EXHIBIT 13

20 ANNUAL

09 REPORT MESSAGE FROM THE CHAIRMAN

CAPITOL BANCORP LIMITED

BOARD OF DIRECTORS

Joseph D. Reid

Chairman & CEO

Capitol Bancorp Limited

Michael L. Kasten

Vice Chairman

Capitol Bancorp Limited

Managing Partner

Kasten Investments, LLC

Lyle W. Miller

Vice Chairman

Capitol Bancorp Limited

President

L.W. Miller Holding Co.

David J. O’Leary

Secretary

Capitol Bancorp Limited

Chairman

O’Leary Paint Company

Paul R. Ballard

Retired President & CEO

Portage Commerce Bank

David L. Becker

Retired Founder

Becker Insurance Agency, PC

Michael J. Devine

Attorney at Law

James C. Epolito

Entrepreneur

Gary A. Falkenberg, DO

Retired Physician

Gary A. Falkenberg, PC

Joel I. Ferguson

Chairman

Ferguson Development, LLC

Kathleen A. Gaskin

Retired Real Estate

Associate Broker

H. Nicholas Genova

Chairman & CEO

Washtenaw News Co. Inc.

President

H. N. Genova Development

Richard A. Henderson, CPA

President

Henderson & Associates, PC

Lewis D. Johns

President

Mid-Michigan Investment Co.

Steven L. Maas

Co-Owner

River Valley Title, LLC

Myrl D. Nofziger

President

Hoogenboom Nofziger

Cristin K. Reid

Corporate President

Capitol Bancorp Limited

Ronald K. Sable

President

Concord Solutions Ltd.

Dear Shareholder:

During the past year and throughout 2010, Capitol Bancorp Limited continues to execute a major restructuring plan for the Corporation. Our primary objective is the preservation of capital for our banking affiliates. The current state of the national economy has significantly impacted the banking industry, in general, and Capitol Bancorp, specifically. The escalation of adverse valuation of nonperforming loans has materially diminished capital ratios at some of our banking affiliates. This, in turn, has imposed upon the Corporation the need to seek other sources of capital which can be infused into these institutions.

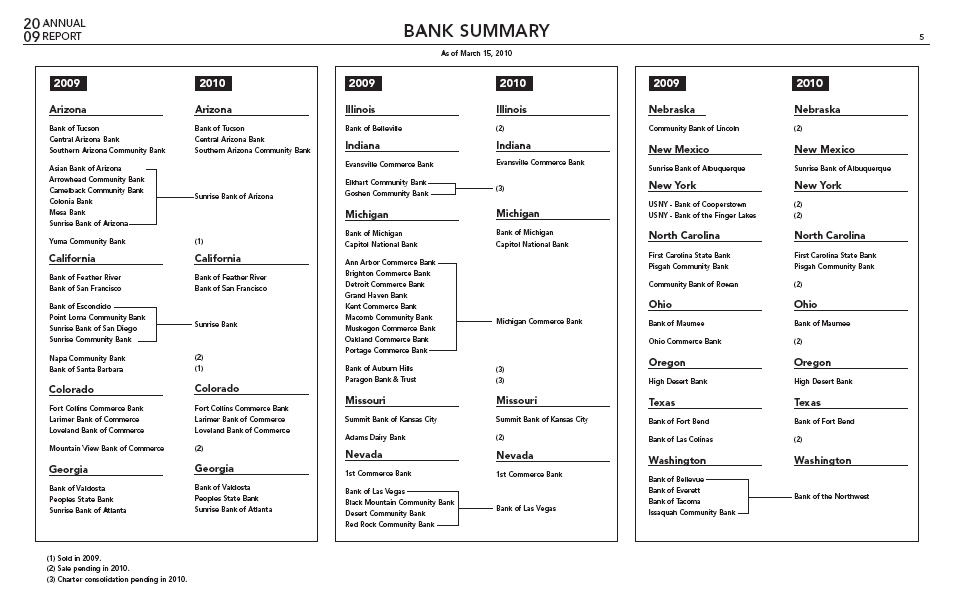

The plan has three fundamental strategies. First, we have embarked upon a balance sheet deleveraging program that resulted in the sale of two banks in 2009 – Yuma Community Bank and Bank of Santa Barbara. Efforts in 2009 contributed to the recently announced sales of eight more banking affiliates which are expected to close mid-year. Currently there are an additional number of affiliates at various stages of discussion regarding sale. The net sale proceeds from this ongoing effort are then being used as capital for our other banking affiliates.

Additionally, deleveraging has occurred through the reduction of bank assets at our existing banks. The reduction in bank assets serves to reduce the need for capital at the respective institution. For example, in the nine months ended December 31, 2009, the newly merged Michigan Commerce Bank reduced risk-weighted assets from $1.1 billion to $927 million, thereby reducing the need for supporting capital by approximately $14 million.

The second strategy has been the consolidation of several bank affiliates into single charters. Operating expenses of the combined banks are thereby reduced, furthering the preservation of capital. In 2009, we merged nine banking

2

affiliates into a single charter under the new name of Michigan Commerce Bank. Included within the Michigan Commerce merger were the following:

■ Ann Arbor Commerce Bank

■ Brighton Commerce Bank

■ Detroit Commerce Bank

■ Grand Haven Bank

■ Kent Commerce Bank

■ Macomb Community Bank

■ Muskegon Commerce Bank

■ Oakland Commerce Bank

■ Portage Commerce Bank

In December 2009, we merged six of our Arizona banking affiliates into a single charter to operate under one name, Sunrise Bank of Arizona. The five other banks combined in this merger included:

■ Arrowhead Community Bank

■ Asian Bank of Arizona

■ Camelback Community Bank

■ Colonia Bank

■ Mesa Bank

During the first quarter of 2010, we completed the merger of four banks based in Las Vegas, Nevada, into a single charter under the existing name, Bank of Las Vegas. The following banks were included in the merger:

■ Bank of Las Vegas

■ Black Mountain Community Bank

■ Desert Community Bank

■ Red Rock Community Bank

In Washington state we merged our four Seattle-area banks into a single charter under the new name, Bank of the Northwest. Included in the February 2010 merger were:

■ Bank of Bellevue

■ Bank of Everett

■ Bank of Tacoma

■ Issaquah Community Bank

In southern California, we have completed the merger of four banks in early 2010 that will be known as Sunrise Bank. They are:

■ Bank of Escondido

■ Point Loma Community Bank

■ Sunrise Bank of San Diego

■ Sunrise Community Bank

We have an application pending in 2010 to merge two affiliate banks in the state of Indiana, currently operating as Elkhart Community Bank and Goshen Community Bank.

Our third capital preservation strategy involves ongoing operational assessment and expense reduction. This will continue throughout 2010.

We remain committed to the successful execution of each of these strategies in our effort to manage through the consequences of the “Great Recession.”

The Capitol family lost a respected board member in 2009. Doug Crist was a member of the board that launched the first bank in 1982 in Lansing, Michigan, Capitol National Bank, and continued serving Capitol Bancorp as a director and chair of the Compensation Committee until his death. We miss his guidance.

JOSEPH D. REID

Chairman & CEO

20 ANNUAL

09 REPORT MESSAGE FROM THE PRESIDENT

Dear Shareholder:

Our operational focus for 2010 emphasizes risk mitigation and operational efficiency. During the course of the year we will continue to focus on the following initiatives:

■ Enhanced credit administration;

■ Consolidated credit review;

■ The engagement of additional risk support specialists;

■ Restructured financial strategic management;

■ Expanded fraud detection and prevention procedures which include tech-based platforms;

■ Ongoing operational assessment in all areas; and

■ Consolidation of bank charters while retaining a local, community presence.

We are adapting to the changing financial industry by treating this down cycle as an opportunity to improve our operations to best prepare us for future growth and performance.

Enterprise risk management is the focus of all operating departments. Managers are being asked to mitigate risk and evaluate their internal processes. Our Board of Directors has adopted an enhanced enterprise risk management process which provides management and directors with a defined structure for the assessment, reporting and management of risk on an enterprise-wide basis. Additionally, the Risk Management Committee, which is responsible for reviewing and approving our risk management framework, including the development of proactive policies, processes and procedures, has been expanded to include the entire Board of Directors.

We work closely with regulatory agencies and have common objectives to appropriately address the challenges faced by banks in this difficult operating environment. Adopting a capital strategy which helps ensure that each bank has the funding support it needs is one of the primary objectives.

We look forward to progress in 2010. As always, we appreciate your loyalty and support of Capitol Bancorp Limited.

