QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14D-9

SOLICITATION/RECOMMENDATION STATEMENT

UNDER SECTION 14(D)(4) OF THE SECURITIES EXCHANGE ACT OF 1934

NORTH COAST ENERGY, INC.

(Name of Subject Company)

NORTH COAST ENERGY, INC.

(Name of Person(s) Filing Statement)

COMMON STOCK, PAR VALUE $0.01 PER SHARE

(Title of Class of Securities)

658649 70 2

(CUSIP Number of Class of Securities)

Gordon O. Yonel

President and Chief Executive Officer

North Coast Energy, Inc.

1993 Case Parkway

Twinsburg, Ohio 44087-2343

(330) 425-2330

(Name, Address and Telephone Number of Person

Authorized to Receive Notices and Communications

on Behalf of the Person(s) Filing Statement)

COPIES TO:

| Dean A. Swift General Counsel and Secretary North Coast Energy, Inc. 1993 Case Parkway Twinsburg, Ohio 44087-2343 (330) 425-2330 | Michael D. Phillips Calfee, Halter & Griswold LLP 1400 McDonald Investment Center 800 Superior Avenue Cleveland, Ohio 44114 (216) 622-8200 |

o Check the box if the filing relates solely to preliminary communications made before the commencement of a tender offer.

Item 1. Subject Company Information.

The name of the subject company to which this Solicitation/Recommendation Statement on Schedule 14D-9 (this "Statement") relates is North Coast Energy, Inc., a Delaware corporation (the "Company"). The address of the principal executive offices of the Company is 1993 Case Parkway, Twinsburg, Ohio 44087-2343. The telephone number of the principal executive offices of the Company is (330) 425-2330.

The title of the class of equity securities to which this Statement relates is the common stock, par value $0.01 per share, of the Company (the "Common Stock"). As of the close of business on December 3, there were 15,251,806 shares of Common Stock issued and outstanding, 432,678 shares of Common Stock were reserved for issuance pursuant to outstanding stock options or stock incentive rights, 140,400 shares of Common Stock were reserved for issuance pursuant to outstanding warrants.

Item 2. Identity and Background of Filing Person.

The name, business address and business telephone number of the Company, which is the subject company and the person filing this Statement, are set forth in Item 1 above, which information is incorporated herein by reference.

This Statement relates to the tender offer by NCE Acquisition, Inc., a Delaware corporation ("Purchaser") and a wholly owned subsidiary of EXCO Resources, Inc., a Texas corporation ("Parent"), disclosed in a Tender Offer Statement on Schedule TO filed by Purchaser and Parent, dated December 5, 2003 (as amended from time to time, the "Schedule TO") to purchase all of the outstanding shares of Common Stock at a purchase price of $10.75 per share, in cash (the "Offer Price"), and on the terms and subject to the conditions set forth in the Offer to Purchase, dated December 5, 2003 (the "Offer to Purchase"), and in the related Letter of Transmittal (which, as may be amended or supplemented from time to time, together constitute the "Offer"). Copies of the Offer to Purchase and the Letter of Transmittal are filed as Exhibits (a)(1) and (a)(2) hereto, respectively, and incorporated by reference. Copies of the Offer to Purchase and the Letter of Transmittal are being furnished to Company stockholders concurrently with this Statement.

The Offer is being made pursuant to the Agreement and Plan of Merger, dated November 26, 2003, as amended and restated on December 4, 2003 (the "Merger Agreement"), by and among Parent, Purchaser, the Company and, for certain specified purposes, Nuon Energy & Water Investments, Inc., a Delaware corporation ("Seller") and the holder of approximately 85.6% of the Common Stock. The Merger Agreement, among other things, provides that, subject to the satisfaction or waiver of certain conditions, following the consummation of the Offer and in accordance with the relevant provisions of the Delaware General Corporation Law (the "DGCL"), Purchaser will be merged with and into the Company (the "Merger"). Following the effective time of the Merger (the "Effective Time"), the Company will continue as the surviving corporation (the "Surviving Corporation") and a wholly owned subsidiary of Parent.

In the Merger, each share of Common Stock outstanding at the Effective Time (other than shares of Common Stock held by Parent, Purchaser or any other wholly owned subsidiary of Parent, the Company, or any wholly owned subsidiary of the Company, which will be cancelled, and other than the shares of Common Stock, if any, held by holders of Common Stock who have properly demanded and perfected their appraisal rights under Section 262 of the DGCL) will, by virtue of the Merger and without any action on the part of the holders of Common Stock, be converted into the right to receive the Offer Price, or any greater amount per share of Common Stock paid pursuant to the Offer, without interest. The Merger Agreement is more fully described in "Section 10. Background of the Offer; the Merger Agreement and Related Agreements" of the Offer to Purchase, which is filed herewith as Exhibit (a)(1) and is incorporated herein by reference.

1

Pursuant to the Merger Agreement, Purchaser commenced the Offer on December 5, 2003. The Offer is currently scheduled to expire at 12:00 midnight, New York City time, on January 23, 2004 (the "Expiration Time"), unless extended by Purchaser or the Company in accordance with the Merger Agreement and the Securities Exchange Act of 1934, as amended (the "Exchange Act") and the rules promulgated thereunder.

Seller has engaged in discussions with Parent and has agreed (subject to the supervisory board approval of its ultimate parent) to enter into a Stock Tender Agreement (the "Tender Agreement") with Parent and Purchaser, within seven days after the Schedule TO is filed with the Securities and Exchange Commission (the "Commission"), pursuant to which Seller will agree, in its capacity as the majority stockholder of the Company, to tender all of its shares of Common Stock, with certain limited exceptions, as well as any additional shares of Common Stock which it may acquire (pursuant to stock options or otherwise), with certain limited exceptions, to Purchaser in the Offer. As of November 24, 2003, Seller held 13,048,277 shares of Common Stock, which represented approximately 85.6% of the outstanding shares of Common Stock. The Tender Agreement is more fully described in "Section 10. Background of the Offer; the Merger Agreement and Related Agreements" of the Offer to Purchase, which is filed herewith as Exhibit (a)(1) and is incorporated herein by reference.

Seller and Parent will make a joint election to have the transaction contemplated by the Merger Agreement, including the Offer and the Merger (the "Transaction"), taxed pursuant to an election pursuant to Section 338(h)(10) of the Internal Revenue Code of 1986, as amended, and the regulations promulgated thereunder and any analogous provisions of applicable state, local and foreign tax law (collectively, the "Section 338(h)(10) Election"). Seller will pay any tax attributable to making the Section 338(h)(10) Election and will indemnify Parent, Purchaser and the Company from such tax liability. In order to cover Seller's tax liability, Seller will enter into an Escrow Agreement (the "Escrow Agreement") with Parent and Citibank, N.A., as escrow agent, within seven days after the Schedule TO is filed with the Commission, to facilitate the payment of such tax liability and remit any balance of deposited funds to Seller. The Escrow Agreement is more fully described in "Section 10. Background of the Offer; the Merger Agreement and Related Agreements" of the Offer to Purchase, which is filed herewith as Exhibit (a)(1) and is incorporated herein by reference.

As described above, Seller is, or will be, a party to the Merger Agreement, the Tender Agreement and the Escrow Agreement, and has agreed to undertake indemnification and other certain obligations under such agreements. Seller is indirectly owned by n.v. NUON, a Dutch company with limited liability ("NUON") and as part of, and to help facilitate the Merger Agreement, NUON has agreed to enter into an Unconditional Guaranty Agreement (the "Guaranty Agreement") with Parent within seven days after the Schedule TO is filed with the Commission. Pursuant to the Guaranty Agreement, NUON will unconditionally guarantee Seller's performance of all of Seller's obligations under the Merger Agreement, the Tender Agreement and the Escrow Agreement, including but not limited to, Seller's indemnity obligations and the prompt payment of obligations of Seller.

Pursuant to the Merger Agreement, in the event that Parent terminates the Merger Agreement because Seller and/or NUON has not timely delivered the Tender Agreement, Escrow Agreement, Guaranty Agreement and an acceptable opinion from Seller's counsel, then the amount of the expense fee payable to Parent will be $4.5 million. In such event, Seller has agreed to reimburse the Company for $3.2 million of such $4.5 million, and NUON has guaranteed Seller's obligation to make such reimbursement payment to the Company, pursuant to the terms and conditions of the Expense Reimbursement Agreement, dated November 26, 2003 (the "Reimbursement Agreement").

