UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-05654 | |||||||

| ||||||||

Morgan Stanley Income Trust | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

522 Fifth Avenue, New York, New York |

| 10036 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Ronald E. Robison 522 Fifth Avenue, New York, New York 10036 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 212-296-6990 |

| ||||||

| ||||||||

Date of fiscal year end: | August 31, 2007 |

| ||||||

| ||||||||

Date of reporting period: | August 31, 2007 |

| ||||||

Item 1 - Report to Shareholders

Welcome, Shareholder:

In this report, you'll learn about how your investment in Morgan Stanley Income Trust performed during the annual period. We will provide an overview of the market conditions, and discuss some of the factors that affected performance during the reporting period. In addition, this report includes the Fund's financial statements and a list of Fund investments.

This material must be preceded or accompanied by a prospectus for the fund being offered.

Market forecasts provided in this report may not necessarily come to pass. There is no assurance that the Fund will achieve its investment objective. The Fund is subject to market risk, which is the possibility that market values of securities owned by the Fund will decline and, therefore, the value of the Fund's shares may be less than what you paid for them. Accordingly, you can lose money investing in this Fund. Please see the prospectus for more complete information on investment risks.

Fund Report

For the year ended August 31, 2007

| Total Return for the 12 Months Ended August 31, 2007 | |||||||||||||||||||||||

| Class A | Class B | Class C | Class D | Lehman Brothers U.S. Corporate Index1 | Lipper Corporate Debt Funds BBB-Rated Index2 | ||||||||||||||||||

| 3.99 | % | 3.25 | % | 3.37 | % | 4.12 | % | 4.32 | % | 4.99 | % | ||||||||||||

The performance of the Fund's four share classes varies because each has different expenses. The Fund's total returns assume the reinvestment of all distributions but do not reflect the deduction of any applicable sales charges. Such costs would lower performance. See Performance Summary for standardized performance and benchmark information.

Market Conditions

Fears stemming from the residential housing downturn and subprime mortgage market troubles accelerated over the course of the one-year period. With them came growing concerns about the impact on financial markets, the financial system, and the broader economy as a re-pricing of risk across all credit markets put a considerable strain on liquidity.

Although the Federal Open Market Committee (the "Fed") held "official interest rates", or the target federal funds rate, steady throughout the fiscal year, it did respond in other ways to the problems in the latter months of the period. The Fed issued a statement modifying its outlook to make it clear that economic growth risks were becoming skewed to the downside. In August 2007, following requests from a handful of district banks, it lowered the discount rate (the rate charged to banks to borrow directly from a central bank) by half a percent, from 6.25 percent to 5.75 percent, in an effort to encourage member banks to make greater use of the discount window and to inject cash into the system. This turn of events was the highlight of an eventful summer, one which brought with it a series of negative headlines and a strong dose of unfavorable news concerning the broader implications of the housing market downturn, especially wi th regard to its effect on mortgage securities and mortgage lenders. However, as we have seen before and will probably see again, markets tend to overreact and move excessively in one direction before correcting themselves.

Clearly, the economic outlook has dimmed. Still, the Fed is on the case, and financial markets have exhibited a bit more stability and rationality entering September. No one can say if the worst is over, but what we do know is that some areas of the bond market are already reflecting a set of extreme outcomes.

Throughout the 12-month period, U.S. Treasury yields fluctuated but overall, shorter-dated Treasury yields experienced the greatest decline, while longer dated yields were little changed. As a result, the shape of the yield curve went from relatively flat to fairly steep. At the end of the reporting period, market expectations were for a reduction in the federal funds rate, which could push short-term rates even lower in the coming months.

In the corporate bond market, spreads widened causing the sector to underperform other areas of the fixed income market for the overall period. Within the investment-grade corporate sector, lower-rated (Baa) and higher-rated (AAA) issues outpaced middle investment-grade issues. Utilities posted the highest returns, while financials, hit hardest by the recent liquidity crisis, posted the lowest returns. Within the below investment-grade sector, B rated issues outperformed the other, lower-rated high yield segments.

2

The mortgage market suffered from the turmoil surrounding residential housing, and especially by its spillover effects on secondary market activity, most notably in the non-agency mortgage area. Much of the growth in mortgage issuance over the past few years has been in the non-agency sector. This was driven by the development of a new array of loan types with payment and interest-rate features appealing to a broader set of borrowers than those available in the traditional agency space. While this helped fuel both the housing boom and a vibrant secondary market for these non-agency mortgages, the subprime meltdown cast a pall across the entire non-agency sector, with little regard for whether or not the securities or loans in question were subprime or prime. The result was a further reduction in mortgage market liquidity, as well as a sharp diminishment in the availability of non-conforming mortgage loans to the general public. For market participants, it became a challenge to price some of these non-agency bonds, let alone trade them, and a process of price discovery unfolded throughout August. While most agency mortgage-backed issues outperformed equal-risk Treasuries, non-agency mortgage issues fared poorly in recent months.

Performance Analysis

All share classes of Morgan Stanley Income Trust underperformed the Lehman Brothers U.S. Corporate Index and the Lipper Corporate Debt Funds BBB-Rated Index for the 12 months ended August 31, 2007, assuming no deduction of applicable sales charges.

The primary contributor to the Fund's underperformance relative to the benchmark Lehman Brothers U.S. Corporate Index was its mortgage position. The Fund holds a small allocation to the mortgage sector in the form of short-dated, high coupon mortgage-backed securities. Despite the good performance of these issues initially, the turmoil in the mortgage market and the drying up of liquidity hurt price performance later in the period and the Fund's position detracted from overall returns.

During the period, we kept the Fund's overall duration* below that of the Lehman Brothers U.S. Corporate Index, underweighting long-dated exposure while overweighting the intermediate area of the curve. Although this position detracted from performance during periods of yield declines, it benefited performance as yields rose and the yield curve steepened. As of the end of the period, much of this defensive position has been removed.

We have held an underweight corporate position in the Fund's portfolio for some time now, and this position detracted from relative performance in the first half of the period. However, as credit spreads widened in the latter months, the underweight to the sector was beneficial to performance. While we are looking for areas to take advantage of this spread widening and add to corporate positions, we are taking a cautious approach because we believe the credit market remains vulnerable to potential credit downgrades and/or an economic downturn.

There is no guarantee that any sectors mentioned will continue to perform as discussed herein or that securities in such sectors will be held by the Fund in the future.

* A measure of the sensitivity of a bond's price to changes in interest rates, expressed in years. Each year of duration represents an expected 1 percent change in the price of a bond for every 1 percent change in interest rates. The longer a bond's duration, the greater the effect of interest-rate movements on its price. Typically, funds with shorter durations perform better in rising-interest-rate environments, while funds with longer durations perform better when rates decline.

3

| PORTFOLIO COMPOSITION** | |||||||

| Corporate Bonds | 55.7 | % | |||||

| Short-Term Investments | 19.0 | ||||||

| U.S. Government Obligations | 14.3 | ||||||

| Commercial Mortgage-Backed Securities | 6.5 | ||||||

| Asset-Backed Securities | 3.0 | ||||||

| Collateralized Mortgage Obligations | 0.9 | ||||||

| Foreign Government Obligations | 0.6 | ||||||

| LONG-TERM CREDIT ANALYSIS | |||||||

| AAA | 31.4 | % | |||||

| AA | 7.8 | ||||||

| A | 22.0 | ||||||

| BBB | 34.2 | ||||||

| BB | 3.7 | ||||||

| B or Below | 0.8 | ||||||

| Not Rated | 0.1 | ||||||

**Does not include open long futures contracts with an underlying face amount of $7,396,720 with unrealized appreciation of $19,640 and open short futures contracts with an underlying face amount of $16,008,236 with unrealized depreciation of $50,899. Also does not include open swap contracts with net unrealized appreciation of $314,824.

Data as of August 31, 2007. Subject to change daily. All percentages for portfolio composition are as a percentage of total investments and all percentages for long-term credit analysis are as a percentage of total long-term investments. These data are provided for informational purposes only and should not be deemed a recommendation to buy or sell the securities mentioned. Morgan Stanley is a full-service securities firm engaged in securities trading and brokerage activities, investment banking, research and analysis, financing and financial advisory services.

Investment Strategy

The Fund will normally invest at least 80 percent of its assets in investment grade fixed-income securities. These securities may include corporate debt securities, preferred stocks, U.S. government securities, mortgage-backed securities, including collateralized mortgage obligations and commercial mortgage-backed securities, asset-backed securities and securities issued by foreign governments or corporations. In deciding which securities to buy, hold or sell, the Fund's "Investment Adviser," Morgan Stanley Investment Advisors Inc., considers domestic and international economic developments, interest rate trends, bond ratings and other factors relating to the issuers.

For More Information About Portfolio Holdings

Each Morgan Stanley fund provides a complete schedule of portfolio holdings in its semiannual and annual reports within 60 days of the end of the fund's second and fourth fiscal quarters. The semiannual reports and the annual reports are filed electronically with the Securities and Exchange Commission (SEC) on Form N-CSRS and Form N-CSR, respectively. Morgan Stanley also delivers the semiannual and annual reports to fund shareholders and makes these reports available on its public web site, www.morganstanley.com. Each Morgan Stanley fund also files a complete schedule of portfolio holdings with the SEC for the fund's first and third fiscal quarters on Form N-Q. Morgan Stanley does not deliver the reports for the first and third fiscal quarters to shareholders, nor are the reports posted to the Morgan Stanley public web site. You may, however, obtain the Form N-Q filings (as well as the Form N-CSR and N-CSRS filings) by access ing the SEC's web site, http://www.sec.gov. You may also review and copy them

4

at the SEC's public reference room in Washington, DC. Information on the operation of the SEC's public reference room may be obtained by calling the SEC at (800) SEC-0330. You can also request copies of these materials, upon payment of a duplicating fee, by electronic request at the SEC's e-mail address (publicinfo@sec.gov) or by writing the public reference section of the SEC, Washington, DC 20549-0102.