CRISTIN K. REID

Corporate President

FINANCIAL INFORMATION

Table of Contents

| F-2 | |

| F-3 | |

| F-5 | |

| F-5 | |

| F-5 | |

| F-6 | |

Results of Operations: | |

| F-11 | |

| F-12 | |

| F-12 | |

| F-16 | |

| F-21 | |

| F-29 | |

| F-35 | |

| F-37 | |

| F-37 | |

| F-41 | |

| F-41 | |

| F-42 | |

| F-42 | |

| F-43 | |

| F-45 | |

| F-46 | |

| F-46 | |

| F-47 | |

| F-48 | |

Control Over Financial Reporting | F-49 |

| Consolidated Financial Statements: | |

| F-51 | |

| F-52 | |

| F-53 | |

| F-54 | |

| F-56 | |

| F-57 |

F-1

(in $1,000s, except per share data)

| As of and for the Year Ended December 31 | ||||||||||||||||||||

2009(1) | 2008(2) | 2007(3) | 2006(4) | 2005(5) | ||||||||||||||||

| For the year: | ||||||||||||||||||||

| Interest income | $ | 266,899 | $ | 304,315 | $ | 330,439 | $ | 279,353 | $ | 224,439 | ||||||||||

| Interest expense | 110,517 | 140,466 | 147,162 | 105,586 | 67,579 | |||||||||||||||

| Net interest income | 156,382 | 163,849 | 183,277 | 173,767 | 156,860 | |||||||||||||||

| Provision for loan losses | 190,680 | 82,492 | 25,340 | 12,156 | 10,960 | |||||||||||||||

| Noninterest income | 28,773 | 26,432 | 24,381 | 21,532 | 21,048 | |||||||||||||||

| Noninterest expense | 240,597 | 190,388 | 176,160 | 137,804 | 117,289 | |||||||||||||||

| Net income (loss) | (264,540 | ) | (52,451 | ) | 3,334 | 29,876 | 30,427 | |||||||||||||

| Net income (loss) attributable to Capitol Bancorp Limited | (195,169 | ) | (28,607 | ) | 21,937 | 42,391 | 35,925 | |||||||||||||

| Net income (loss) per share attributable to Capitol | ||||||||||||||||||||

| Bancorp Limited: | ||||||||||||||||||||

| Basic | (11.28 | ) | (1.67 | ) | 1.29 | 2.69 | 2.42 | |||||||||||||

| Diluted | (11.28 | ) | (1.67 | ) | 1.27 | 2.57 | 2.34 | |||||||||||||

| Cash dividends paid per share | 0.05 | 0.50 | 1.00 | 0.95 | 0.72 | |||||||||||||||

| At end of year: | ||||||||||||||||||||

| Total assets | $ | 5,131,940 | $ | 5,654,836 | $ | 4,901,763 | $ | 4,065,816 | $ | 3,475,721 | ||||||||||

| Total earning assets | 4,855,309 | 5,282,010 | 4,527,006 | 3,743,041 | 3,204,646 | |||||||||||||||

| Portfolio loans | 4,047,101 | 4,735,229 | 4,314,701 | 3,488,678 | 2,991,189 | |||||||||||||||

| Deposits | 4,410,633 | 4,497,612 | 3,844,745 | 3,258,485 | 2,785,259 | |||||||||||||||

| Notes payable and short-term borrowings | 276,159 | 446,925 | 320,384 | 191,154 | 175,729 | |||||||||||||||

| Subordinated debentures | 167,441 | 167,293 | 156,130 | 101,035 | 100,940 | |||||||||||||||

| Noncontrolling interests in consolidated subsidiaries | 72,271 | 159,220 | 156,198 | 126,512 | 83,838 | |||||||||||||||

| Capitol Bancorp Limited stockholders' equity | 161,335 | 353,848 | 389,145 | 361,879 | 301,866 | |||||||||||||||

| Quarterly Results of Operations (unaudited) | ||||||||||||||||||||

Total for the Year | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | ||||||||||||||||

Year ended December 31, 2009:(1) | ||||||||||||||||||||

| As previously reported: | ||||||||||||||||||||

| Interest income | $ | 266,899 | $ | 61,366 | $ | 67,345 | $ | 69,472 | $ | 68,716 | ||||||||||

| Interest expense | 110,517 | 23,075 | 27,293 | 28,890 | 31,259 | |||||||||||||||

| Net interest income | 156,382 | 38,291 | 40,052 | 40,582 | 37,457 | |||||||||||||||

Provision for loan losses(8) | 190,680 | 77,924 | 48,771 | 35,813 | 28,172 | |||||||||||||||

Net loss(8) | (264,540 | ) | (87,107 | ) | (129,174 | ) | (25,354 | ) | (22,905 | ) | ||||||||||

Net loss attributable to Capitol Bancorp Limited(8) | (195,169 | ) | (77,051 | ) | (83,748 | ) | (18,698 | ) | (15,672 | ) | ||||||||||

Net loss per share attributable to Capitol Bancorp Limited – basic and diluted(6)(8) | (11.28 | ) | (4.43 | ) | (4.81 | ) | (1.08 | ) | (0.91 | ) | ||||||||||

| Cash dividends paid per share | 0.05 | -- | -- | -- | 0.05 | |||||||||||||||

As revised:(7) | ||||||||||||||||||||

Provision for loan losses(8) | 190,680 | 75,771 | 47,335 | 33,658 | 33,916 | |||||||||||||||

Net loss(8) | (264,540 | ) | (85,558 | ) | (128,115 | ) | (22,960 | ) | (27,907 | ) | ||||||||||

Net loss attributable to Capitol Bancorp Limited(8) | (195,169 | ) | (75,502 | ) | (82,689 | ) | (16,304 | ) | (20,674 | ) | ||||||||||

Net loss per share attributable to Capitol Bancorp Limited – basic and diluted(6)(8) | (11.28 | ) | (4.34 | ) | (4.75 | ) | (0.95 | ) | (1.20 | ) | ||||||||||

Year ended December 31, 2008:(2) | ||||||||||||||||||||

| Interest income | $ | 304,315 | $ | 73,179 | $ | 75,496 | $ | 76,137 | $ | 79,503 | ||||||||||

| Interest expense | 140,466 | 34,496 | 34,457 | 33,945 | 37,568 | |||||||||||||||

| Net interest income | 163,849 | 38,683 | 41,039 | 42,192 | 41,935 | |||||||||||||||

| Provision for loan losses | 82,492 | 10,705 | 53,810 | 9,019 | 8,958 | |||||||||||||||

| Net loss | (52,451 | ) | (4,866 | ) | (38,880 | ) | (5,437 | ) | (3,268 | ) | ||||||||||

| Net income (loss) attributable to Capitol Bancorp Limited | (28,607 | ) | 1,074 | (32,495 | ) | 623 | 2,191 | |||||||||||||

Net income (loss) per share attributable to Capitol Bancorp Limited – basic and diluted(6) | (1.67 | ) | 0.06 | (1.90 | ) | 0.04 | 0.13 | |||||||||||||

| Cash dividends paid per share | 0.50 | 0.05 | 0.05 | 0.15 | 0.25 | |||||||||||||||

| (1) | Includes Yuma Community Bank's operations through September 21, 2009 (date at which Capitol sold its ownership of that bank) and Bank of Santa Barbara, Community Bank of Rowan, Summit Bank of Kansas City and Capitol Development Bancorp Limited III's operations through September 30, 2009 (the date when these entities ceased to be consolidated with Capitol due to a change in control). |

| (2) | Includes Adams Dairy Bank, effective January 2008 (located in Blue Springs, Missouri), Mountain View Bank of Commerce, effective February 2008 (located in Westminster, Colorado), Colonia Bank, effective April 2008 (located in Phoenix, Arizona) and Pisgah Community Bank, effective May 2008 (located in Asheville, North Carolina). |

| (3) | Includes Bank of Tacoma, effective January 2007 (located in Tacoma, Washington), Sunrise Community Bank, effective February 2007 (located in Palm Desert, California), Larimer Bank of Commerce, effective May 2007 (located in Fort Collins, Colorado), Issaquah Community Bank (located in Issaquah, Washington) and USNY Bank (located in Geneva, New York), both effective July 2007, High Desert Bank, effective September 2007 (located in Bend, Oregon), Loveland Bank of Commerce, effective October 2007 (located in Loveland, Colorado), Bank of Feather River, effective November 2007 (located in Yuba City, California) and Community Bank of Lincoln (located in Lincoln, Nebraska), Bank of Fort Bend (located in Sugar Land, Texas) and Bank of Las Colinas (located in Irving, Texas), each effective December 2007. |

| (4) | Includes Community Bank of Rowan, effective February 2006 (located in Salisbury, North Carolina), Asian Bank of Arizona, effective April 2006 (located in Phoenix, Arizona), Evansville Commerce Bank, effective May 2006 (located in Evansville, Indiana), Bank of Valdosta (located in Valdosta, Georgia), Sunrise Bank of Atlanta (located in Atlanta, Georgia) and Bank of Everett (located in Everett, Washington), all effective June 2006, Bank of Maumee (located in Maumee, Ohio) and 1st Commerce Bank (located in North Las Vegas, Nevada), both effective October 2006, and Ohio Commerce Bank (located in Beachwood, Ohio), effective November 2006. |

| (5) | Includes Bank of Michigan, effective January 2005 (located in Farmington Hills, Michigan), Peoples State Bank, acquired April 7, 2005 (located in Jeffersonville, Georgia), Bank of Bellevue (located in Bellevue, Washington) and Fort Collins Commerce Bank (located in Fort Collins, Colorado), both effective June 2005, Bank of Auburn Hills, effective July 2005 (located in Auburn Hills, Michigan), Bank of San Francisco, effective August 2005 (located in San Francisco, California), Bank of Belleville (located in Belleville, Illinois) and Summit Bank of Kansas City (located in Lee's Summit, Missouri), both effective November 2005, and Bank of Santa Barbara, effective December 2005 (located in Santa Barbara, California). |

| (6) | Each period's computation of net income (loss) per share is performed independently and, accordingly, net income per share for the year (basic and diluted) may not equal the sum of the amounts shown for the quarterly periods. |

| (7) | As-adjusted to reflect revised interpretation of fair-value accounting guidance (FSP FAS 157-4) which was implemented in error in the first quarter of 2009, to properly base fair-value estimates of collateral-dependent loans and other real estate owned upon appraisal data rather than use of alternative valuation methods. |

| (8) | Fourth quarter 2009 results of operations include additional provisions for loan losses approximating $20.7 million relating to regulatory exam reports received after year-end 2009 and approximately $9.6 million of write-downs (and related expense recognition) resulting from appraisal data received after year-end 2009 for collateral-dependent loans and other real estate owned. |

