UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934

Filed by the registranto

Filed by a party other than the registrantx

Check the appropriate box:

| o | Preliminary Proxy Statement |

| o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| o | Definitive Proxy Statement |

| o | Definitive Additional Materials |

| x | Soliciting Material Under §240.14a-12 |

| Walter Energy, Inc. | |

| (Name of Registrant as Specified in Its Charter) | |

| Audley European Opportunities Fund Ltd. | |

| (Name of Person(s) Filing Proxy Statement if Other Than the Registrant) | |

| Payment of Filing Fee (Check the appropriate box): | |

| x No fee required. |

| o Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) Title of each class of securities to which transaction applies: |

| (2) Aggregate number of securities to which transaction applies: |

| (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) Proposed maximum aggregate value of transaction: |

| (5) Total fee paid: |

| o Fee paid previously with preliminary materials. |

| o Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. |

| (1) Amount Previously Paid: |

| (2) Form, Schedule or Registration Statement No.: |

| (3) Filing Party: |

| (4) Date Filed: |

On March 26, 2013, Audley Capital Advisors LLP delivered the attached stockholder presentation to Institutional Shareholder Services.

Further information regarding the Audley Group’s director nominees and other persons who may be deemed participants, and other matters, are set forth in a definitive proxy statement filed with the SEC on March 25, 2013. SHAREHOLDERS OF THE COMPANY ARE STRONGLY ADVISED TO READ THAT PROXY STATEMENT, BECAUSE IT INCLUDES IMPORTANT INFORMATION. THE PROXY STATEMENT IS EXPECTED TO BE SENT TO SHAREHOLDERS BY OR ON BEHALF OF PARTICIPANTS, AND IS ALSO AVAILABLE AT NO CHARGE ON THE SEC’S WEBSITE AT http://www.sec.gov and at http://www.myproxyonline.com/WalterEnergy.

Working to Create Lasting Value at Walter Energy March 2013 CONFIDENTIAL

Table of Contents • Executive Summary • Change at the Board Level is Urgently Needed • Market Outlook and Opportunity • Path to Strategic, Financial and Operational Turnaround • Director Nominees • About Audley Capital • How to Vote for Needed Change 2 CONFIDENTIAL Note: financial data included in presentation pre - dates Walter Energy’s issuance of $450 million of senior notes on March 22, 2013

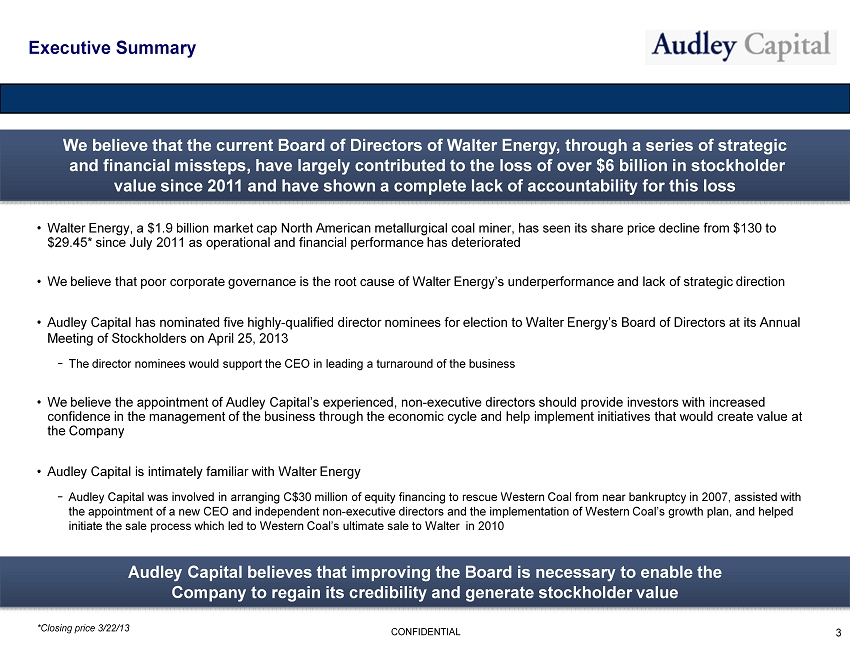

Executive Summary • Walter Energy, a $1.9 billion market cap North American metallurgical coal miner, has seen its share price decline from $130 to $29.45* since July 2011 as operational and financial performance has deteriorated • We believe that poor corporate governance is the root cause of Walter Energy’s underperformance and lack of strategic directi on • Audley Capital has nominated five highly - qualified director nominees for election to Walter Energy’s Board of Directors at its A nnual Meeting of Stockholders on April 25, 2013 − The director nominees would support the CEO in leading a turnaround of the business • We believe the appointment of Audley Capital’s experienced, non - executive directors should provide investors with increased confidence in the management of the business through the economic cycle and help implement initiatives that would create value at the Company • Audley Capital is intimately familiar with Walter Energy − Audley Capital was involved in arranging C$30 million of equity financing to rescue Western Coal from near bankruptcy in 2007 , a ssisted with the appointment of a new CEO and independent non - executive directors and the implementation of Western Coal’s growth plan, and h elped initiate the sale process which led to Western Coal’s ultimate sale to Walter in 2010 3 CONFIDENTIAL We believe that the current Board of Directors of Walter Energy, through a series of strategic and financial missteps, have largely contributed to the loss of over $6 billion in stockholder value since 2011 and have shown a complete lack of accountability for this loss Audley Capital believes that improving the Board is necessary to enable the Company to regain its credibility and generate stockholder value *Closing price 3/22/13

Change at the Board Level is Urgently Needed CONFIDENTIAL

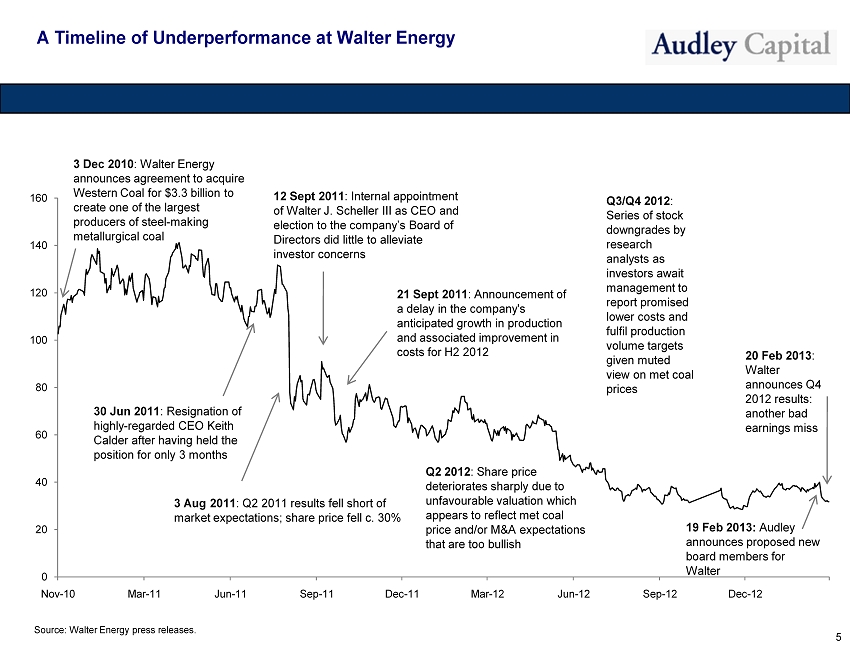

5 Source : Walter Energy press releases . 0 20 40 60 80 100 120 140 160 Nov - 10 Mar - 11 Jun - 11 Sep - 11 Dec - 11 Mar - 12 Jun - 12 Sep - 12 Dec - 12 20 Feb 2013 : Walter announces Q4 2012 results: another bad earnings miss 19 Feb 2013: Audley announces proposed new board members for Walter 30 Jun 2011 : Resignation of highly - regarded CEO Keith Calder after having held the position for only 3 months 3 Aug 2011 : Q2 2011 results fell short of market expectations; share price fell c. 30% 21 Sept 2011 : Announcement of a delay in the company's anticipated growth in production and associated improvement in costs for H2 2012 12 Sept 2011 : Internal appointment of Walter J. Scheller III as CEO and election to the company’s Board of Directors did little to alleviate investor concerns Q3/Q4 2012 : Series of stock downgrades by research analysts as investors await management to report promised lower costs and fulfil production volume targets given muted view on met coal prices 3 Dec 2010 : Walter Energy announces agreement to acquire Western Coal for $3.3 billion to create one of the largest producers of steel - making metallurgical coal Q2 2012 : Share price deteriorates sharply due to unfavourable valuation which appears to reflect met coal price and/or M&A expectations that are too bullish A Timeline of Underperformance at Walter Energy