Proxy Voting Policy and Procedures and Proxy Voting Record

You may obtain a copy of the Fund's Proxy Voting Policy and Procedures without charge, upon request, by calling toll free (800) 869-NEWS or by visiting the Mutual Fund Center on our Web site at www.morganstanley.com. It is also available on the Securities and Exchange Commission's Web site at http://www.sec.gov.

You may obtain information regarding how the Fund voted proxies relating to portfolio securities during the most recent twelve-month period ended June 30 without charge by visiting the Mutual Fund Center on our Web site at www.morganstanley.com. This information is also available on the Securities and Exchange Commission's Web site at http://www.sec.gov.

Householding Notice

To reduce printing and mailing costs, the Fund attempts to eliminate duplicate mailings to the same address. The Fund delivers a single copy of certain shareholder documents, including shareholder reports, prospectuses and proxy materials, to investors with the same last name who reside at the same address. Your participation in this program will continue for an unlimited period of time unless you instruct us otherwise. You can request multiple copies of these documents by calling (800) 350-6414, 8:00 a.m. to 8:00 p.m., ET. Once our Customer Service Center has received your instructions, we will begin sending individual copies for each account within 30 days.

5

Performance Summary

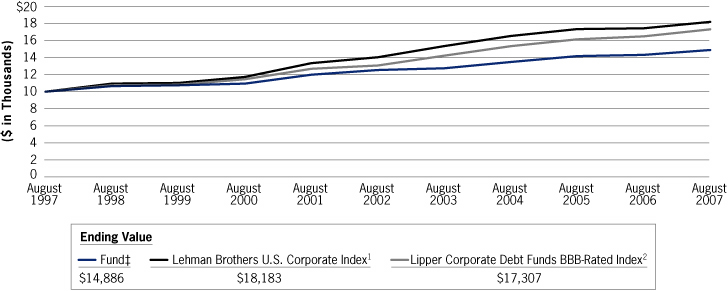

Performance of $10,000 Investment—Class B

6

| Average Annual Total Returns—Period Ended August 31, 2007 | |||||||||||||||||||||||||||||||||||

| Symbol | Class A Shares* (since 07/28/97) IISAX | Class B Shares** (since 05/03/89) IISBX | Class C Shares† (since 07/28/97) IISCX | Class D Shares†† (since 07/28/97) IISDX | |||||||||||||||||||||||||||||||

| 1 Year | 3.99% (0.43) | 3 4 | 3.25% (1.71) | 3 4 | 3.37% 2.38 | 3 4 | 4.12% — | 3 | |||||||||||||||||||||||||||

| 5 Years | 3.89 2.99 | 3 4 | 3.24 2.89 | 3 4 | 3.27 3.27 | 3 4 | 4.09 — | 3 | |||||||||||||||||||||||||||

| 10 Years | 4.69 4.23 | 3 4 | 4.06 4.06 | 3 4 | 3.93 3.93 | 3 4 | 4.78 — | 3 | |||||||||||||||||||||||||||

| Since Inception | 4.59 4.14 | 3 4 | 5.19 5.19 | 3 4 | 3.86 3.86 | 3 4 | 4.69 — | 3 | |||||||||||||||||||||||||||

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. For most recent month-end performance figures, please visit www.morganstanley.com/msim or speak with your Financial Advisor. Investment returns and principal value will fluctuate and fund shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance for Class A, Class B, Class C, and Class D shares will vary due to differences in sales charges and expenses.

* The maximum front-end sales charge for Class A is 4.25%.

** The maximum contingent deferred sales charge (CDSC) for Class B is 5.0%. The CDSC declines to 0% after six years. Effective April 2005, Class B shares will generally convert to Class A shares approximately eight years after the end of the calendar month in which the shares were purchased. Performance for periods greater than eight years reflects this conversion (beginning April 2005).

† The maximum contingent deferred sales charge for Class C is 1.0% for shares redeemed within one year of purchase.

†† Class D has no sales charge.

(1) The Lehman Brothers U.S. Corporate Index covers U.S. dollar-denominated, investment-grade, fixed rate, taxable securities sold by industrial, utility and financial issuers. It includes publicly issued U.S. corporate and foreign debentures and secured notes that meet specified maturity, liquidity and quality requirements. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

(2) The Lipper Corporate Debt Funds BBB-Rated Index is an equally weighted performance index of the largest qualifying funds (based on net assets) in the Lipper Corporate Debt Funds BBB-Rated classification. The Index, which is adjusted for capital gains distributions and income dividends, is unmanaged and should not be considered an investment. There are currently 30 funds represented in this Index. The Fund is in the Lipper Corporate Debt Funds BBB-Rated classification as of the date of this report.

(3) Figure shown assumes reinvestment of all distributions and does not reflect the deduction of any sales charges.

(4) Figure shown assumes reinvestment of all distributions and the deduction of the maximum applicable sales charge. See the Fund's current prospectus for complete details on fees and sales charges.

‡ Ending value assuming a complete redemption on August 31, 2007.

7

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption fees; and (2) ongoing costs, including advisory fees; distribution and service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period 03/01/07 – 08/31/07.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing cost of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) and redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs, and will not help you determine the relative total cost of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value | Ending Account Value | Expenses Paid During Period * | |||||||||||||

| 03/01/07 | 08/31/07 | 03/01/07 – 08/31/07 | |||||||||||||

| Class A | |||||||||||||||

| Actual (-0.17% return) | $ | 1,000.00 | $ | 998.30 | $ | 5.29 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,019.91 | $ | 5.35 | |||||||||

| Class B | |||||||||||||||

| Actual (-0.49% return) | $ | 1,000.00 | $ | 995.10 | $ | 8.30 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,016.89 | $ | 8.39 | |||||||||

| Class C | |||||||||||||||

| Actual (-0.48% return) | $ | 1,000.00 | $ | 995.20 | $ | 8.30 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,016.89 | $ | 8.39 | |||||||||

| Class D | |||||||||||||||

| Actual (-0.07% return) | $ | 1,000.00 | $ | 999.30 | $ | 4.03 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,021.17 | $ | 4.08 | |||||||||

* Expenses are equal to the Fund's annualized expense ratios of 1.05%, 1.65%, 1.65% and 0.80% for Class A, Class B, Class C and Class D shares, respectively, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). If the Fund had borne all of its expenses that were waived by the Investment Adviser and Administrator, the annualized expense ratios would have been 1.42%, 2.02%, 2.02% and 1.17% for Class A, Class B, Class C and Class D shares, respectively.

8

Investment Advisory Agreement Approval

Nature, Extent and Quality of Services

The Board reviewed and considered the nature and extent of the investment advisory services provided by the Investment Adviser under the Advisory Agreement, including portfolio management, investment research and fixed income securities trading. The Board also reviewed and considered the nature and extent of the non-advisory, administrative services provided by the Fund's Administrator under the Administration Agreement, including accounting, clerical, bookkeeping, compliance, business management and planning, and the provision of supplies, office space and utilities at the Investment Adviser's expense. (The Investment Adviser and the Administrator together are referred to as the "Adviser" and the Advisory and Administration Agreements together are referred to as the "Management Agreement.") The Board also compared the nature of the services provided by the Adviser with similar services provided by non-affiliated advisers as rep orted to the Board by Lipper Inc. ("Lipper").

The Board reviewed and considered the qualifications of the portfolio managers, the senior administrative managers and other key personnel of the Adviser who provide the advisory and administrative services to the Fund. The Board determined that the Adviser's portfolio managers and key personnel are well qualified by education and/or training and experience to perform the services in an efficient and professional manner. The Board concluded that the nature and extent of the advisory and administrative services provided were necessary and appropriate for the conduct of the business and investment activities of the Fund. The Board also concluded that the overall quality of the advisory and administrative services was satisfactory.

Performance Relative to Comparable Funds Managed by Other Advisers

On a regular basis, the Board reviews the performance of all funds in the Morgan Stanley Fund Complex, including the Fund, compared to their peers, paying specific attention to the underperforming funds. In addition, the Board specifically reviewed the Fund's performance for the one-, three- and five-year periods ended November 30, 2006, as shown in a report provided by Lipper (the "Lipper Report"), compared to the performance of comparable funds selected by Lipper (the "performance peer group"). The Board also discussed with the Adviser the performance goals and the actual results achieved in managing the Fund. The Board concluded that the Fund's performance was competitive with that of its performance peer group.

Fees Relative to Other Proprietary Funds Managed by the Adviser with Comparable Investment Strategies

The Board reviewed the advisory and administrative fee (together, the "management fee") rate paid by the Fund under the Management Agreement. The Board noted that the management fee rate was comparable to the management fee rates charged by the Adviser to other proprietary funds it manages with investment strategies comparable to those of the Fund taking into account the scope of the services provided.

9

Fees and Expenses Relative to Comparable Funds Managed by Other Advisers

The Board reviewed the management fee rate and total expense ratio of the Fund as compared to the average management fee rate and average total expense ratio for funds, selected by Lipper (the "expense peer group"), managed by other advisers with investment strategies comparable to those of the Fund, as shown in the Lipper Report. The Board concluded that the Fund's management fee rate and total expense ratio were competitive with those of its expense peer group.

