EXHIBIT 99.2

CONFIDENTIAL OUT-OF-COURT EXCHANGE OFFERING MEMORANDUM AND SOLICITATION OF CONSENTS AND DISCLOSURE STATEMENT AND SOLICITATION OF VOTES RELATED TO A PREPACKAGED JOINT PLAN OF REORGANIZATION

(1) Offers to Effect an Out-of-Court Exchange Relating to Any and All of its Outstanding Senior Notes and Trust Preferred Securities for shares of Series B Preferred Stock of Capitol Bancorp Ltd. as described herein, and

(2) Solicitation of Votes on a Prepackaged Joint Plan of Reorganization which may be Implemented Only Upon Receipt of Insufficient Support of an Out-of-Court Exchange, subject to Certain Conditions.

THE OUT-OF-COURT EXCHANGE OFFERS AND VOTES ON THE IN-COURT STANDBY PREPACKAGED JOINT PLAN OF REORGANIZATION WILL EXPIRE AT 5:00 P.M., EASTERN DAYLIGHT TIME, ON JULY 27, 2012 (THE “EXPIRATION TIME” OR “VOTING DEADLINE”, AS APPLICABLE), UNLESS EXTENDED AS DESCRIBED HEREIN. ONCE ANY SENIOR NOTES AND/OR TRUST PREFERRED SECURITIES AND HOLDERS OF TRUST PRFERRED SECURITES HAVE BEEN TENDERED OR VOTES TO ACCEPT OR REJECT THE IN-COURT STANDBY PLAN HAVE BEEN MADE, THEY MAY NOT BE WITHDRAWN OR REVOKED, SUBJECT TO APPLICABLE LAW OR AS OTHERWISE SPECIFIED HEREIN; PROVIDED THAT, IF EITHER THE EXPIRATION TIME OR VOTING DEADLINE (AS APPLICABLE) HAS BEEN EXTENDED PAST AUGUST 10, 2012, HOLDERS SHALL HAVE THE RIGHT TO WITHDRAW THEIR TENDERS AND VOTES RESPECTIVELY. IF THE OUT-OF-COURT EXCHANGE OFFERS ARE SUCCESSFUL, THE VOTES TO ACCEPT OR REJECT THE IN-COURT STANDBY PLAN WILL BE OF NO EFFECT. |

Capitol Bancorp Ltd., a Michigan corporation (the “Company” or “Capitol”) is proposing a financial restructuring of certain of its outstanding indebtedness in an effort to make the Company more attractive to raise needed capital to recapitalize its bank subsidiaries as described in this Confidential Out-of-Court Exchange Offering Memorandum and Solicitation of Consents and Disclosure Statement and Solicitation of Votes Related to an In-Court Standby Prepackaged Joint Plan of Reorganization (this “Offering Memorandum and Disclosure Statement”). The Company is not currently in default with respect to either its outstanding Senior Notes or its Trust Preferred Securities. However, a number of the Company’s subsidiary banks are dangerously close to failing to meet the minimum capital ratios necessary to avoid seizure of the banks by the Federal Deposit Insurance Corporation (the “FDIC”), which is

legally required to seize banks that fall below certain thresholds. Moreover, the failure of even one of the Company’s subsidiary banks endangers the Company and its other subsidiary banks as a result of the FDIC’s ability to assert “cross-guaranty liability” against such banks in order to recover any losses experienced by the FDIC in a bank seizure. Such a bank seizure and liability assessment would virtually destroy any value held by Capitol’s current stakeholders. In order to avoid this calamitous result, the Company is proposing to effect a financial restructuring combined with a coterminous capital raise (as more fully discussed herein) through one of the following two approaches:

Approach 1. An out-of-court financial restructuring and capital raise consisting of the exchange of the Company’s outstanding Senior Notes and Trust Preferred Securities through the out-of-court Exchange Offers (as defined herein) in accordance with the terms and subject to the conditions set forth in this Offering Memorandum and Disclosure Statement, and the related letter of transmittal (the “Letter of Transmittal”) providing for the exchange of outstanding Senior Notes and Trust Preferred Securities for shares of the Corporation’s Series B Preferred Stock and the infusion of new equity from outside investors.

A key factor in the ability of the Company to successfully utilize Approach 1 is the degree of participation in the Exchange Offers by the holders of the Company’s outstanding Senior Notes and Trust Preferred Securities. Unless at least 90% of such holders participate in the Exchange Offer, it is unlikely that, even with a successfully simultaneous capital raise, the Exchange Offers would improve the Company’s financial position to the degree necessary for long-term viability. Another key factor will be whether consummation of the Exchange Offers would cause an ownership shift within the meaning of Section 382 of the Internal Revenue Code of 1986, as amended (the “Tax Code”), which could lead to severe limitations which would eliminate substantially of the Company’s ability to utilize a sizeable portion of its substantial deferred tax assets. The Company intends to carefully balance the advantages of Approach 1 with the potential effect on its potentially valuable deferred tax assets.

—OR, IN THE ALTERNATIVE—

(if conditions to completion of the out-of-court Exchange Offers are not satisfied or waived)

Approach 2. An in-court financial restructuring and capital raise through which the Company and its subsidiary Financial Commerce Corporation1 (“FCC” and together with the Company, in the context of the Standby Plan, collectively, the “Debtors”), would seek to accomplish a coterminous restructuring and capital raise through an in-court standby prepackaged joint plan of reorganization in the form set forth in Annex B (the “Standby Plan”), votes on which the Company is soliciting, concurrently with the Exchange Offers, upon the terms and subject to the conditions set forth in this Offering Memorandum and Disclosure

1 FCC is formerly known as Michigan Commerce Bancorp Limited, which amended its Articles of Incorporation on June 14, 2012 to change its name to Financial Commerce Corporation.

Statement and the related ballots (each a “Ballot” and collectively the “Ballots”) for accepting or rejecting the Standby Plan. If the Exchange Offers are not consummated, and the requisite votes of the classes of the holders of the Senior Notes, Trust Preferred Securities, the Company’s Series A Preferred Stock and the Company’s Common Stock have voted to accept the Standby Plan as of the Expiration Time in a manner that satisfies the Threshold (as defined herein), the Company may file a Voluntary Petition for relief under chapter 11 of the Bankruptcy Code (as defined herein) and seek prompt confirmation of the Standby Plan in the Court (as defined herein). Such a filing could enable the Company to utilize an exception to the ownership change limitations on utilization of deferred tax assets available under Section 382(l)(5) of the Tax Code. This exception is unavailable in a traditional out-of-court restructuring.

A key factor in the ability of the Company to successfully utilize Approach 2 is the lower threshold required to bind certain holders of outstanding Senior Notes and Trust Preferred Securities who might otherwise hold out from the anticipated restructuring and capital raise. Under the Bankruptcy Code, (i) a class of claims votes to accept a plan of reorganization if holders holding at least two-thirds of the aggregate principal amount of the class of claims and more than one half in number of such class of claims that submit votes on the plan of reorganization vote to accept the plan and (ii) a class of interests votes to accept a plan of reorganization if holders of at least two-thirds in amount of the class of interests that submit votes on the plan of reorganization vote to accept the plan. Another key factor will be the Company’s potential ability to use an exception to the ownership change limitations on utilization of deferred tax assets available under Section 382(l)(5) of the Tax Code. As of March 31, 2012, the Company currently estimates (as qualified by the discussion below) that the federal deferred tax assets of the Company and its affiliates are approximately $142.590 million, which could be preserved if Section 382(l)(5) of the Tax Code applies to any ownership changes pursuant to the Standby Plan (subject to an interest “haircut” estimated that is estimated to have a negative $3.6 million impact on such deferred tax asset and other adjustments that are expected to increase the such deferred tax assets).

Estimated Recovery Under Approach 1 and Approach 2 All recovery estimates set forth below are based on principal amount outstanding, exclusive of accrued interest, and are subject to the qualifications set forth herein including the Risk Factors beginning on page 32. Allowed Senior Note Claims and Allowed Trust Preferred Security Claims will include each holder’s pro rata share of such interest (including, in the case of Senior Notes, any applicable post-petition interest). Accordingly, the recovery estimates set forth below will vary for each holder. |

| | Exchange Offer | Standby Plan |

| | Equity Instrument | Value | % Recovery | Equity Instrument | Value | % Recovery |

Senior Notes ($7 million)2 | Series B Preferred | $0.7m | 10% | Class A Common Class B Common | $7m | |

Trust Preferred Securities ($151.3 million) | Series B Preferred | $15.1m | 10% | HoldCaps Redeemable | | 33% |

Series A Preferred Stock ($5 million) | N/A | N/A | N/A | Class A Common and Class B Common | $1m | 20% |

| Common Stock | N/A | N/A | N/A | Class A Common and Class B Common | $15m | N/A |

2 There is currently $8.4 million in outstanding principal amount of Senior Notes; however, pursuant to the Company’s pending agreement to sell its equity interests in Bank of Michigan, approximately $1.6 million in principal amount could be discharged if, as expected, the deal is consummated in July of 2012. In the event that the sale does not close prior to consummation of the Exchange Offers or the Effective Date of the Standby Plan, the additional $1.6 million in outstanding principal amount would receive additional shares of New Capitol Bancorp Class A Common and Class B Common, and would reduce the amount of such securities received by the pre-petition common equity accordingly. For purposes of the tables set forth herein, the Company assumes approximately $7 million in Senior Notes will be outstanding as of the Effective Date. The Plan Value and voting power of the New Capitol Bancorp Class A Common Stock to be issued to Holders of Senior Notes and the Company’s Common Stock is in the aggregate approximately 95.65% of the total Plan Value and voting power of the New Capitol Bancorp Class A Common Stock to be issued pursuant to the Plan. The Plan Value and voting power of the New Capitol Bancorp Class B Common Stock to be issued to Holders of Senior Notes and the Company’s Common Stock is in the aggregate approximately 9.44% of the total Plan Value and voting power of the New Capitol Bancorp Class A Common Stock to be issued pursuant to the Plan.