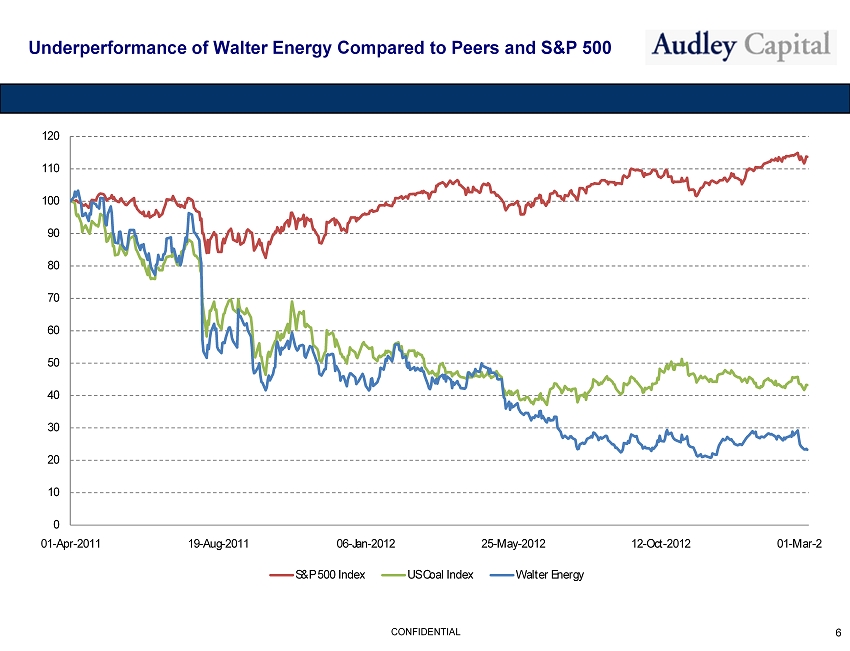

Underperformance of Walter Energy Compared to Peers and S&P 500 6 CONFIDENTIAL 0 10 20 30 40 50 60 70 80 90 100 110 120 01 - Apr - 2011 19 - Aug - 2011 06 - Jan - 2012 25 - May - 2012 12 - Oct - 2012 01 - Mar - 2013 S&P 500 Index US Coal Index Walter Energy

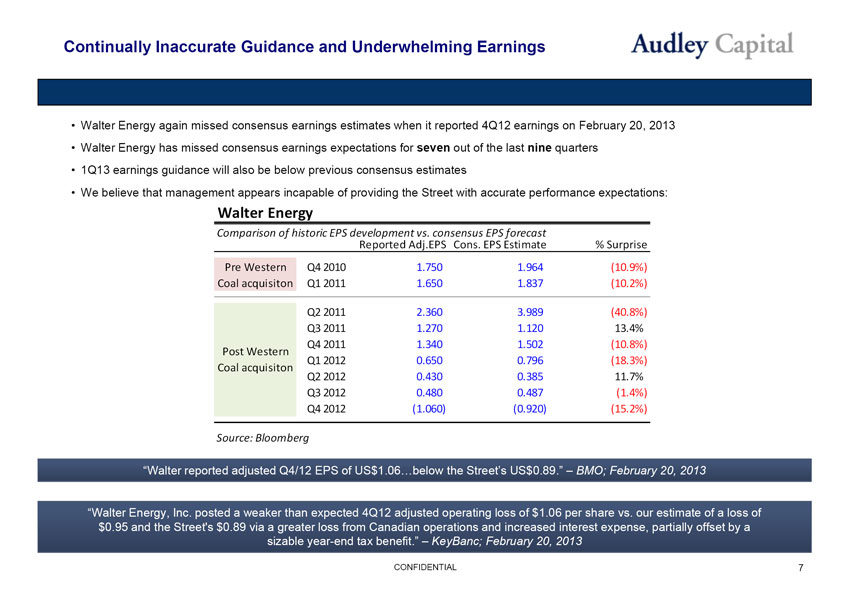

Continually Inaccurate Guidance and Underwhelming Earnings • Walter Energy again missed consensus earnings estimates when it reported 4Q12 earnings on February 20, 2013 • Walter Energy has missed consensus earnings expectations for seven out of the last nine quarters • 1Q13 earnings guidance will also be below previous consensus estimates • We believe that management appears incapable of providing the Street with accurate performance expectations: 7 CONFIDENTIAL “Walter reported adjusted Q4/12 EPS of US$1.06…below the Street’s US$0.89.” – BMO; February 20, 2013 “Walter Energy, Inc. posted a weaker than expected 4Q12 adjusted operating loss of $1.06 per share vs. our estimate of a loss of $ 0.95 and the Street's $0.89 via a greater loss from Canadian operations and increased interest expense, partially offset by a sizable year - end tax benefit.” – KeyBanc ; February 20, 2013 Walter Energy Comparison of historic EPS development vs. consensus EPS forecast Reported Adj.EPSCons. EPS Estimate % Surprise Q4 2010 1.750 1.964 (10.9%) Q1 2011 1.650 1.837 (10.2%) Q2 2011 2.360 3.989 (40.8%) Q3 2011 1.270 1.120 13.4% Q4 2011 1.340 1.502 (10.8%) Q1 2012 0.650 0.796 (18.3%) Q2 2012 0.430 0.385 11.7% Q3 2012 0.480 0.487 (1.4%) Q4 2012 (1.060) (0.920) (15.2%) Source: Bloomberg Pre Western Coal acquisiton Post Western Coal acquisiton Walter Energy Comparison of historic EPS development vs. consensus EPS forecast

Underlying Valuation of Walter Energy Needs to Improve • Walter Energy’s Price/net present value ratio has fallen from a peak of over 1.6x during the first quarter of 2011 to the cur ren t 0.6x, vs. the 3 - year average of 0.97x • While this may be endemic in the industry over the last 12 months, Audley Capital maintains that this could have been allevia ted in Walter’s case and is largely due to governance issues, Walter’s increased financial leverage and disappointment with Canadian operations • We believe that Walter Energy should trade at a much smaller discount to its net present value valuation due to: − It being the only NYSE - listed pure play met coal miner of substantial size − A high proportion of sales of high margin metallurgical coal with scope for significant price recovery vs. the structurally c hal lenged US thermal coal market with limited or no price recovery potential − The potential for superior production growth over the next three years − It being a potential bid candidate for a strategic mining counterpart looking to increase metallurgical coal exposure 8 CONFIDENTIAL Addressing board level issues should provide stockholders with increased confidence in the management of Walter Energy going forward

