As filed with the U.S. Securities and Exchange Commission on May 16, 2006.

Securities Act File No. 333-132344

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

| Pre-Effective Amendment No. 1 |

| Post-Effective Amendment No. |

(Check appropriate box or boxes)

MORGAN STANLEY STRATEGIST FUND

(Exact Name of Registrant as Specified in Charter)

1221 Avenue of the Americas

New York, New York 10020

(Address of Principal Executive Offices: (Number, Street, City, State, Zip Code))

(800) 869-6397

(Area Code and Telephone Number)

Amy R. Doberman, Esq.

Morgan Stanley Investment Management Inc.

1221 Avenue of the Americas

New York, New York 10020

(Name and Address of Agent for Service)

Copy to:

| Carl Frischling, Esq. Kramer Levin Naftalis & Frankel LLP 1177 Avenue of the Americas New York, New York 10036 | Stuart M. Strauss, Esq. Clifford Chance US LLP 31 West 52nd Street New York, New York 10019 | |||||

Approximate Date of Proposed Public Offering: As soon as practicable after the effective date of this Registration Statement.

No filing fee is required because an indefinite number of common shares of beneficial interest of Morgan Stanley Strategist Fund have previously been registered pursuant to Rule 24f-2 under the Investment Company Act of 1940.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

MORGAN STANLEY TOTAL RETURN TRUST

1221 Avenue of the Americas

New York, NY 10020

(800) 869-NEWS

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD JULY 17, 2006

To the Shareholders of Morgan Stanley Total Return Trust

Notice is hereby given of a Special Meeting of the Shareholders of Morgan Stanley Total Return Trust (‘‘Total Return’’) to be held in the Auditorium, 3rd Floor, 1221 Avenue of the Americas, New York, NY 10020, at 2:00 p.m., New York time, on July 17, 2006, and any adjournments thereof (the ‘‘Meeting’’), for the following purposes:

| 1. | To consider and vote upon an Agreement and Plan of Reorganization, dated February 6, 2006 (the ‘‘Reorganization Agreement’’), between Total Return and Morgan Stanley Strategist Fund (‘‘Strategist’’), pursuant to which substantially all of the assets of Total Return would be combined with those of Strategist and shareholders of Total Return would become shareholders of Strategist receiving shares of Strategist with a value equal to the value of their holdings in Total Return (the ‘‘Reorganization’’); and |

| 2. | To act upon such other matters as may properly come before the Meeting. |

The Reorganization is more fully described in the accompanying Proxy Statement and Prospectus and a copy of the Reorganization Agreement is attached as Exhibit A thereto. Shareholders of record at the close of business on April 7, 2006 are entitled to notice of, and to vote at, the Meeting. Please read the Proxy Statement and Prospectus carefully before telling us, through your proxy or in person, how you wish your shares to be voted. Alternatively, if you are eligible to vote telephonically by touchtone telephone or electronically on the Internet (as discussed in the enclosed Proxy Statement) you may do so in lieu of attending the Meeting in person. The Board of Trustees of Total Return recommends you vote in favor of the Reorganization. WE URGE YOU TO SIGN, DATE AND MAIL THE ENCLOSED PROXY PROMPTLY.

| By Order of the Board of Trustees, |

| MARY E. MULLIN, Secretary |

May 18, 2006

You can help avoid the necessity and expense of sending follow-up letters to ensure a quorum by promptly returning the enclosed Proxy. If you are unable to be present in person, please fill in, sign and return the enclosed Proxy in order that the necessary quorum be represented at the Meeting. The enclosed envelope requires no postage if mailed in the United States. Shareholders will be able to vote telephonically by touchtone telephone or electronically on the Internet by following instructions on their proxy cards or on the enclosed Voting Information Card.

MORGAN STANLEY STRATEGIST FUND

1221 Avenue of the Americas

New York, NY 10020

(800) 869-NEWS

Acquisition of the Assets of

Morgan Stanley Total Return Trust

By and in Exchange for Shares of

Morgan Stanley Strategist Fund

This Proxy Statement and Prospectus is being furnished to shareholders of Morgan Stanley Total Return Trust (‘‘Total Return’’) in connection with an Agreement and Plan of Reorganization, dated February 6, 2006 (the ‘‘Reorganization Agreement’’), pursuant to which substantially all the assets of Total Return will be combined with those of Morgan Stanley Strategist Fund (‘‘Strategist’’) in exchange for shares of Strategist (the ‘‘Reorganization’’). As a result of this transaction, shareholders of Total Return will become shareholders of Strategist and will receive shares of Strategist with a value equal to the value of their holdings in Total Return. The terms and conditions of this transaction are more fully described in this Proxy Statement and Prospectus and in the Reorganization Agreement between Total Return and Strategist attached hereto as Exhibit A. The address of Total Return is that of Strategist set forth above. This Proxy Statement also constitutes a Prospectus of Strategist, which is dated May 18, 2006, filed by Strategist with the Securities and Exchange Commission (the ‘‘Commission’’) as part of its Registration Statement on Form N-14 (the ‘‘Registration Statement’’).

Strategist is an open-end management investment company whose investment objective is to seek to maximize the total return on its investments. Strategist actively allocates its assets among the major asset categories of equity securities, fixed income securities and money market instruments, with no limit on the percentage of assets that may be allocated to any one asset class.

This Proxy Statement and Prospectus sets forth concisely information about Strategist that shareholders of Total Return should know before voting on the Reorganization Agreement. A copy of the Prospectus for Strategist dated November 30, 2005, as may be supplemented from time to time, is attached as Exhibit B and is incorporated herein by reference. Also enclosed and incorporated herein by reference are Strategist's Annual Report for the fiscal year ended July 31, 2005 and its succeeding Semi-Annual Report for the six-months ended January 31, 2006. A Statement of Additional Information relating to the Reorganization, described in this Proxy Statement and Prospectus, dated May 18, 2006, has been filed with the Commission and is also incorporated herein by reference. Also incorporated herein by reference are Total Return's Prospectus, dated November 30, 2005, as supplemented, its Annual Report for its fiscal year ended July 31, 2005 and its succeeding Semi-Annual report for the six-months ended January 31, 2006. Such documents, as well as additional information about Strategist, have been filed with the Commission and are available upon request without charge by calling (800) 869-NEWS (toll-free) or by visiting the Commission's website at www.sec.gov.

Investors are advised to read and retain this Proxy Statement and Prospectus for future reference.

These Securities have not been approved or disapproved by the Securities and Exchange Commission or any State Securities Commission, nor has the Securities and Exchange Commission or any State Securities Commission passed on the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

This Proxy Statement and Prospectus is dated May 18, 2006.

TABLE OF CONTENTS

PROXY STATEMENT AND PROSPECTUS

| Page | ||||||

| INTRODUCTION | 1 | |||||

| General | 1 | |||||

| Record Date; Share Information | 1 | |||||

| Proxies | 2 | |||||

| Expenses of Solicitation | 3 | |||||

| Vote Required | 4 | |||||

| SYNOPSIS | 4 | |||||

| The Reorganization | 4 | |||||

| Past Performance | 5 | |||||

| Example | 11 | |||||

| Tax Consequences of the Reorganization | 13 | |||||

| Comparison of Total Return and Strategist | 13 | |||||

| PRINCIPAL RISK FACTORS | 17 | |||||

| THE REORGANIZATION | 20 | |||||

| The Proposal | 20 | |||||

| The Board's Considerations | 20 | |||||

| The Reorganization Agreement | 21 | |||||

| Tax Aspects of the Reorganization | 23 | |||||

| Description of Shares | 24 | |||||

| Capitalization Table (unaudited) | 25 | |||||

| Appraisal Rights | 25 | |||||

| COMPARISON OF INVESTMENT OBJECTIVES, POLICIES AND RESTRICTIONS | 25 | |||||

| Investment Objectives and Policies | 25 | |||||

| Investment Restrictions | 27 | |||||

| ADDITIONAL INFORMATION ABOUT TOTAL RETURN AND STRATEGIST | 27 | |||||

| General | 27 | |||||

| Financial Information | 27 | |||||

| Management | 27 | |||||

| Description of Securities and Shareholder Inquiries | 27 | |||||

| Dividends, Distributions and Taxes | 27 | |||||

| Purchases, Repurchases and Redemptions | 28 | |||||

| FINANCIAL STATEMENTS AND EXPERTS | 28 | |||||

| LEGAL MATTERS | 28 | |||||

| AVAILABLE INFORMATION | 28 | |||||

| OTHER BUSINESS | 28 | |||||

| Exhibit A — Agreement and Plan of Reorganization | A-1 | |||||

| Exhibit B — Prospectus of Morgan Stanley Strategist dated November 30, 2005, as supplemented | B-1 | |||||

i

MORGAN STANLEY TOTAL RETURN TRUST

1221 Avenue of the Americas

New York, NY 10020

(800) 869-NEWS

PROXY STATEMENT AND PROSPECTUS

Special Meeting of Shareholders

to be Held July 17, 2006

INTRODUCTION

General

This Proxy Statement and Prospectus is being furnished to the shareholders of Morgan Stanley Total Return Trust (‘‘Total Return’’), an open-end, diversified management investment company, in connection with the solicitation by the Board of Trustees of Total Return (the ‘‘Board’’) of proxies to be used at the Special Meeting of Shareholders of Total Return to be held in the Auditorium, 3rd Floor, 1221 Avenue of the Americas, New York, NY 10020, at 2:00 p.m., New York time, on July 17, 2006, and any adjournments thereof (the ‘‘Meeting’’). It is expected that the first mailing of this Proxy Statement and Prospectus will be made on or about May 18, 2006.