3 Estimate based on Standby Plan value as reflected in the Projections. Holders of Senior Notes will not be paid in cash and are therefore deemed impaired and entitled to vote under bankruptcy law.

4 The Standby Plan value of the HoldCaps will be $50 million on the Effective Date, based upon the valuation set forth herein. Based on the Projections, and subject to the assumptions therein, if the HoldCaps are redeemed in 2016, the holders would receive approximately $80 million in cash.

It is important at the outset to emphasize the limited dimensions of this process: · No banking subsidiary of Capitol nor their respective depositors will be affected in any way. Each subsidiary bank of Capitol continues to operate and its customers’ deposits remain insured up to the applicable limits by the FDIC. Banks themselves cannot file for reorganization, but bank holding companies — and Capitol and FCC are holding companies, not banks — can use the reorganization process under federal law. · If the Standby Plan is approved, the court-supervised reorganization should move forward very quickly. A prepackaged plan shortens and simplifies the bankruptcy process. It can be very efficient and effective. · All of Capitol’s general unsecured creditors will be paid in full in order to maintain the regular course of business at the Company’s subsidiary banks, as uninterrupted service at the subsidiary bank level is critical to the success of the recapitalization effort. A loss of customer confidence in the safety of their deposits would have disastrous consequences for the Company. Exceptional times call for exceptional and innovative solutions to preserve value. That is why this Offering Memorandum and Disclosure Statement and the Standby Plan are important to Capitol’s creditors and stakeholders and to the banking industry generally. |

* * * * *

In connection with the Exchange Offers, this Offering Memorandum and Disclosure Statement (and all exhibits, schedules and appendices hereto and thereto), the accompanying form of Letter of Transmittal, and the related materials delivered together herewith are being furnished to holders of the Company’s Series A Preferred Stock, holders of the Company’s Common Stock, holders of Trust Preferred Securities issued by Capitol Trust I and Capitol Trust XII (the “Public Trust Preferred Securities”), holders of all the Company’s Trust Preferred Securities other than the Public Trust Preferred Securities (the “Private Trust Preferred Securities”) and holders of the Senior Notes pursuant to section 3(a)(9) of the Securities Act of 1933, as amended (the “Securities Act”).

In connection with the Standby Plan, this Memorandum and Disclosure Statement (and all exhibits, schedules and appendices hereto and thereto), the accompanying forms of Ballot and Master Ballot and the related materials delivered together herewith are being furnished to holders of the Company’s Series A Preferred Stock, holders of the Company’s Common Stock and holders of the Public Trust Preferred Securities pursuant to section 3(a)(9) of the Securities Act and section 1126(b) of the Bankruptcy Code and to holders of the Senior Notes and holders of all the Company’s Private Trust Preferred Securities pursuant to section 4(2) of the Securities Act and section 1126(b) of the Bankruptcy Code. Only holders of the Senior Notes and Private Trust Preferred

Securities that are “accredited investors” (individually, an “Accredited Investor” and collectively, “Accredited Investors”) within the meaning of Rule 501(a) of Regulation D of the Securities Act (each such holder, and each holder of the Company’s Series A Preferred Stock, the Company’s Common Stock, and the Company’s Public Trust Preferred Securities, an “Eligible Holder”), are eligible to vote to accept or reject the Standby Plan.

There is no Voting Record Date for determining the holders of the Senior Notes and Trust Preferred Securities eligible to participate in the Exchange Offers. The Voting Record Date for Eligible Holders to vote on the Standby Plan is June 19, 2012 (the “Voting Record Date”).

* * * * *

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the securities offered hereby or determined if this Offering Memorandum and Disclosure Statement is truthful or complete. Any representation to the contrary is a criminal offense.

You may tender your Senior Notes and Trust Preferred Securities by transferring the Senior Notes and/or Trust Preferred Securities pursuant to the procedures of the Letter of Transmittal described under “The Exchange Offers– Procedures for Participating in the Exchange Offers”.

You should carefully consider the “Risk Factors” beginning on page 32 of this Offering Memorandum and Disclosure Statement before deciding whether or not to participate in the Exchange Offers and whether or not to vote to accept the Standby Plan.

The Information Agent, Exchange Agent and Voting Agent is:

Kurtzman Carson Consultants LLC (“KCC”)

599 Lexington Avenue, 39th Floor

New York, NY 10022

Telephone: 877-833-4150

Email: CapitolBancorpInfo@kccllc.com

___________________

The definitions of certain terms used throughout this Offering Memorandum and Disclosure Statement may be found by referring to the Section captioned “Certain Definitions” at the end of this Offering Memorandum and Disclosure Statement.

Through the Standby Plan, all Eligible Holders would receive the consideration set forth below under “Standby Plan”, provided that sufficient holders of the Senior Notes, Trust Preferred Securities and the Company’s Series A Preferred Stock (i.e., holders representing at least 66 2/3% in amount and more than 50% in number of those impaired creditors and interest

holders entitled to vote in certain classes who actually vote) vote to accept the Standby Plan and the other conditions to effectiveness of the Standby Plan are satisfied. Only those parties who actually vote to accept or reject the Standby Plan are counted for the purposes of determining whether sufficient holders have voted to accept the Standby Plan, and, therefore, it is important that you vote on the Standby Plan or provide the appropriate instruction to your broker, dealer, commercial bank, trust company, or other nominee (each, a “Nominee”) to cast the appropriate vote on your behalf. Tendering of the Senior Notes and the Trust Preferred Securities in the Exchange Offers will not be deemed to be a vote to accept the Standby Plan. You must vote separately to accept or reject the Standby Plan by casting your vote or providing the appropriate instruction to your Nominee. By voting or providing an instruction to your Nominee to participate in the Exchange Offers or vote to accept or reject the Standby Plan, you are making certain certifications, as contained in the Letter of Transmittal or the Ballots, as applicable, and agreeing to certain provisions contained in the Standby Plan including exculpation, injunction and release provisions. In addition, by voting in favor of the Standby Plan, you acknowledge that the Company may issue additional shares of the Series A Preferred in connection with the Equity Infusion and intends to bulk sale non performing assets and loans at any time prior to the Effective Time or after the Effective Time.

* * * * *

Consummation of the Exchange Offers is subject to, among other things, the conditions (unless waived by the Company and the creditors as described herein) that (i) Eligible Holders tender an aggregate principal amount of 100% of the Senior Notes outstanding on or prior to the Expiration Time and (ii) Eligible Holders tender an amount of at least 90% of the liquidation amount of the Trust Preferred Securities outstanding on or prior to the Expiration Time.

Subject to the applicable laws and the terms set forth in this Offering Memorandum and Disclosure Statement, the Company reserves the right to extend or terminate the Exchange Offers and voting deadlines with respect to the Standby Plan in its sole and absolute discretion, which may be for any or no reason, and otherwise to amend any of the Exchange Offers or the Standby Plan in any respect, other than the conditions to consummate the Exchange Offers and the holders’ right to withdraw. The Company reserves the right to amend or waive any and all conditions to consummate the Exchange Offers.

In making a decision in connection with the out-of-court Exchange Offers and the in-court Standby Plan, holders of the Senior Notes, Trust Preferred Securities, the Company’s Series A Preferred Stock and the Company’s Common Stock must rely on their own examination of the terms of the Exchange Offers and the Standby Plan, including the risks and merits involved. Holders of the Senior Notes, Trust Preferred Securities, the Company’s Series A Preferred Stock and the Company’s Common Stock should not construe the contents of this Offering Memorandum and Disclosure Statement as providing any legal, financial, business or tax advice. Each holder of the Senior Notes, Trust Preferred Securities, the Company’s Series A Preferred Stock and the Company’s Common Stock should consult with its own legal, business, financial and tax advisors with

respect to any such matters concerning this Offering Memorandum and Disclosure Statement, the Exchange Offers and the Standby Plan.

