August 2, 2007

Second-Quarter 2007 Results and

Full-Year 2007 Financial Outlook

Exhibit 99.2

Agenda

Company Overview and Business Plan

Bob Rossiter, Chairman and CEO

Second-Quarter 2007 Results and 2007 Outlook

Jim Vandenberghe, Vice Chairman and CFO

Q and A Session

2

Company Overview

and Business Plan

3

What Does the Shareholder Vote

Against the AREP Merger Proposal Mean?*

Lear’s shareholders have voted, and we respect their decision

At the time of the Merger Proposal, we had a clear strategy

and business plan for the future

Nevertheless, the Board was obligated to evaluate the AREP

offer and make a recommendation

Following a comprehensive and objective review, the Board

concluded the AREP offer was fair

While we believed there were benefits to the transaction, we

also believe a standalone, publicly traded Lear has a positive

long-term outlook

The Board and management team are focused on executing

the strategic plan we have in place

We Will Operate The Company Going Forward With The

Same Level Of Intensity And Commitment To Customer

Satisfaction And Shareholder Value We Have Always Had

*

Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

4

Following the Offer,

Near-Term Factors Turned More Positive*

Investor Sentiment Regarding The Auto Sector

Improved In The First Half Of 2007

*

Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

5

Auto sector valuations increased significantly

Big Three production in the first half was relatively stable

and somewhat stronger than we had forecast

Distress in the supply chain has moderated somewhat

There were no labor disruptions in the auto sector, and

there is optimism regarding the outcome of this year’s

union contract negotiations

Lear’s second-quarter operating results and full-year 2007

outlook improved

Business Assessment*

*

Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

6

Near-Term Business Conditions Relatively Stable

Continuing priority focus on quality and business

fundamentals

Seating business performing well globally

Electrical and Electronic business needs further

improvement

Further Industry Restructuring and Volatility Expected

Substantial progress on global restructuring initiative

Continuing to diversify our sales with rapid growth in

total Asian sales

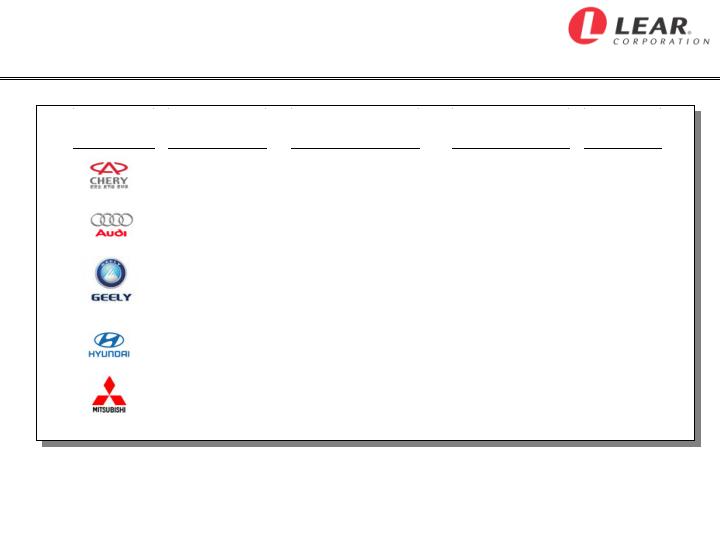

New Asian Program Awards in Second Quarter

New Asian Business Awarded In Second Quarter

Worth About $100 Million Annually *

* Includes consolidated and non-consolidated sales.

** Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

Automaker

Market

Lear Content

Vehicle

Program(s)

SOP**

China

Seats

B13 CV

Jun-08

China

Seats

A4

Nov-08

China

Seats

FC2/3

Apr-08

China

Wire Harness/Junction Box/TPMS

FC2/3

Jun-08

North America

Junction Box

Sonata/Santa Fe

Feb-08

Australia

Tier II Seat Components

380

Apr-07

7

Going Forward,

What is Lear’s Business Plan?*

Product-Line Focus

Operating Priorities

Continue to execute the customer-focused business plan we

have in place:

* Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

8

Focus on strengthening our core businesses:

Leverage leadership position in Seating systems

Strengthen capabilities in Electrical and Electronic segment

Expand capabilities in value-added components

Deliver world-class quality and customer satisfaction

Implement global restructuring and footprint actions

Aggressively pursue growth in Asia and with Asian OEMs globally

Continue product innovation with focus on safety and technology

Second-Quarter Results

and 2007 Outlook

9

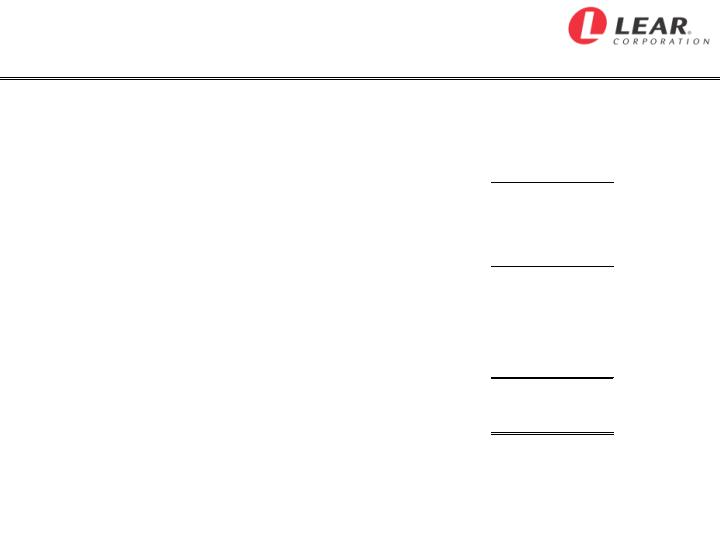

Financial Summary*

* Core operating earnings represent seating and electrical and electronic income before interest, other expense, income taxes, restructuring costs and

other special items. Free cash flow represents net cash provided by operating activities before the net change in sold accounts receivable, less capital

expenditures. Please see slides titled “Non-GAAP Financial Information” and “Forward Looking Statements” at the end of this presentation for further

information.

10

Second-Quarter special items include:

Costs related to restructuring actions

Costs related to AREP merger transaction

Costs related to divestiture of Interior business

Second-Quarter core operating earnings were $229 million,

up $65 million from a year ago, reflecting:

Favorable cost performance and operating efficiencies

Improved operating performance in Europe and Asia

Benefit of new business, mainly Seating outside of North America

Full-Year outlook unchanged from latest status, but we now expect

earnings at or near the high end of the range:

Core operating earnings range remains at $600 to $640 million

Operating performance positive; production outlook uncertain

Free cash flow increased to $275 million, reflecting lower capital

spending

Second Quarter 2007

Industry Environment

Second Quarter

Second Quarter

2007

2007 vs. 2006

North American Production

Industry

4.0 mil

Down 2%

Big Three

2.7 mil

Down 7%

Lear's Top 15 Platforms

1.3 mil

Down 6%

European Production

Industry

5.2 mil

Up 1%

Up 1%

Lear's Top 5 Customers

2.6 mil

Up 1%

Key Commodities (Quarterly Average)

vs. Prior Quarter

Steel (Hot Rolled)

Up 5%

Down 6%

Crude Oil

Up 11%

Down 8%

Copper

Up 28%

Up 11%

11

Second Quarter 2007

Reported Financial Results

(in millions, except net income per share)

Second

Quarter 2007

Second

Quarter 2006

2Q '07

B/(W) 2Q '06

Net Sales

$4,155.3

$4,810.2

($654.9)

Income Before Interest, Other Expense and

Income Taxes*

$194.8

$113.2

$81.6

Pretax Income

$143.9

$31.5

$112.4

Net Income (Loss)

$123.6

($6.4)

$130.0

Net Income (Loss) Per Share

$1.58

($0.10)

$1.68

SG&A % of Net Sales

3.4

%

3.6

%

0.2

pts.