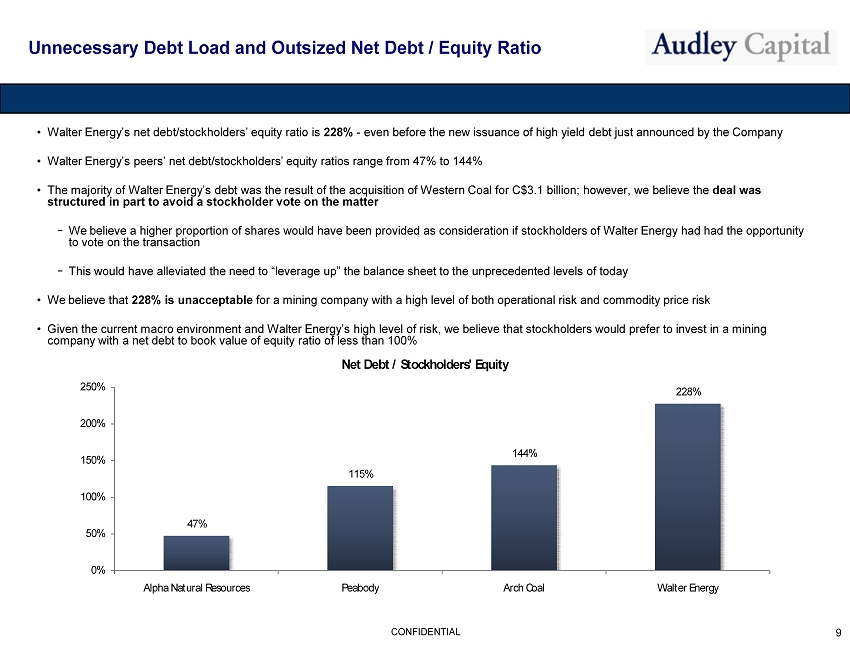

Unnecessary Debt Load and Outsized Net Debt / Equity Ratio • Walter Energy’s net debt/stockholders’ equity ratio is 228% - even before the new issuance of high yield debt just announced by the Company • Walter Energy’s peers’ net debt/stockholders’ equity ratios range from 47% to 144% • The majority of Walter Energy’s debt was the result of the acquisition of Western Coal for C$3.1 billion; however, we believe th e deal was structured in part to avoid a stockholder vote on the matter − We believe a higher proportion of shares would have been provided as consideration if stockholders of Walter Energy had had t he opportunity to vote on the transaction − This would have alleviated the need to “leverage up” the balance sheet to the unprecedented levels of today • We believe that 228% is unacceptable for a mining company with a high level of both operational risk and commodity price risk • Given the current macro environment and Walter Energy’s high level of risk, we believe that stockholders would prefer to inve st in a mining company with a net debt to book value of equity ratio of less than 100% 9 CONFIDENTIAL 47% 115% 144% 228% 0% 50% 100% 150% 200% 250% Alpha Natural Resources Peabody Arch Coal Walter Energy Net Debt / Stockholders' Equity

High CEO Turnover and a Stagnant Clique of Directors • There have been four CEOs over the past five years: − September 2009: Victor P. Patrick appointed CEO − March 2010: Joseph Leonard appointed “interim” CEO; stays on for a full year − April 2011: Keith Calder appointed CEO − September 2011: Walter J. Scheller , III appointed CEO • Of the 5 directors on the Board that we recommend replacing: − 0 have relevant mining experience − 4 have interlocking directorships with Mueller Water Products, Inc , highlighting the lack of diversity of independent views − The average tenure on Walter’s Board is 10 years − The Chairman has been a director of the Company for 26 years 10 CONFIDENTIAL “We agree with Audley that the high turnover at Walter’s CEO position over the past five years has been unsettling.” – Stifel Nicolaus; February 20, 2013 “Further executive turnover or difficulty appointing a permanent CEO could be a risk for WLT’s shares .” – Citigroup; January 22, 2013

Stockholder Input Has Been Ignored • In July 2011, when Walter Energy shares traded well above $100, Audley Capital sent a letter to the Board urging the Board to initiate a managed sale process to best address the Company’s range of issues and achieve fair value for stockholders • At the time, Audley Capital believed Walter Energy’s fair value could be in excess of $150 per share, implying a market valuation of approximately $9.0 billion • Despite our request, the Board elected not to pursue this course of action, but more importantly, provided no explanation for it s rationale and showed little interest in engaging in productive communication • The market value today is about $1.9 billion with shares trading at $29.45* • Audley Capital has also engaged with the Company on several other smaller strategic initiatives, such as spinning off the UK coa l operations, and again, constructive dialogue with the Board or management was not forthcoming • Criticism from some stockholders echoes Audley Capital’s experience regarding interaction and dealings with the Board: painting the Board as non - responsive to stockholder requests in comparison to other similarly sized mining companies 11 CONFIDENTIAL *Closing price 3/22/13

Opportunity and Market Outlook CONFIDENTIAL

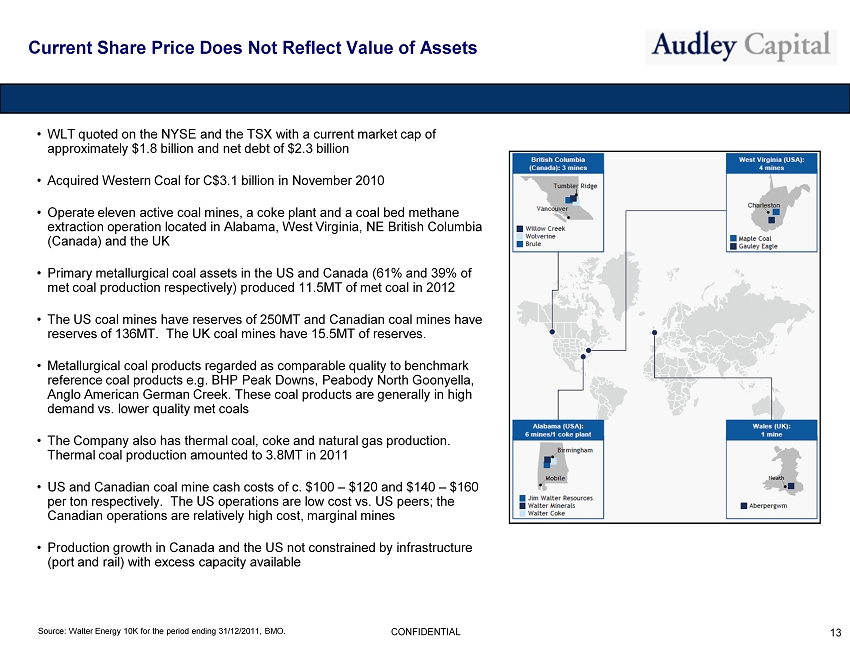

Current Share Price Does Not Reflect Value of Assets • WLT quoted on the NYSE and the TSX with a current market cap of approximately $1.8 billion and net debt of $2.3 billion • Acquired Western Coal for C$3.1 billion in November 2010 • Operate eleven active coal mines, a coke plant and a coal bed methane extraction operation located in Alabama, West Virginia, NE British Columbia (Canada) and the UK • Primary metallurgical coal assets in the US and Canada ( 61% and 39% of met coal production respectively) produced 11.5MT of met coal in 2012 • The US coal mines have reserves of 250MT and Canadian coal mines have reserves of 136MT. The UK coal mines have 15.5MT of reserves. • Metallurgical coal products regarded as comparable quality to benchmark reference coal products e.g. BHP Peak Downs, Peabody North Goonyella , Anglo American German Creek. These coal products are generally in high demand vs. lower quality met coals • The Company also has thermal coal, coke and natural gas production. Thermal coal production amounted to 3.8MT in 2011 • US and Canadian coal mine cash costs of c. $100 – $120 and $ 140 – $ 160 per ton respectively. The US operations are low cost vs. US peers; the Canadian operations are relatively high cost, marginal mines • Production growth in Canada and the US not constrained by infrastructure (port and rail ) with excess capacity available 13 CONFIDENTIAL Source : Walter Energy 10 K for the period ending 31 / 12 / 2011 , BMO .

