Filed by Aixtron Aktiengesellschaft pursuant to

Rule 425 under the Securities Act of 1933 and

deemed filed pursuant to Rule 14a-12 under

the Securities Exchange Act of 1934

Subject Company: Genus, Inc.

Subject Company’s Exchange Act File No.: 0-17139

AIXTRON TRANSACTION ROADSHOW 02 July, 2004 1

Thomas Swan Scientific Equipment

will contain impor- the SEC by The proxy California 94089, telephone (408) 747-

Transaction

This Drive, Sunnyvale, 2 The proxy statement/prospectus will be filed with Thomas Swan Scientific Equipment information. Relations at 1139 Karlstad Information About AIXTRON plans to file a registration statement on Form F-4 with the U.S. Securities and Exchange Commission, or SEC, which will include a prospectus of AIXTRON and a proxy statement of Genus. Investors and security holders are urged to read the proxy statement/prospectus regarding the business combination transaction referenced in the foregoing information, when it becomes available, because it tant AIXTRON. Investors and security holders may obtain a free copy of the proxy statement/prospectus (when it becomes available) and other documents filed by AIXTRON and Genus with the SEC at the SEC’s website at www.sec.gov. statement/prospectus (when it is available) and these other documents may also be obtained for free from AIXTRON or Genus by directing a request to AIXTRON Investor Relations at Kackertstr.15-17, 52072 Aachen, +39 241 8909 444 or Genus Investor 7120.

Additional information filed with the U.S. This document is

(408) 747-7120.

Transaction and Genus described herein. 3 in this and its directors and executive officers may be deemed to be participants in Information regarding the special interests of these directors and executive the merger transaction described herein will be included in the proxy and from Genus by contacting Genus Investor Relations at 1139 Karlstad Thomas Swan Scientific Equipment Participants Aixtron the solicitation of proxies from the shareholders of Genus in connection with the merger. officers in the merger will be included in the proxy statement/prospectus of Aixtron and Genus described herein. Genus and its directors and executive officers may be deemed to be participants in the solicitation of proxies from the shareholders of Genus in connection with the merger. Information regarding the special interests of these directors and executive officers in statement/prospectus of Aixtron regarding these directors and executive officers is also included in Genus’ proxy statement for its 2004 Annual Meeting of Shareholders, which was Securities and Exchange Commission on or about April 28,

2004. available free of charge at the U.S. Securities and Exchange Commission’s web site at www.sec.gov Drive, Sunnyvale, California 94089, telephone

and and variations of and Genus businesses will and and “estimates,” These statements are not guarantees of or Genus shareholders to approve sections, and its Current Reports the date hereof and Aixtron provisions of the Private Securities Litigation “believes,” In any forward-looking statement in which Any reference to the Internet website of Aixtron “plans,” Therefore, actual outcomes and results may differ materially consummated.

“intends,”

Information 4

“anticipates,”

AG and Genus, Inc. within the meaning of the “safe harbor” Words such as “expects,” For example, if either of the companies do not receive required shareholder approvals or fail to or Genus expresses an expectation or belief as to future results, such expectation or belief is expressed in good faith Actual operating results may differ materially from such forward-looking statements and are The forward-looking statements contained in this news release are made as of Thomas Swan Scientific Equipment Forward Looking This presentation may contain forward-looking statements about the financial conditions, results of operations and earnings outlook of Aixtron Reform Act of 1995. these words and similar expressions, identify these forward-looking statements. future performance, involve certain risks, uncertainties and assumptions that are difficult to predict, and are based upon assumptions as to future events that may not prove accurate. from what is expressed herein. satisfy other conditions to closing, the transaction will not be Aixtron and believed to have a reasonable basis, but there can be no assurance that the statement or expectation or belief will result or be achieved or accomplished. subject to certain risks, including risks arising from: actual customer orders received by the companies; the extent to which MOCVD and ALD technology is demanded by the market place; the actual number of customer orders received by the companies; the timing of final acceptance of products by customers; the financial climate and accessibility of financing, general conditions in the thin film equipment market and in the macro-economy; cancellations, rescheduling or delays in product shipments; manufacturing capacity constraints; lengthy sales and qualification cycles; difficulties in the production process; changes in semiconductor industry growth; increased competition; delays in developing and commercializing new products; general economic conditions being less favorable than expected; the risk that the Aixtron not be integrated successfully; costs related to the proposed merger; failure of the Aixtron the proposed merger or the failure of other conditions to the proposed merger to be satisfied; and other factors, including those set forth in Genus’s filings with the U.S. Securities and Exchange Commission, including its Annual Report on Form 10- K for its most recent fiscal year and its most recent Quarterly Report on Form 10-Q, particularly in the “Risk Factors” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” on Form 8-K. Genus do not

assume any obligation to (and expressly disclaim any such obligation to) update the reasons why actual results could differ materially from those projected in the forward-looking statements. or Genus is not an incorporation by reference of such information in this presentation, and you should not interpret such a reference as an incorporation by reference of such information.

• Benefits

• Profile Customers 5 AGENDA Profile / Transaction Overview Markets Swan Equipment Company Summary of

• Company / Thomas Scientific

• Transaction AIXTRON GENUS Products Financial Summary

• • • • •

AIXTRON 6

Transaction Overview Thomas Swan Scientific Equipment

for one Genus share

(American Depository Receipts) on NASDAQ 7

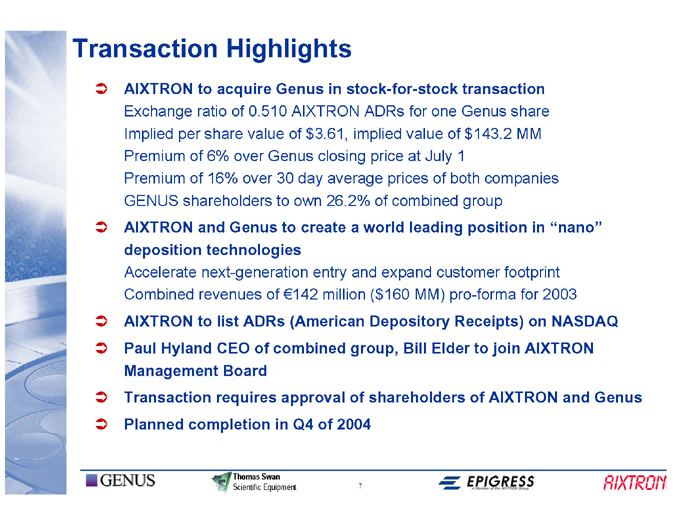

AIXTRON to acquire Genus in stock-for-stock transaction Exchange ratio of 0.510 AIXTRON ADRs Implied per share value of $3.61, implied value of $143.2 MM Premium of 6% over Genus closing price at July 1 Premium of 16% over 30 day average prices of both companies GENUS shareholders to own 26.2% of combined group AIXTRON and Genus to create a world leading position in “nano” deposition technologies Accelerate next-generation entry and expand customer footprint Combined revenues of million ($160 MM) pro-forma for 2003 AIXTRON to list ADRs Paul Hyland CEO of combined group, Bill Elder to join AIXTRON Management Board Transaction requires approval of shareholders of AIXTRON and Genus Planned completion in Q4 of 2004 Thomas Swan Scientific Equipment

