UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-05641 | |||||||

| ||||||||

The Park Avenue Portfolio | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

7 Hanover Square New York, N.Y. |

| 10004 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

|

|

| ||||||

Frank L. Pepe |

| Thomas G. Sorell | ||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | (800) 221-3253 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | December 31, 2005 |

| ||||||

ITEM 1. REPORTS TO STOCKHOLDERS.

The Annual Report to Stockholders follows.

The Park Avenue Portfolio®

Annual Report

to Shareholders

December 31, 2005

The Guardian Park Avenue Fund®

The Guardian UBS Large Cap Value FundSM

The Guardian Park Avenue Small Cap FundSM

The Guardian UBS Small Cap Value FundSM

The Guardian Asset Allocation FundSM

The Guardian S&P 500 Index FundSM

The Guardian Baillie Gifford International Growth FundSM

The Guardian Baillie Gifford Emerging Markets FundSM

The Guardian Investment Quality Bond FundSM

The Guardian Low Duration Bond FundSM

The Guardian High Yield Bond FundSM

The Guardian Tax-Exempt FundSM

The Guardian Cash Management FundSM

Dear Shareholder:

Thomas G. Sorrell, CFA

Chief Investment Officer

QUICK FACTS

• The U.S. economy overcame a number of challenges and continued to expand at a brisk pace in 2005.

• Even though corporate profits were solid, the stock market produced below average returns during the year.

• International stocks generated superior performance in 2005, outpacing their U.S. counterparts.

• Despite continued interest rate hikes by the Federal Reserve Board, the U.S. bond market held up fairly well and generated positive returns in 2005.

• Our outlook for the economy remains positive although it could soften somewhat in 2006. The stock and bond markets could again produce modest gains in the coming year.

The U.S. Economy, Still Going and Going?

Yogi Berra could have best described the economy in 2005 by saying, "It's deja vu all over again."

In our 2004 year-end summary we stated: "...even if you consider all of the headwinds the U.S. economy faced in 2004, one would still be hard pressed to have predicted its resiliency during the year." I would be hard pressed to find a better way to characterize what occurred in 2005. Steadily rising short-term interest rates, record high oil prices, inflationary pressures, a potential housing bubble, a series of devastating hurricanes, terrorist threats and attacks, and geopolitical issues were just some of the issues that could have derailed the economy. Yet, when all was said and done, American consumers, who account for roughly 70% of our gross domestic product (GDP), kept spending and spending, sustaining strong economic growth, but unlike the bunny in that battery commercial that seems to never stop, began to falter in the fourth quarter of 2005. While GDP grew 3.8% in the first quarter, 3.3% in the second quarter, and 4.1% in the third quarter it dropped precipitously to 1.1% in the fourth quarter, principally due to a significant decline in consumer spending. Nevertheless, for the year as a whole GDP grew 3.5% in 2005 versus 4.2% in 2004 year-over-year. The critical economic question for 2006 is to what degree does this decline in consumer spending represent a temporary respite, or a major retrenchment, and to what degree will growth in other sectors of the economy be sufficient to offset any decline? We will address this shortly in our Economic Outlook, but first let's review last year's financial markets and their performance.

A More Modest Year-End Rally

Perhaps we were spoiled by the previous two years, but the market's gains during the fourth quarter of 2005 didn't live up to some people's lofty expectations. During the last three months of the year, the S&P 500 Index returned 2.09%. This wasn't bad, considering the Index rose a fairly modest 4.91% during 2005. However, it didn't stand up to the 12.18% and 9.23% gains in the fourth quarters of 2003 and 2004, respectively.

While consumers may have been upbeat enough to propel the economy forward, investor sentiment was more subdued. Continued solid corporate profit growth in 2005, estimated to be 11% by First Call, did not translate into commensurate price gains for the overall market. In fact, for much of the year stocks traded in a fairly narrow range, sometimes taking two steps forward and then one step back. There were any number of factors impacting the markets, many of which were listed in our economic review. That said, there were pockets of opportunity. In the U.S., mid-capitalization stocks generated superior returns, with the Russell MidCap Index gaining 12.65%. International stocks performed even better, as the MSCI EAFE Index returned 14.02% and emerging market equities, as measured by the MSCI EMF Index, gained an outstanding 34.55%.

Bonds Hold Their Own, Again

Yogi Berra could be called on again to describe the bond market in 2005, as it closely resembled 2004. The outlook for 2004 was much like that of 2005—given continued interest rate hikes by the Federal Reserve Board (the "Fed") both short- and long-term interest rates would increase and bond prices would fall. Yet, as was the case in 2004, during the last 12 months short-term bond yields rose while longer-term bond yields remained fairly stable. During 2005, two-year Treasury yields rose from 3.08% to 4.41%. In contrast, 10-year Treasury yields only moved from 4.24% to 4.37% during the year.

As 2005 ended, much was being made of the fact the yield curve had inverted, meaning two-year Treasury yields were higher than their 10-year counterparts. This is unusual, as investors generally receive higher yields for assuming the greater risks associated with longer-term securities.

This anomaly typically foreshadows an economic recession. In fact, an official from the Federal Reserve Bank of New York concluded that an inverted yield curve "has predicted essentially every U.S. recession since 1950 with only one 'false' signal." We'll discuss this in greater detail in the Bond Outlook that follows.

Looking at 2005 as a whole, the overall bond market, as measured by the Lehman Aggregate Bond Index, returned 2.43%. High yield bonds performed marginally better, with the Lehman High Yield Bond Index returning 2.74% over the same period. While corporate balance sheets continued to improve in 2005, the high yield market was adversely affected by the highly publicized downgrades of General Motors, Ford Motor Company, and both of their finance subsidiaries.

Economic Outlook: A Somewhat Slower Expansion

While a number of economists have expressed concern over the past two years that economic growth was about to falter, we believe that in 2006 they may finally be right. The current Blue Chip consensus forecast for 2006 GDP is 3.4% year-over-year. As mentioned earlier, a critical concern for 2006 economic growth is the willingness and ability of consumers to continue spending at their recent pace. The other important question is will core inflation remain well contained or will rising input prices finally be passed onto the consumer, forcing the Fed to continue tightening monetary policy. As indicated earlier we believe the answer to the first question is that economic growth is more likely to disappoint, while we think inflation will in fact remain well contained.

A strong housing market has to a large degree supported personal consumption expenditures, and a negative savings rate. Consumers have used their homes as ATM's, removing significant equity that was then available for consumption, be it home improvement or a family vacation. Other homeowners took advantage of low interest rates and the ability to reduce their mortgage payments and were able to increase disposable income. Unfortunately, it appears that this economic stimulus is about to decline as the housing market cools and the full effect of rising short-term interest rates is reflected in the economy.

In addition, oil prices remain high, further straining consumer pocketbooks. The economy is near full employment limiting further gains from job growth. Disposable personal income has declined sequentially in real terms in recent quarters. These factors will most likely adversely impact spending by consumers since they have already overstepped income-based spending power. During the second and third quarter of 2005, U.S. households spent more than they earned for the first time since quarterly record keeping began in 1947. Furthermore, the savings rate for all of 2005 fell to a negative .5%, while spending exceeded income, the first time since the Depression. This is clearly not sustainable, and something we do not expect to be repeated in 2006.

On the plus side, corporations are flush with cash and could help pick up the slack by increasing capital expenditures. However, corporations remain conservative with respect to business investment, and capital expenditures have not yet returned to the 10% type growth rates experienced in the 1990's. There is some hope however that this will change if capacity utilization continues to increase above 80%, and creates potential production constraints. In addition to capital spending, export growth, inventory rebuilding, and government spending on hurricane reconstruction may offset some of the decline in personal consumption expenditures.