Copies of the Merger Agreement, form of the Tender Agreement, form of the Escrow Agreement, form of Guaranty Agreement and Reimbursement Agreement are filed herewith as Exhibits (e)(1), (e)(2), (e)(3), (e)(4) and (e)(5), respectively, and are incorporated herein by reference. A copy of the

2

press release issued by the Company on November 26, 2003 is filed herewith as Exhibit (a)(6) and is incorporated herein by reference.

Purchaser has not conducted any activities since its organization, other than those related to the acquisition. As set forth in the Schedule TO, the principal executive offices of Parent and Purchaser are located at 6500 Greenville Avenue, Suite 600, Dallas, Texas 75206. The telephone number of Parent and Purchaser at that address is (214) 368-2084.

Item 3. Past Contacts, Transactions, Negotiations and Agreements.

General

Certain contracts, agreements, arrangements or understandings between the Company or its affiliates and certain of its directors and executive officers and between the Company and Parent and Purchaser are described in the Information Statement pursuant to Section 14(f) of the Exchange Act and Rule 14f-1 thereunder (the "Information Statement") that is attached as Annex A to this Statement and is incorporated herein by reference.

Except as set forth in this Item 3 or in the Information Statement or as incorporated by reference herein, to the knowledge of the Company, as of the date hereof, there are no material agreements, arrangements or understandings and no actual or potential conflicts of interest between the Company or its affiliates and (i) the Company or its executive officers, directors or affiliates or (ii) Parent, Purchaser or their respective executive officers, directors or affiliates.

Interests of Executive Officers, Directors and Affiliates

Employment Agreements with Executive Officers, Directors and Affiliates

The Company has entered into employment agreements with certain of its executive officers. The Merger Agreement provides that the Company will make commercially reasonable efforts to obtain and deliver to Parent the resignation of certain directors of the Company and its subsidiaries and such officers of the Company and its subsidiaries as Parent requests, except that, as more fully described in "Section 10. Background of the Offer; the Merger Agreement and Related Agreements" of the Offer to Purchase, which is filed herewith as Exhibit (a)(1) and is incorporated herein by reference, and in the Information Statement, which discussion is incorporated herein by reference, under certain circumstances up to two of the Company's current directors will remain on the Company's Board of Directors (the "Board of Directors" or the "Board") from the closing of the tender offer through the Effective Time.

Change in Control Protection Agreements with Executive Officers

The Company has entered into Change in Control Protection Agreements with Gordon O. Yonel, its President and Chief Executive Officer, Dale E. Stitt, its Chief Financial Officer and Treasurer, Lawrence J. Risley, its Vice President for Exploration and Production, and Dean A. Swift, its General Counsel and Secretary, that provide for certain severance payments that may be triggered by the termination of their employment in connection with the Merger. These agreements are discussed in more detail in the Information Statement under the caption "Certain Agreements-Change in Control Agreements," which discussion is incorporated herein by reference. Assuming that the Merger is consummated at December 31, 2003 and these agreements are triggered, the following executive officers would receive the following amounts (including gross-up payments resulting from the imposition of excise taxes or a reduction in payments resulting from or to avoid the imposition of excise taxes): Mr. Yonel, $1,612,875 Mr. Stitt, $603,855; Mr. Risley, $91,211; and Mr. Swift, $0.

3

Management Retention Bonus Program

Messrs. Yonel, Stitt, Risley and Swift also participate in the Company's Management Retention Bonus Program, under the terms of which they will be entitled (i) to receive specified percentages of their base salaries for each three month period subsequent to March 21, 2003 during which they remain in the employ of the Company (each a "Stay Bonus") and (ii) to receive a percentage of the total transaction value attributable to any change in control set aside in a separate account (the "Management Retention Bonus Pool") in accordance with a specified formula set forth in the program (which amount will be offset by the Stay Bonus described in clause (i) above). The terms of the plan are described in more detail in the Information Statement under the caption "Certain Agreements—Change in Control Agreements," which discussion is incorporated herein by reference.

Assuming that the Merger is consummated at December 31, 2003, each of the following executive officers will have received the following aggregate amounts in connection with Stay Bonuses from March 21, 2003 through December 31, 2003: Mr. Yonel, $125,550; Mr. Stitt, $67,813; Mr. Risley, $32,550 and Mr. Swift, $46,500. Additionally, each of the following executive officers will receive the following amounts in connection with the Management Retention Bonus Pool (such amounts include offsets for the foregoing Stay Bonus amounts and gross-up payments resulting from the imposition of excise taxes, or a reduction in payments resulting from or to avoid the imposition of excise taxes): Mr. Yonel, $2,645,789; Mr. Stitt, $1,772,289; Mr. Risley, $282,071 and Mr. Swift, $384,588.

Confidentiality Agreement

On June 13, 2003, Parent and Robert W. Baird & Co., Incorporated ("Baird"), as agent for the Company, entered into a confidentiality agreement in connection with Parent's evaluation of the Company and the Company's provision of certain information to Parent (the "Confidentiality Agreement"). The Confidentiality Agreement is filed herewith as Exhibit (e)(6) and is incorporated herein by reference.

Effect of the Transaction on Stock Option Plans

The Merger Agreement provides that the Company has agreed to use its commercially reasonable efforts to cause all holders of an option to purchase shares of Common Stock, whether granted under the Company's 1999 Employee Stock Option Plan, 1988 Stock Option Plan, 2000 Key Employee Stock Bonus Plan and the Key Employees Stock Bonus Plan or otherwise issued or granted (including non-plan grants, a "Company Option"), to execute prior to the Expiration Time an option surrender agreement (a "Surrender Agreement"). A form of Surrender Agreement is filed herewith as Exhibit (e)(8) and is incorporated herein by reference.

The Merger Agreement also provides that on the date Purchaser pays for any shares of Common Stock tendered pursuant to the Offer, Purchaser will pay to such holders who have previously delivered a Surrender Agreement the cash amount equal to the product of (i) the total number of shares of Common Stock subject to such Company Option (irrespective of whether such option is then exercisable) and (ii) the amount by which the Offer Price exceeds the exercise or strike price per share of Common Stock subject to such Company Option, less any required withholding taxes.

The Merger Agreement further specifies that in the event that any holder of a Company Option fails to deliver a Surrender Agreement prior to the Expiration Time, the Company will use its commercially reasonable efforts to cause such holder's Company Options (the "Outstanding Options") to be converted without any action on the part of the holder thereof into the right to receive Merger Consideration upon the exercise of such holder's Company Options in accordance with, and within the time period prescribed by, the applicable stock plan and the holder's stock option agreement(s). The Merger Agreement provides that the Purchaser will pay to each holder of Outstanding Options, the Merger Consideration, less any required withholding taxes, as promptly as practicable after receiving a

4

valid exercise of such Outstanding Options. All other stock plans and any other plan, program or arrangement providing for the issuance or grant of any other interest in respect of the capital stock of the Company or any subsidiary will terminate as of the Effective Time except with respect to any rights granted prior to the date hereof. Upon the consummation of the Merger, the aggregate amount to be received by all holders of Company Options (including, Outstanding Options) will be up to $2,548,651. The following amounts will be payable to each of the Company's executive officers and to all directors and executive officers as a group: Mr. Yonel, $744,380; Mr. Stitt, $489,248; Mr. Risley, $185,522; Mr. Swift $187,756; and all directors and executive officers as a group, $1,967,711.

Effect of the Transaction on Warrants

The Merger Agreement provides that the Company has agreed to use its commercially reasonable efforts to cause all holders of any and all outstanding warrants to purchase shares of Common Stock (the "Warrants") to execute prior to the Expiration Time a warrant relinquishment and release agreement (a "Warrant Relinquishment and Release Agreement"). A form of Warrant Relinquishment and Release Agreement is filed herewith as Exhibit (e)(9) and is incorporated herein by reference.