At the Meeting, Total Return shareholders (‘‘Shareholders’’) will consider and vote upon an Agreement and Plan of Reorganization, dated February 6, 2006 (the ‘‘Reorganization Agreement’’), between Total Return and Morgan Stanley Strategist Fund (‘‘Strategist’’), pursuant to which substantially all of the assets of Total Return will be combined with those of Strategist in exchange for shares of Strategist. As a result of this transaction, Shareholders will become shareholders of Strategist and will receive shares of Strategist equal to the value of their holdings in Total Return on the date of such transaction (the ‘‘Reorganization’’). Pursuant to the Reorganization, each Shareholder will receive the class of shares of Strategist that corresponds to the class of shares of Total Return currently held by that Shareholder. Accordingly, as a result of the Reorganization, each Class A, Class B, Class C and Class D Shareholder of Total Return will receive Class A, Class B, Class C and Class D shares of Strategist, respectively. The shares to be issued by Strategist pursuant to the Reorganization (the ‘‘Strategist Shares’’) will be issued at net asset value without an initial sales charge. Further information relating to Strategist is set forth herein and in Strategist's current Prospectus, dated November 30, 2005 (‘‘Strategist's Prospectus’’), attached to this Proxy Statement and Prospectus as Exhibit B and incorporated herein by reference.

The information concerning Total Return and Strategist contained herein has been supplied by Total Return and Strategist, respectively. Each of Total Return and Strategist is referred to herein as a ‘‘Fund.’’

Record Date; Share Information

The Board has fixed the close of business on April 7, 2006 as the record date (the ‘‘Record Date’’) for the determination of the Shareholders entitled to notice of, and to vote at, the Meeting. As of the Record Date, there were 7,231,196 shares of Total Return issued and outstanding. Shareholders on the Record Date are entitled to one vote per share and a fractional vote for a fractional share on each matter

1

submitted to a vote at the Meeting. Shareholders of each class will vote together as a single class in connection with the Reorganization Agreement. A majority of the outstanding shares entitled to vote, represented in person or by proxy, will constitute a quorum at the Meeting.

The following persons were known to own of record or beneficially 5% or more of the outstanding shares of a class of each of the Funds as of the Record Date:

| Name and Address of Total Return Shareholders | Number of Shares | Percentage of Outstanding Shares | ||||||||

| Class A | ||||||||||

| WINMEX INVESTMENTS LIMITED LOT 220 CLEAR WATER BAY ROAD KOWLOON, HONG KONG | 165,995.931 | 6.34 | % | |||||||

| Class B | ||||||||||

| NONE | ||||||||||

| Class C | ||||||||||

| NONE | ||||||||||

| Class D | ||||||||||

| NONE | ||||||||||

| Name and Address of Strategist Shareholders | Number of Shares | Percentage of Outstanding Shares | ||||||||

| Class A | ||||||||||

| STATE STREET BANK AND TRUST CO. FBO ADP/MORGAN STANLEY ALLIANCE 105 ROSEMONT AVENUE WESTWOOD, MA 02090-2318 | 1,466,761.674 | 5.83 | % | |||||||

| Class B | ||||||||||

| NONE | ||||||||||

| Class C | ||||||||||

| NONE | ||||||||||

| Class D | ||||||||||

| MAC & CO A/C MSWF4000152 MUTUAL FUNDS OPERATIONS MORGAN STANLEY DPSP/START PLAN PO BOX 3198 PITTSBURGH, PA 15230-3198 | 1,588,008.755 | 54.21 | % | |||||||

| STATE STREET BANK AND TRUST CO. FBO ADP/MORGAN STANLEY ALLIANCE 105 ROSEMONT AVENUE WESTWOOD, MA 02090-2318 | 318,346.914 | 10.87 | % | |||||||

As of the Record Date, the trustees and officers of Total Return and Strategist, each as a group, owned less than 1% of the outstanding shares of Total Return and Strategist, respectively.

Proxies

The enclosed form of Proxy, if properly executed and returned, will be voted in accordance with the choice specified thereon. The Proxy will be voted in favor of the Reorganization Agreement unless a choice is indicated to vote against or to abstain from voting on the Reorganization Agreement. The Board

2

knows of no business, other than that set forth in the Notice of Special Meeting of Shareholders, to be presented for consideration at the Meeting. However, the Proxy confers discretionary authority upon the persons named therein to vote as they determine on other business, not currently contemplated, which may come before the Meeting. Abstentions and, if applicable, broker ‘‘non-votes’’ will not count as votes in favor of the Reorganization Agreement, and broker ‘‘non-votes’’ will not be deemed to be present at the meeting for purposes of determining whether the Reorganization Agreement has been approved. Broker ‘‘non-votes’’ are shares held in street name for which the broker indicates that instructions have not been received from the beneficial owners or other persons entitled to vote and for which the broker does not have discretionary voting authority. If a Shareholder executes and returns a Proxy but fails to indicate how the votes should be cast, the proxy will be voted in favor of the Reorganization Agreement. The Proxy may be revoked at any time prior to the voting thereof by: (i) delivering written notice of revocation to the Secretary of Total Return, 1221 Avenue of the Americas, New York, NY 10020; (ii) attending the Meeting and voting in person; or (iii) completing and returning a new Proxy (whether by mail or, as discussed below, by touchtone telephone or the Internet) (if returned and received in time to be voted). Attendance at the Meeting will not in and of itself revoke a Proxy.

In the event that the necessary quorum to transact business or the vote required to approve or reject the Reorganization Agreement is not obtained at the Meeting, the persons named as proxies may propose one or more adjournments of the Meeting to permit further solicitation of Proxies. Any such adjournment will require the affirmative vote of the holders of a majority of shares of Total Return present in person or by proxy at the Meeting. The persons named as proxies will vote in favor of such adjournment those proxies which they are entitled to vote in favor of the Reorganization Agreement and will vote against any such adjournment those proxies required to be voted against the Reorganization Agreement. Abstentions and, if applicable, broker ‘‘non-votes’’ will not be counted for purposes of approving an adjournment.

Expenses of Solicitation

All expenses of this solicitation, including the cost of preparing and mailing this Proxy Statement and Prospectus, will be borne by Total Return, which expenses are expected to approximate $194,641. Total Return and Strategist will bear all of their respective other expenses associated with the Reorganization.

The solicitation of Proxies will be by mail, which may be supplemented by solicitation by mail, telephone or otherwise through officers of Total Return or officers and regular employees of Morgan Stanley Investment Advisors Inc. (the ‘‘Investment Adviser’’), Morgan Stanley Trust (the ‘‘Transfer Agent’’), Morgan Stanley Services Company Inc. and/or Morgan Stanley DW Inc. (‘‘Morgan Stanley DW’’), without special compensation therefor. As described below, Total Return will employ Computershare Fund Services (‘‘Computershare’’) to make telephone calls to Shareholders to remind them to vote. In addition, Total Return may also employ Computershare as proxy solicitor if it appears that the required number of votes to achieve a quorum will not be received. In the event of a solicitation by Computershare, Total Return would pay the solicitor a project advisory fee not to exceed $3,000 and the expenses outlined below.

Shareholders will be able to vote their shares by touchtone telephone or by the Internet by following the instructions on the proxy card or on the Voting Information Card accompanying this Proxy Statement. To vote by Internet or by telephone, Shareholders can access the website or call the toll-free number listed on the proxy card or noted in the enclosed voting instructions.