Current Share Price Does Not Reflect Metallurgical Coal Market Recovery • Current share price implies no recovery in the met coal price over the next 4+ years from the current 1Q 2013 contract settle men t price of $165. Audley Capital believes this market view to be incorrect: − The metallurgical coal market has shown signs of improvement in the past few months . Spot pricing for benchmark metallurgical coal increased 23% since August 2012 due to a combination of global metallurgical coal production cuts (25 – 30Mt) and strengthening Chinese demand. 2Q 2013 contract prices are expected to settle around $172/t, up from recent spot price lows of $140/t but still significantly below ~$250/t from a year ago, and the $300/t peak price in 2H 2011 − Most markets in Asia (China, Japan, USA, South Korea) remain below long run trend growth rates . 2013 YTD macro data from China (the largest consumer of coking coal) has been mixed. The data remains supportive of the trend of a weak recovery since 4Q 2012 − Chinese steel mills remain slow to cut production capacity, providing continued demand for met coal − Longer - term metallurgical coal import growth during the current decade is expected to outstrip that of the last five years, prim arily driven by accelerating demand for hard coking coal and low volatile PCI coal in major growth markets of India and China, and to a lesser extent Brazil, Germany and a recovering Japanese market − China announced over Rmb15.0tn ($2.3 trillion) of national and regional stimulus projects in 2012 vs. Rmb22tn ($3.4 trillion ) i n 2008. Although many of these projects are spread over 3 - 6 years and many regional projects won’t be approved, Audley Capital anticipates steel demand for the national projects and approved regional projects to appear in the coming quarters, prompting steel mills to purchase more met coal 14 CONFIDENTIAL

Trading at a Significant Discount to Net Present Value Based on Coal Price Recovery Forecasts • We believe that there is a significant discount to fair value in Walter Energy’s stock and the current Board seems to struggl e t o deliver on a plan to fix this • Audley Capital’s proposal to improve the governance of Walter Energy and put in place actionable initiatives, with the support and guidance of skilled directors, can let this company once again take advantage of an uplift in coal pricing • Under the leadership of the current Board, we believe the Company has been left with very little room to maneuver without ris kin g operational concerns, impacting stockholders or risk defaulting on debt or seeking expensive refinancings • We see a base case and bull case for hard coking coal pricing in the next few years and it is imperative that the Company, wi th the insight of new, skilled directors, make more thoughtful decisions going forward to create much higher value for stockholders in the future 15 CONFIDENTIAL • Hard coking coal pricing outlook − Base case: $175/t (2013), $200/t (2014 - 2015), $175/t LT − Bull case: $189/t (2013), $205/t (2014), $217/t (2015), $220/t (LT) Note : Bull Case based on MinAxis Pty Ltd coal price forecasts (4Q 2012 )

Now is Not the Time for a Sale of Walter Energy! • Audley Capital believes there is substantial value in Walter Energy that is not reflected by the current share price • Audley Capital believes a sale should be reviewed as part of a series of strategic options when appropriate • NOW IS NOT THE TIME TO SELL WALTER ENERGY: − The balance sheet is weak − The Board is not up to the task − Met coal prices are low • We believe M&A interest will recover once the met coal market shows signs of definitive recovery; during the managed sale proces s of Western Coal in 2010, substantial interest was received from a number of parties, including steel companies and large cap min ing companies • However , Audley Capital is concerned the current Board will NEVER consider the sale of Walter Energy 16 CONFIDENTIAL

Path to Strategic, Financial and Operational Turnaround CONFIDENTIAL

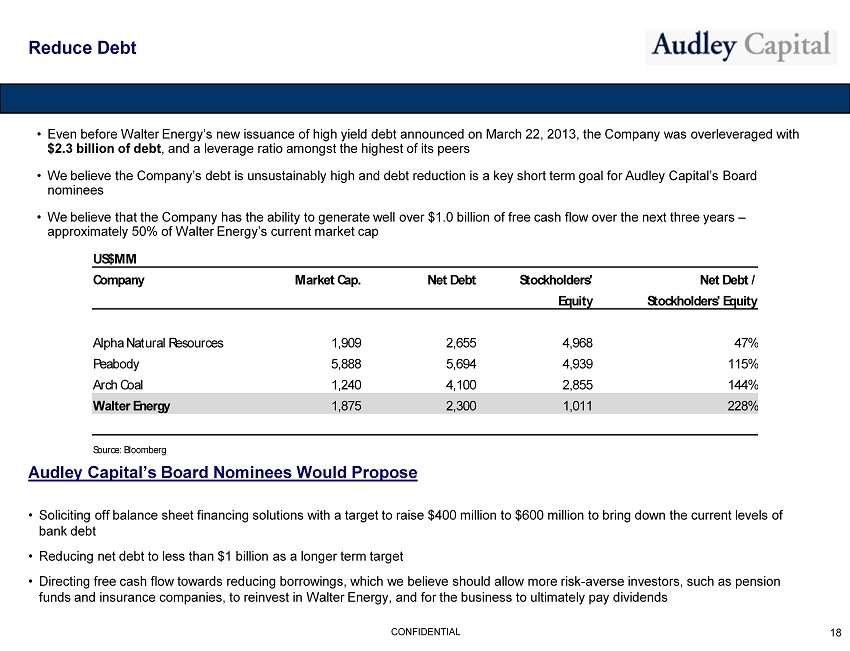

Reduce Debt • Even before Walter Energy’s new issuance of high yield debt announced on March 22, 2013, the Company was overleveraged with $2.3 billion of debt , and a leverage ratio amongst the highest of its peers • We believe the Company’s debt is unsustainably high and debt reduction is a key short term goal for Audley Capital’s Board nominees • We believe that the Company has the ability to generate well over $1.0 billion of free cash flow over the next three years – approximately 50% of Walter Energy’s current market cap 18 CONFIDENTIAL Audley Capital’s Board Nominees Would Propose • Soliciting off balance sheet financing solutions with a target to raise $400 million to $600 million to bring down the curren t l evels of bank debt • Reducing net debt to less than $ 1 billion as a longer term target • Directing free cash flow towards reducing borrowings, which we believe should allow more risk - averse investors, such as pension funds and insurance companies, to reinvest in Walter Energy, and for the business to ultimately pay dividends US$MM Company Market Cap. Net Debt Stockholders' Net Debt / Equity Stockholders' Equity Alpha Natural Resources 1,909 2,655 4,968 47% Peabody 5,888 5,694 4,939 115% Arch Coal 1,240 4,100 2,855 144% Walter Energy 1,875 2,300 1,011 228% Source: Bloomberg

Reduce Cost of Debt • We believe that the high yield debt fundraising of $500 million with a 9.875% coupon in November 2012 was ill - timed, very poorly priced, and provided a rich bonus to debt investors at the expense of Walter Energy’s stockholders • The bonds have traded up to a price of $110 vs. the $99.30 issue price • If this deal was undertaken around the time of the Western Coal acquisition and priced differently, we believe a significantl y l ower interest rate would have been achieved with a better overall debt maturity profile • Furthermore, i n our view, the Company’s recently announced issuance of $450 million of senior notes due 2021 with a coupon of 8.500% per annum reflects another case of questionable financial judgment by the Board – the Company is again: − Locking in expensive long - term debt; − Reducing free cash flow to equity holders; and − Allowing the balance sheet to continue to deteriorate as the cost of annual interest payments continue to rise 19 CONFIDENTIAL “We agree with Audley that Walter entered the current downturn with excessive debt levels following the 2011 acquisition of Western Coal. In retrospect, Walter would have been better served by using equity rather than debt to fund the majority of the transaction, which was the approach taken by top met coal competitor Alpha Natural Resources in its acquisition of Massey Energy in 2011.” – Stifel Nicolaus; 20 February 2013 Audley Capital’s Board Nominees Would Propose • Reviewing all outstanding debt facilities • Refinancing existing term loans at the appropriate time to reduce the overall interest cost burden and increase financial fle xib ility • Considering refinancing with debt financing provided by leading Asian banks where Walter Energy has an established customer base: this source of funding should be significantly cheaper than that provided by traditional U.S. lending banks