Breakpoints and Economies of Scale

The Board reviewed the structure of the Fund's management fee schedule under the Management Agreement and noted that it includes breakpoints. The Board also reviewed the level of the Fund's management fee and noted that the fee, as a percentage of the Fund's net assets, would decrease as net assets increase because the management fee includes a breakpoint. The Board concluded that the Fund's management fee would reflect economies of scale as assets increase.

Profitability of the Adviser and Affiliates

The Board considered information concerning the costs incurred and profits realized by the Adviser and affiliates during the last year from their relationship with the Fund and during the last two years from their relationship with the Morgan Stanley Fund Complex and reviewed with the Adviser the cost allocation methodology used to determine the profitability of the Adviser and affiliates. Based on its review of the information it received, the Board concluded that the profits earned by the Adviser and affiliates were not excessive in light of the advisory, administrative and other services provided to the Fund.

Fall-Out Benefits

The Board considered so-called "fall-out benefits" derived by the Adviser and affiliates from their relationship with the Fund and the Morgan Stanley Fund Complex, such as sales charges on sales of Class A shares and "float" benefits derived from handling of checks for purchases and sales of Fund shares, through a broker-dealer affiliate of the Adviser. The Board also considered that a broker-dealer affiliate of the Adviser receives from the Fund 12b-1 fees for distribution and shareholder services. The Board concluded that the float benefits were relatively small and the sales charges and 12b-1 fees were competitive with those of other broker-dealers.

Soft Dollar Benefits

The Board considered whether the Adviser realizes any benefits from commissions paid to brokers who execute securities transactions for the Fund ("soft dollars"). The Board noted that the Fund invests only in fixed income securities, which do not generate soft dollars.

10

Adviser Financially Sound and Financially Capable of Meeting the Fund's Needs

The Board considered whether the Adviser is financially sound and has the resources necessary to perform its obligations under the Management Agreement. The Board concluded that the Adviser has the financial resources necessary to fulfill its obligations under the Management Agreement.

Historical Relationship Between the Fund and the Adviser

The Board also reviewed and considered the historical relationship between the Fund and the Adviser, including the organizational structure of the Adviser, the policies and procedures formulated and adopted by the Adviser for managing the Fund's operations and the Board's confidence in the competence and integrity of the senior managers and key personnel of the Adviser. The Board concluded that it is beneficial for the Fund to continue its relationship with the Adviser.

Other Factors and Current Trends

The Board considered the controls and procedures adopted and implemented by the Adviser and monitored by the Fund's Chief Compliance Officer and concluded that the conduct of business by the Adviser indicates a good faith effort on its part to adhere to high ethical standards in the conduct of the Fund's business.

General Conclusion

On April 25, 2007, after considering and weighing all of the above factors, the Board concluded that it would be in the best interest of the Fund and its shareholders to approve renewal of the Management Agreement for another year until April 30, 2008. On June 20, 2007, the Board again considered and weighed all of the above factors and concluded that it would be in the best interest of the Fund and its shareholders to approve renewal of the Management Agreement to continue until June 30, 2008.

11

Morgan Stanley Income Trust

Portfolio of Investments n August 31, 2007

| PRINCIPAL AMOUNT IN THOUSANDS | COUPON RATE | MATURITY DATE | VALUE | ||||||||||||||||

| Corporate Bonds (66.8%) | |||||||||||||||||||

| Advertising/Marketing Services (0.1%) | |||||||||||||||||||

| $ | 55 | Interpublic Group of Companies, Inc. (The) | 6.25 | % | 11/15/14 | $ | 49,225 | ||||||||||||

| Aerospace & Defense (1.2%) | |||||||||||||||||||

| 120 | DAE Aviation Holdings, Inc. - 144A** | 11.25 | 08/01/15 | 120,000 | |||||||||||||||

| 175 | Raytheon Co. | 4.50 | 11/15/07 | 174,567 | |||||||||||||||

| 242 | Systems 2001 Asset Trust - 144A** (Cayman Islands) | 6.664 | 09/15/13 | 257,803 | |||||||||||||||

| 552,370 | |||||||||||||||||||

| Air Freight/Couriers (0.5%) | |||||||||||||||||||

| 220 | FedEx Corp. | 7.25 | 02/15/11 | 235,044 | |||||||||||||||

| Airlines (0.5%) | |||||||||||||||||||

| 224 | America West Airlines, Inc. (Series 01-1) | 7.10 | 04/02/21 | 236,695 | |||||||||||||||

| Auto Parts: O.E.M. (0.3%) | |||||||||||||||||||

| 150 | ArvinMeritor, Inc. (a) | 8.75 | 03/01/12 | 149,250 | |||||||||||||||

| Beverages: Alcoholic (1.6%) | |||||||||||||||||||

| 330 | FBG Finance Ltd. - 144A** (Australia) | 5.125 | 06/15/15 | 312,275 | |||||||||||||||

| 430 | Miller Brewing Co. - 144A** | 4.25 | 08/15/08 | 424,175 | |||||||||||||||

| 736,450 | |||||||||||||||||||

| Cable/Satellite TV (1.8%) | |||||||||||||||||||

| 270 | Comcast Cable Communications, Inc. | 6.75 | 01/30/11 | 280,622 | |||||||||||||||

| 80 | Comcast Cable Communications, Inc. | 7.125 | 06/15/13 | 85,218 | |||||||||||||||

| 230 | Comcast Corp. | 6.50 | 01/15/15 | 237,594 | |||||||||||||||

| 245 | EchoStar DBS Corp. | 6.375 | 10/01/11 | 241,325 | |||||||||||||||

| 844,759 | |||||||||||||||||||

| Department Stores (2.4%) | |||||||||||||||||||

| 80 | JC Penney Corp., Inc. | 5.75 | 02/15/18 | 77,408 | |||||||||||||||

| 1,045 | May Department Stores Co. | 5.95 | 11/01/08 | 1,044,126 | |||||||||||||||

| 1,121,534 | |||||||||||||||||||

| Drugstore Chains (1.3%) | |||||||||||||||||||

| 170 | CVS Caremark Corp. | 5.75 | 06/01/17 | 166,451 | |||||||||||||||

| 165 | CVS Corp. | 5.75 | 08/15/11 | 166,909 | |||||||||||||||

| 291 | CVS Lease Pass Through - 144A** | 6.036 | 12/10/28 | 284,349 | |||||||||||||||

| 617,709 | |||||||||||||||||||

| Electric Utilities (7.9%) | |||||||||||||||||||

| 400 | Arizona Public Service Co. | 5.80 | 06/30/14 | 398,451 | |||||||||||||||

| 90 | CenterPoint Energy Resources, Corp. | 6.25 | 02/01/37 | 89,585 | |||||||||||||||

See Notes to Financial Statements

12

Morgan Stanley Income Trust

Portfolio of Investments n August 31, 2007 continued

| PRINCIPAL AMOUNT IN THOUSANDS | COUPON RATE | MATURITY DATE | VALUE | ||||||||||||||||

| $ | 45 | CenterPoint Energy Resources, Corp. (Series B) | 7.875 | % | 04/01/13 | $ | 49,235 | ||||||||||||

| 310 | Consumers Energy Co. (Series H) | 4.80 | 02/17/09 | 307,663 | |||||||||||||||

| 205 | Detroit Edison Co. (The) | 6.125 | 10/01/10 | 210,991 | |||||||||||||||

| 340 | Duquesne Light Co. (Series O) | 6.70 | 04/15/12 | 360,865 | |||||||||||||||

| 255 | Entergy Gulf States, Inc. | 3.60 | 06/01/08 | 250,005 | |||||||||||||||

| 365 | Entergy Gulf States, Inc. | 5.76 | † | 12/01/09 | 361,784 | ||||||||||||||

| 200 | Entergy Gulf States, Inc. - 144A** | 6.11 | † | 12/08/08 | 200,600 | ||||||||||||||

| 230 | Exelon Corp. | 6.75 | 05/01/11 | 238,729 | |||||||||||||||

| 245 | Ohio Edison Co. | 6.40 | 07/15/16 | 253,882 | |||||||||||||||

| 290 | Ohio Power Company (Series K) | 6.00 | 06/01/16 | 294,536 | |||||||||||||||

| 32 | PSEG Energy Holdings Inc. | 8.625 | 02/15/08 | 32,442 | |||||||||||||||

| 100 | Public Service Electric & Gas Co. (Series B) | 5.00 | 01/01/13 | 97,498 | |||||||||||||||

| 200 | Texas Eastern Transmission | 7.00 | 07/15/32 | 221,352 | |||||||||||||||

| 195 | TXU Energy Co. | 7.00 | 03/15/13 | 200,514 | |||||||||||||||

| 130 | Union Electric Co. | 6.40 | 06/15/17 | 135,075 | |||||||||||||||

| 3,703,207 | |||||||||||||||||||

| Electrical Products (0.7%) | |||||||||||||||||||

| 340 | Cooper Industries, Inc. | 5.25 | 11/15/12 | 339,342 | |||||||||||||||

| Electronic Equipment/Instruments (0.2%) | |||||||||||||||||||

| 110 | Xerox Corp. | 5.50 | 05/15/12 | 108,855 | |||||||||||||||

| Electronics/Appliances (0.6%) | |||||||||||||||||||

| 260 | LG Electronics Inc. - 144A** (South Korea) | 5.00 | 06/17/10 | 256,038 | |||||||||||||||

| Environmental Services (0.4%) | |||||||||||||||||||

| 200 | Waste Management, Inc. | 6.875 | 05/15/09 | 206,298 | |||||||||||||||

| Finance/Rental/Leasing (3.8%) | |||||||||||||||||||

| 120 | Capital One Financial Corp. (WI) | 6.75 | 09/15/17 | 119,578 | |||||||||||||||