In certain instances, the Transfer Agent or Computershare may call Shareholders to ask if they would be willing to have their votes recorded by telephone. The telephone voting procedure is designed to

3

authenticate Shareholders' identities, to allow Shareholders to authorize the voting of their shares in accordance with their instructions and to confirm that their instructions have been recorded properly. No recommendation will be made as to how a Shareholder should vote on any proposal other than to refer to the recommendations of the Board. Total Return has been advised by counsel that these procedures are consistent with the requirements of applicable law. Shareholders voting by telephone in this manner will be asked for identifying information and will be given an opportunity to authorize proxies to vote their shares in accordance with their instructions. To ensure that the Shareholders' instructions have been recorded correctly, Shareholders will receive a confirmation of their instructions in the mail. A special toll-free number set forth in the confirmation will be available in case the information contained in the confirmation is incorrect. Although a Shareholder's vote may be taken by telephone, each Shareholder will receive a copy of this Proxy Statement and may vote by mail using the enclosed proxy card or by touchtone telephone or the Internet as set forth above. The last proxy vote received in time to be voted, whether by proxy card, touchtone telephone or the Internet, will be the last vote that is counted and will revoke all previous votes by the Shareholder. With respect to recorded telephone calls by Computershare reminding Shareholders to vote, expenses would be approximately $1.00 per outbound telephone contact. With respect to the solicitation of a telephonic vote by Computershare, approximate additional expenses of $3.75 per telephone vote transacted and $2.75 per outbound or inbound telephone contact and costs relating to obtaining Shareholders' telephone numbers and providing additional materials upon Shareholder request, which would be borne by Total Return.

Vote Required

Approval of the Reorganization Agreement by the Shareholders requires the affirmative vote of a majority (i.e., more than 50%) of the shares of Total Return represented in person or by proxy and entitled to vote at the Meeting, provided a quorum is present at the Meeting. If the Reorganization Agreement is not approved by Shareholders, Total Return will continue in existence and the Board will consider alternative actions.

SYNOPSIS

The following is a synopsis of certain information contained in or incorporated by reference in this Proxy Statement and Prospectus. This synopsis is only a summary and is qualified in its entirety by the more detailed information contained or incorporated by reference in this Proxy Statement and Prospectus and the Reorganization Agreement. Shareholders should carefully review this Proxy Statement and Prospectus and the Reorganization Agreement in their entirety and, in particular, Strategist's Prospectus, which is attached to this Proxy Statement as Exhibit B and incorporated herein by reference.

The Reorganization

The Reorganization Agreement provides for the transfer of substantially all the assets of Total Return, subject to stated liabilities, to Strategist in exchange for the Strategist Shares. The aggregate net asset value of the Strategist Shares issued in the exchange will equal the aggregate value of the net assets of Total Return received by Strategist. On or after the closing date scheduled for the Reorganization (the ‘‘Closing Date’’), Total Return will distribute the Strategist Shares received by Total Return to Shareholders as of the Valuation Date (as defined below) in complete liquidation of Total Return, and Total Return will thereafter be dissolved and deregistered under the Investment Company Act of 1940, as amended (the ‘‘1940 Act’’). As a result of the Reorganization, each Shareholder will receive that number of full and fractional Strategist Shares equal in value to such Shareholder's pro rata interest in the net assets of Total Return transferred to Strategist. Pursuant to the Reorganization, each Shareholder will

4

receive the class of shares of Strategist that corresponds to the class of shares of Total Return currently held by that Shareholder. Accordingly, as a result of the Reorganization, each Class A, Class B, Class C and Class D Shareholder of Total Return will become a holder of Class A, Class B, Class C and Class D shares of Strategist, respectively. Shareholders holding their shares of Total Return in certificate form will be asked to surrender their certificates in connection with the Reorganization. Shareholders who do not surrender their certificates prior to the Closing Date will still receive their Strategist Shares; however, such Shareholders will not be able to redeem, transfer or exchange the Strategist Shares received until the old certificates have been surrendered. The Board has determined that the interests of Shareholders will not be diluted as a result of the Reorganization. The ‘‘Valuation Date’’ is the third business day following the receipt of the requisite approval by the Shareholders of the Reorganization Agreement or at such other time as Total Return and Strategist may agree, on which date the number of Strategist shares to be delivered to Total Return will be determined.

At least one but not more than 20 business days prior to the Valuation Date, Total Return will declare and pay a dividend or dividends which, together with all previous such dividends, will have the effect of distributing to Shareholders substantially all of Total Return's investment company taxable income for all periods since the inception of Total Return through and including the Valuation Date (computed without regard to any dividends paid deduction), and substantially all of Total Return's net capital gain, if any, realized in such periods (after reduction for any capital loss carryovers).

For the reasons set forth below under ‘‘The Reorganization — The Board's Considerations,’’ the Board, including the trustees who are not ‘‘interested persons’’ of Total Return (‘‘Independent Trustees’’), as that term is defined in the 1940 Act, has concluded that the Reorganization is in the best interests of Total Return and the Shareholders and recommends approval of the Reorganization Agreement.

Past Performance

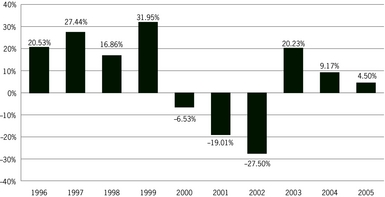

Total Return. The bar chart and table below provide some indication of the risks of investing in Total Return. Total Return's past performance (before and after taxes) does not indicate how Total Return will perform in the future. This chart shows how the performance of Total Return's Class B shares has varied from year to year over the past 10 calendar years.

5

Annual Total Returns — Calendar Years

The bar chart reflects the performance of Class B shares; the performance of the other Classes will differ because the Classes have different ongoing fees. The performance information in the bar chart does not reflect the deduction of sales charges; if these amounts were reflected, returns would be less than shown. The year-to-date total return as of March 31, 2006 was 5.89%.

During the periods shown in the bar chart, the highest return for a calendar quarter was 19.65% (quarter ended December 31, 1998) and the lowest return for a calendar quarter was –21.14% (quarter ended September 30, 2002).

6

This table compares Total Return's average annual total returns with those of an index that represents a broad measure of market performance, as well as an index that represents a group of similar mutual funds, over time. Total Return's returns include the maximum applicable sales charge for each Class and assume you sold your shares at the end of each period (unless otherwise noted).

Average Annual Total Returns (as of December 31, 2005)

| Past 1 Year | Past 5 Years | Past 10 Years | Life of Fund* | ||||||||||||||||||||||||||

| Class A1—Return Before Taxes | −0.26 | % | –4.54 | % | — | 2.28 | % | ||||||||||||||||||||||

| S&P 500® Index2 | 4.91 | % | 0.55 | % | — | 5.07 | % | ||||||||||||||||||||||

| Lipper Multi-Cap Core Funds Index3 | 8.22 | % | 2.21 | % | — | 5.75 | % | ||||||||||||||||||||||

| Class B1—Return Before Taxes | −0.50 | % | −4.62 | % | 5.95 | % | — | ||||||||||||||||||||||

| Return After Taxes on Distributions4 | −0.50 | % | –4.62 | % | 4.97 | % | — | ||||||||||||||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares | −0.33 | % | –3.87 | % | 4.66 | % | — | ||||||||||||||||||||||

| S&P 500® Index2 | 4.91 | % | 0.55 | % | 9.07 | % | — | ||||||||||||||||||||||

| Lipper Multi-Cap Core Funds Index3 | 8.22 | % | 2.21 | % | 8.92 | % | — | ||||||||||||||||||||||

| Class C1—Return Before Taxes | 3.50 | % | –4.24 | % | — | 2.19 | % | ||||||||||||||||||||||

| S&P 500® Index2 | 4.91 | % | 0.55 | % | — | 5.07 | % | ||||||||||||||||||||||

| Lipper Multi-Cap Core Funds Index3 | 8.22 | % | 2.21 | % | — | 5.75 | % | ||||||||||||||||||||||

| Class D1—Return Before Taxes | 5.48 | % | –3.28 | % | — | 3.17 | % | ||||||||||||||||||||||

| S&P 500® Index2 | 4.91 | % | 0.55 | % | — | 5.07 | % | ||||||||||||||||||||||

| Lipper Multi-Cap Core Funds Index3 | 8.22 | % | 2.21 | % | — | 5.75 | % | ||||||||||||||||||||||

| * | Only shown for share classes with less than a ten-year history. |

| (1) | Classes A, C and D commenced operations on July 28, 1997. Class B commenced operations on November 30, 1994. |

| (2) | The Standard & Poor's 500 Index (S&P 500®) is a broad-based index, the performance of which is based on the performance of 500 widely-held common stocks chosen for market size, liquidity and industry group representation. Indexes are unmanaged and their returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index. |

| (3) | The Lipper Multi-Cap Core Funds Index is an equally weighted performance index of the largest qualifying funds (based on net assets) in the Lipper Multi-Cap Core Funds classification. The Index, which is adjusted for capital gains distributions and income dividends, is unmanaged and should not be considered an investment. There are currently 30 funds represented in this Index. |

| (4) | These returns do not reflect any tax consequences from a sale of your shares at the end of each period, but they do reflect any applicable sales charges on such a sale. |