Transaction Highlights

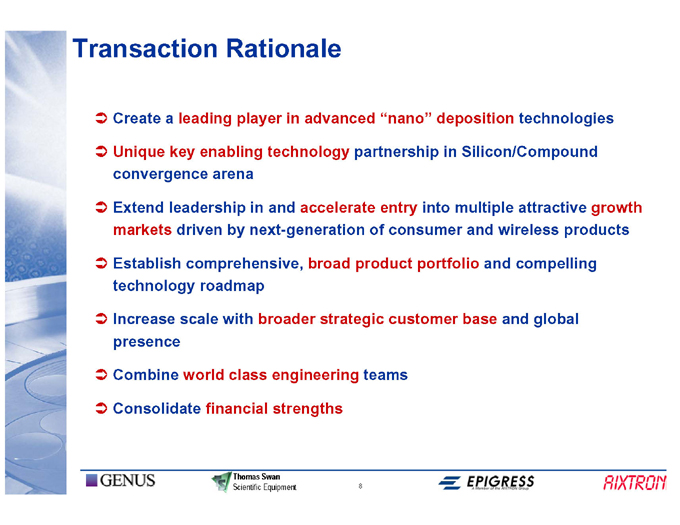

technologies and compelling and global deposition into multiple attractive growth teams partnership in Silicon/Compound 8 Create a leading player in advanced “nano” driven by next-generation of consumer and wireless products Thomas Swan Scientific Equipment Unique key enabling technology convergence arena Extend leadership in and accelerate entry markets Establish comprehensive, broad product portfolio technology roadmap Increase scale with broader strategic customer base presence Combine world class engineering Consolidate financial strengths

Transaction Rationale

AIXTRON Company Profile 9

Thomas Swan Scientific Equipment

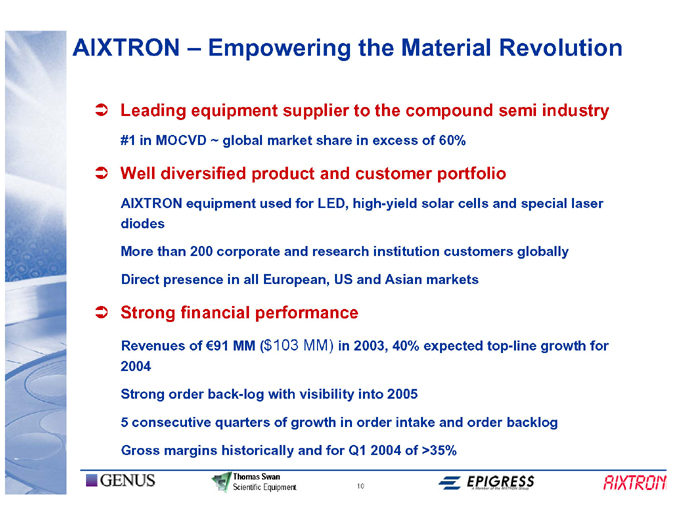

in 2003, 40% expected top-line growth for 10 $103 MM)

Empowering the Material Revolution Gross margins historically and for Q1 2004 of >35% Thomas Swan Scientific Equipment Leading equipment supplier to the compound semi industry #1 in MOCVD ~ global market share in excess of 60% Well diversified product and customer portfolio AIXTRON equipment used for LED, high-yield solar cells and special laser diodes More than 200 corporate and research institution customers globally Direct presence in all European, US and Asian markets Strong financial performance Revenues of MM ( 2004 Strong order back-log with visibility into 2005 5 consecutive quarters of growth in order intake and order backlog

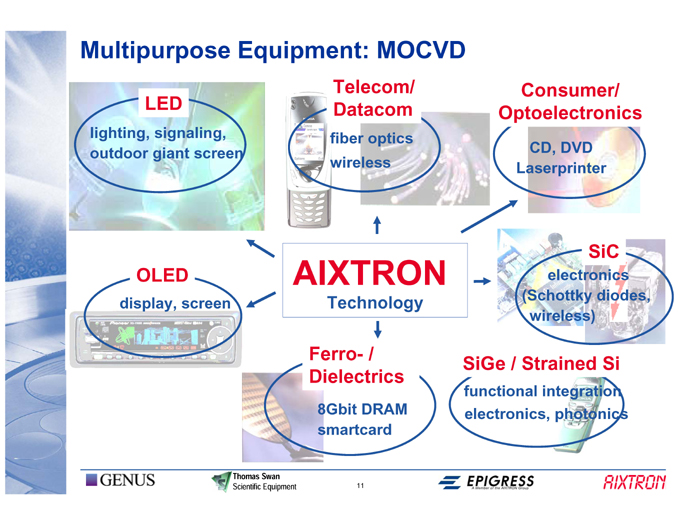

AIXTRON –

SiC electronics diodes, Si integration Consumer/ Optoelectronics CD, DVD Laserprinter (Schottky wireless) / Strained electronics, photonics SiGe functional optics

Telecom/ Datacom fiber wireless AIXTRON Technology Ferro- / Dielectrics 8Gbit DRAM smartcard 11

Thomas Swan Scientific Equipment

screen

LED lighting, signaling, giant OLED display, screen

Multipurpose Equipment: MOCVD outdoor

diodes,

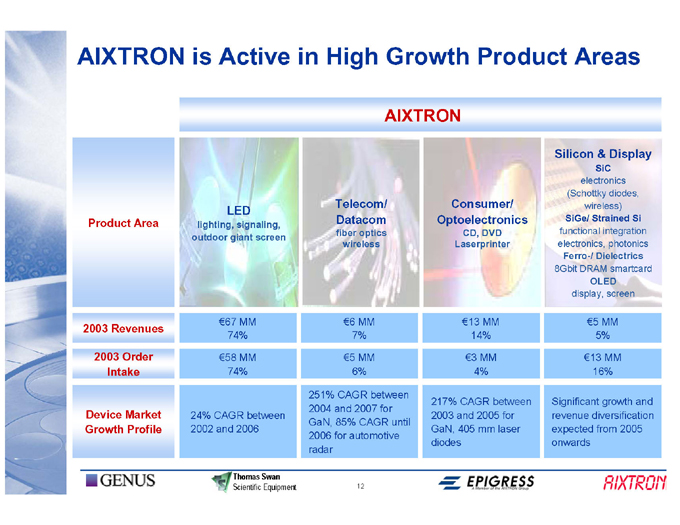

Silicon & Display SiC electronics (Schottky wireless) SiGe/ Strained Si functional integration electronics, photonics Ferro-/ Dielectrics 8Gbit DRAM smartcard OLED display, screen MM 5% MM 16%

Significant growth and revenue diversification expected from 2005 onwards Consumer/ Optoelectronics CD, DVD Laserprinter MM 14% MM 4% CAGR between mm laser AIXTRON 217% 2003 and 2005 for GaN, 405 diodes

Telecom/ Datacom fiber optics wireless MM 7% MM 6% 2004 and 2007 for 12 251% CAGR between GaN, 85% CAGR until 2006 for automotive radar is Active in High Growth Product Areas LED lighting, signaling, outdoor giant screen MM 74% MM 74% 24% CAGR between 2002 and 2006 Thomas Swan Scientific Equipment

AIXTRON Product Area 2003 Revenues 2003 Order Intake Device Market Growth Profile

07 07

06 06

05 05

CVD 04

04 & SSi

03

SiC Equipment 03 YEAR

YEAR Epitaxy 02

02 SiGe Equipment

01

01

00

00 99

99 98

98 500 400 300 200 100 0

40 30 20 10 0

.

SiC CVD TAM [Mio. $] SiGe & StrSi CVD TAM [Mio.

07

06 07

05 06

05

04 04

Compound Equipment 03 03 Semiconductor YEAR 02 YEAR

02 01 13

DRAM 00

01 Technology High-k 99

00 98

300 250 200 150 100 50 0

99

.