F-2

Capitol's common stock is traded on the New York Stock Exchange (NYSE) under the symbol "CBC." Market quotations regarding the range of high and low sales prices of Capitol's common stock, as reported by the NYSE, were as follows:

| 2009 | 2008 | ||||||||||||||

| Low | High | Low | High | ||||||||||||

| Quarter Ended: | |||||||||||||||

| March 31 | $ | 2.50 | $ | 7.96 | $ | 16.30 | $ | 23.52 | |||||||

| June 30 | 2.38 | 7.08 | 8.97 | 21.42 | |||||||||||

| September 30 | 1.79 | 6.06 | 7.08 | 25.40 | |||||||||||

| December 31 | 1.55 | 3.45 | 3.84 | 20.49 | |||||||||||

Below is a graph which summarizes the cumulative return earned by Capitol's shareholders over the last five years compared with the SNL (SNL Financial LC) $5B-$10B Asset-Size Index (SNL) and the cumulative total return on the Russell 2000 Index (R-2000). This presentation assumes the initial value of an investment in Capitol's common stock and each index was $100 on December 31, 2004 and that any subsequent cash dividends were reinvested.

| Period Ending | |||||||

| Index | 12/31/04 | 12/31/05 | 12/31/06 | 12/31/07 | 12/31/08 | 12/31/09 | |

| Capitol Bancorp Ltd. | 100.00 | 108.65 | 137.09 | 62.05 | 24.88 | 6.31 | |

| Russell 2000 | 100.00 | 104.55 | 123.76 | 121.82 | 80.66 | 102.58 | |

| SNL Bank $5B-$10B | 100.00 | 96.89 | 104.56 | 83.86 | 73.57 | 56.56 | |

F-3

INFORMATION REGARDING CAPITOL'S COMMON STOCK—Continued

In the first quarter of 2009, Capitol paid a cash dividend of $0.05 per share. During 2008, Capitol paid quarterly cash dividends of $0.25 per share for the first quarter, $0.15 in the second quarter and $0.05 in the third and fourth quarters. In 2007, Capitol paid quarterly cash dividends of $0.25 per share. Payment of dividends is not currently permitted without prior written approval of the Federal Reserve, Capitol's primary federal regulator (see subsequent discussion of certain regulatory matters in the section captioned "Management's Discussion and Analysis of Capitol's Business, Financial Condition and Results of Operations").

As of March 2, 2010, there were 10,287 beneficial holders of Capitol's common stock, based on information supplied to Capitol from its stock transfer agent and other sources.

At March 2, 2010, 17,544,501 shares of common stock were outstanding. Capitol's stock transfer agent is BNY Mellon Shareowner Services, 480 Washington Blvd., Jersey City, NJ 07310 (telephone 866-205-7090). The website for BNY Mellon Shareowner Services is http://www.bnymellon.com/shareowner/isd.

Capitol has a direct purchase and dividend reinvestment plan, the Capitol Bancorp Limited Direct Purchase and Dividend Reinvestment Plan ("Capitol Bancorp Direct"), which offers a variety of convenient features including dividend reinvestment, certain fee-free transactions, certificate safekeeping and other benefits. For a copy of the Capitol Bancorp Direct prospectus, informational brochure and enrollment materials, contact BNY Mellon Shareowner Services at 866-205-7090 or Capitol at 517-487-6555.

In addition to Capitol's common stock, trust-preferred securities of Capitol Trust I and Capitol Trust XII (each a subsidiary of Capitol) are listed on the NYSE under the symbol "CBCPrA" and "CBCPrB," respectively. The trust-preferred securities have a liquidation amount of $10 per preferred security and are guaranteed by Capitol. Capitol Trust I consists of 2,530,000, 8.5% cumulative preferred securities scheduled to mature in 2027, which are currently callable and may be extended to 2036 if certain conditions are met. Capitol Trust XII consists of 3,805,000, 10.5% cumulative preferred securities scheduled to mature in 2038 and become callable in 2013. In 2009, Capitol commenced the deferral of interest payments on its various trust-preferred securities, as is permitted under the terms of the securities, to conserve cash and capital resources. The payment of interest may be deferred for periods up to five years. During such deferral periods, Capitol is generally prohibited from paying dividends on its common stock and will continue to accrue interest payable on such securities. Holders of the trust-preferred securities will continue to recognize current taxable income relating to the deferred interest payments. Payment of interest on the trust-preferred securities is also not permitted without prior written approval of the Federal Reserve (see subsequent discussion of certain regulatory matters in the section captioned "Management's Discussion and Analysis of Capitol's Business, Financial Condition and Results of Operations").

F-4

Capitol will file with the U.S. Securities and Exchange Commission (SEC) all required certifications regarding the quality of Capitol's public disclosures upon filing of Capitol's 2009 Report on Form 10-K. In addition, Capitol's CEO submitted to the NYSE an annual CEO certification stating that he is not aware of any violation by Capitol of the NYSE's corporate governance listing standards. Further, Capitol will file certifications with the SEC in accordance with the Sarbanes-Oxley Act of 2002 as exhibits to Capitol's 2009 Report on Form 10-K.

A copy of Capitol's 2009 report on Form 10-K, without exhibits, will be available to holders of its common stock or trust-preferred securities without charge, upon written request. Form 10-K includes certain statistical and other information regarding Capitol and its business. Requests to obtain a copy of Form 10-K should be addressed to Investor Relations, Capitol Bancorp Limited, Capitol Bancorp Center, 200 N. Washington Square, Lansing, Michigan 48933.

Form 10-K and certain other periodic reports have been or will be filed with the SEC. The SEC maintains an Internet website that contains reports, proxy and information statements and other information regarding companies which file electronically (which includes Capitol). The SEC's website address is http://www.sec.gov. Capitol's filings with the SEC are also available at Capitol's website, http://www.capitolbancorp.com.

EXECUTIVE OFFICES

| Capitol Bancorp Center | 2777 E. Camelback Road |

| 200 N. Washington Square | Suite 375 |

| Lansing, Michigan 48933 | Phoenix, Arizona 85016 |

| 517-487-6555 | 602-955-6100 |

| website: www.capitolbancorp.com | |

INDEPENDENT AUDITORS

BDO Seidman, LLP

Grand Rapids, Michigan

SHAREHOLDER INFORMATION

ANNUAL MEETING

Capitol's 2009 Annual Meeting of Shareholders will be held on Wednesday, April 28, 2010 at 4:00 p.m. at the Capitol Bancorp Center, located at 200 N. Washington Square, Lansing, Michigan.

F-5

SHAREHOLDER INFORMATION—Continued

DIRECT PURCHASE AND DIVIDEND REINVESTMENT PLAN

Capitol offers an easy and affordable way to invest in Capitol's common stock through its direct purchase and dividend reinvestment plan, Capitol Bancorp Direct. Capitol Bancorp Direct's benefits include the ability to make an initial investment in common stock with as little as $50, reinvestment of dividends in additional common stock (if and when paid), direct deposit of dividends (if and when paid), ability to purchase common stock as frequently as once a month, and the option to make transfers or gifts of Capitol's common stock to another person. Participation in Capitol Bancorp Direct is voluntary and shareholders and prospective investors are eligible. Purchases under Capitol Bancorp Direct are not currently subject to any brokerage fees or commissions. For further information regarding Capitol Bancorp Direct or for a copy of Capitol Bancorp Direct's prospectus, informational brochure and enrollment materials, please contact BNY Mellon Shareowner Services at 866-205-7090 or Capitol at 517-487-6555.

TRUST-PREFERRED SECURITIES TRADING INFORMATION

Preferred securities of Capitol Trust I and Capitol Trust XII (each a subsidiary of Capitol) trade on the NYSE under the trading symbols "CBCPrA" and "CBCPrB," respectively.

TRUST-PREFERRED SECURITIES TRUSTEE

Capitol Trust I: JP Morgan Institutional Trust Services – Tempe, Arizona

Capitol Trust XII: Wells Fargo Delaware Trust Company

Some of the statements contained in this annual report, including Capitol's consolidated financial statements, Management's Discussion and Analysis of Capitol's Business, Financial Condition and Results of Operations and in documents incorporated into this document by reference that are not historical facts, including, without limitation, statements of future expectations, projections of results of operations and financial condition, statements of future economic performance and other forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, are subject to known and unknown risks, uncertainties and other factors which may cause the actual future results, performance or achievements of Capitol and/or its subsidiaries and other operating units to differ materially from those contemplated in such forward-looking statements. The words "intend," "expect," "project," "estimate," "predict," "anticipate," "should," "could," "believe," "may," "might," and similar expressions also are intended to identify forward-looking statements. Important factors which may cause actual results to differ from those contemplated in such forward-looking statements include, but are not limited to: (i) the results of Capitol's efforts to implement its business strategy, (ii) changes in interest rates, (iii) legislation or regulatory requirements adversely impacting Capitol's banking business and/or expansion strategy, (iv) adverse changes in business conditions or inflation, (v) general economic conditions, either nationally or regionally, which are less favorable than expected and that result in, among other things, a deterioration in credit quality and/or loan performance and collectability, (vi) competitive pressures among financial institutions, (vii) changes in securities markets, (viii) actions of competitors of Capitol's banks and Capitol's ability to respond to such actions,

F-6

CAUTIONS REGARDING FORWARD-LOOKING STATEMENTS—Continued

(ix) the cost of and access to capital, which may depend in part on Capitol's asset quality, prospects and outlook, (x) changes in governmental regulation, tax rates and similar matters, (xi) availability of funds under the U.S. Treasury's Capital Assistance Program and Capital Purchase Program, (xii) changes in management, (xiii) Capitol's proposed spin-off of Michigan Commerce Bancorp Limited; (xiv) consummation of pending sales of certain bank subsidiaries, (xv) other risks detailed in Capitol's other filings with the SEC, and (xvi) and the following, among others:

· Management's ability to effectively manage interest rate risk and the impact of interest rates in general on the volatility of Capitol's net interest income;

· The effect of the Emergency Economic Stabilization Act of 2008, the American Recovery and Reinvestment Act of 2009, the implementation by the Department of the U.S. Treasury and federal banking regulators of a number of programs to address capital and liquidity issues within the banking system and additional programs that may apply to Capitol in the future, all of which may have significant effects on Capitol and the financial services industry;