| 270 | Capmark Financial Group Inc. - 144A** | 5.875 | 05/10/12 | 239,361 | |||||||||||||||

| 115 | Capmark Financial Group Inc. - 144A** | 6.30 | 05/10/17 | 93,571 | |||||||||||||||

| 250 | CIT Group, Inc. | 5.65 | 02/13/17 | 219,089 | |||||||||||||||

| 325 | Countrywide Home Loans, Inc. (Series MTN) | 3.25 | 05/21/08 | 313,653 | |||||||||||||||

| 395 | Ford Motor Credit Co. LLC | 7.25 | 10/25/11 | 360,396 | |||||||||||||||

| 475 | Nationwide Building Society - 144A** (United Kingdom) | 4.25 | 02/01/10 | 467,223 | |||||||||||||||

| 1,812,871 | |||||||||||||||||||

See Notes to Financial Statements

13

Morgan Stanley Income Trust

Portfolio of Investments n August 31, 2007 continued

| PRINCIPAL AMOUNT IN THOUSANDS | COUPON RATE | MATURITY DATE | VALUE | ||||||||||||||||

| Financial Conglomerates (1.4%) | |||||||||||||||||||

| $ | 75 | Brookfield Asset Management Inc. (Canada) | 5.80 | % | 04/25/17 | $ | 75,445 | ||||||||||||

| 240 | Citigroup Inc. (a) | 5.25 | 02/27/12 | 239,163 | |||||||||||||||

| 400 | GMAC LLC | 6.875 | 09/15/11 | 357,046 | |||||||||||||||

| 671,654 | |||||||||||||||||||

| Food Retail (0.6%) | |||||||||||||||||||

| 185 | Delhaize America, Inc. | 9.00 | 04/15/31 | 217,375 | |||||||||||||||

| 80 | Kroger Co. (The) | 6.40 | 08/15/17 | 81,855 | |||||||||||||||

| 299,230 | |||||||||||||||||||

| Food: Major Diversified (1.1%) | |||||||||||||||||||

| 165 | ConAgra Foods, Inc. | 7.00 | 10/01/28 | 172,347 | |||||||||||||||

| 130 | ConAgra Foods, Inc. | 8.25 | 09/15/30 | 153,390 | |||||||||||||||

| 195 | Kraft Foods Inc. | 6.00 | 02/11/13 | 199,163 | |||||||||||||||

| 524,900 | |||||||||||||||||||

| Food: Meat/Fish/Dairy (0.6%) | |||||||||||||||||||

| 100 | Pilgrim's Pride Corp. | 7.625 | 05/01/15 | 100,250 | |||||||||||||||

| 50 | Pilgrim's Pride Corp. | 9.625 | 09/15/11 | 51,667 | |||||||||||||||

| 105 | Smithfield Foods, Inc. (Series B) | 8.00 | 10/15/09 | 108,150 | |||||||||||||||

| 260,067 | |||||||||||||||||||

| Gas Distributors (1.0%) | |||||||||||||||||||

| 370 | NiSource Finance Corp. | 6.064 | † | 11/23/09 | 366,879 | ||||||||||||||

| 100 | NiSource Finance Corp. | 7.875 | 11/15/10 | 106,288 | |||||||||||||||

| 473,167 | |||||||||||||||||||

| Home Improvement Chains (0.9%) | |||||||||||||||||||

| 445 | Home Depot Inc. | 5.485 | 12/16/09 | 439,787 | |||||||||||||||

| Insurance Brokers/Services (1.8%) | |||||||||||||||||||

| 360 | Catlin Insurance Co., Ltd. - 144A** (Bahamas) | 7.249 | † | ## | 335,244 | ||||||||||||||

| 485 | Farmers Exchange Capital - 144A** | 7.05 | 07/15/28 | 490,055 | |||||||||||||||

| 825,299 | |||||||||||||||||||

| Integrated Oil (0.8%) | |||||||||||||||||||

| 190 | Hess Corp. | 6.65 | 08/15/11 | 198,536 | |||||||||||||||

| 205 | Petro-Canada (Canada) | 5.95 | 05/15/35 | 191,725 | |||||||||||||||

| 390,261 | |||||||||||||||||||

See Notes to Financial Statements

14

Morgan Stanley Income Trust

Portfolio of Investments n August 31, 2007 continued

| PRINCIPAL AMOUNT IN THOUSANDS | COUPON RATE | MATURITY DATE | VALUE | ||||||||||||||||

| Investment Banks/Brokers (1.8%) | |||||||||||||||||||

| $ | 160 | Bear Stearns Companies Inc. (The) (a) | 5.55 | % | 01/22/17 | $ | 147,571 | ||||||||||||

| 495 | Goldman Sachs Capital II | 5.793 | † | # | 454,672 | ||||||||||||||

| 250 | Lehman Brothers Holdings, Inc. | 6.875 | 07/17/37 | 235,579 | |||||||||||||||

| 837,822 | |||||||||||||||||||

| Major Banks (5.0%) | |||||||||||||||||||

| 200 | Bank of America Corp. | 4.875 | 09/15/12 | 196,799 | |||||||||||||||

| 485 | HSBC Finance Corp. | 6.75 | 05/15/11 | 503,623 | |||||||||||||||

| 685 | Unicredit Luxembourg Finance S.A. - 144A** (Luxembourg) | 5.41 | † | 10/24/08 | 685,212 | ||||||||||||||

| 285 | USB Capital IX | 6.189 | † | # | 286,408 | ||||||||||||||

| 685 | Wachovia Capital Trust III | 5.80 | † | # | 683,823 | ||||||||||||||

| 2,355,865 | |||||||||||||||||||

| Major Telecommunications (6.1%) | |||||||||||||||||||

| 565 | AT&T Corp. (a) | 8.00 | † | 11/15/31 | 674,290 | ||||||||||||||

| 150 | Deutsche Telekom International Finance BV (Netherlands) | 8.00 | † | 06/15/10 | 159,776 | ||||||||||||||

| 310 | France Telecom S.A. (France) | 8.50 | † | 03/01/31 | 396,942 | ||||||||||||||

| 300 | SBC Communications, Inc. | 6.15 | 09/15/34 | 291,761 | |||||||||||||||

| 305 | Sprint Capital Corp. | 8.75 | 03/15/32 | 353,036 | |||||||||||||||

| 255 | Telecom Italia Capital SA (Luxembourg) | 4.00 | 11/15/08 | 250,497 | |||||||||||||||

| 215 | Telecom Italia Capital SA (Luxembourg) | 4.00 | 01/15/10 | 208,116 | |||||||||||||||

| 330 | Telefonica Europe BV (Netherlands) | 8.25 | 09/15/30 | 388,113 | |||||||||||||||

| 165 | Verizon Global Funding Corp. | 7.25 | 12/01/10 | 174,269 | |||||||||||||||

| 2,896,800 | |||||||||||||||||||

| Managed Health Care (0.1%) | |||||||||||||||||||

| 55 | WellPoint, Inc. | 4.25 | 12/15/09 | 54,026 | |||||||||||||||

| Media Conglomerates (1.9%) | |||||||||||||||||||

| 350 | Time Warner, Inc. | 5.73 | † | 11/13/09 | 347,219 | ||||||||||||||

| 240 | Time Warner, Inc. (a) | 5.875 | 11/15/16 | 235,591 | |||||||||||||||

| 295 | Viacom, Inc. | 6.875 | 04/30/36 | 288,150 | |||||||||||||||

| 870,960 | |||||||||||||||||||

| Medical Specialties (0.9%) | |||||||||||||||||||

| 405 | Hospira, Inc. | 5.84 | † | 03/30/10 | 406,260 | ||||||||||||||

| Motor Vehicles (0.9%) | |||||||||||||||||||

| 335 | DaimlerChrysler North America LLC | 8.50 | 01/18/31 | 415,617 | |||||||||||||||

See Notes to Financial Statements

15

Morgan Stanley Income Trust

Portfolio of Investments n August 31, 2007 continued

| PRINCIPAL AMOUNT IN THOUSANDS | COUPON RATE | MATURITY DATE | VALUE | ||||||||||||||||

| Multi-Line Insurance (2.0%) | |||||||||||||||||||

| $ | 450 | AIG SunAmerica Global Financing VI - 144A** | 6.30 | % | 05/10/11 | $ | 464,504 | ||||||||||||

| 485 | American General Finance Corp. (Series H) | 4.625 | 09/01/10 | 479,512 | |||||||||||||||

| 944,016 | |||||||||||||||||||

| Oil & Gas Pipelines (2.2%) | |||||||||||||||||||

| 190 | Colorado Interstate Gas Co. | 6.80 | 11/15/15 | 197,019 | |||||||||||||||

| 165 | Enterprise Products Operating L.P. (Series B) | 5.60 | 10/15/14 | 162,009 | |||||||||||||||

| 320 | Kinder Morgan Finance Co. (Canada) | 5.70 | 01/05/16 | 285,335 | |||||||||||||||

| 125 | Kinder Morgan Energy Partners, L.P. | 5.85 | 09/15/12 | 125,336 | |||||||||||||||

| 290 | Plains All American Pipeline | 6.70 | 05/15/36 | 289,778 | |||||||||||||||