As mentioned earlier, the preliminary fourth quarter 2005 GDP report of 1.1% was much weaker than the prior three quarters, principally due to weak consumer spending. Despite the fact that a closer reading of the data indicates that the bulk of the weakness in personal consumption was the result of a decline in auto sales, possibly a pay back after heavily promoted employee discounts offered to the general public during the third quarter, we believe that weakness in housing, a decline in mortgage equity withdrawals, and other factors mentioned earlier are likely to slow consumption at some point in 2006. While we do not expect a recession, the economy faces greater downside risks and we believe is more likely to grow below the current consensus economic forecasts.

While economic growth may slow, we are not as concerned about inflationary pressures. Core inflation remains low, global sourcing and competition creates disinflation pressures, and we expect the Fed under its new Chairman Bernanke to remain vigilant in containing inflation expectations, despite recent indications that the Fed may be close to ending their 18-month tightening campaign.

While headline inflation levels are still high, the acceleration evident in core inflation measures in 2004 and early 2005 has dissipated. Overall headline Producer Price Index (PPI) ended 2005 at 5.4% year-over-year off the Fall peaks, but still up from 4.2% rate in December 2004. In December, the Consumer Price Index (CPI) was +3.4% year-over-year, up slightly from year earlier levels. The Fed continues to focus on core inflation measures, which have been fairly well behaved lately. Core CPI was 2.2% year-over-year in December, unchanged from the year earlier level, after doubling during 2004 (from 1.1% to 2.2%). Core Personal Consumption Expenditures (PCE) for December was 1.9% year-over-year and is therefore still within the Fed's central tendency forecast, and has been at about the same level for many months.

Equity Outlook: Single-Digit Gains on Tap for 2006?

Our projection for U.S. stocks in 2005 was for a mid single digit return. We believe that a high single digit return, not far from last year's, should be a reasonable estimate for 2006. Low interest rates and solid global economic expansion led to an estimated 11% growth in per share earnings for the S&P 500 Index last year. The modest appreciation of domestic stock prices caused valuations to drift downwards. Stock valuations are now close to long-term historical averages, despite lower than average long-term interest rates. We believe that stocks offer better value than bonds now. The irrational stock valuations of the bubble era are now a distant memory. Strong cash flow generation, healthy balance sheets and low capital expenditures spending have led to record levels of share buybacks and dividends paid. We believe the Fed tightening and the flat-to-inverted yield curve augur an economic slowdown and not a recession, and so corporate profits should continue to grow. On the flip side, an uptick in inflation or lower than expected economic growth could dampen profit margins. Some observers worry about the impact of the coming mandatory expensing of stock options on reported earnings. In addition, oil prices are again hovering around $60 a barrel, significantly higher than a year ago. Another worry is the effect on consumer spending of reduced mortgage equity withdrawal that would likely follow a cooling in home prices in 2006. However, we believe that a stock market that has eked out positive returns even in the face of $70 oil (per barrel), thirteen Fed rate increases, natural disasters, and geo-political uncertainty has considerable resilience, and will likely jump if and when some of the headwinds diminish, such as when the Fed ends the tightening campaign. All told, Thomson First Call consensus estimate for S&P 500 Index earnings per share growth in 2006 is a 7% increase. We believe it's reasonable to expect market returns a litt le over that during the next 12 months.

Should the economy and corporate profit growth slow, as we expect, stocks of more established high quality companies may outperform smaller, more speculative companies in 2006. In addition, if the dollar declines in 2006, domestic firms with substantial export earnings (typically large companies) will benefit. Elsewhere, value stocks have outperformed growth stocks for six years in a row. As a result, growth stock valuations are more attractive than they have been in quite some time. As such, they may be poised to produce better relative performance than value in the year ahead.

Looking overseas, international stocks have now outperformed their U.S. counterparts for three straight years. This has been a surprise to some, especially since economic growth rates in many foreign countries lagged that of the U.S. Supporting stock prices in the Eurozone and Japan were corporate restructuring, solid profit growth, low interest rates, and expectations for improving economic growth. Many emerging market countries have benefited from high energy and commodity prices, as well as rising domestic demand and improving balance sheets. Looking ahead, we continue to see long-term opportunities in international equities. While their returns may not be as robust as in recent years, U.S. investors may get a boost in their returns if the U.S. dollar weakens in 2006. A falling dollar is good news for Americans investing overseas, as returns from international securities are increased when translated back into U.S. dollars.

Bond Outlook: All Eyes on the "New" Fed

Since June 2004, the Fed has raised interest rates at 13 consecutive meetings, bringing the Federal Funds rate from 1.00% (a 45 year low) to 4.25% at the end of 2005. After each of these meetings, market participants have studiously analyzed the Fed's accompanying policy statement in an attempt to determine its next move. To a great extent, there hasn't been much to scrutinize, as the Fed has consistently stated, "policy accommodation can be removed at a pace that is likely to be measured." However, coinciding with the December 13, 2005 rate hike, the Fed modified the language in its statement by eliminating its view that its policy was accommodative. Then, in early January 2006, the release of the Fed's December meeting minutes said, "additional firming steps required probably would not be large." The market assumed this meant the Fed may stop raising rates at its meeting on January 31, 2006 or at its next meeting in March.

The timing of this potential policy shift is even more interesting given the fact that Alan Greenspan will end his 18-year reign as Fed Chairman at the end of January and Ben Bernanke will assume this role in February. All eyes will clearly be on this transition and on how Mr. Bernanke reacts to incoming economic data. This, in turn, could lead to increased volatility in the bond market. Taking a more broad view of the situation, we expect the Fed to raise rates in January and perhaps in March before pausing or officially ending its tightening campaign. This will no doubt be dependent on economic and inflation data.

As for the yield curve inversion we saw in late December, we do not feel this is a sign of an impending recession. Rather, it may have been a result of strong demand for longer-term bonds by foreign investors and pension funds. We would expect the yield curve to move to a more normalized position with longer-term rates again exceeding shorter-term rates. As for the bond market as a whole in 2006, we anticipate modest returns. It's also important to point out that the premium (or additional yield) for assuming incremental risks by investing in lower quality bonds could continue to be minimal in 2006. In this environment, investors would not be substantially rewarded for assuming additional credit risk.

Rebalancing May Be In Order

Given the market's returns in 2005, your portfolio's asset allocation may no longer be consistent with your goals, risk tolerance, and time horizon. We've found the beginning of the new year is an appropriate time to meet with your financial professional to take a fresh look at your individual situation and overall investment portfolio to determine if adjustments are needed. As in the past, we believe that maintaining a diversified portfolio, one that contains U.S. stocks and bonds and an international component as well, can be instrumental in helping to reach one's long-term goals.

Before I conclude, I would like to provide a brief update on The Guardian Park Avenue Fund.® As you may know, in August 2005, Manind ("Mani") Govil joined Guardian Investor Services LLC as Head of Equity Investments and Portfolio Manager of The Guardian Park Avenue Fund®. We are very pleased with the direction of the Fund since Mani's arrival.

I would like to thank you for your business, and the confidence and trust you place in The Park Avenue Portfolio management team to prudently manage your fund investments. We take this fiduciary responsibility very seriously and you can be sure we will continue to endeavor to generate investment returns that warrant your continued commitment and support.

Thomas G. Sorell, CFA

President, The Park Avenue Portfolio

Chief Investment Officer,

Guardian Investor Services LLC

Gross Domestic Product measures the value of goods and services produced in an economy.

The Morgan Stanley Capital International (MSCI) for Europe, Australia, and Far East (EAFE) is an index that is generally considered to be representative of international stock market activity. The MSCI EAFE is an unmanaged index that is not available for direct investment. Unlike mutual funds, there are no expenses associated with the index.

The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000 Index.

The S&P Index is an index of 500 primarily large-cap U.S. stocks that is generally considered to be representative of U.S. stock market activity. The S&P 500 Index is an unmanaged index that is not available for direct investment. Unlike mutual funds, there are no expenses associated with the index.

Please note that the opinions and outlooks about the markets in general and any specific securities expressed above reflect the viewpoints of Tom Sorrell as of December 31, 2005. Keep in mind that market conditions are constantly evolving and that past performance is not a guarantee of future results. This shareholder letter is not part of the funds' shareholder report for legal purposes and is submitted for the general information of The Park Avenue Portfolio shareholders. This letter is not authorized for distribution to prospective investors unless preceded or accompanied by a prospectus. Please consider the funds' investment objective, risks, fees and charges carefully before investing.