* * * * *

THE EXCHANGE OFFERS

| | | | | | | | | | | |

| | Title of Securities | | Aggregate Liquidation Amount Outstanding | | Liquidation Amount Per Share | | Shares of Series B Preferred Stock Offered Per $10 Liquidation Amount of Trust Preferred Security or $1,000 in Principal Amount Outstanding of Senior Notes* |

| 14064 B 208 | | 8.50% Cumulative Trust Preferred Securities due 2027 issued by Capitol Trust I | | $ | 13,493,980 | | $10 | | 0.001 |

________ | | Cumulative Trust Preferred Securities of Capitol Trust II | | $ | 10,000,000 | | $1,000 | | 0.1 |

| | | Floating Rate Capital Securities of Capitol Statutory Trust III | | | 15,000,000 | | $1,000 | | 0.1 |

139990 AG 0 | | Trust Preferred Securities of Capitol Bancorp Capital Trust 4 | | | 3,000,000 | | $1,000 | | 0.1 |

139990 AE 5 | | Trust Preferred Securities of Capitol Trust VI | | | 10,000,000 | | $1,000 | | 0.1 |

139990 AB 1 | | Trust Preferred Securities of Capitol Trust VII | | | 10,000,000 | | $1,000 | | 0.1 |

1406469 Z 5 | | Floating Rate Capital Securities of Capitol Statutory-Trust VIII | | | 20,000,000 | | $1,000 | | 0.1 |

| | | MMCAPS of Capitol Trust IX | | | 10,000,000 | | $1,000 | | 0.1 |

| 14064 W AA 1 | | Trust Preferred Securities of Capitol Bancorp Trust X | | | 33,000,000 | | $1,000 | | 0.1 |

| | Trust Preferred Securities of Capitol Trust XI | | | 20,000,000 | | $1,000 | | 0.1 |

| 14065 D 203 | | 10.50% Cumulative Trust Preferred Securities issued by Capitol Trust XII | | $ | 6,801,660 | | $10 | | 0.001 |

| | Senior Notes | | $ | 7,000,000 | | $1,000 | | 0.1 |

Under the Exchange Offers, Capitol is offering: (i) 0.001 shares of Series B Preferred for each $10 liquidation amount of Trust Preferred Securities of Capitol Trust I and Capitol Trust XII that Capitol accepts in the Exchange Offers, (ii) 0.1 shares of Series B Preferred for each $1,000 liquidation amount of all other series of Trust Preferred Securities (together with the securities issues by Capitol Trust I and Capitol Trust XII, the “Trust Preferred Securities”) that Capitol accepts in the Exchange Offers and (iii) 0.1 shares of Series B Preferred for each principal amount of $1,000 of the promissory notes issued between May and July of 2008 pursuant to that certain Note Purchase Agreement by and between Capitol and the purchasers set forth therein (the “Senior Notes”), that Capitol accepts in the Exchange Offers. No accrued and unpaid interest owed by Capitol with respect to the Senior Notes or the Trust Preferred Securities will be paid to holders who tender any Senior Notes or Trust Preferred Securities in the Exchange Offer.

THE STANDBY PLAN

The Standby Plan would affect the Company’s stakeholders as set forth below5:

5 All recovery estimates set forth in the tables are based on principal amounts outstanding, exclusive of accrued interest, and are subject to the qualifications set forth herein including the Risk Factors begining on page 32. Allowed Senior Note Claims and Allowed Trust Preferred Security Claims will include each holder’s pro rata share of accrued interest (including,

| Current Instrument | Shares of Class A Common | Shares of Class B Common | Shares of HoldCaps | Shares of New Series A Preferred |

$1,000 in Principal Amount of Senior Note | 33.333 | 16.667 | -0- | -0- |

$1,0000 in Liquidation Amount of Trust Preferred Security | -0- | -0- | 16.524 | -0- |

1 Share of Series A Preferred | 0.6538 | 0.3269 | -0- | -0- |

| 1 Common Share | 0.01218 | 0.0060919 | -0- | -0- |

| · | Holders of the approximately $7 million outstanding in Senior Notes would receive $7 million in Standby Plan value consisting of 1/3 in the form of New Capitol Bancorp Class B Common and 2/3 in the form of New Capitol Bancorp Class A Common, representing an estimated recovery of 100%6; |

| · | Holders of the $151.3 million outstanding in Trust Preferred Securities would receive $50 million7 in Standby Plan value consisting of New Capitol Bancorp Class C Redeemable Common Stock (“HoldCaps Common”)8, representing an estimated recovery of approximately 33%; |

| · | Holders of the $5 million outstanding with respect to the Company’s Series A Preferred Stock would receive $1,000,000 in Standby Plan value consisting of 2/3 in the form of New Capitol Bancorp Class A Common and 1/3 in the form of |

in the case of Senior Notes, any applicable post-petition interest). Accordingly, the recovery estimates set forth below will vary for each holder.

6 There is currently $8.4 million in outstanding principal amount of Senior Notes; however, pursuant to the Company’s pending agreement to sell its equity interests in Bank of Michigan, approximately $1.6 million in principal amount could be discharged if, as expected, the deal is consummated in July of 2012. In the event that the sale does not close prior to consummation of the Exchange Offers or the Effective Date of the Standby Plan, the additional $1.6 million in outstanding principal amount would receive additional shares of New Capitol Bancorp Class A Common and Class B Common, and would reduce the amount of such securities received by the pre-petition common equity accordingly. For purposes of the tables set forth herein, the Company assumes approximately $7 million in Senior Notes will be outstanding as of the Effective Date. The Plan Value and voting power of the New Capitol Bancorp Class A Common Stock to be issued to Holders of Senior Notes and the Company’s Common Stock is in the aggregate approximately 95.65% of the total Plan Value and voting power of the New Capitol Bancorp Class A Common Stock to be issued pursuant to the Plan. The Plan Value and voting power of the New Capitol Bancorp Class B Common Stock to be issued to Holders of Senior Notes and the Company’s Common Stock is in the aggregate approximately 9.44% of the total Plan Value and voting power of the New Capitol Bancorp Class A Common Stock to be issued pursuant to the Plan.

7 The Standby Plan value of the HoldCaps will be $50 million on the Effective Date, based upon the valuation set forth herein. Based on the Projections, and subject to the assumptions therein, if the HoldCaps are redeemed in 2016, the holders would receive approximately $80 million in cash.

New Capitol Bancorp Class B Common, representing an estimated recovery of 20%.

| · | Holders of the Company’s Common Stock would receive $15 million in Standby Plan value consisting of shares, 1/3 in the form of New Capitol Bancorp Class B Common and 2/3 in the form of New Capitol Bancorp Class A Common. |

The following tables set forth the consolidated debt and capitalization of the Company and its consolidated subsidiaries pre-transaction and post-restructuring as anticipated by the Standby Plan, using the assumptions in the footnotes to the tables. All of the capital stock rights (below) will be subject to dilution from any future issuances.

Pre-Transaction Capitalization

$ in millions

| | | Amount Outstanding | |

| | | | |

| Secured | | | |

| Senior Notes | | $ | 7.0 | |

| | | | | |

| Unsecured | | | | |

| Trust Preferred Securities | | | 151.3 | |

Series A Preferred(1) | | | 5.0 | |

| | | | | |

| Total Debt | | $ | 163.3 | |

| | | | | |

| Equity Ownership: | | | | |

| | | | | |

| Existing Common Stock | | | N/A | |

(1) | Denotes amount of current obligations outstanding to holders of the Series A Preferred. |

Post-Restructuring Capitalization

(assumes Equity Infusion of $115m, actual amount may range from $70mm to $115mm)

| | TOTAL NEW STOCK |

| | Voting (%) | Standby Plan Value ($ in thousands) |

| $115mm Equity Infusion (1) | 46.9% | $115,000 |

| $7mm Senior Notes (2) | 14.7% | $7,000 |

| $151.3mm Trust Preferred Securities | 4.9% | $50,000 |

| $5mm Series A Preferred | 2.1% | $1,000 |

| Common Stock | 31.4% | $15,000 |

| TOTAL INTEREST HOLDERS | 100% | $188,000 |

| | Class A Common | | | Class B Common |

| | Voting(%) | Standby Plan Value ($in thousands) | | | Voting (%) | Standby Plan Value ($ in thousands) |

| $115mm Equity Infusion | | | | $115mm Equity Infusion | 46.9% | $70,000 |

| $7mm Senior Notes | 13.1% | $4,666 | | $7mm Senior Notes | 1.5% | $2,333 |

| $151.3mm Trust Preferred Securities | | | | $151.3mm Trust Preferred Securities | | |

| $5mm Series A Preferred | 1.8% | $666 | | $5mm Series A Preferred | 0.43% | $333 |

| Common Stock | 28.08% | $10,000 | | Common Stock | 3.35% | $5,000 |

TOTAL INTEREST HOLDERS | 42.98% | $15,332 | | TOTAL INTEREST HOLDERS | 52.21% | $77,666 |

| | HoldCaps Common | | | Series A Preferred |

| | Voting (%) | Standby Plan Value ($ in thousands) | | | Voting (%) | Standby Plan Value ($ in thousands) |