Included in the table above are the after-tax returns for Total Return's Class B shares. The after-tax returns for Total Return's other Classes will vary from the Class B shares' returns. After-tax returns are calculated using the historical highest individual federal marginal income tax rates during the period shown and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor's tax situation and may differ from those shown, and after-tax returns are not relevant to investors who hold their Total Return shares through tax-deferred arrangements, such as 401(k) plans or individual

7

retirement accounts. After-tax returns may be higher than before-tax returns due to foreign tax credits and/or an assumed benefit from capital losses that would have been realized had Total Return shares been sold at the end of the relevant periods, as applicable.

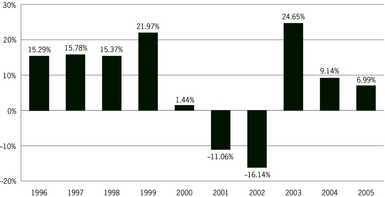

Strategist. The bar chart and table below provide some indication of the risks of investing in Strategist. Strategist's past performance (before and after taxes) does not indicate how Strategist will perform in the future. This chart shows how the performance of Strategist's Class B shares has varied from year to year over the past 10 calendar years.

Annual Total Returns — Calendar Years

The bar chart reflects the performance of Class B shares; the performance of the other Classes will differ because the Classes have different ongoing fees. The performance information in the bar chart does not reflect the deduction of sales charges; if these amounts were reflected, returns would be less than shown. The year-to-date total return as of March 31, 2006 was 4.78%.

During the periods shown in the bar chart, the highest return for a calendar quarter was 13.80% (quarter ended June 30, 2003) and the lowest return for a calendar quarter was –12.84% (quarter ended September 30, 2002).

8

This table compares Strategist's average annual total returns with those of indices that represent broad measures of market performance, as well as an index that represents a group of similar mutual funds, over time. Strategist's returns include the maximum applicable sales charge for each Class and assume you sold your shares at the end of each period (unless otherwise noted).

Average Annual Total Returns (as of December 31, 2005)

| Past 1 Year | Past 5 Years | Past 10 Years | Life of Fund* | ||||||||||||||||||||||||||

| Class A1—Return Before Taxes | 2.15 | % | 1.36 | % | — | 5.50 | % | ||||||||||||||||||||||

| S&P 500® Index2 | 4.91 | % | 0.55 | % | — | 5.07 | % | ||||||||||||||||||||||

| Lehman Brothers U.S. Government/Credit Index3 | 2.37 | % | 6.11 | % | — | 6.36 | % | ||||||||||||||||||||||

| Lipper Flexible Portfolio Funds Index4 | 6.34 | % | 2.54 | % | — | 4.87 | % | ||||||||||||||||||||||

| Class B1—Return Before Taxes | 1.99 | % | 1.28 | % | 7.54 | % | — | ||||||||||||||||||||||

| Return After Taxes on Distributions5 | 1.73 | % | 1.01 | % | 6.11 | % | — | ||||||||||||||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares | 1.29 | % | 0.93 | % | 5.89 | % | — | ||||||||||||||||||||||

| S&P 500® Index2 | 4.91 | % | 0.55 | % | 9.07 | % | — | ||||||||||||||||||||||

| Lehman Brothers U.S. Government/Credit Index3 | 2.37 | % | 6.11 | % | 6.17 | % | — | ||||||||||||||||||||||

| Lipper Flexible Portfolio Funds Index4 | 6.34 | % | 2.54 | % | 6.88 | % | — | ||||||||||||||||||||||

| Class C1—Return Before Taxes | 5.98 | % | 1.66 | % | — | 5.35 | % | ||||||||||||||||||||||

| S&P 500® Index2 | 4.91 | % | 0.55 | % | — | 5.07 | % | ||||||||||||||||||||||

| Lehman Brothers U.S. Government/Credit Index3 | 2.37 | % | 6.11 | % | — | 6.36 | % | ||||||||||||||||||||||

| Lipper Flexible Portfolio Funds Index4 | 6.34 | % | 2.54 | % | — | 4.87 | % | ||||||||||||||||||||||

| Class D1—Return Before Taxes | 8.05 | % | 2.68 | % | — | 6.41 | % | ||||||||||||||||||||||

| S&P 500® Index2 | 4.91 | % | 0.55 | % | — | 5.07 | % | ||||||||||||||||||||||

| Lehman Brothers U.S. Government/Credit Index3 | 2.37 | % | 6.11 | % | — | 6.36 | % | ||||||||||||||||||||||

| Lipper Flexible Portfolio Funds Index4 | 6.34 | % | 2.54 | % | — | 4.87 | % | ||||||||||||||||||||||

| * | Only shown for share classes with less than a ten-year history. |

| (1) | Classes A, C and D commenced operations on July 28, 1997. Class B commenced operations on October 31, 1988. |

| (2) | The Standard & Poor's 500 Index (S&P 500®) is a broad-based index, the performance of which is based on the performance of 500 widely-held common stocks chosen for market size, liquidity and industry group representation. Indexes are unmanaged and their returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index. |

| (3) | The Lehman Brothers U.S. Government/Credit Index tracks the performance of government and corporate obligations, including U.S. government agency and Treasury securities and corporate and Yankee bonds. Indexes are unmanaged and their returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index. |

9

| (4) | The Lipper Flexible Portfolio Funds Index is an equally weighted performance index of the largest qualifying funds (based on net assets) in the Lipper Flexible Portfolio Funds classification. The Index, which is adjusted for capital gains distributions and income dividends, is unmanaged and should not be considered an investment. There are currently 30 funds represented in this Index. |

| (5) | These returns do not reflect any tax consequences from a sale of your shares at the end of each period, but they do reflect any applicable sales charges on such a sale. |

Included in the table above are the after-tax returns for Strategist's Class B shares. The after-tax returns for Strategist's other Classes will vary from the Class B shares' returns. After-tax returns are calculated using the historical highest individual federal marginal income tax rates during the period shown and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor's tax situation and may differ from those shown, and after-tax returns are not relevant to investors who hold their Strategist shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. After-tax returns may be higher than before-tax returns due to foreign tax credits and/or an assumed benefit from capital losses that would have been realized had Strategist shares been sold at the end of the relevant periods, as applicable.

Fee Table

The following table briefly describes the fees and expenses that a shareholder of Total Return and Strategist may pay if they buy and hold shares of each respective Fund. These expenses are deducted from each respective Fund's assets and are based on expenses paid by Total Return for its fiscal year ended July 31, 2005, and by Strategist for its fiscal year ended July 31, 2005. Total Return and Strategist each pays expenses for management of its assets, distribution of its shares and other services, and those expenses are reflected in the net asset value per share of each Fund. The table also sets forth pro forma fees for the surviving combined fund (Strategist) (the ‘‘Combined Fund’’) reflecting what the fee schedule would have been on January 31, 2006, if the Reorganization had been consummated twelve (12) months prior to that date.