The Merger Agreement also provides that on the date Purchaser pays for any shares of Company Stock tendered pursuant to the Offer, Purchaser will pay to such holders who have previously delivered a Warrant Relinquishment and Release Agreement the cash amount equal to the product of (i) the total number of shares of Common Stock subject to such Warrant (irrespective of whether such warrant is then exercisable) and (ii) the amount by which the Offer Price exceeds the exercise price per share of Common Stock subject to such Warrant, less any required withholding taxes.

The Merger Agreement further specifies that in the event that any holder of a Warrant fails to deliver a Warrant Relinquishment and Release Agreement prior to the Expiration Time, the Company will use its commercially reasonable efforts to cause such holder's Warrants (the "Outstanding Warrants") to be converted without any action on the part of the holder thereof into the right to receive Merger Consideration upon the exercise of such holder's Warrants in accordance with, and within the time period prescribed by, the applicable warrant agreement(s). The Merger Agreement provides that the Purchaser will pay to each holder of Outstanding Warrants, the Merger Consideration, less any required withholding taxes, as promptly as practicable after receiving a valid exercise of such Outstanding Warrants. All other warrant agreements, program or arrangement providing for the issuance or grant of any other interest in respect of the capital stock of the Company or any subsidiary will terminate as of the Effective Time except with respect to any rights granted prior to the date hereof. Upon the consummation of the Merger, the aggregate amount to be received by all holders of Warrants (including, Outstanding Warrants) will be up to $857,550. No executive officer or director is a holder of any Warrants.

Effect of the Transaction on Employee Compensation and Benefit Plans

The Merger Agreement provides that all employees of the Company and its subsidiaries who continue employment with Parent, Purchaser, or any subsidiary of Purchaser after the Effective Time ("Continuing Employees") will be eligible to continue to participate in health or welfare benefit plans provided by the Surviving Corporation. The Merger Agreement also provides that Parent or Purchaser can terminate any such health or welfare benefit plan at any time (including as of the Effective Time). If these health or welfare benefit plans are terminated, then the employees will be immediately eligible to participate in Parent's health and welfare plans to substantially the same extent as similarly situated employees of Parent.

The Merger Agreement provides that Parent will cause the Surviving Corporation to honor, pay and perform all of the liabilities and obligations of the Company or any of its subsidiaries under or in respect of (i) each employment, retention, severance, indemnity, termination or similar agreements with

5

any current or former officer, director or other employee of the Company or any Subsidiary and (ii) each incentive compensation, deferred compensation or other equity based plan or arrangement of the Company covering any director, officer or other employee of the Company and its subsidiaries, in each case, in accordance with the terms thereof as in effect on the date hereof.

Parent also will cause the amount of any bonus or other incentive compensation which is payable to any officer or other employee of the Company or its subsidiaries for the fiscal year 2003 to be determined under the terms of the applicable bonus or incentive compensation plans of the Company or any of its subsidiaries as in effect as of the date of the Merger Agreement. In addition, Parent shall permit the Company, by appropriate action of the Company's Board of Directors, prior to or at the Effective Time to make provision for the funding of any such bonus or other incentive compensation, which bonus shall be paid on or after April 1, 2004, although the manner and terms of any trust or similar funding mechanism must be reasonably acceptable to Parent.

The Merger Agreement also provides that if any current or former officer or other employee of the Company or its subsidiaries becomes eligible to participate in any compensation or benefit plan, agreement or arrangement maintained by Parent or Purchaser, Parent shall, to the extent permitted by law or the terms of such plans, cause (i) all service of such current or former officer or other employee completed prior to the Effective Time with the Company or any of its Subsidiaries to be recognized under such plan, agreement or arrangement for eligibility and vesting purposes thereof, (ii) to be waived, any exclusions for pre-existing conditions of any such current or former officer or other employee and his or her dependents, and (iii) to be recognized, all co-payments, deductibles or similar amounts or costs incurred by any such current officer or employee under a comparable plan, agreement or arrangement of the Company, any subsidiary of the Company during the plan year in which such officer or other employee commences participation in an applicable benefit plan, agreement or arrangement of Parent or any subsidiary thereof.

Indemnification and Insurance

The Company's bylaws and certificate of incorporation provide that certain of the directors and officers of the Company (the "Indemnified Persons") have rights to indemnification existing in their favor. The Merger Agreement provides that, for the acts and omissions of the Indemnified Persons occurring prior to the Effective Time, these indemnification rights will survive the Merger and will be observed by the Surviving Corporation to the fullest extent available under Delaware law for a period of six years from the Effective Time.

For a period of not less than six years after the Effective Time, the Merger Agreement provides that the Parent shall cause to be maintained in effect the current policies of directors' and officers' liability insurance maintained by the Company, or substitute policies providing at least the same coverage and amounts and containing terms and conditions which are not less advantageous, in each case with respect to claims arising from facts or events which occurred at or prior to the Effective Time.

The Merger Agreement provides that proper provisions will be made so that the successors and assigns of Parent assume the indemnification and insurance obligations described above in the event Parent or any of its successors or assigns (i) consolidates with or merges into any other person and shall not be the continuing or surviving corporation of such consolidation or merger, or (ii) transfers or conveys all or substantially all of its properties and assets to any person.

Representation on the Board

The Merger Agreement sets forth certain agreements between the Company and Parent, subject to compliance with Section 14(f) of the Exchange Act and Rule 14f-1 promulgated thereunder, regarding the election by Parent of directors to the Company's Board of Directors upon acceptance of shares of

6

Common Stock for payment pursuant to the Offer. These agreements are described in the Information Statement, which description is incorporated herein by reference.

Merger Agreement

A summary of the Merger Agreement and a description of the conditions of the Offer are contained in "Section 10. Background of the Offer; the Merger Agreement and Related Agreements" and "Section 14. Certain Conditions of the Offer" of the Offer to Purchase, which is filed herewith as Exhibit (a)(1) and is incorporated herein by reference. Such summary and description are qualified in their entirety by reference to the Merger Agreement, which is filed herewith as Exhibit (e)(1) and is incorporated herein by reference.

Ancillary Agreements

A summary of the Tender Agreement, the Escrow Agreement and the Guaranty Agreement is contained in "Section 10. Background of the Offer; the Merger Agreement and Related Agreements" and "Section 14. Certain Conditions of the Offer" of the Offer to Purchase, which is filed herewith as Exhibit (a)(1) and is incorporated herein by reference. Each such summary is qualified in its entirety by reference to the form of Tender Agreement, form of Escrow Agreement, form of Guaranty Agreement and Reimbursement Agreement, which are filed herewith as Exhibits (e)(2), (e)(3), (e)(4) and (e)(5), respectively, and are incorporated herein by reference.

Item 4. The Solicitation or Recommendation.

Recommendation of the Board

On November 25, 2003, at a meeting of the Board at which all directors were present, the Board unanimously determined that the Merger Agreement and the transactions contemplated thereby, including the Offer and the Merger, are fair to and in the best interests of the stockholders of the Company, approved and adopted the Merger Agreement and the transactions contemplated thereby, including the Offer and the Merger, in accordance with the DGCL and declared that the Merger Agreement is advisable. Accordingly, the Board unanimously recommends and advises that the stockholders of the Company accept the Offer and tender their shares of Common Stock to Purchaser and adopt the Merger Agreement if required under applicable law.

A letter to the stockholders of the Company communicating the Board's recommendation is filed herewith as Exhibit (a)(7) and is incorporated herein by reference.

Background

In October 2001, Douglas H. Miller, Chairman and Chief Executive Officer of Parent, contacted Gordon O. Yonel to discuss the prospects of a potential transaction between Parent and the Company. Mr. Yonel indicated that he did not know if the Board would entertain an offer. On November 6, 2001, Mr. Miller and Ted Eubank, President of Parent, met with Mr. Yonel to further discuss a potential transaction. On November 16, 2001, Parent sent a letter to Mr. Carel Kok, the then Chairman of the Board of the Company, indicating Parent's interest in pursuing a potential transaction between the two companies. These initial discussions did not advance past this stage and were abandoned at that time.

At the March 21, 2003 Board of Directors meeting, the Board determined that it would be advisable for the Company to evaluate strategic alternatives, including a possible sale of the Company. That decision was based upon a request by Seller to explore methods of enhancing value for the stockholders of the Company.

