audley’s Proposals and Ability to Create Shareholder Value “Most of Walter’s underperformance since 2011 is attributable to factors that a replacement board would not have changed, i.e. a steep decline in metallurgical coal prices, in our view” – Stifel Nicolaus, February 20, 2013 “... we fear that the effort to replace board members revives the 2011 dispute that led to the surprising early exit of former Walter CEO (and Western Coal CEO) Keith Calder. In our view, neither side in a reopening of the dispute would be likely to emerge spotless, considering the severe downturn in world metallurgical coal markets since 2011 and its impact on growth plans and operating results” – Stifel Nicolaus, February 20, 2013 |

| Walter’s Board Is the Best Team for Continued Success 35 Our Board: Steered the Company’s evolution from a diversified conglomerate to the pure-play metallurgical coal producer it is today Pursued strategic initiatives to deliver exceptional shareholder results over the long-term, across multiple cycles Took decisive actions to position the Company for success in response to recent macro challenges and cyclical macro downturn Focused on good corporate governance and added 4 highly qualified directors in the last 2 years Consists of independent directors with a breadth and diversity of expertise committed to creating long-term value for shareholders Audley: Seeking effective control of the Board with minimal ownership, unqualified nominees and a flawed plan looking to change the Company's direction Vote FOR the Walter Nominees on the WHITE form of proxy |

| -Appendix- |

| Walter Energy, Inc. and Subsidiaries Reconciliation of Non-GAAP Financial Measures Unaudited Reconciliation of EBITDA and Adjusted EBITDA to Amounts Reported Under U.S. GAAP: For the Three Months Ended December 31, For the Years Ended December 31, ($ in Thousands) 2012 2011(1) 2012 2011(1) Income (Loss) from Continuing Operations ($) (70,971) 80,252 (1,065,555) 363,598 Add: Interest Expense 49,640 33,575 139,356 96,820 Less: Interest Income (73) (250) (804) (606) Add: Income Tax Expense (Benefit) (71,232) 23,843 (99,204) 131,225 Add: Depreciation and Depletion Expense 92,720 72,709 316,232 230,681 Earnings from Continuing Operations Before Interest, Income Taxes, and Depreciation and Depletion (EBITDA from Continuing Operations) (2) 84 210,129 (709,975) 821,718 Add: Pre-Tax Income from Discontinued Operations – – 8,282 – Earnings Before Interest, Income Taxes, and Depreciation and Depletion (EBITDA) (3) (4,916) 210,129 (701,693) 821,718 Add: Goodwill Impairment (2,345) – 1,064,409 – Add: Asset Impairment and Restructuring Charges 9,109 – 49,070 – Adjusted EBITDA (4) ($) 6,848 210,129 411,786 821,718 Reconciliation of Adjusted Net Income to Amounts Reported Under U.S. GAAP: Net Income (Loss) ($) (70,971) 80,252 (1,060,375) 363,598 Less: Income from Discontinued Operations, Net of Tax ($3.1 Million) – – (5,180) – Add: Asset Impairment and Other Restructuring Charges, Net of Tax ($15 Million for the Year Ended December 31, 2012) 6,877 – 31,868 – Add: Goodwill Impairment (2,345) – 1,064,409 – Adjusted Net Income (Loss) (5) ($) (66,439) 80,252 30,722 363,598 Note: 1) Includes the results of Western Coal since the April 1, 2011 date of acquisition. Certain previously reported three months and year ended December 31, 2011 balances have been recast to reflect the effects of finalizing the allocation of the Western Coal purchase price during the 2012 first quarter. (2) EBITDA from continuing operations is defined as earnings excluding discontinued operations before interest expense, interest income, income taxes, and depreciation and depletion expense. (3) EBITDA is defined as earnings before interest expense, interest income, income taxes, and depreciation and depletion expense. EBITDA is a financial measure which is not calculated in conformity with U.S. Generally Accepted Accounting Principles (GAAP) and should be considered supplemental to, and not as a substitute or superior to financial measures calculated in conformity with GAAP. We believe that EBITDA is a useful measure as some investors and analysts use EBITDA to compare us against other companies and to help analyze our ability to satisfy principal and interest obligations and capital expenditure needs. EBITDA may not be comparable to similarly titled measures used by other entities. (4) Adjusted EBITDA is defined as EBITDA further adjusted to exclude goodwill impairment and asset impairment and restructuring charges. Adjusted EBITDA is not a measure of financial performance in accordance with generally accepted accounting principles, and items excluded from Adjusted EBITDA are significant in understanding and assessing our financial condition. Therefore, Adjusted EBITDA should not be considered in isolation, nor as an alternative to net income, income from operations, cash flows from operations or as a measure of our profitability, liquidity or performance under generally accepted accounting principles. We believe that Adjusted EBITDA presents a useful measure of our ability to incur and service debt based on ongoing operations. Furthermore, analogous measures are used by industry analysts to evaluate our operating performance. Investors should be aware that our presentation of Adjusted EBITDA may not be comparable to similarly titled measures used by other companies. (5) Adjusted net income (loss) is defined as net income (loss) excluding income from discontinued operations, net of tax, goodwill impairment and asset impairment and restructuring charges, net of tax. Adjusted net income (loss) is not a measure of financial performance in accordance with generally accepted accounting principles, and items excluded from Adjusted net income (loss) are significant in understanding and assessing our financial condition. Therefore, Adjusted net income (loss) should not be considered in isolation, nor as an alternative to net income (loss) under generally accepted accounting principles. 37 |