| $115mm Equity Infusion | | | | $115mm Equity Infusion (1) | 0.0% | $45,000 |

| $7mm Senior Notes | | | | $7mm Senior Notes | | |

| $151.3mm Trust Preferred Securities | 4.9% | $50,000 | | $151.3mm Trust Preferred Securities | | |

| $5mm Series A Preferred | | | | $5mm Series A Preferred | | |

| Common Stock | | | | Common Stock | | |

| TOTAL INTEREST HOLDERS | 4.9% | $50,000 | | TOTAL INTEREST HOLDERS | 0.0% | $45,000 |

| (1) | For purposes of the tables set forth above, the Company assumes a total capital raise of $115 million, $45 million of which will come in the form of the New Capitol Bancorp Series A Preferred. The $45 million in Series A Preferred may be higher or lower due a number of factors, including but not limited to the impact of input from the Company’s primary regulators, investor appetite, the need for capital of the Company’s banking subsidiaries, the price at which the Company may bulk sale non performing assets and other customary contingencies associated with a capital raise. |

| (2) | There is currently $8.4 million in outstanding principal amount of Senior Notes; however, pursuant to the Company’s pending agreement to sell its equity interests in Bank of Michigan, approximately $1.6 million in principal amount could be discharged if, as expected, the deal is consummated in July of 2012. In the event that the sale does not close prior to consummation of the Exchange Offers or the Effective Date of the Standby Plan, the additional $1.6 million in outstanding principal amount would receive additional shares of New Capitol Bancorp Class A Common and Class B Common, and would reduce the amount of such securities received by the pre-petition common equity accordingly. For purposes of the tables set forth herein, the Company assumes approximately $7 million in Senior Notes will be outstanding as of the Effective Date. The Plan Value and voting power of the New Capitol Bancorp Class A Common Stock to be issued to Holders of Senior Notes and the Company’s Common Stock is in the aggregate approximately 95.65% of the total Plan Value and voting power of the New Capitol Bancorp Class A Common Stock to be issued pursuant to the Plan. The Plan Value and voting power of the New Capitol Bancorp Class B Common Stock to be issued to Holders of Senior Notes and the Company’s Common Stock is in the aggregate approximately 9.44% of the total Plan Value and voting power of the New Capitol Bancorp Class A Common Stock to be issued pursuant to the Plan. |

IMPORTANT DATES

Holders of the Senior Notes and/or Trust Preferred Securities should take note of the following important dates in connection with the out-of-court Exchange Offers and the solicitation of votes on the in-court Standby Plan:

| | | | | |

| Date | | Calendar Date and Time | | Event |

| Voting Record Date | | June 19, 2012 | | The date to determine holders entitled to vote to accept or reject the Standby Plan. |

| | | |

Expiration Time and Voting Deadline | | 5:00 p.m., Eastern Daylight time, on July 27, 2012, unless extended as described herein. | | The last day for holders to (i) tender their Senior Notes and Trust Preferred Securities in the Exchange Offers, and (ii) vote to accept or reject the Standby Plan. The Senior Notes and Trust Preferred Securities tendered may not be withdrawn once tendered and the votes to accept or reject the Standby Plan may not be revoked once submitted to the Voting Agent, subject to applicable law or as otherwise specified herein; provided that, if either the Expiration Time or Voting Deadline, as applicable, has been extended past August 10, 2012, holders shall have the right to withdraw their tenders and votes respectively. |

| | | |

| Settlement Date | | Promptly after the date on which the Expiration Time, as may be extended, occurs. | | The Eligible Holders that tender their Senior Notes and Trust Preferred Securities in the Exchange Offers will receive shares of Series B Preferred Stock. |

| | | | | |

REQUESTS FOR ASSISTANCE

If you have any questions or need assistance in connection with the Exchange Offers or the solicitation of votes on the Standby Plan, you may contact Vik Ghei, Misha Zaitzeff or the Company’s President, Cristin Reid.

Vik Ghei: (917) 740-8450

Misha Zaitzeff: (917) 409-8555

Cristin Reid: (517) 487-6555.

We have also engaged Kurtzman Carson Consultants LLC (the “Information Agent” and/or the “Exchange Agent” and/or the “Voting Agent”) at the following address and telephone number:

Kurtzman Carson Consultants LLC (“KCC”)

599 Lexington Avenue, 39th Floor

New York, NY 10022

Telephone: 877-833-4150

Email: CapitolBancorpInfo@kccllc.com

The Company’s legal advisor is Honigman Miller Schwartz and Cohn LLP. They can be contacted at:

Honigman Miller Schwartz and Cohn LLP

Columbia Plaza

350 East Michigan Avenue, Suite 300

Kalamazoo, Michigan 49007-3800

Attn: Phillip D. Torrence, Esq.

Direct: (269) 337-7702

Fax: (269) 337-7703

TABLE OF CONTENTS

Notice to Investors................................................................................................................................................................................................................................iii

Where you can find More Information.............................................................................................................................................................................................v

Cautionary Note regarding forward-looking statements........................................................................................................................................................vii

Offering Memorandum and Disclosure Statement Summary....................................................................................................................................................1

Description of the Series B Preferred..............................................................................................................................................................................................24

Risk Factors..............................................................................................................................................................................................................................................32

Selected Historical Consolidated Financial Data.......................................................................................................................................................................45

Capitalization...........................................................................................................................................................................................................................................47

The Exchange Offers and Solicitation of Votes on the Standby Plan...................................................................................................................................48

Material U.S. Federal Income Tax Consequences of the Exchange Offers...........................................................................................................................56

The Solicitations of Votes on the Standby Plan...........................................................................................................................................................................64

Certain U.S. Federal Income Tax Consequences of the Standby Plan....................................................................................................................................71

The Exchange Agent...............................................................................................................................................................................................................................85

Information Agent..................................................................................................................................................................................................................................85

Securities Law Matters........................................................................................................................................................................................................................86

Overview of Chapter 11.........................................................................................................................................................................................................................88

The Standby Plan....................................................................................................................................................................................................................................90

Projections of Certain Financial Information for the Restructuring Transactions......................................................................................................150

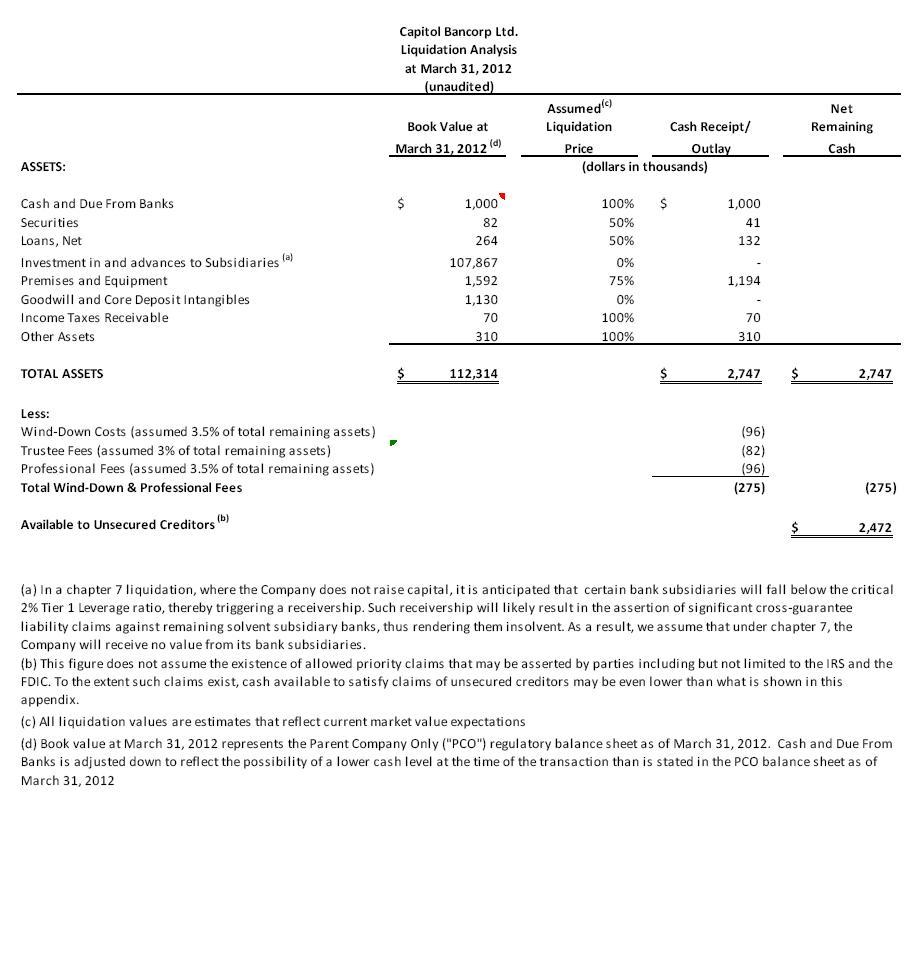

Liquidation Analysis..............................................................................................................................................................................................................................152

Certain Definitions.................................................................................................................................................................................................................................163

| Annex A – | Certificate of Designations of Series B Preferred |

| Annex B – | The Standby Plan |

| Annex C – | Letters of Transmittal |

| Annex D – | Amended and Restated Articles of Incorporation of Capitol Bancorp Ltd. (including Certificate of Designation of Series A Preferred) |

| Annex E – | Amended and Restated Bylaws of Capitol Bancorp Ltd. |

| Annex F – | Amended and Restated Articles of Incorporation of Financial Commerce Corporation |

| Annex G – | Amended and Restated Bylaws of Financial Commerce Corporation |

NOTICE TO INVESTORS

This Offering Memorandum and Disclosure Statement and the Letter of Transmittal and the Ballots contain important information that you should read before making any decision with respect to the out-of court Exchange Offers or solicitation of votes on the in-court Standby Plan.