At this meeting the Board also authorized management to retain the firm of Baird as its financial advisor to assist the Company in evaluating and pursuing strategic alternatives. The Company retained

7

Baird pursuant to an engagement letter dated April 9, 2003. The Company issued a press release announcing Baird's retention on April 21, 2003.

At a June 11, 2003 meeting, the Board authorized Baird to identify and solicit indications of interest from potential buyers. Beginning in June 2003, Baird held discussions with 67 parties identified as potential strategic and financial buyers. These potential buyers were identified by Baird and Company's senior management based upon a number of considerations, including their position in the U.S. oil and gas exploration and production industry, potential interest in acquisitions of businesses such as the Company, familiarity with or interest in the Appalachian region and financial ability to consummate a transaction with the Company.

Representatives of Baird made a presentation at the Board's July 22, 2003, meeting summarizing the progress and status of the discussions with potentially interested parties.

Eighteen parties expressed an interest in a possible transaction, signed confidentiality agreements and received summary due diligence materials concerning the Company's business, operations and financial condition. In July 2003, Baird requested interested parties to submit written, non-binding indications of interest to the Company. On July 17, 2003, indications of interest were received from six parties, including Parent. An additional party submitted a late indication of interest with a range of $10.80 - $11.90 but determined soon thereafter that it was unable to continue with the process. The range of all indicative offers was $7.50 - $11.90. The Board of Directors, in a meeting on July 22, 2003, reviewed the indications received and instructed Baird to invite five of the parties to continue discussions and attend management presentations and review additional non-public information about the Company's business, operations, properties and financial condition.

At the Board's September 12, 2003 meeting Baird provided an updated process review. Calfee, Halter & Griswold LLP, the Company's outside counsel, also reviewed with the directors their fiduciary responsibilities. The Board was also advised that the Seller was willing to make a Section 338(h)(10) Election in connection with the transaction and to assume 100% of the tax liability that would be borne by shareholders as a result of such an election. By allowing a buyer to step-up its basis in the Company's assets to the purchase price, such an election could provide favorable tax consequences to a buyer that might contribute to a higher valuation for the Company in the event of a sale.

The Board authorized Baird to instruct interested parties to submit definitive proposals by September 16, 2003. Potential purchasers were requested to provide comments on a draft merger agreement prepared on behalf of the Company and the Seller and were also advised to consider the possibility of a Section 338(h)(10) Election in submitting their proposals. Four parties submitted definitive proposals with bids ranging from $8.50 per share to $10.26 per share, with Parent submitting a proposal of $10.06 per share, subject to additional environmental and title due diligence, and other conditions.

At a September 24, 2003 Board meeting, Baird summarized the key aspects of each of the four proposals, including pricing, financing arrangements, the status of outstanding due diligence and anticipated timing. Counsel also reviewed with the directors the mark-ups of the draft merger agreement received from each bidder. Baird provided the Board with preliminary input concerning how the prices offered by the various bidders compared with a price range implied by various valuation methodologies. The Board determined that Baird should contact each of the four bidders to ascertain if their proposals could be improved and to confirm the status of their due diligence, financing, and other conditions. Each of the bidders submitted a revised proposal with bids ranging from $8.65 to $10.75.

On October 2, 2003, the Board met via telephone conference. At this Board meeting, the Board discussed each of the four revised proposals and their relative merits with its legal and financial advisors. Baird reviewed each of the four proposals in detail discussing price, key terms, status of due diligence, conditions, financing and open items. Two of the parties had improved their proposals with

8

respect to specific terms but had increased their prices only slightly. Parent increased its offer from $10.06 to $10.75 per share, while another bidder increased its offer from $10.26 to $10.35 per share. That other bidder ultimately determined that it would not be able to increase the price of its proposal and discussions between the Company and that bidder were discontinued.

Because the prices specified in the revised proposals were below the recent market prices for shares of Common Stock and because of volatility in the trading of the Common Stock, the Board also discussed with its legal and financial advisors the advisability of issuing a press release. A press release concerning these matters was issued on October 6, 2003.

From early October 2003 through November 21, 2003, the Company and its legal and financial advisors negotiated the terms of the Merger Agreement with Parent and its advisors. Parent and its advisors also negotiated the terms of the various agreements (including the provisions of the Merger Agreement to which Seller is a party) described herein and in the Offer to Purchase with Seller and its advisors.

On November 17, 2003, the Board met to discuss the status of negotiations and the remaining open issues.

On November 18, 2003, the Company received a revised offer from one of the other bidders, which increased its price to $10.50 per share. The bid was subject to additional due diligence and financing conditions.

Final negotiations among Seller, the Company and Parent were held on November 20, 2003, and on November 21, 2003, the various agreements had reached a point where they could be submitted to the Board for its final consideration.

On November 25, 2003, the Board met to consider the Merger Agreement and the various transactions contemplated by that agreement. At that meeting, the Company's legal and financial advisors reviewed with the Board the terms and conditions of the Merger Agreement and the various ancillary agreements, including the Tender Agreement, the Escrow Agreement and the Reimbursement Agreement. In addition, the Board reviewed the terms and conditions of the Parent's financing commitments. The Board also received a presentation from Baird concerning the financial aspects of the transaction and, at the Board's request, Baird rendered its opinion that the consideration to be received in the transaction was fair, from a financial point of view, to the Company's common stockholders (other than Parent or its affiliates).

On December 4, 2003, Parent, Purchaser, the Company and Seller entered into an Amended and Restated Merger Agreement, to amend certain sections to reflect the closing of the Offer in 2004.

Reasons for the Recommendation of the Board

In approving the Merger Agreement and the Transaction, and recommending that all holders of Common Stock accept the Offer and tender their shares of Common Stock pursuant to the Offer, the Board considered a number of factors, including:

1. Historical and Recent Trading Activity. The Board considered the relationship of the Offer Price to the recent and historical market prices and trading activity of shares of Common Stock. As part of this, the Board considered that the Offer Price represents (a) a discount of 10.7% to the closing price of the Common Stock reported by the Nasdaq National Market on November 21, 2003, (b) a premium of 92.0% to the closing price of shares of Common Stock reported by the Nasdaq National Market on April 21, 2003, the date that the Company announced that it had retained Baird to assist it in exploring strategic alternatives, (c) a premium of 0.1% to the average closing price of shares of Common Stock reported by the Nasdaq National Market for the six month period prior to November 21, 2003, (d) a premium of 32.6% to the average closing price of shares of Common Stock reported by the Nasdaq National Market for the 12 month period prior to November 21, 2003, and (e) a premium of 205.4% to the lowest closing price of shares of Common Stock reported by the Nasdaq National Market for the 12 month period prior to November 21, 2003. The Board considered these periods the most relevant to demonstrate the recent performance of shares of Common Stock.

9

2. Alternative Structures. The Board evaluated various alternative transaction structures and concluded that a forward cash merger (whereby the Company would merge with and into a subsidiary of an acquiror and the acquiror's subsidiary would be the surviving corporation) would not be commercially feasible due to the nature of the Company's business and certain of its assets and properties.

3. Company Operating and Financial Condition. The Board considered the current and historical financial condition and results of operations of the Company, as well as the prospects and strategic objectives of the Company, including the risks involved in achieving those prospects and objectives as an independent entity, and the current and expected conditions in the industry in which the Company operates.

4. Solicitation Process. The Board considered the results of the process that was undertaken by the Board and its legal and financial advisors to identify and negotiate with prospective purchasers of the Company. The Board noted that the Parent's proposal was the result of a process in which 67 potential strategic and financial buyers were contacted regarding their interest in the Company. The Board also took into account the results of the due diligence, bidding and negotiation process which culminated in Parent's submission of the highest proposal for the Company's Common Stock.

5. Terms and Conditions of the Merger Agreement. The Board considered the terms and conditions of the Transaction, including the amount of consideration to be received by the Company's stockholders, the parties' representations, warranties and covenants, conditions to their respective obligations and the ability of the Company, Parent and Purchaser to terminate the Offer and the Merger.

6. Financing Commitments. The Board considered the terms and conditions of the financing commitments received by Parent with respect to the transaction contemplated by the Merger Agreement.