· The decline in commercial and residential real estate values and sales volume and the likely potential for continuing illiquidity in the real estate market;

· The risks associated with the high concentration of commercial real estate loans within Capitol's portfolio;

· The uncertainties in estimating the fair value of developed real estate and undeveloped land relating to collateral-dependent loans and other real estate owned in light of declining demand for such assets, falling prices and continuing illiquidity in the real estate market;

· Negative developments and disruptions in the credit and lending markets, including the impact of the ongoing credit crisis on Capitol's business and on the businesses of its customers as well as other banks and lending institutions with which Capitol has commercial relationships;

· A continuation of unprecedented volatility in the capital markets;

· The risks associated with implementing Capitol's business strategy, including its ability to preserve and access sufficient capital to execute its strategy;

· Rising unemployment and its impact on Capitol's customers' savings rates and their ability to service debt obligations;

· Fluctuations in the value of Capitol's investment securities;

· The ability to attract and retain senior management experienced in banking and financial services;

· The sufficiency of the allowance for loan losses to absorb the amount of actual losses inherent within the loan portfolio;

F-7

CAUTIONS REGARDING FORWARD-LOOKING STATEMENTS—Continued

· Capitol's ability to adapt successfully to technological changes to compete effectively in the marketplace;

· Credit risks and risks from concentrations (by geographic area and by industry) within Capitol's consolidated loan portfolio and individual large loans;

· The effects of competition from other commercial banks, thrifts, mortgage banking firms, consumer finance companies, credit unions, securities brokerage firms, insurance companies, money market and other mutual funds, and other financial institutions operating in Capitol's market or elsewhere or providing similar services;

· The failure of assumptions underlying the establishment of the allowance for loan losses and estimation of values of collateral or cash flow projections and various financial assets and liabilities;

· Volatility of rate sensitive deposits;

· Operational risks, including data processing system failures or fraud;

· Liquidity risks;

· The ability to successfully acquire deposits for funding and the pricing thereof;

· The ability to successfully execute strategies to increase noninterest income;

· Changes in the economic environment, competition or other factors that may influence loan demand and repayment, deposit inflows and outflows, and the quality of the loan portfolio and loan and deposit pricing;

· The impact from liabilities arising from legal or administrative proceedings on the financial condition of Capitol;

· The current prohibition of Capitol's subsidiary banks to pay dividends to Capitol without prior written authorization from regulatory agencies;

· The current prohibition of Capitol's payment of cash dividends on its common stock without prior written regulatory authorization;

· Possible administrative or enforcement actions of banking regulators in connection with any material failure of Capitol or its subsidiary banks to comply with banking laws, rules or regulations or formal agreements with regulatory agencies;

· Capitol's compliance with the terms of its written agreement with the Federal Reserve Bank, amendments thereto or subsequent regulatory agreements;

· The continued availability of credit facilities provided by Federal Home Loan Banks to Capitol's banking subsidiaries;

· The uncertainties of future depositor activity regarding potentially uninsured deposits upon expiration of the FDIC's Transaction Account Guarantee Program;

F-8

CAUTIONS REGARDING FORWARD-LOOKING STATEMENTS—Continued

· The possibility of the FDIC assessing Capitol's bank subsidiaries for any cross-guaranty liability;

· Governmental monetary and fiscal policies, as well as legislative and regulatory changes, that may result in the imposition of costs and constraints on Capitol through higher FDIC insurance premiums, significant fluctuations in market interest rates, increases in capital requirements, and operational limitations;

· Changes in general economic or industry conditions, nationally or in the communities in which Capitol conducts business;

· Changes in legislation or regulatory and accounting principles, policies, or guidelines affecting the business conducted by Capitol;

· The impact of possible future goodwill and other material impairment charges;

· Acts of war or terrorism;

· Capitol's ability to manage fluctuations in the value of its assets and liabilities and maintain sufficient capital and liquidity to support its operations;

· The concentration of Capitol's nonperforming assets by loan type in certain geographic regions and with affiliated borrowing groups;

· The risk of additional future losses if the proceeds Capitol receives upon the liquidation of assets are less than the carrying value of such assets;

· Restrictions or limitations on access to funds from subsidiaries and potential obligations to contribute additional capital to Capitol's subsidiaries, which may restrict its ability to make payments on its obligations;

· The availability and cost of capital and liquidity on favorable terms, if at all;

· Changes in accounting standards or applications and determinations made thereunder;

· The risk that the realization of deferred tax assets and recoverable income taxes may extend beyond 2010;

· The risk that Capitol will not be able to complete its various proposed mergers and consolidations of certain of its subsidiary banks or, if completed, realize the anticipated benefits of the proposed mergers and/or consolidations;

· The impact on Capitol's financial results, reputation and business if it is unable to comply with all applicable federal and state regulations and applicable formal agreements, consent orders, other regulatory actions and any related capital initiatives;

· The costs and effects of litigation, investigations, inquiries or similar matters, or adverse facts and developments related thereto;

F-9

CAUTIONS REGARDING FORWARD-LOOKING STATEMENTS—Continued

· The risk that, if economic conditions worsen or regulatory capital requirements are modified, Capitol may be required to seek additional liquidity and/or capital from external sources, if available;

· The risk that Capitol could have an "ownership change" under Section 382 of the Internal Revenue Code, which could impair its ability to timely and fully utilize its net operating losses for tax purposes and so-called built-in losses that may exist if such an "ownership change" occurs;

· Other factors and other information contained in this document and in other reports and filings that Capitol makes with the SEC under the Exchange Act, including, without limitation, under the caption "Risk Factors"; and

· Other economic, competitive, governmental, regulatory, and technical factors affecting Capitol's operations, products, services, and prices.

For a discussion of these and other risks that may cause actual results to differ from expectations, you should refer to the risk factors and other information in this Annual Report and Capitol's other periodic filings, including quarterly reports on Form 10-Q and current reports on Form 8-K, that Capitol files from time to time with the SEC. All written or oral forward-looking statements that are made by or are attributable to Capitol are expressly qualified by this cautionary notice. You should not place undue reliance on any forward-looking statements, since those statements speak only as of the date on which the statements are made. Capitol undertakes no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made to reflect the occurrence of new information or unanticipated events, except as may otherwise be required by law.

[The remainder of this page intentionally left blank]

F-10

Financial Condition and Results of Operations

This section of the Annual Report is intended to discuss, from management's perspective, matters of importance regarding Capitol's operations, financial position and other things which have a significant effect on Capitol, its business and its banks. This narrative includes some comments about future events and other forward-looking statements and readers are advised to carefully read the cautionary statement about forward-looking statements which is on page F-6 of this Annual Report.

Capitol is unique in the banking industry with its number of individually-chartered community banks. Capitol operates community banks in a wide variety of markets during an era of industry consolidation. Capitol operates in one business segment, community banking. Its banks are staffed with banking professionals, serving customers who desire professional banking services delivered personally.

In recent years, Capitol had expanded significantly through the addition of de novo banks. In 2007, 11 new banks were formed and, in 2006, 9 new banks were formed. Four de novo banks were formed in the first half of 2008. Plans for formation of additional de novo banks were terminated mid-year 2008, due to an unfavorable regulatory and capital-raising environment.

During 2009, to streamline bank operations and reduce expenses, Capitol consolidated some of its individual bank charters regionally and has plans for further charter consolidation activities in 2010. Additionally, in mid-2009, as part of its capital strategies and restructuring activities, Capitol announced plans to selectively divest some banks as a means to raise additional capital and redeploy capital resources to its remaining banks. Several divestiture transactions have been recently announced, which are subject to regulatory approval.

Capitol's community bank model, in a stable economic environment, is intended to maintain a scalable, low overhead structure which is focused on delivering return-on-equity results, while empowering its individual banks with operating autonomy in all areas which impact the customer relationship. Capitol's centralized 'back-office' functions, which support the banks, are capable of expanding coverage in concert with growth in both the number and size of affiliate banks.

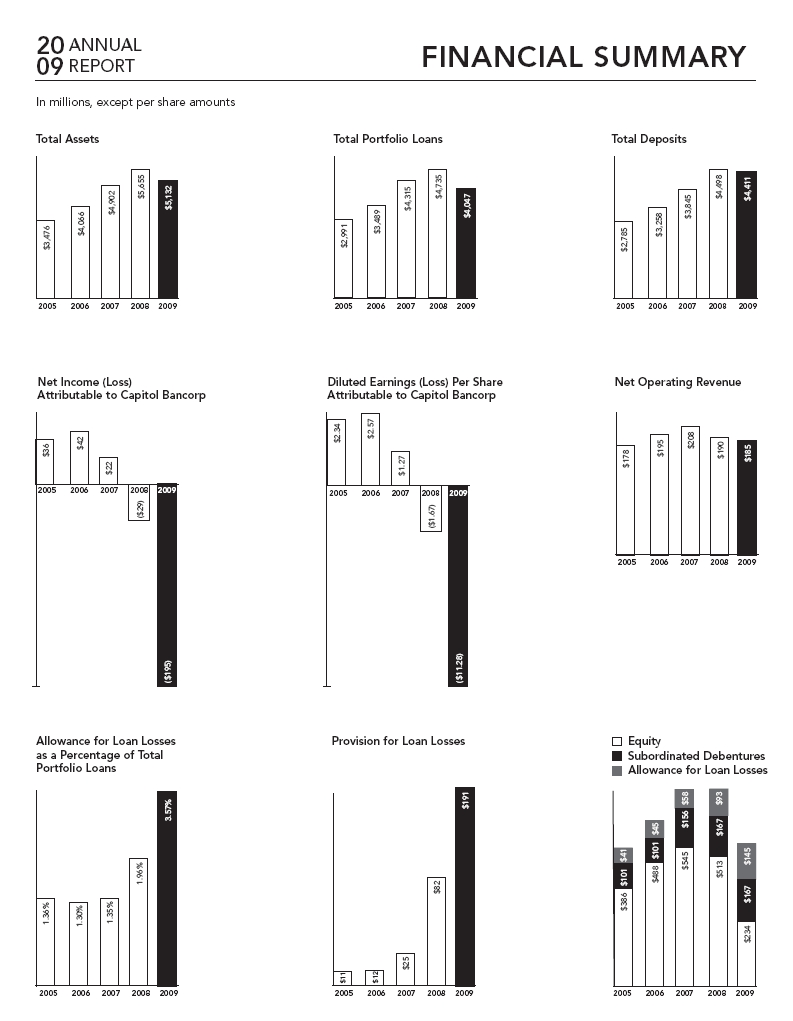

2009 and 2008 have been challenging due to significantly elevated levels of loan losses caused by economic stress on borrowers and depressed real estate collateral values, primarily at Capitol's Michigan and Arizona banks, resulting in a net loss attributable to Capitol of $195.2 million ($11.28 per share) in 2009 compared to a net loss attributable to Capitol of $28.6 million ($1.67 per share) in 2008. In 2007, Capitol reported net income attributable to Capitol of $21.9 million ($1.27 per diluted share).