Evaluate Alternative Financing Solutions • Walter Energy’s latest quarterly results showed interest expense increasing from $30.5 million in third quarter 2012 to $49.6 mi llion in fourth quarter 2012, a 63% increase • When Walter Energy renegotiated debt covenants in the fourth quarter 2012 and issued the expensive $500 million 9.875% high y iel d bond, it unnecessarily incurred major increases in the overall cost of debt • In our view, the recently announced issuance of $450 million of high yield debt only exacerbates the Company’s financial position • It is unknown whether the Board has even considered or solicited alternative financing offers • We believe alternative financing solutions exist that can improve the Company’s overall cash position and help reduce corporate debt 20 CONFIDENTIAL Audley Capital’s Board Nominees Would Propose • Raising off balance sheet financing immediately in order to reduce total debt to more acceptable levels, reducing the risk of breaching banking covenants on the existing bank debt • Potential solutions include: • Offtake financing with coal traders • Collateralized lending based solutions • Sale and leaseback of coal reserves • Less dilutive methods of raising equity capital, such as a convertible bond issuance

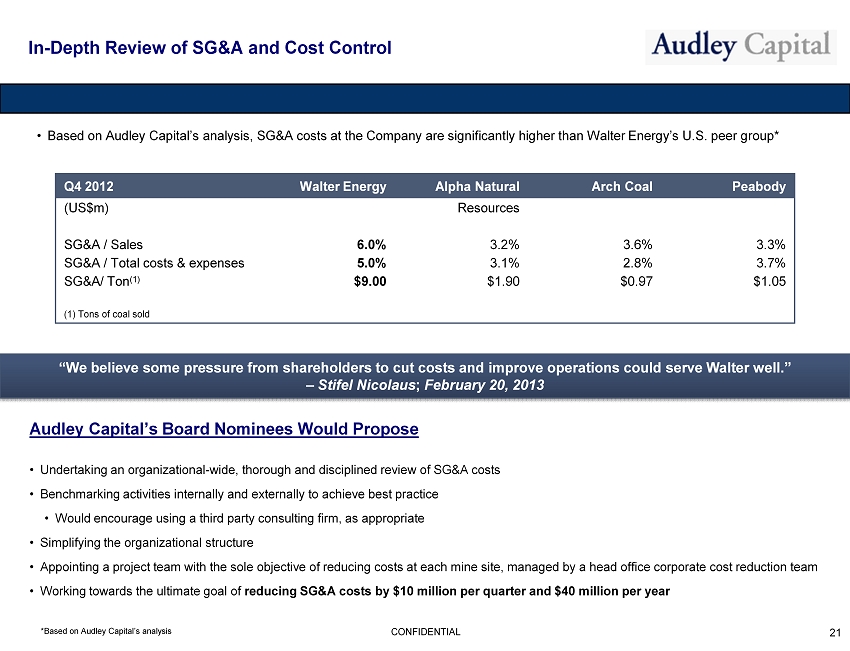

In - Depth Review of SG&A and Cost Control • Based on Audley Capital’s analysis, SG&A costs at the Company are significantly higher than Walter Energy’s U.S. peer group* 21 CONFIDENTIAL Q4 2012 Walter Energy Alpha Natural Arch Coal Peabody ( US$m ) Resources SG&A / Sales 6.0% 3.2% 3.6% 3.3% SG&A / Total costs & expenses 5.0% 3.1% 2.8% 3.7% SG&A/ Ton (1) $9.00 $1.90 $0.97 $1.05 (1) Tons of coal sold Audley Capital’s Board Nominees Would Propose • Undertaking an organizational - wide, thorough and disciplined review of SG&A costs • Benchmarking activities internally and externally to achieve best practice • Would encourage using a third party consulting firm, as appropriate • Simplifying the organizational structure • Appointing a project team with the sole objective of reducing costs at each mine site , managed by a head office corporate cost reduction team • W orking towards the ultimate goal of reducing SG&A costs by $10 million per quarter and $40 million per year *Based on Audley Capital’s analysis “We believe some pressure from shareholders to cut costs and improve operations could serve Walter well.” – Stifel Nicolaus ; February 20, 2013

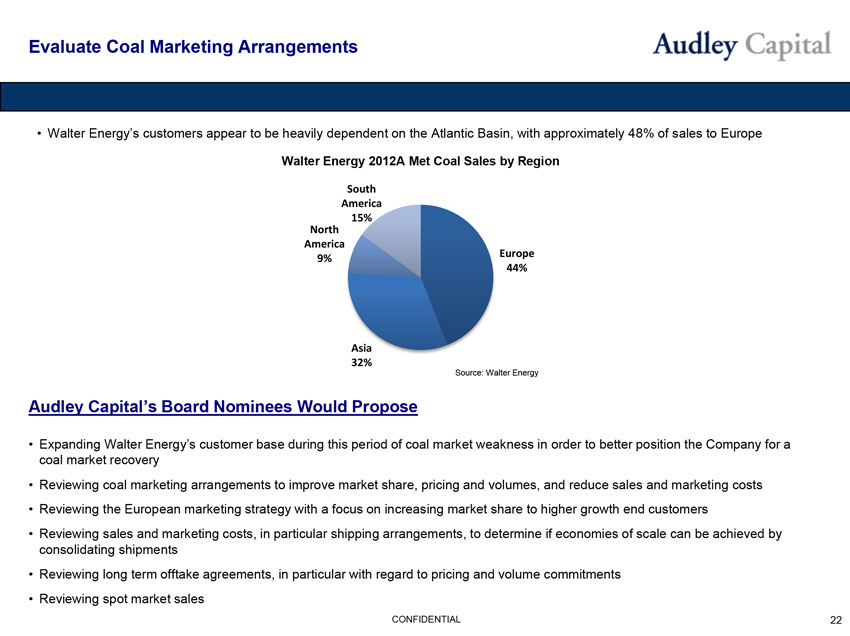

Evaluate Coal Marketing Arrangements • Walter Energy’s customers appear to be heavily dependent on the Atlantic Basin, with approximately 48% of sales to Europe Walter Energy 2012A Met Coal Sales by Region South America 15% North America 9% Europe 44% Asia 32% Source: Walter Energy Audley Capital’s Board Nominees Would Propose • Expanding Walter Energy’s customer base during this period of coal market weakness in order to better position the Company for a coal market recovery • Reviewing coal marketing arrangements to improve market share, pricing and volumes, and reduce sales and marketing costs • Reviewing the European marketing strategy with a focus on increasing market share to higher growth end customers • Reviewing sales and marketing costs, in particular shipping arrangements, to determine if economies of scale can be achieved by consolidating shipments • Reviewing long term offtake agreements, in particular with regard to pricing and volume commitments • Reviewing spot market sales CONFIDENTIAL 22