7. Financing Representation. The Board considered Parent's and Purchaser's representation in the Merger Agreement that Parent has and will have through the Effective Time sufficient funds (including funding to be made available pursuant to its commitment letter from Credit Suisse First Boston and Bank One, N.A.) to permit Purchaser to consummate the transactions contemplated by the Merger Agreement. The Board also noted that the Merger Agreement will require Parent to pay the Company a termination fee of $6.0 million and expenses of up to $1.3 million if the Merger Agreement is terminated due to its inability to obtain financing.

8. Consents. The Board considered that there are no material third party consents required by the Company to consummate the Merger as structured.

9. Indicia of Seller Support. The Board considered the willingness of Seller (subject to the supervisory board approval of its ultimate parent) to enter into the Merger Agreement with respect to certain provisions, the Tender Agreement and tender its shares of Common Stock pursuant to the Offer and the various undertakings to be made and agreements to be entered into by the Seller in connection with the Section 338(h)(10) Election.

10. Timing to Completion. The Board considered the anticipated timing of the Transaction, including the structure of the Transaction as a cash tender offer for all of the outstanding shares of Common Stock to be followed by a short-form merger if 90% of the shares of the Company's Common Stock are validly tendered and not withdrawn pursuant to the Offer.

11. Certainty of Value. The Board considered the form of consideration to be paid to holders of Common Stock in the Offer and the Merger, and the certainty of value of such cash consideration compared to stock or other possible forms of consideration. The Board was aware that the

10

consideration received by holders of Common Stock in the Offer and Merger could be taxable to such holders for income tax purposes.

12. Negotiated Price. The Board considered that, in its judgment, based on the solicitation process and the extended arm's-length negotiations with Parent and Purchaser, that the Offer Price represented the highest price that Parent would be willing to pay in acquiring the Company.

13. Fairness Opinion of Baird. The Board considered the presentation from Baird and the opinion of Baird delivered to the Board that, as of November 25, 2003 and based on and subject to the matters stated in such opinion, the $10.75 in cash per share proposed to be received by holders of Common Stock in the Offer and the Merger (other than Parent or its affiliates) is fair from a financial point of view to such holders. Detailed information regarding Baird's analysis and fairness opinion is presented below. A copy of the opinion of Baird that was delivered to the Board setting forth the assumptions made, procedures followed, matters considered and limits on the review undertaken by Baird in arriving at its opinion, is attached hereto as Annex B and is incorporated herein. Baird's opinion, addressed to the Board, relates only to the fairness, from a financial point of view, of the $10.75 in cash per share to be received by stockholders (other than Parent or its affiliates) and does not constitute an opinion or recommendation to any stockholder as to whether or not such stockholder should tender shares in the Offer, how a stockholder should vote at the stockholders' meeting, if any, held in connection with the Merger, or as to any other matters relating to the Offer or the Merger. Stockholders are urged to read this opinion in its entirety. The Board was aware of and considered that certain fees described in Item 5 below become payable to Baird upon the consummation of the Transaction.

14. Alternative Transactions. The Board considered that the Merger Agreement permits the Company to (1) consider an unsolicited acquisition proposal under certain circumstances and (2) recommend any such proposal that is superior to the Offer and the Merger, if, among other things, (a) the Board determines in good faith that the acquisition proposal is more favorable to the Company's stockholders (based on factors the Board deems relevant, including the additional time necessary to consummate the competing acquisition proposal and the financial advice of the Company's financial advisors that the value of the consideration is superior in the competing acquisition proposal), (b) financing, to the extent required, is (based on the opinion of the Company's financial advisors) reasonably capable of being obtained, (c) after consultation with the Company's legal advisors, the Board determines the failure to take any such action would be a breach of the Board's fiduciary duties, (d) the Company gives Parent three business days notice, and (e) the Company pays Parent a termination fee in the amount of $6.0 million, plus expenses not to exceed $1.3 million. The Board considered the possible effect of these provisions of the Merger Agreement on third parties who might be interested in exploring an acquisition of the Company.

15. The Company's Future Prospects. The Board considered that all holders of shares of Common Stock (except for Parent and Purchaser) whose shares are purchased in the Offer will not participate in the Company's future growth. Because of the risks and uncertainties associated with the Company's future prospects, the Board concluded that this detriment was not reasonably quantifiable. The Board also concluded that obtaining a substantial cash payment for shares of Common Stock now was preferable to affording the stockholders a speculative potential future return.

16. Potential Conflicts of Interest. The Board considered that the interests of certain persons, including Company executives, in the Merger may be different from those of the stockholders (see Item 3 above in this Statement).

11

The Board also considered a number of uncertainties and risks in its deliberations concerning the Transaction:

1. The circumstances under the Merger Agreement in which the termination fee of $6.0 million becomes payable by the Company, and the circumstances under the Merger Agreement in which the Company is required to reimburse Parent's expenses incurred in connection with the Merger Agreement, up to $1.3 million.

2. The fact that the amount of the Company's expense reimbursement obligations would increase to $4.5 million if the Merger Agreement is terminated because of the failure of the Seller to deliver the Tender Agreement, the Guaranty Agreement, the Escrow Agreement or the legal opinion of counsel to Seller, and that the Company would be required to obtain reimbursement of amounts in excess of $1.3 million from the Seller in accordance with the terms of the Reimbursement Agreement.

3. The fact that under the terms of the Merger Agreement, between the execution of the Merger Agreement and the Effective Time, the Company is required to obtain Parent's consent before it can take specified actions.

4. The conditions to Purchaser's and Parent's obligations to purchase Common Stock in the Offer, and the possibility that such conditions might not be satisfied.

5. The possibility that, although the Offer gives stockholders the opportunity to realize a premium over the price at which shares of Common Stock traded historically prior to the public announcement of the Offer and the Merger, the price or value of shares of Common Stock may increase in the future if the Company were to remain an independent company, and that Company stockholders would not benefit from those future increases.

The Board believed that these risks were outweighed by the potential benefits of the Offer and the Merger.

In view of the variety of factors considered in connection with its evaluation of the Merger Agreement, the Board found it impracticable to, and did not, quantify, rank or otherwise assign relative weights to the factors considered or determine that any factor was of particular importance in reaching its determination that the Merger Agreement and the transactions contemplated thereby are advisable to, and in the best interests of, the Company's stockholders. Rather, the decision of each Board member was based upon his own judgment, in light of the totality of the information presented and considered, of the overall effect of the Merger Agreement and the transactions contemplated thereby, including the Offer and the Merger, on the Company's stockholders. After weighing all of these considerations, the Board unanimously approved the Merger Agreement and the transactions contemplated thereby and recommends that the holders of shares of Common Stock tender such shares in the Offer and adopt the Merger Agreement if required under applicable law.

Summary of the Financial Analysis and Opinion of Financial Advisor

As previously disclosed, the Company retained Baird to act as its exclusive financial advisor in connection with the possible sale or disposition of the Company. In connection with this engagement, the Board requested that Baird render an opinion as to the fairness, from a financial point of view, of the Offer Price to be paid to the holders of Common Stock of the Company (other than Parent and its affiliates) pursuant to the Transaction. On November 25, 2003, Baird rendered its oral opinion (which was subsequently confirmed in writing) to the Board to the effect that, as of such date, and based upon and subject to the assumptions, limitations and qualifications contained in its opinion, the consideration was fair, from a financial point of view, to the holders of Common Stock (other than Parent and its affiliates).

12

THE FULL TEXT OF BAIRD'S WRITTEN OPINION, DATED NOVEMBER 25, 2003, IS ATTACHED AS ANNEX B AND IS INCORPORATED BY REFERENCE IN THIS DOCUMENT. BAIRD'S OPINION IS DIRECTED ONLY TO THE FAIRNESS, AS OF THE DATE OF THE OPINION AND FROM A FINANCIAL POINT OF VIEW, OF THE CONSIDERATION TO THE COMPANY'S COMMON STOCKHOLDERS (OTHER THAN PARENT AND ITS AFFILIATES) AND DOES NOT CONSTITUTE A RECOMMENDATION TO ANY STOCKHOLDER AS TO HOW SUCH STOCKHOLDER SHOULD ACT WITH RESPECT TO THE TRANSACTION. BAIRD'S OPINION DOES NOT ADDRESS ANY OTHER ASPECT OF THE TRANSACTION, NOR DOES THE OPINION ADDRESS THE RELATIVE MERITS OF THE TRANSACTION OR ANY OTHER POTENTIAL TRANSACTIONS OR BUSINESS STRATEGIES CONSIDERED BY THE COMPANY'S BOARD OF DIRECTORS. THE SUMMARY OF BAIRD'S OPINION SET FORTH BELOW IS QUALIFIED IN ITS ENTIRETY BY REFERENCE TO THE FULL TEXT OF SUCH OPINION ATTACHED AS ANNEX B. COMPANY STOCKHOLDERS ARE URGED TO READ THE OPINION CAREFULLY AND IN ITS ENTIRETY.