The Park Avenue Portfolio® family of mutual funds is sold by prospectus only. The prospectus contains important information, including fees and expenses and should be read carefully before investing or sending money. You should consider the funds' investment objectives, risks, fees and charges carefully before investing. A prospectus contains this and other important information and can be obtained from your investment professional or by calling 800-221-3253.

Shares of The Park Avenue Portfolio® family of mutual funds are not deposits or obligations of, or guaranteed or endorsed by, any bank or depository institution, nor are they insured by the Federal Deposit Insurance Corporation (FDIC), the National Credit Union Association (NCUA), the Federal Reserve Board, or any other agency. Investment in the funds involves risks, including possible loss of the principal amount invested. Fund shares are subject to market fluctuations and, when redeemed, may be worth more or less than their original cost.

Guardian Investor Services LLC (GIS) is the distributor of The Park Avenue Portfolio family of mutual funds. GIS is an indirect wholly owned subsidiary of The Guardian Life Insurance Company of America (Guardian Life), New York, NY. GIS is located at 7 Hanover Square, New York, NY 10004. 800-221-3253. GIS is a member: NASD, SIPC.

THE PARK AVENUE PORTFOLIO

Table of Contents

| Fund Highlights | Schedule of Investments | ||||||||||

| The Guardian Park Avenue Fund | 2 | 58 | |||||||||

| The Guardian UBS Large Cap Value Fund | 6 | 60 | |||||||||

| The Guardian Park Avenue Small Cap Fund | 10 | 62 | |||||||||

| The Guardian UBS Small Cap Value Fund | 14 | 64 | |||||||||

| The Guardian Asset Allocation Fund | 18 | 66 | |||||||||

| The Guardian S&P 500 Index Fund | 22 | 69 | |||||||||

| The Guardian Baillie Gifford International Growth Fund | 26 | 75 | |||||||||

| The Guardian Baillie Gifford Emerging Markets Fund | 30 | 78 | |||||||||

| The Guardian Investment Quality Bond Fund | 34 | 81 | |||||||||

| The Guardian Low Duration Bond Fund | 40 | 85 | |||||||||

| The Guardian High Yield Bond Fund | 46 | 87 | |||||||||

| The Guardian Tax-Exempt Fund | 51 | 92 | |||||||||

| The Guardian Cash Management Fund | 55 | 95 | |||||||||

| Financial Statements | 98 | ||||||||||

| Notes to Financial Statements | 106 | ||||||||||

| Financial Highlights | 126 | ||||||||||

| Board Approval of Investment Management Agreements (Unaudited) | 141 | ||||||||||

| Shareholder Voting Summary (Unaudited) | 146 | ||||||||||

(This page intentionally left blank)

About Your Annual Report

Information About Indexes:

Index returns are provided for comparative purposes and are quoted throughout the following fund information. Please note that the indices are not available for direct investment and the returns do not reflect the fees and expenses that have been deducted from the Fund. In addition, the return figures for the index do not reflect sales charges that an investor may pay when purchasing or redeeming shares of the Fund.

• The S&P 500 Index is an unmanaged index of 500 primarily large cap U.S. stocks that is generally considered to be representative of U.S. stock market activity.

• The Russell 1000 Value Index offers investors access to the large-cap value segment of the U.S. equity universe. The Russell 1000 Value is constructed to provide a comprehensive and unbiased barometer of the large-cap value market. Based on ongoing empirical research of investment manager behavior, the methodology used to determine growth probability approximates the aggregate large-cap value manager's opportunity set.

• The Russell 2000 Index is an unmanaged index that is generally considered to be representative of small capitalization issues in the U.S. stock market.

• The Russell 2000 Growth Index measures the performance of growth stocks within the Russell 2000 Index and is generally considered to be representative of small capitalization growth issues in the U.S. stock market.

• The Russell 2000 Value Index offers investors access to the small-cap value segment of the U.S. equity universe. The Russell 2000 Value is constructed to provide a comprehensive and unbiased barometer of the small-cap value market. Based on ongoing empirical research of investment manager behavior, the methodology used to determine value probability approximates the aggregate small-cap value manager's opportunity set.

• The Morgan Stanley Capital International (MSCI) Europe, Australasia and Far East (EAFE) Growth Index is an unmanaged index that is generally considered to be representative of the international growth stock market activity.

• The Morgan Stanley Capital International (MSCI) Emerging Markets Free (EMF) Index is an unmanaged index that is generally considered to be representative of the stock market activity of emerging markets. The MSCI EMF Index is a market capitalization weighted index composed of companies representative of the market structure of 22 emerging market countries of Europe, Latin America and the Pacific Basin. The MSCI EMF Index excludes closed markets and those shares in otherwise free markets that may not be purchased by foreigners.

• The Lehman Brothers Aggregate Bond Index is an unmanaged index that is generally considered to be representative of U.S. bond market activity.

• The Lehman Brothers U.S. Government 1-3 Year Bond Index is an unmanaged index that is generally considered to be representative of U.S. short duration bond market activity.

• The Lehman Brothers Corporate High Yield Bond Index is an unmanaged index that is generally considered to be representative of U.S. corporate high yield bond market activity.

• The Lehman Brothers Municipal Bond Index is an unmanaged index that is generally considered to be representative of U.S. municipal bond activity.

• The Lehman Brothers 3-Month Treasury Bill Index is generally considered representative of the average yield of three-month Treasury Bills.

• The Lehman Brothers Treasury Index is generally considered to be representative of U.S. Treasury market activity.

• The Lehman Brothers Municipal Long Index is a subset of the national index with a maturity constraint of greater than or equal to 22 years.

• The Lehman Brothers Municipal 1-Year Index is a subset of the main index rules with a maturity constraint of one year up to but not including two years.

• The Lehman Brothers Municipal 10-Year Index adheres to the same rules as the larger national index with a maturity constraint of years up to but not including 12 years.

Management's Discussion of Fund Performance

The views expressed in the "Update from Fund Management" section of each Fund are those of the Fund's portfolio manager(s) as of December 31, 2005 and are subject to change without notice. They do not necessarily represent the views of Guardian Investor Services LLC, Guardian Baillie Gifford Limited or UBS Global Asset Management (Americas) Inc. The views expressed herein are based on current market conditions and are not intended to predict or guarantee the future performance of any Fund, any individual security, any market or market segment. The composition of each Fund's portfolio is subject to change. No recommendation is made with respect to any security discussed herein.

n The Guardian Park Avenue Fund

Annual Report

to Shareholders

Manind V. Govil, CFA

Portfolio Manager

Objective:

Long-term growth of capital

Portfolio:

At least 80% common stocks and securities convertible into common stocks

Inception Date:

June 1, 1972

Net Assets at

December 31, 2005:

$881,067,068

An Update from Fund Management

U.S. stocks struggled to finish 2005 in positive territory, after two years of double-digit returns in 2003 and 2004. The S&P 500 Index returned 4.91% for the year, but needed an 11th-hour surge in November to move out of negative territory. Throughout 2005, the market was vulnerable to concerns that record-high energy prices, combined with Federal Reserve monetary policy tightening, would depress consumer spending and thereby cause the economic expansion to falter. In addition, investors fretted over the very real impact of high energy prices on the profit margins of industrial and other companies (such as truckers, restaurants and retailers) with heavy energy consumption needs.

Energy stocks led the market in 2005 with a 31% total return, as producers and energy service companies benefited from sustained high commodity prices. Utility stocks were the next best sector with a 17% total return, led by shares of independent power producers. No other sector posted a double-digit gain; financial stocks rose over 6% on the strength of broker-dealer and REIT shares, while healthcare also gained over 6% due to sharp gains in hospital and HMO stocks.