You should not construe the contents of this Offering Memorandum and Disclosure Statement as investment, legal, business or tax advice. You should consult your counsel, accountant and other advisors as to legal, tax, business, financial and related aspects of any exchange of the Senior Notes or Trust Preferred Securities for the shares of the Company’s Series B Preferred Stock (the “Series B Preferred”) or voting on the Standby Plan. The Company is not making any representation to you regarding the legality of the actions of any holder exchanging the Senior Notes and Trust Preferred Securities for the Series B Preferred under applicable securities laws.

In making an investment decision regarding the Series B Preferred offered by this Offering Memorandum and Disclosure Statement in connection with the Exchange Offers and whether to vote in favor of the Standby Plan, you must rely on your own examination of the Company and the terms of the Exchange Offers and the Standby Plan, including, without limitation, the merits and risks involved. The Exchange Offers and solicitation of votes on the Standby Plan are being made on the basis of this Offering Memorandum and Disclosure Statement.

The Series B Preferred have not been, and will not be, registered under the Securities Act, or any state securities laws and are being offered for exchange only to Eligible Holders, pursuant to an exemption from registration. In tendering your Senior Notes and/or Trust Preferred Securities in the Exchange Offers, you will be required to complete and sign the Letter of Transmittal or if you tender your Trust Preferred through DTC (defined below), you will be deemed to have acknowledged and agreed that you are bound by the terms of the Letter of Transmittal, and thereby confirm the acknowledgments, representations and agreements as set forth in the Letter of Transmittal and this Offering Memorandum and Disclosure Statement under the section “Transfers of Series B Preferred and Securities Laws.”

This Offering Memorandum and Disclosure Statement is being provided on a confidential basis to all holders of Trust Preferred Securities or Senior Notes for purposes of consideration of the exchange of the Senior Notes and the Trust Preferred Securities for the Series B Preferred and soliciting consents to the Standby Plan. The information in this Offering Memorandum and Disclosure Statement is being provided to non-Accredited Investors who hold Senior Notes and/or Private Trust Preferred Securities for disclosure purposes as part of the solicitation of votes on the Standby Plan (and such votes are not being solicited hereby). Holders of Senior Notes and Private Trust Preferred Securities that are non-Accredited Investors are not entitled to vote to accept or reject the Standby Plan and will be deemed to have rejected the Standby Plan to the extent such non-Accredited Investors submit ballots indicating that they are non-Accredited Investors by the Voting Deadline. In addition, by voting in favor of the Standby Plan, Eligible Holders acknowledge that the Company may issue additional shares of the Series A Preferred in connection with the Equity Infusion and

intends to bulk sale non performing assets and loans at any time prior to the Effective Time or after the Effective Time. The use of this Offering Memorandum and Disclosure Statement for any other purpose is not authorized.

This Offering Memorandum and Disclosure Statement may not be copied or reproduced in whole or in part, nor may it be distributed or any of its contents be disclosed to anyone other than the holders of the Senior Notes, Trust Preferred Securities, the Company’s Series A Preferred Stock and the Company’s Common Stock (including their respective attorneys, financial advisors, investment bankers, accountants, and other professionals) without the express prior written consent of the Company.

No representation or warranty, express or implied, is made by the Information Agent, Exchange Agent and Voting Agent as to the accuracy or completeness of any of the information set forth in this Offering Memorandum and Disclosure Statement, and nothing contained in this Offering Memorandum and Disclosure Statement is or shall be relied upon as a promise or representation by the Information Agent, Exchange Agent or Voting Agent, whether as to the past or the future.

This Offering Memorandum and Disclosure Statement contains summaries, believed to be accurate, of some of the terms of specific documents, but reference is made to the actual documents, copies of which will be attached hereto and made available upon request in other cases, for the complete information contained in those documents.

No person is authorized in connection with the Exchange Offers or the solicitation of votes on the Standby Plan to give any information or to make any representation not contained in this Offering Memorandum and Disclosure Statement, the Letter of Transmittal, the Standby Plan and the Ballots and, if given or made, any other information or representation must not be relied upon as having been authorized by the Company. The information contained in this Offering Memorandum and Disclosure Statement is as of the date hereof and subject to change, completion or amendment without notice. Neither the delivery of this Offering Memorandum and Disclosure Statement at any time nor any exchange hereunder shall, under any circumstances, create any implication that there has been no change in the information set forth in this Offering Memorandum and Disclosure Statement or in the affairs of the Company since the date of this Offering Memorandum and Disclosure Statement.

Subject to the applicable laws and the terms set forth in this Offering Memorandum and Disclosure Statement, the Company reserves the right to extend or terminate the Exchange Offers and voting deadlines with respect to the Standby Plan in its sole and absolute discretion, which may be for any or no reason, and otherwise to amend the Exchange Offers or the Standby Plan in any respect other than the conditions to consummate the Exchange Offers and the holders’ rights to withdraw. The Company also reserves the right to reject any tender of Senior Notes or Trust Preferred Securities in whole or in part tendered by any holder. The Company reserves the right to amend or waive any and all conditions to consummate the Exchange Offers.

You should rely only on the information contained in this Offering Memorandum and Disclosure Statement or to which the Company has referred you. The Company has not authorized anyone to provide you with information that is different than as set forth

herein or therein. This Offering Memorandum and Disclosure Statement may only be used where it is legal to offer the Series B Preferred. You should not assume that the information in this Offering Memorandum and Disclosure Statement is accurate as of any date other than the date of this Offering Memorandum and Disclosure Statement, or that the information incorporated by reference into this Offering Memorandum and Disclosure Statement is accurate as of any date other than the date of such information.

BECAUSE THE CHAPTER 11 CASES HAVE NOT BEEN FILED, THE ADEQUACY OF THE DISCLOSURE IN THIS OFFERING MEMORANDUM AND DISCLOSURE STATEMENT CONCERNING THE STANDBY PLAN HAS NOT BEEN APPROVED BY THE COURT. IF THE CHAPTER 11 CASES ARE SUBSEQUENTLY COMMENCED, THE COMPANY WILL SEEK AN ORDER OF THE COURT THAT THE SOLICITATION OF VOTES ON THE STANDBY PLAN WAS IN COMPLIANCE WITH SECTION 1126(b) OF THE BANKRUPTCY CODE.

ANY ESTIMATES OF CLAIMS SET FORTH IN THIS OFFERING MEMORANDUM AND DISCLOSURE STATEMENT MAY VARY FROM THE FINAL AMOUNTS OF CLAIMS ALLOWED BY THE COURT.

ONCE MADE, VOTES TO ACCEPT OR REJECT THE STANDBY PLAN MAY NOT BE REVOKED BEFORE THE FILING OF THE CHAPTER 11 CASES, EXCEPT AS REQUIRED BY LAW OR AS OTHERWISE SPECIFIED HEREIN; PROVIDED THAT, IF THE VOTING DEADLINE HAS BEEN EXTENDED PAST JULY 27, 2012, HOLDERS SHALL HAVE THE RIGHT TO WITHDRAW THEIR VOTES. IF THE OUT-OF-COURT EXCHANGE OFFERS ARE SUCCESSFUL, THE VOTES TO ACCEPT OR REJECT THE STANDBY PLAN WILL BE OF NO EFFECT. IF THE CHAPTER 11 CASES HAVE BEEN COMMENCED, REVOCATIONS OF ACCEPTANCES OR REJECTIONS MAY BE EFFECTED ONLY WITH THE APPROVAL OF THE COURT OR AS OTHERWISE SPECIFIED HEREIN.

WHERE YOU CAN FIND MORE INFORMATION

Capitol files annual, quarterly and current reports, proxy statements and other information with the SEC. You may read and copy any document Capitol files with the SEC at the SEC’s public reference room at 100 F Street, N.E., Washington, D.C. 20549. You can also request copies of the documents, upon payment of a duplicating fee, by writing the Public Reference Section of the SEC. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room. These SEC filings are also available to the public from the SEC’s web site at http://www.sec.gov.

None of the information on the Company’s website is incorporated by reference herein or otherwise deemed to be a part of this Offering Memorandum and Disclosure Statement. Any references to the Company’s website are for informational purposes only.