Improve Canadian Operations • Given the limited reserve life and high cash cost nature of the Canadian operations, loss making mines should be placed on ca re and maintenance to conserve reserves for better coal markets • Given the limited reserves at Willow Creek, we recommend and agree that the mine should be put on care and maintenance to conserve reserves for stronger coal markets • Brule has a limited reserve life (approx. 10 years) based on 2mtpa of production, but is a lower cost operation than Willow C ree k with a cash cost of $130 per ton, and is currently running at reduced 1mtpa production run rate • Wolverine produces between 1.8mtpa and 1.9mtpa of hard coking coal at a cash cost of US$120 per ton. This mine is currently profitable 23 CONFIDENTIAL Audley Capital’s Board Nominees Would Propose • Restarting Willow Creek when hard coking coal prices recover to over $ 200 per ton • Reviewing all Canadian operations with a view of further reducing costs to ensure they generate an appropriate rate of return fo r stockholders • Evaluating the merits of accelerating the development of the Wolverine properties to increase hard coking coal production to 3mt pa + with a joint venture partner

Solicit a Joint Venture Partner for Blue Creek • With appropriate funding , we understand the Blue Creek property could add between 2mtpa and 3mtpa of hard coking coal production • Analysts estimate the net present value of this project to be in the region of more than $500 million based on a $200/t coal price • We understand capex of approximately $ 1 billion would be required to bring the Blue Creek property into production • Given Walter Energy’s indebtedness, it seems clear that the Company will be unable to do this on its own 24 CONFIDENTIAL Audley Capital’s Board Nominees Would Propose • Soliciting a strong joint venture partner who will share the development cost burden • Audley Capital is aware of several strategic partners that could be interested in such an opportunity: - Commodity trading houses - S teel mills - M ajor mining companies • We believe that this would accelerate the met coal production growth profile of Walter Energy and increase the attractiveness of the Company to new investors seeking a production growth play story in met coal

Reorganize Assets to Realize Significant Tax Savings • Walter Energy has substantial energy assets, the value of which, we believe, is not recognized by the market • We believe the Company’s natural gas assets, assuming they generate EBITDA of $20 million, could potentially be worth more than $100 million • We maintain that Walter Energy’s lowest cost thermal coal mines may have the potential to generate profits on a thermal coal mar ket recovery • We believe profits from these non - core assets can be used to enhance stockholder dividends in coming years 25 CONFIDENTIAL Audley Capital’s Board Nominees Would Propose • Reorganizing the energy assets, particularly profitable thermal coal and natural gas assets, by placing them into a Master Li mit ed Partnership (MLP) structure: - MLP structure should provide significant tax savings - Investors should be better able to appropriately value these assets through improved financial disclosure - MLPs in the energy space with limited volatility trade at very high multiples of distributable cash flow because of investors’ des ire for yield and stability

Divest Underperforming and Non - Core Assets • We believe that underperforming assets with limited scope for earnings growth, as well non - core assets, should be divested or sp un - off in order to enhance value for Company stockholders • We believe that the result will be a company more focused on the seaborne metallurgical coal market 26 CONFIDENTIAL Audley Capital’s Board Nominees Would Propose • Selling or spinning out idled or marginal mines to mining juniors looking for production ready assets including: - Idled thermal coal mines in West Virginia - Metallurgical coal mines in West Virginia - I dled anthracite coal mines in Wales, United Kingdom

Review All Reserves and Resources, and Upgrade Reserves • We believe there are substantial additional reserves and resources of met coal at both the U.S. and Canadian operations that are not reflected in the current reserve and resource statements • Several mines have reserves of less than 20 years – including Mine No.7 and Wolverine properties • The reserves were determined several years ago in a much lower coal price environment • Additionally, we believe that the Board has failed to focus on replacing mined reserves • As a result, the market appears to be of the opinion that the Company’s resources and reserves are relatively limited 27 CONFIDENTIAL Audley Capital’s Board Nominees Would Propose • Undertaking a review of all coal reserves and resources, with limited exploration drilling where required, to ensure stockholders and potential investors are fully aware of the longevity of the coal mines • We believe that this analysis should only be undertaken once Walter Energy’s cash position has improved

Improve Stockholder Communication to Rebuild Investor Confidence • We believe Walter Energy’s Board and management have failed to clearly articulate a strategic plan for the Company’s turnaround • We believe that the Board and management have demonstrated little interest in engaging in productive communication with stockholders • We believe that the Board and management appear unable to provide accurate quarterly earnings forecasts to the Street • It is our view that financial disclosures continue to be very poor 28 CONFIDENTIAL Audley Capital’s Board Nominees Would Propose • Communicating a clear vision and strategy for the next 3 to 5 years • Initiating a proactive and enhanced investor relations program • Increasing communication between C - level executives and stockholders • Undertaking an immediate review of internal budgeting procedures, financial disclosures and investor relations activities in order to provide the market with more accurate earnings guidance going forward

Board Nominees CONFIDENTIAL

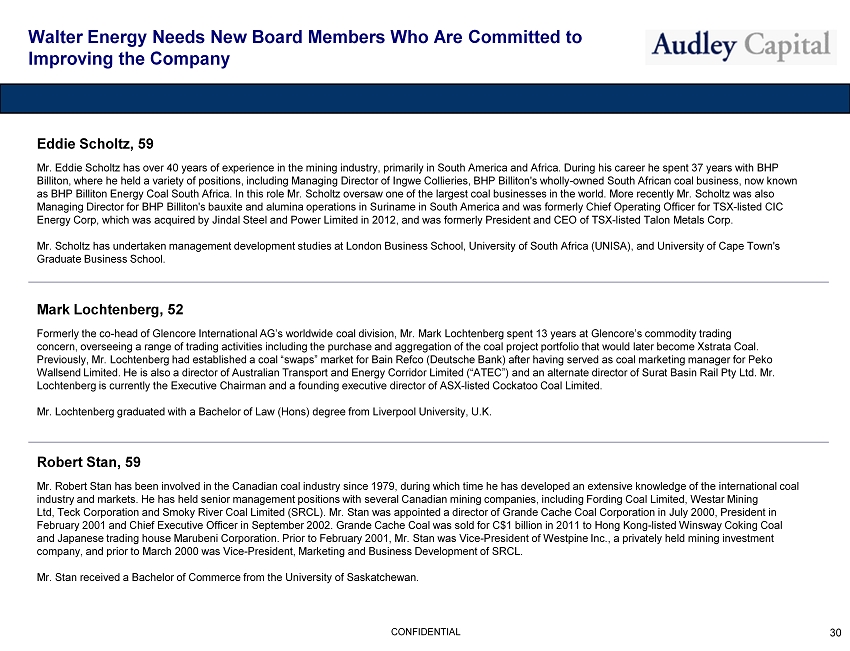

Walter Energy Needs New Board Members Who Are Committed to Improving the Company 30 CONFIDENTIAL Eddie Scholtz , 59 Mr. Eddie Scholtz has over 40 years of experience in the mining industry, primarily in South America and Africa. During his career he spent 37 ye ars with BHP Billiton, where he held a variety of positions, including Managing Director of Ingwe Collieries, BHP Billiton's wholly - owned South African coal business, now known as BHP Billiton Energy Coal South Africa. In this role Mr. Scholtz oversaw one of the largest coal businesses in the world. More recently Mr. Scholtz was also Managing Director for BHP Billiton's bauxite and alumina operations in Suriname in South America and was formerly Chief Operating Officer for TSX - listed CIC Energy Corp, which was acquired by Jindal Steel and Power Limited in 2012, and was formerly President and CEO of TSX - listed Talon Metals Corp. Mr. Scholtz has undertaken management development studies at London Business School, University of South Africa ( UNISA ), and University of Cape Town's Graduate Business School. Mark Lochtenberg , 52 Formerly the co - head of Glencore International AG’s worldwide coal division, Mr. Mark Lochtenberg spent 13 years at Glencore’s commodity trading concern, overseeing a range of trading activities including the purchase and aggregation of the coal project portfolio that w oul d later become Xstrata Coal. Previously, Mr. Lochtenberg had established a coal “swaps” market for Bain Refco (Deutsche Bank) after having served as coal marketing manager for Peko Wallsend Limited. He is also a director of Australian Transport and Energy Corridor Limited (“ ATEC ”) and an alternate director of Surat Basin Rail Pty Ltd. Mr. Lochtenberg is currently the Executive Chairman and a founding executive director of ASX - listed Cockatoo Coal Limited. Mr. Lochtenberg graduated with a Bachelor of Law ( Hons ) degree from Liverpool University, U.K . Robert Stan, 59 Mr. Robert Stan has been involved in the Canadian coal industry since 1979, during which time he has developed an extensive k now ledge of the international coal industry and markets. He has held senior management positions with several Canadian mining companies, including Fording Coal Lim ited, Westar Mining Ltd, Teck Corporation and Smoky River Coal Limited ( SRCL ). Mr. Stan was appointed a director of Grande Cache Coal Corporation in July 2000, President in February 2001 and Chief Executive Officer in September 2002. Grande Cache Coal was sold for C$1 billion in 2011 to Hong Kong - lis ted Winsway Coking Coal and Japanese trading house Marubeni Corporation. Prior to February 2001, Mr. Stan was Vice - President of Westpine Inc., a privately held mining investment company, and prior to March 2000 was Vice - President, Marketing and Business Development of SRCL . Mr. Stan received a Bachelor of Commerce from the University of Saskatchewan.