The Guardian Park Avenue Fund returned 3.90%1. Stock selection was positive across most sectors, most notably industrials and energy, while healthcare was the only significant negative. At the portfolio level, the net benefit from selection was offset by modestly negative sector allocation, most notably in the energy sector where our slight average underweight cost us relative performance in the market's strongest sector.

During 2005 our essential strategy was unchanged: to provide a fundamentally-managed large cap core fund. However, The Guardian Park Avenue Fund did experience a change of portfolio managers and investment process, as well as an interim period of approximately five months between the departure of Richard Goldman and my arrival as Portfolio Manager on August 1, 2005. During that period, the Fund was co-Managed by Tom Sorell, Chief Investment Officer of Guardian Investor Services LLC and President of The Park Avenue Portfolio and Matthew Ziehl, Portfolio Manager of The Guardian Park Avenue Small Cap Fund.

From August 1st through the end of 2005, The Guardian Park Avenue Fund returned 2.87%1 versus 2.09% for the S&P 500 Index. We firmly believe that our most critical mission is to increase performance relative to peers and the benchmark. In our efforts to achieve this objective, we are enhancing the fundamental research process by increasing the depth of research and critical thinking on each investment name in the portfolio. The involvement of our quantitative team is also being enhanced in the investment process. Our investment philosophy and style will likely result in fewer companies and lower turnover in the portfolio and alpha (return relative to the market) being driven primarily through stock selection.

Our endeavor is to invest in companies that we believe will emerge stronger from the current economic environment. We seek companies with improving fundamentals for the long-term, whose stocks we believe are mispriced and therefore do not fully reflect their stronger underlying business prospects. Fundamentals endure long after market emotions that cause volatile short-term swings in share prices are forgotten. We believe this strategy over time has the potential to generate superior long term results.

1 Total return is shown for Class A shares and does not take into account the current maximum sales charge of 4.5%.

About information in this report:

• It is important to consider the Fund's investment objectives, risks, fees and expenses before investing. All funds involve some risk, including possible loss of the principal amount invested.

• Please see the "About Your Annual Report" page for a description of the S&P 500 Index.

2

n The Guardian Park Avenue Fund

Annual Report

to Shareholders

Top Ten Holdings (As of 12/31/2005)

Company | Percentage of Total Net Assets | ||||||

| AT & T, Inc. | 3.80 | % | |||||

| Citigroup, Inc. | 3.07 | % | |||||

| Procter & Gamble Co. | 2.93 | % | |||||

| Wyeth | 2.59 | % | |||||

| Wachovia Corp. | 2.55 | % | |||||

| McDonald's Corp. | 2.19 | % | |||||

| Caterpillar, Inc. | 2.16 | % | |||||

| Chevron Corp. | 2.14 | % | |||||

| General Electric Co. | 2.01 | % | |||||

| Intel Corp. | 1.99 | % | |||||

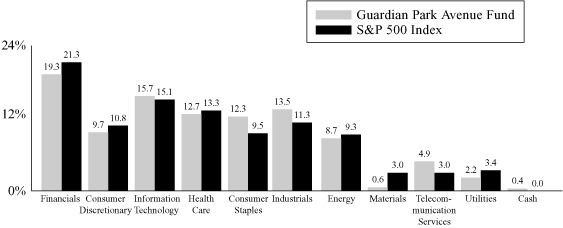

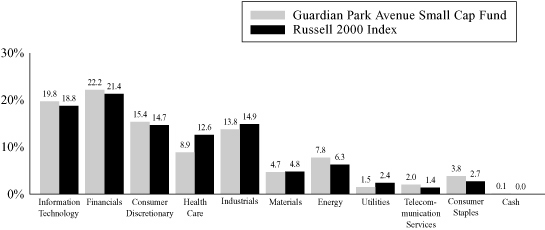

Sector Weightings vs. Index (As of 12/31/2005)

Average Annual Total Returns (For periods ended 12/31/2005)

| Inception Date | 1 Yr | 5 Yrs | 10 Yrs | Since Inception | |||||||||||||||||||||||

| Class A shares | (w/o sales charge) | 6/1/72 | 3.90 | % | -4.01 | % | 5.98 | % | 12.75 | % | |||||||||||||||||

| (w/ sales charge) | 6/1/72 | -0.78 | % | -4.89 | % | 5.49 | % | 12.60 | % | ||||||||||||||||||

| Class B shares | (w/o sales charge) | 5/1/96 | 2.83 | % | -4.94 | % | — | 4.44 | % | ||||||||||||||||||

| (w/ sales charge) | 5/1/96 | -0.17 | % | -5.13 | % | — | 4.44 | % | |||||||||||||||||||

| Class C shares | (w/o sales charge) | 8/7/00 | 2.70 | % | -5.14 | % | — | -9.01 | % | ||||||||||||||||||

| (w/ sales charge) | 8/7/00 | 1.70 | % | -5.14 | % | — | -9.01 | % | |||||||||||||||||||

| Class K shares | (w/o sales charge) | 5/15/01 | 3.51 | % | — | — | -2.13 | % | |||||||||||||||||||

| (w/ sales charge) | 5/15/01 | 2.51 | % | — | — | -2.13 | % | ||||||||||||||||||||

| S&P 500 Index | 4.91 | % | 0.55 | % | 9.07 | % | 11.0 | %* | |||||||||||||||||||

| *Since Class A shares inception | |||||||||||||||||||||||||||

All performance data quoted is historical and the results represent past performance and neither guarantee nor predict future investment results. To obtain performance data current to the most recent month (available within 7 business days of the most recent month end), please call us at (800) 221-3253 or visit our website at www.guardianinvestor.com. Current performance may be higher or lower than the performance quoted here. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost.

Total return figures are historical and assume the reinvestment of dividends and distributions and the deduction of all Fund expenses. The return figures shown do not reflect the deduction of taxes that a shareholder may pay on distributions or redemption of shares. Total return figures for Class A shares do not take into account the current maximum sales charge of 4.5%, except where noted. Total return figures for Class B, Class C and Class K shares do not take into account the contingent deferred sales charge applicable to such shares (maximum 3% for Class B shares and 1% for Class C and Class K shares), except where noted. Prior to August 25, 1988, Class A shares of the Fund were offered at a higher sales charge, so that actual returns would have been somewhat lower.

3

n The Guardian Park Avenue Fund

Annual Report

to Shareholders

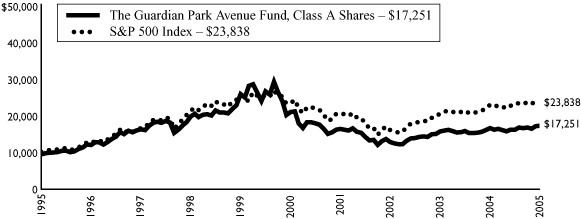

Growth of a Hypothetical $10,000 Investment

To give you a comparison, the chart below shows the performance of a hypothetical $10,000 investment made 10 years ago in Class A shares of The Guardian Park Avenue Fund and in the S&P 500 Index. The starting point of $9,550 for Class A shares reflects the current maximum sales charge 4.5%. This performance does not reflect the deduction of taxes that a shareholder may pay on distributions or redemption of shares. Returns represent past performance and are not indicative of future results. Index returns do not include the fees and expenses of the Fund, but do include the reinvestment of dividends.

Performance for Class B, Class C, and Class K shares, which were first offered on May 1, 1996, August 7, 2000, and May 15, 2001, respectively, will vary due to differences in sales load and other expenses charged to each share class.

Fund Expenses

By investing in the Fund, you incur two types of costs: (1) transaction costs, including, as applicable, sales charges on purchase payments, reinvested dividends, or other distributions; redemption fees and exchange fees; and (2) ongoing costs, including, as applicable, management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested on July 1, 2005 and held for six months ended December 31, 2005.