Interest Expense

$51.3

$53.2

$1.9

Depreciation / Amortization

$75.7

$103.5

$27.8

Other Expense, Net

$0.3

$25.6

$25.3

* Please see slides titled “Non-GAAP Financial Information” at the end of this presentation for further information.

12

Second Quarter 2007

Restructuring Costs and Other Special Items*

(in millions)

Income Before

Interest, Other

Expense and

Income Taxes

Reported Results

2007 Total Company

$ 194.8

2007 Residual Interior business

(0.6)

2007 Seating/Electrical and Electronic businesses

$ 195.4

Reported Results Include the Following Items:

COGS

SG&A

Costs related to restructuring actions

$ 29.8

24.4

$

5.4

$

Costs related to merger transaction

2.3

-

2.3

Costs related to divestiture of Interior business

1.8

1.3

0.5

2007 Core Operating Earnings

229.3

$

2006 Core Operating Earnings

164.7

$

Second Quarter

Income Statement Category

Memo:

* Please see slides titled “Non-GAAP Financial Information” at the end of this presentation for further information.

13

Second Quarter 2007

Net Sales Changes and Margin Impact Versus Prior Year

Net Sales

Margin

Performance Factor

Change

Impact

Comments

(in millions)

Industry Production /

$ (171)

Negative

Primarily lower production in

Platform Mix / Net Pricing /

All Other

North America

Global New Business

266

Positive

Nissan Qashqai, Range Rover, Fiat Bravo

and Audi TT in Europe; Hyundai Veracruz

in Asia; GMT 900 pickup and Hyundai

Santa Fe in N.A.

F/X Translation

143

Neutral

Euro up 7%, Canadian dollar up 2%

Acquisition / Divestiture

(893)

Positive

Divestiture of Interior business

Commodity

Neutral

Steel down 6% and copper up 11%, with

some prior period recovery; crude oil

down 8%

Performance

Positive

Favorable operating performance in core

businesses, including benefits from

restructuring actions and vertical

integration

14

Second Quarter 2007

Business Segment Results

Seating

Margin

Margin

Net Sales

3,264.5

$

3,096.1

$

Reported Segment Earnings*

238.8

$

7.3%

171.5

$

5.5%

Adjusted Earnings**

250.4

$

7.7%

175.4

$

5.7%

Electrical and Electronic

Net Sales

825.1

$

787.7

$

Reported Segment Earnings*

23.5

$

2.8%

38.0

$

4.8%

Adjusted Earnings**

38.6

$

4.7%

50.8

$

6.4%

Headquarters Costs

Reported Segment Earnings*

(66.9)

$

(62.0)

$

Adjusted Earnings**

(59.7)

$

(61.5)

$

Core Business

Net Sales

4,089.6

$

3,883.8

$

Reported Earnings*

195.4

$

4.8%

147.5

$

3.8%

Adjusted Earnings**

229.3

$

5.6%

164.7

$

4.2%

Total Company

Net Sales

4,155.3

$

4,810.2

$

Reported Earnings*

194.8

$

4.7%

113.2

$

2.4%

Adjusted Earnings**

233.7

$

5.6%

139.6

$

2.9%

2007

2006

Second Quarter

($ in millions)

* Reported segment earnings represent income (loss) before interest, other expense and income taxes. Please see slides titled “Non-GAAP Financial

Information” at the end of this presentation for further information.

** Adjusted earnings and margin exclude restructuring costs and other special items as follows – In the Second Quarter ended 06/30/07, adjustments for

Seating - $11.6M, Electrical and Electronic - $15.1M, HQ - $7.2M, Core Business - $33.9M and Total Company - $38.9M and in the Second Quarter

ended 07/01/06, adjustments for Seating - $3.9M, Electrical and Electronic - $12.8M, HQ - - $0.5M, Core Business - $17.2M and Total Company -

$26.4M.