In conducting its investigation and analyses and in arriving at its opinion, Baird reviewed information and took into account financial and economic factors it deemed relevant under the circumstances. In that connection, Baird, among other things:

- •

- reviewed certain internal information, primarily financial in nature, including projections, concerning the business and operations of the Company furnished to it for purposes of its analysis;

- •

- reviewed publicly available information including but not limited to the Company's recent filings with the Commission;

- •

- reviewed the draft Merger Agreement, draft Escrow Agreement and draft Tender Agreement in the forms presented to the Company's Board of Directors;

- •

- reviewed the historical market prices and trading activity of the Common Stock and compared it with the historical market prices of certain other publicly traded companies that Baird deemed relevant;

- •

- compared the financial position and operating results of the Company with those of other publicly traded companies that Baird deemed relevant and considered the trading multiples of such companies;

- •

- compared the proposed financial terms of the Transaction with the financial terms of certain other business combinations that Baird deemed relevant;

- •

- prepared discounted cash flow analyses with respect to the Company using financial projections provided by the Company's senior management;

- •

- was requested to, and did, solicit third party indications of interest in acquiring the Company;

- •

- held discussions with members of the Company's senior management concerning the Company's historical and current financial condition and operating results, as well as the future prospects of the Company; and

- •

- considered such other information, financial studies, analysis and investigations and financial, economic and market criteria that Baird deemed relevant for the preparation of its opinion.

In arriving at its opinion, Baird assumed and relied upon the accuracy and completeness of all of the financial and other information obtained from public sources or provided to it by or on behalf of the Company, and did not attempt to independently verify any such information. Baird assumed, with the Company's consent, that: (i) all material assets and liabilities (contingent or otherwise, known or unknown) of the Company were as set forth in the Company's financial statements, and (ii) the

13

Transaction will be consummated in accordance with the terms of the draft Merger Agreement in the form presented to the Company's Board of Directors, without waiver, modification or amendment of any term or condition set forth therein. Baird also assumed that the financial forecasts examined by it were reasonably prepared on bases reflecting the best available estimates and good faith judgments of the Company's senior management as to future performance of the Company. The Company informed Baird, and Baird assumed, that a Section 338(h)(10) Election will be made with respect to the Transaction. Baird's opinion does not address the tax effect of making the Section 338(h)(10) Election on any of the Company's stockholders or any other tax effect on the Company's stockholders with respect to the Transaction, including Seller's indemnification obligations under the Merger Agreement or any of the terms of the Escrow Agreement.

In conducting its review, Baird did not undertake nor obtain an independent evaluation or appraisal of any of the assets or liabilities (contingent or otherwise) of the Company nor did it make a physical inspection of the properties or facilities of the Company. Baird's opinion does not address the relative merits of the Transaction or any other potential transactions or business strategies considered by the Company's Board of Directors. Baird's opinion necessarily is based upon economic, monetary and market conditions as they existed and could be evaluated on the date of Baird's opinion, and Baird's opinion did not predict or take into account any changes that have occurred or which may occur, or information that has or may become available, after the date of Baird's opinion. The Offer Price was determined by arms' length negotiations between the parties to the Agreement.

The following is a summary of the material factors considered and principal financial analyses performed by Baird to arrive at its opinion. Baird performed certain procedures, including each of the financial analyses described below, and reviewed with the Company's senior management and Board of Directors the assumptions upon which such analyses were based, as well as other factors. This summary is not intended to be an exhaustive description of the analyses performed by Baird, but includes all material factors considered by Baird in rendering it opinion.

Process Review. Baird considered the events that resulted in the negotiation of the Transaction, including the 8-month process that was undertaken by the Company's Board of Directors and its legal and financial advisors to identify and negotiate with prospective purchasers of the Company. Baird also considered the Company's public disclosures regarding the initiatives taken by the Company's Board of Directors to maximize stockholder value. In connection with this process, Baird held discussions with 67 potential parties regarding the sale of the Company, and of those parties, 18 entered into confidentiality agreements with the Company and reviewed summary due diligence materials about the Company's operations and financial condition. Of those 18 parties, five also reviewed data room materials with respect to the Company's operations and financial condition and attended presentations by the Company's senior management.

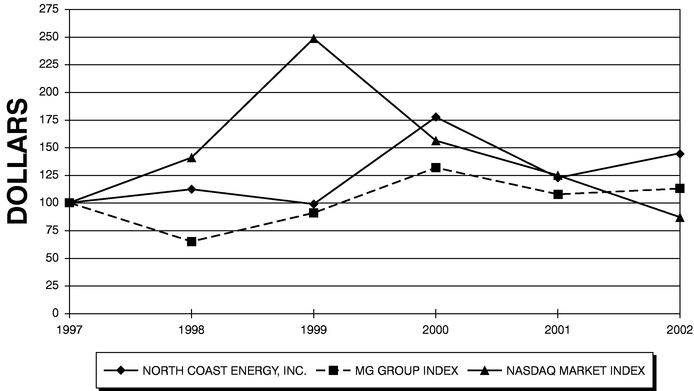

Historical Stock Price Performance Analysis. Baird analyzed the closing stock prices of the Company's Common Stock over the last twelve months ended November 21, 2003, including the period since the announcement of the engagement of Baird by the Company on April 21, 2003. Based on this analysis, Baird determined the following values of the Company's Common Stock during this period. These compare with the Offer Price of $10.75.

| High | $ | 13.61 | |

| Low | $ | 3.52 | |

| Average | $ | 8.11 | |

| Last 6-Month Average | $ | 10.74 | |

| Close on April 21, 2003 | $ | 5.60 | |

| Close on November 21, 2003 | $ | 12.04 |

14

The following table summarizes the implied per share value for the Company's Common Stock derived from the analyses indicated, all of which are described in greater detail below. These compare with the Offer Price of $10.75.

| | Implied Company Per Share Equity Values | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Low | Average | Median | High | ||||||||

| Comparable Public Company Analysis | $ | 4.56 | $ | 9.61 | $ | 9.66 | $ | 14.11 | ||||

| Comparable Corporate Transactions Analysis | $ | 4.15 | $ | 9.83 | $ | 10.10 | $ | 15.48 | ||||

| Discounted Cash Flow Analyses | $ | 6.31 | $ | 9.19 | $ | 9.37 | $ | 11.54 | ||||

Analysis of Implied Transaction Multiples. Based on the Offer Price, Baird calculated the implied "equity value" (defined as the Offer Price multiplied by the total number of common shares outstanding of the Company as of September 30, 2003, including shares issuable upon the exercise of stock options and warrants, less cash proceeds from the exercise of stock options and warrants) to be $167.4 million. Baird then calculated the multiple of the equity value to the Company's latest twelve months ended September 30, 2003 ("LTM") cash flows from operations (defined as the Company's net income plus depletion, depreciation, amortization, deferred taxes and other non-cash items excluding changes in working capital) ("CFFO"). In addition, Baird calculated the implied "enterprise value" (defined as the implied equity value plus the book value of total debt, less cash and equivalents as of September 30, 2003) to be $207.4 million. Baird then calculated the multiples of the enterprise value to (1) the Company's LTM earnings before interest, taxes, depletion, depreciation and amortization ("EBITDA") and projected 2003 EBITDA, as provided by the Company's senior management; (2) the Company's proved reserves in Million cubic feet equivalent ("Mcfe") as of June 30, 2003; and (3) the Company's LTM average daily production in Mcfe and projected 2003 and 2004 average daily production in Mcfe, as provided by the Company's management. Such multiples are summarized in the table below, which is qualified in its entirety by reference to the other disclosures contained in this section and Annex B.

| | Implied Transaction Multiples | |||

|---|---|---|---|---|

| Enterprise Value / LTM EBITDA | 5.8 | x | ||

| Enterprise Value / 2003P EBITDA | 5.3 | x | ||

| Equity Value / LTM CFFO | 5.0 | x | ||

| Enterprise Value / Proved Reserves as of June 30, 2003 ($/Mcfe) | $ | 1.09 | ||

| Enterprise Value / LTM Average Daily Production ($/Mcfe) | $ | 6,695 | ||

| Enterprise Value / 2003P Average Daily Production ($/Mcfe) | $ | 6,552 | ||

| Enterprise Value / 2004P Average Daily Production ($/Mcfe) | $ | 6,257 | ||

Comparable Public Company Analysis. Baird reviewed certain publicly available financial information as of the most recently reported period and stock market information as of November 21, 2003 for eight selected publicly traded companies that Baird deemed relevant. The group of selected publicly traded companies reviewed is listed below.