Actual Expenses

The first line in the table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the applicable line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

4

n The Guardian Park Avenue Fund

Annual Report

to Shareholders

Hypothetical Example for Comparison Purposes

The second line in the table provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if transactional costs were included, your costs would have been higher.

| Beginning Account Value July 1, 2005 | Ending Account Value December 31, 2005 | Expenses Paid During the Period* | Annualized Expense Ratio | ||||||||||||||||

| Class A | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,067.20 | $ | 4.74 | 0.91 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,020.62 | $ | 4.63 | 0.91 | % | |||||||||||

| Class B | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,061.50 | $ | 9.98 | 1.92 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,015.53 | $ | 9.75 | 1.92 | % | |||||||||||

| Class C | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,061.00 | $ | 10.81 | 2.08 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,014.72 | $ | 10.56 | 2.08 | % | |||||||||||

| Class K | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,065.20 | $ | 6.51 | 1.28 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,018.90 | $ | 6.36 | 1.25 | % | |||||||||||

* Expenses are equal to the Fund's annualized expense ratio for the Fund's Class A, B, C and K shares, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the Fund's most recent fiscal half-year).

5

n The Guardian UBS Large Cap Value Fund

Annual Report

to Shareholders

John Leonard,

Lead Portfolio Manager

Objective:

Seeks to maximize total return, consisting of capital appreciation and current income

Portfolio:

At least 80% in equity securities issued by companies with a large market capitalization at the time of purchase

Inception Date:

February 3, 2003

Net Assets at

December 31, 2005:

$93,599,017

An Update from Fund Management

For the year ending December 31, 2005, The Guardian UBS Large Cap Value Fund had a total return of 9.32%1 versus a return of 7.05% for its benchmark, the Russell 1000 Value Index.

Energy was the big story of 2005. During a record-setting hurricane season, Hurricanes Katrina and Rita devastated the United States' Gulf Coast, forcing the evacuation of New Orleans and shutting down a significant portion of the country's oil-refining capacity. Shortly after Katrina made landfall, oil prices jumped to a record-high $70 a barrel, while at the pump, unleaded gasoline broke the $3.00-a-gallon mark in many states. Many economic forecasters expected the worst in the wake of the hurricanes—namely, that the higher cost of energy would act as a brake on the economy—but data showed the economy to be surprisingly resilient. Unemployment, despite a spike in jobless claims related to workers displaced by the hurricanes, remained low throughout the year. Gross domestic product (GDP) growth averaged more than 3.7% for the first three quarters of 2005, inflation continued to be low, corporate earnings remained robu st and consumer confidence, after plunging in the third quarter, made up for those declines to finish the year on a high note.

During the year, the bulk of the Fund's outperformance compared to the benchmark was attributible to stock selection. On a sector level, both energy and equity REITs (in which the portfolio had an underweight position throughout the year) detracted from returns. On the other hand, the Fund's positions in construction and real property, grocery stores and medical services all contributed to returns.

Our investment research focuses on identifying discrepancies between a security's fundamental or intrinsic value and its observed market price. For each stock under our analysis we discount to the present all future cash flows that we believe will accrue to an investor, incorporating our analyst team's considerations of company management, competitive advantage and each company's core competencies. These value estimates are then compared to current market prices and ranked against the other stocks in our valuation universe. The Fund is constructed by focusing on those stocks that rank in the top 20% based on their valuation estimates and takes into account market sensitivity, common characteristic exposures and industry weightings.

1 Total return is shown for Class A shares and does not take into account the current maximum sales charge of 4.5%.

About information in this report:

• It is important to consider the Fund's investment objectives, risks, fees and expenses before investing. All funds involve some risk, including possible loss of the principal amount invested.

• Please see the "About Your Annual Report" page for a description of the Russell 1000 Value Index.

6

n The Guardian UBS Large Cap Value Fund

Annual Report

to Shareholders

Top Ten Holdings (As of 12/31/2005)

Company | Percentage of Total Net Assets | ||||||

| Citigroup, Inc. | 5.23 | % | |||||

| Wells Fargo & Co. | 4.20 | % | |||||

| Morgan Stanley | 4.15 | % | |||||

| J.P. Morgan Chase & Co. | 4.10 | % | |||||

| Exxon Mobil Corp. | 3.52 | % | |||||

| S&P Depositary Receipts Trust Series I | 3.46 | % | |||||

| American Int'l. Group, Inc. | 3.40 | % | |||||

| Marathon Oil Corp. | 3.20 | % | |||||

| Sprint Nextel Corp. | 2.88 | % | |||||

| Federal Home Loan Mortgage Corp. | 2.62 | % | |||||

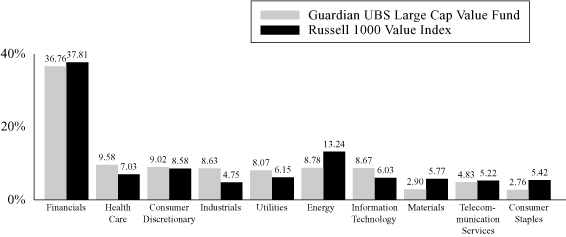

Sector Weightings vs. Index (As of 12/31/2005)

Average Annual Total Returns (For periods ended 12/31/2005)

| Inception Date | 1 Yr | 5 Yrs | 10 Yrs | Since Inception | |||||||||||||||||||||||

| Class A shares | (w/o sales charge) | 2/3/03 | 9.32 | % | — | — | 18.31 | % | |||||||||||||||||||

| (w/ sales charge) | 2/3/03 | 4.40 | % | — | — | 16.39 | % | ||||||||||||||||||||

| Class B shares | (w/o sales charge) | 2/3/03 | 8.54 | % | — | — | 17.43 | % | |||||||||||||||||||

| (w/ sales charge) | 2/3/03 | 5.54 | % | — | — | 16.92 | % | ||||||||||||||||||||

| Class C shares | (w/o sales charge) | 2/3/03 | 8.54 | % | — | — | 17.43 | % | |||||||||||||||||||

| (w/ sales charge) | 2/3/03 | 7.54 | % | — | — | 17.43 | % | ||||||||||||||||||||

| Class K shares | (w/o sales charge) | 2/3/03 | 9.02 | % | — | — | 17.98 | % | |||||||||||||||||||

| (w/ sales charge) | 2/3/03 | 8.02 | % | — | — | 17.98 | % | ||||||||||||||||||||

| Russell 1000 Value Index | 7.05 | % | — | — | 18.84 | %* | |||||||||||||||||||||

| *Since Fund's inception | |||||||||||||||||||||||||||

All performance data quoted is historical and the results represent past performance and neither guarantee nor predict future investment results. To obtain performance data current to the most recent month (available within 7 business days of the most recent month end), please call us at (800) 221-3253 or visit our website at www.guardianinvestor.com. Current performance may be higher or lower than the performance quoted here. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost.

Total return figures are historical and assume the reinvestment of dividends and distributions and the deduction of all Fund expenses. The return figures shown do not reflect the deduction of taxes that a shareholder may pay on distributions or redemption of shares. Total return figures for Class A shares do not take into account the current maximum sales charge of 4.5%, except where noted. Total return figures for Class B, Class C and Class K shares do not take into account the contingent deferred sales charge applicable to such shares (maximum 3% for Class B shares and 1% for Class C and Class K shares), except where noted.

7

n The Guardian UBS Large Cap Value Fund

Annual Report

to Shareholders

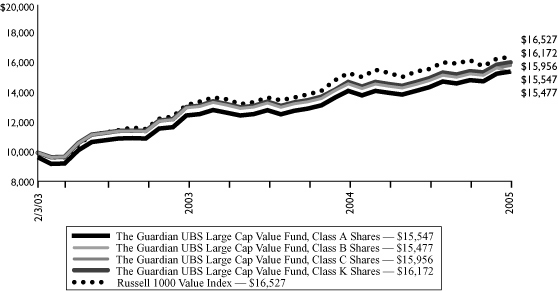

Growth of a Hypothetical $10,000 Investment

To give you a comparison, the chart below shows you the performance of a hypothetical $10,000 investment made in Class A, Class B, Class C, and Class K shares of the Fund and in the Russell 1000 Value Index. The starting point of $9,550 For Class A shares reflects the maximum sales charge of 4.5% that an investor may have to pay when purchasing Class A shares of the Fund. For Class B shares, the contingent deferred sales charge of 3% was imposed at the end of the period. The initial investment amount in the Russell 1000 Value Index, Class B, Class C and Class K shares is $10,000. This performance does not reflect the deduction of taxes that a shareholder may pay on distributions or redemption of shares. Returns represent past performance and are not indicative of future results. Index returns do not include the fees and expenses of the Fund, but do include the reinvestment of dividends.