F-11

Each bank began as a single-location office, led by a bank president and a team of banking professionals with significant local experience, overseen by an independent board of directors composed of business leaders drawn from that local community. Generally, each bank has significant on-site authority to make all decisions which directly affect the customer, such as credit approval and the pricing and structure of both loans and deposits. The philosophy of banking as a profession is key to Capitol's model where its banks' customers seek a relationship with banking professionals to meet their needs, as opposed to transaction-oriented financial institutions pushing financial products at customers and emphasizing market share.

With Capitol's focused banking model, bank development on a national scale has been a natural extension of this business philosophy. Bank development consists of management and oversight of banks in which Capitol has a direct or indirect controlling interest and, through mid-2008, included formation of start-up banks. Some of Capitol's banks were formed with a portion of their start-up capital provided by local investors in the communities of those banks.

Notably, 'market size' is not a big factor in Capitol's approach to bank development. Rather, the key is people. Capitol has recognized from its beginning that its banking focus always has been, and always will be, a people business. Capitol's banks are small in market stature in relation to their competitors, emphasizing personalized banking relationships.

Capitol has monitored and managed its investments in community banks working through regional presidents, supported by Capitol's bank performance group. Capitol's regional presidents and bank performance group assist the banks in the development of detailed budgets, implement asset/liability management strategies, monitor progress on the banks' business plans and review monthly operating results for each bank. In addition to monitoring operating results, Capitol assists in managing capital, including funding supplemental capital needed by the banks, subject to the availability of resources.

Bank performance and capital adequacy have been particularly challenging recently due to adverse operating results attributable to significant loan losses, adverse valuation trends in real estate and material increases in nonperforming assets.

[The remainder of this page intentionally left blank]

F-12

Capitol's relationship with its banks is multidimensional as an investor, mentor and service provider. As investor, Capitol closely monitors the financial performance of its bank subsidiaries. Capitol's mentoring role of providing assistance and guidance when and where necessary to help enhance bank performance is most important for its youngest affiliates where guidance is needed during their early formative stages. As a service provider, Capitol provides efficient back-office support services which can be performed centrally for all of its banks and which do not involve a direct interface with the bank customer, such as:

· | Accounting |

· | Capital management |

· | Credit administration |

· | Data processing |

· | Human resources administration |

· | Internal audit |

· | Legal support |

· | Risk management |

Some of these functions are performed nationally from a single location, while others are performed regionally, where it is more efficient to have personnel located geographically based on their respective responsibilities in relation to the physical location of the banks.

[The remainder of this page intentionally left blank]

F-13

Total assets and revenues of each bank within Capitol's regions are summarized below as of and for the years ended December 31, 2009 and 2008 (in $1,000s):

| Total Assets | Total Revenues(6) | ||||||||||||||

| 2009 | 2008 | 2009 | 2008 | ||||||||||||

| Arizona Region: | |||||||||||||||

| Bank of Tucson | $ | 204,933 | $ | 189,869 | $ | 12,709 | $ | 13,383 | |||||||

| Central Arizona Bank | 95,303 | 79,775 | 4,089 | 4,641 | |||||||||||

| Southern Arizona Community Bank | 94,585 | 88,146 | 5,188 | 5,907 | |||||||||||

| Sunrise Bank of Albuquerque | 78,930 | 81,977 | 4,110 | 5,203 | |||||||||||

Sunrise Bank of Arizona(4) | 495,168 | 592,666 | 23,712 | 36,081 | |||||||||||

Yuma Community Bank(5) | 73,028 | 3,225 | 5,273 | ||||||||||||

| Arizona Region Total | 968,919 | 1,105,461 | 53,033 | 70,488 | |||||||||||

| California Region: | |||||||||||||||

| Bank of Escondido | 103,469 | 96,803 | 4,767 | 5,036 | |||||||||||

| Bank of Feather River | 33,693 | 29,218 | 2,111 | 1,350 | |||||||||||

| Bank of San Francisco | 87,740 | 74,670 | 4,639 | 3,748 | |||||||||||

Bank of Santa Barbara(3) | 72,076 | 2,571 | 4,056 | ||||||||||||

| Napa Community Bank | 166,873 | 149,093 | 9,147 | 8,732 | |||||||||||

| Point Loma Community Bank | 66,700 | 61,514 | 3,400 | 3,804 | |||||||||||

| Sunrise Bank of San Diego | 83,825 | 86,322 | 4,557 | 5,415 | |||||||||||

| Sunrise Community Bank | 42,203 | 36,139 | 2,111 | 1,620 | |||||||||||

| California Region Total | 584,503 | 605,835 | 33,303 | 33,761 | |||||||||||

| Colorado Region: | |||||||||||||||

| Fort Collins Commerce Bank | 93,908 | 80,247 | 5,381 | 4,628 | |||||||||||

| Larimer Bank of Commerce | 89,623 | 88,725 | 5,333 | 4,567 | |||||||||||

| Loveland Bank of Commerce | 40,032 | 32,034 | 2,148 | 1,434 | |||||||||||

Mountain View Bank of Commerce(1) | 50,621 | 37,740 | 2,388 | 1,192 | |||||||||||

| Colorado Region Total | 274,184 | 238,746 | 15,250 | 11,821 | |||||||||||

| Great Lakes Region: | |||||||||||||||

| Bank of Auburn Hills | 35,546 | 43,856 | 2,231 | 2,766 | |||||||||||

| Bank of Maumee | 46,796 | 56,812 | 2,592 | 2,829 | |||||||||||

| Bank of Michigan | 99,344 | 78,716 | 4,860 | 4,902 | |||||||||||

| Capitol National Bank | 200,597 | 245,354 | 11,605 | 14,649 | |||||||||||

| Elkhart Community Bank | 94,163 | 99,917 | 4,558 | 5,684 | |||||||||||

| Evansville Commerce Bank | 56,392 | 63,228 | 3,458 | 4,014 | |||||||||||

| Goshen Community Bank | 81,244 | 87,419 | 4,358 | 5,140 | |||||||||||

Michigan Commerce Bank(2) | 1,089,508 | 1,275,125 | 62,982 | 79,937 | |||||||||||

| Ohio Commerce Bank | 66,175 | 60,678 | 3,263 | 2,672 | |||||||||||

| Paragon Bank & Trust | 108,235 | 107,491 | 6,271 | 7,024 | |||||||||||

| Great Lakes Region Total | 1,878,000 | 2,118,596 | 106,178 | 129,617 | |||||||||||

| Midwest Region: | |||||||||||||||

Adams Dairy Bank(1) | 44,309 | 33,867 | 2,337 | 1,621 | |||||||||||

| Bank of Belleville | 70,502 | 73,901 | 3,711 | 3,640 | |||||||||||

| Community Bank of Lincoln | 60,356 | 53,222 | 3,551 | 2,117 | |||||||||||

Summit Bank of Kansas City (3) | 53,429 | 2,780 | 3,074 | ||||||||||||

| Midwest Region Total | 175,167 | 214,419 | 12,379 | 10,452 | |||||||||||

| Nevada Region: | |||||||||||||||

1st Commerce Bank | 38,811 | 52,622 | 2,315 | 2,353 | |||||||||||

| Bank of Las Vegas | 75,313 | 73,692 | 4,430 | 4,853 | |||||||||||

| Black Mountain Community Bank | 177,822 | 157,545 | 9,479 | 10,739 | |||||||||||

| Desert Community Bank | 98,003 | 100,312 | 5,757 | 7,240 | |||||||||||

| Red Rock Community Bank | 137,648 | 126,993 | 5,810 | 7,709 | |||||||||||

| Nevada Region Total | 527,597 | 511,164 | 27,791 | 32,894 | |||||||||||

F-14

Summary of total assets and revenues – continued:

| Total Assets | Total Revenues(6) | ||||||||||||||

| 2009 | 2008 | 2009 | 2008 | ||||||||||||

| Northeast Region: | |||||||||||||||

| USNY Bank | $ | 64,176 | $ | 49,620 | $ | 3,265 | $ | 1,845 | |||||||

| Northwest Region: | |||||||||||||||

| Bank of Bellevue | 53,279 | 55,841 | 2,553 | 2,909 | |||||||||||

| Bank of Everett | 43,876 | 44,756 | 2,384 | 2,144 | |||||||||||

| Bank of Tacoma | 39,223 | 44,241 | 2,350 | 2,060 | |||||||||||

| High Desert Bank | 41,849 | 41,904 | 2,429 | 1,497 | |||||||||||

| Issaquah Community Bank | 37,627 | 36,942 | 2,105 | 1,296 | |||||||||||

| Northwest Region Total | 215,854 | 223,684 | 11,821 | 9,906 | |||||||||||

| Southeast Region: | |||||||||||||||

| Bank of Valdosta | 55,156 | 58,995 | 2,782 | 3,156 | |||||||||||

Community Bank of Rowan(3) | 138,341 | 4,962 | 7,311 | ||||||||||||

| First Carolina State Bank | 115,716 | 119,774 | 5,473 | 6,076 | |||||||||||

| Peoples State Bank | 26,198 | 29,233 | 1,361 | 1,705 | |||||||||||

Pisgah Community Bank(1) | 62,773 | 36,897 | 2,478 | 691 | |||||||||||

| Sunrise Bank of Atlanta | 55,966 | 62,198 | 3,668 | 4,434 | |||||||||||

| Southeast Region Total | 315,809 | 445,438 | 20,724 | 23,373 | |||||||||||

| Texas Region: | |||||||||||||||

| Bank of Fort Bend | 31,548 | 26,424 | 1,640 | 922 | |||||||||||

| Bank of Las Colinas | 43,003 | 31,354 | 1,979 | 1,288 | |||||||||||

| Texas Region Total | 74,551 | 57,778 | 3,619 | 2,210 | |||||||||||

Other, net(7) | 53,180 | 84,095 | 8,309 | 4,380 | |||||||||||

| Consolidated Totals | $ | 5,131,940 | $ | 5,654,836 | $ | 295,672 | $ | 330,747 | |||||||

| (1) | Became a Capitol affiliate in 2008 and is included for periods after addition to the Capitol banking network. |

| (2) | Effective March 31, 2009, Brighton Commerce Bank, Detroit Commerce Bank, Grand Haven Bank, Kent Commerce Bank, Macomb Community Bank, Muskegon Commerce Bank, Oakland Commerce Bank and Portage Commerce Bank merged with and into Ann Arbor Commerce Bank. Upon completion of the merger, the surviving bank was renamed Michigan Commerce Bank. Prior to the merger, each bank was a wholly-owned subsidiary of Capitol. |

| (3) | Bank of Santa Barbara, Community Bank of Rowan and Summit Bank of Kansas City are majority-owned subsidiaries of Capitol Development Bancorp Limited (CDBL) III of which Capitol ceased to have a majority voting control effective September 30, 2009; consequently those banks and CDBL III ceased to be consolidated subsidiaries of Capitol. CDBL III's ownership interest in Bank of Santa Barbara was sold in November 2009. |

| (4) | Effective December 14, 2009, Arrowhead Community Bank, Asian Bank of Arizona, Colonia Bank, Mesa Bank and Sunrise Bank of Arizona merged with and into Camelback Community Bank. Upon completion of the merger, the surviving bank was renamed Sunrise Bank of Arizona. Prior to the merger, each of the banks were either wholly-owned subsidiaries of Capitol or majority-owned by a bank development subsidiary in which Capitol holds a controlling interest. |

| (5) | Capitol sold its ownership in Yuma Community Bank effective September 21, 2009. The bank's operations are included in Capitol's consolidated totals up to the date of sale. |

| (6) | Total revenues is the sum of interest income and noninterest income. |

| (7) | Includes corporate and other nonbank entities. |

[The remainder of this page intentionally left blank]

F-15

For 2009, a net loss attributable to Capitol was incurred of approximately $195.2 million ($11.28 per share) compared to a net loss attributable to Capitol of $28.6 million ($1.67 per share) in 2008. Net income attributable to Capitol in 2007 approximated $21.9 million ($1.27 per diluted share).

The table below summarizes, for Capitol's banks individually and regionally, net income (loss) (in $1,000s) and the related rates of return on average equity and assets, where applicable:

| Net Income (Loss) | Return on Average Equity | Return on Average Assets | ||||||||||||||||||||||||||||||||||

| 2009 | 2008 | 2007 | 2009 | 2008 | 2007 | 2009 | 2008 | 2007 | ||||||||||||||||||||||||||||

| Arizona Region: | ||||||||||||||||||||||||||||||||||||

| Bank of Tucson | $ | 1,833 | $ | 3,717 | $ | 4,527 | 10.12 | % | 20.56 | % | 26.48 | % | 0.91 | % | 2.04 | % | 2.52 | % | ||||||||||||||||||

| Central Arizona Bank | (5,892 | ) | (1,004 | ) | 327 | 4.10 | % | 0.46 | % | |||||||||||||||||||||||||||

| Southern Arizona Community Bank | 434 | 639 | 1,082 | 4.73 | % | 7.06 | % | 12.04 | % | 0.48 | % | 0.72 | % | 1.22 | % | |||||||||||||||||||||

| Sunrise Bank of Albuquerque | (1,746 | ) | 224 | 601 | 3.05 | % | 8.95 | % | 0.29 | % | 0.86 | % | ||||||||||||||||||||||||

Sunrise Bank of Arizona(4) | (48,628 | ) | (13,505 | ) | 5,639 | 10.29 | % | 6.36 | % | |||||||||||||||||||||||||||

Yuma Community Bank(5) | 372 | 565 | 936 | 7.69 | % | 7.23 | % | 12.09 | % | 0.78 | % | 0.75 | % | 1.08 | % | |||||||||||||||||||||

| Arizona Region Total | (53,627 | ) | (9,364 | ) | 13,112 | |||||||||||||||||||||||||||||||

| California Region: | ||||||||||||||||||||||||||||||||||||

| Bank of Escondido | (1,107 | ) | 361 | 505 | 2.53 | % | 3.54 | % | 0.38 | % | 0.58 | % | ||||||||||||||||||||||||

| Bank of Feather River | (714 | ) | (487 | ) | (576 | ) | ||||||||||||||||||||||||||||||

| Bank of San Francisco | 52 | 43 | (397 | ) | 0.63 | % | 0.51 | % | 0.06 | % | 0.07 | % | ||||||||||||||||||||||||

Bank of Santa Barbara(3) | (1,300 | ) | (420 | ) | (191 | ) | ||||||||||||||||||||||||||||||

| Napa Community Bank | 485 | 1,223 | 1,542 | 3.01 | % | 8.39 | % | 11.73 | % | 0.32 | % | 0.93 | % | 1.29 | % | |||||||||||||||||||||

| Point Loma Community Bank | (1,869 | ) | 294 | 168 | 4.00 | % | 2.37 | % | 0.50 | % | 0.31 | % | ||||||||||||||||||||||||

| Sunrise Bank of San Diego | (2,141 | ) | 300 | 432 | 2.81 | % | 4.06 | % | 0.33 | % | 0.50 | % | ||||||||||||||||||||||||

| Sunrise Community Bank | (3,198 | ) | (646 | ) | (998 | ) | ||||||||||||||||||||||||||||||

| California Region Total | (9,792 | ) | 668 | 485 | ||||||||||||||||||||||||||||||||

| Colorado Region: | ||||||||||||||||||||||||||||||||||||

| Fort Collins Commerce Bank | 15 | 620 | 588 | 0.15 | % | 6.71 | % | 6.81 | % | 0.02 | % | 0.89 | % | 1.07 | % | |||||||||||||||||||||

| Larimer Bank of Commerce | 57 | 465 | (586 | ) | 0.70 | % | 6.09 | % | 0.06 | % | 0.66 | % | ||||||||||||||||||||||||

| Loveland Bank of Commerce | (872 | ) | (458 | ) | (426 | ) | ||||||||||||||||||||||||||||||

Mountain View Bank of Commerce(1) | (31 | ) | (819 | ) | ||||||||||||||||||||||||||||||||

| Colorado Region Total | (831 | ) | (192 | ) | (424 | ) | ||||||||||||||||||||||||||||||

| Great Lakes Region: | ||||||||||||||||||||||||||||||||||||

| Bank of Auburn Hills | (3,938 | ) | (957 | ) | (335 | ) | ||||||||||||||||||||||||||||||

| Bank of Maumee | (2,834 | ) | (774 | ) | (1,063 | ) | ||||||||||||||||||||||||||||||

| Bank of Michigan | 152 | 543 | (136 | ) | 2.16 | % | 7.95 | % | 0.16 | % | 0.76 | % | ||||||||||||||||||||||||

| Capitol National Bank | (7,175 | ) | (766 | ) | 1,977 | 10.45 | % | 0.84 | % | |||||||||||||||||||||||||||

| Elkhart Community Bank | (3,535 | ) | 39 | 766 | 0.45 | % | 8.67 | % | 0.04 | % | 0.90 | % | ||||||||||||||||||||||||

| Evansville Commerce Bank | (1,644 | ) | (248 | ) | (689 | ) | ||||||||||||||||||||||||||||||

| Goshen Community Bank | (39 | ) | 178 | 431 | 2.23 | % | 5.72 | % | 0.22 | % | 0.54 | % | ||||||||||||||||||||||||

Michigan Commerce Bank(2) | (69,569 | ) | (13,768 | ) | 6,050 | 5.66 | % | 0.48 | % | |||||||||||||||||||||||||||

| Ohio Commerce Bank | 206 | (149 | ) | (770 | ) | 2.24 | % | 0.33 | % | |||||||||||||||||||||||||||

| Paragon Bank & Trust | (7,555 | ) | (1,501 | ) | (187 | ) | ||||||||||||||||||||||||||||||

| Great Lakes Region Total | (95,931 | ) | (17,403 | ) | 6,044 | |||||||||||||||||||||||||||||||

| Midwest Region | ||||||||||||||||||||||||||||||||||||

Adams Dairy Bank(1) | (66 | ) | (669 | ) | ||||||||||||||||||||||||||||||||

| Bank of Belleville | 122 | 35 | (572 | ) | 1.79 | % | 0.49 | % | 0.17 | % | 0.06 | % | ||||||||||||||||||||||||

| Community Bank of Lincoln | (1,516 | ) | (643 | ) | (500 | ) | ||||||||||||||||||||||||||||||