In this Offering Memorandum and Disclosure Statement, the Company “incorporates by reference” certain information that the Company files with the SEC, which means that the Company can disclose important information to you by referring to that information. The information incorporated by reference is considered to be a part of this Offering Memorandum and Disclosure Statement, and later information filed with the SEC that is incorporated by reference will update and supersede such information. The Company incorporates by reference the following documents which the Company has filed with the SEC under the Securities Exchange Act of 1934 (the “Exchange Act”):

| 1. | The Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2011, filed with the SEC on March 30, 2012; |

| 2. | The Company’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2012, filed with the SEC on May 3, 2012; and |

| 3. | The Company’s Current Reports on Form 8-K filed on June 7, 2012, May 3, 2012, May 1, 2012, March 29, 2012 and January 20, 2012. |

The Company also incorporates by reference reports filed with the SEC under Sections 13(c), 14 or 15(d) of the Exchange Act after the date of this Offering Memorandum and Disclosure Statement (other than the portion of such reports filed pursuant to Item 2.02 or Item 7.01 of Form 8-K or other information “furnished” to the SEC).

You may request a copy of any of such filings, other than an exhibit to a filing unless that exhibit is specifically incorporated by reference into that filing, at no cost, by telephoning Vik Ghei at (917) 740-8450, Misha Zaitzeff at (917) 409-8555 or writing Capitol at the following address:

Capitol Bancorp Ltd.

Capitol Bancorp Center

200 Washington Square North, Fourth Floor

Lansing, Michigan 48933

Attention: Investor Relations

Telephone: 517-487-6555

Internet website: www.capitolbancorp.com

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this Offering Memorandum and Disclosure Statement, as well as certain statements incorporated by reference herein, may constitute “forward-looking statements.” You may find discussions containing such forward-looking statements within this Offering Memorandum and Disclosure Statement generally. In addition, when used in this Offering Memorandum and Disclosure Statement, the words “believes,” “anticipates,” “expects,” “estimates,” “plans,” “projects,” “intends” and similar expressions are intended to identify forward-looking statements. These forward-looking statements include statements other than historical information or statements of current condition, but instead represent only the Company’s belief regarding future events, many of which, by their nature, are inherently uncertain and outside of the Company’s control. It is possible that the actual results may differ, possibly materially, from the anticipated results indicated in these forward-looking statements, which speak only as of the date made. Important factors that could cause actual results to differ from those in the Company’s specific forward-looking statements include, but are not limited to, those discussed under “Risk Factors,” general business and economic conditions, other risk factors described in the Company’s reports filed from time to time with the SEC, as well as:

| · | the Company may not be able to successfully restructure its existing unsecured debt obligations through the Exchange Offers or the Standby Plan; |

| · | changes in the economic conditions in which the Company operates negatively impacting the Company’s financial resources; |

| · | certain of the Company’s competitors having greater financial resources than the Company; |

| · | Capitol’s ability to continue as a going concern; |

| · | The possibility of the Federal Deposit Insurance Corporation assessing Capitol’s banking subsidiaries for any cross-guaranty liability or otherwise resulting in the FDIC seizing such banks; |

| · | Capitol’s compliance with the terms of its written agreement with the Federal Reserve Bank, amendments thereto or subsequent regulatory agreements; |

| · | the risk that the realization of deferred tax assets may not occur; |

| · | the risk that Capitol could have an “ownership change” under Section 382 of the Internal Revenue Code, which could impair its ability to timely and fully utilize its net operating losses for tax purposes and so-called built-in losses that may exist if such an “ownership change” occurs; |

| · | the Company is dependent on external financing to Capitol or banks; |

| · | the Company may be unable to retain key management personnel; |

| · | the Company’s common stock price may be volatile; and |

| · | other matters discussed in this Offering Memorandum and Disclosure Statement generally. |

Consequently, readers of this Offering Memorandum and Disclosure Statement should consider forward-looking statements only as current plans, estimates and beliefs, and the Company cautions you against relying on such forward-looking statements. The Company does not undertake and specifically declines any obligation to publicly release the results of any revisions to these forward-looking statements that may be made to reflect future events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events. The Company undertakes no obligation to update or revise any forward-looking statement in this Offering Memorandum and Disclosure Statement to reflect any new events or any change in conditions or circumstances. All of the forward-looking statements in this Offering Memorandum and Disclosure Statement are expressly qualified by these cautionary statements. Even if these plans, estimates or beliefs change because of future events or circumstances after the date of these statements, or because anticipated or unanticipated events occur, the Company disclaims any obligation to update these forward-looking statements.

OFFERING MEMORANDUM AND DISCLOSURE STATEMENT SUMMARY

This summary highlights the information contained elsewhere in this Offering Memorandum and Disclosure Statement. This summary should be read in conjunction with, and is qualified in its entirety by, the more detailed information and financial statements (including the accompanying notes) appearing elsewhere, or incorporated by reference, in this Offering Memorandum and Disclosure Statement. When referring to the Standby Plan, this summary and this Offering Memorandum and Disclosure Statement should be read in conjunction with, and are qualified in their entirety by, the Standby Plan. You should read this entire Offering Memorandum and Disclosure Statement carefully, including “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements” and the financial statements and related notes contained herein before making a decision with respect to the Exchange Offers and the solicitation of votes on the Standby Plan.

You should also read the reports incorporated by reference herein, which are an important part of this Offering Memorandum and Disclosure Statement, before you make a decision with respect to the Exchange Offers and the solicitation of votes on the Standby Plan.

Unless otherwise noted or the context otherwise requires, the term “GAAP” refers to Generally Accepted Accounting Principles in the United States.

ABOUT CAPITOL

Capitol is a community banking company, with a current network of individual banks and bank operations in 10 states and total consolidated assets which approximated $2.0 billion as of May 31, 2012. Capitol is registered as a bank holding company under the Bank Holding Company Act of 1956, as amended, with principal executive offices located at the Capitol Bancorp Center, 200 Washington Square North, Fourth Floor, Lansing, Michigan 48933. Capitol’s telephone number is 517-487-6555.

Capitol’s operating strategy is to provide transactional, processing and administrative support and mentoring to aid in the effective operation and development of its banks. It provides access to support services and management with significant experience in community banking. These administrative and operational support services do not require a direct interface with the bank customer and therefore can be consolidated more efficiently without affecting the bank customer relationship.

Economic conditions throughout the United States, and in the regions in which Capitol and its banking operations are located, have deteriorated to an extent not experienced since the “Great Depression” of the 1930s. Capitol’s operations are focused on community banking and helping small, local businesses meet their financial needs, primarily through making loans to those businesses and their owners, funded by locally-gathered deposits. A substantial portion of those loans are secured by commercial real estate property, as part of the overall collateral to support those individual loans. In this adverse economic environment, small businesses and their owners have suffered significant financial hardships, which preclude repaying loans in accordance with their terms. In addition, recent economic factors have resulted in a variety of stresses impacting depositors and the availability of deposits to fund lending activities. Further, and more importantly, the underlying values of the real estate collateral have plummeted in this

sustained adverse environment, resulting in massive loan losses and dramatic growth in levels of nonperforming assets not seen previously in the banking industry in general and, in particular, at Capitol. Prospects of economic recovery are uncertain, unpredictable and subject to variables completely outside the control or influence of financial institutions, including Capitol.

THE RESTRUCTURING AND RECAPITALIZATION TRANSACTIONS

Overview

The Company is pursuing a comprehensive financial restructuring of certain of its outstanding indebtedness (collectively, the “Restructuring Transactions”) and simultaneously raising capital from outside investors through two alternative concurrent mechanisms: (1) an out-of-court restructuring, which includes the Exchange Offers, and (2) if conditions to completion of the out-of court restructuring are not satisfied or waived, an in-court chapter 11 bankruptcy reorganization, which includes soliciting votes on the Standby Plan.

In connection with the transactions contemplated by the Exchange Offers, all holders of Trust Preferred Securities or Senior Notes may elect to either (i) tender your Senior Notes and/or Trust Preferred Securities in the Exchange Offers or (ii) take no action with respect to the Exchange Offers, in which case such holders will have rejected the Exchange Offers. In connection with the Standby Plan, all holders of the Company’s Series A Preferred Stock, all holders of the Company’s Common Stock, all holders of the Company’s Public Trust Preferred Securities, and Accredited Investors who hold the Senior Notes and/or the Private Trust Preferred Securities may elect on the Ballots to either (x) vote to accept or reject the Standby Plan, with or without tendering your Senior Notes or Trust Preferred Securities or (y) take no action with respect to the Standby Plan, in which case such Accredited Investors will have no bearing on the approval of the Standby Plan. Holders of Senior Notes or Private Trust Preferred Securities who are non-Accredited Investors are not entitled to vote on the Standby Plan and will be deemed to have rejected the Standby Plan to the extent such non-Accredited Investors submit ballots indicating that they are non-Accredited Investors prior to the Voting Deadline. If you wish to and are eligible to tender your Senior Notes and/or Trust Preferred Securities and vote to accept the Standby Plan, you need to complete both of these actions in clauses (i) and (x) above.