15

Second Quarter 2007

Seating Segment Performance*

Explanation of

Year-to-Year Change

5.7%

7.7%

Q2 2006

Q2 2007

Adj. Seg.

Earnings

(in millions)

$175.4 $250.4

Adjusted Seating Margin

16

+

Favorable cost performance from

restructuring and ongoing efficiency

actions

+

Margin improvement actions, including

selective vertical integration

+

Benefit of new business, primarily

outside of North America

+

Net raw material favorable

-

Lower production in North America

*

Please see slides titled “Non-GAAP Financial Information” at the end of this presentation for further information and refer to

slide 28 in this presentation for a reconciliation of reported segment earnings to adjusted segment earnings.

Second Quarter 2007

Electrical and Electronic Segment Performance*

Explanation of

Year-to-Year Change

6.4%

4.7%

Q2 2006

Q2 2007

Adj. Seg.

Earnings

(in millions)

$50.8 $38.6

Adjusted

Electrical and Electronic Margin

17

-

Litigation costs and other

commercial items

-

Unfavorable net pricing

-

Lower industry production in N. A.

-

Roll-off of two programs in N. A.

-/+ Higher copper prices offset by prior

period recovery

-

Improving results in Asia

*

Please see slides titled “Non-GAAP Financial Information” at the end of this presentation for further information and refer to

slide 28 in this presentation for a reconciliation of reported segment earnings to adjusted segment earnings.

Adjusted Headquarters Expense**

Explanation of

Year-to-Year Change

Second Quarter 2007

Headquarters Performance*

(in millions)

$61.5

$59.7

Q2 2006

Q2 2007

18

SG&A efficiencies

Restructuring savings

*

Please see slides titled “Non-GAAP Financial Information” at the end of this presentation for further information and refer to slide 28 in

this presentation for a reconciliation of reported segment earnings to adjusted segment earnings.

**

Adjusted expense excludes restructuring costs of $0.5 million in 2006 and restructuring costs of $3.1 million, merger-related costs of

$2.3 million and costs related to the Interior divestiture of $1.8 million in 2007.

Second Quarter 2007

Free Cash Flow*

(in millions)

Second

Quarter

2007

Net Income

$ 123.6

Depreciation / Amortization

75.7

Working Capital / Other

43.8

Cash from Operations

$ 243.1

Capital Expenditures

(39.1)

Free Cash Flow

$ 204.0

19

*

Free Cash Flow represents net cash provided by operating activities ($289.3 million for the three months ended 6/30/07) before

net change in sold accounts receivable (($46.2) million for the three months ended 06/30/07) (Cash from Operations), less

capital expenditures. Please see slides titled “Non-GAAP Financial Information” at the end of this presentation for further

information.

2007 Outlook

Full-Year Production Assumptions*

Full-Year

Change from

2007 Outlook

Prior Year

North American Production

Total Industry

~ 15.1 mil

~

down 1%

Big Three

~ 9.8 mil

~

down 4%

Lear’s Top 15 Platforms

~ 4.6 mil

~

down 7%

European Production

Total Industry

~ 19.7 mil

~

up 3%

Lear’s Top 5 Customers

~ 9.9 mil

~

up 2%

Euro

$1.34 / Euro

up 6%

Key Commodities

moderating

slightly lower

(except copper)

(except copper)

Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

20

2007 Outlook

Full-Year Financial Forecast*

2007 Full-Year

Financial Forecast

for Core Business

(Seating and Electrical and Electronic businesses)

Net Sales

~

~

$15 billion

Core Operating Earnings

$600 to $640 million

Income before interest, other expense,

income taxes, restructuring

costs and other special items

Interest Expense

$210 to $215 million

Pretax Income

$335 to $375 million

before restructuring costs

and other special items

Estimated Tax Expense

~

~

$120 million

**

Pretax Restructuring Costs

~

~

$100 million

Capital Spending

~

~

$235 million

Depreciation and Amortization

~

~

$310 million

Free Cash Flow

~

~

$275 million

** Subject to actual mix of financial results by country.

* Please see slides titled “Non-GAAP Financial Information” and “Forward-Looking Statements” at the end of this presentation for

further information.