Summit Bank of Kansas City(3) | (978 | ) | (97 | ) | (404 | ) | ||||||||||||||||||||||||||||||

| Midwest Region Total | (2,438 | ) | (1,374 | ) | (1,476 | ) | ||||||||||||||||||||||||||||||

F-16

Net income (loss) and the related rates of return on average equity and assets – continued:

| Net Income (Loss) | Return on Average Equity | Return on Average Assets | |||||||||||||||||||||||||||||||||||

| 2009 | 2008 | 2007 | 2009 | 2008 | 2007 | 2009 | 2008 | 2007 | |||||||||||||||||||||||||||||

| Nevada Region: | |||||||||||||||||||||||||||||||||||||

1st Commerce Bank | $ | (3,009 | ) | $ | (1,158 | ) | $ | (578 | ) | ||||||||||||||||||||||||||||

| Bank of Las Vegas | (2,112 | ) | 44 | 608 | 0.51 | % | 6.77 | % | 0.06 | % | 0.83 | % | |||||||||||||||||||||||||

| Black Mountain Community Bank | (1,305 | ) | 2,001 | 2,612 | 13.40 | % | 18.40 | % | 1.30 | % | 1.81 | % | |||||||||||||||||||||||||

| Desert Community Bank | (2,423 | ) | 596 | 1,296 | 5.87 | % | 13.54 | % | 0.58 | % | 1.35 | % | |||||||||||||||||||||||||

| Red Rock Community Bank | (5,435 | ) | 660 | 1,652 | 4.83 | % | 12.34 | % | 0.54 | % | 1.44 | % | |||||||||||||||||||||||||

| Nevada Region Total | (14,284 | ) | 2,143 | 5,590 | |||||||||||||||||||||||||||||||||

| Northeast Region: | |||||||||||||||||||||||||||||||||||||

| USNY Bank | (1,188 | ) | (748 | ) | (908 | ) | |||||||||||||||||||||||||||||||

| Northwest Region: | |||||||||||||||||||||||||||||||||||||

| Bank of Bellevue | (1,929 | ) | (146 | ) | (154 | ) | |||||||||||||||||||||||||||||||

| Bank of Everett | (2,670 | ) | (956 | ) | (636 | ) | |||||||||||||||||||||||||||||||

| Bank of Tacoma | (3,710 | ) | (824 | ) | (1,067 | ) | |||||||||||||||||||||||||||||||

| High Desert Bank | (2,948 | ) | (801 | ) | (514 | ) | |||||||||||||||||||||||||||||||

| Issaquah Community Bank | (1,580 | ) | (627 | ) | (574 | ) | |||||||||||||||||||||||||||||||

| Northwest Region Total | (12,837 | ) | (3,354 | ) | (2,945 | ) | |||||||||||||||||||||||||||||||

| Southeast Region: | |||||||||||||||||||||||||||||||||||||

| Bank of Valdosta | (1,643 | ) | (139 | ) | (423 | ) | |||||||||||||||||||||||||||||||

Community Bank of Rowan(3) | 459 | 945 | (183 | ) | 5.73 | % | 9.39 | % | 0.47 | % | 0.76 | % | |||||||||||||||||||||||||

| First Carolina State Bank | (1,885 | ) | (403 | ) | 539 | 4.52 | % | 0.53 | % | ||||||||||||||||||||||||||||

| Peoples State Bank | (2,320 | ) | (72 | ) | 254 | 5.14 | % | 0.93 | % | ||||||||||||||||||||||||||||

Pisgah Community Bank(1) | (1,417 | ) | (920 | ) | |||||||||||||||||||||||||||||||||

| Sunrise Bank of Atlanta | (4,239 | ) | (554 | ) | (338 | ) | |||||||||||||||||||||||||||||||

| Southeast Region Total | (11,045 | ) | (1,143 | ) | (151 | ) | |||||||||||||||||||||||||||||||

| Texas Region: | |||||||||||||||||||||||||||||||||||||

| Bank of Fort Bend | (1,268 | ) | (829 | ) | (461 | ) | |||||||||||||||||||||||||||||||

| Bank of Las Colinas | (1,259 | ) | (623 | ) | (658 | ) | |||||||||||||||||||||||||||||||

| Texas Region Total | (2,527 | ) | (1,452 | ) | (1,119 | ) | |||||||||||||||||||||||||||||||

Other, net(6) | (60,040 | ) | (20,232 | ) | (14,874 | ) | |||||||||||||||||||||||||||||||

| Consolidated totals | $ | (264,540 | ) | $ | (52,451 | ) | $ | 3,334 | 5.72 | % | 0.49 | % | |||||||||||||||||||||||||

| (1) | Became a Capitol affiliate in 2008 and is included for periods after addition to the Capitol banking network. |

| (2) | Effective March 31, 2009, Brighton Commerce Bank, Detroit Commerce Bank, Grand Haven Bank, Kent Commerce Bank, Macomb Community Bank, Muskegon Commerce Bank, Oakland Commerce Bank and Portage Commerce Bank merged with and into Ann Arbor Commerce Bank. Upon completion of the merger, the surviving bank was renamed Michigan Commerce Bank. Prior to the merger, each bank was a wholly-owned subsidiary of Capitol. |

| (3) | Bank of Santa Barbara, Community Bank of Rowan and Summit Bank of Kansas City are majority-owned subsidiaries of CDBL III of which Capitol ceased to have a majority voting control effective September 30, 2009; consequently those banks and CDBL III ceased to be consolidated subsidiaries of Capitol. CDBL III's ownership interest in Bank of Santa Barbara was sold in November 2009. |

| (4) | Effective December 14, 2009, Arrowhead Community Bank, Asian Bank of Arizona, Colonia Bank, Mesa Bank and Sunrise Bank of Arizona merged with and into Camelback Community Bank. Upon completion of the merger, the surviving bank was renamed Sunrise Bank of Arizona. Prior to the merger, each of the banks were either wholly-owned subsidiaries of Capitol or majority-owned by a bank development subsidiary in which Capitol holds a controlling interest. |

| (5) | Capitol sold its ownership in Yuma Community Bank effective September 21, 2009. The bank's operations are included in Capitol's consolidated totals up to the date of the sale. |

| (6) | Includes corporate and other nonbank entities. |

The preceding table presents net income (loss) of each bank without regard to Capitol's direct or indirect ownership percentage and indicates significant losses incurred at banks within the Great Lakes and Arizona Regions. Dominating the Great Lakes Region are Capitol's three mature, majority-owned banks located in Michigan. Operating results of this group of banks amounted to a net loss of $84.3 million in 2009, compared to $16.0 million in 2008 and net income of $7.8 million in 2007. The unprecedented 2009 operating losses of this group of banks was

F-17

attributable to loan losses stemming from a sustained difficult economy, significant increases in nonperforming assets, depressed real estate valuations, a weak or nonexistent real estate sales environment and elevated collection costs. These, coupled with loan losses incurred at Sunrise Bank of Arizona, where its adverse asset quality and related loans as a percentage of capital exceed other regions, are the largest items adversely impacting Capitol's 2009 consolidated operating results, followed by valuation losses recognized at the parent level and compression in margins and related net interest income.

The principal revenue source for Capitol's banks is interest income from loans. Net interest income is the total of all interest income minus all interest expense. This is an important measure that is used to help determine the amount of net operating revenue for financial institutions. Net operating revenue is the sum of net interest income and noninterest income.

Net interest income totaled $156.4 million in 2009, a 4.6% decrease from the $163.8 million reported in 2008, compared to an 11% decrease in 2008 versus a 5% increase in 2007. The decreases in net interest income are due to sharp increases in nonperforming assets and a challenging interest rate environment which reduced the spread between interest earned on loans and rates paid on deposits. The modest 2007 increase in net interest income was due to balance-sheet growth offset by compression in margins, resulting from lower rates earned on loans and elevated levels of nonperforming loans, coupled with the slower repricing of rates paid on deposits and decreased loan volume.

Combined with noninterest income, total consolidated net operating revenue approximated $185.2 million in 2009, $190.3 million in 2008 and $207.7 million in 2007. Noninterest income for these years was $28.8 million, $26.4 million and $24.4 million, respectively. Noninterest income increased 8.9% in 2009.

Service charges approximated $5.9 million in 2009 and 2008 ($4.8 million in 2007). Revenue from trust and wealth management decreased 20% in 2009, following increases of 20% in 2008 and 54% in 2007, after the late-2005 launch of Capitol Wealth, Inc. (Capitol Wealth), an initiative to expand Capitol's banks' scope of services in meeting the needs of their clients beyond loans and deposits. Full-time Capitol Wealth advisors are located at several of Capitol's banks to work in tandem with their traditional banking colleagues to expand the availability of financial services to the banks' clientele, while increasing noninterest revenues. Capitol Wealth has not yet achieved profitability, although it has recently become cash-flow neutral and its revenues decreased in 2009 due to market volatility and client activity.

In 2009, 2008 and 2007, revenue from mortgage loans originated for sale included in other noninterest income amounted to $3.9 million, $3.6 million and $4.5 million, respectively. Loan origination volume fluctuated in these periods as the instability of residential real estate market conditions has negatively impacted residential mortgage origination volume. Total other noninterest income increased 15.7% in 2009 and 19.2% in 2008. Due to the nature of these revenues, including gains on the sale of government-guaranteed loans and other gains, the amounts can vary significantly from year to year depending on interest rates, business opportunities and other activities, including gains on sale of bank subsidiaries.

F-18

Net interest income was insufficient in 2009 to offset the provision for loan losses. The provision for loan losses approximated $190.7 million, $82.5 million and $25.3 million in 2009, 2008 and 2007, respectively. The dramatic increase in the provision for loan losses in 2009 was primarily associated with loan losses and related significantly elevated levels of nonperforming loans incurred within the Great Lakes Region's Michigan banks and the Arizona-based Sunrise Bank of Arizona. The amount of the provision for loan losses is determined based on management's analysis of amounts necessary for the allowance for loan losses; this is discussed in greater detail later in the Capitol's Financial Position section of this narrative.