| Shareholder Fees (fees paid directly from a shareholder's investment) | Total Return | Strategist | Pro Forma Combined Fund(6) | |||||||||||

| Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) | ||||||||||||||

| Class A | 5.25%(1) | 5.25%(1) | 5.25%(1) | |||||||||||

| Class B | none | none | none | |||||||||||

| Class C | none | none | none | |||||||||||

| Class D | none | none | none | |||||||||||

| Maximum Deferred Sales Charge (Load) (as a percentage based on the lesser of the offering price or net asset value at redemption) | ||||||||||||||

| Class A | none(2) | none(2) | none(2) | |||||||||||

| Class B | 5.00%(3) | 5.00%(3) | 5.00%(3) | |||||||||||

| Class C | 1.00%(4) | 1.00%(4) | 1.00%(4) | |||||||||||

| Class D | none | none | none | |||||||||||

10

| Shareholder Fees (fees paid directly from a shareholder's investment) | Total Return | Strategist | Pro Forma Combined Fund(6) | |||||||||||

| Redemption Fees(5) | ||||||||||||||

| Class A | 2.00% | 2.00% | 2.00% | |||||||||||

| Class B | 2.00% | 2.00% | 2.00% | |||||||||||

| Class C | 2.00% | 2.00% | 2.00% | |||||||||||

| Class D | 2.00% | 2.00% | 2.00% | |||||||||||

| Annual Fund Operating Expenses (expenses that are deducted from fund assets) | Total Return | Strategist | Pro Forma Combined Fund(6) | |||||||||||

| Advisory Fees* | ||||||||||||||

| Class A | 0.67% | 0.42% | 0.42% | |||||||||||

| Class B | 0.67% | 0.42% | 0.42% | |||||||||||

| Class C | 0.67% | 0.42% | 0.42% | |||||||||||

| Class D | 0.67% | 0.42% | 0.42% | |||||||||||

| Distribution and Service (12b-1) Fees(7) | ||||||||||||||

| Class A | 0.25% | 0.25% | 0.25% | |||||||||||

| Class B | 1.00% | 1.00% | 1.00% | |||||||||||

| Class C | 1.00% | 0.97% | 0.97% | |||||||||||

| Class D | none | none | none | |||||||||||

| Other Expenses | ||||||||||||||

| Class A | 0.43% | 0.26% | 0.28% | |||||||||||

| Class B | 0.43% | 0.26% | 0.28% | |||||||||||

| Class C | 0.43% | 0.26% | 0.28% | |||||||||||

| Class D | 0.43% | 0.26% | 0.28% | |||||||||||

| Total Annual Fund Operating Expenses (8) | ||||||||||||||

| Class A | 1.35% | 0.93% | 0.95% | |||||||||||

| Class B | 2.10% | 1.68% | 1.70% | |||||||||||

| Class C | 2.10% | 1.65% | 1.67% | |||||||||||

| Class D | 1.10% | 0.68% | 0.70% | |||||||||||

Example

To attempt to show the effect of these expenses on an investment over time, the hypotheticals shown below have been created. The example assumes that an investor invests $10,000 in either Total Return, Strategist or the Combined Fund, that the investment has a 5% return each year and that the operating expenses for each Fund remain the same (as set forth in the chart above). Although a shareholder's actual costs may be higher or lower, the tables below show a shareholder's costs at the end of each period based on these assumptions depending upon whether or not a shareholder sold his shares at the end of each period.

11

If a Shareholder SOLD His Shares:

| 1 year | 3 years | 5 years | 10 years | |||||||||||||||

| Total Return | ||||||||||||||||||

| Class A | $ | 655 | $ | 930 | $ | 1,226 | $ | 2,064 | ||||||||||

| Class B | $ | 713 | $ | 958 | $ | 1,329 | $ | 2,431 | ||||||||||

| Class C | $ | 313 | $ | 658 | $ | 1,129 | $ | 2,431 | ||||||||||

| Class D | $ | 112 | $ | 350 | $ | 606 | $ | 1,340 | ||||||||||

| Strategist | ||||||||||||||||||

| Class A | $ | 615 | $ | 806 | $ | 1,013 | $ | 1,608 | ||||||||||

| Class B | $ | 671 | $ | 830 | $ | 1,113 | $ | 1,987 | ||||||||||

| Class C | $ | 268 | $ | 520 | $ | 897 | $ | 1,955 | ||||||||||

| Class D | $ | 69 | $ | 218 | $ | 379 | $ | 847 | ||||||||||

| Pro Forma Combined Fund | ||||||||||||||||||

| Class A | $ | 617 | $ | 812 | $ | 1,023 | $ | 1,630 | ||||||||||

| Class B | $ | 673 | $ | 836 | $ | 1,073 | $ | 1,810 | ||||||||||

| Class C | $ | 270 | $ | 526 | $ | 907 | $ | 1,976 | ||||||||||

| Class D | $ | 72 | $ | 224 | $ | 390 | $ | 871 | ||||||||||

If a Shareholder HELD His Shares:

| 1 year | 3 years | 5 years | 10 years | |||||||||||||||

| Total Return | ||||||||||||||||||

| Class A | $ | 655 | $ | 930 | $ | 1,226 | $ | 2,064 | ||||||||||

| Class B | $ | 213 | $ | 658 | $ | 1,129 | $ | 2,431 | ||||||||||

| Class C | $ | 213 | $ | 658 | $ | 1,129 | $ | 2,431 | ||||||||||

| Class D | $ | 112 | $ | 350 | $ | 606 | $ | 1,340 | ||||||||||

| Strategist | ||||||||||||||||||

| Class A | $ | 615 | $ | 806 | $ | 1,013 | $ | 1,608 | ||||||||||

| Class B | $ | 176 | $ | 545 | $ | 939 | $ | 1,987 | ||||||||||

| Class C | $ | 176 | $ | 545 | $ | 939 | $ | 1,955 | ||||||||||

| Class D | $ | 75 | $ | 233 | $ | 406 | $ | 847 | ||||||||||

| Pro Forma Combined Fund | ||||||||||||||||||

| Class A | $ | 617 | $ | 812 | $ | 1,023 | $ | 1,630 | ||||||||||

| Class B | $ | 173 | $ | 536 | $ | 923 | $ | 1,810 | ||||||||||

| Class C | $ | 170 | $ | 526 | $ | 907 | $ | 1,976 | ||||||||||

| Class D | $ | 72 | $ | 224 | $ | 390 | $ | 871 | ||||||||||

While Class B and Class C shares do not have any front-end sales charges, their higher ongoing annual expenses (due to higher 12b-1 fees) mean that over time you could end up paying more for these shares than if you were to pay front-end sales charges for Class A shares.

| * | Expense information has been restated to reflect current fees in effect as of November 1, 2004. |

| (1) | Reduced for purchases of $25,000 and over. See ‘‘Share Class Arrangements — Class A Shares’’ in each Fund's Prospectus. |

12

| (2) | Investments that are not subject to any sales charge at the time of purchase are subject to a contingent deferred sales charge (‘‘CDSC’’) of 1.00% that will be imposed if you sell your shares within one year after purchase, except for certain specific circumstances. See ‘‘Purchases, Exchanges and Redemptions’’ below and ‘‘Share Class Arrangements — Class A Shares’’ in each Fund's Prospectus. |

| (3) | The CDSC is scaled down to 1.00% during the sixth year, reaching zero thereafter. See ‘‘Purchases, Exchanges and Redemptions’’ below and ‘‘Share Class Arrangements — Class B Shares’’ in each Fund's Prospectus. |

| (4) | Only applicable if you sell your shares within one year after purchase. See ‘‘Purchases, Exchanges and Redemptions’’ below and ‘‘Share Class Arrangements — Class C Shares’’ in each Fund's Prospectus. |

| (5) | Payable to the Fund on shares redeemed within seven days of purchase. The redemption fee is based on the redemption proceeds. See ‘‘Shareholder Information — How to Sell Shares’’ in each Fund's Prospectus for more information on redemption fees. |

| (6) | Pro forma expenses are calculated based on the assets of Strategist and Total Return as of January 31, 2006. |

| (7) | Each Fund has adopted a Rule 12b-1 Distribution Plan pursuant to which it reimburses the distributor for distribution-related expenses (including personal services to shareholders) incurred on behalf of Class A, Class B and Class C shares in an amount each month up to an annual rate of 0.25%, 1.00% and 1.00% of the average daily net assets of Class A, Class B and Class C shares, respectively. |

| (8) | The Investment Adviser has agreed to cap the total operating expense ratios of the Combined Fund at 0.92%, 1.67%, 1.64% and 0.67% for Class A, Class B, Class C and Class D shares, respectively, for a period of two years following the consummation of the Reorganization. |

The purpose of the foregoing fee tables is to assist the shareholder in understanding the various costs and expenses that a shareholder in each Fund will bear directly or indirectly. For a more complete description of these costs and expenses, see ‘‘Comparison of Total Return and Strategist — Investment Advisory and Distribution Plan Fees; Other Significant Fees; and Purchases, Exchanges and Redemptions’’ below.

Tax Consequences of the Reorganization

As a condition to the Reorganization, Total Return has requested an opinion of Clifford Chance US LLP to the effect that the Reorganization will constitute a tax-free reorganization for federal income tax purposes, and that no gain or loss will be recognized by Total Return, Strategist or Total Return's shareholders for federal income tax purposes as a result of the transactions included in the Reorganization. For further information about the tax consequences of the Reorganization, see ‘‘The Reorganization — Tax Aspects of the Reorganization’’ below.