98 AIXTRON High-k DRAM CVD TAM [Mio. $

0

500 400 300 200 100 07

06 Thomas Swan Scientific Equipment

TAM [Mio. $] MOCVD CS 07

05 06 04 05 03

04 YEAR

02

03 YEAR

02 01

01 00

OLED equip. 00 CMOS Gate Stack 99 front-end 99 98

98 200 150 100 50 0 600 500 400 300 200 100 0 . [Mio. High-k CMOS CVD TAM

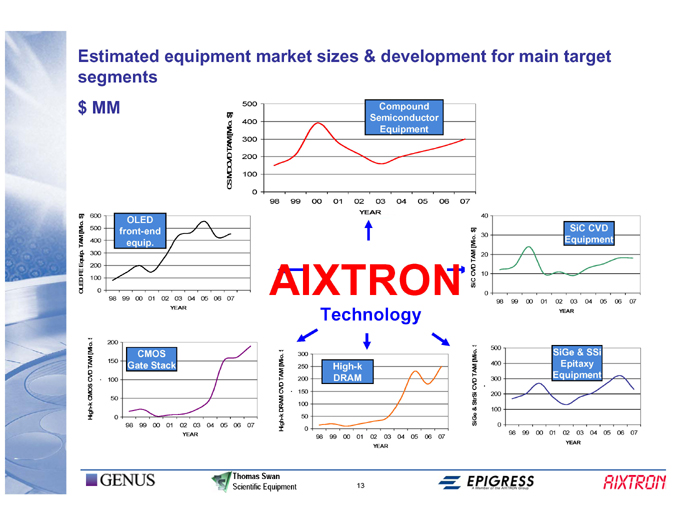

Estimated equipment market sizes & development for main target segments $ MM [Mio. $] FE Equip. TAM OLED

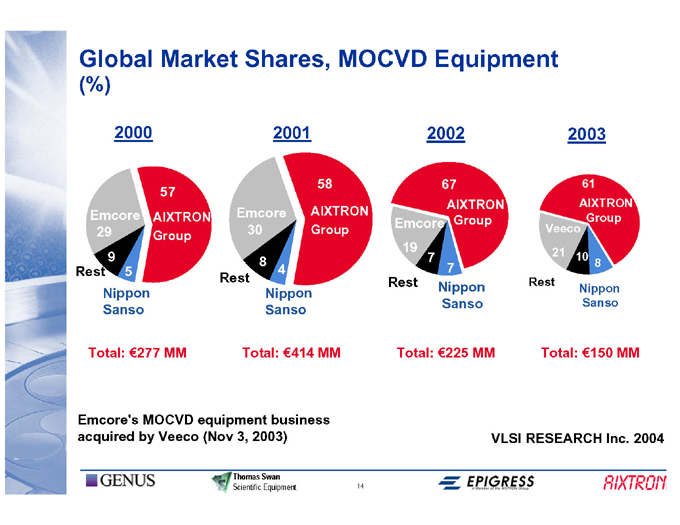

Group 8 Sanso 2003 61 AIXTRON 10 Nippon

Veeco 21 Total: MM

Rest VLSI RESEARCH Inc. 2004

Group

67 AIXTRON 7 Nippon Sanso

2002 7

Emcore 19 Rest Total: MM

14

58

AIXTRON Group n o p o s p n i a

4

2001 N S

8

Emcore 30 Total: MM Thomas Swan Scientific Equipment

Rest (Nov 3, 2003)

57 AIXTRON Group n MOCVD equipment business o p o s 5 p n

2000 i a

9 N S

Global Market Shares, MOCVD Equipment (%) Emcore 29 Rest Total: MM Emcore’s acquired by Veeco

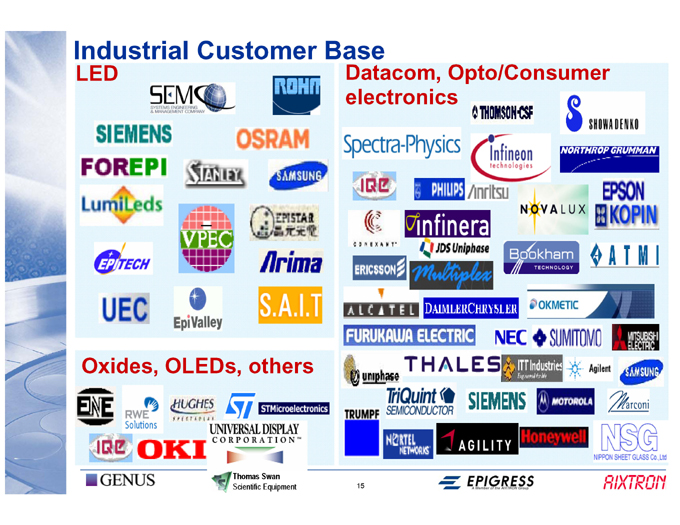

Datacom, Opto/Consumer electronics 15 Oxides, OLEDs, others Thomas Swan Scientific Equipment

Industrial Customer BaseLED

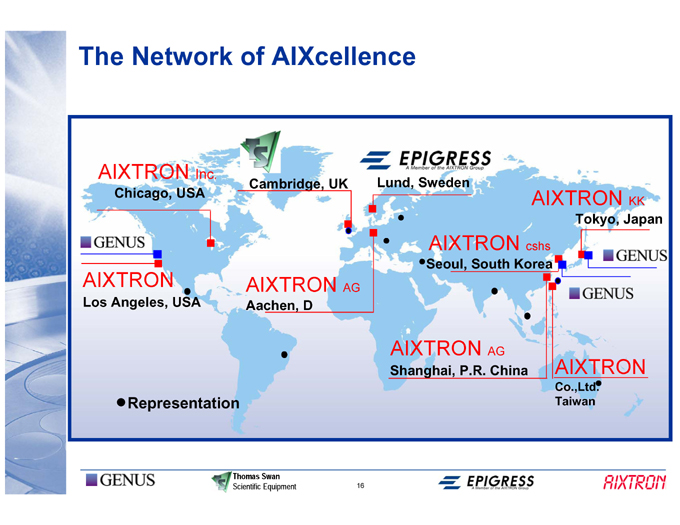

KK Tokyo, Japan

AIXTRON AIXTRON Co.,Ltd. Taiwan

cshs

AIXTRON Seoul, South Korea AG Lund, Sweden AIXTRON Shanghai, P.R. China

16

AG

Cambridge, UK AIXTRON Aachen, D Thomas Swan Scientific Equipment

Inc. Representation

The Network of AIXcellence AIXTRON Chicago, USA AIXTRON Los Angeles, USA

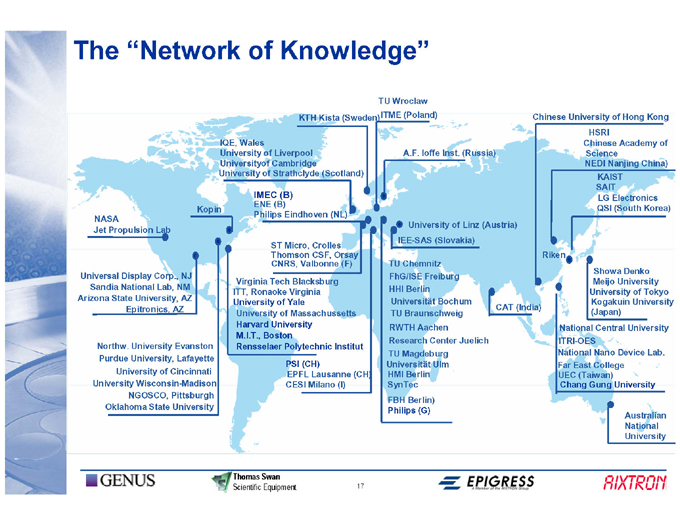

Kong of China) University Lab. Australian University LG Electronics Denko University Device University National HSRI Chinese Academy Science NEDI Nanjing KAIST SAIT QSI (South Korea) Showa Meijo University of Tokyo Kogakuin (Japan) Gung National Central University ITRI-OES National Nano Far East College UEC (Taiwan) Chang Chinese University of Hong Riken CAT (India) Inst. (Russia) University of Linz (Austria) A.F. Ioffe IEE-SAS (Slovakia) TU Chemnitz FhG/ISE Freiburg HHI Berlin Bochum TU Braunschweig RWTH Aachen Research Center Juelich TU Magdeburg HMI Berlin FBH Berlin) TU Wroclaw ITME (Poland) Ulm SynTec Philips (G)