- •

- Brigham Exploration Company

- •

- Carrizo Oil & Gas, Inc.

- •

- Clayton Williams Energy, Inc.

- •

- Comstock Resources, Inc.

- •

- KCS Energy, Inc.

15

- •

- The Meridian Resource Corporation

- •

- Panhandle Royalty Company

- •

- Range Resources Corporation

The selected companies were chosen because they are publicly traded companies with general business, operating and financial characteristics considered to be comparable to the Company's based on the Company's participation in the oil and gas exploration and production industry. Baird noted that none of the companies reviewed is identical to the Company and that, accordingly, the analysis of such companies necessarily involves complex considerations and judgments concerning differences in the business, financial and operating characteristics of each company and other factors that affect the market values of such companies.

Baird calculated multiples as of November 21, 2003 of each selected company's implied "equity value" (defined as the closing market price per share of each company's common stock multiplied by the total number of common shares outstanding of such company, including net shares issuable upon the exercise of stock options and warrants) to its LTM CFFO. In addition, Baird calculated each selected company's implied "enterprise value" (defined as the equity value of each company, plus the latest publicly available book value of total debt, preferred stock and minority interests, less cash and equivalents) to each company's LTM EBITDA, 2003 projected EBITDA, LTM average daily production in Mcfe and 2003 and 2004 projected average daily production in Mcfe. Projected data was obtained from various publicly available equity research reports. Baird then compared the multiples implied in the Transaction with the corresponding trading multiples for the selected companies. A summary of such multiples is provided in the table below, which is qualified in its entirety by reference to the other disclosures contained in this section and Annex B.

| | | Implied Selected Public Company Trading Multiples | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Implied Transaction Multiples | |||||||||||||||

| | Low | Average | Median | High | ||||||||||||

| Enterprise Value / LTM EBITDA | 5.8 | x | 3.0 | x | 5.0 | x | 5.0 | x | 6.4 | x | ||||||

| Enterprise Value / 2003P EBITDA | 5.3 | x | 3.9 | x | 4.9 | x | 4.8 | x | 6.1 | x | ||||||

| Equity Value / LTM CFFO | 5.0 | x | 2.1 | x | 3.9 | x | 3.7 | x | 5.5 | x | ||||||

| Enterprise Value / LTM Avg. Daily Production ($/Mcfe) | $ | 6,695 | $ | 4,727 | $ | 6,445 | $ | 6,496 | $ | 8,301 | ||||||

| Enterprise Value / 2003P Avg. Daily Production ($/Mcfe) | $ | 6,552 | $ | 4,634 | $ | 6,502 | $ | 6,427 | $ | 8,231 | ||||||

| Enterprise Value / 2004P Avg. Daily Production ($/Mcfe) | $ | 6,257 | $ | 4,372 | $ | 5,737 | $ | 6,091 | $ | 6,578 | ||||||

In addition, Baird calculated the implied per share equity values as of November 21, 2003 for the Company's Common Stock based on the trading multiples of the selected public companies and compared such values to the Offer Price of $10.75. The implied per share equity values, based on the multiples that Baird deemed relevant, are summarized in the table below, which is qualified in its entirety by reference to the other disclosures contained in this section and Annex B.

| | Implied Company Per Share Equity Values | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Low | Average | Median | High | ||||||||

| Enterprise Value / LTM EBITDA | $ | 4.56 | $ | 8.90 | $ | 9.07 | $ | 12.07 | ||||

| Enterprise Value / 2003P EBITDA | $ | 7.41 | $ | 9.79 | $ | 9.62 | $ | 12.72 | ||||

| Equity Value / LTM CFFO | $ | 4.66 | $ | 8.39 | $ | 7.99 | $ | 11.83 | ||||

| Enterprise Value / LTM Avg. Daily Production ($/Mcfe) | $ | 6.90 | $ | 10.26 | $ | 10.36 | $ | 13.89 | ||||

| Enterprise Value / 2003P Avg. Daily Production ($/Mcfe) | $ | 6.91 | $ | 10.65 | $ | 10.50 | $ | 14.11 | ||||

| Enterprise Value / 2004P Avg. Daily Production ($/Mcfe) | $ | 6.80 | $ | 9.66 | $ | 10.40 | $ | 11.42 | ||||

16

Comparable Corporate Transactions Analysis. Baird reviewed certain publicly available financial information concerning 14 corporate transactions that were announced since January 1, 2000 in the exploration and production industry that Baird deemed relevant. The group of selected corporate transactions is listed below.

| Target | Acquirer | |

|---|---|---|

| United States Exploration, Inc. | DGL Acquisition Corp. | |

| PetroCorp Incorporated | Unit Corporation | |

| Carbon Energy Corp. | Evergreen Resources, Inc. | |

| EXCO Resources, Inc. | Management Group | |

| 3TEC Energy Corporation | Plains Exploration & Production Co. | |

| Esenjay Exploration, Inc. | Santos Ltd. | |

| Prize Energy Corp. | Magnum Hunter Resources, Inc. | |

| DevX, Energy Inc. | Comstock Resources, Inc. | |

| Synergy Oil & Gas, Inc. | Penn Virginia Corporation | |

| Hallwood Energy Corp. | Pure Resources, Inc. | |

| Classic Resources | 3TEC Energy Corporation | |

| Southern Mineral Corporation | PetroCorp Incorporated | |

| Gothic Energy Corporation | Chesapeake Energy Corporation | |

| Peake Energy, Inc. | North Coast Energy, Inc. |

These selected corporate transactions were chosen because they involve companies that possessed general business, operating and financial characteristics considered to be comparable to the Company's based on the Company's participation in the oil and gas exploration and production industry. Baird noted that none of the selected corporate transactions or subject target companies reviewed is identical to the Transaction or the Company, respectively, and that, accordingly, the analysis of such corporate transactions necessarily involves complex considerations and judgments concerning differences in the business, financial and operating characteristics of each subject target company and each corporate transaction and other factors that affect the values implied in such corporate transactions.

Baird calculated multiples of each corporate transaction's implied "equity value" (defined as the per share purchase price for each target company's common stock multiplied by the total number of common shares outstanding of such company, including net shares issuable upon the exercise of stock options and warrants or, in the case of private companies, defined as the value attributable to the equity of a target company) to each target company's LTM CFFO based on financial information available as of the respective transaction announcement dates. In addition, Baird calculated multiples of each corporate transaction's implied "enterprise value" (defined as the equity value of each target company, plus the book value of the target company's total debt, preferred stock and minority interests, less cash and equivalents) to each target company's LTM EBITDA and LTM average daily production in Mcfe based on information available as of the respective transaction announcement dates. Baird also calculated multiples of each corporate transaction's implied enterprise value to each target company's proved reserves based on information available as of the announcement date of the applicable transaction. Certain outlier multiples were deemed not applicable or meaningful. Baird then compared the multiples implied in the Transaction with the corresponding corporate transaction multiples for the

17

selected corporate transactions. A summary of such multiples is provided in the table below, which is qualified in its entirety by reference to the other disclosures contained in this section and Annex B.