Comparison of Total Return and Strategist

Investment Objectives and Policies. The investment objective of Total Return is to seek high total return from capital growth and income. The investment objective of Strategist is to seek to maximize the total return on its investments. The principal differences between the Funds' investment policies are more fully described under ‘‘Comparison of Investment Objectives, Policies and Restrictions’’ below. The investment policies of both Total Return and Strategist are fundamental and may not be changed without shareholder approval.

13

Total Return seeks to achieve its investment objective by normally investing at least 65% of its assets in common stocks (including depositary receipts) and convertible securities of domestic and foreign companies. Generally, the Fund will invest in companies that (i) have a market capitalization of at least $1 billion and (ii) in the view of the Investment Adviser, are expected to pay dividends or interest income. Up to 35% of Total Return's assets may be invested in foreign securities (including depositary receipts). In addition, up to 35% of Total Return's net assets may be invested in fixed-income securities. Total Return may also invest in forward foreign currency contracts.

Strategist seeks to achieve its investment objective by actively allocating assets among the major asset categories of equity securities (including depositary receipts), fixed income securities and money market instruments, with no limit on the percentage of assets that may be allocated to any one asset class. Within the equity sector, the Investment Adviser actively allocates funds to those economic sectors it expects to benefit from major trends and to individual stocks which it considers to have superior investment potential. Within the fixed-income sector of the market, the Investment Adviser seeks to maximize the return on its investments by adjusting maturities and coupon rates as well as by exploiting yield differentials among different types of investment grade bonds. Within the money market sector of the market, the Investment Adviser seeks to maximize returns by exploiting spreads among short-term instruments.

Strategist may invest in common stock, preferred stock, convertible securities, investment grade debt securities, U.S. government securities, mortgage-backed securities (including collateralized mortgage obligations), asset-backed securities, real estate investment trusts (‘‘REITs’’) and money market instruments. In addition, Strategist may invest up to 20% of its net assets in securities issued by foreign governments and foreign private issuers (but no more than 10% of its net assets in securities denominated in a foreign currency). Strategist may also invest in forward foreign currency exchange contracts and derivatives, including options and futures (including interest rate futures and options thereon). Strategist may also invest in commercial mortgage-backed securities (‘‘CMBS’’), swaps, targeted return index securities (‘‘TRAINs’’), stripped mortgage backed securities and inverse floating obligations (‘‘inverse floaters’’).

Investment Advisory and Distribution Plan Fees. Total Return and Strategist obtain advisory services from the Investment Adviser. Each class of both Funds' shares is subject to the same advisory fee rates applicable to the respective Fund.

For the fiscal year ended July 31, 2005, each Fund paid the Investment Adviser monthly compensation calculated daily by applying the following annual rates to the Fund's average daily net assets:

| Total Return | For the period from November 1, 2004 to July 31, 2005: 0.67% of the portion of the daily net assets not exceeding $500 million, 0.645% of the portion of the daily net assets exceeding $500 million but not exceeding $1 billion; and 0.62% of the portion of the daily net assets exceeding $1 billion; and | |

| For the period from August 1, 2004 to October 31, 2004: 0.75% of the portion of the daily net assets not exceeding $500 million, 0.725% of the portion of the daily net assets exceeding $500 million but not exceeding $1 billion; and 0.70% of the portion of the daily net assets exceeding $1 billion. | ||

14

| Strategist | For the period from November 1, 2004 to July 31, 2005: 0.42% of the portion of the daily net assets not exceeding $1.5 billion; and 0.395% of the portion of the daily net assets exceeding $1.5 billion; and | |

| For the period from August 1, 2004 to October 31, 2004: 0.60% of the portion of the daily net assets not exceeding $500 million, 0.55% of the portion of the daily net assets exceeding $500 million but not exceeding $1 billion; 0.50% of the portion of the daily net assets exceeding $1 billion but not exceeding $1.5 billion; 0.475% of the portion of the daily net assets exceeding $1.5 billion but not exceeding $2 billion; 0.45% of the portion of daily net assets exceeding $2 billion but not exceeding $3 billion; and 0.425% of the portion of the daily net assets exceeding $3 billion. | ||

Both Total Return and Strategist have adopted a distribution plan (together, the ‘‘Plan’’) pursuant to Rule 12b-1 under the 1940 Act. In the case of Class A and Class C shares, the Plan provides that the Funds will reimburse Morgan Stanley Distributors Inc. (the ‘‘Distributor’’) and others for the expenses of certain activities and services incurred by them in connection with the distribution of the Class A and Class C shares of the Fund. Reimbursement for these expenses is made in monthly payments by each Fund to the Distributor which will in no event exceed amounts equal to payments at the annual rates of 0.25% and 1.00% of the average daily net assets of Class A and Class C shares, respectively. In the case of Total Return's Class B shares, Total Return's Plan provides that the Fund will reimburse the Distributor and others for their actual distribution expenses incurred on behalf of Class B Shares and for unreimbursed distribution expenses a fee, the amount of which each monthly payment may in no event exceed an amount equal to payment at the annual rate of 1.00% of the lesser of: (a) the average daily aggregate gross sales of the Class B shares since the inception of Total Return (not including capital gains distributions), less the average daily aggregate net asset value of the Class B shares redeemed since Total Return's inception upon which a CDSC has been imposed or upon which such charge has been waived; or (b) the average daily net assets of Class B shares. In the case of Strategist's Class B Shares, the Plan provides that the Fund will reimburse the Distributor and others for their actual distribution expenses on behalf of Class B Shares and for unreimbursed distribution expenses a fee, the amount of which each monthly payment may in no event exceed an amount equal to payment at the annual rate to 1.00% of the lesser of: (a) the average daily aggregate gross purchases by all shareholders of the Fund's Class B shares since the implementation of the Plan on November 8, 1989 (not including capital gains distributions), less the average daily aggregate net asset value of the Fund's Class B shares sold by all shareholders since the Plan's inception upon which a CDSC has been imposed or upon which charge has been waived, or (b) the average daily net assets of Class B shares attributable to shares purchased by all shareholders, net of related shares sold by all shareholders since the implementation of the Plan, plus 0.25% of the average daily net assets of Class B shares attributable to shares purchased by all shareholders, net of related shares sold by all shareholders prior to the implementation of the Plan. The 12b-1 fee is paid for the services provided and the expenses borne by the Distributor and others in connection with the distribution of each Fund's Class B shares. There are no 12b-1 fees applicable to each Fund's Class D shares. For further information relating to the 12b-1 fees applicable to each class of Strategist's shares, see the section entitled ‘‘Share Class Arrangements’’ in Strategist's Prospectus, attached hereto. The Distributor also receives the

15

proceeds of any CDSC paid by the Funds' shareholders at the time of redemption. The CDSC schedules applicable to each of Total Return and Strategist are set forth below under ‘‘Purchases, Exchanges and Redemptions.’’

Other Significant Fees. Both Total Return and Strategist pay additional fees in connection with their operations, including legal, auditing, transfer agent, trustees fees and custodial fees. See ‘‘Synopsis — Fee Table’’ above for the percentage of average net assets represented by such ‘‘Other Expenses.’’

Purchases, Exchanges and Redemptions. Class A shares of each Fund are sold at net asset value plus an initial sales charge of up to 5.25%. The initial sales charge is reduced for certain purchases. Investments of $1 million or more (and investment by certain other limited categories of investors) are not subject to any sales charges at the time of purchase, but are generally subject to a CDSC of 1.00% on redemptions made within 18 months after the last day of the month of purchase (except for certain specific circumstances fully described in each Fund's Prospectus).

Class B shares of each Fund are offered at net asset value with no initial sales charge, but are subject to the same CDSC schedule set forth below:

| Year Since Purchase Payment Made | Class B Shares of Total Return and Strategist | |||||

| First | 5.0% | |||||

| Second | 4.0% | |||||

| Third | 3.0% | |||||

| Fourth | 2.0% | |||||

| Fifth | 2.0% | |||||

| Sixth | 1.0% | |||||

| Seventh and thereafter | None | |||||

Class C shares of each Fund are sold at net asset value with no initial sales charge, but are subject to a CDSC of 1.00% on redemptions made within one year after the last day of the month of purchase. The CDSC may be waived for certain redemptions (which are fully described under the section ‘‘Share Class Arrangements’’ in each Fund's Prospectus).

Class D shares of each Fund are available only to limited categories of investors and are sold at net asset value with no initial sales charge or CDSC.