21

Summary and Outlook*

Lear is Financially Sound

Successfully refinanced major debt maturities through 2010

Operating results improving; cash flow now solidly positive

Making Progress on Strategic Priorities

Completed divestiture of Interior business

Expanding our presence in Asia and growing Asian sales

globally

Implementing global restructuring actions

Automotive industry conditions, particularly in North

America, remain challenging

Longer-term outlook for Lear continues to be positive

Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

22

ADVANCE RELENTLESSLY™

www.lear.com

LEA

NYSE

Listed

R

23

Non-GAAP Financial Information

In addition to the results reported in accordance with accounting principles generally accepted in the United States (“GAAP”) included

throughout this presentation, the Company has provided information regarding “income before interest, other expense and income taxes,”

“seating and electrical and electronic income before interest, other expense, income taxes, restructuring costs and other special items” (core

operating earnings), “pretax income before restructuring costs and other special items” and “free cash flow” (each, a non-GAAP financial

measure). Other expense includes, among other things, state and local non-income taxes, foreign exchange gains and losses, fees

associated with the Company’s asset-backed securitization and factoring facilities, minority interests in consolidated subsidiaries, equity in

net income of affiliates and gains and losses on the sale of assets. Free cash flow represents net cash provided by operating activities

before the net change in sold accounts receivable, less capital expenditures. The Company believes it is appropriate to exclude the net

change in sold accounts receivable in the calculation of free cash flow since the sale of receivables may be viewed as a substitute for

borrowing activity.

Management believes the non-GAAP financial measures used in this presentation are useful to both management and investors in their

analysis of the Company’s financial position and results of operations. In particular, management believes that income before interest, other

expense and income taxes, core operating earnings and pretax income before restructuring costs and other special items are useful

measures in assessing the Company’s financial performance by excluding certain items (including those items that are included in other

expense) that are not indicative of the Company’s core operating earnings or that may obscure trends useful in evaluating the Company’s

continuing operating activities. Management also believes that these measures are useful to both management and investors in their

analysis of the Company’s results of operations and provide improved comparability between fiscal periods. Management believes that free

cash flow is useful to both management and investors in their analysis of the Company’s ability to service and repay its debt. Further,

management uses these non-GAAP financial measures for planning and forecasting in future periods.

Income before interest, other expense and income taxes, core operating earnings, pretax income before restructuring costs and other

special items and free cash flow should not be considered in isolation or as a substitute for pretax income, net income, cash provided by

operating activities or other income statement or cash flow statement data prepared in accordance with GAAP or as a measure of

profitability or liquidity. In addition, the calculation of free cash flow does not reflect cash used to service debt and therefore, does not reflect

funds available for investment or other discretionary uses. Also, these non-GAAP financial measures, as determined and presented by the

Company, may not be comparable to related or similarly titled measures reported by other companies.

Set forth on the following slides are reconciliations of these non-GAAP financial measures to the most directly comparable financial

measures calculated and presented in accordance with GAAP. Given the inherent uncertainty regarding special items, other expense and

the net change in sold accounts receivable in any future period, a reconciliation of forward-looking financial measures to the most directly

comparable financial measures calculated and presented in accordance with GAAP is not feasible. The magnitude of these items, however,

may be significant.

24

Non-GAAP Financial Information

Cash from Operations and Free Cash Flow

Three Months

(in millions)

Q2 2007

Net cash provided by operating activities

$ 289.3

Net change in sold accounts receivable

(46.2)

Net cash provided by operating activities

before net change in sold accounts receivable

(cash from operations)

243.1

Capital expenditures

(39.1)

Free cash flow

$ 204.0

25

Non-GAAP Financial Information

Core Operating Earnings

Three Months

(in millions)

Q2 2007

Q2 2006

Pretax income

$ 143.9

$ 31.5

Goodwill impairment charge related to Interior business

-

2.9

Divestiture of Interior business

(0.7)