| 1,059,477 | |||||||||||||||||||

| Oil & Gas Production (1.3%) | |||||||||||||||||||

| 120 | Chesapeake Energy Corp. | 7.625 | 07/15/13 | 123,300 | |||||||||||||||

| 230 | Devon Financing Corp. ULC | 6.875 | 09/30/11 | 243,473 | |||||||||||||||

| 230 | Kerr-McGee Corp. | 6.625 | 10/15/07 | 230,160 | |||||||||||||||

| 596,933 | |||||||||||||||||||

| Oil Refining/Marketing (0.3%) | |||||||||||||||||||

| 160 | Valero Energy Corp. | 3.50 | 04/01/09 | 156,420 | |||||||||||||||

| Other Metals/Minerals (0.9%) | |||||||||||||||||||

| 385 | Brascan Corp. (Canada) | 7.125 | 06/15/12 | 412,850 | |||||||||||||||

| Property - Casualty Insurers (3.7%) | |||||||||||||||||||

| 645 | Mantis Reef Ltd. - 144A** (Cayman Islands) | 4.692 | 11/14/08 | 642,720 | |||||||||||||||

| 205 | Platinum Underwriters Finance Inc. (Series B) | 7.50 | 06/01/17 | 218,751 | |||||||||||||||

| 350 | Platinum Underwriters Holdings, Ltd. (Series B) (Bermuda) | 6.371 | 11/16/07 | 349,224 | |||||||||||||||

| 510 | Xlliac Global Funding - 144A** | 4.80 | 08/10/10 | 505,029 | |||||||||||||||

| 1,715,724 | |||||||||||||||||||

| Railroads (1.8%) | |||||||||||||||||||

| 235 | Burlington Northern Santa Fe Corp. | 6.125 | 03/15/09 | 238,110 | |||||||||||||||

| 250 | Union Pacific Corp. | 5.45 | 01/31/13 | 250,002 | |||||||||||||||

| 200 | Union Pacific Corp. | 6.625 | 02/01/08 | 200,577 | |||||||||||||||

| 160 | Union Pacific Corp. (Series E) | 6.79 | 11/09/07 | 160,194 | |||||||||||||||

| 848,883 | |||||||||||||||||||

See Notes to Financial Statements

16

Morgan Stanley Income Trust

Portfolio of Investments n August 31, 2007 continued

| PRINCIPAL AMOUNT IN THOUSANDS | COUPON RATE | MATURITY DATE | VALUE | ||||||||||||||||

| Real Estate Development (1.0%) | |||||||||||||||||||

| $ | 272 | World Financial Properties - 144A** | 6.91 | % | 09/01/13 | $ | 275,926 | ||||||||||||

| 201 | World Financial Properties - 144A** | 6.95 | 09/01/13 | 204,107 | |||||||||||||||

| 480,033 | |||||||||||||||||||

| Real Estate Investment Trusts (0.9%) | |||||||||||||||||||

| 455 | iStar Financial Inc. | 5.71 | † | 03/09/10 | 430,693 | ||||||||||||||

| Restaurants (0.5%) | |||||||||||||||||||

| 230 | Tricon Global Restaurants, Inc. (a) | 8.875 | 04/15/11 | 256,247 | |||||||||||||||

| Savings Banks (3.8%) | |||||||||||||||||||

| 70 | Household Finance Corp. | 4.125 | 11/16/09 | 68,311 | |||||||||||||||

| 170 | Household Finance Corp. | 8.00 | 07/15/10 | 182,098 | |||||||||||||||

| 600 | Sovereign Bancorp, Inc. | 5.59 | † | 03/23/10 | 600,176 | ||||||||||||||

| 685 | Washington Mutual Bank | 5.50 | 01/15/13 | 661,961 | |||||||||||||||

| 300 | Washington Mutual Preferred Funding II (a) | 6.665 | † | # | 262,837 | ||||||||||||||

| 1,775,383 | |||||||||||||||||||

| Tobacco (0.2%) | |||||||||||||||||||

| 105 | Reynolds American Inc. | 6.50 | 07/15/10 | 107,678 | |||||||||||||||

| Total Corporate Bonds (Cost $31,985,817) | 31,475,699 | ||||||||||||||||||

| U.S. Government Obligations (17.1%) | |||||||||||||||||||

| 2,310 | U.S. Treasury Bond (a) | 6.125 | 08/15/29 | 2,699,632 | |||||||||||||||

| 2,000 | U.S. Treasury Note (a) | 3.50 | 08/15/09 | 1,974,532 | |||||||||||||||

| 1,700 | U.S. Treasury Note (a) | 5.375 | 02/15/31 | 1,822,587 | |||||||||||||||

| 1,500 | U.S. Treasury Note (a) | 6.50 | 02/15/10 | 1,579,571 | |||||||||||||||

| Total U.S. Government Obligations (Cost $8,070,989) | 8,076,322 | ||||||||||||||||||

| Commercial Mortgage-Backed Securities (7.8%) | |||||||||||||||||||

| 200 | Banc of America Commercial Mortgage Inc. 2007-2 A4 | 5.866 | 04/10/49 | 200,325 | |||||||||||||||

| 200 | Banc of America Commercial Mortgage Inc. 2007-3 A4 | 5.838 | 06/10/49 | 199,538 | |||||||||||||||

| 250 | Bear Stearns Commercial Mortgage Securities Inc. 2007-PW16 A4 | 5.902 | 06/11/40 | 251,065 | |||||||||||||||

| 175 | Citigroup Commercial Mortgage Trust 2007-C6 A4 | 5.889 | 12/10/49 | 175,615 | |||||||||||||||

| 400 | Commercial Mortgage Pass-Through Certificate 2007-C9 A4 | 6.01 | 12/10/49 | 404,659 | |||||||||||||||

See Notes to Financial Statements

17

Morgan Stanley Income Trust

Portfolio of Investments n August 31, 2007 continued

| PRINCIPAL AMOUNT IN THOUSANDS | COUPON RATE | MATURITY DATE | VALUE | ||||||||||||||||

| $ | 150 | Greenwich Capital Commercial Funding Corp. 2007-GG9 A4 | 5.444 | % | 03/10/39 | $ | 147,132 | ||||||||||||

| 375 | GS Mortgage Securities Corporation II 2007-GG10 A4 | 5.993 | 08/10/45 | 378,608 | |||||||||||||||

| 125 | JP Morgan Chase Commercial Mortgage Securities 2007-CB18 A4 | 5.44 | 06/12/47 | 122,367 | |||||||||||||||

| 200 | JP Morgan Chase Commercial Mortgage Securities 2007-CB19 Class A4 | 5.937 | 02/12/49 | 200,772 | |||||||||||||||

| 275 | JP Morgan Chase Commercial Mortgage Securities Corp. 2007-LD11 A4 | 6.007 | 06/15/49 | 277,793 | |||||||||||||||

| 200 | LB Commercial Conduit Mortgage Trust 2007-C3 A4 | 6.134 | 07/15/44 | 204,242 | |||||||||||||||

| 125 | LB-UBS Commercial Mortgage Trust 2007-C2 A3 | 5.43 | 02/15/40 | 122,419 | |||||||||||||||

| 300 | Wachovia Bank Commercial Mortgage Trust 2007-C30 A5 | 5.342 | 12/15/43 | 291,548 | |||||||||||||||

| 400 | Wachovia Bank Commercial Mortgage Trust 2007-C32 A3 | 5.929 | 06/15/49 | 400,792 | |||||||||||||||

| 300 | Wachovia Bank Commercial Mortgage Trust 2007-C33 A4 | 6.10 | 02/15/51 | 305,845 | |||||||||||||||

| Total Commercial Mortgage-Backed Securities (Cost $3,603,550) | 3,682,720 | ||||||||||||||||||

| Asset-Backed Securities (3.6%) | |||||||||||||||||||

| 43 | CIT Equipment Collateral 2004-EF1 A3 | 3.50 | 09/20/08 | 42,548 | |||||||||||||||

| 58 | Ford Credit Auto Owner Trust 2005-B A3 | 4.17 | 01/15/09 | 57,891 | |||||||||||||||

| 400 | Ford Credit Auto Owner Trust 2007-A A3A | 5.40 | 08/15/11 | 400,623 | |||||||||||||||

| 375 | GS Auto Loan Trust 2007-1 A3 | 5.39 | 12/15/11 | 375,106 | |||||||||||||||

| 332 | Harley-Davidson Motorcycle Trust 2004-2 A2 | 3.56 | 02/15/12 | 327,477 | |||||||||||||||

| 2 | Volkswagen Auto Lease Trust 2005-A A3 | 3.82 | 05/20/08 | 2,346 | |||||||||||||||

| 500 | TXU Electric Delivery Transition Bond Co. LLC 2004-1 A2 | 4.81 | 11/17/14 | 495,342 | |||||||||||||||

| Total Asset-Backed Securities (Cost $1,709,524) | 1,701,333 | ||||||||||||||||||

| Collateralized Mortgage Obligations (1.1%) | |||||||||||||||||||

| 149 | American Home Mortgage Assets 2007-5 A3 | 5.805 | † | 06/25/47 | 133,512 | ||||||||||||||

| 75 | Countrywide Alternative Loan Trust 2006-0A16 M4 | 6.025 | † | 10/25/46 | 50,740 | ||||||||||||||