Fund Expenses

By investing in the Fund, you incur two types of costs: (1) transaction costs, including, as applicable, sales charges on purchase payments, reinvested dividends, or other distributions; redemption fees and exchange fees; and (2) ongoing costs, including, as applicable, management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested on July 1, 2005 and held for six months ended December 31, 2005.

Actual Expenses

The first line in the table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the applicable line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

8

n The Guardian UBS Large Cap Value Fund

Annual Report

to Shareholders

Hypothetical Example for Comparison Purposes

The second line in the table provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if transactional costs were included, your costs would have been higher.

| Beginning Account Value July 1, 2005 | Ending Account Value December 31, 2005 | Expenses Paid During the Period* | Annualized Expense Ratio | ||||||||||||||||

| Class A | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,073.70 | $ | 7.53 | 1.44 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,017.95 | $ | 7.32 | 1.44 | % | |||||||||||

| Class B | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,069.10 | $ | 11.42 | 2.19 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,014.17 | $ | 11.12 | 2.19 | % | |||||||||||

| Class C | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,069.10 | $ | 11.42 | 2.19 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,014.17 | $ | 11.12 | 2.19 | % | |||||||||||

| Class K | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,072.00 | $ | 8.93 | 1.71 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,016.59 | $ | 8.69 | 1.71 | % | |||||||||||

* Expenses are equal to the Fund's annualized expense ratio for the Fund's Class A, B, C and K shares, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the Fund's most recent fiscal half-year).

9

n The Guardian Park Avenue Small Cap Fund

Annual Report

to Shareholders

Matthew Ziehl, CFA, Portfolio Manager

Objective:

Long-term growth of capital

Portfolio:

At least 85% in a diversified portfolio of common stocks issued by companies with a small market capitalization at the time of initial purchase

Inception Date:

May 1, 1997

Net Assets at

December 31, 2005:

$167,028,738

An Update from Fund Management

After five years of outperforming larger companies, small cap stocks slightly lagged their large cap peers in a lackluster overall stock market environment during 2005. The Russell 2000 Index returned 4.55% versus a 4.91% result for the S&P 500 Index. Market leadership shifted a few times during the year, with large caps outperforming in the first and fourth quarters, while smaller companies led during the second and third quarters. Within the small cap space, value stocks slightly outperformed growth stocks in 2005, as the Russell 2000 Value Index returned 4.71% versus 4.15% for the Russell 2000 Growth Index.

At the sector level, energy stocks led the market in dramatic fashion with a 2005 return of nearly 48%, while the next-best performance was by industrial stocks with a 10% gain. Most other sectors posted flat or low single digit returns, while technology and consumer discretionary lagged with 2% declines.

The Guardian Park Avenue Small Cap Fund returned -0.15%1 during 2005. Most of the underperformance was due to stock selection in healthcare, consumer discretionary and financial stocks. In particular, we had disappointing results in our biotech, media and insurance holdings within the above-mentioned sectors. Most of the individual stocks that hurt results were liquidated from the portfolio, as we did not expect near- or intermediate-term recovery in the company fundamentals. These results more than offset solidly positive selection among industrial, technology and consumer staples companies. During 2005 our sector weightings remained very close to the benchmark, consistent with our bottom-up investment process; therefore the "allocation effect" of relative sector weightings was minimal.

Our strategy is to maintain a highly diversified portfolio of quality small cap companies chosen for their individual merits by our team of experienced sector analysts. We do not attempt to predict the direction of the overall stock market, or which economic sectors will outperform or trail. Our investment process generally limits any sector over- or underweight versus benchmark to 5% of the portfolio's value; such differences arise from the "bottom-up," as a result of finding a surplus or scarcity of attractive stock ideas within a particular sector at a given point in time.

With regard to the overall portfolio, we choose from a very broad universe of companies and therefore have never experienced a shortage of attractive investment ideas at any point in time. As a "core" or "blend" small cap fund, we can select individual stocks across the spectrum from growth stocks to value stocks, as well as across industries and sectors. Our mission is to provide our investors with diversified exposure to the U.S. small cap equity market, focusing on companies with strong fundamentals and competitive positions, with the goal of seeking superior long term returns while managing risk.

1 Total return is shown for Class A shares and does not take into account the current maximum sales charge of 4.5%.

About information in this report:

• It is important to consider the Fund's investment objectives, risks, fees and expenses before investing. All funds involve some risk, including possible loss of the principal amount invested. Small-cap investing entails special risks, as small-cap stocks have tended to be more volatile and to drop more in down markets than large-cap stocks. This may happen because small companies may be limited in terms of product lines, financial resources and management.

• Please see the "About Your Annual Report" page for a description of the Russell 2000 Index,the S&P 500 Index, the Russell 2000 Value Index and the Russell 2000 Growth Index.

10

n The Guardian Park Avenue Small Cap Fund

Annual Report

to Shareholders

Top Ten Holdings (As of 12/31/2005)

Company | Percentage of Total Net Assets | ||||||

| Affiliated Managers Group, Inc. | 2.95 | % | |||||

| Benchmark Electronics, Inc. | 2.02 | % | |||||

| Varian Semiconductor Equipment Assoc., Inc. | 2.01 | % | |||||

| Informatica Corp. | 1.98 | % | |||||

| Hanover Insurance Group, Inc. | 1.83 | % | |||||

| FactSet Research Systems, Inc. | 1.82 | % | |||||

| Netlogic Microsystems, Inc. | 1.79 | % | |||||

| Redwood Trust, Inc. | 1.73 | % | |||||

| Nuveen Investments | 1.66 | % | |||||

| Internet Security Systems, Inc. | 1.64 | % | |||||

Sector Weightings vs. Index (As of 12/31/2005)

Average Annual Total Returns (For periods ended 12/31/2005)

| Inception Date | 1 Yr | 5 Yrs | 10 Yrs | Since Inception | |||||||||||||||||||||||

| Class A shares | (w/o sales charge) | 5/1/97 | -0.15 | % | 5.21 | % | — | 9.43 | % | ||||||||||||||||||

| (w/ sales charge) | 5/1/97 | -4.64 | % | 4.25 | % | — | 8.84 | % | |||||||||||||||||||

| Class B shares | (w/o sales charge) | 5/6/97 | -1.21 | % | 4.22 | % | — | 8.05 | % | ||||||||||||||||||

| (w/ sales charge) | 5/6/97 | -4.21 | % | 4.05 | % | — | 8.05 | % | |||||||||||||||||||

| Class C shares | (w/o sales charge) | 8/7/00 | -1.16 | % | 4.09 | % | — | 0.77 | % | ||||||||||||||||||

| (w/ sales charge) | 8/7/00 | -2.15 | % | 4.09 | % | — | 0.77 | % | |||||||||||||||||||

| Class K shares | (w/o sales charge) | 5/15/01 | -0.53 | % | — | — | 6.57 | % | |||||||||||||||||||

| (w/ sales charge) | 5/15/01 | -1.52 | % | — | — | 6.57 | % | ||||||||||||||||||||

| Russell 2000 Index | 4.55 | % | 8.22 | % | — | 9.46 | %* | ||||||||||||||||||||

| *Since Class A shares inception | |||||||||||||||||||||||||||

All performance data quoted is historical and the results represent past performance and neither guarantee nor predict future investment results. To obtain performance data current to the most recent month (available within 7 business days of the most recent month end), please call us at (800) 221-3253 or visit our website at www.guardianinvestor.com. Current performance may be higher or lower than the performance quoted here. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost.