(Sweden) 17 (Scotland) (F) Institut KTH Kista Blacksburg Virginia Polytechnic PSI (CH) EPFL Lausanne (CH) CESI Milano (I) Cambridge IMEC (B) Philips Eindhoven (NL) ST Micro, Crolles Thomson CSF, OrsayCNRS, Valbonne ENE (B) Virginia Tech ITT, Ronaoke University of Yale University of Massachussetts Harvard University M.I.T., Boston Rensselaer Thomas Swan Scientific Equipment IQE, Wales University of Liverpool Universityof University of Strathclyde Kopin Lab National Lab, NM Epitronics, AZ University, Lafayette University of Cincinnati NGOSCO, Pittsburgh Oklahoma State University The “Network of Knowledge” NASA Jet Propulsion Universal Display Corp., NJ Sandia Arizona State University, AZ Northw. University Evanston Purdue University Wisconsin-Madison

18

Core Strategies Enabling technology partner in emerging markets Maintain a strong Balance Sheet, Minimize risk and create value for Thomas Swan Scientific Equipment Maintain a pure play in core competency: Deposition technology engineering delivering customized system solutions for compound semiconductor & complex materials Technology & market leadership: Continuous improvement of technology and market position Diversification of target applications: Leverage AIXTRON technology for new materials and new sectors creating additional growth potential Market positioning: Equity strength: our stakeholders

AIXTRON

Company Profile 19

Thomas Swan Scientific Equipment

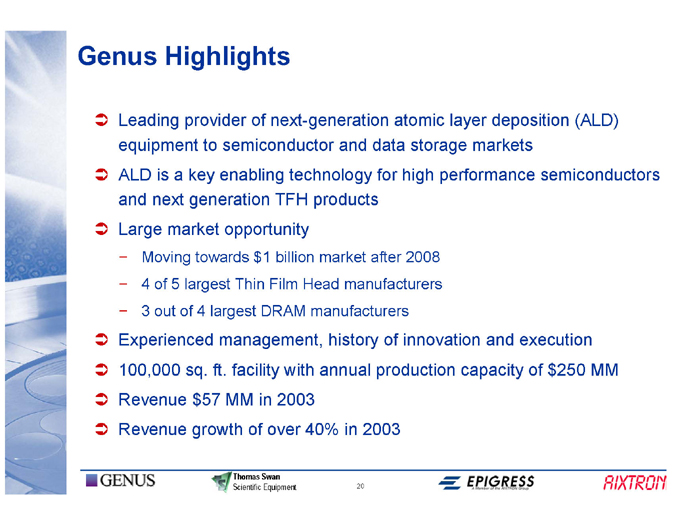

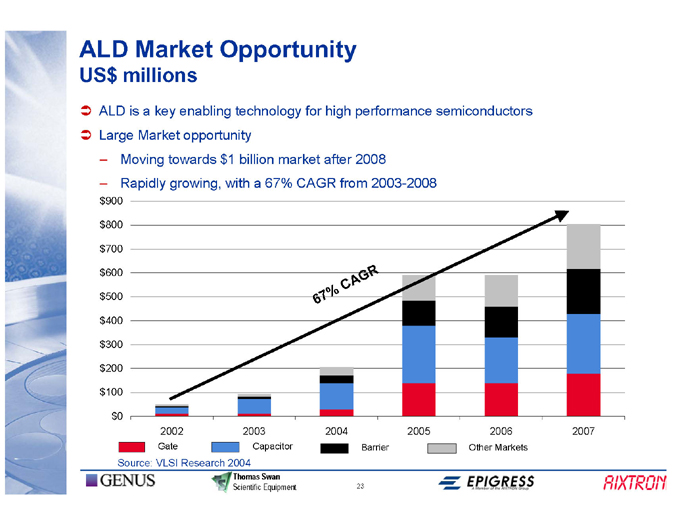

• (ALD) MM semiconductors $250 deposition execution of markets and capacity layer performance atomic storage high 2008 innovation data for after of production 2003

• 20

• and products market manufacturers manufacturers history annual in technology Head 40% next-generation TFH billion with 2003

• Film DRAM over Swan Equipment

• $1 in of Thin facility of Thomas Scientific semiconductor enabling opportunity management, MM largest ft. to provider key generation towards largest 4 sq. $57 growth of

• Highlights a market 5

• is next of out Moving 4 3

• Leading equipment ALD and Large Experienced 100,000 Revenue Revenue

• Genus

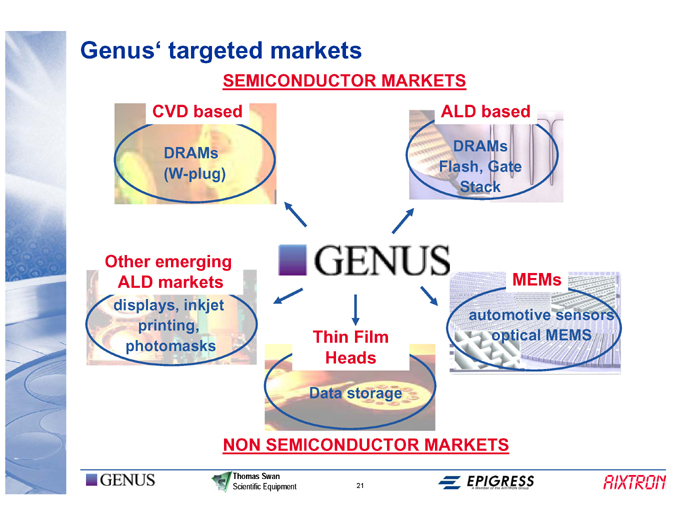

MEMs automotive sensors optical MEMS ALD based DRAMs Flash, Gate Stack

Thin Film Heads Data storage 21 targeted markets SEMICONDUCTOR MARKETS NON SEMICONDUCTOR MARKETS Thomas Swan Scientific Equipment

CVD based DRAMs (W-plug) Other emerging ALD markets displays, inkjet printing, photomasks

Genus’

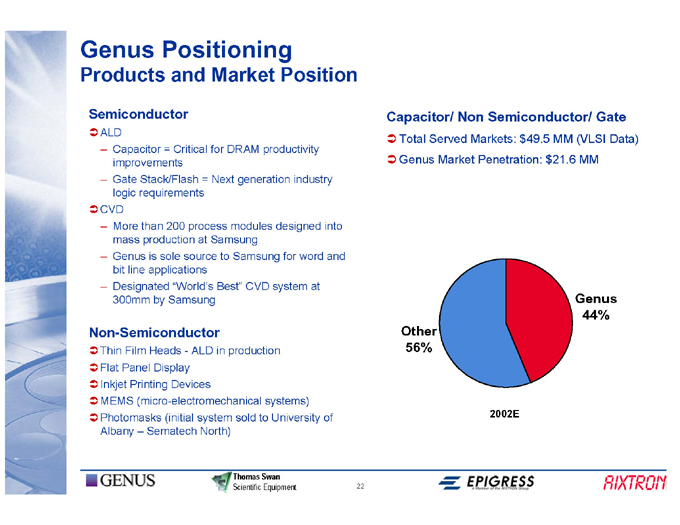

• Gate Data)