Noninterest expense totaled $240.6 million, $190.4 million and $176.2 million in 2009, 2008 and 2007, respectively. In total, these expenses increased 26.4% in 2009, 8.1% in 2008 and 27.8% in 2007. Increases in the components of noninterest expense in 2009 were primarily associated with the costs of foreclosed properties and other real estate owned and FDIC insurance premiums.

The largest element of noninterest expense is salaries and employee benefits which approximated $99.6 million, $108.7 million and $106.6 million in 2009, 2008 and 2007, respectively. Employee compensation costs decreased about 8.4% in 2009 as a result of Capitol's efforts to reduce and streamline staffing at its banks and corporate offices. Increases in employee compensation costs in 2008 and 2007 resulted primarily from the formation of start-up banks during those periods. Most recently, for the fourth quarter of 2009 salaries and employee benefits were reduced 13.5% from the corresponding period of 2008. Further reductions are anticipated during 2010.

Preopening and start-up costs of de novo banks and bank-development subsidiaries approximated $1.9 million in 2008 and $5.7 million in 2007 (none in 2009) which related to the number of new affiliates during those periods.

Occupancy costs increased slightly by 3.4% in 2009, after increasing more significantly in 2008 and 2007 (23.7% and 24.5%, respectively), due to newly-formed banks during those years.

Equipment rent, depreciation and maintenance expense increased $6.9 million (55.6%) in 2009, primarily related to estimated loss accruals on certain leased property. This category increased about 23.3% in 2008 and 19.5% in 2007 due to newly-formed banks.

Costs associated with foreclosed properties and other real estate owned increased significantly in 2009 to $45.7 million from $6.9 million in 2008 and $1.0 million in 2007; such increases corresponded with sharp increases in related other real estate owned which increased from $16.4 million at the beginning of 2008 to $67.2 million at year-end 2008, and $111.8 million at December 31, 2009. Most of the costs associated with foreclosed properties and other real estate owned resulted from adverse valuation adjustments.

F-19

FDIC insurance premiums and other regulatory fees increased significantly by 280% in 2009 as compared with a 49% increase in 2008 and a 210% increase in 2007. FDIC insurance premiums are expected to continue increasing significantly in the future as the FDIC seeks to bolster its insurance fund after incurring numerous losses due to bank failures and higher levels of deposit insurance.

The more significant elements of other noninterest expense consisted of the following (in $1,000s):

| 2009 | 2008 | 2007 | |||||||||

| Legal fees | $ | 2,925 | $ | 1,400 | $ | 644 | |||||

| Professional fees | 2,814 | 1,637 | 1,824 | ||||||||

| Loan and collection expense | 2,650 | 1,990 | 1,952 | ||||||||

Bank services (ATMs, telephone banking and Internet banking) | 2,627 | 2,622 | 2,115 | ||||||||

| Directors' fees | 2,288 | 2,828 | 2,819 | ||||||||

| Paper, printing and supplies | 2,025 | 2,825 | 2,870 | ||||||||

| Advertising | 1,988 | 3,261 | 3,315 | ||||||||

| Travel, lodging and meals | 1,828 | 2,998 | 3,080 | ||||||||

| Communications | 1,728 | 2,197 | 1,728 | ||||||||

| Insurance | 1,361 | 629 | 473 | ||||||||

| Postage | 1,230 | 1,323 | 1,113 | ||||||||

| Taxes other than income taxes | 919 | 825 | 1,786 | ||||||||

| Dues and memberships | 859 | 974 | 928 | ||||||||

| Courier service | 711 | 902 | 997 | ||||||||

| Contracted labor | 285 | 426 | 496 | ||||||||

| Other | 15,195 | 10,974 | 8,951 | ||||||||

| Total | $ | 41,433 | $ | 37,811 | $ | 35,091 | |||||

Income tax expense approximated $18.4 million in 2009, primarily resulting from the combined effect of recording a valuation allowance for deferred income tax assets at December 31, 2009 ($104.5 million), recoverable income taxes of $43.8 million and a credit for deferred income taxes of $43.4 million (subject to the valuation allowance). A valuation allowance for deferred income tax assets was recorded based on management's assessment of the realizability of such assets not meeting the requisite more-likely-than-not criteria at December 31, 2009.

The amount of recoverable income taxes increased significantly in 2009 due to the Corporation's operating loss and a nonrecurring opportunity to "carryback" such losses to recover taxes paid during the preceding five years. Loss carryback rules were previously limited to the most recent two-year period, which resumes as the limitation effective January 1, 2010.

The valuation allowance for deferred income tax assets should reduce future income tax expense to the extent of Capitol's profitability.

Capitol's effective tax rate was 36.5% in 2008 and 45.9% in 2007. The statutory federal income tax rate applicable to Capitol is 35%. The effective tax rate includes state income taxes, but excludes taxes incurred in states which are based on measures other than income (which are shown in the table above).

F-20

Consolidated total assets decreased in 2009 to $5.1 billion from $5.7 billion at the end of 2008. Total assets were $4.9 billion at the beginning of 2008. The 2009 decrease in total assets primarily resulted from Capitol's efforts to 'deleverage' its consolidated balance sheet through reductions in portfolio loans and borrowings.

Key to the balance sheet of Capitol is its total capital position (subordinated debentures and total equity approximating $401.0 million or 7.8% of total assets) and liquidity (cash and cash equivalents of $808.9 million or 15.8% of total assets) at December 31, 2009. Both of those key elements are discussed in the next section, Liquidity, Capital Resources and Capital Adequacy.

When considering Capitol's financial position, as shown in its consolidated balance sheet, clearly the single largest asset category is portfolio loans. Accordingly, the narrative in this section is devoted primarily to loans and related aspects of asset quality.

Net portfolio loans (total portfolio loans after subtracting the allowance for loan losses) approximated $3.9 billion at December 31, 2009 and $4.6 billion at December 31, 2008. These amounts approximated 76% of total consolidated assets at December 31, 2009 and 82% at December 31, 2008. Loan growth slowed in 2008 and Capitol's efforts to deleverage its balance sheet, as previously mentioned, helped reduce portfolio loans in 2009.

Capitol's banks have emphasized commercial loans, consistent with their focus on lending to local entrepreneurs, professional service firms and other businesses. All of Capitol's banks use a common credit policy; however, most credit decisions are made at the local level at each community bank. The utilization of an enterprise-wide credit policy has several key benefits to Capitol and its banks, such as procedural guidance for:

· | Loan underwriting and documentation |

· | Credit granting authorities within the bank |

· | Acceptable collateral and loan structuring |

· | Loan participations amongst other affiliates or other funding sources when proposals exceed an individual bank's limitations |

· | Collections and workouts |

· | Documenting and evaluating the adequacy of the allowance for loan losses |

· | Establishing corporate credit administration resources to aid the banks when needed |

F-21

The underwriting standards to be followed for loans secured by real estate are basic credit granting fundamentals applicable to any extension of credit. For construction loans, the banks follow these general underwriting policies enhanced by awareness of the increased risk of construction loans. General underwriting policies include analyzing and documenting:

· | Borrower and project financial data |

· | Contingent liabilities and related cash flows |

· | Adequacy of liquidity and the components of net worth |

· | Historic and projected cash flow data, including interest and vacancy rates sensitivity analysis |

· | Character, credit history and management ability |

· | Appraisal market valuation, local market conditions and volatility |

· | Proposed use of the project and potential future uses of the property |

Additional lending requirements include regulatory loan-to-value guidelines which are calculated based on current appraised value for loans that finance properties acquired by the borrower.

Variable-rate commercial loans are currently emphasized during today's historically-low interest rate environment. Most variable-rate commercial loans have floors and are underwritten with evaluation of the borrower's ability to repay based on fully-indexed rates. Since substantially all residential mortgage loan origination volume is underwritten to secondary-market standards and the loans are sold into those markets without recourse, Capitol and its banks have no material exposure to hybrid loans such as option-ARMs or subprime credits.

As part of the banks' emphasis on commercial lending, commercial real estate has been sought as the primary source of collateral for commercial loans when possible. This emphasis on use of commercial real estate as collateral has been a consistent practice of Capitol and its banks from their earliest days of operation, based on the use of appropriate loan-to-value ratios at the time of loan origination, avoidance of large real estate development projects and the belief that, even in volatile economies, commercial real estate tends to have substantially less loss potential than other types of business-asset collateral, such as receivables, inventory and equipment.

In the current economic environment, market conditions and related values of real estate as collateral have deteriorated significantly as evidenced by adverse asset quality trends in 2009 and 2008 and related large levels of loan losses and negative valuation adjustments of other real estate owned. Other real estate owned results from properties acquired through a foreclosure proceeding or acceptance of a deed in lieu of foreclosure. Those properties are held for sale at the lower of cost or fair value, less estimated selling cost, and are reviewed periodically for subsequent impairment.

F-22

There is significant uncertainty in future real estate values, appraisal results and the resulting potential impact on valuation of collateral-dependent loans and other real estate owned. The fair value measurement of collateral-dependent loans and other real estate owned is dependent primarily upon appraisal of the underlying property value. Management cautiously monitors real estate and related appraisal data when evaluating the fair value of real estate collateral.

Updated appraisals are generally obtained when it has been determined that a collateral-dependent loan has become impaired or when it is likely a real-estate loan will be foreclosed. Adjustments to the loan's carrying value (or requirements for the allowance for loan losses) are made, when appropriate, after review and acceptance of the appraisal or subsequently adjusted if it is determined that estimated fair value declines further. The timing of the recognition of a collateral-dependent loan as nonperforming is dependent on several factors, including the performance of the loan, the payment history of the loan or the receipt of updated borrower financial information.