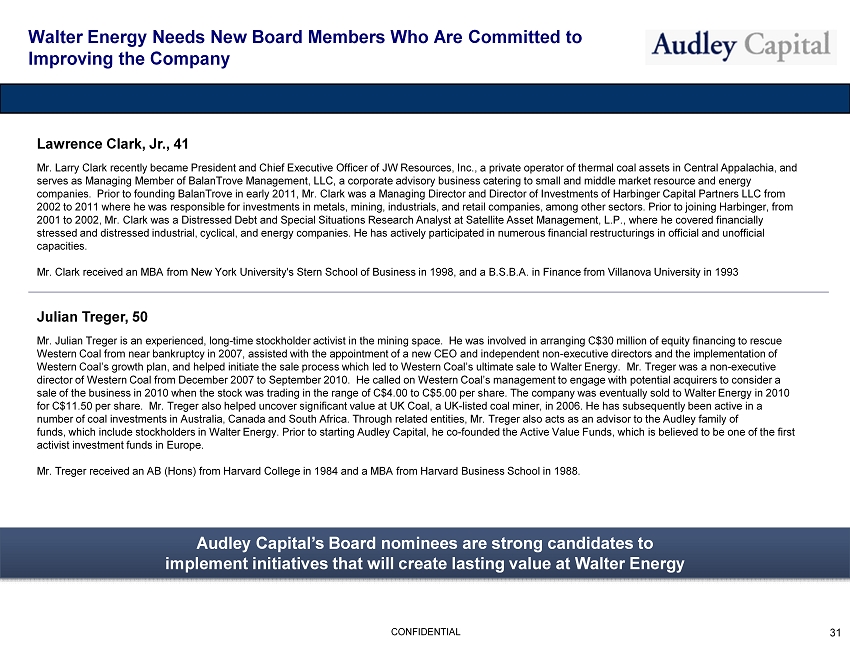

Walter Energy Needs New Board Members Who Are Committed to Improving the Company 31 CONFIDENTIAL Lawrence Clark, Jr., 41 Mr. Larry Clark recently became President and Chief Executive Officer of JW Resources, Inc., a private operator of thermal coal assets in Central Appalachia, and serves as Managing Member of BalanTrove Management, LLC, a corporate advisory business catering to small and middle market resource and energy companies. Prior to founding BalanTrove in early 2011, Mr. Clark was a Managing Director and Director of Investments of Harbinger Capital Partners LLC from 2002 to 2011 where he was responsible for investments in metals, mining, industrials, and retail companies, among other secto rs. Prior to joining Harbinger, from 2001 to 2002, Mr. Clark was a Distressed Debt and Special Situations Research Analyst at Satellite Asset Management, L.P., wh ere he covered financially stressed and distressed industrial, cyclical, and energy companies. He has actively participated in numerous financial restru ctu rings in official and unofficial capacities. Mr. Clark received an MBA from New York University's Stern School of Business in 1998, and a B.S.B.A . in Finance from Villanova University in 1993 Julian Treger , 50 Mr. Julian Treger is an experienced, long - time stockholder activist in the mining space. He was involved in arranging C$30 million of equity fin ancing to rescue Western Coal from near bankruptcy in 2007, assisted with the appointment of a new CEO and independent non - executive directors an d the implementation of Western Coal’s growth plan, and helped initiate the sale process which led to Western Coal’s ultimate sale to Walter Energy. Mr . Treger was a non - executive director of Western Coal from December 2007 to September 2010. He called on Western Coal’s management to engage with potenti al acquirers to consider a sale of the business in 2010 when the stock was trading in the range of C$4.00 to C$5.00 per share. The company was eventuall y s old to Walter Energy in 2010 for C$11.50 per share. Mr. Treger also helped uncover significant value at UK Coal, a UK - listed coal miner, in 2006. He has subsequently been active in a number of coal investments in Australia, Canada and South Africa. Through related entities, Mr. Treger also acts as an advisor to the Audley family of funds, which include stockholders in Walter Energy. Prior to starting Audley Capital, he co - founded the Active Value Funds, which is believed to be one of the first activist investment funds in Europe. Mr. Treger received an AB ( Hons ) from Harvard College in 1984 and a MBA from Harvard Business School in 1988. Audley Capital’s Board nominees are strong candidates to implement initiatives that will create lasting value at Walter Energy