• (VLSI MM Genus 44%

• MM $21.6 $49.5

• Semiconductor/ Markets: Penetration: 2002E Non Market Served Total Genus Other 56%

• Capacitor/

• 22

• into and of industry word at

• Position productivity designed for system systems) University Equipment

• to Swan

• DRAM generation modules Samsung CVD production sold Thomas Scientific Market Next to Best” in for Samsung = process at ALD system North) and Critical source “World’s Samsung - Devices Positioning = 200 sole Display (initial by Heads Stack/Flash requirements than production is applications Sematech line Film Panel Printing (micro-electromechanical –Capacitor improvements Gate logic More mass Genus bit Designated 300mm ALD – – CVD – – Thin Flat Inkjet MEMS Photomasks Albany

• Genus Products Semiconductor Non-Semiconductor

• 2007

• 2006 Markets

• semiconductors Other 2003-2008 2005

• R Barrier

• performance 2008 from G A 23 high after C 2004

• %

• 7

• for market CAGR 6

• 67% Swan Equipment

• technology billion a 2003 Capacitor Thomas Scientific with 2004 Opportunity opportunity $1 enabling towards growing, Research

• key 2002 Gate VLSI

• Market a Market millions is Moving Rapidly Source:

• $900 $800 $700 $600 $500 $400 $300 $200 $100 $0

• ALD Large –

• ALD US$

GENUS

24

AIXTRON - Products/ Markets/ Customers Thomas Swan Scientific Equipment

25

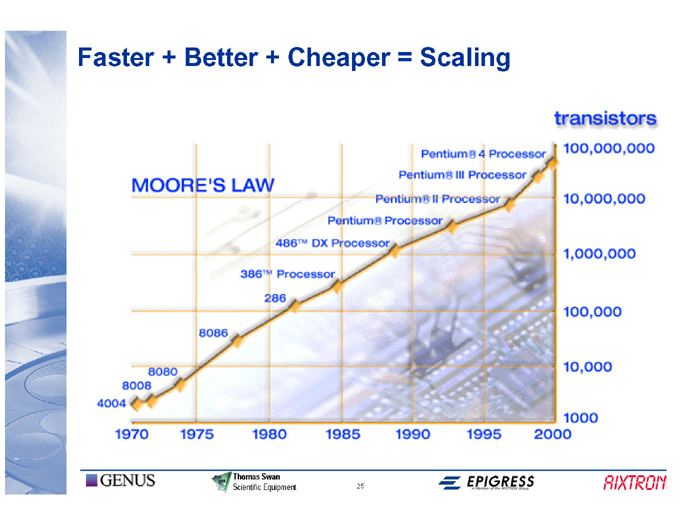

Faster + Better + Cheaper = Scaling Thomas Swan Scientific Equipment

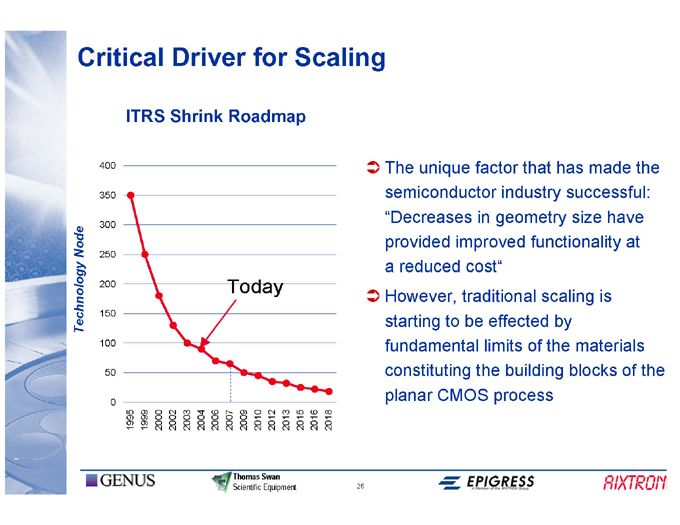

The unique factor that has made the semiconductor industry successful: “Decreases in geometry size have provided improved functionality at a reduced cost” However, traditional scaling is starting to be effected by fundamental limits of the materials constituting the building blocks of the planar CMOS process

26

2018 2016 2015 2013 2012 2010

Today 2009 Thomas Swan Scientific Equipment

2007 2006 2004 2003 2002 2000

ITRS Shrink Roadmap 1999

1995

Critical Driver for Scaling 400 350 300 250 200 150 100 50 0

Technology Node

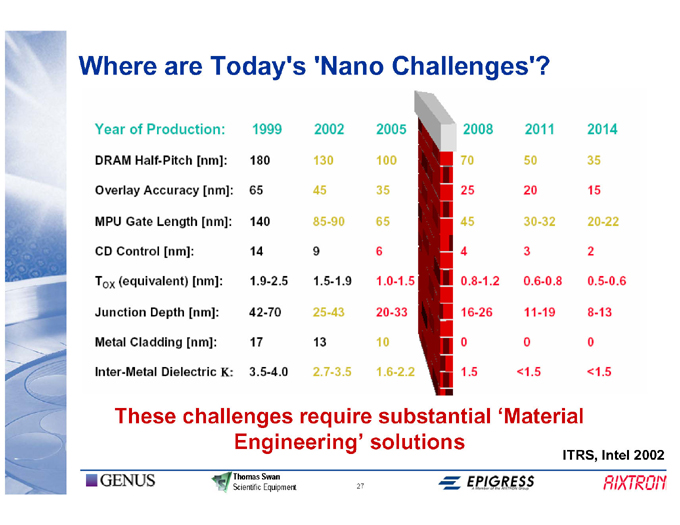

ITRS, Intel 2002

Challenges’? solutions

Engineering’ 27 Where are Today’s ‘Nano These challenges require substantial ‘Material Thomas Swan Scientific Equipment

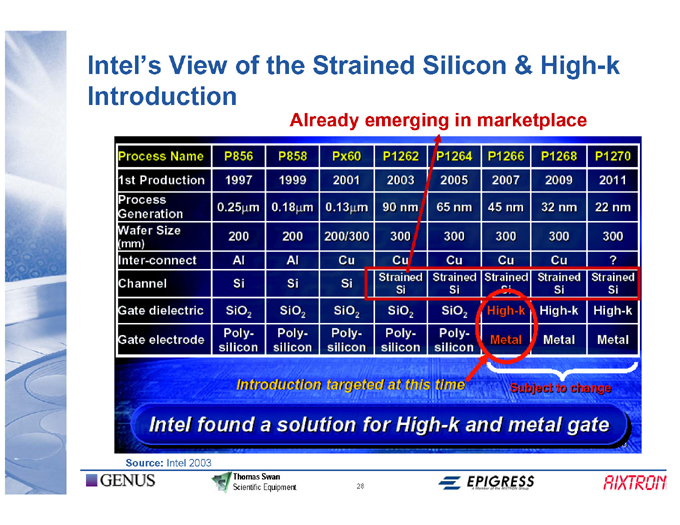

Already emerging in marketplace 28

Thomas Swan Scientific Equipment

Intel 2003

Intel’s View of the Strained Silicon & High-k Introduction Source:

GaN Transition layer Si wafer

r

f e a

w 29

i

S cost and infrastructure

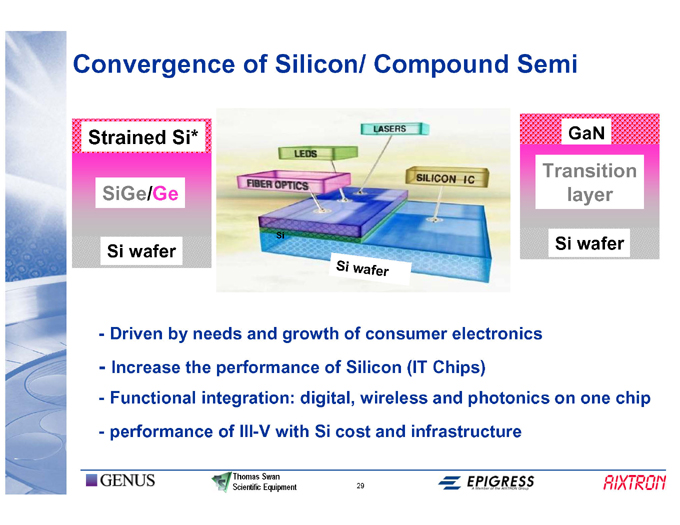

Si

Driven by needs and growth of consumer electronics Increase the performance of Silicon (IT Chips) Functional integration: digital, wireless and photonics on one chip performance of III-V with Si Thomas Swan Scientific Equipment

SiGe/Ge Si wafer

Convergence of Silicon/ Compound Semi Strained Si* - - - -

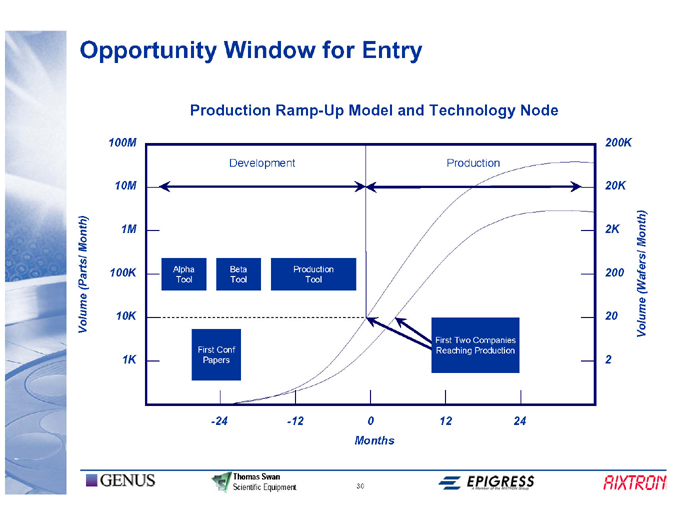

Month) (Wafers/ Volume

200K 20K 2K 200 20 2

24

Production

First Two Companies Reaching Production 12

0

Months 30

Production Tool

-12

Development Beta Tool Thomas Swan Scientific Equipment

Production Ramp-Up Model and Technology Node First Conf Papers -24

Alpha Tool

Opportunity Window for Entry 100M 10M 1M 100K 10K 1K

Month) (Parts/ Volume

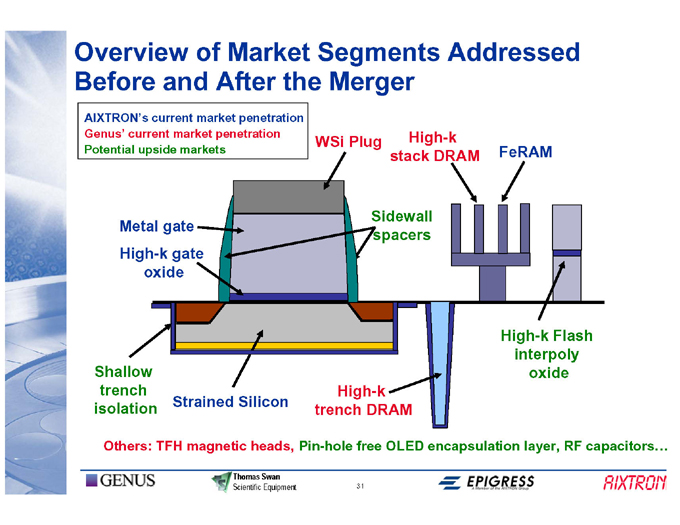

FeRAM High-k Flash interpoly oxide High-k stack DRAM

Sidewall spacers

Plug High-k 31

WSi trench DRAM Pin-hole free OLED encapsulation layer, RF capacitors…

current market penetration Strained Silicon Thomas Swan Scientific Equipment

current market penetration Metal gate High-k gate oxide Others: TFH magnetic heads,

Overview of Market Segments Addressed Before and After the Merger AIXTRON’s Genus’ Potential upside markets Shallow trench isolation

semiconductor processes

32

of New Entity Uniquely positioned to enable scalability requirements for semiconductor industry Core strengths in material knowledge and nanoscale Thomas Swan Scientific Equipment

Leading supplier of enabling technology Multiple markets provide stable growth platform Comprehensive, very competitive product portfolio in deposition equipment Broad customer base seeking stronger, fewer suppliers with ability to partner strategically/ align roadmaps Enhanced critical mass allowing a deeper customer penetration and continued investment in new products More than 20 years successful track record of complex material deposition on an atomic level and more than 60 years collective experience (AIXTRON, Genus, Thomas Swan)

Strength

33

Combination would allow increased and/or accelerated penetration technologies aligned to strategic customer needs Thomas Swan Scientific Equipment Customers seeking fewer, broader, independent suppliers with strong technology portfolios and financial strength to strategically align product raodmaps Combined companies will provide customers with a comprehensive product portfolio and compelling, synergistic technology roadmap of key accounts Increased scale would allow for continued investment in new

Customer Impact

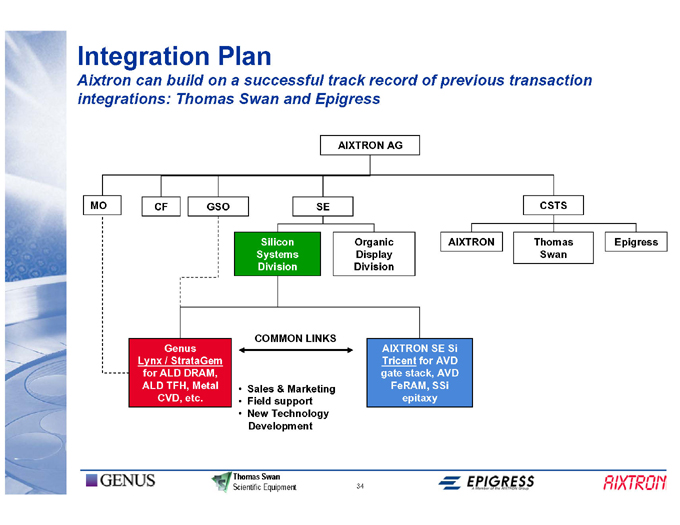

• Epigress transaction CSTS Thomas Swan previous AIXTRON Si SE AVD AVD SSi of for stack, FeRAM, epitaxy record AG AIXTRON Tricent gate track AIXTRON Organic Display Division 34 Epigress SE LINKS Marketing

• and

• & support Technology Equipment Silicon Systems Division COMMON Sales Field Development Swan

• successful New

• Swan • • Thomas Scientific

• Plan a

• on GSO Metal build Thomas StrataGem DRAM, etc.