-

Interest expense

51.3

53.2

Other expense, net *

0.3

25.6

Income before interest, other expense and income taxes

$ 194.8

$ 113.2

Costs related to divestiture of Interior business (included in COS and SG&A)

1.8

-

Fixed asset impairment charges related to Interior business

-

7.2

Costs related to restructuring actions

34.8

19.2

Costs related to merger transaction

2.3

-

Income before interest, other expense, income taxes,

restructuring costs and other special items

233.7

$

139.6

$

Less: Interior business

(4.4)

25.1

Seating and electrical and electronic income before interest, other

expense, income taxes, restructuring costs and other special items

$ 229.3

$ 164.7

(core operating earnings)

* Includes minority interests in consolidated subsidiaries and equity in net income of affiliates.

26

Non-GAAP Financial Information

Segment Earnings Reconciliation

Three Months

(in millions)

Q2 2007

Q2 2006

Seating

$ 238.8

$ 171.5

Electrical and electronic

23.5

38.0

Interior

(0.6)

(34.3)

Segment earnings

261.7

175.2

Corporate and geographic headquarters and elimination of

intercompany activity

(66.9)

(62.0)

Income before interest, other expense and income taxes

$ 194.8

$ 113.2

Goodwill impairment charge related to Interior business

-

2.9

Divestiture of Interior business

(0.7)

-

Interest expense

51.3

53.2

Other expense, net

0.3

25.6

Pretax income

$ 143.9

$ 31.5

27

Non-GAAP Financial Information

Adjusted Segment Earnings

Three Months Q2 2007

Three Months Q2 2006

Electrical and

HQ/

Core

Electrical and

HQ/

Core

(in millions)

Seating

Electronic

Other

Business

Seating

Electronic

Other

Business

Segment earnings

238.8

$

23.5

$

(66.9)

$

195.4

$

171.5

$

38.0

$

(62.0)

$

147.5

$

Costs related to divestiture of

Interior business

-

-

1.8

1.8

-

-

-

-

Costs related to restructuring actions

11.6

15.1

3.1

29.8

3.9

12.8

0.5

17.2

Costs related to merger transaction

-

-

2.3

2.3

-

-

-

-

Adjusted segment earnings

250.4

$

38.6

$

(59.7)

$

229.3

$

175.4

$

50.8

$

(61.5)

$

164.7

$

28

Forward-Looking Statements

This presentation contains forward-looking statements within the meaning of the Private Securities

Litigation Reform Act of 1995, including statements regarding anticipated financial results and

liquidity. Actual results may differ materially from anticipated results as a result of certain risks and

uncertainties, including but not limited to, general economic conditions in the markets in which the

Company operates, including changes in interest rates or currency exchange rates, the financial

condition of the Company’s customers or suppliers, fluctuations in the production of vehicles for

which the Company is a supplier, disruptions in the relationships with the Company’s suppliers,

labor disputes involving the Company or its significant customers or suppliers or that otherwise

affect the Company, the Company’s ability to achieve cost reductions that offset or exceed

customer-mandated selling price reductions, the outcome of customer productivity negotiations, the

impact and timing of program launch costs, the costs and timing of facility closures, business

realignment or similar actions, increases in the Company's warranty or product liability costs, risks

associated with conducting business in foreign countries, competitive conditions impacting the

Company's key customers and suppliers, raw material costs and availability, the Company's ability

to mitigate the significant impact of increases in raw material, energy and commodity costs, the

outcome of legal or regulatory proceedings to which the Company is or may become a party,

unanticipated changes in cash flow, including the Company’s ability to align its vendor payment

terms with those of its customers, the success of the Company's restructuring initiative and other

risks described from time to time in the Company's Securities and Exchange Commission filings.

The forward-looking statements in this presentation are made as of the date hereof, and the

Company does not assume any obligation to update, amend or clarify them to reflect events, new

information or circumstances occurring after the date hereof.

29