See Notes to Financial Statements

18

Morgan Stanley Income Trust

Portfolio of Investments n August 31, 2007 continued

| PRINCIPAL AMOUNT IN THOUSANDS | COUPON RATE | MATURITY DATE | VALUE | ||||||||||||||||

| $ | 75 | Harborview Mortgage Loan Trust 2006-8 B4 | 6.06 | † % | 08/21/36 | $ | 51,682 | ||||||||||||

| 75 | Luminent Mortgage Trust 2006-5 B1 | 5.865 | † | 07/25/36 | 65,475 | ||||||||||||||

| 125 | Mastr Adjustable Rate Mortgages Trust 2007-3 1M1 | 6.355 | † | 05/25/47 | 93,359 | ||||||||||||||

| 125 | Lehman XS Trust 2007-4N M4 | 6.505 | † | 03/25/47 | 99,688 | ||||||||||||||

| Total Collateralized Mortgage Obligations (Cost $500,160) | 494,456 | ||||||||||||||||||

| Foreign Government Obligations (0.7%) | |||||||||||||||||||

| MXN | 2,555 | Mexican Fixed Rate Bonds (Series M20) (Mexico) | 9.50 | 12/18/14 | 253,485 | ||||||||||||||

| $ | 92 | Republic of Argentina (Argentina)†† | 8.28 | 12/31/33 | 77,860 | ||||||||||||||

| Total Foreign Government Obligations (Cost $331,839) | 331,345 | ||||||||||||||||||

| U.S. Government Agencies - Mortgage-Backed Securities (0.1%) | |||||||||||||||||||

| 14 | Federal Home Loan Mortgage Corp. | 7.50 | 09/01/30 | 14,922 | |||||||||||||||

| 20 | Federal National Mortgage Association | 7.50 | 09/01/29 - 04/01/32 | 21,155 | |||||||||||||||

| Total U.S. Government Agencies - Mortgage-Backed Securities (Cost $36,366) | 36,077 | ||||||||||||||||||

| Short-Term Investments (22.7%) | |||||||||||||||||||

| U.S. Government Obligations (c) (0.3%) | |||||||||||||||||||

| U.S. Treasury Bills* | |||||||||||||||||||

| 10 | 4.55 | 01/10/08 | 9,839 | ||||||||||||||||

| 25 | 4.735 | 01/10/08 | 24,579 | ||||||||||||||||

| 100 | 4.845 | 01/10/08 | 98,277 | ||||||||||||||||

| Total U.S. Government Obligations (Cost $132,641) | 132,695 | ||||||||||||||||||

| Security Purchased from Securities Lending Collateral (21.4%) | |||||||||||||||||||

| 10,139 | The Bank of New York Institutional Cash Reserve Fund (Cost $10,139,043) | 10,139,043 | |||||||||||||||||

See Notes to Financial Statements

19

Morgan Stanley Income Trust

Portfolio of Investments n August 31, 2007 continued

| NUMBER OF SHARES (000) | VALUE | ||||||||||||||||||

| Investment Company (b) (1.0%) | |||||||||||||||||||

| 453 | Morgan Stanley Institutional Liquidity Money Market Portfolio - Institutional Class (Cost $453,071) | $ | 453,071 | ||||||||||||||||

| Total Short-Term Investments (Cost $10,724,755) | 10,724,809 | ||||||||||||||||||

| Total Investments (Cost $56,963,000) (d)(e) | 119.9 | % | 56,522,761 | ||||||||||||||||

| Liabilities in Excess of Other Assets | (19.9 | ) | (9,369,499 | ) | |||||||||||||||

| Net Assets | 100.0 | % | $ | 47,153,262 | |||||||||||||||

MTN Medium Term Note.

MXN Mexican New Peso.

WI Security purchased on a when-issued basis.

* A portion of this security has been physically segregated in connection with open futures contracts in an amount equal to $117,950.

** Resale is restricted to qualified institutional investors.

† Floating rate security, rate shown is the rate in effect at August 31, 2007.

†† Securities with a total market value equal to $77,860 have been valued at their fair value as determined in good determined in good faith under procedures established by and under the general supervision of the Fund's Trustees.

# Security issued with perpetual maturity.

## Foreign issued security with perpetual maturity.

(a) All or a portion of this security was on loan as of August 31, 2007.

(b) See Note 4 to the financial statements regarding investments in Morgan Stanley Institutional Liquidity Money Market Portfolio - Institutional Class.

(c) Purchased on a discount basis. The interest rate shown has been adjusted to reflect a money market equivalent yield.

(d) Securities have been designated as collateral in an amount equal to $23,651,180 in connection with open futures contracts and open swap contracts.

(e) The aggregate cost for federal income tax purposes is $57,420,400. The aggregate gross unrealized appreciation is $268,064 and the aggregate gross unrealized depreciation is $1,165,703 resulting in net unrealized depreciation of $897,639.

Futures Contracts Open at August 31, 2007:

| NUMBER OF CONTRACTS | LONG/SHORT | DESCRIPTION, DELIVERY MONTH AND YEAR | UNDERLYING FACE AMOUNT AT VALUE | UNREALIZED APPRECIATION (DEPRECIATION) | |||||||||||||||

| 50 | Long | U.S. Treasury Notes 5 Year, December 2007 | $ | 5,335,157 | $ | 18,057 | |||||||||||||

| 10 | Long | U.S. Treasury Notes 2 Year, December 2007 | 2,061,563 | 1,583 | |||||||||||||||

| 7 | Short | U.S. Treasury Bonds 20 Year, | (782,469 | ) | (17,301 | ) | |||||||||||||

| September 2007 | |||||||||||||||||||

| 20 | Short | U.S. Treasury Notes 10 Year, | (2,189,688 | ) | (8,796 | ) | |||||||||||||

| September 2007 | |||||||||||||||||||

| 51 | Short | U.S. Treasury Notes 10 Year, | (5,561,391 | ) | (3,471 | ) | |||||||||||||

| December 2007 | |||||||||||||||||||

| 67 | Short | U.S. Treasury Bonds 20 Year, December 2007 | (7,474,688 | ) | (21,331 | ) | |||||||||||||

| Net Unrealized Depreciation | $ | (31,259 | ) | ||||||||||||||||

See Notes to Financial Statements

20

Morgan Stanley Income Trust

Portfolio of Investments n August 31, 2007 continued

Credit Default Swap Contracts Open at August 31, 2007:

| SWAP COUNTERPARTY & REFERENCE OBLIGATION | BUY/SELL PROTECTION | NOTIONAL AMOUNT (000's) | PAY/RECEIVE FIXED RATE | TERMINATION DATE | UNREALIZED APPRECIATION (DEPRECIATION) | ||||||||||||||||||

| Goldman Sachs Capital Markets, LP Dow Jones CDX.NA.IG.HVOL.6 | Buy | $ | 1,200 | 0.75 | % | June 20, 2011 | $ | 20,200 | |||||||||||||||

| Goldman Sachs International Dow Jones CDX.NA.IG.HVOL.7 | Buy | 1,000 | 0.75 | December 20, 2011 | 20,940 | ||||||||||||||||||

| Goldman Sachs International Hartford Financial Services Group, Inc. | Buy | 550 | 0.12 | December 20, 2011 | 4,982 | ||||||||||||||||||

| Goldman Sachs International Motorola, Inc. | Buy | 180 | 0.15 | December 20, 2011 | 1,442 | ||||||||||||||||||

| Goldman Sachs International Motorola, Inc. | Buy | 360 | 0.157 | December 20, 2011 | 2,787 | ||||||||||||||||||

| Goldman Sachs International Union Pacific Corp. | Buy | 265 | 0.20 | December 20, 2011 | 1,273 | ||||||||||||||||||

| Citibank, N.A., New York Covidien Ltd. | Buy | 103 | 0.43 | March 20, 2012 | (479 | ) | |||||||||||||||||

| Citibank, N.A., New York Covidien Ltd. | Buy | 53 | 0.43 | March 20, 2012 | (247 | ) | |||||||||||||||||

| Citibank, N.A., New York Tyco Electronics Ltd. | Buy | 103 | 0.43 | March 20, 2012 | 542 | ||||||||||||||||||

| Citibank, N.A., New York Tyco Electronics Ltd. | Buy | 53 | 0.43 | March 20, 2012 | 280 | ||||||||||||||||||

| Citibank, N.A., New York Tyco International Ltd. | Buy | 103 | 0.43 | March 20, 2012 | 542 | ||||||||||||||||||

| Citibank, N.A., New York Tyco International Ltd. | Buy | 53 | 0.43 | March 20, 2012 | 280 | ||||||||||||||||||

| Goldman Sachs International Chubb Corp. | Buy | 510 | 0.10 | March 20, 2012 | 6,181 | ||||||||||||||||||

| Goldman Sachs International Dell Inc. | Buy | 255 | 0.22 | March 20, 2012 | 92 | ||||||||||||||||||

| Goldman Sachs International Gap, Inc. | Buy | 300 | 1.19 | March 20, 2012 | (2,864 | ) | |||||||||||||||||

| JP Morgan Chase Bank, N.A. Belo Corp. | Buy | 90 | 1.18 | June 20, 2014 | (493 | ) | |||||||||||||||||

| JP Morgan Chase Bank, N.A. Belo Corp. | Buy | 250 | 1.30 | June 20, 2014 | (3,050 | ) | |||||||||||||||||

| Bank of America, N.A. Centurytel, Inc. | Buy | 120 | 0.88 | September 20, 2017 | (649 | ) | |||||||||||||||||

| Net Unrealized Appreciation | $ | 51,759 | |||||||||||||||||||||

See Notes to Financial Statements

21

Morgan Stanley Income Trust

Portfolio of Investments n August 31, 2007 continued

| Interest Rate Swap Contracts Open at August 31, 2007: | |||||||||||||||||||||||

| SWAP COUNTERPARTY | NOTIONAL AMOUNT (000's) | PAYMENTS RECEIVED BY FUND | PAYMENTS MADE BY FUND† | TERMINATION DATE | UNREALIZED APPRECIATION | ||||||||||||||||||

| Deutsche Bank AG, New York | $ | 9,975 | Fixed Rate 5.389% | Floating Rate 5.505% | May 25, 2017 | $ | 123,391 | ||||||||||||||||

| Citibank N.A. New York | 1,475 | Fixed Rate 5.44 | Floating Rate 5.506 | May 29, 2017 | 23,969 | ||||||||||||||||||

| J.P. Morgan Chase N.A. New York | 1,500 | Fixed Rate 5.448 | Floating Rate 5.506 | May 29, 2017 | 25,290 | ||||||||||||||||||

| J.P. Morgan Chase N.A. New York | 5,350 | Fixed Rate 5.454 | Floating Rate 5.36 | June 4, 2017 | 90,415 | ||||||||||||||||||

| Total Unrealized Appreciation | $ | 263,065 | |||||||||||||||||||||

† Floating rate represents USD-3 months LIBOR.