• Genus / ALD TFH, CVD, CF can Lynx for ALD

• Integration Aixtron integrations: MO

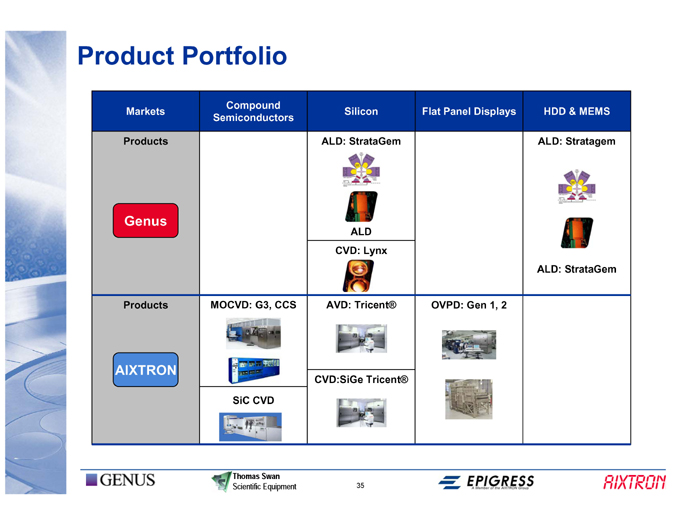

HDD & MEMS ALD: Stratagem ALD: StrataGem Flat Panel Displays OVPD: Gen 1, 2

Silicon ALD: StrataGem ALD CVD: Lynx AVD: CVD:SiGe 35

CVD Thomas Swan Scientific Equipment

Compound Semiconductors MOCVD: G3, CCS SiC Product Portfolio Markets Products Genus Products AIXTRON

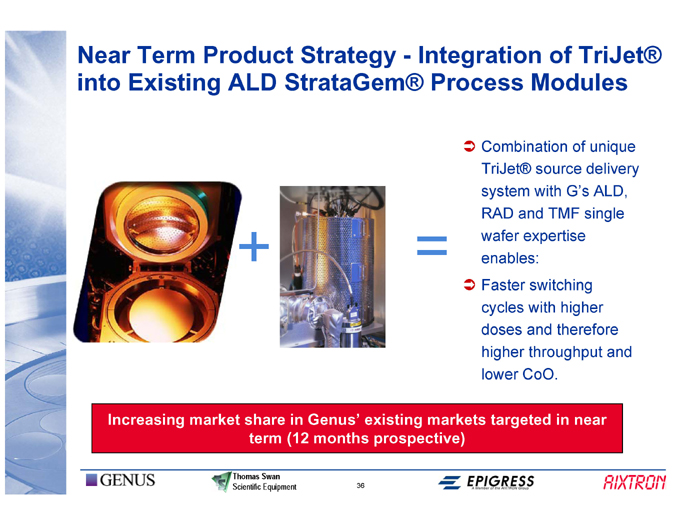

Combination of unique source delivery system with G’s ALD, RAD and TMF single wafer expertise enables: Faster switching cycles with higher doses and therefore higher throughput and lower CoO.

Integration of Process Modules

= existing markets targeted in near term (12 months prospective) 36

Near Term Product Strategy—into Existing ALD + Increasing market share in Genus’ Thomas Swan Scientific Equipment

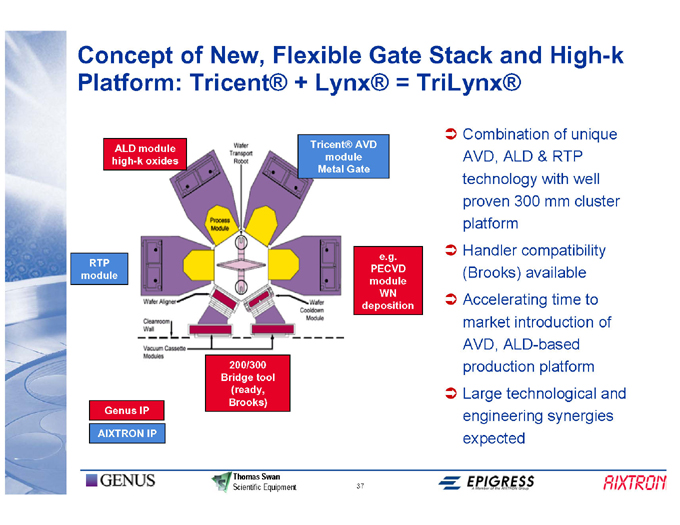

Combination of unique AVD, ALD & RTP technology with well proven 300 mm cluster platform Handler compatibility (Brooks) available Accelerating time to market introduction of AVD, ALD-based production platform Large technological and engineering synergies expected

=

e.g. PECVD module WN deposition

AVD module Metal Gate 37

+

200/300 Bridge tool (ready, Brooks) Thomas Swan Scientific Equipment ALD module high-k oxides IP

Genus IP AIXTRON

Concept of New, Flexible Gate Stack and High-k Platform: RTP module

Existing Genus silicon customers Existing Aixtron Silicon Customers Aixtron/ Genus non- silicon customers / collaboration partners

38

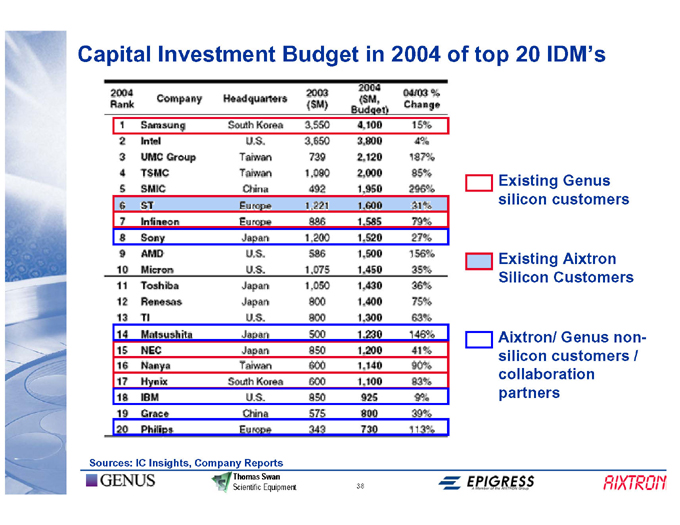

Capital Investment Budget in 2004 of top 20 IDM’s Sources: IC Insights, Company Reports Thomas Swan Scientific Equipment

AIXTRON Financial Summary 39

Thomas Swan Scientific Equipment

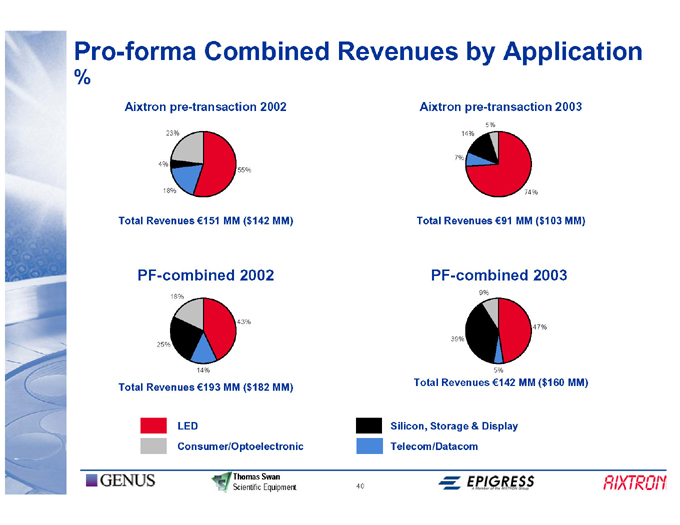

47% 74%

5% 5%

by Application pre-transaction 2003 9% & Display

14%

Aixtron 7% Total Revenues MM ($103 MM) PF-combined 2003 39% Total Revenues MM ($160 MM) Silicon, Storage Telecom/Datacom