| | | Implied Selected Comparable Corporate Transaction Multiples | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Implied Transaction Multiples | |||||||||||||||

| | Low | Average | Median | High | ||||||||||||

| Enterprise Value / LTM EBITDA | 5.8 | x | 3.6 | x | 6.0 | x | 6.6 | x | 7.8 | x | ||||||

| Equity Value / LTM CFFO | 5.0 | x | 2.9 | x | 5.1 | x | 5.3 | x | 7.2 | x | ||||||

| Enterprise Value / Proved Reserves ($/Mcfe) | $ | 1.09 | $ | 0.87 | $ | 1.05 | $ | 0.98 | $ | 1.37 | ||||||

| Enterprise Value / LTM Avg. Daily Production ($/Mcfe) | $ | 6,695 | $ | 3,322 | $ | 4,786 | $ | 4,824 | $ | 6,256 | ||||||

In addition, Baird calculated the implied per share equity values for the Company's Common Stock based on the multiples of the selected corporate transactions and compared such values to the Offer Price of $10.75. The implied per share equity values, based on the multiples that Baird deemed relevant, are summarized in the table below, which is qualified in its entirety by reference to the other disclosures contained in this section and Annex B.

| | Implied Company Per Share Equity Values | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Low | Average | Median | High | ||||||||

| Enterprise Value / LTM EBITDA | $ | 5.74 | $ | 11.25 | $ | 12.53 | $ | 15.29 | ||||

| Equity Value / LTM CFFO | $ | 6.40 | $ | 10.88 | $ | 11.46 | $ | 15.48 | ||||

| Enterprise Value / Proved Reserves ($/Mcfe) | $ | 8.05 | $ | 10.18 | $ | 9.33 | $ | 14.03 | ||||

| Enterprise Value / LTM Avg. Daily Production ($/Mcfe) | $ | 4.15 | $ | 7.01 | $ | 7.09 | $ | 9.89 | ||||

Discounted Cash Flow Analyses. Baird performed discounted cash flow analyses of the Company's projected unlevered free cash flows (defined as net income excluding after-tax net interest, plus depreciation and amortization, less capital expenditures and increases in working capital) from 2004 to 2008 on a stand-alone basis, as provided by the Company's senior management. Baird applied two methodologies for calculating the terminal value portion of the overall enterprise value (1) multiples of 4.5x to 5.5x applied to EBITDA in the year 2008; and (2) growth rates to perpetuity of 4.0% to 5.0% applied to the free cash flow in the year 2008. In such analyses, Baird calculated the present values of the unlevered free cash flows and terminal values by discounting such amounts to December 31, 2003 at rates ranging from 10% to 12% based on its judgment of the weighted average cost of capital of comparable companies. The summation of the present values of the unlevered free cash flows and the present values of the terminal values produced equity values ranging from $6.31 to $11.54 per share, as compared to the Offer Price of $10.75.

The discounted cash flow analysis of the Company does not necessarily indicate actual value or actual future results and does not purport to reflect the prices at which any securities may trade at the present or at any time in the future. Discounted cash flow analysis is a widely used valuation methodology, but the results of this methodology are highly dependent on numerous assumptions that must be made, including the discount rates applied and terminal values.

The foregoing summary does not purport to be a complete description of the analyses performed by Baird or of its presentations to the Company's Board of Directors. The preparation of financial analyses and a fairness opinion is a complex process and is not necessarily susceptible to partial analyses or summary description. Baird believes that its analyses (and the summary set forth above) must be considered as a whole, and that selecting portions of such analyses and any of the factors considered by Baird, without considering all of such analyses and factors, could create an incomplete view of the processes underlying the analyses conducted by Baird and its opinion. Baird did not attempt to assign specific weights to particular analyses. Any estimates contained in Baird's analyses are not necessarily indicative of actual values, which may be significantly more or less favorable than as set

18

forth therein. Estimates of values of companies do not purport to be appraisals or necessarily to reflect the prices at which companies may actually be sold. Because such estimates are inherently subject to uncertainty, Baird does not assume responsibility for their accuracy.

In the ordinary course of its business, Baird may from time to time trade the securities of the Company for its own account or the accounts of its customers and, accordingly, may at any time hold long or short positions in such securities.

Intent to Tender

To the knowledge of the Company, after reasonable inquiry, each executive officer and director of the Company who owns shares of Common Stock currently intends, subject to contractual obligations and compliance with applicable law, including Section 16(b) of the Exchange Act, to tender all outstanding shares of Common Stock held of record or beneficially owned by such person to Purchaser in the Offer. Additionally, Seller who holds approximately 85.6% of the outstanding shares of Common Stock as of November 24, 2003, has agreed (subject to the supervisory board approval of its ultimate parent) to enter into the Tender Agreement within seven days after the Schedule TO is filed with the Commission pursuant to which Seller will agree, in its capacity as the majority stockholder of the Company, to tender all of its shares of Common Stock, with certain limited exceptions, as well as any additional shares of Common Stock which it may acquire, with certain limited exceptions, to Purchaser in the Offer. See Item 2 above.

Item 5. Person/Assets, Retained, Employed, Compensated or Used.

The Company retained Baird to render an opinion to the Board as to the fairness, from a financial point of view, of the consideration proposed to be received pursuant to a transaction with Parent. Pursuant to an engagement letter agreement dated April 9, 2003 between the Company and Baird, the Company agreed to pay Baird (1) an initial non-refundable retainer fee of $50,000, which was paid in April 2003 and additional $25,000 retainer fees payable at the beginning of each three-month period thereafter (all of which are fully creditable against the transaction fee described below); (2) a fee of $350,000, payable upon delivery of its opinion, regardless of the conclusions reached by Baird in such opinion and regardless of whether the Transaction is consummated (such fee is creditable against the transaction fee described below); and (3) a transaction fee, payable upon consummation of the Transaction, equal to 1.0% of the total implied enterprise value. The Company also has agreed to reimburse Baird for its reasonable out-of-pocket expenses. The Company also has agreed to indemnify Baird, its affiliates and related parties and their respective directors, officers, employees, agents and controlling persons against certain liabilities relating to or arising out of its engagement. The terms of the fee arrangements with Baird, which the Company and Baird believe are customary in transactions of this nature, were negotiated at arms' length between the Company and Baird, and the Company's Board of Directors was aware of the nature of the fee arrangements, including the fact that a significant portion of the fees payable to Baird is contingent on the consummation of the Transaction. As mentioned above, in the ordinary course of its business, Baird and its affiliates may trade the debt and equity securities of the Company for its or its affiliates own account or for the accounts of customers and, accordingly, it or its affiliates may at any time hold long or short positions in such securities. In addition, Baird and its affiliates may maintain relationships with the Company, Parent and their respective affiliates.

Neither the Company nor any person acting on its behalf currently intends to employ, retain or compensate any person to make solicitations or recommendations to stockholders on its behalf concerning the Offer.

19

Item 6. Interest in Securities of the Subject Company.

No transactions in shares of Common Stock have been effected during the past 60 days by the Company or any of its subsidiaries or, to the best of the Company's knowledge, by any executive officer, director or affiliate of the Company.

Item 7. Purposes of the Transaction and Plans or Proposals.

Except as set forth in this Statement or the Offer to Purchase, to the Company's knowledge, no negotiation is being undertaken or engaged in by the Company that relates to or would result in:

- •

- a tender offer for or other acquisition of the Company's securities by the Company, any subsidiary of the Company, or any other person;

- •

- any extraordinary transaction, such as a merger, reorganization or liquidation, involving the Company or any subsidiary of the Company;

- •

- any purchase, sale or transfer of a material amount of assets of the Company or any subsidiary of the Company; or

- •

- any material change in the present dividend rate or policy, or indebtedness or capitalization of the Company.

Except as set forth in this Statement or the Offer to Purchase, there are no transactions, resolutions of the Board, agreements in principle, or signed contracts in response to the Offer that relate to one or more of the events referred to in this Item 7.

Item 8. Additional Information.

Section 14(f) Information Statement

The Information Statement attached as Annex A hereto is being furnished in connection with the possible designation by Parent, pursuant to the Merger Agreement, of certain persons to be appointed to the Board other than at a meeting of the Company's stockholders, and such information is incorporated herein by reference.

In addition, the information contained in the Offer to Purchase is incorporated herein by reference.

Anti-Takeover Statute