The CDSC is paid to the Distributor. Shares of Total Return and Strategist are distributed by the Distributor and offered by Morgan Stanley DW and other dealers who have entered into selected dealer agreements with the Distributor. For further information relating to the CDSC schedules applicable to each class of shares of Total Return and Strategist, see the section entitled ‘‘Share Class Arrangements’’ in each Fund's Prospectus.

Shares of each class of Total Return and Strategist may be exchanged for shares of the same class of any other continuously offered Multi-Class Fund, or for shares of a No-Load Fund, a Money Market Fund or Limited Duration U.S. Treasury Trust (each, an ‘‘Exchange Fund’’), without the imposition of an exchange fee. Front-end sales charges are not imposed on exchanges of Class A shares. See the inside back cover of the Strategist Prospectus for each Morgan Stanley Fund's designation as a Multi-Class Fund, No-Load Fund or Money Market Fund. Upon consummation of the Reorganization, the foregoing exchange privileges will still be applicable to shareholders of the Combined Fund.

Strategist shares distributed to Shareholders as a result of the Reorganization will not be subject to an initial sales charge.

16

With respect to both Funds, no CDSC is imposed at the time of any exchange, although any applicable CDSC will be imposed upon ultimate redemption. For purposes of calculating the holding period in determining any applicable CDSC upon redemption of shares received as a result of the Reorganization, any period during which the Shareholder held shares of a fund that charged a CDSC (e.g., Total Return) will be counted. During the period of time a Strategist or Total Return shareholder remains in an Exchange Fund, the holding period (for purposes of determining the CDSC rate) is frozen. Both Total Return and Strategist provide telephone exchange privileges to their shareholders. For greater details relating to exchange privileges applicable to Strategist, see the section entitled ‘‘How to Exchange Shares’’ in Strategist's Prospectus.

Shares of each Fund redeemed within seven days of purchase will be subject to a 2% redemption fee, payable to such Fund. The redemption fee is designed to protect each Fund and its remaining shareholders from the effects of short-term trading. The redemption fee is not imposed on redemptions made: (i) through systematic withdrawal/exchange plans, (ii) through pre-approved asset allocation programs, (iii) of shares received by reinvesting income dividends or capital gain distributions, (iv) through certain collective trust funds or other pooled vehicles and (v) on behalf of advisory accounts where client allocations are solely at the discretion of the Morgan Stanley Investment Management investment team. The redemption fee is based on, and deducted from, the redemption proceeds. Each time shares are redeemed or exchanged, the shares held the longest will be redeemed or exchanged first. The redemption fee may not be imposed on transactions that occur through certain omnibus accounts at financial intermediaries.

Shareholders of Total Return and Strategist may redeem their shares for cash at any time at the net asset value per share next determined; however, such redemption proceeds may be reduced by the amount of any applicable CDSC. Fund shares redeemed within seven days of purchase will be subject to a 2% redemption fee, payable to the Fund. Both Total Return and Strategist offer a reinstatement privilege whereby a shareholder who has not previously exercised such privilege whose shares have been redeemed or repurchased may, within thirty-five days after the date of redemption or repurchase, reinstate any portion or all of the proceeds thereof in shares of the same class from which such shares were redeemed or repurchased and receive a pro rata credit for any CDSC paid in connection with such redemption or repurchase. Total Return and Strategist may redeem involuntarily, at net asset value, most accounts valued at less than $100.

Dividends. Each Fund declares dividends separately for each of its classes. Total Return pays dividends from net investment income annually, while Strategist pays such dividends quarterly. Each Fund usually distributes net capital gains, if any, in December. Each Fund, however, may determine either to distribute or to retain all or part of any net long-term capital gains in any year for reinvestment. With respect to each Fund, dividends and capital gains distributions are automatically reinvested in additional shares of the same class of shares of the Fund at net asset value unless the shareholder elects to receive cash.

PRINCIPAL RISK FACTORS

The share price and return of Strategist and Total Return will fluctuate with changes in the market value of their respective portfolio securities. The market value of the Funds' portfolio securities will increase or decrease due to a variety of economic, market and political factors which cannot be predicted. The principal risks associated with an investment in Strategist and Total Return are summarized below.

Equity Securities. Both Funds invest in common stocks and other equity securities including preferred stocks, debt or preferred stocks convertible into common stocks and depositary receipts. In

17

general, stock and other equity security values fluctuate in response to activities specific to the company as well as general market, economic and political conditions. Stock and other equity security prices can fluctuate widely in response to these factors.

Foreign Securities. Each Fund may invest in foreign securities (including depositary receipts) not traded in the United States on a national securities exchange. Investments in foreign securities involve risks in addition to the risks associated with domestic securities. One additional risk is currency risk. While the price of Fund shares is quoted in U.S. dollars, the Funds generally convert U.S. dollars to a foreign market's local currency to purchase a security in that market. If the value of that local currency falls relative to the U.S. dollar, the U.S. dollar value of the foreign security will decrease. This is true even if the foreign security's local price remains unchanged. Foreign securities also have risks related to economic and political developments abroad, including expropriations, confiscatory taxation, exchange control regulation, limitations on the use or transfer of Fund assets and any effects of foreign social, economic or political instability. Foreign companies, in general, are not subject to the regulatory requirements of U.S. companies and, as such, there may be less publicly available information about these companies. Moreover, foreign accounting, auditing and financial reporting standards generally are different from those applicable to U.S. companies. Finally, in the event of a default of any foreign debt obligations, it may be more difficult for the Funds to obtain or enforce a judgment against the issuers of the securities. Securities of foreign issuers may be less liquid than comparable securities of U.S. issuers and, as such, their price changes may be more volatile. Furthermore, foreign exchanges and broker-dealers are generally subject to less government and exchange scrutiny and regulation than their U.S. counterparts. In addition, differences in clearance and settlement procedures in foreign markets may occasion delays in settlement of the Funds' trades effected in those markets and could result in losses to a Fund due to subsequent declines in the value of the securities subject to the trades.

Depositary receipts involve substantially identical risks to those associated with direct investment in foreign securities. In addition, the underlying issuers of certain depositary receipts, particularly unsponsored or unregistered depositary receipts, are under no obligation to distribute shareholder communications to the holders of such receipts, or to pass through to them any voting rights with respect to the deposited securities.

Fixed-Income Securities. Both Funds may invest in fixed-income securities. All fixed-income securities are subject to two types of risk: credit risk and interest rate risk. Credit risk refers to the possibility that the issuer of a security will be unable to make interest payments and/or repay the principal on its debt. Interest rate risk refers to fluctuations in the value of a fixed-income security resulting from changes in the general level of interest rates. When the general level of interest rates goes up, the prices of most fixed-income securities go down. When the general level of interest rates goes down, the prices of most fixed-income securities go up. (Zero coupon securities are typically subject to greater price fluctuations than comparable securities that pay interest.) Strategist's investment grade securities may have speculative credit risk characteristics.

Convertible Securities. Both Funds may also invest in convertible securities which subject the Funds to the risks associated with both fixed-income securities and common stocks (discussed above). To the extent that a convertible security's investment value is greater than its conversion value, its price will be likely to increase when interest rates fall and decrease when interest rates rise, as with a fixed-income security. If the conversion value exceeds the investment value, the price of the convertible security will tend to fluctuate directly with the price of the underlying equity security. In addition, a portion of the convertible securities in which Total Return may invest may be rated below investment grade. Securities rated below investment grade are commonly known as ‘‘junk bonds’’ and have speculative characteristics. The prices of junk bonds are likely to be more sensitive to adverse economic changes or individual

18

corporate developments than higher rated securities. During an economic downturn or substantial period of rising interest rates, junk bond issuers and, in particular, highly leveraged issuers may experience financial stress that would adversely affect their ability to service their principal and interest payment obligations, to meet their projected business goals or to obtain additional financing. The secondary market for junk bonds may be less liquid than the market for higher quality securities and, as such, may have an adverse effect on the market prices of certain securities.