Subject to the applicable laws and the terms set forth in this Offering Memorandum and Disclosure Statement, the Company reserves the right to extend or terminate the Exchange Offers and voting deadlines with respect to the Standby Plan in its sole and absolute discretion, which may be for any or no reason, and otherwise to amend the Exchange Offers or the Standby Plan in any respect, other than the conditions to consummate the Exchange Offers and the holders’ rights to withdraw. The Company also reserves the right to reject any tender of Senior Notes or Trust Preferred Securities in whole or in part tendered by any holder. The Company reserves the right to amend or waive any and all conditions to consummate the Exchange Offers.

For a more detailed discussion of the Exchange Offers and the solicitation of votes on the Standby Plan, see “The Exchange Offers and Solicitations of Votes on the Standby Plan” and “The Standby Plan”. The description of the Series B Preferred is summarized in “—Description of the Series B Preferred.”

As further described below, many of Capitol’s subsidiary banks have experienced significant capital erosion resulting from the general economic downturn of the past few years. In fact, a number of Capitol’s subsidiary banks are dangerously close to failing to meet the minimum capital ratios necessary to avoid seizure of the banks by the FDIC. The FDIC is legally required to seize banks that fall below certain thresholds. Moreover, the failure of even one of Capitol’s subsidiary banks endangers Capitol and its other subsidiary banks as a result of the FDIC’s ability to assert “cross-guaranty liability” against such banks in order to recover any losses experienced by the FDIC in a bank seizure. Such a bank seizure and liability assessment would virtually destroy any value held by Capitol’s current stakeholders. These dire circumstances have made it necessary for Capitol to take extraordinary measures to restructure and recapitalize in order to preserve value for its stakeholders.

These circumstances have arisen as Capitol has incurred significant losses from operations in periods since 2007. In addition, Capitol has experienced significant increases in nonperforming loans, foreclosed real estate, loan losses and other materially adverse circumstances including, but not limited to, a very material erosion of its common equity and related regulatory capital levels, resulting in Capitol becoming classified as less than adequately-capitalized from a regulatory perspective. In 2009, Capitol entered into a written agreement with the Federal Reserve Bank of Chicago (its primary federal regulator) (the “Reserve Bank”) which requires Capitol to improve operating results and its overall condition, in addition to refraining from a number of activities without prior written consent from that Federal Reserve Bank. The current less than adequately-capitalized classification of Capitol exposes it to increased regulatory scrutiny and enforcement action and other materially adverse consequences.

Like a large number of financial institutions across the United States, Capitol has been materially impacted by adverse economic conditions. As a result of this economic downturn and depressed real estate markets, Capitol’s banking subsidiaries have experienced a decline in the performance of loans, particularly real estate construction and development loans, which has resulted in Capitol incurring a net loss of $195.2 million for the year ended December 31, 2009, a net loss of $225.2 million for the year ended December 31, 2010, a net loss of $45.5 million for the year ended December 31, 2011 and a net loss of $7.9 million for the three months ended March 31, 2012. If Capitol’s banking subsidiaries continue to experience adverse performance in the consolidated loan portfolio, large loan losses and losses associated with foreclosed real estate and, as a result, Capitol continues incurring net losses, some or all of Capitol’s banking subsidiaries may be unable to meet or maintain adequate regulatory capital ratios unless Capitol raises additional capital. Furthermore, during this adverse economic environment, analysts and others have focused on additional measures of a financial institution’s capital position, such as tangible common equity to tangible assets and regulatory “Tier 1” capital as a percentage of risk-weighted assets, to assess the financial health and stability of the institution, which also tends to impact an institution’s stock price.

Over the past four years, the American banking and financial system has been shaken and many banks across the country have struggled to survive in the face of a declining economy. A number of these banks are confronting enormous pressure due to reduced capital, the imposition of regulatory sanctions and orders, and possible defaults under existing credit agreements. If

these pressures are not alleviated, receivership is a near certainty for many of these institutions. The Standby Plan described in this Offering Memorandum and Disclosure Statement is a product of this very difficult operating environment.

In September 2009, Capitol and its second-tier bank holding companies entered into an agreement with the Reserve Bank under which Capitol agreed to refrain from the following actions without the prior written consent of the Reserve Bank: (i) declare or pay dividends; (ii) receive dividends or any other form of payment representing a reduction in capital from Michigan Commerce Bank, or from any of its subsidiary institutions that are subject to any restriction by the institution’s federal or state regulator that limits the payment of dividends or other intercorporate payments; (iii) make any distributions of interest, principal, or other sums on subordinated debentures or Trust Preferred securities; (iv) incur, increase or guarantee any debt; or (v) purchase or redeem any shares of the stock of Capitol, the second-tier bank holding companies, nonbank subsidiaries or any of the subsidiary banks that are held by shareholders other than Capitol.

Many of Capitol’s bank subsidiaries have entered into formal agreements (as well as informal agreements) with their applicable regulatory agencies. Those agreements provide for certain restrictions and other guidelines and/or limitations to be followed by the banks.

The FDIC may issue Prompt Corrective Action Notifications (“PCAN”) to banking subsidiaries falling below the “adequately-capitalized” regulatory-capital classification, and subsequently may issue Prompt Correction Action Directives (“PCAD”). PCADs may be issued when a bank, which has previously received a PCAN, has submitted two consecutive capital restoration plans which have been rejected by the FDIC.

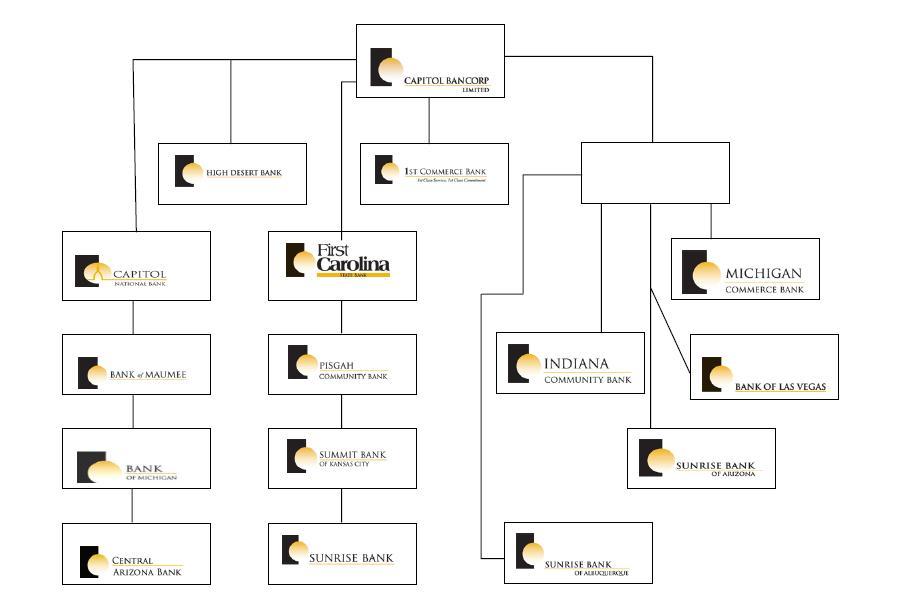

Capitol’s banking subsidiaries which have received a PCAD are as follows as of March 2012 (listed in descending order based on total assets): Michigan Commerce Bank, Bank of Las Vegas, Sunrise Bank of Arizona, Sunrise Bank, First Carolina State Bank, Central Arizona Bank, Sunrise Bank of Albuquerque, 1st Commerce Bank and Pisgah Community Bank. These banks are striving to develop and implement capital restoration plans which may be acceptable to the FDIC. Under the PCAD’s, each subsidiary bank is required to increase its Tier 1 Leverage Ratio9 to not less than eight (8) percent and its Total Risk-Based Capital Ratio10 to not less than twelve (12) percent.

In addition to the above, the FDIC gave notice to many of Capitol’s banking subsidiaries in December 2009 that, to mitigate the effects of any possible assessment arising from potential cross-guaranty liability, they should be encouraged to arrange a sale, merger or recapitalization such that Capitol no longer controls the banking subsidiary. The FDIC’s encouragement is

9 As used in this Offering Memorandum and Disclosure Statement, the term “Tier 1 Leverage Ratio” means the ratio of Tier 1 capital to average total assets, as calculated in accordance with the appropriate banking agency’s capital regulations.

10 As used in this Offering Memorandum and Disclosure Statement, the term “Total Risk-Based Capital Ratio” means the ratio of qualifying total capital to risk-weighted assets, as calculated in accordance with the appropriate banking agency’s capital regulations.

consistent with Capitol’s previously-announced plans to selectively divest of some of its banking subsidiaries in conjunction with reallocating capital resources to the remaining banking subsidiaries.

Capitol’s insured depository institution subsidiaries are also subject to cross-guaranty liability under federal law. This means that if one FDIC-insured depository institution subsidiary of a multi-institution bank holding company fails or requires FDIC assistance, the FDIC may assess “commonly controlled” depository institutions for the estimated losses suffered by the FDIC. Such liability could have a material adverse effect on the financial condition of any assessed subsidiary institution and on Capitol as the common parent.