See Notes to Financial Statements

22

Morgan Stanley Income Trust

Financial Statements

Statement of Assets and Liabilities

August 31, 2007

| Assets: | |||||||

| Investments in securities, at value (cost $56,509,929) (including $9,892,433 for securities loaned) | $ | 56,069,690 | |||||

| Investments in affiliate (cost $453,071) | 453,071 | ||||||

| Unrealized appreciation on open swap contracts | 322,606 | ||||||

| Cash | 973 | ||||||

| Receivable for: | |||||||

| Interest | 543,458 | ||||||

| Periodic interest on swap contracts | 257,371 | ||||||

| Variation margin | 37,033 | ||||||

| Shares of beneficial interest sold | 13,918 | ||||||

| Dividends from affiliate | 10,153 | ||||||

| Prepaid expenses and other assets | 33,713 | ||||||

| Total Assets | 57,741,986 | ||||||

| Liabilities: | |||||||

| Collateral on securities loaned at value | 10,139,043 | ||||||

| Unrealized depreciation on open swap contracts | 7,782 | ||||||

| Payable for: | |||||||

| Investments purchased | 119,659 | ||||||

| Periodic interest payment on swap contracts | 88,681 | ||||||

| Shares of beneficial interest redeemed | 63,706 | ||||||

| Distribution fee | 20,706 | ||||||

| Dividends | 11,632 | ||||||

| Administration fee | 3,199 | ||||||

| Transfer agent fee | 692 | ||||||

| Investment advisory fee | 140 | ||||||

| Accrued expenses and other payables | 133,484 | ||||||

| Total Liabilities | 10,588,724 | ||||||

| Net Assets | $ | 47,153,262 | |||||

| Composition of Net Assets: | |||||||

| Paid-in-capital | $ | 55,732,958 | |||||

| Net unrealized depreciation | (156,712 | ) | |||||

| Dividends in excess of net investment income | (399,766 | ) | |||||

| Accumulated net realized loss | (8,023,218 | ) | |||||

| Net Assets | $ | 47,153,262 | |||||

| Class A Shares: | |||||||

| Net Assets | $ | 24,967,422 | |||||

| Shares Outstanding (unlimited authorized, $.01 par value) | 2,703,061 | ||||||

| Net Asset Value Per Share | $ | 9.24 | |||||

| Maximum Offering Price Per Share, | |||||||

| (net asset value plus 4.44% of net asset value) | $ | 9.65 | |||||

| Class B Shares: | |||||||

| Net Assets | $ | 17,999,872 | |||||

| Shares Outstanding (unlimited authorized, $.01 par value) | 1,965,111 | ||||||

| Net Asset Value Per Share | $ | 9.16 | |||||

| Class C Shares: | |||||||

| Net Assets | $ | 3,328,426 | |||||

| Shares Outstanding (unlimited authorized, $.01 par value) | 362,683 | ||||||

| Net Asset Value Per Share | $ | 9.18 | |||||

| Class D Shares: | |||||||

| Net Assets | $ | 857,542 | |||||

| Shares Outstanding (unlimited authorized, $.01 par value) | 93,888 | ||||||

| Net Asset Value Per Share | $ | 9.13 | |||||

See Notes to Financial Statements

23

Morgan Stanley Income Trust

Financial Statements continued

Statement of Operations

For the year ended August 31, 2007

| Net Investment Income: Income | |||||||

| Interest | $ | 2,699,016 | |||||

| Dividends from affiliate | 24,239 | ||||||

| Income from securities loaned - net | 8,455 | ||||||

| Total Income | 2,731,710 | ||||||

| Expenses | |||||||

| Investment advisory fee | 214,331 | ||||||

| Distribution fee (Class A shares) | 64,667 | ||||||

| Distribution fee (Class B shares) | 174,052 | ||||||

| Distribution fee (Class C shares) | 30,299 | ||||||

| Shareholder reports and notices | 81,664 | ||||||

| Transfer agent fees and expenses | 73,338 | ||||||

| Professional fees | 67,204 | ||||||

| Registration fees | 54,119 | ||||||

| Administration fee | 40,825 | ||||||

| Custodian fees | 29,546 | ||||||

| Trustees' fees and expenses | 5,622 | ||||||

| Other | 23,360 | ||||||

| Total Expenses | 859,027 | ||||||

| Less: amounts waived/reimbursed | (181,596 | ) | |||||

| Less: expense offset | (453 | ) | |||||

| Net Expenses | 676,978 | ||||||

| Net Investment Income | 2,054,732 | ||||||

| Net Realized and Unrealized Gain (Loss): Net Realized Gain (Loss) on: | |||||||

| Investments | (228,705 | ) | |||||

| Futures contracts | (259,169 | ) | |||||

| Swap contracts | (209,670 | ) | |||||

| Foreign exchange transactions | 3,670 | ||||||

| Net Realized Loss | (693,874 | ) | |||||

| Net Change in Unrealized Appreciation/Depreciation on: | |||||||

| Investments | 290,015 | ||||||

| Futures contracts | (94,959 | ) | |||||

| Swap contracts | 314,824 | ||||||

| Translation of other assets and liabilities denominated in foreign curencies | (52 | ) | |||||

| Net Change in Unrealized Appreciation/Depreciation | 509,828 | ||||||

| Net Loss | (184,046 | ) | |||||

| Net Increase | $ | 1,870,686 | |||||

See Notes to Financial Statements

24

Morgan Stanley Income Trust

Financial Statements continued

Statements of Changes in Net Assets

| FOR THE YEAR ENDED AUGUST 31, 2007 | FOR THE YEAR ENDED AUGUST 31, 2006 | ||||||||||

| Increase (Decrease) in Net Assets: | |||||||||||

| Operations: | |||||||||||

| Net investment income | $ | 2,054,732 | $ | 2,478,624 | |||||||

| Net realized loss | (693,874 | ) | (548,116 | ) | |||||||

| Net change in unrealized appreciation/depreciation | 509,828 | (1,912,952 | ) | ||||||||

| Net Increase | 1,870,686 | 17,556 | |||||||||

| Dividends to Shareholders from Net Investment Income: | |||||||||||

| Class A shares | (1,218,023 | ) | (1,351,335 | ) | |||||||

| Class B shares | (833,233 | ) | (1,148,059 | ) | |||||||

| Class C shares | (145,780 | ) | (195,369 | ) | |||||||

| Class D shares | (44,560 | ) | (87,255 | ) | |||||||

| Total Dividends | (2,241,596 | ) | (2,782,018 | ) | |||||||

| Net decrease from transactions in shares of beneficial interest | (8,553,977 | ) | (19,844,812 | ) | |||||||

| Net Decrease | (8,924,887 | ) | (22,609,274 | ) | |||||||

| Net Assets: | |||||||||||

| Beginning of period | 56,078,149 | 78,687,423 | |||||||||

| End of Period (Including dividends in excess of net investment income of $399,766 and $468,099, respectively) | $ | 47,153,262 | $ | 56,078,149 | |||||||

See Notes to Financial Statements

25

Morgan Stanley Income Trust

Notes to Financial Statements n August 31, 2007

1. Organization and Accounting Policies

Morgan Stanley Income Trust (the "Fund") is registered under the Investment Company Act of 1940, as amended (the "Act"), as a diversified, open-end management investment company. The Fund's investment objective is high current income consistent with safety of principal. The Fund was organized as a Massachusetts business trust on September 1, 1988 and commenced operations on May 3, 1989. On July 28, 1997, the Fund converted to a multiple class share structure.

The Fund offers Class A shares, Class B shares, Class C shares and Class D shares. The four classes are substantially the same except that most Class A shares are subject to a sales charge imposed at the time of purchase and some Class A shares, and most Class B shares and Class C shares are subject to a contingent deferred sales charge imposed on shares redeemed within eighteen months, six years and one year, respectively. Class D shares are not subject to a sales charge. Additionally, Class A shares, Class B shares and Class C shares incur distribution expenses.

The Fund will assess a 2% redemption fee, on Class A shares, Class B shares, Class C shares, and Class D shares, which is paid directly to the Fund, for shares redeemed or exchanged within seven days of purchase, subject to certain exceptions. The redemption fee is designed to protect the Fund and its remaining shareholders from the effects of short-term trading.