Collateralized Mortgage Obligations. Strategist may invest in collateralized mortgage obligations (‘‘CMOs’’), which are debt obligations issued in multiple classes that are collateralized by mortgage loans or mortgage pass-through securities (collectively, ‘‘Mortgage Assets’’). The principal and interest on the Mortgage Assets comprising a CMO may be allocated among the several classes of a CMO in many ways. The general goal in allocating cash flows on Mortgage Assets to the various classes of a CMO is to create certain tranches on which the expected cash flows have a higher degree of predictability than do the underlying Mortgage Assets. As a general matter, the more predictable the cash flow is on a particular CMO tranche, the lower the anticipated yield on that tranche at the time of issue will be relative to the prevailing market yields on the Mortgage Assets. As part of the process of creating more predictable cash flows on certain tranches of a CMO, one or more tranches generally must be created that absorb most of the changes in the cash flows on the underlying Mortgage Assets. The yields on these tranches are generally higher than prevailing market yields on other mortgage related securities with similar average lives. Principal prepayments on the underlying Mortgage Assets may cause the CMOs to be retired substantially earlier than their stated maturities or final distribution dates. Because of the uncertainty of the cash flows on these tranches, the market prices and yields of these tranches are more volatile and may increase or decrease in value substantially with changes in interest rates and/or the rates of prepayment. Due to the possibility that prepayments (on home mortgages and other collateral) will alter the cash flow on CMOs, it is not possible to determine in advance the final maturity date or average life. Faster prepayment will shorten the average life and slower prepayments will lengthen it. In addition, if the collateral securing CMOs or any third party guarantees are insufficient to make payments, the Fund could sustain a loss.

Asset-Backed Securities. Strategist may invest in asset-backed securities. Asset-backed securities have risk characteristics similar to mortgage-backed securities. Like mortgage-backed securities, they generally decrease in value as a result of interest rate increases, but may benefit less than other fixed-income securities from declining interest rates, principally because of prepayments. Also, as in the case of mortgage-backed securities, prepayments generally increase during a period of declining interest rates although other factors, such as changes in credit use and payment patterns, may also influence prepayment rates. Asset-backed securities also involve the risk that various federal and state consumer laws and other legal and economic factors may result in the collateral backing the securities being insufficient to support payment on the securities.

REITs. Strategist, and to a lesser extent Total Return, may also invest in REITs, which pool investors' funds for investment primarily in commercial real estate properties. Investment in REITs may be the most practical alternative means for the Fund to invest in the real estate industry (the Fund is prohibited from investing in real estate directly). As a shareholder in a REIT, the Fund would bear its ratable share of the REIT's expenses, including its advisory and administrative fees. At the same time the Fund would continue to pay its own management fees, investment advisory fees and other expenses, as a result of which the Fund and its shareholders in effect will be absorbing duplicate levels of fees with respect to investments in REITs.

Options and Futures. Strategist may invest in options and futures. If the Fund invests in options and/or futures, its participation in these markets would subject the Fund's portfolio to certain risks. The

19

Investment Adviser's predictions of movements in the direction of the stock and/or fixed-income markets may be inaccurate, and the adverse consequences to the Fund (e.g., a reduction in the Fund's net asset value or a reduction in the amount of income available for distribution) may leave the Fund in a worse position than if these strategies were not used. Other risks inherent in the use of options and futures include, for example, the possible imperfect correlation between the price of options and futures contracts and movements in the prices of securities, and the possible absence of a liquid secondary market for any particular instrument.

The foregoing discussion is a summary of the principal risk factors. For a more complete discussion of the risks of each Fund, see ‘‘Principal Risks’’ and ‘‘Additional Risk Information’’ in the Prospectus of Total Return and in Strategist's Prospectus, both of which are incorporated herein by reference.

THE REORGANIZATION

The Proposal

The Board of Trustees of Total Return, including the Independent Trustees, having reviewed the financial position of Total Return and the prospects for achieving economies of scale through the Reorganization and having determined that the Reorganization is in the best interests of Total Return and its Shareholders and that the interests of Shareholders will not be diluted as a result thereof, recommends approval of the Reorganization by Shareholders of Total Return.

The Board's Considerations

At a meeting held on February 6, 2006, the Board, including the Independent Trustees, unanimously approved the Reorganization Agreement and determined to recommend that Shareholders approve the Reorganization Agreement. In reaching this decision, the Board made an extensive inquiry into a number of factors, particularly Total Return's inability to gain assets as expected and the comparative expenses currently incurred in the operations of Total Return and Strategist. The Board also considered other factors, including, but not limited to: the general compatibility of the investment objectives, policies and restrictions of Total Return and Strategist; the terms and conditions of the Reorganization which would affect the price of shares to be issued in the Reorganization; the tax-free nature of the Reorganization; and any direct or indirect costs to be incurred by Total Return and Strategist in connection with the Reorganization.

In recommending the Reorganization to Shareholders, the Board of Total Return considered that the Reorganization would have the following benefits to Shareholders:

1. Once the Reorganization is consummated, the expenses which would be borne by shareholders of each class of the Combined Fund will be substantially lower on a percentage basis than the expenses of each corresponding class of Total Return. The Board noted that the annual management fee (as a percentage of assets) payable by Strategist to the Investment Adviser was lower than that payable by Total Return. The Board also noted that Strategist's ‘‘Other Expenses’’ for its last fiscal year (0.26%) were lower than Total Return's ‘‘Other Expenses’’ for its last fiscal year (0.43%). The Board also considered that, upon completion of the Reorganization, the Investment Adviser has agreed to cap the total operating expense ratios of the Combined Fund at 0.92%, 1.67%, 1.64% and 0.67% for Class A, Class B, Class C and Class D shares, respectively, for a period of two years, making the total annual expense ratios of each class of the Combined Fund following the Reorganization equal to that of Strategist. Furthermore, to the extent that the Reorganization would result in Shareholders becoming shareholders of a combined larger fund, further economies of scale could be achieved since various fixed expenses (e.g., auditing and legal) can be spread over a larger number of shares.

20

2. Shareholders would have continued participation in a fund with similar investment objectives and policies, substantially better performance and lower annual operating expenses per share due to a substantially lower management fee and economies of scale. The Board also considered that the performance record of Strategist is more representative of the portfolio management team than the performance record of Total Return because the team has been managing Strategist since January 1994, whereas it has been managing Total Return only since October 2002.

3. The Reorganization has been structured in a manner intended to qualify as a tax-free reorganization for federal income tax purposes, pursuant to which no gain or loss will be recognized by Total Return, Strategist or their shareholders for federal income tax purposes as a result of transactions included in the Reorganization.

In light of the reduction in annual operating expenses and other potential benefits of the Reorganization, as well as the uncertainty regarding the extent to which any lost capital loss carryovers could have been utilized for the benefit of Total Return Shareholders (as set forth in greater detail herein under ‘‘The Reorganization — Tax Aspects of the Reorganization’’), the Board concluded that the Reorganization was in the best interests of the Shareholders, notwithstanding the potential loss of capital loss carryovers.

The Board of Trustees of Strategist, including a majority of the Independent Trustees of Strategist, also has determined that the Reorganization is in the best interests of Strategist and its shareholders and that the interests of existing shareholders of Strategist will not be diluted as a result thereof. The transaction will enable Strategist to acquire investment securities which are consistent with Strategist's investment objectives, without the brokerage costs attendant to the purchase of such securities in the market.

The Reorganization Agreement

The terms and conditions under which the Reorganization would be consummated, as summarized below, are set forth in the Reorganization Agreement. This summary is qualified in its entirety by reference to the form of Reorganization Agreement, a copy of which is attached as Exhibit A to this Proxy Statement and Prospectus.

The Reorganization Agreement provides that (i) Total Return will transfer all of its assets, including portfolio securities, cash, cash equivalents and receivables to Strategist on the Closing Date in exchange for the assumption by Strategist of stated liabilities of Total Return, including all expenses, costs, charges and reserves, as reflected on an unaudited statement of assets and liabilities of Total Return prepared by the Treasurer of Total Return as of the Valuation Date in accordance with generally accepted accounting principles consistently applied from the prior audited period, and the delivery of the Strategist Shares; (ii) the Strategist Shares would be distributed to Shareholders on the Closing Date or as soon as practicable thereafter; (iii) Total Return would be dissolved and de-registered as an investment company under the 1940 Act; and (iv) the outstanding shares of Total Return would be canceled.

The number of Strategist Shares to be delivered to Total Return will be determined by dividing the aggregate net asset value of each class of shares of Total Return acquired by Strategist by the net asset value per share of the corresponding class of shares of Strategist; these values will be calculated as of the close of business of the New York Stock Exchange on the Valuation Date. As an illustration, assume that on the Valuation Date, Class B shares of Total Return had an aggregate net asset value of $100,000. If the net asset value per Class B share of Strategist were $10 per share at the close of business on the Valuation Date, the number of Class B shares of Strategist to be issued would be 10,000 ($100,000 ÷ $10). These 10,000 Class B shares of Strategist would be distributed to the former Class B shareholders of Total

21

Return. This example is given for illustration purposes only and does not bear any relationship to the dollar amounts or shares expected to be involved in the Reorganization.