Revenues 40

55% 43% Thomas Swan Scientific Equipment

14% Consumer/Optoelectronic LED pre-transaction 2002 23% 18%

4% 18% PF-combined 2002 25%

Aixtron Total Revenues MM ($142 MM) Total Revenues MM ($182 MM)

Pro-forma Combined %

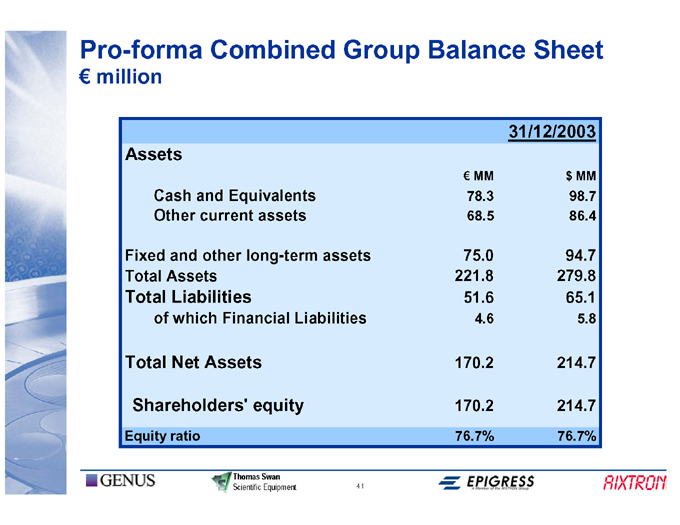

31/12/2003 $ MM 98.7 86.4 94.7 279.8 65.1 5.8 214.7 214.7 76.7% MM 78.3 68.5 75.0 221.8 51.6 4.6 170.2 170.2 76.7%

41

Cash and Equivalents Other current assets of which Financial Liabilities Shareholders’ equity Thomas Swan Scientific Equipment Pro-forma Combined Group Balance Sheet Assets Fixed and other long-term assets Total Assets Total Liabilities Total Net Assets Equity ratio

million

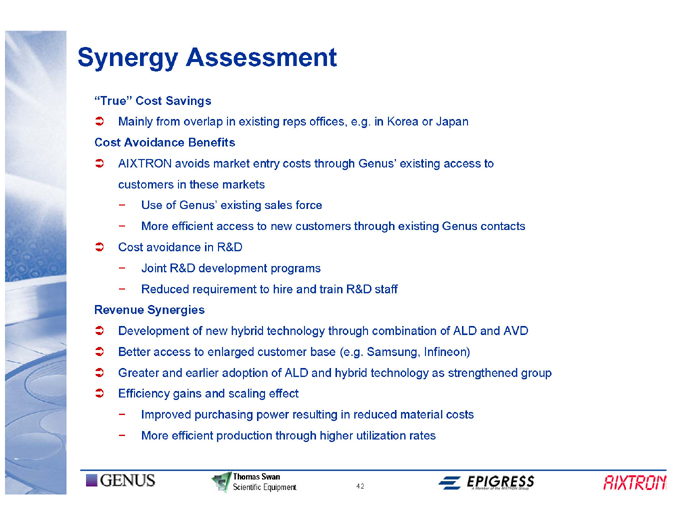

• group AVD to contacts and access Genus ALD strengthened costs Japan of Infineon) as or existing existing material rates Korea in Genus’ staff combination Samsung, technology e.g. through R&D reduced utilization 42 through (e.g. hybrid in offices, through train base and higher costs force customers and ALD resulting reps hire through sales new programs technology of effect Swan Equipment existing entry to to customer power hybrid scaling Thomas Scientific in market markets existing access R&D enlarged adoption production in development new and purchasing Assessment overlap Benefits these Genus’ requirement of to earlier avoids in efficient R&D gains efficient Savings from of avoidance Synergies access and Cost Avoidance Use More Joint Reduced Improved More Mainly AIXTRON customers Cost Development Better Greater Efficiency

• Synergy “True” Cost Revenue

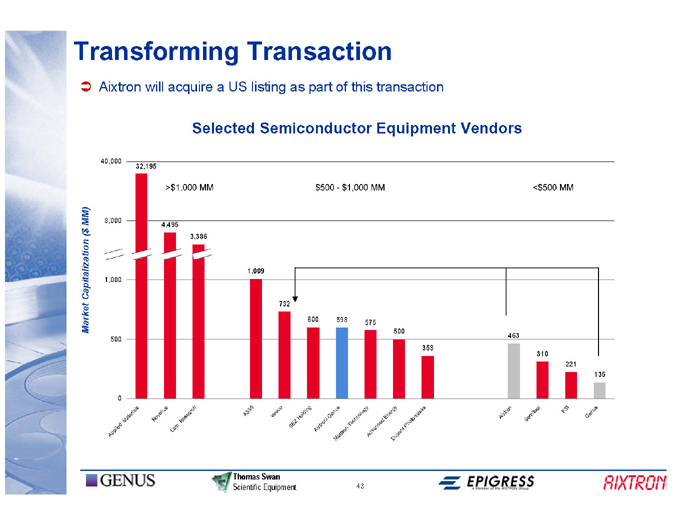

135

Genus

221

FSI

<$500 MM 310

Semitool

463 xtron i

A

358 sk sa omot

Ph

500 tnDupo yg r en

E edc vand

575 A ologynch 43 eT ttson

598 aM

Genus on/ $500—$1,000 MM rixt

600 A

Holding SEZ

732 coee

V

Selected Semiconductor Equipment Vendors 1,009 IASM Thomas Swan Scientific Equipment

3,386 arche

>$1,000 MM Res Lam

4,495 sllu

will acquire a US listing as part of this transaction eNov

32,195 s l riatea M ed

500 0 i Aixtron 40,000 8,000 1,000 Appl

Transforming Transaction ($ MM)Capitalization Market

AIXTRON 44

Summary of Transaction Benefits Thomas Swan Scientific Equipment

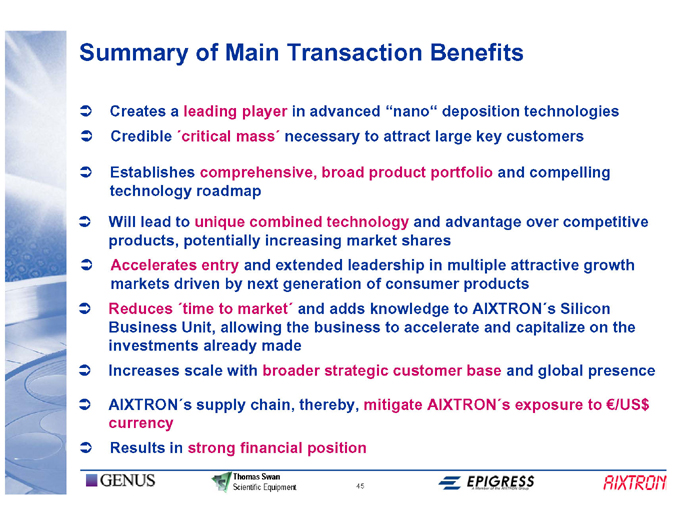

deposition technologies and compelling and advantage over competitive Silicon and global presence exposure to $ in advanced “nano” necessary to attract large key customers and extended leadership in multiple attractive growth and adds knowledge to 45 markets driven by next generation of consumer products supply chain, thereby, mitigate Thomas Swan Scientific

Equipment Creates a leading player Credible Establishes comprehensive, broad product portfolio technology roadmap Will lead to unique combined technology products, potentially increasing market shares Accelerates entry Reduces to Business Unit, allowing the business to accelerate and capitalize on the investments already made Increases scale with broader strategic customer base currency Results in strong financial position

Summary of Main Transaction Benefits