The following is a summary of significant accounting policies:

A. Valuation of Investments — (1) certain portfolio securities may be valued by an outside pricing service approved by the Fund's Trustees; (2) portfolio securities for which over-the-counter market quotations are readily available are valued at the mean between the last reported bid and asked price; (3) futures are valued at the latest price published by the commodities exchange on which they trade; (4) credit default/interest rate swaps are marked-to-market daily based upon quotations from market markers and the change, if any, is recorded as unrealized appreciation or depreciation in the Statement of Operations; (5) when market quotations are not readily available including circumstances under which Morgan Stanley Investment Advisors Inc. (the "Investment Adviser") determines that the market quotations are not reflective of a security's market value, portfolio securities are valued at their fair value as determined in go od faith under procedures established by and under the general supervision of the Fund's Trustees; (6) investments in open-end mutual funds, including the Morgan Stanley Institutional Liquidity Funds, are valued at the net asset value as of the close of each business day; and (7) short-term debt securities having a maturity date of more than sixty days at time of purchase are valued on a mark-to-market basis until sixty days prior to maturity and thereafter at amortized cost based on their value on the 61st day. Short-term debt securities having a maturity date of sixty days or less at the time of purchase are valued at amortized cost.

26

Morgan Stanley Income Trust

Notes to Financial Statements n August 31, 2007 continued

B. Accounting for Investments — Security transactions are accounted for on the trade date (date the order to buy or sell is executed). Realized gains and losses on security transactions are determined by the identified cost method. Discounts are accreted and premiums are amortized over the life of the respective securities and are included in interest income. Interest income is accrued daily.

C. Multiple Class Allocations — Investment income, expenses (other than distribution fees), and realized and unrealized gains and losses are allocated to each class of shares based upon the relative net asset value on the date such items are recognized. Distribution fees are charged directly to the respective class.

D. Foreign Currency Translation and Forward Foreign Currency Contracts — The books and records of the Fund are maintained in U.S. dollars as follows: (1) the foreign currency market value of investment securities, other assets and liabilities and forward foreign currency contracts ("forward contracts") are translated at the exchange rates prevailing at the end of the period; and (2) purchases, sales, income and expenses are translated at the exchange rates prevailing on the respective dates of such transactions. The resultant exchange gains and losses are recorded as realized and unrealized gain/loss on foreign exchange transactions. Pursuant to U.S. federal income tax regulations, certain foreign exchange gains/losses included in realized and unrealized gain/loss are included in or are a reduction of ordinary income for federal income tax purposes. The Fund does not isolate that portion of the results of operations arising as a result of changes in the foreign exchange rates from the changes in the market prices of the securities. Forward contracts are valued daily at the appropriate exchange rates. The resultant unrealized exchange gains and losses are recorded as unrealized foreign currency gain or loss. The Fund records realized gains or losses on delivery of the currency or at the time the forward contract is extinguished (compensated) by entering into a closing transaction prior to delivery.

E. Futures Contracts — A futures contract is an agreement between two parties to buy and sell financial instruments or contracts based on financial indices at a set price on a future date. Upon entering into such a contract, the Fund is required to pledge to the broker cash, U.S. Government securities or other liquid portfolio securities equal to the minimum initial margin requirements of the applicable futures exchange. Pursuant to the contract, the Fund agrees to receive from or pay to the broker an amount of cash equal to the daily fluctuation in the value of the contract. Such receipts or payments known as variation margin are recorded by the Fund as unrealized gains and losses. Upon closing of the contract, the Fund realizes a gain or loss equal to the difference between the value of the contract at the time it was opened and the value at the time it was closed.

F. Credit Default Swaps — A credit default swap is an agreement between two parties to exchange the credit risk of an issuer. The Fund may purchase credit protection on the referenced obligation of the credit default swap ("Buy Contract"), or provide credit protection on the referenced obligation of the credit default swap ("Sale Contract"). A buyer of a credit default swap is said to buy protection by

27

Morgan Stanley Income Trust

Notes to Financial Statements n August 31, 2007 continued

paying periodic fees in return for a contingent payment from the seller if the issuer has a credit event such as bankruptcy, or a failure to pay outstanding obligations while the swap is outstanding. A seller of a credit default swap is said to sell protection and thus collects the periodic fees and profits if the credit of the issuer remains stable or improves while the swap is outstanding. If a credit event occurs, the seller pays to the buyer an agreed amount, which approximates the notional amount of the swap as disclosed in the table following the Portfolio of Investments. During the term of the swap agreement, the Fund receives or pays periodic fixed payments from or to the respective counterparty calculated at the agreed upon interest rate applied to the notional amount. These periodic payments are accrued daily and recorded as realized gains or losses in the Statement of Operations. In addition, upon termination of the s wap contract, gains and losses are also realized. Any upfront payment received or paid by the Fund is recorded as assets/liabilities on the Fund's books.

G. Interest Rate Swaps — Interest rate swaps involve the exchange of commitments to pay and receive interest based on notional principal amount. Net periodic interest payments to be received or paid are accrued daily and are recorded as realized gains or losses in the Statement of Operations.

H. Securities Lending — Fund may lend securities to qualified financial institutions, such as broker-dealers, to earn additional income. Any increase or decrease in the fair value of the securities loaned that might occur and any interest earned or dividends declared on those securities during the term of the loan would remain in the Fund. The Fund receives cash or securities as collateral in an amount equal to or exceeding 100% of the current fair value of the loaned securities. The collateral is marked-to-market daily, by the securities lending agent, to ensure that a minimum of 100% collateral coverage is maintained.

Based on pre-established guidelines, the securities lending agent invests any cash collateral that is received in high-quality short-term investments. Securities lending income is generated from the earnings on the invested collateral and borrowing fees, less any rebates owed to the borrowers and compensation to the lending agent.

The value of loaned securities and related collateral outstanding at August 31, 2007 were $9,892,433 and $10,139,043, respectively. The Fund received cash collateral which was subsequently invested in The Bank of New York Institutional Cash Reserve Fund as reported in the Portfolio of Investments. The Fund has the right under the lending agreement to recover the securities from the borrower on demand.

I. Federal Income Tax Policy — It is the Fund's policy to comply with the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute substantially all of its taxable income to its shareholders. Accordingly, no federal income tax provision is required.

28

Morgan Stanley Income Trust

Notes to Financial Statements n August 31, 2007 continued

J. Dividends and Distributions to Shareholders — Dividends and distributions to shareholders are recorded on the ex-dividend date.

K. Use of Estimates — The preparation of financial statements in accordance with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts and disclosures. Actual results could differ from those estimates.

2. Investment Advisory/Administration Agreements

Pursuant to an Investment Advisory Agreement with the Investment Adviser, the Fund pays the Investment Adviser an advisory fee, accrued daily and payable monthly, by applying the following annual rates to the net assets of the Fund determined as of the close of each business day: 0.42% to the portion of the daily net assets not exceeding $500 million; 0.35% to the portion of the daily net assets exceeding $500 million but not exceeding $1.25 billion; and 0.22% to the portion of the daily net assets exceeding $1.25 billion.

Pursuant to an Administration Agreement with Morgan Stanley Services Company Inc. (the "Administrator"), an affiliate of the Investment Adviser, the Fund pays an administration fee, accrued daily and payable monthly, by applying the annual rate of 0.08% to the Fund's daily net assets.

The Investment Adviser has agreed to cap the Fund's operating expenses (except for brokerage and 12b-1 fees) by assuming the Fund's "other expenses" and/or waiving the Fund's advisory fees, and the Administrator has agreed to waive the Fund's administrative fees, to the extent such operating expenses on an annualized basis exceed 0.80% of the average daily net assets of the Fund.

3. Plan of Distribution

Shares of the Fund are distributed by Morgan Stanley Distributors Inc. (the "Distributor"), an affiliate of the Investment Adviser and Administrator. The Fund has adopted a Plan of Distribution (the "Plan") pursuant to Rule 12b-1 under the Act. The Plan provides that the Fund will pay the Distributor a fee which is accrued daily and paid monthly at the following annual rates: (i) Class A — up to 0.25% of the average daily net assets of Class A shares; (ii) Class B — up to 0.85% of the lesser of: (a) the average daily aggregate gross sales of the Class B shares since the inception of the Fund (not including reinvestment of dividend or capital gain distributions) less the average daily aggregate net asset value of the Class B shares redeemed since the Fund's inception upon which a contingent deferred sales charge has been imposed or waived; or (b) the average daily net assets of Class B shares; and (iii) Class C — u p to 0.85% of the average daily net assets of Class C shares.

In the case of Class B shares, provided that the Plan continues in effect, any cumulative expenses incurred by the Distributor but not yet recovered may be recovered through the payment of future

29

Morgan Stanley Income Trust

Notes to Financial Statements n August 31, 2007 continued

distribution fees from the Fund pursuant to the Plan and contingent deferred sales charges paid by investors upon redemption of Class B shares. Although there is no legal obligation for the Fund to pay expenses incurred in excess of payments made to the Distributor under the Plan and the proceeds of contingent deferred sales charges paid by investors upon redemption of shares, if for any reason the Plan is terminated, the Trustees will consider at that time the manner in which to treat such expenses. The Distributor has advised the Fund that such excess amounts totaled $4,102,384 at August 31, 2007.

In the case of Class A shares and Class C shares, expenses incurred pursuant to the Plan in any calendar year in excess of 0.25% or 0.85% of the average daily net assets of Class A or Class C, respectively, will not be reimbursed by the Fund through payments in any subsequent year, except that expenses representing a gross sales credit to Morgan Stanley Financial Advisors and other authorized financial representatives at the time of sale may be reimbursed in the subsequent calendar year. For the year ended August 31, 2007, the distribution fee was accrued for Class A shares and Class C shares at the annual rate of 0.25% and 0.85%, respectively.

The Distributor has informed the Fund that for the year ended August 31, 2007, it received contingent deferred sales charges from certain redemptions of the Fund's Class B shares and Class C shares of $46,806 and $578, respectively and received $8,928 in front-end sales charges from sales of the Fund's Class A shares. The respective shareholders pay such charges which are not an expense of the Fund.

4. Security Transactions and Transactions with Affiliates