If any of Capitol’s subsidiary banks’ Tier 1 Leverage Ratio were to fall below two percent (2%), the FDIC would be required within ninety (90) days to appoint a receiver or conservator for such bank, or take such other action as it deemed appropriate. If even a single subsidiary bank were to be seized by the FDIC, it is likely that the FDIC would assert cross guarantee claims against the Company’s solvent subsidiary banks, thereby crippling these subsidiary banks as well. As illustrated below, a number of Capitol’s subsidiary banks are dangerously close to falling beneath the fatal 2% ratio. In addition, pursuant to the agreements, no banking subsidiary of Capitol may pay dividends to Capitol. Since Capitol’s subsidiary banks constitute substantially all of Capitol’s consolidated assets, the restrictions under the regulatory agreements mean that Capitol’s financial health is directly (and virtually solely) dependent upon the financial health of Capitol’s banking subsidiaries.

The following comparative analysis summarizes each bank’s regulatory capital position as of the dates indicated based on the banks included in Capitol’s consolidation as of March 31, 2012:

| | | Tier 1 Leverage | | | Tier 1 Risk-Based | | | Total Risk-Based | | | |

| | | Ratio(2) | | | Capital Ratio(2) | | | Capital Ratio(2) | | | Regulatory Classification(1) |

| | | Mar 31, 2012 | | | Dec 31, 2011 | | | Mar 31, 2012 | | | Dec 31, 2011 | | | Mar 31, 2012 | | | Dec 31, 2011 | | | Mar 31, 2012 | | Dec 31, 2011 | |

| Arizona Region: | | | | | | | | | | | | | | | | | | | | | | | |

| Central Arizona Bank | | | 2.07 | % | | | 2.01 | % | | | 2.63 | % | | | 2.65 | % | | | 3.93 | % | | | 3.95 | % | | significantly-undercapitalized | | significantly-undercapitalized | |

| Sunrise Bank of Albuquerque | | | 2.11 | % | | | 2.43 | % | | | 2.79 | % | | | 3.22 | % | | | 4.09 | % | | | 4.50 | % | | significantly-undercapitalized | | significantly-undercapitalized | |

| Sunrise Bank of Arizona | | | 2.00 | % | | | 2.03 | % | | | 2.56 | % | | | 2.56 | % | | | 3.84 | % | | | 3.85 | % | | significantly-undercapitalized | | significantly-undercapitalized | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Great Lakes Region: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Bank of Maumee | | | 5.02 | % | | | 5.41 | % | | | 7.71 | % | | | 7.56 | % | | | 9.00 | % | | | 8.85 | % | | adequately-capitalized | | adequately-capitalized | |

| Bank of Michigan | | | 8.25 | % | | | 8.80 | % | | | 10.59 | % | | | 11.31 | % | | | 11.86 | % | | | 12.58 | % | | well-capitalized | | well-capitalized | |

| Capitol National Bank | | | 6.90 | % | | | 6.90 | % | | | 9.48 | % | | | 9.15 | % | | | 10.75 | % | | | 10.42 | % | | adequately-capitalized(3) | | adequately-capitalized(3) | |

| Indiana Community Bank | | | 6.91 | % | | | 6.66 | % | | | 9.55 | % | | | 9.35 | % | | | 10.83 | % | | | 10.63 | % | | adequately-capitalized(3) | | adequately-capitalized(3) | |

| Michigan Commerce Bank | | | 2.34 | % | | | 2.17 | % | | | 3.00 | % | | | 2.84 | % | | | 4.32 | % | | | 4.16 | % | | significantly-undercapitalized | | significantly-undercapitalized | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Nevada Region: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

1st Commerce Bank | | | 2.61 | % | | | 2.30 | % | | | 3.73 | % | | | 3.88 | % | | | 5.07 | % | | | 5.22 | % | | significantly-undercapitalized | | significantly-undercapitalized | |

| Bank of Las Vegas | | | 2.03 | % | | | 2.16 | % | | | 2.65 | % | | | 2.90 | % | | | 3.95 | % | | | 4.20 | % | | significantly-undercapitalized | | significantly-undercapitalized | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Northwest Region: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| High Desert Bank | | | 5.63 | % | | | 6.47 | % | | | 7.72 | % | | | 8.72 | % | | | 9.01 | % | | | 10.00 | % | | adequately-capitalized | | adequately-capitalized(3) | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Southeast Region: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

First Carolina State Bank | | | 2.06 | % | | | 2.08 | % | | | 3.14 | % | | | 3.09 | % | | | 4.47 | % | | | 4.41 | % | | significantly-undercapitalized | | significantly-undercapitalized | |

| Pisgah Community Bank | | | 2.20 | % | | | 2.09 | % | | | 3.20 | % | | | 2.93 | % | | | 4.56 | % | | | 4.28 | % | | significantly-undercapitalized | | significantly-undercapitalized | |

| Sunrise Bank | | | 2.10 | % | | | 2.16 | % | | | 2.92 | % | | | 2.97 | % | | | 4.24 | % | | | 4.29 | % | | significantly-undercapitalized | | significantly-undercapitalized | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Consolidated totals | | | (5.74 | )% | | | (4.73 | )% | | | (7.62 | )% | | | (6.36 | )% | | | (7.62 | )% | | | (6.36 | )% | | less than adequately-capitalized | | less than adequately-capitalized | |

(1) | Regulatory capital classifications are defined as follows: Well-Capitalized – Total risk-based capital ratio must be 10% or more, and Tier 1 risk-based capital ratio must be 6% or more, and Tier 1 leverage ratio must be 5% or more, and the bank must not be subject to formal regulatory enforcement action requiring non-standard capital ratios. Adequately-Capitalized – Does not meet the criteria for “well-capitalized,” but has total risk-based capital ratio of 8% or more, and Tier 1 risk-based capital ratio of 4% or more, and Tier 1 leverage ratio of 4% or more. Undercapitalized – Does not meet the criteria for “adequately-capitalized,” but has total risk-based capital ratio of 6% or more, and Tier 1 risk-based capital ratio of 3% or more, and Tier 1 leverage ratio of 3% or more. Significantly-Undercapitalized – Does not meet the criteria for “undercapitalized,” but has Tier 1 leverage ratio of 2% or more. Institutions with a Tier 1 leverage ratio below 2% are classified as “critically-undercapitalized.” | | |

(2) | Ratios are based on the banks’ regulatory reports filed on or before April 30, 2012. | | |

(3) | Institution is subject to a regulatory agreement and, accordingly, cannot be classified better than “adequately-capitalized” even though the risk-based capital ratios would otherwise suggest “well-capitalized” classification. | | |

In today’s environment, financial institutions like Capitol and its banking subsidiaries, all of which are operating under regulatory orders, must raise capital or face liquidation. During the past thirty-six (36) months, Capitol has, to no avail, pursued various capital raising alternatives. As a result of the significant losses and reductions of capital which Capitol and Capitol’s banks have experienced over the past three years, combined with the restrictions imposed upon Capitol and its banks by their regulators, unless the Exchange Offers are successful, Capitol must look to the chapter 11 bankruptcy process to restructure its debt obligations and thereby facilitate the raising of needed capital for Capitol’s banks.

This Offering Memorandum and Disclosure Statement describes the Standby Plan that Capitol’s creditors and equity security holders are being asked to approve before Capitol formally commences the Chapter 11 Cases. In sum, Capitol intends to restructure its obligations in order to secure its long term financial viability which, absent restructuring, is in peril.

Simultaneously, but subject to and conditioned upon approval and consummation of the Exchange Offers and the Standby Plan, Capitol is in the process of raising a gross amount of at least $70 million in through the sale of shares of Capitol Class B Common Stock. These additional funds will be used to make the distributions contemplated under the Standby Plan, pay the costs and expenses associated with the Chapter 11 Cases and the transactions related to the recapitalization, support the Debtors’ ongoing working capital needs and contribute the urgently needed capital to Capitol and its subsidiary banks.

It is important at the outset to emphasize the limited dimensions of this process:

| · | No banking subsidiary of Capitol nor its depositors will be affected in any way. Each subsidiary bank of Capitol continues to operate and its customers’ deposits remain insured up to the applicable limits by the FDIC. Banks themselves cannot file for reorganization, but bank holding companies — and Capitol and FCC are |

holding companies, not banks — can use the reorganization process under federal law.

| · | If Capitol’s creditors approve the Standby Plan, the court-supervised reorganization should move forward very quickly. A prepackaged plan shortens and simplifies the bankruptcy process. It can be very efficient and effective. |

| · | All of Capitol’s general unsecured creditors will be paid in full. |

Exceptional times call for exceptional and innovative solutions to preserve value. That is why this Offering Memorandum and Disclosure Statement and the accompanying Standby Plan are important to Capitol’s creditors and stakeholders and to the banking industry generally.