Total return figures are historical and assume the reinvestment of dividends and distributions and the deduction of all Fund expenses. The return figures shown do not reflect the deduction of taxes that a shareholder may pay on distributions or redemption of shares. Total return figures for Class A shares do not take into account the current maximum sales charge of 4.5%, except where noted. Total return figures for Class B, Class C and Class K shares do not take into account the contingent deferred sales charge applicable to such shares (maximum 3% for Class B shares and 1% for Class C and Class K shares), except where noted.

11

n The Guardian Park Avenue Small Cap Fund

Annual Report

to Shareholders

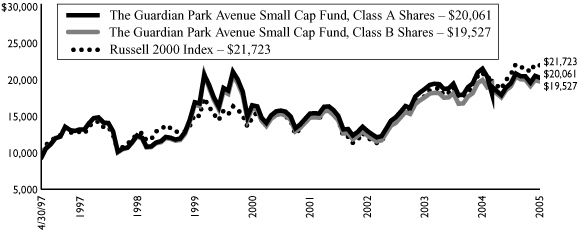

Growth of a Hypothetical $10,000 Investment

To give you a comparison, the chart below shows you the performance of a hypothetical $10,000 investment made in Class A, and Class B shares of the Fund and in the Russell 2000 Index. The starting point of $9,550 for Class A shares reflects the maximum sales charge of 4.5% that an investor may have to pay when purchasing Class A shares of the Fund. The initial investment amount in the Russell 2000 Index, and the Class B share is $10,000. This performance does not reflect the deduction of taxes that a shareholder may pay on distributions or redemption of shares. Returns represent past performance and are not indicative of future results. Index returns do not include the fees and expenses of the Fund, but do include the reinvestment of dividends.

Performance for Class C and Class K shares, which were first offered on August 7, 2000 and May 15, 2001, respectively, will vary due to differences in sales load and other expenses charged to each share class.

Fund Expenses

By investing in the Fund, you incur two types of costs: (1) transaction costs, including, as applicable, sales charges on purchase payments, reinvested dividends, or other distributions; redemption fees and exchange fees; and (2) ongoing costs, including, as applicable, management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested on July 1, 2005 and held for six months ended December 31, 2005.

Actual Expenses

The first line in the table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the applicable line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line in the table provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

12

n The Guardian Park Avenue Small Cap Fund

Annual Report

to Shareholders

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if transactional costs were included, your costs would have been higher.

| Beginning Account Value July 1, 2005 | Ending Account Value December 31, 2005 | Expenses Paid During the Period* | Annualized Expense Ratio | ||||||||||||||||

| Class A | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,040.60 | $ | 6.43 | 1.25 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,018.90 | $ | 6.36 | 1.25 | % | |||||||||||

| Class B | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,034.90 | $ | 11.34 | 2.21 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,014.06 | $ | 11.22 | 2.21 | % | |||||||||||

| Class C | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,035.20 | $ | 11.44 | 2.23 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,013.96 | $ | 11.32 | 2.23 | % | |||||||||||

| Class K | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,038.50 | $ | 8.12 | 1.58 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,017.24 | $ | 8.03 | 1.58 | % | |||||||||||

* Expenses are equal to the Fund's annualized expense ratio for the Fund's Class A, B, C and K shares, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the Fund's most recent fiscal half-year).

13

n The Guardian UBS Small Cap Value Fund

Annual Report

to Shareholders

Wilford Talbot,

Lead Portfolio Manager

Objective:

Seeks to maximize total return, consisting of capital appreciation and current income

Portfolio:

At least 80% in equity securities issued by companies with a small market capitalization at the time of initial purchase

Inception Date:

February 3, 2003

Net Assets at

December 31, 2005:

$44,692,381

An Update from Fund Management

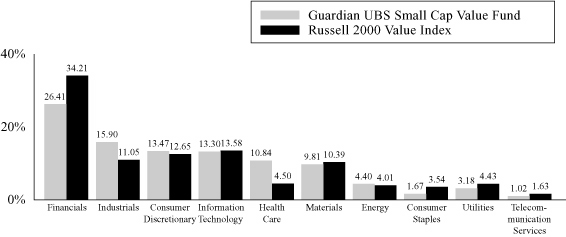

For the year ended December 31, 2005, The Guardian UBS Small Cap Value Fund had a total return of 3.70%1 versus a return of 4.71% for its benchmark, the Russell 2000 Value Index.

Energy was the big story of 2005. During a record-setting hurricane season, Hurricanes Katrina and Rita devastated the United States' Gulf Coast, forcing the evacuation of New Orleans and shutting down a significant portion of the country's oil-refining capacity. Shortly after Katrina made landfall, oil prices jumped to a record-high $70 a barrel, while at the pump, unleaded gasoline broke the $3.00-a-gallon mark in many states. Many economic forecasters expected the worst in the wake of the hurricanes—namely, that the higher cost of energy would act as a brake on the economy—but data showed the economy to be surprisingly resilient. Unemployment, despite a spike in jobless claims related to workers displaced by the hurricanes, remained low throughout the year. Gross domestic product (GDP) growth averaged more than 3.7% for the first three quarters of 2005, inflation continued to be low, corporate earnings remained robu st and consumer confidence, after plunging in the third quarter, made up for those declines to finish the year on a high note.

During the year, the bulk of the Fund's outperformance compared to the benchmark was attributible to stock selection, while industry weightings in general detracted somewhat from performance. On a sector level, equity REITs, airlines and energy reserves detracted from returns. On the other hand, the Fund's positions in securities and asset management companies, medical services and freight all contributed to returns.

Our investment research focuses on identifying discrepancies between a security's fundamental or intrinsic value and its observed market price. For each stock under our analysis we discount to the present all future cash flows that we believe will accrue to an investor, incorporating our analyst team's considerations of company management, competitive advantage, and each company's core competencies. We place particular emphasis on fundamental research conducted on-site at the companies we are covering. We utilize proprietary tools including our post-venture database/valuation system to calculate intrinsic value, and rank stocks by their relative price/intrinsic value attractiveness.

1 Total return is shown for Class A shares and does not take into account the current maximum sales charge of 4.5%.

About information in this report:

• It is important to consider the Fund's investment objectives, risks, fees and expenses before investing. All funds involve some risk, including possible loss of the principal amount invested. Small-cap investing entails special risks, as small-cap stocks have tended to be more volatile and to drop more in down markets than large-cap stocks. This may happen because small companies may be limited in terms of product lines, financial resources and management.

• Please see the "About Your Annual Report" page for a description of the Russell 2000 Value Index.

14

n The Guardian UBS Small Cap Value Fund

Annual Report

to Shareholders

Top Ten Holdings (As of 12/31/2005)

Company | Percentage of Total Net Assets | ||||||

| National Financial Partners Corp. | 2.81 | % | |||||

| Regal-Beloit Corp. | 2.72 | % | |||||

| AMR Corp. | 2.29 | % | |||||

| Coinstar, Inc. | 2.25 | % | |||||

| Cooper Cos., Inc. | 2.25 | % | |||||

| Oceaneering Int'l., Inc. | 2.15 | % | |||||

| Apollo Investment Corp. | 2.02 | % | |||||

| Colonial BancGroup, Inc. | 1.93 | % | |||||

| Equitable Resources, Inc. | 1.92 | % | |||||

| Ryland Group, Inc. | 1.82 | % | |||||

Sector Weightings vs. Index (As of 12/31/2005)

Average Annual Total Returns (For periods ended 12/31/2005)

| Inception Date | 1 Yr | 5 Yrs | 10 Yrs | Since Inception | |||||||||||||||||||||||

| Class A shares | (w/o sales charge) | 2/3/03 | 3.70 | % | — | — | 19.12 | % | |||||||||||||||||||

| (w/ sales charge) | 2/3/03 | –0.97 | % | — | — | 17.19 | % | ||||||||||||||||||||

| Class B shares | (w/o sales charge) | 2/3/03 | 2.98 | % | — | — | 18.22 | % | |||||||||||||||||||

| (w/ sales charge) | 2/3/03 | –0.02 | % | — | — | 17.72 | % | ||||||||||||||||||||

| Class C shares | (w/o sales charge) | 2/3/03 | 2.99 | % | — | — | 18.22 | % | |||||||||||||||||||

| (w/ sales charge) | 2/3/03 | 1.99 | % | — | — | 18.22 | % | ||||||||||||||||||||

| Class K shares | (w/o sales charge) | 2/3/03 | 3.56 | % | — | — | 18.95 | % | |||||||||||||||||||

| (w/ sales charge) | 2/3/03 | 2.56 | % | — | — | 18.95 | % | ||||||||||||||||||||

| Russell 2000 Value Index | 4.71 | % | — | — | 25.36 | %* | |||||||||||||||||||||

| *Since Class A shares inception | |||||||||||||||||||||||||||

All performance data quoted is historical and the results represent past performance and neither guarantee nor predict future investment results. To obtain performance data current to the most recent month (available within 7 business days of the most recent month end), please call us at (800) 221-3253 or visit our website at www.guardianinvestor.com. Current performance may be higher or lower than the performance quoted here. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost.