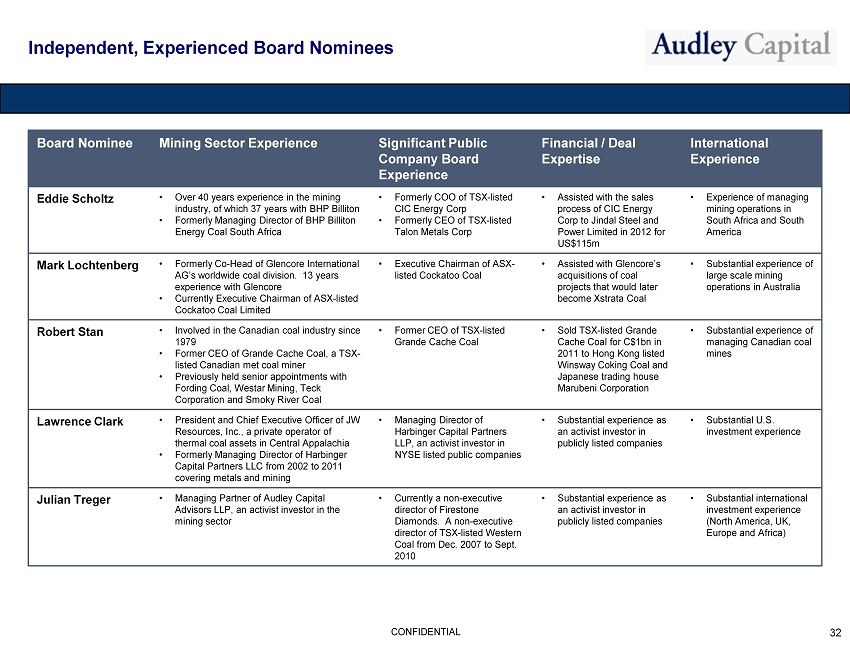

Independent, Experienced Board Nominees 32 CONFIDENTIAL Board Nominee Mining Sector Experience Significant Public Company Board Experience Financial / Deal Expertise International Experience Eddie Scholtz • Over 40 years experience in the mining industry, of which 37 years with BHP Billiton • Formerly Managing Director of BHP Billiton Energy Coal South Africa • Formerly COO of TSX - listed CIC Energy Corp • Formerly CEO of TSX - listed Talon Metals Corp • Assisted with the sales process of CIC Energy Corp to Jindal Steel and Power Limited in 2012 for US$115m • Experience of managing mining operations in South Africa and South America Mark Lochtenberg • Formerly Co - Head of Glencore International AG’s worldwide coal division. 13 years experience with Glencore • Currently Executive Chairman of ASX - listed Cockatoo Coal Limited • Executive Chairman of ASX - listed Cockatoo Coal • Assisted with Glencore’s acquisitions of coal projects that would later become Xstrata Coal • Substantial experience of large scale mining operations in Australia Robert Stan • Involved in the Canadian coal industry since 1979 • Former CEO of Grande Cache Coal, a TSX - listed Canadian met coal miner • Previously held senior appointments with Fording Coal, Westar Mining, Teck Corporation and Smoky River Coal • Former CEO of TSX - listed Grande Cache Coal • Sold TSX - listed Grande Cache Coal for C$1bn in 2011 to Hong Kong listed Winsway Coking Coal and Japanese trading house Marubeni Corporation • Substantial experience of managing Canadian coal mines Lawrence Clark • President and Chief Executive Officer of JW Resources, Inc., a private operator of thermal coal assets in Central Appalachia • Formerly Managing Director of Harbinger Capital Partners LLC from 2002 to 2011 covering metals and mining • Managing Director of Harbinger Capital Partners LLP, an activist investor in NYSE listed public companies • Substantial experience as an activist investor in publicly listed companies • Substantial U.S. investment experience Julian Treger • Managing Partner of Audley Capital Advisors LLP, an activist investor in the mining sector • Currently a non - executive director of Firestone Diamonds. A non - executive director of TSX - listed Western Coal from Dec. 2007 to Sept. 2010 • Substantial experience as an activist investor in publicly listed companies • Substantial international investment experience (North America, UK, Europe and Africa)

Audley Capital Background Information CONFIDENTIAL

Who is Audley Capital? • Audley Capital Advisors LLP provides investment advice and services in connection with investment strategies including hedge funds, private equity funds and co - investment vehicles • The firm advises with respect to a series of products including: The Audley European Opportunities Fund, an event driven/acti vis t hedge fund that focuses primarily on small and mid cap European equities; The Audley Natural Resources Fund, a global metals and mining hedge fund; and The Audley Japan Opportunities Fund, a multi strategy Japanese hedge fund that combines high convictio n Japanese macro investment ideas with a traditional long short large cap equity portfolio • The firm was founded in 2005 and is incorporated in England and Wales • Audley Capital’s intentions are CLEAR AND SIMPLE : e lect a slate of Director nominees that will pursue initiatives to create lasting value at the Company 34 CONFIDENTIAL AUDLEY CAPITAL IS LOOKING TO MAXIMIZE THE VALUE OF WALTER ENERGY FOR ALL STOCKHOLDERS

Audley Capital’s Familiarity with Walter Energy • Audley Capital has had a longstanding knowledge of Walter Energy by way of the Western Coal transaction: • Mr. Treger was a non - executive director of Western Coal from December 2007 to September 2010 • Audley was involved in arranging C$30 million of equity financing to rescue Western Coal from near bankruptcy in 2007 • Audley assisted with the appointment of a new CEO and independent non - executive directors and the implementation of Western Coal’s growth plan • Audley helped initiate the sale process which led to Western Coal’s ultimate sale to Walter Energy: Mr. Treger called on Western Coal’s management to engage with potential acquirers to consider a sale of the business in 2010 when the stock was trading in th e range of C$4.00 to C$5.00 per share • The company was eventually sold to Walter Energy in 2010 for C$11.50 per share • Recent correspondence includes in July 2011, when Walter Energy shares traded above $100 , Audley Capital sent a letter to the Board urging the Board to initiate a managed sale process to best address the Company’s range of issues and achieve fair value for stockholders 35 CONFIDENTIAL

Vote for Needed Change Today! CONFIDENTIAL

Vote the GOLD Proxy Card to Implement Important Change • Vote “For” Audley Capital’s slate of Five Highly - Qualified Director Nominees − They will b ring the needed experience and accountability to Walter Energy’s Board − Each nominee has extensive experience in the metallurgical coal industry on an international basis − All possess the skills required to manage multi - jurisdictional coal operations and their financing − The nominees will bring a fresh, dynamic and creative approach to the Walter Energy Board Vote the GOLD proxy card today . If you have any questions and/or need assistance in voting your shares, please call our proxy solicitor Okapi Partners LLC at (877) 208 - 8903. • Voting Instructions: − Vote by Telephone — Please call the telephone number specified on your GOLD proxy card from a touch - tone phone and follow the simple instructions. You will be required to provide the unique Control Number printed on your GOLD proxy card. − Vote by Internet — Please access the website specified on your GOLD proxy card and follow the simple instructions. You will be required to provide the unique Control Number printed on your GOLD proxy card. − Vote by Mail — If you do not wish to vote by telephone or over the Internet, please simply complete, sign, date and return the GOLD proxy ca rd in the postage - paid envelope provided. 37 CONFIDENTIAL Voting the GOLD proxy card will stop the current Board and management from continuing to lead Walter down a path that has cost stockholders dearly

Legal Disclaimer This presentation is for general informational purposes only and is not intended for distribution to or use by any person or ent ity in any jurisdiction where distribution or use would be contrary to local law or regulation. The views expressed herein represent the o pinions of Audley Capital, whose analysis is based on publicly available information. Certain financial information and data used herein have been derived or obtained from filings made with the Securities and Exchange Commission (“SEC”) or from other sources Audley Capital believes are reliable. Audley Capital shall not be responsible for any inaccurate information contained in any SEC filing or third party report. Furthermore, Audley Capital disclaims any obligations to update the information contained herein and reserves the right to modify or change its conclusions at any time in the future. Audley Capital has not sought or obtained consent from any third party to use the previously published information as proxy soliciti ng material. Any such statements or information should not be viewed as indicating the support of such third party for the views e xpressed herein. No representation or warranty is made that data or information, whether derived or obtained from filings made with the SEC or from any third party, are accurate. The presentation does not recommend the purchase or sale of any security. Furthermore, this presentation is not intended to be, nor should it be construed or used as, investment, tax or legal advice. No representation or warranty is made that Audley Capital’s proposed objectives will be achieved or successful. Any assumptions, assessments, estimates, projections or the like (collectively, “Statements”) regarding future events or whic h a re forward - looking in nature constitute only subjective views, outlooks or estimations, are based upon Audley Capital’s expectations or beliefs, are subject to change due to a variety of factors, including fluctuating market conditions and economic factors, and in volve inherent risks and uncertainties, many of which cannot be predicted or quantified and are beyond Audley Capital’s control. Actual results could differ materially from those set forth in, contemplated by or underlying these Statements. In light of these risk s and uncertainties, there can be no assurance and no representation is given that these Statements are now or will prove to be acc ura te or complete in any way . Further information regarding the director nominees and other persons who may be deemed participants, and other matters, are set forth in a definitive proxy statement filed with the SEC on March 25, 2013. SHAREHOLDERS OF THE COMPANY ARE STRONGLY ADVISED TO READ THAT PROXY STATEMENT, BECAUSE IT INCLUDES IMPORTANT INFORMATION. THE PROXY STATEMENT IS EXPECTED TO BE SENT TO SHAREHOLDERS BY OR ON BEHALF OF PARTICIPANTS, AND IS ALSO AVAILABLE AT NO CHARGE ON THE SEC’S WEBSITE AT http://www.sec.gov and at http://www.myproxyonline.com/WalterEnergy . 38 CONFIDENTIAL