Total return figures are historical and assume the reinvestment of dividends and distributions and the deduction of all Fund expenses. The return figures shown do not reflect the deduction of taxes that a shareholder may pay on distributions or redemption of shares. Total return figures for Class A shares do not take into account the current maximum sales charge of 4.5%, except where noted. Total return figures for Class B, Class C and Class K shares do not take into account the contingent deferred sales charge applicable to such shares (maximum 3% for Class B shares and 1% for Class C and Class K shares), except where noted.

15

n The Guardian UBS Small Cap Value Fund

Annual Report

to Shareholders

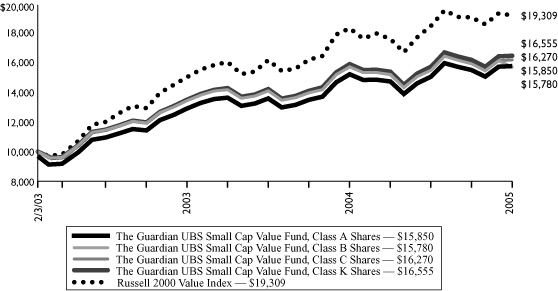

Growth of a Hypothetical $10,000 Investment

To give you a comparison, the chart below shows you the performance of a hypothetical $10,000 investment made in Class A, Class B and Class C shares of the Fund and in the Russell 2000 Value Index. The starting point of $9,550 for Class A shares reflects the maximum sales charge of 4.5% that an investor may have to pay when purchasing Class A shares of the Fund. For Class B shares, the contingent deferred sales charge of 3% was imposed at the end of the period. The initial investment amount in the S&P 500 Index, Class B and Class C shares is $10,000. This performance does not reflect the deduction of taxes that a shareholder may pay on distributions or redemption of shares. Returns represent past performance and are not indicative of future results. Index returns do not include the fees and expenses of the Fund, but do include the reinvestment of dividends.

Fund Expenses

By investing in the Fund, you incur two types of costs: (1) transaction costs, including, as applicable, sales charges on purchase payments, reinvested dividends, or other distributions; redemption fees and exchange fees; and (2) ongoing costs, including, as applicable, management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested on July 1, 2005 and held for six months ended December 31, 2005.

Actual Expenses

The first line in the table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the applicable line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

16

n The Guardian UBS Small Cap Value Fund

Annual Report

to Shareholders

Hypothetical Example for Comparison Purposes

The second line in the table provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if transactional costs were included, your costs would have been higher.

| Beginning Account Value July 1, 2005 | Ending Account Value December 31, 2005 | Expenses Paid During the Period* | Annualized Expense Ratio | ||||||||||||||||

| Class A | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,048.80 | $ | 9.92 | 1.92 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,015.53 | $ | 9.75 | 1.92 | % | |||||||||||

| Class B | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,045.00 | $ | 13.81 | 2.68 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,011.70 | $ | 13.59 | 2.68 | % | |||||||||||

| Class C | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,045.10 | $ | 13.87 | 2.69 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,011.64 | $ | 13.64 | 2.69 | % | |||||||||||

| Class K | |||||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,048.20 | $ | 10.63 | 2.06 | % | |||||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,014.82 | $ | 10.46 | 2.06 | % | |||||||||||

* Expenses are equal to the Fund's annualized expense ratio for the Fund's Class A, B, C and K shares, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the Fund's most recent fiscal half-year).

17

n The Guardian Asset Allocation Fund

Annual Report

to Shareholders

Jonathan C. Jankus, CFA, Co-Portfolio Manager

Stewart Johnson, Co-Portfolio Manager

Objective:

Long- term total investment return consistent with moderate investment risk

Portfolio:

Generally purchases shares of The Guardian S&P 500 Index, The Guardian Park Avenue, The Guardian Investment Quality Bond and/or The Guardian Cash Management Funds. Also invests in individual securities and uses futures to manage allocations among the equity, debt and money market asset classes

Inception Date:

February 16, 1993

Net Assets at

December 31, 2005:

$137,621,022

An Update from Fund Management

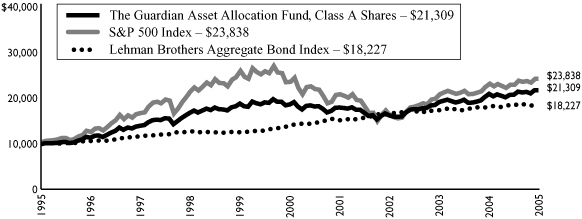

For the year ended December 31, 2005, the Fund's return was 3.91%1 placing it below the average 5.63% return of 378 funds with similar objectives and policies in the Lipper universe. During this period, the Fund's return also slightly lagged the 4.00% return experienced by its not-quite-passive composite benchmark (60% of the S&P 500 Index and 40% of the Lehman Aggregate Bond Index rebalanced monthly without expenses or trading costs). Since its inception on February 16, 1993, the Fund's average annual total return of 8.50% places it behind the annualized return of 9.21% experienced by its composite benchmark.

Stock market returns were positive for a third straight year, with the S&P 500 Index earning a modest total return of 4.91% for 2005. That said, the market's returns for 2001 and 2002 were so poor that the cumulative return on the S&P 500 Index, including dividends, for the five-year period ended December 31, 2005 has only been a modest 0.54% average per year. Over this period, the market has had to deal with volatility due to corporate malfeasance, a mixed economy, the continuing threat of terrorist attacks, a war and record-setting natural disasters.

The Fund's performance was positively impacted by a correctly aggressive stance on the market. After the declines of 2000, 2001 and the first half of 2002, our models viewed the market as being extremely "cheap" relative to fixed income alternatives. In addition, the turnaround in the economy led to a pronounced rebound in corporate profitability.

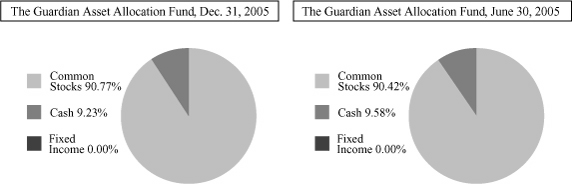

Our investing was guided by our quantitative model which, as of year-end, has us invested 91% in stocks, 0% in bonds and 9% in cash. This compares to our "neutral" position of 60% stocks and 40% bonds.

We believe most signs indicate continuing economic growth, which we hope will continue to feed a rebound in corporate profits. A risk on the horizon is the extent to which interest rates will rise in the near term, especially given such exogenous factors as expensive oil and continued violence in the Middle East. "Real" interest rates (interest rates after subtracting expected inflation) remain relatively low, although not as low as they were two years ago. On balance, we remain optimistic, albeit a bit more cautiously so.

1 Total return is shown for Class A shares and does not take into account the current maximum sales charge of 4.5%.

About information in this report:

• It is important to consider the Fund's investment objectives, risks, fees and expenses before investing. All funds involve some risk, including possible loss of the principal amount invested.